As confidentially submitted to the Securities and Exchange Commission on June 27, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Exmar Energy Partners LP

(Exact name of Registrant as specified in its charter)

| Republic of the Marshall Islands (State or other jurisdiction of incorporation or organization) | 4412 (Primary Standard Industrial Classification Code Number) | Not Applicable (I.R.S. Employer Identification No.) |

Room 3206, 32nd Floor

Lippo Center, Tower Two

No 89 Queensway

Hong Kong

+852 2861 9668

(Address, including zip code, and telephone number,

including area code, of Registrant's principal executive offices)

Watson, Farley & Williams LLP

1133 Avenue of the Americas

New York, New York 10036

(212) 922-2200

(Name, Address, including zip code, and telephone number,

including area code, of agent for service)

| Copies to: | ||

Catherine S. Gallagher Adorys Velazquez Vinson & Elkins L.L.P. 2200 Pennsylvania Avenue NW, Suite 500W Washington, DC 20037 Telephone: (202) 639-6500 Facsimile: (202) 639-6604 | Charles E. Carpenter William N. Finnegan IV Latham & Watkins LLP 885 Third Avenue, Suite 1000 New York, New York 10022 Telephone: (212) 906-1200 Facsimile: (212) 751-4864 | |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Proposed maximum aggregate offering price (1)(2) | Amount of registration fee | ||

|---|---|---|---|---|

Common units representing limited partner interests | $ | $ | ||

| ||||

- (1)

- Includes common units issuable upon exercise of the underwriters' option to purchase additional common units.

- (2)

- Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o).

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Subject to completion, dated , 2014

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Prospectus

Common units representing limited partner interests

Exmar Energy Partners LP

This is the initial public offering of common units representing limited partner interests of Exmar Energy Partners LP. We are offering common units in this offering. Prior to this offering, there has been no public market for our common units. We anticipate that the initial public offering price will be between $ and $ per common unit.

We are a Marshall Islands limited partnership formed to own, operate and acquire floating liquefied natural gas ("LNG") infrastructure assets under long-term charters. Our initial assets, which consist of a 50% interest in each of five joint ventures, will be contributed to us by EXMAR NV (NYSE Euronext Brussels: EXM). Although we are organized as a partnership, we have elected to be treated as a corporation for U.S. federal income tax purposes. We intend to apply to list our common units on the New York Stock Exchange under the symbol " ".

We are an "emerging growth company" as defined under the federal securities laws and, as such, may elect to comply with certain reduced reporting requirements. See "Prospectus Summary—Our Emerging Growth Company Status." Investing in our common units involves a high degree of risk. See "Risk Factors" beginning on page 24. These risks include the following:

- •

- We are dependent on Excelerate Energy as the sole charterer for the vessels in our current portfolio.

- •

- Our only income-generating assets are our interests in our joint ventures.

- •

- We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses to enable us to pay the minimum quarterly distribution on our common units.

- •

- We must make substantial capital expenditures to maintain and replace the operating capacity of the vessels in our joint ventures' fleet, which will reduce cash available for distribution.

- •

- We depend on EXMAR NV and its subsidiaries to assist us in operating and expanding our business.

- •

- Our growth depends on continued growth in demand in the floating LNG infrastructure market.

- •

- Unitholders have limited voting rights, and our partnership agreement restricts the voting rights of the unitholders owning more than 4.9% of our common units.

- •

- Our general partner and its other affiliates own a significant interest in us and have conflicts of interest and limited fiduciary and contractual duties, which may permit them to favor their own interests to your detriment.

- •

- Our general partner has a limited call right that may require you to sell your common units at an undesirable time or price.

- •

- U.S. tax authorities could treat us as a "passive foreign investment company," which would have adverse U.S. federal income tax consequences to U.S. unitholders.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| | Per common unit | Total | |||||

|---|---|---|---|---|---|---|---|

Initial public offering price | $ | $ | |||||

Underwriting discounts and commissions(1) | $ | $ | |||||

Proceeds to Exmar Energy Partners LP, before expenses | $ | $ | |||||

(1) Excludes an aggregate structuring fee of % of the gross proceeds payable to J.P. Morgan Securities LLC. Please read "Underwriting."

We have granted the underwriters an option for a period of 30 days from the date of this prospectus to purchase up to an additional common units. Delivery of the common units will be on or about , 2014.

J.P. Morgan

BofA Merrill Lynch

Citigroup

, 2014

Table of contents

| | Page | |

|---|---|---|

Prospectus summary | 1 | |

Overview | 1 | |

Our charterer | 3 | |

Our relationship with EXMAR | 3 | |

Business opportunities | 4 | |

Competitive strengths | 5 | |

Business strategies | 6 | |

Risk factors | 7 | |

Formation transactions | 8 | |

Holding company structure | 9 | |

Organizational and ownership structure after this offering | 9 | |

Our management | 10 | |

Principal executive offices and internet address | 11 | |

Summary of conflicts of interest and fiduciary duties | 11 | |

Our emerging growth company status | 12 | |

The offering | 14 | |

Summary historical financial and operating data | 20 | |

Risk factors | 24 | |

Risks inherent in our business | 24 | |

Risks inherent in an investment in us | 48 | |

Tax risks | 59 | |

Forward-looking statements | 63 | |

Use of proceeds | 65 | |

Capitalization | 66 | |

Dilution | 67 | |

Our cash distribution policy and restrictions on distributions | 68 | |

General | 68 | |

Forecasted results of operations for the twelve months ending June 30, 2015 | 71 | |

Forecast assumptions and considerations | 74 | |

Forecasted cash available for distribution | 78 | |

How we make cash distributions | 83 | |

Distributions of available cash | 83 | |

Operating surplus and capital surplus | 84 | |

Subordination period | 87 | |

Distributions of available cash from operating surplus during the subordination period | 89 |

i

| | Page | |

|---|---|---|

Distributions of available cash from operating surplus after the subordination period | 89 | |

General partner interest | 89 | |

Incentive distribution rights | 89 | |

Percentage allocations of available cash from operating surplus | 90 | |

Right to reset incentive distribution levels | 91 | |

Distributions from capital surplus | 94 | |

Adjustment to the minimum quarterly distribution and target distribution levels | 94 | |

Distributions of cash upon liquidation | 95 | |

Selected historical financial and operating data | 96 | |

Management's discussion and analysis of financial condition and results of operations | 100 | |

