UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number: 811-22895 |

Capitol Series Trust

(Exact name of registrant as specified in charter)

Ultimus Fund Solutions, LLC

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

(Address of principal executive offices) (Zip code)

Zachary P. Richmond

Ultimus Fund Solutions, LLC

225 Pictoria Drive, Suite 450

Cincinnati, OH 45246

(Name and address of agent for service)

| Registrant’s telephone number, including area code: | 513-587-3400 |

| Date of fiscal year end: | September 30 |

| Date of reporting period: | September 30, 2021 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Guardian Capital Dividend Growth Fund

Class I – DIVGX

Annual Report

September 30, 2021

Guardian Capital LP

Commerce Court West

199 Bay Street, Suite 3100

P.O. Box 201

Toronto, Ontario M5L 1E8

Telephone: (800)-968-2295

Portfolio Managers’ Letter to Shareholders (Unaudited)

Annual Commentary September 30, 2021

Guardian Capital Dividend Growth Fund (the “Fund”) returned 2.42% (USD) in the five month period ended September 30, 2021, in line with the MSCI World Index, which returned 2.95%.

The positive economic momentum continued globally throughout Q3, 2021; however, a renewed wave of COVID-19 cases hindered reopening plans and saw the pace of recovery moderate from early highs. That said, growth remained above pre-crisis trends as governments did not so much reinstate stringent public health measures as much as they just delayed moving into the next stage of reopening — the hard-hit service sector continued on its long path toward normalization while activity among goods producers remained robust against strong demand.

Despite increased capacity utilization, supply chain issues persisted, which constrained overall activity and drove upward price pressures across the production pipeline. Concerns that rising inflation may prove less transitory than previously assumed became more evident, and combined with indications of sustained economic growth, resulted in central banks beginning to take steps toward reigning in the crisis-era stimulus. Some monetary authorities, particularly within emerging markets, even began raising policy rates to keep inflation in check.

As investors re-priced the path for central bank policy, market interest rates moved higher and the yield curve steepened through the quarter, weighing on performance of fixed income securities, especially government bonds and those issues with longer-durations; corporate and short-duration bonds outperformed in Q3, 2021.

The rising interest rate environment provided headwinds to global equity performance, as did growing concerns over government regulatory crackdowns in China, sparring over fiscal policy in the US and the ongoing pandemic. The confluence of these risks weighed on investor sentiment at the end of the quarter and offset the fundamental positives of the still-improving economic growth backdrop and resultant constructive earnings outlook.

During the five month period ended September 30, 2021, the largest detractors of performance came from the Materials and Real Estate sectors. In the Materials sector, an overweight led to a negative allocation effect, coupled with a negative stock selection effect as Air Products lagged the sector. Within Real Estate, Medical Properties Trust had a negative stock selection effect. The Consumer Staples sector was the largest contributor to relative performance due to positive stock selection from Costco and Nestle. In the Industrial sector, positions in Wolters Kluwer, Republic Services, Waste Management and Rockwell Automation led to a positive stock selection effect.

1

Portfolio Managers’ Letter to Shareholders (Unaudited) (continued)

We increased the mandate’s weight in the Health Care sector with purchases of United Health Group and Zoetis, both companies that show strong forecasted earnings growth coupled with strong dividend growth. During the second quarter, we added to the Energy sector with the purchase of Royal Dutch Shell, which offers a strong visible cash flow, which should bode well for future dividend growth.

The concerns that rose to the fore in Q3, 2021 (China, US politics, central bank policy) and took the wind out of equity market sails are likely to persist over the near term, constraining performance of risk assets and leading to bouts of market turmoil (that have been generally scarce over the last year). Barring an escalation of risks or other shocks putting material stress on the global economy, however, the positive underlying fundamentals would appear to be poised to support a resumption of upward market momentum.

Global growth is slowing from the unsustainable highs earlier in the recovery; however, the pace of expansion remains robust compared to pre-crisis norms. A further moderation is expected in the months ahead, as the abundant excess capacity created by the crisis gets fully re-absorbed with the broader, vaccine-supported economic reopening and the cycle matures past the recovery phase and into a sustained expansion. However, the buoyant demand backdrop (underpinned by the strong financial positions of consumers) remains highly constructive for corporate profits.

Sincerely,

Guardian Capital LP

2

Investment Results (Unaudited)

Average Annual Total Returns(a) as of September 30, 2021

| | 5 Months | One Year | Since Inception

05/01/2019 |

Guardian Capital Dividend Growth Fund | | | |

Class I | 2.42% | 17.21% | 12.77% |

MSCI World Index(b) | 2.95% | 28.82% | 16.35% |

| | Expense Ratios(c) |

| | Class I |

Gross | 1.73% |

With Applicable Waivers | 0.95% |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Guardian Capital Dividend Growth Fund (the “Fund”) distributions or the redemption of Fund shares. Current performance of the Fund may be lower or higher than the performance quoted. The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. Performance data current to the most recent month end may be obtained by calling (800) 968-2295.

(a) Return figures reflect any change in price per share and assume the reinvestment of all distributions. The Fund’s returns reflect any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. Total returns for less than one year are not annualized.

(b) The MSCI World Index is an unmanaged free float-adjusted market capitalization index that is designed to measure global developed market equity performance. Currently the MSCI World Index consists of the following 23 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The performance of the index is expressed in terms of U.S. dollars, and does not reflect the deduction of fees and expenses, whereas the Fund’s returns are shown net of fees. Individuals cannot invest directly in an index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index.

(c) The expense ratio is from the Fund’s prospectus dated August 27, 2021. Guardian Capital LP, the Fund’s adviser (the “Adviser”), has contractually agreed to waive its management fee and/or reimburse expenses so that total annual operating expenses for the Fund (excluding (i) interest; (ii) taxes; (iii) brokerage fees and commissions; (iv) other extraordinary expenses not incurred in the ordinary course of the Fund’s business; (v) dividend expense on short sales; and (vi) indirect expenses such as acquired fund fees and expenses) do not exceed 0.95% of the Fund’s average daily net assets through January 31, 2023 (the “Expense Limitation”). During any fiscal year that the Investment Advisory Agreement between the Adviser and the Capitol Series Trust (the “Trust”) is in effect, the Adviser may recoup the sum of all fees previously waived or expenses reimbursed, less any reimbursement previously paid, provided that the Adviser is only permitted to recoup fees or expenses within 36 months from the date the fee waiver or expense reimbursement first occurred and provided further that such recoupment can be achieved within the Expense Limitation Agreement currently in effect and the Expense Limitation Agreement in place when the waiver/reimbursement occurred. This Expense Limitation Agreement may be terminated by the Board of Trustees (the “Board”) at any time. The Class I Shares expense ratio does not correlate to the corresponding ratio of expenses to average net assets included in the financial highlights section of this report, which reflects the operating expenses of the Fund, but does not include acquired fund fees and expenses. Additional information pertaining to the Fund’s expense ratios as of September 30, 2021, can be found in the financial highlights.

The Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Fund and may be obtained by calling (800) 968-2295. Please read it carefully before investing.

The Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

3

Investment Results (Unaudited) (continued)

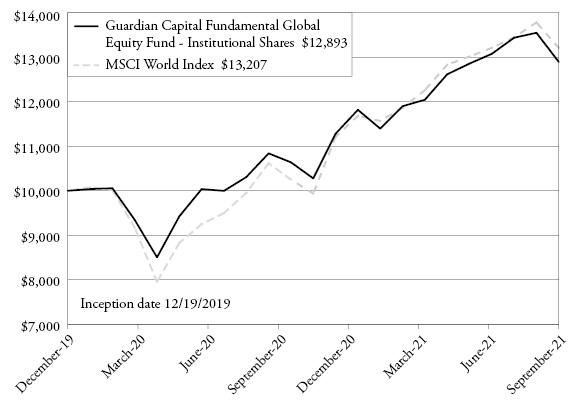

Comparison of the Growth of a $10,000 Investment in the

Guardian Capital Dividend Growth Fund – Class I and the MSCI World Index.

The chart above assumes an initial investment of $10,000 made on May 1, 2019 (commencement of operations) and held through September 30, 2021. THE FUND’S RETURNS REPRESENT PAST PERFORMANCE AND DO NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on the Fund’s distributions or the redemption of the Fund’s shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call (800) 968-2295. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

The Fund is distributed by Ultimus Fund Distributors, LLC, Member FINRA/SIPC.

4

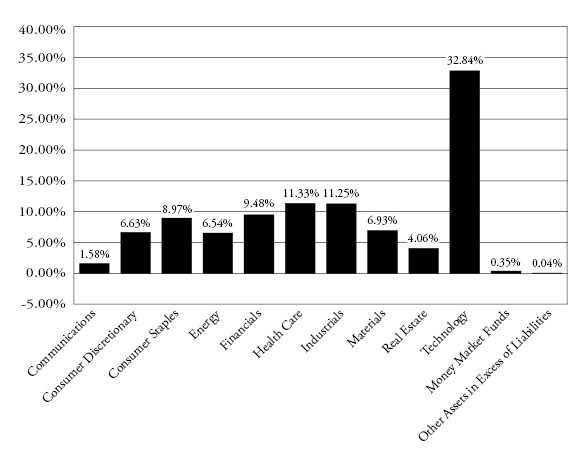

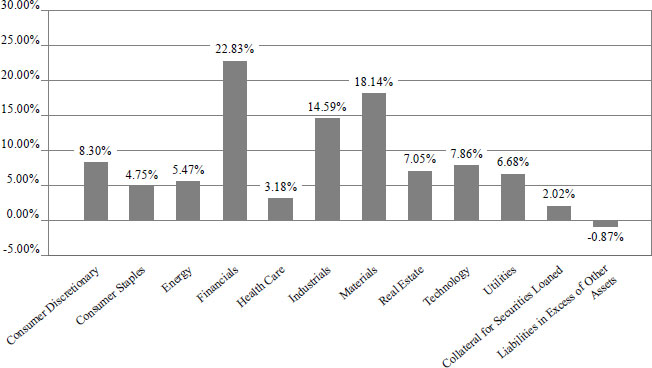

Portfolio Illustration (Unaudited)

September 30, 2021

The following chart gives a visual breakdown of the Fund’s holdings as a percentage of net assets.

Availability of Portfolio Schedule (Unaudited)

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT, within sixty days after the end of the period. The Fund’s portfolio holdings are available on the SEC’s website at http://www.sec.gov and on the Fund’s website at www.guardiancapitalfunds.com.

5

Guardian Capital Dividend Growth Fund

Schedule of Investments

September 30, 2021

| | Shares | | | Fair Value | |

COMMON STOCKS — 99.61% | | | | | | | | |

| | | | | | | | | |

Communications — 1.58% | | | | | | | | |

TELUS Corp. | | | 14,292 | | | $ | 314,090 | |

| | | | | | | | | |

Consumer Discretionary — 6.63% | | | | | | | | |

Home Depot, Inc. (The) | | | 1,502 | | | | 493,046 | |

LVMH Moet Hennessy Louis Vuitton SA - ADR | | | 2,838 | | | | 406,629 | |

McDonald’s Corp. | | | 1,727 | | | | 416,397 | |

| | | | | | | | 1,316,072 | |

Consumer Staples — 8.97% | | | | | | | | |

Costco Wholesale Corp. | | | 1,581 | | | | 710,422 | |

Nestle S.A. - ADR | | | 5,939 | | | | 713,928 | |

Unilever PLC - ADR | | | 6,584 | | | | 356,984 | |

| | | | | | | | 1,781,334 | |

Energy — 6.54% | | | | | | | | |

EOG Resources, Inc. | | | 4,575 | | | | 367,235 | |

Royal Dutch Shell PLC, Class B - ADR | | | 7,581 | | | | 335,611 | |

Total S.E. - ADR | | | 12,452 | | | | 596,825 | |

| | | | | | | | 1,299,671 | |

Financials — 9.48% | | | | | | | | |

Allianz S.E. | | | 1,800 | | | | 406,199 | |

AXA S.A. | | | 13,700 | | | | 382,169 | |

ING Groep NV - ADR | | | 35,281 | | | | 511,222 | |

Royal Bank of Canada | | | 5,861 | | | | 583,092 | |

| | | | | | | | 1,882,682 | |

Health Care — 11.33% | | | | | | | | |

AstraZeneca PLC - ADR | | | 8,878 | | | | 533,212 | |

Johnson & Johnson | | | 2,505 | | | | 404,558 | |

Medtronic PLC | | | 2,360 | | | | 295,826 | |

Novo Nordisk A/S - ADR | | | 3,510 | | | | 336,995 | |

UnitedHealth Group, Inc. | | | 991 | | | | 387,223 | |

Zoetis, Inc. | | | 1,506 | | | | 292,375 | |

| | | | | | | | 2,250,189 | |

Industrials — 11.25% | | | | | | | | |

Exponent, Inc. | | | 2,134 | | | | 241,462 | |

Illinois Tool Works, Inc. | | | 1,319 | | | | 272,545 | |

Republic Services, Inc. | | | 4,113 | | | | 493,806 | |

Rockwell Automation, Inc. | | | 1,082 | | | | 318,151 | |

Schneider Electric SE - ADR | | | 13,574 | | | | 450,990 | |

Waste Management, Inc. | | | 3,061 | | | | 457,191 | |

| | | | | | | | 2,234,145 | |

6 | See accompanying notes which are an integral part of these financial statements. | |

Guardian Capital Dividend Growth Fund

Schedule of Investments (continued)

September 30, 2021

| | Shares | | | Fair Value | |

COMMON STOCKS — (continued) | | | | | | | | |

| | | | | | | | | |

Materials — 6.93% | | | | | | | | |

Air Products & Chemicals, Inc. | | | 2,476 | | | $ | 634,128 | |

BHP Group Ltd. - ADR | | | 6,677 | | | | 357,353 | |

Rio Tinto PLC - ADR | | | 5,770 | | | | 385,552 | |

| | | | | | | | 1,377,033 | |

Real Estate — 4.06% | | | | | | | | |

Digital Realty Trust, Inc. | | | 2,003 | | | | 289,333 | |

Medical Properties Trust, Inc. | | | 25,763 | | | | 517,064 | |

| | | | | | | | 806,397 | |

Technology — 32.84% | | | | | | | | |

Accenture PLC, Class A | | | 3,221 | | | | 1,030,461 | |

Apple, Inc. | | | 7,575 | | | | 1,071,863 | |

Booz Allen Hamilton Holding Corp. | | | 4,072 | | | | 323,113 | |

Broadcom, Inc. | | | 2,142 | | | | 1,038,719 | |

CDW Corp. | | | 2,695 | | | | 490,544 | |

Lam Research Corp. | | | 1,017 | | | | 578,826 | |

MasterCard, Inc., Class A | | | 1,326 | | | | 461,024 | |

Microsoft Corp. | | | 3,779 | | | | 1,065,376 | |

Wolters Kluwer NV - ADR | | | 4,375 | | | | 463,138 | |

| | | | | | | | 6,523,064 | |

| | | | | | | | | |

Total Common Stocks (Cost $15,147,298) | | | | | | | 19,784,677 | |

| | | | | | | | | |

| | | | | | | | | |

MONEY MARKET FUNDS — 0.35% | | | | | | | | |

Morgan Stanley Institutional Liquidity Fund, Institutional Class, 0.01%(a) | | | 70,394 | | | | 70,394 | |

