Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS OF EDGEWATER BANK

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-191125

PROSPECTUS

(Proposed Holding Company for Edgewater Bank)

Up to 897,000 shares of Common Stock

(Subject to Increase to up to 1,031,550 shares)

Edgewater Bancorp, Inc., a Maryland corporation and the proposed holding company for Edgewater Bank, is offering shares of common stock for sale at $10.00 per share in connection with the conversion of Edgewater Bank from the mutual to the stock form of organization. There is currently no established market for our common stock. We expect that our common stock will be quoted on the OTC Bulletin Board upon conclusion of the stock offering. We are an "emerging growth company" as defined in the Jumpstart Our Business Startups Act of 2012.

We are offering up to 897,000 shares of common stock for sale at a price of $10.00 per share on a best efforts basis. We may sell up to 1,031,550 shares of common stock because of demand for the shares of common stock or changes in market conditions, without resoliciting subscribers. We must sell a minimum of 663,000 shares in order to complete the offering.

We are offering the shares of common stock in a "subscription offering" to eligible current and former depositors of Edgewater Bank. Shares of common stock not purchased in the subscription offering may be offered for sale to the public in a "community offering," with a preference given to natural persons and trusts of natural persons residing in Berrien, Van Buren and Cass Counties, Michigan. We also may offer for sale shares of common stock not purchased in the subscription offering or community offering to the general public through a "syndicated community offering" managed by Sterne, Agee & Leach, Inc.

The minimum number of shares of common stock you may order is 25 shares. The maximum number of shares of common stock that can be ordered by any person in the offering is 10,000 shares ($100,000), and no person, together with an associate or group of persons acting in concert, may purchase more than 20,000 shares ($200,000) in the offering.

The offering is expected to expire at 12:00 p.m., Eastern Time, on December 18, 2013. We may extend this expiration date without notice to you until February 1, 2014. The Office of the Comptroller of the Currency may approve a later date, which may not be beyond December 20, 2015. Once submitted, orders are irrevocable unless the offering is terminated or is extended beyond February 1, 2014, or the number of shares of common stock to be sold is increased to more than 1,031,550 shares or decreased to less than 663,000 shares. If the offering is extended past February 1, 2014, we will resolicit subscribers. You will have the opportunity to confirm, change or cancel your order within a specified period of time. If you do not respond during that period, your stock order will be cancelled and your deposit account withdrawal authorizations will be cancelled or your funds submitted will be returned promptly with interest at 0.10% per annum. If the number of shares to be sold is increased to more than 1,031,550 shares or decreased to less than 663,000 shares, all funds submitted for the purchase of shares of common stock in the offering will be returned promptly with interest at 0.10% per annum. All subscribers will be resolicited and given an opportunity to place a new order within a specified period of time. Funds received in the subscription and the community offerings and, if applicable, the syndicated community offering will be held in a segregated account at Edgewater Bank and will earn interest at 0.10% per annum until completion or termination of the offering.

Sterne, Agee & Leach, Inc. will assist us in selling our shares of common stock on a best efforts basis in the offering. Sterne, Agee & Leach, Inc. is not required to purchase any of the shares of common stock that are being offered for sale.

OFFERING SUMMARY

Price: $10.00 per Share

| | Minimum | Midpoint | Maximum | Adjusted Maximum | ||||

|---|---|---|---|---|---|---|---|---|

Number of shares | 663,000 | 780,000 | 897,000 | 1,031,550 | ||||

Gross offering proceeds | $6,630,000 | $7,800,000 | $8,970,000 | $10,315,500 | ||||

Estimated offering expenses, excluding selling agent commissions | $965,000 | $965,000 | $965,000 | $965,000 | ||||

Selling agent commissions(1) | $335,000 | $335,000 | $335,000 | $335,000 | ||||

Estimated net proceeds | $5,330,000 | $6,500,000 | $7,670,000 | $9,015,500 | ||||

Estimated net proceeds per share | $8.04 | $8.33 | $8.55 | $8.74 | ||||

| ||||||||

- (1)

- Selling agent commissions shown assume that all shares are sold in the subscription and community offerings. The amounts shown include: (i) fees and selling commissions payable by us to Sterne, Agee & Leach, Inc. in connection with the subscription and community offerings equal to $200,000; and (ii) other expenses of the offering payable to Sterne, Agee & Leach, Inc. in the subscription and community offerings of up to $135,000. See "The Conversion and Offering—Marketing and Distribution; Compensation" for information regarding compensation to be received by Sterne, Agee & Leach, Inc. and the other broker-dealers that may participate in a syndicated community offering. If all shares of common stock were sold in a syndicated community offering, the maximum selling agent commissions would be 6.0% of the aggregate offering dollar amount of all shares sold in the syndicated community offering (net of shares purchased by our directors and executive officers and shares purchased by our employee stock ownership plan), or approximately $311,976, $376,560, $441,144 and $515,416 at the minimum, midpoint, maximum, and adjusted maximum levels of the offering, respectively.

This investment involves a degree of risk, including the possible loss of principal.

Please read "Risk Factors" beginning on page 18.

These securities are not deposits or accounts and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. None of the Securities and Exchange Commission, the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System or any state securities regulator has approved or disapproved of these securities or determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

Sterne Agee

For assistance, please contact the Stock Information Center, toll-free, at (800) 979-4568.

The date of this prospectus is November 12, 2013.

| | Page | |||

|---|---|---|---|---|

SUMMARY | 1 | |||

RISK FACTORS | 18 | |||

SELECTED FINANCIAL AND OTHER DATA OF EDGEWATER BANK | 37 | |||

RECENT DEVELOPMENTS | 39 | |||

FORWARD-LOOKING STATEMENTS | 52 | |||

HOW WE INTEND TO USE THE PROCEEDS FROM THE OFFERING | 54 | |||

OUR DIVIDEND POLICY | 56 | |||

MARKET FOR THE COMMON STOCK | 57 | |||

HISTORICAL AND PRO FORMA REGULATORY CAPITAL COMPLIANCE | 58 | |||

CAPITALIZATION | 59 | |||

PRO FORMA DATA | 60 | |||

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 65 | |||

BUSINESS OF EDGEWATER BANCORP, INC. | 89 | |||

BUSINESS OF EDGEWATER BANK | 90 | |||

REGULATION AND SUPERVISION | 123 | |||

TAXATION | 135 | |||

MANAGEMENT | 136 | |||

SUBSCRIPTIONS BY DIRECTORS AND EXECUTIVE OFFICERS | 151 | |||

THE CONVERSION AND OFFERING | 152 | |||

RESTRICTIONS ON ACQUISITION OF EDGEWATER BANCORP, INC. | 174 | |||

DESCRIPTION OF CAPITAL STOCK OF EDGEWATER BANCORP, INC. | 180 | |||

TRANSFER AGENT | 181 | |||

EXPERTS | 181 | |||

LEGAL MATTERS | 181 | |||

WHERE YOU CAN FIND ADDITIONAL INFORMATION | 182 | |||

INDEX TO FINANCIAL STATEMENTS OF EDGEWATER BANK | F-1 | |||

i

The following summary explains the significant aspects of Edgewater Bank's mutual-to-stock conversion and the related offering of Edgewater Bancorp, Inc. common stock. It may not contain all of the information that is important to you. For additional information before making an investment decision, you should read this entire document carefully, including the financial statements and the notes to the financial statements, and the section entitled "Risk Factors."

In this prospectus, the terms "we," "our," and "us" refer to Edgewater Bancorp, Inc. and Edgewater Bank, unless the context indicates another meaning. In addition, we sometimes refer to Edgewater Bancorp, Inc. as "Edgewater Bancorp," and to Edgewater Bank as the "Bank."

