Filed Pursuant to Rule 424(b)(3)

Registration No. 333-220046

HINES GLOBAL INCOME TRUST, INC.

SUPPLEMENT NO. 8 DATED NOVEMBER 16, 2018

TO THE PROSPECTUS DATED JULY 18, 2018

This prospectus supplement (this “Supplement”) is part of and should be read in conjunction with the prospectus of Hines Global Income Trust, Inc., dated July 18, 2018 (the “Prospectus”), as supplemented by Supplement No. 1, dated August 15, 2018, Supplement No. 2, dated August 16, 2018, Supplement No. 3, dated September 10, 2018, Supplement No. 4, dated September 14, 2018, Supplement No. 5, dated October 17, 2018, Supplement No. 6, dated October 24, 2018, and Supplement No. 7, dated November 15, 2018. Unless otherwise defined herein, capitalized terms used in this Supplement shall have the same meanings as in the Prospectus.

The purpose of this Supplement is to include our Quarterly Report on Form 10-Q for the quarter ended September 30, 2018, as filed with the Securities and Exchange Commission on November 14, 2018. The report (without exhibits) is attached to this Supplement.

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| (Mark One) | |

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2018

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 000-55599

Hines Global Income Trust, Inc.

(Exact name of registrant as specified in its charter)

| Maryland | 80-0947092 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 2800 Post Oak Boulevard | |

| Suite 5000 | |

| Houston, Texas | 77056-6118 |

| (Address of principal executive offices) | (Zip code) |

(888) 220-6121

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | |

Smaller reporting company x | Emerging growth company x | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13 (a) of the Exchange Act. x | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of November 1, 2018, approximately 19.2 million shares of the registrant’s Class AX common stock, 20.1 million shares of the registrant’s Class TX common stock, 0.1 million shares of the registrant’s Class IX common stock, 2.1 million shares of the registrant’s Class T common stock, 1.1 million shares of the registrant’s Class D common stock and 24,612 shares of the registrant’s Class I common stock were outstanding.

TABLE OF CONTENTS

| PART I – FINANCIAL INFORMATION | ||

| Item 1. | Condensed Consolidated Financial Statements (Unaudited): | |

| Item 2. | ||

| Item 3. | ||

| Item 4. | ||

| PART II – OTHER INFORMATION | ||

| Item 1. | ||

| Item 1A. | ||

| Item 2. | ||

| Item 3. | ||

| Item 4. | ||

| Item 5. | ||

| Item 6. | ||

PART I - FINANCIAL INFORMATION

Item 1. Condensed Consolidated Financial Statements

HINES GLOBAL INCOME TRUST, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(UNAUDITED)

| September 30, 2018 | December 31, 2017 | ||||||

| (in thousands, except per share amounts) | |||||||

| ASSETS | |||||||

| Investment property, net | $ | 618,462 | $ | 572,833 | |||

| Cash and cash equivalents | 92,471 | 18,170 | |||||

| Restricted cash | 7,305 | 6,383 | |||||

| Derivative instruments | 64 | 110 | |||||

| Tenant and other receivables, net | 7,275 | 8,402 | |||||

| Intangible lease assets, net | 83,327 | 95,137 | |||||

| Deferred leasing costs, net | 8,801 | 4,615 | |||||

| Other assets | 3,314 | 3,367 | |||||

| Total assets | $ | 821,019 | $ | 709,017 | |||

| LIABILITIES AND EQUITY | |||||||

| Liabilities: | |||||||

| Accounts payable and accrued expenses | $ | 21,842 | $ | 15,570 | |||

| Due to affiliates | 21,184 | 16,642 | |||||

| Intangible lease liabilities, net | 14,173 | 15,939 | |||||

| Other liabilities | 9,865 | 8,601 | |||||

| Derivative instruments | 100 | — | |||||

| Distributions payable | 1,913 | 1,868 | |||||

| Note payable to affiliate | 75,000 | 11,200 | |||||

| Notes payable, net | 404,506 | 365,652 | |||||

| Total liabilities | $ | 548,583 | $ | 435,472 | |||

| Commitments and contingencies (Note 11) | — | — | |||||

| Equity: | |||||||

| Stockholders’ equity: | |||||||

| Preferred shares, $0.001 par value per share; 500,000 preferred shares authorized, none issued or outstanding as of September 30, 2018 and December 31, 2017 | — | — | |||||

| Common shares, $0.001 par value per share (Note 6) | 42 | 39 | |||||

| Additional paid-in capital | 348,776 | 336,761 | |||||

| Accumulated distributions in excess of earnings | (77,710 | ) | (68,193 | ) | |||

| Accumulated other comprehensive income (loss) | 1,328 | 4,938 | |||||

| Total stockholders’ equity | 272,436 | 273,545 | |||||

| Noncontrolling interests | — | — | |||||

| Total equity | 272,436 | 273,545 | |||||

| Total liabilities and equity | $ | 821,019 | $ | 709,017 | |||

See notes to the condensed consolidated financial statements.

1

HINES GLOBAL INCOME TRUST, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS)

For the Three and Nine Months Ended September 30, 2018 and 2017

(UNAUDITED)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| 2018 | 2017 | 2018 | 2017 | ||||||||||||

| (in thousands, except per share amounts) | |||||||||||||||

| Revenues: | |||||||||||||||

| Rental revenue | $ | 15,643 | $ | 14,869 | $ | 47,811 | $ | 42,951 | |||||||

| Other revenue | 235 | 236 | 770 | 682 | |||||||||||

| Total revenues | 15,878 | 15,105 | 48,581 | 43,633 | |||||||||||

| Expenses: | |||||||||||||||

| Property operating expenses | 3,084 | 2,372 | 8,578 | 6,629 | |||||||||||

| Real property taxes | 1,966 | 2,523 | 6,065 | 7,614 | |||||||||||

| Property management fees | 330 | 249 | 986 | 727 | |||||||||||

| Depreciation and amortization | 6,949 | 7,203 | 21,249 | 22,108 | |||||||||||

| Acquisition related expenses | — | 550 | 144 | 2,641 | |||||||||||

| Asset management and acquisition fees | 1,253 | 1,234 | 3,674 | 8,890 | |||||||||||

| Performance participation allocation | 1,237 | — | 4,013 | — | |||||||||||

| General and administrative expenses | 763 | 787 | 2,275 | 2,065 | |||||||||||

| Total expenses | 15,582 | 14,918 | 46,984 | 50,674 | |||||||||||

| Income (loss) before other income (expenses) | 296 | 187 | 1,597 | (7,041 | ) | ||||||||||

| Other income (expenses): | |||||||||||||||

| Gain (loss) on derivative instruments | (106 | ) | (26 | ) | (153 | ) | (100 | ) | |||||||

| Gain on sale of real estate | — | — | 14,491 | — | |||||||||||

| Foreign currency gains (losses) | (67 | ) | 132 | (382 | ) | 427 | |||||||||

| Interest expense | (2,845 | ) | (2,270 | ) | (8,336 | ) | (6,861 | ) | |||||||

| Interest income | 59 | 49 | 106 | 62 | |||||||||||

| Income (loss) before benefit (provision) for income taxes | (2,663 | ) | (1,928 | ) | 7,323 | (13,513 | ) | ||||||||

| Benefit (provision) for income taxes | (119 | ) | 385 | (138 | ) | 614 | |||||||||

| Net income (loss) | (2,782 | ) | (1,543 | ) | 7,185 | (12,899 | ) | ||||||||

| Net (income) loss attributable to noncontrolling interests | (3 | ) | (3 | ) | (10 | ) | (9 | ) | |||||||

| Net income (loss) attributable to common stockholders | $ | (2,785 | ) | $ | (1,546 | ) | $ | 7,175 | $ | (12,908 | ) | ||||

| Basic and diluted income (loss) per common share | $ | (0.07 | ) | $ | (0.04 | ) | $ | 0.18 | $ | (0.38 | ) | ||||

| Weighted average number of common shares outstanding | 40,397 | 38,932 | 39,765 | 34,326 | |||||||||||

| Comprehensive income (loss): | |||||||||||||||

| Net income (loss) | $ | (2,782 | ) | $ | (1,543 | ) | $ | 7,185 | $ | (12,899 | ) | ||||

| Other comprehensive income (loss): | |||||||||||||||

| Foreign currency translation adjustment | (811 | ) | 1,972 | (3,610 | ) | 6,122 | |||||||||

| Comprehensive income (loss) | $ | (3,593 | ) | $ | 429 | $ | 3,575 | $ | (6,777 | ) | |||||

| Comprehensive (income) loss attributable to noncontrolling interests | (3 | ) | (3 | ) | (10 | ) | (9 | ) | |||||||

| Comprehensive income (loss) attributable to common stockholders | $ | (3,596 | ) | $ | 426 | $ | 3,565 | $ | (6,786 | ) | |||||

See notes to the condensed consolidated financial statements.

2

HINES GLOBAL INCOME TRUST, INC.

