Annual Report

October 31, 2024

Stone Ridge Reinsurance Risk Premium Interval Fund

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-22870

Investment Company Act file number

Stone Ridge Trust II

(Exact name of registrant as specified in charter)

One Vanderbilt Avenue, 65th Floor

New York, New York 10017

(Address of principal executive offices) (Zip code)

Stone Ridge Asset Management LLC

One Vanderbilt Avenue, 65th Floor

New York, New York 10017

(Name and address of agent for service)

(855) 609-3680

Registrant’s telephone number, including area code

Date of fiscal year end: October 31, 2024

Date of reporting period: October 31, 2024

Item 1. Reports to Stockholders.

| (a) |

STONE RIDGE REINSURANCE RISK PREMIUM INTERVAL FUND | ||

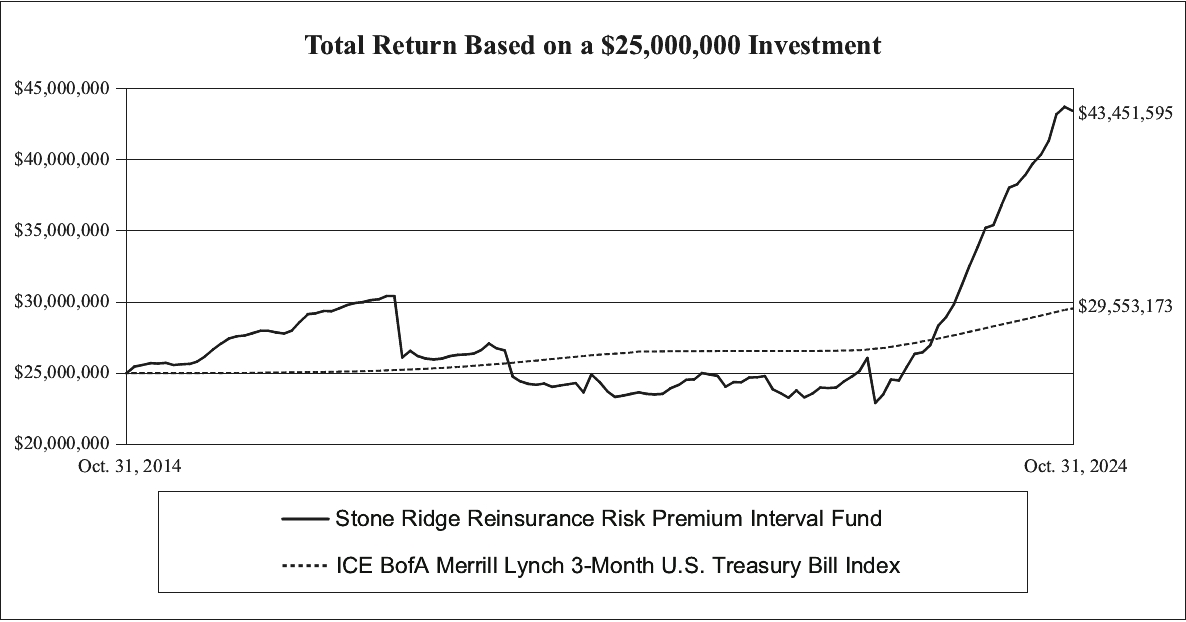

AVERAGE ANNUAL TOTAL RETURNS (FOR PERIODS ENDED OCTOBER 31, 2024) | ||

1-year period ended 10/31/2024 | 5-year period ended 10/31/2024 | 10-year period ended 10/31/2024 | |||||||||

Stone Ridge Reinsurance Risk Premium Interval Fund | 28.25% | 12.24% | 5.68% | ||||||||

ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index | 5.42% | 2.37% | 1.69% | ||||||||

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE | ||

2 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

STONE RIDGE REINSURANCE RISK PREMIUM INTERVAL FUND | ||

Stone Ridge Funds | Annual Report | October 31, 2024 | 3 | |||||

ALLOCATION OF PORTFOLIO HOLDINGS AT October 31, 2024 (Unaudited) | ||

STONE RIDGE REINSURANCE RISK PREMIUM INTERVAL FUND PORTFOLIO ALLOCATION BY YEAR OF SCHEDULED MATURITY | ||||||||

2024 | $27,941,726 | 2.3% | ||||||

2025 | 41,721,060 | 3.4% | ||||||

2026 | 75,859,585 | 6.1% | ||||||

2027 | 82,468,174 | 6.7% | ||||||

2028 | 15,094,119 | 1.2% | ||||||

2029 | 268,001 | 0.0% | ||||||

Not Applicable(1) | 724,008,903 | 58.4% | ||||||

Other(2) | 272,147,213 | 21.9% | ||||||

Net Assets | $1,239,508,781 | |||||||

| (1) | Preference shares do not have maturity dates. |

| (2) | Cash, cash equivalents, short-term investments and other assets in excess of other liabilities. |

4 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Par | Value | ||||||

EVENT LINKED BONDS - 19.6% (a) | |||||||

Chile - 0.2% | |||||||

Earthquake - 0.2% | |||||||

IBRD CAR 131, 9.62% (SOFR + 4.79%), 03/31/2026 (Acquired 03/17/2023 - 02/29/2024; Cost $2,955,143) (b)(c)(d) | $ 2,946,000 | $2,987,484 | |||||

Europe - 0.4% | |||||||

Earthquake - 0.1% | |||||||

Azzurro Re II DAC 2024-1 Class A, 9.72% (3 Month EURIBOR + 6.50%), 04/20/2028 (Acquired 03/21/2024; Cost $681,786) (b)(c)(d) | EUR 628,000 | 683,392 | |||||

Multiperil - 0.1% | |||||||

King Max Re DAC, 8.18% (3 Month EURIBOR + 5.00%), 01/06/2027 (Acquired 12/08/2023; Cost $833,136) (b)(c)(d) | 774,000 | 832,930 | |||||

Lion III Re DAC 2021-1, 7.31% (3 Month EURIBOR + 4.13%), 07/16/2025 (Acquired 06/30/2023; Cost $437,423) (b)(c)(d) | 404,000 | 432,808 | |||||

Taranis Re DAC 2023-1 Class A, 11.39% (3 Month EURIBOR + 8.25%), 01/21/2028 (Acquired 11/29/2023; Cost $282,018) (b)(c)(d) | 257,000 | 280,251 | |||||

1,545,989 | |||||||

Windstorm - 0.2% | |||||||

Blue Sky Re DAC 2023-1, 8.82% (3 Month EURIBOR + 5.75%), 01/26/2027 (Acquired 12/11/2023; Cost $379,987) (b)(c)(d) | 353,000 | 392,124 | |||||

Eiffel Re 2023-1 Class A, 6.54% (3 Month EURIBOR + 3.33%), 01/19/2027 (Acquired 06/22/2023; Cost $1,175,736) (b)(c)(d) | 1,073,000 | 1,148,793 | |||||

Hexagon IV Re 2023-1 Class A, 11.72% (3 Month EURIBOR + 8.50%), 01/21/2028 (Acquired 11/07/2023; Cost $825,695) (b)(c)(d) | 772,000 | 834,698 | |||||

2,375,615 | |||||||

4,604,996 | |||||||

Global - 1.1% | |||||||

Cyber - 0.4% | |||||||

East Lane Re VII 2024-1 Class A, 13.79% (3 Month U.S. Treasury Bill Money Market Yield + 9.25%), 03/31/2026 (Acquired 12/20/2023; Cost $569,000) (b)(c)(d) | $569,000 | 569,863 | |||||

Long Walk Re 2024-1 Class A, 14.27% (3 Month U.S. Treasury Bill Money Market Yield + 9.75%), 01/30/2026 (Acquired 11/13/2023; Cost $360,000) (b)(c)(d) | 360,000 | 365,498 | |||||

Matterhorn Re SR2023-1 Class CYB-A, 16.54% (3 Month U.S. Treasury Bill Money Market Yield + 12.00%), 01/08/2026 (Acquired 12/22/2023; Cost $1,346,000) (b)(c)(d) | 1,346,000 | 1,355,344 | |||||

PoleStar Re 2024-1 Class A, 17.54% (3 Month U.S. Treasury Bill Money Market Yield + 13.00%), 01/07/2026 (Acquired 12/13/2023; Cost $1,000,000) (b)(c)(d) | 1,000,000 | 1,009,840 | |||||

PoleStar Re 2024-3 Class A, 15.04% (3 Month U.S. Treasury Bill Money Market Yield + 10.50%), 01/07/2028 (Acquired 09/19/2024; Cost $1,682,000) (b)(c)(d) | 1,682,000 | 1,679,304 | |||||

4,979,849 | |||||||

Earthquake - 0.0% (e) | |||||||

Ashera Re 2024-1 Class A, 9.54% (3 Month U.S. Treasury Bill Money Market Yield + 5.00%), 04/07/2027 (Acquired 03/21/2024; Cost $506,000) (b)(c)(d) | 506,000 | 511,447 | |||||

Multiperil - 0.6% | |||||||

Aragonite Re 2024-1 Class A, 9.79% (3 Month U.S. Treasury Bill Money Market Yield + 5.25%), 04/07/2027 (Acquired 03/25/2024; Cost $627,000) (b)(c)(d) | 627,000 | 639,459 | |||||

Kendall Re 2024-1 Class A, 10.79% (3 Month U.S. Treasury Bill Money Market Yield + 6.25%), 04/30/2027 (Acquired 04/22/2024; Cost $1,023,000) (b)(c)(d) | 1,023,000 | 1,057,953 | |||||

Matterhorn Re SR2020-2 Class A, 1.50% (3 Month U.S. Treasury Bill Money Market Yield + 1.50%), 01/08/2027 (Acquired 01/29/2020; Cost $1,873,320) (b)(c)(d)(f) | 1,873,320 | 1,498,655 | |||||

Matterhorn Re SR2021-1 Class A, 10.67% (SOFR + 5.75%), 12/08/2025 (Acquired 09/15/2022; Cost $257,724) (b)(c)(d) | 261,000 | 254,193 | |||||

Matterhorn Re SR2022-1 Class A, 10.11% (SOFR + 5.25%), 03/24/2025 (Acquired 07/13/2022; Cost $993,147) (b)(c)(d) | 1,000,000 | 999,999 | |||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 5 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Par | Value | ||||||

Multiperil - 0.6% (continued) | |||||||

Montoya Re 2022-1 Class A, 11.62% (3 Month U.S. Treasury Bill Money Market Yield + 7.10%), 04/07/2025 (Acquired 09/16/2022; Cost $325,511) (b)(c)(d) | $ 326,000 | $329,719 | |||||

Northshore Re II 2022-1 Class A, 12.52% (3 Month U.S. Treasury Bill Money Market Yield + 8.00%), 07/08/2025 (Acquired 05/02/2024; Cost $415,000) (b)(c)(d) | 415,000 | 426,411 | |||||

Sakura Re 2021-1 Class A, 6.93% (3 Month U.S. Treasury Bill Money Market Yield + 2.41%), 04/07/2025 (Acquired 08/04/2023 - 11/09/2023; Cost $634,751) (b)(c)(d) | 638,000 | 640,244 | |||||

Sakura Re 2021-1 Class B, 8.16% (3 Month U.S. Treasury Bill Money Market Yield + 3.64%), 04/07/2025 (Acquired 06/23/2023; Cost $363,687) (b)(c)(d) | 365,000 | 364,951 | |||||

Wrigley Re 2023-1 Class A, 11.02% (3 Month U.S. Treasury Bill Money Market Yield + 6.50%), 08/07/2026 (Acquired 07/14/2023; Cost $507,000) (b)(c)(d) | 507,000 | 520,941 | |||||

6,732,525 | |||||||

Windstorm - 0.1% | |||||||

Queen Street 2023 Re DAC, 12.02% (3 Month U.S. Treasury Bill Money Market Yield + 7.50%), 12/08/2025 (Acquired 05/12/2023; Cost $1,526,000) (b)(c)(d) | 1,526,000 | 1,566,370 | |||||

13,790,191 | |||||||

Jamaica - 0.2% | |||||||

Windstorm - 0.2% | |||||||

IBRD CAR 136, 12.02% (SOFR + 7.19%), 12/29/2027 (Acquired 04/25/2024; Cost $2,108,000) (b)(c)(d) | 2,108,000 | 2,069,019 | |||||

