INVESTMENT MANAGERS SERIES TRUST II

235 W. Galena Street

Milwaukee, Wisconsin 53212

VIA EDGAR

September 30, 2022

U.S. Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549

Attention: Division of Investment Management

| Re: | Investment Managers Series Trust II (the “Registrant”) on behalf of the AXS Brendan Wood TopGun Index ETF |

Ladies and Gentlemen:

This letter summarizes the comments provided to me by Mr. David Orlic of the staff of the Securities and Exchange Commission (the “Commission”) by telephone on September 12, 2022, regarding Post-Effective Amendment No. 336 to the Registrant’s registration statement filed on Form N-1A (the “Registration Statement”) relating to the AXS Brendan Wood TopGun Index ETF (the “Fund”), a newly-created series of the Trust.

Responses to all of the comments are included below and, as appropriate, will be incorporated into a Post-Effective Amendment (the “Amendment”) filing that will be filed separately. Capitalized terms not otherwise defined in this letter have the meanings assigned to them in the Registration Statement.

GENERAL

| 1. | Please provide the Registrant’s written responses to the Commission for review at least five business days prior to the filing of the Amendment. |

| Response: The Registrant will provide the responses to the Commission for review in advance, as requested. |

| 2. | If the Index has disclosed performance information publicly, please provide to the Commission for review. |

| Response: The Index was reported on Bloomberg by Indxx, LLC, an independent index tracking firm (see Exhibit A attached). This tracking firm discontinued its index tracking services to external firms in September 2021. Brendan Wood has not published any performance information for the Index. |

1

SUMMARY SECTION

Principal Investment Strategies

| 3. | The staff notes that the Fund’s “Principal Investment Strategies” section states the following: |

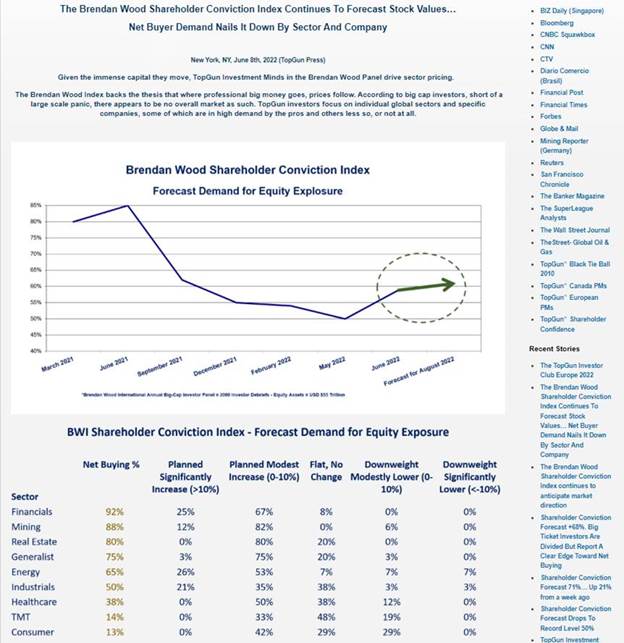

| Construction of the Index begins with the approximately 1,400 companies in the Brendan Wood Shareholder Conviction Index (the “Shareholder Conviction Universe”), generally stocks of liquid large and mid-capitalization companies (with market capitalizations of $2 billion or greater) that trade on a national exchange in the United States, including American Depositary Receipts (“ADRs”). The Shareholder Conviction Universe is the product of up to 2,000 personal interviews with institutional investment professionals conducted during the calendar year by Brendan Wood. The personal interviews with the institutional investment professionals generate data that is used by Brendan Wood to (1) establish the quality of companies in the Shareholder Conviction Universe and then rate and rank the companies based on multiple investment attributes discussed by the investment professionals and (2) forecast demand of the nine Shareholder Conviction Universe sectors (i.e., financials, mining, real estate, generalist, energy, industrials, healthcare, technology media and telecom (“TMT”), and consumer). |

| a) | Please explain how the 2,000 personal interviews are conducted each year and please provide some examples of the professional institutional investment professionals who are interviewed. |

| b) | With respect to the forecast demand discussed in (2) please explain what this means in plain English and how the Advisor determines the level of forecast demand for each of the sectors. |

| c) | Are (1) and (2) equally weighted? Then with respect to (1), are the investment attributes equally weighted, and with respect to (2), are the sectors equally weighted? |

