| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

| Non-IFRS measures, forward-looking statements and market industry data | ||||||||

| 1 | Introduction | |||||||

| 1.1 | Vision and guiding principles | |||||||

| 1.2 | Business overview | |||||||

| 1.3 | Sustainability | |||||||

| 2 | Highlights | |||||||

| 3 | Consolidated financial results | |||||||

| 3.1 | Review of income statements | |||||||

| 3.2 | Review of selected balance sheet items | |||||||

| 3.3 | Subsequent events | |||||||

| 4 | Operating results of businesses | |||||||

| 4.1 | Single-Family Rental | |||||||

| 4.2 | Adjacent residential businesses | |||||||

| 4.2.1 | Multi-Family Rental | |||||||

| 4.2.2 | Residential Development | |||||||

| 4.3 | Strategic Capital | |||||||

| 5 | Liquidity and capital resources | |||||||

| 5.1 | Financial strategy | |||||||

| 5.2 | Liquidity | |||||||

| 5.3 | Capital resources | |||||||

| 6 | Operational key performance indicators | |||||||

| 7 | Accounting estimates and policies, controls and procedures, and risk analysis | |||||||

| 7.1 | Revenue and income recognition | |||||||

| 7.2 | Accounting estimates and policies | |||||||

| 7.3 | Controls and procedures | |||||||

| 7.4 | Transactions with related parties | |||||||

| 7.5 | Dividends | |||||||

| 7.6 | Compensation incentive plans | |||||||

| 7.7 | Risk definition and management | |||||||

| 8 | Historical financial information | |||||||

| Appendix A - Reconciliations | ||||||||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

Non-IFRS measures

This Management’s Discussion and Analysis (“MD&A”) should be read in conjunction with the consolidated financial statements and accompanying notes for the year ended December 31, 2023 (the "Consolidated Financial Statements") of Tricon Residential Inc. (“Tricon", "us", "we" or the “Company”), prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“the IASB”) and consistent with the Company's audited annual consolidated financial statements for the year ended December 31, 2022.

The Company has included herein certain non-IFRS financial measures and non-IFRS ratios, including, but not limited to: "proportionate" metrics, net operating income ("NOI"), NOI margin, proportionate same home NOI and NOI margin, funds from operations ("FFO"), core funds from operations ("Core FFO"), adjusted funds from operations ("AFFO"), Core FFO per share, AFFO per share, Core FFO payout ratio, AFFO payout ratio, as well as certain key indicators of the performance of our businesses which are supplementary financial measures. These measures are commonly used by entities in the real estate industry as useful metrics for measuring performance. We utilize these measures in managing our business, including performance measurement and capital allocation. In addition, certain of these measures are used in measuring compliance with our debt covenants. We believe that providing these performance measures on a supplemental basis is helpful to investors and shareholders in assessing the overall performance of the Company’s business. However, these measures are not recognized under and do not have any standardized meaning prescribed by IFRS as issued by the IASB, and are not necessarily comparable to similar measures presented by other publicly-traded entities. These measures should be considered as supplemental in nature and not as a substitute for related financial information prepared in accordance with IFRS. Because non-IFRS financial measures, non-IFRS ratios and supplementary financial measures do not have standardized meanings prescribed under IFRS, securities regulations require that such measures be clearly defined, identified, and reconciled to their nearest IFRS measure. The definition, calculation and reconciliation of the non-IFRS financial measures and the requisite disclosure for non-IFRS ratios used in this MD&A are provided in Section 4 and Appendix A, and the supplementary financial measures which are key performance indicators presented herein are discussed in detail in Section 6.

The non-IFRS financial measures, non-IFRS ratios and supplementary financial measures presented herein should not be construed as alternatives to net income (loss) or cash flow from the Company’s activities, determined in accordance with IFRS, as indicators of Tricon’s financial performance. Tricon’s method of calculating these measures may differ from other issuers’ methods and, accordingly, these measures may not be comparable to similar measures presented by other publicly-traded entities.

Forward-looking statements

Certain statements in this MD&A are considered “forward-looking information” as defined under applicable securities laws (“forward-looking statements”). This document should be read in conjunction with material contained in the Company’s current Consolidated Financial Statements along with the Company’s other publicly filed documents. Words such as “may”, “would”, “could”, “will”, “anticipate”, “believe”, “plan”, “expect”, “intend”, “estimate”, “aim”, “endeavor”, “project”, “continue”, "target" and similar expressions identify these forward-looking statements. Statements containing forward-looking information are not historical facts but instead reflect management’s expectations, intentions and beliefs concerning anticipated future events, results, circumstances, economic performance or expectations with respect to Tricon and its investments and are based on information currently available to management and on assumptions that management believes to be reasonable.

This MD&A includes forward-looking statements pertaining to: anticipated operational and financial performance; the Company’s strategic and operating plans and growth prospects; expected demographic and economic trends impacting the Company’s key markets; project plans, costs, timelines and sales/rental expectations; expected performance fees; future cash flows; transaction and development timelines; anticipated demand for residential real estate; the anticipated growth of the Company's rental businesses; the acquisition of build-to-rent projects; expected future acquisitions, acquisition pace, rent growth, operating expenses, occupancy and turnover rates, and capital expenditure programs for single-family rental homes and multi-family rental apartments; rollout of operations programs and resident betterment programs; debt financing and refinancing intentions; continuing increases in interest rates, inflation and economic uncertainty; the impact and aftermath of the COVID-19 pandemic; the

Page 1 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

anticipated benefits of the Go-Private Transaction to the Company and its shareholders; shareholder approvals, court approval and required regulatory approvals and other conditions required to complete the Go-Private Transaction; the anticipated timing of the completion of the Go-Private Transaction; future distributions by the Company; and the de-listing of the Common Shares from the TSX and the NYSE and the Company ceasing to be a reporting issuer; and the consequences to the Company and its shareholders if the Go-Private Transaction is not completed. The assumptions underlying these forward-looking statements and a list of factors that may cause actual business performance to differ from current projections are discussed in this MD&A and in the Company’s Annual Information Form dated February 27, 2024 (the “AIF”), which is available under Tricon’s profile on SEDAR+ at www.sedarplus.ca and (as part of its Form 40-F filing) EDGAR at www.sec.gov. The continuing impact and aftermath of COVID-19 on the operations, business and financial results of the Company may cause actual results to differ, possibly materially, from the results discussed in the forward-looking statements.

Forward-looking statements are necessarily based on estimates and assumptions that, while considered reasonable by management of the Company as of the date of this MD&A, are inherently subject to significant business, economic and competitive uncertainties and contingencies. The Company’s estimates, beliefs and assumptions, which may prove to be incorrect, include the various assumptions set forth herein, including, but not limited to, the Company’s future growth potential; results of operations; future prospects and opportunities; demographic and industry trends; no change in legislative or regulatory matters; future levels of indebtedness and prevailing interest rates; the tax laws as currently in effect; the continuing availability of capital and suitable acquisition and investment opportunities; current economic conditions including property value appreciation and overall levels of inflation; and the impact and aftermath of COVID-19.

When relying on forward-looking statements to make decisions, the Company cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant unknown risks and uncertainties. Forward-looking statements should not be read as guarantees of future performance or results and will not necessarily be accurate indications of whether or not the times at or by which such performance or results will be achieved. A number of factors could cause actual results to differ, possibly materially, from the results discussed in the forward-looking statements, including, but not limited to, the failure to obtain necessary approvals or satisfy (or obtain a waiver of) the conditions to closing the Transaction, the occurrence of any event, change or other circumstance that could give rise to the termination of the Transaction, the Company or Blackstone’s failure to consummate the Transaction when required or on the terms as originally negotiated, risks related to the disruption of management time from ongoing business operations due to the Transaction and possible difficulties in maintaining customer, supplier, key personnel and other strategic relationships, potential litigation relating to the Transaction, including the effects of any outcomes related thereto, the Company’s ability to execute its growth strategies; the impact of changing conditions in the multi-family housing market; increasing competition in the single-family and multi-family housing market; the effect of fluctuations and cycles in the Canadian and U.S. real estate market; the marketability and value of the Company’s portfolio; the expected future value of the Company's portfolio; changes in the attitudes, financial condition and demand of the Company’s demographic market; rising interest rates and volatility in financial markets; the potential impact of reduced supply of labor and materials on expected costs and timelines; rates of inflation and overall economic uncertainty; developments and changes in applicable laws and regulations; and the impact of COVID-19 on the operations, business and financial results of the Company.

Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking statements prove incorrect, actual results, performance or achievements could vary materially from those expressed or implied by the forward-looking statements contained in this MD&A. See the AIF and the continuous disclosure documents referenced in Section 7.7 for a more complete list of risks relating to an investment in the Company and an indication of the impact the materialization of such risks could have on the Company, and therefore cause actual results to deviate from the forward-looking statements.

Certain statements included in this MD&A may be considered a “financial outlook” for purposes of applicable securities laws, and as such, the financial outlook may not be appropriate for purposes other than this document. Although the forward-looking statements contained in this MD&A are based upon what management currently believes to be reasonable assumptions (including those noted above), there can be no assurance that actual results, performance or achievements will be consistent with these forward-looking statements. The forward-looking statements contained in this document are expressly qualified in their entirety by this cautionary statement.

Page 2 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

When relying on our forward-looking statements to make decisions with respect to the Company, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. The forward-looking statements in this MD&A are made as of the date of this document and the Company does not intend to, or assume any obligation to, update or revise these forward-looking statements or information to reflect new information, events, results or circumstances or otherwise after the date on which such statements are made to reflect the occurrence of unanticipated events, except as required by law, including securities laws.

Market and industry data

This MD&A may include certain market and industry data and forecasts obtained from third-party sources, industry publications and publicly available information as well as industry data prepared by management on the basis of its knowledge of the industry in which the Company operates (including management’s estimates and assumptions relating to the industry based on that knowledge). Management’s knowledge of the North American residential real estate industry has been developed through its experience and participation in the industry. Management believes that its industry data is accurate and that its estimates and assumptions are reasonable, but there can be no assurance as to the accuracy or completeness of this data. Third-party sources generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy or completeness of included information. Although management believes it to be reliable, the Company has not independently verified any of the data from third-party sources referred to in this MD&A, or analyzed or verified the underlying studies or surveys relied upon or referred to by such sources, or ascertained the underlying economic assumptions relied upon by such sources.

Page 3 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

1. Introduction

This Management’s Discussion and Analysis (“MD&A”) is dated as of February 27, 2024, the date it was approved by the Board of Directors of Tricon Residential Inc. (“Tricon", “us", “we” or the “Company”), and reflects all material events up to that date. It should be read in conjunction with the Company’s audited consolidated financial statements and related notes for the year ended December 31, 2023 ("Consolidated Financial Statements"), which were prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board ("IFRS"). The audited annual consolidated financial statements are available on the Company's website at www.triconresidential.com, on the Canadian Securities Administrators’ website at www.sedarplus.ca, and as part of the Company's annual report (Form 40-F) filed on the EDGAR section of the U.S. Securities and Exchange Commission’s (“SEC”) website at www.sec.gov. Additional information about the Company, including its Annual Information Form, is available on these websites.

The registered office of the Company is at 7 St. Thomas Street, Suite 801, Toronto, Ontario M5S 2B7. The Company’s common shares are traded under the symbol TCN on both the New York Stock Exchange (the "NYSE") and the Toronto Stock Exchange (the "TSX").

On January 19, 2024, the Company announced that it had entered into an arrangement agreement (the "Arrangement Agreement") under which Blackstone Real Estate Partners X L.P. ("BREP X"), together with Blackstone Real Estate Income Trust, Inc. ("BREIT" and, together with BREP X and their respective affiliates, "Blackstone"), will acquire all outstanding common shares of Tricon, resulting in the privatization of the Company. Refer to Section 3.3 of this document or Note 40 to the consolidated financial statements for details.

All dollar amounts in this MD&A are expressed in U.S. dollars unless otherwise indicated.

1.1 Vision and guiding principles

Tricon was founded in 1988 as a fund manager for private clients and institutional investors focused on for-sale residential real estate development. The pursuit of continuous improvement as well as a desire to diversify and facilitate succession planning drove the Company’s decision to become publicly traded in 2010. While the U.S. for-sale housing industry was decimated in the Great Recession of 2007-2009, Tricon's strong foundation and its leaders' resilience helped it endure the downturn and learn valuable lessons that informed the Company's decision to ultimately focus on rental housing.

In the decade that followed, Tricon embarked on a deliberate transformation away from for-sale housing, which is inherently cyclical, to become a rental housing company that addresses the needs of a new generation facing reduced home affordability and a desire for meaningful human connections, convenience and a sense of community. Today, Tricon provides high-quality, essential shelter to residents. Tricon's business is defensive by design, intended to outperform in good times and perform relatively well in more challenging times.

Tricon was among the first to enter into and institutionalize the U.S. single-family rental industry. Our success has been built on a culture of innovation and a willingness to adopt new technologies to drive efficiencies and improve our residents’ lives. We believe that our ability to bring together capital, ideas, people and technology under one roof is unique in real estate and allows us to improve the resident experience, safeguard our stakeholders’ investments, and drive superior returns.

Tricon strives to be North America’s pre-eminent single-family rental housing company serving the middle-market demographic by owning quality properties in attractive markets, focusing on operational excellence, and delivering an exceptional resident experience. Tricon is driven by its purpose statement - Imagine a world where housing unlocks life’s potential - and encourages its employees to conduct themselves every day according to the following guiding principles:

•Go above and beyond to enrich the lives of our residents

•Commit to and inspire excellence in everything we do

Page 4 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

•Ask questions, embrace problems, thrive on the process of innovation

•Do what is right, not what is easy

•Elevate each other so together we leave an enduring legacy

Tricon’s guiding principles underpin our business strategy and culture of taking care of our employees first, who in turn are empowered and inspired to provide residents with superior service and to positively impact local communities. When our residents are satisfied, they rent with us longer, treat our properties as their own, and are likely to refer friends and family to become new customers. We have realized that the best way to drive returns for our shareholders and private investors is to ensure our team and residents are fulfilled. This is why Our People and Our Residents are also two of our key sustainability priorities (see Section 1.3).

1.2 Business overview

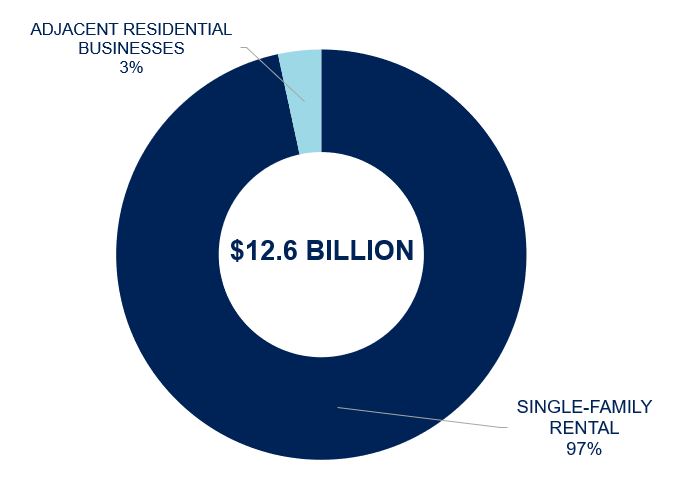

Tricon is an owner, operator and developer of a growing portfolio of approximately 38,000 single-family rental homes located primarily in the U.S. Sun Belt and multi-family apartments in Canada. The Company also invests in adjacent residential businesses which include residential development assets in the United States and Canada. Through its fully integrated operating platform, the Company earns rental income and ancillary revenue from single-family rental properties, income from its investments in multi-family rental properties and residential developments, as well as fees from managing strategic capital associated with its businesses. Our commitment to enriching the lives of our employees, residents and local communities underpins Tricon’s culture and business philosophy. We provide high-quality rental housing options for families across the United States and Canada through our technology-enabled operating platform and dedicated on-the-ground operating teams. Our development programs are also delivering thousands of new rental homes and apartments as part of our commitment to help solve the housing supply shortage. At Tricon, we imagine a world where housing unlocks life’s potential.

As at December 31, 2023, about 97% of the Company’s real estate assets are stabilized single-family rental homes and the remaining 3% are invested in adjacent residential businesses.

(Based on the fair value of single-family homes, equity-accounted investments in multi-family rental properties and Canadian residential developments, Canadian development properties (net of debt) and investments in U.S. residential developments.)

