March 20, 2014

BY EDGAR AND OVERNIGHT COURIER

Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549-4628

| Attn: | H. Roger Schwall, Assistant Director |

| Ronald M. Winfrey |

| Re: | Glori Acquisition Corp. | |

Amendment No. 1 to Registration Statement on Form S-4 Filed February 21, 2014 File No. 333-193387 | ||

Amendment No. 3 to Schedule TO | ||

Amendment No. 3 to Schedule TO |

Ladies and Gentlemen:

Glori Acquisition Corp. (“Infinity”, the “Company”, “we”, “us” or “our”) hereby transmits our response to the letter received by us from the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”), dated March 12, 2014, regarding the filings referenced above. For your convenience, we have repeated below the Staff’s comments in bold and have followed each comment with the Company’s response.

Please note that references to specific paragraphs, pages, captioned sections and capitalized terms used but not defined in our responses herein are to Amendment No. 2 to the Form S-4 (the “Form S-4”) filed contemporaneously with this letter. We intend to file revisions to the two tender offer documents within the next few days in order to conform these filings with the revisions made to the Form S-4.

General

| 1. | We note your response to prior comment 4 that “[t]he warrants issuable pursuant to the Warrant Amendment will either be registered in the Form S-4 or exempt from registration as set forth in 4(b) above” with 4(b) providing for reliance on 4(a)(2) of the Securities Act of 1933. To the extent you decide to register the warrants issuable pursuant to the Warrant Amendment in this Form S-4, please explain to us how these shares are eligible to be registered given your statement that 4(a)(2) of the Securities Act is also available (i.e. the transaction did not involve a public offering). Please see Securities Act Forms Compliance and Disclosure Interpretations 225.10 available at our website. |

Response: We hereby advise the Staff that the issuance of the Insider Warrants pursuant to the Warrant Amendment will be exempt under Section 4(a)(2) of the Securities Act of 1933, as amended, and will not be registered in the Form S-4.

Summary of the Prospectus, page 1 Background of the Business Combination, page 5

| 2. | You disclose on page 2 that the Coke Field acquisition was in furtherance of Glori’s acquisition strategy. Please revise your disclosure in this section to specifically explain how, if at all, this factored into Infinity Corp.’s decision to acquire Glori. |

Response: We have revised the Form S-4 on page 9 in response to the Staff’s comment.

Risk Factors, page 22

| 3. | We note your response to prior comment 13 that you have revised the filing in response to this comment. Please revise your Summary Risk Factors section to quantify these conflicts of interests. We reissue prior comment 13 as it pertains to this point. |

Response: We have revised the Form S-4 on page 17 in response to the Staff’s comment.

The AERO System is currently useable only in oil reservoirs with specific characteristics, which limits the potential market for Glori’s services., page 24

| 4. | In response to prior comment 14, you refer to data belonging to Nehring Associates, University of Wyoming and Knowledge Reservoir as having been furnished to us. The thumb drive we received does not contain such files. Please furnish these items to us. |

Response: The Company is providing the Staff on a supplemental basis the Nehring Associates, Inc. data in the file entitled “Nehring Data.pdf”. Glori is also providing the Staff on a supplemental basis data from Knowledge Reservoir, an engineering consultant firm, and additional data from the University of Wyoming Enhanced Oil Recovery Institute in an Excel spreadsheet entitled “US-Sandstone Field K higher 50 mD.xlsx”.

Glori’s estimated proved reserves are based on many assumptions that may turn out to be inaccurate. The actual quantities and present value of Glori’s proved reserves may prove to be materially lower than it has estimated., page 30

| 5. | In our prior comment 15, we asked that you identify your third party engineer and file its report. On page 85, you state that the engineer’s report attributes to you proved reserves of13 MBOE effective December 31,2013. It appears this does not agree with the third party report in Exhibit 99.1. Please correct these items here and elsewhere in your document. |

Response: We have revised the Form S-4 on page 87 in response to the Staff’s comment.

| 6. | Our review of the third party report does not identify any reference to microbial recovery enhancement. If only conventional methods are being employed, please so state. Otherwise, please describe these microbial recovery methods if they are to be employed and comply with our prior comment 16(d) which, in part, requested you to “Include a line item listing for the components of the future production costs that are projected in the report. Please distinguish those costs associated with microbial recovery from costs required for conventional operations.” |

Response: In response to the Staff’s request, the Company is providing the Staff on a supplemental basis an Excel file entitled “2013 Etzold Well by Well Sumary.xlsx”, which provides a line item for the components of the future production costs projected in the report and distinguishes those costs associated with microbial recovery from costs required for conventional operations.

