Table of Contents

As filed with the U.S. Securities and Exchange Commission on April 4, 2014

Registration No. 333-193438

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 6

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

SABRE CORPORATION

(Exact name of Registrant as specified in its charter)

| Delaware | 7370 | 20-8647322 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

3150 Sabre Drive

Southlake, TX 76092

Telephone: (682) 605-1000

(Address including zip code, telephone number, including area code, of Registrant’s Principal Executive Offices)

Sterling L. Miller, Esq.

General Counsel & Corporate Secretary

Sabre Corporation

3150 Sabre Drive

Southlake, TX 76092

Telephone: (682) 605-1000

Telecopy: (682) 605-7523

(Name, address including zip code, telephone number, including area code, of agent for service)

Copies To:

David Lopez, Esq. Pamela L. Marcogliese, Esq. Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, NY 10006 (212) 225-2000 | Julie H. Jones, Esq. Craig E. Marcus, Esq. Ropes & Gray LLP Prudential Tower, 800 Boylston Street Boston, MA 02199 (617) 951-7000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date hereof.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

CALCULATION OF REGISTRATION FEE

| ||||||||

Title of Each Class of Securities to be Registered | Amount to be | Proposed Maximum Offering Price Per Share | Proposed Offering Price | Amount of Registration Fee(3) | ||||

Common Stock, $0.01 par value per share | 51,447,368 | $20.00 | $1,028,947,360 | $132,529 | ||||

| ||||||||

| ||||||||

| (1) | Includes 6,710,526 shares that the underwriters have an option to purchase from the Registrant. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended (the “Securities Act”). |

| (3) | Includes $12,880 the Registrant previously paid in connection with the initial filing of this Registration Statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Prospectus (Subject to Completion)

Dated April 4, 2014

44,736,842 Shares

Sabre Corporation

Common Stock

This is our initial public offering, and no public market currently exists for our common stock. Sabre Corporation is offering 44,736,842 shares of common stock. After this offering, we will be a “controlled company” within the meaning of the NASDAQ rules.

Prior to this offering, there has been no public market for our common stock. The initial public offering price of the common stock is expected to be between $18.00 and $20.00 per share. We have applied to list our common stock on the NASDAQ Stock Market under the symbol “SABR.”

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 22.

Price $ A Share

Per Share | Total | |||||||

Initial public offering price | $ | $ | ||||||

Underwriting discounts(1) | $ | $ | ||||||

Proceeds to us (before expenses) | $ | $ | ||||||

| (1) | See “Underwriting (Conflicts of Interest)” on page 267 for additional information regarding underwriter compensation. |

We have granted the underwriters an option to purchase up to an additional 6,710,526 shares of common stock at the offering price less the underwriting discount. The underwriters can exercise this right at any time and from time to time, in whole or in part, within 30 days after the offering.

Delivery of the shares of common stock will be made on or about , 2014.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| MORGAN STANLEY | GOLDMAN, SACHS & CO. | BofA MERRILL LYNCH | DEUTSCHE BANK SECURITIES |

| Evercore | Jefferies | TPG Capital BD, LLC | ||

| Cowen and Company | Sanford C. Bernstein | William Blair | ||

| Mizuho Securities | Natixis | The Williams Capital Group, L.P. | ||

The date of this prospectus is , 2014.

Table of Contents

Table of Contents

Prospectus | Page | |||

| 1 | ||||

| 22 | ||||

| 56 | ||||

| 59 | ||||

| 60 | ||||

| 61 | ||||

| 62 | ||||

| 63 | ||||

| 65 | ||||

| 66 | ||||

| 69 | ||||

| 72 | ||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 78 | |||

Prospectus | Page | |||

| 129 | ||||

| 138 | ||||

| 184 | ||||

| 192 | ||||

| 239 | ||||

| 242 | ||||

| 248 | ||||

| 254 | ||||

| 260 | ||||

Material U.S. Federal Income and Estate Tax Considerations to Non-U.S. Holders | 264 | |||

| 267 | ||||

| 276 | ||||

| 277 | ||||

| 278 | ||||

| F-1 | ||||

We are responsible for the information contained in this prospectus and in any related free-writing prospectus we may prepare or authorize to be delivered to you. We have not authorized anyone to give you any other information, and we take no responsibility for any other information that others may give you. We are not, and the underwriters are not, making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus, regardless of the time of delivery of this prospectus or any sale of our common stock.

The information contained on our website or that can be accessed through our website will not be deemed to be incorporated into this prospectus or the registration statement of which this prospectus forms a part, and investors should not rely on any such information in deciding whether to purchase our common stock.

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus. It may not contain all the information that may be important to you. You should read the entire prospectus carefully, including the section entitled “Risk Factors” and our financial statements and the related notes included elsewhere in this prospectus before making an investment decision to purchase shares of our common stock.

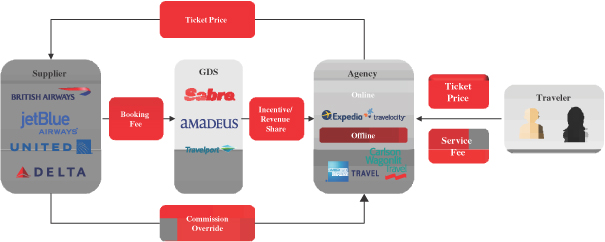

In this prospectus, unless we indicate otherwise or the context requires, references to the “company,” “Sabre,” “we,” “our,” “ours” and “us” refer to Sabre Corporation and its consolidated subsidiaries, references to “Sabre GLBL” refer to Sabre GLBL Inc., formerly known as Sabre Inc., references to “TPG” refer to TPG Global, LLC and its affiliates, references to the “TPG Funds” refer to one or more of TPG Partners IV, L.P. (“TPG Partners IV”), TPG Partners V, L.P. (“TPG Partners V”), TPG FOF V-A, L.P. (“TPG FOF V-A”) and TPG FOF V-B, L.P. (“TPG FOF V-B”), references to “Silver Lake” refer to Silver Lake Management Company, L.L.C. and its affiliates and references to “Silver Lake Funds” refer to either or both of Silver Lake Partners II, L.P. and Silver Lake Technology Investors II, L.P. In the context of our Travel Network business, references to “travel buyers” refer to buyers of travel, such as online and offline travel agencies, travel management companies (“TMCs”) and corporate travel departments, and references to “travel suppliers” refer to suppliers of travel services such as airlines, hotels, car rental brands, rail carriers, cruise lines and tour operators. The following summary is qualified in its entirety by the more detailed information and consolidated financial statements and notes thereto included elsewhere in this prospectus.

Our Company

We are a leading technology solutions provider to the global travel and tourism industry. We span the breadth of a highly complex $6.6 trillion global travel ecosystem, providing key software and services to a broad range of travel suppliers and travel buyers. Through our Travel Network business, we process hundreds of millions of transactions annually, connecting the world’s leading travel suppliers, including airlines, hotels, car rental brands, rail carriers, cruise lines and tour operators, with travel buyers in a comprehensive travel marketplace. We offer efficient, global distribution of travel content from approximately 125,000 travel suppliers to approximately 400,000 online and offline travel agents. To those agents, we offer a platform to shop, price, book and ticket comprehensive travel content in a transparent and efficient workflow. We also offer value-added solutions that enable our customers to better manage and analyze their businesses. Through our airline solutions business (“Airline Solutions”) and hospitality solutions business (“Hospitality Solutions” and, together with Airline Solutions, “Airline and Hospitality Solutions”), we offer travel suppliers an extensive suite of leading software solutions, ranging from airline and hotel reservations systems to high-value marketing and operations solutions, such as planning airline crew schedules, re-accommodating passengers during irregular flight operations and managing day-to-day hotel operations. These solutions allow our customers to market, distribute and sell their products more efficiently, manage their core operations, and deliver an enhanced travel experience. Through our complementary Travel Network and Airline and Hospitality Solutions businesses, we believe we offer the broadest, end-to-end portfolio of technology solutions to the travel industry.

