UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-37725

ViewRay, Inc.

(Exact Name of Registrant as Specified in its Charter)

Delaware | 42-1777485 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

2 Thermo Fisher Way Oakwood Village, OH | 44146 |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (440) 703-3210

Securities registered pursuant to section 12(b) of the Act:

Title of Each Class | | Name of Each Exchange on Which Registered |

Common Stock, par value $0.01 | | The NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Exchange Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | | ☐ | | Accelerated filer | | ☐ |

| | | |

Non-accelerated filer | | ☐ (Do not check if a small reporting company) | | Small reporting company | | ☒ |

| | | | | | |

| | | | Emerging growth company | | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

At June 30, 2017, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $166,918,728 based on the closing sale price as reported on the Nasdaq Global Market. As of March 2, 2018, the registrant had 67,653,974 shares of common stock, $0.01 par value per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement to be delivered to stockholders in connection with the 2018 annual meeting of stockholders are incorporated by reference in Part III of this Form 10-K where indicated.

VIEWRAY, INC.

FORM 10-K

ANNUAL REPORT

TABLE OF CONTENTS

2

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, or this Report, contains forward-looking statements, including, without limitation, in the sections captioned “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and elsewhere. Any and all statements contained in this Report that are not statements of historical fact may be deemed forward-looking statements. Terms such as “may,” “might,” “would,” “should,” “could,” “project,” “estimate,” “pro forma,” “predict,” “potential,” “strategy,” “anticipate,” “attempt,” “develop,” “plan,” “help,” “believe,” “continue,” “intend,” “expect,” “future” and terms of similar import (including the negative of any of the foregoing) may be intended to identify forward-looking statements. However, not all forward-looking statements may contain one or more of these identifying terms. Forward-looking statements in this Report may include, without limitation, statements regarding: (i) the plans and objectives of management for future operations, including plans or objectives relating to the development of products; (ii) a projection of income (including income/loss), earnings (including earnings/loss) per share, capital expenditures, dividends, capital structure or other financial items; (iii) our future financial performance, including any such statement contained in a discussion and analysis of financial condition by management or in the results of operations included pursuant to the rules and regulations of the Securities and Exchange Commission, or the SEC; and (iv) the assumptions underlying or relating to any statement described in points (i), (ii) or (iii) above.

The forward-looking statements are not meant to predict or guarantee actual results, performance, events or circumstances and may not be realized because they are based upon our current projections, plans, objectives, beliefs, expectations, estimates and assumptions and are subject to a number of risks and uncertainties and other influences, many of which we have no control over. Actual results and the timing of certain events and circumstances may differ materially from those described by the forward-looking statements as a result of these risks and uncertainties. Factors that may influence or contribute to the inaccuracy of the forward-looking statements or cause actual results to differ materially from expected or desired results may include, without limitation:

| • | market acceptance of magnetic resonance imaging (“MRI”)-guided radiation therapy; |

| • | the benefits of MRI-guided radiation therapy; |

| • | our ability to successfully sell and market MRIdian in our existing and expanded geographies; |

| • | the performance of MRIdian in clinical settings; |

| • | competition from existing technologies or products or new technologies and products that may emerge; |

| • | the pricing and reimbursement of MRI-guided radiation therapy; |

| • | the implementation of our business model and strategic plans for our business and MRIdian; |

| • | the scope of protection we are able to establish and maintain for intellectual property rights covering MRIdian; |

| • | our ability to obtain regulatory approval in targeted markets for MRIdian; |

| • | estimates of our future revenue, expenses, capital requirements and our need for additional financing; |

| • | our financial performance; |

| • | our expectations related to the MRIdian linear accelerator technology, or MRIdian Linac; |

| • | developments relating to our competitors and the healthcare industry; and |

| • | other risks and uncertainties, including those listed under the section titled “Risk Factors.” |

Any forward-looking statements in this Report reflect our current views with respect to future events or to our future financial performance and involve known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements. Factors that may cause actual results to differ materially from current expectations include, among other things, those listed under Part II, Item 1A, titled “Risk Factors” and discussed elsewhere in this Report. Given these uncertainties, you are cautioned not to place

3

undue reliance on these forward-looking statements. We disclaim any obligation to update the forward-looking statements contained in this Report to reflect any new information or future events or circumstances or otherwise, except as required by law.

This Report also contains estimates, projections and other information concerning our industry, our business, and the markets for certain products, including data regarding the estimated size of those markets. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties and actual events or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained this industry, business, market and other data from reports, research surveys, studies and similar data prepared by market research firms and other third parties, industry, medical and general publications, government data and similar sources.

PART I

Item 1. BUSINESS

Company Overview

We design, manufacture and market the ViewRay MRIdian®, the only clinical MRI-guided radiation therapy system on the market. The MRIdian combines MRI and external-beam radiation therapy to simultaneously image and treat cancer patients. MRI is a broadly used imaging tool that has the ability to clearly differentiate between types of soft tissue. In contrast, X-ray or computed tomography (CT), the most commonly used imaging technologies in radiation therapy today, are often unable to distinguish soft tissues such as the tumor and critical organs. MRIdian integrates MRI technology, radiation delivery and our proprietary software to locate, target and track soft-tissue tumors, while radiation is delivered. These capabilities allow MRIdian to deliver radiation to the tumor more accurately, while reducing the radiation amount delivered to nearby healthy tissue, as compared to other radiation therapy treatments currently available. We believe this will lead to improved patient outcomes and reduced treatment-related side effects.

There are two generations of the MRIdian: the first generation MRIdian with Cobalt-60 based radiation beams and the second generation MRIdian Linac, with more advanced linear accelerator or ‘linac’ based radiation beams. ViewRay’s first generation MRIdian was a breakthrough that integrated high quality radiation therapy with simultaneous magnetic resonance imaging (MRI).

ViewRay first-generation MRIdian System with radiation powered by Cobalt-60 was cleared by the FDA in May 2012. By the end of 2016, the Company had shipped nine of these first generation MRIdian Systems. The MRIdian System demonstrated in clinical practice for the first time the benefits of MRI-guided radiation treatment for cancer, generating a large body of clinical evidence from its use in pancreatic, breast, lung, prostate and other cancers.

ViewRay’s second-generation system, the MRIdian Linac (Linear Accelerator) system received the Conformité Européene, or CE Mark in September 2016 and FDA 510k clearance in February 2017. The MRIdian Linac System has several advantages over the first generation MRIdian System. Linac-based radiation therapy delivery systems allow for higher dose, faster electronic variation of dose and very fast electronic beam activation and deactivation. Linear Accelerator technology obviates the need for the inspection, replacement, and disposal of Cobalt-60, and oversight from the U.S. Nuclear Regulatory Commission (or similar national agency in foreign countries). ViewRay solved two major long-standing problems to integrate a linac beam compactly with an MRI system: 1) linac radiofrequency interference with the operation of the MRI and 2) MRI magnetic interference with the operation of the linac.

