As filed with the Securities and Exchange Commission on April 6, 2017

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________

FORM 20-F

(Mark One)

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2016 |

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 001-37965

TiGenix

(Exact name of Registrant as specified in its charter)

KINGDOM OF BELGIUM

(Jurisdiction of incorporation or organization)

Romeinse straat 12, box 2

3001 Leuven

Belgium

(Address of principal executive offices)

An Moonen, General Counsel

Tel: +32 016 39 7937

Romeinse straat 12, box 2

3001 Leuven

Belgium

an.moonen@tigenix.com

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

____________________

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

| American Depositary Shares, each representing 20 ordinary shares with no nominal value per share | The Nasdaq Stock Market LLC |

| | |

| Ordinary shares, no nominal value per share* | The Nasdaq Stock Market LLC* |

| | |

| *Not for trading, but only in connection with the registration of the American Depositary Shares | |

| | |

____________________

Securities registered or to be registered pursuant to Section 12(g) of the Act:None

____________________

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:None

____________________

The number of outstanding shares of each class of capital stock of TiGenix. at December 31, 2016 was:

259,956,365 Ordinary Shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☐ No ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one):

Large Accelerated Filer ☐ Accelerated Filer ☐ Non-accelerated Filer☒

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

☐ U.S. GAAP

☒ International Financial Reporting Standards as issued by the International Accounting Standards Board

☐ Other

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No☒

table of contents

____________________

Page

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements and our estimates with respect to our anticipated future performance and the market in which we operate. Certain of these statements, forecasts and estimates can be recognized by the use of words such as, without limitation, “believes,” “anticipates,” “expects,” “intends,” “plans,” “seeks,” “estimates,” “may,” “will,” “predicts,” “projects” and “continue” and similar expressions. Such statements, forecasts and estimates are based on various assumptions and assessments of known and unknown risks, uncertainties and other factors, which may or may not prove to be correct. Actual events are difficult to predict and may depend upon factors that are beyond our control. Therefore, our actual results, financial condition or performance may turn out to be materially different from such statements, forecasts and estimates. Factors that might cause such a difference include, but are not limited to, those discussed in the section “Risk Factors” included elsewhere in this Annual Report.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events, competitive dynamics and industry change, and depend on economic circumstances that may or may not occur in the future or may occur on longer or shorter timelines than anticipated. Although we believe that we have a reasonable basis for each forward-looking statement contained in this Annual Report, we caution you that forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors that are in some cases beyond our control. All of our forward-looking statements are subject to risks and uncertainties that may cause our actual results to differ materially from our expectations.

Actual results could differ materially from our forward-looking statements due to a number of factors, including, without limitation, the following:

| · | We may experience delays or failure in the preclinical and clinical development of our product pipeline. |

| · | Regulatory approval of our products may be delayed, not obtained or not maintained. |

| · | We work in a strict regulatory environment, and future changes to any pharmaceutical legislation or guidelines or unexpected events or new scientific insights occurring within the field of cell therapy, could affect our business. |

| · | If we fail to obtain additional financing, we may be unable to complete the development and commercialization of our product candidates. |

| · | We have a history of operating losses and an accumulated deficit and may never become profitable. |

| · | We had an accumulated deficit of 116.2 million euros as of December 31, 2016 and our net losses and significant cash used in operating activities have raised substantial doubt about our ability to continue as a going concern. |

| · | The manufacturing facilities at which our product candidates are made are subject to regulatory requirements, which may affect the development of our product pipeline and the successful commercialization of our products. |

| · | We may not be able to adequately protect our proprietary technology or enforce any rights related thereto. |

| · | Third party claims of intellectual property infringement may prevent or delay our product discovery and development efforts. |

| · | We may need to rely on distributors and other third parties to commercialize our product candidates, and such distributors may not succeed in commercializing our product candidates effectively or at all. |

| · | We rely on third parties to conduct our clinical trials. If these third parties do not successfully carry out their contractual duties or meet expected deadlines, we may not be able to obtain regulatory approval for or commercialize our product candidates. |

| · | The allocation of available resources could affect our ability to carry out our business plan. |

The preceding list is not intended to be an exhaustive list of all of our forward-looking statements. Except as required by law, we undertake no obligation to update publicly any forward-looking statements for any reason after the date of this Annual Report or to conform these statements to actual results or to changes in our expectations.

PART I

Item 1. Identity of Directors, Senior Management and Advisors

A. Directors and Senior Management

Not applicable.

B. Advisers

Not applicable.

C. Auditors

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

A. Selected Financial Data

The tables below present our summary historical consolidated financial data. Our summary historical consolidated financial data as of December 31, 2016, 2015 and 2014 and for the years ended December 31, 2016, 2015 and 2014 has been derived from our audited consolidated financial statements, which are included elsewhere in this Annual Report. The consolidated financial statements have been prepared and presented in accordance with IFRS as issued by the IASB. As an emerging growth company, we are not required to present, and have not presented, selected financial data for any period prior to our most recently completed three fiscal years.

The following summary historical consolidated financial data should be read in conjunction with our historical consolidated financial statements and the related notes thereto and “Item5. Operating and Financial Review and Prospects.” included elsewhere in this Annual Report. The historical results for any prior period are not necessarily indicative of results to be expected for any future period.

Consolidated Income Statement Data:

| Years ended December 31, | | |

| | | 2016 | | 2015 | | 2014 |

| | | In thousands of euros, except per share data |

| | | |

| CONTINUING OPERATIONS | | | | | | | | | | | | |

| Revenues | | | | | | | | | | | | |

| Royalties | | | 395 | | | | 537 | | | | 338 | |

| License revenues | | | 25,000 | | | | — | | | | — | |

| Grants and other operating income | | | 1,395 | | | | 1,703 | | | | 5,948 | |

| Total revenues | | | 26,790 | | | | 2,240 | | | | 6,286 | |

| Research and development expenses | | | (21,454 | ) | | | (19,633 | ) | | | (11,443 | ) |

| General and administrative expenses | | | (8,363 | ) | | | (6,683 | ) | | | (7,406 | ) |

| Total operating charges | | | (29,817 | ) | | | (26,316 | ) | | | (18,849 | ) |

| Operating Loss | | | (3,027 | ) | | | (24,076 | ) | | | (12,563 | ) |

| Financial income | | | 156 | | | | 148 | | | | 115 | |

| Interest on borrowing and other finance costs | | | (7,288 | ) | | | (6,651 | ) | | | (1,026 | ) |

| Fair value gains | | | 11,593 | | | | — | | | | 60 | |

| Fair value losses | | | — | | | | (6,654 | ) | | | — | |

| Impairment and gains/(losses) on disposal of financial instruments | | | — | | | | (161 | ) | | | — | |

| Foreign exchange differences, net | | | 232 | | | | 1,000 | | | | 1,101 | |

| Profit (Loss) before taxes | | | 1,666 | | | | (36,394 | ) | | | (12,313 | ) |

| Income tax benefits / (losses) | | | 2,136 | | | | 1,325 | | | | 927 | |

| Profit (Loss) for the year from continuing operations | | | 3,802 | | | | (35,069 | ) | | | (11,386 | ) |

| DISCONTINUED OPERATIONS | | | | | | | | | | | | |

| Profit (Loss) for the year from discontinued operations | | | — | | | | — | | | | (1,605 | ) |

| Profit (Loss) for the year | | | 3,802 | | | | (35,069 | ) | | | (12,990 | ) |

| Attributable to equity holders of TiGenix | | | 3,802 | | | | (35,069 | ) | | | (12,990 | ) |

| Basic and diluted profit (loss) per share | | | 0.02 | | | | (0.21 | ) | | | (0.08 | ) |

| Basic and diluted profit (loss) per share from continuing operations | | | 0.02 | | | | (0.21 | ) | | | (0.07 | ) |

| Basic and diluted profit (loss) per share from discontinued operations | | | — | | | | — | | | | (0.01 | ) |