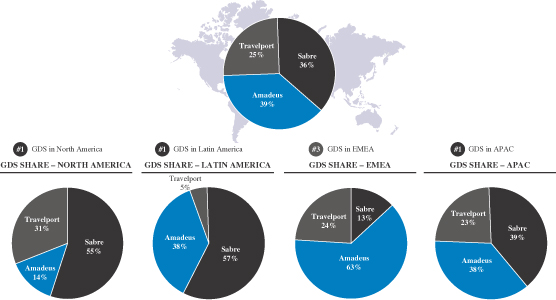

Our portfolio of technology solutions has enabled us to become the leading end-to-end technology provider in the travel industry. For example, we are one of the largest global distribution systems (“GDSs”) providers in the world, with a 36% share of GDS-processed air bookings in 2013. More specifically, we are the #1 GDS provider in North America and also in higher growth markets such as Latin America and Asia Pacific (“APAC”), in each case based on GDS-processed air bookings in 2013. In those three markets, our GDS-processed air bookings share was approximately 50% on a combined basis in 2013. In our Airline and Hospitality Solutions business, we believe we have the most comprehensive portfolio of solutions. In 2013, we had the largest third-party hospitality Central Reservation System (“CRS”) room share based on our approximately 27% share of third-party hospitality CRS hotel rooms distributed through our GDS, and, according to T2RL’s Market for Airline Passenger Services Systems-2013 (“T2RL PSS”) data for 2012, we had the second largest airline reservations system globally. We also believe that we have the leading portfolio of airline marketing and operations products across the solutions that we

1

Table of Contents

provide. In addition, we operate Travelocity, one of the world’s most recognizable brands in the online consumer travel e-commerce industry, which provides us with business insights into our broader customer base.

Through our solutions, which span the breadth of the travel ecosystem, we have developed deep domain expertise. Our success is built on this expertise, combined with our significant technology investment and focus on innovation. This foundation has enabled us to develop highly scalable and technology-rich solutions that directly address the key opportunities and challenges facing our customers. For example, we have invested to scale our GDS platform to meet massive transaction processing requirements. In 2013, our systems processed over $100 billion of estimated travel spending and more than 1.1 trillion system messages, with nearly 100,000 system messages per second at peak times. Our investment in innovation has enabled our Travel Network business to evolve into a dynamic marketplace providing a broad range of highly scalable solutions from distribution to workflow to business intelligence. Our investment in our Airline and Hospitality Solutions offerings has allowed us to create a broad portfolio of value-added products for our travel supplier customers, ranging from reservations platforms to operations solutions typically delivered via highly scalable and flexible software-as-a-service (“SaaS”) and hosted platforms. We have a long history of engineering innovative travel technology solutions. For example, we believe we were the first GDS to enable airlines to sell ancillary products like premium seats through the GDS, the first third-party provider to automate passenger reaccommodation during large operational disruptions and the first GDS to launch a business-to-business (“B2B”) app marketplace for our travel agency customers that allows them to customize and augment our Travel Network platform. Our innovation has been consistently recognized in the market, with awards including the Business Traveler Innovation Award from the Global Business Travel Association, an unaffiliated entity, in 2011 and 2012, for which we applied and were one of eight award winners chosen by popular vote. We were also recognized by the InformationWeek 500 in 2013 as one of the Most Innovative Users of Business Technology for the eleventh consecutive year. These 500 companies are invited to apply and are chosen by InformationWeek, an unaffiliated entity, based on their unconventional approaches and new ways of solving complex business problems with IT.

Our SaaS and hosted technology platforms allow us to serve our customers primarily through a recurring, transaction-based revenue model based primarily on travel events such as air segments booked, passengers boarded (“PBs”) or other relevant metrics. For the year ended December 31, 2013, 91% of our Travel Network and Airline and Hospitality Solutions revenue, on a weighted average basis, was Recurring Revenue. See “Method of Calculation” for a description of Recurring Revenue. This model has benefits for both our customers and for us. For our customers, our delivery model allows otherwise fixed technology investments to be variable, providing flexibility in their cost base and smoothing investment cycles as they grow, while enabling them to benefit from the continuous evolution of our platform. For us, this recurring, transaction-based revenue model allows us to expand with our customers in the travel industry, a segment of the economy which has grown significantly faster than global GDP over the last 40 years. Since our revenues are primarily linked to our customers’ transaction volumes, rather than to airline budget cycles or cyclical end-customer pricing, which we believe are more volatile than transaction volumes, this model facilitates greater stability in our business, particularly during negative economic cycles. In addition, as a technology solutions and transaction processing company, we do not take airline, hotel or other inventory risk, nor are we directly exposed to fuel price volatility or labor unions.

Our recurring, transaction-based revenue model, combined with our high-quality products, reinvestment in our technology, multi-year customer contracts and disciplined operational management, has contributed to our strong growth profile, as demonstrated by our Adjusted EBITDA having increased each year since 2008 despite the global economic downturn and resulting travel slowdown. From 2009 through 2013, we grew our revenue and Adjusted EBITDA at 7% and 11% compound annual growth rates (“CAGRs”), respectively, and increased Adjusted EBITDA margins by 394 basis points (“bps”), in each case, excluding Travelocity and intersegment eliminations. During the same period, net loss attributable to Sabre Corporation decreased 37% and net loss margin decreased by 258 bps. See “Non-GAAP Financial Measures” and “—Summary Consolidated Financial Data” for additional information regarding Adjusted EBITDA, including a reconciliation of Adjusted EBITDA to the most directly comparable GAAP measure.

2

Table of Contents

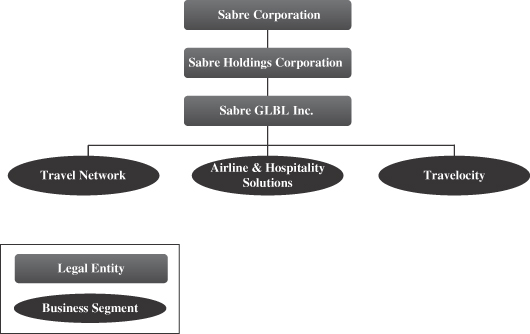

Our Business

We operate through three business segments: (i) Travel Network, (ii) Airline and Hospitality Solutions, and (iii) Travelocity. Our segments operate with shared infrastructure and technology capabilities, and provide key solutions to our customers. Collectively, our integrated business enables the entire travel lifecycle, from route planning to post-trip business intelligence and analysis. The graphic below provides illustrative examples of the points where Sabre enables the travel lifecycle:

Travel Network is our global B2B travel marketplace and consists primarily of our GDS and a broad set of capabilities that integrate with our GDS to add value for travel suppliers and travel buyers. Our GDS offers content from a broad array of travel suppliers, including approximately 400 airlines, 125,000 hotel properties, 30 car rental brands, 50 rail carriers, 16 cruise lines and 200 tour operators, to tens of thousands of travel buyers, including online and offline travel agencies, TMCs and corporate travel departments. Our Airline and Hospitality Solutions business offers a broad portfolio of software technology products and solutions, primarily through SaaS and hosted models, to approximately 225 airlines, 17,500 hotel properties and 700 other travel suppliers. Our flexible software and systems applications help automate and optimize our customers’ business processes, including reservations systems, marketing tools, commercial planning solutions and enterprise operations tools. Travelocity is our family of online consumer travel e-commerce businesses through which we provide travel content and booking functionality primarily for leisure travelers. In August 2013, Travelocity entered into an exclusive, long-term strategic marketing agreement with Expedia which was recently amended and restated in March 2014 to reflect changed commercial terms (as amended and restated, the “Expedia SMA”). Under the Expedia SMA, Expedia will power the technology platforms of Travelocity’s existing U.S. and Canadian websites, as well as provide access to Expedia’s supply and customer service platforms. Additionally, Travelocity recently sold its Travelocity Partner Network (“TPN”) business, a B2B loyalty and private label website offering, to Orbitz.