• | Linacs utilize high-powered microwave generators similar to equipment used in radar at airports. These “radar stations” inside the linac create noise that can corrupt the delicate signals measured from the patient’s body to generate MR images. ViewRay solved this problem by introducing technology similar to that used in stealth aircraft. Stealth aircraft can hide from radar by using a coating that reflects and absorbs microwaves, thus preventing radar beams that strike the aircraft from bouncing back to the radar station. In a similar manner, ViewRay’s linac based system reflects and absorbs the output of the linac “radar station” to prevent it from interfering with the MRI, producing images as noise-free as MRI images with no integrated linac. |

4

• | MRIs utilize high-powered superconducting magnets that are required to image the patient’s tissues. Many linac components will not operate properly when placed close to or inside these strong magnetic fields. Close placement is necessary to produce a compact system that can fit in existing radiation therapy vaults, as the MRIdian linac does. ViewRay overcame this challenge by creating magnetic shielding shells that create voids in the magnetic field without significantly disturbing the magnetic field used for imaging. This allows the linac to operate on the MRIdian linac gantry as if there were no magnetic field present. |

In addition, ViewRay has applied the same double-focused multi-leaf collimator technology, originally designed for the first generation MRIdian System, to ViewRay’s MRIdian linac technology. This new high-resolution beam-shaping multi-leaf collimator (MLC), called the RayZR® MLC, when combined with the already sharp linac radiation source results in the sharpest linac beam commercially available in the industry. Therefore, we believe that ViewRay’s MRIdian linac technology could be transformative to the standard of care in radiation therapy.

Both generations of the MRIdian have received 510(k) marketing clearance from the US Food and Drug Administration, or FDA, and permission to affix the CE mark.

| • | We received initial 510(k) marketing clearance from the US Food and Drug Administration, or FDA, for our treatment planning and delivery software in January 2011. |

| • | We received 510(k) marketing clearance for MRIdian, with Cobalt-60 as the radiation source, in May 2012. We also received permission to affix the CE mark to MRIdian with Cobalt-60 in November 2014, allowing MRIdian with Cobalt-60 to be sold within the European Economic Area, or EEA. In August 2016, we received regulatory approval from the Japanese Ministry of Health, Labor and Welfare to market MRIdian with Cobalt-60 in Japan. In August 2016, we also received approval from the China Food and Drug Administration to market MRIdian with Cobalt-60 in China. |

| • | In September 2016, we received the CE mark for the second generation MRIdian Linac (with a linear accelerator as the radiation source) in the EEA. In February 2017, we received 510(k) clearance from the FDA to market MRIdian Linac. In June 2017, we received 510(k) clearance to market RayZR™, our high-resolution beam-shaping multi-leaf collimator, or MLC. We also received MRIdian Linac regulatory approval in Taiwan and Canada in August 2017, and in Israel in November 2017. We are also seeking required MRIdian Linac approvals in other countries such as Japan and China. |

Cancer is a leading cause of death globally and the second leading cause of death in the United States. Radiation therapy is a common method used to treat cancer that uses lethal doses of ionizing energy to damage genetic material in cells. Nearly two-thirds of all treated cancer patients in the United States will receive some form of radiation therapy during the course of their illness, according to estimates by the American Society for Radiation Oncology, or ASTRO. In 2016, IMV Medical Information Division, Inc., or IMV, reported that 97% of patients receiving radiation therapy in the United States were treated by a linear accelerator, or linac. The global linac market was estimated at approximately $4.6 billion in 2015 and was expected to grow to approximately $6.3 billion by 2020 according to a 2015 Markets and Markets report. IAEA Human Health Campus reported that there are over 11,500 linacs installed at over 7,800 centers worldwide. We currently estimate the annual market for linacs to be 1,000 units per year globally, the majority of which are replacement units. We believe the addressable market for MRIdian is the annual market for linacs due to MRIdian’s ability to treat a broad spectrum of disease sites. However, we believe that MRIdian may initially be used more frequently for complex cancer cases that may be difficult to treat on a standard linac due to the location of the tumor in relation to the surrounding organs at risk for radiation damage.

Despite the prevalence of MRI for diagnostic purposes and its ability to image soft tissue clearly, the radiation therapy industry has previously been unable to integrate MRI into external-beam radiation therapy systems successfully. Existing radiation therapy systems use X-ray-based imaging technologies, such as CT, which do not clearly differentiate between types of soft tissues or provide a fully accurate view of a tumor’s position in relation to critical organs. X-ray based imaging systems integrated into radiation delivery devices also often suffer from imaging artifacts caused by organ motion related to breathing, and artifacts related to air/fluid levels in the stomach and bowels. In addition, existing systems that offer imaging during the course of a treatment are limited by the rate at which they can image, due to the level of additional radiation to which they expose the patient. These constraints can make it difficult for a clinician to locate a soft tissue tumor accurately, track its motion in real-time or adapt treatment as internal anatomy changes. It is very difficult to both irradiate a tumor and minimize the amount of radiation exposure to critical organs, without the ability to see the exact location and shape of the tumor and

5

surrounding critical organs. If a tumor is insufficiently irradiated, it may not respond to the treatment, resulting in a higher rate of local tumor recurrence and lower probability of overall survival for the patient. Excess radiation exposure to healthy organs and other healthy soft tissues can lead to severe side effects, including organ failure, secondary cancers and in the most serious cases, even death. We believe that the MRIdian’s ability to see the exact location and shape of the tumor and surrounding critical organs will lead to improved patient outcomes and reduced treatment related side effects.

MRIdian is the first radiation therapy solution that enables simultaneous radiation treatment delivery and real-time MRI imaging of a patient’s internal anatomy. It generates high-quality images that differentiate between the targeted tumor, surrounding soft tissue and nearby critical organs. MRIdian also records the level of radiation dose that the treatment area has received, enabling physicians to adapt the prescription between treatments, as needed. We believe this improved visualization and accurate dose recording will enable better treatment, improve patient outcomes and reduce side effects. Key benefits to users and patients include: improved imaging and patient alignment; the ability to adapt the patient’s radiation treatments to changes while the patient is still on the treatment table, or “on-table adaptive treatment planning”; MRI-based motion management; and an accurate recording of the delivered radiation dose. Physicians have already used MRIdian to treat a broad spectrum of radiation therapy patients with more than 45 different types of cancer, as well as patients for whom radiation therapy was previously not an option.

We currently market MRIdian through a direct sales force in the United States and Canada and are developing a sales force to assist distributors in the rest of the world. At December 31, 2017, we had installed or delivered 15 MRIdian systems worldwide and had a backlog with total value of $203.6 million. We generated revenue of $34.0 million, $22.2 million, and $10.4 million for the years ended December 31, 2017, 2016 and 2015, respectively. We had net losses of $72.2 million, $50.6 million and $45.0 million for the years ended December 31, 2017, 2016 and 2015, respectively.

Corporate Information

We were incorporated under the laws of the state of Nevada on September 6, 2013 under the name “Mirax Corp”. Prior to the Merger and Split-Off (each as defined below), Mirax developed and supplied mobile communications accessories.

On July 8, 2015, we completed a 1.185763-for-1 forward stock split of our common stock in the form of a dividend. The result was that the 4,343,339 shares of common stock with a par value of $0.001 per share outstanding immediately prior to the stock split, became 5,150,176 shares of common stock, with a par value of $0.001 per share, outstanding immediately thereafter.

On July 15, 2015, we changed our name to ViewRay, Inc. by filing the Certificate of Amendment to our Articles of Incorporation. Additionally, on July 21, 2015, we changed our domicile from the State of Nevada to the State of Delaware by reincorporation, or the Conversion, and as a result of the Conversion, increased our authorized capital stock from 75,000,000 shares of common stock, par value $0.001 per share, to 300,000,000 shares of common stock, par value $0.01 per share and 10,000,000 shares of “blank check” preferred stock, par value $0.01 per share. Upon effectiveness of the Conversion, our corporate matters and affairs ceased to be governed by the Nevada Revised Statutes and became subject to the General Corporation Law of the State of Delaware. All share and per share numbers in this Report relating to our common stock have been adjusted to give effect to this forward stock split and the Conversion, unless otherwise stated. On July 23, 2015, we amended and restated our certificate of incorporation by filing the Amended and Restated Certificate of Incorporation with the Secretary of State of the State of Delaware and adopted the Amended and Restated Bylaws.

