|

Exhibit 99.1

|

APX Group Holdings, Inc.

JP Morgan Global High Yield & Leveraged Finance Conference

February 27, 2017

2

Presenters

Mark Davies

Chief Financial Officer

Dale Gerard

SVP Finance and Treasurer

3

Preliminary Statement

This presentation includes forward-looking statements as defined by the Private Securities Litigation Reform Act of 1995 regarding, among other things, statements with respect to certain preliminary unaudited financial

results for the Company’s quarter and full year ended December 31, 2016, which are subject to finalization and contingencies associated with the Company’s quarterly and annual financial and accounting procedures.

These statements are based on the beliefs and assumptions of management. Although the Company believes that its estimates, plans, intentions and expectations reflected in or suggested by these forward-looking

statements are reasonable, the Company cannot assure you that it will achieve or realize these estimates, plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and

assumptions. Generally, statements that are not historical facts, including statements concerning the Company’s possible or assumed future actions, business strategies, events or results of operations, are forwardlooking

statements. These statements may be preceded by, followed by or include the words “believes,” “estimates,” “expects,” “projects,” “forecasts,” “may,” “will,” “should,” “seeks,” “plans,” “scheduled,” “anticipates” or

“intends” or similar expressions.

Forward-looking statements are not guarantees of performance. You should not put undue reliance on these statements which speak only as of the date hereof. You should understand that the following important

factors, among others, could affect the Company’s future results and could cause those results or other outcomes to differ materially from those expressed or implied in the Company’s forward-looking statements: 1)

risks of the smart home and security industry, including risks of and publicity surrounding the sales, subscriber origination and retention process; 2) the highly competitive nature of the smart home and security industry

and product introductions and promotional activity by the Company’s competitors; 3) litigation, complaints or adverse publicity; 4) the impact of changes in consumer spending patterns, consumer preferences, local,

regional, and national economic conditions, crime, weather, demographic trends and employee availability; 5) adverse publicity and product liability claims; 6) increases and/or decreases in utility and other energy

costs, increased costs related to utility or governmental requirements; 7) cost increases or shortages in smart home and security technology products or components; and the impact to the Company’s business results

of operations, financial conditions, regulatory compliance and customer experience of the Vivint Flex Pay plan In addition, the origination and retention of new subscribers will depend on various factors, including, but

not limited to, market availability, subscriber interest, the availability of suitable components, the negotiation of acceptable contract terms with subscribers, local permitting, licensing and regulatory compliance, and the

Company’s ability to manage anticipated expansion and to hire, train and retain personnel, the financial viability of subscribers and general economic conditions.

These and other factors that could cause actual results to differ from those implied by the forward-looking statements in this presentation are more fully described in the “Risk Factors” section in the Company’s annual

report on form10-K for the year ended December 31, 2015, filed with the Securities Exchange Commission (SEC), as such factors may be updated from time to time in the Company’s periodic filings with the SEC,

which are available on the SEC’s website at www.sec.gov. The risks described in “Risk Factors” are not exhaustive. New risk factors emerge from time to time and it is not possible for us to predict all such risk factors,

nor can we assess the impact of all such risk factors on the Company’s business or the extent to which any factor or combination of factors may cause actual results to differ materially from those contained in any

forward-looking statements. All forward-looking statements attributable to the Company or persons acting on its behalf are expressly qualified in their entirety by the foregoing cautionary statements. The Company

undertakes no obligations to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

This presentation includes Adjusted EBITDA, which is a supplemental measure that is not required by, or presented in accordance with, accounting principles generally accepted in the United States (“GAAP”). Adjusted