Total Money Market Funds (Cost $70,394) | | | | | | | 70,394 | |

| | | | | | | | | |

Total Investments — 99.96% (Cost $15,217,692) | | | | | | | 19,855,071 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 0.04% | | | | | | | 8,857 | |

| | | | | | | | | |

NET ASSETS — 100.00% | | | | | | $ | 19,863,928 | |

(a) | Rate disclosed is the seven day effective yield as of September 30, 2021. |

ADR - American Depositary Receipt.

| | See accompanying notes which are an integral part of these financial statements. | 7 |

Guardian Capital Dividend Growth Fund

Statement of Assets and Liabilities

September 30, 2021

Assets |

Investments in securities at fair value (cost $15,217,692) | | $ | 19,855,071 | |

Cash | | | 12,381 | |

Receivable for fund shares sold | | | 69,645 | |

Dividends receivable | | | 28,924 | |

Tax reclaims receivable | | | 15,414 | |

Receivable from Adviser | | | 8,029 | |

Prepaid expenses | | | 9,622 | |

Total Assets | | | 19,999,086 | |

Liabilities | | | | |

Payable for distributions to shareholders | | | 99,481 | |

Payable to Administrator | | | 7,279 | |

Payable to auditors | | | 15,250 | |

Other accrued expenses | | | 13,148 | |

Total Liabilities | | | 135,158 | |

Net Assets | | $ | 19,863,928 | |

Net Assets consist of: | | | | |

Paid-in capital | | $ | 15,479,881 | |

Accumulated earnings | | | 4,384,047 | |

Net Assets | | $ | 19,863,928 | |

Shares outstanding (unlimited number of shares authorized, no par value) | | | 1,542,986 | |

Net asset value, offering and redemption price per share | | $ | 12.87 | |

8 | See accompanying notes which are an integral part of these financial statements. | |

Guardian Capital Dividend Growth Fund

Statements of Operations

| | | Five Months Ended

September 30, 2021(a) | | | Year Ended

April 30, 2021 | |

Investment Income | | | | | | | | |

Dividend income (net of foreign taxes withheld of $20,062 and $18,734) | | $ | 244,124 | | | $ | 406,326 | |

Total investment income | | | 244,124 | | | | 406,326 | |

Expenses | | | | | | | | |

Adviser | | | 63,443 | | | | 129,166 | |

Administration | | | 25,668 | | | | 52,671 | |

Audit and tax preparation | | | 12,510 | | | | 17,250 | |

Legal | | | 7,917 | | | | 19,057 | |

Trustee | | | 7,500 | | | | 15,453 | |

Compliance services | | | 5,834 | | | | 14,000 | |

Report printing | | | 5,146 | | | | 4,368 | |

Transfer agent | | | 5,000 | | | | 12,000 | |

Registration | | | 4,653 | | | | 6,385 | |

Custodian | | | 4,239 | | | | 6,062 | |

Pricing | | | 350 | | | | 1,264 | |

Miscellaneous | | | 8,396 | | | | 21,449 | |

Total expenses | | | 150,656 | | | | 299,125 | |

Fees contractually waived and expenses reimbursed by Adviser | | | (70,281 | ) | | | (135,107 | ) |

Net operating expenses | | | 80,375 | | | | 164,018 | |

Net investment income | | | 163,749 | | | | 242,308 | |

Net Realized and Change in Unrealized Gain (Loss) on Investments | | | | |

Net realized gain on investment securities transactions | | | 111,703 | | | | 442,487 | |

Net realized gain (loss) on foreign currency transactions | | | 243 | | | | (4,492 | ) |

Net change in unrealized appreciation of investment securities and foreign currency translations | | | 193,126 | | | | 3,872,282 | |

Net realized and change in unrealized gain on investments | | | 305,072 | | | | 4,310,277 | |

Net increase in net assets resulting from operations | | $ | 468,821 | | | $ | 4,552,585 | |

(a) | The Fund changed its fiscal year end to September 30. |

| | See accompanying notes which are an integral part of these financial statements. | 9 |

Guardian Capital Dividend Growth Fund

Statements of Changes in Net Assets

| | For the

Five Months Ended

September 30, 2021(a) | | | For the

Year Ended

April 30, 2021 | | | For the

Period Ended

April 30, 2020(b) | |

Increase (Decrease) in Net Assets due to: | | | | | | | | |

Operations | | | | | | | | | | | | |

Net investment income | | $ | 163,749 | | | $ | 242,308 | | | $ | 258,249 | |

Net realized gain (loss) on investment securities and foreign currency transactions | | | 111,946 | | | | 437,995 | | | | (818,371 | ) |

Net change in unrealized appreciation of investment securities and foreign currency translations | | | 193,126 | | | | 3,872,282 | | | | 572,079 | |

Net increase in net assets resulting from operations | | | 468,821 | | | | 4,552,585 | | | | 11,957 | |

Distributions to Shareholders from Earnings: | | | | | | | | |

Class I | | | (179,059 | ) | | | (224,474 | ) | | | (245,783 | ) |

Total distributions | | | (179,059 | ) | | | (224,474 | ) | | | (245,783 | ) |

Capital Transactions - Class I | | | | | | | | | | | | |

Proceeds from shares sold | | | — | | | | 4,998 | | | | 15,000,010 | |

Reinvestment of distributions | | | 125,357 | | | | 162,721 | | | | 186,795 | |

Net increase in net assets resulting from capital transactions | | | 125,357 | | | | 167,719 | | | | 15,186,805 | |

Total Increase in Net Assets | | | 415,119 | | | | 4,495,830 | | | | 14,952,979 | |

Net Assets | | | | | | | | | | | | |

Beginning of period | | | 19,448,809 | | | | 14,952,979 | | | | — | |

End of period | | $ | 19,863,928 | | | $ | 19,448,809 | | | $ | 14,952,979 | |

Share Transactions - Class I | | | | | | | | | | | | |

Shares sold | | | — | | | | 424 | | | | 1,500,001 | |

Shares issued in reinvestment of distributions | | | 9,700 | | | | 14,370 | | | | 18,491 | |

Net increase in shares | | | 9,700 | | | | 14,794 | | | | 1,518,492 | |

(a) | The Fund changed its fiscal year end to September 30. |

(b) | For the period May 1, 2019 (commencement of operations) to April 30, 2020. |

10 | See accompanying notes which are an integral part of these financial statements. | |

Guardian Capital Dividend Growth Fund – Class I

Financial Highlights

(For a share outstanding during each period)

| | | For the

Five Months Ended

September 30, 2021(a) | | | For the

Year Ended

April 30, 2021 | | | For the

Period Ended

April 30, 2020(b) | |

Net asset value, beginning of period | | $ | 12.68 | | | $ | 9.85 | | | $ | 10.00 | |

Investment operations: | | | | | | | | | | | | |

Net investment income | | | 0.11 | | | | 0.16 | | | | 0.17 | |

Net realized and unrealized gain (loss) on investments | | | 0.20 | | | | 2.82 | | | | (0.16 | ) |