Japan - 0.3% | |||||||

Earthquake - 0.2% | |||||||

Kizuna Re III 2024-1 Class A, 7.29% (3 Month U.S. Treasury Bill Money Market Yield + 2.75%), 04/09/2029 (Acquired 03/13/2024; Cost $266,000) (b)(c)(d) | 266,000 | 268,001 | |||||

Nakama Re 2020-1 Class 1, 6.72% (3 Month U.S. Treasury Bill Money Market Yield + 2.20%), 01/14/2025 (Acquired 02/04/2020; Cost $871,000) (b)(c)(d) | 871,000 | 868,965 | |||||

Nakama Re 2023-1 Class 2, 8.40% (3 Month Term SOFR + 4.00%), 05/09/2028 (Acquired 04/14/2023; Cost $802,000) (b)(c)(d) | 802,000 | 816,907 | |||||

Nakama Re Pte. 2021-1 Class 1, 6.57% (3 Month U.S. Treasury Bill Money Market Yield + 2.05%), 10/13/2026 (Acquired 02/08/2024; Cost $305,631) (b)(c)(d) | 307,000 | 306,027 | |||||

2,259,900 | |||||||

Multiperil - 0.1% | |||||||

Tomoni Re Pte 2024-1 Class A, 7.79% (3 Month U.S. Treasury Bill Money Market Yield + 3.25%), 04/05/2028 (Acquired 03/25/2024; Cost $679,000) (b)(c)(d) | 679,000 | 680,199 | |||||

Tomoni Re Pte 2024-1 Class B, 8.54% (3 Month U.S. Treasury Bill Money Market Yield + 4.00%), 04/05/2028 (Acquired 03/25/2024; Cost $853,000) (b)(c)(d) | 853,000 | 862,693 | |||||

1,542,892 | |||||||

3,802,792 | |||||||

Mexico - 0.4% | |||||||

Earthquake - 0.2% | |||||||

IBRD CAR 132 Class A, 9.05% (SOFR + 4.22%), 04/24/2028 (Acquired 04/03/2024; Cost $1,865,000) (b)(c)(d) | 1,865,000 | 1,886,132 | |||||

IBRD CAR 133 Class B, 16.05% (SOFR + 11.22%), 04/24/2028 (Acquired 04/03/2024; Cost $651,000) (b)(c)(d) | 651,000 | 652,714 | |||||

2,538,846 | |||||||

Windstorm - 0.2% | |||||||

IBRD CAR 134 Class C, 18.55% (SOFR + 13.72%), 04/24/2028 (Acquired 04/03/2024; Cost $1,408,000) (b)(c)(d) | 1,408,000 | 1,479,092 | |||||

IBRD CAR 135 Class D, 17.05% (SOFR + 12.22%), 04/24/2028 (Acquired 05/01/2024; Cost $613,000) (b)(c)(d) | 613,000 | 637,005 | |||||

2,116,097 | |||||||

4,654,943 | |||||||

New Zealand - 0.1% | |||||||

Multiperil - 0.1% | |||||||

Totara Re Pte. 2023-1, 13.39%, 06/08/2027 (Acquired 05/24/2023; Cost $1,325,284) (b)(c)(d) | NZD 2,171,000 | 1,327,615 | |||||

6 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Par | Value | ||||||

United States - 16.9% | |||||||

Earthquake - 3.3% | |||||||

Acorn Re 2021-1 Class A, 7.02% (3 Month U.S. Treasury Bill Money Market Yield + 2.50%), 11/07/2024 (Acquired 10/04/2022 - 05/28/2024; Cost $2,460,107) (b)(c)(d) | $2,461,000 | $2,457,130 | |||||

Acorn Re 2023-1 Class A, 8.87% (3 Month U.S. Treasury Bill Money Market Yield + 4.35%), 11/06/2026 (Acquired 06/22/2023; Cost $1,096,000) (b)(c)(d) | 1,096,000 | 1,119,985 | |||||

Acorn Re 2024-1 Class A, 7.64% (3 Month U.S. Treasury Bill Money Market Yield + 3.10%), 11/05/2027 (Acquired 10/25/2024; Cost $1,080,000) (b)(c)(d) | 1,080,000 | 1,079,945 | |||||

Acorn Re 2024-1 Class B, 7.64% (3 Month U.S. Treasury Bill Money Market Yield + 3.10%), 11/07/2025 (Acquired 10/25/2024; Cost $1,133,000) (b)(c)(d) | 1,133,000 | 1,132,942 | |||||

Herbie Re 2022-1 Class A, 18.02% (3 Month U.S. Treasury Bill Money Market Yield + 13.50%), 01/08/2027 (Acquired 11/18/2022; Cost $392,000) (b)(c)(d) | 392,000 | 429,847 | |||||

Merna Re II 2022-1 Class A, 8.37% (3 Month U.S. Treasury Bill Money Market Yield + 3.85%), 04/07/2025 (Acquired 07/07/2023 - 01/19/2024; Cost $1,376,324) (b)(c)(d) | 1,376,000 | 1,387,904 | |||||

Phoenician Re 2021-1 Class A, 7.42% (3 Month U.S. Treasury Bill Money Market Yield + 2.90%), 12/14/2024 (Acquired 05/21/2024; Cost $454,291) (b)(c)(d) | 455,000 | 454,304 | |||||

Sutter Re 2023-1 Class B, 11.27% (3 Month U.S. Treasury Bill Money Market Yield + 6.75%), 06/19/2026 (Acquired 06/06/2023 - 05/03/2024; Cost $1,975,739) (b)(c)(d) | 1,973,000 | 2,037,410 | |||||

Sutter Re 2023-1 Class E, 14.27% (3 Month U.S. Treasury Bill Money Market Yield + 9.75%), 06/19/2026 (Acquired 06/06/2023 - 09/26/2023; Cost $2,179,143) (b)(c)(d) | 2,177,000 | 2,269,896 | |||||

Torrey Pines Re 2023-1 Class A, 9.73% (3 Month U.S. Treasury Bill Money Market Yield + 5.22%), 06/05/2026 (Acquired 05/18/2023; Cost $1,132,000) (b)(c)(d) | 1,132,000 | 1,155,626 | |||||

Torrey Pines Re 2024-1 Class A, 10.54% (3 Month U.S. Treasury Bill Money Market Yield + 6.00%), 06/07/2027 (Acquired 05/17/2024; Cost $1,862,000) (b)(c)(d) | 1,862,000 | 1,933,416 | |||||

Torrey Pines Re 2024-1 Class B, 11.79% (3 Month U.S. Treasury Bill Money Market Yield + 7.25%), 06/07/2027 (Acquired 05/17/2024; Cost $1,263,000) (b)(c)(d) | 1,263,000 | 1,301,957 | |||||

Torrey Pines Re 2024-1 Class C, 13.54% (3 Month U.S. Treasury Bill Money Market Yield + 9.00%), 06/05/2026 (Acquired 05/17/2024; Cost $598,000) (b)(c)(d) | 598,000 | 614,864 | |||||

Ursa Re 2023-1 Class AA, 10.02% (3 Month U.S. Treasury Bill Money Market Yield + 5.50%), 12/06/2025 (Acquired 04/12/2023; Cost $633,000) (b)(c)(d) | 633,000 | 645,284 | |||||

Ursa Re 2023-1 Class C, 12.77% (3 Month U.S. Treasury Bill Money Market Yield + 8.25%), 12/06/2025 (Acquired 04/12/2023; Cost $341,000) (b)(c)(d) | 341,000 | 350,550 | |||||

Ursa Re 2023-2 Class E, 13.77% (3 Month U.S. Treasury Bill Money Market Yield + 9.25%), 12/07/2026 (Acquired 10/10/2023; Cost $2,489,000) (b)(c)(d) | 2,489,000 | 2,599,351 | |||||

Ursa Re 2023-3 Class AA, 10.04% (3 Month U.S. Treasury Bill Money Market Yield + 5.50%), 12/07/2026 (Acquired 12/01/2023; Cost $2,194,000) (b)(c)(d) | 2,194,000 | 2,272,343 | |||||

Ursa Re 2023-3 Class D, 13.29% (3 Month U.S. Treasury Bill Money Market Yield + 8.75%), 12/07/2026 (Acquired 12/01/2023 - 05/17/2024; Cost $2,619,938) (b)(c)(d) | 2,614,000 | 2,748,352 | |||||

Ursa Re II 2021-1 Class F, 11.15% (3 Month U.S. Treasury Bill Money Market Yield + 6.63%), 12/06/2024 (Acquired 07/13/2022 - 07/27/2022; Cost $9,780,373) (b)(c)(d) | 9,800,000 | 9,790,783 | |||||

Ursa Re II 2022-1 Class A, 9.52% (3 Month U.S. Treasury Bill Money Market Yield + 5.00%), 06/16/2025 (Acquired 10/19/2023; Cost $455,850) (b)(c)(d) | 457,000 | 459,839 | |||||

Ursa Re II 2022-2 Class AA, 11.52% (3 Month U.S. Treasury Bill Money Market Yield + 7.00%), 12/06/2025 (Acquired 12/08/2022; Cost $331,000) (b)(c)(d) | 331,000 | 342,576 | |||||

Ursa Re II 2022-2 Class C, 14.77% (3 Month U.S. Treasury Bill Money Market Yield + 10.25%), 12/06/2025 (Acquired 12/08/2022 - 09/05/2023; Cost $533,357) (b)(c)(d) | 526,000 | 551,539 | |||||

Veraison Re 2023-1 Class A, 11.43% (3 Month U.S. Treasury Bill Money Market Yield + 6.91%), 03/09/2026 (Acquired 12/14/2022; Cost $760,000) (b)(c)(d) | 760,000 | 791,694 | |||||

Veraison Re 2023-1 Class B, 17.05% (3 Month U.S. Treasury Bill Money Market Yield + 12.53%), 03/09/2026 (Acquired 12/14/2022; Cost $729,000) (b)(c)(d) | 729,000 | 780,438 | |||||

Veraison Re 2024-1 Class A, 9.29% (3 Month U.S. Treasury Bill Money Market Yield + 4.75%), 03/08/2027 (Acquired 01/30/2024; Cost $826,000) (b)(c)(d) | 826,000 | 843,144 | |||||

Wrigley Re 2023-1 Class B, 11.52% (3 Month U.S. Treasury Bill Money Market Yield + 7.00%), 08/07/2026 (Acquired 07/14/2023; Cost $1,166,000) (b)(c)(d) | 1,166,000 | 1,217,484 | |||||

40,768,603 | |||||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 7 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Par | Value | ||||||

Flood - 0.7% | |||||||

FloodSmart Re 2022-1 Class A, 16.35% (3 Month U.S. Treasury Bill Money Market Yield + 11.83%), 02/25/2025 (Acquired 07/12/2022; Cost $2,975,500) (b)(c)(d) | $3,000,000 | $3,069,228 | |||||

FloodSmart Re 2022-1 Class B, 18.85% (3 Month U.S. Treasury Bill Money Market Yield + 14.33%), 02/25/2025 (Acquired 10/24/2023; Cost $273,738) (b)(c)(d) | 275,000 | 247,499 | |||||

FloodSmart Re 2024-1 Class A, 18.54% (3 Month U.S. Treasury Bill Money Market Yield + 14.00%), 03/12/2027 (Acquired 02/29/2024; Cost $4,099,000) (b)(c)(d) | 4,099,000 | 4,227,299 | |||||

FloodSmart Re 2024-1 Class B, 21.79% (3 Month U.S. Treasury Bill Money Market Yield + 17.25%), 03/12/2027 (Acquired 02/29/2024; Cost $967,000) (b)(c)(d) | 967,000 | 978,748 | |||||

8,522,774 | |||||||

Mortality/Longevity/Disease - 0.4% | |||||||

Vita Capital VI 2021-1 Class B, 7.98% (SOFR + 3.12%), 01/08/2026 (Acquired 02/22/2023; Cost $438,928) (b)(c)(d)(f) | 449,000 | — | |||||

