Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22906

Virtus Alternative Solutions Trust

(Exact name of registrant as specified in charter)

101 Munson Street

Greenfield, MA 01301

(Address of principal executive offices) (Zip code)

Jennifer Fromm, Esq.

Vice President, Chief Legal Officer, Counsel and Secretary for Registrant

100 Pearl Street

Hartford, CT 06103-4506

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800)-243-1574

Date of fiscal year end: October 31

Date of reporting period: October 31, 2014

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Table of Contents

ANNUAL REPORT

Virtus Alternative Income Solution Fund

Virtus Alternative Inflation Solution Fund

Virtus Alternative Total Solution Fund

Virtus Strategic Income Fund

Table of Contents

Proxy Voting Procedures and Voting Record (Form N-PX)

The subadvisers vote proxies relating to portfolio securities in accordance with procedures that have been approved by the Board of Trustees of the Trust (“Trustees”, or the “Board”). You may obtain a description of these procedures, along with information regarding how the Funds voted proxies during the most recent 12-month period ended June 30, free of charge, by calling toll-free 1-800-243-1574. This information is also available through the Securities and Exchange Commission’s (the “SEC”) website at http://www.sec.gov.

Form N-Q Information

The Trust files a complete schedule of portfolio holdings for each Fund with the SEC for the first and third quarters of each fiscal year on Form N-Q. Form N-Q is available on the SEC’s website at http://www.sec.gov. Form N-Q may be reviewed and copied at the SEC’s Public Reference Room. Information on the operation of the SEC’s Public Reference Room can be obtained by calling toll-free 1-800-SEC-0330.

This report is not authorized for distribution to prospective investors in the Funds presented in this book unless preceded or accompanied by an effective prospectus which includes information concerning the sales charge, each Fund’s record and other pertinent information.

Table of Contents

Dear Fellow Shareholders of Virtus Mutual Funds:

| I am pleased to present this first annual shareholder report of Virtus Alternative Solutions Trust, which comprises four alternative mutual funds. These are the Virtus Alternative Solutions Funds, introduced in April 2014 and subadvised by Cliffwater Investments LLC, and a new fund, Virtus Strategic Income Fund, introduced in September 2014 and subadvised by Newfleet Asset Management. This report contains portfolio commentary for the three funds that have been in existence for more than six months, as well as a listing of each fund’s investments and audited financial statements for the period ended October 31, 2014. |

The current market environment may pose challenges to investors. A traditional core portfolio consisting of equity and fixed income allocations may no longer be sufficient to deliver, on an aggregate basis, inflation-beating returns over time. This far into a bull market, many investors may be reluctant to increase their equity exposure. At the same time, with interest rates at historic lows, traditional fixed income may not offer the return potential many investors need to meet their long-term financial goals.

Alternative investments, which include asset classes such as hedge funds, private equity, and real assets, are attractive to many investors because historically they have not correlated with traditional asset classes. Historically, an allocation to alternative strategies has helped to mitigate volatility and generate more consistent returns in diversified portfolios. Large institutional investors, such as pension funds, have been diversifying with alternative investments for years.

Market uncertainty is an ever-present reminder of the importance of portfolio diversification. While diversification cannot guarantee a profit or prevent loss, owning a variety of asset classes may cushion your portfolio against inevitable market fluctuations. Incorporating alternative investments has been a time-tested approach to reduce portfolio volatility and generate more consistent results through market cycles. Your financial advisor can help you ensure that your portfolio is adequately diversified across asset classes and investment strategies.

Thank you for choosing to invest with Virtus. We appreciate the opportunity to serve you and look forward to supporting your investment needs in the year to come. Should you have questions or require assistance, our customer service team is here to help at 1-866-270-7788.

| Sincerely, |

|

George R. Aylward |

| President, Virtus Mutual Funds |

| December 2014 |

Whenever you have questions about your account, or require additional information, please visit us on the Web at www.virtus.com or call our shareowner service group toll-free at 1-800-243-1574.

Performance data quoted represents past results. Past performance is no guarantee of future results.

1

Table of Contents

VIRTUS ALTERNATIVE SOLUTIONS TRUST

Disclosure of Fund Expenses

For the period ended October 31, 2014

We believe it is important for you to understand the impact of costs on your investment. All mutual funds have operating expenses. As a shareholder of a Virtus Alternative Solutions Trust Fund (each, a “Fund”) you may incur two types of costs: (1) transaction costs, including sales charges on purchases of Class A shares and contingent deferred sales charges on Class A and Class C shares; and (2) ongoing costs, including investment advisory fees, distribution and service fees, and other expenses. Class I shares are sold without sales charges. For further information regarding applicable sales charges, see Note 1 in the Notes to Financial Statements. These examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. These examples are based on an investment of $1,000 invested from May 1, 2014 through October 31, 2014, and held for the entire period. The following Expense Table illustrates your Fund’s costs in two ways.

Actual Expenses

The first section of the accompanying table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your Fund under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second section of the accompanying table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not your Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the accompanying table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges or contingent deferred sales charges. Therefore, the second section of the accompanying table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

| Expense Table | ||||||||||||||||

Beginning Account Value May 1, 2014 | Ending Account Value October 31, 2014 | Annualized Expense Ratio* | Expenses Paid Period** | |||||||||||||

Virtus Alternative Income Solution Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $1,000.00 | $1,017.18 | 2.66% | $13.52 | ||||||||||||

Class C | 1,000.00 | 1,013.80 | 3.41 | 17.31 | ||||||||||||

Class I | 1,000.00 | 1,017.96 | 2.43 | 12.36 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | $1,000.00 | $1,011.63 | 2.66% | $13.58 | ||||||||||||

Class C | 1,000.00 | 1,007.80 | 3.41 | 17.41 | ||||||||||||

Class I | 1,000.00 | 1,012.80 | 2.43 | 12.40 | ||||||||||||

Virtus Alternative Inflation Solution Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $1,000.00 | $1,011.00 | 2.69% | $13.65 | ||||||||||||

Class C | 1,000.00 | 1,007.00 | 3.46 | 17.50 | ||||||||||||

Class I | 1,000.00 | 1,012.00 | 2.47 | 12.53 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | $1,000.00 | $1,011.46 | 2.69% | $13.75 | ||||||||||||

Class C | 1,000.00 | 1,007.55 | 3.46 | 17.66 | ||||||||||||

Class I | 1,000.00 | 1,012.60 | 2.47 | 12.61 | ||||||||||||

Virtus Alternative Total Solution Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $1,000.00 | $1,014.97 | 3.02% | $15.33 | ||||||||||||

Class C | 1,000.00 | 1,010.98 | 3.76 | 19.06 | ||||||||||||

Class I | 1,000.00 | 1,015.97 | 2.77 | 14.08 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | $1,000.00 | $1,009.80 | 3.02% | $15.41 | ||||||||||||