EBITDA is not a measurement of our financial performance under GAAP and should not be considered as an alternative to net income (loss) or any other measure derived in accordance with GAAP or as an alternative

to cash flows from operating activities as a measure of our liquidity. We believe that Adjusted EBITDA provides useful information about flexibility under our covenants to investors, lenders, financial analysts and rating

agencies since these groups have historically used EBITDA-related measures in our industry, along with other measures, to estimate the value of a company, to make informed investment decisions, and to evaluate a

company’s ability to meet its debt service requirements. Adjusted EBITDA eliminates the effect ofnon-cash depreciation of tangible assets and amortization of intangible assets, much of which results from acquisitions

accounted for under the purchase method of accounting. Adjusted EBITDA also eliminates the effects of interest rates and changes in capitalization which management believes may not necessarily be indicative of a

company’s underlying operating performance. Adjusted EBITDA is also used by us to measure covenant compliance under the indenture governing our senior secured notes, the indenture governing our senior

unsecured notes and the credit agreement governing our revolving credit facility. We caution investors that amounts presented in accordance with our definition of Adjusted EBITDA may not be comparable to similar

measures disclosed by other issuers, because not all issuers and analysts calculate Adjusted EBITDA in the same manner. See the Appendix of this presentation for a reconciliation of Adjusted EBITDA to net loss for

the Company, which we believe is the most closely comparable financial measure calculated in accordance with GAAP. Adjusted EBITDA should be considered in addition to and not as a substitute for, or superior to,

financial measures presented in accordance with GAAP.

