UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Pursuant to §240.14a-12 |

VIRIDIAN THERAPEUTICS, INC.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement if Other Than the Registrant)

Payment of Filing Fee (Check all boxes that apply):

| ☒ | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11. |

On April 26, 2024, Viridian Therapeutics, Inc. (“we,” “us,” “our,” “Viridian” or the “Company”) filed a definitive proxy statement on Schedule 14A (the “Proxy Statement”) with the Securities and Exchange Commission in connection with our 2024 Annual Meeting of Stockholders to be held virtually on June 17, 2024 at 3:00 p.m. Eastern Time, or at any other time following adjournment or postponement thereof. This supplement (the “Supplement”) should be read in conjunction with the Proxy Statement.

Viridian Therapeutics, Inc. Definitive Additional Materials (“Supplement”) 2024 Annual Meeting of Stockholders June 2024

Cautionary note regarding forward-looking statements This Supplement contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of words such as, but not limited to, “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “potential,” “predict,” “project,” “should,” “target,” “will,” or “would” or other similar terms or expressions that concern our expectations, plans and intentions. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based on our current beliefs, expectations, and assumptions. Forward-looking statements include, without limitation, statements regarding: our planned equity usage and employee compensation; execution upon our corporate goals and the delivery of catalysts; that without the Share Increase, we anticipate running out of equity to grant from our pool as soon as the first quarter of 2025; anticipated dilution, plan cost and shareholder value transferof the Share Increase; that we currently expect the Share Increase will be sufficient to meet our expected needs for approximately one year based on our historical grant practices and performance; and that we do not expect to grant annual employee awards in 2024, and therefore we anticipate a lower burn rate in 2024 compared to 2023. New risks and uncertainties may emerge from time to time, and it is not possible to predict all risks and uncertainties. No representations or warranties (expressed or implied) are made about the accuracy of any such forward-looking statements. Such forward-looking statements are subject to a number of material risks and uncertainties including those risks set forth under the caption “Risk Factors” in our Quarterly Report on Form 10-Q filed with the Securities and Exchange Commission (“SEC”) on May 8, 2024 and our other subsequent disclosure documents filed with the SEC. The forward-looking statements in this Supplement represent our views as of the date of this Supplement. Neither we, nor our affiliates, advisors, or representatives, undertake any obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. These forward-looking statements should not be relied upon as representing our views as of any date subsequent to the date of this Supplement. 2

Proposals for the 2024 Annual Meeting of Stockholders On April 26, 2024, Viridian Therapeutics, Inc. (“we,” “us,” “our,” “Viridian” or the “Company”) filed a definitive proxy statement on Schedule 14A (the “Proxy Statement”) with the Securities and Exchange Commission in connection with our 2024 Annual Meeting of Stockholders to be held virtually on June 17, 2024 at 3:00 p.m. Eastern Time (the “Annual Meeting”), or at any other time following adjournment or postponement thereof. This Supplement should be read in conjunction with the Proxy Statement. The proposals to be voted upon at the Annual Meeting are as follows: 1. To elect the two Class III director nominees named in the Proxy Statement to serve until the 2027 Annual Meeting of Stockholders and until their successors are duly elected and qualified. 2. To ratify the selection of KPMG LLP as the Company’s independent registered public accounting firm for the year ending December 31, 2024. 3. To approve, on an advisory basis, the compensation of the Company’s named executive officers. 4. To approve a further amendment and restatement of the Company’s Amended and Restated 2016 Equity Incentive Plan, including an increase by 2,000,000 of the shares available for issuance thereunder (the “Share Increase”). 3 3

Supplemental Information Regarding Proposal 4: The Share Increase 4

Stockholders of Viridian should vote for the Share Increase for four key reasons • The Share Increase is critical to support retention and continued hiring of talent at Viridian - talent is key to the execution of Viridian’s goals • Without the Share Increase, our current equity pool is inadequate to support retention and hiring • The Share Increase is reasonable • Our historical share usage (burn rate) is reasonable 5 5

