UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

10-K/A

Amendment No. 1

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended September 30, 2019

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. | Name of Registrant, State of Incorporation, Address of Principal Offices, and Telephone No. | IRS Employer Identification No. | ||||||||||

1-4219 | Spectrum Brands Holdings, Inc. (a Delaware corporation) 3001 Deming Way, Middleton, WI 53562 (608) 275-3340 www.spectrumbrands.com | 74-1339132 | ||||||||||

SB/RH Holdings, LLC | ||||||||||||

333-192634-03 | (a Delaware limited liability company) 3001 Deming Way, Middleton, WI 53562 (608) 275-3340 | 27-2812840 | ||||||||||

Securities registered pursuant to Section 12(b) of the Act:

Registrant | Title of each class | Name of each exchange on which registered | ||||||||||

Spectrum Brands Holdings, Inc. | Common Stock, Par Value $0.01 | New York Stock Exchange | ||||||||||

SB/RH Holdings, LLC | None | None | ||||||||||

Securities registered pursuant to Section 12(g) of the Act:

NoneIndicate by check mark if the registrants are well-known seasoned issuers, as defined in Rule 405 of the Securities Act.

Spectrum Brands Holdings, Inc. | Yes ☒ | No ☐ | ||||

SB/RH Holdings, LLC | Yes ☐ | No ☒ |

Indicate by check mark if the registrants are not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Spectrum Brands Holdings, Inc. | Yes ☐ | No ☒ | ||||

SB/RH Holdings, LLC | Yes ☐ | No ☒ |

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Spectrum Brands Holdings, Inc. | Yes ☒ | No ☐ | ||||

SB/RH Holdings, LLC | Yes ☒ | No ☐ |

Indicate by check mark whether the registrants have submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation

S-T

(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).Spectrum Brands Holdings, Inc. | Yes ☒ | No ☐ | ||||

SB/RH Holdings, LLC | Yes ☒ | No ☐ |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company in Rule 12b-2 of the Exchange Act.:Registrant | Large Accelerated Filer | Accelerated Filer | Non-accelerated Filer | Smaller Reporting Company | Emerging Growth Company | |||||||||||||||

Spectrum Brands Holdings, Inc. | X | |||||||||||||||||||

SB/RH Holdings, LLC | X | |||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Spectrum Brands Holdings, Inc. | ☐ | |||

SB/RH Holdings, LLC | ☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Spectrum Brands Holdings, Inc. | Yes ☐ | No ☒ | ||||

SB/RH Holdings, LLC | Yes ☐ | No ☒ |

The aggregate market value of the voting stock held by

non-affiliates

of Spectrum Brands Holdings, Inc. was approximately $2,439 million based upon the closing price on the last business day of the registrant’s most recently completed second fiscal quarter (March 31, 2019). For the sole purposes of making this calculation, term“non-affiliate”

has been interpreted to exclude directors and executive officers and other affiliates of the registrant. Exclusion of shares held by any person should not be construed as a conclusion by the registrant, or an admission by any such person, or that such person is an “affiliate” of the Company, as defined by applicable securities law.As of January 6, 2020, there were outstanding 46,045,746 shares of Spectrum Brands Holdings, Inc.’s common stock, par value $0.01 per share.

SB/RH Holdings, LLC meets the conditions set forth in General Instruction I(1)(a) and (b) of Form and has therefore omitted the information otherwise called for by Items 10 to 13 of Form as allowed under General Instruction I(2)(c).

10-K

10-K

DOCUMENTS INCORPORATED BY REFERENCE

None.

EXPLANATORY NOTE

Spectrum Brands Holdings, Inc. and SB/RH Holdings, LLC are filing this Amendment No. 1 (this “Form 10-K/A”) to their Annual Report on Form 10-K for the fiscal year ended September 30, 2019 (“Fiscal 2019”) that was filed with the Securities and Exchange Commission (“SEC”) on November 15, 2019 (the “Original Form 10-K”) for the sole purpose of including certain of the information required by Part III of Form 10-K. As required by Rule 12b-15, in connection with this Form 10-K/A, the Company’s Principal Executive Officer and Principal Financial Officer are providing Rule 13a-14(a) certifications included herein.

Except as explicitly set forth herein, this Form 10-K/A does not purport to modify or update the disclosures in, or exhibits to, the Original Form 10-K, or to update the Original Form 10-K to reflect events occurring after the date of such filing.

TABLE OF CONTENTS

Page

| 1 | ||||||

| ITEM 10. | 1 | |||||

| ITEM 11. | 17 | |||||

| ITEM 12. | 51 | |||||

| ITEM 13. | 53 | |||||

| 55 | ||||||

| ITEM 15. | 55 | |||||

| 55 | ||||||

i

PART III

As disclosed in our prior filings, on July 13, 2018 (the “Merger Closing Date”), HRG Group, Inc. (now known as Spectrum Brands Holdings, Inc.) completed a merger (the “Merger”) with its majority owned subsidiary, Spectrum Brands Legacy, Inc. (formerly known as Spectrum Brands Holdings, Inc.). Following the completion of the Merger, HRG Group, Inc. changed its name to Spectrum Brands Holdings, Inc. Except as otherwise specified, all references herein to (i) the “Company,” “Spectrum Brands,” “we,” “us” or “our” refer to Spectrum Brands Holdings, Inc. (formerly known as HRG Group, Inc.) prior to and after the Merger Closing Date; (ii)“SPB Legacy” refers to Spectrum Brands Legacy, Inc. (formerly known as Spectrum Brands Holdings, Inc.) solely prior to the Merger Closing Date; (iii) “HRG Legacy” refers to HRG Group, Inc. (now known as Spectrum Brands Holdings, Inc.) solely prior to the Merger Closing Date; (iv) “New SPB” refers to Spectrum Brands Holdings, Inc. (formerly known as HRG Group, Inc.) solely after the Merger Closing Date; (v) “Board” refers to the Board of Directors of Spectrum Brands Holdings, Inc. (formerly known as HRG Group, Inc.) prior to and after the Merger Closing Date; and (vi) “Fiscal” refers to fiscal year ended September 30 of each applicable year.

ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE |

Our Board of Directors

Our directors are elected at each annual meeting of shareholders and hold office for staggered three-year terms. Our Nominating and Corporate Governance Committee (“NCG Committee”) considers and chooses nominees for our Board with the primary goal of presenting a well-qualified slate of candidates who will serve the interests of our Company and our shareholders, taking into account the attributes of each candidate’s professional skillset and credentials, as well as gender, age, ethnicity and personal background. In evaluating nominees, our NCG Committee reviews each candidate’s background and assesses each candidate’s independence, skills, experience and expertise based upon a number of factors. We seek directors with the highest professional and personal ethics, integrity and character that have experience at the governance and policy-making level in their respective fields. Our NCG Committee reviews the professional background of each candidate to determine whether each candidate has the appropriate experience and the ability to effectively make important decisions as a member on our Board. Our NCG Committee also determines whether a candidate’s skills and experience complement and enhance the collective skills and experience of our existing Board members.

We are committed to ensuring that female and minority candidates are among the pool of individuals from which new Board nominees are selected. During Fiscal 2019, we made progress in advancing this objective by appointing to our Board a female candidate from a diverse background. We are committed to further progressing this objective in Fiscal 2020.