Page 5 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

Tricon’s single-family rental business

Tricon's U.S. single-family rental strategy targets the "middle-market" resident demographic which consists of over seven million U.S. renter households (source: U.S. Census Bureau). The Company defines the middle-market cohort as those households earning between $75,000 and $125,000 per year and with monthly rental payments of $1,600 to $2,300. These rent levels typically represent approximately 20-25% of household income, which provides each household with meaningful cushion to continue paying rent in times of economic hardship. Conversely, Tricon has the flexibility to increase rents and defray higher operating costs in a stronger economic environment without significantly impacting its residents’ financial well-being. Focusing on qualified middle-market families who are likely to be long-term residents is expected to result in lower turnover rates, thereby reducing turn costs and providing stable cash flows for the Company. Tricon offers its residents economic mobility and the convenience of renting a high-quality, renovated home without costly overhead expenses such as maintenance and property taxes, and with a focus on superior customer service.

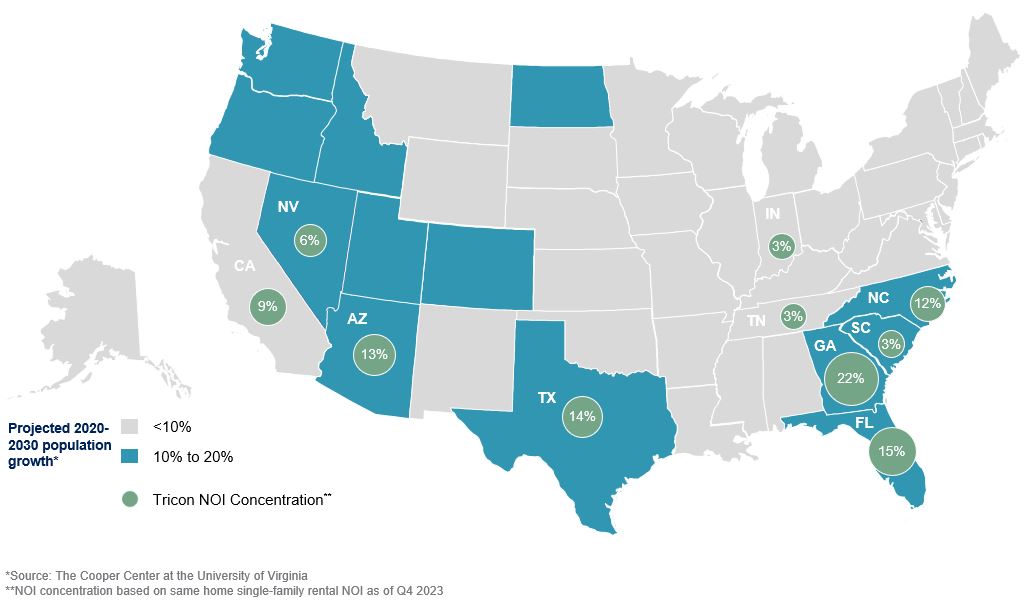

In addition to targeting the middle-market demographic, Tricon is focused on the U.S. Sun Belt, which is home to approximately 40% of all U.S. households and is expected to experience population growth in excess of 10% in most markets from 2020 to 2030 (source: The Cooper Center at the University of Virginia, 2018). The U.S. Sun Belt has experienced significant population and job growth over time, driven by a friendly business environment, lower tax rates, enhanced affordability and a warm climate. The Company expects that the de-urbanization and de-densification trends that were accelerated by the COVID-19 pandemic will continue to support these demographic shifts toward our core markets. Furthermore, the Company believes that work-from-home trends and in-migration to the Sun Belt states will likely continue as employers continue to permit more flexible work arrangements and employees gravitate towards more affordable housing markets.

Tricon is focused on disciplined, long-term growth of its single-family rental home portfolio and has a sophisticated acquisition platform that is capable of deploying large amounts of capital across multiple acquisition channels and markets simultaneously.

In an undersupplied housing market, Tricon also believes in adding to the supply of rental homes and providing accessible housing solutions through its new home growth channels. These include the development of dedicated

Page 6 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

“build-to-rent” communities and the acquisition of both scattered new homes and completed single-family rental communities directly from homebuilders.

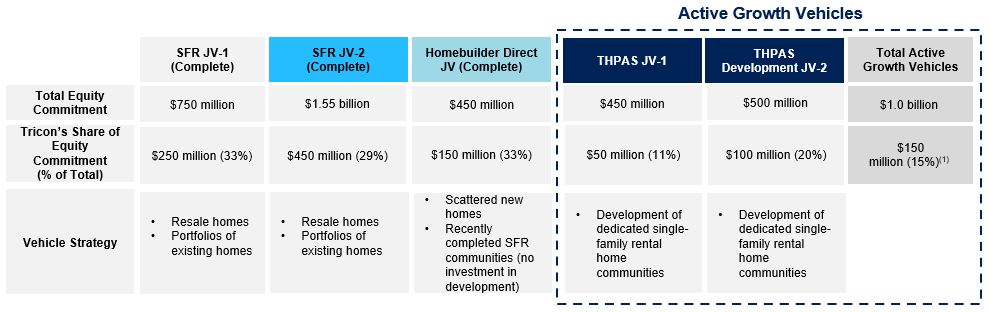

Through its differentiated strategic partnership model, Tricon has demonstrated its ability to raise and deploy third-party capital to accelerate growth, improve operating efficiency, and take development off balance sheet. Partnering with leading global real estate investors, the Company has established complementary single-family rental joint ventures.

(1) As at December 31, 2023, Tricon's unfunded equity commitment to active growth vehicles was approximately $108 million and is expected to be funded over the next two years.

Adjacent residential businesses

Multi-family rental

In Canada, Tricon operates and holds a 20% weighted average ownership interest (based on net asset values) in two Class A rental properties totaling 786 units in downtown Toronto. These properties are managed through Tricon's vertically integrated platform, including local property management employees. Tricon plans to grow the Canadian multi-family rental portfolio as more Class A multi-family rental apartments from the residential development portfolio reach stabilization.

Residential development

Tricon develops new residential real estate properties, predominantly rental housing intended for long-term ownership. Such developments include (i) Class A multi-family rental apartments in Canada, (ii) single-family rental communities in the United States intended to operate as part of the single-family rental portfolio upon stabilization, and (iii) legacy land development and homebuilding projects, predominantly in the United States.

(i) Canadian Class A multi-family rental apartments:

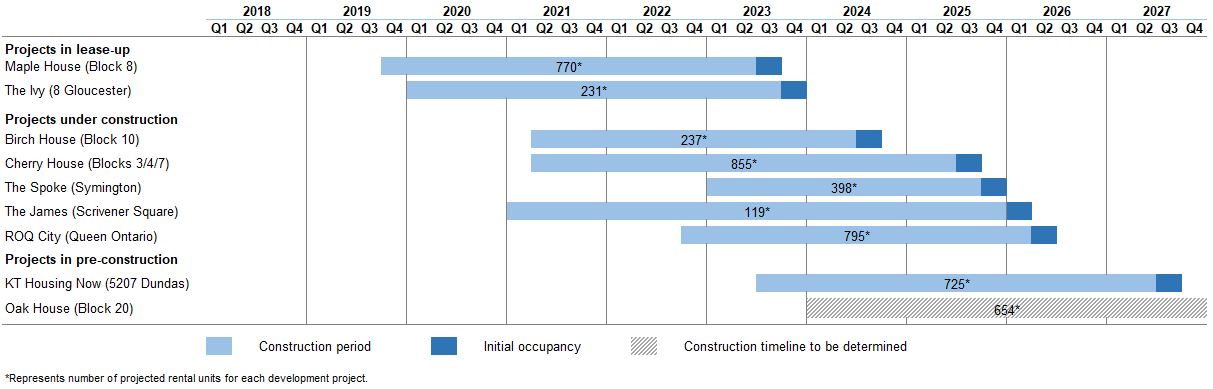

Tricon is one of the most active developers of Class A purpose-built rental apartment buildings in downtown Toronto with seven projects under development and two income-producing properties (Maple House and The Ivy) in the stabilization phase, totaling approximately 4,784 units. Tricon holds a 38% weighted average ownership interest in this portfolio based on net asset values. Tricon holds most of these assets in partnerships with pension plans and strategic partners who have an investment bias towards long-term ownership and stable recurring cash flows. These institutional investors or strategic partners pay Tricon development management fees, asset management fees and possibly performance fees, enabling the Company to enhance its return on investment.