4

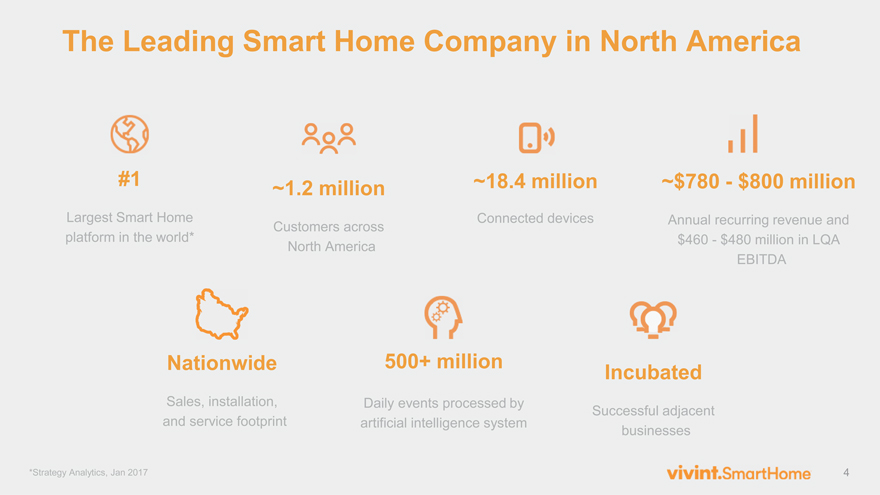

The Leading Smart Home Company in North America

#1

Largest Smart Home

platform in the world*

~1.2 million

Customers across

North America

~18.4 million

Connected devices

~$780—$800 million

Annual recurring revenue and

$460—$480 million in LQA

EBITDA

Incubated

Successful adjacent

businesses

500+ million

Daily events processed by

artificial intelligence system

Nationwide

Sales, installation,

and service footprint

*Strategy Analytics, Jan 2017

5

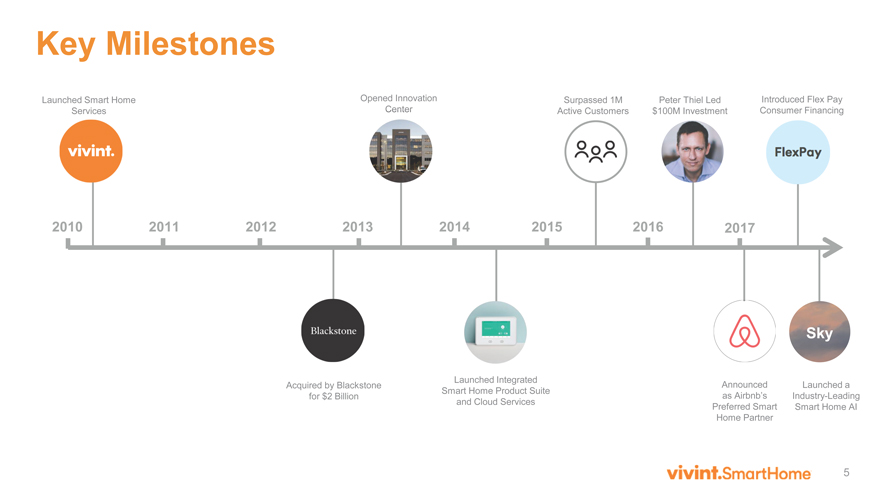

2010 2011 2012 2013 2014 2015 2016 2017

Launched Smart Home

Services

Opened Innovation

Center

Key Milestones

Launched Integrated

Smart Home Product Suite

and Cloud Services

Introduced Flex Pay

Consumer Financing

Surpassed 1M

Active Customers

Announced

as Airbnb’s

Preferred Smart

Home Partner

Acquired by Blackstone

for $2 Billion

Peter Thiel Led

$100M Investment

Launched a

Industry-Leading

Smart Home AI

Sky

6

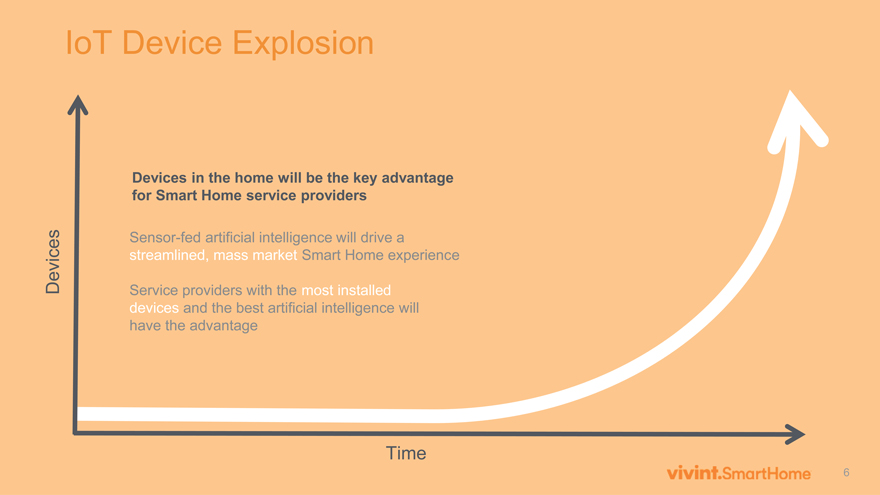

IoT Device Explosion

Devices

Time

