| SKADDEN, ARPS, SLATE, MEAGHER & FLOM | ||||

PARTNERS JOHN ADEBIYI¿ CHRISTOPHER W. BETTS EDWARD H.P. LAM¿* G.S. PAUL MITCHARD QC¿ CLIVE W. ROUGH¿ JONATHAN B. STONE * ALEC P. TRACY * ¿ (ALSO ADMITTEDIN ENGLAND & WALES) * (ALSO ADMITTEDIN NEW YORK)

REGISTERED FOREIGN LAWYERS Z. JULIE GAO (CALIFORNIA) GREGORY G.H. MIAO (NEW YORK) ALAN G. SCHIFFMAN (NEW YORK) |

42/F, EDINBURGH TOWER, THE LANDMARK 15 QUEEN’S ROAD CENTRAL, HONG KONG

TEL: (852) 3740-4700 FAX: (852) 3740-4727 www.skadden.com | AFFILIATE OFFICES

BOSTON CHICAGO HOUSTON LOS ANGELES NEW YORK PALO ALTO WASHINGTON, D.C. WILMINGTON

BEIJING BRUSSELS FRANKFURT LONDON MOSCOW MUNICH PARIS SÃO PAULO SHANGHAI SINGAPORE SYDNEY TOKYO TORONTO |

Confidential

January 10, 2014

Mail Stop 3720

Larry Spirgel, Assistant Director

Celeste M. Murphy, Legal Branch Chief

Ajay Koduri, Staff Attorney

Ivette Leon, Assistant Chief Accountant

Christy Adams, Senior Staff Accountant

Division of Corporation Finance

Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

| RE: | Tarena International, Inc. |

CIK No. 0001592560

Response to the Staff’s Comment Letter Dated December 20,

2013

Dear Mr. Spirgel, Ms. Murphy, Mr. Koduri, Ms. Leon and Ms. Adams:

On behalf of our client, Tarena International, Inc., a foreign private issuer organized under the laws of the Cayman Islands (the “Company”), we submit to the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) this letter setting forth the Company’s responses to the comments contained in the Staff’s letter dated December 20, 2013. Concurrently with the submission of this letter, the Company is submitting its revised draft registration statement on Form F-1 (the “Revised Draft Registration Statement”) and certain exhibits via EDGAR to the Commission for confidential non-public review pursuant to the Jumpstart Our Business Startups Act (the “JOBS Act”).

January 10, 2014

Page 2

To facilitate your review, we have separately delivered to you today four courtesy copies of the Revised Draft Registration Statement, marked to show changes to the draft registration statement confidentially submitted to the Commission on November 26, 2013, and two copies of the submitted exhibits.

The Staff’s comments are repeated below in bold and are followed by the Company’s responses. We have included page references in the Revised Draft Registration Statement where the language addressing a particular comment appears. Capitalized terms used but not otherwise defined herein have the meanings set forth in the Revised Draft Registration Statement.

In addition to adding and revising disclosure in response to the Staff’s comments, the Company has updated the Revised Draft Registration Statement to reflect the Company’s recent developments.

General

| 1. | We remind you of the Rule in Item 8(A)(4) of Form 20-F, that in the case of a company’s initial public offering, the audited financial statements must be as of a date not older than 12 months at the time the document is filed. In this regard, please revise as needed based upon this rule. |

The Staff’s comment is noted. The Company respectfully advises the Staff that the Company is relying on Section 1220.2 of theDivision of Corporate Finance Financial Reporting Manual in submitting the Revised Draft Registration Statement with the latest financial statements as of and for the nine months ended September 30, 2013.

Section 1220.2 (Rule for Initial Filers) provides the following:

The balance sheet date in an initial registration statement must not be more than 134 days old,except that third quarter data is timely through the 45th day after the most recent fiscal year-end for all filers, and except that third quarter data is timely through the 90th day after the most recent fiscal year-end for a Smaller Reporting Company if the SRC expects to report income from continuing operations before taxes in the year just completed and has reported income from continuing operations before taxes in at least one of the two years previous to the year just completed. After the 45th or 90th day, as applicable, audited financial statements for that fiscal year must be included in the registration.

2

January 10, 2014

Page 3

As such, the Company believes that its 2013 third quarter financial data is timely through the 45th day after the end of 2013, which would be February 14, 2014. The Company will include the audited financial statement for the year ended December 31, 2013 in submissions and filings made after February 14, 2014.

| 2. | Please be advised that you should include the price range, size of the offering, and all other required information in an amendment to your Form F-1 prior to any distribution of preliminary prospectuses so that we may complete our review. Note that we may have additional comments once you have provided this disclosure. Therefore, please allow us sufficient time to review your complete disclosure prior to any distribution of preliminary prospectuses. |

The Staff’s comment is noted. The Company confirms that it will include the estimated price range, estimated size of the offering and all other required information in subsequent amendments to its Form F-1 prior to any distribution of preliminary prospectuses as soon as such information becomes available.

| 3. | Please furnish a statement as to whether or not the amount of compensation to be allowed or paid to the underwriters has been cleared with FINRA. Prior to the effectiveness of this registration statement, please provide us with a copy of the letter informing you that FINRA has no objections. |

The Company respectfully advises the Staff that the underwriting arrangement is not yet finalized and FINRA’s clearance is expected to be obtained before the effectiveness of the registration statement. The Company confirms that a copy of FINRA’s no objection letter will be provided as soon as it is available.

| 4. | Please supplementally provide us with copies of all written communications, as defined in Rule 405 under the Securities Act, that you, or anyone authorized to do so on your behalf, present to potential investors in reliance on Section 5(d) of the Securities Act, whether or not they retain copies of the communications. Similarly, supplementally provide us with any research reports about you that are published or distributed in reliance upon Section 2(a)(3) of the Securities Act of 1933 added by Section 105(a) of the Jumpstart Our Business Startups Act by any broker or dealer that is participating or will participate in your offering. |

3

January 10, 2014

Page 4

The Company confirms that neither the Company nor any of its authorized representatives has presented to potential investors any written communication in reliance on Section 5(d) of the Securities Act. The Company further confirms that no broker or dealer that is participating or will participate in the Company’s offering has published or distributed any research reports about the Company in reliance upon Section 2(a)(3) of the Securities Act added by Section 105(a) of the JOBS Act.

| 5. | Provide us with copies of any industry analysis or reports that you cite or upon which you rely, including, but not limited to, market research reports and data prepared by IDC. Confirm for us that these documents are publicly available. Please clearly mark the specific portions that you are relying upon so that we can reference them easily. |

In response to the Staff’s comment, the Company has provided in Annex A copies of the IDC report and other backup documents supporting the various industry-related statements in the Revised Draft Registration Statement. The specific portions of these documents are also marked for your easy reference. The Company further advises the Staff that all of these backup documents, including the IDC report, are publicly available.

| 6. | Please provide us with English versions of your VIE agreements. |

In response to the Staff’s comment, the Company has provided English translations of its VIE agreements as Exhibits 10.4 to 10.25 to the Revised Draft Registration Statement.

Prospectus Summary, page 1

| 7. | Revise your disclosure to distinguish your current operations from any prospective endeavors. Prominently disclose that you derive a majority of your net revenues from Java courses. Disclose that in 2011, 2012 and the nine months ended September 30, 2013, your Java course contributed approximately 73.4%, 73.3% and 65.1% of your net revenues, respectively. To provide balance in this disclosure, state the risk that reduction of usage of Java in the IT industry would impact your operations and financial results. With this in mind, please revise statements indicating more aspirational roles in this business area. By way of example, we include such statements that: |

| • | You are the largest provider in China of IT professional education services; |

4

January 10, 2014

Page 5

| • | The basis for your statement that you believe that you are one of China’s leading brands in professional education; |

| • | What makes your platform innovative; and |

| • | What exactly your “partnership” with global Fortune 500 companies includes. |

Java Courses and Importance of Java to the IT Industry

In response to the Staff’s comment, the Company has revised disclosure on pages 2, 3, 16 and 91 of the Revised Draft Registration Statement to disclose (i) the revenue contribution of the Java course in 2011, 2012 and the nine months ended September 30, 2013 and (ii) the risks to the Company’s results of operations from a decrease in the popularity or usage of Java in the IT industry.

The Company respectfully advises the Staff that Java is one of the most widely used programming languages in the global IT industry (seeTIOBE Programming Community index at http://www.tiobe.com/index.php/content/paperinfo/tpci/index.html), and that Java engineers are the most sought after among all software engineers by employers in China (based on data from51Job, one of the leading recruiting websites in China). According to theTIOBE Programming Community index, Java has been one of the top two most popular programming languages globally since 2002. According to data compiled from51job.com, recruitment ads posted by employers seeking to hire Java engineers in China outnumbered recruitment ads for any other software coding language engineers in the two months ended December 31, 2013. The popularity of Java has made Java one of the most desired skills for prospective entrants into the IT industry, and has made Java courses among the most popular IT professional education courses for education service providers and students in China. Therefore, the fact that the Company generated a significant portion of its revenues from Java training courses reflect the hiring demands in the IT industry in China, which also contributes to the Company’s leading market position in IT professional education services in China.

The Company respectfully advises the Staff that the Company has highlighted its reliance on Java courses in the Prospectus Summary, Risk Factors and the Consolidated Financial Statements of the Revised Draft Registration Statement.

5

January 10, 2014

Page 6

Market Position in China’s IT Professional Education Services Market

The Company respectfully advises the Staff that the Company is the largest provider of IT professional education services in China as measured by revenues in 2013, according to the IDC report. In response to the Staff’s comment, the Company has also revised the referenced disclosure on pages 1, 67 and 89 to include the Company’s market shares in the IT professional education services market in China.

China’s leading brands in professional education

In response to the Staff’s comment, the Company has revised the referenced disclosure on pages 1 and 89 of the Revised Draft Registration Statement to provide the basis for the statement about the “Tarena” brand.

Innovative Platform

The Company respectfully advises the Staff that the Company believes its platform is innovative for the following two reasons:

| • | Uniqueness: The Company sampled ten Chinese education companies that are listed in the U.S. Six of these ten companies primarily deliver their education services offline with teachers in local centers. Four of these ten companies offer their education services primarily online. |

| • | Synergy: The Company’s platform offers a hybrid learning model that combines the benefits of both traditional classroom-based learning and online learning. Unlike the traditional classroom-based learning model, which could be time-consuming and costly |

6

January 10, 2014

Page 7

the hybrid learning model is highly scalable given its ability to deliver instruction via webcast using one teacher to a widespread audience while ensuring consistent teaching quality across geographies. In addition, the hybrid learning model is capable of creating a more disciplined and focused learning environment through requiring class attendance in the learning centers and offering on-site support by teaching assistants to tutor and supervise students in each classroom, which is the main advantage over the pure online learning model. |

The Company respectfully advises the Staff that the advantages of the hybrid learning model over traditional offline and online learning models are described in greater detail in the Industry Overview section of the Revised Draft Registration Statement.

