UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_______________________________________________

FORM 10-Q

_______________________________________________

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

Commission file number 001-36353

_______________________________________________

Perrigo Company plc

(Exact name of registrant as specified in its charter)

_______________________________________________

| Ireland | Not Applicable | |||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

The Sharp Building, Hogan Place, Dublin 2, Ireland D02 TY74

+353 1 7094000

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| Ordinary shares | PRGO | New York Stock Exchange | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||||||||||||||||||||||||

| Emerging growth company | ☐ | |||||||||||||||||||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ | |||||||||||||||||||||||||||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

As of August 6, 2021, there were 133,714,781 ordinary shares outstanding.

PERRIGO COMPANY PLC

FORM 10-Q

INDEX

PAGE NUMBER | ||||||||

| PART I. FINANCIAL INFORMATION | ||||||||

| 1 | ||||||||

| 2 | ||||||||

| 3 | ||||||||

| 4 | ||||||||

| 5 | ||||||||

| 6 | ||||||||

| 7 | ||||||||

| 8 | ||||||||

| 9 | ||||||||

| 10 | ||||||||

| 11 | ||||||||

| 12 | ||||||||

| 13 | ||||||||

| 14 | ||||||||

| 15 | ||||||||

| 16 | ||||||||

| 17 | ||||||||

| 18 | ||||||||

| 19 | Subsequent Events | |||||||

| PART II. OTHER INFORMATION | ||||||||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this report are “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the safe harbor created thereby. These statements relate to future events or our future financial performance and involve known and unknown risks, uncertainties and other factors that may cause our, or our industry’s actual results, levels of activity, performance or achievements to be materially different from those expressed or implied by any forward-looking statements. In particular, statements about our expectations, beliefs, plans, objectives, assumptions, future events or future performance contained in this report, including certain statements contained in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” are forward-looking statements. In some cases, forward-looking statements can be identified by terminology such as “may,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “believe,” “estimate,” "forecast," “predict,” “potential” or the negative of those terms or other comparable terminology.

We have based these forward-looking statements on our current expectations, assumptions, estimates and projections. While we believe these expectations, assumptions, estimates and projections are reasonable, such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond our control, including: the effect of the novel coronavirus (COVID-19) pandemic and the associated economic downturn and supply chain impacts on the Company's business; the timing, amount and cost of any share repurchases; future impairment charges; customer acceptance of new products; competition from other industry participants, some of whom have greater marketing resources or larger market shares in certain product categories than we do; downward pricing pressures from customers and consumers, and upward pricing pressures from suppliers and service providers; resolution of uncertain tax positions, including the Company's appeal of the Notice of Assessment ("NoA") issued by the Irish Office of the Revenue Commissioners (“Irish Revenue”) and the Notices of Proposed Adjustment ("NOPAs") issued by the U.S. Internal Revenue Service and the impact that an adverse result in any such proceeding could have on operating results, cash flows and liquidity; potential third-party claims and litigation, including litigation relating to alleged price-fixing in the generic pharmaceutical industry, alleged class action and individual securities law claims, and alleged product liability claims and litigation relating to uncertain tax positions, including the NoA and NOPAs; developments relating to ongoing or future settlement discussions relating to any such claims or litigation; potential impacts of ongoing or future government investigations and regulatory initiatives; potential costs and reputational impact of product recalls and sales halts; the impact of tax reform legislation and healthcare policy; general economic conditions; fluctuations in currency exchange rates and interest rates; the success of the RX business sale, including the ability to achieve the expected benefits thereof, the risks that potential costs or liabilities incurred or retained in connection with the transaction may exceed the Company's estimates or adversely affect the Company's business or operations; the consummation and success of other announced acquisitions or dispositions, and the Company's ability to realize the desired benefits thereof; the Company’s ability to remain in compliance with its debt covenants, and our ability to execute and achieve the desired benefits of announced cost-reduction efforts, and strategic and other initiatives. An adverse result with respect to our appeal of any material outstanding tax assessments or litigation, could ultimately require the use of corporate assets to pay such assessments, damages from third-party claims, and related interest and/or penalties, and any such use of corporate assets would limit the assets available for other corporate purposes. Moreover, current volatility levels in our business and consumer behavior, in part related to the COVID-19 pandemic, can make planning difficult and projections uncertain, and such difficulty and uncertainty could increase if volatility worsens. These and other important factors, including those discussed in our Form 10-K for the year ended December 31, 2020, this report under “Risk Factors” and in any subsequent filings with the United States Securities and Exchange Commission, may cause actual results, performance or achievements to differ materially from those expressed or implied by these forward-looking statements. The forward-looking statements in this report are made only as of the date hereof, and unless otherwise required by applicable securities laws, we disclaim any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

This report contains trademarks, trade names and service marks that are the property of Perrigo Company plc, as well as, for informational purposes, trademarks, trade names, and service marks that are the property of other organizations. Solely for convenience, certain trademarks, trade names, and service marks referred to in this report appear without the ®, ™ and SM symbols, but those references are not intended to indicate that we or the applicable owner, as the case may be, will not assert, to the fullest extent under applicable law, our or their rights to such trademarks, trade names, and service marks.

1

Perrigo Company plc - Item 1

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS (UNAUDITED)

PERRIGO COMPANY PLC

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(in millions, except per share amounts)

(unaudited)

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||

| July 3, 2021 | June 27, 2020 | July 3, 2021 | June 27, 2020 | ||||||||||||||||||||

| Net sales | $ | 981.1 | $ | 948.8 | $ | 1,991.1 | $ | 2,032.0 | |||||||||||||||

| Cost of sales | 632.1 | 601.6 | 1,273.7 | 1,291.1 | |||||||||||||||||||

| Gross profit | 349.0 | 347.2 | 717.4 | 740.9 | |||||||||||||||||||

| Operating expenses | |||||||||||||||||||||||

| Distribution | 24.1 | 19.8 | 45.8 | 40.0 | |||||||||||||||||||

| Research and development | 33.0 | 30.4 | 64.1 | 58.3 | |||||||||||||||||||

| Selling | 139.8 | 119.3 | 275.2 | 258.9 | |||||||||||||||||||

| Administration | 110.4 | 114.3 | 237.6 | 233.9 | |||||||||||||||||||

| Impairment charges | 158.6 | 0 | 158.6 | 0 | |||||||||||||||||||

| Restructuring | 9.0 | 0.7 | 10.7 | 0.7 | |||||||||||||||||||

| Total operating expenses | 474.9 | 284.5 | 792.0 | 591.8 | |||||||||||||||||||

| Operating income (loss) | (125.9) | 62.7 | (74.6) | 149.1 | |||||||||||||||||||

| Change in financial assets | 0 | (2.1) | 0 | (3.7) | |||||||||||||||||||

| Interest expense, net | 31.6 | 32.2 | 63.6 | 61.1 | |||||||||||||||||||

| Other (income) expense, net | (0.4) | 17.1 | 1.9 | 18.8 | |||||||||||||||||||

| Income (loss) from continuing operations before income taxes | (157.1) | 15.5 | (140.1) | 72.9 | |||||||||||||||||||

| Income tax expense (benefit) | (45.2) | 3.1 | (31.0) | 2.8 | |||||||||||||||||||

| Income (loss) from continuing operations | (111.9) | 12.4 | (109.1) | 70.1 | |||||||||||||||||||

| Income from discontinued operations, net of tax | 54.2 | 48.2 | 89.5 | 96.9 | |||||||||||||||||||

| Net income (loss) | $ | (57.7) | $ | 60.6 | $ | (19.6) | $ | 167.0 | |||||||||||||||

| Earnings (loss) per share | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Continuing operations | $ | (0.84) | $ | 0.09 | $ | (0.82) | $ | 0.52 | |||||||||||||||

| Discontinued operations | 0.41 | 0.35 | 0.67 | 0.71 | |||||||||||||||||||

| Basic earnings per share | $ | (0.43) | $ | 0.44 | $ | (0.15) | $ | 1.23 | |||||||||||||||

| Diluted | |||||||||||||||||||||||

| Continuing operations | $ | (0.84) | $ | 0.09 | $ | (0.82) | $ | 0.51 | |||||||||||||||

| Discontinued operations | 0.41 | 0.35 | 0.67 | 0.71 | |||||||||||||||||||

| Diluted earnings per share | $ | (0.43) | $ | 0.44 | $ | (0.15) | $ | 1.22 | |||||||||||||||

| Weighted-average shares outstanding | |||||||||||||||||||||||

| Basic | 133.6 | 136.4 | 133.4 | 136.3 | |||||||||||||||||||

| Diluted | 133.6 | 137.5 | 133.4 | 137.3 | |||||||||||||||||||

See accompanying Notes to the Condensed Consolidated Financial Statements.

2

Perrigo Company plc - Item 1

PERRIGO COMPANY PLC

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(in millions)

(unaudited)

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||

| July 3, 2021 | June 27, 2020 | July 3, 2021 | June 27, 2020 | ||||||||||||||||||||

| Net income (loss) | $ | (57.7) | $ | 60.6 | $ | (19.6) | $ | 167.0 | |||||||||||||||

| Other comprehensive income (loss): | |||||||||||||||||||||||

| Foreign currency translation adjustments | 32.5 | 86.7 | (79.1) | (5.5) | |||||||||||||||||||

| Change in fair value of derivative financial instruments, net of tax | (1.3) | (0.7) | (7.3) | (10.1) | |||||||||||||||||||

| Change in post-retirement and pension liability, net of tax | (0.8) | (1.2) | (1.5) | (3.1) | |||||||||||||||||||

| Other comprehensive income (loss), net of tax | 30.4 | 84.8 | (87.9) | (18.7) | |||||||||||||||||||

| Comprehensive income (loss) | $ | (27.3) | $ | 145.4 | $ | (107.5) | $ | 148.3 | |||||||||||||||

See accompanying Notes to the Condensed Consolidated Financial Statements.