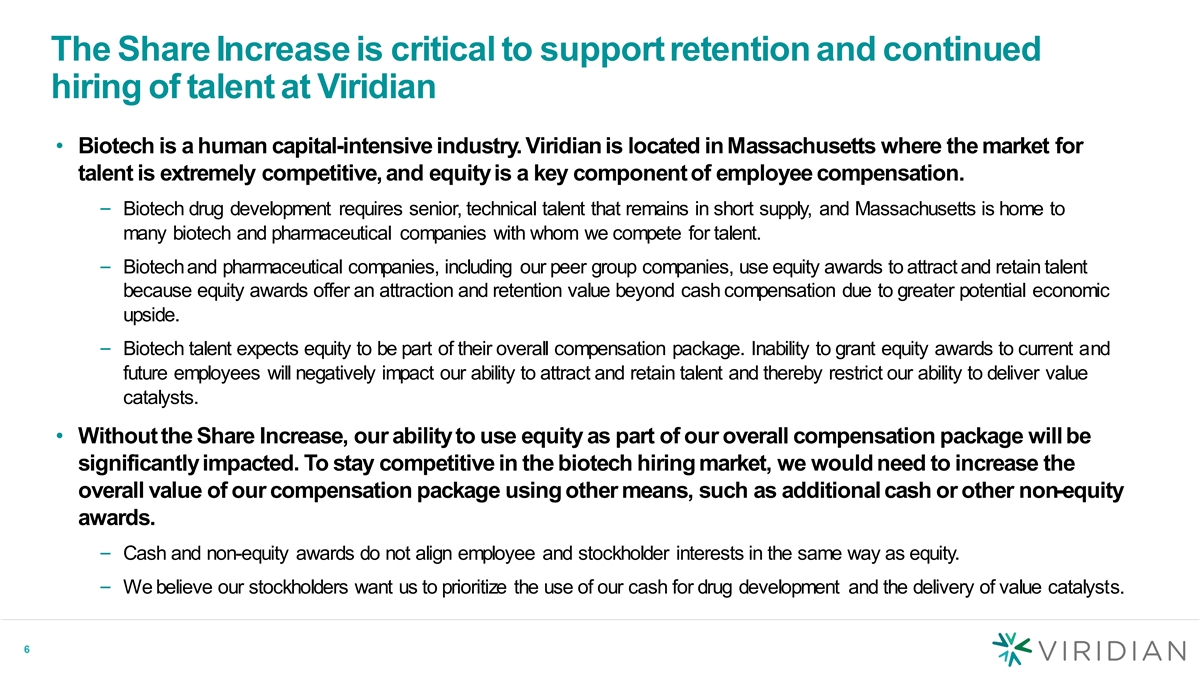

The Share Increase is critical to support retention and continued hiring of talent at Viridian • Biotech is a human capital-intensive industry. Viridian is located in Massachusetts where the market for talent is extremely competitive, and equity is a key component of employee compensation. – Biotech drug development requires senior, technical talent that remains in short supply, and Massachusetts is home to many biotech and pharmaceutical companies with whom we compete for talent. – Biotech and pharmaceutical companies, including our peer group companies, use equity awards to attract and retain talent because equity awards offer an attraction and retention value beyond cash compensation due to greater potential economic upside. – Biotech talent expects equity to be part of their overall compensation package. Inability to grant equity awards to current and future employees will negatively impact our ability to attract and retain talent and thereby restrict our ability to deliver value catalysts. • Without the Share Increase, our ability to use equity as part of our overall compensation package will be significantly impacted. To stay competitive in the biotech hiring market, we would need to increase the overall value of our compensation package using other means, such as additional cash or other non-equity awards. – Cash and non-equity awards do not align employee and stockholder interests in the same way as equity. – We believe our stockholders want us to prioritize the use of our cash for drug development and the delivery of value catalysts. 6 6

Without the ShareIncrease, our current equity pool is inadequate to support retention and hiring • Without the Share Increase, we anticipate running out of equity to grant from our pool as soon as the first quarter of 2025. – This would significantly harm our competitive position and our ability to attract and retain talent. – Talent is key to our ability to execute upon our corporate goals, particularly in preparation for a potential commercial launch of our product candidates, if approved. 7 7

