STROOCK & STROOCK & LAVAN LLP

180 Maiden Lane

New York, New York 10038

April 22, 2014

Via EDGAR and E-mail (pdf)

Ms. Angie Kim

Securities and Exchange Commission

100 F. Street, N.E.

Washington, D.C. 20549

| Re: | PBF Logistics LP |

| File No. 333-195024 |

Dear Ms. Kim:

Pursuant to discussions with the staff of the Division of Corporation Finance (the “Staff”) of the Securities and Exchange Commission (the “Commission”), PBF Logistics LP (the “Partnership”) hereby submits the proposed offering terms of the initial public offering (the “Offering”), including the bona fide price range pursuant to Item 501(b)(3) of Regulation S-K. These pricing terms shall be included in Amendment No. 2 to the Registration Statement on Form S-1, File No. 333-195024 (the “Registration Statement”) to be filed with the Commission on or about April 30, 2014. The provided terms are a bona fide estimate of the range of the minimum and maximum offering price and the maximum number of securities to be offered as of April 22, 2014. Should the bona fide estimates of these terms change between today and April 30, 2014, the figures presented in Amendment No. 2 may increase or decrease accordingly.

The Partnership proposes to price the Offering with a bona fide price range of $19.00 to $21.00 per common unit, with a midpoint of $20.00 per common unit. In the Offering, the Partnership proposes to sell up to 13,750,000 common units representing limited partner interests in the Partnership and up to an additional 2,062,500 common units pursuant to the underwriters’ option to purchase additional common units. As discussed with members of the Staff, this range is initially being provided for your consideration by correspondence given the Partnership’s and the underwriters’ concern regarding providing such information significantly in advance of the launch of the offering given recent market volatility as well as our desire to provide all information necessary for the Staff to complete its review on a timely basis.

Additionally, the Partnership is enclosing its proposed marked copy of those pages of the Registration Statement that will be affected by the offering terms set forth herein. These marked changes will be incorporated into Amendment No. 2, to be filed with the Commission on or about April 30, 2014. Amendment No. 2 will also include the Underwriting Agreement as Exhibit 1.1.

The Partnership seeks confirmation from the Staff that it may launch its Offering with the price range specified herein and include such price range in Amendment No. 2 of the Registration Statement.

Securities and Exchange Commission

Page 2

Please do not hesitate to call the undersigned at (212) 806-5793 with respect to the foregoing or if any additional supplemental information is required by the Staff.

| Sincerely, |

/s/ Todd E. Lenson |

Todd E. Lenson |

| cc: | H. Roger Schwall (Securities and Exchange Commission) |

Jeffrey Dill, Esq. (PBF Logistics LP)

Michael J. Swidler, Esq. (Vinson & Elkins L.L.P.)

Douglas Horowitz, Esq. (Cahill Gordon & Reindel LLP)

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated April 30, 2014

PROSPECTUS

PBF Logistics LP

13,750,000 Common Units

Representing Limited Partner Interests

This is the initial public offering of our common units representing limited partner interests. We are offering 13,750,000 common units in this offering. We currently expect that the initial public offering price will be between $19.00 and $21.00 per common unit. Prior to this offering, there has been no public market for our common units. We have been approved to list our common units on the New York Stock Exchange under the symbol “PBFX,” subject to official notice of issuance. We are an “emerging growth company” as defined under the federal securities laws and, as such, are eligible for reduced reporting requirements.

Investing in our common units involves risks. Please read “Risk Factors” beginning on page 21.

These risks include the following:

| • | We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our general partner and its affiliates, to enable us to pay the minimum quarterly distribution to holders of our common and subordinated units. |

| • | On a pro forma basis, we would not have had sufficient cash available for distribution to pay the full minimum quarterly distribution on any of our common units and subordinated units for the year ended December 31, 2013. |

| • | We have no operating history and, accordingly, you will have a limited basis upon which to evaluate our ability to achieve our business objectives. |

| • | PBF Energy Inc., our sponsor, accounts for all of our revenues. Therefore, we are subject to the business risks of our sponsor. If our sponsor changes its business strategy, fails to satisfy its obligations under our commercial agreements with it for any reason or significantly reduces the volumes throughput at our facilities, our revenues could decline, which would have a material adverse effect on our financial condition, results of operations, cash flows and ability to make distributions to unitholders. |

| • | Each of our commercial agreements and our operation and management services and secondment agreement with our sponsor contains provisions that allow our counterparty to such agreement to suspend, reduce or terminate its obligations under such agreement in certain circumstances, including events of force majeure, which would have a material adverse effect on our financial condition, results of operations, cash flows and ability to make distributions to unitholders. |

| • | All of our revenues are generated at two facilities. Any adverse development at either facility could have a material adverse effect on our financial condition, results of operations, cash flows and ability to make distributions to unitholders. |

| • | Our general partner and its affiliates, including our sponsor, have conflicts of interest with us and limited duties to us and our unitholders, and they may favor their own interests to the detriment of us and our other common unitholders. |

| • | You will experience immediate and substantial dilution in net tangible book value of $18.83 per common unit. |

| • | Our partnership agreement restricts the remedies available to holders of our common units for actions taken by our general partner that might otherwise constitute breaches of fiduciary duty. |

| • | Holders of our common units have limited voting rights and are not entitled to elect our general partner or its directors. |

| • | Our tax treatment depends on our status as a partnership for U.S. federal income tax purposes, as well as our not being subject to a material amount of entity level taxation by individual states. If the IRS were to treat us as a corporation for U.S. federal income tax purposes or we were to become subject to material additional amounts of entity level taxation for state tax purposes, then our cash available for distribution to our unitholders would be substantially reduced. |

| • | Our unitholders’ share of our income will be taxable to them for U.S. federal income tax purposes even if they do not receive any cash distributions from us. |

| Per Common Unit | Total | |||

Public offering price | $ | $ | ||

Underwriting discount (1) | $ | $ | ||

Proceeds to PBF Logistics LP (before expenses) (1) | $ | $ | ||

| (1) | Excludes an aggregate structuring fee equal to 0.25% of the gross proceeds of this offering payable to Barclays Capital Inc. and UBS Securities LLC. Please read “Underwriting.” |

We have granted the underwriters a 30-day option to purchase up to an additional 2,062,500 common units on the same terms and conditions as set forth above.

Thomas D. O’Malley, the Chairman of the board of directors of our general partner, and certain of his affiliates and family members have indicated an interest in purchasing up to an aggregate of $10 million of common units in this offering at the initial public offering price. However, because indications of interest are not binding agreements or commitments to purchase, the underwriters may determine to sell more, less or no common units in this offering to any of these persons, and any of these persons may determine to purchase more, less or no common units in this offering. The underwriters will receive the same underwriting discount on any common units purchased by these persons as they will on any other common units sold to the public in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the common units to purchasers on or about , 2014, through the book-entry facilities of The Depository Trust Company.

| Barclays | UBS Investment Bank |

| Citigroup | Credit Suisse | Deutsche Bank Securities |

Prospectus dated , 2014.

This summary highlights information contained elsewhere in this prospectus. It does not contain all of the information that you should consider before investing in the common units. You should read the entire prospectus carefully, including “Risk Factors” beginning on page 21 and the historical and pro forma financial statements and the notes to those financial statements included elsewhere in this prospectus. Unless indicated otherwise, the information presented in this prospectus assumes (1) an initial public offering price of $20.00 per common unit (the midpoint of the price range set forth on the cover page of this prospectus) and (2) that the underwriters do not exercise their option to purchase additional common units.

