Exhibit 99.2

Exhibit 99.2

SALLIE MAE

Investor Presentation

APRIL 2014

Forward-Looking Statements

The following information is current as of April 17, 2014 (unless otherwise noted) and should be read in connection with the Annual Report on Form 10-K for the year ended December 31, 2013 filed by SLM Corporation (“Sallie Mae”) with the SEC on February 19, 2014 (the “2013 Form 10-K”), the Registration Statement on Form 10, as amended (the “Form 10”), filed by Navient Corporation (“Navient”) with the Securities and Exchange Commission (the “SEC”) on April 10, 2014, and subsequent reports filed by Sallie Mae and Navient with the SEC. Definitions for capitalized terms in this presentation not defined herein can be found in the 2013

Form 10-K. This presentation contains forward-looking statements and information based on management’s current expectations as of the date of this presentation. Statements that are not historical facts, including statements about the beliefs and expectations of Sallie Mae and statements that assume or are dependent upon future events, are forward-looking statements. Forward-looking statements are subject to risks, uncertainties, assumptions and other factors that may cause actual results to be materially different from those reflected in such forward-looking statements. These factors include, among others: the risks and uncertainties set forth in Item 1A “Risk Factors” and elsewhere in the 2013 Form 10-K, in Risk Factors in the Form 10, and the subsequent filings of Sallie Mae and Navient with the SEC; increases in financing costs; limits on liquidity; increases in costs associated with compliance with laws and regulations; changes in accounting standards and the impact of related changes in significant accounting estimates; any adverse outcomes in any significant litigation to which Sallie Mae is a party; credit risk associated with exposure to third parties, including counterparties to derivative transactions; and changes in the terms of student loans and the educational credit marketplace (including changes resulting from new laws and the implementation of existing laws). Sallie Mae could also be affected by, among other things: changes in its funding costs and availability; reductions to its credit ratings or the credit ratings of the United States of America; failures of operating systems or infrastructure, including those of third-party vendors; damage to business reputation; failures to successfully implement cost-cutting and adverse effects of such initiatives on business; risks associated with restructuring initiatives, including the separation of Sallie Mae and Navient into two distinct publicly traded companies; changes in the demand for educational financing or in financing preferences of lenders, educational institutions, students and their families; changes in law and regulations with respect to the student lending business and financial institutions generally; increased competition from banks and other consumer lenders; the creditworthiness of customers; changes in the general interest rate environment, including the rate relationships among relevant money-market instruments and those of earning assets vs. funding arrangements; changes in general economic conditions; and changes in the demand for debt management services. The preparation of Sallie Mae’s consolidated financial statements also require management to make certain estimates and assumptions, including estimates and assumptions about future events. These estimates or assumptions may prove to be incorrect. All forward-looking statements contained in this release are qualified by these cautionary statements and are made only as of the date of this release. Sallie Mae does not undertake any obligation to update or revise these forward-looking statements to conform the statement to actual results or changes in expectations.

For additional information on the proposed separation of Sallie Mae and Navient, please see the 2013 Form 10-K and Form 10 of Sallie Mae and Navient, respectively.

2

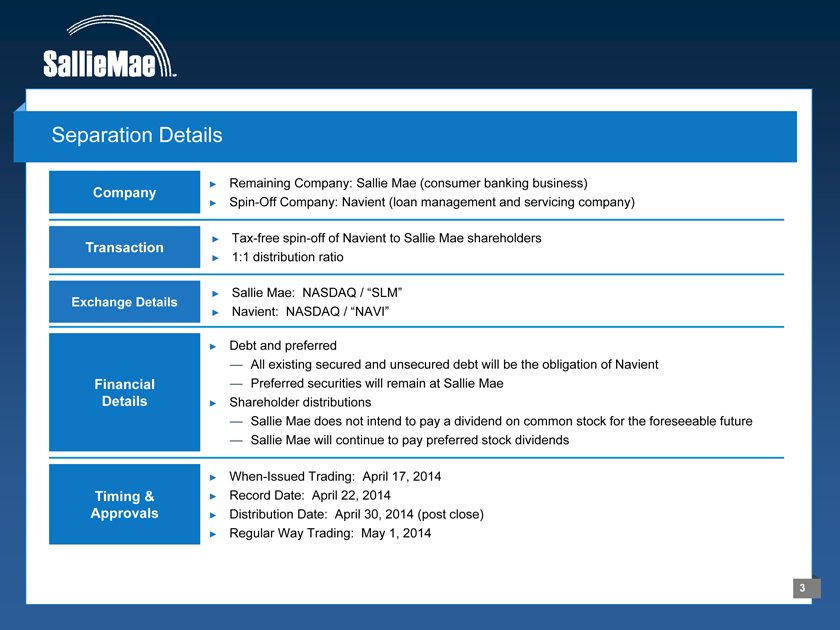

Separation Details

Company

Remaining Company: Sallie Mae (consumer banking business)

Spin-Off Company: Navient (loan management and servicing company)

Transaction

Tax-free spin-off of Navient to Sallie Mae shareholders

1:1 distribution ratio

Exchange Details

Sallie Mae: NASDAQ / “SLM”

Navient: NASDAQ / “NAVI”

Financial Details

Debt and preferred

— All existing secured and unsecured debt will be the obligation of Navient

— Preferred securities will remain at Sallie Mae

Shareholder distributions

— Sallie Mae does not intend to pay a dividend on common stock for the foreseeable future

— Sallie Mae will continue to pay preferred stock dividends

Timing & Approvals

When-Issued Trading: April 17, 2014

Record Date: April 22, 2014

Distribution Date: April 30, 2014 (post close)