Class C | 1,000.00 | 1,006.01 | 3.76 | 19.19 | ||||||||||||

Class I | 1,000.00 | 1,011.07 | 2.77 | 14.14 | ||||||||||||

Virtus Strategic Income Fund*** |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $1,000.00 | $996.74 | 1.40% | $1.99 | ||||||||||||

Class C | 1,000.00 | 995.71 | 2.15 | 3.06 | ||||||||||||

Class I | 1,000.00 | 997.10 | 1.15 | 1.64 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | $1,000.00 | $1,018.06 | 1.40% | $7.15 | ||||||||||||

Class C | 1,000.00 | 1,014.23 | 2.15 | 10.97 | ||||||||||||

Class I | 1,000.00 | 1,019.34 | 1.15 | 5.87 | ||||||||||||

| * | Annualized expense ratios include dividends on short sales. |

| ** | Expenses are equal to the relevant Fund’s annualized expense ratio, which is net of waived fees and reimbursed expenses, if applicable, multiplied by the average account value over the period, multiplied by the number of days (184) expenses were accrued in the most recent fiscal half-year, then divided by 365 to reflect the one half-year period. |

| *** | September 10, 2014 is the date the Fund started accruing expenses. Expenses are equal to the relevant Fund’s annualized expense ratio, which is net of waived fees and reimbursed expenses, if applicable, multiplied by the average account value over the period, multiplied by the number of days (52 for actual and 184 for hypothetical) expenses were accrued in the most recent fiscal half-year, then divided by 365 to reflect the one half-year period. |

For Funds which may invest in other funds, the annualized expense ratios noted above do not reflect fees and expenses associated with the underlying funds. If such fees and expenses had been included, the expenses would have been higher.

You can find more information about the Funds’ expenses in the Financial Statements section that follows. For additional information on operating expenses and other shareholder costs, refer to the prospectus.

| 2 |

Table of Contents

ADR (American Depositary Receipt)

Represents shares of foreign companies traded in U.S. dollars on U.S. exchanges that are held by a U.S. bank or a trust. Foreign companies use ADRs in order to make it easier for Americans to buy their shares.

Alerian MLP Index

The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships (MLPs) that provides investors with an unbiased, comprehensive benchmark for this emerging asset class. The index, which is calculated using a float-adjusted, capitalization-weighted methodology, is disseminated real-time on a price-return basis (NYSE: AMZ) and on a total-return basis (NYSE:AMZX). The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Barclays U.S. Aggregate Bond Index

The Barclays U.S. Aggregate Bond Index measures the U.S. investment grade fixed rate bond market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Barclays U.S. Treasury Inflation Protected Securities (TIPS) Index

The Barclays U.S. TIPS Index includes all publicly issued, U.S. Treasury inflation-protected securities that have at least one year remaining to maturity, are rated investment grade, and have $250 million or more of outstanding face value. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Barclays U.S. 10 year Breakeven Inflation Index

The Barclays U.S. 10 Year breakeven inflation benchmark index provides exposure to U.S. Breakeven Inflation, which are inflation expectations implied by the difference between nominal treasury securities and Treasury Inflation Protected Securities. The index is unmanaged and it is not available for direct investment.

Bloomberg Commodity Index

The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for commodities investments. It provides broad-based exposure to commodities as an asset class, since no single commodity or commodity sector dominates the Index. Rather than being driven by micro-economic events affecting one commodity market or sector, the diversified commodity exposure of BCOM potentially reduces volatility in comparison to non-diversified commodity baskets. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

BofA Merrill Lynch U.S. Dollar 3-Month LIBOR Constant Maturity Index

The BofA Merrill Lynch U.S. Dollar 3-Month LIBOR Constant Maturity Index is based on the assumed purchase of a synthetic instrument having 3 months to maturity and with a coupon equal to the closing quote for 3-Month LIBOR. That issue is sold the following day (priced at a yield equal to the current day closing 3-Month LIBOR rate) and is rolled into a new 3-Month instrument. The index, therefore, will always have a constant maturity equal to exactly 3 months. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Collateralized Loan Obligation (CLO)

A security backed by a pool of debt, often low-rated corporate loans.

Exchange–Traded Funds (ETF)

Portfolios of stocks or bonds that track a specific market index.

Exchange–Traded Notes (ETN)

Senior, unsecured, unsubordinated debt securities whose returns are linked to the performance of a particular market benchmark or strategy minus applicable fees.

3

Table of Contents

KEY INVESTMENT TERMS (Continued)

Federal Farm Credit Bank (FFCB)

Institution backed by the government to manage and merge the financing transactions of the Federal Intermediate Credit Banks and the Federal Land Banks. The institution must abide by rules set forth in the Farm Credit Act, which are enforced by an independent federal regulatory agency.

Federal Home Loan Bank (FHLB)

One of 12 regional banks that comprise the Federal Home Loan Bank System (FHLBank System). The FHLBank System provides stable, on-demand, low-cost funding to American financial institutions (not individuals) for home mortgage loans, small business, rural, agricultural, and economic development lending.

Federal Home Loan Mortgage Company (FHLMC)

A public government-sponsored enterprise which buys mortgages on the secondary market, pools them and sells them as mortgage-backed securities to investors on the open market. Monthly principal and interest payments are guaranteed by FHLMC but not by the U.S. Government. Also called Freddie Mac.

Federal National Mortgage Association (FNMA)

A congressionally chartered corporation which buys mortgages on the secondary market, pools them and sells them as mortgage-backed securities to investors on the open market. Monthly principal and interest payments are guaranteed by FNMA but not by the U.S. Government. Also called Fannie Mae.

Federal Reserve (the “Fed”)

The central bank of the United States, responsible for controlling the money supply, interest rates and credit with the goal of keeping the U.S. economy and currency stable. Governed by a seven-member board, the system includes 12 regional Federal Reserve Banks, 25 branches and all national and state banks that are part of the system.

FTSE NAREIT All Equity REITs Index

The FTSE NAREIT Equity REITs Index is a free-float market capitalization-weighted index containing all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property that also meet minimum size and liquidity criteria. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Global Depositary Receipt (GDR)

A negotiable certificate held in the bank of one country representing a specific number of shares of a stock traded on an exchange of another country. Global Depositary Receipts make it easier for individuals to invest in foreign companies, due to the widespread availability of price information, lower transaction costs, and timely dividend distributions.

HFRX Fixed Income–Credit Index

The HFRX Fixed Income–Credit Index includes strategies with exposure to credit across a broad continuum of credit sub-strategies, including corporate, sovereign, distressed, convertible, asset backed, capital structure arbitrage, multi-strategy, and other relative value and event driven sub-strategies. The investment thesis across all strategies is predicated on realization of a valuation discrepancy between the related credit instruments. Strategies may also include and utilize equity securities, credit derivatives, government fixed income, commodities, currencies, or other hybrid securities. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

HFRX Global Hedge Fund Index

The HFRX Global Hedge Fund Index is designed to be representative of the overall composition of the hedge fund universe. It is comprised of all eligible hedge fund strategies, including but not limited to, convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage, and relative value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Intercontinental Exchange (ICE)

An American network of exchanges and clearing houses for financial and commodity markets.