Partnership with Global Fortune 500 Companies

In response to the Staff’s comment, the Company has revised disclosure on pages 1, 89 and 100 of the Revised Draft Registration Statement.

| 8. | Revise to disclose the more specific findings of the IDC report. Given your reliance on Java, please explain your current disclosure that the IDC report says that you are the largest provider of IT professional education services in China. |

The Company respectfully refers the Staff to the responses to the Staff’s comment 7 above.

| 9. | Include balanced disclosure to present your position in this industry among the competition, by market share, regionally relevant as necessary, revenue, etc. We note your disclosure on page 100. Tell us why the market information you provide with this revision is directly applicable to your business, taking into consideration your reliance on Java. |

The Company respectfully refers the Staff to its responses to the Staff’s comment 7 above.

| 10. | Tell us, with a view toward disclosure, which entity holds your intellectual property, including registered 13 software copyrights for your proprietary TTS and your one trademark, registered 40 domain names relating to your business, including yourwww.tarena.com.cn andwww.it211.com.cn websites, etc. |

7

January 10, 2014

Page 8

The Company respectfully advises the Staff that Tarena Tech (the WFOE) holds 13 registered software copyrights, two trademarks and 39 registered domain names includingwww.tarena.com.cn.

Beijing Tarena (the VIE) only holds one domain name,www.it211.com.cn.

In response to the Staff’s comment, the Company has revised the referenced disclosure on page 102 and 111 of the Revised Draft Registration Statement to disclose the above.

| 11. | Please clarify in plain English your use of “high-demand industry verticals.” |

The Company respectfully advises the Staff that “high-demand industry verticals” means industries with significant growth potential and high employee hiring demands. In response to the Staff’s comment, the Company has revised the referenced disclosure on pages 1, 67, 89 and 96 of the Revised Draft Registration Statement.

| 12. | Please expand your disclosure to explain how you deliver high quality lectures through a group of experienced and passionate instructors in Beijing to a nationwide network of 86 directly operated learning centers in 32 cities in China. For example, if these lectures are broadcast live over your website to students sitting in learning centers, this should be made clear. Articulate the breakdown of in-audience live lectures, broadcast live lectures and pre-recorded videos. Provide a basis for your statement that you do this “without impacting the quality of [y]our course offerings.” |

The Company respectfully advises the Staff that:

| • | for each of its lectures, there is one (and only one) classroom located in Beijing with in-audience live lecture where the instructor delivers lectures to students in the same classroom; |

| • | other students sitting in all other classrooms in learning centers across China simultaneously watch a live webcast of these lectures; |

8

January 10, 2014

Page 9

| • | as a general practice, the Company does not use pre-recorded lectures in classes, except in the event of service interruptions or for the learning sites on university campuses where the students are not able to follow the Company’s class schedules due to logistical reasons. |

The Company respectfully advises the Staff that these lectures arenot broadcast through the Company’s website. Rather, the Company webcasts the lectures to the Company’s learning centers across China via the dedicated telecommunications networks or over public Internet infrastructure.The students are required to physically attend classes and watch the live webcast of the lectures at the Company’s learning centers.

In response to the Staff’s comment, the Company has revised the referenced disclosure on pages 1, 67 and 89 of the Revised Draft Registration Statement.

| 13. | Distinguish between your students’ involvement with instructors as opposed to your in-class teaching assistants who “coach, tutor and supervise” students. |

In response to the Staff’s comment, the Company has revised the referenced disclosure on pages 1, 67, 86, 89, 91, 94, 95 and 98 of the Revised Draft Registration Statement.

| 14. | Please explain how your student-to-instructor ratio is broken down. For example, are these all live lectures broadcast from the Beijing instructors? If so, to what size “classes” in how many cities, etc. |

The Company respectfully advises the Staff that for each of its lectures, there is one (and only one) classroom which is in Beijing where the instructor delivers lectures to students in person, and students sitting in all other classrooms in learning centers across China simultaneously watch a live webcast of these lectures. Therefore, other than the students in one classroom who attend the lectures in-person, the other students in China attend the lectures via live webcast.

As disclosed on page 94 of the Revised Draft Registration Statement, the Company’s classrooms vary in terms of size, being able to host between 30 and 80 students.

| 15. | To provide balance and context, please disclose that the registrant is a holding company and clarify that your operational consolidated |

9

January 10, 2014

Page 10

| affiliated entity in the PRC includes a variable interest entity holding the ICP license, material to your business operations and financial results. Disclose that it is through the contractual arrangements that you have effective control, which allows you to consolidate the financial results of the VIE in your financial statements. Disclose that, if your PRC VIE and its shareholders fail to perform their obligations under the contractual arrangements, you could be limited in your ability to enforce the contractual arrangements that give you effective control. Further, if you are unable to maintain effective control, you would not be able to continue to use the material ICP license to operate your business and that you are not eligible as a FIE to hold an ICP. Disclose the percentage of revenues in your consolidated financial statements that are derived from your use of the ICP held by the VIE. |

The Company respectfully advises the Staff that as disclosed on pages 4 and 60 of the Revised Registration Statement, none of the Company’s two consolidated VIEs, namely Beijing Tarena and Shanghai Tarena, currently generates significant revenues. For the nine months ended September 30, 2013, these two VIEs contributed 14.8% of the Company’s total net revenues. The Company expects that the revenues contribution from the VIEs for the fourth quarter of 2013 is even lower. This is because the Company has gradually transferred most of its operations, including related assets and liabilities of its consolidated VIEs, to the WFOE and the WFOE’s subsidiaries and schools in light of the newPRC Catalogue for the Guidance of Foreign Investment Industries (amended)effective in January 2012, which listed professional education service as an industry for which foreign investment is “encouraged” by the government.

The Company is in the process of winding down Shanghai Tarena. The Company expects to continue to control and consolidate Beijing Tarena, which holds an ICP license. This ICP license held by Beijing Tarena is necessary for the operation of itswww.it211.com.cn website. However,www.it211.com.cn is primarily a marketing platform for the Company, and it does not generate any meaningful revenues for the Company and the Company does not rely on this website for delivering lectures. As explained in detail in the Company’s response to the Staff’s comment 12 above, the lectures arenot broadcast through the Company’s website; rather, the Company webcasts the lectures to the Company’s learning centers across China via the dedicated telecommunications networks or over public Internet

10

January 10, 2014

Page 11

infrastructure. However, in order to provide the investors with full disclosure, the Company has included extensive disclosure on the VIE structure in the Prospectus Summary, Risk Factors and the Corporate History and Structure sections.

In response to the Staff’s comment, the Company has further revised disclosure on pages 2 and 89 of the Revised Draft Registration Statement.

| 16. | We note your disclosure on pages 18 and 19 regarding a risk factor concerning learning centers operating outside their scope or license. Please summarize this risk in the Prospectus Summary or Challenges section, breaking out the categories by degree of risk, e.g., 29.9% of your student enrollments are from learning centers with neither professional education services nor education information related consultation as an authorized scope of business, 14.3% of your student enrollments come from centers operated outside their approved districts without obtaining relevant licenses and permits, etc. The extent of these risks should be prominently disclosed. We note your disclosure on pages 18-19. |

In response to the Staff’s comment, the Company has revised disclosure on page 4 of the Revised Draft Registration Statement.

| 17. | We note your disclosure on page 20 regarding a risk factor concerning your cooperative relationship with certain financing entities. Please summarize this risk in the Prospectus Summary or Challenges section. |

In response to the Staff’s comment, the Company has revised disclosure on page 3 of the Revised Draft Registration Statement.

| 18. | We note your disclosure at the bottom of page 21 and top of page 22 regarding your leasehold interests. Please summarize this risk in the Prospectus Summary or Challenges section. |

In response to the Staff’s comment, the Company has revised disclosure on page 4 of the Revised Draft Registration Statement.

Organizational Chart, page 4

| 19. | Amend your chart to include your subsidiaries and schools, including principals and control people. Please include sponsor information for the schools and distinguish them from subsidiaries of which you hold direct equity. |

11

January 10, 2014

Page 12

In response to the Staff’s comment, the Company has revised disclosure on pages 5 and 61 of the Revised Draft Registration Statement. The Company has included the principals in a foot note to the chart.

Risk Factors, page 14

The operations of certain of our learning centers are, or may be deemed by relevant PRC government authorities to be..., page 19

| 20. | Please revise your disclosure to make clear how you have actually “changed the sponsors of two schools” yet the change is not effective. Make clear what will happen if you do not receive approval. |

The Company respectfully advises the Staff that the final filing for the change of sponsor for Guangzhou Tarena Software Professional Education School (“Guangzhou School”) was duly made on November 25, 2013. The change of sponsor for Guangzhou School has become effective. Therefore, the Company has deleted the referenced disclosure on page 20 of the Revised Draft Registration Statement.

12

January 10, 2014

Page 13

For Wuhan Tarena Professional Education School (“Wuhan School”), the Company changed the shareholder of Wuhan School’s sponsor from the VIE to a subsidiary of the WFOE on December 26, 2013 and hence changed Wuhan School from a school indirectly owned by the VIE to a school indirectly owned by the WFOE. Therefore, the Company has deleted the referenced disclosure on page 20 of the Revised Draft Registration Statement.

Risks Relating to Our Corporate Structure, page 26

If the PRC government finds that the agreements that establish the structure for holding our ICP license do not comply with applicable PRC laws and regulations, we could be subject to severe penalties, page 26

| 21. | Add the PRC law on the foreign ownership restriction on Internet content and other value-added telecommunication services. We note your disclosure on page 108. The force of the prohibitions and restrictions should be prominent at this risk factor. |

13

January 10, 2014

Page 14

In response to the Staff’s comment, the Company has revised disclosure on page 27 of the Revised Draft Registration Statement.

| 22. | Please revise your disclosure throughout this offering document to eliminate reference that you entered into a VIE structure “to comply” with PRC laws and regulations. We note such disclosure on page 108 as well, for example. |

In response to the Staff’s comment, the Company has revised disclosure on pages 27, 31, 61 and 112 of the Revised Draft Registration Statement.

| 23. | Revise your disclosure to state the materiality of the ICP to the entirety of your business operations and financial results. Disclose the portion of your operations that could be run without your ICP license and yourwww.it211.com.cn website. |

In response to the Staff’s comment, the Company has revised disclosure on pages 28 of the Revised Draft Registration Statement.

The Company respectfully advises the Staff that the ICP license is used by the Company in connection with its operation ofwww.it211.com.cn, which is used primarily for the Company’s own marketing activities. The ICP license is not used for the live webcast of lectures in the Company’s business operations and therefore the Company does not believe that the ICP license is material to its overall business operations. Other than the marketing efforts onwww.it211.com.cn, the Company is able to operate its business without the ICP license.

| 24. | Describe the risks to your operations of and financial results from your TTS online platform relative to the risks surrounding the ICP. |

As discussed in the Company’s response to the Staff’s comment 23 above, the ICP license is used by the Company as part of its marketing efforts onwww.it211.com.cn and such ICP license is not used for the provision of online learning modules on the Company’s TTS platform. Therefore, the Company respectfully advises the Staff that the risks surrounding the ICP license are not directly related to the Company’s operations of and financial results from the TTS online platform.

14

January 10, 2014

Page 15

| 25. | Please revise to remove disclosure that reduces the perception of the materiality of the ICP to your entire operations and financial results, including your disclosure here that insignificant revenue is generated from your VIE, Beijing Tarena, etc. |

In response to the Staff’s comment, the Company has revised disclosure on pages 27 and 28 of the Revised Draft Registration Statement.