Regular Way Trading: May 1, 2014

3

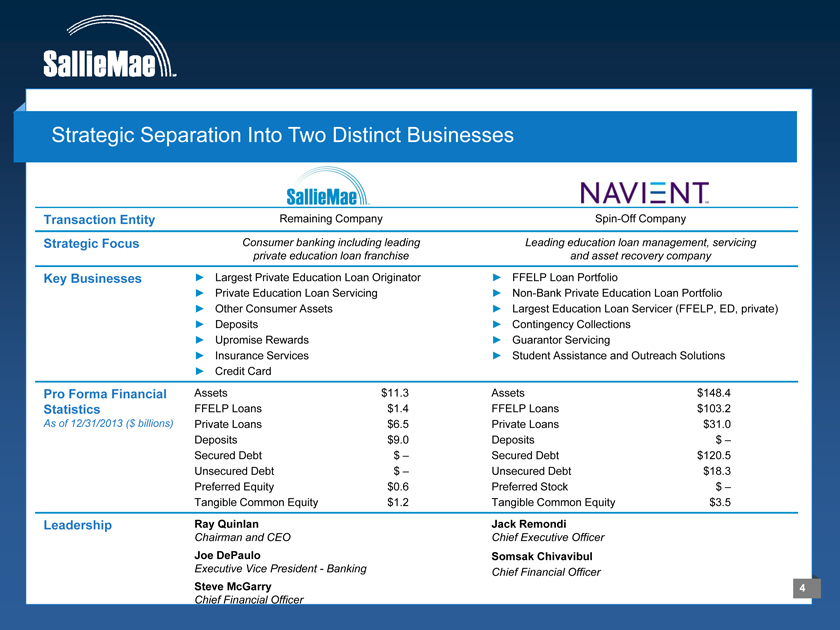

Strategic Separation Into Two Distinct Businesses

Transaction Entity Remaining Company Spin-Off Company

Strategic Focus Consumer banking including leading Leading education loan management, servicing private education loan franchise and asset recovery company

Key Businesses

Largest Private Education Loan Originator

Private Education Loan Servicing

Other Consumer Assets

Deposits

Upromise Rewards

Insurance Services

Credit Card

FFELP Loan Portfolio

Non-Bank Private Education Loan Portfolio

Largest Education Loan Servicer (FFELP, ED, private)

Contingency Collections

Guarantor Servicing

Student Assistance and Outreach Solutions

Pro Forma Financial Statistics

As of 12/31/2013 ($ billions)

Assets $11.3 FFELP Loans $1.4 Private Loans $6.5 Deposits $9.0 Secured Debt $ – Unsecured Debt $ – Preferred Equity $0.6 Tangible Common Equity $1.2

Assets $148.4 FFELP Loans $103.2 Private Loans $31.0 Deposits $ – Secured Debt $120.5 Unsecured Debt $18.3 Preferred Stock $ –Tangible Common Equity $3.5

Leadership

Ray Quinlan

Chairman and CEO

Joe DePaulo

Executive Vice President - Banking

Steve McGarry

Chief Financial Officer

Jack Remondi

Chief Executive Officer

Somsak Chivavibul

Chief Financial Officer

Sallie Mae Investment Highlights

1 Experienced management team with deep industry knowledge

Average of 30+ years of banking and financial services experience

2 Leading brand in the education lending market

40+ years serving the education lending market

50% private education lending market share

3 Simple low cost delivery system

Multi-channel delivery system (on-campus, direct)

40% customer serialization rate and improving

4 Attractive customer base

Higher employment rates for college graduates

90% of portfolio has cosigners; 746 average FICO

Disciplined approach to credit

Robust proprietary scorecard

Strong SmartOption performance; 0.6% ‘13 charge-offs

Strong capital position and 6 funding capabilities

14%+ Total Capital Ratio; all capital ratios significantly in excess of well capitalized

Retail direct deposits; future securitizations

7 Targeting high growth and high return business

Long-term earnings growth target of 20%+

Long-term ROE target of 15%+

Management Presenters

Experienced management team with extensive asset knowledge and industry expertise

Raymond Quinlan

Chairman &

Chief Executive Officer

30+ years of banking and financial services experience

Joined Sallie Mae in 2014

Previously Executive Vice President of Banking at CIT

Previously Chairman & CEO of Citigroup Retail Financial Services

Joseph DePaulo

Executive Vice President—Banking

30+ years of banking and financial services experience

Joined Sallie Mae in 2009 as Executive Vice President & Chief Marketing Officer

Previously Co-Founder & CEO of Credit One Financial Services

Previously U.S. Card group executive at MBNA

Steven McGarry

Chief Financial Officer

30+ years of banking and financial services experience

Joined Sallie Mae in 1997 as a member of the corporate finance team and later took leadership of equity and fixed income investor relations

Previously held various positions in Toronto Dominion’s treasury department

6

Favorable Student Loan Market Trends

Enrollment at Four-Year Degree Granting Institutions

(millions) 15.3

14.4

13.5 13.5 13.7

12.9 13.3

12.1

2008 2009 2010 2011 2012 2013 2017 2022

Source: U.S. Department of Education, National Center for Education Statistics, Projections of Education Statistics to 2022 (NCES 2014-051, February 2014), tables 23 and 25; 2012 actual data from Enrollment in Postsecondary Institutions, Fall 2012; Financial Statistics, Fiscal Year 2012; Graduation Rates, Selected Cohorts, 2004-09; and Employees in Postsecondary Institutions, Fall 2012.

Annual Cost of Education

Public Private

($ thousands)

$39 $41

$36 $38

$34 $35

$30 $32 $29

$16 $17 $18 $18

$14 $14 $15

$12 $13

2005 2006 2007 2008 2009 2010 2011 2012 2013

Source: Trends in College Pricing.© 2013 The College Board,. www.collegeboard.org,

Note: Academic years, average published tuition, fees, room and board charges at four-year institutions; enrollment-weighted

Estimated Total Cost of Education – 2012 / 2013 AY

($ billions)

Ed. Tax Federal Benefit / Loans Work Study $103 Grants $21 $116 Private Family Education Contributions Loans $191 $7 Total Estimated Cost: $438bn

Sources derived from: Department of Education, College Board, McKinsey & Company, MeasureOne, National Student Clearinghouse, Company Analysis

Cost of College (Based on a Four-Year Term)

($ thousands) AY 2012—2013 AY 2002—2003 $ 157.8

$ 99.5 $ 130.8 $ 71.3

$ 82.3 $ 38.7

$ 44.3

$ 21.6 $ 27.0 $ 27.0

$ 17.1 $ 17.1

Full-Time Full-Time Public Full-Time Full-Time Public Private School School Private School School ED Lending Limit Cost of Attendance Gap

Source: Trends in College Pricing.© 2013 The College Board,. www.collegeboard.org, U.S. Department of Education 2013