Response:

a and b), Brendan Wood’s long-standing primary business is a fee for service consulting franchise assisting public companies and broker dealers to enhance their relationships with investors. In this connection, a shareholder confidence survey was developed to provide information services to Brendan Wood’s clients. The interviews (surveys) conducted by Brendan Wood are conducted telephonically by Brendan Wood’s sector specialized personnel. The institutional investment professionals (referred to as the Brendan Wood Shareholder Confidence Panel (the “BWI Panel”)) include financial services companies and registered investment advisory firms. All institutional investment professionals in the BWI Panel are categorized as the Global Panel. Global Resources Panel members are a sub group of the Global Panel (i.e., BWI Panel). All BWI Panel members receive the same interview questions. The questions in these interviews are designed to generate data used by Brendan Wood to establish the quality of companies in the Shareholder Conviction Universe and then rate and rank those companies based on the investment attributes discussed in the interviews. These interviews also seek information regarding nine business sectors (financials, mining, real estate, generalist, energy, industrials, healthcare, technology media and telecom, and consumer) in which the institutional investment professionals intend to increase their exposure. Forecasts for the demand for each of these sectors is determined based on the responses by the BWI Panel. Companies identified with the highest investment quality ratings are selected for inclusion in the Index provided that the company is in a business sector identified by the BWI Panel as having the highest demand. (See Exhibit B regarding the BWI Panel, Exhibit C regarding the overall process and Exhibit D regarding the sector forecast).

c) The investment quality rankings of the companies and the forecast demand of the sectors are not equally weighted. First, a company must be identified with a high investment quality rating and second, that top rated company must be in a higher demand business sector. For example, if a company’s investment attributes give it a high investment quality ranking and such company is also in a sector that has been identified as one that is in high demand, such company (i.e., a TopGun company) may be selected for inclusion in the Index, provided the algorithm places it at the highest level.

2

With respect to the investment quality metrics, including each company’s business strategy, long-term and short-term performance, executive and senior management, governance (including the company’s environmental, social and governance (“ESG”) practices), reporting and disclosure, balance sheet, commitment to own, momentum and price appreciation, these metrics are not equally weighted; however, they are rated the same from one company to the next. For example, the weighting assigned to “Quality of CEO” is assigned the same weight at each company. The sectors forecast to be in demand are identified by net weight of demand for exposure.

The disclosure has been revised as follows:

Construction of the Index begins with the identification of approximately 1,400 companies composing inthe Brendan Wood “Shareholder Conviction Universe”, which are generally stocks of liquid large and mid-capitalization companies (with market capitalizations of $2 billion or greater) that trade on a national exchange in the United States, including American Depositary Receipts (“ADRs”). Companies included in the The Shareholder Conviction Universe are evaluated based on the results of is the product ofup to 2,000 personal interviews with institutional investment professionals, including large financial services companies and advisory firms, conducted by Brendan Wood conductedduring the calendar yearby Brendan Wood.The personal These interviews withthe institutional investment professionals are designed to generate data that is used by Brendan Wood to(1) establish the quality of companies in the Shareholder Conviction Universe and then rate and rank the companies based on multiple investment attributes discussed. These interviews include questions regarding various investment quality metrics, including each company’s business strategy, long-term and short-term performance, executive and senior management, governance (including the company’s environmental, social and governance (“ESG”) practices), reporting and disclosure, balance sheet, commitment to own, momentum and price appreciation. These interviews also seek information regarding sectors in which the institutional investment professionals intend to increase their investment exposure. From these responses, Brendan Wood by the investment professionals and (2)forecasts the demand of the nine Shareholder Conviction Universe sectors (i.e., financials, mining, real estate, generalist, energy, industrials, healthcare, technology media and telecom (“TMT”), and consumer). Those companies that are identified with the highest investment quality ratings and are in high demand sectors are algorithmically selected for inclusion in the Index (collectively, “TopGun companies”). The Index contains approximately 25 TopGun companies.