(ii) U.S. single-family rental communities:

The Company's build-to-rent strategy is focused on developing well-designed, dedicated single-family home rental communities, which often include shared amenities such as parks, playgrounds, pools and community gathering spaces. This strategy adds another growth channel to Tricon’s single-family rental business, and leverages the Company’s complementary expertise in land development, homebuilding and single-family rental property

Page 7 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

management. Once developed and stabilized, these build-to-rent communities will be integrated into the Company’s technology-enabled property management platform. The Company currently has a development pipeline of approximately 2,400 rental homes in 16 communities across the U.S. Sun Belt through its THPAS JV-1 and THPAS Development JV-2 Investment Vehicles.

(iii) U.S. land development and homebuilding:

The Company’s legacy business provides equity or equity-type financing to experienced local or regional developers and builders of for-sale housing primarily in the United States. These investments are typically made through Investment Vehicles that hold an interest in land development and homebuilding projects, including master-planned communities ("MPCs"). Tricon also serves as the developer of certain of its MPCs through its Houston-based subsidiary, The Johnson Companies LP (“Johnson”). Johnson is an integrated development platform with expertise in land entitlement, infrastructure, municipal bond finance and placemaking, and has deep relationships with public and regional homebuilders and commercial developers.

Johnson’s reputation for developing high-quality MPCs is further evidenced by Johnson having two MPCs ranked in the top 50 based on homebuilder sales in 2023 according to RCLCO Real Estate Consulting.

Strategic Capital

Tricon earns fees from managing third-party capital invested in its real estate assets through separate accounts, joint ventures and commingled funds ("Investment Vehicles"). Activities of this business include:

(i) Asset management of third-party capital: Tricon manages capital on behalf of institutional investors, including pension funds, sovereign wealth funds, insurance companies and others who seek exposure to the residential real estate industry. Tricon managed $8.2 billion of Assets Under Management (“AUM”) on behalf of third-party investors (out of total AUM of $16.3 billion) as at December 31, 2023 across its single-family rental, multi-family rental and residential development business segments (refer to Section 6 and Appendix A for further information concerning the Company's AUM). For its services, Tricon earns asset management fees on fee-bearing capital, which totaled $2.6 billion as at December 31, 2023, and periodically earns performance fees when targeted investment returns are achieved.

Tricon manages third-party capital for 12 of the top 100 largest institutional real estate investors in the world (source: "PERE Global Investor 100" ranking, October 2023). In 2023, Tricon ranked 40th globally and second in Canada (compared to 53rd globally and second in Canada in 2022) among global real estate investment managers based on private capital raised over the past five years (source: "2023 PERE 100" manager ranking, June 2023). Within that ranking, Tricon is the largest investment manager exclusively focused on residential real estate.

(ii) Development management and related advisory services: Tricon earns development management fees from its rental development projects in Toronto, which leverage its fully integrated development team. In addition, Tricon earns contractual development fees and sales commissions from the development and sale of single-family lots, residential land parcels, and commercial land within the MPCs managed by its Johnson subsidiary.

(iii) Property management of rental properties: Tricon provides integrated property management services to its entire rental portfolio. The property management business is headquartered in Orange County, California, and provides resident-facing services including marketing, leasing, and repairs and maintenance delivered through a dedicated call center and local field offices. For its services, Tricon earns property management fees, typically calculated as a set percentage of the gross revenues of each property, as well as leasing, construction and acquisition fees.

1.3 Sustainability

Sustainability principles have guided Tricon's history of delivering business excellence since 1988. Tricon remains focused on the following five strategic sustainability priorities:

Page 8 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

Our People: Tricon is committed to engaging, supporting and enriching the lives of its employees so they can thrive and, in turn, take care of our residents and the communities in which we operate. To align our purpose-driven culture with our sustainability strategy, Tricon focuses on: (i) creating an exceptional employee experience by empowering and enabling employees to unlock their potential, (ii) delivering company-wide professional development opportunities that promote high-performing work teams, and (iii) fostering a culture of diversity, inclusion and belonging to increase cognitive diversity and perspective.

Our Residents: Tricon's goal is to build meaningful communities where people can connect, grow and prosper. In that continued effort, Tricon focuses on: (i) providing residents with high-quality housing and best-in-class resident experience, (ii) delivering Tricon Vantage – a market-leading program aimed at providing its U.S. residents with tools and resources to set financial goals and enhance their long-term economic stability, and (iii) giving back to the communities where we operate through our volunteer services and charitable giving programs.

Our Impact: Tricon is committed to making investments and operational decisions that reduce the environmental impact and enhance the sustainability and resource efficiency of our portfolio. The environmental impact portion of our sustainability program focuses on: (i) developing and implementing sustainable methodologies to ensure our investments, developments and renovation projects adhere to our sustainability objectives and commitments, (ii) investigating and investing in new technologies, materials and renovation methods to reduce resource consumption across our real estate portfolio, and (iii) investigating and investing in the reduction of resource consumption across our property management and corporate office operations.

Our Innovation: Tricon is firmly committed to leveraging innovative technologies and housing solutions to drive convenience, connectivity and affordability. Core service offerings are guided by two key desired outcomes: (i) delivering superior service that creates exceptional resident experiences, and (ii) developing offerings that enhance the lives of residents while addressing their housing needs.

Our Governance: Tricon aims to proactively identify, understand and manage the risks to our business while acting in a manner that exemplifies our commitment to ethics, integrity, trust and transparency. Tricon’s sustainability program focuses on the following governance initiatives: (i) maintaining a culture of compliance, integrity and ethics, (ii) embedding a strong risk management culture by setting a foundation for effectively identifying, analyzing and managing material and systemic risks, and (iii) maintaining a diverse Board of Directors composition, in which either gender is represented by one-third of all directors.

Tricon's next annual sustainability report is slated for publication in the spring of 2024. Details of our key sustainability commitments, initiatives, policies and reported performance progress can be found on the Company's website under Sustainability.

Page 9 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

2. Highlights

The following section presents highlights for the quarter on a consolidated and proportionate basis.

On October 18, 2022, the Company sold its remaining 20% equity interest in its U.S. multi-family rental portfolio, held through Tricon US Multi-Family REIT LLC. In accordance with IFRS 5, Non-current Assets Held for Sale and Discontinued Operations, the Company reclassified the prior-period results and cash flows of Tricon US Multi-Family REIT LLC as discontinued operations separate from the Company's continuing operations.

Core funds from operations ("Core FFO"), Core FFO per share, Adjusted funds from operations ("AFFO"), and AFFO per share are non-IFRS financial measures and non-IFRS ratios as identified in Section 6. The Company uses guidance specified by the National Association of Real Estate Investment Trusts ("NAREIT") to calculate FFO, upon which Core FFO and AFFO are based. The measures are presented on a proportionate basis, reflecting only the portion attributable to Tricon's shareholders based on the Company's ownership percentage of the underlying entities and excludes the percentage associated with non-controlling and limited partners' interests. The Company believes that providing FFO, Core FFO and AFFO on a proportionate basis is helpful to investors in assessing the overall performance of the Company’s business. Note that FFO, Core FFO, Core FFO per share, AFFO and AFFO per share are not meant to be used in measuring the Company's liquidity. See “Non-IFRS measures” on page 1 and Appendix A for a reconciliation to the most directly comparable IFRS measures.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||

| (in thousands of U.S. dollars, except per share amounts which are in U.S. dollars, unless otherwise indicated) | 2023 | 2022 | 2023 | 2022 | |||||||||||||

| Financial highlights on a consolidated basis | |||||||||||||||||

| Net (loss) income from continuing operations, including: | $ | (35,470) | $ | 55,883 | $ | 121,824 | $ | 779,374 | |||||||||

| Fair value gain on rental properties | 2,029 | 56,414 | 210,936 | 858,987 | |||||||||||||

| Basic (loss) earnings per share attributable to shareholders of Tricon from continuing operations | (0.14) | 0.19 | 0.42 | 2.82 | |||||||||||||

| Diluted (loss) earnings per share attributable to shareholders of Tricon from continuing operations | (0.14) | 0.11 | 0.41 | 1.98 | |||||||||||||

| Net income from discontinued operations | — | 1,829 | — | 35,106 | |||||||||||||

| Basic earnings per share attributable to shareholders of Tricon from discontinued operations | — | 0.01 | — | 0.13 | |||||||||||||

| Diluted earnings per share attributable to shareholders of Tricon from discontinued operations | — | 0.01 | — | 0.11 | |||||||||||||

| Dividends per share | $ | 0.058 | $ | 0.058 | $ | 0.232 | $ | 0.232 | |||||||||

| Weighted average shares outstanding - basic | 273,847,034 | 274,684,779 | 273,657,451 | 274,483,264 | |||||||||||||

| Weighted average shares outstanding - diluted | 275,664,083 | 311,222,080 | 275,543,799 | 311,100,493 | |||||||||||||