If Beijing Tarena becomes the subject of a bankruptcy or liquidation proceeding, we may lose the ability to use and enjoy its assets, which could materially and adversely affect our business, page 30

| 26. | We note your disclosure that “[i]f the shareholders of Beijing Tarena were to attempt to voluntarily dissolve or liquidate Beijing Tarena without obtaining [y]our prior consent, [you] could effectively prevent such unauthorized voluntary liquidation by exercising [y]our right to request Beijing Tarena’s shareholders to transfer all of their equity ownership interest to a PRC entity or individual designated by [you] in accordance with the exclusive option agreements with the shareholders of Beijing Tarena.” Please explain who at the company would exercise this right, including the anticipated shareholding, officer and director control of Mr. Han and his affiliates, including, but not limited to his wife, Ms. Ying Sun. |

The Company respectfully advises the Staff that the Company has direct contractual rights to exercise the options to request Beijing Tarena’s shareholders to transfer all of their equity ownership interests in Beijing Tarena to a PRC entity or individual designated by the Company in accordance with the exclusive option agreements (the “Options”). Pursuant to the Company’s current memorandum and articles of association and the Companies Law of the Cayman Islands, the business of the Company, including the proposed exercise of the Options, shall be resolved by the board of directors by way of a majority of votes of the members of the board at a board meeting or resolution in writing signed by all directors. The Company’s board is currently comprised of three directors, including Mr. Han and two directors appointed by certain private equity investors of the Company.

Currently, Mr. Han and his affiliates, including his wife Ms. Sun, have one seat on the board of directors of the Company. It is expected that Mr. Han and his affiliates will continue to have one seat on the board of directors of the Company after the completion of the initial public offering. Mr. Han and his affiliates,

15

January 10, 2014

Page 16

currently beneficially own 35.4% of the outstanding shares of the Company on an as-converted basis. It is expected that Mr. Han and his affiliates will have a reduced beneficial ownership in the Company after the completion of the offering. Currently, Mr. Han and Ms. Sun have two officer positions of the Company and will remain so in the foreseeable future.

Prior to the completion of this offering, the Company expects to have a board of directors that includes the necessary number of independent directors, as well as an audit committee, a compensation committee and a nominating and corporate governance committee in compliance with the relevant rules under the Securities Exchange Act of 1934, as amended, and the listing rules of the relevant stock exchange. The decision by the Company to exercise the Options after the completion of this offering will be made by the then board of directors of the Company.

| 27. | Disclose the uncertainties in legal proceedings enforcing your VIE agreements accounting for the prohibition on your VIE holding the ICP to assist a foreign investor in any form. We note that “Under the MIIT Circular, a domestic company that holds an ICP license is prohibited from leasing, transferring or selling the license to foreign investors in any form, and from providing any assistance, including providing resources, sites or facilities, to foreign investors that conduct value-added telecommunications business illegally in China.” Please include this factor in your current discussion of the event that if the shareholders of Beijing Tarena initiate a voluntary liquidation proceeding without your authorization or attempts to distribute the retained earnings or assets of Beijing Tarena without your prior consent, you may need to resort to legal proceedings to enforce the terms of the contractual agreements. Explain why “the outcome of such legal proceeding would be uncertain.” |

In response to the Staff’s comment, the Company has revised the referenced disclosure on page 31 of the Revised Draft Registration Statement.

16

January 10, 2014

Page 17

Use of Proceeds, page 52

| 28. | Please disclose whether you plan to use any of the proceeds from this offering to fund the operations of your VIES and their related entities. Further, disclose whether you plan to use the proceeds from this offering to increase the registered capital of your domestic directly-held PRC subsidiaries and, if so, disclose the names of these entities and regulatory approvals and steps that need to be taken. |

In response to the Staff’s comment, the Company has revised the disclosure on page 53 of the Revised Draft Registration Statement.

Corporate History and Structure, page 59

| 29. | We note that you are in the process of winding down Shanghai Tarena Software Technology Co., Ltd. However, to provide your investors with a complete picture of your current organizational structure, please revise to include Shanghai Tarena in the diagram. Please tell us if any other entities have been excluded from the diagram. |

In response to the Staff’s comment, the Company has revised the referenced disclosure on pages 5 and 61 of the Revised Draft Registration Statement. The Company respectfully advises the Staff that no other entity is excluded from the diagram.

Equity Interest Pledge Agreements, page 62

| 30. | Please state the steps you have taken to date to register these equity interest pledge agreements with the competent Administration for Industry and Commerce. Include in this disclosure the names of the local AIC offices at which you are in the process of registering such equity pledges. |

The Company respectfully advises the Staff that it has completed the registration of the equity interest pledge under the equity interest pledge agreements between Tarena Tech, Beijing Tarena and the shareholders of Beijing Tarena, as amended and restated, with Changping Bureau of Beijing Administration for Industry and Commerce, and it has also completed the registration of the equity interest pledge under the equity interest pledge agreements between Tarena Tech, Shanghai Tarena and the shareholders of Shanghai Tarena, as amended and restated, with Huangpu Bureau of Shanghai Administration for Industry and Commerce. Therefore, the Company has revised the referenced disclosure on page 63 of the Revised Draft Registration Statement.

17

January 10, 2014

Page 18

| 31. | Please reconcile your disclosure that you are in the process of registering the equity pledge agreements with your disclosure on page 27 that in the opinion of Han Kun Law Offices the agreements are valid, binding and enforceable. |

The Company respectfully advises the Staff that two different PRC legal concepts are involved here: (i) “contracts”—the equity pledge agreement itself is a contract and becomes effective and enforceable as a contract without being registered; (ii) “property rights”—the pledge on the equity interests is not effective without being registered with the relevant local administration for industry and commerce.

As contracts, the equity pledge agreements between Tarena Tech, Beijing Tarena and the shareholders of Beijing Tarena became effective on the date when the agreements were duly executed by all the parties thereto. Tarena Tech can enforce its contractual rights under the equity pledge agreements, such as the right to request the shareholders of Beijing Tarena to register the equity pledges and demand the shareholders of Beijing Tarena to perform their obligations under equity pledge agreements. As these are contractual rights, Tarena Tech can resort to legal proceedings to enforce these contractual rights.

On the other hand, in order to perfect an equity pledge, registration with the relevant local administration for industry and commerce is required under the PRC Property Rights Law. If an equity pledge is not perfected as a property right after such registration, Tarena Tech will not be able to exercise those rights that are pertinent to property rights (although it can exercise those rights as contractual rights). In particular, if the equity pledge is not registered, it is possible that a third party may acquire property right interests in the equity in good faith, that is, such third party is not aware of the existence of Tarena Tech’s pledges on the equity. For instance:

| • | If a third party acquires equity interests from the VIE shareholders in good faith, without the knowledge of the existence of Tarena Tech’s pledges on the equity interests and duly registers such equity interests, the original equity pledges to Tarena Tech, if not registered, does not attach to the equity interests transferred to the third party, and Tarena Tech, as the pledgee, cannot enforce the equity pledge against such third party; |

| • | If a VIE shareholder pledges his or her equity interests in the VIE to a third party and such third party duly registers the pledge in good faith, Tarena Tech will not have rights in priority with respect to the pledged equity interests vis-à-vis the third party. |

18

January 10, 2014

Page 19

In summary, the lack of registration of equity pledge does not affect Tarena Tech’s ability to enforce its contractual rights against the VIE shareholders as the equity pledge agreements have been duly executed and therefore are valid, binding and enforceable as contracts. However, the lack of registration of equity pledge will adversely affect Tarena Tech’s ability to enforce the equity pledge against third parties who acquire property right interests in good faith without knowledge of the initial pledge.

Management’s Discussion and Analysis of Financial Condition and Results of Operations, page 65

Net Revenues

| 32. | We refer to your statement that you “generally collect tuition fees in advance.” Please reconcile this statement with your receivable balance of approximately $17 million as of December 31, 2012 and risk factor disclosure on page 25, indicating that your historical outstanding accounts receivable have been relatively high. |

In response to the Staff’s comment, the Company has revised the referenced disclosure on page 67 of the Revised Draft Registration Statement.

The Company respectfully advises the Staff that the Company historically offered an option whereby students could pay tuition fees within a period of time after graduation. The Company has gradually phased out this payment option since the beginning of 2013, and expects to substantially end it in 2014. The gradual cessation of such installment payment option has reduced the Company’s outstanding accounts receivables. Starting in 2013, the Company began to collect tuition fees in advance generally.

| 33. | Expand your disclosure to discuss the economic reasons for your involvement in the Student Loan Program. |

In response to the Staff’s comment, the Company has revised the referenced disclosure on page 67 of the Revised Draft Registration Statement to describe (i) the guarantee fee revenue the Company generated in connection with the Student Loan Program in 2011, 2012 and the nine months ended September 30, 2013 and (ii) the fact that the Company did not generate any interest income in connection with the Student Loan Program.

19

January 10, 2014

Page 20

The Company respectfully advises the Staff that the primary purpose of the Student Loan Program is to offer students a source of financing for the payment of tuition fees. The Company respectfully advises the Staff that the Company’s involvement in the Student Loan Program is not driven by the desire to gain any economic interest or guarantee fee revenue from the Student Loan Program.

Liquidity and Capital Resources, page 78

| 34. | You state that your cash is unrestricted as to withdrawal. Please confirm that this statement applies to cash held in your VIEs. |

The Company confirms that the statement of cash being unrestricted as to withdrawal applies to cash held in its consolidated VIEs. The Company further respectfully advises the Staff that the cash balance of its consolidated VIEs can be used only to settle obligations of the consolidated VIEs. The Company has revised the the referenced disclosure on page 80 of the Revised Draft Registration Statement in response to the Staff’s comment.

Principal [and Selling] Shareholders, page 123

| 35. | Please include the corresponding percentages or portions represented by U.S. holders of your Series A convertible preferred shares and Series B convertible preferred shares. |

In response to the Staff’s comment, the Company has revised the referenced disclosure on page 127 of the Revised Draft Registration Statement.

Description of Share Capital, page 127

| 36. | Please revise your disclosure as follows: |

| • | Make clear, here (under “Voting Rights, page 127”) and under “How do I vote, page 139” the number of days that notice of meetings is to be provided to shareholders; |

| • | Include the number of “clear days” that notice is to be served to shareholders in your discussion under “Calls on Ordinary Shares and forfeiture, page 129”; and |

| • | Consider making clear where your bylaws differ from what may be implied by the bulleted list provided under “Exempted Company, page 129”; |

20

January 10, 2014

Page 21

In response to the Staff’s comment, the Company has revised the referenced disclosure on pages 131, 133, 134 and 143 of the Revised Draft Registration Statement.

Taxation, page 150

| 37. | Please revise your disclosure as follows: |

| • | Consider including discussion of Hong Kong tax consequences and considerations, including the extent that treaties between Hong Kong and the PRC may apply; |

| • | Reconcile your discussion of local tax laws in China with your reference in the introductory paragraph under this heading to not discussing state, local and other tax laws; and |

| • | Revise your reference to “certain” tax considerations in the caption and first sentence under “Certain United States Federal Income Tax Considerations” to make clear that you discuss all material tax consequences and considerations. |

In response to the Staff’s comment, the Company has revised disclosure on pages 154 and 155 of the Revised Draft Registration Statement.

Regarding the “Taxation” section, the Company respectfully submits that the “Taxation” section discloses all material jurisdictions (the Cayman Islands, China, and the United States) that are relevant to prospective U.S. investors in connection with their investment in the offering. Although the Company has a subsidiary in Hong Kong, U.S. investors in the offering should not be subject to or directly impacted by taxation in Hong Kong solely as a result of investing in the offering. Accordingly, the Company believes that including Hong Kong in the “Taxation” section would not provide any meaningful information to potential investors.