Overview and background | 101 | |

Factors affecting our results of operations | 105 | |

Customer | 107 | |

Inflation and cost increases | 107 | |

Results of operations | 108 | |

Liquidity and capital resources | 115 | |

Debt and lease restrictions | 127 | |

Capital commitments | 128 | |

Critical accounting policies | 129 | |

Recently adopted accounting standards | 131 | |

Recently issued accounting standards | 131 | |

Quantitative and qualitative disclosures about market risk | 132 | |

Industry | 134 | |

Overview of the natural gas market | 134 | |

Introduction to LNG | 138 | |

LNG supply | 140 | |

LNG demand | 141 | |

Floating LNG infrastructure technology | 142 | |

Charter contracts | 149 | |

LNG safety and security | 149 | |

Business | 150 | |

Overview | 150 | |

Our charterer | 151 | |

Our relationship with EXMAR | 151 | |

Business opportunities | 152 | |

Competitive strengths | 153 | |

Business strategies | 154 |

ii

| | Page | |

|---|---|---|

Our portfolio | 155 | |

Time charters | 158 | |

Vessel option agreement | 162 | |

Classification, inspection and maintenance | 163 | |

Safety, management of vessel operations and administration | 163 | |

Crewing and staff | 165 | |

Risk of loss, insurance and risk management | 165 | |

Environmental and other regulations | 166 | |

Properties | 178 | |

Legal proceedings | 178 | |

Employees | 178 | |

Taxation of the partnership | 178 | |

Management | 187 | |

Management of Exmar Energy Partners LP | 187 | |

Directors | 189 | |

Executive officers | 189 | |

Reimbursement of expenses of our general partner | 190 | |

Executive compensation | 190 | |

Compensation of directors | 190 | |

Security ownership of certain beneficial owners | 191 | |

Our joint ventures and joint venture agreements | 192 | |

General | 192 | |

Management of our joint ventures | 192 | |

Designation of service providers | 193 | |

Loans from joint venture partners | 194 | |

Dividends | 194 | |

Restrictions on transfer of equity interests; purchase rights | 194 | |

Duration and termination | 195 | |

Certain relationships and related party transactions | 196 | |

Distributions and payments to our general partner and its affiliates | 196 | |

Agreements governing the transactions | 198 | |

Conflicts of interest and fiduciary duties | 207 | |

Conflicts of interest | 207 | |

Fiduciary duties | 211 | |

Description of the common units | 215 | |

The units | 215 | |

Transfer agent and registrar | 215 |

iii

| | Page | |

|---|---|---|

Transfer of common units | 215 | |

The partnership agreement | 217 | |

Organization and duration | 217 | |

Purpose | 217 | |

Cash distributions | 217 | |

Capital contributions | 217 | |

Voting rights | 218 | |

Applicable law; forum, venue and jurisdiction | 220 | |

Limited liability | 220 | |

Issuance of additional securities | 222 | |

Tax status | 222 | |

Amendment of the partnership agreement | 222 | |

Merger, sale, conversion or other disposition of assets | 225 | |

Termination and dissolution | 225 | |

Liquidation and distribution of proceeds | 226 | |

Withdrawal or removal of our general partner | 226 | |

Transfer of general partner interest | 227 | |

Transfer of ownership interests in general partner | 228 | |

Transfer of incentive distribution rights | 228 | |

Change of management provisions | 228 | |

Limited call right | 228 | |

Board of directors | 229 | |

Meetings; voting | 230 | |

Status as limited partner or assignee | 231 | |

Indemnification | 231 | |

Reimbursement of expenses | 231 | |

Books and reports | 232 | |

Right to inspect our books and records | 232 | |

Registration rights | 232 | |

Units eligible for future sale | 233 | |

Material U.S. federal income tax considerations | 234 | |

Election to be treated as a corporation | 234 | |

U.S. federal income taxation of U.S. holders | 235 | |

U.S. federal income taxation of non-U.S. holders | 239 | |

Backup withholding and information reporting | 240 | |

Non-United States tax considerations | 241 | |

Marshall Islands tax consequences | 241 |

iv

| | Page | |

|---|---|---|

Belgium tax consequences | 241 | |

Hong Kong tax consequences | 242 | |

Underwriting | 243 | |

Commissions and expenses | 243 | |

No sales of similar securities | 244 | |

Indemnification | 244 | |

Stock exchange | 244 | |

Price stabilization, short positions | 244 | |

Affiliations | 245 | |

Selling restrictions | 245 | |

Legal matters | 248 | |

Experts | 248 | |

Expenses related to this offering | 249 | |

Where you can find more information | 249 | |

Industry and market data | 250 | |

Index to financial statements | 251 | |

Appendix A—Form of first amended and restated agreement of limited partnership of Exmar Energy Partners LP | A-1 | |

Appendix B—Glossary of terms | B-1 |

You should rely only on the information contained in this prospectus and in any free writing prospectus made available by us. We have not, and the underwriters have not, authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. Please read "Risk Factors" and "Forward-Looking Statements."

Service of process and enforcement of civil liabilities

We are organized under the laws of the Marshall Islands as a limited partnership. Our general partner is organized under the laws of the Marshall Islands as a limited liability company. The Marshall Islands has a less developed body of securities laws as compared to the United States and provides protections for investors to a significantly lesser extent.

Most of our directors and officers and those of our subsidiaries and joint ventures are residents of countries other than the United States. Substantially all of the assets of our subsidiaries and our joint ventures and a substantial portion of the assets of our directors and officers are located outside the United States. As a result, it may be difficult or impossible for United States investors to effect service of process within the United States upon us, the directors or officers of our general partner, our general partner, our subsidiaries or our joint ventures or to realize against us or them judgments obtained in United States courts, including judgments predicated upon the civil liability provisions of the securities laws of the United

v

States or any state in the United States. However, we have expressly submitted to the jurisdiction of the U.S. federal and New York state courts sitting in the City of New York for the purpose of any suit, action or proceeding arising under the securities laws of the United States or any state in the United States, and we have appointed Watson, Farley & Williams LLP to accept service of process on our behalf in any such action.

Watson, Farley & Williams LLP, our counsel as to Marshall Islands law, has advised us that there is uncertainty as to whether the courts of the Marshall Islands would (1) recognize or enforce against us, our general partner or our directors or officers judgments of courts of the United States based on civil liability provisions of applicable U.S. federal and state securities laws; or (2) impose liabilities against us, our general partner or our directors and officers in original actions brought in the Marshall Islands, based on these laws.

We own or have rights to various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties' trademarks, service marks, trade names or products in this prospectus is not intended to, and does not imply a relationship with, or endorsement or sponsorship by us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, service marks and trade names.

As used in this prospectus, unless the context indicates or otherwise requires, references to:

- •

- "Exmar Energy Partners LP," "Exmar Energy," "the Partnership," "we," "our," "us" or similar terms (i) when used in a historical context are to our predecessor for accounting purposes (as described in more detail below under "—Presentation of Financial Information") and (ii) when used in the present tense or prospectively are to Exmar Energy Partners LP and its subsidiaries;

- •

- "our general partner" are to Exmar General Partner Ltd., the general partner of Exmar Energy;

- •

- "EXMAR" are to Exmar NV (NYSE Euronext Brussels: EXM) and its subsidiaries, other than Exmar Energy and its subsidiaries, including Exmar Shipmanagement NV ("Exmar Shipmanagement"), Exmar Marine NV ("Exmar Marine") and Exmar Hong Kong Ltd ("Exmar Hong Kong");

- •

- our "Operating Company" are to Exmar Energy Hong Kong Ltd;

- •

- "our portfolio," "our vessels" or like terms are to the vessels described below that are owned by our joint ventures; we will own a 50.0% equity interest in each joint venture:

- •

- Excelerate,Explorer andExpress, which are owned respectively by Excelerate NV, Explorer NV and Express NV, each a Belgiannaamloze vennootschap (the "Exmar-Excelerate joint ventures"), 50.0% of the equity interests of which will be indirectly owned by each of us and Excelerate Energy, L.P. ("Excelerate Energy") immediately following the closing of this offering;

vi

- •

- Excelsior, which is owned by Excelsior BVBA, a Belgianbesloten vennootschap met beperkte aansprakelijkheid, 50.0% of the equity interests of which will be indirectly owned by each of us and Teekay LNG Partners L.P. (NYSE: TGP) ("Teekay LNG") immediately following the closing of this offering; and

- •

- Excalibur, which is leased by Solaia Shipping L.L.C., a Liberian limited liability company (together with Excelsior BVBA and certain entities related to Solaia Shipping L.L.C., the "Exmar-Teekay joint ventures"), 50.0% of the equity interests of which will be indirectly owned by each of us and Teekay LNG immediately following the closing of this offering;

- •

- "our joint ventures" are to the Exmar-Excelerate joint ventures and the Exmar-Teekay joint ventures, collectively;

- •

- "our charter," "our operations" and like terms refer to the charters and operations of our joint ventures;

- •

- "shareholder loans" include any loans made by us or our joint venture partners to our joint ventures and any bonds issued by our joint ventures to us or our joint venture partners. For a description of each such arrangement, please read "Management's Discussion & Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Borrowing Activities—Joint Venture Facilities"; and

- •

- "vessels" include floating LNG infrastructure assets, including LNG carriers, floating storage and regasification units, LNG regasification vessels and floating liquefaction and storage units.

