| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-177891-06 | ||

|  |

Free Writing Prospectus

Structural and Collateral Term Sheet

$904,354,517

(Approximate Aggregate Cut-off Date Balance of Mortgage Pool)

$796,962,000

(Approximate Aggregate Principal Balance of Offered Certificates)

WFRBS Commercial Mortgage Trust 2013-C17

as Issuing Entity

RBS Commercial Funding Inc.

as Depositor

Wells Fargo Bank, National Association

The Royal Bank of Scotland

Rialto Mortgage Finance, LLC

Liberty Island Group I LLC

Basis Real Estate Capital II, LLC

C-III Commercial Mortgage LLC

The Royal Bank of Scotland

Rialto Mortgage Finance, LLC

Liberty Island Group I LLC

Basis Real Estate Capital II, LLC

C-III Commercial Mortgage LLC

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates Series 2013-C17 | ||

October 28, 2013

RBS | WELLS FARGO SECURITIES | |

Co-Lead Manager and Co-Bookrunner | Co-Lead Manager and Co-Bookrunner | |

| Barclays Co-Manager | Deutsche Bank Securities Co-Manager |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-177891) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-866-884-2071 (8 a.m. – 5 p.m. EST) or by emailing rbscmbs@rbs.com.

Nothing in this document constitutes an offer to sell or a solicitation to buy securities in any jurisdiction where such offer, solicitation or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of RBS Securities Inc. (“RBSSI”), Wells Fargo Securities, LLC (“WFS”), Barclays Capital Inc., Deutsche Bank Securities Inc. or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

RBS is a trade name for the investment banking business of RBSSI. Securities, syndicated loan arranging, financial advisory and other investment banking activities are performed by RBSSI and their securities affiliates. Lending, derivatives and other commercial banking activities are performed by The Royal Bank of Scotland plc and their banking affiliates. RBSSI is a member of SIPC, FINRA and the NYSE.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including Wells Fargo Securities, LLC, a member of FINRA, NYSE, NFA and SIPC, Wells Fargo Institutional Securities, LLC, a member of FINRA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC and Wells Fargo Bank, N.A.

IRS CIRCULAR 230 NOTICE

THIS TERM SHEET IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING U.S. FEDERAL, STATE OR LOCAL TAX PENALTIES. THIS TERM SHEET IS WRITTEN AND PROVIDED BY THE DEPOSITOR IN CONNECTION WITH THE PROMOTION OR MARKETING BY THE DEPOSITOR AND THE CO-LEAD BOOKRUNNING MANAGERS OF THE TRANSACTION OR MATTERS ADDRESSED HEREIN. INVESTORS SHOULD SEEK ADVICE BASED ON THEIR PARTICULAR CIRCUMSTANCES FROM AN INDEPENDENT TAX ADVISOR.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The offered certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. Prospective investors should understand that, when considering the purchase of the offered certificates, a contract of sale will come into being no sooner than the date on which the relevant class of certificates has been priced and the underwriters have confirmed the allocation of certificates to be made to investors; any “indications of interest” expressed by any prospective investor, and any “soft circles” generated by the underwriters, will not create binding contractual obligations for such prospective investors, on the one hand, or the underwriters, the depositor or any of their respective agents or affiliates, on the other hand.

As a result of the foregoing, a prospective investor may commit to purchase certificates that have characteristics that may change, and each prospective investor is advised that all or a portion of the certificates referred to in these materials may be issued that differ from the characteristics described in these materials. The underwriters’ obligation to sell certificates to any prospective investor is conditioned on the certificates and the transaction having the characteristics described in these materials. If the underwriters determine that a condition is not satisfied in any material respect, such prospective investor will be notified, and neither the depositor nor the underwriters will have any obligation to such prospective investor to deliver any portion of the offered certificates which such prospective investor has committed to purchase, and there will be no liability between the underwriters, the depositor or any of their respective agents or affiliates, on the one hand, and such prospective investor, on the other hand, as a consequence of the non-delivery.

Each prospective investor has requested that the underwriters provide to such prospective investor information in connection with such prospective investor’s consideration of the purchase of the certificates described in these materials. These materials are being provided to each prospective investor for informative purposes only in response to such prospective investor’s specific request. The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of, or attached to, any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

| WFRBS Commercial Mortgage Trust 2013-C17 | Issue Characteristics |

I. Certificate Structure

| Approximate | ||||||||||

| Initial Certificate | Weighted | Certificate | ||||||||

| Principal Balance | Approx. | Pass-Through | Average | Expected | Certificate | Principal | ||||

| Expected Ratings | or Notional | Initial Credit | Rate | Life | Principal | Principal to | U/W NOI | |||

| Class | (Fitch/Moody's/DBRS)(1) | Amount(2) | Support(3) | Description | (Years)(4) | Window(4) | Value Ratio(5) | Debt Yield(6) | ||

| Offered Certificates | ||||||||||

| A-1 | AAA(sf)/Aaa(sf)/AAA(sf) | $48,455,000 | 30.000% | (7) | 2.56 | 12/13 - 08/18 | 41.8% | 17.2% | ||

| A-2 | AAA(sf)/Aaa(sf)/AAA(sf) | $166,900,000 | 30.000% | (7) | 4.87 | 08/18 - 11/18 | 41.8% | 17.2% | ||

| A-3 | AAA(sf)/Aaa(sf)/AAA(sf) | $125,000,000 | 30.000% | (7) | 9.86 | 08/23 - 10/23 | 41.8% | 17.2% | ||

| A-4 | AAA(sf)/Aaa(sf)/AAA(sf) | $236,856,000 | 30.000% | (7) | 9.91 | 10/23 - 11/23 | 41.8% | 17.2% | ||

| A-SB | AAA(sf)/Aaa(sf)/AAA(sf) | $55,837,000 | 30.000% | (7) | 7.46 | 11/18 - 08/23 | 41.8% | 17.2% | ||

| A-S | AAA(sf)/Aaa(sf)/AAA(sf) | $73,478,000 | 21.875% | (7) | 9.99 | 11/23 - 11/23 | 46.6% | 15.5% | ||

| B | AA-(sf)/Aa3(sf)/AA(low)(sf) | $58,784,000 | 15.375% | (7) | 9.99 | 11/23 - 11/23 | 50.5% | 14.3% | ||

| C | A-(sf)/A3(sf)/A(low)(sf) | $31,652,000 | 11.875% | (7) | 9.99 | 11/23 - 11/23 | 52.6% | 13.7% | ||

| X-A | AAA(sf)/Aaa(sf)/AAA(sf) | $706,526,000(8) | NAP | Variable(9) | NAP | NAP | N/A | N/A | ||

| X-B | AA-(sf)/Aa3(sf)/AAA(sf) | $58,784,000(10) | NAP | Variable(11) | NAP | NAP | N/A | N/A | ||

Non-Offered Certificates | ||||||||||

| X-C | NR/NR/ AAA(sf) | $59,913,517(12) | NAP | Variable(13) | NAP | NAP | N/A | N/A | ||

| D | BBB-(sf)/NR/ BBB(low)(sf) | $47,479,000 | 6.625% | (7) | 9.99 | 11/23 - 11/23 | 55.7% | 12.9% | ||

| E | BB(sf)/NR/ BB(sf) | $15,826,000 | 4.875% | (7) | 9.99 | 11/23 - 11/23 | 56.8% | 12.7% | ||

| F | B(sf)/NR/ B(sf) | $9,043,000 | 3.875% | (7) | 9.99 | 11/23 - 11/23 | 57.4% | 12.6% | ||

| G | NR/NR/NR | $35,044,517 | 0.000% | (7) | 9.99 | 11/23 - 11/23 | 59.7% | 12.1% |

| Notes: | |||

| (1) | The expected ratings presented are those of Fitch Ratings, Inc. (“Fitch”), Moody’s Investors Service, Inc. (“Moody's”) and DBRS, Inc. (“DBRS”), which the depositor hired to rate the rated offered certificates. One or more other nationally recognized statistical ratings organizations, as defined in Section 3(a)(62) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act or otherwise to rate or provide market reports and/or published commentary related to the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign or that its reports will not express differing, possibly negative, views of the mortgage loans and/or the offered certificates. See “Risk Factors—Risks Related to the Offered Certificates—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May be Downgraded” in the free writing prospectus, dated October 28, 2013 (the “Free Writing Prospectus”). | ||

| (2) | The principal balances and notional amounts set forth in the table are approximate. The actual initial principal balances and notional amounts may be larger or smaller depending on the aggregate cut-off date principal balance of the mortgage loans definitively included in the pool of mortgage loans, which aggregate cut-off date principal balance may be as much as 5% larger or smaller than the amount presented in the Free Writing Prospectus. | ||

| (3) | The approximate initial credit support with respect to the Class A-1, A-2, A-3, A-4 and A-SB Certificates represents the approximate credit enhancement for the Class A-1, A-2, A-3, A-4 and A-SB Certificates in the aggregate. | ||

| (4) | Weighted Average Lives and Expected Principal Windows are calculated based on an assumed prepayment rate of 0% CPR and the “Structuring Assumptions” described on Annex D to the Free Writing Prospectus. | ||

| (5) | The Certificate Principal to Value Ratio for each of the Class A-S, B, C, D, E, F and G Certificates is calculated by dividing the aggregate principal balance of such class of certificates and all classes of certificates (other than Class X-A, X-B and X-C, which are notional amount certificates and will not have principal balances) senior to such class by the aggregate appraised value of $1,515,361,393 (calculated as described in the Free Writing Prospectus) of the mortgaged properties securing the mortgage loans (excluding, with respect to the Matrix MHC Portfolio, Westfield Mission Valley and Home Depot Brush Avenue loan combinations, a pro rata portion of the related appraised value allocated to the related companion loan based on its cut-off date principal balance). The Certificate Principal to Value Ratios for each of the Class A-1, A-2, A-3, A-4 and A-SB Certificates are calculated by dividing the aggregate principal balance of the Class A-1, A-2, A-3, A-4 and A-SB Certificates by such aggregate appraised value (excluding, with respect to the Matrix MHC Portfolio, Westfield Mission Valley and Home Depot Brush Avenue loan combinations, a pro rata portion of the related appraised value allocated to the related companion loan based on its cut-off date principal balance). However, excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan (unless such mortgage loans are cross-collateralized and the cross-collateralization remains in effect). | ||

| (6) | The Certificate Principal U/W NOI Debt Yield for each of the Class A-S, B, C, D, E, F and G Certificates is calculated by dividing the underwritten net operating income (which excludes, with respect to the Matrix MHC Portfolio, Westfield Mission Valley and Home Depot Brush Avenue loan combinations, a pro rata portion of the related underwritten net operating income allocated to the related companion loan based on its cut-off date principal balance) for the mortgage pool of $109,174,369 (calculated as described in the Free Writing Prospectus) by the aggregate principal balance of such class of certificates and all classes of certificates (other than Class X-A, X-B and X-C, which are notional amount certificates and will not have principal balances) senior to such class of certificates. The Certificate Principal U/W NOI Debt Yield for each of the Class A-1, A-2, A-3, A-4 and A-SB Certificates is calculated by dividing such mortgage pool underwritten net operating income (which excludes, with respect to the Matrix MHC Portfolio, Westfield Mission Valley and Home Depot Brush Avenue loan combinations, a pro rata portion of the related underwritten net operating income allocated to the related companion loan based on its cut-off date principal balance) by the aggregate principal balance of the Class A-1, A-2, A-3, A-4 and A-SB Certificates. However, cash flow from each mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan (unless such mortgage loans are cross-collateralized and the cross-collateralization remains in effect). | ||

| (7) | The pass-through rates for the Class A-1, A-2, A-3, A-4, A-SB, A-S, B, C, D, E, F and G Certificates, in each case, will be one of the following: (i) a fixed rate per annum, (ii) the WAC Rate (as defined in the Free Writing Prospectus) for the related distribution date, (iii) a variable rate per annum equal to the lesser of (a) a fixed rate and (b) the WAC Rate for the related distribution date or (iv) a variable rate per annum equal to the WAC Rate for the related distribution date minus a specified percentage. | ||

| (8) | The Class X-A Certificates are notional amount certificates. The Notional Amount of the Class X-A Certificates will be equal to the aggregate principal balance of the Class A-1, A-2, A-3, A-4, A-SB and A-S Certificates outstanding from time to time. The Class X-A Certificates will not be entitled to distributions of principal. | ||

| (9) | The pass-through rate for the Class X-A Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-1, A-2, A-3, A-4, A-SB and A-S Certificates for the related distribution date, weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. | ||

| (10) | The Class X-B Certificates are notional amount certificates. The Notional Amount of the Class X-B Certificates will be equal to the principal balance of the Class B Certificates outstanding from time to time. The Class X-B Certificates will not be entitled to distributions of principal. | ||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| WFRBS Commercial Mortgage Trust 2013-C17 | Issue Characteristics |

| (11) | The pass-through rate for the Class X-B Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the pass-through rates on the Class B Certificates for the related distribution date. | ||

| (12) | The Class X-C Certificates are notional amount certificates. The Notional Amount of the Class X-C Certificates will be equal to the aggregate principal balance of the Class E, F and G Certificates outstanding from time to time. The Class X-C Certificates will not be entitled to distributions of principal. | ||

| (13) | The pass-through rate for the Class X-C Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the weighted average of the pass-through rates on the Class E, F and G Certificates for the related distribution date, weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| WFRBS Commercial Mortgage Trust 2013-C17 | Issue Characteristics |