For the years ended December 31, 2013 and 2012, we recorded revenue of $3,050 million and $2,974 million, respectively, net loss attributable to Sabre Corporation of $100 million and $611 million respectively, and Adjusted EBITDA of $791 million and $787 million, respectively, reflecting a 3% and 21% net loss margin and a 26% and 26% Adjusted EBITDA margin, respectively. For additional information regarding Adjusted

3

Table of Contents

EBITDA, including a reconciliation of Adjusted EBITDA to the most directly comparable GAAP measure, see “Non-GAAP Financial Measures” and “—Summary Consolidated Financial Data.” For the year ended December 31, 2013, Travel Network contributed 58%, Airline and Hospitality Solutions contributed 23%, and Travelocity contributed 19% of our revenue (excluding intersegment eliminations). During this period, shares of Adjusted EBITDA for Travel Network, Airline and Hospitality Solutions, and Travelocity were approximately 77%, 21% and 2%, respectively (excluding corporate overhead allocations such as finance, legal, human resources and certain information technology shared services).

Our Industry

The travel and tourism industry is one of the world’s largest industry segments, contributing $6.6 trillion to global GDP in 2012, according to the World Travel & Tourism Council’s Economic Impact of Travel & Tourism 2013 (“WTTC”). The industry encompasses travel suppliers, including airlines, hotels, car rental brands, rail carriers, cruise lines and tour operators around the world, as well as travel buyers, including online and offline travel agencies, TMCs and corporate travel departments.

The travel and tourism industry has been a growing area of the broader economy. For example, based on 40 years of data from the IATA Monthly Traffic Analysis Archives (“IATA Traffic”), air traffic has historically grown at an average rate of approximately 1.5x the rate of global GDP growth. Going forward, Euromonitor International Passport Travel and Tourism Database (“Euromonitor Database”) expects a 4% CAGR in air travel and hotel spending from 2013 to 2017, with air traffic in developing markets such as APAC, Latin America and the Middle East expected to grow at even faster rates of 6%, 6% and 7%, respectively, from 2012 to 2032, according to Airbus Global Market Forecast 2013-2032 (“Airbus”). In addition to growth in emerging geographies, hybrid carriers and low-cost carriers (“LCCs”, and collectively, “LCC/hybrids”) have continued to grow, with LCCs’ share of global air travel volume expected to increase from 17% of revenue passenger kilometers in 2012 to 21% of revenue passenger kilometers by 2032, according to Airbus.

Technology is integral to that growth, enabling the operation of the modern travel ecosystem by powering the industry lifecycle from distribution to operations. With the increasing complexity created by the large, fragmented and global nature of the travel industry, reliance on technology will only increase. That reliance drove technology spending by the air transportation and hospitality industries to $60 billion in 2013, with expenditures expected to exceed $70 billion in 2017, according to Gartner Enterprise IT Spending by Vertical Industry Market, Worldwide, 2011-2017 (“Gartner Enterprise”). Some recent trends in the travel industry which we expect to further technology innovation and spending include:

Outsourcing:Historically, technology solutions were built in-house by travel suppliers and travel buyers. As complexity and the pace of innovation have increased, third-party providers have emerged to offer more cost-effective and advanced solutions. Additionally, the travel technology industry has shifted to a more flexible and scalable technology delivery model including SaaS and hosted implementations that allow for shared development, reduced deployment costs, increased scalability and a “pay-as-you-go” cost model.

Airline Ancillary Revenue:The sale of ancillary products is now a major source of revenue for many airlines worldwide, and has grown to comprise as much as 20% of total revenues for some carriers and more than $36 billion in the aggregate across the travel industry in 2012, according to CarTrawler Worldwide Estimate of Ancillary Revenue (“IdeaWorks”). Enabling the sale of ancillary products is technologically complex and requires coordinated changes to multiple interdependent systems including reservations platforms, inventory systems, point of sale locations, revenue accounting, merchandising, shopping, analytics and other systems. Technology providers such as Sabre have already significantly enhanced their systems to provide these capabilities and we expect these providers to take further advantage of this significant opportunity going forward.

4

Table of Contents

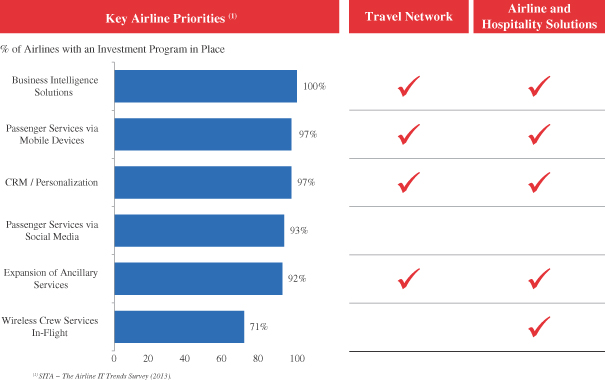

Mobile:Mobile platforms have created new ways for customers to research, book and experience travel, and are expected to account for over 30% of online travel sales by 2017, according to Euromonitor International World Travel Market Global Trends Report 2013 (“Euromonitor Report”). Accordingly, travel suppliers, including airlines and hospitality providers, are upgrading their systems to allow for delivery of services via mobile platforms from booking to check-in to travel management. According to SITA’s 2013 Air Transport Industry Insights: The Airline IT Trends Survey (“SITA Survey”), 97% of airlines are investing in mobile channels with the intention of increasing mobile access across the entire travel experience. This mobile trend also extends to the use of tablets and wireless connectivity by the airline workforce, such as automating cabin crew services and providing flight crews with electronic flight bags. Travel technology companies like Sabre are enabling and benefitting from this trend as travel suppliers upgrade their systems and travel buyers look for new sources of client connectivity.

Personalization:Concurrently with the rise of ancillary products and mobile devices as a customer service tool, travel suppliers have an opportunity to provide increased personalization across the customer travel experience, from seat selection and on-board entertainment to loyalty program management and mobile concierge services. Data-driven business intelligence products can help travel companies use available customer data to identify the types of products, add-ons and upgrades customers are more likely to purchase and market these products effectively to various customer segments according to their needs and preferences. In addition to providing the technology platform to facilitate these services, we believe technology providers like Sabre can leverage their data-rich platforms and travel technology domain expertise to offer analytics and business intelligence to support travel suppliers in delivering more personalized service offerings.

Increasing Use of Data and Analytics: The use of data has always been an asset in the travel industry. Airlines were pioneers in the use of data to optimize seat pricing, crew scheduling and flight routing. Similarly, hotels employed data to manage room inventory and optimize pricing. The travel industry was also one of the first to capitalize on the value of customer data by developing products such as customer loyalty programs. Historically, this data has largely been transaction-based, such as booking reservations, recording account balances, and tracking points in loyalty programs. Today, analytics-driven business intelligence products are evolving to further and better utilize available data to help travel companies make decisions, serve customers, optimize their operations and analyze their competitive landscape. Technology providers like Sabre have developed and continue to develop large-scale, data-rich platforms that include these business intelligence and data analytics tools that can identify new business opportunities and global, integrated and high-value solutions for travel suppliers.

Our Competitive Strengths

We believe the following attributes differentiate us from our competitors and have enabled us to become a leading technology solutions provider to the global travel industry.

Broadest Portfolio of Leading Technology Solutions in the Travel Industry

We offer the broadest, most comprehensive technology solutions portfolio available to the travel industry from a single provider, and our solutions are key to the operations of many of our travel supplier and travel agency customers. Travel Network, for example, provides a key technology platform that enables efficient shopping, booking and management of travel itineraries for online and offline travel agencies, TMCs and corporate travel departments. In addition to offering these and other advanced functionalities, it is a valuable distribution and merchandising channel for travel suppliers to market to a broad array of customers, particularly outside their home countries and regions. Additionally, we provide SaaS and hosted solutions that run many of the most important operations systems for our travel supplier customers, such as airline and hotel reservations systems, revenue management, crew scheduling and flight operations. We believe that our Travel Network and

5

Table of Contents

Airline and Hospitality Solutions offerings address customer needs across the entire travel lifecycle, and that we are the only company that provides such a broad portfolio of technology solutions to the travel industry. This breadth affords us significant competitive advantages including the ability to leverage shared infrastructure, a common technology organization and product development. Beyond scale and efficiency, our position spanning the breadth of the travel ecosystem helps us to develop deep domain expertise and to anticipate the needs of our customers. Taken together, the value, quality, and breadth of our technology, software and related customer services contribute to our strong competitive position.