The Company further advises the Staff that disclosure of taxation in Hong Kong related to the Company’s results of operations is included in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section on page 67 of the Revised Draft Registration Statement.

21

January 10, 2014

Page 22

Consolidated Balance Sheets, page F-3

| 38. | Please revise to include a pro forma balance sheet alongside your most recent historical balance sheet to reflect the conversion of preferred into common stock (excluding effects of offering). |

In response to the Staff’s comment, the Company has revised its unaudited condensed consolidated balance sheet on page F-40 of the Revised Draft Registration Statement to include a pro forma balance sheet as of September 30, 2013 presented alongside the historical balance sheet giving effect to the conversion of the Company’s Series A, B and C convertible redeemable preferred shares into ordinary shares (excluding effects of offering proceeds).

Note 1. Description of Business, Organization, Basis of Presentation and Significant Concentrations and Risks

Note 1(b) Organization, page F-7

| 39. | We direct you to the fourth sentence in the second paragraph of this section on page F-7. You refer to a series of contractual agreements and arrangements “among Tarena International,Beijing Tarena Technology Co., Ltd.(a wholly-owned subsidiary of Tarena International or the “WFOE”)” and the Tarena Entities. Revise to correctly identify the name of the WFOE or explain. We note that Tarena Technologies Inc. is identified as the WFOE in your organizational chart presented on pages 4 and 60. |

In response to the Staff’s comment, the Company has revised the disclosure on page F-7 of the Revised Draft Registration Statement.

| 40. | Please identify the individuals of the board of directors, management and legal representatives of Tarena International, Inc., Tarena Technologies, Inc. and Beijing Tarena. For each of those identified, tell us their percentage of ownership and beneficial voting interest in each entity before and after the conversion of preferred shares into Class B shares and the offering. In your response describe any relationships among those identified (e.g., contractual, familial, business, or otherwise) and specifically including Mr. Shaoyun Han and Mr. Jianguang Li, the nominee shareholders of Beijing Tarena. |

The Company respectfully refers the Staff to the table below for information on (i) the percentage of ownership, (ii) beneficial voting interest and (iii) relationships of the directors, managers and legal representatives identified before the conversion into Class B ordinary shares and the offering.

22

January 10, 2014

Page 23

Tarena International, Inc.

Percentage of ownership | Beneficial voting interest | Relationships among the individuals identified in this table | ||||

Directors | ||||||

Shaoyun Han | 35.4% | 35.4% | Shaoyun Han and Ying Sun are husband and wife | |||

Jianguang Li | 24.4% | 24.4% | none | |||

Yang Zhang | 15.0% | 15.0% | none | |||

Management | ||||||

Suhai Ji | less than 1% | less than 1% | none | |||

Ying Sun | 35.4% | 35.4% | Shaoyun Han and Ying Sun are husband and wife | |||

Yinan Qi | less than 1% | less than 1% | none | |||

Yi Li | less than 1% | less than 1% | none | |||

Jiangyou Wang | less than 1% | less than 1% | none | |||

Xiaolan Tang | less than 1% | less than 1% | none | |||

Legal representative | ||||||

none |

Tarena Technologies, Inc.

Percentage of ownership | Beneficial voting interest | Relationships among the individuals identified in this table | ||||

Directors | ||||||

Shaoyun Han | 0% | 35.4% | Shaoyun Han and Ying Sun are husband and wife | |||

Ying Sun | 0% | 35.4% | Shaoyun Han and Ying Sun are husband and wife | |||

Dan Liu | 0% | less than 1% | none | |||

Yinan Qi | 0% | less than 1% | none | |||

Jiangyou Wang | 0% | less than 1% | none | |||

Management | ||||||

Shaoyun Han | 0% | 35.4% | none | |||

Yi Li | 0% | less than 1% | none | |||

Legal representative | ||||||

Shaoyun Han | 0% | 35.4% | none |

23

January 10, 2014

Page 24

Beijing Tarena

| Percentage of ownership | Relationships among the individuals identified in this table | |||

Directors | ||||

Shaoyun Han | 70% | none | ||

Management | ||||

Shaoyun Han | 70% | none | ||

Yi Li | 0% | none | ||

Legal representative | ||||

Shaoyun Han | 70% | none |

In terms of Shaoyun Han’s voting interest in Beijing Tarena, the Company respectfully advises the Staff that pursuant to the power of attorney granted to Tarena Technologies, Inc. by Mr. Shaoyun Han and acknowledged by Beijing Tarena, Shaoyun Han had irrevocably appointed Tarena Technologies, Inc. as the attorney-in-fact to act on his behalf on all matters pertaining to Beijing Tarena and to exercise all of his rights as a shareholder of Beijing Tarena, including but not limited to attend shareholders’ meetings, vote on his behalf on all matters of Beijing Tarena requiring shareholders’ approval under PRC laws and regulations and the articles of association of Beijing Tarena, and designate and appoint directors and senior management members.

The Company respectfully advises the Staff that the Company currently does not know the number of shares it will issue as part of its initial public offering. Therefore, the Company is unable to calculate the percentage of ownership or beneficial voting interest of any of the persons identified after the initial public offering and the conversion into Class B ordinary shares.

The Company respectfully advises the Staff that the mechanism for re-designating and converting ordinary and preferred shares issued and outstanding prior to the initial public offering into Class B ordinary shares has not been finally determined. However, it is the preliminary consensus of the board and the shareholders of the Company that all ordinary shares and preferred shares issued and outstanding immediately prior to the consummation of the initial public offering will be re-designated or converted into Class B ordinary shares. Therefore, it is expected that the percentage of ownership and beneficial voting interest in the Company of each of the directors and officers of the Company will decrease after the consummation of the initial public offering.

24

January 10, 2014

Page 25

| 41. | We note that you base your determination to consolidate the Tarena Entities on the VIE Agreements, one of which is the Equity Interest Pledge Agreement. Please tell us how you concluded that you are the primary beneficiary despite the fact that the Equity Interest Pledge agreements are not yet effective. |

The Company respectfully advises the Staff that the lack of registration of equity pledge does not affect the WFOE’s ability to enforce its contractual rights against the Tarena Entities’ nominee equity holders as the equity interest pledge agreements have been duly executed and therefore are valid, binding and enforceable as contracts. Notwithstanding the above, the Company did not form its conclusion that it was the primary beneficiary of the Tarena Entities based solely on its rights under the equity interest pledge agreements. Rather, the Company determined that it was the primary beneficiary of the Tarena Entities based on the totality of all the VIE agreements, all of which were effective during the periods presented and have been duly executed. The Company has revised the disclosure on page F-9 of the Revised Draft Registration Statement to clarify that the equity interest pledge agreements are effective and have been duly executed.

| 42. | Revise to clearly present each of the following separately on the face of the statement of financial position per ASC 810-10-45-25: |

| • | Assets of your consolidated VIEs that can be used only to settle obligations of the consolidated VIEs; and |

| • | Liabilities of your consolidated VIEs for which creditors (or beneficial interest holders) do not have recourse to the general credit of the primary beneficiary. |

The Company believes that it had previously presented on the face of its consolidated balance sheets on pages F-3 and F-40 (i) assets of our consolidated VIEs that can be used only to settle obligations of our consolidated VIEs and (ii) liabilities of our consolidated VIEs for which creditors (or beneficial interest holders) do not have recourse to the general credit of the primary beneficiary. The amounts of these VIE assets and liabilities were presented parenthetically on each balance sheet captions to comply with ASC 810-10-45-25.

25

January 10, 2014

Page 26

| 43. | Please disclose how your involvement with the VIEs affects your financial position, financial performance, and cash flows per ASC 810-10-50-2AA(d). |

In response to the Staff’s comment, the Company has revised the disclosure on pages F-11, F-12, F-44 and F-45 of the Revised Draft Registration Statement.

| 44. | We note that you disclose total current and non-current assets and liabilities of your VIEs on page F-20. Expand your disclosure to present the carrying amounts and classification of the VIEs’ assets and liabilities on a more disaggregated basis, including qualitative information about the relationships between those assets and liabilities, and include the intercompany payable to the WFOE for accrued service fees. Please refer to ASC 810-10-50-3(bb). |

In response to the Staff’s comment, the Company has revised the disclosure on pages F-11 and F-44 of the Revised Draft Registration Statement.

| 45. | We refer to ASC 810-10-50-5A(c). Please revise to disclose whether Tarena International or Tarena Tech has provided financial or other support (explicitly or implicitly) during the periods presented to the VIEs that it was not previously contractually required to provide or whether the reporting entity intends to provide that support, including both of the following: |

| • | The type and amount of support, including situations in which the reporting entity assisted the VIE in obtaining another type of support; and |

| • | The primary reasons for providing the support. |

In response to the Staff’s comment, the Company has revised the disclosure on pages F-12 and F-45 of the Revised Draft Registration Statement.

| 46. | We refer to ASC 810-10-50-5A(d). Please revise to comply by disclosing qualitative and quantitative information about your involvement (giving consideration to both explicit arrangements and implicit variable interests) with the VIEs, including, but not limited to, the nature, purpose, size, and activities of the VIEs, including how they are financed. Specifically describe the recognized and unrecognized revenue-producing assets that are held by the VIEs. These assets may include licenses, trademarks, other intellectual property, facilities or assembled workforce. |

26

January 10, 2014

Page 27

In response to the Staff’s comment, the Company has revised the disclosure on page F-7 of the Revised Draft Registration Statement.

| 47. | Please expand your disclosures of risks in relation to the VIE structure to disclose risks related to potential conflicts of interests. Your disclosure should describe the relationships that result in the potential conflicts of interests. |

In response to the Staff’s comment, the Company has revised the disclosure on pages F-10 and F-43 of the Revised Draft Registration Statement.

Note 1(c) Basis of Presentation, page F-10

| 48. | Revise to comply with ASC 275-10-50-4 regarding management’s estimates used in the preparation of financial statements in conformity with US GAAP. |

The Company respectfully advises the Staff that it had previously provided the disclosures required under ASC 275-10-50-4 and refers to the Staff note 2(b) to the consolidated financial statements on page F-13.

Note 2. Summary of Significant Accounting Policies

Off-Balance Sheet Commitments and Arrangements

| 49. | We note from your disclosures on page F-23, that you serve as the guarantor of loans taken out by students from Chuanbang, a credit-sourcing company owned by Mr. Shaoyun Han, your chief executive officer. Please refer to ASC 310-10-50-9 and 10 and revise to provide a description of the accounting policies and methodology used to estimate your liability for off-balance-sheet credit exposures and related charges for those credit exposures. |

In response to the Staff’s comment, the Company has revised the disclosure on page F-17 of the Revised Draft Registration Statement.

27

January 10, 2014

Page 28

Note 2(e) Accounts Receivable, page F-12

| 50. | Revise to disclose your policy for determining past due or delinquency status of accounts receivable. Please refer to ASC 310-10-50-6(e). |

In response to the Staff’s comment, the Company has revised the disclosure on page F-14 of the Revised Draft Registration Statement.

| 51. | Revise to disclose your policy for charging off uncollectible accounts receivable in accordance with ASC 310-10-50-4A. |

In response to the Staff’s comment, the Company has revised the disclosure on page F-14 of the Revised Draft Registration Statement.