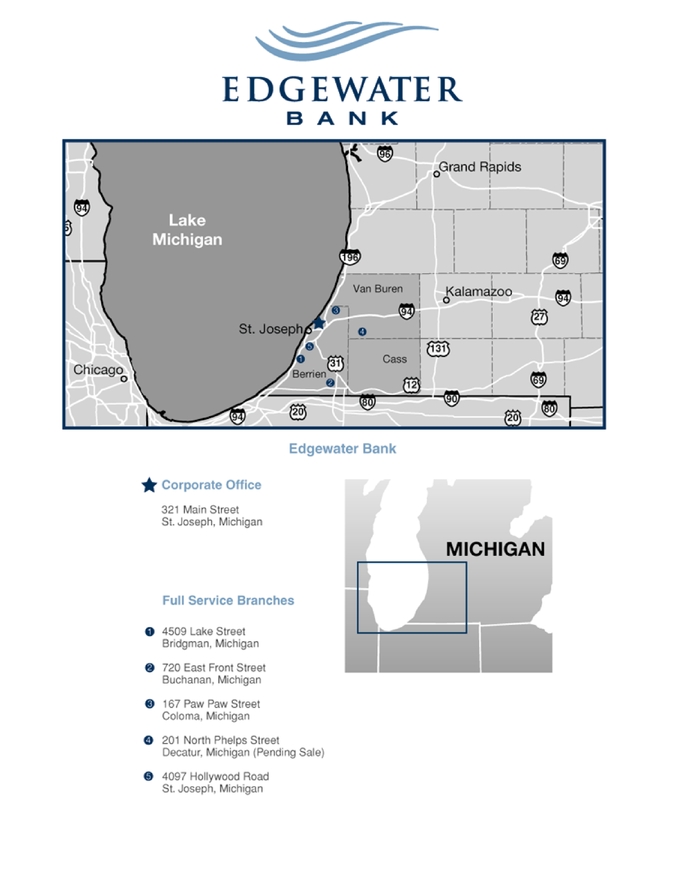

Edgewater Bank

Edgewater Bank is a federal mutual savings association that was originally organized in 1910 as a state-chartered mutual savings and loan association under the name Industrial Building and Loan. In 1938, the Bank converted to a federal charter and changed its name to Buchanan Federal Savings and Loan Association. The Bank changed its name in 1965 to LaSalle Federal Savings and Loan Association of Buchanan and in 1989 to LaSalle Federal Savings Bank. The Bank changed its name to Edgewater Bank in 2005. We conduct our operations from our main office in St. Joseph, Michigan and our five additional full-service banking offices located in Royalton Township, Coloma, Bridgman, Buchanan and Decatur, Michigan. Our primary market area includes Berrien County, Van Buren County, and, to a lesser extent, Cass County, Michigan, all of which are located in southwestern Michigan near the border of Indiana, and portions of northern Indiana that are contiguous with Berrien and Cass Counties.

We have entered into an agreement to sell our Decatur office to a third party, and we expect to complete this sale by the end of 2013. In connection with the sale of the Decatur office, our deposits are expected to decrease by approximately $15.2 million, including $9.7 million of core deposits (which we define to include demand deposit, money market and savings accounts) and $5.5 million of certificates of deposit, based on our deposits at June 30, 2013. We will retain all loans associated with the Decatur office. We intend to fund the assumption of deposits by the purchaser with cash on hand and approximately $10.0 million of advances from the Federal Home Loan Bank of Indianapolis ("FHLB-Indianapolis").

Our business consists primarily of taking deposits from the general public and investing those deposits, together with funds generated from operations, in one- to four-family residential real estate, commercial and industrial, and commercial real estate loans, and, to a lesser extent, home equity lines of credit and other consumer loans. At June 30, 2013, $43.5 million, or 51.0% of our total loan portfolio, was comprised of one- to four-family residential real estate loans. We also invest in securities, which consist primarily of U.S. government agency obligations and mortgage-backed securities and to a lesser extent, state and municipal securities and collateralized mortgage obligations. We offer a variety of deposit accounts, including checking accounts, NOW accounts, savings accounts, money market accounts and certificate of deposit accounts. We utilize advances from the FHLB-Indianapolis for asset/liability management purposes and, to a much lesser extent, for additional funding for our operations. At June 30, 2013, we had $1.0 million in advances outstanding with FHLB-Indianapolis.

Edgewater Bank is subject to comprehensive regulation and examination by its primary federal regulator, the Office of the Comptroller of the Currency ("OCC").

Our executive and administrative office is located at 321 Main Street, St. Joseph, Michigan 49085, and our telephone number at this address is (269) 982-4175. Our website address is www.edgewaterbank.com. Information on our website is not incorporated into this prospectus and should not be considered part of this prospectus.

Legacy Loan Losses

Prior to 2009, our previous management team engaged in significant non-owner occupied commercial real estate and speculative construction and land development lending, and relied on inadequate underwriting processes and controls in extending credit. In addition, weak economic conditions and ongoing strains in the financial and housing markets beginning in 2008 in many portions of the United States, including our market area, contributed to a challenging environment for financial institutions. Due to these adverse conditions, our market area has experienced substantial declines in home prices, historically low levels of existing home sale activity, high levels of foreclosures and high levels of unemployment.

As a result of the economic conditions and loan origination practices by our previous management team, Edgewater Bank experienced unusually high levels of classified loans and charge-offs, particularly in speculative construction and land development loans. As a result, in October 2009, Edgewater Bank entered into a Cease and Desist Order (the "Order") with the Office of Thrift Supervision. The Order required Edgewater Bank to, among other things, implement and file a loan portfolio management plan (to provide for the timely identification of problem loans as well as procedures to ensure conformity with loan approval, collateral documentation, credit information and analysis and risk assessment requirements); a problem assets plan (to provide for the reduction of classified assets); and a business plan (to provide for increases in earnings and capital levels). The Order was terminated in February 2012.

Our efforts to comply with the Order, particularly the resolution of problem assets, resulted in declining levels of capital. As a result of declining capital levels and our continuing high levels of classified assets, on January 23, 2013, the OCC notified Edgewater Bank that the OCC had established an individual minimum capital requirement ("IMCR"). The IMCR requires Edgewater Bank to maintain a tier 1 leverage capital ratio of 8.00% and a total risk-based capital ratio of 12.00% beginning March 31, 2013. At September 30, 2013, Edgewater Bank's tier 1 leverage capital ratio was 8.18% and its total risk-based capital ratio was 14.44%, and Edgewater Bank has been in compliance with the IMCR at all times since its issuance. Assuming completion of the offering at the minimum of the offering range and the contribution to Edgewater Bank of $4.3 million, and Edgewater Bank's planned payment of $1.65 million of expenses related to the withdrawal from a defined benefit plan, Edgewater Bank's tier 1 leverage capital ratio and total risk-based capital ratio would have been 9.51% and 16.80%, respectively, at September 30, 2013, both significantly in excess of the requirements of the IMCR.

New Management Team

Our current executive management team is comprised of individuals with strong commercial banking backgrounds who have joined Edgewater Bank since 2009. In 2009, we hired Richard E. Dyer as our President and Chief Executive Officer to replace our former chairman and chief executive officer and our former president. Mr. Dyer has 33 years of banking experience, specifically as a community bank chief executive officer and in the areas of troubled institution management, problem asset resolution and commercial and industrial lending. In addition, Mr. Dyer is a native of St. Joseph, and has familiarity with and significant business contacts in our market area. We recently also hired Coleen S. Frens-Rossman as Senior Vice President and Chief Financial Officer. Ms. Frens-Rossman has over 27 years of experience managing the accounting and financial reporting of financial institutions. In addition, we recently hired Maria Kibler as Vice President and Senior Retail Officer. Ms. Kibler has over 30 years of retail banking experience, almost exclusively in the St. Joseph market area. Finally, we recently hired James Higgins as Vice President and Senior Lender. Mr. Higgins has over 25 years of lending and credit administration experience.