Our directors collectively represent a robust and diverse set of skills and experience, which we believe positions our Board and its committees well to effectively oversee the execution of our business strategy and to advance the interests of the Company and its stakeholders. The following table summarizes some of the key categories of skills and experience of our current directors:

Director Skills and Experience | |||

✓ 83% | ✓ 100% | ||

✓ 67% | ✓ 100% | ||

✓ 100% | ✓ 83% | ||

✓ 83% | ✓ 83% | ||

✓ 83% | ✓ 83% | ||

✓ 67% | ✓ 83% | ||

✓ 83% Mergers & Acquisitions | ✓ 67 % | ||

1

In accordance with our Third Restated

By-laws,

our Board currently consists of eight members. In accordance with our Amended and Restated Certificate of Incorporation (our “Charter”), our Board is divided into three classes (designated as Class I, Class II, and Class III, respectively). Two of the eight seats on the Board are currently vacant as we search for appropriate candidates to fill the recently created vacancies. The names of our six current directors and their respective classes, ages, Board tenures and committee memberships are each set forth in the following table:Committee Membership*** | |||||||||||||||

Name | Class* | Age | Tenure** | A | C | NCG | |||||||||

Sherianne James Independent Director | I | 51 | 2018 | o | |||||||||||

Norman S. Matthews Independent Director | I | 87 | 2018 | o | ● | ||||||||||

Kenneth C. Ambrecht Independent Director | II | 74 | 2018 | o | ● | o | |||||||||

Hugh R. Rovit Independent Director | II | 59 | 2018 | o | |||||||||||

David M. Maura Executive Chairman | III | 47 | 2018 | ||||||||||||

Terry L. Polistina Lead Independent Director | III | 56 | 2018 | ● | o | ||||||||||

| * | The term of our Class I directors expires at our 2022 annual stockholders meeting, our Class II directors expires at our 2020 annual stockholders meeting and our Class III directors expires at our 2021 annual stockholders meeting. |

| ** | Tenure represents service on the Board of the Company following the Merger. |

| *** | Committee membership: A = Audit Committee, C = Compensation Committee, NCG = NCG Committee; ● indicates committee Chair, o indicates committee member. |

Director Biographies

Set forth below are biographies for each of our directors, accompanied by descriptions of some of their key skills and experiences. The absence of any given category of key skills or experiences from the list preceding a director’s biography does not necessarily signify a lack of qualification in any such category.

Class I Directors

Sherianne James Independent Director since October 2018 Age: 51 Race/Ethnicity: African American Gender: Female | |||||

Independence & Committees: ● Independent Director● NCG Committee | Key Skills/Experience: ● Business Operations● Consumer Products● Corporate Governance● Corporate Strategy & Business Development● Executive Leadership & Management● International Business Experience● Marketing/Sales & Brand Management | ||||

Sherianne James was appointed to our Board in October 2018. Ms. James has served as Chief Marketing Officer of Essilor of America since August 2017 and previously was Vice President, Consumer Marketing for the company since July 2016. From February 2011 to July 2016, she held positions of increasing responsibility in marketing and operations for Transitions Optical, a division of Essilor of America, culminating in her role as Vice President of Transitions Optical from April 2014 to July 2016. From July 2005 through December 2010, Ms. James was Senior Marketing Manager for Russell Hobbs/Applica. She previously held a number of key project manager, research manager and brand manager positions with Kraft Foods, Inc. and, later, Kraft/Nabisco Foods from June 1995 to June 2005. Ms. James earned a Bachelor of Science degree in chemical engineering from the University of Florida in 1994 and a Master’s degree in Business Administration (“MBA”) from Northwestern University’s Kellogg Graduate School of Management in 2002. Ms. James currently serves as a member of our NCG Committee. | |||||

2

Norman S. Matthews Independent Director since July 2018 Age: 87 Race/Ethnicity: Caucasian Gender: Male | |||||

Independence & Committees: ● Independent Director● Chair of our NCG Committee● Compensation Committee | Key Skills/Experience: ● Accounting/Auditing● Business Operations● Corporate Governance● Corporate Strategy & Business Development● Ethics/Corporate Social Responsibility● Executive Leadership & Management● Public Company Board Experience● Finance/Capital Management & Allocation● Human Resources & Compensation● International Business Experience● Marketing/Sales & Brand Management● Mergers & Acquisitions● Public Company Executive Experience | ||||

Norman S. Matthews was appointed to our Board on the Merger Closing Date. From June 2010 to the Merger Closing Date, Mr. Matthews served as one of the directors of SPB Legacy. Prior to that time, he had served as a director of Spectrum Brands, Inc., one of our subsidiaries (“SBI”), since August 2009. Mr. Matthews has over three decades of experience as a business leader in marketing and merchandising and is currently an independent business consultant. As former President of Federated Department Stores, he led the operations of one of the nation’s leading department store retailers with over 850 department stores, including those under the names of Bloomingdales, Burdines, Foley’s, Lazarus and Rich’s, as well as various specialty store chains, discount chains and Ralph’s Grocery. In addition to his senior management roles at Federated Department Stores, Mr. Matthews also served as Senior Vice President and General Merchandise Manager at E.J. Korvette and Senior Vice President of Marketing and Corporate Development at Broyhill Furniture Industries. Mr. Matthews is a Princeton University graduate, and earned his MBA from Harvard Business School. He also currently serves on the Boards of Directors of Grocery Outlet Holding Corp., Party City Holdco, Inc. and The Children’s Place Retail Stores, Inc., and previously has served as a director of Henry Schein, Inc., Sunoco, The Progressive Corporation, Toys “R” Us, Duff & Phelps Corporation, and Federated Department Stores. He is a trustee emeritus at the American Museum of Natural History. Mr. Matthews is the Chair of our NCG Committee and is a member of our Compensation Committee. | |||||

3

Class II Directors

Kenneth C. Ambrecht Independent Director since July 2018 Age: 74 Race/Ethnicity: Caucasian Gender: Male | |||||

Independence & Committees: ● Independent Director● Chair of our Compensation Committee | Key Skills/Experience: ● Accounting/Auditing● Business Operations | ||||

● Audit Committee● NCG Committee | ● Corporate Governance● Corporate Strategy & Business Development● Ethics/Corporate Social Responsibility● Public Company Board Experience● Finance/Capital Management & Allocation● Human Resources & Compensation● International Business Experience● Marketing/Sales & Brand Management● Mergers & Acquisitions | ||||

Kenneth C. Ambrecht was appointed to our Board on the Merger Closing Date. From June 2010 until the Merger Closing Date, Mr. Ambrecht served as one of the directors of SPB Legacy. Prior to that time, he had served as a director of SBI from August 2009 to June 2010. Since December 2005, Mr. Ambrecht has served as a principal of KCA Associates LLC, through which he provides advice on financial transactions. From July 2004 to December 2005, Mr. Ambrecht served as a Managing Director with the investment banking firm First Albany Capital, Inc. Prior to that, Mr. Ambrecht was a Managing Director with Royal Bank Canada Capital Markets. Prior to that post, Mr. Ambrecht worked with the investment bank Lehman Brothers as Managing Director with its capital market division. Mr. Ambrecht is also a member of the Board of Directors of American Financial Group, Inc. Mr. Ambrecht has also served as a director of Dominion Petroleum Ltd. and Fortescue Metals Group Limited. Mr. Ambrecht serves as the Chair of our Compensation Committee and is a member of our Audit and our NCG Committees. | |||||

Hugh R. Rovit Independent Director since July 2018 Age: 59 Race/Ethnicity: Caucasian Gender: Male | |||||

Independence & Committees: | Key Skills/Experience: | ||||

● Independent Director● Audit Committee | ● Accounting/Auditing● Business Operations● Consumer Products● Corporate Governance● Corporate Strategy & Business Development● Ethics/Corporate Social Responsibility● Executive Leadership & Management● Public Company Board Experience● Finance/Capital Management & Allocation● Human Resources & Compensation● Marketing/Sales & Brand Management● Mergers & Acquisitions | ||||

Hugh R. Rovit was appointed to our Board on the Merger Closing Date. From June 2010 until the Merger Closing Date, Mr. Rovit served as one of the directors of SPB Legacy. Prior to that time, he had served as a director of SBI from August 2009 to June 2010. Mr. Rovit served as Chief Executive Officer of Ellery Homestyles, a leading supplier of branded and private label home fashion products to major retailers, offering curtains, bedding, throws and specialty products, from May 2013 until its sale in September 2018 to a strategic competitor. Previously, Mr. Rovit served as Chief Executive Officer of Sure Fit Inc., a marketer and distributor of home furnishing products from 2006 through 2012 and was a Principal at turnaround management firm Masson & Company from 2001 through 2005. Previously, Mr. Rovit held the positions of Chief Financial Officer of Best Manufacturing, Inc., a manufacturer and distributor of institutional service apparel and textiles, from 1998 through 2001 and Chief Financial Officer of Royce Hosiery Mills, Inc., a manufacturer and distributor of men’s and women’s hosiery, from 1991 through 1998. Mr. Rovit is a director of Xpress Retail, PlayPower, Inc. and Brown Jordan International and previously has served as a director of Nellson Nutraceuticals, Inc., Kid Brands Inc., Atkins Nutritional, Inc., Oneida, Ltd., Cosmetic Essence, Inc. and Twin Star International. Mr. Rovit received his Bachelor of Arts degree from Dartmouth College and has an MBA from Harvard Business School. Mr. Rovit is a member of our Audit Committee. | |||||