The Index contains approximately 25 companies. The algorithm of the Index automatically selects for inclusion those companies to which Brendan Wood attributes (1) the highest ratings across all investment quality metrics, such as business strategy, long-term and short-term performance, executive and senior management, governance including environmental, social and governance (“ESG”) practices, reporting and disclosure, balance sheet, commitment to own, momentum, and price appreciation, and (2) the highest demand ratings in the Shareholder Conviction Universe sector of their principal business(es) (collectively, “TopGun companies”).

3

| 4. | The staff notes that the Fund’s “Principal Investment Strategies” section states “[t]he Index contains approximately 25 companies. The algorithm of the Index automatically selects for inclusion those companies to which Brendan Wood attributes (1) the highest ratings across all investment quality metrics, such as business strategy, long-term and short-term performance, executive and senior management, governance including environmental, social and governance (“ESG”) practices, reporting and disclosure, balance sheet, commitment to own, momentum, and price appreciation, and (2) the highest demand ratings in the Shareholder Conviction Universe sector of their principal business(es) (collectively, “TopGun companies”).” |

| a) | Please explain the relevant importance of “investment quality metrics” versus “demand ratings” in selecting companies. Are they equally weighted and do those companies with the highest aggregate scores get included in the Index? Is there a limit on the number of companies that come from one sector? Are these investment quality metrics equally weighted in arriving at the ratings? If so, please disclose. |

| b) | Please disclose in the Item 9 disclosure the Fund’s definition of ESG and specific ESG areas of focus and criteria considered. |

| c) | Please also disclose in Item 9 whether the Fund selects investments by reference to, for example, (i) an ESG index, (ii) ESG scores or data from a third-party rating organization, (iii) a proprietary screen and the factors the screen applies, or (iv) a combination of the above methods. |

| Response: a) As noted above in the response to comment #3, a company must first be identified based on its high investment quality metrics and then, second, be in a sector that has been identified by the BWI Panel as high demand. If a company’s investment attributes give it a high investment quality ranking and such company is also in a sector that has been identified as one that is in demand (i.e., the TopGun companies), such company will be selected for inclusion in the Index. The investment quality metrics identified (as noted in the response to comment #3) are not equally weighted; however, they are rated the same from one company to the next. The TopGun companies included in the Index generally represent the top 2% of the Shareholder Conviction Universe. |

| b and c) The interview questions received by the BWI Panel include questions regarding a company’s ESG practices and is one of several investment quality metrics evaluated by the BWI Panel. As the Fund’s strategy is a replication strategy, the advisor is not making any separate ESG considerations with respect to the Fund’s investments; therefore, no additional disclosure has been added to the Fund’s “Principal Investment Strategies.” |

| 5. | The principal investment strategy disclosure appears to describe a quantitative investment strategy being run by Brendan Wood based on individual investment determinations. Please advise how you determined it is appropriate to characterize this as an index given the amount of discretion the provider has with respect to Index constitution. |

| Response: As noted in the response to comment #3 above, a company’s selection into the Index is based on an algorithm based on scores and rankings of the companies in the Shareholder Conviction Universe and sector demand. As the TopGun companies are identified based upon an algorithm, there is no subjective judgment or opinion applied by Brendan Wood regarding the companies identified as a TopGun company. |

4

| 6. | Since the Fund is following a replication strategy and since Brendan Wood seems to be the primary party selecting companies for the Index, please explain why Brendan Wood should not be considered an investment advisor to the Fund. |

Response: As noted in the responses above, a company’s selection into the Index is based on an algorithm based on scores and rankings of the companies in the Shareholder Conviction Universe and sector demands. The TopGun companies are identified based upon an algorithm. There are no subjective determinations by Brendan Wood. Brendan Wood is not an investment adviser because it does not advise the Fund as to the advisability of investing in, purchasing, or selling securities, nor does it have the authority to make investment decisions for the Fund.