Mr. Dyer's and the management team's primary focus to date has been to oversee Edgewater Bank's asset quality initiatives, troubled loan resolution and the implementation of new, more stringent underwriting and loan administration policies and procedures, including increased emphasis on lower

2

debt-to-income ratios, higher credit scores, and lower loan-to-value ratios. In addition, in order to respond to changes in the market for financial services, we have begun to leverage our management team's commercial banking experience to implement a strategic shift from traditional thrift operations to an institution whose balance sheet and operations more closely resemble that of a full-service community-focused commercial bank with a comprehensive offering of financial services.

Resolution of Non-Performing Assets

From April 1, 2008 through June 30, 2013, we experienced net losses of approximately $9.1 million, including net losses of $498,000 for the six months ended June 30, 2013 and $769,000 for the year ended December 31, 2012. These losses were due primarily to approximately $6.7 million in charge-offs, $548,000 in losses on sales of real estate owned, $3.1 million in valuation write downs of real estate owned because our prior management team incorrectly carried real estate owned at loan value rather than fair market value, and $1.7 million in collection and other expenses related to problem loans as we aggressively focused on reducing classified and nonperforming loans, particularly speculative construction and land development loans and certain non-owner occupied commercial real estate loans, originated prior to 2009.

Despite significant losses in recent periods, we believe that our asset quality and portfolio management initiatives have been successful, and that the actions we took were necessary to ensure our survival and to enable us to operate profitably in the future. Our non-performing assets have decreased to $5.4 million, or 4.5% of total assets, at June 30, 2013, from approximately $10.1 million, or 5.4% of total assets at January 31, 2009 (the first date for which certain detailed information is available), and our classified assets have decreased to $5.6 million, or 4.7% of total assets, at June 30, 2013, from $19.4 million, or 10.4% of total assets, at January 31, 2009. In addition, our special mention loans have decreased to $2.5 million, or 2.1% of total assets, at June 30, 2013 from $9.0 million, or 4.8% of total assets, at January 31, 2009. The reductions in non-performing assets, classified assets and special mention loans as a percentage of total assets during this period occurred while we were also reducing the size of our balance sheet to improve our capital ratios and maintain compliance with the Order. Our total assets have decreased 35.8% to $120.3 million at June 30, 2013 from $187.5 million at December 31, 2008. Specifically, we have reduced our speculative construction and land development loans from $14.5 million, or 9.6% of total loans, at December 31, 2008 to approximately $383,000, or 0.45% of total loans, at June 30, 2013. In addition, commercial real estate loans decreased from $38.0 million, or 25.1% of total loans, at December 31, 2008 to $24.0 million, or 28.2% of total loans at June 30, 2013.

Shift in Business Strategy

We have branded and market Edgewater Bank as "TheReal Local Bank" because we are the only remaining bank or savings association headquartered in St. Joseph, Michigan. Our principal objective is to continually develop our model of personalized customer service, localized decision-making, employee involvement and efficiency to become the financial institution of choice for more customers in our communities and to fulfill our corporate mission: "To Profitably Provide Complete Financial Solutions and Total Customer Satisfaction".

Subject to market conditions and our asset-liability analysis, we expect to take advantage of unique opportunities presented by the geographic characteristics of our market area and our evolving customer base to increase our residential mortgage lending and our generation of low-cost core deposits. In order to diversify our portfolio and increase profitability, we also intend to develop a portfolio of commercial and industrial loans, including loans guaranteed by the U.S. Small Business Administration ("SBA"), and to significantly increase our consumer loan portfolio. We will continue to originate commercial real estate loans secured by properties in our market area where we have or can develop a banking relationship with the borrower. We do not currently contemplate engaging in speculative construction and land development lending.

3

Our market area is located between the Chicago/Detroit and Grand Rapids/Indianapolis business and population clusters, and is approximately 90 miles from Chicago, 30 miles from South Bend, Indiana, 45 miles from Kalamazoo, Michigan, 70 miles from Grand Rapids, Michigan, 180 miles from Detroit, and 210 miles from Indianapolis. Our market area is situated on the eastern or "sunset" shore of Lake Michigan and includes a 50-mile sandy shoreline and unobstructed views. The area is bolstered by large international companies, a growing and award-winning medical center, an agricultural and small business market, and desirable residential and cultural environments. The area has a multi-modal transportation network including interstate and other major highways, passenger and freight rail service, a regional commercial and recreational port with average commercial traffic that exceeds 550,000 tons per year, and air service through multiple general aviation facilities, three regional airports within 60 miles, and two major Chicago airports within 90 miles.

The area draws large numbers of tourists and retirees due to its proximity to major population centers, its shoreline location, the extensive services offered, including recreational, restaurants and hotels and medical services, and its relative modest cost of living compared to larger metropolitan markets. The area includes a high number of second or vacation homes, many of whose occupants retire to the area. In addition, our market area has solid manufacturing base, including the international headquarters of Whirlpool, Inc., a Fortune 100™ company, and Leco Corporation, as well as agriculture and farming in the surrounding areas. Additionally, the area houses two nuclear power plants that serve as large employers in the area and also provide plentiful and cost-efficient energy to support business retention and growth. Cornerstone Alliance, a local economic development organization, proactively works to not only retain employers in the area but also attract business from an international perspective. The strength of the medical services industry is highlighted by Lakeland Regional Medical Center, a hospital and medical center group with 48 locations and 4,100 employees, and the more than 470 practicing physicians.

We intend to focus on relationship-based banking, rather than simply generating loan originations, and customer service, and will continue to hire additional personnel with residential, commercial and consumer lending experience, which we expect will allow us to develop a broader, more flexible array of residential, commercial and industrial and consumer loan products specifically suited to the customers and potential customers in our market area. In addition, we intend to develop and offer additional financial products targeted at business and individual customers who desire full service, "high touch" banking and a full complement of efficient electronic banking services.

Highlights of our current business strategy following the completion of this stock offering include, subject to regulatory approval where applicable and market conditions:

- •

- improving our asset quality by continuing to reduce loan delinquencies and classified loans and improving our risk profile through enhancements of our credit risk management systems and credit administration procedures;

- •

- prudently and opportunistically growing our earnings base, particularly the size of our loan portfolio, by focusing on lending to homeowners, high net worth individuals, and small- to medium-sized traditional commercial and industrial customers and professional organizations, in order to cover expenses and achieve profitability;

- •

- increasing our focus on commercial and industrial and consumer lending in our market area, including developing a SBA loan program expertise to facilitate prudent growth of our commercial and industrial loan portfolio, in order to diversify and increase the yield on our total loan portfolio;

- •

- developing new products and services, tailoring suites of products and services, and emphasizing personalized customer service to meet the demands of current customers and attract new customers in our market area;

4

- •

- expanding our originations of one- to four-family residential mortgage loans by capitalizing on our unique geographical market area and customer base and continuing to service mortgage loans that we sell in order to maintain customer relations and our status as a community-oriented bank;

- •

- continuing to sell the majority of fixed-rate one- to four-family residential mortgage loans on a servicing-retained basis and to retain variable rate and certain fixed-rate one- to four-family residential loans in order to increase servicing fee income, recognize gains on sale and manage the overall maturity of our loan portfolio; and

- •

- continuing to focus on generating low-cost core deposits within our market area in order to decrease our dependence on certificates of deposit, reduce our interest rate sensitivity, and generate fee income to fund our operations.

These strategies are intended to guide our investment of the net proceeds of the offering. We intend to continue to pursue our business strategy after the conversion and the offering, subject to changes necessitated by future market conditions, regulatory restrictions and other factors. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Business Strategy" for a further discussion of our business strategy. We have adopted a strategic plan to achieve profitability by leveraging the capital raised in this offering to increase our earnings base, especially the size of our loan portfolio. Our strategic plan assumes that, beginning in 2014, we will not incur the same level of charge-offs, provisions for loan losses, write downs on real estate owned and losses on sales of real estate owned or expenses related to problem assets as we have in recent periods. However, the conversion will have a short-term adverse impact on our operating results, due to additional costs related to becoming a public company, increased compensation expenses associated with our employee stock ownership plan and the possible implementation of one or more stock-based benefit plans after the completion of the conversion. In addition, growth of earning assets is essential to our future profitability, and we expect to incur expenses related to the implementation of our growth plan, including hiring initiatives and the development and marketing of new products and services. Accordingly, even if we successfully implement our strategic plan, we do not anticipate a return to profitability until 2015. We may not be able to successfully implement our strategic plan, and therefore may not return to profitability in the timeframe that we expect or at all.