On July 23, 2015, our wholly-owned subsidiary, Vesuvius Acquisition Corp., a corporation formed in the State of Delaware on July 16, 2015, or the Acquisition Sub, merged with and into ViewRay Technologies, Inc. Pursuant to this transaction, or the Merger, ViewRay Technologies, Inc. was the surviving corporation and became our wholly-owned subsidiary. All of the outstanding capital stock of ViewRay Technologies, Inc. was converted into shares of our common stock, as described in more detail below.

Immediately prior to the closing of the Merger, under the terms of a split-off agreement, or the Split-Off Agreement, and a general release agreement, we transferred all of our pre-Merger operating assets and liabilities to our wholly-owned special-purpose subsidiary, Mirax Enterprise Corp., a Nevada corporation, or the Split-Off Subsidiary, formed on July 16, 2015. Thereafter, pursuant to the Split-Off Agreement, we transferred all of the outstanding

6

shares of capital stock of the Split-Off Subsidiary to our pre-Merger majority stockholders, and our former sole officer and director, in consideration of and in exchange for: (i) the surrender and cancellation of an aggregate of 4,150,171 shares of our common stock; and (ii) certain representations, covenants and indemnities, together referred to as the Split-Off.

As a result of the Merger and Split-Off, we discontinued our pre-Merger business, acquired the business of ViewRay Technologies, Inc. and continue the business operations of ViewRay Technologies, Inc. as a publicly-traded company under the name ViewRay, Inc.

On March 31, 2016, our shares of common stock commenced trading on the Nasdaq Global Market under the symbol “VRAY.” Prior to this time, our common stock was quoted on the OTC Markets, OTCQB tier of OTC Markets Group, Inc. under the same symbol.

As a result of the Merger we have ceased to be a “shell company” (as such term is defined in Rule 12b-2 under the Exchange Act).

As used in this Report henceforward, unless otherwise stated or the context clearly indicates otherwise, the terms the “Company,” the “Registrant,” “ViewRay,” “we,” “us” and “our” refer to ViewRay, Inc., incorporated in Delaware, after giving effect to the Merger and the Split-Off.

ViewRay, Inc. is the sole stockholder of ViewRay Technologies, Inc., which commenced operations as a Florida corporation in 2004, subsequently reincorporated in Delaware in in 2007, and changed its name to ViewRay Technologies, Inc. in July 2015.

Our authorized capital stock currently consists of 300,000,000 shares of common stock, and 10,000,000 shares of the preferred stock. Our common stock is listed on The NASDAQ Global Market under the symbol “VRAY.”

Our principal corporate headquarters are located at 2 Thermo Fisher Way, Oakwood Village, Ohio 44146. Our telephone number is (440) 703-3210. Our website address is www.viewray.com. (Any information on ViewRay’s website or which can be accessed through it, are not a part of this Annual Report on Form 10-K.)

Cancer and Radiation Therapy Market

Incidence of Cancer

Cancer is a leading cause of death globally and the second leading cause of death in the United States behind cardiovascular disease. According to the American Cancer Society, nearly 1.7 million people were expected to be diagnosed with cancer in the United States during 2016 and approximately 0.6 million were expected to die from cancer, accounting for nearly one of every four deaths. As a result of a growing and aging population, the World Health Organization’s, or WHO, Global Initiative for Cancer Registry Development estimates that the number of new cancer cases worldwide will grow from 14.1 million in 2008 to 19.3 million in 2025.

Cancer Therapy

The primary goal of cancer therapy is to kill cancerous tissues, while minimizing damage to healthy tissues. There are three main ways to treat cancer: surgery, chemotherapy and radiation therapy. Surgery attempts to remove the tumor from the body, while minimizing trauma to healthy tissue and preventing the spread or translocation of the disease to other parts of the body. Surgery is particularly effective because the surgeon can see the tumor and surrounding healthy tissue directly throughout the course of the procedure and can adapt his or her planned removal approach mid-procedure accordingly. Chemotherapy uses drugs to kill cancer cells. Unlike surgery, most forms of chemotherapy circulate throughout the patient’s body to reach cancer cells almost anywhere in the body systemically. Chemotherapy is most effective at destroying microscopic levels of disease. Radiation therapy is typically used as a local treatment, directed at a tumor and surrounding areas where microscopic cancerous cells are assumed to have spread. Radiation may be used as the primary treatment modality, or in combination with either chemotherapy or surgery or both. Radiation therapy works by damaging genetic material in cells and other cell components through interaction with ionizing energy. Effective radiation therapy balances destroying cancer cells with minimizing damage to normal cells. It can be used at high doses to ablate a tumor, an effect similar to surgery, or at moderate doses to target local microscopic disease, as is done with chemotherapy. Other, more recently developed ways of treating cancer, include hormone therapy and targeted therapy, such as immunotherapy.

7

Radiation Therapy

Radiation therapy has become widespread, with nearly two-thirds of all treated cancer patients in the United States receiving some form of radiation therapy during the course of their cancer treatments, according to estimates by ASTRO. For most cancer types treated with radiation therapy, at least 75% of the patients are treated with the intent to cure the cancer. For lung and brain cancers, that number is somewhat lower, with 59% of lung cancer patients and 50% of brain cancer patients being treated with the goal of curing cancer. The remainder of cases are treated with palliative intent to relieve pain or other tumor related symptoms. The type of radiation therapy delivered by linac or Cobalt 60 based devices is a non-invasive outpatient procedure with little or no recovery time and can be used on patients who are unable to undergo conventional surgery. According to IMV, 97% of patients receiving radiation therapy in the United States are treated using a linac.

Radiation is used to kill cancer cells primarily by damaging their DNA but can also kill healthy cells in the same way or cause them to become cancerous themselves. As a result, the goal of curative radiation therapy is to balance delivery of a sufficiently high dose of radiation to a tumor to kill the cancer cells while, at the same time, minimizing damage to healthy cells, particularly those in critical organs. Normal cells are better able to repair themselves after radiation than tumor cells, so doses of radiation are often fractionated, or delivered in separate sessions with rest periods in between. As a result, standard radiation therapy is often given once a day, five times a week, for one to nine weeks. According to a 2017 IMV report, patients made an estimated 20.2 million radiation therapy treatment visits in the United States from March 2016 to March 2017.

Radiation Therapy Equipment Market

According to a 2015 Markets and Markets report, the global linac market was estimated at approximately $4.6 billion in 2015 and was expected to grow to approximately $6.3 billion by 2020. According to IAEA Human Health Campus, there are more than 11,500 linacs installed at over 7,800 centers worldwide. In the United States, there are approximately 3,600 linacs installed at approximately 2,100 centers. The annual market for linacs is estimated to be 1,000 units per year globally, the majority of which are replacements for older machines.

In the radiation therapy market, new technologies have historically been adopted at a rapid rate. According to IMV, the percentage of centers performing intensity modulated radiation therapy, or IMRT, grew from 30% in 2002 to 96% in 2012. The percentage of sites utilizing image-guided radiation therapy, or IGRT, grew even more quickly: from 15% in 2004 to 83% in 2012. The majority of IGRT procedures use on-board X-ray systems. As leading cancer centers adopt and study MRI-guided radiation therapy, we believe that our next-generation linac based MRI system will also follow a rapid adoption curve in the broader linac replacement market.