4

Table of Contents

KEY INVESTMENT TERMS (Continued)

iShares®

Represents shares of an open-end exchange-traded fund.

London Interbank Offered Rate (LIBOR)

A benchmark rate that some of the world’s leading banks charge each other for short-term loans.

Master Limited Partnership (MLP)

Investment which combines the tax benefits of a limited partnership with the liquidity of publicly traded securities. To be classified as an MLP, a partnership must derive most of its cash flows from real estate, natural resources and commodities.

MSCI EAFE® Index

The MSCI EAFE® Index is a free float-adjusted market capitalization-weighted index that measures developed foreign market equity performance, excluding the U.S. and Canada. The index is calculated on a total return basis with gross dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

MSCI Emerging Markets Index

The MSCI Emerging Markets Index is a free float-adjusted market capitalization-weighted index designed to measure equity market performance in the global emerging markets. The index is calculated on a total return basis with gross dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Over–the–Counter (OTC)

Trading that is done directly between two parties, without any supervision of an exchange.

Payment–in–Kind Security (PIK)

A bond which pays interest in the form of additional bonds, or preferred stock which pays dividends in the form of additional preferred stock.

Real Estate Investment Trust (REIT)

A publicly traded company that owns, develops and operates income-producing real estate such as apartments, office buildings, hotels, shopping centers and other commercial properties.

Russell 2000® Index

The Russell 2000® Index is a market capitalization-weighted index that measures the performance of the smallest 2,000 companies in the Russell Universe which comprises the 3,000 largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

S&P 500® Index

The S&P 500® Index is a free-float market capitalization-weighted index of 500 of the largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges, and it is not available for direct investment.

Standard & Poor’s Depositary Receipt (SPDR)

Shares of a security designed to track the value of the S&P 500® Index. SPDRs trade on the American Stock Exchange under the symbol SPY. One SPDR unit is valued at approximately one-tenth of the value of the S&P 500® Index. Dividends are distributed quarterly, and are based on the accumulated stock dividends held in trust, less any expenses of the trust.

UBS Global Infrastructure/Utilities 50/50 Index

The UBS Global Infrastructure/Utilities 50/50 Index is a derivative of the UBS Developed Infrastructure & Utilities Index. The infrastructure sector and the utilities sector each have a 50% weighting in terms of free-float market capitalization, which removes the skew towards utilities found in the UBS Developed Infrastructure & Utilities Index. Constituents of the index are all listed in developed markets. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges, and it is not available for direct investment.

5

Table of Contents

Alternative Income Solution Fund

Fund Summary | Ticker Symbols: Class A: VAIAX Class C: VAICX Class I : VAIIX |

| ¢ | The Fund is non-diversified and has an investment objective of maximizing current income while considering capital appreciation. |

| ¢ | For the fiscal period April 23, 2014 (inception date) through October 31, 2014, the Fund’s Class A shares at NAV returned 1.82%*, Class C shares returned 1.38%*, and Class I shares returned 1.90%*. For the same period, the HFRX Fixed Income–Credit Index, which serves as the broad-based and style-specific benchmark index appropriate for comparison, returned -1.88%*. |

| * | Returns less than 1 year are not annualized. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above.

How did the markets perform during the Fund’s partial fiscal year?

| ¢ | Most global equity markets saw strong performance during the Fund’s partial fiscal year, from its inception date of April 23, 2014 through October 31, 2014. The S&P 500® Index, which measures the performance of large company stocks, finished the period up 9.02% and saw a number of new closing highs. In contrast, the Russell 2000® Index, a metric of small-cap stock performance, returned 0.77%, showing the dispersion of returns between large- and small-cap stocks. Non-U.S. stocks in developed markets did not perform well, with the MSCI EAFE® Index returning -3.17% for the partial fiscal year due to European stocks being down 6.49%. Emerging market stocks, as measured by the MSCI Emerging Markets Index, ended the period up 4.08%. The partial fiscal year saw a flurry of corporate merger activity, including Twenty-First Century Fox’s $80 billion offer for Time Warner, online real estate company Zillow’s $2.6 billion bid for Trulia, and speculation regarding a number of potential tax inversion deals. A highlight in September was the initial public offering (“IPO”) of Alibaba, the China-based e-commerce giant, whose blockbuster public debut at $21.8 billion was the largest U.S. IPO ever. |

| ¢ | The economic divergence among the United States, the United Kingdom, the eurozone, and |

Japan has become increasingly stark, and markets were heavily dominated by remarks from their central banks over the partial fiscal year. The timing of any Federal Reserve interest rate increase remains an issue of strong debate. While hawks argue that the interest rate cycle should be normalized before creating another bubble, the doves argue the economy is not yet strong enough to stand on its own. Geopolitical instability in Ukraine, the Middle East, a widening war against ISIS, protests in Hong Kong, the Ebola scare, as well as Argentina’s selective default, dominated headlines. New sanctions imposed by the U.S. and EU on Russia ushered in the winds of a new “Cold War,” which weighed heavily on Russian equity markets. In Europe, all eyes were on Scotland. Its September 18 referendum, in which the citizens chose to remain part of the United Kingdom, created volatility in European equity markets. |

| ¢ | Long-dated U.S. bonds have been one of the biggest bull markets this year, against the nearly unanimous consensus at the start of the year that interest rates would rise. U.S. 10-year Treasury yields finished October at 2.34%, down from a yield of 3.03% at year-end 2013. As a result, the Barclays U.S. Aggregate Bond Index finished the partial fiscal year up 3.22%. Credit spreads widened across the board, but particularly for lower quality issues. Selling pressure in the high yield market intensified in September as a confluence of factors such as abundant supply, strapped cash balances, tepid equities, rate concerns, and decreased risk appetite all weighed on demand. The European Central Bank (ECB) surprised the market in September by lowering its interest rates across the board. The ECB also announced it would buy asset-backed securities and bonds issued by eurozone banks. This contributed to the third calendar quarter’s massive euro sell-off of -7.9% versus the U.S. dollar. Additionally, the Bank of Japan’s surprise Halloween announcement regarding a big boost to its quantitative easing stimulus program contributed to the Japanese reflation theme, pushing Japanese equities higher and the yen lower versus the U.S. dollar. |

| ¢ | Real assets, with the exception of commodities, delivered the strongest gains for the partial fiscal year with U.S. REITs, as |

measured by the FTSE NAREIT® All Equity REIT Index, posting a +13.84% return. Earnings reports and company statements showed good cash flow growth across most property sectors, driven by improving demand, limited new supply, and the continued availability of low-cost financing. Master limited partnerships (MLPs) also had a strong partial fiscal year with the Alerian MLP IndexSM delivering a +11.88% return. Falling Treasury yields were particularly beneficial for the more interest rate-sensitive and bond-like MLPs. Increased mergers/consolidation activity, most notably the announcement of the Kinder Morgan restructuring deal, provided additional stock-specific catalysts. Commodities, as measured by the Bloomberg Commodity Index, declined 12.47% in the partial fiscal year with weakness across the board, as inflation concerns waned and there were concerns regarding global growth prospects. Global infrastructure stocks had gains for the partial fiscal year but were negatively affected during the third calendar quarter due to faltering economic growth, especially in Europe and China. |

| ¢ | Hedge fund strategies posted modest gains for the partial fiscal year, with losses in event-driven and convertible strategies offset by slight positive gains in equity long/short and credit strategies, as well as large gains in global macro strategies, which benefited from the rising U.S. dollar and fluctuating U.S. interest rates. Credit and convertible strategies were buffeted by spread widening, and event-driven strategies were negatively impacted by a number of merger and acquisition deals (most notably Sprint/T-Mobile, 21st Century Fox/Time Warner, and Shire/AbbVie) breaking down, as well as the cessation of a number of anticipated tax inversion mergers after the U.S. Treasury announced new rules to curtail such deals. |