Edgewater Bancorp, Inc.

The shares being offered will be issued by Edgewater Bancorp, Inc. a newly formed Maryland corporation that will own all of the outstanding shares of common stock of Edgewater Bank upon completion of Edgewater Bank's mutual-to-stock conversion. Edgewater Bancorp, Inc. was incorporated on July 11, 2013 and has not engaged in any business to date. Upon completion of the conversion, Edgewater Bancorp will register as a savings and loan holding company and will be subject to comprehensive regulation and examination by the Board of Governors of the Federal Reserve System ("Federal Reserve Board").

Edgewater Bancorp's executive and administrative office is located at 321 Main Street, St. Joseph, Michigan 49085, and its telephone number at this address is (269) 982-4175.

The Conversion and Our Organizational Structure

Pursuant to the terms of the plan of conversion, Edgewater Bank will convert from a mutual (meaning no stockholders) savings association to a stock savings association. As part of the conversion, Edgewater Bancorp, the newly formed proposed holding company for Edgewater Bank, will offer for sale shares of its common stock in a subscription offering, and, if necessary, a community offering and a syndicated community offering. Upon the completion of the conversion and stock offering, Edgewater Bancorp will be 100% owned by stockholders and Edgewater Bank will be a wholly owned subsidiary of

5

Edgewater Bancorp. A full description of the conversion begins on page 152 of this prospectus under the heading "The Conversion and Offering."

Reasons for the Conversion and Offering

Consistent with our business strategy, our primary reasons for converting and raising additional capital through the offering are:

- •

- to increase capital to support modest organic growth while maintaining compliance with the IMCR;

- •

- to retain and attract qualified personnel by establishing stock-based benefit plans for management and employees;

- •

- to have greater flexibility to structure and finance the opportunistic expansion of our operations; and

- •

- to offer our customers and employees an opportunity to purchase our stock.

As of June 30, 2013, Edgewater Bank was considered "well capitalized" for regulatory purposes. As a result of the conversion, the proceeds from the stock offering will further improve our capital position during a period of significant economic, regulatory and political uncertainty.

See "The Conversion and Offering" for a more complete discussion of our reasons for conducting the conversion and offering.

Terms of the Offering

We are offering between 663,000 shares and 897,000 shares of common stock to eligible depositors of Edgewater Bank and to our tax-qualified employee benefit plans in a subscription offering. To the extent shares remain available, we may offer shares for sale in a community offering, with a preference given to natural persons and trusts of natural persons residing in Berrien, Van Buren and Cass Counties, Michigan. We may also offer for sale shares of common stock not purchased in the subscription offering or the community offering to the general public in a syndicated community offering. The number of shares of common stock to be sold may be increased to up to 1,031,550 shares as a result of demand for the shares of common stock in the offering or changes in market conditions. Unless the number of shares of common stock offered is increased to more than 1,031,550 shares or decreased to fewer than 663,000 shares, or the offering is extended beyond February 1, 2014, subscribers will not have the opportunity to change or cancel their stock orders once submitted. If the offering is extended past February 1, 2014, we will resolicit subscribers. You will have the opportunity to confirm, change or cancel your order within a specified period of time. If you do not respond during that period of time, your stock order will be cancelled and your deposit account withdrawal authorizations will be cancelled or your funds submitted will be returned promptly with interest at 0.10% per annum. If the number of shares to be sold is increased to more than 1,031,550 shares or decreased to less than 663,000 shares, all subscribers' stock orders will be cancelled, their deposit account withdrawal authorizations will be cancelled and funds delivered for the purchase of shares of common stock in the offering will be returned promptly with interest at 0.10% per annum. We will give these subscribers an opportunity to place new orders for a specified period of time.

The purchase price of each share of common stock to be offered for sale in the offering is $10.00. All investors will pay the same purchase price per share. Investors will not be charged a commission to purchase shares of common stock in the offering. Sterne, Agee & Leach, Inc., our marketing agent in the offering, will use its best efforts to assist us in selling shares of our common stock but is not obligated to purchase any shares of common stock in the offering.

6

How We Determined the Offering Range and the $10.00 Per Share Stock Price

The amount of common stock we are offering for sale is based on an independent appraisal of the estimated market value of Edgewater Bancorp, assuming the conversion and offering are completed. Keller & Company, Inc., our independent appraiser, has estimated that, as of November 6, 2013, this market value was $7.8 million. Based on regulations of the OCC, this market value forms the midpoint of a valuation range with a minimum of $6.6 million and a maximum of $9.0 million. Based on this valuation and a $10.00 per share price, the number of shares of common stock being offered for sale by us will range from 663,000 shares to 897,000 shares. We may sell up to 1,031,550 shares of common stock because of demand for the shares or changes in market conditions without resoliciting subscribers. The $10.00 per share price was selected primarily because it is the price most commonly used in mutual-to-stock conversions of financial institutions.

The appraisal is based in part on Edgewater Bank's financial condition and results of operations, the pro forma effect of the additional capital raised by the sale of shares of common stock in the offering, the pro forma effect of the costs associated with our withdrawal from the defined benefit plan, and an analysis of a peer group of ten publicly traded thrift holding companies with assets between $287.1 million and $597.8 million as of June 30, 2013 that Keller & Company, Inc. considers comparable to Edgewater Bancorp. See, "The Conversion and Offering—Determination of Share Price and Number of Shares to be Issued."

The following table presents a summary of selected pricing ratios for the peer group companies and for Edgewater Bancorp (on a pro forma basis) utilized by Keller & Company, Inc. in its appraisal. These ratios are based on Edgewater Bancorp's book value, tangible book value and core earnings as of and for the 12 months ended September 30, 2013, as adjusted for the impact of the cost to withdraw from the defined benefit plan. The peer group ratios are based on the latest date for which complete financial data are publicly available and stock prices as of October 17, 2013. Compared to the average pricing of the peer group, our pro forma pricing ratios at the midpoint of the offering range indicated a discount of 30.42% on a price-to-book value basis and a discount of 30.51% on a price-to-tangible book value basis.

| | Price-to-core earnings multiple | Price-to-book value ratio | Price-to-tangible book value ratio | ||||||

|---|---|---|---|---|---|---|---|---|---|

Edgewater Bancorp (on a pro forma basis, assuming completion of the conversion): | |||||||||

Adjusted Maximum | n/m | 65.02 | % | 67.25 | % | ||||

Maximum | n/m | 61.09 | % | 63.37 | % | ||||

Midpoint | n/m | 57.18 | % | 59.45 | % | ||||

Minimum | n/m | 52.52 | % | 54.79 | % | ||||

Valuation of peer group companies, all of which are fully converted (on an historical basis): | |||||||||

Averages | 24.08x | 82.11 | % | 85.51 | % | ||||

Medians | 23.51x | 77.88 | % | 84.01 | % | ||||

(n/m) Not meaningful.

The independent appraisal does not indicate trading market value. Do not assume or expect that our valuation as indicated in the appraisal means that after the conversion and offering the shares of our common stock will trade at or above the $10.00 per share purchase price. Furthermore, the pricing ratios presented in the appraisal were utilized by Keller & Company, Inc. to estimate ourpro forma appraised value for regulatory purposes and not to compare the relative value of shares of our common stock with the value of the capital stock of the peer group. The value of the capital stock of a particular company may be affected by a number of factors such as financial performance, asset size and market location.

7

For a more complete discussion of the amount of common stock we are offering for sale and the independent appraisal, see "The Conversion and Offering—Determination of Share Price and Number of Shares to be Issued."