4

Class III Directors

David M. Maura Director since July 2018 Age: 47 Race/Ethnicity: Caucasian Gender: Male | |||||

Independence & Committees: ● None | Key Skills/Experience: ● Accounting/Auditing● Business Operations● Consumer Products● Corporate Governance● Corporate Strategy & Business Development● Ethics/Corporate Social Responsibility● Executive Leadership & Management● Public Company Board Experience● Finance/Capital Management & Allocation● Human Resources & Compensation● Mergers & Acquisitions● Public Company Executive Experience | ||||

David M. Maura was appointed our Executive Chairman and our Chief Executive Officer on the Merger Closing Date. Previously, he had served as the Executive Chairman, effective as of January 2016, and as Chief Executive Officer, effective as of April 2018, of SPB Legacy. Prior to such appointment, Mr. Maura served as non-executive Chairman of the Board of SPB Legacy since July 2011 and served as interim Chairman and as one of the directors of SPB Legacy since June 2010. Mr. Maura was a Managing Director and the Executive Vice President of Investments at HRG Legacy from October 2011 until November 2016 and had been a member of HRG Legacy’s board of directors from May 2011 until December 2017. Mr. Maura previously served as a Vice President and Director of Investments of Harbinger Capital Partners LLC (“Harbinger Capital”) from 2006 until 2012. Prior to joining Harbinger Capital in 2006, Mr. Maura was a Managing Director and Senior Research Analyst at First Albany Capital, Inc., where he focused on distressed debt and special situations, primarily in the consumer products and retail sectors. Prior to First Albany, Mr. Maura was a Director and Senior High Yield Research Analyst in Global High Yield Research at Merrill Lynch & Co. Previously, Mr. Maura was a Vice President and Senior Analyst in the High Yield Group at Wachovia Securities, where he covered various consumer product, service, and retail companies. Mr. Maura began his career at ZPR Investment Management as a Financial Analyst.Mr. Maura served as Chairman, President and Chief Executive Officer of Mosaic Acquisition Corp., a special purpose acquisition company, from October 2017 to January 2020, when the company merged with Vivint Smart Home, Inc. (“Vivint”). Following completion of the merger, he remains a director of Vivint and owns less than five percent of the outstanding common stock of Vivint. He previously has served on the boards of directors of Ferrous Resources, Ltd., Russell Hobbs, and Applica. Mr. Maura received a B.S. in Business Administration from Stetson University and is a CFA charterholder. | |||||

5

Terry L. Polistina Lead Independent Director since July 2018 Age: 56 Race/Ethnicity: Caucasian Gender: Male | |||||

Independence & Committees: ● Independent Director● Chair of our Audit Committee● Compensation Committee | Key Skills/Experience: ● Accounting/Auditing● Business Operations● Consumer Products● Corporate Governance● Corporate Strategy & Business Development● Ethics/Corporate Social Responsibility● Executive Leadership & Management● Public Company Board Experience● Finance/Capital Management & Allocation● Human Resources & Compensation● International Business Experience● Marketing/Sales & Brand Management● Mergers & Acquisitions● Public Company Executive Experience | ||||

Terry L. Polistina was appointed to our Board on the Merger Closing Date. From June 2010 until the Merger Closing Date, Mr. Polistina served as one of the directors of SPB Legacy. Since July 2018, Mr. Polistina has also served as the Lead Independent Director of the Board. Prior to that, he served as a director of SBI from August 2009 to June 2010. Mr. Polistina served as the President, Small Appliances of SPB Legacy beginning in June 2010 and became President – Global Appliances of SPB Legacy in October 2010 until September 2013. Prior to that, Mr. Polistina served as the Chief Executive Officer and President of Russell Hobbs from 2007 until 2010. Mr. Polistina served as Chief Operating Officer at Applica from 2006 to 2007 and Chief Financial Officer from 2001 to 2007, at which time Applica combined with Russell Hobbs. Mr. Polistina is a director of privately held Entic, Inc. Mr. Polistina received an undergraduate degree in finance from the University of Florida and holds an MBA from the University of Miami. Mr. Polistina is the Chair of our Audit Committee, a member of our Compensation Committee and serves as the Lead Independent Director of the Board. | |||||

6

Our Executive Officers

Our executive officers serve at the discretion of our Board. Our Board selected each of our executive officers because his or her background provides each executive with the experience and skillset geared toward helping us succeed in our business strategy. Our management team is comprised of seasoned executives who all focus on the performance of our Company to drive long-term outcomes for us. We are committed to ensuring that female and minority candidates are among the pool of individuals from which new executive officers are selected. During Fiscal 2019, we made progress in advancing this objective by appointing to our executive team a woman and a candidate from a diverse background. We are committed to further progressing this objective in the future.

Included in the discussion below is information regarding our executive officers who do not serve as directors of our Company. See “” above for certain information regarding David Maura, our only director-employee.

Our Board of Directors

Randal Lewis Executive Vice President, Chief Operating Officer since October 2018 Age: 53 Race/Ethnicity: Caucasian Gender: Male | ||

Randal Lewis was appointed our Chief Operating Officer in October 2018 and Executive Vice President in September 2019. He has direct responsibility for all operating divisions. Mr. Lewis previously led our former Pet, Home & Garden Division since November 2014. Prior to that, he was Senior Vice President and General Manager of our Home & Garden business since January 2011, where he led the restructuring of that business. From April 2005 to January 2011, Mr. Lewis served as our Home & Garden business’s Vice President, Manufacturing and Vice President, Operations. Prior to that, Mr. Lewis held various leadership roles from October 1997 to April 2005 with the former owners of United Industries Corporation, which is now owned by the Company, and from January 1989 to October 1997 Mr. Lewis worked at Unilever. Mr. Lewis earned a Bachelor of Science degree in mechanical engineering from the University of Illinois, Urbana-Champaign. |

Rebeckah Long Senior Vice President, Global Human Resources since September 2019 Age: 45 Race/Ethnicity: Caucasian Gender: Female | ||

Rebeckah Long was appointed our Senior Vice President, Global Human Resources in September 2019 and has direct responsibility for consistent delivery and execution of the Human Resource function globally. Ms. Long previously served as Vice President of Global Human Resources of Spectrum Brands since April 2019. Prior to that, she was Human Resource Business Partner for several business divisions within Spectrum Brands since March 2008, with a focus on talent strategy and organizational effectiveness. Prior to joining Spectrum Brands, she was the Regional Human Resources Manager for United Rentals, lnc. from June 2000 to February 2008 and was responsible for the integration of over 25 businesses into the United Rentals portfolio. Rebeckah holds a Bachelor of Science degree in Economics from Illinois State University. |

Jeremy W. Smeltser Executive Vice President, Chief Financial Officer since November 2019 Age: 45 Race/Ethnicity: Caucasian Gender: Male | ||

Jeremy W. Smeltser was appointed our Executive Vice President on October 1, 2019 and was appointed our Chief Financial Officer on November 17, 2019. He previously served as Vice President and Chief Financial Officer of SPX Flow, Inc. (“SPX Flow”). Prior to his role at SPX Flow, he served as Vice President and Chief Financial Officer of SPX Corporation, where he served in various roles, including as Vice President and Chief Financial Officer, Flow Technology, and became an officer of SPX Corporation in April 2009. Mr. Smeltser joined SPX Corporation in 2002 from Ernst & Young LLP, where he was an audit manager in Tampa, Florida. Prior to that, he held various positions with Arthur Andersen LLP, in Tampa, Florida, and Chicago, Illinois, focused primarily on assurance services for global manufacturing clients. Mr. Smeltser earned a Bachelor of Science degree in Accounting from Northern Illinois University. |