CONDENSED CONSOLIDATED STATEMENTS OF EQUITY

For the Nine Months Ended September 30, 2018 and 2017

(UNAUDITED)

(In thousands)

| Hines Global Income Trust, Inc. Stockholders | ||||||||||||||||||||||||||

| Common Shares | Additional Paid-in Capital | Accumulated Distributions in Excess of Earnings | Accumulated Other Comprehensive Income (Loss) | Total Stockholders’ Equity | Noncontrolling Interests | |||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||

| Balance as of January 1, 2018 | 39,256 | $ | 39 | $ | 336,761 | $ | (68,193 | ) | $ | 4,938 | $ | 273,545 | $ | — | ||||||||||||

| Issuance of common shares | 2,694 | 3 | 26,960 | — | — | 26,963 | — | |||||||||||||||||||

Distributions declared (1) | — | — | — | (16,692 | ) | — | (16,692 | ) | (10 | ) | ||||||||||||||||

| Redemption of common shares | (866 | ) | — | (9,837 | ) | — | — | (9,837 | ) | — | ||||||||||||||||

| Selling commissions, dealer manager fees and distribution and stockholder servicing fees | — | — | (1,370 | ) | — | — | (1,370 | ) | — | |||||||||||||||||

| Offering costs | — | — | (3,738 | ) | — | — | (3,738 | ) | — | |||||||||||||||||

| Net income (loss) | — | — | — | 7,175 | — | 7,175 | 10 | |||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | (3,610 | ) | (3,610 | ) | — | |||||||||||||||||

| Balance as of September 30, 2018 | 41,084 | $ | 42 | $ | 348,776 | $ | (77,710 | ) | $ | 1,328 | $ | 272,436 | $ | — | ||||||||||||

| (1) | For the three months ended September 30, 2018, the Company declared cash distributions, net of any applicable distributions and stockholder servicing fees, of approximately $0.15 for Class AX, Class IX, Class D, and Class I shares, and $0.13 for Class TX, Class T, and Class S shares. For the nine months ended September 30, 2018, the Company declared cash distributions, net of any applicable distributions and stockholder servicing fees, of approximately $0.46 for Class AX and Class I shares, $0.38 for Class TX, Class T, and Class S shares, and $0.44 for Class IX and Class D shares. |

| Hines Global Income Trust, Inc. Stockholders | ||||||||||||||||||||||||||

| Common Shares | Additional Paid-in Capital | Accumulated Distributions in Excess of Earnings | Accumulated Other Comprehensive Income (Loss) | Total Stockholders’ Equity | Noncontrolling Interests | |||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||

| Balance as of January 1, 2017 | 26,542 | $ | 26 | $ | 224,134 | $ | (31,222 | ) | $ | (2,755 | ) | $ | 190,183 | $ | — | |||||||||||

| Issuance of common shares | 14,427 | 15 | 143,012 | — | — | 143,027 | — | |||||||||||||||||||

Distributions declared (1) | — | — | — | (14,132 | ) | — | (14,132 | ) | (9 | ) | ||||||||||||||||

| Redemption of common shares | (166 | ) | — | (1,445 | ) | — | — | (1,445 | ) | — | ||||||||||||||||

| Selling commissions, dealer manager fees and distribution and stockholder servicing fees | — | — | (11,131 | ) | — | — | (11,131 | ) | — | |||||||||||||||||

| Offering costs | — | — | (2,947 | ) | — | — | (2,947 | ) | — | |||||||||||||||||

| Net income (loss) | — | — | — | (12,908 | ) | — | (12,908 | ) | 9 | |||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | 6,122 | 6,122 | — | |||||||||||||||||||

| Balance as of September 30, 2017 | 40,803 | $ | 41 | $ | 351,623 | $ | (58,262 | ) | $ | 3,367 | $ | 296,769 | $ | — | ||||||||||||

| (1) | For the three months ended September 30, 2017, the Company declared cash distributions, net of any applicable distributions and stockholder servicing fees, of approximately $0.15 for Class AX shares, $0.13 for Class TX shares, and $0.15 for Class IX shares. For the nine months ended September 30, 2017, the Company declared cash distributions, net of any applicable distributions and stockholder servicing fees, of approximately $0.45 for Class AX shares, $0.37 for Class TX shares, and $0.24 for Class IX shares. |

See notes to the condensed consolidated financial statements.

3

HINES GLOBAL INCOME TRUST, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

For the Nine Months Ended September 30, 2018 and 2017

(UNAUDITED)

| 2018 | 2017 | ||||||

| (In thousands) | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | |||||||

| Net income (loss) | $ | 7,185 | $ | (12,899 | ) | ||

| Adjustments to reconcile net income (loss) to net cash from (used in) operating activities: | |||||||

| Depreciation and amortization | 21,063 | 21,710 | |||||

| Gain on sale of real estate | (14,491 | ) | — | ||||

| Foreign currency (gains) losses | 382 | (427 | ) | ||||

| (Gain) loss on derivative instruments | 153 | 100 | |||||

| Changes in assets and liabilities: | |||||||

| Change in other assets | 669 | (821 | ) | ||||

| Change in tenant and other receivables | 1,026 | (2,606 | ) | ||||

| Change in deferred leasing costs | (8,548 | ) | (620 | ) | |||

| Change in accounts payable and accrued expenses | 4,352 | 2,331 | |||||

| Change in other liabilities | 1,216 | 1,750 | |||||

| Change in due to affiliates | 3,141 | (868 | ) | ||||

| Net cash from operating activities | 16,148 | 7,650 | |||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | |||||||

| Investments in acquired properties and lease intangibles | (72,094 | ) | (131,758 | ) | |||

| Capital expenditures at operating properties | (10,900 | ) | (1,305 | ) | |||

| Proceeds from sale of real estate | 37,087 | — | |||||

| Net cash from (used in) investing activities | (45,907 | ) | (133,063 | ) | |||

| CASH FLOWS FROM FINANCING ACTIVITIES: | |||||||

| Proceeds from issuance of common shares | 18,003 | 137,085 | |||||

| Redemption of common shares | (8,498 | ) | (1,590 | ) | |||

| Payment of offering costs | — | (3,449 | ) | ||||

| Payment of selling commissions, dealer manager fees and distribution and stockholder servicing fees | (2,198 | ) | (6,525 | ) | |||

| Distributions paid to stockholders and noncontrolling interests | (7,697 | ) | (6,316 | ) | |||

| Proceeds from notes payable | 45,000 | 24,386 | |||||

| Payments on notes payable | (1,270 | ) | (1,233 | ) | |||

| Proceeds from related party note payable | 90,500 | 7,000 | |||||

| Payments on related party note payable | (26,700 | ) | (63,000 | ) | |||

| Change in security deposit liability | 46 | (24 | ) | ||||

| Deferred financing costs paid | (929 | ) | (471 | ) | |||

| Payments related to interest rate contracts | (10 | ) | (169 | ) | |||

| Net cash from (used in) financing activities | 106,247 | 85,694 | |||||

| Effect of exchange rate changes on cash, restricted cash and cash equivalents | (1,265 | ) | 1,138 | ||||

| Net change in cash, restricted cash and cash equivalents | 75,223 | (38,581 | ) | ||||

| Cash, restricted cash and cash equivalents, beginning of period | 24,553 | 99,713 | |||||

| Cash, restricted cash and cash equivalents, end of period | $ | 99,776 | $ | 61,132 | |||

See notes to the condensed consolidated financial statements.

4

HINES GLOBAL INCOME TRUST INC, INC.

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

For the Three and Nine Months Ended September 30, 2018 and 2017

1. ORGANIZATION

The accompanying interim unaudited condensed consolidated financial information has been prepared according to the rules and regulations of the United States Securities and Exchange Commission (“SEC”). In the opinion of management, all adjustments and eliminations, consisting only of normal recurring adjustments, necessary to present fairly and in conformity with accounting principles generally accepted in the United States of America (“GAAP”) the financial position of Hines Global Income Trust, Inc. as of September 30, 2018 and December 31, 2017, the results of operations for the three and nine months ended September 30, 2018 and 2017 and cash flows for the nine months ended September 30, 2018 and 2017 have been included. The results of operations for such interim periods are not necessarily indicative of the results for the full year. Certain information and footnote disclosures normally included in financial statements prepared in accordance with GAAP have been condensed or omitted according to such rules and regulations. For further information, refer to the financial statements and footnotes included in Hines Global Income Trust, Inc.’s Annual Report on Form 10-K for the year ended December 31, 2017.

Hines Global Income Trust, Inc. (the “Company”), formerly known as Hines Global REIT II, Inc., was incorporated in Maryland on July 31, 2013, to invest in a diversified portfolio of quality commercial real estate properties and other real estate investments throughout the United States and internationally, and to a lesser extent, invest in real-estate related securities. The Company is sponsored by Hines Interests Limited Partnership (“Hines”), a fully integrated global real estate investment and management firm that has acquired, developed, owned, operated and sold real estate for over 60 years. The Company is managed by Hines Global REIT II Advisors LP (the “Advisor”), an affiliate of Hines. The Company intends to conduct substantially all of its operations through Hines Global REIT II Properties, LP (the “Operating Partnership”). An affiliate of the Advisor, Hines Global REIT II Associates LP, owns less than a 1% limited partner interest in the Operating Partnership as of September 30, 2018 and the Advisor also owns the special limited partnership interest in the Operating Partnership. The Company has elected to be taxed as a real estate investment trust, or REIT, for U.S. federal income tax purposes beginning with its taxable year ended December 31, 2015.