II. Transaction Highlights

Mortgage Loan Sellers:

| Number of | Number of | % of Cut-off | ||||||||

| Mortgage | Mortgaged | Aggregate Cut-off | Date Pool | |||||||

| Mortgage Loan Seller | Loans | Properties | Date Balance | Balance | ||||||

| Wells Fargo Bank, National Association | 35 | 44 | $310,523,181 | 34.3 | % | |||||

The Royal Bank of Scotland(1) | 13 | 16 | 221,057,500 | 24.4 | ||||||

| Rialto Mortgage Finance, LLC | 8 | 28 | 173,864,840 | 19.2 | ||||||

| Liberty Island Group I LLC | 7 | 14 | 83,681,740 | 9.3 | ||||||

| Basis Real Estate Capital II, LLC | 7 | 18 | 63,311,424 | 7.0 | ||||||

| C-III Commercial Mortgage LLC | 14 | 14 | 51,915,832 | 5.7 | ||||||

| Total | 84 | 134 | $904,354,517 | 100.0 | % | |||||

| (1) | The mortgage loan seller referred to herein as The Royal Bank of Scotland is comprised of two affiliated companies: The Royal Bank of Scotland plc and RBS Financial Products Inc. With respect to the mortgage loans being sold for the deposit into the trust by The Royal Bank of Scotland: (a) eight (8) mortgage loans, having an aggregate cut-off date principal balance of $115,457,500 and representing 12.8% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date, are being sold for deposit into the trust only by The Royal Bank of Scotland plc (b) five (5) mortgage loans, having a cut-off date principal balance of $105,600,000 and representing 11.7% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date are being sold for deposit into the trust by RBS Financial Products Inc. |

| Loan Pool: | ||

| Cut-off Date Balance: | $904,354,517 | |

| Number of Mortgage Loans: | 84 | |

| Average Cut-off Date Balance per Mortgage Loan: | $10,766,125 | |

| Number of Mortgaged Properties: | 134 | |

Average Cut-off Date Balance per Mortgaged Property(1): | $6,748,914 | |

| Weighted Average Mortgage Interest Rate: | 5.194% | |

| Ten Largest Mortgage Loans as % of Cut-off Date Pool Balance: | 45.3% | |

| Weighted Average Original Term to Maturity or ARD (months): | 109 | |

| Weighted Average Remaining Term to Maturity or ARD (months): | 108 | |

Weighted Average Original Amortization Term (months)(2): | 346 | |

Weighted Average Remaining Amortization Term (months)(2): | 346 | |

| Weighted Average Seasoning (months): | 1 |

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. |

| (2) | Excludes any mortgage loan that does not amortize. |

| Credit Statistics: | ||

Weighted Average U/W Net Cash Flow DSCR(1): | 1.80x | |

Weighted Average U/W Net Operating Income Debt Yield Ratio(1): | 12.1% | |

Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 62.6% | |

Weighted Average Balloon or ARD Loan-to-Value Ratio(1): | 54.4% | |

| % of Mortgage Loans with Additional Subordinate Debt: | 7.2% | |

% of Mortgage Loans with Single Tenants(2): | 5.7% |

| (1) | With respect to the Matrix MHC Portfolio, Westfield Mission Valley and Home Depot Brush Avenue mortgage loans, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. The information for each mortgaged property that relates to a mortgage loan that is cross-collateralized with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio, or debt yield for each such mortgaged property is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgaged property securing a mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. See Annex A to the Free Writing Prospectus. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. |

| (2) | Excludes mortgage loans that are secured by multiple single-tenant properties with different tenants at such properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| WFRBS Commercial Mortgage Trust 2013-C17 | Issue Characteristics |

Loan Structural Features:

Amortization: Based on the Cut-off Date Pool Balance, 80.6% of the mortgage pool (79 mortgage loans) has scheduled amortization, as follows:

55.1% (65 mortgage loans) requires amortization during the entire loan term

25.4% (14 mortgage loans) provides for an interest-only period followed by an amortization period

Interest-Only: Based on the Cut-off Date Pool Balance, 19.4% of the mortgage pool (5 mortgage loans) provides for interest-only payments during the entire loan term. The Weighted Average Cut-off Date Loan-to-Value Ratio and Weighted Average U/W Net Cash Flow DSCR for those mortgage loans is 44.6% and 3.00x, respectively.

Hard Lockboxes: Based on the Cut-off Date Pool Balance, 35.5% of the mortgage pool (20 mortgage loans) has hard lockboxes in place.

Reserves: The mortgage loans require amounts to be escrowed monthly as follows (excluding any mortgage loans with springing provisions):

| Real Estate Taxes: | 76.4% of the pool | |

| Insurance Premiums: | 65.8% of the pool | |

| Capital Replacements: | 79.2% of the pool | |

| TI/LC: | 67.2% of the pool | (1) |

| (1) The percentage of Cut-off Date Balance for loans with TI/LC reserves is based on the aggregate principal balance allocable to office, retail, industrial and mixed use properties. | ||

Call Protection/Defeasance: Based on the Cut-off Date Pool Balance, the mortgage pool has the following call protection and defeasance features:

89.7% of the mortgage pool (79 mortgage loans) features a lockout period, then defeasance only until an open period

6.1% of the mortgage pool (1 mortgage loan) features a lockout period, then defeasance or the greater of a prepayment premium or yield maintenance until an open period

4.3% of the mortgage pool (4 mortgage loans) features a lockout period, then the greater of a prepayment premium or yield maintenance until an open period

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| WFRBS Commercial Mortgage Trust 2013-C17 | Issue Characteristics |

| III. | Issue Characteristics | ||

| Securities Offered: | $796,962,000 approximate monthly pay, multi-class, commercial mortgage REMIC pass-through certificates consisting of ten classes (Classes A-1, A-2, A-3, A-4, A-SB, A-S, B, C, X-A and X-B), which are offered pursuant to a registration statement filed with the SEC. | ||

| Mortgage Loan Sellers: | Wells Fargo Bank, National Association (“WFB”); The Royal Bank of Scotland (“RBS”); Rialto Mortgage Finance, LLC (“RMF”); Liberty Island Group I LLC (“LIG I”); Basis Real Estate Capital II, LLC (“Basis”) and C-III Commercial Mortgage LLC (“CIIICM”) | ||

| Co-lead Bookrunning | |||

| Managers: | RBS Securities Inc. and Wells Fargo Securities, LLC | ||

| Co-Managers: | Barclays Capital Inc. and Deutsche Bank Securities Inc. | ||

| Rating Agencies: | Fitch Ratings, Inc., Moody’s Investors Service, Inc. and DBRS, Inc., | ||

| Master Servicer: | Wells Fargo Bank, National Association | ||

| Special Servicer: | Rialto Capital Advisors, LLC | ||

| Certificate Administrator: | Wells Fargo Bank, National Association | ||

| Trustee: | U.S. Bank National Association | ||

| Trust Advisor: | Trimont Real Estate Advisors, Inc. | ||

Initial Majority Subordinate Certificateholder: | RREF II CMBS AIV, LP, an affiliate of Rialto Real Estate Fund, LP, or another affiliate of Rialto Real Estate Fund, LP | ||

| Cut-off Date: | The Cut-off Date with respect to each mortgage loan is the due date for the monthly debt service payment that is due in November 2013 (or, in the case of any mortgage loan that has its first due date in December 2013, the date that would have been its due date in November 2013 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). | ||

| Expected Closing Date: | On or about November 20, 2013. | ||

| Determination Dates: | The eleventh day of each month (or if that day is not a business day, the next succeeding business day), commencing in December 2013. | ||

| Distribution Dates: | The fourth business day following the Determination Date in each month, commencing in December 2013. | ||

| Rated Final Distribution Date: | The Distribution Date in December 2046. | ||

| Interest Accrual Period: | With respect to any Distribution Date, the calendar month preceding the month in which such Distribution Date occurs. | ||

| Day Count: | The Offered Certificates will accrue interest on a 30/360 basis. | ||

| Minimum Denominations: | $10,000 for each Class of Offered Certificates (other than the class X-A and class X-B Certificates) and $1,000,000 for the class X-A and Class X-B Certificates. Investments may also be made in any whole dollar denomination in excess of the applicable minimum denomination. | ||

| Clean-up Call: | 1% | ||

| Delivery: | DTC, Euroclear and Clearstream Banking | ||

| ERISA/SMMEA Status: | Each Class of Offered Certificates is expected to be eligible for exemptive relief under ERISA. No Class of Offered Certificates will be SMMEA eligible. | ||

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. SEE THE “RISK FACTORS” SECTION OF THE FREE WRITING PROSPECTUS. | ||

Bond Analytics Information: | The Certificate Administrator will be authorized to make distribution date settlements, CREFC® reports and certain supplemental reports (other than confidential information) available to certain financial modeling and data provision services, including Bloomberg Financial Markets L.P., Trepp LLC, Intex Solutions, Inc., Markit Group Limited, Interactive Data Corp.,BlackRock Financial Management, Inc. and CMBS.com, Inc. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| WFRBS Commercial Mortgage Trust 2013-C17 | Characteristics of the Mortgage Pool |

IV. Characteristics of the Mortgage Pool(1)

A. Ten Largest Mortgage Loans

| % of Cut- | ||||||||||||||||||||||||||||||

| Number of | off Date | Number of | Cut-off Date | |||||||||||||||||||||||||||

| Mortgage | Mortgage Loans / | Mortgage Loan | Pool | SF, Rooms, | Balance Per | Cut-off Date | Balloon or | U/W NOI | ||||||||||||||||||||||

| Loan | Mortgaged | Cut-off Date | Balance | Property | Pads or | Unit of | LTV Ratio | ARD LTV | U/W NCF | Debt Yield | ||||||||||||||||||||

| Seller | Mortgage Loan Name | City | State | Properties | Balance ($) | (%) | Type | Beds | Measure($) | (%) | Ratio (%) | DSCR (x) | (%) | |||||||||||||||||