Non-IFRS(1) measures on a proportionate basis | |||||||||||||||||

| Core funds from operations ("Core FFO") | $ | 45,651 | $ | 96,841 | $ | 172,597 | $ | 237,288 | |||||||||

| Adjusted funds from operations ("AFFO") | 38,159 | 88,694 | 139,110 | 198,264 | |||||||||||||

Core FFO per share(2) | 0.15 | 0.31 | 0.56 | 0.76 | |||||||||||||

AFFO per share(2) | 0.12 | 0.28 | 0.45 | 0.64 | |||||||||||||

| Select balance sheet items reported on a consolidated basis | December 31, 2023 | December 31, 2022 | |||||||||||||||

| Total assets | $ | 13,248,425 | $ | 12,450,946 | |||||||||||||

Total liabilities(3) | 9,378,884 | 8,653,921 | |||||||||||||||

| Net assets attributable to shareholders of Tricon | 3,863,764 | 3,790,249 | |||||||||||||||

| Rental properties | 12,190,792 | 11,445,659 | |||||||||||||||

| Debt | 5,778,000 | 5,728,184 | |||||||||||||||

(1) Non-IFRS measures are presented to illustrate alternative relevant measures to assess the Company's performance. Refer to “Non-IFRS measures” on page 1 and Appendix A.

Page 10 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

(2) Core FFO per share and AFFO per share are calculated using the total number of weighted average potential dilutive shares outstanding, including the assumed conversion of convertible debentures and exchange of preferred units issued by Tricon PIPE LLC, which were 310,408,201 and 310,287,917 for the three and twelve months ended December 31, 2023, respectively, and 311,222,080 and 311,100,493 for the three and twelve months ended December 31, 2022, respectively.

(3) Includes limited partners' interests in SFR JV-1, SFR JV-HD and SFR JV-2.

IFRS measures on a consolidated basis

Net loss from continuing operations in the fourth quarter of 2023 was $35.5 million compared to net income of $55.9 million in the fourth quarter of 2022, and included:

•Fair value gain on rental properties of $2.0 million compared to $56.4 million in the fourth quarter of 2022, attributable to a moderation in home price appreciation within the single-family rental portfolio. This moderation is attributed to persistently higher mortgage rates and ongoing economic uncertainty which have introduced a level of caution among homebuyers.

•Fair value loss of $23.2 million on derivative financial instruments compared to a gain of $25.8 million in the fourth quarter of 2022, and foreign exchange loss of $13.9 million compared to $0.2 million in the prior year period. The fair value loss on derivative financial instruments was primarily driven by an unrealized loss on the exchange and redemption options associated with the preferred units issued by Tricon PIPE LLC, correlated with an increase in Tricon's share price.

•Revenue from single-family rental properties increased by 14.3% to $206.8 million from $180.9 million in the fourth quarter of 2022, driven primarily by growth of 3.6% in the single-family rental portfolio to 37,183 homes, a 5.2% year-over-year increase in average effective monthly rent (from $1,785 to $1,877) and a 3.2% increase in total portfolio occupancy to 95.0%.

•Direct operating expenses increased by 15.7% to $67.5 million from $58.4 million in the fourth quarter of 2022, primarily reflecting an expansion in the rental portfolio and higher property tax expenses associated with increasing property value assessments, as well as general cost and labor market inflationary pressures.

•Revenue from strategic capital services (previously reported as Revenue from private funds and advisory services) of $19.6 million compared to $14.8 million in the fourth quarter of 2022, primarily attributable to a $6.2 million increase in performance fees earned from the U.S. residential development portfolio, partially offset by a decrease in property management and asset management fees following the Company's sale of the U.S. multi-family rental portfolio in October 2022.

•Interest expense of $80.3 million compared to $71.1 million in the fourth quarter of 2022, attributable to a 0.12% increase in the weighted average interest rate, driven by elevated benchmark interest rates, in addition to an increase in the outstanding debt balance ($5.8 billion as at December 31, 2023 compared to $5.7 billion as at December 31, 2022).

Net income from continuing operations for the year ended December 31, 2023 was $121.8 million compared to $779.4 million for the year ended December 31, 2022, and included:

•Fair value gain on rental properties of $210.9 million compared to $859.0 million in the prior year for the same reasons discussed above.

•Revenue from single-family rental properties of $795.3 million and direct operating expenses of $261.9 million compared to $645.6 million and $209.1 million in the prior year, respectively, which translated to a net operating income ("NOI") increase of $96.9 million, attributable to the continued expansion of the single-family rental portfolio and strong rent growth.

•Revenue from strategic capital services of $54.5 million compared to $160.1 million in the prior year, primarily attributable to $99.9 million of performance fees earned from the sale of Tricon’s remaining 20% equity interest in the U.S. multi-family rental portfolio in October 2022.

Page 11 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

•Interest expense of $316.5 million compared to $213.9 million in the prior year, primarily attributable to a 0.74% increase in the weighted average interest rate, as discussed above, in addition to a 14.4% increase in the average outstanding debt balance throughout the year.

Non-IFRS measures on a proportionate basis

Core FFO for the fourth quarter of 2023 was $45.7 million, a decrease of $51.2 million or 53% compared to $96.8 million in the fourth quarter of 2022. The change was driven by a net Core FFO impact of $50.3 million, net of LTIP and performance fee expense paid, that was recognized in the fourth quarter of 2022 with respect to the sale of Tricon's remaining 20% equity interest in the U.S. multi-family rental portfolio. While the NOI growth in the SFR business in the fourth quarter was offset by higher borrowing costs, continued stronger performance from U.S. residential developments contributed positively to the Core FFO. During the twelve months ended December 31, 2023, Core FFO decreased by $64.7 million or 27% to $172.6 million compared to $237.3 million in the prior year, for the reasons noted above.

AFFO for the three and twelve months ended December 31, 2023 was $38.2 million and $139.1 million, respectively, a decrease of $50.5 million (57%) and $59.2 million (30%) from the same periods in the prior year. This change in AFFO was driven by the decrease in Core FFO discussed above, partially offset by lower recurring capital expenditures as a result of disciplined cost containment and scoping refinement when turning homes, and the absence of recurring capital expenditures from the U.S. multi-family rental portfolio following its sale.

Page 12 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

3. Consolidated financial results

The following section should be read in conjunction with the Company’s consolidated financial statements and related notes for the three and twelve months ended December 31, 2023.

On October 18, 2022, the Company completed the sale of its remaining 20% equity interest in its U.S. multi-family rental portfolio that was held through Tricon US Multi-Family REIT LLC. Accordingly, the Company reclassified its prior-year results as discontinued operations separate from the Company’s continuing operations in accordance with IFRS 5, Non-current Assets Held for Sale and Discontinued Operations ("IFRS 5").

3.1 Review of income statements

Consolidated statements of income

Page 13 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars, except per share amounts which are in U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Revenue from single-family rental properties | $ | 206,780 | $ | 180,893 | $ | 25,887 | $ | 795,317 | $ | 645,585 | $ | 149,732 | |||||||||||

| Direct operating expenses | (67,529) | (58,371) | (9,158) | (261,936) | (209,089) | (52,847) | |||||||||||||||||

| Net operating income from single-family rental properties | 139,251 | 122,522 | 16,729 | 533,381 | 436,496 | 96,885 | |||||||||||||||||

| Revenue from strategic capital services | 19,627 | 14,820 | 4,807 | 54,458 | 160,088 | (105,630) | |||||||||||||||||

Income from equity-accounted investments in multi-family rental properties(1) | 4,768 | 1,051 | 3,717 | 5,297 | 1,550 | 3,747 | |||||||||||||||||

Income from equity-accounted investments in Canadian residential developments(2) | 1,614 | 7,690 | (6,076) | 4,348 | 11,198 | (6,850) | |||||||||||||||||

Other income(3) | 196 | 2,017 | (1,821) | 518 | 10,886 | (10,368) | |||||||||||||||||