7

Ehsan Zargar Executive Vice President, General Counsel and Corporate Secretary since October 2018 Age: 42 Race/Ethnicity: Asian (Middle East) Gender: Male | ||

Ehsan Zargar was appointed our Executive Vice President, General Counsel and Corporate Secretary on October 1, 2018. Mr Zargar is responsible for the Company’s legal, insurance and real estate functions. From June 2011 until the Merger Closing Date, Mr. Zargar held a number of increasingly senior positions with HRG Legacy, including serving as its Executive Vice President and Chief Operating Officer from January 2017 until the Merger Closing Date, as its General Counsel since April 2015, and as Corporate Secretary since February 2012. From August 2017 until the Merger Closing Date, Mr. Zargar served as a director of SPB Legacy. From November 2006 to June 2011, Mr. Zargar worked in the New York office of Paul, Weiss, Rifkind, Wharton & Garrison LLP. Previously, Mr. Zargar practiced law at another major law firm focusing on general corporate matters. Mr. Zargar received a law degree from Faculty of Law at the University of Toronto and a B.A. from the University of Toronto. |

Corporate Governance

The following table provides an overview of our corporate governance, including recent enhancements and existing practices.

Recent Enhancements |

✓ Increased diversity among Board and executive team |

✓ Adopted majority voting and a director resignation policy |

✓ Strengthened our stock ownership guidelines |

✓ Strengthened our anti-hedging policy |

✓ Adopted an anti-pledging policy |

✓ Hired a second independent compensation consultant |

✓ Completed our transition to a stand-alone independent company |

Existing Practices |

✓ Independent lead director |

✓ Majority of the Board comprised of independent directors |

✓ All committees comprised entirely of independentdirectors |

✓ Anti-hedging policy |

✓ Robust clawback policy |

✓ Independent compensation consultant |

✓ All three members of our Audit Committee are financialexperts |

8

Board Structure

Lead Independent Director

Mr. Polistina was appointed to our Board, and as our Lead Independent Director in July 2018. In his capacity as our Lead Independent Director, Mr. Polistina:

.

| • | presides at all meetings of the Board at which the Chairman of the Board is not present; |

| • | presides at all executive sessions of the independent members of the Board, and has the authority to call meetings of the independent members of the Board; |

| • | serves as liaison between the management and the independent members of the Board, and provides our Chief Executive Officer (“CEO”) and other members of management with feedback from executive sessions of the independent members of the Board; |

| • | reviews and approves the information to be provided to the Board; |

| • | reviews and approves meeting agendas and coordinates with management to develop such agendas; |

| • | approves meeting schedules to assure there is sufficient time for discussion of all agenda items; |

| • | if requested by major shareholders, ensures that he is available for consultation and direct communication; |

| • | interviews, along with the Chair of our NGC Committee, Board and senior management candidates and makes recommendations with respect to Board candidates and hiring of senior management; |

| • | consults with the Chair and other members of our Compensation Committee with respect to the performance review of our CEO and other member of our senior management team; and |

| • | performs such other functions and responsibilities as requested by the Board from time to time. |

Mr. Maura serves as our Executive Chairman and our CEO. Given Mr. Maura’s broad experience in mergers and acquisitions, the consumer products and retail sectors, and finance and investments, as well as his role in SPB Legacy’s strategy and growth since 2010, our Board believes that it is in the best interest of the Company for Mr. Maura to concurrently serve as our Executive Chairman and CEO.

Director Independence

In accordance with the New York Stock Exchange Listed Company Manual (the “NYSE Rules”) and our Corporate Governance Guidelines, a majority of our Board is required to be comprised of independent directors. All of our directors, except for David Maura (our Chairman and CEO), qualify as independent directors. More specifically, our Board has affirmatively determined that none of the following directors has a material relationship with the Company (either directly or as a partner, stockholder, or officer of an organization that has a relationship with the Company): Kenneth C. Ambrecht, Sherianne James, Norman S. Matthews, Terry L. Polistina and Hugh R. Rovit. Our Board has adopted the definition of “independent director” set forth under Section 303A.02 of the NYSE Rules to assist it in making determinations of independence. Our Board has determined that the directors referred to above currently meet these standards and qualify as independent.

Meetings of Independent Directors

The Company generally holds executive sessions at each Board and committee meeting. In his capacity as our Lead Independent Director, Mr. Polistina presides over executive sessions of the entire Board and the Chair of each committee presides over the executive sessions of that committee.

Committees Established by Our Board of Directors

Our Board has designated three principal standing committees: our Audit Committee, our Compensation Committee, and our NCG Committee, each of which has a written charter addressing each such committee’s purpose and responsibilities. Each such committee is comprised entirely of independent directors.

Audit Committee

Our Audit Committee has been established in accordance with Section 303A.06 of the NYSE Rules and Rule

10A-3

of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), for the purpose of overseeing the Company’s9

accounting and financial reporting processes and audits of our financial statements. Our Audit Committee is responsible for monitoring (i) the integrity of our financial statements, (ii) our independent registered public accounting firm’s qualifications and independence, (iii) the performance of our internal audit function and independent auditors, and (iv) our compliance with legal and regulatory requirements. The responsibilities and authority of our Audit Committee are described in further detail in the Charter of the Audit Committee, as adopted by our Board in July 2018, a copy of which is available at our website www.spectrumbrands.com under “”.

Investor Relations—Corporate Governance Documents

The current members of our Audit Committee are Terry L. Polistina (Chair), Kenneth C. Ambrecht, and Hugh R. Rovit. Our Board has determined that each member of our Audit Committee qualifies as an “audit committee financial expert” as defined in the rules promulgated by the SEC in furtherance of Section 407 of the Sarbanes-Oxley Act of 2002. Our Board has determined that all of the members of our Audit Committee qualify as independent, as such term is defined in Section 303A.02 of the NYSE Rules, Section 10A(m)(3)(B) of the Exchange Act, and Exchange Act Rule

10A-3(b).

Compensation Committee

Our Compensation Committee is responsible for (i) overseeing our compensation and employee benefits plans and practices, including our executive compensation plans and our incentive-compensation and equity-based plans, (ii) evaluating and approving the performance of our Executive Chairman and CEO and other executive officers in light of those goals and objectives, and (iii) reviewing and discussing with management our compensation discussion and analysis disclosure and compensation committee reports in order to comply with our public reporting requirements. The responsibilities and authority of our Compensation Committee are described in further detail in the Charter of the Compensation Committee, as adopted by our Board in July 2018, a copy of which is available at our website www.spectrumbrands.com under “”.

Investor Relations—Corporate Governance Documents

The current members of our Compensation Committee are Kenneth C. Ambrecht (Chair), Norman S. Matthews and Terry L. Polistina. Our Board has determined that all of the members of our Compensation Committee qualify as independent, as such term is defined in Section 303A.02 of the NYSE Rules.

NCG Committee

Our NCG Committee is responsible for (i) identifying and recommending to our Board individuals qualified to serve as our directors and on our committees of our Board, (ii) advising our Board with respect to board composition, procedures and committees, (iii) developing and recommending to our Board a set of corporate governance principles applicable to the Company, and (iv) overseeing the evaluation process of our Board and our Executive Chairman and CEO. The responsibilities and authority of our NCG Committee are described in further detail in the Charter of the NCG Committee, as adopted by our Board in July 2018, a copy of which is available at our website www.spectrumbrands.com under “”.

Investor Relations—Corporate Governance Documents

The current members of our NCG Committee are Norman S. Matthews (Chair), Kenneth C. Ambrecht, and Sherianne James. Ms. James was appointed as a member of the NCG Committee on January 28, 2020. Our Board has determined that all of the members of our NCG Committee qualify as independent, as such term is defined in Section 303A.02 of the NYSE Rules.

Board and Committee Activities

During Fiscal 2019, our Board held a total of 11 meetings, and acted by unanimous written consent on a total of 6 occasions. Our Audit Committee held a total of 7 meetings during Fiscal 2019. Our Compensation Committee held 8 meetings and acted by unanimous written consent on 2 occasions during Fiscal 2019. Our NCG Committee held 3 meetings during Fiscal 2019.