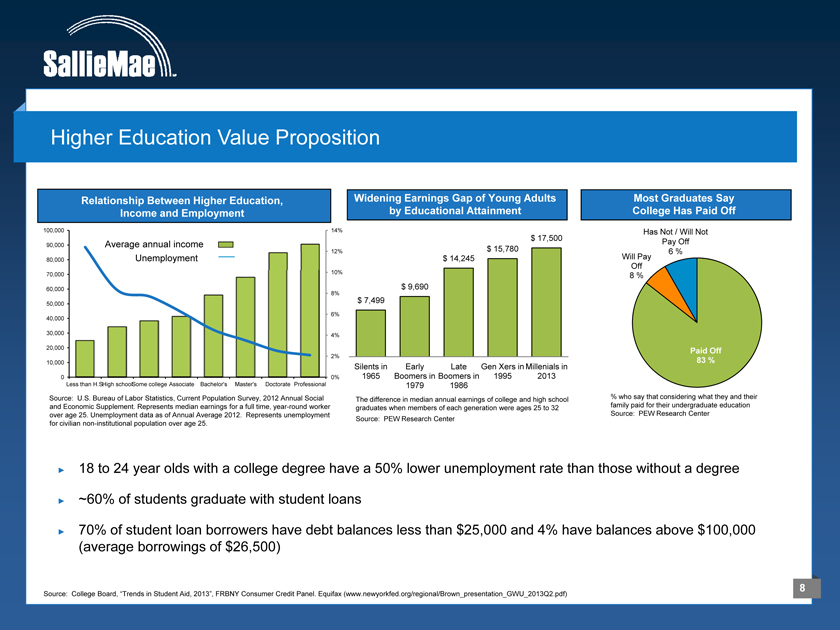

Higher Education Value Proposition

Relationship Between Higher Education, Income and Employment

100,000 14%

90,000 Average annual income

Unemployment 12%

80,000

70,000 10%

60,000

8% 50,000 6% 40,000

30,000 4% 20,000 2% 10,000

0 0% Less than H.SHigh . schoolSome college Associate Bachelor’s Master’s Doctorate Professional

Source: U.S. Bureau of Labor Statistics, Current Population Survey, 2012 Annual Social and Economic Supplement. Represents median earnings for a full time, year-round worker over age 25. Unemployment data as of Annual Average 2012. Represents unemployment for civilian non-institutional population over age 25.

Widening Earnings Gap of Young Adults by Educational Attainment

$ 17,500 $ 15,780 $ 14,245

$ 9,690 $ 7,499

Silents in Early Late Gen Xers in Millenials in 1965 Boomers in Boomers in 1995 2013 1979 1986

The difference in median annual earnings of college and high school graduates when members of each generation were ages 25 to 32 Source: PEW Research Center

Most Graduates Say College Has Paid Off

Has Not / Will Not Pay Off

6 % Will Pay Off

8 %

Paid Off

83 %

% who say that considering what they and their family paid for their undergraduate education Source: PEW Research Center

18 to 24 year olds with a college degree have a 50% lower unemployment rate than those without a degree

~60% of students graduate with student loans

70% of student loan borrowers have debt balances less than $25,000 and 4% have balances above $100,000 (average borrowings of $26,500)

Source: College Board, “Trends in Student Aid, 2013”, FRBNY Consumer Credit Panel. Equifax (www.newyorkfed.org/regional/Brown_presentation_GWU_2013Q2.pdf)

The Sallie Mae Brand

#1 saving, planning and paying for education company with 40-years of leadership in the education lending market

Top ranked brand: 6 out of 10 consumers of education finance recognize the Sallie Mae brand

Industry leading market share in private education lending; 50% market share for 2012 / 2013 AY

Over 2,400 actively managed university relationships across the U.S.

Complementary consumer product offerings

Over one million long-term engaged customers across the Sallie Mae brands

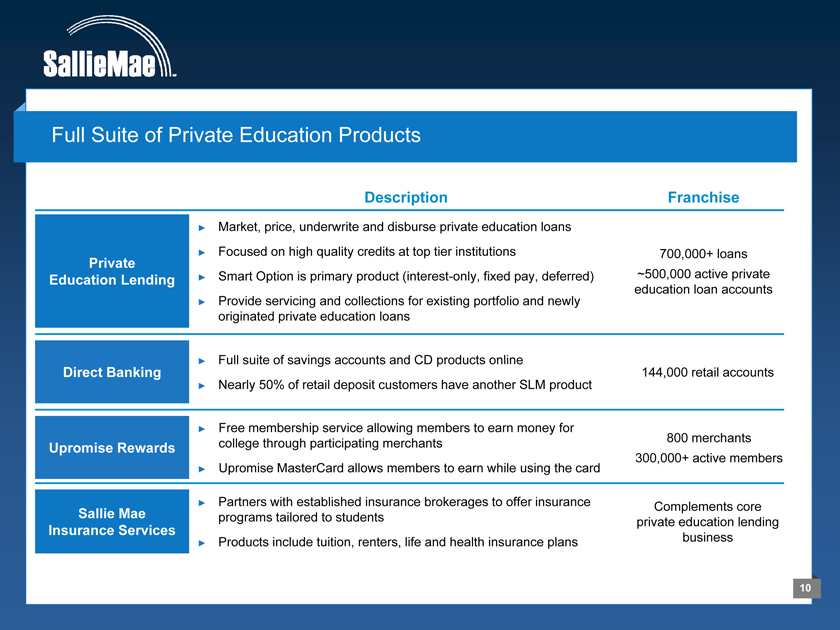

Full Suite of Private Education Products

Description Franchise

Private Education Lending

Market, price, underwrite and disburse private education loans

Focused on high quality credits at top tier institutions

Smart Option is primary product (interest-only, fixed pay, deferred)

Provide servicing and collections for existing portfolio and newly originated private education loans

700,000+ loans

~500,000 active private education loan accounts

Direct Banking

Full suite of savings accounts and CD products online

Nearly 50% of retail deposit customers have another SLM product

144,000 retail accounts

Upromise Rewards

Free membership service allowing members to earn money for college through participating merchants

Upromise MasterCard allows members to earn while using the card

800 merchants 300,000+ active members

Sallie Mae Insurance Services

Partners with established insurance brokerages to offer insurance programs tailored to students