After-Market Stock Price Performance

The following table presents stock price performance information for all standard mutual-to-stock conversions completed between January 11, 2012 and July 26, 2013. These companies did not constitute the group of ten comparable public companies utilized in Keller & Company, Inc.'s valuation analysis.

Mutual-to-Stock Conversion Offerings with Closing Dates between January 11, 2012 and July 26, 2013

| | | | Percentage Price Change From Initial Trading Date | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Company Name and Ticker Symbol | Conversion Date | Exchange | One Day | One Week | One Month | Through October 17, 2013 | |||||||||||

Quarry City S&L Assn. (QRRY) | 7/26/2013 | OTCBB | 7.50 | % | 2.00 | % | 0.50 | % | 0.10 | % | |||||||

Sunnyside Bancorp, Inc. (SNNY) | 7/16/2013 | OTCBB | 5.00 | % | 4.50 | % | 0.10 | % | (1.30 | )% | |||||||

Westbury Bancorp, Inc. (WBB) | 4/10/2013 | NASDAQ | 35.20 | % | 36.00 | % | 33.30 | % | 41.30 | % | |||||||

Meetinghouse Bancorp (MTGB) | 11/20/2012 | OTCBB | 12.50 | % | 27.50 | % | 20.00 | % | 21.00 | % | |||||||

Hamilton Bancorp, Inc. (HBK) | 10/10/2012 | NASDAQ | 19.00 | % | 16.50 | % | 12.60 | % | 45.20 | % | |||||||

Madison County Financial, Inc. (MCBK) | 10/04/2012 | NASDAQ | 48.90 | % | 45.50 | % | 43.60 | % | 73.10 | % | |||||||

Hometrust Bancshares, Inc. (HTBI) | 07/11/2012 | NASDAQ | 17.00 | % | 25.80 | % | 25.80 | % | 61.50 | % | |||||||

FS Bancorp, Inc. (FSBW) | 07/10/2012 | NASDAQ | 0.10 | % | 0.40 | % | 2.10 | % | 66.60 | % | |||||||

Wellesley Bancorp, Inc. (WEBK) | 01/26/2012 | NASDAQ | 20.00 | % | 21.00 | % | 22.90 | % | 74.50 | % | |||||||

West End Indiana Bancshares, Inc. (WEIN) | 01/11/2012 | OTCBB | 12.60 | % | 11.50 | % | 20.00 | % | 91.00 | % | |||||||

Average | 17.78 | % | 19.07 | % | 18.09 | % | 47.30 | % | |||||||||

Median | 14.80 | % | 18.75 | % | 20.00 | % | 53.35 | % | |||||||||

Stock price performance is affected by many factors, including, but not limited to: general market and economic conditions; the interest rate environment; the amount of proceeds a company raises in its offering; and numerous factors relating to the specific company, including the experience and ability of management, historical and anticipated operating results, the nature and quality of the company's assets, and the company's market area. None of the companies listed in the table above are exactly similar to Edgewater Bancorp, the pricing ratios for their stock offerings may have been different from the pricing ratios for Edgewater Bancorp shares of common stock and the market conditions in which these offerings were completed may have been different from current market conditions. Furthermore, this table presents only short-term performance with respect to companies that recently completed their mutual-to-stock conversions and may not be indicative of the longer-term stock price performance of these companies.The performance of these stocks may not be indicative of how our stock will perform.

Our stock price may trade below $10.00 per share, as the stock prices of certain mutual-to-stock conversions have decreased below the initial offering price. Before you make an investment decision, we urge you to carefully read this prospectus, including, but not limited to, the section entitled "Risk Factors" beginning on page 18.

How We Intend to Use the Proceeds From the Stock Offering

Edgewater Bank will receive a capital contribution equal to at least 50% of the net proceeds of the offering, plus such additional amounts as may be necessary so that, upon completion of the offering, Edgewater Bank will have a tier 1 leverage ratio of at least 9.50% at the minimum of the offering range and at least 10.00% at the midpoint, maximum and adjusted maximum of the offering range, after payment of costs to withdraw from the defined benefit plan. Based on this formula, we anticipate that

8

Edgewater Bancorp will invest, at the minimum, midpoint, maximum and adjusted maximum of the offering range, approximately $4.3 million, $5.1 million, $5.3 million and $5.5 million, respectively, of the net proceeds from the stock offering in Edgewater Bank. Of the remaining funds, we intend that Edgewater Bancorp will loan funds to our employee stock ownership plan to fund the plan's purchase of shares of common stock in the stock offering, and retain the remainder of the net proceeds from the offering. Assuming we sell 780,000 shares of common stock in the stock offering and have net proceeds of $6.5 million, based on the above formula, we anticipate that Edgewater Bancorp will invest $5.1 million in Edgewater Bank, loan $624,000 to our employee stock ownership plan to fund its purchase of shares of common stock, and retain the remaining $741,000 of the net proceeds.

Edgewater Bancorp may use the remaining funds that it retains to pay cash dividends, to repurchase shares of common stock (subject to compliance with regulatory requirements), for investments, or for other general corporate purposes. Edgewater Bank intends to use approximately $1.65 million of the proceeds that it receives from us to pay costs associated with its withdrawal from a defined benefit plan, and may use the remaining net proceeds it receives from us to fund new loans, enhance existing products and services, invest in securities, expand its banking franchise by establishing or acquiring a new branch or acquiring another financial institution as opportunities arise, or for general corporate purposes.

For more information on the proposed use of the proceeds from the offering, see "How We Intend to Use the Proceeds from the Offering."

Persons Who May Order Shares of Common Stock in the Offering

We are offering the shares of common stock in a subscription offering in the following descending order of priority:

- (i)

- First, to depositors with accounts at Edgewater Bank with aggregate balances of at least $50 at the close of business on June 30, 2012.

- (ii)

- Second, to our tax-qualified employee benefit plans (including Edgewater Bank's employee stock ownership plan), which will receive, without payment therefor, nontransferable subscription rights to purchase in the aggregate up to 10% of the shares of common stock sold in the offering. We expect our employee stock ownership plan to purchase up to 8% of the shares of common stock sold in the offering.

- (iii)

- Third, to depositors with accounts at Edgewater Bank with aggregate balances of at least $50 at the close of business on September 30, 2013.

- (iv)

- Fourth, to depositors of Edgewater Bank at the close of business on October 31, 2013.

Shares of common stock not purchased in the subscription offering may be offered for sale in a community offering, with a preference given to natural persons and trusts of natural persons residing in Berrien, Van Buren and Cass Counties, Michigan. The community offering may begin concurrently with, during or after the subscription offering. We also may offer for sale shares of common stock not purchased in the subscription offering or the community offering to the general public through a syndicated community offering, which will be managed by Sterne, Agee & Leach, Inc. We have the right to accept or reject, in our sole discretion, orders received in the community offering or syndicated community offering. Any determination to accept or reject stock orders in the community offering or the syndicated community offering will be based on the facts and circumstances available to management at the time of the determination.

9

If we receive orders for more shares than we are offering, we may not be able to fully or partially fill your order. Shares will be allocated first to categories in the subscription offering. A detailed description of the subscription offering, the community offering and the syndicated community offering, as well as a discussion regarding allocation procedures, can be found in the section of this prospectus entitled "The Conversion and Offering."

Limits on How Much Common Stock You May Purchase

The minimum number of shares of common stock that may be purchased is 25.

Generally, no individual may purchase more than 10,000 shares ($100,000) of common stock. If any of the following purchase shares of common stock, their purchases, in all categories of the offering combined, when combined with your purchases, cannot exceed 20,000 shares ($200,000) of common stock:

- •

- your spouse or relatives of you or your spouse who reside with you;

- •

- most companies, trusts or other entities in which you are a trustee, have a substantial beneficial interest or hold a senior position; or

- •

- other persons who may be your associates or persons acting in concert with you.