Material U.S. Federal Income Tax Consequences, page 39

| 7. | You disclose in this section that “Ellenoff Grossman & Schole LLP has rendered a tax opinion to Infinity Corp. to the effect that the discussion in this prospectus under the caption ‘Material U.S. Federal Income Tax Consequences,’ insofar as it purports to summarize United States federal income tax law, is accurate in all material respects.” Please revise this section and Exhibit 8.1 to clearly: |

| • | state that the disclosure in this section of the prospectus is the opinion of counsel; and |

| • | identify and articulate the opinion being rendered. |

Please see Section III.B.2 of Staff Legal Bulletin No. 19.

Response: We have revised the Form S-4 on pages 38, 39 and 43 in response to the Staff’s comment. We believe that the tax opinion in Exhibit 8.1 satisfies the requirements of a “short form” opinion as described in Section III.B.2 of Staff Legal Bulletin No. 19.

| 8. | You disclose in this section that several tax consequences are subject to uncertainty. For example, you disclose on page 41 that “[t]he Redomestication should, and is very likely to, qualify as a reorganization within the meaning of Section 368(a) for U.S. federal income tax purposes. However, due to the absence of guidance directly on how the provisions of Section 368(a) apply in the case of a merger of a corporation with no active business and only investment-type assets, this result is not entirely free from doubt.” Please provide risk factor disclosure setting forth this and other risks of uncertain tax treatment to investors. Please see Section III.C.4 of Staff Legal Bulletin No. 19. |

Response: We have revised the Form S-4 on pages 38 and 39 in response to the Staff’s comment.

Minimum Balance Requirement, page 53

Unaudited Condensed Combined Pro Forma Financial Statements, page 66

| 9. | We note that the terms associated with the PIPE investments shown in your two pro forma scenarios have changed to now indicate you may receive in exchange for the incremental shares to be issued either cash or “in kind, including debt instruments.” Please expand your disclosure to (i) clarify how the objective for the PIPE investment disclosed on page 4, “to ensure that Infinity Corp. meets the $25.0 million minimum balance requirement set forth in the Merger Agreement,” is accomplished if you accept non-cash consideration, (ii) explain the reason for the “in kind” provision, (iii) describe the terms that would be associated with any “in kind” payment that you receive, and (iv) state the basis for your pro forma adjustments reflecting all cash and no “in kind” consideration. |

Response: We have revised the Form S-4 on pages 4 and 55 in response to the Staff’s comment. In addition, we have clarified the adjustments in the pro formas related to the in kind consideration in footnotes 1, 6 and 20 on pages 70 and 72.

| 10. | We note that the number of shares disclosed in both balance sheet pro forma adjustment notes 13 on pages 68 and 70 (812,500 and 1,875,000 shares) do not agree with the number of shares you indicate would be issued under the PIPE Investment Agreement on page 66 (1,062,500 and 2,125,000 shares). Please revise as necessary to reconcile or clarify the reasons for these differences. Also disclose in tabular form how the $25 million minimum balance requirement correlates with your pro forma adjustments. |

Response: We have revised the Form S-4 in footnotes 6 and 16 on pages 70 and 72 in response to the Staff’s comment.