Products include tuition, renters, life and health insurance plans

Complements core private education lending business

10

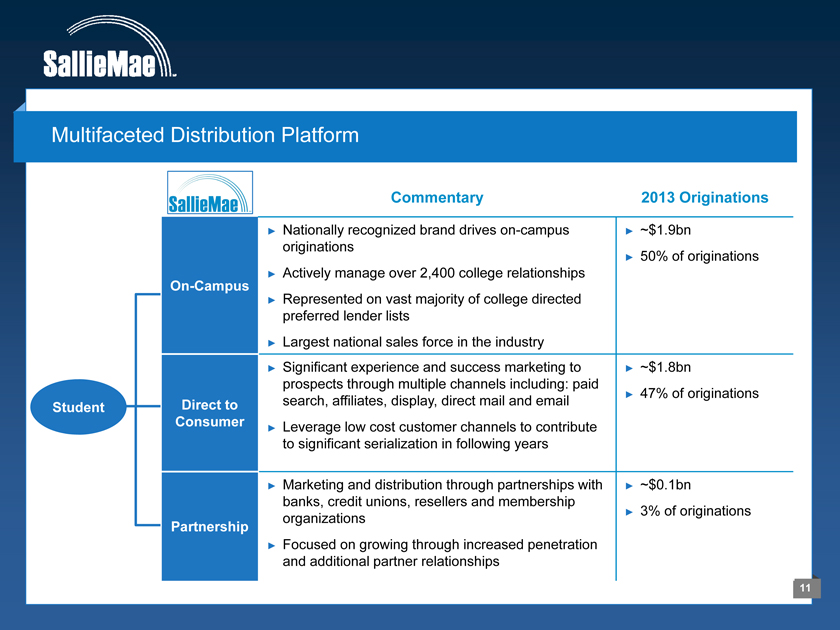

Multifaceted Distribution Platform

Commentary

2013 Originations

Student

On-Campus

Nationally recognized brand drives on-campus originations

Actively manage over 2,400 college relationships

Represented on vast majority of college directed preferred lender lists

Largest national sales force in the industry

~$1.9bn

50% of originations

Direct to Consumer

Significant experience and success marketing to prospects through multiple channels including: paid search, affiliates, display, direct mail and email

Leverage low cost customer channels to contribute to significant serialization in following years

~$1.8bn

47% of originations

Partnership

Marketing and distribution through partnerships with banks, credit unions, resellers and membership organizations

Focused on growing through increased penetration and additional partner relationships

~$0.1bn

3% of originations

11

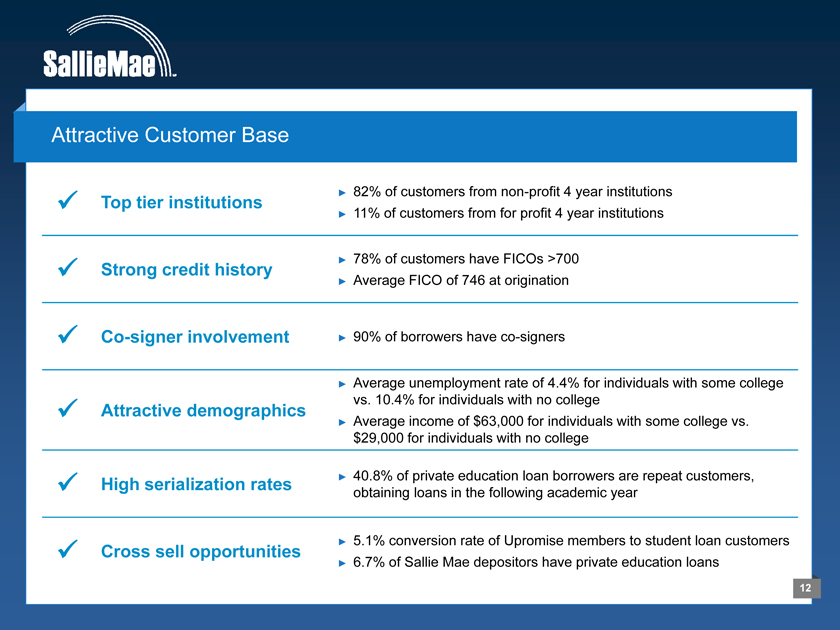

Attractive Customer Base

Top tier institutions

82% of customers from non-profit 4 year institutions

11% of customers from for profit 4 year institutions

Strong credit history

78% of customers have FICOs >700

Average FICO of 746 at origination

Co-signer involvement

90% of borrowers have co-signers

Attractive demographics

Average unemployment rate of 4.4% for individuals with some college vs. 10.4% for individuals with no college

Average income of $63,000 for individuals with some college vs. $29,000 for individuals with no college

High serialization rates

40.8% of private education loan borrowers are repeat customers, obtaining loans in the following academic year

Cross sell opportunities

5.1% conversion rate of Upromise members to student loan customers

6.7% of Sallie Mae depositors have private education loans

12

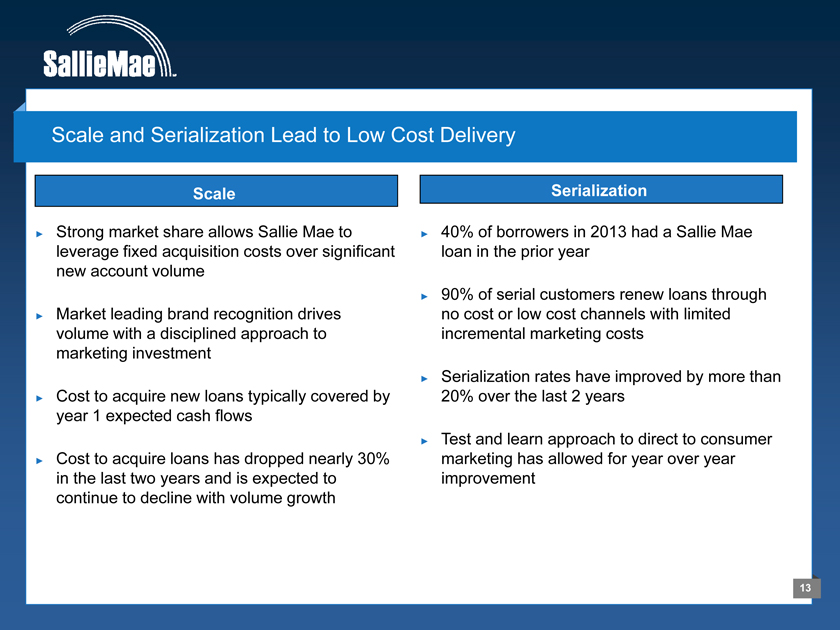

Scale and Serialization Lead to Low Cost Delivery

Scale

Strong market share allows Sallie Mae to leverage fixed acquisition costs over significant new account volume

Market leading brand recognition drives volume with a disciplined approach to marketing investment

Cost to acquire new loans typically covered by year 1 expected cash flows

Cost to acquire loans has dropped nearly 30% in the last two years and is expected to continue to decline with volume growth

Serialization

40% of borrowers in 2013 had a Sallie Mae loan in the prior year

90% of serial customers renew loans through no cost or low cost channels with limited incremental marketing costs

Serialization rates have improved by more than 20% over the last 2 years

Test and learn approach to direct to consumer marketing has allowed for year over year improvement