Note 3. Accounts Receivable, page F-18

| 52. | Revise to provide the disclosures required by ASC 310-10-50-7 and 7(A), including an analysis of the age of accounts receivable at the end of the reporting period that are considered to be past due. |

In response to the Staff’s comment, the Company has revised the disclosure on pages F-20 and F-47 of the Revised Draft Registration Statement.

| 53. | Please tell us the basis upon which you determine your allowance for doubtful accounts and how you have considered your historical experience, which indicates that you have not written off any bad debts during any of the periods presented. |

The Company respectfully advises the Staff that in determining the allowance for doubtful accounts for estimated losses resulting from the inability of our students to make the required payments, it considered other factors besides historical write-offs experience. These other factors consisted of the students’ financial condition, the amount of accounts receivable in dispute, the accounts receivable aging and the students’ payment patterns. The Company further advises the Staff that there is always a time lag between when the Company estimates a portion of or the entire account balances to be uncollectible and when a write off of the account balances is taken. The Company takes a write off of the account balances when it meets the requirements as a tax deductible item. That is, either the Company can demonstrate all means of collection on the outstanding balances have been exhausted or the balances have been overdue for more than three years. In response to the Staff’s comment, the Company has revised the disclosure on page F-14 of the Revised Draft Registration Statement.

28

January 10, 2014

Page 29

Note 8. Income Taxes, page F-20

| 54. | Please revise to provide the following disclosures in accordance with ASC 740-10-50- 15(d). For positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly increase or decrease within 12 months of the reporting date, describe: |

| • | The nature of the uncertainty; |

| • | The nature of the event that could occur in the next 12 months that would cause the change; and |

| • | An estimate of the range of the reasonably possible change or a statement that an estimate of the range cannot be made. |

In response to the Staff’s comment, the Company has revised the disclosure on page F-25 of the Revised Draft Registration Statement.

| 55. | Please provide us with an analysis of your current tax provision for each of your tax jurisdictions, specifically including your VIEs and WFOEs. Please provide sufficient information to allow us to understand how the components reconcile to your consolidated tax provision. |

In response to the Staff’s comment, the Company has set forth below the analysis of current tax provision for each of our tax jurisdictions, specifically including our consolidated VIEs and WFOEs.

| Year Ended December 31, 2012 | ||||||||||||||||

| Income before income taxes | Current income tax expense | Deferred income tax expense (benefit) | Total income tax expense | |||||||||||||

| US$ | US$ | US$ | US$ | |||||||||||||

PRC: | ||||||||||||||||

Wholly-owned subsidiaries | 7,449,071 | 1,529,695 | (27,230 | ) | 1,502,465 | |||||||||||

Consolidated VIEs | 4,324,377 | 710,606 | 6,039 | 716,645 | ||||||||||||

Hong Kong | (280 | ) | — | — | — | |||||||||||

Cayman Islands | (1,587 | ) | — | — | — | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | 11,771,581 | 2,240,301 | (21,191 | ) | 2,219,110 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

29

January 10, 2014

Page 30

| Year Ended December 31, 2011 | ||||||||||||||||

| Income before income taxes | Current income tax expense | Deferred income tax benefit | Total income tax expense | |||||||||||||

| US$ | US$ | US$ | US$ | |||||||||||||

PRC: | ||||||||||||||||

Wholly-owned subsidiaries | 1,189,236 | 113,684 | (229,179 | ) | (115,495 | ) | ||||||||||

Consolidated VIEs | 2,138,071 | 410,473 | (155,863 | ) | 254,610 | |||||||||||

Hong Kong | — | — | — | — | ||||||||||||

Cayman Islands | (2,487,510 | ) | — | — | — | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | 839,797 | 524,157 | (385,042 | ) | 139,115 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

| 56. | Please revise to describe the nature and effect of all significant matters affecting comparability of information for all periods presented per ASC 740-10-50-14. |

In response to the Staff’s comment, the Company has revised the disclosure on page F-23 of the Revised Draft Registration Statement.

Note 9. Related Party Transactions, page F-23

| 57. | Please tell us in detail about the nature of Connion Capital Ltd. and Chuanbang Business Consulting (Beijing) Co. Ltd., entities which are both wholly-owned by Mr. Han, and the extent of your involvement in their activities. |

The Company respectfully advises the Staff that Connion Capital Ltd., is an investment holding company and wholly-owned by Mr. Shaoyun Han.Connion Capital Ltd. does not have any operations or have subsidiaries engaged in operations. Other than the repurchase of our ordinary shares held by Connion Capital Ltd. in September 2011, the Company had no other transactions or involvements with Connion Capital Ltd. (including providing financial or other support) during the periods presented.

30

January 10, 2014

Page 31

Chuanbang Business Consulting (Beijing) Co., Ltd. (“Chuanbang”) is a company engaged in the provision of person-to-person lending service and provision of collection service in China.

The person-to-person or peer-to-peer (“P2P”) lending service of Chuanbang is made available to students of the Company. The Company’s involvement with Chuanbang consisted of (i) referring students who require student loans to finance their tuition to the P2P service providers, such as Chuanbang and CreditEase, and (ii) starting from August 2013, engaging Chuanbang to provide cash collection service on the Company’s receivable for a fee. The Company has no involvements with Chuanbang (including providing financial or other support) other than the aforementioned activities.

| 58. | We note that Chuanbang acts as an intermediary to facilitate P2P lending with your students. Please revise to describe the business reason for including Chuanbang as an intermediary in the lending process and describe the role of the third-party P2P lenders. |

In response to the Staff’s comment, the Company has revised the disclosure on page F-26 of the Revised Draft Registration Statement.

| 59. | Your disclosures regarding your Student Loan Program on pages 20, 125 and herein are inconsistent. To help us understand the program please describe in more detail the lending process from the time the student request financial assistance up to when the loan is collected. Also please tell us the parties involved at each phase of the lending process. |

The Company respectfully advises the Staff that the Student Loan Program operates in the following manner:

| Phases of the Student Loan Program | Parties involved | |

1. A student makes a loan request to Chuanbang, the P2P lending intermediary. | Student; Chuanbang | |

2. Chuanbang performs borrower credit checks and filters out unqualified students. Students that qualify enter into a loan agreement with Mr. Shaoyun Han, the designated representative of Chuanbang. | Student; Mr. Shaoyun Han; Chuanbang | |

31

January 10, 2014

Page 32

| 3. Shortly thereafter, the student loans are assigned to a third-party individual lender. Generally, the student loans arranged or identified by Chuanbang meet the lending criteria of the third party lender. Pursuant to the assignment agreement, Chuanbang is responsible for processing the student repayment of the loan and forwarding the repayment to the third party lender. Chuanbang retains a certain percentage of the interest rate (“interest rate differential”) as compensation. See phase 7 below. The Company guarantees the student loans that are assigned to the third-party individual lender. | Mr. Shanyun Han; third-party individual lender; Chuanbang; the Company | |

| 4. The third-party individual lender remits the loan amount to a bank account opened in the name of Mr. Shaoyun Han. The third-party individual lender remits the loan amount to Mr. Shaoyun Han, the representative of Chuanbang, rather than directly to the Company, because the P2P lending arrangement is between Chuanbang (rather than the Company) and the third party individual lender. The Company has no direct involvement in or is a party to the P2P lending arrangement, other than serving as the guarantor of the student loan. | Mr. Shaoyun Han; third-party individual lender | |

| 5. Mr. Shaoyun Han transfers the money received from the third-party individual lender to the Company’s bank account as payment for the tuition fees of the student. | Mr. Shaoyun Han; the Company; student | |

| 6. The student makes monthly loan repayments to the bank account opened in the name of Mr. Shaoyun Han. | Student; Mr. Shaoyun Han | |

| 7. Mr. Shaoyun Han processes payments from student borrowers and forwards those payments to the third-party individual lender (after deducting an interest rate differential as a form of compensation to Chuanbang). | Mr. Shaoyun Han; third-party individual lender | |

32

January 10, 2014

Page 33

In response to the staff’s comment, we have made revisions on pages 21 and 129 to be consistent with pages F-26.

| 60. | In addition it is unclear to us why the third-party lenders remit cash directly to Mr. Han rather than to the company. Further we note that Mr. Han assigned the loans to the third-party lenders; if true, it would appear that the student should make their payments directly to the third party lenders. Please advise. |

The Company respectfully advises the Staff that as described in the responses to comments 58 and 59, Chuanbang, the P2P lending intermediary assists the students in obtaining loans to pay for their tuition fees by identifying potential third-party individual lenders. The third-party lenders remit the loan amount to Mr. Han, who is a representative of Chuanbang, rather than directly to the Company, because the P2P arrangement is between Chuanbang and the third party individual lenders. The Company has no direct involvement in or is a party to the P2P arrangement, other than serving as the guarantor. As a P2P intermediary and pursuant to the relevant agreements between the two parties, Chuanbang is responsible for processing payments from student borrowers and forwarding those payments to individual lenders.

The Company has revised its disclosure on page F-26 to clarify the above P2P arrangements in regards to the remittance of the loan amount from the third-party lenders and the processing of the student loan repayments by Chuanbang.

| 61. | We note that as of December 31, 2012, the company’s maximum exposure to guarantees of student loans was $7.4 million. Please tell us whether you recognized a liability for your guarantee under the Student Loan Program in accordance with ASC 460-10-25-4 and if so, how you determined such amount. If no liability was recognized, please tell us your basis for that conclusion and how you determined there was no value to the guarantee. |

The Company respectfully advises the Staff that upon the inception of the guarantee, the Company recognized an initial liability based on the estimated fair value of the guarantee. The estimated fair value of the guarantee was determined based on what premium would be required by the guarantor to issue the same guarantee in a stand-alone arm’s length

33

January 10, 2014

Page 34

transaction with an unrelated party. In response to the Staff’s comment, the Company has revised the disclosure on page F-26 and F-50 of the Revised Draft Registration Statement.

| 62. | Please revise to comply with the disclosure requirements of ASC 460-10-50-4, with respect to your guarantee of payments under the Student Loan Program, including, but not limited to the following: |

| • | The approximate term of the guarantees; |

| • | The events or circumstances that would require you to perform under the guarantee; |

| • | The current status of the payment/performance risk of the guarantee; |

| • | The maximum potential amount of future payments on an undiscounted basis, if the amount disclosed on page F-23 is discounted, that you could be required to make under the guarantee; and |

| • | The current carrying amount of the liability, if any, for your obligations under the guarantees. |

In response to the Staff’s comment, the Company has revised the disclosure on pages F-26 and F-50 of the Revised Draft Registration Statement.