Glori Technology Services, page 76

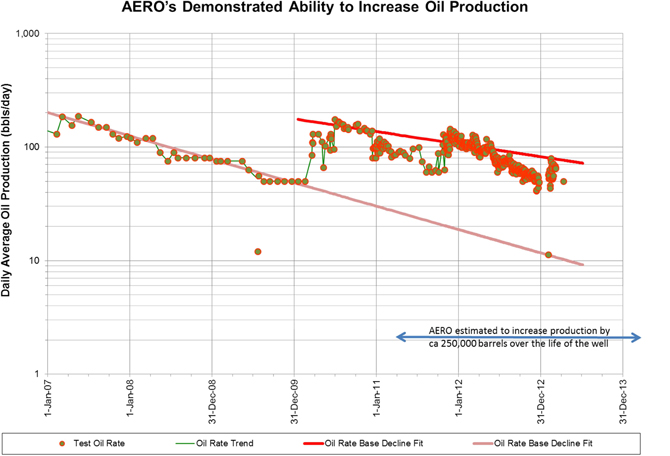

| 11. | Our prior comment 26, in part, asked that you furnish us with support for the statements that your operating costs are less than $6 per incremental barrel of oil. The spreadsheet that you furnished in response presented a cost estimate of about $6, but we note that your estimate included a cost reduction of $100,000 for your fee and used 80,000 barrels of incremental oil instead of the 40,000 BO presented on page 8 of the SPE paper SPE 144205-PP (Exhibit 99.2). We found no provision for contingencies which could be a 10%-20% increase. This appears to increase the unit production cost to about $ 17/BO ($600,602 x 1.15/40,000 BO). Please explain/justify your differences to us or amend your document to incorporate these cost increases. Address the fact that the cost estimate(s) are derived from the results for only 1 project. |

Response: In response to the Staff’s request, the Company is providing the Staff on a supplemental basis the following support for Glori’s cost estimate of approximately $6 per incremental barrel of oil:

Notes:

| 1. | Graph depicts results from one project. |

| 2. | The AERO System was deployed in April 2010. |

| 3. | Drop in production from early 2011 to end Q3 2011 caused by third party interference. Specifically, there was an introduction of corrosion inhibitor and scale inhibitor chemicals which caused corruption of the AERO System nutrients. |

| 4. | Project negative test initiated April 2012 and ended Dec 2012 (nutrient stopped in order to cause biological actions to die off in the reservoir). |

| 5. | In summer 2013, Glori conducted a workover of the well which included acidization. The project had a huge response, lifting production temporarily above 300 barrels of oil per day. |

Cost analysis per barrel of incremental oil:

The initial analysis presented in the previously submitted spreadsheet entitled “Unit economics.xlsx” was performed very early in the life of this project. Many of the assumptions were cautiously made because the process itself is very low cost. As a result, Glori considered it prudent to be conservative in calculation of costs.

The low cost application of microbial processes is further supported in the book Petroleum Microbiology, by Bernard Ollivier and Michel Magot, wherein in chapter 11, page 216, Dr. Michael McInerney (George Lynn Cross Research Professor, George Lynn Cross Endowed Professor, Applied Microbial Physiology at University of Oklahoma and former advisor to Glori Energy) states the following:

“Microbial processes have several unique advantages that may result in the development of economically attractive technologies. Microbial processes do not consume large amounts of energy as do thermal processes, nor do microbial processes depend upon the price of crude oil as many chemical processes do. Because Microbial growth occurs at exponential rates, it should be possible to produce large amounts of useful products rapidly from inexpensive and renewable resources. The results of several microbial field trials show that incremental oil can be produced for less than $3 per barrel (Brown et al., 2002; Bryant et al., 1993; Lazar et al., 1993; Strappa et al., 2004) indicating that microbial processes can be cost effective.”

Glori’s calculation in 2011 in the Excel spreadsheet entitled “Unit economics.xlsx” regarding estimated cost per barrel utilized 80,000 incremental barrels of oil as this was the estimate at the time of filing Glori’s Form S-1 in 2011. In order to remain conservative, Glori did not increase the potential recovery total based on subsequent results, which indicated that the project produced approximately 250,000 incremental barrels of oil.

Additionally, when the original estimates of cost were made, Glori’s calculation was a straight-line extrapolation of approximate costs from the early life of the project. Actual costs are less than the projected costs for the period in particular because the number of “hot-shot trips to the field” and “unscheduled responses” decreased to two per year. These unscheduled field visits were to trouble shoot or measure unplanned events. Once the project had run for approximately one year, these unscheduled field visits became unnecessary. Consequently, Glori believes the costs in the Excel spreadsheet entitled “Unit economics.xlsx” are conservative and does not believe it is necessary to add a contingent factor. Glori chose not to update these costs as the statement of costs of approximately $6 per incremental barrel of oil is still accurate.