Unless otherwise noted, references in this prospectus to “PBF Logistics,” “we,” “our,” “us” or like terms when used in a historical context refer to the businesses and assets of PBF MLP Predecessor as described in “Summary Historical and Pro Forma Financial and Operating Data” beginning on page 17, our predecessor for accounting purposes, also referenced as “our predecessor,” and when used in the present tense or prospectively, refer to PBF Logistics LP and its subsidiaries. Unless the context otherwise requires, references in this prospectus to “PBF Holding” are to PBF Holding Company LLC and its consolidated subsidiaries, other than us. References to “PBF LLC” refer to PBF Energy Company LLC, and to “PBF Energy” or “our sponsor” refer to PBF Energy Inc., a Delaware corporation and managing member of PBF LLC, which trades on the New York Stock Exchange under the symbol “PBF,” and, unless the context otherwise requires, its consolidated subsidiaries, including PBF LLC and PBF Holding. References to our “general partner” are to PBF Logistics GP LLC, the general partner of PBF Logistics and a wholly owned subsidiary of PBF LLC. References to affiliates of our sponsor are to PBF Energy’s subsidiaries, excluding us, our general partner and our subsidiary.

PBF Logistics LP

Overview

We are a fee-based, growth-oriented, traditional Delaware master limited partnership recently formed by PBF Energy to own or lease, operate, develop and acquire crude oil and refined petroleum products terminals, pipelines, storage facilities and similar logistics assets. We receive, handle and transfer crude oil from sources located throughout the United States and Canada for PBF Energy in support of its three refineries located in Toledo, Ohio, Delaware City, Delaware and Paulsboro, New Jersey. Our initial assets consist of a light crude oil rail unloading terminal at the Delaware City refinery that also services the Paulsboro refinery (which we refer to as the “Delaware City Rail Terminal”), and a crude oil truck unloading terminal at the Toledo refinery (which we refer to as the “Toledo Truck Terminal”) that are integral components of the crude oil delivery operations at all three of PBF Energy’s refineries. We generate revenue by charging fees for receiving, handling and transferring crude oil. We do not take ownership of or receive any payments based on the value of the crude oil that we handle and do not engage in the trading of any commodities. As a result, we have no direct exposure to commodity price fluctuations.

At the closing of this offering, all of our revenue will be derived from long-term, fee-based commercial agreements with subsidiaries of PBF Energy, which we believe will enhance the stability of our cash flows. Our commercial agreements with PBF Energy will include minimum quarterly volume commitments, inflation escalators and an initial term of seven years.

We intend to seek opportunities to grow our business by acquiring additional logistics assets from PBF Energy and third parties and through organic growth, including by potentially constructing new assets and increasing the utilization of our existing assets. We were formed by PBF Energy to be the primary vehicle to expand the logistics assets supporting its business. We expect that PBF Energy will serve as a critical source of our future growth by providing us with opportunities to purchase additional logistics assets that it currently owns

1

training and development programs. We will continue to emphasize safety in all aspects of our operations. For example, we believe our and our sponsor’s operations comply with the recently enacted emergency orders governing shipments of petroleum crude oil transported by rail. We believe these objectives are integral to maintaining stable cash flows and are critical to the success of our business. |

Competitive Strengths

We believe we are well positioned to successfully execute our business strategies because of the following competitive strengths:

| • | Relationship with PBF Energy. One of our key strengths is our relationship with PBF Energy. We will serve as PBF Energy’s primary vehicle to expand the logistics assets supporting its business. We believe that PBF Energy will be incentivized to grow our business as a result of its significant indirect economic interest in us, including 100% ownership of our general partner, a 56.7% limited partnership interest in us and all of our incentive distribution rights. In particular, we expect to benefit from the following aspects of our relationship with PBF Energy: |

| — | Acquisition Opportunities. Under the omnibus agreement, PBF Energy has granted us a right of first offer on certain logistics assets that it will retain following this offering and may, under certain circumstances, offer us the opportunity to purchase additional logistics assets that it may acquire or construct in the future. We also expect to jointly pursue strategic acquisitions with PBF Energy that complement and grow our asset base. |

| — | Strength of PBF Energy’s Refining Business. PBF Energy’s Delaware City, Paulsboro and Toledo refineries have a combined throughput capacity of 540,000 bpd, making PBF Energy the fifth largest independent refiner in the United States. PBF Energy’s refineries provide it with buying power advantages, and it benefits from the cost efficiencies that result from operating three large refineries. In addition, its refinery assets are located in high-demand regions where product demand exceeds refining capacity. |

| — | Access to Operational and Industry Expertise.We expect to benefit from PBF Energy’s extensive operational, commercial and technical expertise, as well as its industry relationships throughout the midstream and downstream value chain, as we look to optimize and expand our existing asset base. |

| • | Stable Cash Flows Supported by Long-Term, Fee-Based Contracts with Minimum Volume Commitments.We will initially generate all of our revenue under long-term, fee-based contracts with PBF Energy. Each of our commercial agreements with PBF Energy will include minimum volume commitments and will have fees adjusted for changes in the Producer Price Index and any increase in our operating costs for providing such services under such agreements, thereby providing us with stable and predictable minimum cash flows. |

| • | Strategically Located and Highly Integrated Assets. Our logistics assets are integral to the operations of PBF Energy’s refineries. Our Delaware City Rail Terminal currently receives a substantial portion of the light crude oil processed by the Delaware City and Paulsboro refineries, and the Toledo Truck Terminal provides important feedstock supply infrastructure for the Toledo refinery. |

| • | High-Quality, Well-Maintained Asset Base. We continually invest in the maintenance and integrity of our assets and have developed various programs to help us efficiently monitor and maintain the assets. We employ an asset integrity program, which focuses on risk analysis, assessment, inspection, preventive measures, repair and data integration to provide reliable operations and to prevent, control and mitigate unintentional releases of hazardous materials. We also have developed and use industrial processes to monitor and control our operations. In addition, our Delaware City Rail Terminal commenced operations in February 2013 and requires a relatively small amount of maintenance capital expenditure, relative to peers with older assets. |

3

| • | Financial Flexibility. We believe that we will have the financial flexibility to execute our growth strategy through access to the debt and equity capital markets, as well as the approximately $275.0 million of available capacity under our revolving credit facility that we expect to enter into at the closing of this offering. |

| • | Experienced Management and Operations Teams with a Demonstrated Track Record of Acquiring, Integrating and Operating Logistics Assets. Both our management and our operations teams have significant experience in the management and operation of logistics assets and the execution of expansion and acquisition strategies. Our management team has a proven track record of working together successfully to operate refining and logistics assets and to execute expansion and acquisition strategies, including while previously at Tosco Corporation and Premcor Inc. |

Our Assets and Operations

Our initial assets include:

| • | Delaware City Rail Terminal. Our Delaware City Rail Terminal is a light crude oil rail unloading terminal which commenced operations in February 2013 and serves our sponsor’s Delaware City refinery and Paulsboro refinery delivered by barge by our sponsor. It is capable of discharging up to 105,000 bpd and has a double-loop track, which can hold up to two 100-car unit trains. The terminal is capable of unloading a single unit train in approximately 14 hours. An expansion project is underway that will increase the Delaware City Rail Terminal’s unloading capacity from 105,000 bpd to 130,000 bpd in the third quarter of 2014. The operational flexibility afforded by the rail terminal has the potential to enhance the profitability at both refineries by allowing the refineries to optimize their respective crude oil slates. The Delaware City Rail Terminal allows our sponsor’s East Coast refineries to source crude oil from Western Canada and the Midcontinent, which currently provide significant cost advantages compared to international crude oil that has historically been processed at our sponsor’s East Coast refineries and that is priced off of Brent. Our sponsor’s East Coast refineries at Delaware City and Paulsboro have a combined refining capacity of 370,000 bpd. |

| • | Toledo Truck Terminal. Our Toledo Truck Terminal serves our sponsor’s Toledo refinery. The Toledo Truck Terminal has unloading capacity of 15,000 bpd. PBF Energy acquired the Toledo refinery in 2011 and has added additional truck crude oil unloading capabilities that provide feedstock sourcing flexibility for the refinery and enable Toledo to run a more cost-advantaged crude oil slate. The Toledo refinery processes light, sweet crude oil and has a throughput capacity of 170,000 bpd. |