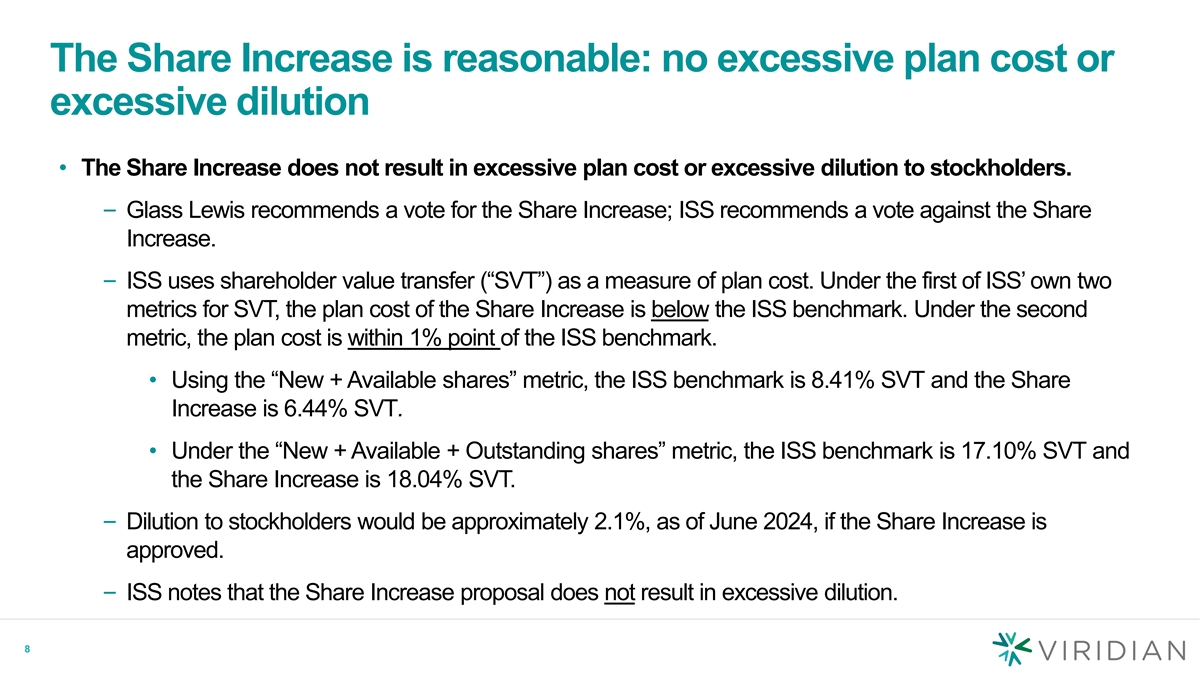

The Share Increase is reasonable: no excessive plan cost or excessive dilution • The Share Increase does not result in excessive plan cost or excessive dilution to stockholders. – Glass Lewis recommends a vote for the Share Increase; ISS recommends a vote against the Share Increase. – ISS uses shareholder value transfer (“SVT”) as a measure of plan cost. Under the first of ISS’ own two metrics for SVT, the plan cost of the Share Increase is below the ISS benchmark. Under the second metric, the plan cost is within 1% point of the ISS benchmark. • Using the “New + Available shares” metric, the ISS benchmark is 8.41% SVT and the Share Increase is 6.44% SVT. • Under the “New + Available + Outstanding shares” metric, the ISS benchmark is 17.10% SVT and the Share Increase is 18.04% SVT. – Dilution to stockholders would be approximately 2.1%, as of June 2024, if the Share Increase is approved. – ISS notes that the Share Increase proposal does not result in excessive dilution. 8 8