A glossary of certain industry and other terms used in this prospectus is included as Appendix B.

Presentation of financial information

Predecessor and Rule 3-09 financial statements

Our predecessor for accounting purposes, Exmar Energy Partners LP Predecessor ("our Predecessor"), accounts for its equity interests in the joint ventures owning the vessels in our portfolio as equity method investments in its combined financial statements. Rule 3-09 of Regulation S-X requires separate financial statements ("Rule 3-09 financial statements") of 50% or less owned persons accounted for under the equity method by a registrant such as us if either the income or the investment test in Rule 1-02(w) of Regulation S-X exceeds 20%. Furthermore, Rule 3-09(c) of Regulation S-X provides for the combination of Rule 3-09 financial statements if the underlying investments exhibit common control or common management. In such scenarios, the significance of investments under Rule 1-02(w) of Regulation S-X are to be measured on a combined basis. We have determined that common management exists among the Exmar-Excelerate joint ventures and among the Exmar-Teekay joint ventures, both of which exceed on a combined basis the 20% significance tests of Rule 3-09. Accordingly, this prospectus includes audited combined financial statements as of and for the years ended December 31, 2013 and 2012 and unaudited combined interim financial statements as of March 31, 2014 and for the three months ended March 31, 2014 and 2013, for both the Exmar-Excelerate joint ventures and the Exmar-Teekay joint ventures. Such financial statements, including the applicable notes thereto, have been prepared in accordance with U.S. generally accepted accounting principles ("U.S. GAAP").

vii

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the historical financial statements and the notes to those financial statements. You should read "Risk Factors" for more information about important risks that you should consider carefully before buying our common units. The information presented in this prospectus assumes, unless otherwise noted, that (i) the initial public offering price of the common units will be $ per unit (the midpoint of the range set forth on the cover page of the prospectus) and (ii) the underwriters' option to purchase additional common units is not exercised.

All references in this prospectus to "our portfolio," "our vessels" or like terms are to the vessels Excelerate, Explorer, Express, Excelsior and Excalibur, which are owned by our joint ventures. Following the completion of this offering, we will own a 50% equity interest in each of our joint ventures. Unless otherwise indicated, all references to "dollars" and "$" in this prospectus are to, and amounts are presented in, U.S. Dollars. Please read "Certain Definitions" for definitions of certain terms used in, and "Presentation of Financial Information" for information pertaining to the financial information included in, this prospectus.

We are a growth-oriented limited partnership formed by EXMAR to own, operate and acquire floating LNG infrastructure assets under long-term charters, which we define as charters of five years or more. Our goal is to be a primary provider of floating LNG liquefaction, transportation, storage and regasification services to the natural gas industry. Following the completion of this offering, EXMAR will own a significant interest in us and we believe EXMAR will be incentivized to help us grow. We intend to leverage EXMAR's expertise, relationships, reputation, focus on project development and ability to work with joint venture partners to pursue strategic and accretive opportunities across the floating LNG infrastructure industry.

EXMAR specializes in marine infrastructure solutions for liquefaction, transportation, storage and regasification of natural gas, the transportation of liquefied petroleum gas ("LPG"), ammonia and petrochemical gases as well as the provision of other offshore services within the global oil and natural gas industry. We believe that EXMAR has pioneered certain technological advances in the LNG sector. For example, in 2002, EXMAR was the first company to order and build an LNG regasification vessel ("LNGRV"), a vessel fitted to discharge high pressure natural gas directly into a shoreside pipeline system, and subsequently developed the commercialization of LNG ship-to-ship transfer technology. Having successfully introduced these innovative technologies, EXMAR is currently developing the world's first floating liquefaction and storage unit ("FLSU"). Historically, EXMAR has grown its portfolio of vessels in part through 50/50 joint ventures with partners with whom they have developed strong and longstanding relationships. In each case, EXMAR is the manager of the vessel.

1

Upon the closing of this offering, our initial portfolio will consist of interests in four LNGRVs and one LNG carrier, all of which are in joint ventures (in each of which we will own a 50% equity interest) and operating under long-term time charters with Excelerate Energy:

The following table provides information about our four LNGRVs:

| LNGRV | Capacity (cbm) | Delivery date | Our joint venture interest | Joint venture counterparty | Charterer | Charter expiration | Charter extension option period(s) | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Excelsior | 138,000 | January 2005 | 50% | Teekay LNG | Excelerate Energy | January 2025 | Five years plus five years | |||||||||||||||

Excelerate(1) | 138,000 | October 2006 | 50% | Excelerate Energy | Excelerate Energy | October 2026 | Five years plus five years | |||||||||||||||

Explorer(1) | 150,900 | April 2008 | 50% | Excelerate Energy | Excelerate Energy | April 2033 | Five years | |||||||||||||||

Express(1) | 150,900 | May 2009 | 50% | Excelerate Energy | Excelerate Energy | May 2034 | Five years | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Total capacity | 577,800 | |||||||||||||||||||||

(1) TheExcelerate, Explorer and Express are subject to a vessel option agreement pursuant to which Excelerate Energy is permitted to offer to sell or grant a purchase option on each such vessel to a customer who charters the vessel for a minimum five-year period. Excelerate Energy can sell or grant a purchase option on the vessels at any time, but no such offer or purchase option may call for a transfer of any vessel prior to January 2024. See "Business—Vessel option agreement."

The following table provides information about our LNG carrier:

| LNG carrier | Capacity (cbm) | Year of delivery | Our joint venture interest | Joint venture counterparty | Charterer | Charter expiration | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Excalibur(1)(2) | 138,000 | October 2002 | 50% | Teekay LNG | Excelerate Energy | March 2022 | ||||||||||

(1) Excelerate Energy was granted an option to purchase theExcalibur prior to September 2021. Even if the option is exercised,Excalibur will not be sold to Excelerate Energy until March 2022. See "Business—Time charters—LNG carrier charter—Purchase option."

(2) TheExcalibur is subject to a UK capital lease, and the title thereto is held by the LNG carrier lessor. Please read "Management's Discussion and Analysis of Financial Condition and Results of Operations—Debt and Lease Restrictions—UK Capital Lease."

Pursuant to the omnibus agreement that we will enter into with EXMAR at the closing of this offering, we will have the right to purchase from EXMAR any floating LNG infrastructure asset operating under a charter of five or more years. In addition, we will have the right to purchase the following interests from EXMAR:

- •

- all or a portion of EXMAR's 90% to 100% interest in theCaribbean FLNG, a newbuilding FLSU, within 24 months following the commencement of its operations, which is currently scheduled for the second half of 2015. TheCaribbean FLNG will operate under a 15-year contract (tolling agreement) with Pacific Rubiales Energy Corp. ("PRE"), an independent oil and gas exploration company in Colombia, and will be located off the Colombian Caribbean coast; and

- •

- a 50% interest inExcel, an LNG carrier delivered in 2003 that is jointly owned with Mitsui O.S.K. Lines, Ltd., within 24 months following the commencement of a charter for theExcel of five or more years.

2

We will not be obligated to purchase any such interests from EXMAR. The terms and conditions of any such purchase (including, among other things, whether we purchase all or less than all of EXMAR's interests in any such vessel) will be negotiated with EXMAR at the time any such offer is made to us, and will be based on the facts and circumstances at the time any such offer is made to us, all in accordance with the provisions of the omnibus agreement. Please read "Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Omnibus Agreement" for a description of our rights to acquire certain assets of EXMAR.

Each of the vessels in our portfolio is under time charter with Excelerate Energy. Excelerate Energy is a private, U.S. based developer of LNG transportation, storage and regasification infrastructure as well as a trader of LNG. Excelerate Energy is owned by George B. Kaiser, an American entrepreneur and the principal owner of the Kaiser Francis Oil Company, one of the largest private energy producers in the United States, as well as the Bank of Oklahoma. George B. Kaiser was ranked number 40 on the Forbes 400 list of wealthy Americans in 2013.

