July 17, 2014

Ms. Mara L. Ransom

Assistant Director

Division of Corporation Finance

Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

Telephone Number: (202) 551-3720

| Re: | Principal Solar, Inc. |

Form S-1 | ||

Filed December 23, 2013 | ||

File No. 333-193058 |

Dear Ms. Ransom,

In response to your comment letter dated May 29, 2014, Principal Solar, Inc. (the “Company” or “Principal Solar”) has the following responses. We have reproduced your comments for your convenience and have followed each comment with our response. References in this letter to “we,” “our,” or “us” means the Company or its advisors, as the context may require.

Prospectus Summary, page 2 Business, page 2

1. Please provide further disclosure clarifying what is meant by the “world’s first distributed solar utility.”

The wording has been revised to read:

" To date, we have completed the acquisition of four entities (including three solar power production companies). We have begun to create what we call the “world’s first distributed solar utility” - although there are many individual solar projects in operation throughout the world, we don’t believe that anyone has previously attempted to bring together multiple, disparate, geographically diverse solar projects under common ownership thereby building a complete utility-scale solar power generation company."

Risks Factors, page 11

General Risks, page 11

We believe that certain prior corporate actions undertaken by us . . ., page 17

2700 Fairmont Street, Dallas, Texas 75201

Ph. 855.774.7799 • Fax: 855.774.7799

Securities and Exchange Commission

July 17, 2014

Page 2 of 12

2. Please remove the statement that you “also believe that the risks associated with the prior failure of the Company to formally file a preferred stock designation for the Series A Preferred Stock and to obtain valid shareholder approval for the reverse stock is minimal” as it mitigates the risk you disclose. Please also tell us the basis for your belief as to the minimal risk you describe here.

The referenced language has been removed. The Company believes the risk related to the prior failure to the Company to formally file a preferred stock designation for the Series A Preferred Stock and to obtain valid shareholder approval for the reverse stock split is minimal because:

1) | While no preferred stock designation was ever filed with New York, the rights associated with the designation were validly approved by the Board of Directors; |

2) | We are aware of no way to cure such failure or to remedy such failure to file the designation under New York law (notwithstanding the fact that as described below the Company is now subject to Delaware law); |

3) | A period of more than three years has elapsed from the date of the purported designation of preferred stock, issuance and reverse stock split and the Company is not aware of any actions, claims or disputes relating to such failure to designate the preferred stock or obtain shareholder approval for the prior action to date; |

4) | The reverse stock split has previously been affected by New York (pursuant to the filing of a Certificate of Amendment) and in the marketplace (and approved by FINRA in connection with such corporation action); |

5) | The Company subsequently re-domiciled to Delaware (and adopted a Certificate of Incorporation in connection with re-domiciling) and as such is no longer governed by New York law; and |

6) | The effect of overturning the reverse stock split; notwithstanding the fact that we are not aware of any rights that exist or claimants that could enforce such overturning, and notwithstanding the fact that we do not have a sufficient number of authorized but unissued shares to allow for such overturning, would only result in the total number of shares of common stock outstanding increasing by a factor of four to one, but would not have an effect on the relative ownership percentages of our shareholders. |

Notwithstanding the above, the Company may in the future choose to seek shareholder approval to “ratify” (after the fact), the prior reverse stock-split in the event such action was deemed necessary and reasonable at such time as the Company holds its next annual meeting of shareholders.

Risks Relating To the Company’s Operations and Planned Operations, page 18 Our estimates and business plan are built around the assumption that grid parity . . ., page 25

3. Please remove the statement regarding the GBI Research report stating that “grid parity in the United States (on average) will occur between 2014 and 2017” as it mitigates the risk that you discuss here.

The referenced language has been removed.

Description of Business, page 31

Securities and Exchange Commission

July 17, 2014

Page 3 of 12

Business Strategies, page 33

4. We note your response to comment 10 in our letter dated January 22, 2014. Please provide further details regarding “the experience of the Company’s management that the solar industry is fragmented, has experienced rapid expansion, growing acceptance, and declining costs.”