What factors affected the Fund’s performance during its partial fiscal year?

| ¢ | The Fund generated a positive return for its partial fiscal year and outperformed its benchmark, the HFRXSM Fixed Income Credit Index. Each of the Fund’s six underlying strategies were either flat or generated a positive return. The largest contributors to the Fund’s total return were the real asset |

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

6

Table of Contents

Alternative Income Solution Fund (Continued)

| strategies, benefiting from the market dynamics in their respective asset classes. The MLP and REIT strategies performed well due to portfolio positioning, while MLPs also benefited from merger and acquisition activity in the sector. Although global stocks were positive during the period, driven primarily by the performance of the U.S. stock market, the income-oriented equities strategy underperformed due to country market exposures. |

| ¢ | With respect to the credit-oriented strategies, two of the three had flat returns for the partial fiscal year, reflecting general credit spread widening. The third strategy, focusing on emerging market debt, had modest positive gains for the period, driven by gains in the second calendar quarter attributable to security selection and the overall strong performance of emerging market debt. Gains were pared back in the third calendar quarter as the strategy was affected by volatility in emerging market debt, which has largely been driven by events in Argentina and Brazil as well as a cooling Chinese economy. Several of the strategies have been layering on interest rate and credit hedges in order to offset future declines, but overall, derivatives had a negligible impact on the total portfolio. These strategies are diversified across both high yield bonds and bank loans emphasizing middle market companies. |

| ¢ | No changes were made to the roster of managers subadvising the underlying strategies during the partial fiscal year. The credit (-5%) and MLP (-5%) target allocations were modestly lowered during the fiscal year due to valuation concerns, while there were offsetting modest increases in the allocation targets to emerging market debt (+5%) and income-oriented equities (+5%) due to the more attractive market opportunity set in emerging market debt, as well as the more attractive valuations in developed non-U.S. equities, in particular European and emerging market equities. |

The preceding information is the opinion of portfolio management. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objective.

Alternative investments are not suitable for all investors.

Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a security may fail to make payments in a timely manner. Values of debt securities may rise and fall in response to changes in interest rates. This risk may be enhanced with longer-term maturities.

There is a greater level of credit risk and price volatility involved with high-yield securities than investment-grade securities.

There may be no ready market for loan participation interests. The Fund may have to sell the interests at a substantial discount. Such interests are subject to the credit risk of the underlying corporate borrower.

Investing internationally involves additional risks such as currency, political, accounting, economic, and market risk.

The market price of equity securities may be affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

The Fund may engage in short sales, and may experience a loss if the price of a borrowed security increases before the date on which the Fund replaces the security.

When a fund leverages its portfolio, the value of its shares may be more volatile and all other risks may be compounded.

Investments in derivatives such as futures, options, forwards, and swaps may increase volatility or cause a loss greater than the principal investment.

Investments in Master Limited Partnerships may be impacted by tax law changes, regulation, or factors affecting underlying assets.

The Fund may be negatively affected by factors specific to the real estate market, including interest rates, leverage, property, and management.

The Fund is non-diversified and may be more susceptible to factors negatively impacting its holdings to the extent that each security represents a larger portion of the Fund’s assets.

The Fund’s principal investments strategies will result in a consistently high portfolio turnover rate. A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account.

| Asset Allocation | ||

| The following table presents asset allocations within certain sectors and as a percentage of total investments as of October 31, 2014. | ||

Corporate Bonds | 36% | |

Loan Agreement | 18% | |

Master Limited Partnerships | 13% | |

Common Stocks | 12% | |

Real Estate Investment Trusts | 12% | |

Foreign Government Securities | 3% | |

Municipal Bonds | 1% | |

Preferred Stock | 1% | |

Asset-Backed Securities | 1% | |

Other (includes short-term investments) | 3% | |

| ||

Total | 100% | |

| ||

| ||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

7

Table of Contents

Alternative Income Solution Fund (Continued)

Total Returns1 for periods ended October 31, 2014

| ||||||||

Since Inception | Inception Date | |||||||

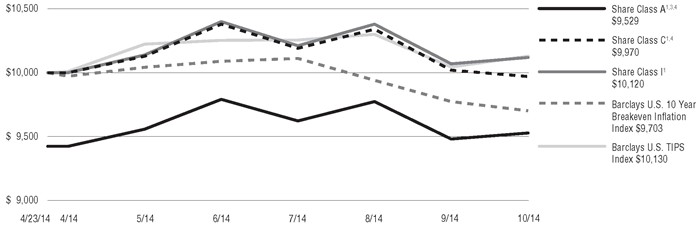

| Class A Shares at NAV2 | 1.82% | 4/23/14 | ||||||

| Class A Shares at POP3,4 | -4.04 | 4/23/14 | ||||||

| Class C Shares at NAV2 | 1.38 | 4/23/14 | ||||||

| Class C Shares with CDSC4 | 0.38 | 4/23/14 | ||||||

| Class I Shares at NAV | 1.90 | 4/23/14 | ||||||

| HFRX Fixed Income–Credit Index | -1.885 | — | ||||||

Fund Expense Ratios6: A Shares: Gross 3.50%, Net 2.60%; C Shares: Gross 4.25%, Net 3.35%; I Shares: Gross 3.25%, Net 2.35%.

|

| |||||||

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

1 Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. Total returns are not annualized.

2 “NAV” (Net Asset Value) total returns do not include the effect of any sales charge.

3 “POP” (Public Offering Price) total returns include the effect of the maximum front-end 5.75% sales charge.

4 “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter.

5 The since inception index returns are from the Fund’s inception date.

6 The expense ratios of the Fund are set forth according to the prospectus for the Fund effective April 22, 2014, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by the contractual fee waiver in effect through April 30, 2015. Gross Expense: Does not reflect the effect of the fee waiver.