| 7. | The disclosure states that the Brendan Wood TopGun Index will contain 25 companies. Please enhance the disclosure on how exchange traded funds (“ETFs”) will be used to gain exposure to this select, limited group of companies. Also, please consider whether an acquired fund fees and expenses line item is necessary for the Fund’s fees and expenses table. |

Response: The Fund’s advisor does not intend to invest in ETFs as part of its principal investment strategies; therefore, this disclosure has been removed from the “Principal Investment Strategies.” The Registrant confirms that it has considered whether an Acquired Fund Fees and Expenses line is required based on the fees and expenses for the first year of operations and has determined that this caption is not required.

| 8. | Please disclose if the Index is currently concentrated and if so, please disclose. |

Response: The Registrant confirms that the Index is not currently concentrated in any industry or group of industries, but rather is focused in particular sectors of the Shareholder Conviction Universe. It is anticipated that at the Fund’s inception the Index will invest significant portions in the following Shareholder Conviction Universe sectors: financial, mining and real estate. The Fund has revised the following disclosure:

To the extent the Index concentrates (i.e., holds more than 25% of its total assets) in the securities of a particular industry, the Fund will concentrate its investments to approximately the same extent as the Index. In addition, to the extent the Index focuses on particular sectors, the Fund intends to focus on the same sectors. As of the date of this Prospectus, the Index is focused in the following Shareholder Conviction Universe sectors: financial, real estate and mining. As of the date of this Prospectus, the Index is not concentrated in any particular industries.

In addition, the Fund has removed “Concentration Risk” and replaced it with “Sector Focus Risk” in the Fund’s “Principal Risks” section:

Sector Focus Risk. The Fund may invest a significant portion of its assets in one or more sectors and thus will be more susceptible to the risks affecting those sectors. While the Fund’s sector exposure is expected to vary over time based on the composition of the Index, the Fund anticipates that it may be subject to the risks associated with the financial, mining and real estate sectors.

| · | Financial Sector Risk. Performance of companies in the financial sector may be adversely impacted by many factors, including, among others: government regulations of, or related to, the sector; governmental monetary and fiscal policies; economic, business or political conditions; credit rating downgrades; changes in interest rates; price competition; and decreased liquidity in credit markets. This sector has experienced significant losses and a high degree of volatility in the recent past, and the impact of more stringent capital requirements and of recent or future regulation on any individual financial company or on the sector as a whole cannot be predicted. |

5

| · | Mining Sector Risk. The exploration and development of mineral deposits involve significant financial risks over a significant period of time, which even a combination of careful evaluation, experience and knowledge may not eliminate. Few properties which are explored are ultimately developed into producing mines. Major expenditures may be required to establish reserves by drilling and to construct mining and processing facilities at a site. In addition, mineral exploration companies typically operate at a loss and are dependent on securing equity and/or debt financing, which might be more difficult to secure for an exploration company than for a more established counterpart. |

| · | Real Estate Sector Risk. Performance of companies in the real estate sector may be adversely impacted by many factors, including, among others: increasing vacancies or declining rents resulting from unanticipated economic, legal, employment, cultural or technological developments; fluctuations in rent schedules and operating expenses; unfavorable changes in applicable taxes; governmental regulations, zoning, building, environmental and other laws and interest rates; operating or development expenses; unexpected increases in the cost of energy and environmental factors; and lack of available financing. In addition, local, regional or global events such as war, acts of terrorism, the spread of infectious illness or other public health issues, or other events could have a significant impact on the real estate sector. The value of real estate company securities also may decline because of the failure of borrowers to pay their loans and poor property management. Residential developers, in particular, could be negatively impacted by falling home prices, slower mortgage origination and rising construction costs. |

| 9. | The staff noted that the “Principal Investment Strategies” states “[w]hen the algorithm determines that a TopGun company’s investment score or sector demand of its principal business has decreased to a level beneath the ratings threshold established by Brendan Wood, the company will be sold and removed from the Fund’s portfolio. The proceeds from such sale are invested in other TopGun companies. In the event that no new TopGun companies are identified, the proceeds from such sale will be invested in U.S. government securities, corporate bonds that are rated investment grade at time of purchase, money market instruments, and/or cash.” Please reconcile this language with the language contained in the methodology disclosure provided to the staff. |