Sensor-fed artificial intelligence will drive a

streamlined, mass market Smart Home experience

Service providers with the most installed

devices and the best artificial intelligence will

have the advantage

Devices in the home will be the key advantage

for Smart Home service providers

7

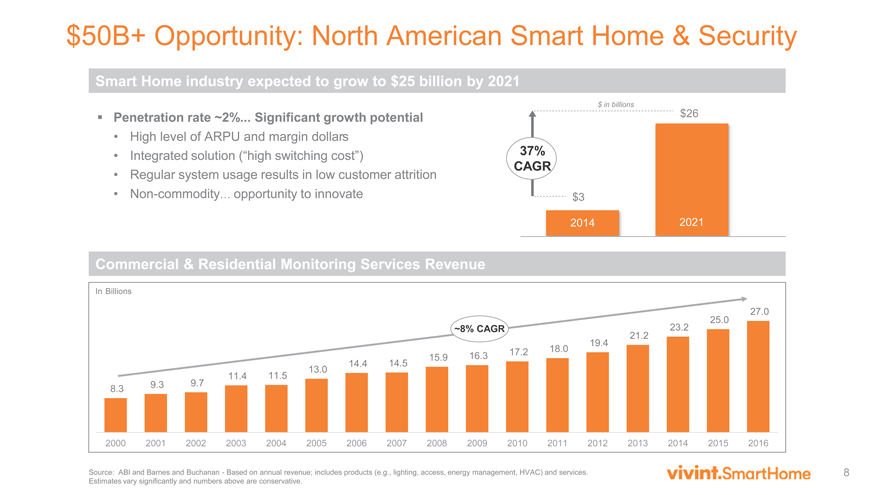

Accelerating Momentum as the Smart Home Leader

8

8.3 9.3 9.7

11.4 11.5

13.0

14.4 14.5

15.9 16.3 17.2 18.0

19.4

21.2

23.2

25.0

27.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$50B+ Opportunity: North American Smart Home & Security

? Penetration rate ~2%... Significant growth potential

• High level of ARPU and margin dollars

• Integrated solution (“high switching cost”)

• Regular system usage results in low customer attrition

•Non-commodity… opportunity to innovate

2014 2021

$3

$26

37%

CAGR

Source: ABI and Barnes and Buchanan—Based on annual revenue; includes products (e.g., lighting, access, energy management, HVAC) and services.

Estimates vary significantly and numbers above are conservative.