Upon completion of this offering, EXMAR will own our general partner, as well as % of our common units and all of our subordinated units, which we believe will provide it with significant incentives to contribute to our success. EXMAR has informed us that it intends to utilize us as its primary growth vehicle to pursue acquisitions of long-term stable cash flow generating assets across the floating LNG infrastructure industry. Please read "Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Omnibus Agreement" for a description of our rights to acquire certain assets of EXMAR.

We believe one of our principal strengths is our relationship with EXMAR. EXMAR is a fully integrated provider of LNG solutions within the broader LNG value chain, operating a portfolio of 14 LNG vessels (including our vessels) that is comprised of nine LNGRVs and five LNG carriers. We believe EXMAR has pioneered the development of floating LNG import terminals through LNGRVs. In the second half of 2015, EXMAR is scheduled to commence operations of the world's first FLSU, theCaribbean FLNG. EXMAR's other activities include the provision of offshore services within the global oil and natural gas industry as well as the transportation of LPG, ammonia and petrochemical gases through the operation of 39 LPG carriers, including 12 newbuildings, and three accommodation barges in the offshore sector.

We expect our association with EXMAR will give us access to the relationships that EXMAR has established with major energy companies, shipbuilders and financial institutions as a result of its history and experience in providing LNG solutions. In addition, Exmar Shipmanagement, a wholly-owned subsidiary of EXMAR, will continue to provide our joint ventures with technical and crewing management services. EXMAR Shipmanagement has a strong reputation in the floating LNG infrastructure industry and is a key partner to companies such as Teekay LNG, Excelerate Energy, ENI S.p.A., OLT Offshore LNG Toscana S.p.A. and Avance Gas Holding Ltd. We can provide no assurance, however, that we will realize any benefits from our relationship with EXMAR, or that EXMAR's relationships with major energy companies, shipbuilders and financial institutions will continue in the future.

3

We believe that the following factors create opportunities for us to successfully execute our business plan and grow our operations:

- •

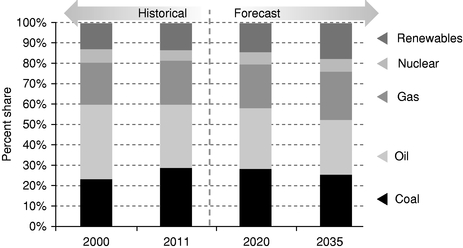

- Increased global consumption and changing supply dynamics for natural gas. According to theWorld Energy Outlook 2013 of the International Energy Agency ("IEA"), natural gas is the only hydrocarbon projected to expand its share of the global primary energy market, with market share declines expected for oil and coal, a trend that is currently underway in many key regions. Global demand for natural gas increased 37% from 2000 to 2012 as world economies sought cleaner energy sources to reduce pollution and meet incremental power demand and public support for nuclear power declined following the Fukushima Daiichi nuclear incident. According to the IEA, these trends are expected to continue with natural gas demand projected to grow by approximately 50% from 3.3 trillion cubic meters ("Tcm") in 2012 to nearly 5.0 Tcm in 2035. While member countries of the Organisation of Economic Co-operation and Development ("OECD") historically have been the primary driver of incremental demand for natural gas, the IEA forecasts that demand growth will be the greatest in emerging markets, with the largest demand increases expected in China and India. The increase in demand for natural gas has been met with an even greater increase in supply, driven by technological advances, including horizontal and deepwater drilling as well as hydraulic fracturing, which are enabling recovery of significant reserves of unconventional natural gas (i.e. shale gas, tight gas and coal bed methane). According to the IEA, technically recoverable remaining global natural gas reserves totaled 810.0 Tcm at year-end 2012, representing a reserve-to-production ("R/P") ratio of 238 years based on natural gas production for the year ended December 31, 2011.

- •

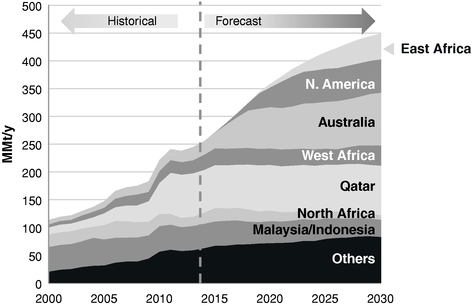

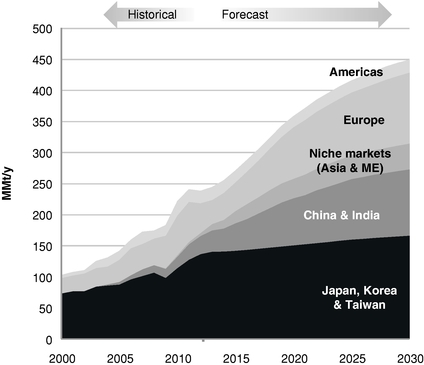

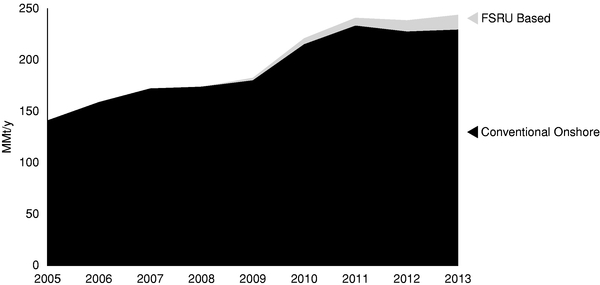

- Growing demand for floating LNG infrastructure solutions. Rapidly shifting demand and supply dynamics for natural gas have created new regional imbalances and spurred an increasing need for fast-track, floating LNG solutions. A combination of growing environmental and regulatory pressures, new LNG production capacity and competitive pricing is projected to increase LNG demand in the future, which, according to Poten & Partners, Inc. ("Poten"), is forecasted to surpass 350.0 million tons per year ("MMt/y") by 2020 and 450.0 MMt/y by 2030, as compared to 238.0 MMt/y in 2013. According to Poten, LNG demand growth is forecasted to be strong in Asia and in the new markets of Central and South America and the Middle East. We believe that floating LNG infrastructure solutions are timely, cost-effective, flexible and reliable ways of bringing LNG to the marketplace because of their relatively low capital costs and short development time compared to conventional onshore solutions. Floating LNG infrastructure solutions include:

- •

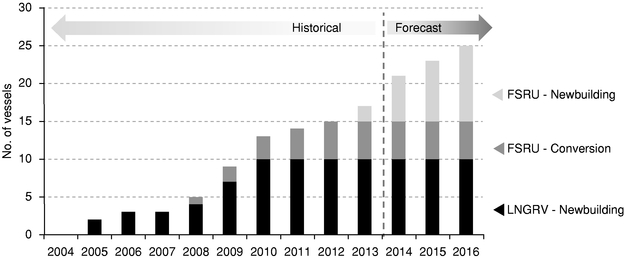

- Floating storage and regasification. Compared to onshore terminals, floating storage and regasification units offer many advantages, including a relatively shorter construction schedule, lower capital costs, less geographic and political constraints and ease of relocation. We believe that customers, particularly those in developing countries, benefit from floating regasification units because they require less local competency and time to implement relative to onshore facilities. According to Poten, the number of floating regasification units operating around the world is projected to reach 25 units by 2020 from 14 units operating as of February 2014.