During Fiscal 2019, all of our directors attended at least 75% of the meetings of the Board and committees on which they served.

Our Practices and Policies

Corporate Governance Guidelines and Code of Ethics and Business Conduct

Our Board has adopted our Corporate Governance Guidelines to assist it in the exercise of its responsibilities. These guidelines reflect our Board’s commitment to monitor the effectiveness of policy and decision-making both at our Board and management level, with a view to enhancing stockholder value over the long-term. Our Corporate Governance Guidelines address, among other things, our Board and Board committee composition and responsibilities, director qualifications standards and selection and evaluation of our CEO.

10

Our Board has adopted a Code of Business Conduct and Ethics Policy for directors, officers and employees and a Code of Ethics for the Principal Executive and Senior Financial Officers to provide guidance to our CEO, chief financial officer (“CFO”), principal accounting officer or controller, and our business segment chief financial officers or persons performing similar functions.

Majority Voting and Director Resignation Policy

During Fiscal 2019, our Board adopted a majority voting policy for the election of directors. Pursuant to this policy, which applies in the case of uncontested director elections, a director must be elected by a majority of the votes cast with respect to the election of such director. For purposes of this policy, a “majority of the votes cast” means that the number of shares voted “for” a director must exceed the number of shares voted “against” that director and abstentions and broker

non-votes

are not counted as “votes cast.”The policy also provides that in the event that an incumbent director nominee receives a greater number of votes “against” than votes “for” his or her election, he or she must (within five business days following the final certification of the related election results) offer to tender his or her written resignation from the Board to the NCG Committee. The NCG Committee will review such offer of resignation and will consider such factors and circumstances as it may deem relevant, and, within 90 days following the final certification of the election results, will make a recommendation to the Board concerning the acceptance or rejection of such tendered offer of resignation. The policy requires the decision of the Board to be promptly publicly disclosed.

Anti-Hedging Policy

The Company believes it is improper and inappropriate for our directors, officers and employees and certain of their family members (each, a “Subject Person”) to engage in hedging, short-term or speculative transactions involving the Company’s securities. Our anti-hedging policy, which we further strengthened during Fiscal 2019, applies to all Subject Persons. The Company prohibits Subject Persons from engaging in (i) derivative, speculative, hedging, or monetization transactions in Company securities (including, but not limited to, any trading on derivatives (such as swaps, forwards, and/or futures) of Company securities that allow a stockholder to lock in the value of Company securities in exchange for all or part of the potential upside appreciation in the value of such stock), (ii) short sales (i.e., selling stock the Subject Person does not own and borrowing shares to make delivery), and (iii) buying or selling puts, calls, options or other derivatives in respect of Company securities.

Anti-Pledging Policy

In addition, the Company believes it is improper and inappropriate for any Subject Person to engage in pledging transactions involving the Company’s securities. During Fiscal 2019, we adopted a robust anti-pledging policy, which prohibits Subject Persons from pledging or encumbering Company securities as collateral for a loan or other indebtedness. This prohibition includes, but is not limited to, holding such shares in a margin account as collateral for a margin loan or borrowing against Company securities on margin. Any pledges (and any modifications or replacements of such pledges) that existed prior to the adoption of our policy are grandfathered unless otherwise prohibited by applicable law or Company policy and so long as any modification or replacement of any

pre-existing

pledge does not result in additional shares being pledged.Securities Trading Policy

Our Company believes that it is appropriate to monitor and prohibit certain trading in the securities of our Company. Accordingly, trading of the Company’s securities by directors, executive officers and certain other employees who are so designated by the office of the Company’s General Counsel is subject to trading period limitations or must be conducted in accordance with a previously established trading plan that meets SEC requirements. At all times, including during approved

11

trading periods, directors, executive officers and certain other employees notified by the office of the Company’s General Counsel are required to obtain preclearance from the Company’s General Counsel or his designee prior to entering into any transactions in Company securities, unless those transactions occur in accordance with a previously established trading plan that meets SEC requirements.

Transactions subject to our securities trading policy include, among others, purchases and sales of Company stock, bonds, options, puts and calls, derivative securities based on securities of the Company, gifts of Company securities, contributions of Company securities to a trust, sales of Company stock acquired upon the exercise of stock options, broker-assisted cashless exercises of stock options, market sales to raise cash to fund the exercise of stock options, and trades in Company’s stock made under an employee benefit plan.

Stock Ownership Guidelines

Our Board believes that our directors, NEOs and certain of the Company’s other officers and employees should own and hold Company common stock to further align their interests with the interests of stockholders and to further promote the Company’s commitment to sound corporate governance.

To memorialize this commitment, effective January 29, 2013, our Board, upon the recommendation of our Compensation Committee, established stock ownership and retention guidelines (the “SOG”) applicable to the Company’s directors, NEOs and all other officers of the Company and its subsidiaries with a level of Vice President or above (such officers and our NEOs, our “Covered Officers”). Effective January 1, 2020, the Company improved and enhanced the SOG to further align it with best practices by: (i) increasing our directors’ and Covered Officers’ retention requirement from 25% to 50% of their net

after-tax

shares received under awards granted (other than equity awards granted pursuant to the annual cash bonus plan) until they reach their required stock ownership under the SOG; and (ii) extending the applicable time period for our directors and Covered Officers to achieve the minimum ownership requirements to five (5) years from the date of eligibility or promotion. Even when the required stock ownership is obtained, all employee incentive plan participants, including NEOs, are subject to an additional stock retention requirement requiring them to retain at least 25% of their netafter-tax

shares of Company stock received under awards for one year after date of vesting.Under the updated SOG, our directors are expected to achieve stock ownership with a value of at least five times their annual cash retainer. In addition, our Covered Officers are expected to achieve the levels of stock ownership indicated below (which equal a dollar value of stock based on a multiple of the Covered Officer’s base salary).

Position �� | $ Value of Stock to be Retained (Multiple of Base Salary or Cash Retainer) | Years to Achieve | |||

Board Members | 5x Cash Retainer | 5 years | |||

Executive Chairman and CEO | 5x Base Salary | 5 years | |||

COO, CFO, General Counsel, and Presidents of business units | 3x Base Salary | 5 years | |||

Senior Vice Presidents | 2x Base Salary | 5 years | |||

Vice Presidents | 1x Base Salary | 5 years | |||

The stock ownership levels attained by a director or a Covered Officer are based on shares directly owned by the director or Covered Officer, whether through earned and vested restricted stock units (“RSU”) or performance stock units (“PSU”) or restricted stock grants or open market purchases. Unvested restricted shares, unvested RSUs and PSUs, and stock options do not count toward the ownership goals; provided, that, effective January 1, 2020, unvested time-based restricted stock and unvested time-based RSUs will count. On an annual basis, our Compensation Committee reviews the progress of our directors and Covered Officers in meeting these guidelines. In some circumstances, failure to meet the guidelines by a director or a Covered Officer could result in additional retention requirements or other actions by our Compensation Committee.