~8% CAGR

Smart Home industry expected to grow to $25 billion by 2021

Commercial & Residential Monitoring Services Revenue

In Billions

$ in billions

9

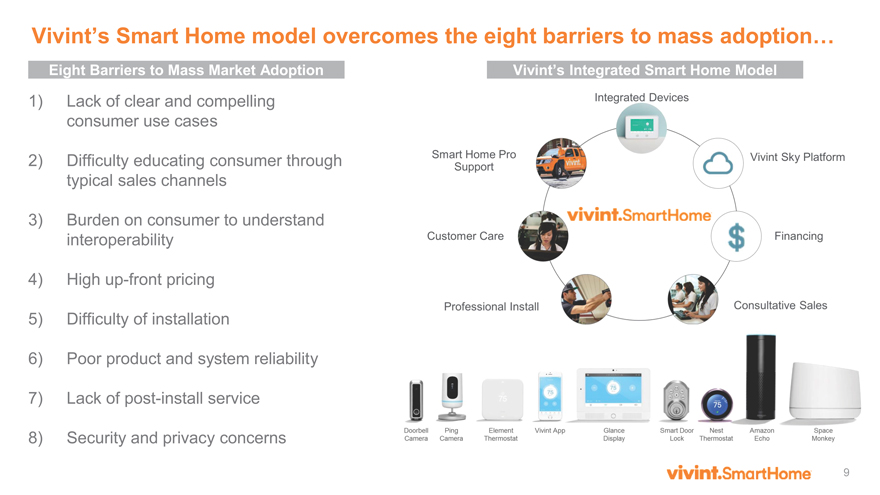

Vivint’s Smart Home model overcomes the eight barriers to mass adoption…

1) Lack of clear and compelling

consumer use cases

2) Difficulty educating consumer through

typical sales channels

3) Burden on consumer to understand

interoperability

4) Highup-front pricing

5) Difficulty of installation

6) Poor product and system reliability

7) Lack of post-install service

8) Security and privacy concerns

Eight Barriers to Mass Market Adoption Vivint’s Integrated Smart Home Model

10

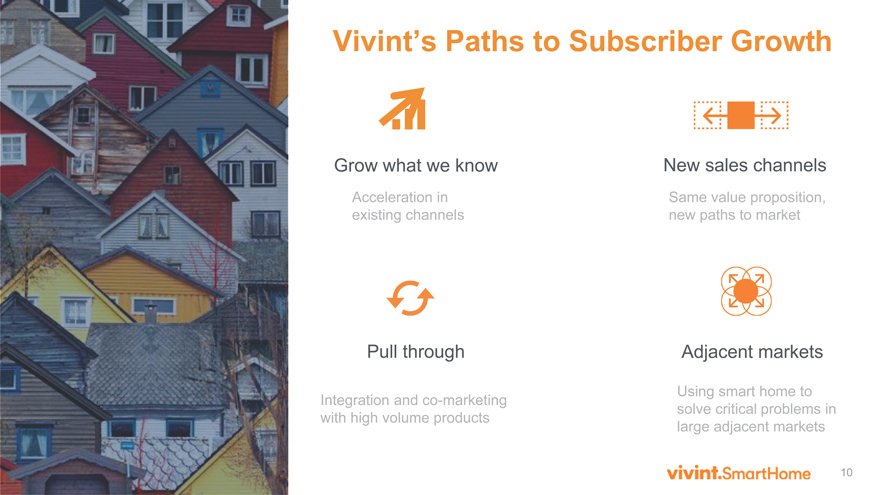

Vivint’s Paths to Subscriber Growth

Grow what we know

Pull through Adjacent markets

Acceleration in

existing channels

New sales channels

Same value proposition,

new paths to market

Using smart home to

solve critical problems in

large adjacent markets

Integration andco-marketing

with high volume products

11

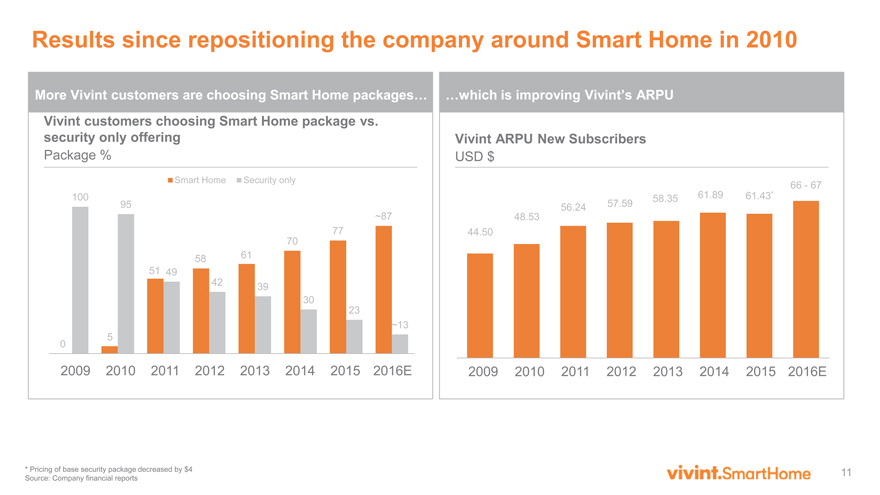

Results since repositioning the company around Smart Home in 2010

Vivint ARPU New Subscribers

USD $

Vivint customers choosing Smart Home package vs.

security only offering

Package %

More Vivint customers are choosing Smart Home packages… …which is improving Vivint’s ARPU