With the benefit of three years of project data, we can now develop a more accurate estimate of actual cost per incremental barrel as follows:

Project economics

Based on actual costs

| Unit | Frequency | Cost | Annualized | Monthly | ||||||||||||||

| Nutrient | 12 gpd | 365 | $ | 2.25 | $ | 9 ,855 | $ | 821 | ||||||||||

| Nutrient transportation | 5 months supply | 2 2/5 | $ | 2 ,000 | $ | 4 ,800 | $ | 400 | ||||||||||

| QC visits | Visit | 6 | $ | 1 ,500 | $ | 9 ,000 | $ | 750 | ||||||||||

| Total | $ | 23,655 | $ | 1,971 | ||||||||||||||

| Field Unit Capital costs | 5 year amortize | 1 | 50000 | $ | 10,000 | $ | 833 | |||||||||||

| Total | $ | 33,655 | $ | 2,805 | ||||||||||||||

| Days | BOPD* | |||||||||||||||||

| Incremental barrels of oil | 365 | 40 | 14600 | Total BBLS | ||||||||||||||

| $ | 2.31 | per barrel | ||||||||||||||||

*40 barrels used as low end estimate of production uplift during active phases of the project

The current data indicates less than $3 per barrel of incremental oil using a very low estimate of incremental oil recovery, which supports Glori’s claim of costs of approximately $6 per incremental barrel of oil.

Finally, we have revised the Form S-4 on page 79 in response to the Staff’s comment to clarify that these cost estimates are based on one project.

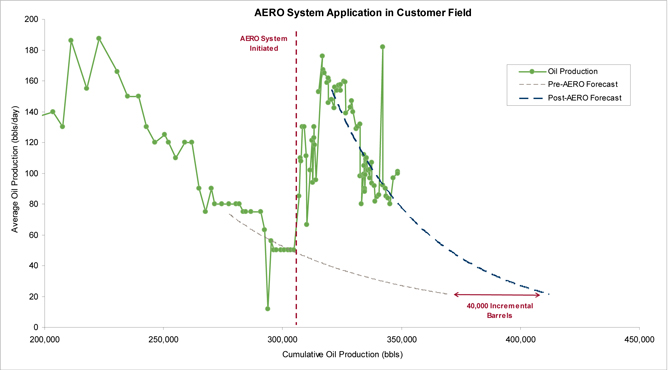

| 12. | On page 77, you state “Glori’s initial results on commercial field deployment indicate that the AERO System may recover up to 20% of the oil that remains trapped in a reservoir after the application of conventional oil recovery operations, and may improve total production rates by 60% to 100%.” We understand that the residual (immovable) oil saturation remaining after secondary recovery depletion in sandstone reservoirs can be of the order of 25-35% which makes the AERO incremental recovery 5% to 7% versus results the 9% to 12% recovery disclosed on page 76. Please explain how you arrived at the 9-12% figures. |

Response:

As set forth in the paper Glori published with Merit Energy Company and Statoil and presented at a July 2011 Society of Petroleum Engineers conference (the “SPE Paper”, which was previously provided as Exhibit 99.2 to the Form S-4), the following graph demonstrates the change in production rate as Glori’s AERO System became established at the affected production well in the pilot area. The figure was created by plotting production rate against cumulative production and shows a discontinuity where the AERO System becomes functional. This type of analysis is typically used to project ultimate recovery from the oil well by extrapolating trend lines. According to the SPE Paper, approximately 17,600 barrels of incremental oil had been produced from this project by Dec 31, 2010. The SPE Paper also states that the production rate increased 60% to 100% from the initial rate for this well and predicts an ultimate recovery potential of an additional 9-12% of original oil in place, or OOIP, in the pilot area of the field, or approximately 40,000 incremental barrels of oil over the life of the well. Secondary recovery for the field was forecast to yield ultimate recovery of approximately 27% OOIP, which would imply that the additional 9-12% OOIP recovered through the AERO System constitutes 18 - 23% of all oil recovered in the pilot area.

Generally, traditional oil production is carried out through primary or pressure-driven mechanisms followed by water injection, also known as waterflood, which increases reservoir pressure and displaces some of the oil remaining in the reservoir. However, approximately 60% of the OOIP typically remains trapped in the oil reservoir even after waterflooding, not 25% to 35% as referenced by the Staff. See, e.g.,http://en.wikipedia.org/wiki/Extraction_of_petroleum#cite_note-EUR-2;http://www.halliburton.com/en-US/ps/solutions/mature-fields/default.page?node-id=h8cyv98p. Assuming that the AERO System can recover approximately 9% to 12% of OOIP as set forth in the SPE Paper, the AERO System may recover up to 20% of the oil that remains trapped in a reservoir after the application of primary and waterflood recovery operations (12% of OOIP / 60% of OOIP = 20% of oil remaining after conventional oil recovery operations).