Total from investment operations | | | 0.31 | | | | 2.98 | | | | 0.01 | |

Distributions from: | | | | | | | | | | | | |

Net investment income | | | (0.12 | ) | | | (0.15 | ) | | | (0.16 | ) |

Total from distributions | | | (0.12 | ) | | | (0.15 | ) | | | (0.16 | ) |

Net asset value, end of period | | $ | 12.87 | | | $ | 12.68 | | | $ | 9.85 | |

Total Return(c) | | | 2.42 | %(d) | | | 30.41 | % | | | 0.10 | %(d) |

| | | | | | | | | | | | | |

Ratios/Supplemental Data: | | | | | | | | | | | | |

Net assets, end of period (000 omitted) | | $ | 19,864 | | | $ | 19,449 | | | $ | 14,953 | |

Ratio of expenses to average net assets | | | 0.95 | %(e) | | | 0.95 | % | | | 0.95 | %(e) |

Ratio of expenses to average net assets before waiver | | | 1.78 | %(e) | | | 1.73 | % | | | 1.94 | %(e) |

Ratio of net investment income to average net assets | | | 1.94 | %(e) | | | 1.40 | % | | | 1.64 | %(e) |

Portfolio turnover rate | | | 6 | %(d) | | | 47 | % | | | 29 | %(d) |

(a) | The fund changed its fiscal year ended to September 30. |

(b) | For the period May 1, 2019 (commencement of operations) to April 30, 2020. |

(c) | Total return represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

| | See accompanying notes which are an integral part of these financial statements. | 11 |

Guardian Capital Dividend Growth Fund

Notes to the Financial Statements

September 30, 2021

NOTE 1. ORGANIZATION

The Guardian Capital Dividend Growth Fund (the “Fund”, formerly known as Guardian Dividend Growth Fund) is registered under the Investment Company Act of 1940, as amended (“1940 Act”), as a diversified series of Capitol Series Trust (the “Trust”) on April 15, 2019. The Trust is an open-end investment company established under the laws of Ohio by an Agreement and Declaration of Trust dated September 18, 2013 (the “Trust Agreement”). The Trust Agreement permits the Board of Trustees of the Trust (the “Board”) to issue an unlimited number of shares of beneficial interest of separate series without par value. The Fund is one of a series of funds currently authorized by the Board. The Fund’s investment adviser is Guardian Capital LP (the “Adviser”). The investment objective of the Fund is to seek long-term capital appreciation and current income. The Fund changed its fiscal year end from April 30 to September 30 effective with these financial statements.

The Fund currently offers one class of shares, Class I. Each share represents an equal proportionate interest in the assets and liabilities belonging to the Fund and is entitled to such dividends and distributions out of income belonging to the Fund as are declared by the Board.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies.” The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Foreign Currency Translation – The accounting records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars at the current rate of exchange each business day to determine the value of investments, and other assets and liabilities. Purchases and sales of foreign securities, and income and expenses, are translated at the prevailing rate of exchange on the respective date of these transactions. The Fund does not isolate that portion of the results of operations resulting from changes in foreign exchange rates on investments from fluctuation arising from changes in market prices of securities held. These fluctuations are included with the unrealized gain or loss from investments.

12

Guardian Capital Dividend Growth Fund

Notes to the Financial Statements (continued)

September 30, 2021

Federal Income Taxes – The Fund makes no provision for federal income or excise tax. The Fund has qualified and intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also intends to distribute sufficient net investment income and net realized capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

The Fund may be subject to taxes imposed by countries in which it invests. Such taxes are generally based on income and/or capital gains earned or repatriated. Taxes are accrued and applied to net investment income, net realized gains and unrealized appreciation as such income and/or gains are earned.

The Fund recognizes tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management of the Fund has reviewed tax positions taken in tax years that remain subject to examination by all major tax jurisdictions, including federal (i.e., the previous two tax year ends and the interim tax period since then, as applicable) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements and does not expect this to change over the next twelve months. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the period, the Fund did not incur any interest or penalties.

Expenses – Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds based on each fund’s relative net assets or another appropriate basis (as determined by the Board).

Security Transactions and Related Income – Throughout the reporting period, security transactions are accounted for no later than one business day following the trade date. For financial reporting purposes, security transactions are accounted for on trade date on the last business day of the reporting period. The specific identification method is used for determining gains or losses for financial statements and income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis and includes, where applicable, the amortization of premium or accretion of discount. Dividend income from real estate investment trusts (REITs) and distributions from limited partnerships are recognized on the ex-date and included in dividend income. The calendar year-end classification of distributions received from REITs during the fiscal year, which may include return of capital, are reported subsequent to year end; accordingly, the Fund estimates the character of REIT distributions based on the most recent information available. Income or loss from limited partnerships is reclassified among the components

13

Guardian Capital Dividend Growth Fund

Notes to the Financial Statements (continued)

September 30, 2021

of net assets upon receipt of K-1’s. Discounts and premiums on fixed income securities are accreted or amortized over the life of the respective securities using the effective interest method.

Dividends and Distributions – The Fund intends to distribute substantially all of its net investment income, if any, at least quarterly. The Fund intends to distribute its net realized long-term and short-term capital gains, if any, annually. Distributions to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the year from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset value (“NAV”) per share of the Fund.

NOTE 3. SECURITIES VALUATION AND FAIR VALUE MEASUREMENTS

The Fund values its portfolio securities at fair value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern time) on each business day the NYSE is open for business. Fair value is defined as the price that the Fund would receive upon selling an investment in a timely transaction to an independent buyer in the principal or most advantageous market of the investment. GAAP establishes a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes.

Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk (the risk inherent in a particular valuation technique used to measure fair value including a pricing model and/or the risk inherent in the inputs to the valuation technique). Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained and available from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the

14

Guardian Capital Dividend Growth Fund

Notes to the Financial Statements (continued)

September 30, 2021

reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| | ● | Level 1 – unadjusted quoted prices in active markets for identical investments and/or registered investment companies where the value per share is determined and published and is the basis for current transactions for identical assets or liabilities at the valuation date |

| | ● | Level 2 – other significant observable inputs (including, but not limited to, quoted prices for an identical security in an inactive market, quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| | ● | Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments based on the best information available) |

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy which is reported is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

In computing the NAV of the Fund, fair value is based on market valuations with respect to portfolio securities for which market quotations are readily available. Pursuant to Board approved policies, the Fund relies on independent third-party pricing services to provide the current market value of securities. Those pricing services value equity securities, including exchange-traded funds, exchange-traded notes, closed-end funds and preferred stocks, traded on a securities exchange at the last reported sales price on the principal exchange. Equity securities quoted by NASDAQ are valued at the NASDAQ Official Closing Price. If there is no reported sale on the principal exchange, equity securities are valued at the mean between the most recent quoted bid and asked price. When using market quotations or close prices provided by the pricing service and when the market is considered active, the security will be classified as a Level 1 security. Investments in open-end mutual funds, including money market mutual funds, are generally priced at the ending NAV provided by the pricing service of the funds and are generally categorized as Level 1 securities. Debt securities are valued using evaluated prices furnished by a pricing vendor selected by the Board and are generally classified as Level 2 securities.

In the event that market quotations are not readily available, the Adviser determines that the market quotation or the price provided by the pricing service does not accurately reflect the current fair value, such securities are valued as determined in good faith by the Trust’s Valuation Committee, based on recommendations from a pricing committee comprised of certain officers of the Trust, certain employees of the Fund’s administrator,

15

Guardian Capital Dividend Growth Fund

Notes to the Financial Statements (continued)

September 30, 2021

and representatives of the Adviser (together the “Pricing Review Committee”). These securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used.