0

5

51

58 61

70

77

~87

100

95

49

42 39

30

23

~13

Smart Home Security only

2009 2011 2012 2013 2014

44.50

48.53

56.24 57.59

58.35 61.89 61.43*

66—67

2010 2015 2016E 2009 2010 2011 2012 2013 2014 2015 2016E

* Pricing of base security package decreased by $4

Source: Company financial reports

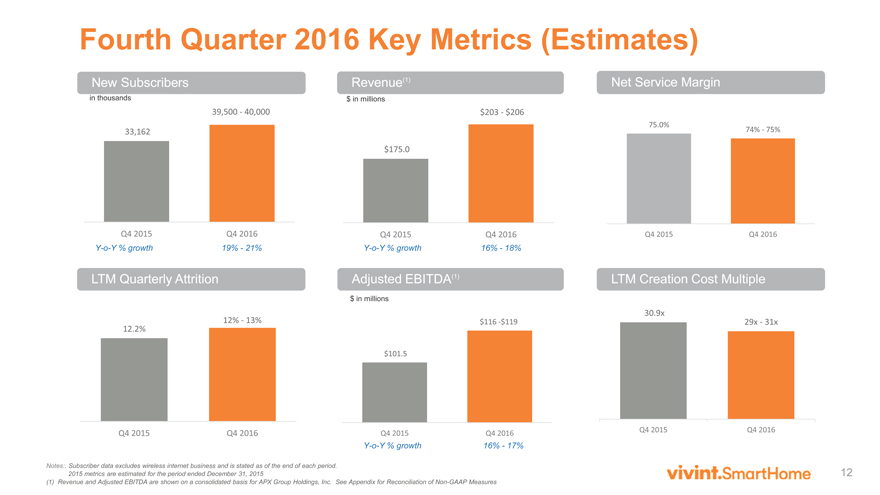

12

$101.5

$116 -$119

Q4 2015 Q4 2016

33,162

39,500—40,000

Q4 2015 Q4 2016

Fourth Quarter 2016 Key Metrics (Estimates)

Notes:. Subscriber data excludes wireless internet business and is stated as of the end of each period.

2015 metrics are estimated for the period ended December 31, 2015

(1) Revenue and Adjusted EBITDA are shown on a consolidated basis for APX Group Holdings, Inc. See Appendix for Reconciliation ofNon-GAAP Measures

Y-o-Y % growth 16%—18%

Y-o-Y % growth 16%—17%

Revenue(1)

Adjusted EBITDA(1) LTM Quarterly Attrition

$ in millions

$ in millions

New Subscribers

in thousands

Y-o-Y % growth 19%—21%

LTM Creation Cost Multiple

Net Service Margin

12.2%

12%—13%

Q4 2015 Q4 2016

$175.0

$203—$206

Q4 2015 Q4 2016

30.9x

29x—31x

Q4 2015 Q4 2016

75.0%

74%—75%

Q4 2015 Q4 2016

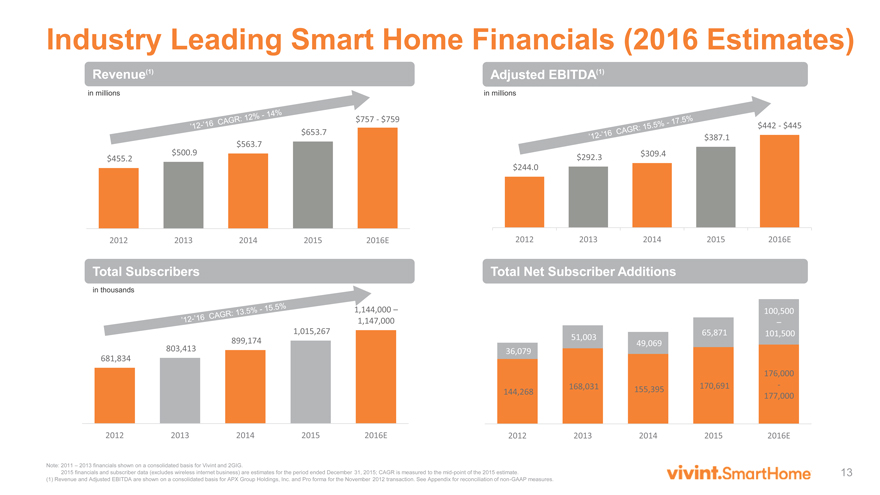

13

681,834

803,413

899,174

1,015,267

1,144,000 –

1,147,000

2012 2013 2014 2015 2016E

$455.2

$500.9

$563.7

$653.7

$757—$759

2012 2013 2014 2015 2016E

$244.0

$292.3 $309.4

$387.1

$442—$445

2012 2013 2014 2015 2016E

Industry Leading Smart Home Financials (2016 Estimates)

Note: 2011 – 2013 financials shown on a consolidated basis for Vivint and 2GIG.