Income from investments in U.S. residential developments(4) | 6,926 | 3,910 | 3,016 | 30,773 | 16,897 | 13,876 | |||||||||||||||||

| Compensation expense | (26,161) | (22,408) | (3,753) | (89,343) | (99,256) | 9,913 | |||||||||||||||||

| Performance fees expense | (1,850) | (3,798) | 1,948 | (2,550) | (35,854) | 33,304 | |||||||||||||||||

| General and administration expense | (26,877) | (18,163) | (8,714) | (86,502) | (58,991) | (27,511) | |||||||||||||||||

| Gain (loss) on debt modification and extinguishment | — | — | — | 1,326 | (6,816) | 8,142 | |||||||||||||||||

| Transaction costs | (3,459) | (7,178) | 3,719 | (16,632) | (18,537) | 1,905 | |||||||||||||||||

| Interest expense | (80,252) | (71,120) | (9,132) | (316,473) | (213,932) | (102,541) | |||||||||||||||||

| Fair value gain on rental properties | 2,029 | 56,414 | (54,385) | 210,936 | 858,987 | (648,051) | |||||||||||||||||

| Fair value loss on Canadian development properties | — | — | — | — | (440) | 440 | |||||||||||||||||

| Realized and unrealized (loss) gain on derivative financial instruments | (23,201) | 25,818 | (49,019) | (2,424) | 184,809 | (187,233) | |||||||||||||||||

| Amortization and depreciation expense | (4,727) | (4,764) | 37 | (17,794) | (15,608) | (2,186) | |||||||||||||||||

| Realized and unrealized foreign exchange (loss) gain | (13,928) | (164) | (13,764) | (13,859) | 498 | (14,357) | |||||||||||||||||

| Net change in fair value of limited partners’ interests in single-family rental business | (26,954) | (50,828) | 23,874 | (145,497) | (297,381) | 151,884 | |||||||||||||||||

| (191,876) | (81,523) | (110,353) | (437,876) | 338,010 | (775,886) | ||||||||||||||||||

| (Loss) income before income taxes from continuing operations | $ | (32,998) | $ | 55,819 | $ | (88,817) | $ | 149,963 | $ | 934,594 | $ | (784,631) | |||||||||||

| Income tax (expense) recovery from continuing operations | (2,472) | 64 | (2,536) | (28,139) | (155,220) | 127,081 | |||||||||||||||||

| Net (loss) income from continuing operations | $ | (35,470) | $ | 55,883 | $ | (91,353) | $ | 121,824 | $ | 779,374 | $ | (657,550) | |||||||||||

| Basic (loss) earnings per share attributable to shareholders of Tricon from continuing operations | (0.14) | 0.19 | (0.33) | 0.42 | 2.82 | (2.40) | |||||||||||||||||

| Diluted (loss) earnings per share attributable to shareholders of Tricon from continuing operations | (0.14) | 0.11 | (0.25) | 0.41 | 1.98 | (1.57) | |||||||||||||||||

| Net income from discontinued operations | — | 1,829 | (1,829) | — | 35,106 | (35,106) | |||||||||||||||||

| Basic earnings per share attributable to shareholders of Tricon from discontinued operations | — | 0.01 | (0.01) | — | 0.13 | (0.13) | |||||||||||||||||

| Diluted earnings per share attributable to shareholders of Tricon from discontinued operations | — | 0.01 | (0.01) | — | 0.11 | (0.11) | |||||||||||||||||

| Weighted average shares outstanding - basic | 273,847,034 | 274,684,779 | (837,745) | 273,657,451 | 274,483,264 | (825,813) | |||||||||||||||||

Weighted average shares outstanding - diluted(5) | 275,664,083 | 311,222,080 | (35,557,997) | 275,543,799 | 311,100,493 | (35,556,694) | |||||||||||||||||

(1) Includes income from The Selby and The Taylor (from October 1, 2023) (Section 4.2.1).

Page 14 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

(2) Includes income from The Taylor (until September 30, 2023), Maple House, Birch House, Cherry House, Oak House, The Ivy, The Spoke, ROQ City and KT Housing Now (Section 4.2.2).

(3) Includes commercial rental income from The Shops of Summerhill (Section 4.2.2) and interest income, partially offset by the inclusion of a net operating loss from non-core single-family rental homes, which were disposed of during the quarter.

(4) Reflects the net change in the fair values of the underlying investments in the build-to-rent and legacy for-sale housing businesses (Section 4.2.2).

(5) For the three and twelve months ended December 31, 2023, the exchangeable preferred units of Tricon PIPE LLC were anti-dilutive (2022 - dilutive). Refer to Note 30 to the Consolidated Financial Statements.

Page 15 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

Revenue from single-family rental properties

The following table provides further details regarding revenue from single-family rental properties for the three and twelve months ended December 31, 2023 and 2022.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

Rental revenue(1) | $ | 196,236 | $ | 172,252 | $ | 23,984 | $ | 755,247 | $ | 610,375 | $ | 144,872 | |||||||||||

Other revenue(1) | 10,544 | 8,641 | 1,903 | 40,070 | 35,210 | 4,860 | |||||||||||||||||

| Revenue from single-family rental properties | $ | 206,780 | $ | 180,893 | $ | 25,887 | $ | 795,317 | $ | 645,585 | $ | 149,732 | |||||||||||

(1) All rental and other revenue is reflected net of bad debt. The Company has reserved 100% of residents’ accounts receivable balances aged more than 30 days, less the amount of residents' security deposits on hand.

Revenue from single-family rental properties for the three months ended December 31, 2023 totaled $206.8 million, an increase of $25.9 million or 14.3% compared to $180.9 million for the same period in the prior year. The increase is attributable to:

•Growth of $24.0 million in rental revenue, driven by portfolio expansion of 3.6% (37,183 rental homes compared to 35,908 at December 31, 2022), and a 5.2% year-over-year increase in average effective monthly rent per home ($1,877 compared to $1,785) attributable to the continued strong demand for single-family rental homes. This strong demand also contributed to a 3.2% increase in occupancy (95.0% compared to 91.8%) notwithstanding the acquisition of 264 vacant homes this quarter.

•An increase of $1.9 million in other revenue driven by portfolio expansion, as well as incremental ancillary revenue from the rollout of the Company's smart-home technology initiative (76% of single-family rental homes were smart-home enabled at December 31, 2023 compared to 69% at December 31, 2022), along with higher resident enrollment in the renters insurance program.

Revenue from single-family rental properties for the twelve months ended December 31, 2023 totaled $795.3 million, an increase of $149.7 million or 23.2% compared to the prior year. This favorable variance was primarily driven by growth of the rental portfolio, an improvement in the average monthly rent, as well as higher other revenue for the reasons discussed above.

Direct operating expenses

The following table provides further details regarding direct operating expenses of the single-family rental portfolio for the three and twelve months ended December 31, 2023 and 2022.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Property taxes | $ | 34,804 | $ | 28,392 | $ | 6,412 | $ | 131,217 | $ | 100,122 | $ | 31,095 | |||||||||||

| Repairs and maintenance | 7,375 | 7,353 | 22 | 30,849 | 29,006 | 1,843 | |||||||||||||||||

| Turnover | 2,459 | 1,881 | 578 | 10,944 | 7,829 | 3,115 | |||||||||||||||||

| Property management expenses | 12,838 | 11,656 | 1,182 | 50,154 | 41,404 | 8,750 | |||||||||||||||||

| Property insurance | 2,298 | 2,029 | 269 | 8,988 | 7,544 | 1,444 | |||||||||||||||||

| Marketing and leasing | 606 | 648 | (42) | 2,300 | 2,554 | (254) | |||||||||||||||||

| Homeowners' association (HOA) costs | 3,638 | 3,449 | 189 | 13,855 | 9,933 | 3,922 | |||||||||||||||||

Other direct expense(1) | 3,511 | 2,963 | 548 | 13,629 | 10,697 | 2,932 | |||||||||||||||||

| Direct operating expenses | $ | 67,529 | $ | 58,371 | $ | 9,158 | $ | 261,936 | $ | 209,089 | $ | 52,847 | |||||||||||

(1) Other direct expense includes property utilities, landscaping costs on vacant homes and other property operating costs associated with ancillary revenue offerings. Utility expenses including water, sewer, waste, gas and electricity, as well as landscaping costs, are borne by the resident when a home is occupied; such expenses are only incurred by Tricon when a home is vacant or is being turned.

Page 16 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

Direct operating expenses for the three months ended December 31, 2023 were $67.5 million, an increase of $9.2 million or 15.7% compared to the same period in the prior year. The variance is primarily attributable to:

•An increase of $6.4 million in property taxes driven by 3.6% growth in the size of the portfolio, as well as a higher property tax expense per home arising from significant year-over-year assessed home value appreciation and tax increases in Tricon's markets.