Growth of $10,000 For period ended 10/31

This chart assumes an initial investment of $10,000 made on April 23, 2014 (inception date of the Fund), for Class A, Class C, and Class I shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

8

Table of Contents

Alternative Inflation Solution Fund

Fund Summary | Ticker Symbols: Class A: VSAIX Class C: VSICX Class I : VIASX |

| ¢ | The Fund is non-diversified and has an investment objective of total return that exceeds the rate of inflation. |

| ¢ | For the fiscal period April 23, 2014 (inception date) through October 31, 2014, the Fund’s Class A shares at NAV returned 1.10%*, Class C shares at NAV returned 0.70%*~ and Class I shares returned 1.20%*. For the same period, the Barclays U.S. TIPS Index, a broad-based fixed income index, returned 1.30%* and the Barclays U.S. 10 Year Breakeven Inflation Benchmark Index, which is the Fund’s style-specific benchmark appropriate for comparison, returned -2.97%*. |

| * | Returns less than 1 year are not annualized. |

| ~ | See Footnote 7 on page 11. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the markets perform during the Fund’s partial fiscal year?

| ¢ | Most global equity markets saw strong performance during the Fund’s partial fiscal year, from its inception date of April 23, 2014 through October 31, 2014. The S&P 500® Index, which measures the performance of large company stocks, finished the period up 9.02% and saw a number of new closing highs. In contrast, the Russell 2000® Index, a metric of small-cap stock performance, returned 0.77%, showing the dispersion of returns between large- and small-cap stocks. Non-U.S. stocks in developed markets did not perform well, with the MSCI EAFE® Index returning -3.17% for the partial fiscal year due to European stocks being down 6.49%. Emerging market stocks, as measured by the MSCI Emerging Markets Index, ended the period up 4.08%. The partial fiscal year saw a flurry of corporate merger activity, including Twenty-First Century Fox’s $80 billion offer for Time Warner, online real estate company Zillow’s $2.6 billion bid for Trulia, and speculation regarding a number of potential tax inversion deals. A highlight in September was the IPO of Alibaba, the China-based e-commerce giant, whose blockbuster public debut at $21.8 billion was the largest U.S. IPO ever. |

| ¢ | The economic divergence among the United States, the United Kingdom, the eurozone, and Japan has become increasingly stark, and markets were heavily dominated by remarks from their central banks over the partial fiscal year. The timing of any Federal Reserve interest rate increase remains an issue of strong debate. While hawks argue that the |

interest rate cycle should be normalized before creating another bubble, the doves argue the economy is not yet strong enough to stand on its own. Geopolitical instability in Ukraine, the Middle East, a widening war against ISIS, protests in Hong Kong, the Ebola scare, as well as Argentina’s selective default, dominated headlines. New sanctions imposed by the U.S. and EU on Russia ushered in the winds of a new “Cold War,” which weighed heavily on Russian equity markets. In Europe, all eyes were on Scotland. Its September 18 referendum, in which the citizens chose to remain part of the United Kingdom, created volatility in European equity markets. |

| ¢ | Long-dated U.S. bonds have been one of the biggest bull markets this year, against the nearly unanimous consensus at the start of the year that interest rates would rise. U.S. 10-year Treasury yields finished October at 2.34%, down from a yield of 3.03% at year-end 2013. As a result, the Barclays U.S. Aggregate Bond Index finished the partial fiscal year up 3.22%. Credit spreads widened across the board, but particularly for lower quality issues. Selling pressure in the high yield market intensified in September as a confluence of factors such as abundant supply, strapped cash balances, tepid equities, rate concerns, and decreased risk appetite all weighed on demand. The European Central Bank (ECB) surprised the market in September by lowering its interest rates across the board. The ECB also announced it would buy asset-backed securities and bonds issued by eurozone banks. This contributed to the third calendar quarter’s massive euro sell-off of -7.9% versus the U.S. dollar. Additionally, the Bank of Japan’s surprise Halloween announcement regarding a big boost to its quantitative easing stimulus program contributed to the Japanese reflation theme, pushing Japanese equities higher and the yen lower versus the U.S. dollar. |

| ¢ | Real assets, with the exception of commodities, delivered the strongest gains for the partial fiscal year with U.S. REITs, as measured by the FTSE NAREIT® All Equity REIT Index, posting a +13.84% return. Earnings reports and company statements showed good cash flow growth across most property sectors, driven by improving demand, limited new supply, and the continued availability of low-cost financing. Master limited partnerships (MLPs) also had a strong partial fiscal year with the Alerian MLP IndexSM delivering a +11.88% return. Falling Treasury yields were particularly beneficial for the more interest rate-sensitive and bond-like MLPs. Increased mergers/consolidation activity, most notably the announcement of the Kinder Morgan restructuring deal, provided additional stock-specific catalysts. Commodities, as measured by the Bloomberg |

Commodity Index, declined 12.47% in the partial fiscal year with weakness across the board, as inflation concerns waned and there were concerns regarding global growth prospects. Global infrastructure stocks had gains for the partial fiscal year but were negatively affected during the third calendar quarter due to faltering economic growth, especially in Europe and China. |

| ¢ | Hedge fund strategies posted modest gains for the partial fiscal year, with losses in event-driven and convertible strategies offset by slight positive gains in equity long/short and credit strategies, as well as large gains in global macro strategies, which benefited from the rising U.S. dollar and fluctuating U.S. interest rates. Credit and convertible strategies were buffeted by spread widening, and event-driven strategies were negatively impacted by a number of merger and acquisition deals (most notably Sprint/T-Mobile, 21st Century Fox/Time Warner, and Shire/AbbVie) breaking down, as well as the cessation of a number of anticipated tax inversion mergers after the U.S. Treasury announced new rules to curtail such deals. |

What factors affected the Fund’s performance during its partial fiscal year?

| ¢ | The Fund generated a positive return for its partial fiscal year and outperformed its benchmark, the Barclays U.S. 10 Year Breakeven Inflation Index. Four of the Fund’s six underlying strategies generated a flat or positive return for the partial fiscal year. The largest contributors to the Fund’s total return were the MLP and REIT strategies, benefiting from the market dynamics in their respective asset classes. The MLP and REIT strategies performed well due to portfolio positioning, while MLPs also benefited from merger and acquisition activity in the sector. |

| ¢ | The largest negative return for the partial fiscal year was the commodity portion of the portfolio – which consists of exposure to the Bloomberg Commodity Index, implemented via derivatives – as commodities across the board had declines in the wake of lowered global growth projections. While global infrastructure stocks in general had modest gains for the partial fiscal year, they also were negatively affected during the third calendar quarter due to slowing global economic growth prospects. Additionally, the infrastructure strategy performed below its benchmark, the UBS Global Infrastructure/ Utilities 50/50 Index, due to country market exposures. |

| ¢ | The strategy that focuses on U.S. credit had flat returns for the partial fiscal year, reflecting general credit spread widening. The strategy is diversified across both high-yield bonds and |

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

9

Table of Contents

Alternative Inflation Solution Fund (Continued)

bank loans, and the manager of the strategy has been layering on interest rate and credit hedges in order to offset future declines. The global inflation-linked strategy replicates the Barclays U.S. 10 Year Breakeven Index using a combination of inflation-linked bonds and Treasury futures, and as expected, had losses in Treasury futures in doing so. However, although this strategy had negative absolute returns due to lowered U.S. inflation expectations, it outperformed the Barclays U.S. 10 Year Breakeven Index return due to currency positioning and security selection. |

| ¢ | No changes were made to the roster of managers subadvising the Fund’s underlying strategies during the partial fiscal year. The MLP (-5%) target allocation was modestly lowered during the fiscal year due to valuation concerns, while there was an offsetting modest increase in the target allocation to infrastructure equities (+5%) due to the more attractive valuations in developed market non-U.S. equities, in particular European equities. |

The preceding information is the opinion of portfolio management. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objective.