Vitality Re XII 2021 Class A, 6.77% (3 Month U.S. Treasury Bill Money Market Yield + 2.25%), 01/07/2025 (Acquired 10/28/2022 - 03/20/2024; Cost $2,122,772) (b)(c)(d) | 2,133,000 | 2,132,889 | |||||

Vitality Re XII 2021 Class B, 7.27% (3 Month U.S. Treasury Bill Money Market Yield + 2.75%), 01/07/2025 (Acquired 09/21/2023; Cost $265,287) (b)(c)(d) | 266,000 | 265,556 | |||||

Vitality Re XIII 2022 Class A, 6.52% (3 Month U.S. Treasury Bill Money Market Yield + 2.00%), 01/06/2026 (Acquired 01/04/2023; Cost $597,591) (b)(c)(d) | 611,000 | 607,503 | |||||

Vitality Re XIV 2023 Class A, 8.02% (3 Month U.S. Treasury Bill Money Market Yield + 3.50%), 01/05/2027 (Acquired 03/07/2024 - 03/14/2024; Cost $637,981) (b)(c)(d) | 629,000 | 637,337 | |||||

Vitality Re XIV 2023 Class B, 9.02% (3 Month U.S. Treasury Bill Money Market Yield + 4.50%), 01/05/2027 (Acquired 01/25/2023; Cost $334,000) (b)(c)(d) | 334,000 | 337,010 | |||||

Vitality Re XV 2024 Class A, 7.04% (3 Month U.S. Treasury Bill Money Market Yield + 2.50%), 01/07/2028 (Acquired 01/22/2024; Cost $372,000) (b)(c)(d) | 372,000 | 371,765 | |||||

Vitality Re XV 2024 Class B, 8.04% (3 Month U.S. Treasury Bill Money Market Yield + 3.50%), 01/07/2028 (Acquired 01/22/2024; Cost $255,000) (b)(c)(d) | 255,000 | 255,041 | |||||

4,607,101 | |||||||

Multiperil - 5.9% | |||||||

Aquila Re I 2023-1 Class A-1, 10.17% (3 Month U.S. Treasury Bill Money Market Yield + 5.65%), 06/08/2026 (Acquired 05/10/2023; Cost $265,000) (b)(c)(d) | 265,000 | 274,195 | |||||

Aquila Re I 2023-1 Class B-1, 12.79% (3 Month U.S. Treasury Bill Money Market Yield + 8.27%), 06/08/2026 (Acquired 05/10/2023; Cost $1,079,000) (b)(c)(d) | 1,079,000 | 1,138,238 | |||||

Aquila Re I 2023-1 Class C-1, 13.70% (3 Month U.S. Treasury Bill Money Market Yield + 9.18%), 06/08/2026 (Acquired 05/10/2023; Cost $1,241,000) (b)(c)(d) | 1,241,000 | 1,322,286 | |||||

Aquila Re I 2024-1 Class A-1, 10.04% (3 Month U.S. Treasury Bill Money Market Yield + 5.50%), 06/07/2027 (Acquired 04/26/2024; Cost $492,000) (b)(c)(d) | 492,000 | 502,805 | |||||

Aquila Re I 2024-1 Class B-1, 13.54% (3 Month U.S. Treasury Bill Money Market Yield + 9.00%), 06/07/2027 (Acquired 04/26/2024; Cost $299,000) (b)(c)(d) | 299,000 | 312,607 | |||||

Baldwin Re 2021-1 Class A, 6.56% (3 Month U.S. Treasury Bill Money Market Yield + 2.04%), 07/07/2025 (Acquired 07/25/2022 - 11/08/2023; Cost $3,907,387) (b)(c)(d) | 3,933,000 | 3,927,740 | |||||

Baldwin Re 2023-1 Class A, 9.02% (3 Month U.S. Treasury Bill Money Market Yield + 4.50%), 07/07/2027 (Acquired 06/21/2023; Cost $423,000) (b)(c)(d) | 423,000 | 433,050 | |||||

Blue Halo Re 2022-1 Class B, 19.79% (3 Month U.S. Treasury Bill Money Market Yield + 15.25%), 02/24/2025 (Acquired 01/30/2024; Cost $373,387) (b)(c)(d) | 372,000 | 349,680 | |||||

Bonanza Re 2023-2 Class A, 4.54% (3 Month U.S. Treasury Bill Money Market Yield + 0.00%), 01/08/2025 (Acquired 12/19/2023; Cost $436,990) (b)(c)(d) | 458,000 | 377,283 | |||||

Caelus Re 2018-1 Class A, 5.02% (3 Month U.S. Treasury Bill Money Market Yield + 0.50%), 06/09/2025 (Acquired 05/04/2018; Cost $2,681,000) (b)(c)(d) | 2,681,000 | 2,117,990 | |||||

Caelus Re 2018-1 Class B, 4.62% (3 Month U.S. Treasury Bill Money Market Yield + 0.10%), 06/09/2025 (Acquired 05/04/2018 - 07/24/2018; Cost $1,743,791) (b)(c)(d)(f) | 1,745,000 | 4,450 | |||||

Foundation Re 2023-1 Class A, 10.79% (3 Month U.S. Treasury Bill Money Market Yield + 6.25%), 01/08/2027 (Acquired 12/19/2023; Cost $968,000) (b)(c)(d) | 968,000 | 996,104 | |||||

Four Lakes Re 2021-1 Class A, 8.91% (3 Month U.S. Treasury Bill Money Market Yield + 4.39%), 01/07/2025 (Acquired 07/13/2022 - 07/14/2022; Cost $1,743,840) (b)(c)(d) | 1,750,000 | 1,751,356 | |||||

Four Lakes Re 2022-1 Class A, 10.98% (3 Month U.S. Treasury Bill Money Market Yield + 6.46%), 01/07/2026 (Acquired 12/22/2022; Cost $187,000) (b)(c)(d) | 187,000 | 191,747 | |||||

8 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Par | Value | ||||||

Multiperil - 5.9% (continued) | |||||||

Four Lakes Re 2023-1 Class A, 10.29% (3 Month U.S. Treasury Bill Money Market Yield + 5.75%), 01/07/2027 (Acquired 12/08/2023; Cost $314,000) (b)(c)(d) | $314,000 | $320,097 | |||||

Fuchsia 2023-1 Class A, 14.54% (3 Month U.S. Treasury Bill Money Market Yield + 10.00%), 04/06/2027 (Acquired 12/14/2023; Cost $815,000) (b)(c)(d) | 815,000 | 850,725 | |||||

Galileo Re 2023-1 Class A, 11.54% (3 Month U.S. Treasury Bill Money Market Yield + 7.00%), 01/07/2028 (Acquired 12/04/2023; Cost $1,313,000) (b)(c)(d) | 1,313,000 | 1,359,722 | |||||

Galileo Re 2023-1 Class B, 11.54% (3 Month U.S. Treasury Bill Money Market Yield + 7.00%), 01/08/2026 (Acquired 12/04/2023; Cost $409,000) (b)(c)(d) | 409,000 | 417,330 | |||||

Herbie Re 2020-2 Class A, 11.25% (3 Month U.S. Treasury Bill Money Market Yield + 6.73%), 01/08/2025 (Acquired 04/08/2024; Cost $405,076) (b)(c)(d) | 406,000 | 406,516 | |||||

High Point Re 2023-1 Class A, 10.29% (3 Month U.S. Treasury Bill Money Market Yield + 5.75%), 01/06/2027 (Acquired 12/01/2023; Cost $2,582,000) (b)(c)(d) | 2,582,000 | 2,642,245 | |||||

Hypatia Ltd. 2023-1 Class A, 15.02% (3 Month U.S. Treasury Bill Money Market Yield + 10.50%), 04/08/2026 (Acquired 03/27/2023; Cost $377,000) (b)(c)(d) | 377,000 | 394,279 | |||||

Kilimanjaro III Re 2019-2 Class A-2, 21.18% (3 Month U.S. Treasury Bill Money Market Yield + 16.66%), 12/19/2024 (Acquired 04/29/2020 - 07/17/2020; Cost $9,942,354) (b)(c)(d) | 9,960,445 | 9,149,664 | |||||

Locke Tavern Re 2023-1 Class A, 9.30% (3 Month U.S. Treasury Bill Money Market Yield + 4.78%), 04/09/2026 (Acquired 03/23/2023 - 08/21/2023; Cost $1,165,353) (b)(c)(d) | 1,161,000 | 1,191,107 | |||||

Long Point Re IV 2022-1 Class A, 8.77% (3 Month U.S. Treasury Bill Money Market Yield + 4.25%), 06/01/2026 (Acquired 09/28/2023; Cost $259,956) (b)(c)(d) | 261,000 | 265,560 | |||||

Merna Re II 2023-1 Class A, 12.27% (3 Month U.S. Treasury Bill Money Market Yield + 7.75%), 07/07/2026 (Acquired 04/05/2023; Cost $1,066,000) (b)(c)(d) | 1,066,000 | 1,120,310 | |||||

Merna Re II 2023-2 Class A, 14.77% (3 Month U.S. Treasury Bill Money Market Yield + 10.25%), 07/07/2026 (Acquired 04/05/2023; Cost $1,279,000) (b)(c)(d) | 1,279,000 | 1,355,964 | |||||

Merna Re II 2024-1 Class A, 11.79% (3 Month U.S. Treasury Bill Money Market Yield + 7.25%), 07/07/2027 (Acquired 05/08/2024; Cost $1,379,000) (b)(c)(d) | 1,379,000 | 1,440,810 | |||||

Merna Re II 2024-2 Class A, 13.29% (3 Month U.S. Treasury Bill Money Market Yield + 8.75%), 07/07/2027 (Acquired 05/08/2024; Cost $1,758,000) (b)(c)(d) | 1,758,000 | 1,795,445 | |||||

Merna Re II 2024-3 Class A, 13.04% (3 Month U.S. Treasury Bill Money Market Yield + 8.50%), 07/07/2027 (Acquired 05/08/2024; Cost $2,931,000) (b)(c)(d) | 2,931,000 | 3,081,765 | |||||

Montoya Re 2022-2 Class A, 18.30% (3 Month U.S. Treasury Bill Money Market Yield + 13.78%), 04/07/2026 (Acquired 12/08/2022; Cost $181,000) (b)(c)(d) | 181,000 | 196,328 | |||||

Mountain Re 2023-1 Class A, 11.34% (3 Month U.S. Treasury Bill Money Market Yield + 6.82%), 06/05/2026 (Acquired 05/24/2023 - 03/05/2024; Cost $810,343) (b)(c)(d) | 804,000 | 834,857 | |||||

Mystic Re IV 2021-2 Class A, 10.62% (3 Month U.S. Treasury Bill Money Market Yield + 6.10%), 01/08/2025 (Acquired 07/06/2022; Cost $3,488,633) (b)(c)(d) | 3,500,000 | 3,514,613 | |||||

Mystic Re IV 2023-1 Class A, 13.69% (3 Month U.S. Treasury Bill Money Market Yield + 9.17%), 01/08/2026 (Acquired 12/16/2022 - 06/12/2024; Cost $1,158,043) (b)(c)(d) | 1,154,000 | 1,199,226 | |||||

Residential Re 2019-I Class 12, 4.62% (3 Month U.S. Treasury Bill Money Market Yield + 0.10%), 06/06/2026 (Acquired 05/08/2019; Cost $186,919) (b)(c)(d)(f) | 186,919 | 106,590 | |||||

Residential Re 2020-II Class 3, 12.65% (3 Month U.S. Treasury Bill Money Market Yield + 8.13%), 12/06/2024 (Acquired 10/30/2020 - 07/12/2022; Cost $1,485,790) (b)(c)(d) | 1,486,000 | 1,478,771 | |||||

Residential Re 2020-II Class 4, 10.81% (3 Month U.S. Treasury Bill Money Market Yield + 6.29%), 12/06/2024 (Acquired 10/30/2020; Cost $1,269,000) (b)(c)(d) | 1,269,000 | 1,263,531 | |||||

Residential Re 2021-I Class 12, 10.03% (3 Month U.S. Treasury Bill Money Market Yield + 5.51%), 06/06/2025 (Acquired 07/12/2023; Cost $286,195) (b)(c)(d) | 301,000 | 296,697 | |||||

