UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-36402

LOMBARD MEDICAL, INC.

(Exact name of Registrant as specified in its charter)

Cayman Islands

(Jurisdiction of incorporation or organization)

6440 Oak Canyon, Suite 200

Irvine, California 92618

(Address of principal executive offices)

Simon Hubbert, Chief Executive Officer

Lombard Medical, Inc.

4 Trident Park

Didcot

Oxfordshire OX11 7HJ

United Kingdom

Telephone No. +44 (0) 1235 750800

E-Mail: globalinfo@lombardmedical.com

Facsimile: +44 (0) 1235 750879

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| | |

Title of each class | | Name of each exchange on which registered |

| Ordinary shares, $0.01 par value per share | | The Nasdaq Global Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 16,185,965 ordinary shares, par value $0.01 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | | | |

| U.S. GAAP ¨ | | International Financial Reporting Standards as issued by the International Accounting Standards Board x | | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

TABLE OF CONTENTS

i

ii

GENERAL INFORMATION

In this annual report on Form 20-F (“Annual Report”), “Lombard Medical,” the Group,” the “company,” “we,” “us” and “our” refer to Lombard Medical, Inc. and its consolidated subsidiaries, except where the context otherwise requires.

CHANGE OF DOMICILE

Prior to April 30, 2014, we conducted our business through Lombard Medical Technologies plc and its subsidiaries. On April 30, 2014 we effected a change of domicile pursuant to which Lombard Medical Technologies plc became a wholly-owned subsidiary of Lombard Medical, Inc., a newly formed Cayman Islands exempted company with limited liability. Except where the context otherwise requires or where otherwise indicated, the terms “we,” “us,” “our,” “our Company,” “the Company,” “our business” and “Lombard” refer, prior to such change of domicile, to Lombard Medical Technologies plc and, after such change of domicile, to Lombard Medical, Inc., in each case together with its consolidated subsidiaries as a consolidated entity.

PRESENTATION OF FINANCIAL AND OTHER DATA

The consolidated financial statement data as at December 31, 2014 and 2013 and for the years ended December 31, 2014, 2013 and 2012 have been derived from our consolidated financial statements, as presented elsewhere in this Annual Report, which have been prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB, and as adopted by the European Union and audited in accordance with the standards of the Public Company Accounting Oversight Board (United States).

We have historically conducted our business through Lombard Medical Technologies plc and its subsidiaries. On April 30, 2014, we effected the change of domicile described in “Change of Domicile” above pursuant to which Lombard Medical Technologies plc became a wholly-owned subsidiary of Lombard Medical, Inc., a newly formed Cayman Islands exempted company with limited liability. Following this change of domicile our financial statements present the results of operations of Lombard Medical, Inc. and its consolidated subsidiaries. Our loss per share numbers reflect the new capital structure of Lombard Medical, Inc.

All references in this Annual Report on Form 20-F to “$” are to U.S. dollars, all references to “£” are to pounds sterling and all references to “€” are to Euros. Solely for the convenience of the reader, unless otherwise indicated, all pounds sterling amounts as at and for the year ended December 31, 2014 have been translated into U.S. dollars at the rate at December 31, 2014, the last business day of our year ended December 31, 2014, of £0.6451 to $1.00. These translations should not be considered representations that any such amounts have been, could have been or could be converted into U.S. dollars at that or any other exchange rate as at that or any other date.

TRADEMARKS

We own or have rights to trademarks or trade names that we use in conjunction with the operation of our business. In addition, our name, logo and website name and address are our service marks or trademarks. Each trademark, trade name or service mark by any other company appearing in this Annual Report on Form 20-F belongs to its holder. Our principal trademarks or trade names that we use are Aorfix™ and Aorflex™.

INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 20-F contains forward-looking statements that involve risks and uncertainties. Words such as “project,” “believe,” “anticipate,” “plan,” “expect,” “estimate,” “intend,” “should,” “would,” “could,” “will,” “may” or other words that convey judgments about future events or outcomes indicate such forward-looking statements. Forward-looking statements in this Annual Report on Form 20-F may include statements about:

| | • | | continued market acceptance of our products; |

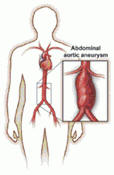

| | • | | continued growth in the number of patients qualifying for treatment of Abdominal Aortic Aneurysms (AAAs) through our products; |

| | • | | our ability to effectively compete with the products offered by our competitors; |

| | • | | the level and availability of third party payor coverage and reimbursement for our products; |

| | • | | our ability to successfully commercialize Aorfix in the United States and other jurisdictions; |

| | • | | our ability to effectively develop new or complementary technologies; |

| | • | | our ability to manufacture Aorfix to meet demand; |

| | • | | changes to our international operations; |

| | • | | our ability to effectively manage our business and keep pace with our anticipated growth; |

1

| | • | | our ability to retain and further develop our direct sales force in the United States, Germany and the United Kingdom; |

| | • | | the nature of and any changes to legislative, regulatory and other legal requirements that apply to us, our products, our suppliers and our competitors; |

| | • | | the timing of and our ability to obtain and maintain any required regulatory clearances and approvals; |

| | • | | our ability to protect our intellectual property rights and proprietary technologies; |

| | • | | our ability to operate our business without infringing the intellectual property rights and proprietary technology of third parties; |

| | • | | product liability claims and litigation expenses; |

| | • | | reputational damage to our products caused by mis-use or off-label use or government or voluntary product recalls; |

| | • | | our ability to attract, retain, and motivate qualified personnel; |

| | • | | our ability to make future acquisitions and successfully integrate any such future-acquired businesses; |

| | • | | our ability to maintain adequate liquidity to fund our operational needs and research and developments expenses; and |

| | • | | general macroeconomic and world-wide business conditions. |

The forward-looking statements included in this Annual Report on Form 20-F are subject to risks, uncertainties and assumptions. Our actual results of operations may differ materially from those stated in or implied by such forward-looking statements as a result of a variety of factors, including those described under “Risk Factors” and elsewhere in this Annual Report on Form 20-F.

We operate in an evolving environment. New risks emerge from time to time, and it is not possible for our management to predict all risks, nor can we assess the effect of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

You should not rely upon forward-looking statements as predictions of future events. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

2

PART I

| Item 1 | Identity of Directors, Senior Management and Advisers |

Not applicable.

| Item 2 | Offer Statistics and Expected Timetable |

Not applicable.

| | A. | Selected Consolidated Financial Data |

The following selected consolidated financial data as of December 31, 2014 and 2013 and for the years ended December 31, 2014, 2013 and 2012 have been derived from our consolidated financial statements included elsewhere in this Annual Report on Form 20-F. The selected consolidated financial data as of and for the year ended December 31, 2011 has been derived from our consolidated financial statements not appearing in this Annual Report on Form 20-F. Our historical results for any prior period are not necessarily indicative of results to be expected in any future period. The information set forth below should be read in conjunction with the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section of this Annual Report on Form 20-F and with our consolidated financial statements and notes thereto included elsewhere in this Annual Report on Form 20-F. We have not declared or paid any dividends in the periods presented. All our operations are continuing. As described elsewhere in this Annual Report on Form 20-F under “Change of Domicile,” subsequent to the effectiveness of the registration statement and the listing of our ordinary shares on the NASDAQ Global Market, holders of ordinary shares of Lombard Medical Technologies plc received one ordinary share of Lombard Medical, Inc. for every four shares previously held in Lombard Medical Technologies plc. Our loss per share numbers have been retrospectively adjusted to reflect the issuance of one ordinary share in Lombard Medical, Inc. for four ordinary shares in Lombard Medical Technologies plc as if it had occurred at January 1, 2011. Our loss per share numbers have been adjusted to give effect to the issuance and sale by us of 5,000,000 ordinary shares in the U.S. IPO.

| | | | | | | | | | | | | | | | |

| | | AS OF AND FOR THE YEAR ENDED

DECEMBER 31, | |

| | | 2014 | | | 2013 | | | 2012 | | | 2011 | |

| | | ($ in thousands, except per share data) | |

Statement of income data–continuing: | | | | | | | | | | | | | | | | |

Revenue | | | 13,277 | | | | 6,960 | | | | 6,175 | | | | 6,425 | |

Operating loss | | | (36,143 | ) | | | (20,034 | ) | | | (13,086 | ) | | | (18,331 | ) |

Net loss | | | (34,752 | ) | | | (19,204 | ) | | | (13,162 | ) | | | (16,184 | ) |

| | | | |

Basic and diluted loss per ordinary share (cents) | | | (238.7 | ) | | | (214.0 | ) | | | (261.1 | ) | | | (396.8 | ) |