| 13. | Your response 27 presented a calculation of an “annual incremental production opportunity” utilizing AERO recovery - $10 billion - that incorporated the US daily oil production - 5 MMBOPD. However, on page 78, you state that the production from US waterflood projects is about 2.5 MMBOPD. Given that the AERO system is applicable only to waterflood operations, the $10 billion figure does not appear supportable. Please amend your document accordingly. |

Response: In response to the Staff’s comment, we are providing on a supplemental basis the calculation below supporting the disclosure that the annual incremental production opportunity utilizing the AERO System is greater than $10 billion in the United States: The United States produced approximately 5,000,000 BOPD from onshore fields, while approximately 2,500,000 BOPD are produced from onshore waterflood projects. Utilizing a 30% increase in onshore waterflood production rates based on application of the AERO System (compared to the approximate increase of 60% to 100% in the total production rate from May 2010 through June 2011 at Glori’s first commercial application of the AERO System), results in incremental production of approximately 750,000 BOPD (2,500,000 BOPD * .30). With approximately 46% of the onshore waterflood projects in the United States involving reservoirs composed of sandstone with permeability greater than 50 milli-darcies and with suitable water sources, the AERO System offers an incremental production opportunity of approximately 345,000 BOPD (750,000 BOPD * .46). Assuming an oil price of $80.00 per barrel over the course of a 365-day year results in a potential incremental production opportunity for onshore waterflood projects of $10,074,000,000 (345,000 BOPD * $80.00 * 365).

Milestones and Commercialization Strategy, page 82

| 14. | Your response to prior comment 32 presents tabular results of your sampling and testing with regard to the presence in reservoirs of microbes “capable of utilizing the residual hydrocarbon to grow, and in doing so create biomass as biofilms.” Please amend your document to disclose these results. |

Response: We have revised the Form S-4 on page 84 in response to the Staff’s comment.

Acquisition of the Etzold Field, page 85

| 15. | Please expand the discussion here to disclose that the production rate increase of 45% will have a duration limited by the amount of oil remaining in the reservoir after previous recovery operations. |

Response: We have revised the Form S-4 on page 87 in response to the Staff’s comment.

| 16. | We note that your phase 2 development of the Etzold field “did not prove commercially viable.” With reasonable detail, please explain to us reasons for the Etzold phase 2 production shortfall. Address how this result affects the reliability of your reserve estimates for phase 3. |

Response: We have revised the Form S-4 on page 87 in response to the Staff’s comment.

Management’s Discussion and Analysis of Financial Condition and Results of Operations of Glori. page 94

Pro Forma Oil and Natural Gas Production Prices and Production Costs, page 95

| 17. | We note the tabular presentation of “Average sales priceper Boe”. Please amend your document to disclose separately the sales prices for oil, natural gas and natural gas liquids. Please refer to Item 1204(b)(1) of Regulation S-K. |

Response: We have revised the Form S-4 on page 97 in response to the Staff’s comment.

Pro Forma Oil and Natural Gas Data, page 96

| 18. | On page 98, you present pro forma proved reserves as of September 30, 2013 for the Coke field acquisition - 2.2 MMBOE - that are about 20% lower than those - 2.8 MMBOE - from the in-house pro forma reserve report effective “l-January-2014” for the Coke Field/Petro-Hunt acquisition which you furnished us. On page 5 you present Coke Field acquisition proved reserves as 1.75 MMBOE. Please explain the differences in reserve figures to us and correct your document if appropriate. |

Response: We are now relying on the third party reserve report of William M. Cobb & Associates, Inc. for the Coke Field Assets (the “Cobb Report”) and for preparation of our pro forma estimates. We have revised the Form S-4 on page 5 and the pro form proved reserves on pages 100 to incorporate the proved reserve estimates set forth in the Cobb Report. The Cobb Report is being filed as exhibit 99.4 to the Form S-4.

| 19. | The in-house reserve report effective “1-January-2014” for your Coke Field acquisition uses prices - S85/BO and $2.50/MCFG - that do not appear to be the average of first day of the month for the prior 12 months as required by Rule 4-10(a)(22)(v) of Regulation S- X. Please ensure that disclosed proved reserve estimates, whether pro forma or not, incorporate prices that comply with Regulation S-X. You may disclose also reserves that are priced as described in Item 1202(b) of Regulation S-K. |