Residential Re 2021-II Class 3, 10.57% (3 Month U.S. Treasury Bill Money Market Yield + 6.05%), 12/06/2025 (Acquired 07/12/2022; Cost $986,929) (b)(c)(d) | 1,000,000 | 980,178 | |||||

Residential Re 2022-I Class 14, 8.73% (3 Month U.S. Treasury Bill Money Market Yield + 4.21%), 06/06/2026 (Acquired 07/12/2022; Cost $1,989,000) (b)(c)(d) | 2,000,000 | 1,969,929 | |||||

Residential Re 2023-I Class 13, 15.68% (3 Month U.S. Treasury Bill Money Market Yield + 11.16%), 06/06/2027 (Acquired 04/28/2023; Cost $1,887,000) (b)(c)(d) | 1,887,000 | 1,870,149 | |||||

Residential Re 2023-I Class 14, 11.05% (3 Month U.S. Treasury Bill Money Market Yield + 6.53%), 06/06/2027 (Acquired 04/28/2023 - 09/22/2023; Cost $3,066,372) (b)(c)(d) | 3,072,000 | 3,063,965 | |||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 9 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Par | Value | ||||||

Multiperil - 5.9% (continued) | |||||||

Residential Re 2023-II Class 3, 12.94% (3 Month U.S. Treasury Bill Money Market Yield + 8.42%), 12/06/2027 (Acquired 11/07/2023; Cost $817,000) (b)(c)(d) | $817,000 | $827,265 | |||||

Residential Re 2023-II Class 5, 10.44% (3 Month U.S. Treasury Bill Money Market Yield + 5.92%), 12/06/2027 (Acquired 11/07/2023; Cost $1,906,000) (b)(c)(d) | 1,906,000 | 1,958,929 | |||||

Residential Re 2024-I Class 14, 10.29% (3 Month U.S. Treasury Bill Money Market Yield + 5.75%), 06/06/2028 (Acquired 04/25/2024; Cost $439,000) (b)(c)(d) | 439,000 | 439,680 | |||||

Sakura Re 2022-1 Class A, 18.02% (3 Month U.S. Treasury Bill Money Market Yield + 13.50%), 01/05/2026 (Acquired 12/22/2022; Cost $841,000) (b)(c)(d) | 841,000 | 890,813 | |||||

Sanders Re II 2021-1 Class A, 7.77% (3 Month U.S. Treasury Bill Money Market Yield + 3.25%), 04/07/2025 (Acquired 07/15/2022 - 07/24/2023; Cost $1,522,308) (b)(c)(d) | 1,533,000 | 1,534,341 | |||||

Sanders Re II 2021-2 Class A, 7.52% (3 Month U.S. Treasury Bill Money Market Yield + 3.00%), 04/07/2025 (Acquired 07/15/2022 - 07/26/2022; Cost $4,294,184) (b)(c)(d) | 4,315,000 | 4,325,787 | |||||

Sanders Re III 2022-1 Class A, 7.93% (3 Month U.S. Treasury Bill Money Market Yield + 3.41%), 04/07/2026 (Acquired 09/28/2023; Cost $871,543) (b)(c)(d) | 900,000 | 895,284 | |||||

Sanders Re III 2022-2 Class B, 12.98% (3 Month U.S. Treasury Bill Money Market Yield + 8.46%), 06/07/2025 (Acquired 03/28/2024; Cost $361,039) (b)(c)(d) | 357,000 | 365,389 | |||||

Sanders Re III 2022-3 Class A, 10.79% (3 Month U.S. Treasury Bill Money Market Yield + 6.27%), 04/07/2027 (Acquired 12/01/2022; Cost $789,000) (b)(c)(d) | 789,000 | 821,725 | |||||

Sanders Re III 2023-1 Class A, 10.07% (3 Month U.S. Treasury Bill Money Market Yield + 5.55%), 04/07/2027 (Acquired 03/24/2023; Cost $423,000) (b)(c)(d) | 423,000 | 433,205 | |||||

Sanders Re III 2023-1 Class B, 15.50% (3 Month U.S. Treasury Bill Money Market Yield + 15.50%), 04/07/2027 (Acquired 03/24/2023; Cost $528,000) (b)(c)(d) | 528,000 | 508,792 | |||||

Sanders Re III 2023-2 Class A, 12.66% (3 Month U.S. Treasury Bill Money Market Yield + 8.14%), 06/05/2026 (Acquired 05/24/2023; Cost $2,129,000) (b)(c)(d) | 2,129,000 | 2,262,628 | |||||

Sanders Re III 2024-1 Class A, 10.29% (3 Month U.S. Treasury Bill Money Market Yield + 5.75%), 04/07/2028 (Acquired 01/16/2024; Cost $1,627,000) (b)(c)(d) | 1,627,000 | 1,684,100 | |||||

Solomon Re 2023-1 Class A, 10.04% (3 Month U.S. Treasury Bill Money Market Yield + 5.52%), 06/08/2026 (Acquired 06/12/2023; Cost $379,000) (b)(c)(d) | 379,000 | 389,468 | |||||

73,603,310 | |||||||

Windstorm - 6.6% | |||||||

Alamo Re 2022-1 Class A, 12.04% (3 Month U.S. Treasury Bill Money Market Yield + 7.52%), 06/07/2025 (Acquired 07/27/2022 - 03/27/2024; Cost $1,352,456) (b)(c)(d) | 1,356,000 | 1,383,202 | |||||

Alamo Re 2023-1 Class A, 12.91% (3 Month U.S. Treasury Bill Money Market Yield + 8.39%), 06/07/2026 (Acquired 04/12/2023; Cost $2,579,000) (b)(c)(d) | 2,579,000 | 2,686,949 | |||||

Alamo Re 2024-1 Class A, 6.00% (3 Month U.S. Treasury Bill Money Market Yield + 6.00%), 06/07/2027 (Acquired 04/04/2024; Cost $3,571,000) (b)(c)(d) | 3,571,000 | 3,730,527 | |||||

Alamo Re 2024-1 Class B, 12.29% (3 Month U.S. Treasury Bill Money Market Yield + 7.75%), 06/07/2027 (Acquired 04/04/2024; Cost $4,761,000) (b)(c)(d) | 4,761,000 | 4,949,352 | |||||

Alamo Re 2024-1 Class C, 15.79% (3 Month U.S. Treasury Bill Money Market Yield + 11.25%), 06/07/2026 (Acquired 04/04/2024; Cost $3,851,000) (b)(c)(d) | 3,851,000 | 4,069,425 | |||||

Armor Re II 2024-1 Class A, 14.79% (3 Month U.S. Treasury Bill Money Market Yield + 10.25%), 05/07/2027 (Acquired 04/11/2024; Cost $1,321,000) (b)(c)(d) | 1,321,000 | 1,378,285 | |||||

Bayou Re 2023-1 Class A, 17.43% (3 Month U.S. Treasury Bill Money Market Yield + 12.91%), 05/26/2026 (Acquired 05/11/2023; Cost $750,000) (b)(c)(d) | 750,000 | 802,988 | |||||

Bayou Re 2023-1 Class B, 24.22% (3 Month U.S. Treasury Bill Money Market Yield + 19.70%), 05/26/2026 (Acquired 05/11/2023; Cost $1,206,000) (b)(c)(d) | 1,206,000 | 1,338,584 | |||||

Bayou Re 2024-1 Class A, 13.04% (3 Month U.S. Treasury Bill Money Market Yield + 8.50%), 04/30/2027 (Acquired 04/18/2024; Cost $1,257,000) (b)(c)(d) | 1,257,000 | 1,317,943 | |||||

Bayou Re 2024-1 Class B, 23.04% (3 Month U.S. Treasury Bill Money Market Yield + 18.50%), 04/30/2027 (Acquired 04/18/2024; Cost $419,000) (b)(c)(d) | 419,000 | 454,519 | |||||

Blue Ridge Re 2023-1 Class A, 9.77% (3 Month U.S. Treasury Bill Money Market Yield + 5.25%), 01/08/2027 (Acquired 11/14/2023; Cost $2,068,000) (b)(c)(d) | 2,068,000 | 2,104,692 | |||||

Blue Ridge Re 2023-1 Class B, 12.52% (3 Month U.S. Treasury Bill Money Market Yield + 8.00%), 01/08/2027 (Acquired 11/14/2023; Cost $2,518,000) (b)(c)(d) | 2,518,000 | 2,616,440 | |||||

Bonanza Re 2020-2 Class A, 9.45% (3 Month U.S. Treasury Bill Money Market Yield + 4.93%), 12/23/2024 (Acquired 12/15/2020; Cost $1,490,000) (b)(c)(d) | 1,490,000 | 1,484,985 | |||||

10 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Par | Value | ||||||

Windstorm - 6.6% (continued) | |||||||

Cape Lookout Re 2023-1 Class A, 12.94% (3 Month U.S. Treasury Bill Money Market Yield + 8.42%), 04/28/2026 (Acquired 04/14/2023 - 09/17/2024; Cost $3,454,849) (b)(c)(d) | $3,445,000 | $3,591,624 | |||||

Cape Lookout Re 2024-1 Class A, 12.54% (3 Month U.S. Treasury Bill Money Market Yield + 8.00%), 04/05/2027 (Acquired 03/12/2024 - 09/13/2024; Cost $4,189,274) (b)(c)(d) | 4,180,000 | 4,281,281 | |||||

Catahoula Re II 2022-1 Class A, 15.76% (3 Month U.S. Treasury Bill Money Market Yield + 11.24%), 06/16/2025 (Acquired 09/02/2022; Cost $1,995,471) (b)(c)(d) | 2,000,000 | 2,115,919 | |||||

Charles River Re 2024-1 Class A, 11.29% (3 Month U.S. Treasury Bill Money Market Yield + 6.75%), 05/10/2027 (Acquired 04/05/2024; Cost $885,000) (b)(c)(d) | 885,000 | 909,012 | |||||

Citrus Re 2023-1 Class A, 11.11% (3 Month U.S. Treasury Bill Money Market Yield + 6.59%), 06/07/2026 (Acquired 04/27/2023; Cost $1,009,000) (b)(c)(d) | 1,009,000 | 1,052,505 | |||||

Citrus Re 2023-1 Class B, 13.29% (3 Month U.S. Treasury Bill Money Market Yield + 8.77%), 06/07/2026 (Acquired 04/27/2023; Cost $876,000) (b)(c)(d) | 876,000 | 914,899 | |||||

Citrus Re 2024-1 Class B, 15.04% (3 Month U.S. Treasury Bill Money Market Yield + 10.50%), 06/07/2027 (Acquired 03/19/2024; Cost $508,000) (b)(c)(d) | 508,000 | 525,177 | |||||

Commonwealth Re 2023-1 Class A, 8.79% (3 Month U.S. Treasury Bill Money Market Yield + 4.27%), 07/08/2026 (Acquired 06/07/2023; Cost $783,000) (b)(c)(d) | 783,000 | 803,853 | |||||

Everglades Re II 2024-1 Class A, 15.04% (3 Month U.S. Treasury Bill Money Market Yield + 10.50%), 05/13/2027 (Acquired 05/15/2024; Cost $2,964,000) (b)(c)(d) | 2,964,000 | 3,101,046 | |||||

Everglades Re II 2024-1 Class B, 16.04% (3 Month U.S. Treasury Bill Money Market Yield + 11.50%), 05/13/2027 (Acquired 05/15/2024; Cost $2,980,000) (b)(c)(d) | 2,980,000 | 3,116,910 | |||||

Everglades Re II 2024-1 Class C, 17.29% (3 Month U.S. Treasury Bill Money Market Yield + 12.75%), 05/13/2027 (Acquired 05/15/2024; Cost $2,066,000) (b)(c)(d) | 2,066,000 | 2,169,693 | |||||

First Coast Re III 2021-1 Class A, 11.26% (3 Month U.S. Treasury Bill Money Market Yield + 6.74%), 04/07/2025 (Acquired 08/18/2023; Cost $372,948) (b)(c)(d) | 378,000 | 380,174 | |||||

Fish Pond Re 2024-1 Class A, 8.54% (3 Month U.S. Treasury Bill Money Market Yield + 4.00%), 01/08/2027 (Acquired 12/22/2023; Cost $842,000) (b)(c)(d) | 842,000 | 858,467 | |||||