Alternative investments are not suitable for all investors.

Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a security may fail to make payments in a timely manner. Values of debt securities may rise and fall in response to changes in interest rates. This risk may be enhanced with longer-term maturities.

Inflation-linked securities will react differently from other fixed income securities to changes in interest rates. Generally, the value of an inflation-linked security will fall when real interest rates rise and will rise when real interest rates fall.

The market price of equity securities may be affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Investments in Master Limited Partnerships may be impacted by tax law changes, regulation, or factors affecting underlying assets.

The Fund may be negatively affected by factors specific to the real estate market, including interest rates, leverage, property, and management.

A fund that focuses its investments in infrastructure-related companies will be more sensitive to conditions affecting their business or operations.

There is a greater level of credit risk and price volatility involved with high-yield securities than investment-grade securities.

There may be no ready market for loan participation interests. The Fund may have to sell the interests at a substantial discount. Such interests are subject to the credit risk of the underlying corporate borrower.

Events negatively affecting a particular commodity in which the Fund focuses its investments may cause the value of the Fund’s shares to decrease, perhaps significantly.

The Fund may engage in short sales, and may experience a loss if the price of a borrowed security increases before the date on which the Fund replaces the security.

When a fund leverages its portfolio, the value of its shares may be more volatile and all other risks may be compounded.

Investments in derivatives such as futures, options, forwards, and swaps may increase volatility or cause a loss greater than the principal investment.

Investing internationally involves additional risks such as currency, political, accounting, economic, and market risk.

The Fund is non-diversified and may be more susceptible to factors negatively impacting its holdings to the extent that each security represents a larger portion of the Fund’s assets.

The Fund’s principal investments strategies will result in a consistently high portfolio turnover rate. A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account.

Alternative Inflation Solution Fund

| ||

| The following table presents asset allocations within certain sectors and as a percentage of total investments as of October 31, 2014. | ||

U.S. Government Securities | 21% | |

Common Stocks | 19% | |

Master Limited Partnerships | 18% | |

Real Estate Investment Trusts | 18% | |

Corporate Bonds | 13% | |

Loan Agreements | 7% | |

Municipal Bonds | 1% | |

Asset-Backed Securities | 1% | |

Preferred Stock | 1% | |

Other (includes short-term investments) | 1% | |

| ||

Total | 100% | |

| ||

| ||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

10

Table of Contents

Alternative Inflation Solution Fund (Continued)

Total Returns1 for period ended 10/31/14

| ||||||||

Since Inception | Inception Date | |||||||

| Class A Shares at NAV2 | 1.10% | 4/23/14 | ||||||

| Class A Shares at POP3,4 | -4.71 | 4/23/14 | ||||||

| Class C Shares at NAV2,7 | 0.70 | 4/23/14 | ||||||

| Class C Shares with CDSC4 | -0.30 | 4/23/14 | ||||||

| Class I Shares at NAV | 1.20 | 4/23/14 | ||||||

| Barclays U.S. TIPS Index | 1.305 | — | ||||||

| Barclays U.S. 10 Year Breakeven Inflation Benchmark Index | -2.975 | — | ||||||

| Fund Expense Ratios6: A Shares: Gross 3.76%, Net 2.64%; C Shares: Gross 4.51%, Net 3.39%, I Shares: Gross 3.51%, Net 2.39%. | ||||||||

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

1 Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. Total returns are not annualized.

2 “NAV” (Net Asset Value) total returns do not include the effect of any sales charge.

3 “POP” (Public Offering Price) total returns include the effect of the maximum front-end 5.75% sales charge.

4 “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid are 1% and 0% thereafter.

5 The since inception index returns are from the Fund’s inception date.

6 The expense ratios of the Fund are set forth according to the prospectus for the Fund effective April 22, 2014, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by the contractual fee waiver in effect through April 30, 2015. Gross Expense: Does not reflect the effect of the fee waiver.

7 Total Return for the report period presented in the table differs from the return in the Financial Highlights. The total return presented in the above table is calculated based on the NAV at which shareholder transactions were processed. The total return presented in the Financial Highlights section of the report is calculated in the same manner, but also takes into account certain adjustments that are necessary under generally accepted accounting principles required in the annual report and semi-annual report.

Growth of $10,000 For period ended 10/31

This chart assumes an initial investment of $10,000 made on April 23, 2014 (inception date of the Fund), for Class A shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

11

Table of Contents

Alternative Total Solution Fund

Fund Summary | Ticker Symbols: Class A: VATAX Class C: VATCX Class I : VATIX |

| ¢ | The Fund is non-diversified and has an investment objective of long-term capital appreciation through investments that have a low correlation to traditional asset classes. |

| ¢ | For the fiscal period April 23, 2014 (inception date) through October 31, 2014, the Fund’s Class A shares at NAV returned 1.70%*, Class C shares returned 1.30%*, and Class I shares returned 1.80%.* For the same period, the HFRX Global Hedge Fund Index, which serves as the broad-based index and style-specific benchmark appropriate for comparison, returned -0.77%*. |

| * | Returns less than 1 year are not annualized. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the markets perform during the Fund’s partial fiscal year?

| ¢ | Most global equity markets saw strong performance during the Fund’s partial fiscal year, from its inception date of April 23, 2014 through October 31, 2014. The S&P 500® Index, which measures the performance of large company stocks, finished the period up 9.02% and saw a number of new closing highs. In contrast, the Russell 2000® Index, a metric of small-cap stock performance, returned 0.77%, showing the dispersion of returns between large- and small-cap stocks. Non-U.S. stocks in developed markets did not perform well, with the MSCI EAFE® Index returning -3.17% for the partial fiscal year due to European stocks being down 6.49%. Emerging market stocks, as measured by the MSCI Emerging Markets Index, ended the period up 4.08%. The partial fiscal year saw a flurry of corporate merger activity, including Twenty-First Century Fox’s $80 billion offer for Time Warner, online real estate company Zillow’s $2.6 billion bid for Trulia, and speculation regarding a number of potential tax inversion deals. A highlight in September was the IPO of Alibaba, the China-based e-commerce giant, whose blockbuster public debut at $21.8 billion was the largest U.S. IPO ever. |

