Exhibit (c)(iii)

Morgan Stanley Board of Directors Update Tricon Residential October 24, 2023

Board of Directors Update As of 10/24/23 • Following receipt of Blackstone’s non-binding proposal on 10/2/23, the Board of Directors formed a Special Committee (the “Committee”) at its Board Meeting on 10/5 • After the formation and convening of the Committee, Morgan Stanley communicated to Blackstone that the Company was prepared to enter into a confidentiality agreement and provide non-public information so that it could solidify and improve its proposal • On 10/13, the confidentiality agreement was executed, and a virtual data room was opened to Blackstone. The data room contained an initial set of documents that has been regularly expanded over the past 10 days in response to Blackstone’s ongoing diligence requests – As of 10/23, Blackstone has made over 450 diligence requests spanning business, tax, legal, financial and accounting topics – Since opening of the virtual data room, the Company, through Morgan Stanley, has responded to over 300 of Blackstone’s Blackstone due diligence requests via written responses and supporting files uploaded to the data room Proposal • In addition to regular-way diligence through the data room, the Company’s management team has held 5 virtual diligence sessions with Blackstone covering various topics, including: (1) tax on 10/17, (2) insurance and SFR operations on 10/20, (3) SFR acquisitions on 10/20, (4) corporate / FP&A on 10/23 and (5) Canadian properties on 10/24. Other due diligence activities that have been scheduled include: – Property tours this week in select markets (Dallas, Atlanta, Charlotte, Nashville, Houston, Jacksonville, Orlando, Tampa and Toronto) – Two additional sessions with management are currently scheduled to cover capital markets (10/24) and accounting (10/25) • Blackstone has indicated that they will provide a revised proposal the week of 10/30 • See page 3 for a summary of events related to Blackstone and the ongoing diligence activities • On 10/17, Jonathan Litt of Land & Buildings (a real estate-focused activist investor) presented at the 13D Active-Passive Land & Investor Summit in New York, where he pitched the Company as a substantially undervalued investment Buildings (which was subsequently publicly published) including initial Presentation • See pages 4-6 for a summary of the Land & Buildings presentation share price and equity analyst reactions TRICON RESIDENTIAL 2