Gateway Re 2023-1 Class A, 18.48% (3 Month U.S. Treasury Bill Money Market Yield + 13.96%), 02/24/2026 (Acquired 02/03/2023; Cost $2,215,000) (b)(c)(d) | 2,215,000 | 2,383,752 | |||||

Gateway Re 2023-1 Class B, 24.92% (3 Month U.S. Treasury Bill Money Market Yield + 20.40%), 02/24/2026 (Acquired 02/03/2023; Cost $479,000) (b)(c)(d) | 479,000 | 518,663 | |||||

Gateway Re 2023-3 Class A, 14.52% (3 Month U.S. Treasury Bill Money Market Yield + 10.00%), 07/08/2026 (Acquired 07/14/2023; Cost $594,000) (b)(c)(d) | 594,000 | 619,056 | |||||

Gateway Re 2024-1 Class A, 4.54% (3 Month U.S. Treasury Bill Money Market Yield + 0.00%), 12/23/2024 (Acquired 03/11/2024; Cost $733,242) (b)(c)(d) | 744,000 | 734,989 | |||||

Gateway Re 2024-1 Class AA, 10.04% (3 Month U.S. Treasury Bill Money Market Yield + 5.50%), 07/08/2027 (Acquired 03/11/2024; Cost $638,000) (b)(c)(d) | 638,000 | 655,206 | |||||

Gateway Re 2024-2 Class C, 4.54% (3 Month U.S. Treasury Bill Money Market Yield + 0.00%), 12/23/2024 (Acquired 03/28/2024; Cost $1,121,119) (b)(c)(d) | 1,141,000 | 1,121,407 | |||||

Gateway Re 2024-4 Class A, 4.54% (3 Month U.S. Treasury Bill Money Market Yield + 0.00%), 01/08/2025 (Acquired 06/24/2024; Cost $399,613) (b)(c)(d) | 425,000 | 410,335 | |||||

Gateway Re II 2023-1 Class A, 13.42% (3 Month U.S. Treasury Bill Money Market Yield + 8.90%), 04/27/2026 (Acquired 04/13/2023; Cost $608,000) (b)(c)(d) | 608,000 | 647,442 | |||||

Hestia Re 2022-1 Class A, 14.60% (3 Month U.S. Treasury Bill Money Market Yield + 10.08%), 04/22/2025 (Acquired 02/05/2024; Cost $305,441) (b)(c)(d) | 309,000 | 254,925 | |||||

Integrity Re 2023-1 Class A, 17.38% (3 Month U.S. Treasury Bill Money Market Yield + 12.86%), 06/06/2025 (Acquired 03/23/2023; Cost $687,000) (b)(c)(d) | 687,000 | 673,259 | |||||

Integrity Re 2024-1 Class A, 15.04% (3 Month U.S. Treasury Bill Money Market Yield + 10.50%), 06/06/2026 (Acquired 03/01/2024; Cost $542,000) (b)(c)(d) | 542,000 | 525,567 | |||||

Integrity Re 2024-1 Class B, 17.79% (3 Month U.S. Treasury Bill Money Market Yield + 13.25%), 06/06/2026 (Acquired 03/01/2024; Cost $310,000) (b)(c)(d) | 310,000 | 253,657 | |||||

Integrity Re 2024-1 Class C, 21.54% (3 Month U.S. Treasury Bill Money Market Yield + 17.00%), 06/06/2026 (Acquired 03/01/2024; Cost $542,000) (b)(c)(d) | 542,000 | 425,469 | |||||

Integrity Re 2024-1 Class D, 27.54% (3 Month U.S. Treasury Bill Money Market Yield + 23.00%), 06/06/2026 (Acquired 03/01/2024; Cost $852,000) (b)(c)(d) | 852,000 | 551,669 | |||||

Lightning Re 2023-1 Class A, 15.52% (3 Month U.S. Treasury Bill Money Market Yield + 11.00%), 03/31/2026 (Acquired 03/20/2023 - 04/10/2024; Cost $4,290,197) (b)(c)(d) | 4,190,000 | 4,430,923 | |||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 11 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Par | Value | ||||||

Windstorm - 6.6% (continued) | |||||||

Longleaf Pine Re 2024-1 Class A, 22.04% (3 Month U.S. Treasury Bill Money Market Yield + 17.50%), 05/25/2027 (Acquired 05/10/2024; Cost $1,190,000) (b)(c)(d) | $1,190,000 | $1,291,797 | |||||

Lower Ferry Re 2023-1 Class A, 8.95% (3 Month U.S. Treasury Bill Money Market Yield + 4.43%), 07/08/2026 (Acquired 06/23/2023; Cost $456,000) (b)(c)(d) | 456,000 | 468,192 | |||||

Lower Ferry Re 2023-1 Class B, 9.79% (3 Month U.S. Treasury Bill Money Market Yield + 5.27%), 07/08/2026 (Acquired 06/23/2023; Cost $1,139,000) (b)(c)(d) | 1,139,000 | 1,175,377 | |||||

Mayflower Re 2023-1 Class A, 4.69% (3 Month U.S. Treasury Bill Money Market Yield + 4.69%), 07/08/2026 (Acquired 06/26/2023; Cost $837,000) (b)(c)(d) | 837,000 | 861,421 | |||||

Mayflower Re 2023-1 Class B, 10.53% (3 Month U.S. Treasury Bill Money Market Yield + 6.02%), 07/08/2026 (Acquired 06/26/2023; Cost $2,082,000) (b)(c)(d) | 2,082,000 | 2,169,391 | |||||

Mayflower Re 2024-1 Class A, 4.50% (3 Month U.S. Treasury Bill Money Market Yield + 4.50%), 07/08/2027 (Acquired 06/21/2024; Cost $650,000) (b)(c)(d) | 650,000 | 667,935 | |||||

Metrocat Re 2023-1 Class A, 5.75% (3 Month U.S. Treasury Bill Money Market Yield + 5.75%), 05/08/2026 (Acquired 05/12/2023; Cost $321,000) (b)(c)(d) | 321,000 | 329,065 | |||||

Nature Coast Re 2023-1 Class A, 14.54% (3 Month U.S. Treasury Bill Money Market Yield + 10.00%), 12/07/2026 (Acquired 11/16/2023; Cost $1,341,000) (b)(c)(d) | 1,341,000 | 1,358,323 | |||||

Nature Coast Re 2023-1 Class B, 18.04% (3 Month U.S. Treasury Bill Money Market Yield + 13.50%), 12/07/2026 (Acquired 11/16/2023; Cost $470,000) (b)(c)(d) | 470,000 | 474,207 | |||||

Nature Coast Re 2024-1 Class A, 19.29% (3 Month U.S. Treasury Bill Money Market Yield + 14.75%), 06/07/2028 (Acquired 06/17/2024; Cost $469,000) (b)(c)(d) | 469,000 | 491,422 | |||||

Palm Re 2024-1 Class A, 14.04% (3 Month U.S. Treasury Bill Money Market Yield + 9.50%), 06/07/2027 (Acquired 04/04/2024; Cost $928,000) (b)(c)(d) | 928,000 | 960,708 | |||||

Purple Re 2023-1 Class A, 17.55% (1 Month Term SOFR + 12.81%), 04/24/2026 (Acquired 04/06/2023; Cost $959,000) (b)(c)(d) | 959,000 | 950,176 | |||||

Purple Re 2023-2 Class A, 15.02% (3 Month U.S. Treasury Bill Money Market Yield + 10.50%), 06/05/2026 (Acquired 06/27/2023; Cost $674,000) (b)(c)(d) | 674,000 | 692,486 | |||||

Purple Re 2024-1 Class A, 13.54% (3 Month U.S. Treasury Bill Money Market Yield + 9.00%), 06/07/2027 (Acquired 04/02/2024; Cost $2,373,000) (b)(c)(d) | 2,373,000 | 2,419,784 | |||||

Sabine Re 2024-1 Class A, 12.79% (3 Month U.S. Treasury Bill Money Market Yield + 8.25%), 04/07/2027 (Acquired 03/26/2024; Cost $488,000) (b)(c)(d) | 488,000 | 505,909 | |||||

Winston Re 2024-1 Class A, 14.79% (3 Month U.S. Treasury Bill Money Market Yield + 10.25%), 02/26/2027 (Acquired 02/14/2024; Cost $927,000) (b)(c)(d) | 927,000 | 927,227 | |||||

Winston Re 2024-1 Class B, 16.29% (3 Month U.S. Treasury Bill Money Market Yield + 11.75%), 02/26/2027 (Acquired 02/14/2024; Cost $387,000) (b)(c)(d) | 387,000 | 320,507 | |||||

82,408,697 | |||||||

209,910,485 | |||||||

TOTAL EVENT LINKED BONDS (Cost $242,160,936) | 243,147,525 | ||||||

QUOTA SHARES AND OTHER REINSURANCE-RELATED SECURITIES - 58.4% (a) | |||||||

Participation Notes - 0.0% (e) | |||||||

Global - 0.0% (e) | |||||||

Multiperil - 0.0% (e) | |||||||

Eden Re II 2021-1 Class B (Acquired 12/21/2020; Cost $621,595) (b)(c)(d)(f)(g)(h) | 621,595 | 76,434 | |||||

Eden Re II 2022-1 Class B (Acquired 12/17/2021; Cost $19,608) (b)(c)(d)(f)(g)(h) | 19,608 | 17,841 | |||||

Eden Re II 2023-1 Class B (Acquired 12/22/2022; Cost $5,282) (b)(c)(d)(f)(g) | 5,282 | 99,376 | |||||

Sussex Re 2021-A (Acquired 12/29/2020; Cost $340,698) (c)(d)(f)(g) | 344,570 | 5,328 | |||||

Sussex Re 2022-A (Acquired 01/05/2022; Cost $1,817,006) (c)(d)(f)(g) | 1,820,000 | 6,162 | |||||

205,141 | |||||||

Total Participation Notes (Cost $2,804,189) | 205,141 | ||||||

12 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Shares | Value | ||||||

Preference Shares - 58.4% | |||||||

Global - 57.4% | |||||||

Marine/Energy - 0.0% (e) | |||||||

Kauai (Artex Segregated Account Company) (Acquired 01/07/2016; Cost $22,374,485) (c)(d)(f)(g)(h) | 51,394 | $51,814 | |||||

Multiperil - 57.4% | |||||||

Arenal (Artex Segregated Account Company) (Acquired 05/07/2015 - 12/22/2017; Cost $30,738,112) (c)(d)(f)(g) | 165,450 | 43,213,928 | |||||

Baldwin (Horseshoe Re) (Acquired 01/04/2018 - 01/22/2019; Cost $25,096,972) (c)(d)(f)(g)(h) | 1,328,746 | — | |||||

Bowery (Artex Segregated Account Company) (Acquired 09/29/2017; Cost $29,078,495) (c)(d)(f)(g) | 200,075 | 39,731,619 | |||||

Brighton (Horseshoe Re) (Acquired 06/12/2020; Cost $-) (c)(d)(f)(g) | 1,022,526 | 274,097 | |||||

Cypress (Horseshoe Re) (Acquired 05/31/2017 - 09/29/2017; Cost $5,611,293) (c)(d)(f)(g)(h) | 125,090,500 | 2,478,293 | |||||

Emerald Lake (Artex Segregated Account Company) (Acquired 12/16/2015 - 12/17/2018; Cost $28,051,854) (c)(d)(f)(g)(h) | 504,899 | — | |||||

Florblanca (Artex Segregated Account Company) (Acquired 12/29/2016 - 12/21/2017; Cost $11,047,610) (c)(d)(f)(g) | 77,550 | 15,486,802 | |||||

Freeport (Horseshoe Re) (Acquired 04/04/2018; Cost $22,890,927) (c)(d)(f)(g)(h) | 750,718 | — | |||||

Harambee Re 2018 (Acquired 12/15/2017; Cost $-) (c)(d)(f)(g) | 276 | — | |||||

Harambee Re 2019 (Acquired 12/21/2018; Cost $-) (c)(d)(f)(g) | 2,199 | — | |||||

Hatteras (Artex Segregated Account Company) (Acquired 12/30/2014 - 04/11/2019; Cost $61,009,247) (c)(d)(f)(g) | 58,673 | 54,570,755 | |||||