Tarena International Inc. and Subsidiaries

Notes to Consolidated Financial Statements

Note 1(a) Organization, page F-39

| 63. | We refer to the table disclosing total assets and liabilities of the Tarena Entities as of September 30, 2013 and December 31, 2012. The amounts presented do not appear to be consistent with disclosures elsewhere in your registration statement. For example, on page 4 you disclose that total assets of the consolidated VIEs represented 7.1% of total assets at September 30, 2013; however, on page F-39, you report total assets of your consolidated VIEs in the amount of $11.9 million which represents approximately 16% of total assets. Please revise to clarify the differences in amounts presented throughout your document. |

The Company respectfully advises the Staff that the percentage on page 4 excludes the amounts due from Tarena International and its wholly-owned subsidiaries in the amount of US$6.5 million as of September 30,

34

January 10, 2014

Page 35

2013, which are eliminated on consolidation. Total assets excluding the amounts due from Tarena International and its wholly-owned subsidiaries were US$5.0 million which represents 7.1% of the consolidated total assets as of September 30, 2013. In response to the Staff’s comment, the Company has revised the disclosure on pages F-11 and F-44 of the Revised Draft Registration Statement to separately present amounts due from Tarena International and its wholly-owned subsidiaries and indicate that such amounts are eliminated on consolidation.

| 64. | We note that in 2012 you began to transfer most of the operations, including related assets and liabilities of VIEs to the wholly-owned subsidiaries of Tarena International, and that as of September 30, 2013 Tarena International is still in the process of transferring the remaining learning center operations of the VIEs to other subsidiaries of Tarena International. Please expand your disclosure to describe the operations, licenses, and other revenue-producing assets that were transferred to Beijing Tarena and Shanghai Tarena and describe those operations, licenses, assets and liabilities that will remain with the VIE. Please also revise to disclose the expected transfer completion date of the remaining 12 learning centers. |

In response to the Staff’s comment, the Company has revised the disclosure on page F-7 of the Revised Draft Registration Statement.

| 65. | Please tell us how you accounted for the transfer of assets and related liabilities of your VIEs to the wholly-owned subsidiaries of Tarena International. |

The Company respectfully advises the Staff that the Company accounted for the transfer of assets and liabilities of Tarena Entities to the wholly-owned subsidiaries of Tarena International at their historical carrying amounts. The Tarena Entities and the wholly-owned subsidiaries of Tarena International are both under common control of Tarena International immediately prior to and after such transfer.

* * *

35

If you have any questions regarding the Revised Draft Registration Statement, please contact the undersigned by phone at +852-3740-4850 or via e-mail at julie.gao@skadden.com. Questions pertaining to accounting and auditing matters may be directed to the audit engagement partner at KPMG Huazhen (SGP), Francis Duan, by telephone at +86-10-8508-7802, or by email at francis.duan@kpmg.com, or the filing review partner at KPMG Huazhen (SGP), David Kong, by telephone at 86-10-8508-7033, or by email at david.kong@kpmg.com. KPMG Huazhen (SGP) is the independent registered public accounting firm of the Company.

/s/ Z. Julie Gao |

| Very truly yours, |

| Z. Julie Gao |

Enclosures

| cc: | Shaoyun Han, Chairman and Chief Executive Officer, Tarena International, Inc. |

Suhai Ji, Chief Financial Officer, Tarena International, Inc.

David Kong, KPMG Huazhen (SGP)

Francis Duan, KPMG Huazhen (SGP)

David Roberts, O’Melveny & Myers LLP

Ke Geng, O’Melveny & Myers LLP

Annex A

Industry Data Backup Chart

Item | Statement in the Latest F-1 | Page No. in the Latest | Source Location | |||

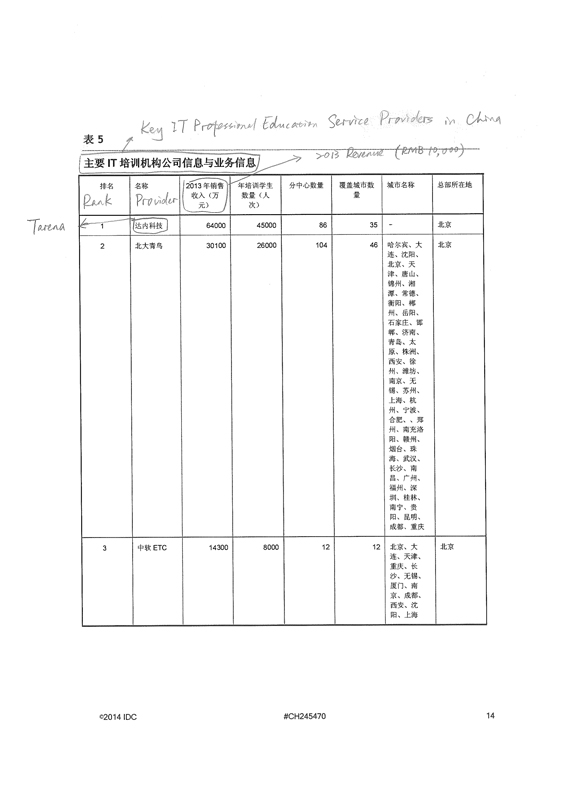

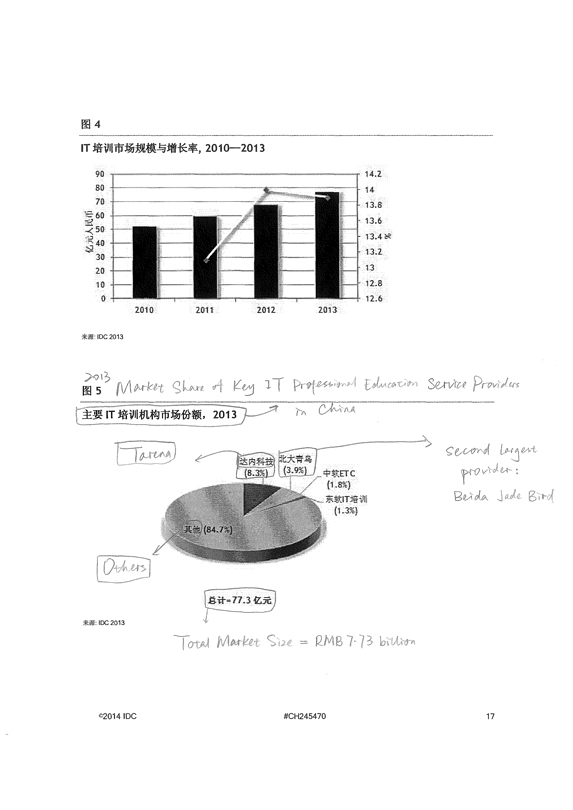

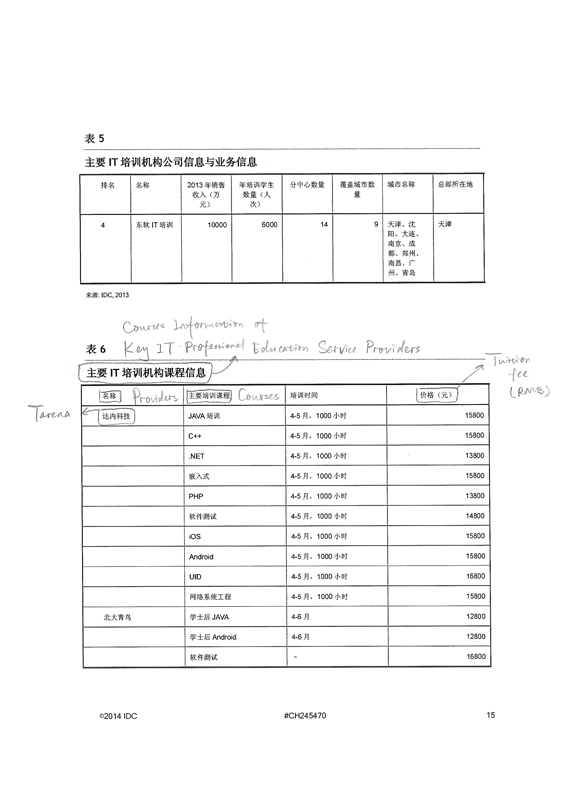

| 1. | Our core strength is in IT professional education services, where we are the largest provider in China with a market share of 8.3% as measured by revenues in 2013 according to IDC, a third-party research firm. | p.1, 67, 89 | IDC Report, pages 14, 17 | |||

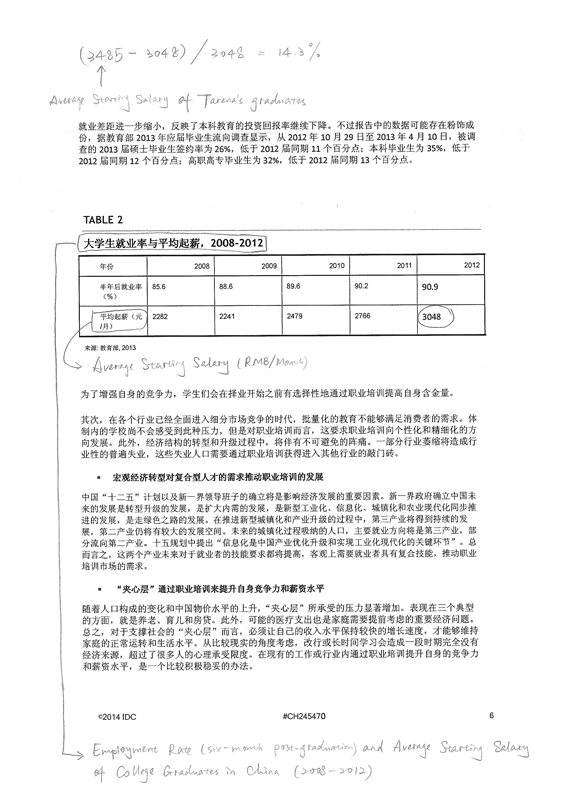

| 2. | The average starting salary of our students enrolled in 2012 was 14.3% higher than the national average of college graduates in 2012, calculated based on data from IDC. | p.1, 89 | IDC Report, page 6 | |||

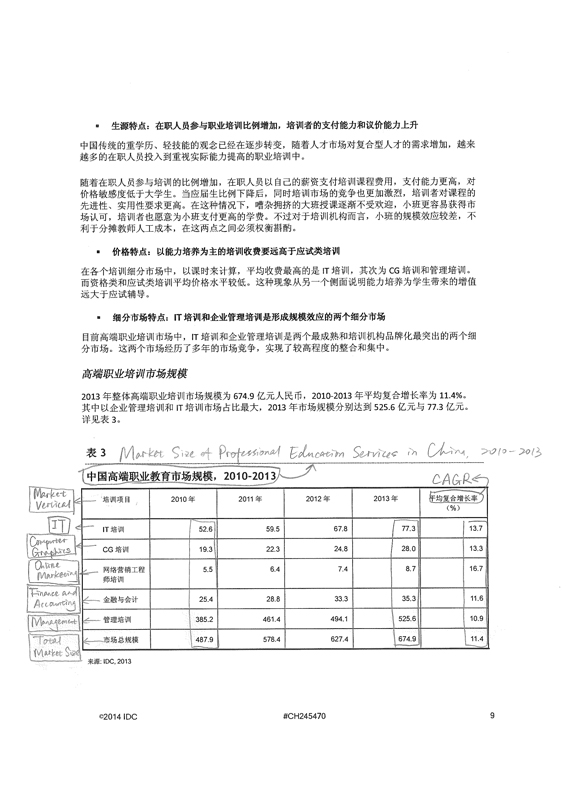

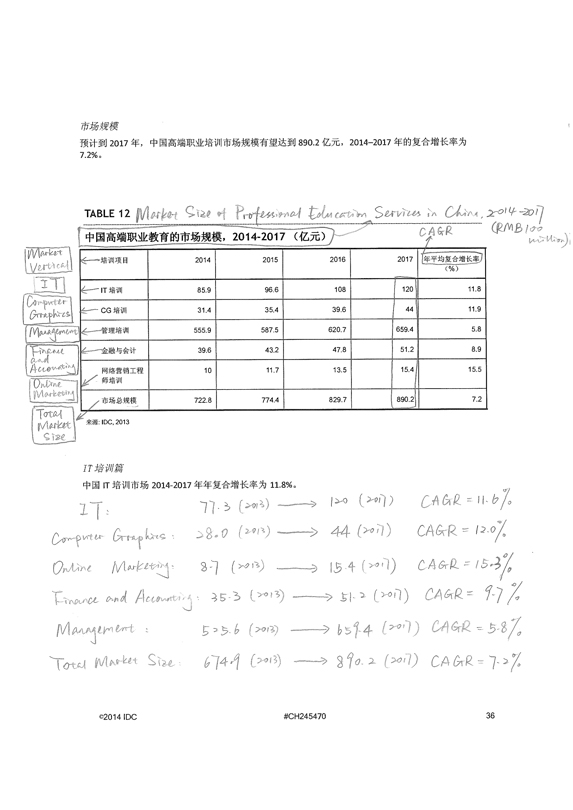

| 3. | According to IDC, the market size of professional education services in China, which includes industries with high employment demand such as IT, computer graphics, online marketing, finance and accounting, and management, grew from RMB48.8 billion (US$8.0 billion) in 2010 to RMB67.5 billion (US$11.0 billion) in 2013, representing a compound annual growth rate, or CAGR, of 11.4% and is projected to grow to RMB89.0 billion (US$14.5 billion) in 2017, representing a CAGR of 7.2% from 2013 to 2017. | p.2-3, 85 | IDC Report, pages 9, 36 | |||