4

- •

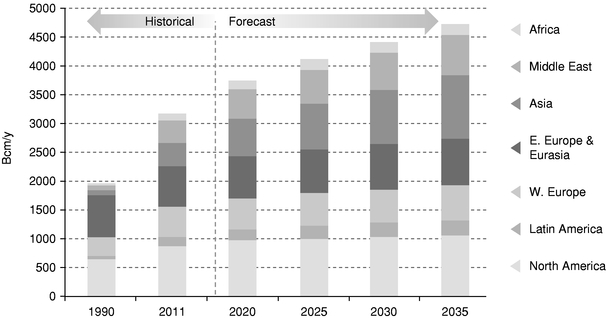

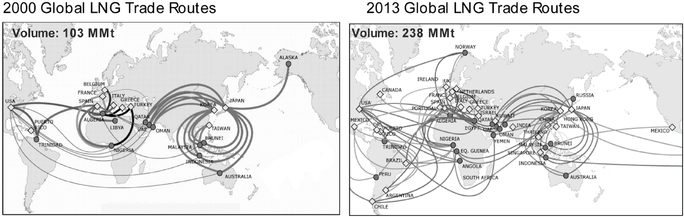

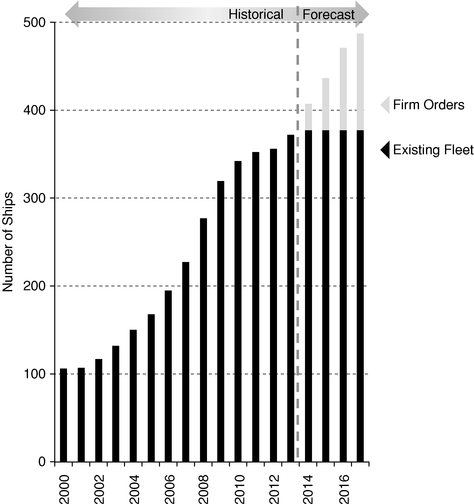

- LNG transportation. The transportation of LNG has helped enable the growth in global trade of natural gas and created efficiency between regional natural gas markets. Driven by the growth in LNG supply and the longer-haul nature of the trades, the number of specialized LNG carriers has grown by more than 250% since 2000 to approximately 370 in 2013. Growing inter-regional trades have been fostered by local producer market surpluses located far from demand centers. The IEA forecasts inter-regional natural gas trades will increase by nearly 60% from 685 billion cubic meters per year ("Bcm/y") in 2011 to 1.1 Tcm/y in 2035. The IEA projects that inter-regional trades will be split equally between pipelines and LNG by 2030 as compared to a trade split of 58% and 42% for pipeline and LNG, respectively, in 2010. With an abundance of unconventional natural gas reserves, North America has the potential to become a major LNG exporter, creating new long-haul trading routes. We believe these aforementioned trends suggest a strong future demand for LNG carriers.

- •

- Floating liquefaction. Floating liquefaction represents the next phase of development in the floating LNG infrastructure industry. We believe that mobile and re-deployable floating liquefaction ("FLNG") units will offer the potential to unlock natural gas reserves without the need to invest in capital-intensive pipeline infrastructure, infield platforms and onshore infrastructure, allowing development in areas where the cost of onshore terminals would be prohibitive. We believe that the relatively lower start-up costs and shorter construction periods for FLNG units as compared to conventional onshore LNG projects will enable the efficient monetization of more challenging, smaller and/or remote natural gas resources. There are four floating liquefaction units currently being built with another 13 announced projects under study.

- •

- High barriers to entry. We believe the capital investment and technical expertise required to build and operate sophisticated floating LNG infrastructure assets creates significant barriers to entry, especially as they relate to floating regasification and liquefaction units. As a result, there are currently a limited number of companies that operate such assets, and only three operators have announced plans to build and operate FLNG units. Given that these assets play a key role in the broader supply chain to provide power generation to specific markets, we believe customers will place a premium on high quality, experienced operators of floating LNG storage, regasification and liquefaction units at the onset of the project to avoid potential costly power plant outages.

We can provide no assurance, however, that any of the projections and forecasts described in the factors above will occur.

We believe that our future prospects for success are enhanced by the following aspects of our business:

- •

- Long-term time charter agreements provide significant cash flow security and stability. Our initial vessels operate under long-term time charters with an established counterparty, Excelerate Energy. As of March 31, 2014, these charters had an average remaining term of approximately 14.1 years (excluding extension options), with no exposure to commodity prices. Through our partnership with Excelerate Energy, our vessels ultimately serve the complex needs of global energy providers such as Petróleo Brasileiro S.A. ("Petrobras") and Yacimientos Petrolíferos Fiscales ("YPF"). Additionally, three of our five time charters include provisions that allow us to pass our actual operating costs through to our customer, enhancing the stability of our cash flows.

5

- •

- Modern, technologically advanced and versatile vessels. We own a strategic portfolio of modern floating LNG infrastructure assets equipped with advanced technologies, which will allow us to expand our presence across the rapidly growing floating LNG infrastructure industry. The average age of our initial vessels was approximately 7.8 years as of March 31, 2014. We believe the reliability, efficiency and technological sophistication of our assets give us a competitive advantage. In addition, our LNGRVs are capable of performing as conventional LNG carriers, sailing at a service speed of 19 knots, which we believe gives us an advantage over peers operating fully docked, immobile floating regasification units. Furthermore, two sets of our vessels are sister ships, which enables us to benefit from economies of scale and operating efficiencies in vessel construction, crew training, crew rotation and shared spare parts.

- •

- Opportunities for significant future growth. We intend to leverage our relationship with EXMAR to make strategic and accretive acquisitions from EXMAR and third parties to enhance our position in the global LNG value chain. Pursuant to our omnibus agreement with EXMAR, we have a right to purchase from EXMAR any floating LNG infrastructure asset operating under a long-term charter of five years or more. In addition, we will have the right to purchase the following interests from EXMAR: (i) all or a portion of EXMAR's 90% to 100% interest in theCaribbean FLNG, a newbuilding FLSU, within 24 months following the commencement of its operations, which is currently scheduled in the second half of 2015, and, (ii) a 50% interest in theExcel, an LNG carrier, within 24 months following the commencement of a charter for theExcel of five or more years. We believe these identified acquisition opportunities and future potential acquisition opportunities from EXMAR and third parties provide us significant avenues to diversify our portfolio and increase our cash distributions to unitholders.

- •

- EXMAR's expertise and relationships. EXMAR has over 40 years of experience operating in the offshore oil and gas markets, including a distinguished track record of innovation and established technical, commercial and managerial expertise. We believe our access to EXMAR's technological expertise, strong relationships with customers, financing providers and shipyards and pool of experienced and qualified global seafarers will enable us to successfully grow our business. Our relationship with EXMAR also offers us access to the technical and crewing managerial expertise of Exmar Shipmanagement, a wholly-owned subsidiary of EXMAR with a reputation for providing best-in-class service to its customers.

- •

- Experienced senior management team. Our senior management team, including the executive members of our board of directors, has demonstrated the ability to maintain strong relationships with established joint venture partners, including our joint venture partners, Excelerate Energy and Teekay LNG, and to successfully undertake independent projects as well as make accretive acquisitions. The members of our senior management team and the executive members of our board of directors have an average of over 25 years of experience in the floating LNG infrastructure industry. Members of our senior management team have been operating and growing the assets of EXMAR for over ten years. During that time, EXMAR has grown both through establishing several successful strategic joint venture relationships with established partners and successfully completing several independent strategic acquisitions.

Our primary business objective is to increase quarterly distributions per unit over time by executing the following strategies:

- •

- Pursue growth through strategic and accretive acquisitions. We intend to leverage our relationship with EXMAR to make strategic and accretive acquisitions. Pursuant to our omnibus agreement with EXMAR, we will have opportunities to acquire additional floating LNG infrastructure assets from EXMAR.

6

In addition to diversifying our customer base, an acquisition by us of all of EXMAR's interest in theCaribbean FLNG from EXMAR pursuant to the terms of our omnibus agreement would provide us with significant additional revenues based on its current charter agreement, nearly doubling revenues generated by our joint ventures for the year ended December 31, 2013. In addition to acquisitions from EXMAR, we intend to capitalize on opportunities to grow our portfolio and diversify our customer base through accretive acquisitions from third parties and potential new joint ventures.