13

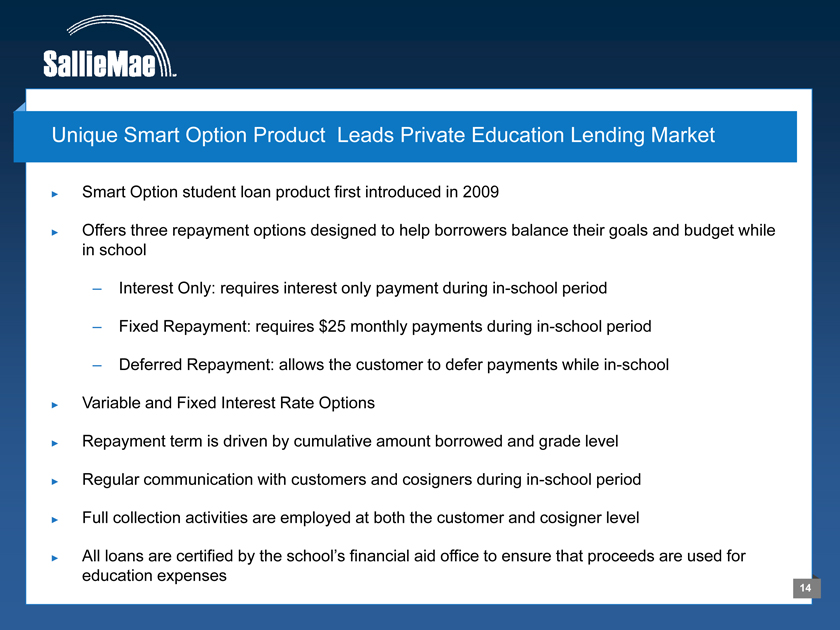

Unique Smart Option Product Leads Private Education Lending Market

Smart Option student loan product first introduced in 2009

Offers three repayment options designed to help borrowers balance their goals and budget while in school

– Interest Only: requires interest only payment during in-school period

– Fixed Repayment: requires $25 monthly payments during in-school period

– Deferred Repayment: allows the customer to defer payments while in-school

Variable and Fixed Interest Rate Options

Repayment term is driven by cumulative amount borrowed and grade level

Regular communication with customers and cosigners during in-school period

Full collection activities are employed at both the customer and cosigner level

All loans are certified by the school’s financial aid office to ensure that proceeds are used for education expenses

14

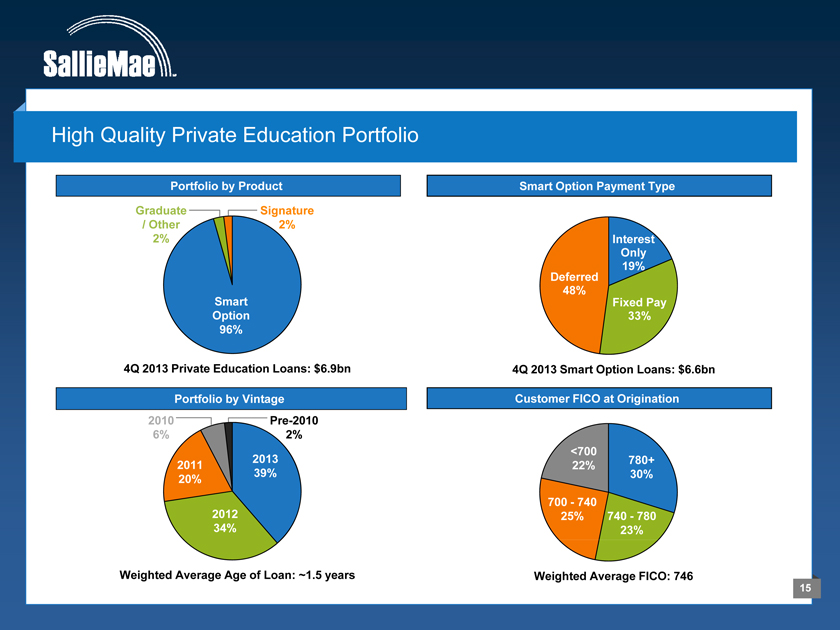

High Quality Private Education Portfolio

Portfolio by Product

Graduate Signature / Other 2% 2%

Smart Option 96%

4Q 2013 Private Education Loans: $6.9bn

Smart Option Payment Type

Interest Only Deferred 19% 48% Fixed Pay 33%

4Q 2013 Smart Option Loans: $6.6bn

Portfolio by Vintage

2010 Pre-2010

6% 2%

2013 2011 39% 20%

2012 34%

Weighted Average Age of Loan: ~1.5 years

Customer FICO at Origination

<700

22% 780+ 30%

700—740

25% 740—780 23%

Weighted Average FICO: 746

15

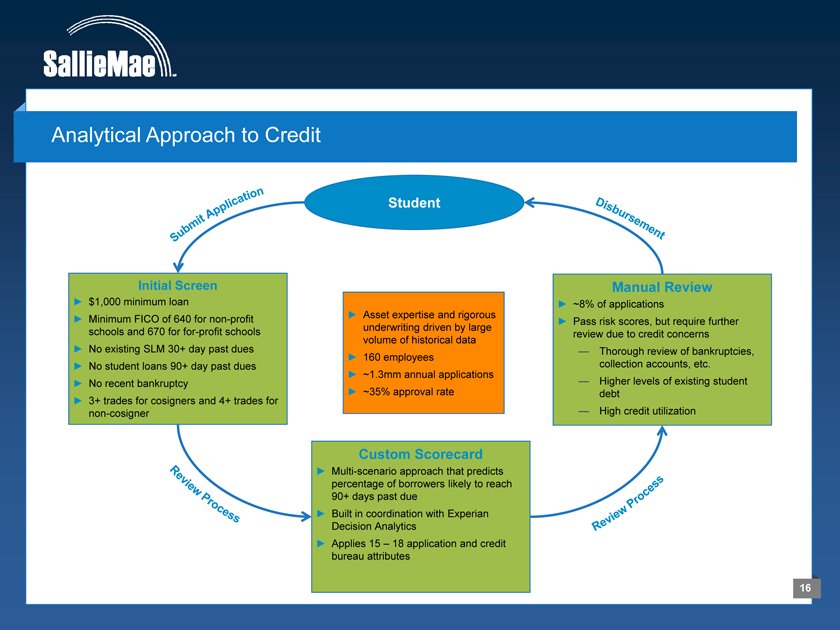

Analytical Approach to Credit

Student

Initial Screen

$1,000 minimum loan

Minimum FICO of 640 for non-profit schools and 670 for for-profit schools

No existing SLM 30+ day past dues

No student loans 90+ day past dues

No recent bankruptcy

3+ trades for cosigners and 4+ trades for non-cosigner

Custom Scorecard

Multi-scenario approach that predicts percentage of borrowers likely to reach 90+ days past due

Built in coordination with Experian Decision Analytics

Applies 15 – 18 application and credit bureau attributes

Asset expertise and rigorous underwriting driven by large volume of historical data

160 employees

~1.3mm annual applications

~35% approval rate

Manual Review

~8% of applications

Pass risk scores, but require further review due to credit concerns

— Thorough review of bankruptcies, collection accounts, etc.