12

Compensation Clawback Policy

We have adopted a Compensation Clawback Policy setting forth the conditions under which applicable incentive compensation provided to our executive officers may be subject to forfeiture, disgorgement, recoupment, or diminution (“clawback”). This policy provides that our Board or our Compensation Committee shall require the clawback or adjustment of incentive-based compensation to the Company in the following circumstances:

| ● | As required by Section 304 of the Sarbanes Oxley Act of 2002, which generally provides that if the Company is required to prepare an accounting restatement due to material noncompliance as a result of misconduct with financial reporting requirements under the securities laws, then the CEO and CFO must reimburse the Company for any incentive-based compensation or equity compensation and profits from the sale of the Company’s securities during the 12-month period following initial publication of the financial statements that had been restated; |

| ● | As required by Section 954 of the Dodd-Frank Act and Rule 10D-1 of the Exchange Act, which generally require that, in the event the Company is required to prepare an accounting restatement due to its material noncompliance with financial reporting requirements under the securities laws, the Company may recover from any of its current or former executive officers who received incentive compensation, including stock options, during the three-year period preceding the date on which the Company is required to prepare a restatement based on the erroneous financial reporting, any amount that exceeds what would have been paid to the executive officer after giving effect to the restatement; and |

| ● | As required by any other applicable law, regulation, or regulatory requirement. |

Additionally, our Board or Compensation Committee in their discretion may require that any executive officer who has been awarded incentive-based compensation shall forfeit, disgorge, return, or adjust such compensation in the following circumstances:

| ● | If the Company suffers significant financial loss, reputational damage, or similar adverse impact as a result of actions taken or decisions made by the executive officer in circumstances constituting illegal or intentionally wrongful conduct or gross negligence; or |

| ● | If the executive officer is awarded or is paid out under any incentive compensation plan of the Company on the basis of a material misstatement of financial calculations or information, or if events coming to light after the award disclose a material misstatement which would have significantly reduced the amount of the award or payout if known at the time of the award or payout. |

The awards and incentive compensation subject to clawback under this policy include vested and unvested equity awards, shares acquired upon vesting or lapse of restrictions, short- and long-term incentive bonuses and similar compensation, discretionary bonuses, and any other awards or compensation under the Company’s equity plans, and any other incentive compensation plan of the Company. Any clawback under this policy may, in the discretion of our Board or Compensation Committee, be effectuated through the reduction, forfeiture, or cancellation of awards, the return of

paid-out

cash or exercised or released shares, adjustments to future incentive compensation opportunities, or in such other manner as our Board and Compensation Committee determine to be appropriate, except as otherwise required by law.In addition, under the Company’s equity plans, any equity award granted may be cancelled by our Compensation Committee in its sole discretion, except as prohibited by applicable law, if the participant, without the consent of the Company, while employed by or providing services to the Company or any affiliate or after termination of such employment or service, violates a

non-competition,

non-solicitation,

ornon-disclosure

covenant or agreement or otherwise engages in activity that is in conflict with or is adverse to the interests of the Company or any affiliate, including fraud or conduct contributing to any financial restatements or irregularities engaged in, as determined by our Compensation Committee in its sole discretion. Our Compensation Committee may also provide in any award agreement that the participant will forfeit any gain realized on the vesting or exercise of such award, and must repay the gain to the Company, in each case except as prohibited by applicable law, if (i) the participant engages in any activity referred to in the preceding sentence, or (ii) the amount of any such gain is in excess of what the participant should have received under the terms of the award for any reason (including without limitation by reason of a financial restatement, mistake in calculations, or other administrative error). Additionally, awards are subject to claw-back, forfeiture, or similar requirements to the extent required by applicable law (including without limitation Section 304 of the Sarbanes-Oxley Act and Section 954 of the Dodd Frank Act). Equity awards issued have included these provisions.13

Risk Oversight

The Company’s risk assessment and management function is led by the Company’s senior management, which is responsible for

day-to-day

management of the Company’s risk profile, with oversight from our Board and its committees. Central to our Board’s oversight function is our Audit Committee. In accordance with our Audit Committee Charter, our Audit Committee is responsible for the oversight of the financial reporting process and internal controls. In this capacity, our Audit Committee is responsible for reviewing and evaluating guidelines and policies governing the process by which senior management of the Company and the relevant departments of the Company, including the internal audit department, assess and manage the Company’s exposure to risk, as well as the Company’s major financial risk exposures and the steps management has taken to monitor and control such exposures.The Company has implemented an annual formalized risk assessment process. In accordance with this process, a governance risk and compliance committee of certain members of senior management has the responsibility to identify, assess and oversee the management of risk for the Company. This committee obtains input from other members of management and subject matter experts as needed. Management uses the collective input received to measure the potential likelihood and impact of key risks and to determine the adequacy of the Company’s risk management strategy. Periodically, representatives of this committee report to our Audit Committee on its activities and the Company’s risk exposure.

In Fiscal 2019, our management and our Audit Committee reviewed our reporting processes and took a number of actions to further enhance such processes. In connection with such efforts, we made changes to our internal control over financial reporting and successfully remediated the material weakness that we disclosed in our Annual Report on Form

10-K

for Fiscal 2018. See Item 9A of the Original Form10-K

for a detailed discussion of this remediation process.Environmental, Social and Governance Matters

We are committed to sustainability and recognize the impact our business has on the world. We believe in making a positive difference in the communities in which we live and work and strive to discharge our corporate social responsibilities from a global perspective and throughout every aspect of our operations. Our Board recognizes the negative effect poor environmental practices and human capital management may have on us and our returns. Our Board carefully considers and balances the impact on the environment, people and the communities of which we are a part in deciding how to operate our business. Our Board receives periodic reports regarding our risk exposure and risk mitigation efforts in these areas.

Related Person Transactions Policy

Our Board has adopted a written policy for the review, approval and ratification of transactions that involve related persons and potential conflicts of interest. Seefor discussion of this policy and disclosure of our related person transactions.

“Certain Relationships and Related Transactions”

Transfer of Our Shares of Common Stock

Our Company has substantial deferred tax assets related to net operating losses and tax credits (together, “Tax Attributes”) for U.S. federal and state income tax purposes. These Tax Attributes are an important asset of the Company because we expect to use these Tax Attributes to offset future taxable income. The Company’s ability to utilize or realize the carrying value of such Tax Attributes may be impacted if the Company experiences an “ownership change” or certain other events under applicable tax rules. If an “ownership change” were to occur, we could lose the ability to use a significant portion of its Tax Attributes, which could have a material adverse effect on the Company’s results of operations and financial condition.

Accordingly, we have adopted certain transfer restrictions designed to limit an “ownership change.” These transfer restrictions are subject to certain exceptions, including, among others, prior approval of a Prohibited Transfer by our Board. As previously disclosed, our Board has granted

pre-approvals

to certain large institutional investors and their affiliates. The foregoing description of the transfer restrictions contained within our Charter is not complete and is qualified in its entirety by reference to the full text of the Charter, which is incorporated by reference into this report.Governance Documents Availability

We have posted our Corporate Governance Guidelines, Code of Business Conduct and Ethics for directors, officers and employees, Code of Ethics for the Principal Executive and Senior Financial Officers, Audit Committee Charter, Compensation Committee Charter, and NCG Committee Charter on our website www.spectrumbrands.com under “”. We intend to disclose any amendments to, and, if applicable, any waivers of, these governance documents on that section of our website. These governance documents are also available in print without charge to any stockholder of record that makes a written request to the Company. Inquiries must be directed to the Investor Relations Department at Spectrum Brands Holdings, Inc., 3001 Deming Way, Middleton, WI 53562.

Investor Relations—Corporate Governance Documents

14

Director Compensation

Our Compensation Committee is responsible for approving, subject to review by our Board as a whole, compensation programs for our

non-employee

directors. In that function, our Compensation Committee considers market and peer company data regarding director compensation and annually evaluates the Company’s director compensation practices in light of that data and the characteristics of the Company as a whole, with the assistance of its independent compensation advisors. Under our director compensation program, at the beginning of each fiscal year, eachnon-employee

director receives an annual grant of RSUs equal to that number of shares of the Company’s common stock with a value on the date of grant of $125,000. Additionally, each director is eligible to receive an annual cash retainer of $105,000 which is paid quarterly. In addition, the Lead Independent Director receives an additional annual cash retainer of $40,000 and an additional annual equity retainer amount of $20,000.For Fiscal 2019, compensation for service on the standing committees of our Board, was paid in an annual amount as follows below. Mr. Maura, our only director who is an employee of the Company, does not receive compensation for his service as a director.

