Filed pursuant to Rule 424(b)(3)

Registration Statement No. 333-197476

Prospectus Supplement No. 5

(To Prospectus dated January 22, 2015)

ENERGY 11, L.P.

An Offering of Common Units of Limited Partnership Interest

Minimum Offering: 1,315,790 Common Units

Maximum Offering: 100,263,158 Common Units

This Prospectus Supplement No. 5 supplements and amends the prospectus dated January 22, 2015, referred to herein as the Prospectus. Prospective investors should carefully review the Prospectus, Prospectus Supplement No. 3 dated August 11, 2015 (which was cumulative and replaced all prior Prospectus Supplements), Prospectus Supplement No. 4 dated August 19, 2015 and this Prospectus Supplement No. 5.

This Prospectus Supplement No. 5 is qualified by reference to the Prospectus, except to the extent that the information in this Prospectus Supplement No. 5 updates or supersedes the information contained in the Prospectus, including any supplements and amendments thereto. This Prospectus Supplement No. 5 is not complete without, and may not be delivered or utilized except in connection with, the Prospectus, including any supplements and amendments thereto.

There are significant risks associated with an investment in our common units. These risks are described under the caption “Risk Factors” beginning on page 20 of the Prospectus, as the same may be updated in prospectus supplements.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus supplement is September 18 2015.

S-1

The Table of Contents on page i of the Prospectus is hereby amended to include the following items.

TABLE OF CONTENTS

| Status of the Offering | S-2 | |

| Recent Developments | S-2 |

The following disclosure is hereby inserted as a new section following the section entitled “Terms of the Offering—Acceptance of Subscriptions” on page 57 of the Prospectus.

As of August 19, 2015, we completed our minimum offering of 1,315,790 common units at $19.00 per common unit. As of August 31, 2015, we had completed the sale of a total of 1,645,710 common units at $19.00 per common unit for total gross proceeds of $31,268,490 and proceeds net of selling commissions and marketing expenses of $29,392,381. We are continuing the offering at $19.00 per common unit in accordance with the prospectus. As of August 31, 2015, 98,617,448 common units remained unsold. We will offer common units until January 22, 2017, unless the offering is extended by our general partner, provided that the offering will be terminated if all of the common units are sold before then.

The following disclosure is hereby inserted as a new section following the section entitled “Proposed Activities—Well Operations” on page 68 of the Prospectus.

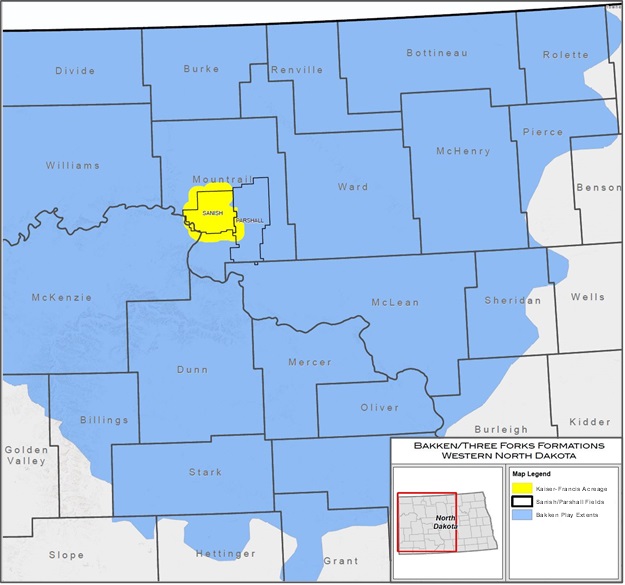

On September 15, 2015, Energy 11 Operating Company, LLC, our wholly owned subsidiary, entered into an Interest Purchase Agreement (“Purchase Agreement”) by and among Kaiser-Whiting, LLC (“Seller”) and the owners of all the limited liability company interests therein, for the potential purchase of certain of the limited liability company interests in Seller (the “Transferred Interests”) resulting in an 11.5% working interest in approximately 215 existing producing wells and approximately 262 future development locations in the Sanish field located in Mountrail County, North Dakota (collectively, the “Sanish Field Assets”). The Sanish field is part of the Greater Williston Basin where industry activity is focused on development of the prolific Bakken Shale formation. Whiting Petroleum Corporation (NYSE:WLL) (“Whiting”), a publicly traded oil and gas company operates the asset on behalf of Seller and other working interest owners. If we close on the Purchase Agreement, we will be a non-operator, with Whiting, the largest producer in this basin, acting as operator. We anticipate drilling capital expenditure requirements for the Sanish Field Assets to be an estimated $75 million through 2020.

The Bakken Shale and its close geologic cousin, the Three Forks Shale, are found in the Williston Basin, centered in North Dakota. The Bakken Shale in the Williston Basin is one of the largest oil fields in the U.S., covering an area of approximately 17,500 square miles. While oil has been produced in North Dakota from the Williston Basin since the 1950s, it is only since 2007 through the application of horizontal drilling and hydraulic fracturing technologies that the Bakken has seen an increase in production activities.

Pursuant to the Purchase Agreement, the cash purchase price for the Transferred Interests consists of (i) an initial $160 million (with the Deposit, as defined below, applied at closing) payable at closing subject to customary adjustments, and (ii) a contingent payment of up to $95 million. The contingent payment will provide for a sharing between us and Seller to the extent the NYMEX price for WTI is between the current five-year strip oil price and $89 per barrel. The contingent payment will be calculated as follows: if on December 31, 2017 (the “Measurement Date”) the average of the monthly NYMEX:CL strip prices for future contracts during the delivery period beginning December 31, 2017 and ending December 31, 2022 (the “Measurement Date Average Price”) is greater than $56.61, then the Sellers will be entitled to a contingent payment equal to (a) (i) the lesser of (A) the Measurement Date Average Price and (B) $89.00, minus (ii) $56.61, multiplied by (b) 586,601 bbls per year for each of the five years from 2018 through 2022 represented by the contracts for the entire acquisition. The contingent consideration is capped at $95 million and is to be paid on January 1, 2018.

S-2

On September 17, 2015 we funded a deposit of $10 million (the “Deposit”) with the manager of Seller to be applied toward the purchase price at closing or to be released to the owners of Seller if the transaction does not close by the outside closing date due to our breach of the Purchase Agreement. In the event the transaction does not close due to a breach by Sellers or if the aggregate value of any title defects, environmental defects and casualty losses exceeds 10% of the unadjusted initial purchase price, the Deposit will be refunded to us. If we do not perform under the contract as a result of our diligence review or otherwise breach the Purchase Agreement, the Sellers’ sole remedy against us is release of the Deposit to the Sellers.

The closing of the Purchase Agreement is subject to the satisfaction of a number of required conditions which currently remain unsatisfied under the Purchase Agreement. Consummation of the acquisition is subject to our satisfactory completion of the review of title, environmental investigations, financial analysis and geological analysis, obtaining sufficient financing to fund the purchase price and other due diligence. Accordingly, there can be no assurance at this time that all of the conditions precedent to consummating the Purchase Agreement will be satisfied, that we will find the results of our diligence investigation acceptable, that we will be able to obtain sufficient financing on terms reasonably acceptable to us or that the transaction will be successfully completed.

S-3

Asset Map

S-4