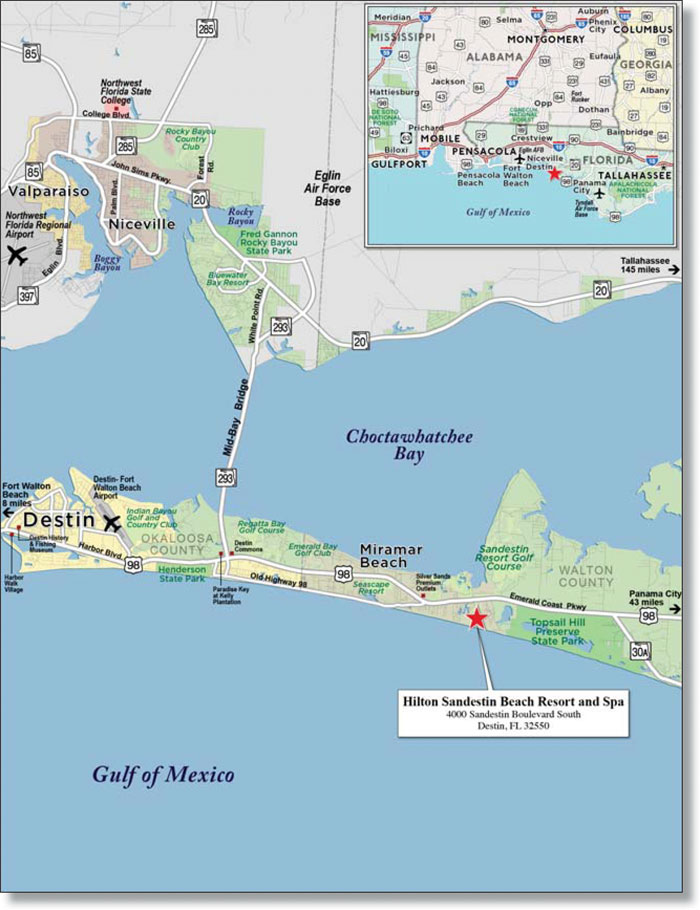

| WFB | Hilton Sandestin Beach Resort & Spa | Destin | FL | 1 / 1 | $75,000,000 | 8.3 | % | Hospitality | 598 | $125,418 | 36.6 | % | 36.6 | % | 3.37 | x | 19.8 | % | ||||||||||||

| Manufactured | ||||||||||||||||||||||||||||||

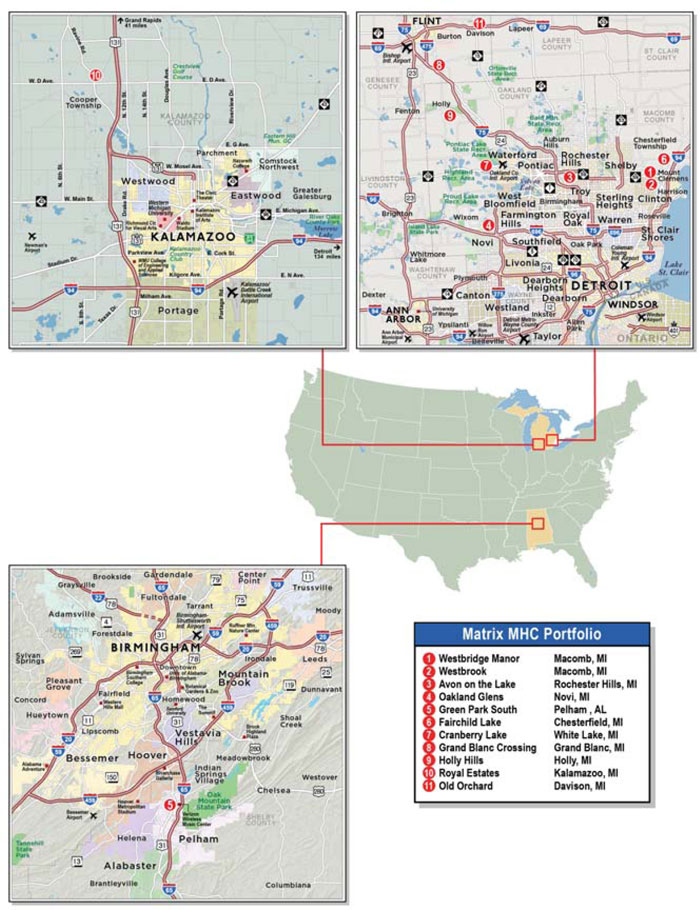

| RMF | Matrix MHC Portfolio | Various | Various | 1 / 11 | 65,500,000 | 7.2 | Housing | 5,347 | 25,248 | 69.4 | 66.2 | 1.47 | 11.1 | |||||||||||||||||

| Community | ||||||||||||||||||||||||||||||

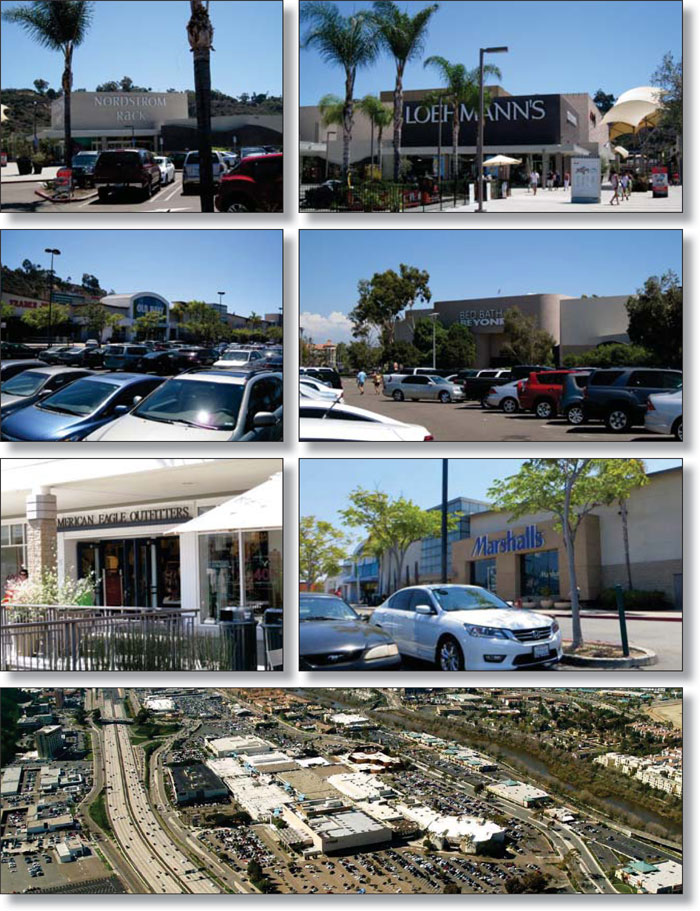

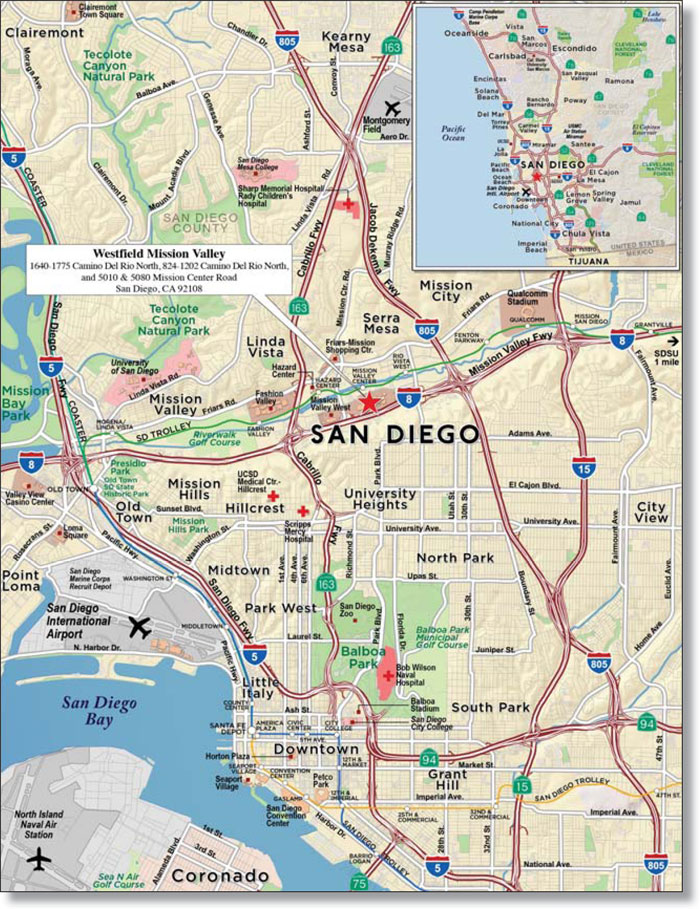

| RBS | Westfield Mission Valley | San Diego | CA | 1 / 1 | 55,000,000 | 6.1 | Retail | 997,549 | 155 | 43.9 | 43.9 | 3.12 | 14.9 | |||||||||||||||||

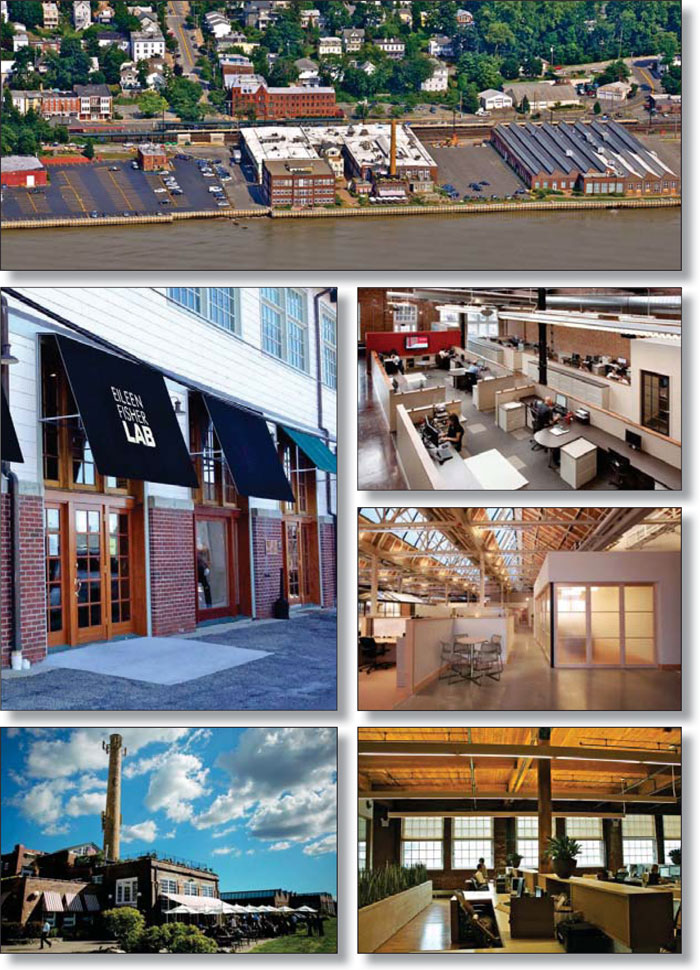

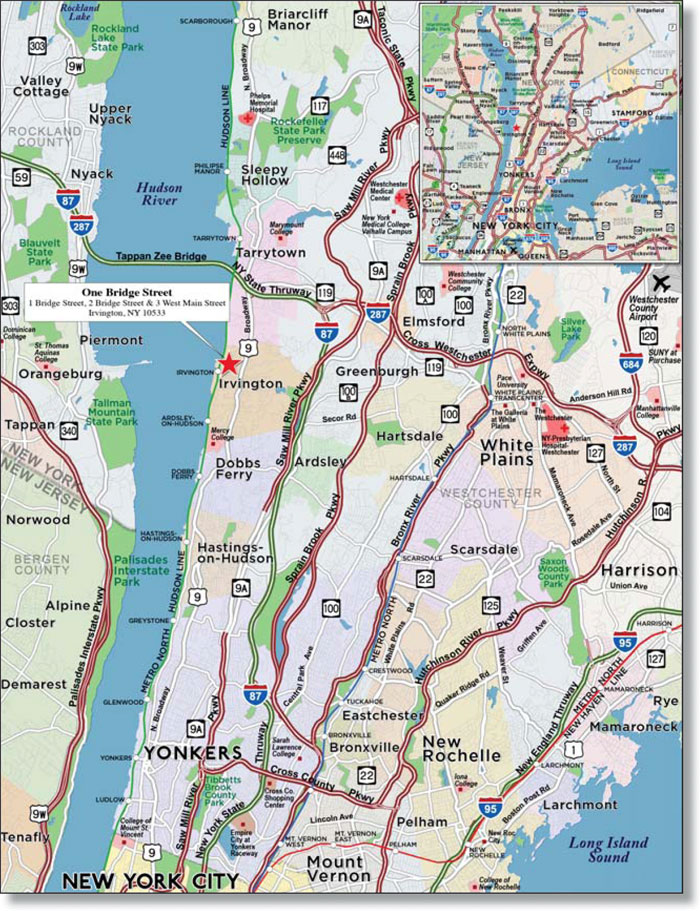

| RBS | One Bridge Street | Irvington | NY | 1 / 1 | 52,000,000 | 5.7 | Office | 195,402 | 266 | 74.3 | 61.6 | 1.31 | 9.2 | |||||||||||||||||

| RMF | Olympia Development Portfolio I | Various | Various | 1 / 10 | 35,130,000 | 3.9 | Various | Various | Various | 69.5 | 65.9 | 1.30 | 9.8 | |||||||||||||||||