Logistics Assets Owned by PBF Energy

We believe that our relationship with PBF Energy should provide us with a number of potential future growth opportunities, including the potential to acquire assets to which PBF Energy has granted us a right of first offer for a period of 10 years after the closing of this offering and, under certain circumstances, a purchase option. The assets subject to our right of first offer are traditional logistics assets of PBF Energy that are critical to supporting its core refining operations and include the following:

| • | Delaware City Storage Facility. The Delaware City Storage Facility has approximately 10.0 million barrels of total storage capacity, with 3.6 million barrels dedicated to crude oil and feedstock storage and the remaining 6.4 million barrels allocated to finished, intermediate and other products. |

| • | Delaware City Heavy Crude Oil Terminal. The Delaware City Heavy Crude Oil Terminal includes a heavy crude oil unloading facility at the Delaware City refinery with total throughput capacity of approximately 40,000 bpd. Additionally, PBF Energy recently announced a project to add approximately 40,000 bpd of incremental heavy crude oil unloading capability at the Delaware City refinery. PBF Energy expects this project to be completed by the end of the third quarter of 2014, |

4

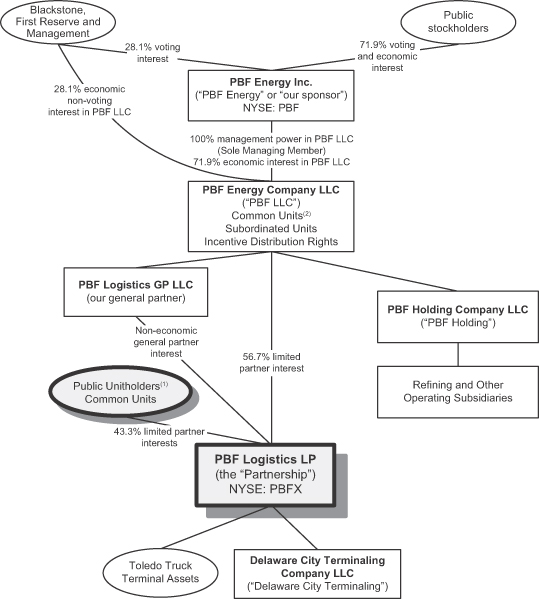

As of March 31, 2014, PBF Energy’s sole asset is a controlling economic interest of approximately 71.9% in PBF LLC, with the remaining 28.1% of the economic interests in PBF LLC held by funds affiliated with The Blackstone Group L.P., or Blackstone, and First Reserve Management, L.P., or First Reserve, and our executive officers and directors and certain employees (we refer to the holders of the remaining interests in PBF LLC as “the members of PBF LLC other than PBF Energy”). The public stockholders of PBF Energy have approximately 71.9% of the voting power in PBF Energy, and the members of PBF LLC other than PBF Energy have the remaining approximately 28.1% of the voting power in PBF Energy. As a result, Blackstone and First Reserve and the other members of PBF LLC are able to significantly influence PBF Energy. Blackstone and First Reserve are in the business of making investments in companies and may from time to time acquire and hold interests in businesses that compete directly or indirectly with us. Our partnership agreement contains a provision renouncing our interest and expectancy in certain corporate opportunities identified by Blackstone or First Reserve. See “Risk Factors—Risks Related to our Business—Blackstone and First Reserve through their ownership of units of PBF LLC have substantial influence or control over PBF LLC, and their interests may differ from those of PBF LLC, us and our public unitholders.”

Following the closing of this offering, PBF Energy, through its ownership in PBF LLC, will retain a significant interest in us. PBF LLC owns 100% of our general partner and all of our incentive distribution rights, which will entitle it to increasing percentages, up to a maximum of 50.0%, of the cash we distribute in excess of $0.345 per unit per quarter after the closing of our initial public offering. In addition, PBF Energy, through its ownership in PBF LLC, will own 2,136,553 common units and 15,886,553 subordinated units, representing a 56.7% limited partner interest in us. Our general partner will own a noneconomic general partner interest in us. Please read “Certain Relationships and Related Party Transactions.”

While our relationship with PBF Energy is a significant strength, it is also a source of potential conflicts. Please read “Risk Factors” and “Conflicts of Interest and Fiduciary Duties.”

Risk Factors

An investment in our common units involves risks associated with our business (including PBF Energy’s business and creditworthiness), our regulatory and legal matters, our limited partnership structure and the tax characteristics of our common units. You should carefully consider the risks described in “Risk Factors.”

Formation Transactions and Partnership Structure

We were formed in February 2013 by PBF Energy to own or lease, operate, develop and acquire crude oil, refined products and similar logistics assets. In connection with the closing of this offering, we will acquire from PBF Holding (1) a 100% interest in Delaware City Terminaling, which owns the Delaware City Rail Terminal, and (2) the Toledo Truck Terminal.

At the closing of this offering the following transactions, which we refer to as the formation transactions, will occur:

| • | Delaware City Refining Company LLC (“DCR”), a wholly owned subsidiary of PBF Holding, distributes all of the interests in Delaware City Terminaling and Toledo Refining distributes the Toledo Truck Terminal, in each case, to PBF Holding. |

| • | PBF Holding contributes (i) all of the interests in Delaware City Terminaling and (ii) the Toledo Truck Terminal to us in exchange for (a) 74,053 common units and 15,886,553 subordinated units representing an aggregate 50.2% limited partner interest in us, (b) all of our incentive distribution rights, (c) the right to receive distributions from us as reimbursement for certain preformation capital expenditures attributable to the contributed assets, (d) the right to receive the distribution of $245.8 million and |

7

(e) the right to either (A) receive up to an additional 2,062,500 common units representing a 6.5% limited partner interest in us, (B) receive a cash distribution if the underwriters’ option to purchase additional units is exercised, or (C) a combination of both (A) and (B), and in connection with the foregoing, we will redeem PBF Holding’s initial partner interests in us for $1,000. |

| • | We will issue 13,750,000 common units to the public in this offering, representing a 43.3% limited partner interest in us, and will apply the net proceeds as described in “Use of Proceeds.” |

| • | PBF Holding distributes to PBF LLC (i) its interest in our general partner, (ii) the common units, subordinated units and incentive distribution rights, (iii) the right to receive a distribution as reimbursement for certain preformation capital expenditures, (iv) the right to receive the distribution of $245.8 million and (v) the right to receive additional common units and/or cash depending on whether the underwriters’ option to purchase additional units is exercised in whole or in part. |

| • | We will borrow approximately $215.8 million of term debt and use the proceeds to make a distribution to PBF LLC. |

| • | We will enter into a new $275.0 million revolving credit facility, which will remain undrawn at the closing of this offering. |

| • | We will enter into long-term commercial agreements with PBF Energy. |

| • | We and our general partner will enter into an omnibus agreement with PBF Energy. |

| • | We, our general partner and our subsidiary will enter into an operation and management services and secondment agreement with PBF Energy. |