As of September 30, 2018, the Company owned direct real estate investments in eight properties totaling 2.8 million square feet that were 97% leased. The Company raises capital for its investments through public offerings of its common stock. The Company commenced its initial public offering of up to $2.5 billion in shares of its common stock (the “Initial Offering”) in August 2014, and commenced its second public offering of up to $2.5 billion in shares of common stock including $500.0 million of shares offered under its distribution reinvestment plan (the “Follow-On Offering”) in December 2017. As of November 1, 2018, the Company had received gross offering proceeds of $449.7 million from the sale of 45.8 million shares through its public offerings, including shares issued pursuant to its distribution reinvestment plan.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The condensed consolidated financial statements of the Company included in this Quarterly Report on Form 10-Q include the accounts of Hines Global Income Trust, Inc. and the Operating Partnership (over which the Company exercises financial and operating control). All intercompany balances and transactions have been eliminated in consolidation.

Tenant and Other Receivables

Tenant and other receivable balances consist primarily of base rents, tenant reimbursements and receivables attributable to straight-line rent. Straight-line rent receivables were $4.8 million and $4.0 million as of September 30, 2018 and December 31, 2017, respectively. Straight-line rent receivable consists of the difference between the tenants’ rents calculated on a straight-line basis from the date of acquisition or lease commencement over the remaining terms of the related leases and the tenants’ actual rents due under the lease agreements and is included in tenant and other receivables in the accompanying consolidated condensed balance sheets.

Additionally, as of December 31, 2017, tenant and other receivables included $2.3 million in receivables from third-parties related to working capital reserves and transactions costs related to the acquisition of the Queen’s Court Student Residences. There were no such receivables remaining as of September 30, 2018.

5

Other Assets

Other assets included the following (in thousands):

| September 30, 2018 | December 31, 2017 | |||||||

Deferred offering costs (1) | $ | — | $ | 1,525 | ||||

| Prepaid insurance | 69 | 97 | ||||||

| Prepaid property taxes | 80 | 76 | ||||||

| Deferred tax assets | 773 | 944 | ||||||

| Other | 2,392 | (2) | 725 | |||||

| Other assets | $ | 3,314 | $ | 3,367 | ||||

| (1) | Represents offering costs incurred by the Advisor which will be released into equity as gross proceeds from the Follow-On Offering are raised. See Note 7—Related Party Transactions for additional information regarding the Company’s organization and offering costs. |

| (2) | Includes $2.0 million of capitalized acquisition costs related primarily to the acquisition of Fresh Park Venlo, which was acquired on October 5, 2018 and discussed in Note 12—Subsequent Events. |

Revenue Recognition

The Financial Accounting Standards Board ("FASB") issued accounting standards update ("ASU") 2014-09 which superseded the revenue recognition requirements under previous guidance. We adopted ASU 2014-09 on January 1, 2018. ASU 2014-09 requires the use of a new five-step model to recognize revenue from contracts with customers. The five-step model requires that the Company identify the contract with the customer, identify the performance obligations in the contract, determine the transaction price, allocate the transaction price to the performance obligations in the contract and recognize revenue when it satisfies the performance obligations. Management has concluded that the majority of the Company’s total revenue, with the exception of gains and losses from the sale of real estate, consist of rental income from leasing arrangements, which is specifically excluded from the standard. Excluding gains and losses on the sale of real estate (as discussed further below), the Company concluded that its remaining revenue streams were immaterial and, as such, the adoption of ASU 2014-09 did not have a material impact on the Company’s condensed consolidated financial statements.

As of January 1, 2018, the Company began accounting for the sale of real estate properties under ASU 2017-05 and provides for revenue recognition based on completed performance obligations, which typically occurs upon the transfer of ownership of a real estate asset. The Company sold 2819 Loker Avenue East on March 30, 2018, which was considered a non-financial real estate asset with no performance obligations subsequent to the transfer of ownership. The Company recognized a gain on sale of real estate of $14.5 million related to this sale. The Company has had no other sales of real estate assets since its inception.

Recently Adopted Accounting Pronouncements

In May 2014, the FASB, issued ASU 2014-09 to provide guidance on recognizing revenue from contracts with customers. This ASU’s core objective is for an entity to recognize revenue based on the consideration it expects to receive in exchange for goods or services. The Company has evaluated controls around the implementation of ASU 2014-09 and there was no significant impact on our control structure. See “— Revenue Recognition” above for additional information regarding the adoption of this standard.

In October 2016, the FASB issued ASU 2016-16 which removes the prohibition in ASC 740 against the immediate recognition of the current and deferred income tax effects of intra-entity transfers of assets other than inventory. The ASU is intended to reduce the complexity of ASC 740 and the diversity in practice related to the tax consequences of certain types of intra-entity asset transfers. ASU 2016-16 will be effective for annual periods beginning after December 31, 2017. The Company adopted ASU 2016-16 beginning January 1, 2018 and recorded deferred tax assets, along with a full valuation allowance, related to its subsidiaries in Ireland.

In January 2017, the FASB issued ASU 2017-01 to clarify the definition of a business with the objective of adding guidance to assist entities with evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets

6

or businesses. The Company expects that most of its real estate transactions completed after January 1, 2018 will be accounted for using the asset acquisition guidance and, accordingly, acquisition fees (if any) and expenses related to those acquisitions will be capitalized. The amendments to the FASB Accounting Standards Codification were effective for public entities for annual and interim periods in fiscal years beginning after December 15, 2017. The Company adopted ASU 2017-01 on January 1, 2018.

In February 2017, the FASB issued ASU 2017-05 to clarify that a financial asset is within the scope of Subtopic 610-20 if it meets the definition, as amended, of an in substance nonfinancial asset. The provisions of ASU 2017-05 are effective for the Company as of January 1, 2018 as described above in “— Revenue Recognition.”

New Accounting Pronouncements

In February 2016, the FASB issued ASU 2016-02 which will require companies that lease assets to recognize on the balance sheet the right-of-use assets and related lease liabilities. The accounting by companies that own the assets leased by the lessee (the lessor) will remain largely unchanged from current GAAP. The new standard requires a modified retrospective transition approach for all leases existing at, or entered into after, the date of initial application, with an option to use certain transition relief. The guidance is effective for public entities for fiscal years beginning after December 15, 2018 and interim periods within those fiscal years. Early adoption is permitted.

In July 2018, the FASB issued ASU 2018-11, which allows lessors to account for lease and non-lease components by class of underlying assets, as a single lease component if certain criteria are met. Also, the new standard indicates that companies are permitted to recognize a cumulative-effect adjustment to the opening balance of retained earnings in the period of adoption in lieu of the modified retrospective approach and provides other optional practical expedients.

The Company is in the process of evaluating the impact that the adoption of ASU 2016-02 will have on the Company’s consolidated financial statements relating to its leases, regardless of whether it is the lessor or the lessee. For leases in which the Company is the lessor, it is entitled to receive tenant reimbursements for operating expenses such as real estate taxes, insurance and common area maintenance, of which it expects to account for these lease and non-lease components as a single lease component since the timing and pattern of transfer is the same in accordance with ASU 2018-11. The Company has currently identified certain areas the Company believes may be impacted by the adoption of ASU 2016-02, which include:

| • | From time to time, the Company may have ground lease agreements in which the Company is the lessee of the land at its investment properties that the Company would account for as an operating lease. Upon adoption of ASU 2016-02, the Company will record any rights and obligations under these leases as an asset and liability at fair value in the Company’s consolidated balance sheets. |

| • | Determination of costs to be capitalized associated with leases. ASU 2016-02 will limit the capitalization associated with certain costs to costs that are a direct result of obtaining a lease. |

3. INVESTMENT PROPERTY

Investment property consisted of the following amounts as of September 30, 2018 and December 31, 2017 (in thousands):

| September 30, 2018 | December 31, 2017 | ||||||

Buildings and improvements (1) | $ | 535,611 | $ | 491,289 | |||

| Less: accumulated depreciation | (26,380 | ) | (18,172 | ) | |||

| Buildings and improvements, net | 509,231 | 473,117 | |||||

| Land | 109,231 | 99,716 | |||||

| Investment property, net | $ | 618,462 | $ | 572,833 | |||

| (1) | Included in buildings and improvements is approximately $14.0 million and $4.3 million of construction-in-progress related to the expansion of Bishop’s Square as of September 30, 2018 and December 31, 2017, respectively. In October 2017, the Company commenced construction at Bishop’s Square to add an additional floor and make various upgrades to the property. |

7

Recent Dispositions of Investment Property

In March 2018, the Company sold 2819 Loker Avenue East, a Class–A industrial property located in Carlsbad, California. The contract sales price for 2819 Loker Avenue East was $38.3 million. The Company acquired 2819 Loker Avenue East in December 2014 for a contract purchase price of $25.4 million. The Company recognized a gain on sale of this asset of $14.5 million, which was recorded in gain on sale of real estate on the condensed consolidated statements of operations and comprehensive income (loss).