Committee | Chair Annual Retainer | Member Annual Retainer | |||||||

Audit | $ | 20,000 | N/A | ||||||

Compensation | $ | 15,000 | N/A | ||||||

NCG | $ | 15,000 | N/A | ||||||

Director Compensation Table for Fiscal 2019

The table set forth below, together with its footnotes, provides information regarding compensation paid to our directors in Fiscal 2019. In Fiscal 2019, Mr. Polistina (who was appointed Lead Independent Director in July 2018) received the $60,000 paid in cash for his service as Lead Independent Director in Fiscal 2019. Mr. Polistina also received an additional $11,500 representing theportion of these fees for his service in Fiscal 2018, which was not paid in Fiscal 2018. Directors are permitted to make an annual election to receive all of their director compensation (including for service on committees of our Board) in the form of Company stock in lieu of cash. For Fiscal 2019, the grants of RSUs were made on October 1, 2018 (except for Ms. James who became a director on October 23, 2018 and received a grant of RSUs on November 1, 2018). All such RSUs (including those awarded to Ms. James) vested on October 1, 2019.

pro rata

Name (1) | Fees Earned or Paid in Cash (2) | Stock Awards (3)(4) | All Other Compensation (5) | Total | |||||||||||||

Kenneth C. Ambrecht | $ - | $ 244,122 | $9,071 | $253,193 | |||||||||||||

David S. Harris (6) | $ - | $ 229,157 | $5,171 | $234.328 | |||||||||||||

Sherianne James | $100,042 | $ 121,334 | $3,081 | $224,457 | |||||||||||||

Norman S. Matthews | $ - | $ 244,122 | $6,383 | $250,505 | |||||||||||||

Terry L. Polistina | $71,500 | $ 249,110 | $5,621 | $326,231 | |||||||||||||

Hugh R. Rovit | $ - | $ 229,157 | $5,705 | $234,862 | |||||||||||||

Joseph S. Steinberg (2)(5)(6) | $ - | $ 229,157 | $5,171 | $234,328 | |||||||||||||

| (1) | This table includes only directors who received compensation during Fiscal 2019. |

| (2) | Amounts reflected in this column include the annual retainer fees and committee Chair fees paid in cash to the applicable director during Fiscal 2019. |

| (3) | Amounts in this column represent the aggregate grant date fair value of each award computed in accordance with FASB ASC Topic 718. The value was computed by multiplying the number of shares underlying the stock award by the closing price per share of the Company’s common stock on each grant date (or, as applicable, the last trading date immediately prior to the grant date if the grant date fell on a date when the New York Stock Exchange was closed), which was $74.45 on October 1, 2018, and was $66.17 on November 1, 2018. The directors received RSUs on October 1, 2018, which vested on October 1, 2019 as follows: Mr. Ambrecht, 3,279; Mr. Harris, 3,078; Mr. Matthews, 3,279; Mr. Polistina, 3,346; Mr. Rovit, 3,079; and Mr. Steinberg, 3,078. In connection with her appointment to our Board on October 23, 2018, Ms. James received 1,834 RSUs on November 1, 2018, which vested on October 1, 2019. |

| (4) | As of September 30, 2019, Messrs. Ambrecht, Harris, Matthews, Polistina, Rovit and Steinberg held 3,279, 3,078, 4,103, 3,346, 3,078 and 3,078 outstanding unvested RSUs respectively, and Ms. James held 1,834 outstanding unvested RSUs. |

| (5) | Includes dividends paid on RSUs which were not factored into the grant date fair value of the RSUs. The amount of the dividends for Messrs. Ambrecht, Harris, Matthews, Polistina, Rovit and Steinberg was $5,509, $5,171, $5,509, $5,621, $5,171, $5,171, respectively and $3,081 for Ms. James. |

| (6) | In connection with the termination of the Company’s shareholder agreement with Jefferies Financial Group, Inc. (“Jefferies Financial”), Messrs. Joseph S. Steinberg and David S. Harris (each of whom had been appointed as Board designees of Jefferies Financial pursuant to such agreement) resigned from our Board. |

15

Compensation Committee Interlocks and Insider Participation

The current members of our Compensation Committee are Kenneth C. Ambrecht (Chair), Norman S. Matthews, and Terry L. Polistina. During Fiscal 2019, none of the members of our Compensation Committee was one of our officers or employees. In addition, during Fiscal 2019, none of our executive officers served as a member of the compensation committee of any other entity that has one or more executive officers serving on our Board or our Compensation Committee.

16

| ITEM 11. | EXECUTIVE COMPENSATION |

Compensation Discussion and Analysis

This section provides an overview and analysis of our compensation programs and policies, the material compensation decisions made under those programs and policies, and the material factors considered in making those decisions. The discussion below is intended to help you understand the detailed information provided in our executive compensation tables and put that information into context within our overall compensation philosophy.

Fiscal 2019 Business Highlights

Fiscal 2019 was a year of significant achievement for the Company as we commenced or completed a number of strategic and transformational initiatives and, alongside these accomplishments delivered positive economic and financial results. A few highlights for Fiscal 2019 include:

● We continued our momentum after completing the merger with HRG Legacy in Fiscal 2018.● We streamlined our business focus by completing the sales of our global battery and lighting (“GBL”) business and our global auto care (“GAC”) business.● We no longer have a controlling stockholder and, in Fiscal 2019, Jefferies Financial announced, and ultimately completed, the distribution of its shares, further accelerating our transition to a stand-alone independent company.● We simplified and streamlined our overall compensation structure, focusing our ongoing program on a combination of an annual bonus and a single long-term equity program with a three-year performance period.● We made changes to our executive team, including the hiring of a new CFO, General Counsel, and the promotion of individuals to Chief Operating Officer (“COO”) and head of HR positions.● We made changes to our senior operating team in our businesses to align with our new business strategy.● We added diversity to our Board and to our executive team.● We hired a second compensation consulting firm to review Company practices. | ● We maintained our global market positions as the #1 leading market position with a number of our products.● Despite foreign exchange headwinds and a reported sales decrease of 0.2%, we delivered organic sales growth of 1.4%.● We significantly improved our capital structure as net debt (outstanding debt less cash) declined from 5.2 to 3.1 times adjusted EBITDA at the end of 2019. We reduced total debt by $2.4 billion during Fiscal 2019.● We returned over $350 million to our shareholders in Fiscal 2019 in dividends and share repurchases.● We plan to repurchase up to $250 million of our shares in Fiscal 2020, and have purchased $206 million as of December 29, 2019.● We delivered our Fiscal 2019 adjusted EBITDA results within our guidance despite incurring $60 million of cash tariff headwinds.● We implemented a Global Productivity Improvement Plan, which is expected to improve our overall annualized operating costs by $100 million in the next16-22 months.● We achieved and exceeded our Fiscal 2019 annual operating plan.● We engaged in a thorough and complete review of the Company’s operations and made significant changes to our business strategy. |

As noted in the highlights, we have made substantial changes, including restructuring our business and simplifying our capital structure, compensation program and operating model. These changes are designed to provide significant and positive outcomes for the Company and our shareholders in the future.

17

We began Fiscal 2019 by building on the completion of our Merger with our previous majority stockholder, HRG Legacy. The Merger was a significant achievement for the Company and its stockholders and was negotiated and completed over a significant period of time and consumed a substantial amount of our management’s and directors’ time and efforts. Among other things, the Merger enabled us to acquire certain Tax Attributes of HRG Legacy at a meaningful discount, advance the transformation of the Company into an independent company without a controlling stockholder and increase the float and reduce the volatility in the trading of our common stock.

During and following the time that we were completing the Merger with HRG Legacy, we also sought and ran a process to dispose of three of our business segments: our GBL business, our GAC business and our appliances business. On January 15, 2018, we announced the sale of the GBL business (the “GBL Sale”), which took over 12 months to consummate, to Energizer Holdings, Inc. (“Energizer”) and on November 5, 2018, we announced the sale of the GAC business (the “GAC Sale”), also to Energizer. Both sales were completed in January 2019, resulting in aggregate net proceeds of $2.9 billion to the Company, prior to purchase price adjustments. We ultimately retained our appliances business as part of our continuing operations. The sales process and related negotiation and completion (as applicable) of these three businesses was the source of a significant amount of time and effort for the Company, its management and employees, both domestically and abroad. In particular, the sale of our GBL business was completed only after a protracted and extended regulatory approval process, particularly in Europe.