Global Leadership Across Growing End Markets

We operate in areas of the global travel industry that have large and growing addressable customer bases. Each of our businesses is a leader in its respective area. Sabre is the leading GDS provider in North America, Latin America, and APAC, with 55%, 57%, and 39% share ofGDS-processed air bookings, respectively, in 2013. Additionally, Airline Solutions is the second largest provider of reservations systems, with an 18% global share of 2012 PBs, according to T2RL PSS. We believe that we have the leading portfolio of airline marketing and operations products across the solutions that we provide. We also believe our Hospitality Solutions business is the leader in hotel reservations, handling 27% of third-party hospitality CRS hotel rooms through our GDS in 2013. See “Method of Calculation” for an explanation of the methodology underlying ourGDS-processed air bookings share and third-party hospitality CRS hotel room share calculations.

Looking forward, we expect to benefit from attractive growth in our end markets. Euromonitor expects a 4% CAGR in air travel and hotel spending from 2013 to 2017. Gartner, Inc. (“Gartner”) expects technology spending by the air transportation and hospitality sectors to grow significantly from $60 billion in 2013 to over $70 billion in 2017. Within our Travel Network business, we also expect our presence in economies with strong GDP growth and regions with faster air traffic growth, such as APAC, Latin America and the Middle East and Africa (“MEA”), will further contribute to the growth of our businesses. Similarly, our Airline Solutions reservations products customers are weighted toward faster-growing LCC/hybrids, which represented approximately 45% of our 2012 PBs.

Innovative and Scalable Technology

Two pillars underpin our technology strategy: innovation and scalability. To drive innovation in our travel marketplace business, we make significant investments in technology to develop new products and add incremental features and functionality, including advanced algorithms, decision support, data analysis and other valuable intellectual property. This investment is supported by our global technology teams comprising approximately 4,000 employees and contractors. This scale and cross-business technology organization creates efficiency and a flexible environment that allows us to apply knowledge and resources across our broad product portfolio, which in turn fuels innovation. In addition, our investments in technology have created a highly scalable set of solutions across our businesses. For example, we believe our GDS is one of the most heavily utilized Service Oriented Architecture (“SOA”) environments in the world, processing more than 1.1 trillion system messages in 2013, with nearly 100,000 system messages per second at peak times. Our Airline and Hospitality Solutions business employs highly reliable software technology products and SaaS and hosted infrastructure. Compared to traditional in-house software installations, SaaS and hosted technology offers our customers advantages in terms of cost savings, more robust functionality, increased flexibility and scale, and faster upgrades. As an example of the SaaS and hosted scalability benefit, our delivery model has facilitated an increase in the number of PBs in our Airline Solutions business from 288 million to 478 million from 2009 to 2013. Our investments in technology maintain and extend our technology platform which has supported our industry-leading product innovation. On the scale at which we operate, we believe that the combination of an expanding network and technology investments continues to create a significant competitive advantage for us.

6

Table of Contents

Stable, Resilient, and Diversified Business Models

Travel Network and much of Airline and Hospitality Solutions operate with a transaction-based business model that ties our revenue to a travel supplier’s transaction volumes rather than to its unit pricing for an airplane ticket, hotel room or other travel product. Travel-related businesses with volume-based revenue models have generally shown strong visibility, predictability and resilience across economic cycles because travel suppliers have historically sought to maintain traveler volumes by reducing prices in an economic downturn.

Our resilience is also partially attributable to our non-exclusive, multi-year contracts in our Travel Network business. For example, although most of our contracts have terms of one to three years, contracts with our major travel buyer and travel supplier customers, which represent the majority of Travel Network revenue, have five to ten year terms and three to five year terms, respectively. Similarly, our Airline Solutions business has contracts that typically range from three to seven years in length, and our Hospitality Solutions business has contracts that typically range from one to five years in length. Our Travel Network and Airline and Hospitality Solutions businesses also deliver solutions that are integral components of our customers’ businesses and have historically remained in place once implemented. In our Travel Network business and our Airline and Hospitality Solutions business, 94% and 84% of our revenue was Recurring Revenue, respectively, in 2013.

In addition to being stable, our businesses are also diversified. Travel Network and Airline and Hospitality Solutions generate a broad geographic revenue mix, with a combined 43% of revenue generated outside the United States in 2013. None of our travel buyers or travel suppliers accounted for more than 10% of our revenue for the years ended December 31, 2013 or 2012.

Strong, Long-Standing Customer Relationships

We have strong, long-standing customer relationships with both travel suppliers and travel buyers. These relationships have allowed us to gain a deep understanding of our customers’ needs, which positions us well to continue introducing new products and services that add value by helping our customers improve their business performance. In our Travel Network business, for example, by providing efficient and quality services, we have developed and maintained strong customer relationships with TMCs, major corporate travel departments and travel suppliers, with some of these relationships dating back over 20 years. Through our Travelocity business, we have gained important insights into what online travel companies need in order to best serve their customers, and we are able to leverage that knowledge to develop products and services to address those needs.

We believe that our strong value proposition is demonstrated by our ability to retain customers in a highly competitive marketplace. For each of the years ended December 31, 2013, 2012 and 2011, our Customer Retention rate for Travel Network was 99%. For our Airline Solutions business, our Customer Retention rate was 98%, 96% and 96% for the years ended December 31, 2013, 2012 and 2011 respectively, and our Customer Retention rate for our Hospitality Solutions business was 96%, 96% and 98% for the same periods, respectively. See “Method of Calculation” for a description of Customer Retention.

Deep and Experienced Leadership Team with Informed Insight into the Travel Industry

Our management team is highly experienced, with comprehensive expertise in the travel and technology industries. Many of our leaders have more than 20 years of experience in multiple segments of the travel industry and have held positions in more than one of our businesses, which provides them with a holistic and interdisciplinary perspective on our company and the travel industry.

By investing in training, skills development and rotation programs, we seek to develop leaders with broad knowledge of our company, the industry, technology, and specific customer needs. We also hire externally as needed to bring in new expertise. Our blend of experience and new hires across our team provides a solid foundation on which we develop new capabilities, new business models and new solutions to complex industry problems.

7

Table of Contents

Our Growth Strategy

We believe we are well-positioned for future growth. First, we expect the continued macroeconomic recovery to generate travel growth, compounded by the continuing trend towards the outsourcing of travel technology. In addition, we are well-positioned in market segments which are growing faster than the overall travel industry, with leading market positions in our Travel Network business in Latin America and APAC. In our Airline Solutions reservations systems, LCC/hybrids, which are growing traffic faster than traditional airlines, accounted for approximately 45% of our PBs in 2012. Supported by these industry trends, we believe both our Travel Network and our Airline and Hospitality Solutions businesses have significant opportunities to expand their customer bases, further penetrate existing customers, extend their geographic footprint and develop new products. By executing on the following strategies and, when appropriate, selective strategically aligned acquisitions, we intend to capitalize on these positive trends:

Leverage our Industry-Leading Technology Platforms

We have made significant investments in our technology platforms and infrastructure to develop robust, scalable software as well as SaaS and hosted solutions. We plan to continue leveraging these investments across our organization, particularly in our Travel Network and Airline and Hospitality Solutions businesses, to catalyze product innovation and speed-to-market. We will also continue to shift toward SaaS and hosted infrastructure and solutions as we further develop our product portfolio.