Recent Acquisitions of Investment Property

In September 2018, the Company acquired Venue Museum District, a multi-family community located in Houston, Texas. The contract purchase price was $72.9 million, exclusive of transaction costs and closing prorations. Venue Museum District was constructed in 2009 and consists of 224 units that are presently 92% leased. The amount recognized for the asset acquisition as of the acquisition date was determined by allocating the net purchase price as follows (in thousands):

| Building and Improvements | Land | In-place Lease Intangibles | Total | |||

| $52,538 | $17,409 | $3,240 | $73,187 | |||

In October 2018, the Company acquired a leasehold interest in Fresh Park Venlo, a specialized logistics park located in Venlo, the Netherlands. The purchase price for Fresh Park Venlo was €117.5 million (approximately $136.3 million assuming a rate of $1.16 per EUR as of the acquisition date), exclusive of transaction costs and working capital reserves. See Note 12—Subsequent Events for additional information regarding the acquisition of Fresh Park Venlo.

As of September 30, 2018, the cost basis and accumulated amortization related to lease intangibles are as follows (in thousands):

| Lease Intangibles | |||||||||||

| In-Place Leases | Out-of-Market Lease Assets | Out-of-Market Lease Liabilities | |||||||||

| Cost | $ | 108,676 | $ | 4,689 | $ | (17,968 | ) | ||||

| Less: accumulated amortization | (27,964 | ) | (2,074 | ) | 3,795 | ||||||

| Net | $ | 80,712 | $ | 2,615 | $ | (14,173 | ) | ||||

As of December 31, 2017, the cost basis and accumulated amortization related to lease intangibles were as follows (in thousands):

| Lease Intangibles | |||||||||||

| In-Place Leases | Out-of-Market Lease Assets | Out-of-Market Lease Liabilities | |||||||||

| Cost | $ | 116,222 | $ | 4,716 | $ | (18,490 | ) | ||||

| Less: accumulated amortization | (24,430 | ) | (1,371 | ) | 2,551 | ||||||

| Net | $ | 91,792 | $ | 3,345 | $ | (15,939 | ) | ||||

Amortization expense of in-place leases was $3.7 million and $4.3 million for the three months ended September 30, 2018 and 2017, respectively. Net amortization of out-of-market leases resulted in an increase to rental revenue of $0.5 million and $0.3 million for the three months ended September 30, 2018 and 2017, respectively.

Amortization expense of in-place leases was $11.5 million and $13.9 million for the nine months ended September 30, 2018 and 2017, respectively. Net amortization of out-of-market leases resulted in an increase to rental revenue of $0.9 million and $0.8 million for the nine months ended September 30, 2018 and 2017, respectively.

8

Anticipated amortization of the Company’s in-place leases and out-of-market leases, net for the period from October 1, 2018 through December 31, 2018 and for each of the years ending December 31, 2019 through December 31, 2022 are as follows (in thousands):

| In-Place Lease | Out-of-Market Leases, Net | ||||||

| October 1, 2018 through December 31, 2018 | $ | 4,063 | $ | (157 | ) | ||

| 2019 | $ | 11,650 | $ | (694 | ) | ||

| 2020 | $ | 7,433 | $ | (1,076 | ) | ||

| 2021 | $ | 5,475 | $ | (939 | ) | ||

| 2022 | $ | 3,507 | $ | (1,007 | ) | ||

Leases

The Company has entered into non-cancelable lease agreements with tenants for space. As of September 30, 2018, the approximate fixed future minimum rentals for the period from October 1, 2018 through December 31, 2018, for each of the years ending December 31, 2019 through 2022 and thereafter related to the Company’s commercial properties are as follows (in thousands):

| Fixed Future Minimum Rentals | |||

| October 1, 2018 through December 31, 2018 | $ | 9,747 | |

| 2019 | 37,838 | ||

| 2020 | 31,555 | ||

| 2021 | 27,443 | ||

| 2022 | 22,187 | ||

| Thereafter | 124,143 | ||

| Total | $ | 252,913 | |

During the nine months ended September 30, 2018 and 2017, the Company did not earn more than 10% of its revenue from any individual tenant.

9

4. DEBT FINANCING

As of September 30, 2018 and December 31, 2017, the Company had approximately $482.5 million and $379.3 million of debt outstanding, with weighted average years to maturity of 2.6 years and 3.8 years, and a weighted average interest rate of 3.04% and 2.63%, respectively. The following table provides additional information regarding the Company’s debt outstanding at September 30, 2018 and December 31, 2017 (in thousands):

| Description | Origination or Assumption Date | Maturity Date | Maximum Capacity in Functional Currency | Interest Rate Description | Interest Rate as of September 30, 2018 | Principal Outstanding at September 30, 2018 | Principal Outstanding at December 31, 2017 | |||||||||||||

| Secured Mortgage Debt | ||||||||||||||||||||

| Bishop's Square | 3/3/2015 | 3/2/2022 | € | 55,200 | Euribor + 1.30% (1) | 1.30% | $ | 64,043 | $ | 66,124 | ||||||||||

| Domain Apartments | 1/29/2016 | 1/29/2020 | $ | 34,300 | Libor + 1.60% | 3.86% | 34,300 | 34,300 | ||||||||||||

| Cottonwood Corporate Center | 7/5/2016 | 8/1/2023 | $ | 78,000 | Fixed | 2.98% | 74,540 | 75,811 | ||||||||||||

| Goodyear Crossing II | 8/18/2016 | 8/18/2021 | $ | 29,000 | Libor + 2.00% | 4.11% | 29,000 | 29,000 | ||||||||||||

| Rookwood Commons | 1/6/2017 | 7/1/2020 | $ | 67,000 | Fixed | 3.13% | 67,000 | 67,000 | ||||||||||||

| Rookwood Pavilion | 1/6/2017 | 7/1/2020 | $ | 29,000 | Fixed | 2.87% | 29,000 | 29,000 | ||||||||||||

| Montrose Student Residences | 3/24/2017 | 3/23/2022 | € | 22,605 | Euribor + 1.85% (2) | 1.85% | 26,226 | 27,079 | ||||||||||||

| Queen's Court Student Residences | 12/18/2017 | 12/18/2022 | £ | 29,500 | Libor + 2.00% (3) | 2.68% | 38,424 | 39,798 | ||||||||||||

| Venue Museum District | 9/21/2018 | 10/9/2020 | $ | 45,000 | Libor + 1.95% (4) | 4.13% | 45,000 | — | ||||||||||||

| Notes Payable | $ | 407,533 | $ | 368,112 | ||||||||||||||||

| Affiliate Note Payable | ||||||||||||||||||||

| Credit Facility with Hines | 10/2/2017 | 12/31/2018 | $ | 75,000 | Variable | 3.71% | 75,000 | 11,200 | ||||||||||||

| Total Note Payable to Affiliate | $ | 75,000 | $ | 11,200 | ||||||||||||||||

| Total Principal Outstanding | $ | 482,533 | $ | 379,312 | ||||||||||||||||

| Unamortized discount | (369 | ) | (528 | ) | ||||||||||||||||

| Unamortized financing fees | (2,658 | ) | (1,932 | ) | ||||||||||||||||

| Total | $ | 479,506 | $ | 376,852 | ||||||||||||||||

| (1) | On the loan origination date, and as extended on February 20, 2018, the Company entered into a 2.00% Euribor interest rate cap agreement for the full amount borrowed as an economic hedge against the variability of future interest rates on this borrowing. |

| (2) | On the loan origination date, the Company entered into a 1.25% Euribor interest rate cap agreement for €17.0 million (approximately $19.7 million assuming a rate of $1.16 per EUR as of September 30, 2018) of the full amount borrowed as an economic hedge against the variability of future interest rates on this borrowing. |

| (3) | On the loan origination date, the Company entered into a 2.00% Libor interest rate cap agreement for £22.1 million (approximately $28.8 million assuming a rate of $1.30 per GBP as of September 30, 2018) of the full amount borrowed as an economic hedge against the variability of future interest rates on this borrowing. |

| (4) | On the loan origination date, the Company entered into a 3.50% Libor interest rate cap agreement for the full amount borrowed as an economic hedge against the variability of future interest rates on this borrowing. |

Hines Credit Facility

For the period from January 2018 through September 2018, the Company made draws of $90.5 million and made payments of $26.7 million under its uncommitted loan agreement with Hines (the “Hines Credit Facility”). The Company had $75.0 million outstanding on September 30, 2018. No subsequent draws or payments were made under the Hines Credit Facility from October 1, 2018 through November 14, 2018.

Financial Covenants

The Company’s loan documents for the debt described in the table above contain customary events of default, with corresponding grace periods, including payment defaults, bankruptcy-related defaults, and customary covenants, including limitations on liens and indebtedness and maintenance of certain financial ratios. The Company is not aware of any instances of noncompliance with financial covenants as of September 30, 2018.