Unless we determine otherwise, persons having the same address and persons exercising subscription rights through qualifying accounts registered to the same address will be subject to the overall purchase limitation of 20,000 shares ($200,000). See the detailed descriptions of "acting in concert" and "associate" in the section of this prospectus headed "The Conversion and Offering—Limitations on Common Stock Purchases."

Subject to OCC approval, we may increase or decrease the purchase limitations at any time. See the detailed description of the purchase limitations in the section of this prospectus headed "The Conversion and Offering—Limitations on Common Stock Purchases."

How You May Purchase Shares of Common Stock in the Subscription Offering and the Community Offering

In the subscription offering and community offering, you may pay for your shares only by:

- •

- personal check, bank check or money order made payable directly to Edgewater Bancorp, Inc.; or

- •

- authorizing us to withdraw available funds from the types of Edgewater Bank deposit accounts identified on the stock order form.

Please do not submit cash or wire transfers. Edgewater Bank is not permitted to lend funds to anyone for the purpose of purchasing shares of common stock in the offering. Additionally, you may not use an Edgewater Bank line of credit check or any type of third-party check to pay for shares of common stock.On the stock order form, you may not designate withdrawal from Edgewater Bank accounts with check-writing privileges; instead, please submit a check. If you request that we directly withdraw the funds from an account with check writing privileges, we reserve the right to interpret that as your authorization to treat those funds as if we had received a check for the designated amount, and we will immediately withdraw the amount from your checking account. Funds received in the subscription and community offerings and, if applicable, the syndicated community offering will be held in a segregated account at Edgewater Bank and will earn interest at 0.10% per annum until completion or termination of the offering. You may not authorize direct withdrawal from an Edgewater Bank retirement account. See "—Using Retirement Account Funds to Purchase Shares of Common Stock in the Subscription and Community Offerings."

10

You may subscribe for shares of common stock in the offering by delivering a signed and completed stock order form, together with full payment payable to Edgewater Bancorp, Inc. or authorization to withdraw funds from one or more of your Edgewater Bank deposit accounts, provided that the stock order form isreceived before 12:00 p.m., Eastern Time, on December 18, 2013. You may submit your stock order form and payment by mail using the stock order reply envelope provided, by overnight delivery to our Stock Information Center at the address noted on the stock order form or by hand-delivery to Edgewater Bank's office, located at 321 Main Street, St. Joseph, Michigan.Please do not mail stock order forms to Edgewater Bank. Once submitted, your order will be irrevocable unless the offering is terminated or is extended beyond February 1, 2014, or the number of shares of common stock to be sold is increased to more than 1,031,550 shares or decreased to less than 663,000 shares.

For a complete description of how to purchase shares in the stock offering, see "The Conversion and Offering—Procedure for Purchasing Shares."

Using Retirement Account Funds to Purchase Shares of Common Stock in the Subscription and Community Offerings

You may be able to subscribe for shares of common stock using funds in your individual retirement account ("IRA"), or other retirement account. If you wish to use some or all of the funds in your IRA or other retirement account held at Edgewater Bank, the applicable funds must be transferred to a self-directed account maintained by an independent custodian or trustee, such as a brokerage firm,before you place your stock order. If you do not have such an account, you will need to establish one. An annual administrative fee may be payable to the independent custodian or trustee. Because individual circumstances differ and the processing of retirement fund orders takes additional time, we recommend that you contact our Stock Information Center promptly, preferably at least two weeks before the December 18, 2013 offering deadline, for assistance with purchases using funds in your IRA or other retirement account held at Edgewater Bank or elsewhere. Whether you may use such funds for the purchase of shares in the stock offering may depend on timing constraints and, possibly, limitations imposed by the institution where the funds are held.

For a complete description of how to use IRA funds to purchase shares in the stock offering, see "The Conversion and Offering—Procedure for Purchasing Shares—Using Retirement Account Funds."

You May Not Sell or Transfer Your Subscription Rights

Federal regulations prohibit you from transferring your subscription rights. If you order shares of common stock in the subscription offering, you will be required to state that you are purchasing the common stock for yourself and that you have no agreement or understanding to sell or transfer your subscription rights. We intend to take legal action against anyone who we believe has sold or transferred his or her subscription rights. In addition, we intend to advise the appropriate federal agencies of any person who we believe has sold or transferred his or her subscription rights. We will not accept your order if we have reason to believe that you have sold or transferred your subscription rights. On the stock order form, you may not add the names of others for joint stock registration who do not have subscription rights or who qualify only in a lower subscription offering priority than you do. You may add only those who were eligible to purchase shares of common stock in the subscription offering at your date of eligibility. In addition, the stock order form requires that you list all qualifying accounts, giving all names on each account and the account number at the applicable eligibility date. Failure to provide this information, or providing incomplete or incorrect information, may result in a loss of part or all of your share allocation if there is an oversubscription.

11

Purchases by Executive Officers and Directors

We expect our directors and executive officers, together with their associates, to subscribe for 90,000 shares ($900,000) of common stock in the offering, representing 13.6% of shares to be sold at the minimum of the offering range. However, there can be no assurance that any individual director or executive officer, or the directors and executive officers as a group, will purchase any specific number of shares of our common stock. The purchase price paid by them will be the same $10.00 per share price paid by all other persons who purchase shares of common stock in the offering. Our directors and executive officers will be subject to the same minimum purchase requirements and purchase limitations as other participants in the offering set forth under "—Limits on How Much Common Stock You May Purchase."

Purchases by our directors, executive officers and their associates will be included in determining whether the required minimum number of shares has been subscribed for in the offering. Any purchases made by our directors or executive officers, or their associates, for the explicit purpose of meeting the minimum number of shares of common stock required to be sold in order to complete the offering shall be made for investment purposes only and not with a view toward redistribution.

For more information on the proposed purchases of shares of common stock by our directors and executive officers, see "Subscriptions by Directors and Executive Officers."

Deadline for Orders of Shares of Common Stock in the Subscription and Community Offerings

The deadline for submitting orders for shares of common stock in the subscription and community offerings is 12:00 p.m., Eastern Time, on December 18, 2013, unless we extend the subscription offering and/or the community offering. If you wish to purchase shares of common stock, a properly completed and signed original stock order form, together with full payment, must bereceived (not postmarked) by this time.

Although we will make reasonable attempts to provide this prospectus and offering materials to holders of subscription rights, the subscription offering and all subscription rights will expire at 12:00 p.m., Eastern Time, on December 18, 2013, whether or not we have been able to locate each person entitled to subscription rights.

For a complete description of the deadline for purchasing shares in the stock offering, see "The Conversion and Offering—Procedure for Purchasing Shares—Expiration Date."

Steps We May Take if We Do Not Receive Orders for the Minimum Number of Shares

If we do not receive orders for at least 663,000 shares of common stock, we may take additional steps in order to issue the minimum number of shares of common stock in the offering range. Specifically, we may:

- •

- increase the purchase limitations; and/or

- •

- seek regulatory approval to extend the offering beyond February 1, 2014.

If we extend the offering past February 1, 2014, we will resolicit subscribers. You will have the opportunity to confirm, change or cancel your order within a specified period of time. If you do not respond during that period of time, your stock order will be cancelled and your deposit account withdrawal authorizations will be cancelled or your funds submitted will be returned promptly with interest at 0.10% per annum from the date the stock order was processed. If one or more purchase limitations are increased, subscribers in the subscription offering who ordered the maximum amount and who indicated a desire to be resolicited on the stock order form will be and, in our sole discretion, some other large subscribers may be, given the opportunity to increase their subscriptions up to the newly applicable limit.

12

Conditions to Completion of the Conversion

The board of directors of Edgewater Bank has approved the plan of conversion. In addition, the OCC has conditionally approved the plan of conversion and the Federal Reserve Board has conditionally approved our holding company application. We cannot complete the conversion unless:

- •

- The plan of conversion is approved by a majority of votes eligible to be cast by members of Edgewater Bank (depositors of Edgewater Bank) as of October 31, 2013;

- •

- We have received orders for at least the minimum number of shares of common stock offered; and

- •

- We receive the final approval required from the OCC to complete the conversion and offering and the final approval from the Federal Reserve Board on the holding company application.