Expand our Global Travel Marketplace Leadership

Travel Network intends to remain the global B2B travel marketplace of choice for travel suppliers and travel buyers by executing on the following initiatives:

| • | Targeting Geographic Expansion: From 2009 to 2013, we increased our GDS-processed air bookings share in the Middle East, Russia and Brazil by 744 bps, 327 bps and 267 bps, respectively. We currently have initiatives in place across Europe, APAC and Latin America to further expand in those regions. |

| • | Attracting and Enabling New Marketplace Content: We are actively adding new travel supplier content which generates revenue directly through incremental booking volumes associated with the new content and reinforces the virtuous cycle of our Travel Network business: as we add more supplier content to our marketplace, we experience increased participation from travel buyers, which, in turn, encourages travel suppliers to contribute additional content to our marketplace. We have been successful in converting notable carriers that previously only used direct distribution, such as JetBlue and Norwegian, to join our GDS, and we believe there is a similar opportunity to increase the participation of less-penetrated content types like hotel properties, where we estimate that only approximately one-third participate in a GDS. In addition to attracting new supplier content, we aim to expand the content available for sale from existing travel suppliers, including ancillary revenue—a category of airline revenue worth more than $36 billion in the aggregate across the travel industry in 2012, according to IdeaWorks. We seek additional opportunities to capitalize on this trend, such as by supporting our airline customers’ branded fare initiatives. |

| • | Continuing to Invest in Innovative Products and Capabilities: The development of cutting-edge products and capabilities has been critical to our success. We plan to continue to invest significant resources in solutions that address key customer needs, including mobility (e.g., TripCase), data analytics and business intelligence (e.g., Sabre Dev Studio, Hotel Heatmaps, Contract Optimization Services), and workflow optimization (e.g., Sabre Red App Centre, TruTrip). |

8

Table of Contents

Drive Continued Airline and Hospitality Solutions Growth and Innovation

Our Airline and Hospitality Solutions business has been a key growth engine for us, increasing both revenue and Adjusted EBITDA by 72% from 2009 to 2013. We believe Airline and Hospitality Solutions will continue to drive company growth through a combination of underlying customer and market growth, as well as through the following strategic growth initiatives:

| • | Invest in Innovative Airline Products and Capabilities: We have a long history of investment in innovation. For example, we believe we were the first technology solutions provider to provide real-time revenue integrity and the first third-party provider to automate passenger reaccommodation during large operational disruptions. We see a continued opportunity to innovate in areas such as retailing solutions, mobile capabilities, data analytics and business intelligence offerings. |

| • | Continue to Add New Airline Reservations Customers: Over the last four years, we have added airline customers representing over 110 million annual PBs from many innovative, fast-growing airlines such as Etihad Airways, Virgin Australia, JetBlue and LAN. Although the number of new reservations opportunities varies materially by year, in 2013, T2RL estimated that contracts representing over 1.3 billion PBs will come up for renewal between 2014 to 2017, of which over 1.1 billion PBs are from airlines who do not pay us PB fees today. As of this filing, airlines won but not yet implemented by Sabre boarded over 220 million PBs in 2012, according to T2RL. This includes a long-term agreement announced in January 2014 with American Airlines for Sabre to be its reservations system provider following its merger with US Airways. |

| • | Further Penetrate Existing Airline Solutions Customers: We believe there is an opportunity to sell more of our extensive solution set to our existing customers. Of our 2013 customers in T2RL’s top 100 passenger airlines, 35% had one or two non-reservations solution sets, 36% had three to five and 29% had more than five. Historically, the average revenue would have approximately tripled if a customer moved from the first category to the second, and nearly tripled again if a customer moved to the third category. Leveraging our brand, we intend to continue to promote the adoption of our products within and across our existing customers. |

| • | Invest Behind Rapidly Growing Hospitality Solutions Business: Our Hospitality Solutions business has grown rapidly, with 19% revenue CAGR from 2009 to 2013, and we are focused on continuing that growth going forward. We currently have initiatives to grow in our existing footprint and expand our presence in APAC and in Europe, the Middle East and Africa (“EMEA”), which collectively accounted for only 32% of our Hospitality Solutions business revenue in 2013. We plan to accomplish this through a combination of cross-selling additional products to our existing customers, expanding our global reseller network and enhancing our product offering. |

Continue to Focus on Operational Efficiency Supported by Leading Technology

As an organization, we have a track record of improving operational efficiency and capitalizing on our scalable technology platform and operating leverage in our business model. We have expanded Adjusted EBITDA margins by over 550 bps since 2009 in our Travel Network business while growing the business and introducing new products. We intend to continue to increase our operational efficiency by following a shared capabilities, technology and insights approach across our businesses. For example, through the Expedia SMA, we intend to reduce direct costs associated with Travelocity and expect to improve our Adjusted EBITDA by providing our customers with the benefit of Expedia’s long-term investment in its technology platform to increase conversion, improve operational efficiency, and shift our focus to Travelocity’s strengths in marketing and retailing. Additionally, Travelocity recently sold its TPN business, a B2B loyalty and private label website offering, to Orbitz. We will continue to work toward identifying operational and technological efficiencies while continuing to support our investments and strategic priorities to maintain our leadership position in the travel industry.

9

Table of Contents

Summary of Risks

Significant risks that could materially and adversely affect our business, financial condition and results of operations include:

| • | factors affecting transaction volumes in the global travel industry, particularly air travel transaction volumes, including global and regional economic and political conditions, financial instability or fundamental corporate changes to travel suppliers, natural or man-made disasters, safety concerns or changes to regulations governing the travel industry; |

| • | our ability to renew existing contracts or to enter into new contracts with travel supplier and buyer customers, third-party distributor partners and joint ventures on economically favorable terms or at all; |

| • | our Travel Network business’ exposure to pricing pressures from travel suppliers and its dependence on relationships with several large travel buyers; |

| • | the fact that travel supplier customers may experience financial instability, consolidate with one another, pursue cost reductions, change their distribution model or experience other changes adverse to us; |

| • | travel suppliers’ use of alternative distribution models, such as direct distribution channels, technological incompatibilities between suppliers’ travel content and our GDS, and the diversion of consumer traffic to other channels; |

| • | our reliance on third-party distributors and joint ventures to extend GDS services to certain regions, which exposes us to risks associated with lack of direct management control and potential conflicts of interest; |

| • | competition in the travel distribution market from other GDS providers, direct distribution by travel suppliers and new entrants or technologies that could challenge the existing GDS business model; maintaining and growing our Airline and Hospitality Solutions business could be negatively impacted by competition from other third-party solutions providers and from new participants entering the solutions market; |

| • | risks associated with implementing the Expedia SMA and the fact that the benefits anticipated by the parties to the Expedia SMA may not materialize; |

| • | availability and performance of information technology services provided by third parties, such as HP, which manages a significant portion of our systems; |

| • | systems and infrastructure failures or other unscheduled shutdowns or disruptions, including those due to natural disasters or cybersecurity attacks; |

| • | the fact that we qualify as a “controlled company” within the meaning of the NASDAQ Stock Market (the “NASDAQ”) rules and, therefore we also qualify to be exempt from certain corporate governance requirements, which means that our stockholders may not have the same protections afforded to stockholders of companies that are subject to such requirements; |

| • | the fact that our Principal Stockholders (as defined below) will, following the completion of the offering, retain significant influence over us and key decisions about our business, with approximately 80% of our voting power to be held by our affiliates following the completion of the offering, which may prevent new investors from influencing significant corporate decisions and result in conflicts of interest; and |

| • | our significant amount of long-term indebtedness and the related restrictive covenants in the agreements governing our indebtedness. |

See “Risk Factors” beginning on page 22 for additional risks that could impact our business.