| ¢ | The economic divergence among the United States, the United Kingdom, the eurozone, and Japan has become increasingly stark, and markets were heavily dominated by remarks from their central banks over the partial fiscal year. The timing of any Federal Reserve interest rate increase remains an issue of strong debate. While hawks argue that the interest rate cycle should be normalized before creating another bubble, the doves argue the economy is not yet strong enough to stand on its own. Geopolitical instability in Ukraine, the Middle East, a widening war against ISIS, protests in Hong Kong, the Ebola scare, as well as Argentina’s selective default, dominated headlines. New sanctions imposed by the U.S. and EU on Russia ushered in the winds of a new “Cold War,” which weighed heavily on Russian equity markets. In Europe, all eyes were on Scotland. Its September 18 referendum, in which the citizens chose to remain part of the United Kingdom, created volatility in European equity markets. |

| ¢ | Long-dated U.S. bonds have been one of the biggest bull markets this year, against the nearly unanimous consensus at the start of the year that interest rates would rise. U.S. 10-year Treasury yields finished October at 2.34%, down from a yield of 3.03% at year-end 2013. As a result, the Barclays U.S. Aggregate Bond Index finished the partial fiscal year up 3.22%. Credit spreads widened across the board, but particularly for lower quality issues. Selling pressure in the high yield market intensified in September as a confluence of factors such as abundant supply, strapped cash balances, tepid equities, rate concerns, and decreased risk appetite all weighed on demand. The European Central Bank (ECB) surprised the market in September by lowering its interest rates across the board. The ECB also announced it would buy asset-backed securities and bonds issued by eurozone banks. This contributed to the third calendar quarter’s massive euro sell-off of -7.9% versus the U.S. dollar. Additionally, the Bank of Japan’s surprise Halloween announcement regarding a big boost to its quantitative easing stimulus program contributed to the Japanese reflation theme, pushing Japanese equities higher and the yen lower versus the U.S. dollar. |

| ¢ | Real assets, with the exception of commodities, delivered the strongest gains for the partial fiscal year with U.S. REITs, as measured by the FTSE NAREIT ® All Equity REIT Index, posting a +13.84% return. Earnings reports and company statements showed good cash flow growth across most property sectors, driven by improving demand, limited new supply, and the continued availability of low-cost financing. Master limited partnerships (MLPs) also had a strong partial fiscal year with the Alerian MLP IndexSM delivering a +11.88% return. Falling Treasury yields were particularly beneficial for the more interest rate-sensitive and bond-like MLPs. Increased mergers/consolidation activity, most notably the announcement of the Kinder Morgan restructuring deal, provided additional stock-specific catalysts. Commodities, as measured by the Bloomberg Commodity Index, declined 12.47% in the partial fiscal year with weakness across the board, as inflation concerns waned and there were concerns regarding global growth prospects. Global infrastructure stocks had gains for the partial fiscal year but were negatively affected during the third calendar quarter due to faltering economic growth, especially in Europe and China. |

| ¢ | Hedge fund strategies posted modest gains for the partial fiscal year, with losses in event-driven and convertible strategies offset by slight positive gains in equity long/short and credit strategies, as well as large gains in global macro strategies, which benefited from the rising U.S. dollar and fluctuating U.S. interest rates. Credit and convertible strategies were buffeted by spread widening, and event-driven strategies were negatively impacted by a number of merger and acquisition deals (most notably Sprint/T-Mobile, 21st Century Fox/Time Warner, and Shire/AbbVie) breaking down, as well as the cessation of a number of anticipated tax inversion mergers after the U.S. Treasury announced new rules to curtail such deals. |

What factors affected the Fund’s performance during its partial fiscal year?

| ¢ | The Fund generated a positive return for its partial fiscal year and outperformed its benchmark, the HFRXSM Global Hedge Fund Index. Although performance of the Fund’s |

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

12

Table of Contents

Alternative Total Solution Fund (Continued)

underlying strategies was mixed, a number generated positive results. Overall, the Fund’s diversified exposure to a broad range of alternative strategies allowed it to capture returns from strategies that were performing well, such as global macro, equity long/short, MLPs, and REITs, while mitigating losses when there was a pullback in the U.S. stock market, such as there was in September when the Fund outperformed the S&P 500® Index. The overall impact of derivatives on the portfolio was minimal for the partial fiscal year. |

| ¢ | The largest contributors to the Fund’s total return were the real asset strategies, which benefited from the market dynamics in their respective asset classes. The MLP and REIT strategies performed well due to portfolio positioning, while MLPs also benefited from merger and acquisition activity in the sector. In contrast, global infrastructure stocks in general had modest gains for the partial fiscal year but were negatively affected during the third calendar quarter due to slowing global economic growth prospects. The infrastructure strategy performed below its benchmark, the UBS Global Infrastructure/ Utilities 50/50 Index, due to country market exposures. |

| ¢ | With respect to the credit-oriented strategies, two of the three had flat returns for the partial fiscal year, reflecting general credit spread widening. The third strategy, focusing on emerging market debt, had modest positive gains for the period, driven by gains in the second calendar quarter, attributable to security selection and the overall strong performance of emerging market debt. Gains were pared back in the third calendar quarter as the strategy was affected by volatility in emerging market debt, which has largely been driven by events in Argentina and Brazil, as well as a cooling Chinese economy. Several of the strategies have been layering on interest rate and credit hedges in order to offset future declines. The portfolios are diversified across both high-yield bonds and bank loans emphasizing middle market companies. |

| ¢ | The hedge fund strategies had mixed returns during the partial fiscal year with positive gains from the manager of the equity long/ short strategy, who added value via stock selection, although their hedges, via derivatives, detracted value for the fiscal year |

in an overall rising U.S. stock market. The global macro exposure, implemented via derivatives, also benefited the Fund, especially during a period of U.S. stock market losses in September, as the strategy had gains in currency and rate trading. The convertible bond market was negatively affected by volatile equity markets, spread widening, and heavy new issuance during the third calendar quarter, resulting in modest losses, while the strategy was also negatively affected by security selection. The event-driven strategy posted a negative return for the partial fiscal year due to several telecom merger and acquisition deal-breaks in the third calendar quarter. |

| ¢ | No changes were made to the roster of managers subadvising the underlying strategies during the partial fiscal year. The credit (-4%) and MLP (-2%) target allocations were modestly lowered during the period due to valuation concerns, while there were offsetting modest increases in the target allocations to emerging market debt (+4%) and equity long/short (+2%) due to the more attractive market opportunity set and to increase the hedged exposure in the portfolio. |

The preceding information is the opinion of portfolio management. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objective.

Alternative investments are not suitable for all investors.

The Fund may engage in short sales, and may experience a loss if the price of a borrowed security increases before the date on which the Fund replaces the security.

When a fund leverages its portfolio, the value of its shares may be more volatile and all other risks may be compounded.

The market price of equity securities may be affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Investments in derivatives such as futures, options, forwards, and swaps may increase volatility or cause a loss greater than the principal investment.

Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk.

Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a security may fail to make payments in a timely manner. Values of debt securities may rise and fall in response to changes in interest rates. This risk may be enhanced with longer-term maturities.