Radiation Therapy Treatment Process

Following diagnosis of the disease state, radiation treatment generally consists of the following steps:

| • | Imaging and tumor contouring. To design the treatment plan, physicians obtain initial images of the tumor. This is done most commonly using a CT scan, often supplemented by an MRI, a positron emission tomography, or PET, scan, or both. These images, also known as simulation scans, are then imported into a treatment planning software system and aligned or “registered” to each other. Based on clinical experience, a physician will manually delineate, or “draw”, specific areas on the aligned images to define the location and extent of the tumor highlighting the following: |

| • | Gross tumor volume, or GTV, a volumetric region encompassing the visible tumor. |

| • | Clinical target volume, or CTV, is the GTV plus a larger, surrounding area where cancer cells are already likely to have spread. |

| • | Planning target volume, or PTV, is the CTV plus a further enlarged area to allow for: inexact imaging; patient movement during treatment; tumor movement between planning and treatment; and organ motion caused by breathing. The PTV margin unavoidably includes only normal, healthy tissues and may be many times larger than the CTV. While the PTV margin is necessary to reduce the risk of local tumor recurrence, it does increase the risk of radiation damage to healthy tissue and critical organs. |

8

| • | Treatment planning and dose prescription. Once the clinician has a three-dimensional map of the tumor, surrounding healthy tissues and nearby critical organs, a physician determines a treatment plan using one of the methods below. Creation of these plans typically takes days but can require up to several weeks. A typical curative radiation therapy treatment dose will be delivered over the course of several weeks with 10 to 43 radiation therapy sessions, referred to as fractions, lasting from a few minutes to an hour or more depending on the treatment plan. |

| • | 3D-CRT planning. Using a method called three-dimensional conformal radiation therapy, or 3D-CRT, a clinician will choose both the beam angles and shapes the machine will use to direct the radiation beam towards the tumor, and the time period that each beam will be delivered. A computer will then calculate a prediction of the radiation dose delivered, and the radiation planning team will adjust the treatment plan on an iterative basis to arrive at a clinically acceptable radiation dose plan. |

| • | IMRT planning. Using a method called intensity modulated radiation therapy, or IMRT, a physician will use computer software that calculates hundreds or even thousands of beamlets (small radiation beams) to optimize a treatment plan in order to achieve a more precise dose distribution than 3D-CRT. IMRT plans often allow better radiation coverage of tumors, while simultaneously sparing more healthy tissues from high radiation doses. In select cancers, IMRT has been shown to result in better patient outcomes than 3D-CRT. |

| • | SRS and SBRT planning. Stereotactic radiosurgery, or SRS, and stereotactic body radiation therapy, or SBRT, are methods of delivery using 3D-CRT or IMRT, in a reduced number of sessions. SRS and SBRT deliver precisely targeted radiation in usually one to five fractions delivered in one treatment session on the same day. SRS is frequently used in brain and spine applications, while SBRT is used most often in the rest of the body, and has been shown to be particularly effective in early-stage lung cancer. |

| • | Alignment. Just prior to radiation delivery, clinicians typically take further images to assist with alignment of the patient’s tumor to the radiation beam. Most systems use a form of on-board CT, called “cone-beam CT” or “CBCT” to create this image and then move the patient so that the tumor’s location that day matches the prior planning position. However, cone beam CT may suffer from poor soft-tissue contrast, motion artifacts and may use a higher radiation dose than that available from the types of CT used for diagnosis purposes. Cumulatively, when applied every day prior to radiation delivery, the radiation exposure from CBCT (or other x-ray based image-guidance technologies) may increase the clinically relevant additional radiation dose delivered to the patient and may cause clinicians to adjust the intended radiation treatment plan. |

A less commonly used imaging technology is fluoroscopy, a real-time 2D X-ray system. However, fluoroscopy can expose a patient to even higher doses of radiation than does cone-beam CT.

Because of the limited soft tissue contrast of X-ray-based imaging, clinicians often use registration or fiducial markers to assist with alignment of the patient’s tumor to the treatment beams, such as the patient’s visible bone structures near the tumor or surgically implanted markers which identify the tumor’s location. To minimize motion due to breathing or other normal body activity, patients may also be immobilized by restraining devices, such as abdominal compression or by “respiratory control,” techniques such as cameras that monitory a patient’s breathing during treatments or by asking the patient not to breathe at certain intervals during the treatment delivery. To account for breathing and other body motions during treatment, specific trackers may be used, through a technique known as “4D radiation therapy.

| • | Delivery. Following an assessment of the tumor location relative to the radiation beam geometry, treatment is initiated, and radiation is delivered to the patient. In some cases, additional 2D X-ray images are taken intermittently or registration makers are monitored during treatment to try to account for tumor movement. However, there is no ability for physicians or other clinicians to see the tumor’s location throughout the entire radiation treatment delivery with traditional linacs. |

9

| • | Review. After a treatment session, the physician will review data gathered from the linac system to validate that the treatment it is proceeding according to his or her treatment plan. But, traditional linac systems have no ability to record the actual dose that was delivered to the tumor and nearby critical structures. In certain rare types of cancers, where the tumor is visible simply by looking at the patient without imaging equipment, the physician may decide to adjust the treatment plan during the course of the patient’s overall treatment. However, revising a treatment plan may take several days and will delay completion of the patient’s overall treatment. |

Limitations of Traditional Radiation Therapy

Limitations with traditional radiation therapy result from imaging technologies that make accurate visualization of a tumor and its relation to critical organs difficult or impossible during the treatment delivery. Most current traditional systems take images of the tumor before and after treatments, but, none do so continuously during the treatments in real time. As a result, treatments may not be delivered with the precision assumed by the physician and may not result in the necessary efficacy or reduction in local tumor recurrence. Also, healthy tissues may be exposed to radiation levels different from those predicted by the planning system and can result in patient injury.

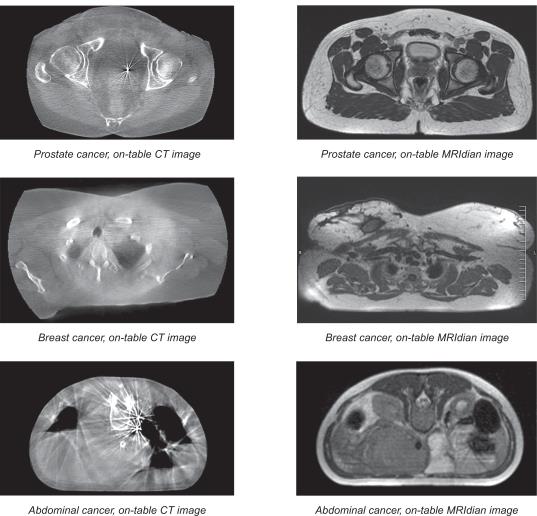

| • | Inability to accurately locate a tumor for treatment alignment. To locate a tumor, current radiation therapy systems rely on CT scans taken while the patient is on the delivery unit treatment table, or “on-table.” Because it is difficult for differentiate between the tumor and nearby soft tissues with CT images, clinicians use surrogate registration markers, including existing bone structures, external marks and surgically implanted fiducials, to align a patient’s tumor to the treatment beams prior to commencing treatment. |

10

| • | Comparison of On-Table CT Images to On-Table MRIdian Images |

11

However, the spatial relationship between tumors and the registration markers used to locate them often changes between the time of the patient’s initial imaging and the time of his or her first treatment session. This is particularly true for tumors which are located in soft tissue. By relying on a marker as a proxy for the tumor location, rather than on the tumor itself, clinicians risk missing the tumor when they deliver radiation beams into the patient’s body. In addition, placement of surgically implanted fiducial markers comes with inherent risks: the procedures are invasive; there is a risk of pain, infection, bleeding and lung collapse; and fiducials may change location and even migrate inside the body. Despite placement of fiducials, physicians are often unable to track changes in tumor shape. Also, fiducials made of dense metals, such as gold, may cause artifacts which interfere with imaging.