In accordance with the Trust’s Portfolio Valuation Procedures, the Pricing Review Committee, in making its recommendations with the Adviser’s participation, is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. No single standard exists for determining fair value, because fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of an issue of securities being valued pursuant to the Trust’s Fair Value Guidelines would be the amount which the Fund might reasonably expect to receive for them upon their current sale. Methods which are in accordance with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market prices of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt issues, or a combination of these and other methods. Fair value pricing is permitted if, in accordance with the Trust’s Portfolio Valuation Procedures, the validity of market quotations appears to be questionable based on factors such as evidence of a thin market in the security based on a small number of quotations, a significant event occurs after the close of a market but before the Fund’s NAV calculation that may affect a security’s value, or other data calls into question the reliability of market quotations.

The following is a summary of the inputs used to value the Fund’s investments as of September 30, 2021:

| | | Valuation Inputs | | | | | |

Assets | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Common Stocks(a) | | $ | 19,784,677 | | | $ | — | | | $ | — | | | $ | 19,784,677 | |

Money Market Funds | | | 70,394 | | | | — | | | | — | | | | 70,394 | |

Total | | $ | 19,855,071 | | | $ | — | | | $ | — | | | $ | 19,855,071 | |

(a) | Refer to Schedule of Investments for sector classifications. |

The Fund did not hold any investments at the end of the reporting period for which significant unobservable inputs (Level 3) were used in determining fair value; therefore, no reconciliation of Level 3 securities is included for this reporting period.

NOTE 4. ADVISER FEES AND OTHER TRANSACTIONS

Under the terms of the investment advisory agreement (the “Agreement”), the Adviser manages the Fund’s investments subject to approval of the Board. As compensation for its management services, the Fund is obligated to pay the Adviser a fee computed and accrued

16

Guardian Capital Dividend Growth Fund

Notes to the Financial Statements (continued)

September 30, 2021

daily and paid monthly at an annual rate of 0.75% of the Fund’s average daily net assets. For the fiscal period ended September 30, 2021, the Adviser earned fees of $63,443 from the Fund. At September 30, 2021, the Adviser owed the Fund $8,029.

The Adviser has contractually agreed to waive its management fee and/or reimburse expenses so that total annual operating expenses (excluding (i) interest; (ii) taxes; (iii) brokerage fees and commissions; (iv) other extraordinary expenses not incurred in the ordinary course of the Fund’s business; (v) dividend expenses on short sales; and (vi) indirect expenses such as acquired fund fees and expenses) and expenses) do not exceed 0.95% of the Fund’s average daily net assets through January 31, 2023 (“Expense Limitation”). During any fiscal year that the Agreement between the Adviser and the Trust is in effect, the Adviser may recoup the sum of all fees previously waived or expenses reimbursed, less any reimbursement previously paid, provided that the Adviser is only permitted to recoup fees or expenses within 36 months from the date the fee waiver or expense reimbursement took effect and provided further that such recoupment can be achieved within the Expense Limitation currently in effect and the Expense Limitation in place when the waiver/reimbursement occurred. This expense cap agreement may be terminated by the Board at any time. As of September 30, 2021, the Adviser may seek repayment of investment advisory fee waivers and expense reimbursements in the amount as follows:

Recoverable through | | | |

April 30, 2023 | | $ | 155,420 | |

April 30, 2024 | | | 135,107 | |

September 30, 2024 | | | 70,281 | |

The Trust retains Ultimus Fund Solutions, LLC (the “Administrator”) to provide the Fund with administration, compliance, fund accounting and transfer agent services, including all regulatory reporting. For the fiscal period ended September 30, 2021, the Administrator earned fees of $25,668 for fund accounting and administration services, $5,834 for compliance services and $5,000 for transfer agent services. At September 30, 2021, the Fund owed the Administrator $7,279 for such services.

The Board supervises the business activities of the Trust. Each Trustee serves as a Trustee for the lifetime of the Trust or until the earlier of his or her retirement as a Trustee at age 78 (which may be extended for up to two years in an emeritus non-voting capacity at the pleasure and request of the Board), or until he/she dies, resigns, or is removed, whichever is sooner. “Independent Trustees,” meaning those Trustees who are not “interested persons” of the Trust, as defined in the 1940 Act, as amended, have each received an annual retainer of $1,000 per Fund and $500 per Fund for each quarterly in-person Board meeting. In addition, each Independent Trustee may be compensated for preparation related to and participation in any special meetings of the Board and/or any Committee of the Board, with

17

Guardian Capital Dividend Growth Fund

Notes to the Financial Statements (continued)

September 30, 2021

such compensation determined on a case-by-case basis based on the length and complexity of the meeting. The Trust also reimburses Trustees for out-of-pocket expense incurred in conjunction with attendance at Board meetings.

The officers and one trustee of the Trust are employees of the Administrator. Ultimus Fund Distributors, LLC (the “Distributor”) acts as the principal distributor of the Fund’s shares. The Distributor is a wholly-owned subsidiary of the Administrator.

NOTE 5. PURCHASES AND SALES OF SECURITIES

For the fiscal period ended September 30, 2021, purchases and sales of investment securities, other than short-term investments, were $1,441,523 and $1,131,857, respectively.

There were no purchases or sales of long-term U.S. government obligations during the fiscal period ended September 30, 2021.

NOTE 6. FEDERAL TAX INFORMATION

At September 30, 2021, the net unrealized appreciation (depreciation) and tax cost of investments for tax purposes was as follows:

Gross unrealized appreciation | | $ | 4,937,884 | |

Gross unrealized depreciation | | | (300,505 | ) |

Net unrealized appreciation/(depreciation) on investments | | $ | 4,637,379 | |

Tax cost of investments | | $ | 15,217,692 | |

The tax character of distributions paid for the fiscal periods ended September 30, 2021, April 30, 2021 and April 30, 2020 were as follows:

| | September 2021 | | | April 2021 | | | April 2020 | |

Distributions paid from: | | | | | | | | | | | | |

Ordinary income(a) | | $ | 79,578 | | | $ | 224,474 | | | $ | 245,783 | |

Total distributions paid | | $ | 79,578 | | | $ | 224,474 | | | $ | 245,783 | |

(a) | Short-term capital gain distributions are treated as ordinary income for tax purposes. |

At September 30, 2021, the components of accumulated earnings (deficit) on a tax basis were as follows:

Undistributed Ordinary Income | | $ | 106,113 | |

Distributions Payable | | | (99,481 | ) |

Accumulated Capital and Other Losses | | | (260,072 | ) |

Unrealized Appreciation (Depreciation) on Investments | | | 4,637,487 | |

Total Accumulated Earnings (Deficit) | | $ | 4,384,047 | |

18

Guardian Capital Dividend Growth Fund

Notes to the Financial Statements (continued)

September 30, 2021

As of September 30, 2021, the Fund had available for tax purposes unused capital loss carryforwards of $260,071 and $1 of short-term and long-term capital loss carryforwards, respectively, with no expiration, which was available to offset against future taxable net capital gains. To the extent that these carryforwards are used to offset future gains, it is probable that the amount offset will not be distributed to shareholders.