•An increase of $0.6 million in turnover expense primarily attributable to a higher annualized turnover rate (22.6% in the current period compared to 17.7% in the prior period for the total portfolio) on a larger portfolio of homes which led to an increased volume of work orders, partly offset by effective cost control through scope refinement and higher utilization of in-house maintenance personnel on turn projects.

•An increase of $1.2 million in property management expense as a result of inflationary pressures and a tighter labor market within a larger portfolio. Despite these market conditions, the rise in property management expense for the quarter was contained.

•An increase of $0.5 million in other direct expense resulting from the additional costs of supplying access to smart-home technology in more homes and providing renters insurance to more residents (these costs are offset by higher revenue), as well as increased utility costs on vacant homes from higher rates and a growing portfolio.

Direct operating expenses for the twelve months ended December 31, 2023 were $261.9 million, an increase of $52.8 million or 25.3% compared to the prior year, primarily for the reasons described above as well as a $3.9 million increase in homeowners' association (HOA) costs. The higher HOA costs were driven by growth in the size of the portfolio, with more homes being situated in HOAs as well as increases in annual HOA dues. A heightened level of rule enforcement by HOAs became more prevalent as pandemic-era regulations eased, which also increased violation/penalty fees.

Revenue from strategic capital services (previously reported as Revenue from private funds and advisory services)

The following table provides further details regarding revenue from strategic capital services for the three and twelve months ended December 31, 2023 and 2022, net of inter-segment revenues eliminated upon consolidation.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Asset management fees | $ | 2,862 | $ | 2,977 | $ | (115) | $ | 11,290 | $ | 12,431 | $ | (1,141) | |||||||||||

| Performance fees | 6,225 | — | 6,225 | 10,359 | 110,330 | (99,971) | |||||||||||||||||

| Development fees | 9,962 | 9,753 | 209 | 31,034 | 26,826 | 4,208 | |||||||||||||||||

| Property management fees | 578 | 2,090 | (1,512) | 1,775 | 10,501 | (8,726) | |||||||||||||||||

| Revenue from strategic capital services | $ | 19,627 | $ | 14,820 | $ | 4,807 | $ | 54,458 | $ | 160,088 | $ | (105,630) | |||||||||||

Revenue from strategic capital services for the three months ended December 31, 2023 totaled $19.6 million, an increase of $4.8 million from the same period in the prior year, mainly attributable to:

•An increase of $6.2 million in performance fees earned primarily from the U.S. residential development portfolio, compared to no performance fee recognized in the fourth quarter of 2022. Performance fees are earned by the Company when third-party realized returns exceed set targets within the Investment Vehicles. As such, performance fees are generally episodic in nature and can fluctuate materially on a year-over-year basis.

•A decrease of $1.5 million in property management fees primarily related to loss of revenue of $1.8 million following the Company's sale of the U.S. multi-family rental portfolio in October 2022, partially offset by an increase in property management fees from the Canadian multi-family rental portfolio as additional properties entered the lease-up phase.

Revenue from strategic capital services for the twelve months ended December 31, 2023 totaled $54.5 million, a decrease of $105.6 million from the prior year. This decline was mainly attributable to the $99.9 million in

Page 17 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

performance fees earned in respect of the sale of the Company's remaining 20% equity interest in its U.S. multi-family rental portfolio in 2022, along with a loss of fee income from the portfolio. This was partially offset by an increase of $4.2 million in development fees driven primarily by incentive fees earned as a result of a substantial commercial land bulk sale in Johnson communities in the first quarter of 2023.

Income from equity-accounted investments in multi-family rental properties

Equity-accounted investments in multi-family rental properties include equity holdings in two Class A multi-family rental apartments in Toronto, namely The Selby and The Taylor. The Taylor achieved stabilization on September 30, 2023, and was reclassified from equity-accounted investments in Canadian residential developments to investments in multi-family rental properties in the fourth quarter of 2023.

The following table presents the income from equity-accounted investments in multi-family rental properties for the three and twelve months ended December 31, 2023 and 2022.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Income from equity-accounted investments in multi-family rental properties | $ | 4,768 | $ | 1,051 | $ | 3,717 | $ | 5,297 | $ | 1,550 | $ | 3,747 | |||||||||||

Income from equity-accounted investments in multi-family rental properties for the three months ended December 31, 2023 was $4.8 million, a $3.7 million increase from the same period in the prior year. The variance was primarily driven by a fair value gain recognized at The Taylor in the fourth quarter of 2023, which, in the comparative period, was classified within equity-accounted investments in Canadian residential developments.

Income from equity-accounted investments in multi-family rental properties for the twelve months ended December 31, 2023 was $5.3 million, an increase of $3.7 million compared to the prior year, for the reason discussed above.

Income from equity-accounted investments in Canadian residential developments

Equity-accounted investments in Canadian residential developments include joint ventures and equity holdings in development projects, namely Maple House, Birch House, Cherry House, Oak House, The Ivy, ROQ City, The Spoke and KT Housing Now. The James and The Shops of Summerhill are accounted for as Canadian development properties. The income earned from The Shops of Summerhill is presented as other income.

The following table presents the income from equity-accounted investments in Canadian residential developments for the three and twelve months ended December 31, 2023 and 2022.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Income from equity-accounted investments in Canadian residential developments | $ | 1,614 | $ | 7,690 | $ | (6,076) | $ | 4,348 | $ | 11,198 | $ | (6,850) | |||||||||||

Income from equity-accounted investments in Canadian residential developments for the three months ended December 31, 2023 was $1.6 million, a decrease of $6.1 million from the same period in the prior year. The decrease is mainly attributable to lower fair value gains recognized during the period and the absence of income from The Taylor as the property was reclassified to investments in multi-family rental properties at the beginning of the fourth quarter of 2023. In the comparative period, higher fair value gains, including those from The Taylor, were recognized across the portfolio due to increases in land value and the achievement of development milestones.

Income from investments in Canadian residential developments for the twelve months ended December 31, 2023 was $4.3 million, which decreased by $6.9 million compared to the prior year, primarily attributable to the reasons discussed above.

Page 18 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

Income from investments in U.S. residential developments

The following table presents income from investments in U.S. residential developments for the three and twelve months ended December 31, 2023 and 2022.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Income from investments in U.S. residential developments | $ | 6,926 | $ | 3,910 | $ | 3,016 | $ | 30,773 | $ | 16,897 | $ | 13,876 | |||||||||||

Income from investments in U.S. residential developments for the three months ended December 31, 2023 was $6.9 million, an increase of $3.0 million from the same period in the prior year. The increase was primarily driven by strong demand for new housing, bolstered by builders offering customer incentives to maintain a healthy sales velocity despite escalating mortgage rates.

Income from investments in U.S. residential developments for the twelve months ended December 31, 2023 was $30.8 million, an increase of $13.9 million from the same period in the prior year. This year-over-year increase is attributable to the same reasons mentioned above.

Management continues to monitor the macroeconomic factors that are fundamental to the for-sale housing market, including higher mortgage rates, which could impact consumer demand and pricing, development timelines as well as new for-sale housing supply.

Compensation expense

The following table provides further details regarding compensation expense for the three and twelve months ended December 31, 2023 and 2022.

| For the periods ended December 31 | Three months | Twelve months | ||||||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | ||||||||||||||||||||

| Salaries, benefits and bonus | A | $ | 11,524 | $ | 14,106 | $ | (2,582) | $ | 53,672 | $ | 55,040 | $ | (1,368) | |||||||||||||

Cash-based(1) | 4,090 | 3,990 | 100 | 12,519 | 20,307 | (7,788) | ||||||||||||||||||||

| Equity-based | 6,201 | 1,364 | 4,837 | 16,183 | 6,894 | 9,289 | ||||||||||||||||||||

| Annual incentive plan ("AIP") | B | 10,291 | 5,354 | 4,937 | 28,702 | 27,201 | 1,501 | |||||||||||||||||||

| Cash-based | 4,346 | 3,047 | 1,299 | 6,969 | 16,635 | (9,666) | ||||||||||||||||||||

| Equity-based | — | (99) | 99 | — | 380 | (380) | ||||||||||||||||||||

| Long-term incentive plan ("LTIP") | C | 4,346 | 2,948 | 1,398 | 6,969 | 17,015 | (10,046) | |||||||||||||||||||

| Total compensation expense | A+B+C | $ | 26,161 | $ | 22,408 | $ | 3,753 | $ | 89,343 | $ | 99,256 | $ | (9,913) | |||||||||||||

(1) The cash-based AIP figure for the year ended December 31, 2022 includes one-time allocations for special awards.