| • | Inability to adapt treatment on-table. A physician designs a treatment plan and dose prescription based on images that are captured days or even weeks prior to initiation of radiation therapy. Creating a treatment plan can take up to several weeks in complex cases, and treatment itself can take up to nine weeks. However, during the course of therapy, tumors often change size, orientation or shape, and patient anatomy can change for reasons such as weight loss or gain. These changes can alter the planned radiation exposure to both the targeted regions and nearby healthy organs; this has the potential to increase the risk of local tumor recurrence and to reduce the safety of the radiation delivery. Adjusting for these changes on conventional delivery units requires re-planning, which includes getting new patient images needed to create a new treatment plan. This process may take several days and is highly resource intensive. As a result of these limitations, re-planning is infrequently performed. |

Due to limitations in imaging technologies, physicians may actually be unaware of changes in the tumor and surrounding anatomy. Consequently, they may continue to administer radiation dose according to the original treatment plan, without realizing its potential to reduce the effectiveness of the tumor treatment and to increase the risk of patient injury.

| • | Inability to track tumor and organ motion accurately. In addition to the difficulty of locating a tumor accurately in a patient’s body at the time treatment begins, a further challenge is accounting for ongoing tumor movement that takes place during treatment. Tumors have been shown to move multiple centimeters relative to surrogate registration markers over the course of only a few seconds. Breathing and other normal bodily functions, such as changes in the bladder or bowel during treatment, can cause significant tumor motion. Although physicians use internal markers, external cameras and blocks placed on the patients’ body to track respiratory and other motion, they are typically unable to track the tumor itself. As a result, physicians usually enlarge the total region to be irradiated. This limitation increases the probability of missing the targeted treatment area and exposing healthy tissues to unnecessary radiation. |

| • | Inability to record cumulative radiation delivered. In order to determine treatment effectiveness, it is important to track how much radiation has been delivered to a tumor and its surrounding healthy tissue. Currently, there are no methods to record the actual dose of radiation that was delivered to the tumor and nearby critical structures. Therefore, physicians must assume that the radiation is delivered according to plan, rather than making decisions based on actual radiation dose delivered. |

Each of these limitations increases the risk of missing a tumor and hitting healthy tissue during treatment. If a tumor is insufficiently irradiated, it may not respond to treatment, resulting in a greater probability of local tumor recurrence and reduced overall survival for the patient. The ability to avoid irradiating healthy tissue has been shown to reduce side effects. If healthy tissues, particularly critical organs, are irradiated, the side effects can be severe, including: scarring of lung tissue; fibrosis and cardiotoxicity in lung and breast cancers; incontinence and sexual dysfunction in pelvic and prostate cancers; infertility in pediatric cancers; memory loss, seizures and necrosis in brain cancer; secondary cancers, and in serious cases, death.

Although MR technology is an imaging tool broadly used to differentiate between types of soft tissue in diagnostic settings, MR technology had not been available in the radiation treatment delivery room before the launch of ViewRay’s MRIdian System. In the past, MR was not used with radiation therapy because the technologies interfered with each other: the magnetic field generated by an MRI interfered with the linac beam, while the radiofrequencies produced by the linac distorted the MR images. Current forms of CT have improved over time, but issues with radiation dose and image quality limit the utility of these technologies. Fluoroscopy and cone-beam CT

12

involve the use of X-rays, a form of ionizing radiation, and pose an increased risk of radiation-induced cancer to the patient.

Our Solution

We developed MRIdian to address the key limitations of existing external-beam radiation therapy technologies. MRIdian employs MRI-based technology to provide real-time imaging that clearly defines the targeted tumor from the surrounding soft tissue and other critical organs, both before and during radiation treatment delivery. MRIdian also allows physicians to record the level of radiation exposure that the tumor has received and adapt the prescription between treatment fractions as needed. We believe this combination of enhanced visualization and accurate dose recording will significantly improve the safety and efficacy of radiation therapy, leading to better outcomes for patients suffering from cancer.

We believe that MRIdian provides the following clinical and commercial benefits to physicians, hospitals and patients:

| • | Improved tumor visibility and patient alignment. The soft-tissue contrast of MRIdian’s on-board MRI enables clinicians to locate, target and track the tumor and healthy tissues and more accurately align a patient to the treatment beams without the use of X-ray, CT or surrogate registration markers. If the clinician prefers, the software has the ability to map the patient’s soft tissue anatomy each treatment session in less than one minute, and clinicians can use that information to align the patient. |

| • | On-table adaptive planning. Due to changes in tumor shape or the patient’s internal anatomy, the clinician may be unable to obtain an optimal setup of the target location during image-guidance using CT-based systems while a patient is on the treatment table. Further, a nearby organ at risk for radiation damage may be exposed to higher radiation doses than anticipated. Using an MR image captured at the beginning of each therapy session, MRIdian software enables clinicians to map each patient’s soft tissue anatomy in 3D. The software also allows for the calculation of the dose that would be delivered to the radiation target and organs at risk using the current treatment plan. If the predicted radiation exposure is not clinically acceptable to the physician, the system provides software tools for tumor and organ at risk re-contouring based on the setup MR-images. The MRIdian system also provides the ability to recalculate the intended radiation dose and adapt the plan to the changed tumor shape or location, and overall anatomy for the respective day of treatment. Utilizing our proprietary algorithm and software, adaptive re-planning can be done with the patient still “on table”. Also, integral to the adaptive planning process are quality assurance protocols, or QA, to enhance the safety of adapted radiation dose delivery. Users in the United States are currently generally reimbursed for the additional time and effort spent by their physicians, medical physicists, dosimetrists and therapists for on-table adaptive planning. When medically necessary, we believe hospitals and physicians will continue to receive additional reimbursement when they perform adaptive radiation therapy. |

| • | Ability to track tumors and manage patient motion. MRIdian can capture dedicated or multiple soft-tissue imaging planes concurrently during the radiation treatment delivery, refreshing the image multiple times per second. This real-time imaging enables physicians to see, watch and track the movement of the tumor and its surrounding healthy tissue directly; they do not need to rely on proxies such as registration markers, existing bones or surgically implanted fiducials. If a tumor or critical organ moves beyond a physician’s defined boundary or allowable range of motion (as individually defined in our dedicated tracking and gating software), MRIdian will automatically detect this and pause the treatment beam. This automatic beam control becomes especially important in the situations where a tumor may be in close proximity to a critical organ, such as the heart during lung and breast cancer treatments, or the rectum during prostate cancer treatments. This ability to actually see the tumor location continuously throughout radiation delivery has enabled physicians to treat patients with greater confidence, including patients who would not have been given radiation therapy for their cancers previously. |

13

| • | Record and evaluate the delivered dose. Using our proprietary algorithm and advanced MR imaging, MRIdian calculates the dose delivered after each treatment, enabling the physician to review and re-optimize the patient’s treatment session, if needed. In addition, MRIdian can utilize diagnostic CT images that are fused with the MR images at each treatment in order to more accurately calculate dose. MRIdian also captures and records a video, known as a MRIdian Movie™, of the delivered treatments, which can be evaluated by the physician or shared with patients. |

| • | Fits into existing treatment paradigms and workflow. MRIdian can treat a broad spectrum of radiation therapy indications and disease sites, because it can perform 3D-CRT, IMRT, IGRT, SBRT and SRS. MRIdian treatments are supported by existing radiation therapy reimbursement codes. In addition, MRIdian fits inside most standard radiation therapy vaults without the need for significant construction costs such as wall or ceiling removal to enable it to be placed inside. In addition, we believe MRIdian’s increased tumor target accuracy will allow physicians to treat patients with higher radiation doses over fewer treatment fractions; this potentially enables the clinic to treat more patients each day and with greater overall efficiency, or patient throughput. |

We believe the ability to image with MRI and treat cancer patients with radiation simultaneously will lead to improved patient outcomes.