Any approval by the OCC or the Federal Reserve Board does not constitute a recommendation or endorsement of the plan of conversion.

Our Dividend Policy

Following completion of the stock offering, our board of directors will have the authority to declare dividends on our common stock, subject to statutory and regulatory requirements. We do not intend to pay dividends until such time as we generate sufficient net income to support our planned growth and the payment of dividends. Growth of earning assets is essential to our future profitability, and we expect to incur expenses related to the implementation of our growth plan. Accordingly, even if we successfully implement our strategic plan, we do not anticipate a return to profitability until 2015. We may not be able to successfully implement our strategic plan, and therefore may not return to profitability in the timeframe that we expect or at all. The payment and amount of any dividend payments will depend upon a number of factors, including the following: regulatory capital requirements; our financial condition and results of operations; our other uses of funds for the long-term value of stockholders; tax considerations; statutory and regulatory limitations; and general economic conditions. See "Our Dividend Policy" for additional information regarding our dividend policy. In addition, beginning in 2016, Edgewater Bank's ability to pay dividends will be limited if Edgewater Bank does not have the capital conservation buffer required by the new capital rules, which may limit our ability to pay dividends to stockholders. See "Regulation and Supervision—Federal Banking Regulation—New Capital Rule."

Market for Common Stock

We anticipate that the common stock sold in the offering will be quoted on the OTC Bulletin Board. Sterne, Agee & Leach, Inc. currently intends to make a market in the shares of our common stock, but is under no obligation to do so. See "Market for the Common Stock."

Delivery of Stock Certificates

Certificates representing shares of common stock sold in the subscription offering and community offering will be mailed to purchasers at the certificate registration address noted by them on the stock order form. Shares of common stock sold in the syndicated community offering may be delivered electronically through the services of The Depository Trust Company. Stock certificates will be sent to purchasers by first-class mail as soon as practicable after the completion of the conversion and stock offering, which is expected to occur as soon as practicable following satisfaction of the conditions described above in "—Conditions to Completion of the Conversion." We expect trading in the stock to begin on the business day of or on the business day immediately following the completion of the conversion and stock offering.It is possible that until certificates for the common stock are delivered, purchasers might not be able to sell the shares of common stock that they ordered, even though the

13

common stock will have begun trading. Your ability to sell the shares of common stock before receiving your stock certificate will depend on arrangements you may make with a brokerage firm.

Possible Change in the Offering Range

Keller & Company, Inc. will update its appraisal before we complete the offering. If, as a result of demand for the shares or changes in market conditions, Keller & Company, Inc. determines that our pro forma market value has increased, we may sell up to 1,031,550 shares in the offering without further notice to you. If our pro forma market value at that time is either below $6.6 million or above $10.3 million, then, after consulting with the OCC, we may:

- •

- terminate the stock offering, cancel deposit account withdrawal authorizations and promptly return all funds received in the offering with interest at 0.10% per annum;

- •

- set a new offering range; or

- •

- take such other actions as may be permitted by the OCC, the Federal Reserve Board, the Financial Industry Regulatory Authority ("FINRA") and the Securities and Exchange Commission.

If we set a new offering range, we will promptly return funds, with interest at 0.10% per annum for funds received in the offering, cancel deposit account withdrawal authorizations and commence a resolicitation. In connection with the resolicitation, we will notify subscribers of their right to place a new stock order for a specified period of time.

Possible Termination of the Offering

We may terminate the offering at any time prior to the special meeting of members of Edgewater Bank that is being called to vote on the conversion, and at any time after member approval with the concurrence of the OCC. If we terminate the offering, we will promptly return funds, as described above.

Benefits to Management and Potential Dilution to Stockholders Resulting from the Conversion

We expect our employee stock ownership plan, which is a tax-qualified retirement plan for the benefit of all of our employees being established in connection with the conversion and stock offering, to purchase up to 8% of the shares of common stock that we sell in the offering. If we receive orders for more shares of common stock than the maximum of the offering range, the employee stock ownership plan will have first priority to purchase shares over this maximum, up to a total of 8% of the shares of common stock that we sell in the offering. This would reduce the number of shares available for allocation to eligible depositors. For further information, see "Management—Benefit Plans and Agreements—Employee Stock Ownership Plan."

Purchases by the employee stock ownership plan in the offering will be included in determining whether the required minimum number of shares have been sold in the offering. Subject to market conditions and receipt of regulatory approval, the employee stock ownership plan may instead elect to purchase shares of common stock in the open market following the completion of the offering in order to fill all or a portion of the employee stock ownership plan's intended subscription.

We also intend to implement one or more stock-based benefit plans no earlier than six months after completion of the conversion. Stockholder approval of these plans will be required, and the stock-based benefit plans cannot be implemented until at least six months after the completion of the conversion pursuant to applicable OCC regulations. If adopted within 12 months following the completion of the conversion, and provided that upon completion of the offering Edgewater Bank has at least a 10% tangible capital to assets ratio, the OCC regulations conversion would allow for the stock-based benefit plans to reserve a number of shares of common stock equal to not more than 4% of the shares sold in the offering, or up to 35,880 shares of common stock at the maximum of the offering range, for restricted

14

stock awards to key employees and directors, at no cost to the recipients. If adopted within 12 months following the completion of the conversion, the stock-based benefit plans will also reserve a number of shares equal to not more than 10% of the shares of common stock sold in the offering, or up to 89,700 shares of common stock at the maximum of the offering range, for the exercise of stock options granted to key employees and directors. If the stock-based benefit plans are adopted after one year from the date of the completion of the conversion, the 4% and 10% limitations described above will no longer apply, and we may adopt stock-based benefit plans encompassing more than 125,580 shares of our common stock assuming the maximum of the offering range. We have not yet determined whether we will present these plans for stockholder approval within 12 months following the completion of the conversion or whether we will present these plans for stockholder approval more than 12 months after the completion of the conversion.

The following table summarizes the number of shares of common stock and aggregate dollar value of grants (valuing each share granted at the offering price of $10.00) that would be available under one or more stock-based benefit plans if such plans are adopted within one year following the completion of the conversion and the offering and Edgewater Bank has at least a 10% tangible capital to assets ratio at that time. The table shows the dilution to stockholders if all these shares are issued from authorized but unissued shares, instead of shares purchased in the open market. The table also sets forth the number of shares of common stock to be acquired by the employee stock ownership plan for allocation to all employees. A portion of the stock grants shown in the table below may be made to non-management employees.

| | Number of Shares to be Granted or Purchased(1) | Dilution Resulting From Issuance of Shares for Stock Benefit Plans | | | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Value of Grants(2) | ||||||||||||||||||

| | | | As a Percentage of Common Stock to be Issued | ||||||||||||||||

| | At Minimum of Offering Range | At Maximum of Offering Range | At Minimum of Offering Range | At Maximum of Offering Range | |||||||||||||||

Employee stock ownership plan | 53,040 | 71,760 | 8.00 | % | n/a | (3) | $ | 530 | $ | 718 | |||||||||

Stock awards | 26,520 | 35,880 | 4.00 | 3.85 | % | 265 | 359 | ||||||||||||

Stock options | 66,300 | 89,700 | 10.00 | 9.09 | % | 217 | 293 | ||||||||||||

Total | 145,860 | 197,340 | 22.00 | % | 12.28 | % | $ | 1,012 | $ | 1,370 | |||||||||

- (1)

- The stock-based benefit plans may award a greater number of options and shares, respectively, if the plans are adopted more than 12 months after the completion of the conversion. If Edgewater Bank has a tangible capital to assets ratio of less than 10%, the stock-based benefit plans would only be permitted to award a number stock awards equal to 2.0% of the common stock to be issued in the offering, or 13,260 shares at the minimum of the offering range and 17,940 shares at the maximum of the offering range.