Weighted average number of ordinary shares-basic and diluted (thousands) | | | 14,556 | | | | 8,972 | | | | 5,041 | | | | 4,080 | |

Balance sheet data: | | | | | | | | | | | | | | | | |

Cash and cash equivalents | | | 53,334 | | | | 40,866 | | | | 4,450 | | | | 11,620 | |

Total assets | | | 72,899 | | | | 58,470 | | | | 14,965 | | | | 23,646 | |

Total equity | | | 64,833 | | | | 49,333 | | | | 6,729 | | | | 19,070 | |

Share capital | | | 162 | | | | 52,406 | | | | 44,800 | | | | 44,800 | |

| | B. | Capitalization and Indebtedness |

Not applicable.

| | C. | Reasons for the offer and use of proceeds |

Not applicable.

3

Our business, financial condition or results of operations could be materially and adversely affected if any of these risks occurs, and as a result, the market price of our ordinary shares could decline. This Annual Report also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially and adversely from those anticipated in these forward-looking statements as a result of certain factors.

Risks Related to Our Business

If we fail to successfully commercialize Aorfix in the United States and other jurisdictions our business, results of operations and prospects would suffer.

We launched Aorfix commercially in the United States only in November 2013. The commercial roll-out of Aorfix in the United States is essential to our business strategy and our prospects would be significantly harmed if we are not successful in obtaining market share in the U.S. Endovascular Aneurysm Repair (EVAR) repair market, the largest market worldwide for AAA repair. We may not succeed in commercializing Aorfix in the United States for several reasons, including:

| | • | | physicians and hospitals may continue relying on open surgical repair or use outside the scope of the labels of the five other FDA-approved EVAR devices available in the United States for patients with high angle neck anatomies; |

| | • | | our direct U.S. sales force may not be large enough or effective to sufficiently train and educate physicians and hospitals about the benefits of Aorfix not only for high angle neck anatomies but also for less challenging anatomies; |

| | • | | coverage and reimbursement for Aorfix may not be sufficient for customers to choose our device when in need of an EVAR device; |

| | • | | new technologies or improved products by competitors; and |

| | • | | negative publicity about, or actual or perceived problems with Aorfix could discourage physician and hospital adoption of Aorfix. |

If we are not able to capitalize on the FDA approval of Aorfix to successfully market the product and our related products in the United States, we will not be able to generate the revenues we expect. In addition, we will not be able to offset the significant costs we have incurred and expect to continue to incur in facilitating the U.S. roll-out. This would have a material adverse effect on our business, results of operations and prospects.

In collaboration with our distribution partner Medico’s Hirata, we obtained regulatory approval, in August 2014, for Aorfix in Japan, which is the second largest worldwide EVAR repair market. Should we and Medico’s Hirata not be able to successfully commercialize Aorfix in Japan, our business, results of operations and prospects could suffer.

We have a history of operating losses and may be required to obtain additional funds.

We have incurred significant losses to date, consistent with typical early stage medical device companies. We had a loss for the year of $34.8 million in 2014, $19.2 million in 2013 and $13.2 million in 2012. As of December 31, 2014, we had an accumulated deficit of $192.9 million.

Based on current forecasts, the Company will use up its cash resources at December 31, 2014 by the end of Q1 2016. On April 24, 2015 the Company received $11 million loan funding as part of a $26 million secured loan facility with Oxford Finance LLC. The company has the option of drawing another $10 million after achieving specified revenue milestones, with a final $5 million becoming available after reaching additional revenue targets. This funding will extend cash resources beyond Q1 2016.

We will in the future need to seek additional capital. Our cash requirements in the future may be significantly different from our current estimates and depend on many factors, including:

| | • | | the results of our commercialization efforts for Aorfix and future products; |

| | • | | the need for additional capital to fund future development programs; |

| | • | | the costs involved in obtaining and enforcing patents or any litigation by third parties regarding intellectual property; |

| | • | | the establishment and maintenance of high volume manufacturing and increased sales and marketing capabilities; and |

| | • | | our success in entering into collaborative relationships with other parties. |

4

To finance these activities, we may seek funds through borrowings or through additional rounds of financing, including private or public equity or debt offerings and collaborative arrangements with corporate partners. We may be unable to raise funds on favorable terms, or at all.