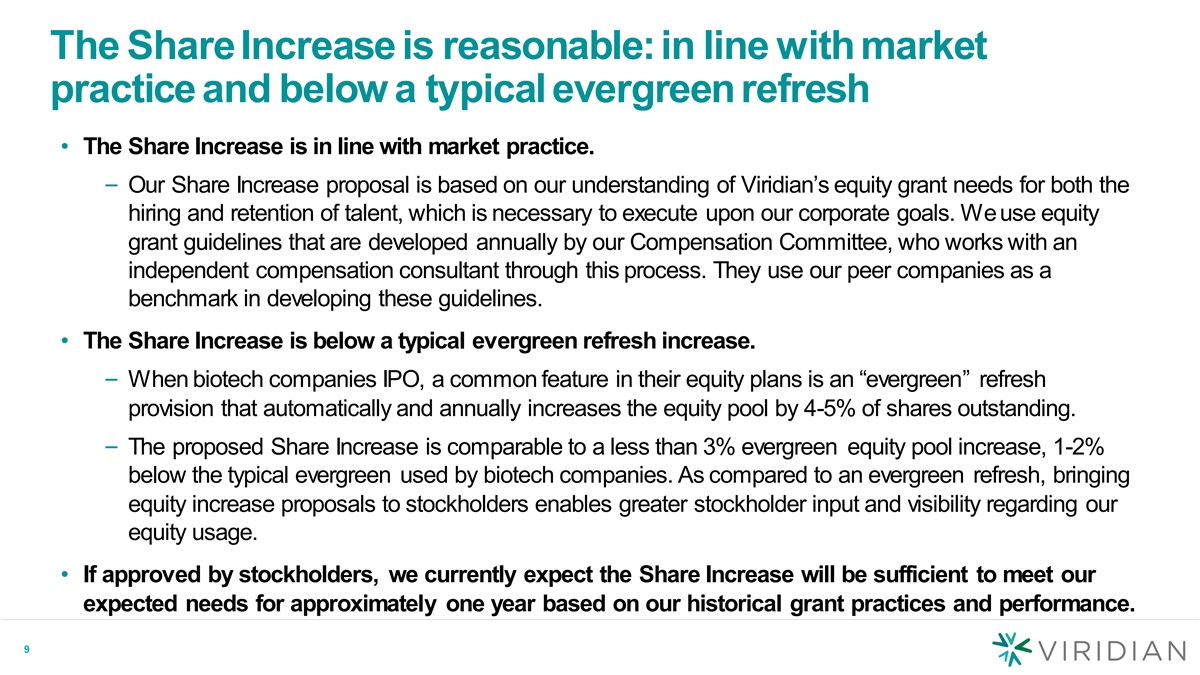

The Share Increase is reasonable:in line with market practice and below a typical evergreen refresh • The Share Increase is in line with market practice. – Our Share Increase proposal is based on our understanding of Viridian’s equity grant needs for both the hiring and retention of talent, which is necessary to execute upon our corporate goals. We use equity grant guidelines that are developed annually by our Compensation Committee, who works with an independent compensation consultant through this process. They use our peer companies as a benchmark in developing these guidelines. • The Share Increase is below a typical evergreen refresh increase. – When biotech companies IPO, a common feature in their equity plans is an “evergreen” refresh provision that automatically and annually increases the equity pool by 4-5% of shares outstanding. – The proposed Share Increase is comparable to a less than 3% evergreen equity pool increase, 1-2% below the typical evergreen used by biotech companies. As compared to an evergreen refresh, bringing equity increase proposals to stockholders enables greater stockholder input and visibility regarding our equity usage. • If approved by stockholders, we currently expect the Share Increase will be sufficient to meet our expected needs for approximately one year based on our historical grant practices and performance. 9 9