2015 financials and subscriber data (excludes wireless internet business) are estimates for the period ended December 31, 2015; CAGR is measured to themid-point of the 2015 estimate.

(1) Revenue and Adjusted EBITDA are shown on a consolidated basis for APX Group Holdings, Inc. and Pro forma for the November 2012 transaction. See Appendix for reconciliation ofnon-GAAP measures.

Revenue(1) Adjusted EBITDA(1)

Total Subscribers Total Net Subscriber Additions

in millions in millions

in thousands

144,268

168,031 155,395 170,691

176,000

-

177,000

36,079

51,003

49,069

65,871

100,500

–

101,500

2012 2013 2014 2015 2016E

14

2017 Strategic Priorities

Platform Innovation Channel Expansion Funding

“Powered by AI … Sky will lock doors, arm a security

system, and adjust the thermostat with an eye toward

energy conservation … intuitively knowing when to make

adjustments … learning how to operate on its own.”

“All that silicon made my home smart, but not

intelligent. Vivint says its new Sky system can

change that.”

15

APX Group Holdings, Inc.

Annex A

16

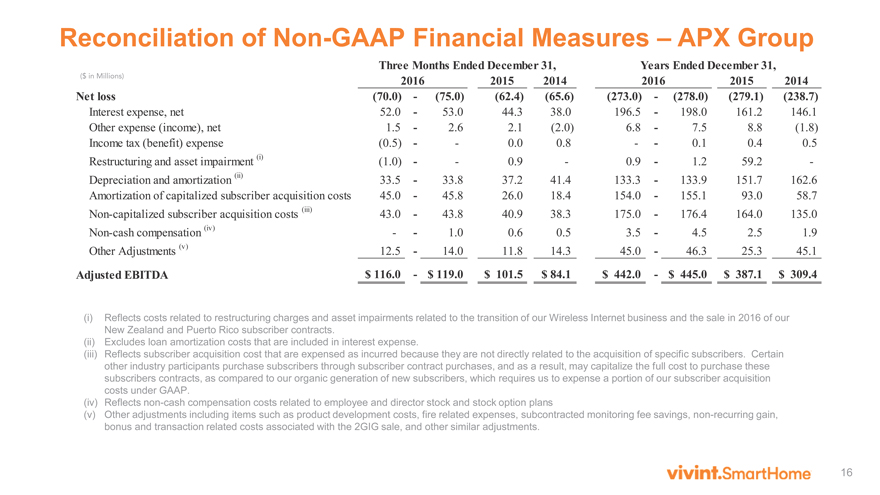

2015 2014 2015 2014

Net loss (70.0)—(75.0) (62.4) (65.6) (273.0)—(278.0) (279.1) (238.7)

Interest expense, net 52.0—53.0 44.3 38.0 196.5—198.0 161.2 146.1

Other expense (income), net 1.5—2.6 2.1 (2.0) 6.8—7.5 8.8 (1.8)

Income tax (benefit) expense (0.5) — 0.0 0.8 — 0.1 0.4 0.5

Restructuring and asset impairment (i) (1.0) — 0.9—0.9—1.2 59.2 -

Depreciation and amortization (ii) 33.5—33.8 37.2 41.4 133.3—133.9 151.7 162.6

Amortization of capitalized subscriber acquisition costs 45.0—45.8 26.0 18.4 154.0—155.1 93.0 58.7

Non-capitalized subscriber acquisition costs (iii) 43.0—43.8 40.9 38.3 175.0—176.4 164.0 135.0

Non-cash compensation (iv) — 1.0 0.6 0.5 3.5—4.5 2.5 1.9

Other Adjustments (v) 12.5—14.0 11.8 14.3 45.0—46.3 25.3 45.1

Adjusted EBITDA $ 116.0—$ 119.0 $ 101.5 $ 84.1 $ 442.0—$ 445.0 $ 387.1 $ 309.4

Three Months Ended December 31, Years Ended December 31,

2016 2016

Reconciliation ofNon-GAAP Financial Measures – APX Group

($ in Millions)

(i) Reflects costs related to restructuring charges and asset impairments related to the transition of our Wireless Internet business and the sale in 2016 of our

New Zealand and Puerto Rico subscriber contracts.