3

Perrigo Company plc - Item 1

PERRIGO COMPANY PLC

CONDENSED CONSOLIDATED BALANCE SHEETS

(in millions, except per share amounts)

(unaudited)

| July 3, 2021 | December 31, 2020 | ||||||||||

| Assets | |||||||||||

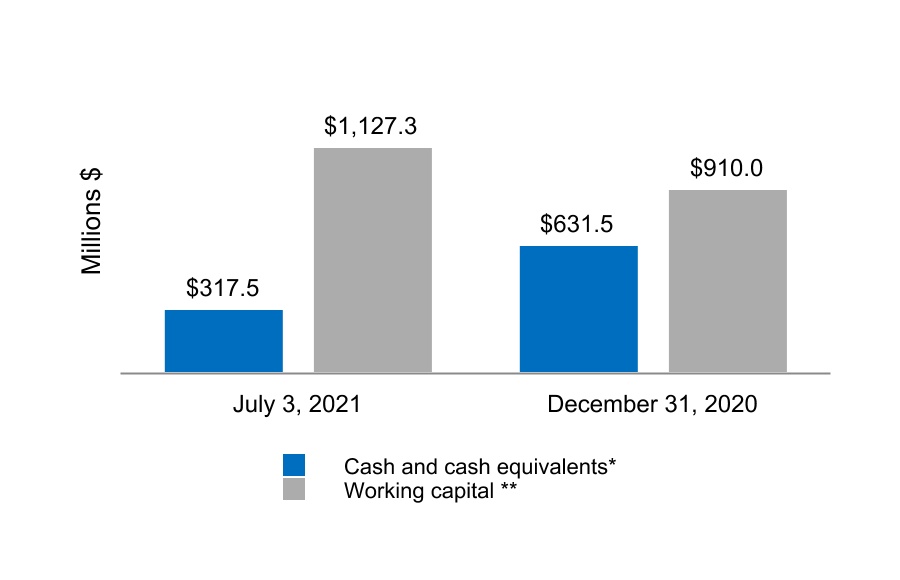

| Cash and cash equivalents | $ | 317.5 | $ | 631.5 | |||||||

| Accounts receivable, net of allowance for credit losses of $7.7 and $6.5, respectively | 620.2 | 593.5 | |||||||||

| Inventories | 1,115.9 | 1,059.4 | |||||||||

| Prepaid expenses and other current assets | 277.3 | 182.2 | |||||||||

| Current assets held for sale | 2,089.3 | 666.9 | |||||||||

| Total current assets | 4,420.2 | 3,133.5 | |||||||||

| Property, plant and equipment, net | 833.8 | 864.6 | |||||||||

| Operating lease assets | 171.3 | 154.7 | |||||||||

| Goodwill and indefinite-lived intangible assets | 3,063.1 | 3,102.7 | |||||||||

| Definite-lived intangible assets, net | 2,313.8 | 2,481.5 | |||||||||

| Deferred income taxes | 49.0 | 40.6 | |||||||||

| Non-current assets held for sale | 0 | 1,364.0 | |||||||||

| Other non-current assets | 379.1 | 346.8 | |||||||||

| Total non-current assets | 6,810.1 | 8,354.9 | |||||||||

| Total assets | $ | 11,230.3 | $ | 11,488.4 | |||||||

| Liabilities and Shareholders’ Equity | |||||||||||

| Accounts payable | $ | 402.4 | $ | 451.6 | |||||||

| Payroll and related taxes | 106.2 | 152.9 | |||||||||

| Accrued customer programs | 132.6 | 128.5 | |||||||||

| Other accrued liabilities | 235.5 | 183.1 | |||||||||

| Accrued income taxes | 9.4 | 9.0 | |||||||||

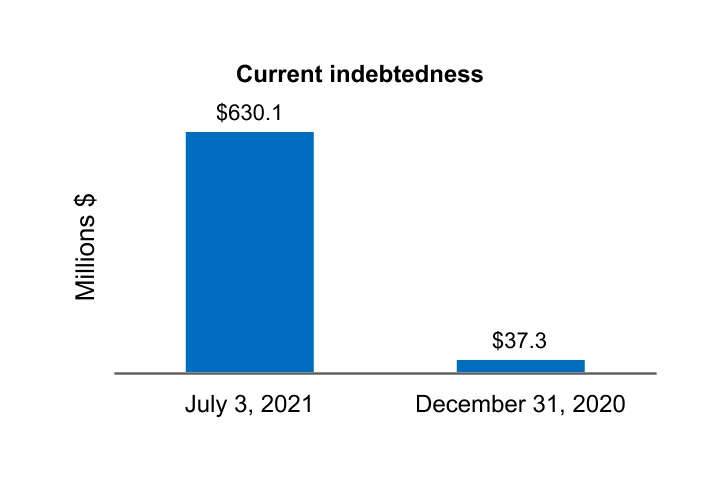

| Current indebtedness | 630.1 | 37.3 | |||||||||

| Current liabilities held for sale | 468.3 | 419.6 | |||||||||

| Total current liabilities | 1,984.5 | 1,382.0 | |||||||||

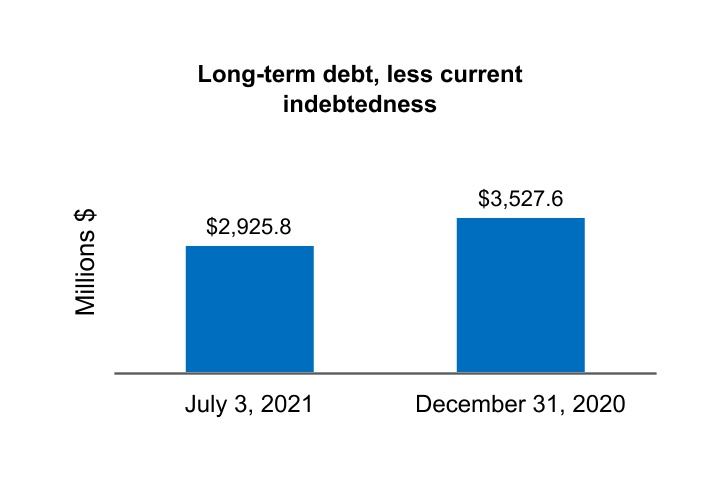

| Long-term debt, less current portion | 2,925.8 | 3,527.6 | |||||||||

| Deferred income taxes | 254.9 | 276.2 | |||||||||

| Non-current liabilities held for sale | 0 | 108.3 | |||||||||

| Other non-current liabilities | 554.0 | 539.2 | |||||||||

| Total non-current liabilities | 3,734.7 | 4,451.3 | |||||||||

| Total liabilities | 5,719.2 | 5,833.3 | |||||||||

| Commitments and contingencies - Refer to Note 16 | 0 | 0 | |||||||||

| Shareholders’ equity | |||||||||||

| Controlling interests: | |||||||||||

| Preferred shares, $0.0001 par value per share, 10 shares authorized | 0 | 0 | |||||||||

| Ordinary shares, €0.001 par value per share, 10,000 shares authorized | 7,081.7 | 7,118.2 | |||||||||

| Accumulated other comprehensive income | 307.1 | 395.0 | |||||||||

| Retained earnings (accumulated deficit) | (1,877.7) | (1,858.1) | |||||||||

| Total shareholders’ equity | 5,511.1 | 5,655.1 | |||||||||

| Total liabilities and shareholders' equity | $ | 11,230.3 | $ | 11,488.4 | |||||||

| Supplemental Disclosures of Balance Sheet Information | |||||||||||

| Preferred shares, issued and outstanding | 0 | 0 | |||||||||

| Ordinary shares, issued and outstanding | 133.6 | 133.1 | |||||||||

See accompanying Notes to the Condensed Consolidated Financial Statements.

4

Perrigo Company plc - Item 1

PERRIGO COMPANY PLC

CONDENSED CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

(in millions, except per share amounts)

(unaudited)

| Ordinary Shares Issued | Accumulated Other Comprehensive Income | Retained Earnings (Accumulated Deficit) | Total | ||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||

| Balance at December 31, 2019 | 136.1 | $ | 7,359.9 | $ | 139.4 | $ | (1,695.5) | $ | 5,803.8 | ||||||||||||||||||||

| Net income | — | — | — | 106.4 | 106.4 | ||||||||||||||||||||||||

| Other comprehensive loss | — | — | (103.5) | — | (103.5) | ||||||||||||||||||||||||

| Restricted stock plan | 0.3 | — | — | — | — | ||||||||||||||||||||||||

| Compensation for stock options | — | 0.8 | — | — | 0.8 | ||||||||||||||||||||||||

| Compensation for restricted stock | — | 15.4 | — | — | 15.4 | ||||||||||||||||||||||||

| Cash dividends, $0.23 per share | — | (30.9) | — | — | (30.9) | ||||||||||||||||||||||||

| Shares withheld for payment of employees' withholding tax liability | (0.1) | (5.6) | — | — | (5.6) | ||||||||||||||||||||||||

| Balance at March 28, 2020 | 136.3 | $ | 7,339.6 | $ | 35.9 | $ | (1,589.1) | $ | 5,786.4 | ||||||||||||||||||||

| Net income | — | — | — | 60.6 | 60.6 | ||||||||||||||||||||||||

| Other comprehensive income | — | — | 84.8 | — | 84.8 | ||||||||||||||||||||||||

| Restricted stock plan | 0.3 | — | — | — | — | ||||||||||||||||||||||||

| Compensation for stock options | — | 0.4 | — | — | 0.4 | ||||||||||||||||||||||||

| Compensation for restricted stock | — | 13.1 | — | — | 13.1 | ||||||||||||||||||||||||

| Cash dividends, $0.23 per share | — | (31.0) | — | — | (31.0) | ||||||||||||||||||||||||

| Shares withheld for payment of employees' withholding tax liability | (0.1) | (3.9) | — | — | (3.9) | ||||||||||||||||||||||||

| Balance at June 27, 2020 | 136.5 | $ | 7,318.2 | $ | 120.7 | $ | (1,528.5) | $ | 5,910.4 | ||||||||||||||||||||

| Ordinary Shares Issued | Accumulated Other Comprehensive Income | Retained Earnings (Accumulated Deficit) | Total | ||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||

| Balance at December 31, 2020 | 133.1 | $ | 7,118.2 | $ | 395.0 | $ | (1,858.1) | $ | 5,655.1 | ||||||||||||||||||||

| Net income | — | — | — | 38.1 | 38.1 | ||||||||||||||||||||||||

| Other comprehensive loss | — | — | (118.3) | — | (118.3) | ||||||||||||||||||||||||

| Restricted stock plan | 0.6 | — | — | — | — | ||||||||||||||||||||||||

| Compensation for stock options | — | 0.4 | — | — | 0.4 | ||||||||||||||||||||||||

| Compensation for restricted stock | — | 24.6 | — | — | 24.6 | ||||||||||||||||||||||||

| Cash dividends, $0.24 per share | — | (32.6) | — | — | (32.6) | ||||||||||||||||||||||||

| Shares withheld for payment of employees' withholding tax liability | (0.2) | (9.3) | — | — | (9.3) | ||||||||||||||||||||||||

| Balance at April 3, 2021 | 133.5 | $ | 7,101.3 | $ | 276.7 | $ | (1,820.0) | $ | 5,558.0 | ||||||||||||||||||||

| Net loss | — | — | — | (57.7) | (57.7) | ||||||||||||||||||||||||

| Other comprehensive income | — | — | 30.4 | — | 30.4 | ||||||||||||||||||||||||

| Restricted stock plan | 0.1 | — | — | — | — | ||||||||||||||||||||||||

| Compensation for stock options | — | 0.2 | — | — | 0.2 | ||||||||||||||||||||||||

| Compensation for restricted stock | — | 13.9 | — | — | 13.9 | ||||||||||||||||||||||||

| Cash dividends, $0.24 per share | — | (32.5) | — | — | (32.5) | ||||||||||||||||||||||||

| Shares withheld for payment of employees' withholding tax liability | 0 | (1.2) | — | — | (1.2) | ||||||||||||||||||||||||

| Balance at July 3, 2021 | 133.6 | $ | 7,081.7 | $ | 307.1 | $ | (1,877.7) | $ | 5,511.1 | ||||||||||||||||||||

See accompanying Notes to the Condensed Consolidated Financial Statements.