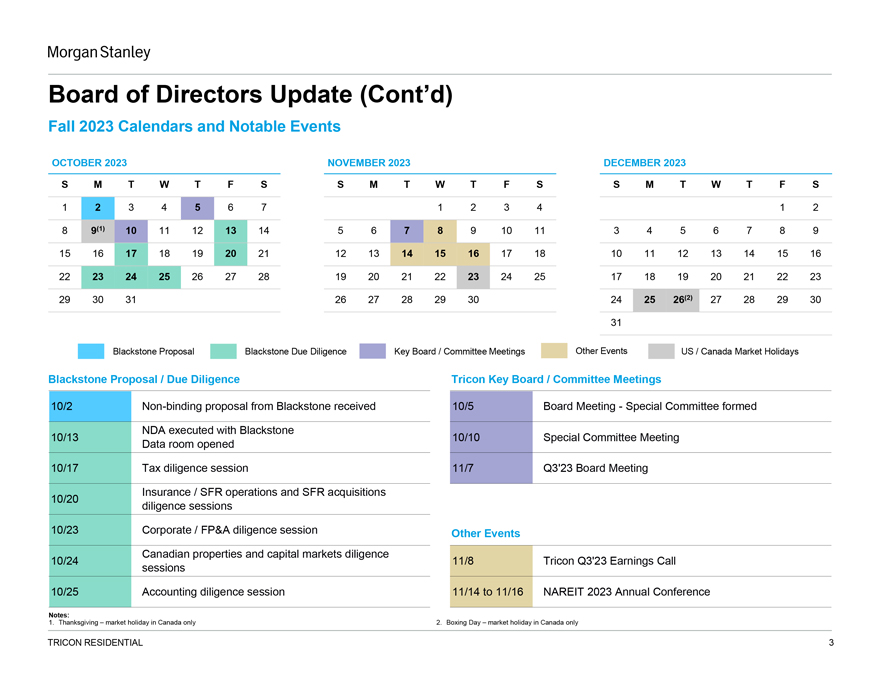

Board of Directors Update (Cont’d) Fall 2023 Calendars and Notable Events OCTOBER 2023 NOVEMBER 2023 DECEMBER 2023 S M T W T F S S M T W T F S S M T W T F S 1 2 3 4 5 6 7 1 2 3 4 1 2 8 9(1) 10 11 12 13 14 5 6 7 8 9 10 11 3 4 5 6 7 8 9 15 16 17 18 19 20 21 12 13 14 15 16 17 18 10 11 12 13 14 15 16 22 23 24 25 26 27 28 19 20 21 22 23 24 25 17 18 19 20 21 22 23 29 30 31 26 27 28 29 30 24 25 26(2) 27 28 29 30 31 Blackstone Proposal Blackstone Due Diligence Key Board / Committee Meetings Other Events US / Canada Market Holidays Blackstone Proposal / Due Diligence Tricon Key Board / Committee Meetings 10/2 Non-binding proposal from Blackstone received 10/5 Board Meeting—Special Committee formed NDA executed with Blackstone 10/13 10/10 Special Committee Meeting Data room opened 10/17 Tax diligence session 11/7 Q3’23 Board Meeting Insurance / SFR operations and SFR acquisitions 10/20 diligence sessions 10/23 Corporate / FP&A diligence session Other Events Canadian properties and capital markets diligence 10/24 11/8 Tricon Q3’23 Earnings Call sessions 10/25 Accounting diligence session 11/14 to 11/16 NAREIT 2023 Annual Conference Notes: 1. Thanksgiving – market holiday in Canada only 2. Boxing Day – market holiday in Canada only TRICON RESIDENTIAL 3

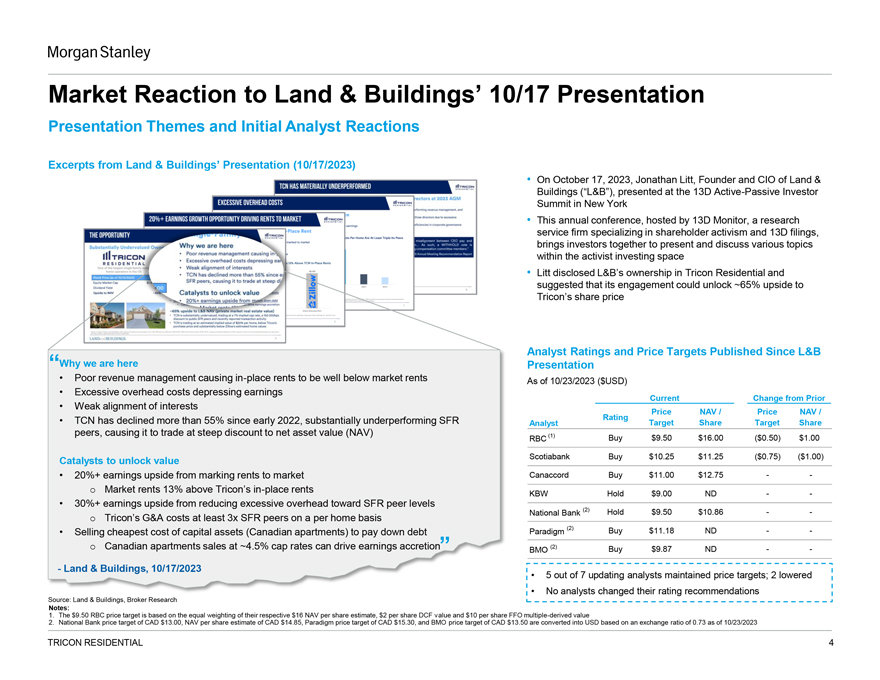

Market Reaction to Land & Buildings’ 10/17 Presentation Presentation Themes and Initial Analyst Reactions Excerpts from Land & Buildings’ Presentation (10/17/2023) • On October 17, 2023, Jonathan Litt, Founder and CIO of Land & Buildings (“L&B”), presented at the 13D Active-Passive Investor Summit in New York • This annual conference, hosted by 13D Monitor, a research service firm specializing in shareholder activism and 13D filings, brings investors together to present and discuss various topics within the activist investing space • Litt disclosed L&B’s ownership in Tricon Residential and suggested that its engagement could unlock ~65% upside to Tricon’s share price Analyst Ratings and Price Targets Published Since L&B “Why we are here Presentation • Poor revenue management causing in-place rents to be well below market rents As of 10/23/2023 ($USD) • Excessive overhead costs depressing earnings • Weak alignment of interests Current Change from Prior Price NAV / Price NAV / • TCN has declined more than 55% since early 2022, substantially underperforming SFR Rating Analyst Target Share Target Share peers, causing it to trade at steep discount to net asset value (NAV) (1) RBC Buy $9.50 $16.00 ($0.50) $1.00 Catalysts to unlock value Scotiabank Buy $10.25 $11.25 ($0.75) ($1.00) • 20%+ earnings upside from marking rents to market Canaccord Buy $11.00 $12.75—-o Market rents 13% above Tricon’s in-place rents KBW Hold $9.00 ND — • 30%+ earnings upside from reducing excessive overhead toward SFR peer levels (2) National Bank Hold $9.50 $10.86—-o Tricon’s G&A costs at least 3x SFR peers on a per home basis • Selling cheapest cost of capital assets (Canadian apartments) to pay down debt Paradigm (2) Buy $11.18 ND—-o Canadian apartments sales at ~4.5% cap rates can drive earnings accretion” BMO (2) Buy $9.87 ND ——Land & Buildings, 10/17/2023 • 5 out of 7 updating analysts maintained price targets; 2 lowered • No analysts changed their rating recommendations Source: Land & Buildings, Broker Research Notes: 1. The $9.50 RBC price target is based on the equal weighting of their respective $16 NAV per share estimate, $2 per share DCF value and $10 per share FFO multiple-derived value 2. National Bank price target of CAD $13.00, NAV per share estimate of CAD $14.85, Paradigm price target of CAD $15.30, and BMO price target of CAD $13.50 are converted into USD based on an exchange ratio of 0.73 as of 10/23/2023 TRICON RESIDENTIAL 4