NOTE 7. SECTOR RISK

If the Fund has significant investments in the securities of issuers within a particular sector, any development affecting that sector will have a greater impact on the value of the net assets of the Fund than would be the case if the Fund did not have significant investments in that sector. In addition, this may increase the risk of loss in the Fund and increase the volatility of the Fund’s NAV per share. For instance, economic or market factors, regulatory changes or other developments may negatively impact all companies in a particular sector, and therefore the value of the Fund’s portfolio will be adversely affected. As of September 30, 2021, the Fund had 32.84% of its net assets invested in stocks within the Technology sector.

NOTE 8. COMMITMENTS AND CONTINGENCIES

The Trust indemnifies its officers and Trustees for certain liabilities that may arise from their performance of their duties to the Trust or the Fund. Additionally, in the normal course of business, the Trust enters into contracts that contain a variety of representations and warranties which provide general indemnifications. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred.

NOTE 9. SUBSEQUENT EVENTS

Management of the Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date at which these financial statements were issued. Based upon this evaluation, management has determined there were no items requiring adjustment of the financial statements or additional disclosure.

19

Report of Independent Registered Public Accounting Firm

To the Shareholders and the Board of Trustees of Guardian Capital Dividend Growth Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Guardian Capital Dividend Growth Fund (formerly, Guardian Dividend Growth Fund) (the “Fund”) (one of the funds constituting Capitol Series Trust (the “Trust”)), including the schedule of investments, as of September 30, 2021, and the related statements of operations for the period from May 1, 2021 through September 30, 2021 and for the year ended April 30, 2021, the statements of changes in net assets and the financial highlights for the period from May 1, 2021 through September 30, 2021, the year ended April 30, 2021 and for the period May 1, 2019 (commencement of operations) through April 30, 2020 and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund (one of the funds constituting Capitol Series Trust) at September 30, 2021, the results of its operations for the period from May 1, 2021 through September 30, 2021 and for the year ended April 30, 2021, the changes in its net assets and its financial highlights for the period from May 1, 2021 through September 30, 2021, the year ended April 30, 2021 and for the period May 1, 2019 (commencement of operations) through April 30, 2020, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Trust’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Trust in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Trust is not required to have, nor were we engaged to perform, an audit of Trust’s internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Trust’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2021, by correspondence with the custodian. Our audits also included evaluating the accounting principles used and

20

Report of Independent Registered Public Accounting Firm (continued)

significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more Capitol Series Trust investment companies since 2017.

Cincinnati, Ohio

November 24, 2021

21

Guardian Capital Dividend Growth Fund

Liquidity Risk Management Program (Unaudited)

The Fund has adopted and implemented a written liquidity risk management program (the “Program”) as required by Rule 22e-4 (the “Liquidity Rule”) under the 1940 Act. The Program is reasonably designed to assess and manage the Fund’s liquidity risk, taking into consideration, among other factors, the Fund’s investment strategy and the liquidity of its portfolio investments during normal and reasonably foreseeable stressed conditions; its short and long-term cash flow projections; and its cash holdings and access to other funding sources. The Board approved the appointment of the Liquidity Administrator Committee, comprising certain Trust officers and employees of the Adviser. The Liquidity Administrator Committee maintains Program oversight and reports to the Board on at least an annual basis regarding the Program’s operational effectiveness through a written report (the “Report”). The Report outlined the operation of the Program and the adequacy and effectiveness of the Program’s implementation and was presented to the Board for consideration at its meeting held on September 15 and 16, 2021. During the review period, the Fund did not experience unusual stress or disruption to its operations related to purchase and redemption activity. Also, during the review period the Fund held adequate levels of cash and highly liquid investments to meet shareholder redemption activities in accordance with applicable requirements. The Report concluded that the Program is reasonably designed to prevent violation of the Liquidity Rule and has been effectively implemented.

22

Guardian Capital Dividend Growth Fund

Approval of Investment Advisory Agreement (Unaudited)

At a quarterly meeting of the Board of Trustees of Capitol Series Trust (the “Trust”) on March 17 and 18, 2021, the Trust’s Board of Trustees (the “Board”), including all of the Trustees who are not “interested persons” of the Trust (the “Independent Trustees”) as that term is defined in Section 2(a)(19) of the Investment Company Act of 1940, as amended (the “1940 Act”), considered and approved the continuation for an additional one-year period the Investment Advisory Agreement between the Trust and Guardian Capital LP (“Guardian”) (the “Investment Advisory Agreement”) with respect to the Guardian Capital Dividend Growth Fund (the “Fund”), a series of the Trust.

Prior to the meeting, the Trustees received and considered information from Guardian and the Trust’s administrator designed to provide the Trustees with the information necessary to evaluate the terms of the Investment Advisory Agreement between the Trust and Guardian, including, but not limited to, Guardian’s response to counsel’s due diligence letter requesting information relevant to the approval of the Investment Advisory Agreement, the operating expense limitation agreement between the Trust and Guardian (the “Expense Limitation Agreement”), and certain expense and performance data provided by Broadridge for comparison purposes (collectively, the “Support Materials”). At various times, the Trustees reviewed the Support Materials with Guardian, Trust management, and with counsel to the Independent Trustees. The Trustees noted the completeness of the Support Materials that Guardian provided, which included both responses and materials provided in response to initial and supplemental due diligence requests. Representatives from Guardian met with the Trustees and provided additional information, including but not limited to information concerning the services it provides to the Fund, firm ownership, resources available to service the Fund, including compliance resources, the experience and qualifications of the portfolio management team, other investment strategies that Guardian manages, including a Canadian mutual fund strategy similar to that of the Fund, succession planning, future plans for the fund family, distribution capabilities, recent growth in the firm, and profitability (both as it relates to the Adviser generally and with the respect to the profitability of the Fund to the Adviser). This information formed the primary, but not exclusive, basis for the Board’s determinations.

Before voting to approve the Investment Advisory Agreement, the Trustees reviewed the terms and the form of the Investment Advisory Agreement and the Support Materials with Trust management and with counsel to the Independent Trustees. The Trustees also received a memorandum from counsel discussing the legal standards for their consideration of the Investment Advisory Agreement, which memorandum described the various factors that the U.S. Securities and Exchange Commission (“SEC”) and U.S. Courts over the years have suggested would be appropriate for trustee consideration in the advisory agreement approval process, including the factors outlined in the case of Gartenberg v. Merrill Lynch Asset Management Inc., 694 F.2d 923, 928 (2d Cir. 1982); cert. denied sub. nom. and Andre v. Merrill Lynch Ready Assets Trust, Inc., 461 U.S. 906 (1983).

23

Guardian Capital Dividend Growth Fund

Approval of Investment Advisory Agreement (Unaudited)

(continued)

In determining whether to approve the Investment Advisory Agreement, the Trustees considered all factors they believed relevant with respect to the Fund, including the following: (1) the nature, extent, and quality of the services that Guardian provides, including the Fund’s performance; (2) the cost of the services provided and the profits realized by Guardian from services rendered to the Trust with respect to the Fund; (3) comparative fee and expense data for the Fund and other investment companies with similar investment objectives, as well as other accounts that Guardian manages in the same investment strategy; (4) the extent to which economies of scale may be realized as the Fund grows and whether the advisory fee for the Fund reflects these economies of scale for the Fund’s benefit; and (5) other financial benefits to Guardian resulting from services rendered to the Fund. In their deliberations, the Trustees did not identify any particular information that was all-important or controlling.