Consolidated Statements of Financial Position Data—Summary

| | | As at December 31, |

| | | 2016 | | 2015 | | 2014 |

| | | In thousands of euros |

| ASSETS | | | | | | |

| Non-current assets | | | 52,081 | | | | 54,241 | | | | 36,808 | |

| Current assets | | | 84,120 | | | | 24,930 | | | | 17,113 | |

| TOTAL ASSETS | | | 136,201 | | | | 79,171 | | | | 53,921 | |

| EQUITY AND LIABILITIES | | | | | | | | | | | | |

| Equity attributable to equity holders | | | 79,679 | | | | 13,145 | | | | 34,757 | |

| Total equity | | | 79,679 | | | | 13,145 | | | | 34,757 | |

| Non-current liabilities | | | 36,395 | | | | 52,137 | | | | 10,681 | |

| Current liabilities | | | 20,127 | | | | 13,889 | | | | 8,483 | |

| TOTAL EQUITY AND LIABILITIES | | | 136,201 | | | | 79,171 | | | | 53,921 | |

Consolidated Statements of Cash Flows Data—Summary

| | | As at December 31, |

| | | 2016 | | 2015 | | 2014 |

| | | In thousands of euros |

| Net cash (used in) /provided by operating activities | | | 3,548 | | | | (19,574 | ) | | | (13,367 | ) |

| Net cash (used in) / provided by investing activities | | | 510 | | | | (4,434 | ) | | | 3,307 | |

| Net cash provided by financing activities | | | 55,929 | | | | 28,523 | | | | 7,969 | |

| Cash and cash equivalents at end of year | | | 77,969 | | | | 17,982 | | | | 13,471 | |

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

RISK FACTORS

You should carefully consider the risks and uncertainties described below, together with other information contained in this Annual Report. Any of the following risks and uncertainties could have a material adverse effect on our business, prospects, results of operations and financial condition. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business operations.

Risks Related to the Clinical Development and Regulatory Approval of Our Product Candidates

We may experience delays or failure in the preclinical and clinical development of our product candidates.

As part of the regulatory approval process, we conduct preclinical studies and clinical trials for each of our unapproved product candidates to demonstrate safety and efficacy. The number of required preclinical studies and clinical trials varies depending on the product, the indication being evaluated, the trial results and the applicable regulations. Clinical testing is expensive and can take many years to be completed, and its outcome is inherently uncertain. Failure can occur at any time during the clinical trial process. The results of preclinical studies and initial clinical trials do not necessarily predict the results of later-stage clinical trials, and products may fail to show the desired safety, efficacy and quality despite having progressed through initial clinical trials. The data collected from preclinical studies and clinical trials may not be sufficient to support the U.S. Food and Drug Administration, or FDA, the European Medicines Agency, or EMA, or other regulatory approval or approval by ethics committees in various jurisdictions. In addition, the review of a study by an independent data safety monitoring board or review body does not necessarily indicate that the clinical trial will ultimately be successfully completed.

We cannot accurately predict when our current preclinical studies and clinical trials or future clinical trials will be completed, if at all, nor when planned preclinical studies and clinical trials will begin or be completed. Successful and timely completion of clinical trials will require us to recruit a sufficient number of patient candidates, locate or develop manufacturing facilities with regulatory approval sufficient for production of the product to be tested and enter into agreements with third party contract research organizations to conduct the trials. We may need to engage or further engage in preclinical studies and clinical trials with partners, which may reduce any future revenues from any future products.

Our products may cause unexpected side effects or serious adverse events that could interrupt, delay or halt the clinical trials and could result in the FDA, the EMA or other regulatory authorities denying approval of our products for any or all targeted indications. An institutional review board or ethics board, the FDA, the EMA, any other regulatory authorities or we ourselves, based on the recommendation of an independent data safety review board or otherwise, may suspend or terminate clinical trials at any time, and none of our product candidates may ultimately prove to be safe and effective for human use.

In addition, even if the data from our clinical trials is sufficient to support an application for marketing authorization, detailed analysis of such data, including analysis of secondary end-points and follow-up data from later periods, and the interpretation of such data by the regulatory authorities, prescribing physicians and others, including potential partners, could have a significant impact on the value of the asset and our ability to realize its full value.

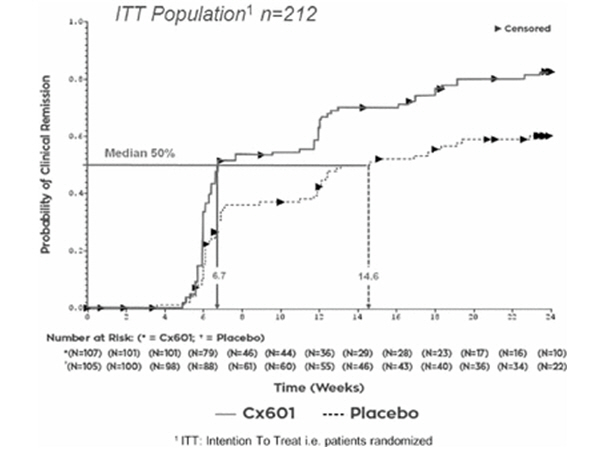

If the EMA does not approve Cx601 for the treatment of complex perianal fistulas in patients with Crohn’s disease, Takeda may not be able to commercialize Cx601 in Europe, and we may not receive our milestone payment in connection with approval of marketing authorization and subsequent milestone payments and royalties in a timely manner or at all.

In March 2016, we submitted a marketing authorization application for Cx601 to the EMA for the treatment of complex perianal fistulas in adult patients with non-active or mildly active luminal Crohn’s disease whose fistulas have shown an inadequate response to at least one conventional or biologic therapy. In July 2016, the EMA sent us its initial response to our application for marketing authorization, which we refer to as “the Day 120 List of Questions”. In its response, the EMA informed us of certain major objections and, following its standard protocol for review at day 120, stated that our application was not approvable at the present time. These objections would preclude a recommendation for marketing authorization, unless we were able to address them adequately. These objections were as follows:

| · | inadequate data with respect to the stability of the intermediate master cell stock for Cx601 and the questionable relevance of the potency test for stability of the master cell stock |

| · | incomplete information with respect to the details on donor selection and testing |

| · | an insufficient viral safety risk assessment |

| · | uncertainty as to whether the primary endpoint of the trial is adequately representative of complete closure of fistulas and is adequately sensitive as a measure of improvement. |

In addition, as part of the marketing authorization application process, we had a routine Good Clinical Practice inspection in September 2016. The inspectors identified certain critical and major deviations from Good Clinical Practices, in particular, a potential violation of patient privacy. In their report to the EMA’s Committee for Human Medicinal Products, the inspectors recommend that the data from the trial should be disregarded as part of the marketing authorization application. We included our replies to the issues raised in the inspection report as part of our replies to the Day 120 List of Questions, which we submitted in December 2016. In February 2017, the EMA sent TiGenix its “Day 180 List of Outstanding Issues”.