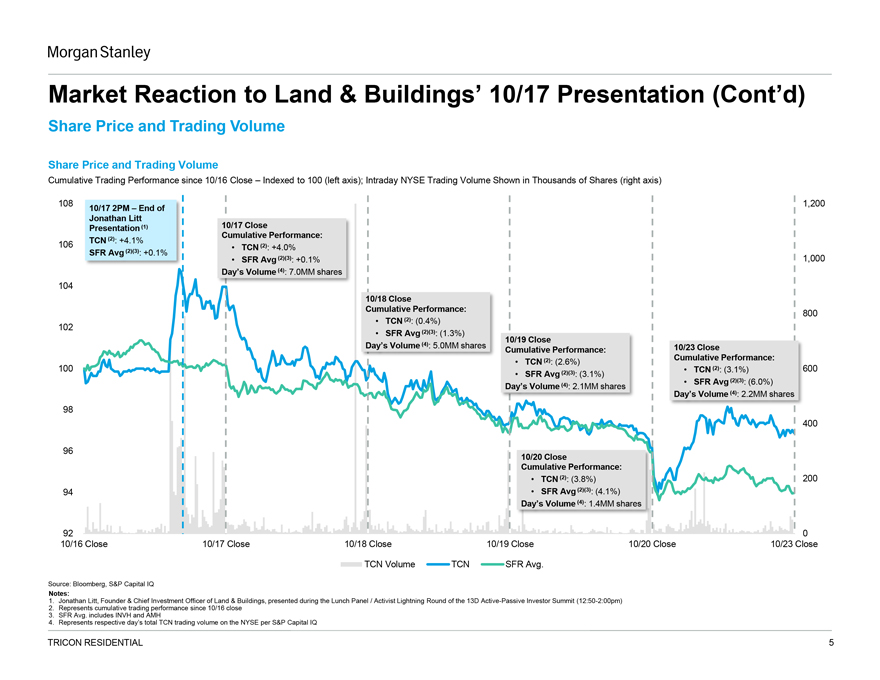

Market Reaction to Land & Buildings’ 10/17 Presentation (Cont’d) Share Price and Trading Volume Share Price and Trading Volume Cumulative Trading Performance since 10/16 Close – Indexed to 100 (left axis); Intraday NYSE Trading Volume Shown in Thousands of Shares (right axis) 108 1,200 10/17 2PM – End of Jonathan Litt 10/17 Close Presentation (1) Cumulative Performance: TCN (2): +4.1% 106 SFR Avg (2)(3): +0.1% • TCN (2): +4.0% • SFR Avg (2)(3): +0.1% 1,000 Day’s Volume (4): 7.0MM shares 104 10/18 Close Cumulative Performance: • TCN (2): (0.4%) 800 102 • SFR Avg (2)(3): (1.3%) 10/19 Close Day’s Volume (4): 5.0MM shares 10/23 Close Cumulative Performance: Cumulative Performance: • TCN (2): (2.6%) 100 • SFR Avg (2)(3): (3.1%) • TCN (2): (3.1%) 600 Day’s Volume (4): 2.1MM shares • SFR Avg (2)(3): (6.0%) Day’s Volume (4): 2.2MM shares 98 400 96 10/20 Close Cumulative Performance: • TCN (2): (3.8%) 200 94 • SFR Avg (2)(3): (4.1%) Day’s Volume (4): 1.4MM shares 92 0 10/16 Close 10/17 Close 10/18 Close 10/19 Close 10/20 Close 10/23 Close TCN Volume TCN SFR Avg. Source: Bloomberg, S&P Capital IQ Notes: 1. Jonathan Litt, Founder & Chief Investment Officer of Land & Buildings, presented during the Lunch Panel / Activist Lightning Round of the 13D Active-Passive Investor Summit (12:50-2:00pm) 2. Represents cumulative trading performance since 10/16 close 3. SFR Avg. includes INVH and AMH 4. Represents respective day’s total TCN trading volume on the NYSE per S&P Capital IQ TRICON RESIDENTIAL 5