If and to the extent the underwriters exercise their option to purchase up to 2,062,500 additional common units, the number of common units purchased by the underwriters pursuant to such exercise will be issued to the public and the remaining common units, if any, will be issued to PBF LLC at the expiration of the option period. Any such units issued to PBF LLC will be issued for no additional consideration. Accordingly, the exercise of the underwriters’ option will not affect the total number of common units outstanding or the amount of cash needed to pay the minimum quarterly distribution on all units. If the underwriters’ option is exercised in full, PBF LLC will own 0.5% of the common units and the public will own 99.5% of the common units. Please read “Underwriting.” If the underwriters exercise their option to purchase additional common units in full, the additional net proceeds would be approximately $38.7 million. The net proceeds received in connection with any exercise of such option will be used to purchase a corresponding amount of additional U.S. Treasury or other investment grade securities, which will be used to fund anticipated capital expenditures. In addition, we will borrow under our term loan an amount equal to the net proceeds received upon any exercise of the underwriters’ option to purchase additional common units and distribute the proceeds of such borrowing to PBF LLC.

Ownership of PBF Logistics LP

After giving effect to the formation transactions and this offering, assuming the underwriters’ option to purchase additional common units is not exercised, all of our incentive distribution rights will be held indirectly by PBF Energy and our units will be held as follows:

Public Common Units (1)(2) | 43.3% | |||

PBF Energy Units: | ||||

Common Units | 6.7% | |||

Subordinated Units | 50.0% | |||

Non-Economic General Partner Interest | — | |||

|

| |||

Total | 100.0% | |||

|

|

8

The following diagram depicts our simplified organizational and ownership structure, as of March 31, 2014, after giving effect to the formation transactions and this offering.

| (1) | Includes up to 687,500 common units that may be purchased by certain of our directors, officers and related persons pursuant to direct sales or a directed unit program, as described in more detail in “Underwriting—Direct Sales to Insiders and Directed Unit Program.” |

| (2) | Includes 2,062,500 common units that will be issued to PBF Energy (through its ownership in PBF LLC), for no additional consideration, at the expiration of the underwriters’ option to purchase additional common units, if the underwriters do not exercise their option to purchase additional common units. If the underwriters exercise their option to purchase up to 2,062,500 additional common units, the number of common units purchased by the underwriters pursuant to such exercise will be sold to the public instead of being issued to PBF Energy. Accordingly, the exercise of the underwriters’ option will not affect the total number of units outstanding. If the underwriters’ option is exercised in full, PBF Energy will own 0.5% of the common units and the public will own 99.5% of the common units. |

9

The Offering

Common units offered to the public | 13,750,000 common units, or 15,812,500 common units if the underwriters exercise their option to purchase additional common units in full. |

Units outstanding after this offering | 15,886,553 common units and 15,886,553 subordinated units, for a total of 31,773,106 limited partner units, regardless of whether the underwriters exercise their option to purchase any additional common units, representing 100% of the limited partner interests in us. If and to the extent the underwriters exercise their option to purchase up to 2,062,500 additional common units, the number of common units purchased by the underwriters pursuant to any exercise will be sold to the public, and any remaining common units not purchased by the underwriters pursuant to any exercise of the option will be issued to PBF Energy (through its ownership in PBF LLC) at the expiration of the option period for no additional consideration. Accordingly, the exercise of the underwriters’ option will not affect the total number of common units outstanding or the amount of cash needed to pay the minimum quarterly distribution on all units. In addition, our general partner will own a noneconomic general partner interest in us and PBF Energy (through its ownership in PBF LLC) will own all of our incentive distribution rights. |

Use of proceeds | We expect the net proceeds from this offering, after deducting underwriting discounts, the structuring fee and estimated offering expenses, to be approximately $252.8 million. We intend to use the net proceeds of this offering: |

| • | to distribute approximately $30.0 million to PBF LLC to reimburse it for certain capital expenditures incurred prior to the closing of this offering with respect to the contributed assets; |

| • | to pay debt issuance costs of approximately $2.0 million related to our new revolving credit facility and term loan facility; |

| • | to purchase $215.8 million in U.S. Treasury or other investment grade securities which will be used to fund anticipated capital expenditures; and |

| • | to retain approximately $5.0 million for general partnership purposes. |

| We will also borrow $215.8 million (or $254.5 million if the underwriters exercise in full their option to purchase additional common units) under our term loan and distribute the proceeds of such borrowings to PBF LLC. |

| At the closing of this offering, we will also enter into a new $275.0 million revolving credit facility which will remain undrawn at the closing. |

If and to the extent the underwriters exercise their option to purchase up to 2,062,500 additional common units, the number of common units purchased by the underwriters pursuant to such exercise will be issued to the public and the remaining common units, if any, will be |

12

issued to PBF Energy (through its ownership in PBF LLC) at the expiration of the option period. Any such units issued to PBF Energy will be issued for no additional consideration. Accordingly, the exercise of the underwriters’ option will not affect the total number of common units outstanding or the amount of cash needed to pay the minimum quarterly distribution on all units. Please read “Underwriting.” If the underwriters exercise their option to purchase additional common units in full, the additional net proceeds would be approximately $38.7 million. The net proceeds received in connection with any exercise of such option will be used to purchase a corresponding amount of additional U.S. Treasury or other investment grade securities, which will be used to fund anticipated capital expenditures. In addition, we will borrow under our term loan an amount equal to the net proceeds received upon any exercise of the underwriters’ option to purchase additional common units and use the proceeds to make a distribution to PBF LLC. See “Use of Proceeds.” |

Cash distributions | We intend to pay a minimum quarterly distribution of $0.300 per unit ($1.20 per unit on an annualized basis) to the extent we generate sufficient earnings. However, since it will be our policy to set our distributions based on the level of success of our operations, the actual amount of cash we will distribute on our common and subordinated units will depend principally on the amount of earnings we can generate from our operations. Our ability to pay the minimum quarterly distribution is subject to various restrictions and other factors described in more detail under the caption “Our Cash Distribution Policy and Restrictions on Distributions.” |

| We will adjust the amount of our distribution for the period from the closing of this offering through June 30, 2014, based on the actual length of that period. |

| Our partnership agreement generally provides that we will make our distribution, if any, each quarter in the following manner: |

| • | first, 100% to the holders of common units, until each common unit has received the minimum quarterly distribution of $0.300 plus any arrearages from prior quarters; |

| • | second, 100% to the holders of subordinated units, until each subordinated unit has received the minimum quarterly distribution of $0.300; and |

| • | third, 100% to all unitholders, pro rata, until each unit has received a distribution of $0.345. |

If cash distributions to our unitholders exceed $0.345 per unit in any quarter, the holders of our incentive distribution rights will receive increasing percentages, up to 50.0%, of the cash we distribute in excess of that amount. We refer to these distributions as “incentive distributions.” In certain circumstances, PBF Energy, as the initial holder of our incentive distribution rights, will have the right to reset |