Hudson Charles (Mt. Logan Re) (Acquired 01/02/2014 - 01/13/2017; Cost $12,736,141) (c)(d)(f)(g) | 12,736 | 19,838,027 | |||||

Hudson Charles 2 (Mt. Logan Re) (Acquired 03/31/2017; Cost $19,105,594) (c)(d)(f)(g) | 19,106 | 35,943,403 | |||||

Iseo (Artex Segregated Account Company) (Acquired 09/08/2017; Cost $-) (c)(d)(f)(g)(h) | 183,543 | — | |||||

Kensington (Horseshoe Re) (Acquired 08/16/2018 - 08/11/2020; Cost $-) (c)(d)(f)(g) | 954,585 | 228,358 | |||||

Latigo (Artex Segregated Account Company) (Acquired 01/06/2014 - 11/01/2018; Cost $16,290,758) (c)(d)(f)(g) | 473 | 22,641,423 | |||||

LRe 2019 (Lorenz Re Ltd.) (Acquired 07/30/2019; Cost $-) (c)(d)(f)(g) | — | 19,983 | |||||

Mackinac (Artex Segregated Account Company) (Acquired 02/05/2015 - 01/09/2018; Cost $-) (c)(d)(f)(g)(h) | 55,584 | 7,523,303 | |||||

Madison (Artex Segregated Account Company) (Acquired 12/12/2016 - 02/03/2020; Cost $32,872,553) (c)(d)(f)(g)(h) | 97,141 | 17,824,455 | |||||

Magnolia (Artex Segregated Account Company) (Acquired 06/20/2024; Cost $24,436,480) (c)(d)(f)(g) | 24,436 | 28,666,899 | |||||

Mohonk (Artex Segregated Account Company) (Acquired 12/24/2013 - 04/11/2019; Cost $63,132,654) (c)(d)(f)(g) | 103 | 56,241,608 | |||||

Mulholland (Artex Segregated Account Company) (Acquired 12/26/2013 - 12/31/2015; Cost $607,673) (c)(d)(f)(g)(h) | 114 | 64,251 | |||||

Pelham (Horseshoe Re) (Acquired 01/02/2018 - 04/25/2018; Cost $18,357,632) (c)(d)(f)(g)(h) | 264,553 | 6,061,760 | |||||

Peregrine LCA (Acquired 12/28/2018 - 06/07/2019; Cost $12,768,157) (c)(d)(f)(g) | 2,252,060 | 35,701,191 | |||||

Peregrine LCA2 (Acquired 01/09/2024; Cost $29,902,397) (c)(d)(f)(g)(h) | 2,990,240 | 35,304,598 | |||||

Rondout (Artex Segregated Account Company) (Acquired 07/15/2019; Cost $16,962,302) (c)(d)(f)(g) | 48,289 | 42,636,520 | |||||

Sheepshead (Horseshoe Re) (Acquired 06/12/2020; Cost $-) (c)(d)(f)(g) | 969,034 | 259,202 | |||||

SR0001 (Horseshoe Re) (Acquired 07/10/2015 - 06/28/2016; Cost $-) (c)(d)(f)(g) | 1,757 | 74,392 | |||||

St. Kevins (Artex Segregated Account Company) (Acquired 12/29/2016 - 06/27/2018; Cost $22,149,263) (c)(d)(f)(g) | 42,944 | 2,569,725 | |||||

Thopas Re Ltd. 2024-2 (S) (Acquired 06/26/2024; Cost $24,405,926) (c)(d)(f)(g)(h) | 244,059 | 26,557,263 | |||||

Viribus Re 2018 (Acquired 12/22/2017; Cost $-) (c)(d)(f)(g) | 265,173 | — | |||||

Viribus Re 2019 (Acquired 12/26/2018 - 10/23/2020; Cost $507,130) (c)(d)(f)(g) | 526,336 | — | |||||

Windsor (Horseshoe Re) (Acquired 12/29/2017; Cost $-) (c)(d)(f)(g) | 1,230,204 | — | |||||

Woodside (Horseshoe Re) (Acquired 06/12/2020; Cost $-) (c)(d)(f)(g) | 1,012,875 | 268,102 | |||||

Yoho (Artex Segregated Account Company) (Acquired 05/17/2016 - 06/05/2020; Cost $49,210,984) (c)(d)(f)(g)(h) | 357,363 | 3,948,272 | |||||

Yorkville (Artex Segregated Account Company) (Acquired 05/31/2019 - 06/03/2020; Cost $95,132,000) (c)(d)(f)(g) | 143,394 | 213,782,470 | |||||

711,910,699 | |||||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 13 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

Shares | Value | ||||||

United States - 1.0% | |||||||

Multiperil - 1.0% | |||||||

SR0005 (Horseshoe Re) (Acquired 04/15/2016; Cost $6,360,627) (c)(d)(f)(g)(h) | 6,966,774 | $— | |||||

Trouvaille Re Ltd. (Acquired 03/25/2024; Cost $10,606,960) (c)(d)(f)(g)(h) | 1,060,696 | 11,772,688 | |||||

11,772,688 | |||||||

Windstorm - 0.0% (e) | |||||||

Riverdale (Horseshoe Re) (Acquired 06/10/2020; Cost $11,107,565) (c)(d)(f)(g)(h) | 251,610 | — | |||||

SR0006 (Horseshoe Re) (Acquired 08/09/2016; Cost $2,274,842) (c)(d)(f)(g)(h) | 39,381,541 | 273,702 | |||||

273,702 | |||||||

| 12,046,390 | ||||||

Total Preference Shares ($704,826,631) | 724,008,903 | ||||||

TOTAL QUOTA SHARES AND OTHER REINSURANCE-RELATED SECURITIES (Cost $707,630,820) | 724,214,044 | ||||||

LIMITED LIABILITY PARTNERSHIPS - 1.5% | |||||||

Point Dume LLP (d)(f)(h)(g)(i) | 18,433,834 | ||||||

TOTAL LIMITED LIABILITY PARTNERSHIPS (Cost $9,042,607) | 18,433,834 | ||||||

SHORT-TERM INVESTMENTS - 20.0% | |||||||

Money Market Funds - 20.0% | |||||||

Fidelity Investments Money Market Funds - Government Portfolio - Class Institutional, 4.70% (j) | 123,746,405 | 123,746,405 | |||||

First American Government Obligations Fund - Class X, 4.78% (j) | 100,489 | 100,489 | |||||

First American Treasury Obligations Fund - Class X, 4.79% (j) | 100,489 | 100,489 | |||||

Invesco Treasury Portfolio - Class Institutional, 4.74% (j) | 100,489 | 100,489 | |||||

Morgan Stanley Institutional Liquidity Funds - Government Portfolio - Class Institutional, 4.78% (j) | 123,846,895 | 123,846,895 | |||||

TOTAL SHORT-TERM INVESTMENTS (Cost $247,894,767) | 247,894,767 | ||||||

TOTAL INVESTMENTS - 100.6% (Cost $1,206,729,130) | 1,233,690,170 | ||||||

ASSETS in Excess of Other LIABILITIES - 0.5% | 5,818,311 | ||||||

TOTAL NET ASSETS - 100.0% | $1,239,508,781 | ||||||

| (a) | Country shown is geographic area of peril risk. |

| (b) | Although security is restricted as to resale, the Fund’s Adviser has determined this security to be liquid based upon procedures approved by the Board of Trustees. The aggregate value of these securities at October 31, 2024 was $243,341,176, which represented 19.6% of net assets. |

| (c) | Security is restricted as to resale. |

| (d) | Foreign issued security. Total foreign securities by country of domicile are $985,795,403 Value determined using significant unobservable inputs. Foreign concentration is as follows: Bermuda: 75.3%, Great Britain 1.6% Cayman Islands: 1.1%, Supranational: 0.8%, Singapore: 0.5% and Ireland: 0.3%. |

| (e) | Rounds to zero. |

| (f) | Value determined using significant unobservable inputs |

| (g) | Security is fair valued by the Adviser Valuation Committee using an insurance industry model pursuant to procedures approved by the Board of Trustees. The aggregate value of these securities is $742,647,878, which represents 59.9% of net assets. |

14 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Consolidated Schedule of Investments | October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | ||

| (h) | Non-income producing security. |

| (i) | The partnership, a subsidiary of Point Dume Holdings Ltd, is a member of the Lloyd’s of London marketplace through which it may generate profits from participations in the insurance or reinsurance of activities of certain underwriters. Members are required to post collateral for potential losses, which is in the form of a trust deed and is included on the consolidated Statement of Assets and Liabilities. |

| (j) | The rate shown represents the 7-day annualized effective yield as of October 31, 2024. |

Stone Ridge Funds | Annual Report | October 31, 2024 | 15 | |||||

Consolidated Statement of Assets and Liabilities | As of October 31, 2024 | ||

STONE RIDGE REINSURANCE RISK PREMIUM INTERVAL FUND | |||||

ASSETS: | |||||

Investments, at fair value(1) | $1,233,690,170 | ||||

Foreign currencies at custodian, at value(2) | 17,835 | ||||

Receivable for fund shares sold | 366,030 | ||||

Interest receivable | 3,412,149 | ||||

Collateral held for LLP(3) | 6,585,670 | ||||

Other assets | 70,951 | ||||

Total assets | 1,244,142,805 | ||||

LIABILITIES: | |||||

Payable to Adviser | 2,072,508 | ||||

Due to other | 1,739,690 | ||||

Payable for Chief Compliance Officer compensation | 5,000 | ||||

Payable to Trustees | 36,657 | ||||

Accrued service fees | 51,813 | ||||

Accrued distribution and servicing fees | 51,813 | ||||

Accrued fund accounting and administration fees | 112,383 | ||||

Accrued audit and tax related fees | 340,207 | ||||

Accrued printing and mailing fees | 59,228 | ||||

Other accrued expenses | 164,725 | ||||

Total liabilities | 4,634,024 | ||||

Total net assets | $1,239,508,781 | ||||

NET ASSETS CONSIST OF: | |||||

Capital stock | $2,016,325,316 | ||||

Total accumulated loss | (776,816,535) | ||||

Total net assets | $1,239,508,781 | ||||

Net Assets | $1,239,508,781 | ||||

Shares outstanding | 21,116,680 | ||||

Net asset value, offering and redemption price per share | $58.70 | ||||

(1)Cost of Investments | $1,206,729,130 | ||||

(2)Cost of foreign currencies at custodian | $17,762 | ||||

(3)Represents cash pledged as collateral for Point Dume LLP. The cash pledged as collateral is restricted as to withdrawal or use under the terms of a contractual agreement. | |||||

16 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Consolidated Statement of Operations | For the Year Ended October 31, 2024 | ||

STONE RIDGE REINSURANCE RISK PREMIUM INTERVAL FUND | |||||

INVESTMENT INCOME: | |||||

Dividend income | $175,399,244 | ||||

Interest income | 41,819,415 | ||||

Total investment income | 217,218,659 | ||||

EXPENSES: | |||||

Advisory fees (See Note 4) | 22,306,018 | ||||

Fund accounting and administration fees | 812,650 | ||||

Service fees | 709,655 | ||||

Distribution and service fees | 709,649 | ||||

Audit and tax related fees | 386,332 | ||||

Legal fees | 222,658 | ||||

Transfer agency fees and expenses | 220,699 | ||||

Trustees fees and expenses | 144,641 | ||||

Custody fees | 70,853 | ||||

Chief Compliance Officer compensation | 60,284 | ||||

Federal and state registration fees | 48,255 | ||||

Other expenses | 150,606 | ||||

Total expenses | 25,842,300 | ||||

Net investment income | 191,376,359 | ||||

NET REALIZED AND UNREALIZED GAIN (LOSS): | |||||

Net realized loss on: | |||||

Investments | (24,182,233) | ||||

Foreign currency | (26,654) | ||||

Net change in unrealized appreciation (depreciation) on: | |||||

Investments | 108,322,656 | ||||

Foreign currency | (434) | ||||

Net realized and unrealized gain | 84,113,335 | ||||

Net increase in net assets resulting from operations | $275,489,694 | ||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 17 | |||||