While we believe that we will be able to provide adequate responses to the outstanding issues, the EMA reviewers may not be satisfied with our responses or may require additional information, which we may not be able to provide in a timely manner or at all. If we are not able to provide the EMA with satisfactory responses, we may not receive marketing authorization for Cx601, or if we need additional time to provide the required information, approval for marketing authorization could be delayed. This would delay or preclude our receipt of the milestone payment of 15 million euros from Takeda for receipt of marketing authorization of Cx601 in Europe, additional milestone payments for favorable pricing decisions in certain European markets and royalties from sales of Cx601 in Europe. In addition, Takeda has the option to terminate the licensing agreement if we do not receive marketing authorization in Europe by July 2020.

Regulatory approval of our product candidates may be delayed, not obtained or not maintained.

In the United States, all of our cell-based product candidates are subject to a biologics license application, or BLA, issued by the FDA. In Europe, all of our product candidates require regulatory approval through the centralized marketing authorization procedure coordinated by the EMA for advanced therapy medicinal products.

Besides the marketing authorization, we also need to obtain and maintain specific national licenses to perform our commercial operations, including manufacturing and distribution licenses, as well as authorizations to obtain and handle human cells and tissues.

Regulatory approval may be delayed, limited or denied for a number of reasons, most of which are beyond our control, including the following:

| · | The requirement to perform additional clinical trials. |

| · | The failure of the product to meet the safety or efficacy requirements. |

| · | Our ability to successfully conclude the transfer of our technology to our contract manufacturers. |

| · | Our ability to scale up manufacturing processes to the level required to successfully run the clinical trials for our product candidates and to commercialize them. |

| · | The failure of the relevant manufacturing processes or facilities to meet the applicable requirements. |

Any delay or denial of regulatory approval of our product candidates or any failure to comply with post-approval regulatory policies is likely to have a significant impact on our operations and prospects, in particular on our expected revenues.

Regulatory authorities, including the FDA and the EMA, may disagree with our interpretations of data from preclinical studies and clinical trials, our interpretation of applicable regulations including, without limitations, regulations relating to patent term extensions or restorations. They may also approve a product for narrower

spectrum of indications than requested or may grant approval subject to the performance of post-marketing studies for a product. Such post-approval studies, if required, may not corroborate the results of earlier trials. Furthermore, the general use of such products may result in either or both of the safety and efficacy profiles differing from those demonstrated in the trials on which marketing approval was based, which could lead to the withdrawal or suspension of marketing approval for the product. In addition, regulatory authorities may not approve the labelling claims that are necessary or desirable for the successful commercialization of our products.

In addition, a marketed product continues to be subject to strict regulation after approval. Changes in applicable legislation or regulatory policies or discovery of problems with the product, production process, site or manufacturer may result in delays in bringing products to the market, the imposition of restrictions on the product’s sale or manufacture, including the possible withdrawal of the product from the market, or may otherwise have an adverse effect on our business.

The failure to comply with applicable regulatory requirements may, among other things, result in criminal and civil proceedings and lead to imprisonment, fines, injunctions, damages, total or partial suspension of regulatory approvals, refusal to approve pending applications, recalls or seizures of products and operating and production restrictions.

We may not receive regulatory clearance for trials at each stage and approval for our products and product candidates still in development without delay or at all. If we fail to obtain or maintain regulatory approval for our products, we will be unable to market and sell such products, and such failure or any delay could prevent us from ever generating meaningful revenues or achieving sustained profitability.

We work in a strict regulatory environment, and future changes in any pharmaceutical legislation or guidelines, or unexpected events or new scientific insights occurring within the field of cell therapy, could affect our business.

Regulatory guidelines may change during the course of a product development and approval process, making the chosen development strategy suboptimal. This may delay development, necessitate additional clinical trials or result in failure of a future product to obtain marketing authorization or the targeted price levels and could ultimately adversely impact commercialization of the authorized product. Market conditions may change, resulting in the emergence of new competitors or new treatment guidelines, which may require alterations in our development strategy. This may result in significant delays, increased trial costs, significant changes in commercial assumptions or the failure of future product candidates to obtain marketing authorization.

In the past, the regulatory environment in Europe and certain EU member states has negatively affected our ChondroCelect business. In accordance with applicable advanced therapy medicinal product regulations, after January 1, 2013, in principle, all advanced therapy medicinal products required central marketing authorization from the EMA. This should have been beneficial for ChondroCelect, which was the first advanced therapy medicinal product to have obtained such central marketing authorization. However, the advanced therapy medicinal product regulation provided for an exemption for hospitals, which allowed EU member states to permit the non-routine production of advanced therapy medicinal product in their markets without central marketing authorization from the EMA. The implementation of this exemption by certain EU member states, notably Spain and Germany, which had very developed markets for autologous chondrocyte implantation procedures, has allowed such countries to keep local products in the market without central marketing authorization from the EMA even after January 1, 2013, thereby significantly reducing the market potential for ChondroCelect.

Although the basic regulatory frameworks appear to be in place in the United States and in Europe for cell-based products, at present regulators have limited experience with such products and the interpretation of these frameworks is sometimes difficult to predict. Moreover, the regulatory frameworks themselves will continue to evolve as the FDA and the EMA issue new guidelines. The interpretation of existing rules or the issuance of new regulations may impose additional constraints on the research, development, regulatory approval, manufacturing or distribution processes of future and existing product candidates, and could prevent us from generating revenues or achieving sustained profitability and force us to withdraw our products from the market.

Unexpected events may occur in the cell therapy field, in particular unforeseen safety issues of any cell therapy product. Moreover, scientific progress might yield new insights on the biology of stem cells which might in turn impact the requirements of safety and efficacy demonstration for stem cell or other cell therapies. Such events or

new insights might change the regulatory requirements and framework, in particular strengthening the required clinical research package and increasing the amount of data required to be provided. This could result in additional constraints on our product development process and lead to significant delays, which could prevent us from ever generating meaningful revenues or achieving sustained profitability.

Expedited pathways for Cx601, if obtained, may not lead to a faster development process.