There is a greater level of credit risk and price volatility involved with high-yield securities than investment-grade securities.

There may be no ready market for loan participation interests. The Fund may have to sell the interests at a substantial discount. Such interests are subject to the credit risk of the underlying corporate borrower.

A convertible security may be called for redemption at a time and price unfavorable to the fund.

Investments in Master Limited Partnerships may be impacted by tax law changes, regulation, or factors affecting underlying assets.

The Fund may be negatively affected by factors specific to the real estate market, including interest rates, leverage, property, and management.

A fund that focuses its investments in infrastructure-related companies will be more sensitive to conditions affecting their business or operations.

Commodity-linked instruments may experience a return different than the commodity they attempt to track and may also be exposed to counterparty risk.

The Fund’s principal investments strategies will result in a consistently high portfolio turnover rate. A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

13

Table of Contents

Alternative Total Solution Fund (Continued)

| Asset Allocation | ||

| The following table presents asset allocations within certain sectors and as a percentage of total investments as of October 31, 2014. | ||

Common Stocks | 34% | |

Corporate Bonds | 18% | |

Convertible Bonds | 11% | |

Master Limited Partnerships | 8% | |

Loan Agreements | 8% | |

Real Estate Investment Trusts | 6% | |

Foreign Government Securities | 2% | |

Preferred Stock | 1% | |

Municipal Bonds | 1% | |

Asset-Backed Securities | 1% | |

Other (includes short-term investments) | 10% | |

| ||

Total | 100% | |

| ||

| �� | ||

| ||

| Total Returns1 for period ended 10/31/14 | ||||||||

Since Inception | Inception Date | |||||||

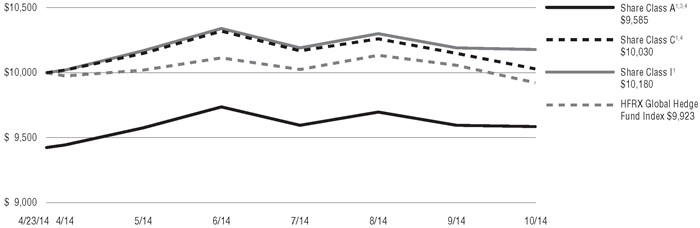

Class A Shares at NAV2

| 1.70% | 4/23/14 | ||||||

Class A Shares at POP3,4

| -4.15 | 4/23/14 | ||||||

Class C Shares at NAV2

| 1.30 | 4/23/14 | ||||||

Class C Shares with CDSC4

| 0.30 | 4/23/14 | ||||||

Class I Shares at NAV

| 1.80 | 4/23/14 | ||||||

HFRX Global Hedge Fund Index

| -0.775 | — | ||||||

Fund Expense Ratios6: A Shares: Gross 3.98%, Net 3.18%; C Shares: Gross 4.73%, Net 3.93%; I Shares: Gross 3.73%, Net 2.93%.

|

| |||||||

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

1 Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. Total returns are not annualized.

2 “NAV” (Net Asset Value) total returns do not include the effect of any sales charge.

3 “POP” (Public Offering Price) total returns include the effect of the maximum front-end 5.75% sales charge.

4 “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter.

5 The since inception index return is from the Fund’s inception date.

6 The expense ratios of the Fund are set forth according to the prospectus for the Fund effective April 22, 2014, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by the contractual fee waiver in effect through April 30, 2015. Gross Expense: Does not reflect the effect of the fee waiver.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

14

Table of Contents

Alternative Total Solution Fund (Continued)

Growth of $10,000 For periods ended 10/31

This chart assumes an initial investment of $10,000 made on April 23, 2014 (inception date of the Fund), for Class A, Class C, and Class I shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

15

Table of Contents

Fund Summary | Ticker Symbols: Class A: VASBX Class C: VSBCX Class I : VISBX |

| ¢ | The Fund is diversified and has an investment objective of seeking total return comprised of income and capital appreciation. |

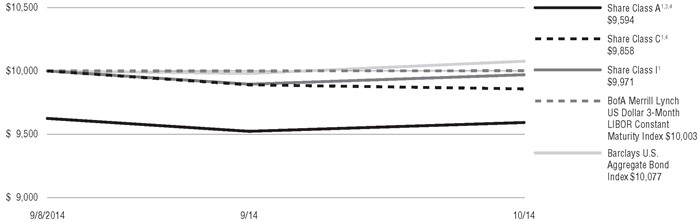

| ¢ | For the fiscal period from September 8, 2014 (inception date) through October 31, 2014, the Fund’s Class A shares at NAV returned -0.33%*, Class C shares returned -0.43%*, and Class I shares returned -0.29%*. For the same period, the Barclays U.S. Aggregate Bond Index, a broad-based fixed income index, returned 0.77%* and the BofA Merrill Lynch U.S. Dollar 3-Month LIBOR Constant Maturity Index, which is the Fund’s style-specific benchmark index appropriate for comparison, returned 0.03%*. |

| * Returns less than 1 year are not annualized. |

| All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above. |

There is no guarantee that the Fund will meet its objective.

† The Fund is less than six months old - No commentary required.

Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a security may fail to make payments in a timely manner. Values of debt securities may rise and fall in response to changes in interest rates. This risk may be enhanced with longer-term maturities.

There is a greater level of credit risk and price volatility involved with high-yield securities than investment-grade securities.

Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk.

There may be no ready market for loan participation interests. The Fund may have to sell the interests at a substantial discount. Such interests are subject to the credit risk of the underlying corporate borrower.

Changes in interest rates can cause both extension and prepayment risks for asset and mortgage-backed securities. These securities are also subject to risks associated with the repayment of underlying collateral.

Investments in derivatives such as futures, options, forwards, and swaps may increase volatility or cause a loss greater than the principal investment.

The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track. The costs of owning the ETF may exceed the cost of investing directly in the underlying securities.

| Asset Allocation | ||

The following table presents asset allocations within certain sectors and as a percentage of total investments as of October 31, 2014. | ||

Corporate Bonds | 45% | |

U.S. Government Securities | 18% | |

Loan Agreements | 13% | |

Mortgaged-Backed Securities | 8% | |

Asset-Backed Securities | 7% | |

Foreign Government Securities | 3% | |

Preferred Stock | 1% | |

Other (includes short-term investments) | 5% | |

| ||

Total |

100% | |

| ||

| ||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 3.

16

Table of Contents

Strategic Income Fund (Continued)

| Total Returns1 for periods ended 10/31/14 | ||||||||

Since Inception

| Inception Date

| |||||||

Class A Shares at NAV2

| -0.33% | 9/08/14 | ||||||

Class A Shares at POP3,4

| -4.06 | 9/08/14 | ||||||

Class C Shares at NAV2

| -0.43 | 9/08/14 | ||||||

Class C Shares with CDSC4

| -1.42 | 9/08/14 | ||||||

Class I Shares at NAV

| -0.29 | 9/08/14 | ||||||

Barclays U.S. Aggregate Bond Index

| 0.775 | — | ||||||