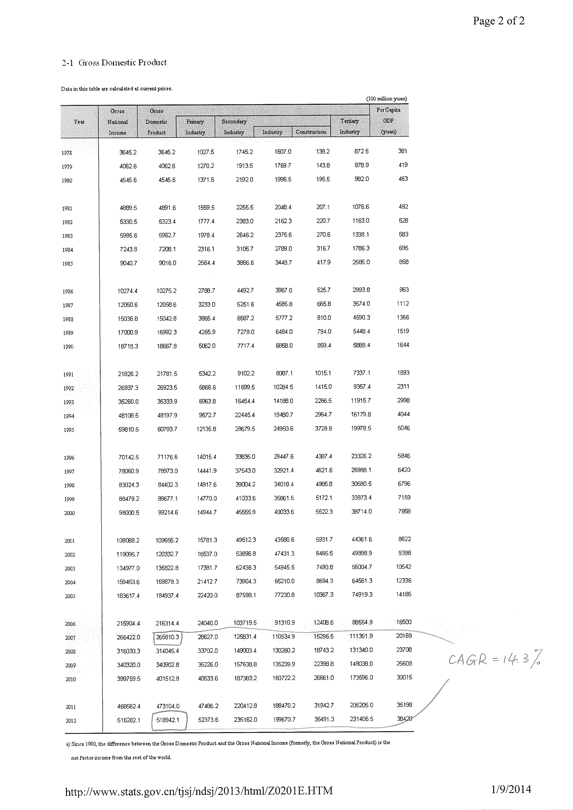

| 4. | According to the National Bureau of Statistics of China, or NBSC, China’s GDP reached RMB51.9 trillion (US$8.5 trillion) in 2012, representing a CAGR of 14.3% from 2007. | p.85 | Sources publicly available from the National Bureau of Statistics of China

http://www.stats.gov.cn/tjsj/ndsj/2013/indexeh.htm(2012 GDP: 2-1 Gross Domestic Product ) | |||

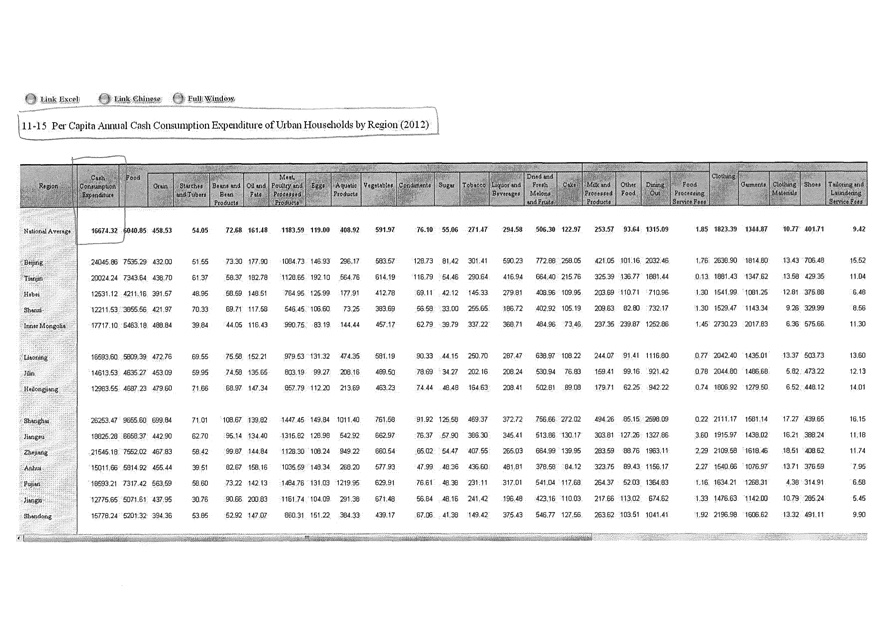

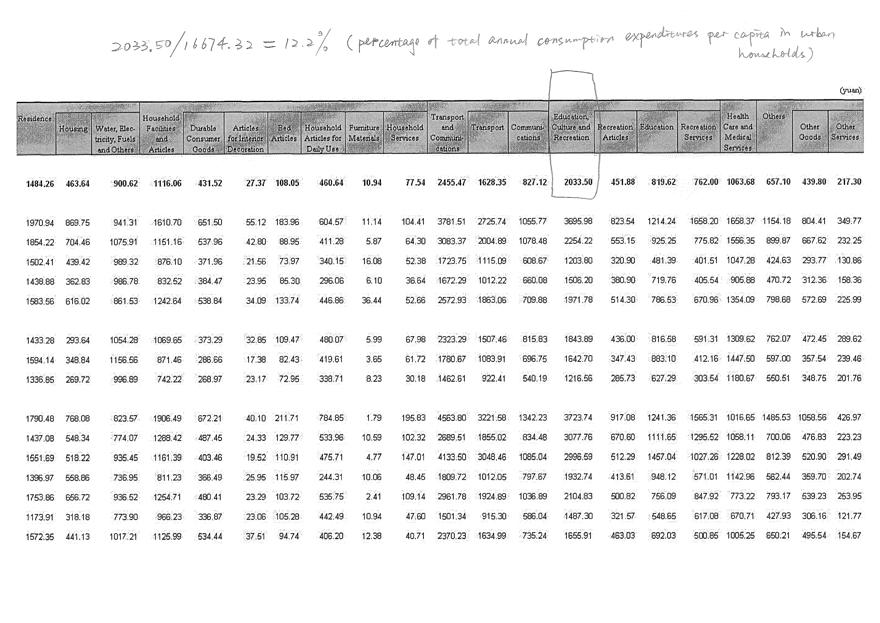

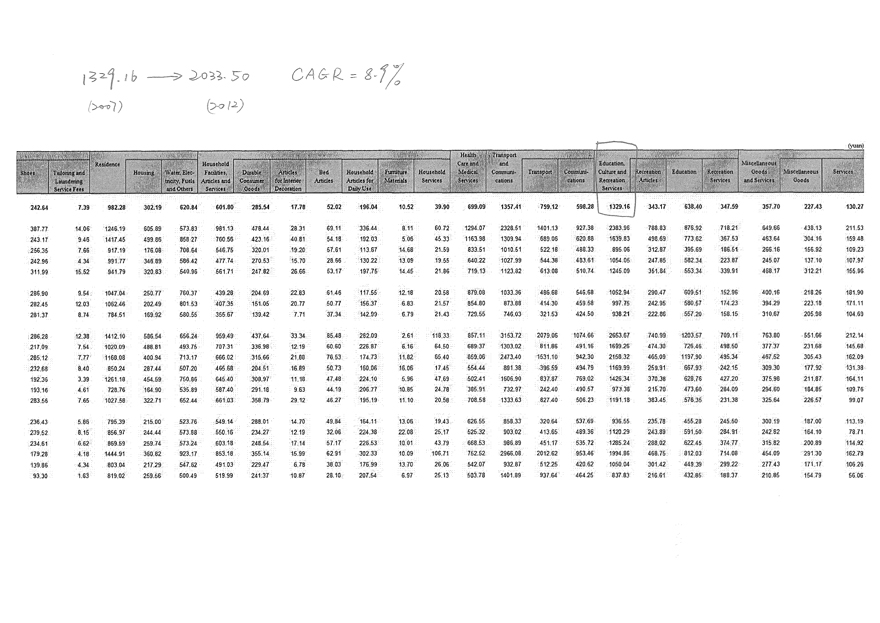

| 5. | In addition, annual consumption expenditure on education, cultural and recreational services per capita in urban households reached RMB2,034 (US$332.3) in 2012, representing a CAGR of 8.9% from 2007 according to NBSC. | p.85 | Sources publicly available on the website of the National Bureau of Statistics of China

http://www.stats.gov.cn/tjsj/ndsj/2013/indexeh.htm[2012 data: 11-15 Per Capita Annual Cash Consumption Expenditure of Urban Households by Region (2012)] | |||

Annex A-1

Item | Statement in the Latest F-1 | Page No. in the Latest | Source Location | |||

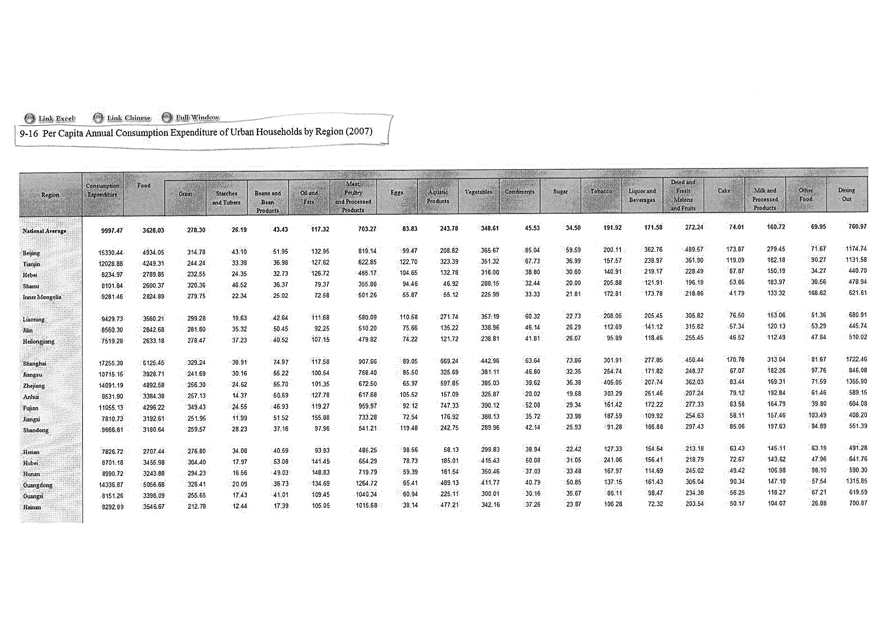

| http://www.stats.gov.cn/tjsj/ndsj/2008/indexeh.htm [2007 data: 9-16 Per Capita Annual Consumption Expenditure of Urban Households by Region (2007)] | ||||||