10

Principal Payments on Debt

The Company is required to make the following principal payments on its outstanding notes payable for the period from October 1, 2018 through December 31, 2018, for each of the years ending December 31, 2019 through December 31, 2022 and for the period thereafter (in thousands).

| Payments Due by Year | |||||||||||||||||||||||

| October 1, 2018 through December 31, 2018 | 2019 | 2020 | 2021 | 2022 | Thereafter | ||||||||||||||||||

| Principal payments | $ | 75,430 | $ | 1,751 | $ | 177,104 | $ | 30,859 | $ | 130,608 | $ | 66,781 | |||||||||||

5. DERIVATIVE INSTRUMENTS

The Company has entered into several interest rate cap contracts in connection with certain of its secured mortgage loans in order to limit its exposure against the variability of future interest rates on its variable interest rate borrowings. The Company’s interest rate cap contracts have economically limited the interest rate on the loan to which they relate. The Company has not designated these derivatives as hedges for accounting purposes. The Company has not entered into a master netting arrangement with its third-party counterparty and does not offset on its condensed consolidated balance sheets the fair value amount recorded for its derivative instruments.

The Company has also entered into foreign currency forward contracts as economic hedges against the variability of foreign exchange rates related to its international investments. These forward contracts fixed the currency exchange rates on each of the investments to which they related. The Company did not designate any of these contracts as fair value or cash flow hedges for accounting purposes. In September 2018, the Company entered into a €43.0 million foreign currency forward contract with an effective date of September 28, 2018 and a trade date of October 1, 2018, in connection with the purchase of Fresh Park Venlo. See Note 12—Subsequent Events for additional information regarding the purchase of Fresh Park Venlo.

The table below provides additional information regarding the Company’s interest rate contracts (in thousands, except percentages).

| Interest Rate Contracts | |||||||||||||

| Type | Effective Date | Expiration Date | Notional Amount (1) | Interest Rate Received | Pay Rate /Strike Rate | ||||||||

| Interest rate cap | March 3, 2015 | April 25, 2020 (2) | $ | 64,043 | Euribor | 2.00 | % | ||||||

| Interest rate cap | March 24, 2017 | March 23, 2022 | $ | 19,670 | Euribor | 1.25 | % | ||||||

| Interest rate cap | December 20, 2017 | December 20, 2020 | $ | 28,818 | Libor | 2.00 | % | ||||||

| Interest rate cap | September 21, 2018 | October 9, 2020 | $ | 45,000 | Libor | 3.50 | % | ||||||

| (1) | For notional amounts denominated in a foreign currency, amounts have been translated at a rate based on the rate in effect on September 30, 2018. |

| (2) | On February 20, 2018, the Company extended the expiration date on its interest rate cap contract relating to the Bishop’s Square secured facility agreement with DekaBank Deutsche Girozentrale from April 25, 2018 to April 25, 2020. |

6. STOCKHOLDERS’ EQUITY

Public Offering

On November 30, 2017, the Company (i) redesignated its issued and outstanding Class A shares of common stock, Class T shares of common stock, Class I shares of common stock and Class J shares of common stock as “Class AX shares,” “Class TX shares,” “Class IX shares” and “Class JX shares,” (collectively, the “IPO Shares”) respectively, and (ii) reclassified the authorized but unissued portion of its common stock into four additional classes of shares of common stock: “Class T shares,” “Class S shares,” “Class D shares,” and “Class I shares.” The Company is offering its shares of common stock in the Follow-On Offering in any combination of Class T shares, Class S shares, Class D shares and Class I shares (collectively, the “Follow-On Offering Shares”). All shares of the Company’s common stock have the same voting rights and rights upon liquidation,

11

although distributions received by the Company’s stockholders are expected to differ due to the distribution and stockholder servicing fees payable with respect to the applicable share classes, which reduce distributions.

Common Stock

As of September 30, 2018 and December 31, 2017, the Company had the following classes of shares of common stock authorized, issued and outstanding (in thousands):

| September 30, 2018 | December 31, 2017 | ||||||||||

| Shares Authorized | Shares Issued | Shares Outstanding | Shares Authorized | Shares Issued | Shares Outstanding | ||||||

| Class AX common stock, $0.001 par value per share | 40,000 | 19,178 | 19,178 | 40,000 | 19,206 | 19,206 | |||||

| Class TX common stock, $0.001 par value per share | 40,000 | 20,026 | 20,026 | 40,000 | 19,958 | 19,958 | |||||

| Class IX common stock, $0.001 par value per share | 10,000 | 95 | 95 | 10,000 | 92 | 92 | |||||

| Class JX common stock, $0.001 par value per share | 10,000 | — | — | 10,000 | — | — | |||||

| Class T common stock, $0.001 par value per share | 350,000 | 1,195 | 1,195 | 350,000 | — | — | |||||

| Class S common stock, $0.001 par value per share | 350,000 | — | — | 350,000 | — | — | |||||

| Class D common stock, $0.001 par value per share | 350,000 | 583 | 583 | 350,000 | — | — | |||||

| Class I common stock, $0.001 par value per share | 350,000 | 7 | 7 | 350,000 | — | — | |||||

The tables below provide information regarding the issuances and redemptions of each class of the Company’s common stock during the nine months ended September 30, 2018 and 2017 (in thousands). There were no Class JX and S shares issued, redeemed or outstanding during the nine months ended September 30, 2018.

| Class AX | Class TX | Class IX | Class T | Class D | Class I | Total | ||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | Shares | Amount | Shares | Amount | Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||

| Balance as of January 1, 2018 | 19,206 | $ | 19 | 19,958 | $ | 20 | 92 | $ | — | — | $ | — | — | $ | — | — | $ | — | 39,256 | $ | 39 | |||||||||||||||||||||||||||

| Issuance of common shares | 428 | — | 478 | 1 | 3 | — | 1,195 | 1 | 583 | 1 | 7 | — | 2,694 | 3 | ||||||||||||||||||||||||||||||||||

| Redemption of common shares | (456 | ) | — | (410 | ) | — | — | — | — | — | — | — | — | — | (866 | ) | — | |||||||||||||||||||||||||||||||

| Balance as of September 30, 2018 | 19,178 | $ | 19 | 20,026 | $ | 21 | 95 | $ | — | 1,195 | $ | 1 | 583 | $ | 1 | 7 | $ | — | 41,084 | $ | 42 | |||||||||||||||||||||||||||

| Class AX | Class TX | Class IX | Total | ||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | Shares | Amount | ||||||||||||||||||||

| Balance as of January 1, 2017 | 16,468 | $ | 16 | 10,074 | $ | 10 | — | $ | — | 26,542 | $ | 26 | |||||||||||||||

| Issuance of common shares | 3,711 | 4 | 10,625 | 11 | 91 | — | 14,427 | 15 | |||||||||||||||||||

| Redemption of common shares | (151 | ) | — | (15 | ) | — | — | — | (166 | ) | — | ||||||||||||||||

| Balance as of September 30, 2017 | 20,028 | $ | 20 | 20,684 | $ | 21 | 91 | $ | — | 40,803 | $ | 41 | |||||||||||||||

Distributions

With the authorization of the Company’s board of directors, the Company declared distributions monthly from January 2018 through November 2018 at a gross distribution rate of $0.05083 per month for each share class, less any applicable distribution and stockholder servicing fees.

Distributions will be made on all classes of the Company’s common stock at the same time. All distributions were paid in cash or reinvested in shares of the Company’s common stock for those participating in the Company’s distribution reinvestment plan and have been paid or issued, respectively, on the first business day following the completion of the month to which they relate. Distributions reinvested pursuant to the Company’s distribution reinvestment plan were reinvested in shares of the same class as the shares on which the distributions were made. Some or all of the cash distributions may be paid from sources other than cash flows from operations.

12

The following table outlines the Company’s total cash distributions declared to stockholders for each of the quarters ended during 2018 and 2017, including the breakout between the distributions declared in cash and those reinvested pursuant to the Company’s distribution reinvestment plan (in thousands).

| Stockholders | ||||||||||||

| Distributions for the Three Months Ended | Cash Distributions | Distributions Reinvested | Total Declared | |||||||||

| 2018 | ||||||||||||

| September 30, 2018 | $ | 2,617 | $ | 3,033 | $ | 5,650 | ||||||

| June 30, 2018 | 2,554 | 2,974 | 5,528 | |||||||||

| March 31, 2018 | 2,544 | 2,970 | 5,514 | |||||||||

| Total | $ | 7,715 | $ | 8,977 | $ | 16,692 | ||||||

| 2017 | ||||||||||||

| December 31, 2017 | $ | 2,636 | $ | 3,005 | $ | 5,641 | ||||||

| September 30, 2017 | 2,532 | 2,901 | 5,433 | |||||||||

June 30, 2017 (1) | 2,225 | 2,565 | 4,790 | |||||||||

March 31, 2017 (2) | 1,833 | 2,076 | 3,909 | |||||||||

| Total | $ | 9,226 | $ | 10,547 | $ | 19,773 | ||||||

| (1) | Includes $1.5 million of distributions that were declared on March 23, 2017 with respect to daily record dates for each day during the month of April 2017, which were paid in cash or reinvested in shares on May 1, 2017. |

| (2) | Includes distributions declared as of daily record dates for the three months ended March 31, 2017, but excludes $1.5 million of distributions that were declared on March 23, 2017 with respect to daily record dates for each day during the month of April 2017. These April 2017 distributions were paid in cash or reinvested in shares on May 1, 2017. |