10

Table of Contents

Concurrent Transactions

Redemption of Preferred Stock

Prior to the closing of this offering, we will exercise our right to redeem (the “Redemption”) all of our Series A Preferred Stock (the “Series A Preferred Stock”). The redemption price will be paid with a mix of cash and stock, which we will deliver pro rata to the holders thereof concurrently with the closing of this offering. Assuming we sell the total number of shares set forth on the cover of this prospectus at an initial public offering price equal to the midpoint of the price range on the cover of this prospectus, we will deliver an estimated aggregate of $235 million in cash and 21,470,518 shares of our common stock in payment of the related redemption price plus accumulated but unpaid dividends as of March 31, 2014 (the “Redemption Payment”). A $1.00 increase in the estimated net proceeds of this offering would increase the aggregate cash component of the Redemption Payment by $1.00 and decrease the common stock component by 0.053 shares, which represents a value of $1.00 based on the assumed offering price. Conversely, a $1.00 decrease in the estimated net proceeds of this offering would cause us to decrease the aggregate cash component of the Redemption Payment by $1.00 and to increase the common stock component by 0.053 shares, which represents a value of $1.00 based on the assumed offering price. In all cases, the common stock delivered in the Redemption will be valued at the actual initial public offering price and will also reflect shares of our common stock to be issued in satisfaction of dividends that accrue on or after April 1, 2014 and to, but excluding, the closing date of this offering.

The Redemption of the Series A Preferred Stock will simplify our capital structure by leaving only one class of capital stock – our common stock – outstanding following the closing of this offering. For more information, see “Description of Capital Stock—Series A Preferred Stock.”

Tax Receivable Agreement

Immediately prior to the completion of this offering, we will enter into a tax receivable agreement (“TRA”) that provides the right to receive future payments from us to certain of our stockholders and equity award holders that are our stockholders and equity award holders, respectively, prior to the completion of this offering (collectively, the “Existing Stockholders”) of 85% of the amount of cash savings, if any, in U.S. federal income tax that we and our subsidiaries realize as a result of the utilization of certain tax assets attributable to periods prior to our initial public offering, including federal net operating losses, capital losses and the ability to realize tax amortization of certain intangible assets (collectively, the “Pre-IPO Tax Assets”). Based on current tax laws and assuming that we and our subsidiaries earn sufficient taxable income to realize the full tax benefits subject to the TRA, (i) we expect that future payments under the TRA relating to the Pre-IPO Tax Assets could aggregate to between $330 million and $380 million over the next six years (assuming no changes to current limitations on our ability to utilize our net operating loss carryforwards (“NOLs”) under Section 382 of the Internal Revenue Code (the “Code”)), which we estimate will represent approximately 85% to 95% of the total payments we will be required to make under the TRA and (ii) we do not expect material payments to occur before 2016. See “Certain Relationships and Related Party Transactions—Tax Receivable Agreement.”

Redemption of the Sabre GLBL 2019 Notes

We intend to use a portion of the net proceeds from this offering to redeem $320 million in aggregate principal amount of Sabre GLBL’s 8.5% senior secured notes due 2019 at a redemption price of 108.5% of the principal amount of the notes redeemed, plus accrued and unpaid interest to, but excluding, the date of redemption. Substantially concurrent with the launch of this offering, Sabre GLBL will issue a notice of redemption, pursuant to which we will effect such redemption on May 7, 2014 contingent on the consummation of this offering. In the event that consummation of this offering has not occurred on or prior to such date, Sabre GLBL may extend such date one or more times to a date not later than 60 days after the date of

11

Table of Contents

the redemption notice. After giving effect to this redemption, Sabre GLBL will have $480 million in aggregate principal amount of our 2019 Notes outstanding. See “Description of Other Indebtedness” for a description of the 8.5% senior secured notes due 2019.

Corporate and Other Information

Sabre Holdings Corporation is a Delaware corporation formed in 1996. It was operated as a division of AMR Corporation, its parent company, until it was spun off completely in 2000. Sabre Corporation is a Delaware corporation formed in December 2006 and is the parent company of Sabre Holdings Corporation and Sabre GLBL. Prior to our acquisition in 2007 by the Principal Stockholders (as defined below), we were previously a publicly-held travel technology company. We are headquartered in Southlake, Texas, and employ approximately 10,000 people in approximately 60 countries around the world. We serve our customers through cutting-edge technology developed in six facilities located across four continents.

Our principal executive offices are located at 3150 Sabre Drive, Southlake, TX 76092, and our telephone number is (682) 605-1000. Our corporate website address is www.sabre.com. The information contained on our website or that can be accessed through our website will not be deemed to be incorporated into this prospectus or the registration statement of which this prospectus forms a part, and investors should not rely on any such information in deciding whether to purchase our common stock.

Principal Stockholders

Our Relationship with the TPG Funds and Silver Lake Funds

We are currently privately held as a result of our acquisition in 2007 by the TPG Funds and the Silver Lake Funds. On March 30, 2007, we entered into a Stockholders’ Agreement by and among the TPG Funds, the Silver Lake Funds, Sovereign Co-Invest, LLC (“Sovereign Co-Invest,” an entity co-managed by TPG and Silver Lake, and together with the TPG Funds and the Silver Lake Funds, the “Principal Stockholders”), and Sabre Corporation (formerly known as Sovereign Holdings, Inc.), which will be amended and restated in connection with the completion of this offering (as amended and restated, the “Stockholders’ Agreement”). See “Certain Relationships and Related Party Transactions—Stockholders’ Agreement.”

Following the completion of this offering, the Principal Stockholders will own approximately 79% of our common stock, or 77% if the underwriters’ option to purchase additional shares is fully exercised. The TPG Funds, the Silver Lake Funds and the Sovereign Co-Invest will own approximately 37%, 23% and 19%, respectively, of our common stock, or 36%, 22% and 19%, respectively, if the underwriters’ option to purchase additional shares is fully exercised. As a result, we expect to be a “controlled company” within the meaning of the corporate governance requirements of the NASDAQ on which we have applied to list our shares of common stock. See “Risk Factors—Risks Related to the Offering and Our Common Stock—We expect to be a “controlled company” within the meaning of the NASDAQ rules and, as a result, we will qualify for exemptions from certain corporate governance requirements. You may not have the same protections afforded to stockholders of companies that are subject to such requirements.”

TPG

TPG is a leading global private investment firm founded in 1992 with over $59 billion of assets under management as of December 31 2013, as adjusted for commitments accepted on January 2, 2014 and offices in San Francisco, Fort Worth, Austin, Beijing, Chongqing, Hong Kong, London, Luxembourg, Melbourne, Moscow, Mumbai, New York, Paris, São Paulo, Shanghai, Singapore and Tokyo. TPG has extensive experience with global public and private investments executed through leveraged buyouts, recapitalizations, spinouts,

12

Table of Contents

growth investments, joint ventures and restructurings. The firm’s investments span a variety of industries, including financial services, travel and entertainment, technology, energy, industrials, retail, consumer, real estate, media and communications, and healthcare. For more information please visit www.tpg.com.

Silver Lake

Silver Lake is a global investment firm focused on the technology, technology-enabled and related growth industries with offices in Silicon Valley, New York, London, Hong Kong, Shanghai and Tokyo. Silver Lake was founded in 1999 and has over $20 billion in combined assets under management and committed capital across its large-cap private equity, middle-market private equity, growth equity and credit investment strategies.

Summary of Corporate Structure

13

Table of Contents

THE OFFERING

Common stock we are offering | 44,736,842 shares |

Common stock to be outstanding after this offering | 245,338,645 shares |

Underwriters’ option to purchase additional shares | We may sell up to 6,710,526 additional shares if the underwriters exercise their option to purchase additional shares. |

Use of proceeds | We estimate that our net proceeds from this offering will be approximately $797 million at an assumed initial public offering price of $19.00 per share, the midpoint of the range set forth on the cover page of this prospectus, after deducting the underwriting discounts and commissions and estimated offering expenses. |

| We intend to use the net proceeds of this offering to repay $180 million of our outstanding indebtedness under the Term C Facility (as defined in “Description of Certain Indebtedness”) portion of our senior secured credit facilities and redeem $320 million in aggregate principal amount of the 2019 Notes (as defined in “Description of Certain Indebtedness”) at a redemption price of 108.5% of the principal amount of the 2019 Notes redeemed, plus accrued and unpaid interest to, but excluding, the date of redemption. We intend to use $256 million, the remaining portion of the net proceeds from this offering, to pay a $21 million fee, in the aggregate, to TPG and Silver Lake pursuant to the management services agreement (“MSA”) which will thereafter be terminated, and $235 million to redeem the Series A Preferred Stock. If the underwriters exercise their option to acquire additional shares of common stock, we intend to use any net proceeds we receive to repay additional outstanding indebtedness under our Term C Facility. See “Use of Proceeds.” |