- •

- Manage our operations to provide a stable and secure base of cash flows. We intend to manage our portfolio of floating LNG infrastructure assets to provide stable cash flows by continuing to pursue long-term charters with established customers. We believe the projected growth in demand for floating LNG infrastructure solutions coupled with EXMAR's established industry relationships will provide us with attractive opportunities to acquire new vessels. We intend to continue to utilize long-term charters to maintain stability of our cash flows by actively seeking the extension or renewal of existing charters and by entering into new long-term charters with existing and other reputable customers. In addition, we intend to continue to structure our long-term charters with provisions that allow us to mitigate operating cost overruns and inflation, thereby enhancing the stability of our cash flows.

- •

- Continue to be a leader in providing floating LNG infrastructure solutions and excellent customer service. Following the completion of this offering, EXMAR will own a significant interest in us and we believe EXMAR will be incentivized to help us grow. We intend to leverage EXMAR's experience and operating history to maintain our leadership in the floating LNG infrastructure industry. In addition, we intend to provide innovative solutions to maintain our high operating standards and safety record. We believe that EXMAR has developed a reputation for offering high quality service to its customers. We intend to utilize our relationship with EXMAR to continue to focus on providing exceptional performance to our customers.

None of the EXMAR relationships described above are contractual or formal, except to the extent that Exmar and our joint ventures have entered into charters with certain of our and their respective customers. EXMAR has developed informal relationships with major energy companies, shipbuilders and financial institutions in connection with providing marine infrastructure solutions. EXMAR has informal relationships with, among others, Statoil ASA, Royal Dutch Shell plc, Itochu Corporation, Daewoo Shipbuilding & Marine Engineering Co., Ltd, Hyundai Heavy Industries Co., Ltd., Hanjin Shipping Co. Ltd, the International Finance Corporation (World Bank Group), DNB ASA and Nordea Bank AB.

An investment in our common units involves risks associated with our business, our partnership structure and the tax characteristics of our common units. Please read carefully the risks described under "Risk Factors" beginning on page 24 of this prospectus.

We were formed as a Marshall Islands limited partnership to own, operate and acquire floating LNG infrastructure assets under long-term charters. In connection with this offering, EXMAR will contribute all of its equity interests in each of the entities owning or leasing our five initial vessels to us.

7

Additionally, each of the following transactions have occurred or will occur in connection with the closing of this offering:

- •

- we will issue common units and subordinated units, representing an aggregate % limited partner interest in us, to EXMAR;

- •

- we will issue all of our incentive distribution rights to our general partner;

- •

- we will issue common units to the public in this offering, representing a % limited partner interest in us, and will apply the net proceeds as described in "Use of Proceeds";

- •

- We will grant the underwriters a 30-day option to purchase up to add itional common units;

- •

- we will enter into a new $20.0 million revolving credit facility with EXMAR;

- •

- we will enter into an omnibus agreement with EXMAR, our general partner, our Operating Company and certain subsidiaries of EXMAR governing, among other things:

- •

- the extent to which we and EXMAR may compete with each other;

- •

- our right to purchase all or a portion of EXMAR's interest in theCaribbean FLNG, within 24 months following the commencement of its operations;

- •

- our right to purchase an interest in theExcel, within 24 months following the commencement of a charter for theExcel of five years or more;

- •

- our right to purchase from EXMAR any floating LNG infrastructure assets operating under charters of five or more years as described under "Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Omnibus Agreement;" and

- •

- EXMAR's provision of certain indemnities to us;

- •

- our joint ventures will remain parties to management agreements with Exmar Shipmanagement pursuant to which Exmar Shipmanagement provides our joint ventures with crewing and technical management services;

- •

- we will enter into a management and administrative services agreement with Exmar Hong Kong, a wholly owned subsidiary of EXMAR, and our general partner pursuant to which Exmar Hong Kong will agree to provide certain management and administrative services to us and our general partner;

- •

- we will enter into an amendment to the credit facility relating toExcelerate;and

- •

- the Exmar-Teekay joint ventures will enter into a new $175.0 million credit facility to refinance into one credit facility the credit facilities relating toExcelsior andExcalibur.

The Exmar-Excelerate joint ventures are parties to services agreements with EXMAR and its subsidiaries pursuant to which EXMAR and its subsidiaries provide management and administrative services to the Exmar-Excelerate joint ventures; accounting and corporate administration services are provided by EXMAR and its subsidiaries to the Exmar-Teekay joint ventures pursuant to each applicable joint venture agreement.

The number of common units to be issued to EXMAR includes common units that will be issued at the expiration of the underwriters' option to purchase additional common units, assuming that

8

the underwriters do not exercise the option. Any exercise of the underwriters' option to purchase additional common units would reduce the common units shown as issued to EXMAR by the number to be purchased by the underwriters in connection with such exercise. If and to the extent the underwriters exercise their option to purchase additional common units, the number of common units purchased by the underwriters pursuant to any exercise will be sold to the public, and any remaining common units not purchased by the underwriters pursuant to any exercise of the option will be issued to EXMAR at the expiration of the option period for no additional consideration.

For further details on our agreements with EXMAR and its affiliates, please read "Certain Relationships and Related Party Transactions."

We are a holding entity and conduct our operations and business through subsidiaries and joint ventures. We derive all of our income from our interests in our joint ventures. We own a 50% interest in five joint ventures, each of which owns one vessel in our initial portfolio. Teekay LNG is our partner in the joint ventures that ownExcalibur andExcelsior. Excelerate Energy is our partner in the joint ventures that ownExcelerate,Express andExplorer. Teekay LNG and Excelerate Energy are leading companies with substantial industry experience. Neither we nor our joint venture partners exercise affirmative control over our joint ventures. We are entitled to appoint one half of the members of the board of directors governing each such joint venture. A majority of votes is required for the board of directors of each joint venture to act and as a result, neither we nor our joint venture partners are able to cause the joint venture to act over the objection of the other joint venture partner. Our joint ventures are further described in "Our Joint Ventures and Joint Venture Agreements."

Organizational and ownership structure after this offering

After giving effect to the transactions described above, assuming no exercise of the underwriters' option to purchase additional common units, our units will be held as follows:

| | Number of units | Percentage ownership | |||||

|---|---|---|---|---|---|---|---|

Public common units | % | ||||||

EXMAR common units | |||||||

EXMAR subordinated units | |||||||

Total | 100.0% | ||||||

9

The following diagram depicts our simplified organizational and ownership structure after giving effect to the offering and related transactions described above:

(1) The remaining 50% equity interest in the joint ventures owningExcelerate, Explorer andExpress are owned by an affiliate of Excelerate Energy.

(2) We and our joint venture partner are each entitled to appoint one half of the members of the joint venture's board of directors.

(3) The remaining 50% equity interest in the joint venture owningExcelsior and in the joint ventures that are parties to agreements related to the UK capital lease ofExcalibur are owned by an affiliate of Teekay LNG.

(4) Excalibur is subject to a UK capital lease, and the title thereto is held by the LNG carrier lessor. In addition to Solaia Shipping LLC, we will own a 50% equity interest in two joint ventures that are parties to ancillary agreements executed in connection with the UK capital lease: (i) Exmar Excalibur Shipping Company Limited (England) and (ii) Excalibur Shipping Company Limited (Isle of Man). Please read "Management's Discussion and Analysis of Financial Condition and Results of Operations—Debt and Lease Restrictions—UK Capital Lease."

Our partnership agreement provides that our general partner will irrevocably delegate to our board of directors the authority to oversee and direct our operations, management and policies on an exclusive basis. We do not have any executive officers and rely solely on the executive officers of EXMAR and its subsidiaries who will perform executive officer services for our benefit pursuant to the management and

10

administrative services agreement and who will be responsible for our day-to-day management subject to the direction of our board of directors. All references in this prospectus to "our officers" refer to those officers of EXMAR and its subsidiaries who perform executive officer functions for our benefit.

Our joint ventures are parties to management agreements with Exmar Shipmanagement pursuant to which Exmar Shipmanagement provides certain crewing and technical management services. Pursuant to the management agreements, our joint ventures pay Exmar Shipmanagement fees for providing crewing and technical management services.