Our Strategy

Our objective is to make MRI-guided radiation delivery the standard of care for radiation therapy. To achieve this goal, we intend to do the following:

| • | Invest in Commercialization of the MRIdian Linac. The public response to the clinical release of the second generation MRIdian Linac has been positive as it builds upon and improves the capabilities of the first generation MRIdian. We believe the MRIdian Linac has the potential to broaden our addressable market, accelerate our sales cycle, reduce our backlog conversion time and improve our gross margins. We intend to: |

| • | Broaden awareness of MRIdian’s capabilities and clinical benefits to expand our share of the radiation therapy market. We intend to continue to educate radiation oncologists, medical physicists and radiation oncology administrators about the capabilities and resulting benefits of MRIdian over traditional radiation therapy systems. In order to drive awareness and adoption, we also intend to support the publication of clinical and scientific data and analysis, work with key opinion leaders, present at leading academic conferences and engage in outreach at leading hospitals worldwide. We also plan to leverage our existing customer network as a reference for new potential users to experience our technology in-use in the clinical setting. |

| • | Target top-tier hospitals in initial global sales efforts, followed by their community practice networks. We intend to market MRIdian to a broad range of customers worldwide, including university research and teaching hospitals, private practices, community hospitals, government institutions and freestanding cancer centers. We are focusing initially on the leading hospitals worldwide which are typically early adopters of best-in-class technology, such as MRIdian, and are able to influence and promote adoption by other centers both locally and globally. We plan to continue to work with these institutions to promote broader market awareness of the benefits of MRI-guided radiation therapy and then expand into the community practice networks that many of these leading centers have developed. |

| • | Commercialize MRIdian with a targeted sales force in the United States and through a sales force-assisted distribution network in international markets. We market MRIdian through a combination of direct sales and distributors. We are expanding our sales force for the United States and Canada and are developing a sales force to assist distributors in international markets. We intend to continue to expand our presence in key markets to capitalize on the growing international opportunity for MRIdian. |

14

| • | Perform Clinical Trials to Develop Evidence Supporting the Value of the MRIdian. We have launched the ViewRay Clinical Cooperative Think Tank (C2T2), a group of MRIdian clinical users and customers that are gathering evidence to support MR-guided radiation therapy. ViewRay's C2T2 comprises clinicians from leading institutions around the world who are focused on evidence gathering to support MR-guided radiation therapy. This group includes: |

| • | Dana-Farber/Brigham and Women's Cancer Center in Boston |

| • | Henry Ford Cancer Institute, Detroit |

| • | Institut du Cancer de Montpellier, France |

| • | Institut Paoli Calmettes, Marseille, France |

| • | Loyola Center for Cancer Care and Research at Palos Health South Campus in Illinois |

| • | Moffitt Cancer Center in Tampa, Florida |

| • | Miami Cancer Institute, Baptist Health South Florida |

| • | National Cancer Center (NCC) in Tokyo, Japan |

| • | NewYork-Presbyterian Hospital |

| • | Orlando Health UF Health Cancer Center |

| • | Policlinico Agostino Gemelli, Universita Cattolica del Sacro Cuore, Gemelli ART in Rome, Italy |

| • | Seoul National University Hospital (SNUH) in Seoul, South Korea |

| • | Sylvester Comprehensive Cancer Center, UHealth - University of Miami Health System |

| • | University of California, Los Angeles Health System and Jonsson Comprehensive Cancer Center |

| • | University of Heidelberg, Germany |

| • | University of Wisconsin Carbone Cancer Center in Madison |

| • | VU University Medical Center in Amsterdam, Netherlands |

| • | Washington University and Siteman Cancer Center at Barnes-Jewish Hospital, St. Louis |

At the inaugural meeting of the C2T2 on September 23, 2017, participants formalized the group's first key initiative – a multi-center, prospective, single-arm clinical trial focused on locally advanced unresectable pancreatic cancer. Pancreatic cancer presents considerable radiation targeting challenges given the known limitations of conventional CT image guidance. The novel abilities provided by live MRI guidance combined with daily online treatment adaptation have enabled a new approach in pancreatic cancer therapy. Through this trial the group looks to explore new opportunities to improve survival and quality of life for this deadly disease.

| • | Maintain our competitive lead in MRI-guided radiation therapy through continued innovation. We plan to continue to invest in our technology to maintain our leadership position in the emerging MRI-guided radiation therapy market. We intend to develop and introduce enhancements to the system and software to provide improved capabilities for MRIdian users and patients. In addition, we plan to explore potential benefits of integrating our MRI technology with alternative beam technologies. We believe we have a strong intellectual property portfolio that covers the MRIdian, as well as its critical design elements and key aspects of its subsystem and components. |

15

| • | Continue to work with leading hospitals to optimize efficiency and patient throughput. We strive to maximize the efficiency and effectiveness of the MRIdian system for our customers. We plan to continue to work closely with key opinion leaders, clinicians and hospitals in a proactive manner to determine how best to refine and improve MRIdian’s features, optimize clinical workflow and maximize patient throughput while incorporating our advanced features. |

| • | Drive cost reductions in the design and manufacture of MRIdian and improve our margins. We plan to continue to explore ways to bring down our cost of goods to improve margins for MRIdian. |

The MRIdian System

The MRIdian is comprised of four major components, (i) the MRI system, (ii) the radiation delivery system, (iii) integrated treatment planning and delivery software and (iv) a safety and control system.

| | |

MRIdian Cobalt-60 | | MRIdian Linac |

| |

| |

|

MRI System

The MRI system is the component of MRIdian that captures soft tissue images of the patient’s body. To address the technical complications that arise from combining an MRI with an external-beam radiation delivery unit, we have designed a proprietary split superconducting magnet that will allow radiation doses to be delivered through a central gap, which eliminates MRI components from the path of the beam. Our MRI system captures and displays live, high-quality images in one plane, four times per second or in three planes, two times per second. These real-time images automatically track selected structures and control radiation treatment beam delivery.

We have engineered our MRI system to be able to produce clear images using a mid-field strength 0.35 Tesla magnet, which enables us to avoid image and radiation dose distortions that result when higher field strength magnets are used. In addition, MRIdian’s 0.35 Tesla field strength prevents over-heating of the patient during uninterrupted imaging, which could occur when a higher field strength magnet is used for fast imaging during radiation delivery. Over-heating can require interruption or termination of the imaging or of the overall treatment.

16

MRI System

MRIdian Radiation Delivery System

In the first-generation MRIdian, radiation is delivered from three Cobalt-60 radiation therapy heads symmetrically mounted on a rotating ring gantry, providing full 360-degree coverage and simultaneous dose delivery. Each head is equipped with a double-focused multi-leaf collimator designed to overcome the wide-beam edge of previous-generation Cobalt-60 systems and to shape the beam for precision radiation therapy treatments. It allows the delivery of treatment plans for 3D-CRT, IMRT and SBRT that are clinically equivalent to those produced on the most advanced linear accelerators available today. Stereotactic procedures are possible with a positioning accuracy of less than one millimeter. Cobalt-60 was used in the first-generation devices because it does not create any radio frequency, which interferes with the MRI.