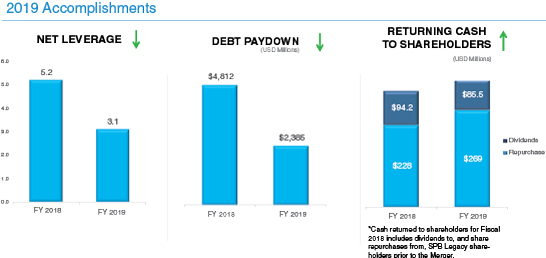

Through the completion of the sales of our GBL and GAC businesses we streamlined our Company and our operational focus. We were able to effectively realize the benefits of having acquired HRG Legacy’s Tax Attributes in the Merger, sheltering the gains we realized on the completion of the GBL Sale and substantially reducing the taxes that would otherwise have been payable. The $2.9 billion in proceeds, prior to purchase price adjustments, that we received from the GBL Sale and GAC Sale has enabled us to aggressively pay down debt, materially reduce our leverage and strengthen our balance sheet. Our net leverage ratio was 5.2x at the end of Fiscal 2018 and was reduced to 3.1x at the end of Fiscal 2019. Our improved balance sheet will allow us to be more nimble and act strategically as opportunities arise, and also to better withstand any future downturns in the economy. In addition, as part of the respective asset sales, we acquired shares in Energizer so that we have indirectly retained potential upside in the value of our sold businesses.

Following the completion of the asset sales, we commenced a thorough review of the Company’s operations with a view towards resetting our operating model and business strategies to lower costs, improve efficiencies and enable greater organic growth for each of our divisions. This assessment yielded key findings that we are using to overhaul our operating and strategy model, our commercial

go-to-market

plans, our sourcing and procurement processes, and our use of technology and automation to operate our business more efficiently. We are referring to this project as our Global Productivity Improvement Program and anticipate it will reduce our overall annualized operating costs by at least $100 million within the next 16 to 22 months. These savings will place the Company on a positive trajectory in the future because we expect that a substantial portion of the savings will be reinvested in growth-enabling activities, including improved consumer insights and additional research and development and marketing.We also made significant changes to our executive management team, including the hiring of a new CFO, the hiring of a new General Counsel, the promotion of an executive to be our COO and the promotion of an executive to be the global head of HR. We also made changes to the senior management team at our business units in order to align our business unit senior management team with our new operating model and business strategy. These changes are designed to provide fresh new ideas, build on the success for the future, and show our commitment to diversity and inclusion.

We also undertook a complex and comprehensive project of consolidating certain of our distribution centers, which required a significant amount of time and resources. While we experienced some operational challenges with respect to this initiative, we took positive steps to address those challenges and, ultimately, were successful in reaching this milestone, which positions the Company well to achieve its goals for Fiscal 2020 and beyond.

The amount of time and effort required to operate our business (including achieving positive economic and financial results) alongside with pursuing these strategic and transformational initiatives (including the asset sales and the distribution center consolidation) created disruption and distraction for our employees and presented us with additional challenges in Fiscal 2019. Our management and employees devoted substantial additional time and effort to pursue or complete these initiatives, which were quite difficult to achieve particularly during the period of operational challenges and uncertainty facing the Company.

In Fiscal 2019, we transitioned away from annual Equity Incentive Program (“EIP”) grants with

one-year

performance periods and ourtwo-year

stretch Spectrum 3B Plan (“S3B Plan”) to a new program with cliff vesting following a three-year cumulative performance period. This transition to a three-year cliff vesting performance and service period under the new long term incentive program (“LTIP”) created a “gap” in our employees’ compensation opportunity, in that, under this new plan, there would be no long-term incentive vesting opportunity until September 30, 2021. The lack of any potential vesting or payout oflong-term

compensation opportunities during this gap period, which represents a significant portion of overall compensation, raised retention concerns. To address this gap, our Compensation Committee granted our NEOs and other selected employees special “Bridge Grants” (which will not be part of ongoing compensation) comprised of RSUs and PSUs that were primarily designed to: (i) provide annual vesting opportunities until the first of the new, annually granted long-term incentive awards would potentially vest after September 30, 2021, and (ii) address the related potential retention concerns.18

These Bridge Grants were granted at the beginning of Fiscal 2019 and were designed as two grants to cover two performance cycles, namely the Fiscal 2019 compensation cycle and the Fiscal 2020 compensation cycle. The vesting criteria applicable for the Bridge Grants are:

| ● | Fiscal 2019 Bridge Grant: |

| ● | Fiscal 2020 Bridge Grant: |

In addition, in recognition of the additional work and completion of the sales, we rewarded our NEOs with special transaction success bonuses (which represented in the aggregate 0.22% of the $2.9 billion net proceeds, prior to purchase price adjustments, received from the sales). No amounts would have been paid if the sales were not consummated. Because of the special circumstances surrounding the sale of our GBL and GAC businesses and our transition to a new long-term equity plan noted above, we do not believe that the Bridge Grants and the transaction success bonuses are indicative of our regular, ongoing annual compensation.

In conjunction with these changes to our equity compensation plans, we made further enhancements to our executive compensation programs by introducing for Fiscal 2020 a third performance metric (Adjusted Return on Equity) that will be weighted equally with Adjusted EBITDA and Adjusted Free Cash Flow for purposes of our equity performance programs; eliminating tax equalization on our financial and tax planning benefit, automobile allowance, and life insurance for all executives in Fiscal 2020; our CEO voluntarily agreeing to eliminate, commencing in Fiscal 2020, his tax planning and financial assistance benefit (including tax equalization) and his executive automobile allowance.

We also made improvements to our corporate governance and executive policies, including adopting a robust anti-pledging policy and strengthening our anti-hedging policy. We also added a majority voting and director resignation policy. In addition, as of January 1, 2020, we increased the required retention of netfor more information on these policies. Furthermore, we eliminated certain perquisites including any related tax equalization.

after-tax

shares by our directors, NEOs and other executives to 50% until they satisfy our stock ownership guidelines. See“Item 10: Directors, Executive Officers and Corporate Governance—Corporate Governance—Our Practices and Policies”

As Fiscal 2019 came to a close, Jefferies Financial announced, and shortly thereafter completed, the distribution of its 14% stake in the Company to its stockholders. Following the distribution, the representative of Jefferies Financial left our Board, completing our Company’s transition from being a controlled company to a widely-held public stockholder constituency.

Our Fiscal 2019 Results

Alongside all of the transformational activities, operational and management changes, and additional demands placed on our team, we attained positive financial results in Fiscal 2019, including those discussed below.

| ● | We increased or maintained our market positions, which includes our #1 position in the U.S. with residential and luxury locksets, outdoor insect control, grills, toaster ovens, indoor grills and our #1 global position with aquatics and rawhide chews. |

| ● | Our efforts with respect to our transformational and strategic initiatives are being recognized by the market, as our stock has increased 52.2% in price in calendar 2019, and has returned 56.2% in calendar 2019, including dividends. |

| ● | Revenue of $3,802.1 million and net loss from continuing operations of $186.7 million, including $151.4 million of non-cash impairment charges. |

| ● | Adjusted EBITDA of $567 million. |

| ● | Adjusted EBITDA stabilized and in line with guidance with increased investments across the divisions. |

| ● | Reduced total debt by $2.4 billion with proceeds from divestitures of the GBL and GAC businesses. |

19

| ● | Increased liquidity (cash and cash equivalent plus available credit under our revolving credit facility) by 5.7% to $1.4 billion. |

| ● | Reduced net leverage (net debt to Adjusted EBITDA) to 3.1x from 5.2x. |

| ● | Launched our Global Productivity Improvement Plan, expecting to improve overall annualized operating costs by approximately $100 million within the next 16 to 22 months. |

| ● | In Fiscal 2019, we returned over $355 million to our shareholders through share repurchases of $269 million and $86 million in dividends. |

| ● | In Fiscal 2020, we plan to further repurchase up to $250 million of our shares and have purchased $206 million as of December 29, 2019. |

| ● | Issued $300 million in 5.00% 10-year senior notes and retired all $570 million of our 6.625% senior notes. |

| ● | Incurred $60 million of cash tariffs in Fiscal 2019 that were mostly offset with pricing and productivity. |

Fiscal 2019 Named Executive Officers

The following individuals were our NEOs for Fiscal 2019:

David M. Maura | our Chief Executive Officer and Executive Chairman | ||

Douglas L. Martin (1) | our former Executive Vice President and Chief Financial Officer | ||