The wording has been revised to read:

"Our Primary objective is to build a significant, innovative and valuable solar company. We are currently employing our business expertise, our Board of Directors, advisory team and employee expertise with the goal of accelerating growth in an industry that we believe is ripe for consolidation today based upon our management’sobservation that the solar industry has many unrelated participants (i.e., that it is "fragmented"), our observation of the industry's rapid expansion and growing acceptance of solar generation, and the observable declining costs for solar panels and inverters. These observations have caused us to believe the solar industry is on the brink of building very large scale projects in the next two to three years due to the number of projects currently proposed. Each of these observationsis described in greater detail below under "Industry"."

5. Please provide further details regarding how you plan to “[d]evelop, opportunistically, new commercial and utility solar projects utilizing our partnerships and relationships” and “[b]uild an entity capable of creating innovative, very large gigawatt (GW) scale projects around the world based on solid economics,” including how you plan to finance such projects.

The wording has been revised to read:

"Develop new commercial utility-scale solar projects leveraging our existing partnerships and relationships and those of our Board members and advisors, many of whom have spent decades in management roles within the traditional utility or energy industries, to make introductions to solar project developers, financiers, and utility industry executives with whom we hope to negotiate power purchase agreements, interconnection agreements, and other agreements."

- and-

"Build an entity capable of creating innovative large-scale solar projects by hiring capable and experienced engineers and engaging developers experienced in the design and construction of large-scale solar projects, both domestically and abroad; by hiring capable executives in accounting, legal, real estate, etc., necessary to manage such an endeavor; and by obtaining financing from commercial banks, non-bank lenders (assuming such financing is available), and one or more public or private offerings of our equity securities in combination sufficient to fund the project. We expect such financing needs could fall within the range of $1.5 to $2.0 billion, which funding may not be available on favorable terms, if it all."

Industry, page 35

6. We note that many of your charts showing the declining cost of PV panels and the retail cost of electricity reflect data as of 2012 and 2009, respectively. We also note your disclosure that the cost of PV panels has increased from $0.60 in October 2013 to approximately $0.70 per watt in March 2014. Please provide updated disclosure regarding the costs of PV panels and retail electricity.

The wording has been revised to read:

"As of March 2014, the price is averaging approximately $.70 per watt, comparable to the forecasted amount in the chart above. "

Securities and Exchange Commission

July 17, 2014

Page 4 of 12

The adjacent chart forecasted $.74 in 2013, and the earlier reference to $.60 was a typographical error.

Further Business Strategies, page 40

7. Please provide the basis for management’s belief that “it has strong enough contacts in some of the world’s largest companies and in the decision making segments of utilities and governments that give us the opportunities to build gigawatt scale projects in key global locations.”

The wording has been revised to read:

"Through its management team, Board members, and advisors, many of whom have spent decades in management roles within some of the largest and best known traditional utilities (TXU Corp., Oncor), energy companies (Hunt Consolidated Energy), and others (Electronic Data Systems, Luminant Worldwide Corporation, McKinsey & Company, and 7-Eleven) management believes it has strong enough contacts in some of the world’s largest companies and in the decision making segments of utilities and governments that give us the opportunities to build gigawatt scale projects in key global locations."

Key Project Assessment Criteria, page 41

Tax Strategies, page 43

8. Please provide the rationale for your statement that the bonus depreciation incentive that expired at the end of 2013 “may be extended through 2014 and applied retroactively to January 1st of 2014.”

| The wording has been revised to read: | ||

| | "Tax strategies. Our finance model assumes various tax benefits and strategies to include bonus depreciation, accelerated depreciation schedules and investment tax credits. For example, Modified Accelerated Cost Recovery System (MACRS) allows tangible property to be depreciated on an accelerated basis. Solar projects qualify for MACRS treatment and are depreciated, for tax purposes, over the course of six years. In recent years, Congressional legislation has amplified the tax benefits related to accelerated depreciation to include a 50% first-year ‘bonus depreciation’ provision for qualified renewable energy systems. The bonus depreciation incentive expired at the end of 2013 yet, provided that, as in prior years, it may yet be extended and applied retroactively to January 1st of 2014. |