Consolidated Statement of Changes in Net Assets | |||

STONE RIDGE REINSURANCE RISK PREMIUM INTERVAL FUND | ||||||||

Year Ended October 31, 2024 | Year Ended October 31, 2023 | |||||||

OPERATIONS: | ||||||||

Net investment income | $191,376,359 | $39,357,897 | ||||||

Net realized gain (loss) on: | ||||||||

Investments | (24,182,233) | (24,923,278) | ||||||

Foreign currency | (26,654) | 9,757 | ||||||

Net change in unrealized appreciation (depreciation) on: | ||||||||

Investments | 108,322,656 | 363,164,041 | ||||||

Foreign currency | (434) | (256) | ||||||

Net increase in net assets resulting from operations | 275,489,694 | 377,608,161 | ||||||

DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||

Distributions | (188,300,000) | (5,618,485) | ||||||

Total distributions | (188,300,000) | (5,618,485) | ||||||

CAPITAL SHARE TRANSACTIONS: | ||||||||

Proceeds from shares sold | 179,877,556 | 128,256,089 | ||||||

Proceeds from shares issued to holders in reinvestment of dividends | 44,383,083 | 3,714,500 | ||||||

Cost of shares redeemed | (229,731,648) | (351,694,101) | ||||||

Net decrease in net assets from capital share transactions | (5,471,009) | (219,723,512) | ||||||

Total increase in net assets | 81,718,685 | 152,266,164 | ||||||

NET ASSETS: | ||||||||

Beginning of year | 1,157,790,096 | 1,005,523,932 | ||||||

End of year | $1,239,508,781 | $1,157,790,096 | ||||||

18 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Consolidated Statement of Cash Flows | For Year Ended October 31, 2024 | ||

Stone Ridge Reinsurance Risk Premium Interval Fund | |||||

CASH FLOWS FROM OPERATING ACTIVITIES | |||||

Net increase in net assets resulting from operations | $275,489,694 | ||||

Adjustments to reconcile net increase in net assets resulting from operations to net cash provided by operating activities: | |||||

Net realized and unrealized gain on investments: | (84,140,423) | ||||

Amortization and accretion of premium & discount | (3,232,515) | ||||

Changes in assets and liabilities: | |||||

Interest receivable | 636,439 | ||||

Payable to Adviser | 145,858 | ||||

Payable to Custodian | (23,366) | ||||

Payable to Trustees | (1,730) | ||||

Accrued distribution and servicing fees | (11,917) | ||||

Accrued service fees | (11,910) | ||||

Payable for Chief Compliance Officer compensation | 284 | ||||

Accrued fund accounting and administration fees | (58,179) | ||||

Accrued audit and tax related fees | 126,874 | ||||

Due to other | 1,739,690 | ||||

Accrued printing and mailing fees | (116,220) | ||||

Other accrued expenses | (207,875) | ||||

Other assets | (11,770) | ||||

Purchases of investments | (203,062,187) | ||||

Proceeds from sale of investments | 237,419,083 | ||||

Proceeds from cost adjustments | 63,635,583 | ||||

Net purchases and sales of short-term investments | (130,023,254) | ||||

Net cash provided by operating activities | 158,292,159 | ||||

CASH FLOWS FROM FINANCING ACTIVITIES: | |||||

Proceeds from shares issued | 179,711,036 | ||||

Payment on shares repurchased | (229,731,648) | ||||

Cash distributions to shareholders | (143,916,917) | ||||

Net cash used in financing activities | (193,937,529) | ||||

Net decrease in cash and restricted cash | (35,645,370) | ||||

Cash and restricted cash, beginning of year | 42,248,875 | ||||

Cash and restricted cash, end of year | $6,603,505 | ||||

Supplemental Disclosures of CASH FLOW AND NON-CASH INFORMATION: | |||||

Reinvested distributions | $44,383,083 | ||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 19 | |||||

Consolidated Financial Highlights | |||

STONE RIDGE REINSURANCE RISK PREMIUM INTERVAL FUND | |||||||||||||||||

Year Ended October 31, 2024 | Year Ended October 31, 2023 | Year Ended October 31, 2022 | Year Ended October 31, 2021 | Year Ended October 31, 2020(1) | |||||||||||||

Per Share Data: | |||||||||||||||||

Net asset value, beginning of year | $54.75 | $38.17 | $37.82 | $40.84 | $41.15 | ||||||||||||

Income (loss) from investment operations | |||||||||||||||||

Net investment income (loss)(2) | 9.26 | 1.75 | 0.37 | 0.54 | 0.21 | ||||||||||||

Net realized and unrealized gains (losses) | 4.00 | 15.10 | (0.02) | (2.59) | 0.04(3) | ||||||||||||

Total from investment operations | 13.26 | 16.85 | 0.35 | (2.05) | 0.25 | ||||||||||||

Less distributions to shareholders | |||||||||||||||||

Dividends from net realized gains | — | — | — | — | — | ||||||||||||

Dividends from net investment income | (9.31) | (0.27) | — | (0.97) | (0.56) | ||||||||||||

Total distributions | (9.31) | (0.27) | — | (0.97) | (0.56) | ||||||||||||

Net asset value, end of year | $58.70 | $54.75 | $38.17 | $37.82 | $40.84 | ||||||||||||

Total return(4) | 28.25% | 44.18% | 0.93% | (5.18)% | 0.67% | ||||||||||||

Supplemental Data and Ratios: | |||||||||||||||||

Net assets, end of period (000s) | $1,239,509 | $1,157,790 | $1,005,524 | $1,658,681 | $2,818,599 | ||||||||||||

Ratio of expenses to average net assets | 2.32% | 2.34% | 2.45% | 2.36% | 2.35% | ||||||||||||

Ratio of net investment income (loss) to average net assets | 17.16% | 3.89% | 0.95% | 1.34% | 0.52% | ||||||||||||

Portfolio turnover rate | 21.52% | 11.31% | 6.54% | 1.49% | 32.67% | ||||||||||||

| (1) | Effective July 31, 2020, the Fund effected a 1:5 reverse stock split. All historical per share information has been retroactively adjusted to reflect this reverse stock split. |

| (2) | Net investment income (loss) per share has been calculated based on average shares outstanding during the period. |

| (3) | The amount of net realized and unrealized gain per share does not correspond with the net realized and unrealized loss reported within the Statement of Changes due to the timing of capital share transactions and fluctuating market values. |

| (4) | Total return represents the rate that a shareholder would have earned (or lost) on an investment in the Fund (assuming the reinvestment of all dividends and distributions). |

20 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

Stone Ridge Funds | Annual Report | October 31, 2024 | 21 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

22 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

Stone Ridge Funds | Annual Report | October 31, 2024 | 23 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

DESCRIPTION | LEVEL 1 | LEVEL 2 | LEVEL 3 | TOTAL | ||||||||||

Assets | ||||||||||||||

Event-Linked Bonds | ||||||||||||||

Chile | $— | $2,987,484 | $— | $2,987,484 | ||||||||||

Europe | — | 4,604,996 | — | 4,604,996 | ||||||||||

Global | — | 12,291,536 | 1,498,655 | 13,790,191 | ||||||||||

Jamaica | — | 2,069,019 | — | 2,069,019 | ||||||||||

Japan | — | 3,802,792 | — | 3,802,792 | ||||||||||

Mexico | — | 4,654,943 | — | 4,654,943 | ||||||||||

New Zealand | — | 1,327,615 | — | 1,327,615 | ||||||||||

United States(1) | — | 209,799,445 | 111,040 | 209,910,485 | ||||||||||

Total Event-Linked Bonds | — | 241,537,830 | 1,609,695 | 243,147,525 | ||||||||||

Quota Shares and Other Reinsurance-Related Securities | ||||||||||||||

Participation Notes(2) | — | — | 205,141 | 205,141 | ||||||||||

Preference Shares | ||||||||||||||

Global(1) | — | — | 711,962,513 | 711,962,513 | ||||||||||

United States(1) | — | — | 12,046,390 | 12,046,390 | ||||||||||

Total Preference Shares | — | — | 724,008,903 | 724,008,903 | ||||||||||

Total Quota Shares and Other Reinsurance-Related Securities | — | — | 724,214,044 | 724,214,044 | ||||||||||

Limited Liability Partnership(2) | — | — | 18,433,834 | 18,433,834 | ||||||||||

Money Market Funds | 247,894,767 | — | — | 247,894,767 | ||||||||||

Total Assets | $247,894,767 | $241,537,830 | $744,257,573 | $1,233,690,170 | ||||||||||

| (1) | Includes Level 3 investments with a value of zero. |

| (2) | For further security characteristics, see the Fund’s Consolidated Schedule of Investments. |

Event- Linked Bonds | Participation Notes | Preference Shares | Private Fund Units | Limited Liability Partnership | |||||||||||||

Beginning Balance—November 1, 2023 | $1,943,701 | $9,918,495 | $753,578,077 | $651,592 | $4,929,014 | ||||||||||||

Acquisitions | 39,552 | 501,790 | 89,351,763 | — | — | ||||||||||||

Dispositions | (2,058,513) | (10,444,816) | (121,128,977) | (558,230) | — | ||||||||||||

Realized gain (loss) | (2,789,430) | (1,969,634) | (14,689,692) | (1,547,268) | — | ||||||||||||

Return of capital | — | (16,613) | (61,865,320) | — | (1,753,650) | ||||||||||||

Change in unrealized appreciation/ (depreciation) | 3,408,537 | 2,215,919 | 78,763,052 | 1,453,906 | 15,258,470 | ||||||||||||

Transfers out of Level 3 | (432,808) | — | — | — | — | ||||||||||||

Transfers into Level 3 | 1,498,656 | — | — | — | — | ||||||||||||

Ending Balance—October 31, 2024 | $1,609,695 | $205,141 | $724,008,903 | $— | $18,433,834 | ||||||||||||

24 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

TYPE OF SECURITY | INDUSTRY | FAIR VALUE AT 10/31/24 | VALUATION TECHNIQUES | UNOBSERVABLE INPUTS | RANGE | WEIGHTED AVERAGE(1) | ||||||||||||||

Participation Notes | Financial Services | $205,141 | Insurance industry model | Estimated losses: | $0.1MM-$4.4MM | $1.7MM | ||||||||||||||

Estimated premiums earned: | $0.1MM-$3.9MM | $1.7MM | ||||||||||||||||||

Preference Shares | Financial Services | $ 724,008,903 | Insurance industry model | Estimated losses: | $0.0MM-$284.1MM | $21.6MM | ||||||||||||||

Estimated premiums earned: | $0.0MM-$451.6MM | $46.5MM | ||||||||||||||||||

Limited Liability Partnership | Financial Services | $18,433,834 | Insurance industry model | Estimated losses: | $0.0MM-$22.9MM | $11.2MM | ||||||||||||||

Estimated premiums earned: | $0.0MM-$38.4MM | $21.1MM | ||||||||||||||||||

| (1) | Weighed by relative fair value. |

Stone Ridge Funds | Annual Report | October 31, 2024 | 25 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

26 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

Stone Ridge Funds | Annual Report | October 31, 2024 | 27 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

28 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

TOTAL DISTRIBUTABLE EARNINGS/(LOSS) | PAID IN CAPITAL | |||||||

Reinsurance Risk Premium Interval Fund | $ (1) | $ 1 | ||||||

Tax cost of investments | $1,474,564,478 | ||||

Unrealized appreciation | 267,487,709 | ||||

Unrealized depreciation | (481,405,409) | ||||

Net unrealized appreciation (depreciation) | (213,917,700) | ||||

Undistributed ordinary income | 236,195,535 | ||||

Undistributed long-term gains/(capital loss carryover) | (801,675,584) | ||||

Total distributable earnings/(loss) | (565,480,049) | ||||

Other temporary differences | 2,581,214 | ||||

Total accumulated loss | $(776,816,535) | ||||

ORDINARY INCOME | LONG-TERM CAPITAL GAIN | FOREIGN TAX CREDIT | RETURN OF CAPITAL | TOTAL | |||||||||||||

Reinsurance Risk Premium Interval Fund | $ 188,300,000 | $— | $— | $— | $188,300,000 | ||||||||||||