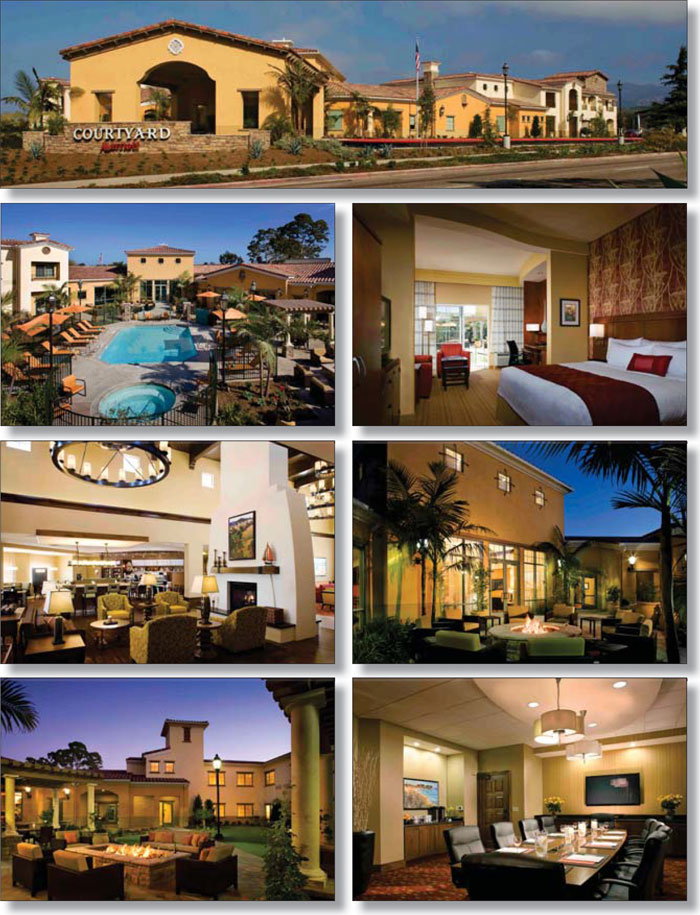

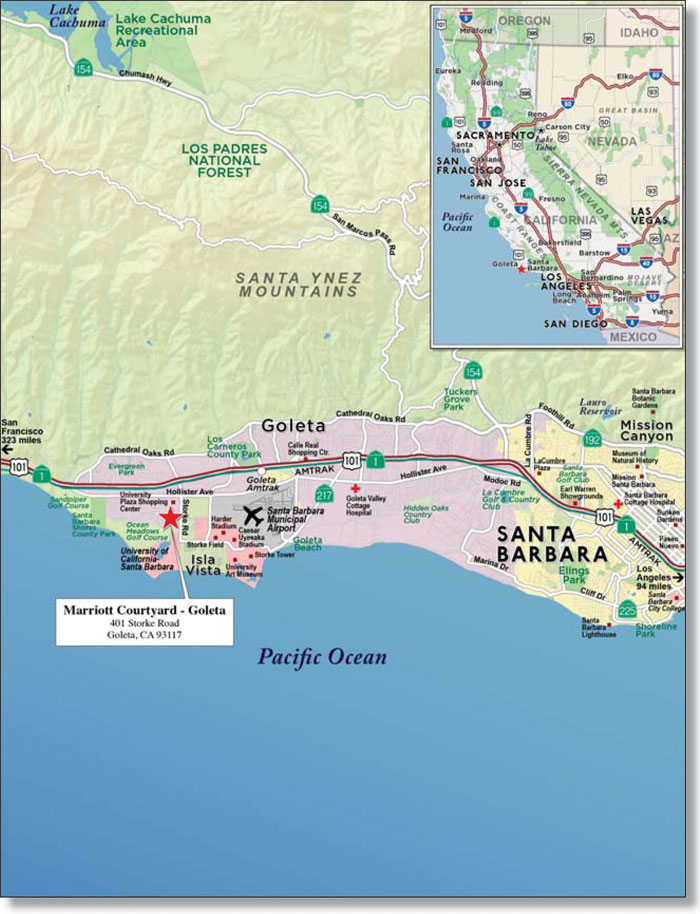

| RBS | Marriott Courtyard - Goleta | Goleta | CA | 1 / 1 | 30,100,000 | 3.3 | Hospitality | 115 | 261,739 | 69.7 | 57.3 | 1.57 | 11.0 | |||||||||||||||||

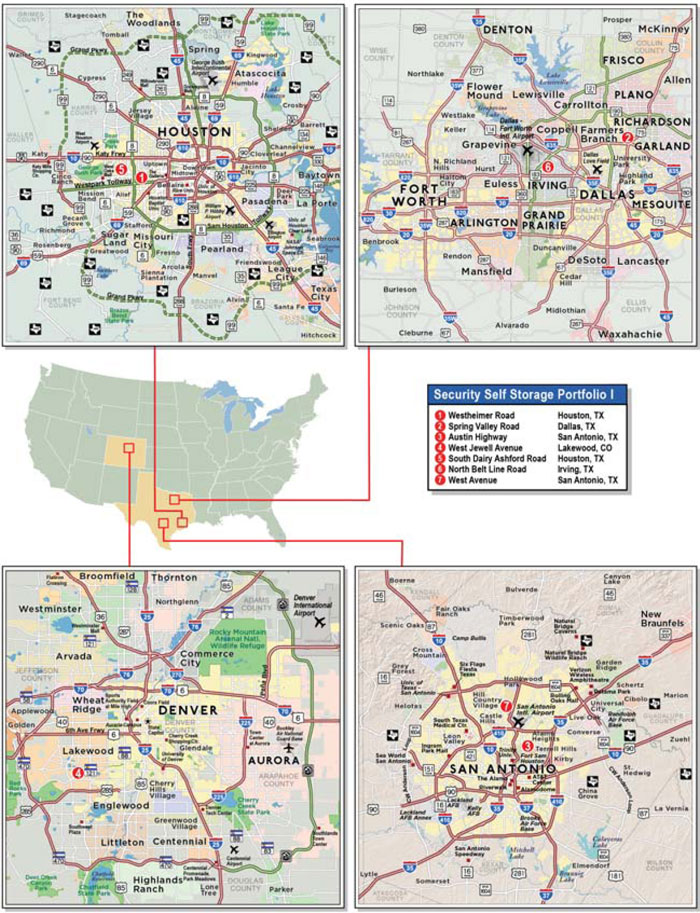

| WFB | Security Self Storage Portfolio I | Various | Various | 1 / 7 | 26,800,000 | 3.0 | Self Storage | 381,700 | 70 | 71.2 | 58.2 | 1.52 | 9.9 | |||||||||||||||||

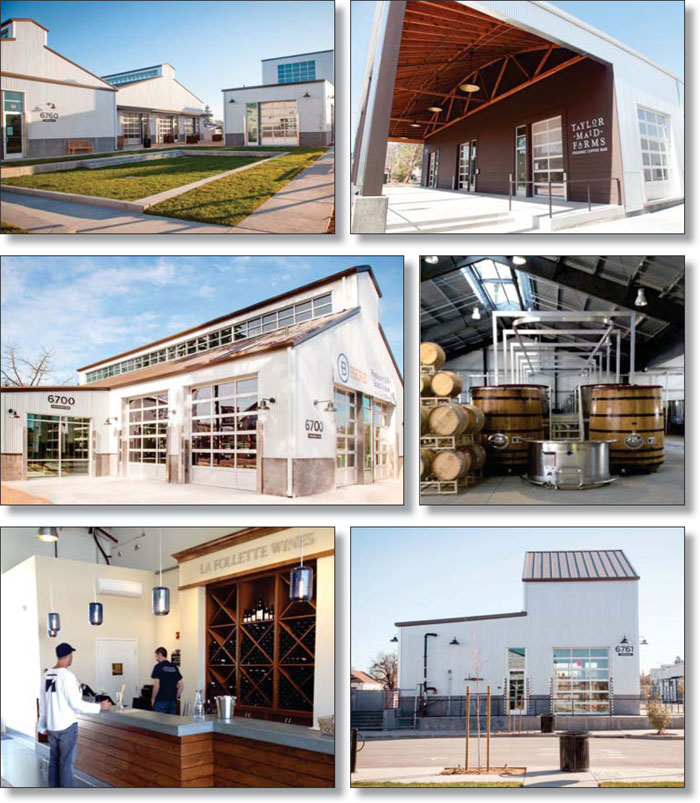

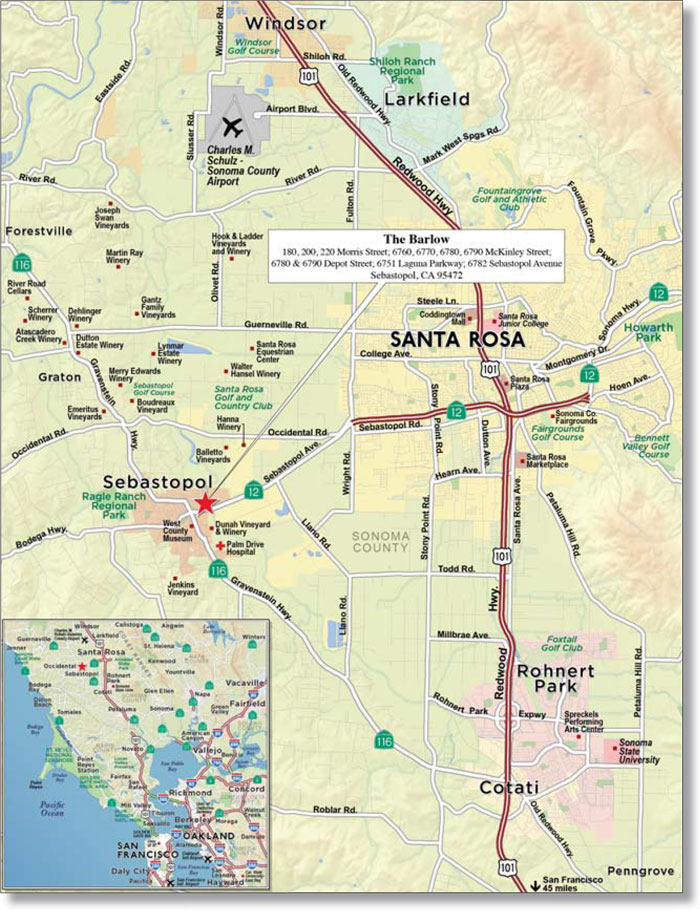

| WFB | The Barlow | Sebastopol | CA | 1 / 1 | 23,800,000 | 2.6 | Mixed Use | 174,901 | 136 | 67.6 | 63.1 | 1.48 | 9.6 | |||||||||||||||||