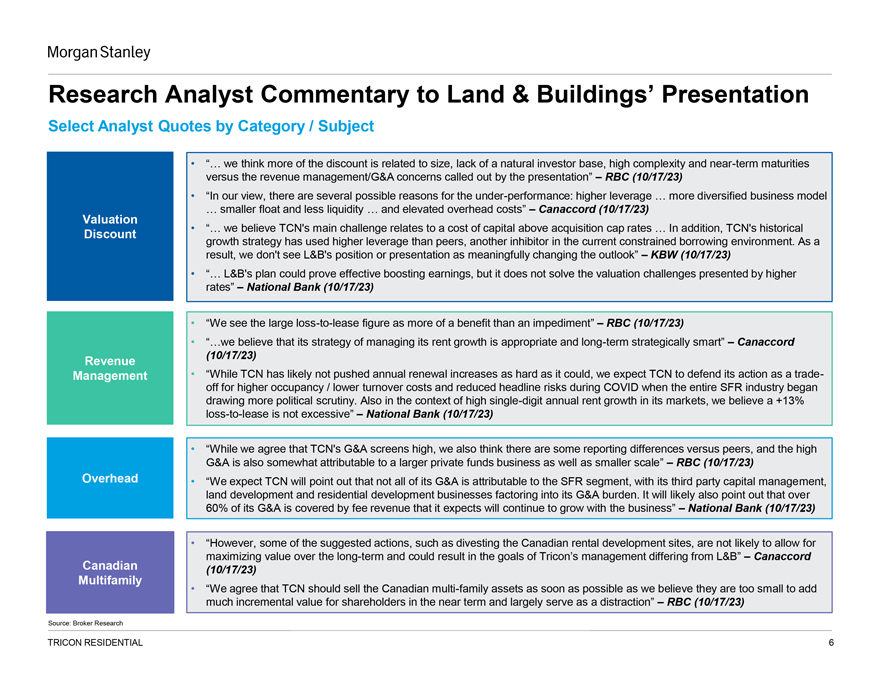

Research Analyst Commentary to Land & Buildings’ Presentation Select Analyst Quotes by Category / Subject • “… we think more of the discount is related to size, lack of a natural investor base, high complexity and near-term maturities versus the revenue management/G&A concerns called out by the presentation” – RBC (10/17/23) • “In our view, there are several possible reasons for the under-performance: higher leverage … more diversified business model Valuation … smaller float and less liquidity … and elevated overhead costs” – Canaccord (10/17/23) • “… we believe TCN’s main challenge relates to a cost of capital above acquisition cap rates … In addition, TCN’s historical Discount growth strategy has used higher leverage than peers, another inhibitor in the current constrained borrowing environment. As a result, we don’t see L&B’s position or presentation as meaningfully changing the outlook” – KBW (10/17/23) • “… L&B’s plan could prove effective boosting earnings, but it does not solve the valuation challenges presented by higher rates” – National Bank (10/17/23) • “We see the large loss-to-lease figure as more of a benefit than an impediment” – RBC (10/17/23) • “…we believe that its strategy of managing its rent growth is appropriate and long-term strategically smart” – Canaccord (10/17/23) Revenue Management • “While TCN has likely not pushed annual renewal increases as hard as it could, we expect TCN to defend its action as a tradeoff for higher occupancy / lower turnover costs and reduced headline risks during COVID when the entire SFR industry began drawing more political scrutiny. Also in the context of high single-digit annual rent growth in its markets, we believe a +13% loss-to-lease is not excessive” – National Bank (10/17/23) • “While we agree that TCN’s G&A screens high, we also think there are some reporting differences versus peers, and the high G&A is also somewhat attributable to a larger private funds business as well as smaller scale” – RBC (10/17/23) Overhead • “We expect TCN will point out that not all of its G&A is attributable to the SFR segment, with its third party capital management, land development and residential development businesses factoring into its G&A burden. It will likely also point out that over 60% of its G&A is covered by fee revenue that it expects will continue to grow with the business” – National Bank (10/17/23) • “However, some of the suggested actions, such as divesting the Canadian rental development sites, are not likely to allow for maximizing value over the long-term and could result in the goals of Tricon’s management differing from L&B” – Canaccord Canadian (10/17/23) Multifamily • “We agree that TCN should sell the Canadian multi-family assets as soon as possible as we believe they are too small to add much incremental value for shareholders in the near term and largely serve as a distraction” – RBC (10/17/23) Source: Broker Research TRICON RESIDENTIAL 6