13

the minimum quarterly distribution and the target distribution levels at which the incentive distributions receive increasing percentages of the cash we distribute to higher levels based on our cash distributions at the time of the exercise of this reset election. Please read “Provisions of Our Partnership Agreement Relating to Cash Distributions.” |

| Prior to making distributions, we will pay PBF Energy an annual fee of initially $2.3 million for the provision of centralized administrative services and reimburse our general partner and its affiliates, including PBF Energy, for direct or allocated costs and expenses incurred on our behalf pursuant to the omnibus agreement. In addition, prior to making distributions, we will pay an annual fee of $0.5 million to PBF Energy for the provision of certain utilities and other infrastructure-related services with respect to our business pursuant to the operation and management services and secondment agreement. Please read “Certain Relationships and Related Party Transactions—Agreements Governing the Transactions.” |

| Pro forma cash available for distribution during the year ended December 31, 2013 was approximately $33.5 million. The amount of cash we will need to pay the minimum quarterly distribution for four quarters on our common units and subordinated units to be outstanding immediately after this offering will be approximately $38.1 million (or an average of approximately $9.5 million per quarter). As a result, we would not have had sufficient cash available for distribution to pay the full minimum quarterly distribution of $0.300 per unit per quarter ($1.20 per unit on an annualized basis) on any of our common units or subordinated units for the year ended December 31, 2013. Please read “Our Cash Distribution Policy and Restrictions on Distributions—Unaudited Pro Forma Cash Available for Distribution for the Year Ended December 31, 2013.” |

| We believe that, based on the financial forecasts and related assumptions included under the caption “Our Cash Distribution Policy and Restrictions on Distributions—Estimated Cash Available for Distribution for the twelve months ending June 30, 2015,” we will have sufficient cash available for distribution to make cash distributions for the twelve months ending June 30, 2015, at the minimum quarterly distribution rate of $0.300 per unit per quarter ($1.20 per unit on an annualized basis) on all common units and subordinated units outstanding immediately after closing of this offering. However, our actual results of operations, cash flows and financial condition during the forecast period may vary from the forecast. |

Subordinated units | PBF Energy (through its ownership in PBF LLC) will initially own all of our subordinated units. The principal difference between our common units and subordinated units is that in any quarter during the subordination period, holders of the subordinated units are not |

14

entitled to receive any distribution of available cash until the common units have received the minimum quarterly distribution plus any arrearages in the payment of the minimum quarterly distribution from prior quarters. If we do not pay distributions on our subordinated units, our subordinated units will not accrue arrearages for those unpaid distributions. |

Conversion of subordinated units | The subordination period will end on the first business day after we have earned and paid at least (i) $1.20 (the minimum quarterly distribution on an annualized basis) on each outstanding common and subordinated unit, for each of three consecutive, non-overlapping four-quarter periods ending on or after March 31, 2017, or (ii) $1.80 (150% of the annualized minimum quarterly distribution) on each outstanding common unit and subordinated unit, in addition to any distribution made in respect of the incentive distribution rights, for any four-consecutive-quarter period ending on or after March 31, 2015, in each case provided that there are no arrearages on our common units at that time. In addition, the subordination period will end upon the removal of our general partner other than for cause if the units held by our general partner and its affiliates are not voted in favor of such removal. |

| When the subordination period ends, all subordinated units will convert into common units on a one-for-one basis, and all common units thereafter will no longer be entitled to arrearages. Please read “Provisions of Our Partnership Agreement Related to Cash Distributions—Subordination Period.” |

Issuance of additional units | Our partnership agreement authorizes us to issue an unlimited number of additional units without the approval of our unitholders. Please read “Units Eligible for Future Sale” and “The Partnership Agreement—Issuance of Additional Interests.” |

Limited voting rights | Our general partner will manage and operate us. Unlike the holders of common stock in a corporation, holders of our common units will have only limited voting rights on matters affecting our business. Holders of our common units will not have the right to elect our general partner or its directors on an annual or other continuing basis. Our general partner may not be removed except by a vote of the holders of at least 66 2/3% of our outstanding common and subordinated units, including any common and subordinated units owned by our general partner and its affiliates, voting together as a single class. Upon closing of this offering, PBF Energy will own an aggregate of approximately 56.7% of our common and subordinated units (or 50.2% of our common and subordinated units if the underwriters exercise their option to purchase additional common units in full). This will give PBF Energy the ability to prevent the involuntary removal of our general partner. Please read “The Partnership Agreement—Voting Rights.” |

15

Limited call right | If at any time PBF Energy and its controlled affiliates own more than 80% of the outstanding common units, PBF Energy will have the right, but not the obligation, to purchase all, but not less than all, of the remaining common units at a price not less than the then-current market price of the common units, as calculated in accordance with our partnership agreement. |

Estimated ratio of taxable income to distributions | We estimate that if you own the common units you purchase in this offering through the record date for distributions for the period ending December 31, 2016, you will be allocated, on a cumulative basis, an amount of U.S. federal taxable income for that period that will be approximately 20.0% of the cash distributed to you with respect to that period. For example, if you receive an annual distribution of $1.20 per common unit, we estimate that your average allocable taxable income per year will be no more than approximately $0.24 per common unit. Thereafter, the ratio of allocable taxable income to cash distributions to you could substantially increase. Please read “Material U.S. Federal Income Tax Consequences—Tax Consequences of Unit Ownership—Ratio of Taxable Income to Distributions.” |

Material U.S. federal income tax consequences | For a discussion of other material U.S. federal income tax consequences that may be relevant to prospective unitholders who are individuals who are citizens or residents of the United States, please read “Material U.S. Federal Income Tax Consequences.” |

Directed unit program | The underwriters have reserved for sale at the initial public offering price up to 5% of the common units being offered by this prospectus for sale to the directors and executive officers of our general partner and certain other employees and consultants of our sponsor and certain other participants who have expressed an interest in purchasing common units in the offering. We do not know if these persons will choose to purchase all or any portion of these reserved common units, but any purchases they do make will reduce the number of common units available to the general public. Please read “Underwriting—Direct Sales to Insiders and Directed Unit Program.” |

New York Stock Exchange listing | We have been approved to list our common units on the New York Stock Exchange under the symbol “PBFX,” subject to official notice of issuance. |

Thomas D. O’Malley, the Chairman of the board of directors of our general partner, and certain of his affiliates and family members have indicated an interest in purchasing up to an aggregate of $10 million of common units in this offering, or 500,000 common units at an assumed initial public offering price of $20.00 per common unit (the midpoint of the price range set forth on the cover page of this prospectus). However, because indications of interest are not binding agreements or commitments to purchase, the underwriters may determine to sell more, less or no common units in this offering to any of these persons, and any of these persons may determine to purchase more, less or no common units in this offering.

16

Summary Historical and Pro Forma Financial and Operating Data

The following table shows summary historical combined financial and operating data of PBF MLP Predecessor, our predecessor for accounting purposes, and summary pro forma combined financial data of PBF Logistics LP for the periods and as of the dates indicated. Our summary historical combined financial data as of December 31, 2013 and for the year ended December 31, 2013 are derived from the audited combined financial statements of our predecessor appearing elsewhere in this prospectus. The following table should be read together with, and is qualified in its entirety by reference to, the historical and unaudited pro forma combined financial statements and the accompanying notes included elsewhere in this prospectus. The table should also be read together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

PBF MLP Predecessor consists of the assets, liabilities and results of operations of the Delaware City Rail Terminal assets, operated and held by Delaware City Terminaling, a wholly owned indirect subsidiary of PBF Holding, which such entity is to be conveyed to us in connection with this offering, and the Toledo Truck Terminal. The historical financial data include the assets, liabilities and results of operations of the contributed assets.