5

Perrigo Company plc - Item 1

PERRIGO COMPANY PLC

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in millions)

(unaudited)

| Six Months Ended | |||||||||||

| July 3, 2021 | June 27, 2020 | ||||||||||

| Cash Flows From (For) Operating Activities | |||||||||||

| Net income (loss) | $ | (19.6) | $ | 167.0 | |||||||

| Adjustments to derive cash flows: | |||||||||||

| Depreciation and amortization | 165.3 | 187.8 | |||||||||

| Loss (Gain) on sale of business | 0 | 17.4 | |||||||||

| Share-based compensation | 39.1 | 29.7 | |||||||||

| Impairment charges | 158.6 | 0 | |||||||||

| Change in financial assets | 0 | (3.7) | |||||||||

| Restructuring charges | 10.7 | 1.1 | |||||||||

| Deferred income taxes | (25.4) | 11.7 | |||||||||

| Amortization of debt premium | (1.4) | (1.3) | |||||||||

| Other non-cash adjustments, net | 18.8 | (11.5) | |||||||||

| Subtotal | 346.1 | 398.2 | |||||||||

| Increase (decrease) in cash due to: | |||||||||||

| Accounts receivable | (108.2) | 227.9 | |||||||||

| Inventories | (106.0) | (38.6) | |||||||||

| Prepaid expenses | 1.8 | (32.4) | |||||||||

| Accounts payable | (22.5) | (21.6) | |||||||||

| Payroll and related taxes | (61.1) | (20.4) | |||||||||

| Accrued customer programs | 4.3 | (31.9) | |||||||||

| Accrued liabilities | (32.1) | (7.9) | |||||||||

| Accrued income taxes | (135.6) | (12.8) | |||||||||

| Other, net | 31.2 | 2.2 | |||||||||

| Subtotal | (428.2) | 64.5 | |||||||||

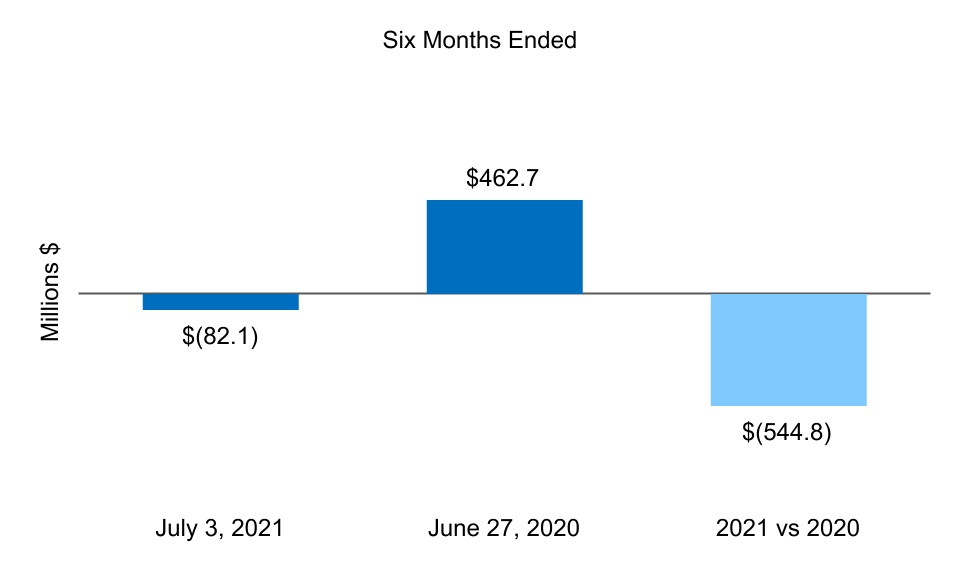

| Net cash from (for) operating activities | (82.1) | 462.7 | |||||||||

| Cash Flows From (For) Investing Activities | |||||||||||

| Proceeds from royalty rights | 1.9 | 2.4 | |||||||||

| Purchase of equity method investment | 0 | (15.0) | |||||||||

| Acquisitions of businesses, net of cash acquired | 0 | (106.0) | |||||||||

| Asset acquisitions | (70.6) | (32.8) | |||||||||

| Additions to property, plant and equipment | (68.4) | (60.1) | |||||||||

| Net proceeds from sale of business | 0 | 187.8 | |||||||||

| Other investing, net | 1.3 | 2.0 | |||||||||

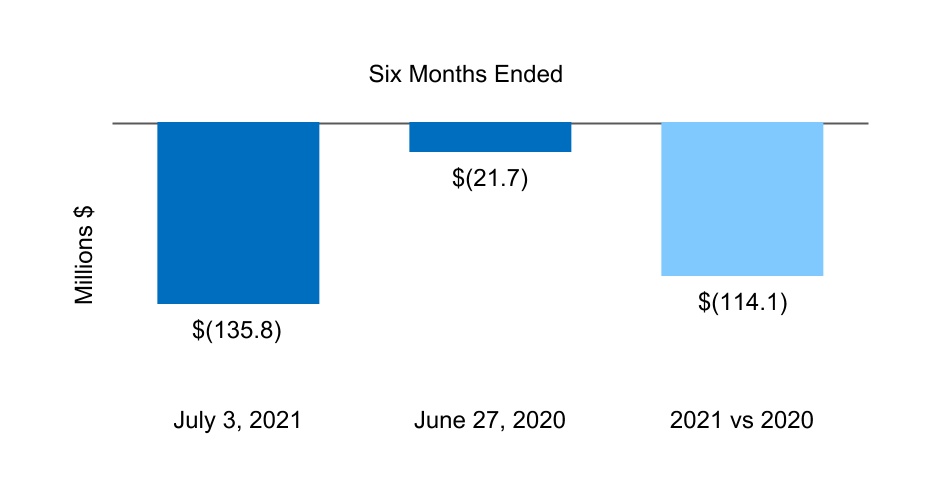

| Net cash from (for) investing activities | (135.8) | (21.7) | |||||||||

| Cash Flows From (For) Financing Activities | |||||||||||

| Issuances of long-term debt | 0 | 743.8 | |||||||||

| Borrowings (repayments) of revolving credit agreements and other financing, net | (5.8) | 1.6 | |||||||||

| Deferred financing fees | 0 | (5.0) | |||||||||

| Cash dividends | (65.1) | (61.9) | |||||||||

| Other financing, net | (13.5) | (11.7) | |||||||||

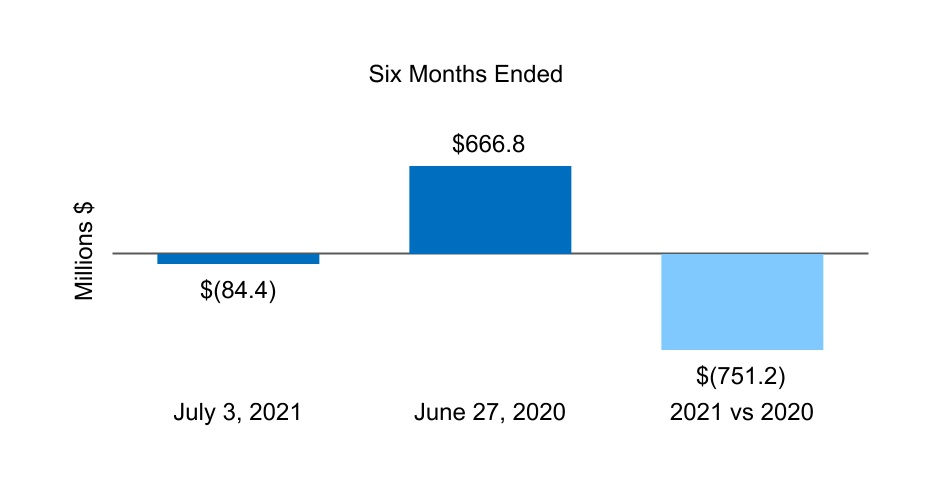

| Net cash from (for) financing activities | (84.4) | 666.8 | |||||||||

| Effect of exchange rate changes on cash and cash equivalents | (3.2) | (5.8) | |||||||||

| Net increase (decrease) in cash and cash equivalents | (305.5) | 1,102.0 | |||||||||

| Cash and cash equivalents of continuing operations, beginning of period | 631.5 | 344.5 | |||||||||

| Cash and cash equivalents held for sale, beginning of period | 10.0 | 9.8 | |||||||||

| Less cash and cash equivalents held for sale, end of period | (18.5) | (18.7) | |||||||||

| Cash and cash equivalents of continuing operations, end of period | $ | 317.5 | $ | 1,437.6 | |||||||

See accompanying Notes to the Condensed Consolidated Financial Statements.

6

Perrigo Company plc - Item 1

Note 1

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

General Information

The Company

Perrigo Company plc was incorporated under the laws of Ireland on June 28, 2013 and became the successor registrant of Perrigo Company, a Michigan corporation, on December 18, 2013 in connection with the acquisition of Elan Corporation, plc ("Elan"). Unless the context requires otherwise, the terms "Perrigo," the "Company," "we," "our," "us," and similar pronouns used herein refer to Perrigo Company plc, its subsidiaries, and all predecessors of Perrigo Company plc and its subsidiaries.

Our vision is to make lives better by bringing Quality, Affordable Self-Care Products that consumers trust everywhere they are sold. We are a leading provider of over-the-counter ("OTC") health and wellness solutions that enhance individual well-being by empowering consumers to proactively prevent or treat conditions that can be self-managed.

Basis of Presentation

The accompanying unaudited Condensed Consolidated Financial Statements have been prepared in accordance with U.S. generally accepted accounting principles ("GAAP") for interim financial information and with the instructions to Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. The unaudited Condensed Consolidated Financial Statements should be read in conjunction with the Consolidated Financial Statements and footnotes included in our Annual Report on Form 10-K for the year ended December 31, 2020. In the opinion of management, all adjustments (consisting of normal recurring accruals and other adjustments) considered necessary for a fair presentation of the unaudited Condensed Consolidated Financial Statements have been included and include our accounts and the accounts of all majority-owned subsidiaries. All intercompany transactions and balances have been eliminated in consolidation.

On March 1, 2021, we announced a definitive agreement to sell our generic RX Pharmaceuticals business ("RX business") to Altaris Capital Partners, LLC ("Altaris"). On July 6, 2021, we completed the sale of the RX business. The financial results of our RX business, which were previously reported in our Prescription Pharmaceuticals ("RX") segment, have been classified as discontinued operations in the Condensed Consolidated Statements of Operations for all periods presented. The assets and liabilities of our RX business are reflected as assets and liabilities held for sale in the Condensed Consolidated Balance Sheets for all periods presented. Refer to Note 8 for additional information regarding discontinued operations. Unless otherwise noted, amounts and disclosures throughout the Notes to the unaudited Condensed Consolidated Financial Statements relate to our continuing operations.

Segment Reporting

Our reporting and operating segments are as follows:

•Consumer Self-Care Americas ("CSCA") comprises our consumer self-care business (OTC, infant formula, and oral self-care categories, and contract manufacturing) in the U.S., Mexico and Canada.

•Consumer Self-Care International ("CSCI") comprises our consumer self-care business primarily branded in Europe and Australia, our store brand business in the United Kingdom and parts of Europe and Asia, and our liquid licensed products business in the United Kingdom until it was disposed on June 19, 2020.