During the recent economic instability, it has been difficult for many companies to obtain financing in the public markets or to obtain debt financing on commercially reasonable terms, if at all. In addition, the sale of additional equity or convertible debt securities could result in additional dilution to our stockholders. If we borrow additional funds or issue debt securities, these securities could have rights superior to holders of our common stock, and could contain covenants that will restrict our operations. We might have to obtain funds through arrangements with collaborative partners or others that may require us to relinquish rights to our technologies, product candidates, or products that we otherwise would not relinquish. If we do not obtain additional resources, our ability to capitalize on business opportunities will be limited, and the growth of our business will be harmed.

We have limited resources to invest in research and development and to grow our business and we may need to raise additional funds in the future for these activities.

We believe that our growth will depend, in significant part, on our ability to commercialize Aorfix in the United States and in Japan, as well as to develop new or improved technologies for the treatment of AAA and other aortic disorders, and technology complementary to Aorfix. Our existing resources may not allow us to conduct all of the sales and marketing and research and development activities that we believe would be beneficial for our future growth. As a result, we may need to seek funds in the future to finance these activities. If we are unable to raise funds on favorable terms, or at all, we may not be able to increase our research and development activities and the growth of our business may be negatively impacted.

If our competitors obtain approval for expanded indications of their EVAR devices to include high angle neck anatomy or are otherwise better able to develop and market products that are safer, more effective, less costly, easier to use, or otherwise more attractive than Aorfix, our business will be adversely impacted.

Our industry is highly competitive and subject to rapid and profound technological change. Currently, Aorfix is the only FDA-approved EVAR device for neck angulations between 0 and 90 degrees and one of only two EVAR devices CE-marked in the European Union for neck angulations up to and including 90 degrees. If one or more of our existing or future competitors is able to obtain regulatory approval for an EVAR device within these high angle neck ranges, we would lose what we believe is a significant competitive advantage and may not be able to increase future Aorfix sales or maintain sales at current levels.

We face competition from both established and development stage companies. Many of the companies developing or marketing competing products enjoy several advantages over us, including:

| | • | | greater financial and human resources for product development, sales and marketing and patent litigation; |

| | • | | greater name recognition; |

| | • | | long established relationships with physicians, customers and third-party payors; |

| | • | | additional lines of products, and the ability to offer rebates or bundle products to offer greater discounts or incentives; |

| | • | | more established sales and marketing programs, and distribution networks; and |

| | • | | greater experience in conducting research and development, manufacturing, clinical trials, preparing regulatory submissions, obtaining regulatory clearance or approval for products and marketing approved products. |

We may also face competition from lower profile devices, repositionable devices, devices that are able to provide improved flexibility. All of such potential competition could narrow the potential market for Aorfix.

Our competitors may develop and patent processes or products earlier than us, obtain regulatory clearance or approvals for competing products more rapidly than us, and develop more effective or less expensive products or technologies that render our technology or products obsolete or less competitive. We also face fierce competition in recruiting and retaining qualified scientific, sales, and management personnel, establishing clinical trial sites and patient enrolment in clinical trials, as well as in acquiring technologies and technology licenses complementary to our products or advantageous to our business. If our competitors are more successful than us in these matters, our business, results of operations and financial condition could be materially adversely affected.

5

If we fail to properly manage our growth, our business could suffer.

Following the February 2013 FDA approval of Aorfix and the commencement of our commercialization efforts in the United States, we are experiencing and expect to continue to experience a period of rapid growth and expansion, which could place a significant strain on our personnel, information technology systems and other resources. In particular, the creation, maintenance and potential need to further expand our direct sales force in the United States requires significant management and other supporting resources. We also plan to leverage the FDA approval of Aorfix to expand sales efforts in the European Union, including by increasing the size of our direct sales force in Germany. In addition, we obtained regulatory approval for Aorfix in Japan in August 2014 and commercial sales by our distribution partner Medico’s Hirata began soon thereafter. Any failure by us to manage our growth effectively could have an adverse effect on our ability to achieve our development and commercialization goals, which could materially adversely affect our business, results of operations and financial condition.

To achieve our revenue goals, we must successfully increase production output as required by customer demand in the United States, in the European Union and in Japan. We may experience difficulties in increasing production at our manufacturing facility, including problems with production yields and quality control, component supply, and shortages of qualified personnel. We will also be required to manage a larger stock of inventory than we have had to manage historically and such inventory going forward will be stocked in multiple locations. These problems could result in delays in product availability and increases in expenses. Any such delay or increased expense could adversely affect our ability to generate revenues in the markets we are selling Aorfix.