— Higher levels of existing student debt

— High credit utilization

16

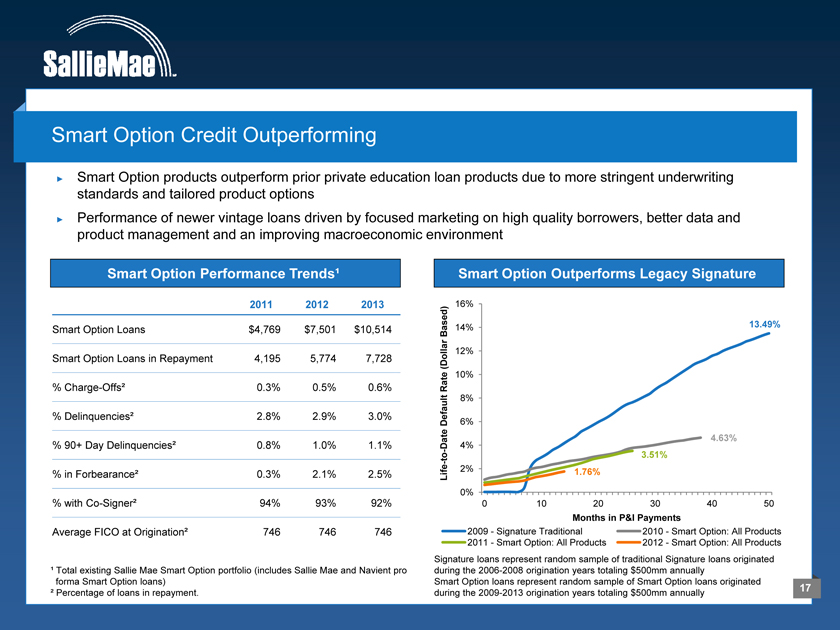

Smart Option Credit Outperforming

Smart Option products outperform prior private education loan products due to more stringent underwriting standards and tailored product options

Performance of newer vintage loans driven by focused marketing on high quality borrowers, better data and product management and an improving macroeconomic environment

Smart Option Performance Trends¹

2011 2012 2013

Smart Option Loans $4,769 $7,501 $10,514

Smart Option Loans in Repayment 4,195 5,774 7,728

% Charge-Offs² 0.3% 0.5% 0.6%

% Delinquencies² 2.8% 2.9% 3.0%

% 90+ Day Delinquencies² 0.8% 1.0% 1.1% % in Forbearance² 0.3% 2.1% 2.5% % with Co-Signer² 94% 93% 92% Average FICO at Origination² 746 746 746

¹ Total existing Sallie Mae Smart Option portfolio (includes Sallie Mae and Navient pro forma Smart Option loans)

² Percentage of loans in repayment.

Smart Option Outperforms Legacy Signature

16%

Based) 14% 13.49% Dollar 12%

( 10% Rate

8%

Default 6%

4.63% Date 4% to - 3.51% -Life 2% 1.76%

0%

0 1020 3040 50

Months in P&I Payments

2009—Signature Traditional 2010—Smart Option: All Products 2011—Smart Option: All Products 2012—Smart Option: All Products

Signature loans represent random sample of traditional Signature loans originated during the 2006-2008 origination years totaling $500mm annually Smart Option loans represent random sample of Smart Option loans originated during the 2009-2013 origination years totaling $500mm annually