We intend to seek expedited review for Cx601 in the United States. The fast track program is intended to expedite or facilitate the process for reviewing new drugs and biologics that meet certain criteria. Specifically, new drugs and biologics are eligible for expedited review if they are intended, alone or in combination with one or more drugs or biologics, to treat a serious or life-threatening disease or condition and demonstrate the potential to address unmet medical needs for the disease or condition. Expedited review applies to the combination of the product candidate and the specific indication for which it is being studied. The FDA has broad discretion in determining whether to grant review under any of its expedited development and review programs for a drug or biologic. Obtaining expedited review does not change the standards for product approval, but may expedite the development or approval process. There is no assurance that the FDA will grant such review. Even if the FDA does grant expedited review for Cx601, it may not actually result in faster clinical development or regulatory review or approval. Furthermore, such a review does not increase the likelihood that Cx601 will receive marketing approval in the United States.

In addition, we are broadly exploring available options, which could result in the BLA being filed before the Phase III study (which we expect to begin during the first half of 2017) is complete. There is no guarantee, however, that any of these options will be successful.

Although we have entered into a special protocol assessment, or SPA, agreement with the FDA relating to the U.S. Phase III trial of Cx601 for the treatment of perianal fistulas, this agreement does not guarantee any particular outcome with respect to regulatory review of the trial or any associated biologics license application, or BLA.

The protocol for our U.S. Phase III trial of Cx601 for the treatment of perianal fistulas was reviewed and agreed upon by the FDA under an SPA agreement in 2015. The FDA’s SPA process is designed to facilitate the FDA’s review and approval of drugs by allowing the FDA to evaluate the proposed design and size of clinical trials that are intended to form the primary basis for determining a drug product’s safety and efficacy. Upon specific request by a clinical trial sponsor, the FDA will evaluate the protocol and respond to a sponsor’s questions regarding, among other things, primary efficacy endpoints, trial conduct and data analysis. The FDA ultimately assesses whether the protocol design and planned analysis of the trial are acceptable to support regulatory approval of the product candidate with respect to the effectiveness of the indication studied.

Because the SPA provides for the evaluation of protocols for trials that have not been initiated, the conduct and results of the subsequent trial are not part of the evaluation. Therefore, the existence of an SPA agreement does not guarantee that the FDA will accept a new drug application or a BLA or that the trial results will be adequate to support approval. Those issues are addressed during the review of a submitted application; however, it is hoped that trial quality will be improved by the SPA process.

In rare cases, the FDA may rescind an SPA agreement. In particular, an SPA agreement is not binding on the FDA if public health concerns emerge that were unrecognized at the time of the SPA agreement, other new scientific concerns regarding product safety or efficacy arise, the sponsor company fails to comply with the agreed upon trial protocols, or the relevant data, assumptions or information provided by the sponsor in a request for the SPA change or are found to be false or omit relevant facts.

An SPA agreement may be modified, and such modification will be deemed binding on the FDA review division, except under the circumstances described above, if the FDA and the sponsor agree in writing to modify the protocol and such modification is intended to improve the study.

In January 2017, we had a Type C meeting (which is any meeting other than a Type A or Type B meeting between CBER or CDER and a sponsor or applicant regarding the development and review of a product) with the FDA to discuss changes to our Phase III Cx601 clinical trial protocol relating to sample size and patient recruitment, among other aspects. Based on feedback from that meeting, we submitted a revised protocol in February 2017. There is no guarantee, however, that our revised protocol will be accepted by the FDA.

Risks Related to Our Financial Condition and Capital Requirements

If we fail to obtain additional financing, we may be unable to complete the development and commercialization of our product candidates.

Our operations have consumed substantial amounts of cash since inception. We expect to continue to spend substantial amounts to continue the clinical development of our product candidates. If our product candidates are approved, we will require significant additional funds in order to launch and commercialize such product candidates in the United States and internationally. We may also need to spend substantial amounts to expand our manufacturing infrastructure.

As at December 31, 2016, we had cash and cash equivalents of 78.0 million euros, and we believe that this amount will be sufficient to fund our operations through at least 12 months. However, changing circumstances may cause us to consume capital significantly faster than we currently anticipate, and we may need to spend more money than currently expected because of circumstances beyond our control. As a result, we may require additional capital for the further development and commercialization of our product candidates.

Our future funding requirements, both near and long-term, will depend on many factors, including, but not limited to, the following:

| · | The initiation, progress, timing, costs and results of clinical trials for our product candidates. |

| · | The clinical development plans we establish for these product candidates. |

| · | The number and characteristics of the product candidates that we develop and for which we seek regulatory approval. |

| · | The outcome, timing and cost of regulatory approvals by the FDA, the EMA and any other comparable foreign regulatory authorities, including the potential for the FDA, the EMA or any other comparable foreign regulatory authorities to require that we perform more studies than those that we currently expect. |

| · | The ability to enter into licensing agreements with appropriate partners and to negotiate favorable terms with such partners. |

| · | The cost of preparing, filing, prosecuting, defending and enforcing any patent claims and other intellectual property rights. |

| · | The effects of competing technological and market developments. |

| · | The cost and timing of completing the technology transfer to contract manufacturing organizations in the United States and other international markets. |

| · | The ability to scale up manufacturing activities for our product candidates and approved products to a commercial scale. |

| · | The cost and timing of completion of commercial-scale manufacturing activities. |

| · | The cost of establishing sales, marketing and distribution capabilities for any product candidates for which we may receive regulatory approval in regions where we choose to commercialize our products on our own. |

| · | The cost of obtaining favorable pricing and market access decisions from public and private payers for our products. |

Additional funding may not be available on a timely basis, on favorable terms, or at all, and such funds, if raised, may not be sufficient to enable us to continue to implement our business strategy. Our ability to borrow may

also be affected by the conditions under our financing agreements, including our 9% senior unsecured bonds due 2018 for 25.0 million euros in total principal amount, convertible into our ordinary shares, that we issued on March 6, 2015. If we are unable to raise additional funds through equity or debt financing, we may need to delay, scale back or eliminate expenditures for some of our research, development and commercialization plans, or grant rights to develop and market products that we would otherwise prefer to develop and market ourselves, thereby reducing their ultimate value to us.

We have a history of operating losses and an accumulated deficit and may never achieve sustained profitability.

We experienced operating losses since our founding in February 2000 until December 31, 2015. We experienced net losses of 13.0 million euros for the year ended December 31, 2014, net losses of 35.1 million euros for the year ended December 31, 2015 and net income of 3.8 million euros for the year ended December 31, 2016. As of December 31, 2016, we had an accumulated deficit of 116.2 million euros. Our losses resulted mainly from the following:

| · | Preclinical, clinical, manufacturing and regulatory efforts we undertook to advance the product candidates in our pipeline and to obtain marketing authorization from the EMA with respect to ChondroCelect and Cx601. |

| · | Our commercial efforts in launching ChondroCelect. |

| · | General and administrative costs associated with our operations. |

Except for the year ended December 31, 2016, our costs have always exceeded our revenues, which have been historically generated mainly through grants and income from the sale of ChondroCelect. In July 2016, TiGenix requested the withdrawal of marketing authorization for ChondroCelect for commercial reasons, which became effective as of November 30, 2016. TiGenix no longer generates revenues from ChondroCelect.