13

7. RELATED PARTY TRANSACTIONS

The table below outlines fees and expense reimbursements incurred that are payable by the Company to Hines and its affiliates for the periods indicated below (in thousands):

| Incurred | ||||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | Unpaid as of | ||||||||||||||||||||||

| Type and Recipient | 2018 | 2017 | 2018 | 2017 | September 30, 2018 | December 31, 2017 | ||||||||||||||||||

| Selling Commissions- Dealer Manager | $ | 313 | $ | 971 | $ | 349 | $ | 4,006 | $ | — | $ | — | ||||||||||||

| Dealer Manager Fee- Dealer Manager | 55 | 474 | 61 | 1,735 | — | — | ||||||||||||||||||

| Distribution & Stockholder Servicing Fees- Dealer Manager | 978 | 1,719 | 960 | 5,390 | 7,421 | 8,249 | ||||||||||||||||||

| Organization and Offering Costs- the Advisor | 711 | 1,535 | 2,213 | 3,921 | 7,941 | 5,728 | ||||||||||||||||||

| Acquisition Fees- the Advisor | — | — | — | 5,273 | — | 2 | ||||||||||||||||||

| Asset Management Fees- the Advisor | 1,253 | 1,234 | 3,674 | 3,617 | 1,388 | 1,561 | ||||||||||||||||||

Other- the Advisor (1) | 366 | 534 | 1,038 | 1,027 | 273 | 464 | ||||||||||||||||||

Performance Participation Allocation- the Advisor (2) | 1,237 | — | 4,013 | — | 4,013 | 251 | ||||||||||||||||||

Interest expense- Hines (3) | 56 | — | 254 | 388 | 56 | 10 | ||||||||||||||||||

| Property Management Fees- Hines | 259 | 237 | 712 | 618 | 20 | 37 | ||||||||||||||||||

| Construction Management Fees- Hines | 75 | — | 326 | — | — | 19 | ||||||||||||||||||

| Leasing Fees- Hines | 95 | — | 205 | — | 62 | 17 | ||||||||||||||||||

| Expense Reimbursement- Hines (with respect to management and operations of the Company's properties) | 472 | 477 | 1,374 | 1,159 | 10 | 304 | ||||||||||||||||||

| Total | $ | 5,870 | $ | 7,181 | $ | 15,179 | $ | 27,134 | $ | 21,184 | $ | 16,642 | ||||||||||||

| (1) | Includes amounts the Advisor paid on behalf of the Company such as general and administrative expenses and acquisition-related expenses. These amounts are generally reimbursed to the Advisor during the month following the period in which they are incurred. |

| (2) | As of December 6, 2017, through its ownership of the special limited partner interest in the Operating Partnership, the Advisor is entitled to an annual performance participation allocation of 12.5% of the Operating Partnership’s total return. Total return is defined as distributions paid or accrued plus the change in net asset value of the Company’s shares of common stock for the applicable period. This performance participation allocation is subject to investors earning a 5% return, after considering the effect of any losses carried forward from the prior period (as defined in the Operating Partnership agreement). The performance participation allocation accrues monthly and is payable after the completion of each calendar year. |

| (3) | Includes amounts paid related to the Hines Credit Facility. |

8. FAIR VALUE MEASUREMENTS

Fair values determined by Level 1 inputs utilize quoted prices (unadjusted) in active markets for identical assets or liabilities the Company has the ability to access. Fair values determined by Level 2 inputs utilize inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. Level 2 inputs include quoted prices for similar assets and liabilities in active markets and inputs other than quoted prices observable for the asset or liability, such as interest rates and yield curves observable at commonly quoted intervals. Level 3 inputs are unobservable inputs for the asset or liability, and include situations where there is little, if any, market activity for the asset or liability. In instances in which the inputs used to measure fair value may fall into different levels of the fair value hierarchy, the level in the fair value hierarchy within which the fair value measurement in its entirety has been determined is based on the lowest level input significant to the fair value measurement in its entirety. The Company’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment, and considers factors specific to the asset or liability.

14

As of September 30, 2018, the Company estimated that the fair value of its notes payable, excluding deferred financing costs, which had a book value of $482.5 million, was $476.2 million. As of December 31, 2017, the Company estimated that the fair value of its notes payable, excluding deferred financing costs, which had a book value of $379.3 million, was $376.5 million. Management has utilized available market information such as interest rate and spread assumptions of notes payable with similar terms and remaining maturities, to estimate the amounts required to be disclosed. Although the Company has determined that the majority of the inputs used to value its notes payable fall within Level 2 of the fair value hierarchy, the credit quality adjustments associated with its fair value of notes payable utilize Level 3 inputs. However, the Company has assessed the significance of the impact of the credit quality adjustments on the overall valuations of the fair market value of its notes payable and has determined they are not significant. Other financial instruments not measured at fair value on a recurring basis include cash and cash equivalents, restricted cash, tenant and other receivables, accounts payable and accrued expenses, other liabilities, due to affiliates and distributions payable. The carrying value of these items reasonably approximates their fair value based on their highly-liquid nature and/or short-term maturities. Due to the short-term nature of these instruments, Level 1 inputs are utilized to estimate the fair value of the cash and cash equivalents and restricted cash and Level 2 inputs are utilized to estimate the fair value of the remaining financial instruments.

9. REPORTABLE SEGMENTS

As described previously, the Company intends to invest the net proceeds from its public offerings in a diversified portfolio of quality commercial real estate properties and other real estate investments throughout the United States and internationally. The Company’s current business consists of owning, operating, acquiring, developing, investing in, and disposing of real estate assets. All of the Company’s consolidated revenues and property operating expenses as of September 30, 2018 are from the Company’s consolidated real estate properties owned as of that date, other than 2819 Loker Avenue East, which was sold on March 30, 2018. As a result, the Company’s operating segments have been classified into six reportable segments: domestic office investments, domestic residential/living investments, domestic retail investments, domestic other investments, international office investments, and international residential/living investments.

The tables below provide additional information related to each of the Company’s segments (in thousands) and a reconciliation to the Company’s net income (loss), as applicable. “Corporate-Level Accounts” includes amounts incurred by the corporate-level entities which are not allocated to any of the reportable segments.

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| 2018 | 2017 | 2018 | 2017 | ||||||||||||

| Total Revenue | |||||||||||||||

| Domestic office investments | $ | 4,109 | $ | 3,986 | $ | 12,246 | $ | 11,582 | |||||||

| Domestic residential/living investments | 1,467 | 1,155 | 3,910 | 3,496 | |||||||||||

| Domestic retail investments | 5,262 | 4,876 | 15,316 | 14,523 | |||||||||||

| Domestic other investments | 1,254 | 1,884 | 4,547 | 5,706 | |||||||||||

| International office investments | 1,947 | 2,413 | 6,009 | 6,703 | |||||||||||

| International residential/living investments | 1,839 | 791 | 6,553 | 1,623 | |||||||||||

| Total Revenue | $ | 15,878 | $ | 15,105 | $ | 48,581 | $ | 43,633 | |||||||

For the three and nine months ended September 30, 2018 and 2017, the Company’s total revenue was attributable to the following countries:

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||

| 2018 | 2017 | 2018 | 2017 | ||||||||

| Total Revenue | |||||||||||

| United States | 76 | % | 79 | % | 74 | % | 81 | % | |||

| Ireland | 17 | % | 21 | % | 18 | % | 19 | % | |||

| United Kingdom | 7 | % | — | % | 8 | % | — | % | |||

15

For the three and nine months ended September 30, 2018 and 2017, the Company’s property revenues in excess of expenses by segment were as follows (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| 2018 | 2017 | 2018 | 2017 | ||||||||||||

Property revenues in excess of expenses (1) | |||||||||||||||

| Domestic office investments | $ | 2,756 | $ | 2,729 | $ | 8,328 | $ | 7,896 | |||||||

| Domestic residential/living investments | 991 | 719 | 2,582 | 2,228 | |||||||||||

| Domestic retail investments | 3,426 | 2,566 | 9,833 | 7,672 | |||||||||||

| Domestic other investments | 1,015 | 1,449 | 3,535 | 4,396 | |||||||||||

| International office investments | 1,563 | 2,030 | 4,688 | 5,424 | |||||||||||

| International residential/living investments | 747 | 468 | 3,986 | 1,047 | |||||||||||

| Property revenues in excess of expenses | $ | 10,498 | $ | 9,961 | $ | 32,952 | $ | 28,663 | |||||||

| (1) | Revenues less property operating expenses, real property taxes and property management fees. |