MRIdian Linear Accelerator Technology Radiation Delivery System

In the second generation MRIdian Linac, we developed solutions to two long-standing problems that had prevented compact integration of a linac beam with an MRI system: 1) linac radiofrequency interference with the operation of the MRI; and 2) MRI magnetic interference with the operation of the linac. First, linacs utilize high-powered microwave generators similar to equipment used in radar at airports. These “radar stations” inside the linac create radiofrequency emissions, or “noise” that can corrupt the delicate signals measured from the patient’s body to generate MR images. ViewRay solved this problem by introducing technology similar to that used in stealth aircraft. Airplanes built with stealth technology can hide from radar by using a coating that absorbs microwaves, thus preventing radar beams that strike the aircraft from bouncing back to the radar station. In a similar manner, we absorb the output of the linac “radar station” to hide it from the MRI, producing images as noise-free as those created without an integrated linac.

Second, MRIs utilize high-powered superconducting magnets required to image the patient’s tissues that must be placed close to the linac components used for radiation therapy. But many linac components will not operate properly when placed close to or inside these strong magnetic fields. ViewRay overcame this challenge by creating magnetic shielding shells that create voids in the magnetic field, without significantly disturbing the magnetic field used for imaging. This allows the linac to operate on the MRIdian gantry as if there were no magnetic field present. MRIdian Linac uses the same split-magnet MRI system used in the first generation MRIdian system. It is specifically designed to fit in standard radiotherapy vaults so that customers do not need to build new vaults in order to replace an X-ray guided linear accelerator with a MRIdian. Existing MRIdian systems currently in use can be upgraded to the MRIdian Linac in the field.

Both MRIdian and MRIdian Linac can provide continuous MR based soft-tissue imaging during radiation beam delivery. Being able to constantly see both the tumor and surrounding organs means physicians can accurately align the tumor to the treatment beams, adapt or reshape the treatment volume to accommodate changes in the shape and

17

location of the tumor and healthy tissues, and track soft tissues in real time to avoid missing a moving tumor or irradiating sensitive internal structures.

Integrated Treatment Planning and Delivery Software

Our proprietary treatment planning and delivery software can create treatment plans and manage the treatment delivery process. It is designed to create optimized 3D-CRT, IMRT, IGRT, SBRT and SRS plans for delivery by MRIdian. Using this software, the on-table adaptive planning process typically takes fifteen additional minutes on average, depending on the treatment plan and includes: auto-contouring, dose prediction and adaptive treatment plan optimization. For contouring, the software will automatically contour the outline of the tumor and nearby organs by matching the MR images with the images used in the original treatment plan. The physician will then make refinements as necessary. Dose prediction can be calculated immediately before treatment, allowing the current state of the patient’s anatomy to be taken into account. If dose parameters for the radiation target or organs at risk no longer meet goals or safety criteria, the software can then generate an optimized adaptive treatment plan, while the patient is on the treatment table. Following physician review and approval, as well as medical physics quality assurance assessment, the adapted plan can be delivered to provide a more accurate treatment.

Independent of the ability to create an adapted treatment plan, the MRIdian system has the ability to use a soft-tissue tracking beam to control or “gate” the radiation beam, by turning it on and off. While the radiation dose is being delivered, our software analyzes images of the patient’s tumor and surrounding anatomy; it can use them to determine tumor or organ location relative to tolerances set by the physician. If the targeted tumor or a critical organ moves beyond a physician-defined boundary, the treatment beams will automatically pause. When the tumor moves back into the target zone, the treatment will automatically resume. Physicians can set both spatial and time thresholds for pausing radiation beam delivery. This enables the system to account for tumor and patient motion during treatment.

The software archives all the information generated during treatment and builds a database of patient-specific planning, delivery and imaging data. It also includes a review tool which provides clinicians with a visual comparison of the delivered treatment versus the treatment as originally planned. At the end of each treatment, the software determines the delivered dose by combining the recorded actions of the radiation delivery system with the daily image and auto-contouring of the patient. With this information, clinicians can fine-tune prescriptions based on the actual dose delivered, rather than estimates. In addition, it provides a MRIdian Movie™ of each delivered treatment, which can be evaluated by the physician or exported and then shared with the patients or their families.

Safety and Control System for MRIdian with Cobalt-60

In addition to complying with the applicable FDA and Nuclear Regulatory Commission, or NRC, requirements, the Cobalt-60 radiation delivery subsystem also meets a double fault tolerant design standard and has redundant safety systems. If any two components in the Cobalt-60 radiation delivery subsystem fail simultaneously, such as power and pneumatics, the system reverts to a safe state. MRIdian also contains redundant computer control for safety and system logging and double encoders on all axes of motion for safety. The control system continuously monitors performance to ensure systems are performing and communicating appropriately.

Installed Base and Clinical Use

At December 31, 2017, we had installed six units at five leading cancer centers in the United States and installed five units outside the United States. One MRIdian with Cobalt-60 has been delivered and is expected to be installed in early 2018 at Edogawa Hospital in Japan. Three MRIdian Linacs have been delivered and are expected to be installed in 2018 at hospitals in Israel, Korea and China.

In January 2014, Washington University in St. Louis, a National Cancer Institute Designated Comprehensive Cancer Center, became the first center to treat patients with MRIdian with Cobalt-60. Washington University in St. Louis has since scaled up its use of MRIdian in its clinical practice. In September 2014, Washington University in St. Louis used MRIdian to perform the first on-table adaptive treatments as part of an ongoing clinical service. Also, in September 2014, the University of Wisconsin–Madison treated its first patients with MRIdian with Cobalt-60 and became the first center to employ the soft-tissue tracking and beam gating control capability unique to MRIdian. In

18

July 2017, Henry Ford Health System in Detroit treated the first cancer patients using the second generation MRIdian Linac. We are working with each of these centers to determine how best to refine and improve MRIdian’s features, optimize workflow and maximize patient throughput.

As of December 31, 2017, over 2,000 patients with over 3000 on-table adapted fractions have been treated by MRIdian systems. These included cancers of the prostate, breast, lung, colorectal and bladder, which are among the most prevalent types of cancer in the United States, according to the Centers for Disease Control and Prevention, or CDC. MRIdian has also been used to treat liver, stomach, esophagus and pancreatic cancer.

New Orders and Backlog

New orders are defined as the sum of gross product orders, representing MRIdian contract price, recorded during the period. Backlog is the accumulation of all orders for which revenue has not been recognized and which we consider valid. Backlog includes customer deposits or letters of credit, except when the sale is to a customer where a deposit is not deemed necessary or customary. Deposits received are recorded as a liability on the balance sheet. Orders may be revised or cancelled according to their terms or upon mutual agreement between the parties. Therefore, it is difficult to predict with certainty the amount of backlog that will ultimately result in revenue. The determination of backlog includes objective and subjective judgment about the likelihood of an order contract becoming revenue. We perform a quarterly review of backlog to verify that outstanding orders in backlog remain valid, and based upon this review, orders that are no longer expected to result in revenue are removed from backlog. Among other criteria we use to determine whether a transaction to be in backlog, we must possess both an outstanding and effective written agreement for the delivery of a MRIdian signed by a customer with a minimum customer deposit or a letter of credit requirement, except when the sale is to a customer where a deposit is not deemed necessary or customary (i.e. sale to a government entity, a large hospital, group of hospitals or cancer care group that has sufficient credit, sales via tender awards, or indirect channel sales that have signed contracts with end-customers). We decide whether to remove an order from our backlog by evaluating the following criteria: changes in customer or distributor plans or financial conditions; the customer’s or distributor’s continued intent and ability to fulfill the order contract; changes to regulatory requirements; the status of regulatory approval required in the customer’s jurisdiction, if any; and other reasons for potential cancellation of order contracts.