Our ability to achieve sustained profitability depends on our ability to develop and commercialize our product candidates, and we do not know when, or if, we will generate significant revenues from their sale in the future.

Even if we do generate sales from our product candidates in the future, we may never achieve sustained profitability. We anticipate substantial operating losses over the next several years as we execute our plan to expand our research, development and commercialization activities, including the clinical development and planned commercialization of our product candidates, and incur the additional costs of operating as a U.S.-listed public company. In addition, if we obtain regulatory approval of our product candidates, we may incur significant sales and marketing expenses. Because of the numerous risks and uncertainties associated with developing pharmaceutical products, we are unable to predict the extent of any future losses or when we will become profitable, if ever.

Our net losses and significant cash used in operating activities have raised substantial doubt regarding our ability to continue as a going concern.

We have a limited operating history and have experienced net losses and significant cash used in operating activities in each period since inception except for the year ended December 31, 2016. We expect to have significant cash outflows for at least the next twelve months following that date and had an accumulated deficit of 116.2 million euros as of December 31, 2016. In addition, we have debt service obligations under our convertible bonds and the loan facility agreement with Kreos Capital IV (UK) (“Kreos”), which have an impact on our cash flow. These conditions, among others, raise substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern could materially limit our ability to raise additional funds through the issuance of new debt or equity securities or otherwise. Future reports on our financial statements may include an emphasis of matter paragraph with respect to our ability to continue as a going concern. Except for the year 2016, we have not been profitable since inception, and it is possible we will never achieve sustained profitability. None of our product candidates can be marketed until governmental approvals have been obtained. Accordingly, there is no substantial source of revenues, much less profits, to sustain our present activities, and no substantial revenues will likely be available until, and unless, our product candidates are approved by the EMA, FDA or comparable regulatory agencies in other countries and successfully marketed, either by us or a partner, an outcome which may not occur. Based upon our currently expected level of operating expenditures, we expect to be able to fund our operations through at least 12 months after December 31, 2016 but we will require significant additional cash resources to

launch new development phases of existing projects in our pipeline. In addition, this period could be shortened if there are any significant increases in planned spending on development programs or more rapid progress of development programs than anticipated. Other financing may not be available when needed to allow us to continue as a going concern. The perception that we may not be able to continue as a going concern may cause others to choose not to deal with us due to concerns about our ability to meet our contractual obligations.

Our revenues and operating results may fluctuate and may not be sufficient to cover our fixed costs.

Our revenues and operating results have fluctuated in the past and are likely to do so in the future due to a number of factors, many of which are not under our control. Some of the factors that could cause our operating results to fluctuate include, but are not limited to, those listed below and identified throughout this Annual Report:

| · | The (positive or negative) success rate of our development efforts. |

| · | Our ability to manage future clinical trials, given the regulatory environment. |

| · | The timing of approval, if any, of our products by the appropriate regulatory bodies. |

| · | Our ability to commercialize our products whether by ourselves or in conjunction with licensing partners (including our ability to obtain funding or reimbursement from public and private payers for our products). |

| · | Our ability to scale up manufacturing activities for our product candidates and approved products to a commercial scale. |

There is no direct link between the level of our expenses in connection with developing our pipeline of expanded adipose-derived stem cell-based, or eASC-based, product candidates or our pipeline of cardiac stem cell-based, or CSC-based, product candidates and our revenues, which will primarily consist of royalties from sales of Cx601 under our licensing agreement with Takeda, once the product comes to market until we are able to bring another product to market. Accordingly, if revenues decline or do not grow as we expect, we may not be able to reduce our operating expenses correspondingly and may suffer losses accordingly.

Our ability to borrow and maintain outstanding borrowings is subject to certain restrictions under our convertible bonds.

On March 6, 2015, we issued 9% senior unsecured bonds due 2018 for 25.0 million euros in total principal amount, convertible into our ordinary shares. Under the terms of the convertible bonds, we are restricted from creating any security interests over any of our assets, including any part of our business, unless certain conditions are met. We may not be able to meet the conditions imposed by the trustee under the notes or the bondholders, which may restrict our ability to borrow and maintain outstanding borrowings. In addition, a breach of the covenant or other provisions of the bonds could result in an event of default, which, if not cured or waived, could result in outstanding borrowings becoming immediately due and payable.

The allocation of available resources could affect our ability to carry out our business plan.

We have significant flexibility and broad discretion to allocate and use our available resources. If such resources are not wisely allocated, our ability to carry out our business plan could be threatened. Our board of directors and management determines, in their sole discretion and without the need for approval from the holders of our ordinary shares and ADSs, the amounts and timing of our actual expenditures, which will depend upon numerous factors, including the status of our product development and commercialization efforts, if any, and the amount of cash received resulting from partnerships and out-licensing activities.

For example, after our acquisition of Coretherapix, we decided to prioritize the ongoing Phase I/II clinical trial of AlloCSC-01 in acute myocardial infarction, which resulted in our decision to put our planned Phase IIb trial for Cx611 in early rheumatoid arthritis on hold. Likewise, in prior years, we did not have sufficient resources to both pursue the clinical development of the products coming from the allogeneic eASC platform while simultaneously aggressively commercializing ChondroCelect. As a result, our board of directors decided to license ChondroCelect to Sobi in order to concentrate our existing human and capital resources on the clinical development of product candidates from the eASC-based platform, which we perceived to be of more value than commercializing ChondroCelect. In July 2016, TiGenix requested the withdrawal of marketing authorization for ChondroCelect for commercial reasons, which became effective as of November 30, 2016. TiGenix no longer generates revenues from ChondroCelect.

More generally, before the launch of ChondroCelect, we were expecting the product to be approved in both Europe and the United States. In order to approve the product in the United States, the FDA would have required us to perform a second Phase III trial in the United States, and the costs associated with such a trial made it impossible for us to launch the product into the United States, which we perceive to be our most important market. In Europe, we had anticipated that funding or reimbursement would be granted more rapidly in Spain and in the United Kingdom, that reimbursement would be approved on an unrestricted basis in Germany, and that reimbursement would be approved in France (see also “—There may be uncertainty over reimbursement from third parties for newly approved healthcare products or such reimbursement may be refused, which could affect our ability to commercialize our product candidates” below). We had also expected that the advanced therapy medicinal product regulation would be more strictly enforced (see “—We work in a strict regulatory environment, and future changes in any pharmaceutical legislation or guidelines, or unexpected events or new scientific insights occurring within the field of cell therapy, could affect our business” above), which would have forced all existing autologous chondrocyte implantation products that had not been approved through the advanced therapy medicinal product regulation to exit the market. Therefore, our expectations in respect of the potential market and the uptake of the product were higher than the results that were effectively obtained.

In addition, we constantly evaluate opportunities to acquire businesses and technologies that we believe are complementary to our business activities, such as our acquisition of Coretherapix, which has a platform of allogeneic cardiac stem cell products, and we also expend our human and capital resources on the integration of such acquired businesses and the development of their technologies, which may affect our ability to develop our own product candidates.

Our international operations pose currency risks, which may adversely affect our operating results and net income.