ORDINARY INCOME | LONG-TERM CAPITAL GAIN | FOREIGN TAX CREDIT | RETURN OF CAPITAL | TOTAL | |||||||||||||

Reinsurance Risk Premium Interval Fund | $5,618,485 | $— | $— | $— | $5,618,485 | ||||||||||||

SHORT-TERM | LONG-TERM | TOTAL | |||||||||

Reinsurance Risk Premium Interval Fund | $ (25,524,442) | $(776,151,142) | $(801,675,584) | ||||||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 29 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

30 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Notes to Consolidated Financial Statements | October 31, 2024 | ||

YEAR ENDED OCTOBER 31, 2024 | YEAR ENDED OCTOBER 31, 2023 | |||||||

Shares sold | 3,322,431 | 2,811,677 | ||||||

Shares issued to holders in reinvestment of dividends | 935,168 | 71,861 | ||||||

Shares repurchased. | (4,288,263) | (8,078,837) | ||||||

Net decrease in shares… | (30,664) | (5,195,299) | ||||||

Shares outstanding: | ||||||||

Beginning of year | 21,147,344 | 26,342,643 | ||||||

End of year…. | 21,116,680 | 21,147,344 | ||||||

Repurchase Request Deadline | REPURCHASE OFFER AMOUNT (SHARES) | SHARES TENDERED | ||||||

December 2, 2022(1) | 1,983,804 | 2,521,330 | ||||||

February 24, 2023 | 4,407,029 | 3,035,898 | ||||||

May 19, 2023(1) | 1,094,878 | 1,236,815 | ||||||

August 18, 2023(1) | 1,103,795 | 1,284,794 | ||||||

November 10, 2023 | 1,059,522 | 1,065,193 | ||||||

February 23, 2024 | 3,528,230 | 1,871,215 | ||||||

May 17, 2024 | 1,030,107 | 741,347 | ||||||

August 16, 2024 | 1,020,353 | 610,508 | ||||||

| (1) | In connection with the repurchase request deadline on December 2, 2022, May 19, 2023, August 18, 2023 and November 10, 2023, the Fund repurchased an additional amount, 2.0%, 0.7%, 0.8% and 0.3%, respectively, of the shares outstanding on the repurchase request deadline, in order to accommodate shareholder repurchase requests. |

Stone Ridge Funds | Annual Report | October 31, 2024 | 31 | |||||

Report of Independent Registered Public Accounting Firm | |||

32 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Expense Example (Unaudited) | |||

Beginning Account Value May 1, 2024 | Ending Account Value October 31, 2024 | Expenses Paid During Period* May 1, 2024 – October 31, 2024 | |||||||||

Actual | $1,000.00 | $1,116.60 | $12.18 | ||||||||

Hypothetical (5% annual return before expenses) | $1,000.00 | $1,013.62 | $11.59 | ||||||||

| * | Expenses are equal to the Fund’s annualized six-month expense ratio of 2.29%, multiplied by the average account value over the period, multiplied by 184/366 to reflect the partial year period. |

Stone Ridge Funds | Annual Report | October 31, 2024 | 33 | |||||

Additional Information (Unaudited) | |||

34 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Additional Information (Unaudited) | |||

Name (Year of Birth) | Position(s) Held with the Trust | Term of Office and Length of Time Served(1) | Principal Occupation(s) During the Past 5 Years | Number of Portfolios in the Fund Complex Overseen by Trustee(2) | Other Directorships / Trusteeships Held by Trustee During the Past 5 Years | ||||||||||||

Jeffery Ekberg (1965) | Trustee | since inception | Self-employed (personal investing), since 2011; Principal, TPG Capital, L.P. (private equity firm) until 2011; Chief Financial Officer, Newbridge Capital, LLC (subsidiary of TPG Capital, L.P.) until 2011 | 40 | None. | ||||||||||||

Daniel Charney (1970) | Trustee | since inception | Co-President, Cowen and Company, Cowen Inc. (financial services firm) since 2012 | 40 | None. | ||||||||||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 35 | |||||

Additional Information (Unaudited) | |||

Name (Year of Birth) | Position(s) Held with the Trust | Term of Office and Length of Time Served(1) | Principal Occupation(s) During the Past 5 Years | Number of Portfolios in the Fund Complex Overseen by Trustee(2) | Other Directorships / Trusteeships Held by Trustee During the Past 5 Years | ||||||||||||

Ross Stevens (1969)(3) | Trustee, Chairman | since inception | Founder and Chief Executive Officer of Stone Ridge since 2012 | 40 | None. | ||||||||||||

| (1) | Information as of October 31, 2024. |

| (2) | Each Trustee serves until resignation or removal from the Board. |

| (3) | The Fund Complex includes the Trust and Stone Ridge Trust, Stone Ridge Trust II, Stone Ridge Trust IV, Stone Ridge Trust V, and Stone Ridge Trust VIII, other investment companies managed by the Adviser. |

| (4) | Mr. Stevens is an “interested person” of the Trust, as defined in Section 2(a)(19) of the 1940 Act, due to his position with the Adviser. |

Name (Year of Birth) and Address(1)(2) | Position(s) Held with the Trust | Term of Office and Length of Time Served(3) | Principal Occupation(s) During Past 5 Years | ||||||||

Ross Stevens (1969) | President, Chief Executive Officer and Principal Executive Officer | since inception | Founder and Chief Executive Officer of the Adviser, since 2012. | ||||||||

Lauren D. Macioce (1978) | Chief Compliance Officer, Secretary, Chief Legal Officer and Anti-Money Laundering Compliance Officer | since 2016 | General Counsel and Chief Compliance Officer of the Adviser, since 2016. | ||||||||

Maura Keselowsky (1983) | Treasurer, Principal Financial Officer, Chief Financial Officer and Chief Accounting Officer | since July 2024 | Supervising Fund Controller at the Adviser, since 2022; member of Finance at the Adviser, since 2018 | ||||||||

Anthony Zuco (1975) | Assistant Treasurer | since 2018 | Supervising Fund Controller at the Adviser, since 2015-2022; member of Finance at the Adviser, since 2015. | ||||||||

Alexander Nyren (1980) | Assistant Secretary | since 2018 | Head of Reinsurance of the Adviser, since 2018; member of Reinsurance portfolio management team at the Adviser, since 2013. | ||||||||

Leson Lee (1975) | Assistant Treasurer | since 2019 | Member of Operations at the Adviser, since 2018. | ||||||||

Domingo Encarnacion (1983) | Assistant Treasurer | since 2020 | Tax Manager at the Adviser, since 2016. | ||||||||

Stanley Weinberg (1989) | Assistant Treasurer | since 2023 | Member of Operations at the Adviser, since 2019. | ||||||||

Daniel Gross (1984) | Assistant Treasurer | since 2023 | Member of Operations at the Adviser, since 2019. | ||||||||

36 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

Additional Information (Unaudited) | |||

Name (Year of Birth) and Address(1)(2) | Position(s) Held with the Trust | Term of Office and Length of Time Served(3) | Principal Occupation(s) During Past 5 Years | ||||||||

Connor O’Neill (1990) | Assistant Treasurer | since April 2024 | Member of Operations at the Adviser, since 2020; Operations Manager at Junto Capital Management (2015-2019). | ||||||||

Shamil Kotecha (1986) | Assistant Treasurer | since October 2024 | Member of Legal and Compliance at the Adviser, since 2018. | ||||||||

| (1) | Each officer’s mailing address is c/o Stone Ridge Asset Management LLC, One Vanderbilt Avenue, 65th Floor, New York, NY 10017. |

| (2) | Each of the officers is an affiliated person of the Adviser as a result of his or her position with the Adviser. |

| (3) | The term of office of each officer is indefinite. |

PERCENTAGES | |||||

Reinsurance Risk Premium Interval Fund | 0.00% | ||||

PERCENTAGES | |||||

Reinsurance Risk Premium Interval Fund | 0.00% | ||||

PERCENTAGES | |||||

Reinsurance Risk Premium Interval Fund | 0.00% | ||||

PERCENTAGES | |||||

Reinsurance Risk Premium Interval Fund | 2.04% | ||||

Stone Ridge Funds | Annual Report | October 31, 2024 | 37 | |||||

Additional Information (Unaudited) | |||

38 | Stone Ridge Funds | Annual Report | October 31, 2024 | |||||

| (b) | Not applicable. |

Item 2. Code of Ethics.

The registrant has adopted a code of ethics that applies to the registrant’s principal executive officer and principal financial officer. The registrant has not made any substantive amendments to its code of ethics during the period covered by this report. The registrant has not granted any waivers from any provisions of the code of ethics during the period covered by this report.

A copy of the registrant’s Code of Ethics is filed herewith.

Item 3. Audit Committee Financial Expert.

The registrant’s board of trustees has determined that there is at least one audit committee financial expert serving on its audit committee. Jeffery Ekberg is the “audit committee financial expert” and is considered to be “independent” as each term is defined in Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) - (d) The following table details the aggregate fees billed or expected to be billed for each of the last two fiscal years for audit fees, audit-related fees, tax fees and all other fees by the principal accountant. “Audit fees” includes amounts related to an audit of the registrant’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years. “Audit-related fees” covers the assurance and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant’s annual financial statements and are not covered under “audit fees,” including review of the Fund’s prospectus. “Tax fees” covers the professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning, including review of the Fund’s tax returns, asset diversification and income testing, excise taxes, and fiscal year end income calculations. “All other fees” covers the aggregate fees for products and services provided by the principal accountant, other than the services reported in the foregoing three categories.

| FYE 10/31/2024 | FYE 10/31/2023 | |

| Audit Fees | $221,320 | $210,780 |

| Audit-Related Fees | $8,750 | $8,350 |

| Tax Fees | $183,025 | $202,300 |

| All Other Fees | $0 | $0 |

(e)(1) To the extent required by applicable law, pre-approval by the audit committee is needed for all audit and permissible non-audit services rendered to the registrant and all permissible non-audit services rendered to Stone Ridge Asset Management LLC (the “Adviser”) or to various entities either controlling, controlled by, or under common control with the Adviser that provide ongoing services to the registrant if the services relate directly to the operations and financial reporting of the registrant. Pre-approval is currently on an engagement-by-engagement basis.

(e)(2) The percentage of fees billed by Ernst & Young, LLP applicable to non-audit services that were approved by the audit committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X (which permits waiver of pre-approval, if certain conditions are satisfied) were as follows:

| FYE 10/31/2024 | FYE 10/31/2023 | |

| Audit-Related Fees | 0% | 0% |

| Tax Fees | 0% | 0% |

| All Other Fees | 0% | 0% |

(f) All of the principal accountant’s hours spent on auditing the registrant’s financial statements were attributed to work performed by full-time permanent employees of the principal accountant.

(g) The following table indicates the non-audit fees billed or expected to be billed by the registrant’s accountant for services to the registrant and to the registrant’s investment adviser and any entity controlling, controlled by, or under common control with the registrant’s investment adviser that provides ongoing services to the registrant for the last two fiscal years of the registrant.

| Non-Audit Related Fees | FYE 10/31/2024 | FYE 10/31/2023 |

| Registrant | $183,025 | $202,300 |

| Registrant’s Investment Adviser | $206,495 | $253,160 |

(h) The audit committee of the board of trustees has considered whether the provision of any non-audit services that were rendered to the registrant’s investment adviser and any entity controlling, controlled by, or under common control with the registrant’s investment adviser that provides ongoing services to the registrant that were not pre-approved pursuant to paragraph (c)(7)(ii) of Rule 2-01 of Regulation S-X is compatible with maintaining the principal accountant’s independence.

(i) Not applicable

(j) Not applicable

Item 5. Audit Committee of Listed Registrants.

Not applicable to registrants who are not listed issuers (as defined in Rule 10A-3 under the Securities Exchange Act of 1934).

Item 6. Investments.

| (a) | Schedule of Investments is included as part of the financial statements filed under Item 1 of this Form N-CSR. |

| (b) | Not Applicable. |

Item 7. Financial Statements and Financial Highlights for Open-End Investment Companies.

Not applicable to closed-end investment companies.

Item 8. Changes in and Disagreements with Accountants for Open-End Investment Companies.

Not applicable to closed-end investment companies.

Item 9. Proxy Disclosure for Open-End Investment Companies.

Not applicable to closed-end investment companies.