Response: The Registrant has revised the disclosure as follows:

When the algorithm for the Index determines that a TopGun company’s investment score or sector demand of its principal business has decreased to a level beneath the ratings threshold established in the algorithm, the company will besold and removed from the Index.Fund’s portfolio. The proceeds that woud have been generated from any such sale are allocated to invested in other TopGun companies, as determined by the algorithm. In the event that no more than 15 companies meet the Index’s selection criteria at any time, the Index will reflect allocations tonew TopGun companies are identified, the proceeds from such sale will be invested in cash, fixed income securities, including U.S. government securities, corporate bonds that are rated investment grade at time of purchase, and money market instruments, and/or exchange-traded funds (“ETFs”) that invest in large cap companies until a new TopGun company is identified, and/or cash.

6

Principal Risks

| 10. | Please add to “ETF Structure Risks” that, in stressed market conditions, the market for an ETF’s shares may become less liquid in response to deteriorating liquidity in the markets for the ETF’s underlying portfolio holdings, and that this could lead to wider bid/ask spreads and differences between the market price of the ETF’s shares and NAV. |

Response: The Registrant has added the following disclosure:

| · | Fluctuation of Net Asset Value Risk. As with all ETFs, shares may be bought and sold in the secondary market at market prices. Although it is expected that the market prices of shares will approximate the Fund’s NAV, there may be times when the market prices of shares is more than the NAV intra-day (premium) or less than the NAV intra-day (discount). Differences in market price and NAV may be due, in large part, to the fact that supply and demand forces at work in the secondary trading market for shares will be closely related to, but not identical to, the same forces influencing the prices of the holdings of the Fund trading individually or in the aggregate at any point in time. These differences can be especially pronounced during times of market volatility or stress. During these periods, the demand for Fund shares may decrease considerably and cause the market price of Fund shares to deviate significantly from the Fund’s NAV. In addition, the market for the Fund’s shares may become less liquid in response to deteriorating liquidity in the markets for the Fund’s underlying portfolio holdings, and this could lead to wider bid/ask spreads and differences between the market price of the Fund’s shares and NAV. |

| 11. | Please revise the “Index Provider Risk” disclosure to indicate the relative inexperience of the Index Provider. |

Response: The Registrant has revised the disclosure as follows:

Index Provider Risk. Brendan Wood, the Fund’s Index Provider, developed the Brendan Wood TopGun Index in 2010. There is no assurance that the Index Provider, or any agents that act on its behalf, will compile the Index accurately, or that the Index will be determined, maintained, constructed, reconstituted, rebalanced, composed, calculated or disseminated accurately. Any losses or costs associated with errors made by the Index Provider or its agents generally will be borne by the Fund and its shareholders.

MORE INFORMATION ABOUT THE FUND’S INVESTMENT OBJECTIVE, PRINCIPAL INVESTMENT STRATEGIES AND RISKS

Principal Investment Strategies

| 12. | Apply all applicable comments from the summary section for the Fund to Item 9 of Form N-1A. |

Response: The Registrant confirms that all applicable comments have been applied to this section of the Prospectus.

7

PART C

| 13. | The Registrant should include any index license or sub-license agreement to which the Fund is a party as an exhibit to the registration statement, if applicable, as it is considered an “other material contract” pursuant to Item 28(h) of Form N-1A. |

Response: The Advisor’s ability to use the Index in connection with the Fund will be addressed in the license agreement between the Advisor and the Index Provider. The Fund is not party to a sub-license agreement with the Adviser. Accordingly, no sub-license agreement will be filed as an exhibit.

* * * * *

The Registrant believes that it has fully responded to each comment. If, however, you have any further questions or required further clarification of any response, please contact me at (626) 385-5777. I may also be reached at diane.drake@mfac-ca.com.

Sincerely,

/s/ Diane J. Drake

Diane J. Drake

Secretary

8

Exhibit A

Exhibit B – The Brendan Wood Shareholder Confidence Panel (“BWI Panel”)

9

Exhibit C

10

Exhibit D

11