Our operating results may be affected by volatility in currency exchange rates and our ability to manage effectively our currency transaction risks. We use the euro as our currency for financial reporting purposes. In the future, a significant portion of our operating costs may be in U.S. dollars, because we have entered into an agreement with Lonza, a U.S.-based contract manufacturing organization, to manufacture our lead product candidate in the United States, and will enter into research and development collaborations, trial collaborations, and professional services contracts in the United States. We also expect a share of our future revenues to be in U.S. dollars. Our exposure to currency risks could increase over time. We do not currently manage our foreign currency exposure in a manner that would eliminate the effects of changes in foreign exchange rates. For example, we have not engaged in any active hedging techniques, and we have not employed any derivative instruments to date. Therefore, unfavorable fluctuations in the exchange rate between the euro and U.S. dollars could have a negative impact on our financial results.

Risks Related to Our Business

The manufacturing facilities where our product candidates are made are subject to regulatory requirements that may affect the development of our product candidates and the successful commercialization of our product candidates.

Our product candidates must be manufactured to high standards in compliance with regulatory requirements. The manufacture of such product candidates is subject to regulatory authorization and to the current good manufacturing practice, or cGMP, requirements prescribed in the relevant country or territory of manufacture or supply.

The cGMP requirements govern quality control of the manufacturing process and require written documentation of policies and procedures. Compliance with such procedures requires record keeping and quality control to ensure that the product meets applicable specifications and other requirements including audits of vendors, contract laboratories and suppliers. Manufacturing facilities are subject to inspection by regulatory authorities at any time. If an inspection by a regulatory authority indicates that there are deficiencies, we or our contract manufacturer could be required to take remedial actions, stop production or close the relevant facility. If we fail to comply with these requirements, we also may be required to curtail the relevant clinical trials, might not be permitted to sell our product candidates or may be limited as to the countries or territories in which we are permitted to sell them.

Our eASC-based development and clinical stage product candidates are manufactured in our facilities in Madrid, Spain, which have been certified by the Spanish Medicines and Medical Devices Agency under cGMP requirements. Cx601 will be manufactured by Lonza, a U.S.-based contract manufacturing organization, at its facility in Walkersville, Maryland, for our expected Phase III trial following the completion of technology transfer. Outside the United States, under our licensing agreement, we expect Takeda to assume responsibility for manufacturing Cx601 following the completion of technology transfer no later than January 1, 2021. AlloCSC-01, the CSC-based product candidate developed by our subsidiary Coretherapix, is manufactured by 3P Biopharmaceuticals, which has been certified as cGMP-compliant by the Spanish Medicines and Medical Devices Agency, based on a process developed by Coretherapix. However, the certification may be interrupted, suspended or discontinued because of a failure to maintain compliance or for any other reason. In addition, the regulations or policies applied by the relevant authorities may change, and any such change would require us to undertake additional work, which may not be sufficient for us to comply with the revised standards.

Any failure to comply with applicable cGMP requirements and other regulations may result in fines and civil penalties, suspension of production, product seizure or recall, import ban or detention, imposition of a consent decree, or withdrawal of product approval, and may limit the availability of our product candidates. Any manufacturing defect or error discovered after our product candidates have been produced and distributed also could result in significant consequences, including adverse health consequences, injury or death to patients, costly recall procedures, damage to our reputation and potential for product liability claims. An inability to continue manufacturing adequate supplies of our product candidates at our facilities in Madrid, Spain, or elsewhere could result in a disruption in the supply of our product candidates.

There may be uncertainty over funding or reimbursement from third parties for newly approved healthcare products or such funding or reimbursement may be refused, which could affect our ability to commercialize our product candidates.

Our ability to commercialize future product candidates will depend, in part, on the availability of reimbursement from government and health administration authorities, private health insurers, managed care programs and other third-party payers. Significant uncertainty exists as to the pricing, market access or reimbursement status of newly approved healthcare products. In many countries, medicinal products are subject to a regime of reimbursement by government health authorities, private health insurers or other organizations. Such organizations are under significant pressure to limit healthcare costs by restricting the availability and level of reimbursement. For example, we were not successful in obtaining certain forms of reimbursement with respect to ChondroCelect, such as the opinion of the French Haute Autorité de la Santé that ChondroCelect should not be reimbursed in France, the delays in obtaining funding or reimbursement in Spain and the United Kingdom, the decision to grant limited reimbursement in Germany, and the reversal of the decision to reimburse ChondroCelect in Belgium. Negative decisions or reversals of reimbursement decisions by certain authorities or third-party payers may have an unfavorable spillover effect on pending or future funding or reimbursement applications.

We may not be able to obtain or maintain prices for products sufficient to realize an appropriate return on investment if adequate public health service or health insurance coverage is not available. In addition, rules and regulations regarding funding or reimbursement may change, in some cases at short notice, especially in light of the global cost pressures on healthcare and pharmaceutical markets. Such changes could affect whether funding or reimbursement is available at adequate levels or at all.

The regulatory landscape that will govern our product candidates is evolving, and changes in regulatory requirements could result in delays or discontinuation of development of our product candidates or unexpected costs in obtaining regulatory approval.

Because we are developing novel stem cell therapy product candidates that are unique biological entities, the regulatory requirements that we will be subject to may change. Even with respect to more established products that fit into the categories of cell therapies, the regulatory landscape is still developing and will likely continue to change in the future. In particular, such products may be subject to increased scrutiny by regulatory authorities. For example, the EMA established a special committee called the Committee for Advanced Therapies to assess the quality, safety and efficacy of advanced-therapy medicinal products, a category that includes cell therapy products including our product candidates. This committee advises the Committee for Medicinal Products for Human Use, or CHMP, which is responsible for a final opinion on the granting, variation, suspension or revocation of an application for marketing authorization in the European Union.

Likewise, in the United States, the FDA has established the Office of Tissues and Advanced Therapies (OTAT), formerly known as the Office of Cellular, Tissue and Gene Therapies (OCTGT) within its Center for Biologics Evaluation and Research, or CBER, to consolidate the review of cell therapy and related products, and the Cellular, Tissue and Gene Therapies Advisory Committee to advise CBER on its review. Cell therapy clinical trials are also subject to review and oversight by an institutional biosafety committee, or IBC, a local institutional committee that reviews and oversees basic and clinical research conducted at the institution participating in the clinical trial. Although the FDA decides whether individual cell therapy protocols may proceed, review process and determinations of other reviewing bodies can impede or delay the initiation of a clinical study, even if the FDA has reviewed the study and approved its initiation. Conversely, the FDA can place an IND application on clinical hold even if such other entities have provided a favorable review. Furthermore, each clinical trial must be reviewed and approved by an independent institutional review board, or IRB, at or servicing each institution at which a clinical trial will be conducted. Similarly complex regulatory environments exist in other jurisdictions in which we might consider seeking regulatory approvals for our product candidates, further complicating the regulatory landscape.

As we advance our product candidates, we will be required to consult with these regulatory and advisory groups and comply with all applicable guidelines, rules and regulations. If we fail to do so, we may be required to delay or discontinue development of our product candidates. Delay or failure to obtain, or unexpected costs in obtaining, the regulatory approval necessary to bring a potential product to market could decrease our ability to generate sufficient product revenue to maintain our business.