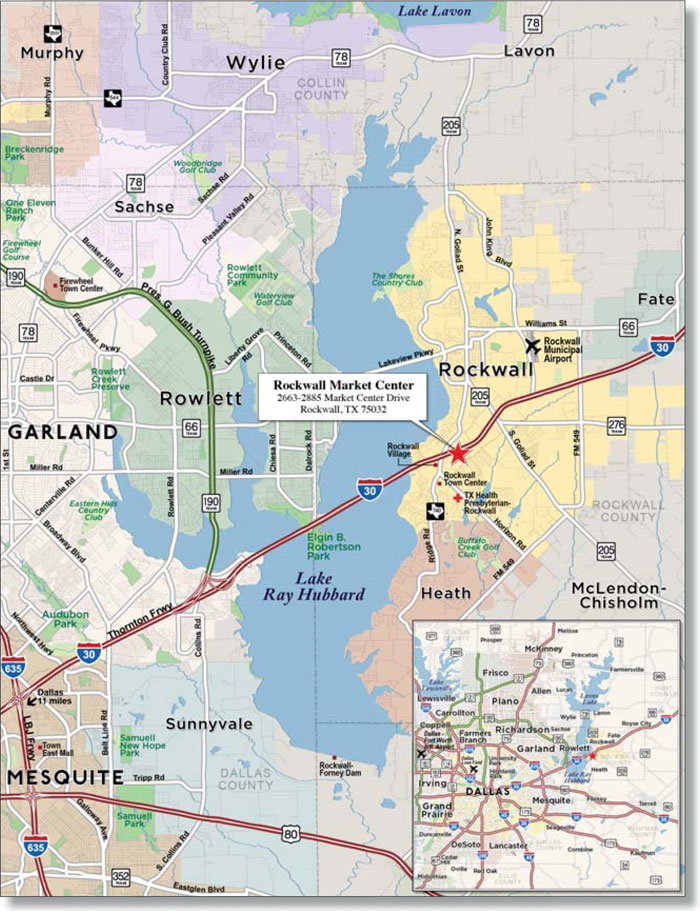

| WFB | Rockwall Market Center | Rockwall | TX | 1 / 1 | 23,070,000 | 2.6 | Retail | 209,054 | 110 | 72.5 | 65.6 | 1.33 | 9.4 | |||||||||||||||||

| Basis | Crowne Tundra Hotel Portfolio | Various | Various | 1 / 2 | 22,968,294 | 2.5 | Hospitality | 480 | 47,851 | 55.9 | 50.3 | 1.75 | 15.6 | |||||||||||||||||

| Top Three Total/Weighted Average | 3 / 13 | $195,500,000 | 21.6 | % | 49.6 | % | 48.6 | % | 2.66 | x | 15.5 | % | ||||||||||||||||||

| Top Five Total/Weighted Average | 5 / 24 | $282,630,000 | 31.3 | % | 56.6 | % | 53.1 | % | 2.24 | x | 13.6 | % | ||||||||||||||||||

| Top Ten Total/Weighted Average | 10 / 36 | $409,368,294 | 45.3 | % | 60.0 | % | 54.9 | % | 2.02 | x | 12.8 | % | ||||||||||||||||||

| Non-Top Ten Total/Weighted Average | 74 / 98 | $494,986,223 | 54.7 | % | 64.7 | % | 53.9 | % | 1.62 | x | 11.4 | % | ||||||||||||||||||

(1) With respect to the Matrix MHC Portfoilo and Westfield Mission Valley mortgage loans, Cut-off Date Balance per unit of measure, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. | ||||||||||||||||||||||||||||||

B. Summary of Pari Passu Split Loan Structures

| Whether Note is | |||||||||||||

| Related Notes in | Lead Servicing for | ||||||||||||

| Mortgage Loan | Loan Group | the Entire Loan | Current Master Servicer Under Related | Current Special Servicer Under Related | |||||||||

| Mortgage Loan Name | Seller | (Original Balance) | Holder of Note | Combination | Securitization PSA | Securitization PSA | |||||||

| Matrix MHC Portfolio | RMF | $65,500,000 | WFRBS 2013-C17 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |||||||

| RMF | $69,500,000 | GSMS 2013-GCJ16(1) | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | ||||||||

| Westfield Mission Valley | RBS | $55,000,000 | WFRBS 2013-C17 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |||||||

| Home Depot Brush Avenue | RBS | $100,000,000 | WFRBS 2013-C16 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |||||||

| RMF | $14,400,000 | WFRBS 2013-C17 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | ||||||||

| RMF | $12,600,000 | GSMS 2013-GCJ16(1) | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | ||||||||

(1) The related pari passu companion loans are currently held by the mortgage loan seller for the mortgage loan included in the WFRBS 2013-C17 trust, but is expected to be held by the trustee for the GSMS 2013-GCJ16 Trust upon the closing of such securitization.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| WFRBS Commercial Mortgage Trust 2013-C17 | Characteristics of the Mortgage Pool |

C. Previous Securitization History(1) |

| Mortgage Loan | ||||||||||||||||

| Mortgage | or Mortgaged | % of Cut-off | ||||||||||||||

| Loan | Mortgage | Loan or Mortgaged | Property | Property Cut-off | Date Pool | |||||||||||

| No. | Loan Seller | Property Name | City | State | Type | Date Balance ($) | Balance (%) | Previous Securitization | ||||||||

| 1 | WFB | Hilton Sandestin Beach Resort & Spa | Destin | FL | Hospitality | $75,000,000 | 8.3% | BSCMS 2004-PWR6 | ||||||||

| 4 | RBS | One Bridge Street | Irvington | NY | Office | 52,000,000 | 5.7 | CSFB 2005-C6 | ||||||||

| 5.01 | RMF | Publix Supermarket & Retail: H&R Block, UPS, Domino's | Temple Terrace | FL | Retail | 6,750,000 | 0.7 | WBCMT 2005-C17 | ||||||||

| 5.03 | RMF | Walgreens #4398 | Dunedin | FL | Retail | 4,880,000 | 0.5 | WBCMT 2005-C17 | ||||||||

| 5.04 | RMF | Walgreens #5447 | Marietta | GA | Retail | 3,840,000 | 0.4 | WBCMT 2005-C17 | ||||||||

| 5.05 | RMF | Walgreens #5580 | Decatur | GA | Retail | 3,680,000 | 0.4 | WBCMT 2005-C17 | ||||||||

| 5.06 | RMF | Walgreens #4480 | Oldsmar | FL | Retail | 3,127,500 | 0.3 | WBCMT 2005-C17 | ||||||||

| 5.07 | RMF | Applebee's | Lithia Springs | GA | Retail | 2,390,000 | 0.3 | WBCMT 2005-C17 | ||||||||

| 5.08 | RMF | Dunedin Office (Da Vinci & BayCare) | Dunedin | FL | Office | 2,217,500 | 0.2 | WBCMT 2005-C17 | ||||||||

| 5.09 | RMF | Bank of America | Dunedin | FL | Retail | 1,575,000 | 0.2 | WBCMT 2005-C17 | ||||||||

| 5.10 | RMF | Anytime Fitness/Dunkin' Donuts | Dunedin | FL | Retail | 1,500,000 | 0.2 | WBCMT 2005-C17 | ||||||||

| 12 | LIG I | Midway Shopping Center | Mill Creek Hundred | DE | Retail | 17,000,000 | 1.9 | WBCMT 2003-C4 | ||||||||

| 16 | RBS | 450 - 460 N. Canon Drive | Beverly Hills | CA | Retail | 14,500,000 | 1.6 | MLMT 2005-CIP1 | ||||||||

| 19 | LIG I | Holiday Inn Express Old Town San Diego | San Diego | CA | Hospitality | 13,985,158 | 1.5 | JPMCC 2004-PNC1 | ||||||||

| 30 | BASIS | Huntington Ridge | Irving | TX | Multifamily | 8,500,000 | 0.9 | CSFB 2005-C1 | ||||||||

| 33 | LIG I | 690 Merrill Road | Pittsfield | MA | Retail | 8,000,000 | 0.9 | PNCMA 1999-CM1 | ||||||||

| 40 | WFB | Locust Grove Village | Locust Grove | GA | Retail | 7,189,771 | 0.8 | MLMT 2003-KEY1 | ||||||||

| 43 | WFB | Park Plaza Shopping Center | Chico | CA | Retail | 6,500,000 | 0.7 | BSCMS 2004-PWR3 | ||||||||

| 44 | CIIICM | Lincoln Park MHC | West Allis | WI | Manufactured Housing Community | 6,493,382 | 0.7 | BACM 2004-C1 | ||||||||

| 51 | CIIICM | Wheatland Estates MHC | Burlington | WI | Manufactured Housing Community | 5,084,817 | 0.6 | BACM 2004-C1 | ||||||||

| 56 | CIIICM | Arlington MHC | Bloomington | IN | Manufactured Housing Community | 4,130,790 | 0.5 | BACM 2004-C1 | ||||||||

| 58 | CIIICM | Champions Business Park | Houston | TX | Mixed Use | 4,000,000 | 0.4 | LBUBS 2004-C1 | ||||||||

| 59 | WFB | Royal Plaza Building | Los Angeles | CA | Mixed Use | 3,994,402 | 0.4 | MSC 2004-T13 | ||||||||

| 62 | RBS | Torrey Highlands Plaza | San Diego | CA | Retail | 3,500,000 | 0.4 | JPMCC 2004-C1 | ||||||||

| 63 | WFB | Walgreens - Prattville | Prattville | AL | Retail | 3,495,009 | 0.4 | WGL 2002-1 | ||||||||

| 64 | WFB | Walgreens - Suwanee | Suwanee | GA | Retail | 3,292,541 | 0.4 | MLMT 2003-KEY1 | ||||||||

| 66 | WFB | Antelope Self Storage | Sacramento | CA | Self Storage | 3,096,963 | 0.3 | MSC 2004-T13 | ||||||||

| 67 | CIIICM | Sunset MHC | Marshalltown | IA | Manufactured Housing Community | 3,096,844 | 0.3 | BACM 2004-1 | ||||||||

| 71 | WFB | Shops at Dana Park | Mesa | AZ | Retail | 2,622,503 | 0.3 | MSC 2004-HQ3 | ||||||||

| 72 | WFB | Fort Security Self Storage | Fort Wayne | IN | Self Storage | 2,597,683 | 0.3 | CSFB 2004-C1 | ||||||||

| 73 | RBS | Budget Self Storage Portfolio | Various | CA | Self Storage | 2,500,000 | 0.3 | BSCMS 2005-PWR8 | ||||||||

| 73.01 | RBS | Lancaster | Lancaster | CA | Self Storage | 1,302,100 | 0.1 | BSCMS 2005-PWR8 | ||||||||

| 73.02 | RBS | Palmdale | Palmdale | CA | Self Storage | 1,197,900 | 0.1 | BSCMS 2005-PWR8 | ||||||||

| 74 | WFB | Village Plaza Shopping Center | Redding | CA | Retail | 2,196,537 | 0.2 | MSC 2003-T11 | ||||||||

| 76 | WFB | Walgreens - Leander | Leander | TX | Retail | 1,993,018 | 0.2 | WBCMT 2003-C8 | ||||||||

| 77 | CIIICM | Thousand Oaks | Mansfeld | TX | Manufactured Housing Community | 1,835,000 | 0.2 | JPMCC 2004-C1 | ||||||||

| 78 | WFB | All Climate Controlled Self Storage | Miramar Beach | FL | Self Storage | 1,700,000 | 0.2 | LBUBS 2004-C1 | ||||||||

| 83 | WFB | Charger Square | Mesquite | TX | Mixed Use | 1,000,000 | 0.1 | LBUBS 2003-C8 | ||||||||

| Total | $291,764,418 | 32.3% |

| (1) | The table above represents the most recent securitization with respect to the mortgaged property securing the related mortgage loan, based on information provided by the related borrower or obtained through searches of a third-party database. While the above mortgage loans may have been securitized multiple times in prior transactions, mortgage loans are only listed in the above chart if the mortgage loan paid off a mortgage loan in another securitization. The information has not otherwise been confirmed by the mortgage loan sellers. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| WFRBS Commercial Mortgage Trust 2013-C17 | Characteristics of the Mortgage Pool |