As of September 30, 2018 and December 31, 2017, the Company’s total assets by segment were as follows (in thousands):

| September 30, 2018 | December 31, 2017 | ||||||

| Total Assets | |||||||

| Domestic office investments | $ | 131,690 | $ | 130,901 | |||

| Domestic residential/living investments | 126,643 | 53,344 | |||||

| Domestic retail investments | 198,959 | 202,093 | |||||

| Domestic other investments | 49,255 | 76,745 | |||||

| International office investments | 124,066 | 116,494 | |||||

| International residential/living investments | 116,716 | 121,919 | |||||

| Corporate-level accounts | 73,690 | 7,521 | |||||

| Total Assets | $ | 821,019 | $ | 709,017 | |||

As of September 30, 2018 and December 31, 2017, the Company’s total assets were attributable to the following countries:

| September 30, 2018 | December 31, 2017 | ||||

| Total Assets | |||||

| United States | 71 | % | 67 | % | |

| Ireland | 21 | % | 23 | % | |

| United Kingdom | 8 | % | 10 | % | |

16

For the three and nine months ended September 30, 2018 and 2017 the Company’s reconciliation of the Company’s property revenues in excess of expenses to the Company’s net income (loss) is as follows (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| 2018 | 2017 | 2018 | 2017 | ||||||||||||

| Reconciliation to property revenue in excess of expenses | |||||||||||||||

| Net income (loss) | $ | (2,782 | ) | $ | (1,543 | ) | $ | 7,185 | $ | (12,899 | ) | ||||

| Depreciation and amortization | 6,949 | 7,203 | 21,249 | 22,108 | |||||||||||

| Acquisition related expenses | — | 550 | 144 | 2,641 | |||||||||||

| Asset management and acquisition fees | 1,253 | 1,234 | 3,674 | 8,890 | |||||||||||

| Performance participation allocation | 1,237 | — | 4,013 | — | |||||||||||

| General and administrative expenses | 763 | 787 | 2,275 | 2,065 | |||||||||||

| (Gain) loss on derivative instruments | 106 | 26 | 153 | 100 | |||||||||||

| Gain on sale of real estate | — | — | (14,491 | ) | — | ||||||||||

| Foreign currency (gains) losses | 67 | (132 | ) | 382 | (427 | ) | |||||||||

| Interest expense | 2,845 | 2,270 | 8,336 | 6,861 | |||||||||||

| Interest income | (59 | ) | (49 | ) | (106 | ) | (62 | ) | |||||||

| (Benefit) provision for income taxes | 119 | (385 | ) | 138 | (614 | ) | |||||||||

| Total property revenues in excess of expenses | $ | 10,498 | $ | 9,961 | $ | 32,952 | $ | 28,663 | |||||||

10. SUPPLEMENTAL CASH FLOW DISCLOSURES

Supplemental cash flow disclosures for the nine months ended September 30, 2018 and 2017 (in thousands):

| Nine Months Ended September 30, | |||||||

| 2018 | 2017 | ||||||

| Supplemental Disclosure of Cash Flow Information | |||||||

| Cash paid for interest | $ | 7,784 | $ | 6,173 | |||

| Supplemental Schedule of Non-Cash Investing and Financing Activities | |||||||

| Distributions declared and unpaid | $ | 1,913 | $ | 1,833 | |||

| Distributions reinvested | $ | 8,959 | $ | 7,187 | |||

| Shares tendered for redemption | $ | 1,360 | $ | — | |||

| Other receivables | $ | — | $ | 384 | |||

| Non-cash net liabilities assumed | $ | 1,146 | $ | 1,652 | |||

| Assumption of mortgage upon acquisition of property | $ | — | $ | 95,260 | |||

| Offering costs payable to the Advisor | $ | 2,213 | $ | 472 | |||

| Selling commissions, dealer manager fees and distribution and stockholder servicing fees payable to the Dealer Manager | $ | 960 | $ | 4,662 | |||

| Accrued capital additions | $ | 2,385 | $ | 754 | |||

| Accrued acquisition costs | $ | 1,730 | $ | — | |||

11. COMMITMENTS AND CONTINGENCIES

The Company may be subject to various legal proceedings and claims that arise in the ordinary course of business. These matters are generally covered by insurance. While the resolution of these matters cannot be predicted with certainty, management believes the final outcome of such matters will not have a material adverse effect on the Company’s condensed consolidated financial statements.

17

12. SUBSEQUENT EVENTS

Fresh Park Venlo

In October 2018, the Company acquired a leasehold interest in Fresh Park Venlo, a specialized logistics park located in Venlo, the Netherlands. Fresh Park Venlo is comprised of 23 buildings constructed between 1960 and 2018, and consists of 2,863,630 square feet of net rentable area that is, in the aggregate, 95% leased to more than 60 tenants. The purchase price for Fresh Park Venlo was €117.5 million (approximately $136.3 million assuming a rate of $1.16 per EUR as of the acquisition date), exclusive of transaction costs and working capital reserves. In connection with the acquisition of the property, the Company entered into a third-party mortgage loan for the principal sum of approximately €75.0 million (approximately $87.0 million assuming a rate of $1.16 per EUR as of the acquisition date). The mortgage loan has a floating interest rate of Euribor + 1.50% per annum. Repayment of principal is due upon the maturity of the mortgage loan on August 15, 2023.

*****

18

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited condensed consolidated financial statements and the notes thereto included in Item 1 in this Quarterly Report on Form 10-Q. The following discussion should also be read in conjunction with our audited consolidated financial statements and the notes thereto and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in our Annual Report on Form 10-K for the year ended December 31, 2017.

Cautionary Note Regarding Forward-Looking Statements

This Quarterly Report on Form 10-Q includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 (the “Securities Act”), as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as amended. Such statements include statements concerning future financial performance and distributions, future debt and financing levels, acquisitions and investment objectives, payments to Hines Global REIT II Advisors LP (the “Advisor”), and its affiliates and other plans and objectives of management for future operations or economic performance, or assumptions or forecasts related thereto as well as all other statements that are not historical statements. These statements are only predictions. We caution that forward-looking statements are not guarantees. Actual events or our investments and results of operations could differ materially from those expressed or implied in forward-looking statements. Forward-looking statements are typically identified by the use of terms such as “may,” “should,” “expect,” “could,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “continue,” “predict,” “potential” or the negative of such terms and other comparable terminology.

The forward-looking statements included in this Quarterly Report on Form 10-Q are based on our current expectations, plans, estimates, assumptions and beliefs that involve numerous risks and uncertainties. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions, the availability of future financing and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. Any of the assumptions underlying forward-looking statements could prove to be inaccurate. To the extent that our assumptions differ from actual results, our ability to meet such forward-looking statements, including our ability to generate positive cash flow from operations, pay distributions to our shareholders and maintain the value of any real estate investments and real estate-related investments in which we may hold an interest in the future, may be significantly hindered.

The following are some of the risks and uncertainties, which could cause actual results to differ materially from those presented in certain forward-looking statements:

| — | Whether we will have the opportunity to invest offering and distribution reinvestment plan proceeds to acquire properties or other investments or whether such proceeds will be needed to redeem shares or for other purposes, and if proceeds are available for investment, our ability to make such investments in a timely manner and at appropriate amounts that provide acceptable returns; |

| — | Competition for tenants and real estate investment opportunities, including competition with other programs sponsored by or affiliated with Hines Interests Limited Partnership (“Hines”); |

| — | Our reliance on our Advisor, Hines and affiliates of Hines for our day-to-day operations and the selection of real estate investments, and our Advisor’s ability to attract and retain high-quality personnel who can provide service at a level acceptable to us; |

| — | Risks associated with conflicts of interests that result from our relationship with our Advisor and Hines, as well as conflicts of interests certain of our officers and directors face relating to the positions they hold with other entities; |

| — | The potential need to fund tenant improvements, lease-up costs or other capital expenditures, as well as increases in property operating expenses and costs of compliance with environmental matters or discovery of previously undetected environmentally hazardous or other undetected adverse conditions at our properties; |

| — | The availability and timing of distributions we may pay is uncertain and cannot be assured; |

19

| — | Our distributions have been paid using cash flows from financing activities, including proceeds from our public offering, as well as cash from the waiver of fees by our Advisor, and some or all of the distributions we pay in the future may be paid from similar sources or sources such as cash advances by our Advisor, cash resulting from a waiver or deferral of fees, borrowings and/or proceeds from the offering. When we pay distributions from sources other than our cash flow from operations, we will have less funds available for the acquisition of properties, and your overall return may be reduced; |

| — | Risks associated with debt and our ability to secure financing; |

| — | Risks associated with adverse changes in general economic or local market conditions, including terrorist attacks and other acts of violence, which may affect the markets in which we and our tenants operate; |

| — | Catastrophic events, such as hurricanes, earthquakes, tornadoes and terrorist attacks; and our ability to secure adequate insurance at reasonable and appropriate rates; |

| — | The failure of any bank in which we deposit our funds could reduce the amount of cash we have available to pay distributions and make additional investments; |

| — | Changes in governmental, tax, real estate and zoning laws and regulations and the related costs of compliance and increases in our administrative operating expenses, including expenses associated with operating as a public company; |

| — | International investment risks, including the burden of complying with a wide variety of foreign laws and the uncertainty of such laws, the tax treatment of transaction structures, political and economic instability, foreign currency fluctuations, and inflation and governmental measures to curb inflation may adversely affect our operations and our ability to make distributions; |

| — | The lack of liquidity associated with our assets; and |

| — | Our ability to qualify as a real estate investment trust (“REIT”) for federal income tax purposes. |

These risks are more fully discussed in, and all forward-looking statements should be read in light of, all of the risk factors discussed in “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2017.