Allowance for Credit Losses

Expected credit losses on trade receivables and contract assets are measured collectively by geographic location. The estimate of expected credit losses considers historical credit loss information that is adjusted for current conditions and for reasonable and supportable forecasts. Historical credit loss experience provides the primary basis for estimation of expected credit losses. Adjustments to historical loss information may be made for

7

Perrigo Company plc - Item 1

Note 1

significant changes in a geographic location’s economic conditions. Receivables that do not share risk characteristics are evaluated on an individual basis. These receivables are not included in the collective evaluation.

The allowance for credit losses is a valuation account that is deducted from the instruments’ cost basis to present the net amount expected to be collected. Trade receivables and contract assets are charged off against the allowance when the balance is no longer deemed collectible.

The following table presents the allowance for credit losses activity (in millions):

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||

| July 3, 2021 | June 27, 2020 | July 3, 2021 | June 27, 2020 | ||||||||||||||||||||

| Beginning balance | $ | 9.1 | $ | 6.2 | $ | 6.5 | $ | 6.0 | |||||||||||||||

| Provision for credit losses, net | 0.4 | 0.1 | 3.7 | 0.7 | |||||||||||||||||||

| Receivables written-off | (0.6) | (0.9) | (0.9) | (1.1) | |||||||||||||||||||

| Recoveries collected | 0 | 0 | 0 | 0 | |||||||||||||||||||

| Transfer to held for sale | (1.4) | 0 | (1.4) | 0 | |||||||||||||||||||

| Currency translation adjustment | 0.2 | 0.1 | (0.2) | (0.1) | |||||||||||||||||||

| Ending balance | $ | 7.7 | $ | 5.5 | $ | 7.7 | $ | 5.5 | |||||||||||||||

NOTE 2 – REVENUE RECOGNITION

Revenue is recognized when or as a customer obtains control of promised products. The amount of revenue recognized reflects the consideration we expect to be entitled to receive in exchange for these products.

Disaggregation of Revenue

We generated net sales in the following geographic locations(1) (in millions):

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||

| July 3, 2021 | June 27, 2020 | July 3, 2021 | June 27, 2020 | ||||||||||||||||||||

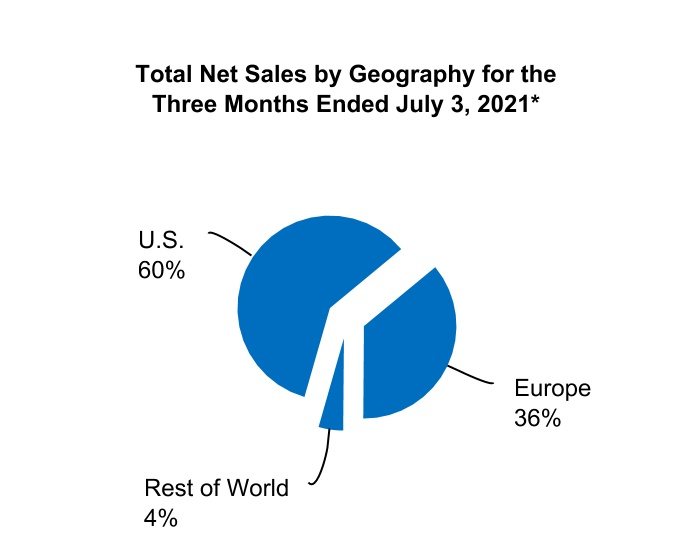

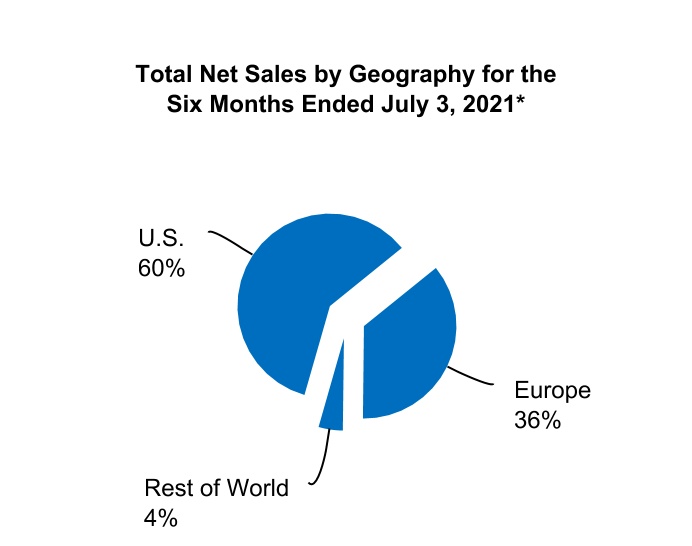

| U.S. | $ | 590.3 | $ | 604.0 | $ | 1,201.6 | $ | 1,274.6 | |||||||||||||||

Europe(2) | 348.1 | 311.8 | 704.1 | 684.4 | |||||||||||||||||||

All other countries(3) | 42.7 | 33.0 | 85.4 | 73.0 | |||||||||||||||||||

| Total net sales | $ | 981.1 | $ | 948.8 | $ | 1,991.1 | $ | 2,032.0 | |||||||||||||||

(1) Derived from the location of the entity that sells to a third party.

(2) Includes Ireland net sales of $5.3 million and $9.8 million for the three and six months ended July 3, 2021 respectively, and $7.8 million and $11.5 million for the three and six months ended June 27, 2020, respectively.

(3) Includes net sales generated primarily in Mexico, Australia and Canada.

8

Perrigo Company plc - Item 1

Note 2

Product Category

The following is a summary of our net sales by category (in millions):

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||

| July 3, 2021 | June 27, 2020 | July 3, 2021 | June 27, 2020 | ||||||||||||||||||||

CSCA(1) | |||||||||||||||||||||||

| Upper respiratory | $ | 102.4 | $ | 116.7 | $ | 216.4 | $ | 271.3 | |||||||||||||||

| Digestive health | 110.4 | 112.1 | 223.9 | 219.0 | |||||||||||||||||||

| Nutrition | 95.6 | 88.6 | 187.6 | 190.8 | |||||||||||||||||||

| Pain and sleep-aids | 87.1 | 97.7 | 179.5 | 218.1 | |||||||||||||||||||

| Oral self-care | 74.5 | 63.2 | 148.2 | 118.5 | |||||||||||||||||||

| Healthy lifestyle | 63.6 | 81.5 | 139.1 | 167.3 | |||||||||||||||||||

| Skincare and personal hygiene | 52.9 | 42.9 | 106.2 | 89.6 | |||||||||||||||||||

| Vitamins, minerals, and supplements | 8.4 | 6.4 | 16.2 | 12.8 | |||||||||||||||||||

Other CSCA(2) | 27.4 | 18.6 | 45.7 | 40.8 | |||||||||||||||||||

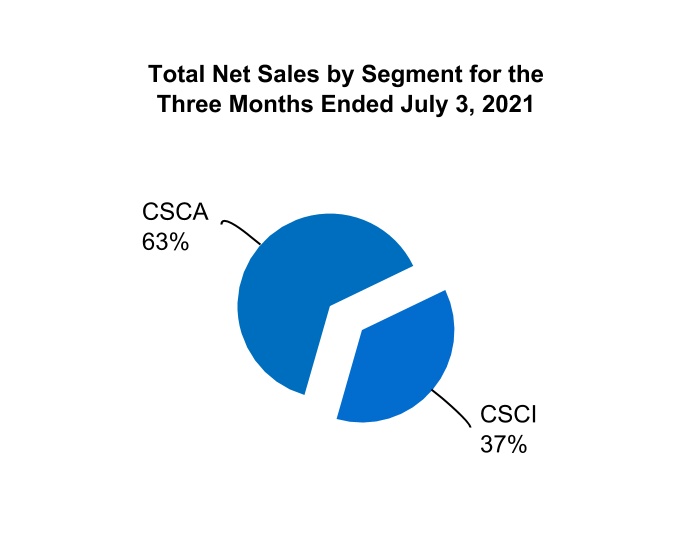

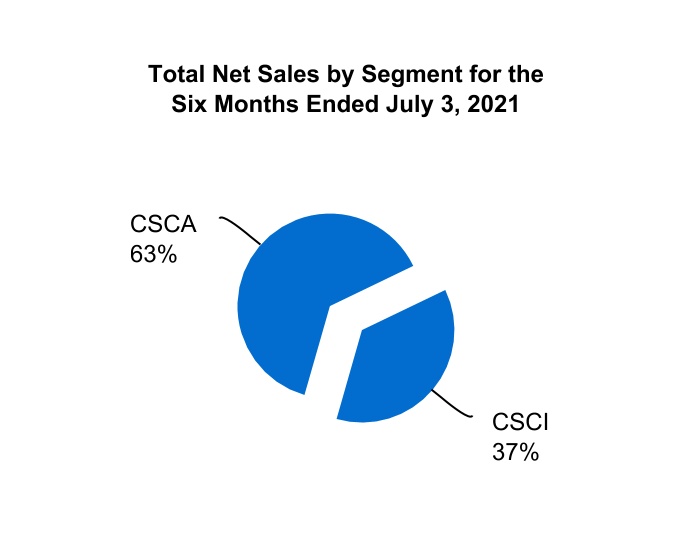

| Total CSCA | 622.3 | 627.7 | 1,262.8 | 1,328.2 | |||||||||||||||||||

| CSCI | |||||||||||||||||||||||

| Skincare and personal hygiene | 112.4 | 97.6 | 219.4 | 192.3 | |||||||||||||||||||

| Vitamins, minerals, and supplements | 49.1 | 38.5 | 108.1 | 87.0 | |||||||||||||||||||

| Healthy lifestyle | 48.0 | 40.5 | 98.3 | 84.1 | |||||||||||||||||||

| Pain and sleep-aids | 47.3 | 40.2 | 96.3 | 87.0 | |||||||||||||||||||

| Upper respiratory | 42.6 | 45.5 | 85.5 | 129.6 | |||||||||||||||||||

| Oral self-care | 22.5 | 20.4 | 48.0 | 43.6 | |||||||||||||||||||

| Digestive health | 9.7 | 5.1 | 18.2 | 11.1 | |||||||||||||||||||

Other CSCI(3) | 27.2 | 33.3 | 54.5 | 69.1 | |||||||||||||||||||

| Total CSCI | 358.8 | 321.1 | 728.3 | 703.8 | |||||||||||||||||||

| Total net sales | $ | 981.1 | $ | 948.8 | $ | 1,991.1 | $ | 2,032.0 | |||||||||||||||

(1) Includes net sales from our OTC contract manufacturing business.

(2) Consists primarily of diagnostic and other miscellaneous or otherwise uncategorized product lines and markets, none of which is greater than 10% of the segment net sales.

(3) Consists primarily of our distribution business and other miscellaneous or otherwise uncategorized product lines and markets, none of which is greater than 10% of the segment net sales.

While the majority of revenue is recognized at a point in time, certain of our product revenue is recognized on an over time basis. Predominately, over time customer contracts exist in contract manufacturing arrangements, which occur in both the CSCA and CSCI segments. Contract manufacturing revenue was $69.8 million and $132.9 million for the three and six months ended July 3, 2021, respectively and $64.5 million and $113.7 million for the three and six months ended June 27, 2020, respectively.