D. Mortgage Loans with Scheduled Balloon Payments and Related Classes |

Class A-2(1) | ||||||||||||||||||||||||||||||||

Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Pool Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-2 Certificate Principal Balance (%)(2) | Pads/ Units/SF /Rooms | Loan per Pad/Unit/ SF/ Room ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) | ||||||||||||||||

| 2 | RMF | Matrix MHC Portfolio | Various | Manufactured Housing Community | $65,500,000 | 7.2% | $62,483,509 | 37.4% | 5,347 | $25,248 | 1.47x | 11.1% | 69.4% | 66.2% | 9 | 57 | ||||||||||||||||

| 5 | RMF | Olympia Development Portfolio I | Various | Various | 35,130,000 | 3.9 | 33,308,227 | 20.0 | Various | Various | 1.30 | 9.8 | 69.5 | 65.9 | 18 | 60 | ||||||||||||||||

| 8 | WFB | The Barlow | CA | Mixed Use | 23,800,000 | 2.6 | 22,220,965 | 13.3 | 174,901 | 136 | 1.48 | 9.6 | 67.6 | 63.1 | 12 | 60 | ||||||||||||||||

| 10 | Basis | Crowne Tundra Hotel Portfolio | Various | Hospitality | 22,968,294 | 2.5 | 20,665,581 | 12.4 | 480 | 47,851 | 1.75 | 15.6 | 55.9 | 50.3 | 0 | 59 | ||||||||||||||||

| 18 | RBS | 21st Century Storage Portfolio | Various | Self Storage | 14,200,000 | 1.6 | 14,200,000 | 8.5 | 225,776 | 63 | 2.24 | 9.9 | 66.6 | 66.6 | 60 | 60 | ||||||||||||||||

| 28 | RMF | Reserve at Garden Lake | GA | Multifamily | 8,750,000 | 1.0 | 8,186,085 | 4.9 | 278 | 31,475 | 1.51 | 10.2 | 75.0 | 70.1 | 11 | 59 | ||||||||||||||||

| 74 | WFB | Village Plaza Shopping Center | CA | Retail | 2,196,537 | 0.2 | 1,953,327 | 1.2 | 75,750 | 29 | 1.83 | 15.9 | 43.2 | 38.5 | 0 | 59 | ||||||||||||||||

| Total/Weighted Average | $172,544,831 | 19.1% | $163,017,694 | 97.7% | 1.54x | 11.1% | 67.1% | 63.5% | 14 | 59 | ||||||||||||||||||||||

(1) The table above presents the mortgage loans whose balloon payments would be applied to pay down the principal balance of the Class A-2 Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Free Writing Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of Certificates, including the Class A-2 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. (1) Reflects the percentage of the Mortgage Loan Balance at Maturity divided by the initial Class A-2 Certificate Principal Balance. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

(THIS PAGE INTENTIONALLY LEFT BLANK)

11

| WFRBS Commercial Mortgage Trust 2013-C17 | Characteristics of the Mortgage Pool |

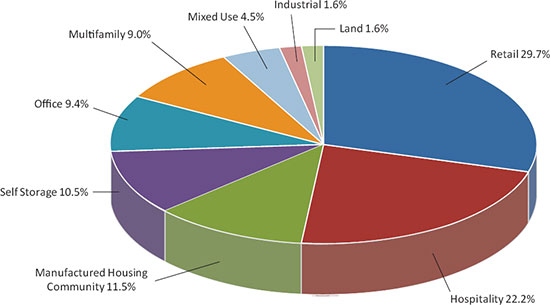

E. Property Type Distribution(1)

| % of Cut- | Weighted | Weighted | Weighted | Weighted | |||||||||||||||||||||||

| off Date | Average | Average | Weighted | Average | Average | Weighted | |||||||||||||||||||||

| Number of | Aggregate Cut- | Pool | Cut-off | Balloon or | Average | U/W NOI | U/W NCF | Average | |||||||||||||||||||

| Mortgaged | off Date Balance | Balance | Date LTV | ARD LTV | U/W NCF | Debt | Debt | Mortgage | |||||||||||||||||||

| Property Type | Properties | ($) | (%) | Ratio (%) | Ratio (%) | DSCR (x) | Yield (%) | Yield (%) | Rate (%) | ||||||||||||||||||

| Retail | 46 | $268,748,461 | 29.7 | % | 61.0 | % | 53.2 | % | 1.83 | x | 11.5 | % | 10.6 | % | 5.004 | % | |||||||||||

| Anchored | 15 | 135,534,741 | 15.0 | 67.8 | 58.0 | 1.51 | 10.3 | 9.3 | 5.089 | ||||||||||||||||||

| Regional Mall | 1 | 55,000,000 | 6.1 | 43.9 | 43.9 | 3.12 | 14.9 | 14.4 | 4.554 | ||||||||||||||||||

| Single Tenant | 21 | 42,271,068 | 4.7 | 64.3 | 54.9 | 1.41 | 10.9 | 9.9 | 5.175 | ||||||||||||||||||

| Unanchored | 6 | 23,576,769 | 2.6 | 57.3 | 47.3 | 1.53 | 11.3 | 10.4 | 5.181 | ||||||||||||||||||

Shadow Anchored(2) | 3 | 12,365,883 | 1.4 | 57.6 | 47.6 | 1.68 | 11.9 | 10.9 | 5.142 | ||||||||||||||||||

| Hospitality | 16 | 200,895,094 | 22.2 | 52.2 | 45.2 | 2.36 | 16.2 | 14.1 | 5.202 | ||||||||||||||||||

| Full Service | 4 | 103,138,294 | 11.4 | 42.5 | 41.1 | 2.91 | 18.4 | 15.7 | 5.127 | ||||||||||||||||||

| Limited Service | 11 | 87,771,354 | 9.7 | 63.0 | 50.2 | 1.70 | 13.1 | 11.7 | 5.277 | ||||||||||||||||||

| Extended Stay | 1 | 9,985,446 | 1.1 | 57.1 | 43.2 | 2.56 | 20.2 | 18.6 | 5.310 | ||||||||||||||||||

| Manufactured Housing Community | 23 | 104,264,527 | 11.5 | 69.4 | 62.6 | 1.52 | 11.1 | 10.8 | 5.898 | ||||||||||||||||||

| Manufactured Housing Community | 23 | 104,264,527 | 11.5 | 69.4 | 62.6 | 1.52 | 11.1 | 10.8 | 5.898 | ||||||||||||||||||

| Self Storage | 25 | 95,012,025 | 10.5 | 66.1 | 56.4 | 1.68 | 10.5 | 10.3 | 4.985 | ||||||||||||||||||

| Self Storage | 25 | 95,012,025 | 10.5 | 66.1 | 56.4 | 1.68 | 10.5 | 10.3 | 4.985 | ||||||||||||||||||

| Office | 6 | 84,907,378 | 9.4 | 71.7 | 60.3 | 1.39 | 9.9 | 9.2 | 5.220 | ||||||||||||||||||

| Suburban | 6 | 84,907,378 | 9.4 | 71.7 | 60.3 | 1.39 | 9.9 | 9.2 | 5.220 | ||||||||||||||||||

| Multifamily | 11 | 80,960,767 | 9.0 | 71.6 | 61.9 | 1.44 | 10.2 | 9.5 | 5.264 | ||||||||||||||||||

| Garden | 9 | 60,370,308 | 6.7 | 72.9 | 63.3 | 1.42 | 10.2 | 9.5 | 5.313 | ||||||||||||||||||

| Mid Rise | 1 | 11,850,000 | 1.3 | 71.2 | 62.0 | 1.36 | 9.5 | 9.1 | 5.290 | ||||||||||||||||||

| Student Housing | 1 | 8,740,459 | 1.0 | 63.3 | 51.9 | 1.62 | 11.0 | 10.3 | 4.890 | ||||||||||||||||||

| Mixed Use | 5 | 40,261,266 | 4.5 | 66.8 | 57.9 | 1.54 | 11.3 | 10.3 | 4.923 | ||||||||||||||||||

| Industrial/Retail | 1 | 23,800,000 | 2.6 | 67.6 | 63.1 | 1.48 | 9.6 | 9.0 | 4.500 | ||||||||||||||||||

| Office/Retail | 3 | 12,461,266 | 1.4 | 63.0 | 48.5 | 1.73 | 14.6 | 12.8 | 5.518 | ||||||||||||||||||

| Office/Warehouse/Storage | 1 | 4,000,000 | 0.4 | 74.1 | 56.5 | 1.34 | 10.8 | 10.0 | 5.590 | ||||||||||||||||||

| Industrial | 1 | 14,905,000 | 1.6 | 55.0 | 41.7 | 1.69 | 13.0 | 12.3 | 5.400 | ||||||||||||||||||

| Warehouse | 1 | 14,905,000 | 1.6 | 55.0 | 41.7 | 1.69 | 13.0 | 12.3 | 5.400 | ||||||||||||||||||

| Land | 1 | 14,400,000 | 1.6 | 56.0 | 56.0 | 1.60 | 7.9 | 7.9 | 4.905 | ||||||||||||||||||

| Land | 1 | 14,400,000 | 1.6 | 56.0 | 56.0 | 1.60 | 7.9 | 7.9 | 4.905 | ||||||||||||||||||

| Total/Weighted Average | 134 | $904,354,517 | 100.0 | % | 62.6 | % | 54.4 | % | 1.80 | x | 12.1 | % | 11.1 | % | 5.194 | % | |||||||||||

(1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, (a) the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate), and (b) the information for each mortgaged property that relates to a mortgage loan that is cross-collateralized with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio or debt yield for each such mortgaged property is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgaged property securing a mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. With respect to the Matrix MHC Portfolio, Westfield Mission Valley and Home Depot Brush Avenue mortgage loans, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. |

(2) | A mortgaged property is classified as shadow anchored if it is located in close proximity to an anchored retail property. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| WFRBS Commercial Mortgage Trust 2013-C17 | Characteristics of the Mortgage Pool |

F. Geographic Distribution(1)(2)

| % of | Weighted | Weighted | Weighted | ||||||||||||||||||||

| Cut-off | Weighted | Average | Weighted | Average | Average | Weighted | |||||||||||||||||

| Number of | Date | Average Cut-off | Balloon or | Average | U/W NOI | U/W NCF | Average | ||||||||||||||||

| Mortgaged | Aggregate Cut-off | Pool | Date LTV Ratio | ARD LTV | U/W NCF | Debt Yield | Debt | Mortgage | |||||||||||||||