The 50% first-year bonus depreciation provision, first enacted in 2008, was extended in February 2009 (retroactively for the entire 2009 tax year) under the same terms as originally enacted by the American Recovery and Reinvestment Act of 2009 (House of Representatives Resolution (H.R.) 1). It was renewed again in September 2010 (retroactively for the entire 2010 tax year) by the Small Business Jobs Act of 2010 (H.R. 5297). In December 2010 the provision for bonus depreciation was amended and extended yet again by the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (H.R. 4853). Under these amendments, eligible property placed in service after September 8, 2010 and before January 1, 2012 was permitted to qualify for 100% first-year bonus depreciation. The December 2010 amendments also permitted bonus depreciation to be claimed for property placed in service during 2012, but reduced the allowable amount from 100% to 50% of the eligible basis. The 50% first-year bonus depreciation allowance was further extended for property placed in service during 2013 by the American Taxpayer Relief Act of 2012 (H.R. 8, Sec. 331) in January 2013. As of May 21, 2014, an extension of the 50% bonus depreciation through 2016 is being considered by the U.S. Congress as a part of the "Expiring Provisions Improvement Reform and Efficiency (EXPIRE) Act", though no assurance can be made as to its ultimate passage or final terms." |

Securities and Exchange Commission

July 17, 2014

Page 5 of 12

White Papers, Standards, and Thought Leadership, page 43

9. Please provide further details regarding the Lifetime Energy Production (LEP) ranking metric, including additional disclosure regarding how LEP is calculated and if this ranking metric is widely accepted by the solar industry.

The Company has added significant additional disclosures regarding how LEP is calculated and acceptance of the ranking metric under “Description of Business” – “Business Strategies” - “Principal Solar Institute PV Module Rating”.

10. We note your response to comment 15 in our letter dated January 22, 2014. While we note that you do not produce or sell PV modules, photovoltaic modules and solar power generation systems, both play a direct role in your business. In addition, the Principal Solar Institute brings together individuals chosen by your management, and, in some cases, members of your management, who draft white papers and articles published on behalf of you. As such, please provide further details regarding your belief that the Principal Solar Ratings System is unbiased.

"We believe the Principal Solar Institute PV Module Ratings are unbiased in the sense that we run all PV modules through the same algorithms, with no bias toward results. Since all modules are rated based initially on information supplied by the manufacturer, we believe that by using the same criteria for each module evaluated we eliminate our ability to effect the results of the review process. However, the weighting of the individual factors that comprise the ratings was determined by us and may be perceived as biased by some. For example, if someone believes that Negative Power Tolerance should be more impactful in a rating of LEP than Total Area Efficiency or should carry a heavier coefficient of weighting, they may perceive the ratings as biased. That said, it is our opinion that by being consistent in the application of a standard and uniform algorithm to all modules we evaluate, and by using data supplied by manufacturers, we are being consistent and unbiased in our evaluation of any individual PV module."

Material Acquisitions, page 49

11. We note your response to comment 18 in our letter dated January 22, 2014. We note that, while your disclosure described each of the three acquisitions, it does not describe the terms of each of the Power Purchase Agreements. Here or in an appropriate place in your prospectus, please revise to provide the terms of your Power Purchase Agreements.

The wording has been amended to include in addition to the prior language the following:

"SunGen Mill 77 LLC and SunGen StepGuys LLC

Power generated by these facilities is sold to the users upon whose property the solar facility is installed at a floating price indexed to electricity prices in the area for a term expiring in 2025, with an option for the purchaser to extend for two additional terms of 25 years each.

Securities and Exchange Commission

July 17, 2014

Page 6 of 12

Powerhouse One

Power generated by the facility is sold to a utility in Franklin County Tennessee under a PPA having a fixed premium of $0.12 per kilowatt-hour (“kWh”) over the GSA-1 scheduled rate (currently approximately $0.10 per kWh) resulting in a forecasted rate of $0.22 per kWh through 2021, and a market rate based upon the GSA-1 scheduled rate for the remaining 10 years of the initial 20 year term.