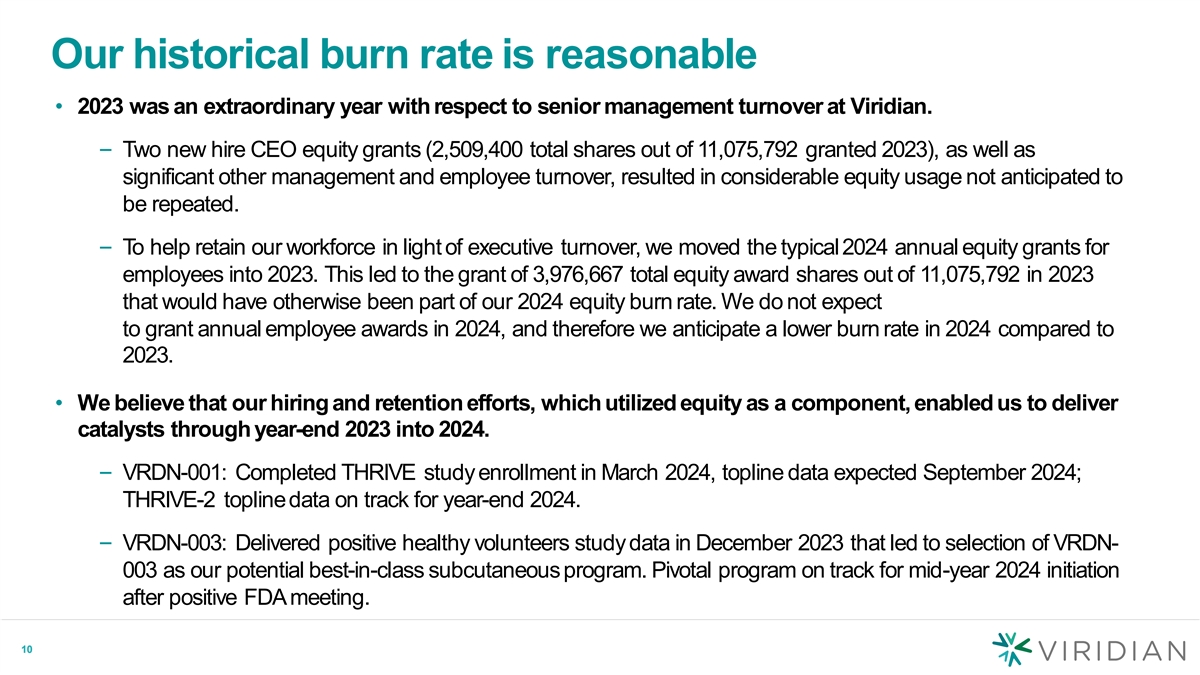

Our historical burn rate is reasonable • 2023 was an extraordinary year with respect to senior management turnover at Viridian. – Two new hire CEO equity grants (2,509,400 total shares out of 11,075,792 granted 2023), as well as significant other management and employee turnover, resulted in considerable equity usage not anticipated to be repeated. – To help retain our workforce in light of executive turnover, we moved the typical2024 annual equity grants for employees into 2023. This led to the grant of 3,976,667 total equity award shares out of 11,075,792 in 2023 that would have otherwise been part of our 2024 equity burn rate. We do not expect to grant annual employee awards in 2024, and therefore we anticipate a lower burn rate in 2024 compared to 2023. • We believe that our hiring and retention efforts, which utilized equity as a component, enabled us to deliver catalysts through year-end 2023 into 2024. – VRDN-001: Completed THRIVE study enrollment in March 2024, topline data expected September 2024; THRIVE-2 topline data on track for year-end 2024. – VRDN-003: Delivered positive healthy volunteers study data in December 2023 that led to selection of VRDN- 003 as our potential best-in-class subcutaneous program. Pivotal program on track for mid-year 2024 initiation after positive FDA meeting. 10 10

Our historical burn rate is reasonable • Our three-year burn rate is reasonable, as there were substantial mitigating factors in 2023. – 2024 annual employee equity awards, which typically would have been granted in the first half of 2024, were instead granted in 2023 for retention purposes. We do not expect to grant annual employee awards in 2024, and therefore we anticipate a lower burn rate in 2024 compared to 2023. – In the first quarter of 2024 and in the 2023 fiscal year, an aggregate of approximately 4.7 million equity award shares were cancelled or forfeited, relating to awards that were granted in previous years. A significant number of these awards were equity grants to former management roles that required backfilling and, therefore, resulted in a higher burn rate. These include additional CEO grants consisting of 2,509,400 total shares (Scott Myers 1,250,000; Steve Mahoney 1,259,400). • Based on the mitigating factors noted above, we calculate our three-year, value adjusted burn rate to be 6.36%. – Our as-converted preferred stock is not counted in many traditional metrics of burn rate, including certain ISS burn rate calculations. We believe any burn rate calculation should include these as-converted preferred shares because they are a significant part of our capital structure, and these preferred shares are economically equivalent to the common stock given their conversion rights. – In our value adjusted burn rate, we also subtract the grants that were made in 2023 for retention purposes that would have otherwise been granted as annual employee equity awards in 2024. – As disclosed in our Proxy Statement, our three-year average burn rate through December 31, 2023 was approximately 13.8%, which does not include the adjustments for mitigating factors noted above. We calculate it to be 6.36% when they are. 11 11