Compensation expense for the three months ended December 31, 2023 was $26.2 million, an increase of $3.8 million or 16.7% compared to the same period in the prior year. The variance is attributable to:

•An increase of $4.9 million in AIP expense, primarily attributable to a $4.8 million increase in equity-based AIP expense in the current year. The closing of the Go-Private Transaction (see section 3.3) will result in the acceleration of vesting for outstanding equity-based awards that have not yet fully vested. This accelerated vesting led to increased expenses recognized in the current period. All outstanding equity-based awards will be fully vested by the completion date of the Go-Private Transaction.

•An increase of $1.4 million in LTIP expense, reflecting the higher performance fee income generated from the U.S residential development Investment Vehicles.

Page 19 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

•An offsetting decrease in salaries and benefits of $2.6 million, primarily driven by a reduction in the 2023 bonus pool and a 4% decrease in headcount compared to the prior period.

Compensation expense for the twelve months ended December 31, 2023 was $89.3 million, a decrease of $9.9 million or 10.0% compared to the prior year. The variance is attributable to:

•A decrease of $10.0 million in LTIP expense, driven by a smaller increase in unrealized carried interest as a result of lower fair value gains of underlying Investment Vehicles compared to the prior period. In addition, the comparative period also included the accrual of performance fees payable related to the U.S. multi-family rental Investment Vehicle which was sold in October 2022.

•A decrease of $1.4 million in salaries and benefits for the same reason discussed above.

•An offsetting increase of $1.5 million in AIP expense, which included an increase of $9.3 million in equity-based AIP expense, countered by a reduction of $7.8 million in cash-based AIP expense. The increase in equity-based AIP expense was driven by the impact of accelerated vesting, as discussed earlier, and the revaluation of the performance share units liability based on a higher price for the Company's common shares as at year-end. The decrease in cash-based AIP expense was driven by a reduction in the AIP pool for the current year.

Performance fees expense

Performance fees expense reflects amounts that are expected to be paid to key management equity participants who have an equity interest in entities that earn performance fee revenue, whereas LTIP participants do not have said equity interests. In aggregate, cash-based LTIP expense and performance fees expense represent no more than 50% of the performance fees earned from each Investment Vehicle and both are paid to participants if and when the performance fees are in fact realized and paid.

The following table presents performance fees expense for the three and twelve months ended December 31, 2023 and 2022.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Performance fees expense | $ | 1,850 | $ | 3,798 | $ | (1,948) | $ | 2,550 | $ | 35,854 | $ | (33,304) | |||||||||||

Performance fees expense for the three months ended December 31, 2023 was $1.9 million, a decrease of $1.9 million compared to the same period of the prior year, driven by a smaller increase in unrealized carried interest during the current period as a result of lower fair value gains of underlying Investment Vehicles.

Performance fees expense for the twelve months ended December 31, 2023 was $2.6 million, a decrease of $33.3 million compared to the prior period, for the same reason described above. In addition, the U.S. multi-family rental Investment Vehicle was disposed of in the fourth quarter of 2022 and generated significant performance fees in the prior year.

Page 20 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

General and administration expense

The following table presents general and administration expense for the three and twelve months ended December 31, 2023 and 2022.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| General and administration expense | $ | 26,877 | $ | 18,163 | $ | 8,714 | $ | 86,502 | $ | 58,991 | $ | 27,511 | |||||||||||

General and administration expense for the three months ended December 31, 2023 was $26.9 million, an increase of $8.7 million compared to the same period in the prior year. This increase was primarily attributable to a substantial investment in an enterprise resource planning system implementation, which commenced on January 1, 2023, and continued throughout the year with ongoing enhancements. This major technology upgrade aims to enhance operating efficiency and streamline various business processes.

General and administration expense for the twelve months ended December 31, 2023 was $86.5 million, an increase of $27.5 million compared to the prior year. This increase primarily resulted from one-time expenses, notably the substantial investment in the new enterprise resource planning system mentioned previously, significant upgrades to the Company's technology-enabled operating platform, and SOX-compliance consulting expenses.

Interest expense

The following table provides details regarding interest expense for the three and twelve months ended December 31, 2023 and 2022 by borrowing type and nature.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Corporate borrowings | $ | 4,999 | $ | 1,192 | $ | 3,807 | $ | 13,705 | $ | 6,779 | $ | 6,926 | |||||||||||

| Property-level borrowings | 64,370 | 60,102 | 4,268 | 261,306 | 170,847 | 90,459 | |||||||||||||||||

| Due to Affiliate | 4,245 | 4,245 | — | 16,981 | 17,022 | (41) | |||||||||||||||||

| Amortization of deferred financing costs, discounts and lease obligations | 6,638 | 5,581 | 1,057 | 24,481 | 19,284 | 5,197 | |||||||||||||||||

| Total interest expense | $ | 80,252 | $ | 71,120 | $ | 9,132 | $ | 316,473 | $ | 213,932 | $ | 102,541 | |||||||||||

Weighted average interest rate(1) | 4.23 | % | 3.49 | % | 0.74 | % | |||||||||||||||||

(1) The weighted average effective interest rates are calculated based on the average debt balances and the average applicable reference rates for the twelve months ended December 31, 2023.

Interest expense was $80.3 million for the three months ended December 31, 2023, an increase of $9.1 million compared to $71.1 million for the same period last year. The variance is primarily attributable to an increase of $4.3 million in interest expense on property-level borrowings and $3.8 million in interest expense on corporate borrowings. These increases were driven by a 0.12% increase in the weighted average interest rate applicable to the Company’s debt in the current period compared to the same period in the prior year, resulting from higher benchmark interest rates, in addition to an increase in the outstanding balance on the corporate credit facility.

Interest expense was $316.5 million for the twelve months ended December 31, 2023, an increase of $102.5 million compared to $213.9 million in the prior period. The variance is primarily attributable to the year-over-year increase in average property-level and corporate borrowings and increased interest rates, as discussed above.

Fair value gain on rental properties

The following table presents the fair value gain on rental properties held by the Company for the three and twelve months ended December 31, 2023 and 2022.

Page 21 of 65 | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2023 | ||||

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Fair value gain on rental properties | $ | 2,029 | $ | 56,414 | $ | (54,385) | $ | 210,936 | $ | 858,987 | $ | (648,051) | |||||||||||

Fair value gain on single-family rental properties was $2.0 million for the three months ended December 31, 2023, compared to $56.4 million for the same period last year. For the twelve months ended December 31, 2023, the fair value gain totaled $210.9 million, compared to $859.0 million for the prior year. The fair value of single-family rental homes is determined based on comparable sales, primarily by using the adjusted Home Price Index (“HPI”) methodology and periodically Broker Price Opinions (“BPOs”), where applicable. Refer to Note 6 in the consolidated financial statements for further details.

Home values in the U.S. Sun Belt markets have increased over the past several years driven by a number of factors, including strong population and job growth, an acceleration of migration trends driven by the pandemic, historically low mortgage rates during 2020 and 2021, and an overall shortage of new housing supply. However, higher mortgage rates and rising economic uncertainty beginning in the second half of 2022 led to a deceleration in home price growth and in some cases, a decline in certain markets over the course of 2022 and into 2023. While home prices in Tricon's markets improved throughout the year, mainly as a result of improved consumer confidence and a continued shortage of housing supply, there has been a discernible decrease in home buying activity and the pace of home price appreciation remains below that in the comparative period. Adjusted HPI growth in the quarter was 0.3%, net of capital expenditures, compared to 0.7% in the same period in the prior year. The combination of adjusted HPI and BPOs resulted in lower fair value gains in the current period. Adjusted HPI growth for the year was 2.8%, net of capital expenditures, compared to 12.3% in the prior year, driving lower fair value gains in the current year.

Realized and unrealized (loss) gain on derivative financial instruments

The following table presents the realized and unrealized (loss) gain on derivative financial instruments for the three and twelve months ended December 31, 2023 and 2022.

| For the periods ended December 31 | Three months | Twelve months | |||||||||||||||||||||

| (in thousands of U.S. dollars) | 2023 | 2022 | Variance | 2023 | 2022 | Variance | |||||||||||||||||

| Realized and unrealized (loss) gain on derivative financial instruments | $ | (23,201) | $ | 25,818 | $ | (49,019) | $ | (2,424) | $ | 184,809 | $ | (187,233) | |||||||||||