."

Legal Proceedings, page 53

12. We note your response to comment 26 in our letter dated January 22, 2014. Please revise your disclosure to include the percentage of your common stock beneficially owned by Pegasus Funds.

"The wording has been amended to read:

“Management believes all such liabilities have been indemnified by Pegasus Funds, LLC to which (including its assigns) the Company issued 2,138,617 shares of its common stock as part of the reverse merger transaction. As of the date of this Prospectus, and to the best knowledge of the Company, without independent confirmation, Pegasus Funds, LLC (and its related parties) beneficially owns less than 5% of our outstanding common stock."

Directors, Executive Officers, Promoters and Control Persons, page 54

Biographical Information, page 54

13. Please further revise this section to provide abrief description of the business experience during the past five years of each director and executive officer, including the dates of each person’s principal occupations and employment during the past five years. You should identify the type of occupation and the nature of the business of prior employers but you should not include additional disclosure that appears to constitute your opinion, or does not specifically satisfy the requirements of the federal securities laws, such as “[d]uring the next three years, Ms. Laine became the number one ranked independent artist on the Country Music Chart, was nominated for best female artist by Country Music Radio DJs in 2002, and put six songs on the charts.” Please see Item 401(e) of Regulation S-K.

The biographical information for each Director and officer has been shortened and information reflecting an opinion, either management's or others, have been removed.

Security Ownership of Certain Beneficial Holders and Management, page 64

14. | We note that Ray L. Hunt, father of your former director Hunter Hunt, is deemed to have beneficial ownership over the shares held by Steuben Investment Company II, L.P. Please confirm if Hunter Hunt can also be deemed to be a beneficial owner of such shares. Please see Rule 13d-1 under the Securities Exchange Act of 1934, as amended. |

Securities and Exchange Commission

July 17, 2014

Page 7 of 12

We have been advised that Steuben Investment Company II, L.P. (“Steuben”) has two general partners, RLH Management, Inc. (“RLH Management”) and Steuben Co-GP, Inc. (“Steuben Co-GP”), each of which has the power to vote and dispose of the Company’s common stock held by Steuben. RLH Management is 100% owned and controlled by Ray L. Hunt. Steuben Co-GP is owned and controlled by Loyal Trust No. 1, whose sole trustee is R. Gerald Turner and whose sole current lifetime beneficiary is Ray L. Hunt. While Hunter L. Hunt (i) is a contingent remainder beneficiary of Loyal Trust No. 1 and (ii) is the beneficiary of another trust which holds a minority limited partnership interest in Steuben and whose sole trustee is Ray L. Hunt, Hunter L. Hunt has no power which would allow him to control the vote or disposition of any Company common stock held by Steuben. Based on the foregoing, Hunter L. Hunt (who resigned as a director of the Company on October 27, 2013) is not deemed to be the beneficial owner of any of the shares of common stock held by Steuben.

15. | We note your statement that “Mr. Dauterman may also be deemed to beneficially own additional securities in the Company other than as set forth in the table above.” Please note that your disclosure should include all of the shares beneficially owned by any person who is the beneficial owner of more than 5% of your voting securities. (emphasis added) Please also include the name of each individual or entity that is a direct beneficial holder of your shares (for example, Pegasus Funds LLC) in your beneficial ownership table. Please see Item 403(a) of Regulation S-K. |

We have determined that, as of the date of this Prospectus, neither Mr. Dauterman nor Pegasus is a greater than 5% stockholder of the Company and the Registration Statement has been modified accordingly.