Legal Disclaimer We have prepared this document solely for informational purposes. You should not definitively rely upon it or use it to form the definitive basis for any decision, contract, commitment or action whatsoever, with respect to any proposed transaction or otherwise. You and your directors, officers, employees, agents and affiliates must hold this document and any oral information provided in connection with this document in strict confidence and may not communicate, reproduce, distribute or disclose it to any other person, or refer to it publicly, in whole or in part at any time except with our prior written consent. If you are not the intended recipient of this document, please delete and destroy all copies immediately. We have prepared this document and the analyses contained in it based, in part, on certain assumptions and information obtained by us from the recipient, its directors, officers, employees, agents, affiliates and/or from other sources. Our use of such assumptions and information does not imply that we have independently verified or necessarily agree with any of such assumptions or information, and we have assumed and relied upon the accuracy and completeness of such assumptions and information for purposes of this document. Neither we nor any of our affiliates, or our or their respective officers, employees or agents, make any representation or warranty, express or implied, in relation to the accuracy or completeness of the information contained in this document or any oral information provided in connection herewith, or any data it generates and accept no responsibility, obligation or liability (whether direct or indirect, in contract, tort or otherwise) in relation to any of such information. We and our affiliates and our and their respective officers, employees and agents expressly disclaim any and all liability which may be based on this document and any errors therein or omissions therefrom. Neither we nor any of our affiliates, or our or their respective officers, employees or agents, make any representation or warranty, express or implied, that any transaction has been or may be effected on the terms or in the manner stated in this document, or as to the achievement or reasonableness of future projections, management targets, estimates, prospects or returns, if any. Any views or terms contained herein are preliminary only, and are based on financial, economic, market and other conditions prevailing as of the date of this document and are therefore subject to change. We undertake no obligation or responsibility to update any of the information contained in this document. Past performance does not guarantee or predict future performance. This document and the information contained herein do not constitute an offer to sell or the solicitation of an offer to buy any security, commodity or instrument or related derivative, nor do they constitute an offer or commitment to lend, syndicate or arrange a financing, underwrite or purchase or act as an agent or advisor or in any other capacity with respect to any transaction, or commit capital, or to participate in any trading strategies, and do not constitute legal, regulatory, accounting or tax advice to the recipient. We recommend that the recipient seek independent third party legal, regulatory, accounting and tax advice regarding the contents of this document. This document does not constitute and should not be considered as any form of financial opinion or recommendation by us or any of our affiliates. This document is not a research report and was not prepared by the research department of Morgan Stanley or any of its affiliates. Notwithstanding anything herein to the contrary, each recipient hereof (and their employees, representatives, and other agents) may disclose to any and all persons, without limitation of any kind from the commencement of discussions, the U.S. federal and state income tax treatment and tax structure of the proposed transaction and all materials of any kind (including opinions or other tax analyses) that are provided relating to the tax treatment and tax structure. For this purpose, “tax structure” is limited to facts relevant to the U.S. federal and state income tax treatment of the proposed transaction and does not include information relating to the identity of the parties, their affiliates, agents or advisors. This document is provided by Morgan Stanley & Co. LLC and/or certain of its affiliates or other applicable entities, which may include Morgan Stanley Realty Incorporated, Morgan Stanley Senior Funding, Inc., Morgan Stanley Bank, N.A., Morgan Stanley & Co. International plc, Morgan Stanley Securities Limited, Morgan Stanley Bank AG, Morgan Stanley MUFG Securities Co., Ltd., Mitsubishi UFJ Morgan Stanley Securities Co., Ltd., Morgan Stanley Asia Limited, Morgan Stanley Australia Securities Limited, Morgan Stanley Australia Limited, Morgan Stanley Asia (Singapore) Pte., Morgan Stanley Services Limited, Morgan Stanley & Co. International plc Seoul Branch and/or Morgan Stanley Canada Limited Unless governing law permits otherwise, you must contact an authorized Morgan Stanley entity in your jurisdiction regarding this document or any of the information contained herein. © Morgan Stanley and/or certain of its affiliates. All rights reserved. TRICON RESIDENTIAL 7