17

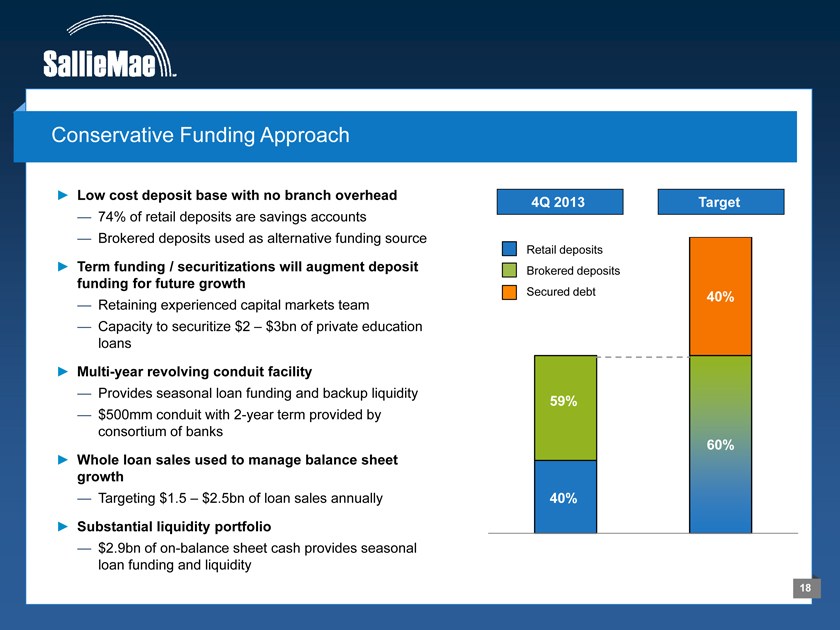

Conservative Funding Approach

Low cost deposit base with no branch overhead

— 74% of retail deposits are savings accounts

— Brokered deposits used as alternative funding source

Term funding / securitizations will augment deposit funding for future growth

— Retaining experienced capital markets team

— Capacity to securitize $2 – $3bn of private education loans

Multi-year revolving conduit facility

— Provides seasonal loan funding and backup liquidity

— $500mm conduit with 2-year term provided by consortium of banks

Whole loan sales used to manage balance sheet growth

— Targeting $1.5 – $2.5bn of loan sales annually

Substantial liquidity portfolio

— $2.9bn of on-balance sheet cash provides seasonal loan funding and liquidity

4Q 2013

Target

Retail deposits Brokered deposits Secured debt

59%

40%

40%

60%

18

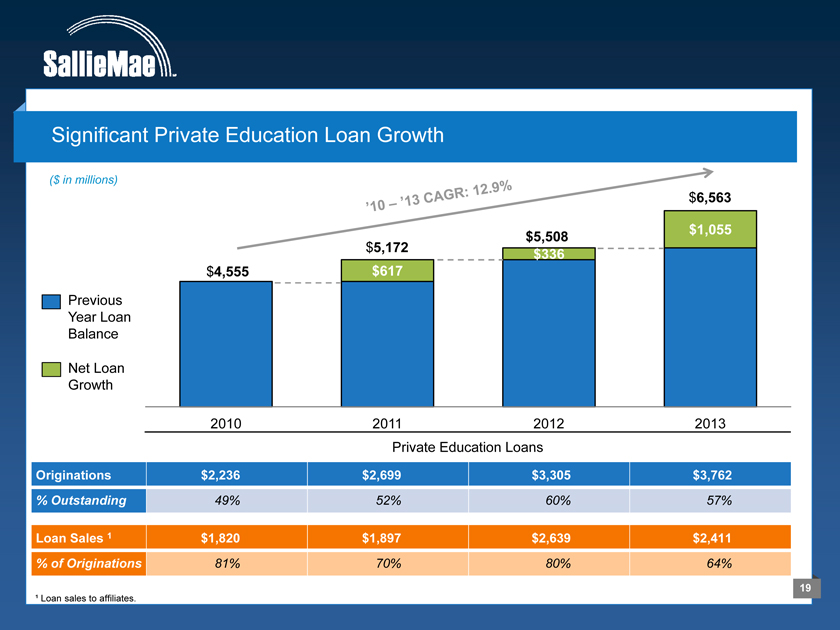

Significant Private Education Loan Growth

($ in millions)

Previous Year Loan Balance

Net Loan Growth

$4,555

2010

$5,172 $617

2011

$5,508 $336

2012

$6,563

$1,055

2013

Private Education Loans

Originations $2,236 $2,699 $3,305 $3,762

% Outstanding 49% 52% 60% 57%

Loan Sales 1 $1,820 $1,897 $2,639 $2,411

% of Originations 81% 70% 80% 64%

19

¹ Loan sales to affiliates.

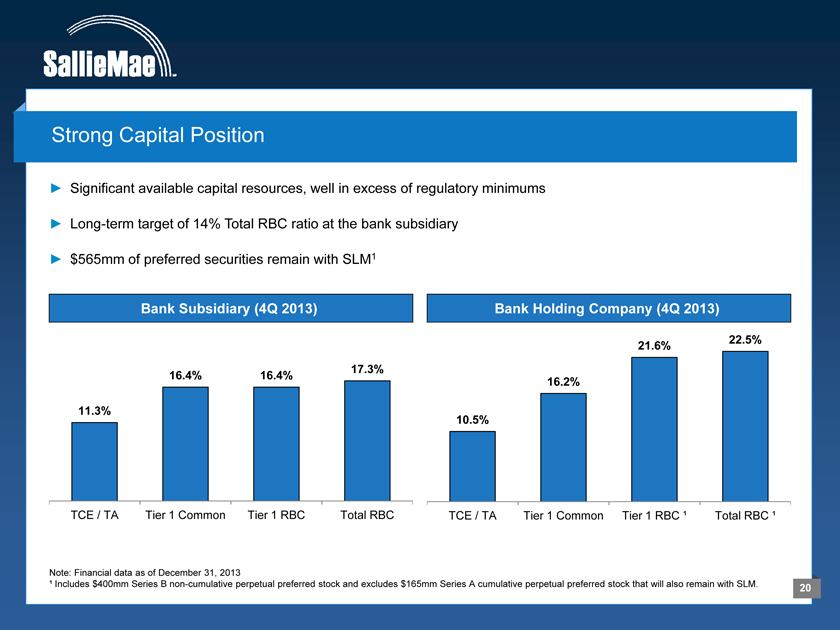

Strong Capital Position

Significant available capital resources, well in excess of regulatory minimums

Long-term target of 14% Total RBC ratio at the bank subsidiary

$565mm of preferred securities remain with SLM1

Bank Subsidiary (4Q 2013)

Bank Holding Company (4Q 2013)

22.5%

21.6%

17.3%

16.4% 16.4%

16.2%

11.3%

10.5%

TCE / TA Tier 1 Common Tier 1 RBC Total RBC TCE / TA Tier 1 Common Tier 1 RBC ¹ Total RBC ¹

Note: Financial data as of December 31, 2013

1 Includes $400mm Series B non-cumulative perpetual preferred stock and excludes $165mm Series A cumulative perpetual preferred stock that will also remain with SLM.

20

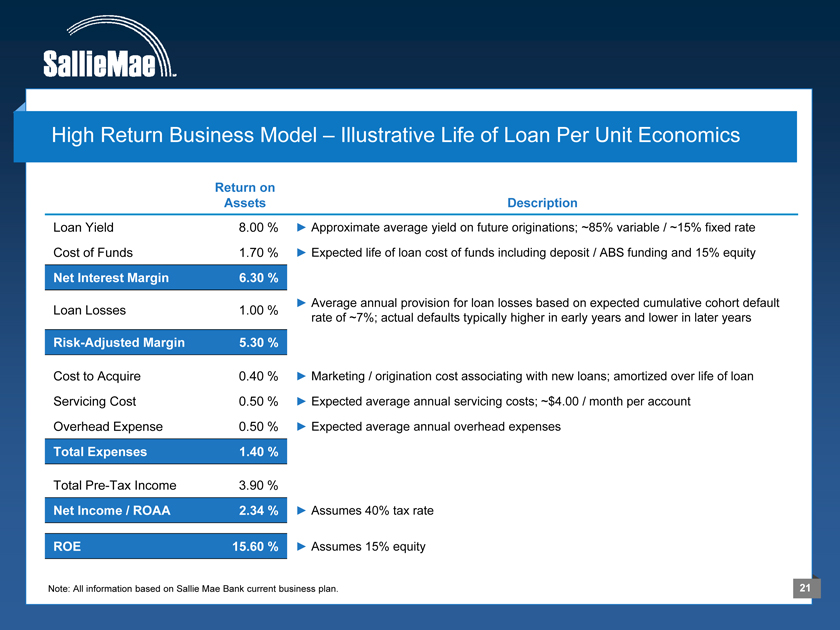

High Return Business Model – Illustrative Life of Loan Per Unit Economics

Return on Assets

Loan Yield 8.00 % Cost of Funds 1.70 %

Net Interest Margin 6.30 %

Loan Losses 1.00 %

Risk-Adjusted Margin 5.30 %

Cost to Acquire 0.40 % Servicing Cost 0.50 % Overhead Expense 0.50 %

Total Expenses 1.40 %

Total Pre-Tax Income 3.90 %

Net Income / ROAA 2.34 %

ROE 15.60 %

Description

Approximate average yield on future originations; ~85% variable / ~15% fixed rate

Expected life of loan cost of funds including deposit / ABS funding and 15% equity

Average annual provision for loan losses based on expected cumulative cohort default rate of ~7%; actual defaults typically higher in early years and lower in later years

Marketing / origination cost associating with new loans; amortized over life of loan

Expected average annual servicing costs; ~$4.00 / month per account

Expected average annual overhead expenses

Assumes 40% tax rate

Assumes 15% equity

21

Note: All information based on Sallie Mae Bank current business plan.