We also recognize a portion of the store brand OTC product revenues in the CSCA segment on an over time basis; however, the timing difference between over time and point in time revenue recognition for store brand contracts is not significant due to the short time period between the customization of the product and shipment or delivery.

Contract Balances

The following table provides information about contract assets from contracts with customers (in millions):

| Balance Sheet Location | July 3, 2021 | December 31, 2020 | |||||||||||||||

| Short-term contract assets | Prepaid expenses and other current assets | $ | 22.4 | $ | 19.7 | ||||||||||||

9

Perrigo Company plc - Item 1

Note 3

NOTE 3 – ACQUISITIONS AND DIVESTITURES

Acquisitions Accounted for as a Business Combination During the Year Ended December 31, 2020

Eastern European OTC Dermatological Brands Acquisition

On October 30, 2020, we acquired 3 Eastern European OTC dermatological brands ("Eastern European Brands"), skincare brands Emolium® and Iwostin® and hair loss treatment brand Loxon®, from Sanofi. The transaction closed for €53.3 million ($62.3 million). We capitalized $52.5 million as brand-named intangible assets and allocated the remainder of the purchase price to goodwill, inventory, customer relationships and deferred tax assets.

The addition of these market-leading OTC brands complements our already robust skincare portfolio and adds scale to our Eastern European business. The acquisition also serves as another step for Perrigo’s CSCI growth plans and provides new opportunities for self-care revenue synergy in the European markets. The operating results of the brands are reported within our CSCI segment. The acquisition of the Eastern European Brands was accounted for as a business combination and has been reported in our Consolidated Statements of Operations as of the acquisition date.

The goodwill arising from the acquisition consists largely of the assembled workforce, and the cost and revenue synergies expected from integrating the business into the CSCI segment. The goodwill was allocated to our CSCI segment, none of which is deductible for income tax purposes. The definite-lived intangible assets acquired consisted of brands and customer relationships which are being amortized over a weighted average useful life of approximately 18.8 years. Both the brands and customer relationships were valued using the multi-period excess earnings method. Significant judgment was applied in estimating the fair value of the intangible assets acquired, which involved the use of significant estimates and assumptions with respect to the timing and amounts of cash flow projections, including revenue growth rates, projected profit margins, and discount rates. The opening balance sheet is final.

Oral Care Assets of High Ridge Brands

On April 1, 2020, we acquired the oral care assets of High Ridge Brands ("Dr. Fresh") for total purchase consideration of $113.0 million, subject to customary adjustments, including a working capital settlement. After such adjustments as of December 31, 2020, total cash consideration paid was $106.2 million net of $2.0 million that we allocated as prepayment of contract consideration for transitional services to be received related to the transaction.

This acquisition includes the children’s oral care value brand, Firefly®, in addition to the REACH® and Dr. Fresh® brands, and a licensing portfolio. The U.S. operations, which represent a significant portion of the business, are reported in our CSCA segment and the non-U.S. operations are reported in our CSCI segment.

10

Perrigo Company plc - Item 1

Note 3

The following table summarizes the consideration paid for Dr. Fresh and the amounts of the assets acquired and liabilities assumed (in millions):

| Oral Care Assets of High Ridge Brands (Dr. Fresh) | |||||

| Purchase price paid | $ | 106.2 | |||

| Assets acquired: | |||||

| Accounts receivable | 13.1 | ||||

| Inventories | 22.2 | ||||

| Prepaid expenses and other current assets | 0.4 | ||||

| Property, plant and equipment, net | 0.7 | ||||

| Operating lease assets | 2.6 | ||||

| Goodwill | 17.2 | ||||

| Distribution and license agreements and supply agreements | $ | 2.2 | |||

| Developed product technology, formulations, and product rights | 0.1 | ||||

| Customer relationships and distribution networks | 20.6 | ||||

| Trademarks, trade names, and brands | 43.2 | ||||

| Total intangible assets | $ | 66.1 | |||

| Total assets | $ | 122.3 | |||

| Liabilities assumed: | |||||

| Accounts payable | $ | 6.1 | |||

| Other accrued liabilities | 3.8 | ||||

| Payroll and related taxes | 0.7 | ||||

| Accrued customer programs | 3.0 | ||||

| Other non-current liabilities | 2.5 | ||||

| Total liabilities | $ | 16.1 | |||

| Net assets acquired | $ | 106.2 | |||

The goodwill of $17.2 million arising from the acquisition consists largely of the anticipated growth from new product sales, sales to new customers, the assembled workforce, and the synergies expected from combining the operations of Dr. Fresh into Perrigo. The goodwill is attributable to our CSCA segment and is tax deductible for income tax purposes. The definite-lived intangible assets acquired consisted of trademarks and trade names, license agreements, and customer relationships, which are being amortized over a weighted average useful life of approximately 17.8 years. Customer relationships were valued using the multi-period excess earnings method. Trademarks and trade names and developed technology were valued using the relief from royalty method. Significant judgment was applied in estimating the fair value of the intangible assets acquired, which involved the use of significant estimates and assumptions with respect to the timing and amounts of cash flow projections, including revenue growth rates, projected profit margins, and discount rates. The opening balance sheet is final.

11

Perrigo Company plc - Item 1

Note 3

Pro Forma Impact of Business Combinations

The following table presents unaudited pro forma information as if the acquisitions of Dr. Fresh and the Eastern European Brands occurred on January 1, 2019, and had been combined with the results reported in our Condensed Consolidated Statements of Operations for all periods presented (in millions):

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||

| (Unaudited) | June 27, 2020 | June 27, 2020 | |||||||||||||||||||||

| Net sales | $ | 955.0 | $ | 2,074.1 | |||||||||||||||||||

| Income from continuing operations | $ | 17.6 | $ | 80.2 | |||||||||||||||||||

The unaudited pro forma information is presented for information purposes only and is not indicative of the results that would have been achieved if the acquisition had taken place at such time. The unaudited pro forma information presented above includes adjustments primarily for amortization charges for acquired intangible assets, depreciation of property, plant and equipment that have been revalued, certain acquisition-related charges, and related tax effects.

Acquisitions During the Six Months Ended June 27, 2020

Dexsil®

On February 13, 2020, we acquired Dexsil®, a silicon supplement brand, from RXW Group Nv, for total cash consideration paid of approximately $8.0 million. The transaction was accounted for as an asset acquisition, in which we capitalized the consideration paid as a brand-named intangible asset. We began amortizing the brand intangible over a 25-year useful life. Operating results attributable to the product are included within our CSCI segment.

Steripod®

On January 3, 2020, we acquired Steripod®, a leading toothbrush accessory brand and innovator in the toothbrush protector market, from Bonfit America Inc. Total consideration paid was $26.0 million. The transaction was accounted for as an asset acquisition, in which we capitalized $25.1 million as a brand-named intangible asset. The remainder of the purchase price was allocated to working capital. We began amortizing the brand intangible asset over a 25-year useful life. Operating results attributable to Steripod® are included within our CSCA segment.

Divestitures During the Six Months Ended June 27, 2020

Rosemont Pharmaceuticals Business

On June 19, 2020, we completed the sale of our U.K.-based Rosemont Pharmaceuticals business, a generic prescription pharmaceuticals manufacturer focused on liquid medicines, to a U.K.-headquartered private equity firm for cash consideration of £155.6 million (approximately $195.0 million). The sale resulted in a pre-tax loss of $17.4 million during the three and six months ended June 27, 2020, $1.3 million during the three months ended September 26, 2020 and $2.4 million during the three months ended December 31, 2020. These losses were recorded in our CSCI segment in Other (income) expense, net on the Consolidated Statements of Operations. These losses included professional fees and a $46.4 million write-off of foreign currency translation adjustment from Accumulated other comprehensive income.

12

Perrigo Company plc - Item 1

Note 4

NOTE 4 – GOODWILL AND INTANGIBLE ASSETS

Goodwill

Changes in the carrying amount of goodwill, by reportable segment, were as follows (in millions):

| December 31, 2020 | Purchase accounting adjustments | Impairments | Currency translation adjustments | July 3, 2021 | ||||||||||||||||||||||||||||||||||||||||||||||

CSCA(1) | $ | 1,905.0 | $ | 2.4 | $ | (6.1) | $ | (0.1) | $ | 1,901.2 | ||||||||||||||||||||||||||||||||||||||||

CSCI(2) | 1,190.7 | (2.4) | 0 | (32.7) | 1,155.6 | |||||||||||||||||||||||||||||||||||||||||||||

| Total goodwill | $ | 3,095.7 | $ | 0 | $ | (6.1) | $ | (32.8) | $ | 3,056.8 | ||||||||||||||||||||||||||||||||||||||||

(1) We had 0 accumulated goodwill impairments as of December 31, 2020 and $6.1 million as of July 3, 2021.

(2) We had accumulated goodwill impairments of $868.4 million as of December 31, 2020 and July 3, 2021.

CSCA Reporting Unit Goodwill

On May 18, 2021, we announced a definitive agreement to sell our Mexico and Brazil-based OTC businesses ("Latin American businesses"), both within our CSCA segment, to Advent International. As a result, we prepared a goodwill impairment test. We determined the carrying value of this business exceeded the fair value and recorded an impairment of $6.1 million within our CSCA segment during the three months ended July 3, 2021 (refer to Note 6 and Note 9).

Intangible Assets

Intangible assets and related accumulated amortization consisted of the following (in millions):

| July 3, 2021 | December 31, 2020 | ||||||||||||||||||||||||||||||||||

| Gross | Accumulated Amortization | Gross | Accumulated Amortization | ||||||||||||||||||||||||||||||||

| Indefinite-lived intangibles: | |||||||||||||||||||||||||||||||||||

| Trademarks, trade names, and brands | $ | 3.6 | $ | — | $ | 4.3 | $ | — | |||||||||||||||||||||||||||

| In-process research and development | 2.7 | — | 2.7 | — | |||||||||||||||||||||||||||||||

| Total indefinite-lived intangibles | $ | 6.3 | $ | — | $ | 7.0 | $ | — | |||||||||||||||||||||||||||

| Definite-lived intangibles: | |||||||||||||||||||||||||||||||||||

| Distribution and license agreements and supply agreements | $ | 69.4 | $ | 51.7 | $ | 74.8 | $ | 55.4 | |||||||||||||||||||||||||||

| Developed product technology, formulations, and product rights | 302.0 | 184.5 | 303.3 | 177.3 | |||||||||||||||||||||||||||||||

| Customer relationships and distribution networks | 1,877.9 | 863.7 | 1,920.5 | 823.7 | |||||||||||||||||||||||||||||||

| Trademarks, trade names, and brands | 1,534.0 | 369.6 | 1,581.5 | 342.2 | |||||||||||||||||||||||||||||||

| Non-compete agreements | 2.1 | 2.1 | 2.9 | 2.9 | |||||||||||||||||||||||||||||||

| Total definite-lived intangibles | $ | 3,785.4 | $ | 1,471.6 | $ | 3,883.0 | $ | 1,401.5 | |||||||||||||||||||||||||||

| Total intangible assets | $ | 3,791.7 | $ | 1,471.6 | $ | 3,890.0 | $ | 1,401.5 | |||||||||||||||||||||||||||

We recorded amortization expense of $53.4 million and $106.6 million for the three and six months ended July 3, 2021, respectively, and $51.6 million and $104.2 million for the three and six months ended June 27, 2020, respectively.