These various regulatory review committees and advisory groups may also promulgate new or revised guidelines from time to time that may lengthen the regulatory review process, require us to perform additional studies, increase our development costs, lead to changes in regulatory positions and interpretations, delay or prevent approval and commercialization of our product candidates or lead to significant post-approval limitations or restrictions. Because the regulatory landscape for our stem cell therapy product candidates is evolving, we may face even more cumbersome and complex regulations in the future. Furthermore, even if our product candidates obtain required regulatory approvals, such approvals may later be withdrawn as a result of changes in regulations or the interpretation of regulations by applicable regulatory agencies.

In addition, adverse developments in clinical trials of cell therapy products conducted by others may cause the FDA or other regulatory bodies to change the requirements for approval of any of our product candidates.

Tissue-based products are regulated differently in different countries. These requirements may be costly and result in delay or otherwise preclude the distribution of our products in some foreign countries, any of which would adversely affect our ability to generate operating revenues.

Tissue-based products are regulated differently in different countries. Many foreign jurisdictions have a different and sometimes more difficult regulatory pathway for human tissue-based products, which may prohibit the distribution of these products until the applicable regulatory agencies grant marketing approval or licensure. The process of obtaining regulatory approval is lengthy, expensive and uncertain, and we may never seek such approvals, or if we do, we may never gain those approvals. Any adverse events in our clinical trials for a future product under development could negatively impact our products.

Safe and efficacious human medical applications may never be developed using cell therapy products or related technology.

If serious adverse events related to cell therapy products were to arise in clinical trials or after marketing approval, the EMA or FDA could impose more restrictive safety requirements on cell therapy products generally, including in the manner of use and manufacture, could require safety warnings in product labeling, and could limit, restrict or deny permission for new cell therapy products to enter clinical trials or to be marketed.

Our cell therapy product candidates represent new classes of therapy and may not be accepted by patients or medical practitioners.

Our ability to commercialize Cx601 and future product candidates will depend, in part, on market acceptance, including the willingness of medical practitioners to invest in training programs to use the products. Cell therapy products are a novel treatment, and such products may not be immediately accepted as complementary or alternative treatments to the current standards of care. We may not be able to obtain or maintain recommendations and endorsements from influential physicians, which are an essential factor for market acceptance of our product candidates, or our product candidates may not gain sufficient market recognition in spite of favorable opinions from key leaders.

The degree of market acceptance of our cell therapy product candidates will depend on a number of factors, including the following:

| · | The clinical safety and effectiveness of our products and their demonstrated advantage over alternative treatment methods. |

| · | Our ability to demonstrate to healthcare providers that our products provide a therapeutic advancement over standard of care or other competitive products or methods. |

| · | Our ability to educate healthcare providers on the use of patient-specific human tissue, to avoid potential confusion with and differentiate ourselves from the ethical controversies associated with human fetal tissue and engineered human tissue. |

| · | Our ability to educate healthcare providers, patients and payers on the safety and adverse reactions involving our products. |

| · | Our ability to meet supply and demand and develop a core group of medical professionals familiar with and committed to the use of our products. |

| · | The cost-effectiveness of our products and the reimbursement policies of government and third-party payers. |

If the medical community or patients do not accept the safety and effectiveness of our product candidates or they fail to demonstrate a favorable risk/benefit profile, this could negatively affect any future sales.

Ethical, legal, social and other concerns surrounding the use of human tissue in synthetic biologically engineered products may negatively affect public perception of us or our product candidates, or may result in increased scrutiny of our product candidates from a regulatory perspective.

The public perception of ethical and social issues surrounding the use of tissue-engineered products or stem cells may limit or discourage the use of our product candidates. The use of human cells, such as differentiated cartilage cells, eASCs, CSCs and other adult stem cells, as starting material for the development of our product candidates could generate negative public perceptions of our product candidates and public expressions of concern could result in stricter governmental regulation, which may, in turn, increase the cost of manufacturing and marketing our product or impede market acceptance of our product candidates.

The manufacture of cell therapy products is characterized by inherent risks and challenges and may be a more costly endeavor than manufacturing other therapeutic products.

The manufacture of cell therapy products, such as our product candidates, is highly complex and is characterized by inherent risks and challenges, such as raw material inconsistencies, logistical challenges, significant quality control and assurance requirements, manufacturing complexity, and significant manual processing. Unlike products that rely on chemicals for efficacy, such as most pharmaceuticals, cell therapy products are difficult to characterize due to the inherent variability of biological input materials. As a result, assays of the finished product may not be sufficient to ensure that the product will perform in the intended manner. Accordingly, we employ multiple steps to control our manufacturing process to ensure that the process works and that our product candidate is made strictly and consistently in compliance with the process. Problems with the manufacturing process, even minor deviations from the normal process, could result in product defects or manufacturing failures that result in lot failures, product recalls, product liability claims or insufficient inventory, which could be costly to us or result in reputational damage. We have experienced lot failures in the past and we might experience such failures in the future.

We may encounter problems achieving adequate quantities and quality of clinical-grade materials that meet EMA, FDA or other applicable standards or specifications with consistent and acceptable production yields and costs. In addition, the FDA, the EMA and other foreign regulatory authorities may require us to submit samples of any lot of any approved product together with the protocols showing the results of applicable tests at any time. Under some circumstances, the FDA, the EMA or other foreign regulatory authorities may require that we not distribute a lot until the agency authorizes its release.

Successfully transferring complicated manufacturing techniques to contract manufacturing organizations and scaling up these techniques for commercial quantities is time consuming and subject to potential difficulties and delays. We have entered into an agreement with Lonza, a leading U.S.-based contract manufacturing organization active in biological and cell therapy manufacturing, to produce Cx601 in the United States in connection with the proposed Phase III clinical trial to register Cx601 in the United States. Our technology transfer to Lonza may result in setbacks in replicating the current manufacturing process at a new facility and in scaling up production. Likewise, we or any other third parties with whom we enter into strategic relationships, including Takeda, might not be successful in streamlining manufacturing operations or implementing efficient, low-cost manufacturing capabilities and processes that will enable us to meet the quality, price and production standards or production volumes to achieve profitability. Our failure to develop these manufacturing processes in a timely manner could prevent us from achieving our growth and profitability objectives as projected or at all.

We face competition and technological change, which could limit or eliminate the market opportunity for our product candidates.

The pharmaceutical industry is characterized by intense competition and rapid innovation. Our product candidates will compete against a variety of therapies in development for inflammatory and autoimmune diseases that use therapeutic modalities such as biologics and cell therapy, including products under development by Anterogen, Delenex Therapeutics, Novartis, Celgene, Bristol Myers Squibb, Sanofi/Regeneron, Johnson & Johnson, GlaxoSmithKline and others, including various hospitals and research centers. Finally, with respect to the product candidates of our subsidiary Coretherapix, there are a variety of cell therapy treatments in development for acute myocardial infarction, including products under development by Pharmicell, Caladrius, Athersys, Mesoblast and Capricor.