The summary pro forma combined financial data presented in the following table for the year ended December 31, 2013 are derived from the unaudited pro forma combined financial statements of PBF Logistics LP included elsewhere in this prospectus. The pro forma balance sheet assumes that the offering and the related formation transactions occurred as of December 31, 2013 and the pro forma statement of operations for the year ended December 31, 2013 assumes that the offering and the related transactions occurred as of January 1, 2013. These transactions include, and the pro forma financial data give effect to, the following:

| • | PBF Holding’s contribution of all of our initial assets and operations, including Delaware City Terminaling and the Toledo Truck Terminal to us; |

| • | our entry into a new $275.0 million revolving credit facility, which will remain undrawn at the closing of this offering; |

| • | $215.8 million of borrowings under our term loan facility; |

| • | our entry into long-term commercial agreements with PBF Energy and recognition of incremental revenues under those agreements as discussed in “Certain Relationships and Related Party Transactions—Commercial Agreements with PBF Energy”; |

| • | our entry into an omnibus agreement with PBF Energy; |

| • | our entry into an operation and management services and secondment agreement with PBF Energy; |

| • | the consummation of this offering and our issuance of common units to the public and common units, subordinated units and the incentive distribution rights to PBF LLC; and |

| • | the application of the net proceeds of this offering, together with the proceeds from borrowings under our new term loan, as described in “Use of Proceeds.” |

The pro forma combined financial data do not give effect to the estimated $4.0 million in incremental annual general and administrative expense we expect to incur as a result of being a separate publicly traded partnership.

17

The following table presents the Non-GAAP financial measure of EBITDA, which we use in our business as a measure of performance and liquidity. For a definition of EBITDA and a reconciliation to our most directly comparable financial measures calculated and presented in accordance with GAAP, please read “—Non-GAAP Financial Measure.”

| PBF MLP Predecessor Historical | PBF Logistics LP Pro Forma | |||||||

| Year Ended December 31, 2013 | Year Ended December 31, 2013 | |||||||

| (unaudited) | ||||||||

(in thousands, except per unit data and operating information) | ||||||||

Statement of Operations Data: | ||||||||

Net revenues | $ | — | $ | 50,625 | ||||

Cost of goods sold | — | — | ||||||

Operating expenses | 6,024 | 6,408 | ||||||

General and administrative expenses | 1,834 | 3,200 | ||||||

Depreciation and amortization | 1,032 | 1,032 | ||||||

|

|

|

| |||||

Operating income (loss) | (8,890 | ) | 39,985 | |||||

Interest expense, net | — | (1,987 | ) | |||||

|

|

|

| |||||

Net income (loss) | $ | (8,890 | ) | $ | 37,998 | |||

|

|

|

| |||||

Common unitholders interest in net income | ||||||||

Subordinated unitholders interest in net income | ||||||||

Pro forma net income per common unit | ||||||||

Pro forma net income per subordinated unit | ||||||||

Balance Sheet Data (at period end): | ||||||||

Cash and marketable securities | $ | — | | $ | 220,788 | |||

Property, plant and equipment, net | 29,996 | 29,996 | ||||||

Total assets | 29,996 | 252,809 | ||||||

Total debt, including current maturities | — | 215,788 | ||||||

Total liabilities | 499 | 215,788 | ||||||

Total net investment/partners’ equity | 29,497 | 37,021 | ||||||

Cash Flow Data: | ||||||||

Cash flows (used in) provided by operating activities | $ | (7,858 | ) | |||||

Cash flows used in investing activities | (11,654 | ) | ||||||

Cash flows (used in) provided by financing activities | 19,512 | |||||||

Other Financial Data: | ||||||||

EBITDA (1) | $ | (7,858 | ) | $ | 41,017 | |||

Capital expenditures: | ||||||||

Maintenance | $ | — | ||||||

Expansion | 7,471 | |||||||

|

| |||||||

Total | $ | 7,471 | ||||||

|

| |||||||

Operating Information: | ||||||||

Delaware City Rail Terminal throughput (kbpd) | 69.7 | |||||||

Toledo Truck Terminal throughput (kbpd) | 5.4 | |||||||

| (1) | For a definition of EBITDA and reconciliations to its most directly comparable GAAP financial measures, please read “—Non-GAAP Financial Measure” below. |

18

The following table presents a reconciliation of EBITDA to net income (loss) and net cash provided by (used in) operating activities, the most directly comparable GAAP financial measures, on a historical basis and pro forma basis, as applicable, for each of the periods indicated.

| PBF MLP Predecessor Historical | PBF Logistics LP Pro Forma | |||||||

| Year Ended December 31, 2013 | Year Ended December 31, 2013 | |||||||

| (unaudited) | ||||||||

(in thousands) | ||||||||

Reconciliation of EBITDA to net income (loss): | ||||||||

Net income (loss) | $ | (8,890 | ) | $ | 37,998 | |||

Add: | ||||||||

Depreciation and amortization | 1,032 | 1,032 | ||||||

Interest expense, net | — | 1,987 | ||||||

|

|

|

| |||||

EBITDA | $ | (7,858 | ) | $ | 41,017 | |||

|

|

|

| |||||

Reconciliation of EBITDA to net cash provided by operating activities: | ||||||||

Net cash provided by (used in) operating activities | $ | (7,858 | ) | |||||

|

| |||||||

EBITDA | $ | (7,858 | ) | |||||

|

| |||||||

20

| • | our sponsor’s obligations under its tax receivable agreement for certain tax benefits it may claim, and in particular that our sponsor’s assumptions regarding such payments are subject to change due to various factors outside of its control; |

| • | our sponsor’s expectations and timing with respect to its acquisition and capital improvements activity; |

| • | disruptions due to equipment interruption or failure at our sponsor’s facilities, or at third-party facilities on which our sponsor’s business is dependent; |

| • | the price volatility of crude oil, other feedstocks, blendstocks, refined products and fuel and utility services in commodity prices and demand for our sponsor’s refined products, and the availability and costs of crude oil and other refinery feedstocks; |

| • | fluctuations in crude oil differentials and any narrowing of these differentials; |

| • | concentration of our sponsor’s earnings in operations of its Toledo, Ohio refinery; |

| • | the impact of disruptions to crude oil or feedstock supply to any of our sponsor’s refineries, including disruptions due to problems with third-party logistics infrastructure or operations, including pipeline and rail transportation; |

| • | the impact of current and future laws, rulings and governmental regulations, including any change by the federal government in the restrictions on exporting U.S. crude oil; |

| • | the effects of continued economic turmoil in the global financial system on our sponsor’s business and the business of its suppliers, customers, business partners and lenders; |

| • | changes in the cost or availability of third-party logistics services; |

| • | state and federal environmental, economic, health and safety, energy and other policies and regulations, including any changes in those policies and regulations, and adverse impacts resulting from actions taken by environmental interest groups; |

| • | terrorist attacks, cyber-attacks, political instability, military strikes, sustained military campaigns, changes in foreign policy, threats of war, or actual war may negatively affect our and our sponsor’s operations, financial condition, results of operations, cash flows, and our ability to make distributions to our unitholders; |

| • | environmental incidents and violations and related remediation costs, fines and other liabilities; and |

| • | changes in crude oil and refined product inventory levels and carrying costs. |

We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our general partner and its affiliates, to enable us to pay the minimum quarterly distribution to holders of our common and subordinated units.