13

Perrigo Company plc - Item 1

Note 5

NOTE 5 – INVENTORIES

Major components of inventory were as follows (in millions):

| July 3, 2021 | December 31, 2020 | ||||||||||

| Finished goods | $ | 607.5 | $ | 574.1 | |||||||

| Work in process | 241.0 | 220.4 | |||||||||

| Raw materials | 267.4 | 264.9 | |||||||||

| Total inventories | $ | 1,115.9 | $ | 1,059.4 | |||||||

NOTE 6 – FAIR VALUE MEASUREMENTS

The table below summarizes the valuation of our financial instruments carried at fair value by the applicable pricing categories (in millions):

| July 3, 2021 | December 31, 2020 | |||||||||||||||||||||||||||||||||||||

| Level 1 | Level 2 | Level 3 | Level 1 | Level 2 | Level 3 | |||||||||||||||||||||||||||||||||

| Measured at fair value on a recurring basis: | ||||||||||||||||||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||||||||||||||

| Investment securities | $ | 1.6 | $ | 0 | $ | 0 | $ | 2.5 | $ | 0 | $ | 0 | ||||||||||||||||||||||||||

| Foreign currency forward contracts | 0 | 5.7 | 0 | 0 | 9.8 | 0 | ||||||||||||||||||||||||||||||||

| Cross-currency swap | 0 | 4.2 | 0 | 0 | 6.3 | 0 | ||||||||||||||||||||||||||||||||

| Total assets | $ | 1.6 | $ | 9.9 | $ | 0 | $ | 2.5 | $ | 16.1 | $ | 0 | ||||||||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||||||||||||||

| Foreign currency forward contracts | $ | 0 | $ | 2.7 | $ | 0 | $ | 0 | $ | 7.9 | $ | 0 | ||||||||||||||||||||||||||

| Total liabilities | $ | 0 | $ | 2.7 | $ | 0 | $ | 0 | $ | 7.9 | $ | 0 | ||||||||||||||||||||||||||

| Measured at fair value on a non-recurring basis: | ||||||||||||||||||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||||||||||||||

Assets held for sale, net(1) | $ | 0 | $ | 0 | $ | 1,621.0 | $ | 0 | $ | 0 | $ | 0 | ||||||||||||||||||||||||||

| Total assets | $ | 0 | $ | 0 | $ | 1,621.0 | $ | 0 | $ | 0 | $ | 0 | ||||||||||||||||||||||||||

(1) We measured the assets held for sale for impairment purposes and recorded a total impairment of $158.6 million (refer to Note 9).

There were no transfers within Level 3 fair value measurements during the three and six months ended July 3, 2021 or the year ended December 31, 2020.

14

Perrigo Company plc - Item 1

Note 6

Royalty Pharma Contingent Milestone Receipts

During the year ended December 31, 2020, Royalty Pharma payments from Biogen for Tysabri® sales, as defined in the agreement between the parties, did not exceed the 2020 global net sales threshold. Therefore, we were not entitled to receive the remaining contingent milestone payment. As of December 31, 2020, there were 0 contingent milestone payments outstanding.

The table below summarizes the change in fair value of the Royalty Pharma contingent milestone (in millions):

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||||||||

| June 27, 2020 | June 27, 2020 | ||||||||||||||||||||||||||||

| Beginning balance | $ | 96.9 | $ | 95.3 | |||||||||||||||||||||||||

| Change in fair value | 2.1 | 3.7 | |||||||||||||||||||||||||||

| Ending balance | $ | 99.0 | $ | 99.0 | |||||||||||||||||||||||||

We valued our contingent milestone payment from Royalty Pharma using a modified Black-Scholes Option Pricing Model ("BSOPM"). Key inputs in the BSOPM are the estimated volatility and rate of return of royalties on global net sales of Tysabri® that are received by Royalty Pharma until the contingent milestones are resolved. As of June 27, 2020, volatility and the estimated fair value of the milestones had a positive relationship such that higher volatility translates to a higher estimated fair value of the contingent milestone payments. Rate of return and the estimated fair value of the milestones had an inverse relationship, such that a lower rate of return correlates with a higher estimated fair value of the contingent milestone payments. We assessed volatility and rate of return inputs quarterly by analyzing certain market volatility benchmarks and the risk associated with Royalty Pharma achieving the underlying projected royalties. The table below represents the volatility and rate of return:

| Three Months Ended | |||||||||||

| June 27, 2020 | |||||||||||

| Volatility | 37.5 | % | |||||||||

| Rate of return | 6.91 | % | |||||||||

During the three and six months ended June 27, 2020, the fair value of the Royalty Pharma contingent milestone payment related to 2020 increased by $2.1 million and $3.7 million,respectively, to $99.0 million, driven by higher volatility, higher projected global net sales of Tysabri® compared to the estimates in the prior period, and the estimated probability of achieving the earn-out. As of December 31, 2020, there were 0 contingent milestone payments outstanding and, accordingly, no asset recorded in the Condensed Consolidated Balance Sheet.

Non-recurring Fair Value Measurements

The non-recurring fair values represent only those assets whose carrying values were adjusted to fair value during the reporting period.

Goodwill

During the three months ended July 3, 2021, as a result of our definitive agreement to sell our Latin American businesses, we prepared a goodwill impairment test. We determined the carrying value of this business exceeded the fair value and recorded an impairment in the CSCA segment (refer to Note 4).

Assets held for sale, net

During the three months ended July 3, 2021, as a result of our definitive agreement to sell our Latin American businesses, we prepared an impairment test on the net assets held for sale related to this business. We determined the carrying value of the net assets held for sale exceed the fair value less cost to sell and recorded an impairment in the CSCA segment (refer to Note 9).

15

Perrigo Company plc - Item 1

Note 6

Fixed Rate Long-term Debt

Our fixed rate long-term debt consisted of the following (in millions):

| July 3, 2021 | December 31, 2020 | ||||||||||||||||||||||

| Level 1 | Level 2 | Level 1 | Level 2 | ||||||||||||||||||||

| Public Bonds | |||||||||||||||||||||||

| Carrying Value (excluding discount) | $ | 2,760.0 | $ | — | $ | 2,760.0 | $ | — | |||||||||||||||

| Fair value | $ | 2,946.3 | $ | — | $ | 3,031.1 | $ | — | |||||||||||||||

| Private placement note | |||||||||||||||||||||||

| Carrying value (excluding premium) | $ | — | $ | 160.2 | $ | — | $ | 164.9 | |||||||||||||||

| Fair value | $ | — | $ | 172.0 | $ | — | $ | 177.5 | |||||||||||||||

The fair values of our public bonds for all periods were based on quoted market prices. The fair values of our private placement note for all periods were based on interest rates offered for borrowings of a similar nature and remaining maturities.

The carrying amounts of our other financial instruments, consisting of cash and cash equivalents, accounts receivable, accounts payable, short-term debt, revolving credit agreements, promissory notes related to our equity method investment in Kazmira, and variable rate long-term debt, approximate their fair value.

NOTE 7 – INVESTMENTS

The following table summarizes the measurement category, balance sheet location, and balances of our equity securities (in millions):

| Measurement Category | Balance Sheet Location | July 3, 2021 | December 31, 2020 | |||||||||||||||||

| Fair value method | Prepaid expenses and other current assets | $ | 1.6 | $ | 2.5 | |||||||||||||||

Fair value method(1) | Other non-current assets | $ | 1.7 | $ | 1.9 | |||||||||||||||

| Equity method | Other non-current assets | $ | 69.1 | $ | 69.8 | |||||||||||||||

(1) Measured at fair value using the Net Asset Value practical expedient.

The following table summarizes the expense (income) recognized in earnings of our equity securities (in millions):

| Three Months Ended | Six Months Ended | |||||||||||||||||||||||||||||||

| Measurement Category | Income Statement Location | July 3, 2021 | June 27, 2020 | July 3, 2021 | June 27, 2020 | |||||||||||||||||||||||||||

| Fair value method | Other (income) expense, net | $ | 0.9 | $ | (0.4) | $ | 0.9 | $ | 2.5 | |||||||||||||||||||||||

| Equity method | Other (income) expense, net | $ | 0 | $ | (0.8) | $ | 0.7 | $ | (1.5) | |||||||||||||||||||||||

NOTE 8 – DISCONTINUED OPERATIONS

Our discontinued operations primarily consist of our RX segment, which held our prescription pharmaceuticals business in the U.S. and our pharmaceuticals and diagnostic businesses in Israel (collectively, the “RX business”).

On March 1, 2021, we announced a definitive agreement to sell our RX business to Altaris. On July 6, 2021, we completed the sale of the RX business for aggregate consideration of $1.55 billion, subject to customary adjustments for cash, debt, working capital and certain transaction expenses. The consideration includes approximately $53.0 million of reimbursements which Altaris will be required to deliver in cash to Perrigo pursuant to the terms of the Agreement.

16

Perrigo Company plc - Item 1

Note 8

As of March 1, 2021, we determined that the RX business met the criteria to be classified as a discontinued operation and, as a result, its historical financial results have been reflected in our consolidated financial statements as a discontinued operation and its assets and liabilities have been classified as held for sale. We ceased recording depreciation and amortization on the RX business assets from March 1, 2021. We have not allocated any general corporate overhead to the discontinued operation.

Under the terms of the agreement, we will provide transition services for up to 24 months after the close of the transaction and also enter into a reciprocal supply agreement pursuant to which Perrigo will supply certain products to the RX business and the RX business will supply certain products to Perrigo. The supply agreements have a term of four years, extendable up to seven years by the party who is the purchaser of the products under such agreement. We will also extend distribution rights to the RX business for certain OTC products owned and manufactured by Perrigo that may be fulfilled through pharmacy channels, in return for a share of the net profits.

The agreement provides that Perrigo will retain certain pre-closing liabilities arising out of antitrust (refer to Note 16 - Contingencies under the header "Price-Fixing Lawsuits") and opioid matters and the Company’s Albuterol recall, subject to, in each case, the buyer's obligation to indemnify the Company for 50 percent of these liabilities up to an aggregate cap on the buyer's obligation of $50.0 million.