Our competitors may be able to develop other products that are able to achieve similar or better results than our product candidates. Our potential competitors include established and emerging pharmaceutical and biotechnology companies and universities and other research institutions. Many of our competitors have substantially greater financial, technical and other resources, such as larger research and development staff and experienced marketing and manufacturing organizations and well-established sales forces. Smaller or early-stage companies may also prove to be significant competitors, particularly through collaborative arrangements with large, established companies. Mergers and acquisitions in the pharmaceutical and biotechnology industries may result in even more resources being concentrated in our competitors. Competition may increase further as a result of advances in the commercial applicability of technologies and greater availability of capital for investment in these industries. Our competitors may succeed in developing, acquiring or licensing on an exclusive basis products that are more effective or less costly than our product candidates. We believe the key competitive factors that will affect the development and commercial success of our product candidates are efficacy, safety and tolerability profile, reliability, price and reimbursement.

Our employees may engage in misconduct or other improper activities, including noncompliance with regulatory standards and requirements.

We are exposed to the risk of employee fraud or other misconduct. Misconduct by employees could include intentional failures to comply with EMA or FDA regulations, to provide accurate information to the EMA or FDA, to comply with manufacturing standards we have established, to comply with federal and state healthcare fraud and abuse laws and regulations, to report financial information or data accurately or to disclose unauthorized activities to us. In particular, sales, marketing and business arrangements in the healthcare industry are subject to extensive laws and regulations intended to prevent off-label promotion, fraud, kickbacks, self-dealing and other abusive practices in

the United States and in jurisdictions outside of the United States where we conduct our business. These laws and regulations may restrict or prohibit a wide range of pricing, discounting, marketing and promotion, sales commission, customer incentive programs and other business arrangements. Employee misconduct could also involve the improper use of information obtained in the course of clinical trials, which could result in regulatory sanctions and serious harm to our reputation. If governmental investigations or other actions or lawsuits stemming from a failure to be in compliance with such laws or regulations are instituted against us, and we are not successful in defending ourselves or asserting our rights, those actions could have a significant impact on our business, including the imposition of significant fines or other sanctions, up to and including criminal prosecution, fines and imprisonment.

We could face product liability claims, resulting in damages against which we are uninsured or underinsured.

Our business exposes us to potential product liability and professional indemnity risks, which are inherent in the research, development, manufacturing, marketing and use of medical treatments. It is impossible to predict the potential adverse effects that our product candidates may have on humans. The use of our product candidates in human clinical trials may result in adverse effects, and long-term adverse effects may only be identified following clinical trials and approval for commercial sale. In addition, physicians and patients may not comply with any warnings that identify the known potential adverse effects and the types of patients who should not receive our product candidates. We may not be able to obtain necessary insurance at an acceptable cost or at all. We currently carry 20-million euros of liability insurance. In the event of any claim, the level of insurance we carry now or in the future may not be adequate, and a product liability or other claim may materially and adversely affect our business. If we cannot adequately protect ourselves against potential liability claims, we may find it difficult or impossible to commercialize our product candidates. Moreover, such claims may require significant financial and managerial resources, may harm our reputation if the market perceives our drugs or drug candidates to be unsafe or ineffective due to unforeseen side effects, and may limit or prevent the further development or commercialization of our product candidates and future product candidates.

We use various chemical and biological products to conduct our research and to manufacture our medicines. Despite the existence of strict internal controls, these chemical and biological products could be the object of unauthorized use or could be involved in an accident that could cause personal injury to people or damage to the environment, which could result in a claim against us. Our activities are subject to specific environmental regulations that impose obligations which, if not complied with, could give rise to third party or administrative claims and could even result in fines being imposed or, in the worst case scenario, to our operations being suspended or shut down.

Our international operations subject us to various risks, and our failure to manage these risks could adversely affect our results of operations.

We face significant operational risks as a result of doing business internationally, such as the following:

| · | fluctuations in foreign currency exchange rates; |

| · | potentially adverse and/or unexpected tax consequences, including penalties due to the failure of tax planning or due to the challenge by tax authorities on the basis of transfer pricing and liabilities imposed from inconsistent enforcement; |

| · | potential changes to the accounting standards, which may influence our financial situation and results; |

| · | becoming subject to the different, complex and changing laws, regulations and court systems of multiple jurisdictions and compliance with a wide variety of foreign laws, treaties and regulations; |

| · | difficulties in attracting and retaining qualified personnel; |

| · | rapid changes in global government, economic and political policies and conditions, political or civil unrest or instability, terrorism or epidemics and other similar outbreaks or events, and potential failure in confidence of our suppliers or customers due to such changes or events; and |

| · | tariffs, trade protection measures, import or export licensing requirements, trade embargoes and other trade barriers. |

Our inability to manage our expansion, both internally and externally, could have a material adverse effect on its business.

We may in the future acquire other businesses, companies with complementary technologies or products to expand our activities. As a consequence, intangible assets, including goodwill, may account for a larger part of the balance sheet total than is currently the case. Despite the fact that we carefully investigate every acquisition, the risk remains, amongst others, that corporate cultures may not match, expected synergies may not be fully realized, restructurings may prove to be more costly than initially anticipated and that acquired companies may prove to be more difficult to integrate than foreseen. We can therefore not guarantee that we will successfully be able to integrate any acquired companies.

Our ability to manage our growth effectively will require us to continue to improve our operations, financial and management controls, reporting systems and procedures, and to train, motivate and manage our employees and, as required, to install new management information and control systems. We may not be able to implement improvements to our management information and control systems in an efficient and timely manner or such improvements, if implemented, may not be adequate to support our operations.

The results of the United Kingdom’s referendum on leaving the European Union may have a negative effect on our business.

On June 23, 2016, a majority of voters in the United Kingdom voted to leave the European Union in a referendum and on March 29, 2017 the United Kingdom delivered its official withdrawal notification to the President of the European Council. The terms of the United Kingdom’s withdrawal are subject to a negotiation period that could last up to two years from the date the withdrawal notification was delivered. The United Kingdom’s decision has created significant uncertainty about the future relationship between the United Kingdom and the European Union, including with respect to the laws and regulations that will apply in the future. These developments have had and may continue to have a material adverse effect on global economic conditions and the stability of global financial markets, and may significantly reduce global market liquidity and restrict the ability of key market participants to operate in certain financial markets. Any of these factors could depress economic activity and restrict our access to capital. In addition, it is uncertain whether our EMA approvals, if granted, will cover the United Kingdom. If not, it is not yet known what the new U.K. approval process will involve.

Risks Related to Our Intellectual Property

We may not be able to protect adequately our proprietary technology or enforce any rights related thereto.

Our ability to compete effectively with other companies depends, among other things, on the exploitation of our technology. In addition, filing, prosecuting and defending patents on all of our product candidates throughout the world would be prohibitively expensive. Our competitors may, therefore, develop equivalent technologies or otherwise gain access to our technology, particularly in jurisdictions in which we have not obtained patent protection or in which enforcement of such protection is not as strong as it is in the United States.