Dividend policy | Contingent upon the closing of this offering, we intend to pay quarterly cash dividends on our common stock. We expect that our first dividend will be paid in the third quarter of 2014 (in respect of the second quarter of 2014) and will be $0.09 per share of our common stock. We intend to fund our initial dividend, as well as any future dividends, from distributions made by our operating subsidiaries from their available cash generated from operations. |

The ability of our subsidiaries to pay cash dividends, which could then be further distributed to holders of our common stock, is currently restricted in certain circumstances by the covenants in our Credit Facility (as defined in “Description of Certain Indebtedness”) and the indenture governing the 2019 Notes and may be further restricted by the terms of future debt or preferred securities. No dividend can be declared or paid with respect of our common stock unless and until the full amount of unpaid dividends accrued on our |

14

Table of Contents

Series A Preferred Stock, if any, has been paid or contemporaneously declared and paid. See “Dividend Policy.” Prior to the closing of this offering, we will exercise our right to redeem all of our Series A Preferred Stock. See “Description of Capital Stock—Series A Preferred Stock.” |

Risk factors | Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 22 for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

Proposed NASDAQ symbol | “SABR” |

Conflicts of interest | Certain affiliates of TPG Capital BD, LLC, an underwriter of this offering, will own in excess of 10% of our issued and outstanding common stock following this offering. In addition, the TPG Funds are affiliates of TPG Capital BD, LLC and, as holders of a portion of our Series A Preferred Stock, they will receive more than 5% of the net proceeds of this offering, based upon an assumed initial public offering price of $19.00 per share, the midpoint of the range set forth on the cover page of this prospectus. |

| As a result of the foregoing relationships, TPG Capital BD, LLC is deemed to have a “conflict of interest” within the meaning of FINRA Rule 5121. Accordingly, this offering will be made in compliance with the applicable provisions of FINRA Rule 5121. Pursuant to that rule, the appointment of a qualified independent underwriter is not necessary in connection with this offering. In accordance with FINRA Rule 5121(c), no sales of the shares will be made to any discretionary account over which TPG Capital BD, LLC exercises discretion without the prior specific written approval of the account holder. See “Use of Proceeds” and “Underwriting (Conflicts of Interest).” |

The number of shares of common stock to be outstanding after this offering is based on 179,131,285 shares of common stock outstanding as of March 31, 2014, 44,736,842 shares to be sold in this offering and 21,470,518 shares to be issued in the share component of the Redemption in payment of the related redemption price plus accumulated and unpaid dividends as of March 31, 2014 (assuming we sell in this offering the total number of shares set forth on the cover of this prospectus at an initial public offering price equal to the midpoint of the range set forth on the cover of the prospectus). In all cases, the common stock delivered in the Redemption will be valued at the actual initial public offering price and will also reflect shares of our common stock to be issued in satisfaction of dividends that accrue on or after April 1, 2014 and to, but excluding, the closing date of this offering.

15

Table of Contents

The number of shares of common stock to be outstanding after this offering assumes no issuance of shares of common stock reserved for issuance under our equity incentive plans. As of March 31, 2014, an aggregate of 16,099,118 shares of common stock were reserved for future issuance under the Sabre Corporation 2014 Omnibus Incentive Compensation Plan (the “2014 Omnibus Plan”) which includes 2,599,118 shares of common stock that were available for future issuance under our prior equity plans. Additionally, the number of shares of common stock to be outstanding after this offering assumes:

| • | no exercise of performance-based stock options outstanding under our Sovereign MEIP plan. As of March 31, 2014 there were 724,337 performance-based stock options outstanding under this plan with a weighted average exercise price of $5.00; |

| • | no exercise of time-based stock options outstanding under our Sovereign MEIP plan. As of March 31, 2014 there were 15,352,970 time-based stock options outstanding under this plan with a weighted average exercise price of $4.80; |

| • | no exercise of time-based stock options outstanding under our Sovereign 2012 MEIP plan. As of March 31, 2014 there were 4,200,683 time-based stock options outstanding under this plan with a weighted average exercise price of $11.31; |

| • | no vesting and settlement of the 960,151 performance-based restricted stock units unvested and outstanding as of March 31, 2014 under our Sovereign 2012 MEIP plan; |

| • | no vesting and settlement of time-based restricted stock units outstanding as of March 31, 2014 under the Sovereign RSU Agreement, with a value equal to $520,000; |

| • | no vesting and settlement of the 140,000 restricted stock unit award, unvested and outstanding as of March 31, 2014; and |

| • | no exercise of time-based stock options or Tandem SARs under our TVL.com SOA or Travelocity Equity 2012 plans, respectively. It is expected that these plans will be terminated in connection and concurrent with this offering and all awards under these plans will be cancelled. |

In addition, except as otherwise noted, all information in this prospectus assumes the underwriters do not exercise their option to purchase additional shares.

16

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables present summary consolidated financial data for our business. You should read these tables along with “Risk Factors,” “Use of Proceeds,” “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Business” and our audited consolidated financial statements and the notes thereto included elsewhere in this prospectus.

The consolidated statements of operations data and consolidated statements of cash flow data for the years ended December 31, 2013, 2012 and 2011 and the consolidated balance sheet data as of December 31, 2013 and 2012 are derived from our audited consolidated financial statements and the notes thereto included elsewhere in this prospectus. The consolidated balance sheet data as of December 31, 2011 are derived from our unaudited consolidated financial statements and the notes thereto not included in this prospectus. The unaudited consolidated financial statements have been prepared on the same basis as our audited consolidated financial statements and, in the opinion of our management, reflect all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of this data.

The summary consolidated financial data presented below are not necessarily indicative of the results to be expected for any future period.

| Year Ended December 31, | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

| (Amounts in thousands) | ||||||||||||

Consolidated Statements of Operations Data(1): | ||||||||||||

Revenue | $ | 3,049,525 | $ | 2,974,364 | $ | 2,855,961 | ||||||

Cost of revenue | 1,904,850 | 1,819,235 | 1,736,041 | |||||||||

Selling, general and administrative | 792,929 | 1,188,248 | 806,435 | |||||||||

Impairment | 138,435 | 573,180 | 185,240 | |||||||||

Restructuring and other costs | 36,551 | — | — | |||||||||

Operating income (loss) | 176,760 | (606,299 | ) | 128,245 | ||||||||

Net loss attributable to Sabre Corporation | (100,494 | ) | (611,356 | ) | (66,074 | ) | ||||||

Net loss attributable to common shareholders | (137,198 | ) | (645,939 | ) | (98,653 | ) | ||||||

Basic and diluted loss per share attributable | (0.77 | ) | (3.65 | ) | (0.56 | ) | ||||||

Weighted average common shares outstanding: | 178,125 | 177,206 | 176,703 | |||||||||

Consolidated Statements of Cash Flows Data: | ||||||||||||

Cash provided by operating activities | $ | 157,188 | $ | 312,336 | $ | 356,444 | ||||||

Cash used in investing activities | (246,502 | ) | (236,034 | ) | (176,260 | ) | ||||||

Cash provided by (used in) financing activities | 262,172 | (25,120 | ) | (271,540 | ) | |||||||