Income from discontinued operations, net of tax was as follows (in millions):

| Three Months Ended | Six Months Ended | ||||||||||||||||||||||

| July 3, 2021 | June 27, 2020 | July 3, 2021 | June 27, 2020 | ||||||||||||||||||||

| Net sales | $ | 204.5 | $ | 270.4 | $ | 404.5 | $ | 528.1 | |||||||||||||||

| Cost of sales | 119.9 | 180.6 | 258.2 | 346.4 | |||||||||||||||||||

| Gross profit | 84.6 | 89.8 | 146.3 | 181.7 | |||||||||||||||||||

| Operating expenses | |||||||||||||||||||||||

| Distribution | 2.8 | 3.8 | 6.1 | 7.8 | |||||||||||||||||||

| Research and development | 17.3 | 16.4 | 30.6 | 30.1 | |||||||||||||||||||

| Selling | 8.8 | 7.4 | 16.2 | 14.7 | |||||||||||||||||||

| Administration | 12.4 | 8.1 | 30.6 | 14.5 | |||||||||||||||||||

| Restructuring | 0 | 0.4 | 0 | 0.4 | |||||||||||||||||||

| Other operating expense (income) | 0.5 | (0.9) | (0.4) | 0.2 | |||||||||||||||||||

| Total operating expenses | 41.8 | 35.2 | 83.1 | 67.7 | |||||||||||||||||||

| Operating income (loss) | $ | 42.8 | $ | 54.6 | 63.2 | 114.0 | |||||||||||||||||

| Interest expense, net | 0.2 | 1.1 | 0.8 | 2.5 | |||||||||||||||||||

| Other (income) expense, net | (0.2) | (2.9) | (1.7) | (2.1) | |||||||||||||||||||

| Income before income taxes | 42.8 | 56.4 | 64.1 | 113.6 | |||||||||||||||||||

| Income tax expense (benefit) | (11.4) | 8.2 | (25.4) | 16.7 | |||||||||||||||||||

| Income from discontinued operations, net of tax | $ | 54.2 | $ | 48.2 | $ | 89.5 | $ | 96.9 | |||||||||||||||

During the three and six months ended July 3, 2021, we incurred $2.4 million and $11.7 million, respectively, of separation costs related to the sale of the RX business, which are recorded in administration expenses.

17

Perrigo Company plc - Item 1

Note 8

Select cash flow information related to discontinued operations was as follows (in millions):

| Six Months Ended | |||||||||||

| July 3, 2021 | June 27, 2020 | ||||||||||

| Cash flows from discontinued operations operating activities: | |||||||||||

| Depreciation and amortization | $ | 15.3 | $ | 48.2 | |||||||

| Cash flows from discontinued operations investing activities: | |||||||||||

| Asset acquisitions | $ | (69.7) | $ | (0.1) | |||||||

| Additions to property, plant and equipment | $ | (6.1) | $ | (5.6) | |||||||

Asset acquisitions related to discontinued operations consisted of 2 ANDAs purchased under a contractual arrangement entered into on May 15, 2015 with a third party that specializes in research and development and obtaining approval for various drug candidates to develop specific products. On December 31, 2020, we purchased an ANDA for a generic topical gel for $16.4 million, which was subsequently paid during the three months ended April 3, 2021 and on March 8, 2021, we purchased an ANDA for a generic topical lotion for $53.3 million. The generic topical lotion acquisition was assumed by Altaris in connection with the sale of the RX business.

18

Perrigo Company plc - Item 1

Note 8

The assets and liabilities classified as held for sale related to discontinued operations were as follows (in millions):

| July 3, 2021 | December 31, 2020 | ||||||||||

| Cash and cash equivalents | $ | 9.3 | $ | 10.0 | |||||||

| Accounts receivable, net of allowance for credit losses of $1.0 and $1.1, respectively | 496.4 | 460.7 | |||||||||

| Inventories | 143.4 | 140.8 | |||||||||

| Prepaid expenses and other current assets | 21.4 | 55.4 | |||||||||

| Current assets held for sale* | 666.9 | ||||||||||

| Property, plant and equipment, net | 133.3 | 131.4 | |||||||||

| Operating lease assets | 30.0 | 31.3 | |||||||||

| Goodwill and indefinite-lived intangible assets | 680.0 | 681.2 | |||||||||

| Definite-lived intangible assets, net | 532.9 | 492.8 | |||||||||

| Deferred income taxes | 4.2 | 3.6 | |||||||||

| Other non-current assets | 22.6 | 23.7 | |||||||||

| Non-current assets held for sale* | 1,364.0 | ||||||||||

| Total assets held for sale | $ | 2,073.5 | $ | 2,030.9 | |||||||

| Accounts payable | $ | 91.6 | $ | 92.2 | |||||||

| Payroll and related taxes | 14.1 | 22.3 | |||||||||

| Accrued customer programs | 235.6 | 237.4 | |||||||||

| Other accrued liabilities | 27.4 | 67.2 | |||||||||

| Accrued income taxes | 0.1 | 0 | |||||||||

| Current indebtedness | 0.5 | 0.5 | |||||||||

| Current liabilities held for sale* | 419.6 | ||||||||||

| Long-term debt, less current portion | 0.4 | 0.7 | |||||||||

| Deferred income taxes | 3.2 | 3.1 | |||||||||

| Other non-current liabilities | 64.6 | 104.5 | |||||||||

| Non-current liabilities held for sale* | 108.3 | ||||||||||

| Total liabilities held for sale | $ | 437.5 | $ | 527.9 | |||||||

*The non-current assets and liabilities of the RX business have been reclassified to current assets and liabilities held for sale, respectively, and the sale was completed on July 6, 2021.

NOTE 9 – ASSETS HELD FOR SALE

We classify assets as "held for sale" when, among other factors, management approves and commits to a formal plan of sale with the expectation the sale will be completed within one year. The net assets of the business held for sale are then recorded at the lower of their current carrying value and the fair market value, less costs to sell.

During the three months ended July 3, 2021, management committed to a plan to sell our Latin American businesses; as a result, such assets were classified as held for sale. The assets associated with this business were reported within our CSCA segment. The sale is expected to close in the second half of 2021. At July 3, 2021, we determined the carrying value of the net assets held for sale of this business exceeded their fair value less cost to sell, resulting in an impairment charge of $152.5 million. We also recorded a goodwill impairment charge of $6.1 million within our CSCA segment, related to the Latin American businesses (refer to Note 4), resulting in a total impairment charge of $158.6 million.

In addition to the assets and liabilities held for sale related to discontinued operations (refer to Note 8), the assets and liabilities held for sale related to the Latin American businesses were reported within Current assets held for sale and Current liabilities held for sale on the Condensed Consolidated Balance Sheets. Net of impairment

19

Perrigo Company plc - Item 1

Note 9

charges, the assets and liabilities of the Latin American businesses reported as held for sale as of July 3, 2021 totaled $15.8 million and $30.8 million, respectively.

NOTE 10 – DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES

Cross Currency Swaps

On August 15, 2019, we entered into a cross-currency swap designated as a net investment hedge to hedge the EUR currency exposure of our net investment in European operations. This agreement is a contract to exchange floating-rate Euro payments for floating-rate U.S. dollar payments through August 15, 2022. The payments are based on a notional basis of €450.0 million ($498.0 million) and settle quarterly.

Interest Rate Swaps

There were no active designated or non-designated interest rate swaps as of July 3, 2021 or December 31, 2020.

Foreign Currency Forwards

Foreign currency forward contracts were as follows (in millions):

| Notional Amount | ||||||||||||||

| July 3, 2021 | December 31, 2020 | |||||||||||||

| European Euro (EUR) | $ | 209.3 | $ | 312.6 | ||||||||||

| British Pound (GBP) | 104.4 | 92.3 | ||||||||||||

| Israeli Shekel (ILS) | 71.6 | 94.4 | ||||||||||||

| Danish Krone (DKK) | 44.7 | 65.2 | ||||||||||||

| Swedish Krona (SEK) | 42.2 | 41.2 | ||||||||||||

| Chinese Yuan (CNY) | 41.5 | 49.1 | ||||||||||||

| United States Dollar (USD) | 26.3 | 101.5 | ||||||||||||

| Canadian Dollar (CAD) | 23.3 | 36.8 | ||||||||||||

| Polish Zloty (PLZ) | 22.2 | 21.8 | ||||||||||||

| Norwegian Krone (NOK) | 10.5 | 7.8 | ||||||||||||

| Romanian New Leu (RON) | 5.7 | 3.6 | ||||||||||||

| Switzerland Franc (CHF) | 5.1 | 8.2 | ||||||||||||

| Australian Dollar (AUD) | 5.0 | 11.3 | ||||||||||||

| Turkish Lira (TRY) | 4.3 | 4.0 | ||||||||||||

| Mexican Peso (MPX) | 1.0 | 15.6 | ||||||||||||

| Other | 2.6 | 2.3 | ||||||||||||

| Total | $ | 619.7 | $ | 867.7 | ||||||||||

The maximum term of our forward currency exchange contracts is 60 months.

20

Perrigo Company plc - Item 1

Note 10

Effects of Derivatives on the Financial Statements

The below tables indicate the effects of all derivative instruments on the Condensed Consolidated Financial Statements. All amounts exclude income tax effects.

The balance sheet location and gross fair value of our outstanding derivative instruments were as follows (in millions):

| Asset Derivatives | |||||||||||||||||

| Fair Value | |||||||||||||||||

| Balance Sheet Location | July 3, 2021 | December 31, 2020 | |||||||||||||||

| Designated derivatives: | |||||||||||||||||

| Foreign currency forward contracts | Prepaid expenses and other current assets | $ | 5.1 | $ | 5.0 | ||||||||||||

| Foreign currency forward contracts | Other non-current assets | 0.3 | 0.5 | ||||||||||||||

| Cross-currency swap | Other non-current assets | 4.2 | 6.3 | ||||||||||||||

| Total designated derivatives | $ | 9.6 | $ | 11.8 | |||||||||||||

| Non-designated derivatives: | |||||||||||||||||

| Foreign currency forward contracts | Prepaid expenses and other current assets | $ | 0.3 | $ | 4.3 | ||||||||||||

| Liability Derivatives | |||||||||||||||||

| Fair Value | |||||||||||||||||

| Balance Sheet Location | July 3, 2021 | December 31, 2020 | |||||||||||||||

| Designated derivatives: | |||||||||||||||||

| Foreign currency forward contracts | Other accrued liabilities | $ | 0.9 | $ | 5.5 | ||||||||||||

| Non-designated derivatives: | |||||||||||||||||

| Foreign currency forward contracts | Other accrued liabilities | $ | 1.8 | $ | 2.4 | ||||||||||||

The following tables summarize the effect of derivative instruments designated as hedging instruments in Accumulated Other Comprehensive Income ("AOCI") (in millions):

| Three Months Ended | ||||||||||||||||||||||||||||||||

| July 3, 2021 | ||||||||||||||||||||||||||||||||

| Instrument | Amount of Gain/(Loss) Recorded in OCI | Classification of Gain/(Loss) Reclassified from AOCI into Earnings | Amount of Gain/(Loss) Reclassified from AOCI into Earnings | Classification of Gain/(Loss) Recognized into Earnings Related to Amounts Excluded from Effectiveness Testing | Amount of Gain/(Loss) Recognized in Earnings on Derivatives Related to Amounts Excluded from Effectiveness Testing | |||||||||||||||||||||||||||

| Cash flow hedges: | ||||||||||||||||||||||||||||||||

| Interest rate swap agreements | $ | 0 | Interest expense, net | $ | (0.4) | Interest expense, net | $ | 0 | ||||||||||||||||||||||||

| Foreign currency forward contracts | 1.1 | Net sales | (1.0) | Net sales | 0 | |||||||||||||||||||||||||||

| Cost of sales | 0.9 | Cost of sales | 0.4 | |||||||||||||||||||||||||||||

| Other (income) expense, net | 0.4 | |||||||||||||||||||||||||||||||

| $ | 1.1 | $ | (0.5) | $ | 0.8 | |||||||||||||||||||||||||||

| Net investment hedges: | ||||||||||||||||||||||||||||||||

| Cross-currency swap | $ | (1.5) | Interest expense, net | $ | (1.1) | |||||||||||||||||||||||||||