Response: We are now relying on the third party Cobb Report for the Coke Field Assets and for preparation of our pro forma estimates. Accordingly, we have revised the Form S-4 with respect to our proved reserve estimates on pages 87 and 100 to incorporate the proved reserve estimates set forth in the Cobb Report. The Cobb Report is being filed as exhibit 99.4 to the Form S-4.

| 20. | Page 81 of the in-house report indicates that the development plan for the proved undeveloped reserves will not be available until after the closing of Coke Field acquisition even though you have included them with the pro forma proved reserves in this filing. Your response to our prior comment 3(c) includes the statement that you do not have the necessary information to identify the 30 PUD locations and thus their nearby analogy wells. PUD reserves require that a development plan has been adopted and that there is demonstrated reasonable certainty of economic recovery. Please furnish us the development plan for these PUD reserves which should include: a base map for the PUD locations and their Sub-Clarksville analogies with production histories and RRC lease numbers; AFE or line item list of the projected PUD well costs; legible copies of Figures B1 and B2 from the in-house report. Alternatively, you may remove these volumes from your pro forma proved reserves. |

Response: We have revised the Form S-4 on page 100 and the related pro forma estimates to exclude the Sub Clarksville PUD from the Coke Field Assets PUD.

Liquidity and Capital Resources, page 105

| 21. | We note your response to prior comment 35. Please significantly expand this section to account for the Coke Fields acquisition and the impact of this acquisition on Glori’s liquidity, capital resources and results of operations. Please see Item 303(a) of Regulation S-K. |

Response: We have revised the Form S-4 on page 106 in response to the Staff’s comment. Specifically, we have revised the Liquidity and Capital Resources section of the Form S-4 to include the anticipated demands, commitments and capital expenditures associated with the Coke Field Acquisition as required by item 303(a) of Regulation S-K.

Certain Relationships and Related Transactions, page 136

| 22. | We note your response to prior comment 12. Please revise the tables in this section as of a recent practicable date to quantify the value of Infinity shares (including all accumulated shares paid as dividends) each beneficial holder will receive in connection with this transaction. For the Series C and C-l Preferred, please revise to also include an approximation of the preference anticipated to be received in conjunction with the consummation of this transaction. Please see Item 404(a) of Regulation S-K. |

Response: We have revised the Form S-4 on pages 5 and 21, and pages 138 through 141 in response to the Staff’s comment

Financial Statements, page F-l

| 23. | We understand from your response to prior comment 39 that you will update all of the historical and pro forma financial statements in your filing prior to the effective date of the registration statement. We will review these statements and related disclosures once they appear in the registration statement. |

Response: We have revised the Form S-4 to update all historical and pro forma financial statements to December 31, 2013.

Exhibit 99.1

| 24. | Please file third party reports for December 31, 2012 and 2013 (as referenced on page 96) that include the information required by Item 1202(a)(8) of Regulation S-K: (i) the purpose for which the report was prepared; (iv) the assumptions used in preparation of the report; (v) source and treatment of future capital costs. |

Response: We have revised the Form S-4 on page 98 to update the third party reserve engineer reports being utilized in preparing Glori’s reserve estimates. In addition, copies of the reserve reports of Collarini Associates and William M. Cobb and Associates, Inc. are being filed as exhibits 99.3 and 99.4, respectively.

| 25. | We note that the two Phase 1 producing wells’ projected cashflow analysis for 2013 has unit production cost of about $55/BO (=$358,000/6500 BO) compared to actual incurred costs (on page 95) of $100/B0 and $77/BO for 2012 and 2013, respectively. Please explain this difference to us. Include a line item list for the actual cost components and the projected cost components. |

Response: We have revised the Form S-4 on page 98 to state that Glori has reduced the number of producing wells being operated from two to one, which has reduced its direct production costs, primarily electricity cost. By removing this well, we have reduced costs per barrel greater than the loss of corresponding production.

We thank the Staff in advance for its consideration of the enclosed and the foregoing responses. Should you have any questions concerning the foregoing responses, please contact our counsel, Stuart Neuhauser, Esq. or Joshua Englard, Esq. at (212) 370-1300.

| Very truly yours, | ||

| Glori Acquisition Corp. | ||

| By: | /s/ Mark Chess | |

| Name: Mark Chess | ||

| Title: Chief Executive Officer | ||

| cc: | Ellenoff Grossman & Schole LLP |

Enclosure