In order to pay the minimum quarterly distribution of $0.300 per unit, or $1.20 per unit on an annualized basis, we will require available cash of approximately $9.5 million per quarter, or $38.1 million per year, based on the number of common and subordinated units to be outstanding immediately after closing of this offering. We may not have sufficient available cash from operating surplus each quarter to enable us to pay the minimum quarterly distribution. The amount of cash we can distribute on our units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on, among other things:

| • | the volume of crude oil we throughput; |

| • | our entitlement to payments associated with minimum volume commitments; |

| • | the fees we charge for the volumes we throughput; |

22

| • | the level of our operating, maintenance and general and administrative costs; and |

| • | prevailing economic conditions. |

In addition, the actual amount of cash we will have available for distribution will depend on other factors, some of which are beyond our control, including:

| • | the level and timing of capital expenditures we make; |

| • | the amount of our operating expenses and general and administrative expenses, including reimbursements to our general partner and its affiliates, including our sponsor, in respect of those expenses and payment of the administrative fees under the omnibus agreement and the operation and management services and secondment agreement for services provided to us by our general partner and its affiliates, including our sponsor; |

| • | the cost of acquisitions, if any; |

| • | our debt service requirements and other liabilities; |

| • | fluctuations in our working capital needs; |

| • | our ability to borrow funds and access capital markets; |

| • | restrictions contained in our revolving credit agreement and term loan facility and other debt service requirements; |

| • | the amount of cash reserves established by our general partner; and |

| • | other business risks affecting our cash levels. |

For a description of additional restrictions and factors that may affect our ability to make cash distributions, please read “Our Cash Distribution Policy and Restrictions on Distributions.”

We have no operating history and, accordingly, you will have a limited basis upon which to evaluate our ability to achieve our business objectives.

We have no operating results to date. Construction of our Delaware City Rail Terminal was completed and the terminal began operating in February 2013. At our Toledo Truck Terminal, one lease automatic custody transfer, or LACT, unit commenced operations in December 2012 and two additional units were made operational in May 2013. A fourth LACT unit, which has been owned and operated by our sponsor’s vendor in connection with a crude oil supply agreement, was purchased in July 2013. Since our initial assets have limited or no operating history, you will have a limited basis upon which to evaluate our ability to achieve our business objectives, which are to maintain stable cash flows and grow the quarterly distributions paid to our unitholders.

On a pro forma basis, we would not have had sufficient cash available for distribution to pay the full minimum quarterly distribution on any of our common units or subordinated units for the year ended December 31, 2013.

Pro forma cash available for distribution during the year ended December 31, 2013 was approximately $33.5 million. We would not have had sufficient cash available for distribution to pay the full minimum quarterly distribution of $0.300 per unit per quarter ($1.20 per unit on an annualized basis) on any of our common units or subordinated units for the year ended December 31, 2013. Please read “Our Cash Distribution Policy and Restrictions on Distributions—Unaudited Pro Forma Cash Available for Distribution for the Year Ended December 31, 2013.”

23

operations of more geographically diversified competitors and any unforeseen events or circumstances that affect the area could also materially adversely affect our revenues and profitability. These factors include, among other things, changes in the economy, damages to infrastructure, weather conditions, demographics and population.

Restrictions in our new revolving credit and term loan facilities could adversely affect our business, financial condition, results of operations and ability to make quarterly cash distributions to our unitholders and the value of our units.

We expect to enter into new revolving credit and term loan facilities in connection with the closing of this offering. We will be dependent upon the earnings and cash flow generated by our operations in order to meet our debt service obligations and to allow us to make cash distributions to our unitholders. The operating and financial restrictions and covenants in our new revolving credit and term loan facilities and any future financing agreements could restrict our ability to finance future operations or capital needs or to expand or pursue our business activities, which may, in turn, limit our ability to make cash distributions to our unitholders. Our new credit facility will limit our ability to, among other things:

| • | incur or guarantee additional debt; |

| • | incur certain liens on assets; |

| • | dispose of assets; |

| • | make certain cash distributions or redeem or repurchase units; |

| • | change the nature of our business; |

| • | engage in certain mergers or acquisitions; |

| • | make certain investments and acquisitions; and |

| • | enter into non arms-length transactions with affiliates. |

Our new credit facility will contain covenants requiring us to maintain certain financial ratios. The provisions of our new credit facility may affect our ability to obtain future financing and pursue attractive business opportunities and our flexibility in planning for, and reacting to, changes in business conditions. In addition, a failure to comply with the provisions of our new credit facility could result in a default or an event of default that could enable our lenders to declare the outstanding principal of that debt, together with accrued and unpaid interest and other outstanding amounts, to be immediately due and payable. Such event of default would also permit our lenders to foreclose on our assets serving as collateral for our obligations under the credit facility. If the payment of our debt is accelerated, our assets may be insufficient to repay such debt in full, and our unitholders could experience a partial or total loss of their investment. Our revolving credit facility will also have cross-default provisions that apply to our term loan facility and to any other material indebtedness we may have. Our term loan facility will have cross default provisions that apply to our revolving credit facility and to any other material indebtedness we may have. Please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Capital Resources and Liquidity—New Credit Facilities.”

Our future debt levels may limit our flexibility to obtain financing and to pursue other business opportunities.

After giving effect to this offering and the related transactions, we estimate that we would have had approximately $215.8 million of debt outstanding on a pro forma basis as of December 31, 2013. Following the closing of this offering, we will have the ability to incur additional debt, including under our new revolving credit facility that we will enter into in connection with this offering. Our level of debt could have important consequences to us, including the following:

| • | making it more difficult for us to satisfy our obligations with respect to our credit facilities; |

32

| • | Our general partner determines which costs incurred by it are reimbursable by us. |

| • | Our general partner may cause us to borrow funds in order to permit the payment of cash distributions, even if the purpose or effect of the borrowing is to make a distribution on the subordinated units, to make incentive distributions or to accelerate the expiration of the subordination period. |

| • | Our partnership agreement permits us to classify up to $20.0 million as operating surplus, even if it is generated from asset sales, non-working capital borrowings or other sources that would otherwise constitute capital surplus. This cash may be used to fund distributions to PBF LLC as the holder of all of our subordinated units and the incentive distribution rights. |

| • | Our partnership agreement does not restrict our general partner from causing us to pay it or its affiliates for any services rendered to us or entering into additional contractual arrangements with any of these entities on our behalf. |

| • | Our general partner intends to limit its liability regarding our contractual and other obligations. |

| • | PBF Energy and its controlled affiliates may exercise their right to call and purchase all of the common units not owned by them if they own more than 80% of the common units. |

| • | Our general partner controls the enforcement of the obligations that it and its affiliates owe to us, including our sponsor’s obligations under the omnibus agreement and its commercial agreements with us. |

| • | Our general partner decides whether to retain separate counsel, accountants or others to perform services for us. |

| • | Our general partner may elect to cause us to issue common units to PBF Energy in connection with a resetting of the target distribution levels related to our incentive distribution rights without the approval of the conflicts committee of the board of directors of our general partner or our unitholders. This election may result in lower distributions to our common unitholders in certain situations. |

Please read “Conflicts of Interest and Fiduciary Duties.”

PBF Energy may compete with us.

PBF Energy may compete with us. Under the omnibus agreement, PBF Energy and its affiliates will agree not to engage in, whether by acquisition or otherwise, the business of owning or operating any crude oil or refined products pipelines, terminals or storage facilities in the United States that are not within, directly connected to, substantially dedicated to, or otherwise an integral part of, any refinery owned, acquired or constructed by our sponsor. This restriction, however, does not apply to:

| • | any assets owned by our sponsor at the closing of this offering (including replacements or expansions of those assets); |

| • | any assets acquired or constructed by our sponsor that are within, substantially dedicated to, or an integral part of any refinery owned, acquired or constructed by our sponsor; |

| • | any asset or business that our sponsor acquires or constructs that has a fair market value of less than $25 million; |

| • | any asset or business that our sponsor acquires or constructs that has a fair market value of $25 million or more; |

| • | any logistics asset that our sponsor acquires or constructs that has a fair market value of $25 million or more but comprises less than half of the fair market value (as determined in good faith by our sponsor) |

43

There is no existing market for our common units, and a trading market that will provide you with adequate liquidity may not develop. Following this offering, the market price of our common units may fluctuate significantly, and you could lose all or part of your investment.