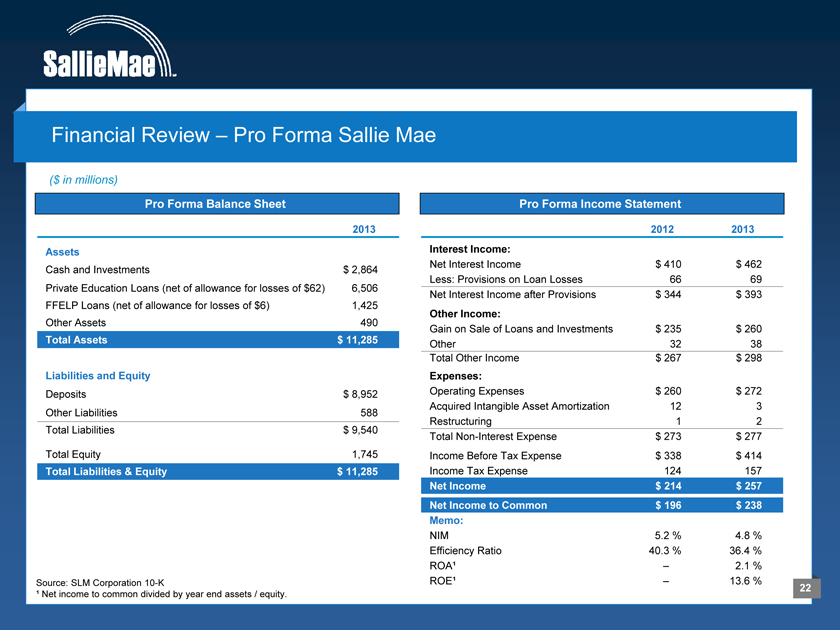

Financial Review – Pro Forma Sallie Mae

($ in millions)

Pro Forma Balance Sheet

2013

Assets

Cash and Investments $ 2,864 Private Education Loans (net of allowance for losses of $62) 6,506 FFELP Loans (net of allowance for losses of $6) 1,425 Other Assets 490

Total Assets $ 11,285

Liabilities and Equity

Deposits $ 8,952 Other Liabilities 588 Total Liabilities $ 9,540

Total Equity 1,745

Total Liabilities & Equity $ 11,285

Source: SLM Corporation 10-K

¹ Net income to common divided by year end assets / equity.

Pro Forma Income Statement

2012 2013 Interest Income:

Net Interest Income $ 410 $ 462 Less: Provisions on Loan Losses 66 69 Net Interest Income after Provisions $ 344 $ 393

Other Income:

Gain on Sale of Loans and Investments $ 235 $ 260 Other 32 38 Total Other Income $ 267 $ 298

Expenses:

Operating Expenses $ 260 $ 272 Acquired Intangible Asset Amortization 12 3 Restructuring 1 2 Total Non-Interest Expense $ 273 $ 277 Income Before Tax Expense $ 338 $ 414 Income Tax Expense 124 157

Net Income $ 214 $ 257 Net Income to Common $ 196 $ 238 Memo:

NIM 5.2 % 4.8 % Efficiency Ratio 40.3 % 36.4 % ROA1 – 2.1 % ROE1 – 13.6 %

22

Key Financial Targets

Target

Annual Originations $4 bn +

Asset Growth 15.0% – 17.5%

Earnings Growth 20% + Annual Loan Sales $1.5 – $2.5 bn ROA 2.0% + ROE 15% + Total RBC 14%

23

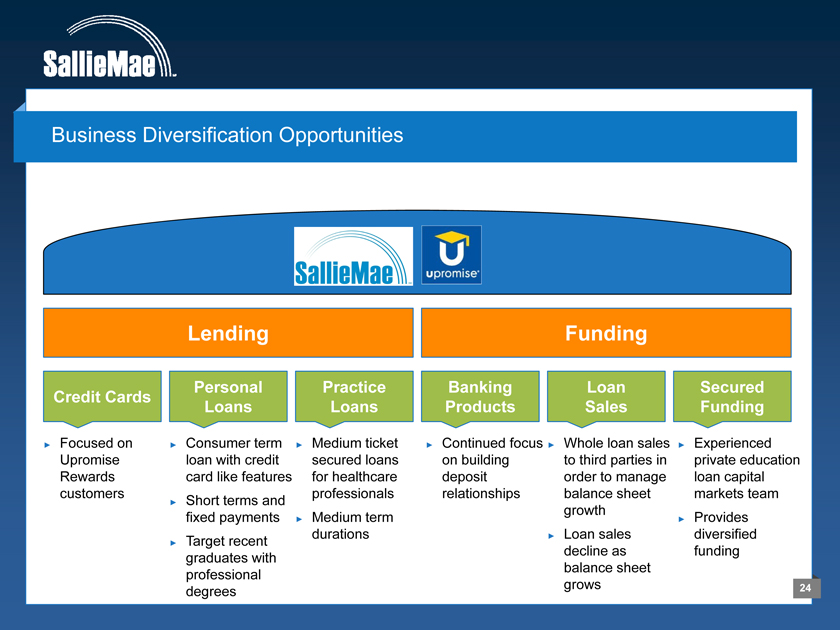

Business Diversification Opportunities

Lending

Funding

Credit Cards

Focused on Upromise Rewards customers

Personal Loans

Consumer term loan with credit card like features

Short terms and fixed payments

graduates with professional degrees

Practice Loans

Medium ticket secured loans for healthcare professionals Medium term durations

Banking Products

Continued focus on building deposit relationships

Loan Sales

Whole loan sales to third parties in order to manage balance sheet growth Loan sales decline as balance sheet grows

Secured Funding

Experienced private education loan capital markets team

Provides diversified funding

24

Sallie Mae Investment Highlights

1 Experienced management team with deep industry knowledge

Leading brand in the education lending market

3 Simple low cost delivery system

4 Attractive customer base

5 Disciplined approach to credit

6 Strong capital position and funding capabilities

7 Targeting high growth and high return business

25