In addition, we and our general partner will enter into a management and administrative services agreement with Exmar Hong Kong, pursuant to which Exmar Hong Kong will provide management and administrative services to us and our general partner. We will reimburse Exmar Hong Kong for its reasonable costs and expenses incurred in connection with the provision of these services. We project that we will reimburse Exmar Hong Kong approximately $2.2 million in total under the management and administrative services agreement for the twelve months ending June 30, 2015.

The Exmar-Excelerate joint ventures are parties to services agreements with EXMAR and its subsidiaries pursuant to which EXMAR and its subsidiaries provide management and administrative services. Accounting and corporate administration services are provided by EXMAR and its subsidiaries to the Exmar-Teekay joint ventures pursuant to each applicable joint venture agreement. Our joint ventures pay EXMAR and its subsidiaries a monthly fee in connection with the provision of these services.

For a more detailed description of these agreements, please read "Our Joint Ventures and Joint Venture Agreements," "Certain Relationships and Related Party Transactions—Agreements Governing the Transaction—Management and Administrative Services Agreement" and "Certain Relationships and Related Party Transactions—Agreements Governing the Transactions—Joint Venture Services Agreements."

Principal executive offices and internet address

Our registered and principal executive offices are located at Room 3206, 32nd Floor, Lippo Center, Tower Two, No 89 Queensway, Hong Kong and our phone number is +852 2861 9668. We expect to make our periodic reports and other information filed with or furnished to the United States Securities and Exchange Commission (the "SEC") available, free of charge, through our website at www.exmarenergypartners.com, which will be operational after this offering, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Please read "Where You Can Find More Information" for an explanation of our reporting requirements as a foreign private issuer.

Summary of conflicts of interest and fiduciary duties

Our general partner and our directors will have a legal duty to manage us in a manner beneficial to our unitholders, subject to the limitations described under "Conflicts of Interest and Fiduciary Duties." This legal duty is commonly referred to as a "fiduciary duty." Our directors have fiduciary duties to manage us in a manner beneficial to us, our general partner and our limited partners. As a result of these relationships, conflicts of interest may arise between us and our unaffiliated limited partners on the one hand, and EXMAR and its affiliates, including our general partner, on the other hand. The resolution of these conflicts may not be in the best interest of us or our unitholders. In particular:

- •

- our chief executive officer, chief financial officer and of our current directors also serve as executive officers and/or directors of EXMAR;

11

- •

- EXMAR and its affiliates may compete with us, subject to the restrictions contained in the omnibus agreement, and our ability to compete with EXMAR will be limited because we will be prohibited from owning, operating or chartering LNG infrastructure assets under short-term charters, subject to certain exceptions; and

- •

- we have entered into arrangements, and may enter into additional arrangements, with EXMAR and certain of its subsidiaries, relating to our right to purchase additional vessels, the provision of certain services to us by Exmar Shipmanagement, Exmar Marine and Exmar Hong Kong and other matters. In the performance of their obligations under these agreements, EXMAR and its subsidiaries, other than our general partner, are not held to a fiduciary duty standard of care to us, our general partner or our limited partners, but rather to the standard of care specified in these agreements.

For a more detailed description of the conflicts of interest and fiduciary duties of our general partner and its affiliates, please read "Conflicts of Interest and Fiduciary Duties."

Although a majority of our directors will over time be elected by common unitholders, our general partner will likely have substantial influence on decisions made by our board of directors. For a more detailed description of our management structure, please read "Management—Directors," "Management—Executive Officers" and "Certain Relationships and Related Party Transactions."

In addition, our partnership agreement contains provisions that restrict the standards to which our general partner and our directors would otherwise be held under Marshall Islands law. For example, our partnership agreement limits the liability and reduces the fiduciary duties of our general partner and our directors to our unitholders. Our partnership agreement also restricts the remedies available to unitholders. By purchasing a common unit, you are treated as having agreed to the modified standard of fiduciary duties and to certain actions that may be taken by our general partner, its affiliates or our directors, all as set forth in the partnership agreement. Please read "Conflicts of Interest and Fiduciary Duties" for a description of the fiduciary duties that would otherwise be imposed on our general partner, its affiliates and our directors under Marshall Islands law, the material modifications of those duties contained in our partnership agreement and certain legal rights and remedies available to our unitholders under Marshall Islands law.

Our emerging growth company status

Our Predecessor had less than $1.0 billion in revenue during its last fiscal year, which means that we qualify as an "emerging growth company" as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As an emerging growth company, we may, for up to five years, take advantage of specified exemptions from reporting and other regulatory requirements that are otherwise applicable generally to public companies. These exemptions include:

- •

- the presentation of only two years of audited financial statements and only two years of related Management's Discussion and Analysis of Financial Condition and Results of Operations;

- •

- exemption from the auditor attestation requirement on the effectiveness of our system of internal control over financial reporting;

- •

- exemption from the adoption of new or revised financial accounting standards until they would apply to private companies; and

- •

- exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board requiring mandatory audit firm rotation or a supplement to the auditor's report in

12

which the auditor would be required to provide additional information about the audit and the financial statements of the issuer.

We may take advantage of these provisions until we are no longer an emerging growth company, which will occur on the earliest of (i) the last day of the fiscal year following the fifth anniversary of this offering, (ii) the last day of the fiscal year in which we have more than $1.0 billion in annual revenue, (iii) the date on which we have more than $700.0 million in market value of our common units held by non-affiliates and (iv) the date on which we issue more than $1.0 billion of non-convertible debt over a three-year period.

We have elected to take advantage of all of the applicable JOBS Act provisions, except that we will elect to opt out of the exemption that allows emerging growth companies to extend the transition period for complying with new or revised financial accounting standards (such election being irrevocable).

13

| Common units offered to the public | common units. | |

common units if the underwriters exercise their option to purchase additional common units in full. | ||

Units outstanding after this offering | common units and subordinated units, representing a % and % limited partner interest in us, respectively. If the underwriters do not exercise their option to purchase additional common units, we will issue common units to EXMAR upon the option's expiration for no additional consideration. Accordingly, the exercise of the underwriters' option will not affect the total number of common units outstanding. Our general partner will own a non-economic general partner interest in us. | |

Use of proceeds | We intend to use the net proceeds from this offering (approximately $ million, after deducting an aggregate of approximately $ million of underwriting discounts and commissions and structuring fees and estimated offering expenses payable by us) to repay approximately $31.9 million of outstanding debt and to pay refinancing fees of approximately $3.3 million. The remainder of the proceeds will be used for general partnership purposes, which may include the funding of any future acquisitions. We do not currently have any commitments to make any future acquisitions following the completion of this offering. | |

We intend to use the net proceeds of any exercise of the underwriters' option to purchase additional common units ($ million, if exercised in full, after deducting an aggregate of approximately $ million of underwriting discounts and commissions) to make a cash distribution to EXMAR. | ||

Cash distributions | We intend to make minimum quarterly distributions of $ per common unit ($ per unit on an annualized basis) to the extent we have sufficient cash from operations after establishment of cash reserves and payment of fees and expenses, including payments to our general partner. In general, we will pay any cash distributions we make each quarter in the following manner: | |

• first, to the holders of common units, until each common unit has received a minimum quarterly distribution of $ plus any arrearages from prior quarters; |

14

• second, to the holders of subordinated units, until each subordinated unit has received a minimum quarterly distribution of $ ; and | ||

• third, to all unitholders, until each unit has received an aggregate distribution of $ . | ||

Within 45 days after the end of each fiscal quarter (beginning with the quarter ending , 2014), we will distribute all of our available cash to unitholders of record on the applicable record date. We will adjust the minimum quarterly distribution for the period from the closing of the offering through , 2014 based on the actual length of the period. Our ability to pay our minimum quarterly distribution is subject to various restrictions and other factors described in more detail under the caption "Our Cash Distribution Policy and Restrictions on Distributions." | ||