(ii) Excludes loan amortization costs that are included in interest expense.

(iii) Reflects subscriber acquisition cost that are expensed as incurred because they are not directly related to the acquisition of specific subscribers. Certain

other industry participants purchase subscribers through subscriber contract purchases, and as a result, may capitalize the full cost to purchase these

subscribers contracts, as compared to our organic generation of new subscribers, which requires us to expense a portion of our subscriber acquisition

costs under GAAP.

(iv) Reflectsnon-cash compensation costs related to employee and director stock and stock option plans

(v) Other adjustments including items such as product development costs, fire related expenses, subcontracted monitoring fee savings,non-recurring gain,

bonus and transaction related costs associated with the 2GIG sale, and other similar adjustments.

17

Total Subscribers – The aggregate number of active security and home automation subscribers at the end of a given period

Monthly Revenue per User (“RPU”) – The recurring monthly revenue billed to a smart home and security subscriber

Total Revenue per User – The aggregate RPU billed for all smart home and security subscribers

Average RPU – The Total RPU divided by Total Subscribers.

Average Revenue per New User (“ARPNU’)– The aggregate RPU for new subscribers originated during a period divided by the number of new subscribers originated during such period

Attrition – The aggregate number of canceled security and home automation subscribers during a period divided by the monthly weighted average number of total security and home automation

subscribers for such period. Subscribers are considered canceled when they terminate in accordance with the terms of their contract, are terminated by us, or if payment from such subscribers is

deemed uncollectible (when at least four monthly billings become past due). Sales of contracts to third parties and moves are excluded from the attrition calculation

Net Subscriber Acquisition Costs – Defined as direct and indirect costs to create a new security and home automation subscriber. These include commissions, equipment, installation, marketing and

other allocations (G&A and overhead), less activation fees and up sell revenue. These costs also exclude residuals and long-term equity expenses associated with thedirect-to-home sales channel.

Net Creation Cost Multiple – Defined as Net Subscriber Acquisition Costs, divided by the number of net new subscribers originated, and then divided by the ARPNU

Adjusted EBITDA – Net Income (loss) before interest expense (net of interest income), income and franchise taxes and depreciation and amortization (including amortization of capitalized subscriber

acquisition costs), further adjusted to exclude the effects of certain contract sales to third parties,non-capitalized subscriber acquisition costs, stock-based compensation, the historical results of the

Company’s Solar variable interest entity and certain unusual,non-cash,non-recurring and other items permitted in certain covenant calculations under the indentures governing the notes

Last Quarter Annualized Adjusted EBITDA (“LQA Adjusted EBITDA”) – A common industry measure used to reflect the step-function in earnings during the sales season related to the subscribers

generated from April to August. LQA Adjusted EBITDA, calculated by multiplying Adjusted EBITDA for the most recent fiscal quarter by 4, represents the ongoing earnings power of Vivint’s current

subscriber base and is potentially a more relevant metric than LTM due to the recurring nature of the revenue and expected earnings

Net Service Cost – Defined as total service costs, including monitoring, customer service, field service and other allocations (G&A and overhead) costs, less total service revenue divided by total

service subscribers

Net Service Margin – Defined as Average RPU per subscriber less Net Service Costs divided by Average RPU

Steady State Free Cash Flow (“SSFCF”) – Provides an estimate of the cash flow of a company, if it were to invest in new RPU only to the extent required to replace attrition. SSFCF is defined as LQA

Adjusted EBITDA less cost to replace RPU attrited, plus anadd-back for pro forma G&A expenses. Cost to replace RPU attrited is calculated by multiplying RPU by the attrition rate in steady state by

the Net Creation Cost Multiple

Certain Definitions