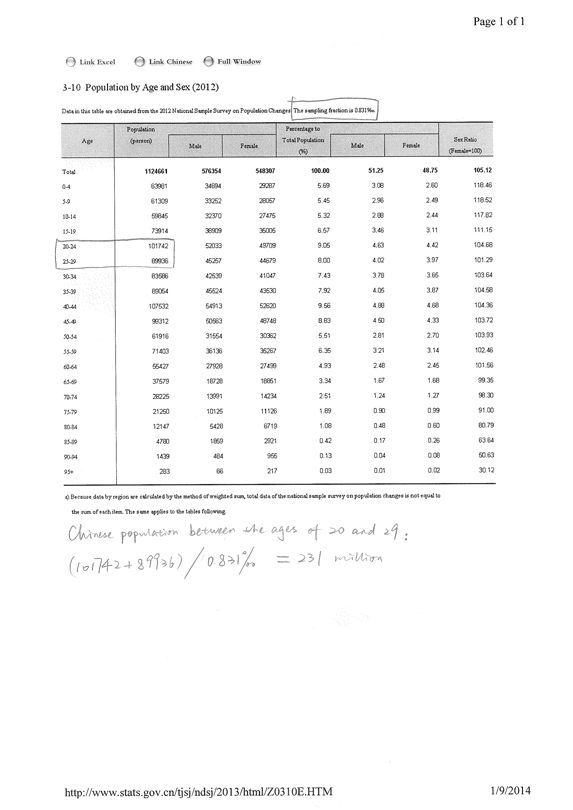

| 6. | Based on figures cited in NBSC’s 2013 China Statistical Yearbook, the Chinese population between the ages of 20 and 29 reached 231 million in 2012. | p.85 | Sources publicly available on the website of the National Bureau of Statistics of China

http://www.stats.gov.cn/tjsj/ndsj/2013/indexeh.htm[3-10 Population by Age and Sex (2012)] | |||

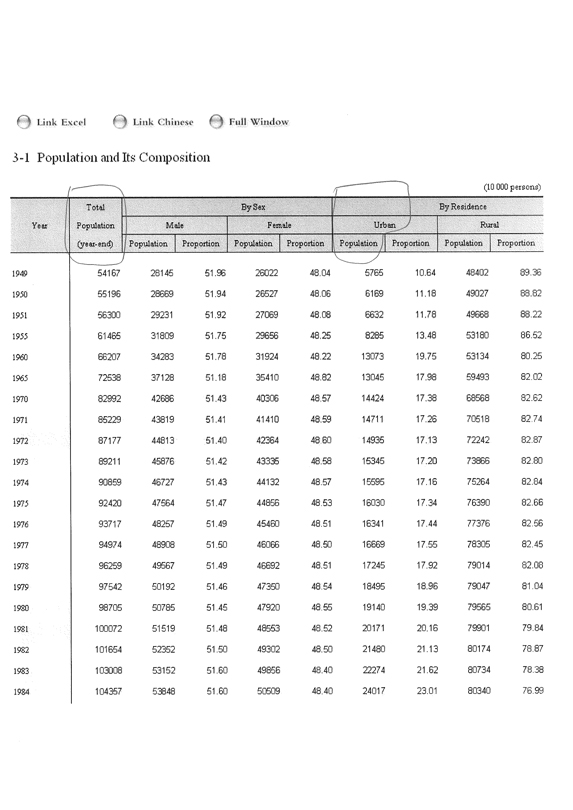

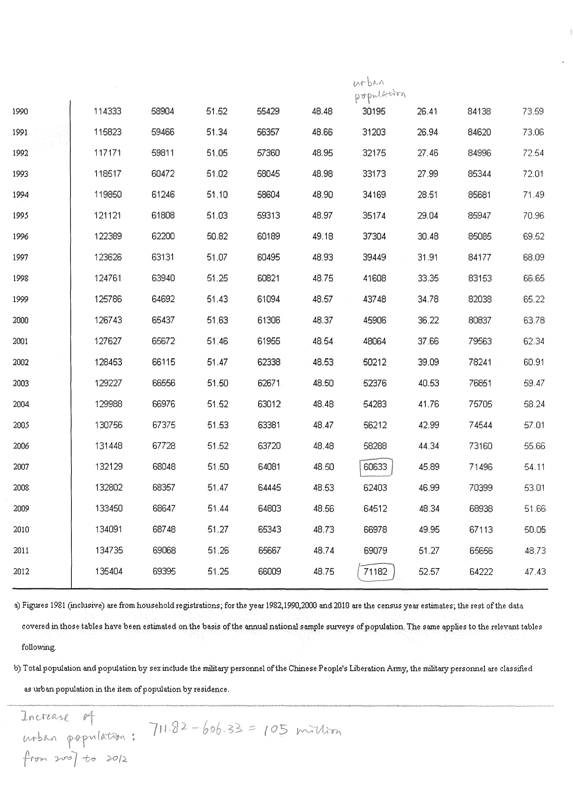

| 7. | China has also experienced tremendous urban population growth, which increased by 105 million from 2007 to 2012, according to the NBSC. | p.85 | Sources publicly available on the website of the National Bureau of Statistics of China

http://www.stats.gov.cn/tjsj/ndsj/2013/indexeh.htm(2012 & 2007 urban population) | |||

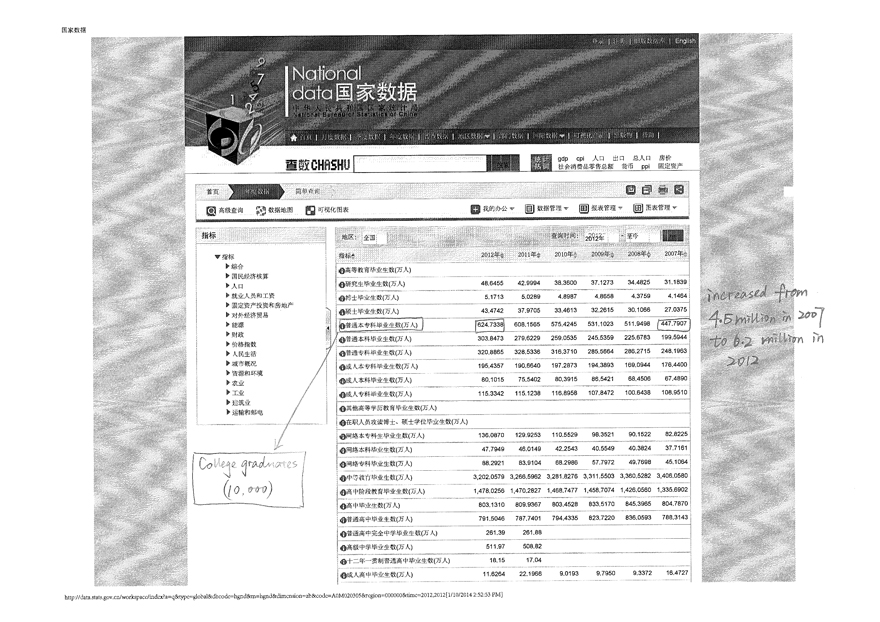

| 8. | According to NBSC, the number of college graduates in China increased from 4.5 million in 2007 to 6.2 million in 2012. | p.85 | Sources publicly available on the website of the National Bureau of Statistics of China Database

http://data.stats.gov.cn/workspace/index?a=q&type=global&dbcode =hgnd&m=hgnd&dimension=zb &code=A0M020305®ion=000000&time=2012,2012(number of college graduates in China from 2007 to 2012) | |||

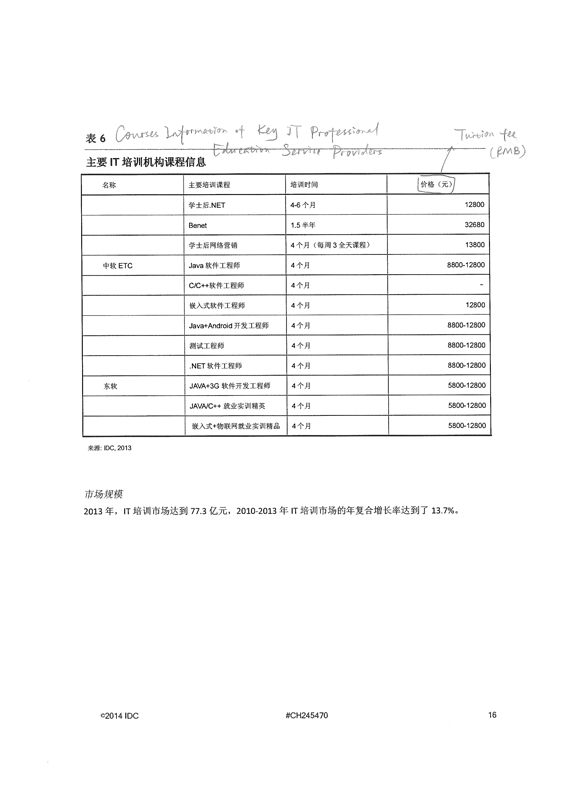

| 9. | According to IDC, the IT professional education services market in China grew from RMB5.3 billion (US$859 million) in 2010 to RMB7.7 billion (US$1.3 billion) in 2013, representing a CAGR of 13.7%, and is expected to further grow at a CAGR of 11.6% to RMB12.0 billion (US$2.0 billion) in 2017. | p.87 | IDC Report, pages 9, 36 | |||

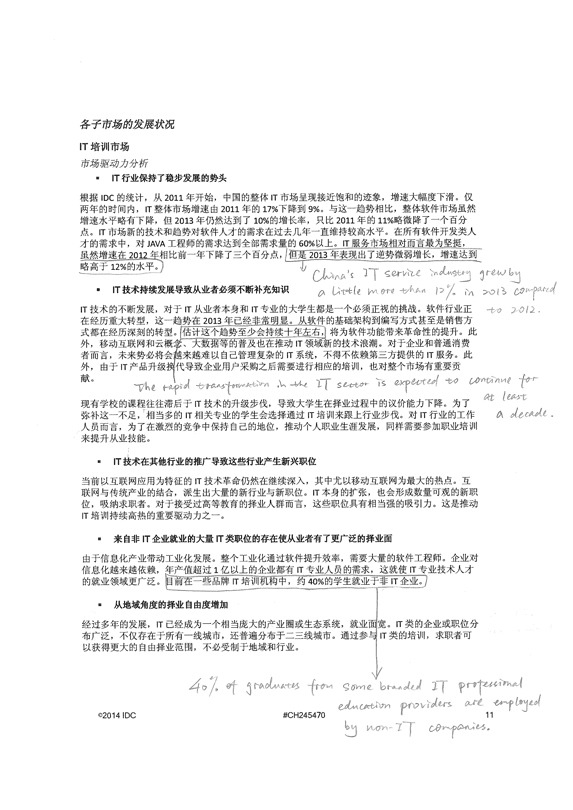

| 10. | According to IDC, China’s IT services industry grew at a CAGR of 12% in 2013 compared to 2012. | p.87 | IDC Report, page 11 | |||

Annex A-2

Item | Statement in the Latest F-1 | Page No. in the Latest F-1 | Source Location | |||