We received new orders for MRIdian systems, totaling $113.6 million, $77.0 million and $40.1 million for fiscal years 2017, 2016 and 2015, respectively. We have two cancellations for fiscal year 2017. At December 31, 2017, we had a backlog with a total value of $203.6 million. There can be no assurance that backlog will result in revenue in any particular time period or at all.

Installation Process

Following execution of a contract, it generally takes nine to 12 months for a customer to prepare an existing facility or construct a new vault, although in some cases customers may request installation for a date later in the future to meet their own clinical or business requirements. After the customer completes its vault customization, it typically takes approximately ninety days to complete the installation and on-site testing of the system, including the completion of acceptance test procedures. MRIdian is designed to fit into a typical radiation therapy vault, similar to other replacement linear accelerators. MRIdian’s components all fit through standard hospital vault entrances for assembly. On-site training takes approximately one week and can be conducted concurrent with installation and acceptance testing.

Our customers are responsible for removing any outgoing linear accelerator and preparing the mounting pad, power and support system connections. Additional room modifications required are consistent with those generally required for MRI systems, such as radio frequency shielding of the room and additional power.

Clinical Development

To date, we have primarily relied on clinical symposia and case studies presented at ASTRO and the European Society for Radiotherapy and Oncology, or ESTRO, to raise awareness of MRI-guided radiation therapy and to market MRIdian to leading cancer centers. In order to promote broader adoption rates at other cancer centers and

19

hospitals, we plan to work with our customers to collect and publish data on clinical efficacy, treatment times and clinical results for patients who have been treated on a MRIdian. Outcomes data presented at the 2017 Annual Meeting of ASTRO highlighted compelling early results using the Company's MRIdian system for the treatment of inoperable, locally advanced pancreatic cancer. These early clinical data suggested nearly 2X prolonged median survival with reduced toxicity for inoperable, locally advanced pancreatic cancer. These results will be tested in a multi-center, prospective, single-arm clinical trial for inoperable, locally advanced or borderline resectable pancreatic cancer. The trial will be conducted by ViewRay's Clinical Cooperative Think Tank (C2T2), a group of MRIdian medical institutions focused on evidence gathering to support MRI-guided radiation therapy. Additionally, Washington University has published a prospective study on Magnetic Resonance Image Guided Radiation Therapy for External Beam Accelerated Partial-Breast Irradiation using a one-week course of treatment. This study demonstrated that on-board MR image-guidance allowed for a greater than 50% reduction of margins while maintaining the same dose to the tumor with patients reporting 100% Excellent/Good Cosmesis.

While we do not currently have statistically significant, prospective evidence that MRIdian improves patient outcomes or decreases healthcare costs relative to CT-based radiotherapy, we believe supporting studies will demonstrate the benefits of MRI-guided radiation therapy and adaptive treatment planning. As data accumulate from the use of MRIdian, we plan to work with professional healthcare organizations to support further global marketing efforts, additional product clearances, approvals and/or registrations and potential improvements in reimbursement.

Selling and Marketing

We currently market MRIdian through a direct sales force in the United States and Canada and are developing a sales force to assist distributors in the rest of the world. We market MRIdian to a broad range of worldwide customers, including university research and teaching hospitals, community hospitals, private practices, government institutions and freestanding cancer centers. As with the traditional linac market, our sales and revenue cycle varies based on the particular customer and can be lengthy, sometimes lasting up to 18 to 24 months (or more) from initial customer contact to order contract execution.

To sell MRIdian globally, we use a combination of sales executives, sales directors and a network of international third-party distributors with internal support from sales operations, product management and application specialists. A targeted group of eight senior sales directors are responsible for selling MRIdian within the United States and Canada. Our product management function helps market MRIdian and works with our engineering group to identify and develop upgrades and enhancements. We also have a team of application specialists who provide post-sales support.

We engage in various physician-targeted advertising efforts, and our selling and marketing practices include participating in trade shows and symposia.

Competition

We compete directly with companies marketing IGRT devices for the treatment of cancer using CT, ultrasound, optical tracking and X-ray imaging. We also compete with companies developing next-generation IGRT devices, specifically those developing MRI-guided devices, amongst others. We expect the following to drive worldwide competitive market dynamics: technological advances, including the ability to provide real-time imaging; clinical outcomes; system size, price, and operational complexity; and operational efficiency.

Our major competitors with devices approved for distribution in the United States or globally include Varian Medical Systems, Inc., or Varian, Elekta AB, or Elekta, and Accuray Incorporated, or Accuray. Many of our direct competitors have greater financial, sales and marketing, service infrastructure and research and development capabilities than we do, as well as more established reputations and current market share. The main limitations of currently approved devices are the lack of real-time, clear images before and during the treatment, as well as the ability to perform on-table adaptive planning.

We are also aware of one commercial and two academic ongoing research efforts to develop radiation therapy systems incorporating MRI. Elekta and Royal Philips have formed a consortium to develop a commercial Elekta-Philips MRI-linac. The University of Sydney, Ingham Institute and the University of Queensland have formed a

20

partnership to develop an MRI-linac and the University of Alberta’s Cross Cancer Institute is working on a MRI-linac as well. Although these academic research centers may not compete directly with us commercially, if they were to form a partnership or other relationship with one of our competitors, it could impact our sales negatively. Of these three, we believe the Elekta-Philips MRI-linac is the most advanced in development, although we believe this combined system may not be commercially available for some time because it has not been cleared or approved by regulatory authorities for patient treatments anywhere in the world. MRIdian is the first and only commercially available MRI-guided radiation therapy device to image and treat cancer patients simultaneously.

The limited capital expenditure budgets of our customers result in all suppliers to these entities competing for a limited pool of funds. Our customers may be required to select between two items of capital equipment. For example, some of our potential customers are considering expensive proton therapy systems, which could consume a significant portion of their capital expenditure budgets.

Manufacturing

We have adopted a model in which we rely on subsystem manufacturing, assembly and testing by our key suppliers. The MRIdian subsystems are then fully integrated at the customer site. Through this approach, we avoid the majority of the fixed cost structure of manufacturing facilities. We purchase major components and subsystems for MRIdian from national and international third-party original equipment manufacturers, or OEM, suppliers and contract manufacturers. These major components include the magnet, MRI electronics, ring gantry, radiation therapy heads, Cobalt-60 sources, linear accelerator, multi-leaf collimators, patient-treatment table and computers. We also purchase minor components and parts directly ourselves. For sales for which we are responsible for installation, we assemble and integrate these components with our proprietary software and perform multiple levels of testing and qualification at the customer site. The system undergoes a final acceptance test, which is performed in conjunction with the customer.

Many of the major subsystems and components of MRIdian are currently procured through single and sole source suppliers. Among these are the magnet, MRI electronics, MRI coils, ring gantry, Cobalt-60 sources, linear accelerator and the patient-treatment table. We have entered into multi-year supply agreements for most of our major components and subsystems. Except for the MRI power, control and image reconstruction subsystem, we own the design of all other major subsystems and components.

We manage our supplier relationships with scheduled business reviews and periodic program updates. We closely monitor supplier quality and delivery performance to ensure compliance with all MRIdian system specifications. We believe our supply chain has adequate capacity to meet our projected sales over the next several years.

Intellectual Property