- (2)

- The actual value of restricted stock grants will be determined based on their fair value as of the date grants are made. For purposes of this table, fair value is assumed to be the same as the offering price of $10.00 per share. The fair value of stock options has been estimated at $3.27 per option using the Black-Scholes option pricing model with the following assumptions: a grant-date share price and option exercise price of $10.00; dividend yield of 0%; an expected option life of 10 years; a risk-free interest rate of 2.79%; and a volatility rate of 16.48%. The actual expense of stock options granted under a stock-based benefit plan will be determined by the grant-date fair value of the options, which will depend on a number of factors, including the valuation assumptions used in the option pricing model ultimately adopted, which may or may not be the Black-Scholes model.

- (3)

- Represents the dilution of stock ownership interest. No dilution is reflected for the employee stock ownership plan because these shares are assumed to be purchased in the offering.

In addition to the stock-based benefit plans that we may adopt, Edgewater Bancorp and Edgewater Bank each intend to enter into employment agreements with Richard E. Dyer, our President and Chief Executive Officer, and Coleen S. Frens-Rossman, our Senior Vice President and Chief Financial Officer, and change in control agreements with certain other of our officers subject to regulatory approval. See "Management—Executive Compensation" in this prospectus for a further discussion of these agreements, including their terms and potential costs, as well as a description of other benefits arrangements.

15

Tax Consequences

Edgewater Bank and Edgewater Bancorp have received an opinion of counsel, Luse Gorman Pomerenk & Schick, P.C., regarding the material federal income tax consequences of the conversion, including an opinion that it is more likely than not that the fair market value of the nontransferable subscription rights to purchase the common stock will be zero and, accordingly, no gain or loss will be recognized by depositors upon the distribution to them of the nontransferable subscription rights to purchase the common stock and no taxable income will be realized by depositors as a result of the exercise of the nontransferable subscription rights. Edgewater Bank and Edgewater Bancorp have also received an opinion of BKD LLP regarding the material Michigan state tax consequences of the conversion. As a general matter, the conversion will not be a taxable transaction for purposes of federal or state income taxes to Edgewater Bank, Edgewater Bancorp or persons eligible to subscribe in the subscription offering. See the section of this prospectus entitled "Taxation" for additional information regarding taxes.

Emerging Growth Company Status

The Jumpstart Our Business Startups Act (the "JOBS Act"), which was signed into law on April 5, 2012, has made numerous changes to the federal securities laws to facilitate access to capital markets. Under the JOBS Act, a company with total annual gross revenues of less than $1.0 billion during its most recently completed fiscal year qualifies as an "emerging growth company." We qualify as an "emerging growth company" and believe that we will continue to qualify as an "emerging growth company" for five years from the completion of the stock offering.

As an "emerging growth company" we have elected to use the extended transition period to delay adoption of new or revised accounting pronouncements applicable to public companies until such pronouncements are made applicable to private companies. Accordingly, our financial statements may not be comparable to the financial statements of public companies that comply with such new or revised accounting standards.

Additionally, we are in the process of evaluating the benefits of relying on the reduced reporting requirements provided by the JOBS Act. Subject to certain conditions set forth in the JOBS Act, if, as an "emerging growth company", we choose to rely on such exemptions we may not be required to, among other things, (i) provide an auditor's attestation report on our system of internal controls over financial reporting, (ii) provide all of the compensation disclosure that may be required of non-emerging growth public companies under the Dodd-Frank Act, (iii) hold non-binding stockholder votes regarding annual executive compensation or executive compensation payable in connection with a merger or similar corporate transaction, (iv) comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor's report providing additional information about the audit and the financial statements (auditor discussion and analysis), and (v) disclose certain executive compensation related items such as the correlation between executive compensation and performance and comparisons of the chief executive officer's compensation to median employee compensation.

We could remain an "emerging growth company" for up to five years, or until the earliest of (a) the last day of the first fiscal year in which our annual gross revenues exceed $1.0 billion, (b) the date that we become a "large accelerated filer" as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (c) the date on which we have issued more than $1.0 billion in non-convertible debt during the preceding three-year period.

16

How You Can Obtain Additional Information—Stock Information Center

Our banking personnel may not, by law, assist with investment-related questions about the offering. If you have questions regarding the conversion or offering, please call our Stock Information Center. The toll-free telephone number is (800) 979-4568. The Stock Information Center is open for telephone calls Monday through Friday between 10:00 a.m. and 5:00 p.m., Eastern Time, and for walk-in customers on Tuesdays and Wednesdays, between 10:00 a.m. and 2:00 p.m., Eastern Time. The Stock Information Center will be closed on weekends and bank holidays.

17

You should consider carefully the following risk factors in evaluating an investment in the shares of common stock.

Risks Related to Our Business

We incurred a net loss for the six months ended June 30, 2013 and the year ended December 31, 2012 and may not achieve profitability by implementing our business strategies.

During the six months ended June 30, 2013 we had a net loss of $498,000, and during the year ended December 31, 2012, we had a net loss of $769,000. These losses were due primarily to in charge-offs, losses on sales of real estate owned, valuation write downs of real estate owned and collection and other expenses related to nonperforming assets as we aggressively focused on reducing classified and nonperforming loans, particularly speculative construction and land development loans and certain non-owner occupied commercial real estate loans, originated prior to 2009. We have continued to experience these types of expenses in the third and fourth quarters of 2013, and may continue to incur additional expenses as we continue to resolve our problem assets. Our growth is essential to our future profitability, and we expect to incur expenses related to the implementation of our growth plan, including hiring initiatives and the development and marketing of new products and services. In addition, the conversion will have a short-term adverse impact on our operating results, due to additional costs related to becoming a public company, increased compensation expenses associated with our employee stock ownership plan and the possible implementation of one or more stock-based benefit plans after the completion of the conversion. Accordingly, even if we successfully implement our strategic plan, we do not anticipate a return to profitability until 2015. We may not be able to successfully implement our strategic plan, and therefore may not return to profitability in the timeframe that we expect or at all.

Our ability to achieve profitability depends upon a number of factors, including our ability to manage expenses related to nonperforming and classified assets, general economic conditions, competition with other financial institutions, changes to the interest rate environment that may reduce our profit margins or impair our business strategy, adverse changes in the securities markets, changes in laws or government regulations, changes in consumer spending, borrowing, or saving, and changes in accounting policies, as well as other risks and uncertainties described in this "Risk Factors" section. Continued net losses after the completion of our mutual-to-stock conversion could adversely affect our capital levels and our ability to comply with the IMCR. If we fail to comply with the IMCR, our regulators could impose a capital directive requiring us to maintain additional capital levels, subject us to a formal written agreement or cease and desist order, restrict Edgewater Bank's ability to pay dividends, restrict Edgewater Bank's growth or ability to engage in certain types of lending, require Edgewater Bank to take remedial actions with respect to any capital deficiency, require Edgewater Bank to submit a capital plan for approval, or take other adverse regulatory actions, any one of which would negatively impact our stock price. For additional information, see "—Our provision for loan losses and net loan charge-offs have increased significantly in recent years, and we may be required to make further increases in our provision for loan losses and to charge-off additional loans in the future, which could adversely affect our results of operations. If our allowance for loan losses is not sufficient to cover actual loan losses, we may be required to make additional provisions for loans losses, which would cause our earnings to decrease," "—If our nonperforming assets increase, our earnings will be adversely affected" and "—We are subject to an IMCR with the OCC, and we may because subject to regulatory restrictions if we fail to comply with the terms."

18

We have a high concentration of loans secured by real estate in our market area. Adverse economic conditions, both generally and in our market area, could adversely affect our financial condition and results of operations.

We have relatively few loans outside of our market area, and, as a result, we have a greater risk of loan defaults and losses in the event of a further economic downturn in our market area, as adverse economic conditions may have a negative effect on the ability of our borrowers to make timely payments of their loans. During the last several years, economic conditions and real estate values within our market area have declined significantly. We believe that such conditions have contributed to our non-performing assets, loan charge-offs and our provisions for loan losses.