Additions to property and equipment | 226,026 | 193,262 | 164,638 | |||||||||

Cash payments for interest | 255,620 | 264,990 | 184,449 | |||||||||

Other Financial Data: | ||||||||||||

Adjusted Gross Margin | $ | 1,383,809 | $ | 1,389,862 | $ | 1,330,514 | ||||||

Adjusted Net Income | 217,151 | 150,886 | 236,166 | |||||||||

Adjusted EBITDA | 791,323 | 786,629 | 720,163 | |||||||||

Adjusted Capital Expenditures | 284,840 | 271,805 | 223,747 | |||||||||

Adjusted Free Cash Flow | 160,923 | 285,221 | 233,586 | |||||||||

17

Table of Contents

| As of December 31, | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

| (Amounts in thousands) | ||||||||||||

Consolidated Balance Sheet Data | ||||||||||||

Cash and cash equivalents | $ | 308,236 | $ | 126,695 | $ | 58,350 | ||||||

Total assets | 4,755,708 | 4,711,245 | 5,252,780 | |||||||||

Long-term debt | 3,643,548 | 3,420,927 | 3,307,905 | |||||||||

Working capital deficit | (273,591 | ) | (428,569 | ) | (411,482 | ) | ||||||

Redeemable preferred stock | 634,843 | 598,139 | 563,557 | |||||||||

Noncontrolling interest | 508 | 88 | (18,693 | ) | ||||||||

Total stockholders’ equity (deficit) | (952,536 | ) | (876,875 | ) | (196,919 | ) | ||||||

Key Metrics | ||||||||||||

Travel Network | ||||||||||||

Direct Billable Bookings—Air | 314,275 | 326,175 | 328,200 | |||||||||

Direct Billable Bookings—Non-Air | 53,503 | 53,669 | 53,683 | |||||||||

Total Direct Billable Bookings | 367,778 | 379,844 | 381,883 | |||||||||

Airline Solutions Passengers Boarded | 478,088 | 405,420 | 364,420 | |||||||||

| (1) | Certain amounts previously reported in our December 31, 2012 and 2011 financial statements have been reclassified to conform to the December 31, 2013 presentation. See Note 2, Summary of Significant Accounting Policies—Reclassifications, to our audited consolidated financial statements included elsewhere in this prospectus. In June 2013, we sold certain assets of our Holiday Autos operations to a third party and in November 2013, we completed the closing of the remainder of the Holiday Autos operations such that it represented a discontinued operation. See Note 4, Discontinued Operations and Dispositions, to our audited consolidated financial statements included elsewhere in this prospectus. The impact on our revenue was a reduction of $65 million and $76 million for the years ended December 31, 2012 and 2011, respectively. The impact on our operating income was an increase of $12 million for the year ended December 31, 2012 and a reduction of less than $1 million for the year ended December 31, 2011. |

Non-GAAP Measures

The following table sets forth the reconciliation of Adjusted Gross Margin to operating income (loss), the most directly comparable GAAP measure:

| Year Ended December 31, | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

| (Amounts in thousands) | ||||||||||||

Operating income (loss) | $ | 176,760 | $ | (606,299 | ) | $ | 128,245 | |||||

Add back: | ||||||||||||

Selling, general and administrative | 792,929 | 1,188,248 | 806,435 | |||||||||

Impairment | 138,435 | 573,180 | 185,240 | |||||||||

Restructuring charges | 36,551 | — | — | |||||||||

Depreciation and amortization in cost of revenue(3) | 202,485 | 198,206 | 172,846 | |||||||||

Amortization of upfront incentive consideration(8) | 36,649 | 36,527 | 37,748 | |||||||||

|

|

|

|

|

| |||||||

Adjusted gross margin | $ | 1,383,809 | $ | 1,389,862 | $ | 1,330,514 | ||||||

|

|

|

|

|

| |||||||

18

Table of Contents

The following table sets forth the reconciliation of Adjusted Net Income and Adjusted EBITDA to net loss attributable to Sabre Corporation, the most directly comparable GAAP measure.

For Adjusted EBITDA by segment, see “Selected Historical Consolidated Financial Data—Non-GAAP Measures.”

| Year Ended December 31, | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

| (Amounts in thousands) | ||||||||||||

Reconciliation of net loss to Adjusted | ||||||||||||

Net loss attributable to Sabre Corporation | $ | (100,494 | ) | $ | (611,356 | ) | $ | (66,074 | ) | |||

Loss from discontinued operations, net of tax | 7,176 | 48,947 | 23,461 | |||||||||

Net income (loss) attributable to noncontrolling interests(1) | 2,863 | (59,317 | ) | (36,681 | ) | |||||||

|

|

|

|

|

| |||||||

Loss from continuing operations | (90,455 | ) | (621,726 | ) | (79,294 | ) | ||||||

Adjustments: | ||||||||||||

Impairment(2) | 138,435 | 596,980 | 185,240 | |||||||||

Acquisition related amortization expense(3a) | 143,765 | 162,517 | 162,312 | |||||||||

Gain on sale of business and assets | — | (25,850 | ) | — | ||||||||

Loss on extinguishment of debt | 12,181 | — | — | |||||||||

Other expense (income), net(4) | 6,724 | 1,385 | (1,156 | ) | ||||||||

Restructuring and other costs(5) | 59,052 | 6,776 | 12,986 | |||||||||

Litigation and taxes, including penalties(6) | 39,431 | 418,622 | 21,601 | |||||||||

Stock-based compensation | 9,086 | 9,834 | 7,334 | |||||||||

Management fees(7) | 8,761 | 7,769 | 7,191 | |||||||||

Tax impact of net income adjustments | (109,829 | ) | (405,421 | ) | (80,048 | ) | ||||||

|

|

|

|

|

| |||||||

Adjusted Net Income from continuing operations | 217,151 | 150,886 | 236,166 | |||||||||

Adjustments: | ||||||||||||

Depreciation and amortization of property and equipment(3b) | 131,483 | 135,561 | 122,640 | |||||||||

Amortization of capitalized implementation costs(3c) | 35,551 | 20,855 | 11,365 | |||||||||

Amortization of upfront incentive consideration(8) | 36,649 | 36,527 | 37,748 | |||||||||

Interest expense, net | 274,689 | 232,450 | 174,390 | |||||||||

Remaining (benefit) provision for income taxes | 95,800 | 210,350 | 137,854 | |||||||||

|

|

|

|

|

| |||||||

Adjusted EBITDA | $ | 791,323 | $ | 786,629 | $ | 720,163 | ||||||

|

|

|

|

|

| |||||||

The components of Adjusted Capital Expenditures are presented below:

| Year Ended December 31, | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

(Amounts in thousands) | ||||||||||||

Additions to property and equipment | $ | 226,026 | $ | 193,262 | $ | 164,638 | ||||||

Capitalized implementation costs | 58,814 | 78,543 | 59,109 | |||||||||

|

|

|

|

|

| |||||||

Adjusted capital expenditures | $ | 284,840 | $ | 271,805 | $ | 223,747 | ||||||

|

|

|

|

|

| |||||||

19

Table of Contents

The following tables present historical information from our statements of cash flows and sets forth the reconciliation of Adjusted Free Cash Flow to cash provided by operating activities, the most directly comparable GAAP measure:

| Year Ended December 31, | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

| (Amounts in thousands) | ||||||||||||

Cash provided by operating activities | $ | 157,188 | $ | 312,336 | $ | 356,444 | ||||||

Cash used in investing activities | (246,502 | ) | (236,034 | ) | (176,260 | ) | ||||||

Cash provided by (used in) financing activities | 262,172 | (25,120 | ) | (271,540 | ) | |||||||

| Year Ended December 31, | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

(Amounts in thousands) | ||||||||||||

Cash provided by operating activities | $ | 157,188 | $ | 312,336 | $ | 356,444 | ||||||

Adjustments: | ||||||||||||

Additions to property and equipment | (226,026 | ) | (193,262 | ) | (164,638 | ) | ||||||

Restructuring and other costs(5)(10) | 29,069 | 6,776 | 12,988 | |||||||||

Litigation settlement and tax payments for certain unusual items(6)(11) | 150,584 | 100,000 | — | |||||||||

Other litigation costs(6)(10) | 17,419 | 51,602 | 21,601 | |||||||||

Management fees(7)(10) | 8,761 | 7,769 | 7,191 | |||||||||

Travelocity Travel Supplier Liabilities and Accounts Payable as impacted by the Expedia SMA(9) | 23,928 | — | — | |||||||||

|

|

|

|

|

| |||||||

Adjusted Free Cash Flow | $ | 160,923 | $ | 285,221 | $ | 233,586 | ||||||

|

|

|

|

|

| |||||||