Together with the Support Materials, and after having received and reviewed investment performance, compliance, operating, and distribution reports of the Fund on a quarterly basis since the Fund’s inception, and noting additional discussions with representatives of Guardian that had occurred at various times, the Trustees determined that they had all of the information they deemed reasonably necessary to make an informed decision concerning the approval of the continuation of the Investment Advisory Agreement. The Trustees discussed the facts and factors relevant to the approval of the Investment Advisory Agreement, which incorporated and reflected their knowledge of the services that Guardian provides to the Fund. The Trustees also noted the inclusion of comparative fee and performance reports of the Fund to the World Large Stock Morningstar category and the custom peer group compiled by Broadridge. The Trustees discussed Guardian’s ownership and subsidiary companies and profitability, and noted that the firm was profitable in 2020. The Trustees discussed the growth of assets of the Fund since its inception and Guardian’s continued commitment to promote the Fund. Based upon Guardian’s presentation and the Support Materials, the Board concluded that the overall arrangements between the Trust and Guardian, as set forth in the Investment Advisory Agreement, are fair and reasonable in light of the services Guardian performs, the investment advisory fees that the Fund pays, and such other matters as the Trustees considered relevant in the exercise of their reasonable business judgment. The material factors and conclusions that formed the basis of the Trustees’ determination to approve the Investment Advisory Agreement are summarized below.

Nature, Extent and Quality of Services Provided. The Trustees considered the scope of services that Guardian provides under the Investment Advisory Agreement, noting that such services include, but are not limited to, the following: (1) investing the Fund’s assets consistent with the Fund’s investment objective and investment policies; (2) determining the portfolio securities to be purchased, sold or otherwise disposed of and the timing of such transactions; (3) voting all proxies with respect to the Fund’s portfolio securities;

24

Guardian Capital Dividend Growth Fund

Approval of Investment Advisory Agreement (Unaudited)

(continued)

(4) maintaining the required books and records for transactions that Guardian effects on behalf of the Fund; (5) selecting broker-dealers to execute orders on behalf of the Fund; (6) performing compliance services on behalf of the Fund; and (7) engaging in marketing activities. The Trustees noted no changes to the services that Guardian provides to the Fund under the terms of the Investment Advisory Agreement. The Trustees considered Guardian’s capitalization and its assets under management. The Trustees further considered the investment philosophy and investment industry experience of the portfolio managers. The Trustees also noted the research models utilized by Guardian which combine artificial intelligence, human intelligence and experience with innovation to manage the Fund’s portfolio in accordance with its investment strategy. The Trustees also noted the Fund’s performance compared to its benchmark index, including the fact that the Fund had underperformed its benchmark index for the one-year, year-to-date, and since inception periods ended December 31, 2020. The Trustees also considered the Fund’s performance compared to the World Large Stock Morningstar category and the custom Broadridge peer group. The Trustees noted that the Fund underperformed both the medians of the Morningstar category and custom peer group for the period since its inception on May 1, 2019 to December 31, 2020. The Trustees further considered Guardian’s discussion and explanation with regard to periods of unfavorable performance. Based upon the foregoing, the Trustees concluded that they are satisfied with the nature, extent, and quality of services that Guardian provides to the Fund under the Investment Advisory Agreement.

Cost of Advisory Services and Profitability. The Trustees considered the annual management fee that the Fund pays to Guardian under the Investment Advisory Agreement, as well as Guardian’s profitability from the services that it renders to the Fund, noting the said services were slightly unprofitable during the last fiscal year and were projected to be slightly unprofitable in the current fiscal year. The Trustees considered that Guardian has contractually agreed to reduce its management fees and, if necessary, reimburse the Fund for operating expenses, as specified in the Fund’s prospectus. The Trustees further considered the strong cash flow and fiscal health of Guardian as it considered the firm’s financial wherewithal to support the Fund. The Trustees concluded that Guardian’s profitability with respect to its advisory relationship with the Fund is reasonable.

Comparative Fee and Expense Data. The Trustees noted that the Fund’s contractual management fee was equal to the median and less than the average contractual management fee reported for the Broadridge custom peer group. The Trustees further noted that the Fund’s contractual management fee was equal to the median and average net contractual management fee reported for the Morningstar World Large Stock category. The Trustees then reviewed the Fund’s gross and net total expense ratios (reflected with and without the effect of fee waivers and expense reimbursements) relative to the custom peer group and the Morningstar category. The Trustees noted that Fund’s gross expense ratio was below the average and above the median gross total expense ratios reported for the Broadridge

25

Guardian Capital Dividend Growth Fund

Approval of Investment Advisory Agreement (Unaudited)

(continued)

custom peer group, and that the net expense ratio was equal to the median and less than the average reported for the custom peer group. With regard to comparison to the Morningstar category, the Trustees noted that the Fund’s gross expense ratio was above the median and below the average gross expense ratio reported for the category. The Trustees also noted that the Fund’s total net expense ratio was lower than both the average and median total net expense ratios reported for the same category. They further considered the fees paid by Guardian’s separately managed accounts and other investment advisory relationships to other accounts with similar investment objectives and strategies to that of the Fund, noting the differences in the services provided to these accounts compared to the services provided to the Fund. In particular, they noted that Guardian has additional responsibilities with respect to the Fund, including compliance, reporting and operational responsibilities. While recognizing that it is difficult to compare advisory fees because the scope of advisory services provided may vary from one investment adviser to another, or from one investment product to another, the Trustees concluded that Guardian’s advisory fee continues to be reasonable.

Economies of Scale. The Trustees considered whether the Fund may benefit from any economies of scale, but did not find that any material economies exist at this time. The Trustees also noted Guardian’s view that that due to the Fund’s low net asset total and Guardian’s current unprofitability with respect to the Fund, fee breakpoints are not necessary or appropriate at this time.

Other Benefits. The Trustees noted that Guardian does not utilize soft dollar arrangements with respect to portfolio transactions and does not use affiliated brokers to execute the Fund’s portfolio transactions. The Trustees noted that Guardian had confirmed that there were no economic or other benefits to the Adviser associated with the selection or use of any particular providers for the Fund’s portfolio. The Trustees concluded that all things considered, Guardian does not receive material additional financial benefits from services rendered to the Fund.

Other Considerations. The Trustees also considered potential conflicts for Guardian with respect to relationships forged with service providers to the Fund. The Trustees noted that both they and Counsel have discussed with representatives of Guardian their duty of loyalty relative to the selection of service providers and the conflicts that could develop relative to any relationship that Guardian may form with a specific service provider. Based on the assurances and representations from Guardian, the Trustees concluded that no material conflict of interest currently exists that could adversely impact the Fund.

26

Summary of Fund Expenses (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction and (2) ongoing costs, including management fees and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2021 through September 30, 2021.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second line of the table below is useful in comparing ongoing costs only and will not help you determine the relative costs of owning different funds. In addition, if transaction costs were included, your costs would have been higher.

| | | Beginning

Account Value

April 1,

2021 | Ending

Account Value

September 30,

2021 | Expenses Paid

During

Period(a) | Annualized

Expense

Ratio |

Guardian Capital Dividend Growth Fund | | | |

Class I | Actual | $ 1,000.00 | $ 1,071.50 | $ 4.93 | 0.95% |

| | | | | | |

| | Hypothetical(b) | $ 1,000.00 | $ 1,020.31 | $ 4.81 | 0.95% |

(a) | Expenses are equal to the Fund’s annualized expense ratios, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

(b) | Hypothetical assumes 5% annual return before expenses. |

27

Additional Federal Income Tax Information (Unaudited)

The Form 1099-DIV you receive in January 2022 will show the tax status of all distributions paid to your account in calendar year 2021. Shareholders are advised to consult their own tax adviser with respect to the tax consequences of their investment in the Fund. As required by the Internal Revenue Code and/or regulations, shareholders must be notified regarding the status of qualified dividend income for individuals and the dividends received deduction for corporations.