21

Perrigo Company plc - Item 1

Note 10

| Six Months Ended | ||||||||||||||||||||||||||||||||

| July 3, 2021 | ||||||||||||||||||||||||||||||||

| Instrument | Amount of Gain/(Loss) Recorded in OCI(1) | Classification of Gain/(Loss) Reclassified from AOCI into Earnings | Amount of Gain/(Loss) Reclassified from AOCI into Earnings | Classification of Gain/(Loss) Recognized into Earnings Related to Amounts Excluded from Effectiveness Testing | Amount of Gain/(Loss) Recognized in Earnings on Derivatives Related to Amounts Excluded from Effectiveness Testing | |||||||||||||||||||||||||||

| Cash flow hedges: | ||||||||||||||||||||||||||||||||

| Interest rate swap agreements | 0 | Interest expense, net | (0.9) | Interest expense, net | 0 | |||||||||||||||||||||||||||

| Foreign currency forward contracts | (1.2) | Net sales | (1.9) | Net sales | 0 | |||||||||||||||||||||||||||

| Cost of sales | 2.8 | Cost of sales | 0.5 | |||||||||||||||||||||||||||||

| Other (income) expense, net | 0.4 | |||||||||||||||||||||||||||||||

| $ | (1.2) | $ | 0 | $ | 0.9 | |||||||||||||||||||||||||||

| Net investment hedges: | ||||||||||||||||||||||||||||||||

| Cross-currency swap | $ | (2.0) | Interest expense, net | $ | (2.2) | |||||||||||||||||||||||||||

(1) Net loss of $8.9 million is expected to be reclassified out of AOCI into earnings during the next 12 months.

| Three Months Ended | ||||||||||||||||||||||||||||||||

| June 27, 2020 | ||||||||||||||||||||||||||||||||

| Instrument | Amount of Gain/(Loss) Recorded in OCI | Classification of Gain/(Loss) Reclassified from AOCI into Earnings | Amount of Gain/(Loss) Reclassified from AOCI into Earnings | Classification of Gain/(Loss) Recognized into Earnings Related to Amounts Excluded from Effectiveness Testing | Amount of Gain/(Loss) Recognized in Earnings on Derivatives Related to Amounts Excluded from Effectiveness Testing | |||||||||||||||||||||||||||

| Cash flow hedges: | ||||||||||||||||||||||||||||||||

| Interest rate swap agreements | $ | 0 | Interest expense, net | $ | (0.5) | Interest expense, net | $ | 0 | ||||||||||||||||||||||||

| Foreign currency forward contracts | 0.5 | Net sales | 0.3 | Net sales | 0 | |||||||||||||||||||||||||||

| Cost of sales | 0.1 | Cost of sales | 0.3 | |||||||||||||||||||||||||||||

| $ | 0.5 | $ | (0.1) | $ | 0.3 | |||||||||||||||||||||||||||

| Net investment hedges: | ||||||||||||||||||||||||||||||||

| Cross-currency swap | $ | (3.3) | Interest expense, net | $ | 1.8 | |||||||||||||||||||||||||||

22

Perrigo Company plc - Item 1

Note 10

| Six Months Ended | ||||||||||||||||||||||||||||||||

| June 27, 2020 | ||||||||||||||||||||||||||||||||

| Instrument | Amount of Gain/(Loss) Recorded in OCI | Classification of Gain/(Loss) Reclassified from AOCI into Earnings | Amount of Gain/(Loss) Reclassified from AOCI into Earnings | Classification of Gain/(Loss) Recognized into Earnings Related to Amounts Excluded from Effectiveness Testing | Amount of Gain/(Loss) Recognized in Earnings on Derivatives Related to Amounts Excluded from Effectiveness Testing | |||||||||||||||||||||||||||

| Cash flow hedges: | ||||||||||||||||||||||||||||||||

| Interest rate swap agreements | $ | 0 | Interest expense, net | $ | (0.9) | Interest expense, net | $ | 0 | ||||||||||||||||||||||||

| Foreign currency forward contracts | 9.8 | Net sales | (0.1) | Net sales | 0 | |||||||||||||||||||||||||||

| Cost of sales | (1.0) | Cost of sales | 0.7 | |||||||||||||||||||||||||||||

| $ | 9.8 | $ | (2.0) | $ | 0.7 | |||||||||||||||||||||||||||

| Net investment hedges: | ||||||||||||||||||||||||||||||||

| Cross-currency swap | $ | (18.3) | Interest expense, net | $ | 4.6 | |||||||||||||||||||||||||||

The amounts of (income)/expense recognized in earnings related to our non-designated derivatives on the Condensed Consolidated Statements of Operations were as follows (in millions):

| Three Months Ended | Six Months Ended | |||||||||||||||||||||||||||||||

| Non-Designated Derivatives | Income Statement Location | July 3, 2021 | June 27, 2020 | July 3, 2021 | June 27, 2020 | |||||||||||||||||||||||||||

| Foreign currency forward contracts | Other (income) expense, net | $ | (3.1) | $ | (7.0) | $ | (5.9) | $ | (0.2) | |||||||||||||||||||||||

| Interest expense, net | 0.4 | 1.1 | 0.9 | 1.4 | ||||||||||||||||||||||||||||

| $ | (2.7) | $ | (5.9) | $ | (5.0) | $ | 1.2 | |||||||||||||||||||||||||

The classification and amount of gain/(loss) recognized in earnings on fair value and hedging relationships were as follows (in millions):

| Three Months Ended | ||||||||||||||||||||||||||

| July 3, 2021 | ||||||||||||||||||||||||||

| Net Sales | Cost of Sales | Interest Expense, net | Other (Income) Expense, net | |||||||||||||||||||||||

| Total amounts of income and expense line items presented on the Condensed Consolidated Statements of Operations in which the effects of fair value or cash flow hedges are recorded | $ | 981.1 | $ | 632.1 | $ | 31.6 | $ | (0.4) | ||||||||||||||||||

| The effects of cash flow hedging: | ||||||||||||||||||||||||||

| Gain (loss) on cash flow hedging relationships | ||||||||||||||||||||||||||

| Foreign currency forward contracts | ||||||||||||||||||||||||||

| Amount of gain or (loss) reclassified from AOCI into earnings | $ | (1.0) | $ | 0.9 | $ | 0 | $ | 0 | ||||||||||||||||||

| Amount excluded from effectiveness testing recognized using a systematic and rational amortization approach | $ | 0 | $ | 0.4 | $ | 0 | $ | 0.4 | ||||||||||||||||||

| Interest rate swap agreements | ||||||||||||||||||||||||||

| Amount of gain or (loss) reclassified from AOCI into earnings | $ | 0 | $ | 0 | $ | (0.4) | $ | 0 | ||||||||||||||||||

23

Perrigo Company plc - Item 1

Note 10

| Six Months Ended | ||||||||||||||||||||||||||

| July 3, 2021 | ||||||||||||||||||||||||||

| Net Sales | Cost of Sales | Interest Expense, net | Other (Income) Expense, net | |||||||||||||||||||||||

| Total amounts of income and expense line items presented on the Condensed Consolidated Statements of Operations in which the effects of fair value or cash flow hedges are recorded | $ | 1,991.1 | $ | 1,273.7 | $ | 63.6 | $ | 1.9 | ||||||||||||||||||

| The effects of cash flow hedging: | ||||||||||||||||||||||||||

| Gain (loss) on cash flow hedging relationships | ||||||||||||||||||||||||||

| Foreign currency forward contracts | ||||||||||||||||||||||||||

| Amount of gain or (loss) reclassified from AOCI into earnings | $ | (1.9) | $ | 2.8 | $ | 0 | $ | 0 | ||||||||||||||||||

| Amount excluded from effectiveness testing recognized using a systematic and rational amortization approach | $ | 0 | $ | 0.5 | $ | 0 | $ | 0.4 | ||||||||||||||||||

| Interest rate swap agreements | ||||||||||||||||||||||||||

| Amount of gain or (loss) reclassified from AOCI into earnings | $ | 0 | $ | 0 | $ | (0.9) | $ | 0 | ||||||||||||||||||

| Three Months Ended | ||||||||||||||||||||||||||

| June 27, 2020 | ||||||||||||||||||||||||||

| Net Sales | Cost of Sales | Interest Expense, net | Other (Income) Expense, net | |||||||||||||||||||||||

| Total amounts of income and expense line items presented on the Condensed Consolidated Statements of Operations in which the effects of fair value or cash flow hedges are recorded | $ | 948.8 | $ | 601.6 | $ | 32.2 | $ | 17.1 | ||||||||||||||||||

| The effects of cash flow hedging: | ||||||||||||||||||||||||||

| Gain (loss) on cash flow hedging relationships | ||||||||||||||||||||||||||

| Foreign currency forward contracts | ||||||||||||||||||||||||||

| Amount of gain or (loss) reclassified from AOCI into earnings | $ | 0.3 | $ | 0.1 | $ | 0 | $ | 0 | ||||||||||||||||||

| Amount excluded from effectiveness testing recognized using a systematic and rational amortization approach | $ | 0 | $ | 0.3 | $ | 0 | $ | 0 | ||||||||||||||||||

| Interest rate swap agreements | ||||||||||||||||||||||||||

| Amount of gain or (loss) reclassified from AOCI into earnings | $ | 0 | $ | 0 | $ | (0.5) | $ | 0 | ||||||||||||||||||

24

Perrigo Company plc - Item 1

Note 10

| Six Months Ended | ||||||||||||||||||||||||||

| June 27, 2020 | ||||||||||||||||||||||||||

| Net Sales | Cost of Sales | Interest Expense, net | Other (Income) Expense, net | |||||||||||||||||||||||

| Total amounts of income and expense line items presented on the Condensed Consolidated Statements of Operations in which the effects of fair value or cash flow hedges are recorded | $ | 2,032.0 | $ | 1,291.1 | $ | 61.1 | $ | 18.8 | ||||||||||||||||||

| The effects of cash flow hedging: | ||||||||||||||||||||||||||

| Gain (loss) on cash flow hedging relationships | ||||||||||||||||||||||||||

| Foreign currency forward contracts | ||||||||||||||||||||||||||

| Amount of gain or (loss) reclassified from AOCI into earnings | $ | (0.1) | $ | (1.0) | $ | 0 | $ | 0 | ||||||||||||||||||

| Amount excluded from effectiveness testing recognized using a systematic and rational amortization approach | $ | 0 | $ | 0.7 | $ | 0 | $ | 0 | ||||||||||||||||||

| Interest rate swap agreements | ||||||||||||||||||||||||||

| Amount of gain or (loss) reclassified from AOCI into earnings | $ | 0 | $ | 0 | $ | (0.9) | $ | 0 | ||||||||||||||||||

NOTE 11 – LEASES

The balance sheet locations of our lease assets and liabilities were as follows (in millions):

| Assets | Balance Sheet Location | July 3, 2021 | December 31, 2020 | |||||||||||||||||

| Operating | Operating lease assets | $ | 171.3 | $ | 154.7 | |||||||||||||||

| Finance | Other non-current assets | 31.0 | 29.8 | |||||||||||||||||

| Total | $ | 202.3 | $ | 184.5 | ||||||||||||||||