You are cautioned not to place undue reliance on any forward-looking statements included in this Quarterly Report on Form 10-Q. All forward-looking statements are made as of the date of this Quarterly Report on Form 10-Q and the risk that actual results will differ materially from the expectations expressed in this Quarterly Report on Form 10-Q may increase with the passage of time. In light of the significant uncertainties inherent in the forward-looking statements included in this Quarterly Report on Form 10-Q, the inclusion of such forward-looking statements should not be regarded as a representation by us or any other person that the objectives and plans set forth in this Quarterly Report on Form 10-Q will be achieved. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by reference to these risks and uncertainties. Each forward-looking statement speaks only as of the date of the particular statement, and we do not undertake to update any forward-looking statement.

The Company

Hines Global Income Trust, Inc. (“Hines Global”), formerly known as Hines Global REIT II, Inc., was formed as a Maryland corporation on July 31, 2013, for the purpose of investing in a diversified portfolio of quality commercial real estate properties and other real estate investments located throughout the United States and internationally, and to a lesser extent, invest in real-estate related securities. Hines Global is sponsored by Hines Interests Limited Partnership (“Hines”), a fully integrated global real estate investment and management firm that has acquired, developed, owned, operated and sold real estate for over 60 years. The Company has elected to be taxed as a real estate investment trust (“REIT”) for U.S. federal income tax purposes beginning with its taxable year ended December 31, 2015.

We raise capital for our investments through public offerings of our common stock. We commenced our initial public offering of up to $2.5 billion in shares of our common stock (the “Initial Offering”) in August 2014 and commenced our second public offering of up to $2.5 billion in shares of common stock including $500.0 million of shares offered under our distribution reinvestment plan (the “Follow-On Offering”) in December 2017. It is our intention to conduct a continuous offering for an indefinite period of time by conducting additional offerings of our shares following the conclusion of the Follow-On Offering. As of November 1, 2018, we had received gross offering proceeds of $449.7 million from the sale of 45.8 million shares through our public offerings, including shares issued pursuant to our distribution reinvestment plan.

20

Portfolio Highlights

We intend to meet our primary investment objectives by investing in a portfolio of real estate properties and other real estate investments that relate to properties that are generally diversified by geographic area, lease expirations and tenant industries. As of September 30, 2018 and including the effect of the acquisition of Fresh Park Venlo in October 2018, we owned nine real estate investments consisting of 5.7 million square feet that were 96% leased.

Recent Dispositions of Investment Property

We sold 2819 Loker Avenue East on March 30, 2018 for a contract sales price of $38.3 million. We acquired 2819 Loker Avenue East in December 2014 for a net purchase price of $25.4 million and recognized a $14.5 million gain on the sale.

Recent Acquisitions of Investment Property

We acquired Venue Museum District in September 2018 for a contract purchase price of $72.9 million, exclusive of transaction costs and closing prorations.

In October 2018, we acquired a leasehold interest in Fresh Park Venlo, a specialized logistics park located in Venlo, the Netherlands. The purchase price for Fresh Park Venlo was €117.5 million (approximately $136.3 million assuming a rate of $1.16 per EUR as of the acquisition date), exclusive of transaction costs and working capital reserves. See “—Subsequent Events” for additional information regarding the purchase of Fresh Park Venlo.

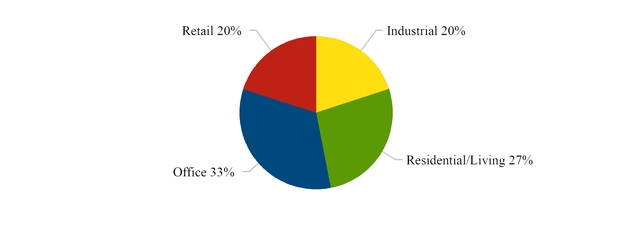

The following chart depicts the percentage of our portfolio’s investment types based on the estimated value of each real estate investment as of September 30, 2018 (“Estimated Values”), which are consistent with the values used to determine our net asset value per share on that date, for properties acquired prior to September 30, 2018 and as of the date of acquisition with respect to Fresh Park Venlo, which was acquired on October 5, 2018.

21

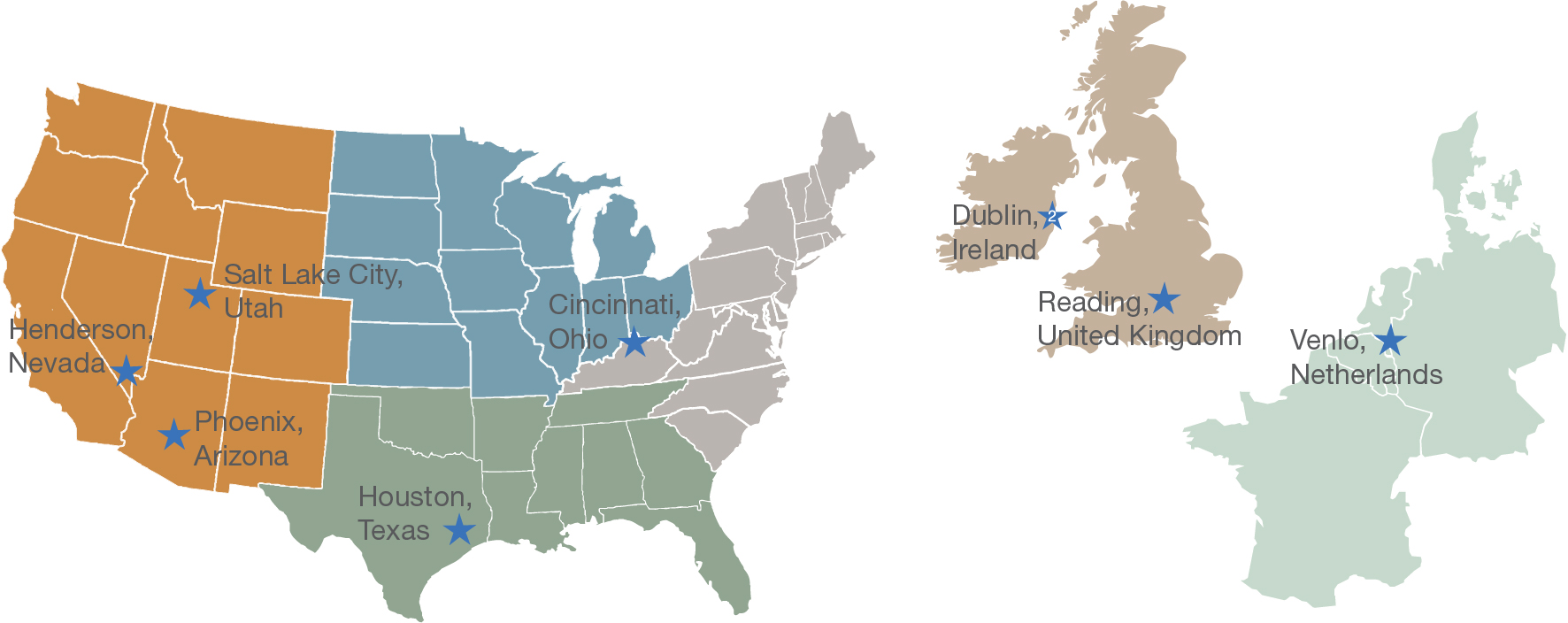

The following charts depict the location of our real estate investments as of September 30, 2018 and also includes the effect of the acquisition of Fresh Park Venlo, which was acquired on October 5, 2018. Approximately 56% of our portfolio is located throughout the United States and approximately 44% is located internationally, based on the Estimated Values, and including the effect of the acquisition of Fresh Park Venlo.

The following table provides additional information regarding each of our properties and is presented as of September 30, 2018 for properties acquired prior to September 30, 2018 and as of the date of acquisition with respect to Fresh Park Venlo, which was acquired on October 5, 2018.

| Property | Location | Investment Type | Date Acquired/ Net Purchase Price (in millions) (1) | Estimated Going-in Capitalization Rate (2) | Leasable Square Feet | Percent Leased | ||||||||

| Bishop’s Square | Dublin, Ireland | Office | 3/2015; $103.2 | 6.1% | 153,387 | 89 | % | |||||||

| Domain Apartments | Las Vegas, Nevada | Residential/Living | 1/2016; $58.1 | 5.5% | 331,038 | 98 | % | |||||||

| Cottonwood Corporate Center | Salt Lake City, Utah | Office | 7/2016; $139.2 | 6.9% | 490,030 | 99 | % | |||||||

| Goodyear Crossing II | Phoenix, Arizona | Industrial | 8/2016; $56.2 | 8.5% | 820,384 | 100 | % | |||||||

| Rookwood | Cincinnati, Ohio | Retail | 1/2017; $193.7 | 6.0% | 573,991 | 98 | % | |||||||

| Montrose Student Residences | Dublin, Ireland | Residential/Living | 3/2017; $40.6 | 5.5% | 53,827 | 100 | % | |||||||

| Queen’s Court Student Residences | Reading, United Kingdom | Residential/Living | 10/2017; $65.3 | 6.2% | 79,115 | 92 | % | |||||||

| Venue Museum District | Houston, Texas | Residential/Living | 9/2018; $72.9 | 3.9% | 294,964 | 92 | % | |||||||

| Fresh Park Venlo | Venlo, The Netherlands | Industrial | 10/2018; $136.3 | 6.7% | 2,863,628 | 95 | % | |||||||

| Total for All Investments | 5,660,364 | 96 | % | |||||||||||