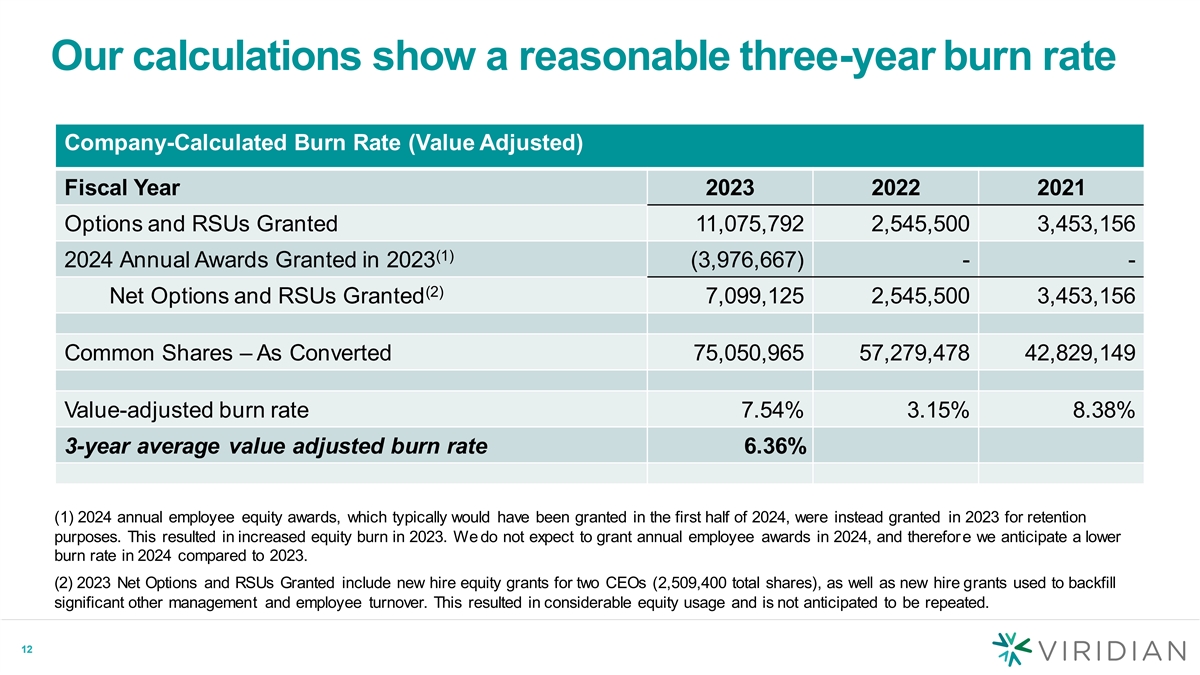

Our calculations show a reasonable three-year burn rate Company-Calculated Burn Rate (Value Adjusted) Fiscal Year 2023 2022 2021 Options and RSUs Granted 11,075,792 2,545,500 3,453,156 (1) 2024 Annual Awards Granted in 2023 (3,976,667) - - (2) Net Options and RSUs Granted 7,099,125 2,545,500 3,453,156 Common Shares – As Converted 75,050,965 57,279,478 42,829,149 Value-adjusted burn rate 7.54% 3.15% 8.38% 3-year average value adjusted burn rate 6.36% (1) 2024 annual employee equity awards, which typically would have been granted in the first half of 2024, were instead granted in 2023 for retention purposes. This resulted in increased equity burn in 2023. We do not expect to grant annual employee awards in 2024, and therefore we anticipate a lower burn rate in 2024 compared to 2023. (2) 2023 Net Options and RSUs Granted include new hire equity grants for two CEOs (2,509,400 total shares), as well as new hire grants used to backfill significant other management and employee turnover. This resulted in considerable equity usage and is not anticipated to be repeated. 12 12

Summary of Key Points in Support of the Share Increase • The Share Increase is critical to support retention and continued hiring of talent at Viridian - talent is key to the execution of Viridian’s goals – Biotech is a human capital-intensive industry. Viridian is located in Massachusetts where the market fortalent is extremely competitive, and equity is a key component of employee compensation. – Without the Share Increase, our ability to use equity as part of our overall compensation package will be significantly impacted and will reduce our ability to hire and retain talent, unless we were to use additional cash or other non-equity awards as part of overall compensation. • Without the Share Increase, our current equity pool is inadequate to support retention and hiring – Without the Share Increase, we anticipate running out of equity to grant from our pool as soon as the first quarter of 2025. • The Share Increase is reasonable – The Share Increase does not result in excessive plan cost or excessive dilution to stockholders, and our equity use is in line with market practice and our peer group companies. • Our historical share usage (burn rate) is reasonable – 2023 was an unusual year with respect to senior management turnover at Viridian. – We believe that our hiring and retention efforts, which utilized equity as a component, enabled us to deliver catalysts through year-end 2023 into 2024. – There were substantial mitigating factors in 2023, which makes our three-year burn rate reasonable. Based on these factors, we calculate our three-year, value adjusted burn rate to be 6.36%. – The Share Increase will be sufficient to meet our expected needs for approximately one year based on our historical grant practices and performance, if approved by stockholders. 13 13