Location(3) | Properties | Date Balance ($) | Balance | (%) | Ratio (%) | DSCR (x) | (%) | Yield (%) | Rate (%) | ||||||||||||||

| California | 15 | $195,498,060 | 21.6 | % | 58.1 | % | 50.9 | % | 2.03x | 12.2 | % | 11.5 | % | 4.837 | % | ||||||||

| Southern | 9 | 139,329,560 | 15.4 | 57.0 | 49.6 | 2.19 | 12.7 | 11.9 | 4.842 | ||||||||||||||

| Northern | 6 | 56,168,501 | 6.2 | 60.8 | 54.0 | 1.63 | 10.9 | 10.3 | 4.826 | ||||||||||||||

| Florida | 12 | 121,361,864 | 13.4 | 48.0 | 45.1 | 2.60 | 16.2 | 14.0 | 5.054 | ||||||||||||||

| Michigan | 23 | 105,834,445 | 11.7 | 65.7 | 58.1 | 1.53 | 12.1 | 11.3 | 6.000 | ||||||||||||||

| Texas | 21 | 102,251,596 | 11.3 | 70.9 | 60.0 | 1.43 | 10.3 | 9.5 | 5.199 | ||||||||||||||

| New York | 3 | 72,500,000 | 8.0 | 70.2 | 60.2 | 1.38 | 9.0 | 8.6 | 5.178 | ||||||||||||||

| Georgia | 11 | 60,412,612 | 6.7 | 67.0 | 57.8 | 1.51 | 10.8 | 10.0 | 5.088 | ||||||||||||||

Other States(4) | 49 | 246,495,940 | 27.3 | 65.2 | 55.2 | 1.69 | 11.9 | 11.0 | 5.228 | ||||||||||||||

| Total/Weighted Average | 134 | $904,354,517 | 100.0 | % | 62.6 | % | 54.4 | % | 1.80x | 12.1 | % | 11.1 | % | 5.194 | % | ||||||||

| (1) | The Mortgaged Properties are located in 28 states and the District of Columbia. |

| (2) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, (a) the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate), and (b) the information for each mortgaged property that relates to a mortgage loan that is cross-collateralized with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio or debt yield for each such mortgaged property is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgaged property securing a mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. With respect to the Matrix MHC Portfolio, Westfield Mission Valley and Home Depot Brush Avenue mortgage loans, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. |

| (3) | For purposes of determining whether a mortgaged property is in Northern California or Southern California, Northern California includes areas with zip codes above 93600 and Southern California includes areas with zip codes of 93600 and below. |

| (4) | Includes 22 other states and the District of Columbia. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| WFRBS Commercial Mortgage Trust 2013-C17 | Characteristics of the Mortgage Pool |

G. Characteristics of the Mortgage Pool(1)

| CUT-OFF DATE BALANCE | LOAN PURPOSE | |||||||||||||||||

| Number of | Aggregate Cut- | % of Cut-off | Number of | Aggregate Cut- | % of Cut-off | |||||||||||||

| Range of Cut-off Date | Mortgage | off Date Balance | Date Pool | Mortgage | off Date Balance | Date Pool | ||||||||||||

| Balances ($) | Loans | ($) | Balance | Loan Purpose | Loans | ($) | Balance | |||||||||||

| 1,000,000 - 2,000,000 | 9 | $13,799,679 | 1.5% | Refinance | 67 | $700,692,852 | 77.5% | |||||||||||

| 2,000,001 - 3,000,000 | 8 | 20,299,102 | 2.2 | Acquisition | 15 | 119,109,376 | �� | 13.2 | ||||||||||

| 3,000,001 - 4,000,000 | 11 | 39,344,139 | 4.4 | Various | 2 | 84,552,290 | 9.3 | |||||||||||

| 4,000,001 - 5,000,000 | 5 | 22,988,419 | 2.5 | Total: | 84 | $904,354,517 | 100.0% | |||||||||||

| 5,000,001 - 6,000,000 | 4 | 22,234,817 | 2.5 | |||||||||||||||

| 6,000,001 - 7,000,000 | 7 | 45,490,238 | 5.0 | MORTGAGE RATE | ||||||||||||||

| 7,000,001 - 8,000,000 | 8 | 61,601,207 | 6.8 | Number of | Aggregate Cut- | % of Cut-off | ||||||||||||

| 8,000,001 - 9,000,000 | 5 | 42,788,459 | 4.7 | Range of Mortgage Rates | Mortgage | off Date Balance | Date Pool | |||||||||||

| 9,000,001 - 10,000,000 | 2 | 19,885,446 | 2.2 | (%) | Loans | ($) | Balance | |||||||||||

| 10,000,001 - 15,000,000 | 12 | 154,752,427 | 17.1 | 4.295 - 4.500 | 2 | $38,000,000 | 4.2% | |||||||||||

| 15,000,001 - 20,000,000 | 3 | 51,802,290 | 5.7 | 4.501 - 4.750 | 3 | 80,750,000 | 8.9 | |||||||||||

| 20,000,001 - 30,000,000 | 4 | 96,638,294 | 10.7 | 4.751 - 5.000 | 12 | 192,951,997 | 21.3 | |||||||||||

| 30,000,001 - 50,000,000 | 2 | 65,230,000 | 7.2 | 5.001 - 5.250 | 24 | 277,001,031 | 30.6 | |||||||||||

| 50,000,001 - 70,000,000 | 3 | 172,500,000 | 19.1 | 5.251 - 5.500 | 20 | 118,239,936 | 13.1 | |||||||||||

| 70,000,001 - 75,000,000 | 1 | 75,000,000 | 8.3 | 5.501 - 5.750 | 18 | 114,752,547 | 12.7 | |||||||||||

| Total: | 84 | $904,354,517 | 100.0% | 5.751 - 6.275 | 5 | 82,659,007 | 9.1 | |||||||||||

| Average: | $10,766,125 | Total: | 84 | $904,354,517 | 100.0% | |||||||||||||

| Weighted Average: | 5.194% | |||||||||||||||||

| UNDERWRITTEN NOI DEBT SERVICE COVERAGE RATIO | ||||||||||||||||||

| Number of | Aggregate Cut- | % of Cut-off | UNDERWRITTEN NOI DEBT YIELD | |||||||||||||||

| Range of U/W NOI | Mortgage | off Date Balance | Date Pool | Number of | Aggregate Cut- | % of Cut-off | ||||||||||||

| DSCRs (x) | Loans | ($) | Balance | Range of U/W NOI | Mortgage | off Date Balance | Date Pool | |||||||||||

| 1.23 - 1.30 | 4 | $23,280,568 | 2.6% | Debt Yields (%) | Loans | ($) | Balance | |||||||||||

| 1.31 - 1.40 | 4 | 84,000,000 | 9.3 | 7.9 - 8.9 | 3 | $44,650,000 | 4.9% | |||||||||||

| 1.41 - 1.50 | 18 | 130,026,691 | 14.4 | 9.0 - 9.9 | 15 | 251,588,391 | 27.8 | |||||||||||

| 1.51 - 1.60 | 14 | 238,172,791 | 26.3 | 10.0 - 10.9 | 20 | 125,872,346 | 13.9 | |||||||||||

| 1.61 - 1.70 | 11 | 90,262,653 | 10.0 | 11.0 - 11.9 | 17 | 175,479,209 | 19.4 | |||||||||||

| 1.71 - 1.80 | 11 | 64,821,130 | 7.2 | 12.0 - 12.9 | 11 | 40,105,539 | 4.4 | |||||||||||

| 1.81 - 1.90 | 5 | 17,697,847 | 2.0 | 13.0 - 13.9 | 6 | 46,252,007 | 5.1 | |||||||||||

| 1.91 - 2.00 | 2 | 9,298,000 | 1.0 | 14.0 - 14.9 | 6 | 99,262,347 | 11.0 | |||||||||||

| 2.01 - 2.25 | 6 | 59,918,452 | 6.6 | 15.0 - 17.9 | 2 | 25,164,831 | 2.8 | |||||||||||

| 2.26 - 2.50 | 3 | 18,896,537 | 2.1 | 18.0 - 19.9 | 3 | 85,994,402 | 9.5 | |||||||||||

| 2.51 - 2.75 | 2 | 10,994,402 | 1.2 | 20.0 - 20.2 | 1 | 9,985,446 | 1.1 | |||||||||||

| 2.76 - 3.00 | 1 | 9,985,446 | 1.1 | Total: | 84 | $904,354,517 | 100.0% | |||||||||||

| 3.01 - 3.50 | 2 | 72,000,000 | 8.0 | Weighted Average: | 12.1% | |||||||||||||

| 3.51 - 3.91 | 1 | 75,000,000 | 8.3 | |||||||||||||||

| Total: | 84 | $904,354,517 | 100.0% | UNDERWRITTEN NCF DEBT YIELD | ||||||||||||||

| Weighted Average: | 1.96x | Number of | Aggregate Cut- | % of Cut-off | ||||||||||||||

| Range of U/W NCF | Mortgage | off Date Balance | Date Pool | |||||||||||||||

| UNDERWRITTEN NCF DEBT SERVICE COVERAGE RATIO | Debt Yields (%) | Loans | ($) | Balance | ||||||||||||||

| Number of | Aggregate Cut- | % of Cut-off | 7.7 - 7.9 | 2 | $28,900,000 | 3.2% | ||||||||||||

| Range of U/W NCF | Mortgage | off Date Balance | Date Pool | 8.0 - 8.9 | 6 | 149,627,429 | 16.5 | |||||||||||

| DSCRs (x) | Loans | ($) | Balance | 9.0 - 9.9 | 21 | 207,539,030 | 22.9 | |||||||||||

| 1.20 - 1.30 | 10 | $121,365,287 | 13.4% | 10.0 - 10.9 | 24 | 203,341,826 | 22.5 | |||||||||||

| 1.31 - 1.40 | 16 | 159,157,174 | 17.6 | 11.0 - 11.9 | 7 | 32,998,524 | 3.6 | |||||||||||

| 1.41 - 1.50 | 15 | 166,379,453 | 18.4 | 12.0 - 12.9 | 14 | 66,924,409 | 7.4 | |||||||||||

| 1.51 - 1.60 | 12 | 131,829,010 | 14.6 | 13.0 - 13.9 | 4 | 61,543,452 | 6.8 | |||||||||||

| 1.61 - 1.70 | 10 | 59,810,099 | 6.6 | 14.0 - 18.6 | 6 | 153,479,848 | 17.0 | |||||||||||

| 1.71 - 1.80 | 3 | 34,766,294 | 3.8 | Total: | 84 | $904,354,517 | 100.0% | |||||||||||

| 1.81 - 1.90 | 7 | 18,717,195 | 2.1 | Weighted Average: | 11.1% | |||||||||||||

| 1.91 - 2.00 | 1 | 6,075,000 | 0.7 | |||||||||||||||

| 2.01 - 2.50 | 6 | 49,269,560 | 5.4 | |||||||||||||||

| 2.51 - 3.37 | 4 | 156,985,446 | 17.4 | |||||||||||||||

| Total: | 84 | $904,354,517 | 100.0% | |||||||||||||||

| Weighted Average: | 1.80x | |||||||||||||||||

| (1) | Information regarding mortgage loans that are cross-collateralized with other mortgage loans is based upon the individual loan balances, except that the applicable loan-to value ratio, debt service coverage ratio or debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group. On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. Debt service coverage ratio, debt yield and loan-to-value ratio information takes no account of subordinate debt (whether or not secured by the mortgaged property), if any, that is allowed under the terms of any mortgage loan. With respect to the Matrix MHC Portfoilo, Westfield Mission Valley and Home Depot Brush Avenue mortgage loans, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan (unless otherwise stated) in total debt. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| WFRBS Commercial Mortgage Trust 2013-C17 | Characteristics of the Mortgage Pool |