Management’s Discussion and Analysis of Financial Condition and Results of Operations, page 67

Plan of Operations, page 67

16. | We note your response to comment 22 in our letter dated January 22, 2014 and your revised disclosure on pages 67 and 71. However, we note your revised disclosure now states that you need to raise approximately $5,000,000 of additional funding to satisfy your cash requirements for the next 24 months, exclusive of acquisitions. We also note your disclosure that in the event you are unable to raise funding or funding is not available on favorable terms, you can continue your operations at the current level for approximately six months. Please revise your disclosures to provide a reasonably detailed discussion of your viable plan to continue in business for at least the 12 month period following the date of the most recent financial statements included in the filing. If you are unable to raise funds to satisfy your anticipated cash requirements over the next 12 months, please disclose what other actions you might take in order to continue in business as a going concern. Please refer to Section 607.07 of the Codification of Financial Reporting Releases. |

Other than continuing to obtain additional funding, there is no viable plan that would allow the Company to continue operations beyond the next six months from the date of this Registration Statement, and the need for additional funding for both administrative needs and to support future acquisitions has appeared throughout this Registration Statement. As such, the Plan of Operations has been augmented to include:

" To date, we have funded our operations primarily through private placements of common stock and convertible debt securities. Since the date of the reverse merger with Principal Solar Texas, we have sold 6,162,829 shares of our common stock for aggregate proceeds of $5,672,940. These sales of our common stock reflect issuance prices ranging from $0.55 to $1.69 per share (weighted average of $0.92).

In the event we are unable to obtain additional funding through similar means in the future to support our administrative needs, we believe we can continue our operations at the level currently conducted, without consummating any acquisitions or expanding our operations, for approximately six months from the date hereof. As a result, our independent registered public accounting firm issued a qualified "going concern" opinion in connection their audit of our financial statements as of and for the year ended December 31, 2013."

Securities and Exchange Commission

July 17, 2014

Page 8 of 12

Our repeated and demonstrated ability to obtain funding to support our administrative needs was sufficient to satisfy our accountants as to the propriety of presenting our statements on the basis of being a going concern. Had we been able to develop a plan to continue operations for a period of 12 months from the last Balance Sheet date without additional financing, we would not have received a qualified opinion on those statements.

17. | Please expand your disclosure to address how you intend to find and finance your acquisitions. In this regard, we note your statement that acquisition activity and acquisition expenses can vary widely, and, as such, it is “impossible” to “estimate monthly expenses with any degree of certainty.” However, we also note that acquisitions are one of the four prongs of your business strategy. Please provide further details regarding how you expect to find and finance such acquisitions. |

The wording has been amended to read:

“We intend to find new acquisition opportunities in several important ways including:

● | Leveraging our existing partnerships and relationships and those of our Board members and advisors, many of whom have spent decades in management roles within the traditional utility or energy industries, to make introductions to solar project developers. |

● | Continuing to author technical white papers, hold informational seminars, post on solar industry blogs, and comment on other industry websites, all with the intention of increasing our recognition within the industry and driving solar developers and solar projects to us. |

● | Continuing an active internal business development function of scanning publications, news releases, and other materials to become aware of and pro-actively solicit new opportunities. |

● | Continuing to participate in trade shows, seminars, and presentations sponsored by others in the industry. |

We intend to finance acquisitions on a project-by-project basis separate and apart from financing for the administrative needs of the Company. Toward this end, we have engaged Carlyle Capital Markets, Inc. (as described above under “Description of Business” – “Recent Events”), to lead our efforts to secure project specific financing in the form of tax equity, traditional equity, and debt financing. We might also affect one or more public (following the effectiveness of our registration statement of which this Prospectus forms a part) or private offerings of our equity securities to fund a portion of the projects.

Securities and Exchange Commission

July 17, 2014

Page 9 of 12

Making an acquisition is comprised of at least six stages: identification, evaluation, negotiation, due diligence, financing, and finally closing. Given the several and varied nature of our efforts to find acquisition opportunities, the uncertainty of when suitable opportunities will be identified, the uncertainties of the scale of those opportunities, the uncertainty of the time it takes to evaluate and close those opportunities, and the uncertainties of how long it takes to obtain the project specific financing for those opportunities, if such funding can be obtained at all, a schedule and quantification of acquisition related expenses with any degree of certainty is not possible, and acquisition related expenses comprise a significant portion of our current monthly expenses.”