Prior to this offering, there has been no public market for our common units. After this offering, there will be only 13,750,000 publicly traded common units, assuming no exercise of the underwriters’ option to purchase additional common units. In addition, PBF Energy will own 2,136,553 common units (74,053 common units if the underwriters exercise such option in full) and 15,886,553 subordinated units, representing an aggregate of approximately 56.7% limited partner interest in us (50.2% if the underwriters exercise such option in full). We do not know the extent to which investor interest will lead to the development of a trading market or how liquid that market might be. You may not be able to resell your common units at or above the initial public offering price. Additionally, the lack of liquidity may result in wide bid-ask spreads, contribute to significant fluctuations in the market price of the common units and limit the number of investors who are able to buy the common units.

The initial public offering price for the common units will be determined by negotiations between us and the representatives of the underwriters and may not be indicative of the market price of the common units that will prevail in the trading market. The market price of our common units may decline below the initial public offering price. The market price of our common units may also be influenced by many factors, some of which are beyond our control, including:

| • | the level of our quarterly distributions; |

| • | our quarterly or annual earnings or those of other companies in our industry; |

| • | announcements by us or our competitors of significant contracts or acquisitions; |

| • | changes in accounting standards, policies, guidance, interpretations or principles; |

| • | general economic conditions, including interest rates and governmental policies impacting interest rates; |

| • | the failure of securities analysts to cover our common units after this offering or changes in financial estimates by analysts; |

| • | future sales of our common units; and |

| • | other factors described in these “Risk Factors.” |

You will experience immediate and substantial dilution in net tangible book value of $18.83 per common unit.

The estimated initial public offering price of $20.00 per common unit (the mid-point of the price range set forth on the cover of this prospectus) exceeds our pro forma net tangible book value of $1.17 per unit. Based on the estimated initial public offering price of $20.00 per common unit, you will incur immediate and substantial dilution of $18.83 per common unit. This dilution results primarily because the assets contributed by our sponsor are recorded in accordance with GAAP at their historical cost, and not their fair value. Please read “Dilution.”

Our partnership agreement replaces our general partner’s fiduciary duties to holders of our common units with contractual standards governing its duties.

Our partnership agreement contains provisions that eliminate the fiduciary standards to which our general partner would otherwise be held by state fiduciary duty law and replace those duties with several different contractual standards. For example, our partnership agreement permits our general partner to make a number of decisions in its individual capacity, as opposed to in its capacity as our general partner, free of any duties to us and our unitholders other than the implied contractual covenant of good faith and fair dealing, which means that a court will enforce the reasonable expectations of the partners where the language in the partnership agreement does not provide for a clear course of action. This provision entitles our general partner to consider only the

45

PBF Energy will indirectly own 56.7% of our outstanding common and subordinated units. Also, if our general partner is removed without cause during the subordination period and units held by our general partner and its affiliates are not voted in favor of that removal, all remaining subordinated units will automatically convert into common units and any existing arrearages on our common units will be extinguished. A removal of our general partner under these circumstances would adversely affect our common units by prematurely eliminating their distribution and liquidation preference over our subordinated units, which would otherwise have continued until we had met certain distribution and performance tests. Cause is narrowly defined to mean that a court of competent jurisdiction has entered a final, non-appealable judgment finding our general partner liable to us or any limited partner for actual fraud or willful misconduct in its capacity as our general partner. Cause does not include most cases of charges of poor management of the business, so the removal of our general partner because of unitholder dissatisfaction with the performance of our general partner in managing our partnership will most likely result in the termination of the subordination period and conversion of all subordinated units to common units.

Our partnership agreement restricts the voting rights of unitholders owning 20% or more of our common units.

Unitholders’ voting rights are further restricted by a provision of our partnership agreement providing that any units held by a person that owns 20% or more of any class of units then outstanding, other than our general partner, its affiliates, their transferees and persons who acquired such units with the prior approval of the board of directors of our general partner, cannot vote on any matter.

Our general partner interest or the control of our general partner may be transferred to a third-party without unitholder consent.

Our general partner may transfer its general partner interest to a third-party in a merger or in a sale of all or substantially all of any assets it may own without the consent of the unitholders. Furthermore, there is no restriction in the partnership agreement on the ability of PBF Energy to transfer its membership interest in our general partner to a third-party. The new members of our general partner would then be in a position to replace the board of directors and officers of our general partner with their own choices and to control the decisions taken by the board of directors and officers.

The incentive distribution rights held by PBF Energy may be transferred to a third-party without unitholder consent.

PBF Energy may transfer its incentive distribution rights to a third-party at any time without the consent of our unitholders. If PBF Energy transfers its incentive distribution rights to a third-party but retains its ownership interest in our general partner, our general partner may not have the same incentive to grow our partnership and increase quarterly distributions to unitholders over time as it would if PBF Energy had retained ownership of the incentive distribution rights. For example, a transfer of incentive distribution rights by PBF Energy could reduce the likelihood of PBF Energy, accepting offers made by us relating to assets owned by it or its subsidiaries, as PBF Energy would have less of an economic incentive to grow our business, which in turn would impact our ability to grow our asset base.

We may issue additional units without unitholder approval, which would dilute unitholder interests.

Our partnership agreement does not limit the number of additional limited partner interests, including limited partner interests that rank senior to the common units that we may issue at any time without the approval of our unitholders. The issuance by us of additional common units or other equity securities of equal or senior rank will have the following effects:

| • | our existing unitholders’ proportionate ownership interest in us will decrease; |

| • | the amount of cash available for distribution on each unit may decrease; |

48

| • | because a lower percentage of total outstanding units will be subordinated units, the risk that a shortfall in the payment of the minimum quarterly distribution will be borne by our common unitholders will increase; |

| • | because the amount payable to holders of incentive distribution rights is based on a percentage of the total cash available for distribution, the distributions to holders of incentive distribution rights will increase even if the per unit distribution on common units remains the same; |

| • | the ratio of taxable income to distributions may increase; |

| • | the relative voting strength of each previously outstanding unit may be diminished; and |

| • | the market price of the common units may decline. |

PBF Energy may sell units in the public or private markets, and such sales could have an adverse impact on the trading price of the common units.

After the sale of the common units offered by this prospectus, assuming that the underwriters do not exercise their option to purchase additional common units, PBF Energy will hold 2,136,553 common units and 15,886,553 subordinated units. All of the subordinated units will convert into common units at the end of the subordination period and may convert earlier under certain circumstances. In addition, we have agreed to provide PBF Energy with certain registration rights. The sale of these units in the public or private markets could have an adverse impact on the price of the common units or on any trading market that may develop.

Our general partner intends to limit its liability regarding our obligations.

Our general partner intends to limit its liability under contractual arrangements so that the counterparties to such arrangements have recourse only against our assets and not against our general partner or its assets. Our general partner may therefore cause us to incur indebtedness or other obligations that are nonrecourse to our general partner. Our partnership agreement permits our general partner to limit its liability, even if we could have obtained more favorable terms without the limitation on liability. In addition, we are obligated to reimburse or indemnify our general partner to the extent that it incurs obligations on our behalf. Any such reimbursement or indemnification payments would reduce the amount of cash otherwise available for distribution to our unitholders.

PBF Energy has a limited call right that may require you to sell your units at an undesirable time or price.