| ORIGINAL TERM TO MATURITY OR ARD | CUT-OFF DATE LOAN-TO-VALUE RATIO | ||||||||||||||||||

| Number of | Aggregate Cut- | % of Cut-off | Number of | Aggregate Cut- | % of Cut-off | ||||||||||||||

| Range of Original Terms to | Mortgage | off Date Balance | Date Pool | Range of Cut-off Date LTV | Mortgage | off Date Balance | Date Pool | ||||||||||||

| Maturity or ARD (months) | Loans | ($) | Balance | Ratios (%) | Loans | ($) | Balance | ||||||||||||

| 60 - 83 | 7 | $172,544,831 | 19.1% | 36.6 - 40.0 | 3 | $85,994,402 | 9.5% | ||||||||||||

| 120 | 77 | 731,809,686 | 80.9 | 40.1 - 45.0 | 2 | 57,196,537 | 6.3 | ||||||||||||

| Total: | 84 | $904,354,517 | 100.0% | 45.1 - 50.0 | 3 | 17,075,000 | 1.9 | ||||||||||||

| Weighted Average: | 109 months | 50.1 - 55.0 | 8 | 57,082,981 | 6.3 | ||||||||||||||

| 55.1 - 60.0 | 7 | 70,935,056 | 7.8 | ||||||||||||||||

| REMAINING TERM TO MATURITY OR ARD | 60.1 - 65.0 | 14 | 81,155,793 | 9.0 | |||||||||||||||

| Range of Remaining Terms | Number of | Aggregate Cut- | % of Cut-off | 65.1 - 70.0 | 20 | 259,405,751 | 28.7 | ||||||||||||

| to Maturity or ARD | Mortgage | off Date Balance | Date Pool | 70.1 - 75.0 | 26 | 274,011,030 | 30.3 | ||||||||||||

| (months) | Loans | ($) | Balance | 75.1 - 76.8 | 1 | 1,497,967 | 0.2 | ||||||||||||

| 57 - 60 | 7 | $172,544,831 | 19.1% | Total: | 84 | $904,354,517 | 100.0% | ||||||||||||

| 85 - 120 | 77 | 731,809,686 | 80.9 | Weighted Average: | 62.6% | ||||||||||||||

| Total: | 84 | $904,354,517 | 100.0% | ||||||||||||||||

| Weighted Average: | 108 months | BALLOON OR ARD LOAN-TO-VALUE RATIO | |||||||||||||||||

| Number of | Aggregate Cut- | % of Cut-off | |||||||||||||||||

| ORIGINAL AMORTIZATION TERM(2) | Range of Balloon or ARD | Mortgage | off Date Balance | Date Pool | |||||||||||||||

| Range of Original | Number of | Aggregate Cut- | % of Cut-off | LTV Ratios (%) | Loans | ($) | Balance | ||||||||||||

| Amortization Terms | Mortgage | off Date Balance | Date Pool | 22.0 - 30.0 | 1 | $1,993,018 | 0.2% | ||||||||||||

| (months) | Loans | ($) | Balance | 30.1 - 35.0 | 2 | 10,994,402 | 1.2 | ||||||||||||

| Non-Amortizing | 5 | $175,600,000 | 19.4% | 35.1 - 40.0 | 5 | 94,064,079 | 10.4 | ||||||||||||

| 180 - 240 | 2 | 5,285,559 | 0.6 | 40.1 - 45.0 | 10 | 110,846,222 | 12.3 | ||||||||||||

| 241 - 300 | 22 | 144,293,097 | 16.0 | 45.1 - 50.0 | 6 | 44,095,432 | 4.9 | ||||||||||||

| 301 - 360 | 55 | 579,175,861 | 64.0 | 50.1 - 55.0 | 21 | 143,181,610 | 15.8 | ||||||||||||

| Total: | 84 | $904,354,517 | 100.0% | 55.1 - 60.0 | 21 | 190,133,930 | 21.0 | ||||||||||||

Weighted Average(3): | 346 months | 60.1 - 65.0 | 12 | 150,850,824 | 16.7 | ||||||||||||||

| (2) | The original amortization term shown for any mortgage loan that is interest-only for part of its term does not include the number of months in its interest-only period and reflects only the number of months as of the commencement of amortization remaining from the end of such interest-only period. | 65.1 - 70.1 | 6 | 158,195,000 | 17.5 | ||||||||||||||

| Total: | 84 | $904,354,517 | 100.0% | ||||||||||||||||

| Weighted Average: | 54.4% | ||||||||||||||||||

| (3) | Excludes the non-amortizing loans. | ||||||||||||||||||

| AMORTIZATION TYPE | |||||||||||||||||||

| REMAINING AMORTIZATION TERM(4) | Number of | Aggregate Cut- | % of Cut-off | ||||||||||||||||

| Range of Remaining | Number of | Aggregate Cut- | % of Cut-off | Mortgage | off Date Balance | Date Pool | |||||||||||||

| Amortization Terms | Mortgage | off Date Balance | Date Pool | Type of Amortization | Loans | ($) | Balance | ||||||||||||

| (months) | Loans | ($) | Balance | Amortizing Balloon | 63 | $468,004,017 | 51.8% | ||||||||||||

| Non-Amortizing | 5 | $175,600,000 | 19.4% | Interest-only, Amortizing | |||||||||||||||

| 179 - 240 | 2 | 5,285,559 | 0.6 | Balloon | 11 | 182,613,000 | 20.2 | ||||||||||||

| 241 - 300 | 22 | 144,293,097 | 16.0 | Interest-only, Balloon | 5 | 175,600,000 | 19.4 | ||||||||||||

| 301 - 360 | 55 | 579,175,861 | 64.0 | Interest-only, Amortizing ARD | 3 | 47,482,500 | 5.3 | ||||||||||||

| Total: | 84 | $904,354,517 | 100.0% | Amortizing ARD | 2 | 30,655,000 | 3.4 | ||||||||||||

Weighted Average(5): | 346 months | Total: | 84 | $904,354,517 | 100.0% | ||||||||||||||

| (4) | The remaining amortization term shown for any mortgage loan that is interest-only for part of its term does not include the number of months in its interest-only period and reflects only the number of months as of the commencement of amortization remaining from the end of such interest-only period. | ||||||||||||||||||

| ORIGINAL TERM OF INTEREST-ONLY PERIOD FOR PARTIAL IO LOANS | |||||||||||||||||||

| Number of | Aggregate Cut- | % of Cut-off | |||||||||||||||||

| (5) | Excludes the non-amortizing loans. | Mortgage | off Date Balance | Date Pool | |||||||||||||||

| IO Term (months) | Loans | ($) | Balance | ||||||||||||||||

| LOCKBOXES | 6 | 1 | $5,700,000 | 0.6% | |||||||||||||||

| Number of | Aggregate Cut- | % of Cut-off | 12 | 5 | 108,912,500 | 12.0 | |||||||||||||

| Mortgage | off Date Balance | Date Pool | 13 - 24 | 3 | 61,480,000 | 6.8 | |||||||||||||

| Type of Lockbox | Loans | ($) | Balance | 25 - 36 | 1 | 3,500,000 | 0.4 | ||||||||||||

| Springing (W/Out Estab. Account) | 39 | $393,198,326 | 43.5% | 37 - 48 | 1 | 23,070,000 | 2.6 | ||||||||||||

| Hard/Springing Cash Management | 18 | 311,419,011 | 34.4 | 49 - 60 | 2 | 19,843,000 | 2.2 | ||||||||||||

| Soft/Springing Cash Management | 4 | 101,252,271 | 11.2 | 61 - 84 | 1 | 7,590,000 | 0.8 | ||||||||||||

| None | 20 | 85,289,900 | 9.4 | Total: | 14 | $230,095,500 | 25.4% | ||||||||||||

| Hard/Upfront Cash Management | 2 | 9,195,009 | 1.0 | Weighted Average: | 25 months | ||||||||||||||

| Springing (With Estab. Account) | 1 | 4,000,000 | 0.4 | ||||||||||||||||

| Total: | 84 | $904,354,517 | 100.0% | SEASONING | |||||||||||||||

| Number of | Aggregate Cut- | % of Cut-off | |||||||||||||||||

| PREPAYMENT PROVISION SUMMARY | Mortgage | off Date Balance | Date Pool | ||||||||||||||||

| Number of | Aggregate Cut- | % of Cut-off | Seasoning (months) | Loans | ($) | Balance | |||||||||||||

| Mortgage | off Date Balance | Date Pool | 0 | 42 | $424,420,000 | 46.9% | |||||||||||||

| Prepayment Provision | Loans | ($) | Balance | 1 - 3 | 42 | 479,934,517 | 53.1 | ||||||||||||

| Lockout/Defeasance/Open | 79 | $810,904,210 | 89.7% | Total: | 84 | $904,354,517 | 100.0% | ||||||||||||

| Lockout/Defeasance or GRTR 1% | Weighted Average: | 1 month | |||||||||||||||||

| or YM/Open | 1 | 55,000,000 | 6.1 | ||||||||||||||||

| Lockout/GRTR 1% or YM/Open | 4 | 38,450,307 | 4.3 | ||||||||||||||||

| Total: | 84 | $904,354,517 | 100.0% | ||||||||||||||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| WFRBS Commercial Mortgage Trust 2013-C17 | Certain Terms and Conditions |

| V. | Certain Terms and Conditions | |||

| Interest Entitlements: | The interest entitlement of each Class of Offered Certificates on each Distribution Date generally will be the interest accrued during the related Interest Accrual Period on the related Certificate Principal Balance or Notional Amount at the related pass-through rate, net of any prepayment interest shortfalls allocated to that Class for such Distribution Date as described below. If prepayment interest shortfalls arise from voluntary prepayments (without Special Servicer consent) on particular non-specially serviced mortgage loans during any collection period, the Master Servicer is required to make a compensating interest payment to offset those shortfalls, generally up to an amount equal to the portion of its master servicing fees that accrue at one basis point per annum. The remaining amount of prepayment interest shortfalls will be allocated to reduce the interest entitlement on all Classes of Certificates (other than the Class X-A, X-B and Class X-C Certificates), pro rata, based on their respective amounts of accrued interest for the related Distribution Date. If a Class receives less than the entirety of its interest entitlement on any Distribution Date, then the shortfall, excluding any shortfall due to prepayment interest shortfalls, will be added to its interest entitlement for the next succeeding Distribution Date. Interest entitlements on the Class E, D, C and B Certificates, in that order, may be reduced by certain Trust Advisor expenses. | |||

Principal Distribution Amount: | The Principal Distribution Amount for each Distribution Date generally will be the aggregate amount of principal received or advanced in respect of the mortgage loans, net of any non-recoverable advances and interest thereon that are reimbursed to the Master Servicer, the Special Servicer or the Trustee during the related collection period. Non-recoverable advances and interest thereon are reimbursable from principal collections and advances before reimbursement from other amounts. The Principal Distribution Amount may also be reduced, with a corresponding loss, to the Class E, D, C, B and A-S Certificates, then to the Class A-1, A-2, A-3, A-4 and A-SB Certificates (with any losses on the Class A-1, A-2, A-3, A-4 and A-SB Certificates allocated pro rata according to their respective Certificate Principal Balances immediately prior to that Distribution Date), in that order, in connection with certain Trust Advisor expenses to the extent that interest entitlements on the Class B, C, D and E Certificates are insufficient to absorb the effect of the expense on any particular Distribution Date. | |||

| Distributions: | On each Distribution Date, funds available for distribution from the mortgage loans, net of specified trust fees, expenses and reimbursements will generally be distributed in the following amounts and order of priority (in each case to the extent of remaining available funds): | |||

| 1. | Class A-1, A-2, A-3, A-4, A-SB, X-A, X-B and X-C Certificates: To interest on the Class A-1, A-2, A-3, A-4, A-SB, X-A, X-B and X-C Certificates, pro rata, according to their respective interest entitlements. | |||