Future growth will also impose significant added responsibilities on management, including the need to identify, recruit, train, and integrate additional employees other than sales force representatives. In addition, rapid and significant growth will place a strain on our administrative and operational infrastructure. We expect that sales of Aorfix in the United States will increasingly represent a significant portion of our worldwide Aorfix sales, which could place additional strain on our ability to manage U.S. operations.

In order to manage our operations and growth we will need to continue to improve our operational and management controls, reporting and information technology systems, and financial internal control procedures. If we are unable to manage our growth effectively, it may be difficult for us to execute our business strategy and our operating results and business could suffer.

Our revenue is generated primarily from the sale of Aorfix, and any decline in the sales of Aorfix will negatively impact our business.

We have focused extensively on the development and commercialization of Aorfix for the treatment of AAA. If we are unable to continue to achieve and maintain market acceptance of Aorfix and do not achieve sustained positive cash flow from operations, we will be constrained in our ability to fund development and commercialization of improvements in Aorfix for the treatment of AAA and other product lines. In addition, if we are unable to commercialize Aorfix in the United States or elsewhere as a result of a quality problem or failure to maintain regulatory approvals, we would lose our primary source of revenue and our business would be negatively affected.

Reduction or interruption in supply, and an inability to develop alternative sources for supply could adversely affect our manufacturing operations and related product sales.

We manufacture all of our products at our UK facility in Didcot. We purchase many of the components and raw materials used in manufacturing these products from numerous suppliers in various countries. Generally we have been able to obtain adequate supplies of such raw materials and components. However, for reasons of quality assurance, cost effectiveness, or availability, we procure certain components and raw materials from single-source suppliers. Our use of these single-source suppliers of raw materials and components exposes us to several risks, including disruptions in supply, price increases, late deliveries and an inability to meet customer demand. Finding alternative sources for these raw materials and components and could be difficult and in many cases could entail a significant amount of time, disruption and cost. We work closely with our suppliers to try to ensure continuity of supply while maintaining high quality and reliability. However, we cannot guarantee that these efforts will be successful. In addition, due to the stringent regulations and requirements of the FDA regarding the manufacture of our products, we may not be able to quickly establish additional or replacement sources for certain components or materials. A reduction or interruption in supply, and an inability to develop alternative sources for such supply, could adversely affect our ability to manufacture our products in a timely or cost-effective manner and to make our related product sales. In addition, as discussed below, we expect to require significantly more supply of the raw materials and components necessary to manufacture Aorfix as we expand sales into the United States and Japan.

Quality problems with Aorfix could harm our reputation and erode our competitive position, sales, and market share.

Quality is extremely important to us and our customers due to the serious and costly consequences of product failure. Our quality certifications are critical to the marketing success of Aorfix. If we fail to meet these standards, our reputation could be harmed, we could lose customers, we could have to conduct a public recall, our roll-out of Aorfix in the United States could be hindered and our revenue and results of operations could decline. Aside from specific customer standards, our success depends generally on our ability to manufacture precision-engineered components, subassemblies, and finished devices from multiple materials. If our components fail to meet these standards or fail to adapt to evolving standards, our reputation will be harmed, our competitive position could be damaged, and we could lose customers and market share. Any of the foregoing could have a material adverse effect on our business, results of operations and financial condition.

6

If we experience decreasing prices for Aorfix and we are unable to reduce our expenses, our results of operations will suffer.

We may experience decreasing prices for Aorfix due to pricing pressure experienced by our customers from managed care organizations and other third-party payors, increased market power of hospitals, and increased competition among medical engineering and manufacturing services providers. If the prices for Aorfix decrease and we are unable to reduce our expenses, our results of operations will be adversely affected.

Our success depends on our being able to capture a meaningful share of the U.S. EVAR market.