Plan of Distribution and Selling Stockholders, page 80

18. | We note your disclosure in footnote 5 that the beneficial owner of the shares held by Pathfinder Worldwide Financial Group LLC is Grant Seabolt. Please also disclose that Mr. Seabolt is your outside counsel in connection with this registration statement. Please see Item 507 of Regulation S-K. |

The wording has been amended to read:

"(5) The beneficial owner of the shares held by Pathfinder Worldwide Financial Group LLC is Grant Seabolt, our outside general counsel."

19. | We note your response to comment 29 in our letter dated January 22, 2014. Please identify in the registration statement the person or persons who have voting or investment control over your securities that the entity owns. Please refer to Question 140.02 of our Regulation S-K Compliance and Disclosure Interpretations located at our web-site, www.sec.gov. |

The footnotes to the table have been amended to identify the beneficial owner wherever the individual ownership would not otherwise be apparent.

Financial Statements for the Fiscal Years Ended December 31, 2013 and 2012, page F-2

Notes to Consolidated Financial Statements, page F-7

Note 2. Summary of Significant Accounting Policies, page F-8

Revenue Recognition, page F-10

20. Please address the following comments:

● | Please tell us if your solar power facilities generate renewable energy credits, performance-based incentives, or other similar credits. If so, tell us in sufficient detail and disclose how you account for such arrangements. |

The footnote has been amended to read "Our current power generation operations do not generate renewable energy credits, performance-based incentives, or similar credits to the benefit of the Company."

● | Please explain to us in sufficient detail if your Powerhouse One Power Purchase Agreement (“PPA”) qualifies as a lease under ASC 840-10-15-6. If so, explain to us how you determined the appropriate lease classification and clarify if you consider the lease payments to be minimum lease payments, contingent rents, or a combination of the two. |

Securities and Exchange Commission

July 17, 2014

Page 10 of 12

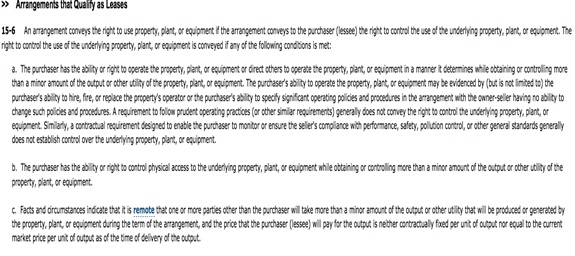

ASC 840-10-15-6 reads as follows:

Under a PPA, the purchaser has the right and the obligation to purchase electricity produced by the facility at a pre-determined fixed or determinable indexed price per kWh for a specified period. The purchaser has no right to operate the facility, to direct others to do so, to replace the operations and maintenance (O&M) provider, nor to specify operating policies beyond the initial interconnect agreement which primarily consists of prudent operating practices consistent with the generation and delivery of high voltage electricity.

The purchaser has the right to access the property for its needs to monitor and manage its meters, but does not have the right to control the access of others.

By contract, the purchaser will purchase 100% of the output for the term of the PPA, but the price at which it will do so is determined or determinable at the time of signing the PPA.

Note 5. Acquisitions, page F-11

21. We note your response to comment 38 in our letter dated January 22, 2014. We do not agree with your statement that you are not required to provide financial statements and pro form financial information for this acquired business because you acquired it while you were still a private company. Since the acquisition of Powerhouse One LLC is significant at greater than the 40 percent level, historical audited financial statements of the acquired business for the two most recent fiscal years and unaudited financial statements for the most recent subsequent interim period preceding the date of the acquisition and the corresponding interim period of the preceding year are required and should be filed with your next amendment. Please refer to Rule 8-04(c) of Regulation S-X. Please also provide the pro forma financial information required by Rule 8-05 of Regulation S-X.