If cash distributions to our unitholders exceed $ per unit in a quarter, holders of our incentive distribution rights (initially, our general partner) will receive increasing percentages, up to 50.0%, of the cash we distribute in excess of that amount. We refer to these distributions as "incentive distributions." We must distribute all of our cash on hand at the end of each quarter, less reserves established by our board of directors to provide for the proper conduct of our business, to comply with any applicable debt instruments or to provide funds for future distributions. We refer to this cash as "available cash," and we define its meaning in our partnership agreement attached as Appendix A hereto. The amount of available cash may be greater than or less than the aggregate amount of the minimum quarterly distribution to be distributed on all units. | ||

We believe, based on the estimates contained in and the assumptions listed under "Our Cash Distribution Policy and Restrictions on Distributions—Forecasted Cash Available for Distribution," that we will have sufficient cash available for distribution to enable us to pay the minimum quarterly distribution of $ on all of our common and subordinated units for the twelve months ending June 30, 2015. However, unanticipated events may occur which could adversely affect the actual results we achieve during the forecast period. Consequently, our actual results of operations, cash flows and financial condition during the forecast period may vary from the forecast, and such variations may be material. Prospective investors are cautioned to not place undue reliance on the forecast and should make their own independent assessment of our future results of operations, cash flows and financial condition. |

15

| Please read "Our Cash Distribution Policy and Restrictions on Distributions—Forecasted Cash Available for Distribution." | ||

Subordinated units | EXMAR will initially own all of our subordinated units. The principal difference between our common units and subordinated units is that in any quarter during the subordination period the subordinated units are entitled to receive the minimum quarterly distribution of $ per unit only after the common units have received the minimum quarterly distribution and arrearages in the payment of the minimum quarterly distribution from prior quarters. Subordinated units will not accrue arrearages. The subordination period generally will end if we have earned and paid at least $ on each outstanding common and subordinated unit for any three consecutive four-quarter periods ending on or after , 2017. For purposes of determining whether the subordination period will end, the three consecutive four-quarter periods for which the determination is being made may include one or more quarters with respect to which arrearages in the payment of the minimum quarterly distribution on the common units have accrued, provided that all such arrearages have been repaid prior to the end of each such four-quarter period. | |

The subordination period also will end upon the removal of our general partner other than for cause if no subordinated units or common units held by the holders of subordinated units or their affiliates are voted in favor of that removal. When the subordination period ends, all subordinated units will convert into common units on a one-for-one basis, and the common units will no longer be entitled to arrearages. Please read "How We Make Cash Distributions—Subordination Period." | ||

Issuance of additional units | We can issue an unlimited number of additional units, including units that are senior to the common units in rights of distribution, liquidation and voting, on the terms and conditions determined by our board of directors, without the consent of our unitholders. Please read "Units Eligible for Future Sale" and "The Partnership Agreement—Issuance of Additional Securities." |

16

| Board of directors | Our current board of directors consists of members appointed by our general partner. Prior to our first annual meeting of unitholders in 2015, our general partner expects to appoint additional directors, increasing the size of our board of directors to five. We will hold a meeting of the limited partners every year to elect one or more members of our board of directors and to vote on any other matters that are properly brought before the meeting. Our general partner will have the right to appoint two of the five members of our board of directors who will serve as directors for terms determined by our general partner. At our 2015 annual meeting, the common unitholders will elect three of our directors. The three directors elected by our common unitholders at our 2015 annual meeting will be divided into three classes to be elected by our common unitholders annually on a staggered basis to serve for three-year terms. The majority of our directors will be non-U.S. citizens or residents. | |

Voting rights | Each outstanding common unit is entitled to one vote on matters subject to a vote of common unitholders. However, to preserve our ability to be exempt from U.S. federal income tax under Section 883 of the U.S. Internal Revenue Code of 1986, as amended (the "Code"), if at any time, any person or group owns beneficially more than 4.9% of any class of units then outstanding, any such units owned by that person or group in excess of 4.9% may not be voted on any matter and will not be considered to be outstanding when sending notices of a meeting of unitholders, calculating required votes (except for purposes of nominating a person for election to our board), determining the presence of a quorum or for other similar purposes under our partnership agreement, unless otherwise required by law. The voting rights of any such unitholders in excess of 4.9% will effectively be redistributed pro rata among the other common unitholders holding less than 4.9% of the voting power of all classes of units entitled to vote. Our general partner, its affiliates and persons who acquired common units with the prior approval of our board of directors will not be subject to this 4.9% limitation except with respect to voting their common units in the election of the elected directors. |

17

| You will have no right to elect our general partner on an annual or other continuing basis. Our general partner may not be removed except by a vote of the holders of at least 662/3% of the outstanding common and subordinated units, including any common and subordinated units owned by our general partner and its affiliates, voting together as a single class. Upon consummation of this offering, EXMAR will own % of our outstanding common and subordinated units (or % of our outstanding common and subordinated units if the underwriters' option to purchase additional common units is exercised in full). As a result, you will initially be unable to remove our general partner without its consent because EXMAR will own sufficient units upon completion of this offering to be able to prevent the general partner's removal. Please read "The Partnership Agreement—Voting Rights." | ||

Limited call right | If at any time our general partner and its affiliates own more than 80% of the outstanding common units, our general partner has the right, but not the obligation, to purchase all, but not less than all, of the remaining common units at a price equal to the greater of (x) the average of the daily closing prices of the common units over the 20 trading days preceding the date three days before the notice of exercise of the call right is first mailed and (y) the highest price per-unit paid by our general partner or any of its affiliates for common units during the 90-day period preceding the date such notice is first mailed. | |

U.S. federal income tax considerations | Although we are organized as a partnership, we have elected to be treated as a corporation for U.S. federal income tax purposes. Consequently, all or a portion of the distributions you receive from us will constitute dividends for such purposes. The remaining portion of such distributions will be treated first as a non-taxable return of capital to the extent of your tax basis in your common units and, thereafter, as capital gain. We estimate that if you hold the common units that you purchase in this offering through the period ending December 31, 2016, the distributions you receive, on a cumulative basis, that will constitute dividends for U.S. federal income tax purposes will be approximately % of the total cash distributions received during that period. Please read "Material U.S. Federal Income Tax Considerations—U.S. Federal Income Taxation of U.S. Holders—Ratio of Dividend Income to Distributions" for the basis for this estimate. For a discussion of other material U.S. federal income tax consequences that may be relevant to prospective unitholders who are individual citizens or residents of the United States, please read "Material U.S. Federal Income Tax Considerations." |

18

| Non-U.S. tax considerations | We and our general partner are expected to be centrally managed and controlled in Hong Kong. For a discussion of material Belgium, Marshall Islands and Hong Kong income tax considerations that may be relevant to prospective unitholders, please read "Non-United States Tax Considerations." Please also read "Business—Taxation of the Partnership" and "Risk Factors—Tax Risks." | |

Exchange listing | We intend to apply to list our common units on the New York Stock Exchange (the "NYSE") under the symbol " ". |

19

Summary historical financial and operating data

All of the vessels in our portfolio are owned by our joint ventures, each of which is owned 50% by us. Under applicable accounting rules, we do not consolidate the financial results of our joint ventures into our Predecessor's financial results. Our Predecessor accounts for its equity interest in the joint ventures owning the vessels in our portfolio as equity method investments in its combined financial statements. We derive cash flows from the operations of our joint ventures from several sources. Relative to the Exmar-Teekay joint ventures, our cash flows are generated from dividend payments, which are calculated to pay out all cash flows after debt service obligations. The Exmar-Excelerate joint ventures historically have not paid dividends. Instead, the Exmar-Excelerate joint ventures have been capitalized with shareholder loans in lieu of equity. Substantially all of the operating cash flows of these joint ventures are used to pay interest and principal on these shareholder loans.