Qualified Dividend Income. The Fund designates approximately 100% or up to the maximum amount of such dividends allowable pursuant to the Internal Revenue Code, as qualified dividend income eligible for a reduced tax rate.

Qualified Business Income. The Fund designates approximately 0% of its ordinary income dividends, or up to the maximum amount of such dividends allowable pursuant to the Internal Revenue Code, as qualified business income.

Dividends Received Deduction. Corporate shareholders are generally entitled to take the dividends received deduction on the portion of the Fund’s dividend distribution that qualifies under tax law. For the Fund’s calendar year 2021 ordinary income dividends, 58% qualifies for the corporate dividends received deduction.

28

Trustees and Officers (Unaudited)

The Board supervises the business activities of the Trust and is responsible for protecting the interests of shareholders. The Chairman of the Board is Walter B. Grimm, who is an Independent Trustee of the Trust.

Each Trustee serves as a Trustee for the lifetime of the Trust or until the earlier of his or her retirement as a Trustee at age 78, death, resignation or removal. Officers are re-elected annually by the Board. The address of each Trustee and officer is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246.

As of the date of this report, the Trustees oversee the operations of 12 series.

Interested Trustee Background. The following table provides information regarding the Interested Trustee.

Name, (Age), Position with Trust,

Term of Position with Trust | Principal Occupation During

Past 5 Years and Other Directorships |

David James* Birth Year: 1970 TRUSTEE Began Serving: March 2021 | Principal Occupation(s): Executive Vice President and Chief Legal and Risk Officer of Ultimus Fund Solutions, LLC (2018 to present). Previous Position(s): Managing Director and Senior Managing Counsel, State Street Bank and Trust Company (2009 to 2018). |

* | Mr. James is considered an “interested person” of the Trust within the meaning of Section 2(a)(19) of the 1940 Act because of his relationship with the Trust’s administrator, transfer agent, and distributors. |

Independent Trustee Background. The following table provides information regarding the Independent Trustees.

Name, (Age), Position with Trust,

Term of Position with Trust | Principal Occupation During

Past 5 Years and Other Directorships |

Walter B. Grimm Birth Year: 1945 TRUSTEE AND CHAIR Began Serving: November 2013 | Principal Occupation(s): President, Leigh Management Group, LLC (consulting firm) (October 2005 to present); and President, Leigh Investments, Inc. (1988 to present) Board member, Boys & Girls Club of Coachella (2020 to present). |

Lori Kaiser Birth Year: 1963 TRUSTEE Began Serving: July 2018 | Principal Occupation(s): Founder and CEO, Kaiser Consulting since 1992. |

29

Trustees and Officers (Unaudited) (continued)

Name, (Age), Position with Trust,

Term of Position with Trust | Principal Occupation During

Past 5 Years and Other Directorships |

Janet Smith Meeks Birth Year: 1955 TRUSTEE Began Serving: July 2018 | Principal Occupation(s): Co-Founder and CEO, Healthcare Alignment Advisors, LLC (consulting company) since August 2015. Previous Position(s): President and Chief Operating Officer, Mount Carmel St. Ann’s Hospital (2006 to 2015). |

Mary M. Morrow Birth Year: 1958 TRUSTEE Began Serving: November 2013 | Principal Occupation(s): President, US Health Holdings (2020 to present). Previous Position(s): President (2019 to 2020) and Chief Operating Officer (2018 to 2019), Dignity Health Managed Services Organization; Chief Operating Officer, Pennsylvania Health and Wellness (fully owned subsidiary of Centene Corporation) (2016 to 2018); Vice President, Gateway Heath (2015 to 2016). |

30

Trustees and Officers (Unaudited) (continued)

Officers. The following table provides information regarding the Officers.

Name, (Age), Position with Trust,

Term of Position with Trust | Principal Occupation During

Past 5 Years and Other Directorships |

Matthew J. Miller Birth Year: 1976 PRESIDENT and CHIEF EXECUTIVE OFFICER Began Serving: September 2013 (as VP); September 2018 (as President) | Principal Occupation(s): Assistant Vice President, Relationship Management, Ultimus Fund Solutions, LLC (December 2015 to present); Vice President, Valued Advisers Trust (December 2011 to present). Previous Position(s): Vice President, Relationship Management, Huntington Asset Services, Inc. (n/k/a Ultimus Asset Services, LLC) (2008 to December 2015). |

Zachary P. Richmond Birth Year: 1980 TREASURER AND CHIEF FINANCIAL OFFICER Began Serving: August 2014 | Principal Occupation(s): Vice President, Director of Financial Administration for Ultimus Fund Solutions, LLC (February 2019 to present). Previous Position(s): Assistant Vice President, Associate Director of Financial Administration for Ultimus Fund Solutions, LLC (December 2015 to February 2019). |

Martin R. Dean Birth Year: 1963 CHIEF COMPLIANCE OFFICER Began Serving: May 2019 | Principal Occupation(s): Senior Vice President, Head of Fund Compliance, Ultimus Fund Solutions, LLC (January 2016 to present). |

Paul F. Leone Birth Year: 1963 SECRETARY Began Serving: June 2021 | Principal Occupation(s): Vice President and Senior Counsel, Ultimus Fund Solutions, LLC (2020 to present). Previous Position(s): Managing Director, Leone Law Office, P.C. (2019 to 2020); and served in the roles of Senior Counsel – Distribution and Senior Counsel - Compliance, Empower Retirement/Great-West Life & Annuity Ins. Co. (2015 to 2019). |

Stephen Preston Birth Year: 1966 ANTI-MONEY LAUNDERING OFFICER Began Serving: December 2016 | Principal Occupation(s): Chief Compliance Officer, Ultimus Fund Distributors, LLC (June 2011 to present). Previous Position(s): Chief Compliance Officer, Ultimus Fund Solutions, LLC (June 2011 to August 2019). |

Other Information (Unaudited)

The Fund’s Statement of Additional Information (“SAI”) includes additional information about the trustees and is available without charge, upon request. You may call toll-free at (800) 968-2295 to request a copy of the SAI or to make shareholder inquiries.

31

FACTS | WHAT DOES GUARDIAN CAPITAL DIVIDEND GROWTH FUND (THE “FUND”) DO WITH YOUR PERSONAL INFORMATION? |

| | |

Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. |

| | |

What? | The types of personal information we collect and share depend on the product or service you have with us. This information can include: ■ Social Security number ■ account balances and account transactions ■ transaction or loss history and purchase history ■ checking account information and wire transfer instructions When you are no longer our customer, we continue to share your information as described in this notice. |

| | |

How? | All financial companies need to share customers’ personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information; the reasons the Fund chooses to share; and whether you can limit this sharing. |

| | |

Reasons we can share your personal information | Does the Fund share? |

For our everyday business purposes—

such as to process your transactions, maintain your account(s), respond to court orders and legal investigations, or report to credit bureaus | Yes |

For our marketing purposes—

to offer our products and services to you | No |

For joint marketing with other financial companies | No |

For our affiliates’ everyday business purposes—

information about your transactions and experiences | No |

For our affiliates’ everyday business purposes—

information about your creditworthiness | No |

For nonaffiliates to market to you | No |

| | |

Questions? | Call (800) 968-2295 |

32

Who we are |

Who is providing this notice? | Guardian Capital Dividend Growth Fund

Ultimus Fund Distributors, LLC (Distributor)

Ultimus Fund Solutions, LLC (Administrator) |

What we do |