Securities and Exchange Commission

July 17, 2014

Page 11 of 12

An audit of the acquired company as of and for the years ended December 31, 2012 and 2011, and a review as of and for the three months ended March 31, 2013 and 2012, have been completed and the separate financials included in the amended Registration Statement. Additionally, pro forma statements have been included as an exhibit to the Registration Statement to include a Statement of Operations for the year ended December 31, 2012, and the three months ended March 31, 2013. No pro forma Balance Sheets are provided pursuant to the Division of Corporation Finance Financial Reporting Manual section 3220.1 as the acquisition has been presented in a subsequent Balance Sheet previously filed.

22. Please address the following comments related to your Powerhouse One acquisition:

● | We note that the acquisition was largely funded by a $5 million loan obtained by the acquiree. Please explain to us the mechanics of this transaction in greater detail, including an explanation of why the acquiree, not you, appeared to directly obtain financing and a summary of how the cash physically flowed between the involved parties. |

The Powerhouse One ("Ph1") acquisition was financed, in part, by a $5,050,000 loan from Bridge Bank, NA. The acquired assets and liabilities of Ph1 were purposefully segregated into a separate "bankruptcy remote" subsidiary of the Company so as to fully protect the lender from any potential pitfalls coming to the parent company, the other operating facilities, or any future acquisitions in which they do not participate in the financing. This is a common practice in our industry as well as other industries as a single lender may or may not participate in the financing of all projects.

On the advice of counsel, in order to ensure the segregation of assets and liabilities in a separate entity in both appearance and in fact, the debt was obtained directly by the subsidiary rather than the parent company and the proceeds from the loan went directly to the sellers, passing through the bank accounts of neither the parent Company nor the subsidiary itself.

● | We note that the acquisition did not result in any purchase price allocation to intangible assets, such as customer-related or contract-based intangible assets. We note, for example, that Powerhouse One generates revenues under an 8-year PPA. See ASC 805-20-25-10. |

Having a single customer for the power generated by the acquired Ph1 assets, the Company has concluded it has no typical customer-related intangible assets, but is still assessing the existence and valuation of any contract-based intangible assets and goodwill.

In accordance with Accounting Standards Codification 805-10-25-14 "The Measurement Period" for identifying assets, liabilities, and the valuation thereof for purposes of adjusting the provisional allocation of the purchase "shall not exceed one year from the acquisition date. The acquisition of Powerhouse One occurred on June 17, 2013, and the Company is continuing its efforts to identify appropriate assets and allocate the purchase price accordingly.

Current Report on Form 8-K, filed May 5, 2014

23. We note the Form 8-K dated May 5, 2014 that you filed on EDGAR, even though you are not yet subject to any periodic reporting obligations. Please tell us the purpose of the materials that are attached as exhibits, with a view to understanding the reason for the presentation and the intended audience. If these materials were presented to potential investors, please provide us with your analysis as to whether these materials constitute offers of securities and, if so, how the materials are consistent with Section 5 of the Securities Act of 1933.

Securities and Exchange Commission

July 17, 2014

Page 12 of 12

While the Company is not currently a reporting company with the SEC, its common stock does trade publicly on the OTC Pink Sheets market. As such, the Company felt it prudent and within the intent of Regulation FD to file the presentation included as part of the above referenced Form 8-K (which as referenced in the Form 8-K, the Company was presenting to ‘a small gathering of current investors and bankers’), which the Company determined could contain material non-public information, to avoid any potential issues which could occur had persons who had knowledge of the presentation (had such information not been made publicly available) traded on such information. For example, to avoid a situation where persons with knowledge of the information could be found to have traded on material non-public information and to not prejudice current (and potential) shareholders of the Company and the market in general by providing potential material non-public information to some persons and not others. The Company chose to file the presentation as part of a Form 8-K instead of through the OTC news service as it believed dissemination with the SEC would reach a broader audience and would be more consistent with how it will file future presentations and reports in the future, assuming the registration statement is declared effective and the Company becomes subject to reporting requirements. Notwithstanding the above, neither the prepared presentation filed with the Form 8-K, nor remarks made at the presentation itself were meant to be treated as an offer to sell or the solicitation of an offer to buy any securities of the Company.

Sincerely,

David N. Pilotte

Chief Financial Officer