According to Medtech Ventures, it is estimated that more than 500,000 AAA patients are diagnosed annually in the developed world, with 200,000 of such patients receiving treatment. According to iData Research, Inc., in the United States alone, each year, approximately 200,000 patients are diagnosed with AAA. Our growth will depend upon an increasing percentage of patients with AAA being diagnosed, and an increasing percentage of those diagnosed receiving EVAR, as opposed to an open surgical procedure. Initiatives to increase screening for AAA include the Screening Abdominal Aortic Aneurysms Very Efficiently, or SAAAVE, Act, which was signed into law on February 8, 2006 in the United States. For people who meet certain eligibility criteria, and as implemented by CMS, SAAAVE provides one-time AAA screening for certain men who have smoked cigarettes at some time in their life, and men or women who have a family history of the disease. Screening is provided as part of the “Welcome to Medicare” physical. Such general screening programs may never gain wide acceptance. The failure of physicians to diagnose more patients with AAA could negatively impact our revenue growth.

Our success depends on educating physicians so that they will use, and continue to use, Aorfix in endovascular AAA procedures.

Aorfix has a broader label than any approved EVAR product in the United States and Japan and than all but one approved EVAR product in the European Union. However, many of our competitors with EVAR products not approved for angles above 60 degrees in the United States and Japan and 75 degrees, and one product at 90 degrees, in the European Union are well known by physicians and their products may be chosen by physicians over Aorfix despite the absence of regulatory approval for use in these high angle anatomies. Below angles of 60 degrees in the United States and Japan and 75 degrees in the European Union, there are several approved products in all jurisdictions where we compete and many are supported by competitors who have greater resources than we do. If we are unable to educate physicians with regard to the use Aorfix both in high angle neck anatomies as well as for less challenging anatomies, our business could be negatively impacted.

The continuing development of Aorfix depends upon us maintaining strong relationships with physicians.

If we fail to maintain our working relationships with physicians and build relationships with new physicians, Aorfix may not be marketed in line with the needs and expectations of the professionals who use and support it, which could cause a decline in our revenues. The research, development, marketing, and sales of Aorfix is dependent upon our maintaining working relationships with physicians. We rely on these professionals to provide us with considerable knowledge and experience regarding the development, marketing, and sale of our products. Physicians assist us as researchers, marketing and product consultants, inventors, and public speakers. If we are unable to maintain our strong relationships with these professionals and continue to receive their advice and input, the development and marketing of Aorfix could suffer, which could have a material adverse effect on our consolidated earnings, financial condition, and cash flows.

If we fail to further develop and maintain our direct sales forces in the United States, the United Kingdom and Germany, our business could suffer.

We have direct sales forces for Aorfix in the United States, the United Kingdom and Germany, three of our four largest markets. We utilize a network of third-party distributors for other European jurisdictions. As we launch Aorfix in the United States and increase our marketing efforts in both the United States and Europe with respect to Aorfix, we will need to maintain our current sales representatives and also likely increase the size of our sales force in the United States and Germany primarily. There is significant competition for sales personnel experienced in relevant medical device sales. If we are unable to attract, motivate, develop, and retain qualified sales personnel and thereby grow our sales forces in the United States, Germany and the United Kingdom, we may not be able to maintain or increase our revenues.

Our third-party distributors may not effectively distribute Aorfix.

We depend in part on medical device distributors and strategic relationships for the marketing and selling of Aorfix as well as the training of physicians in the proper use of Aorfix in the European Union, outside of the United Kingdom and Germany, in Asia and in Latin America. Having obtained regulatory approval for Aorfix in Japan, we depend on Medico’s Hirata to distribute Aorfix in Japan and to train physicians in Japan in how to properly use Aorfix. We depend on these distributors’ efforts to market Aorfix and train physicians, yet we are unable to control their efforts completely. In addition, we are unable to ensure that our distributors comply with all applicable laws regarding the sale of Aorfix. If our distributors fail to effectively market and sell Aorfix and to train physicians in full compliance with applicable laws our operating results and business may suffer.

7

If clinical trials of our current or future products do not produce results necessary to support regulatory clearance or approval in the United States or elsewhere, we will be unable to continue to commercialize these products.

To market a medical device in the United States, we must obtain approval of a premarket approval application, or PMA, or clearance from the FDA under Section 510(k) of the Federal Food, Drug and Cosmetic Act, or the FDCA, unless an exemption from pre-market review applies. See “ Our future success depends on our ability to develop, receive regulatory clearance or approval for, and introduce new products or product enhancements that will be accepted by the market in a timely manner. ” In order to obtain premarket approval and, in some cases, a 510(k) clearance, a product sponsor must conduct well controlled clinical trials designed to test the safety and effectiveness of the product. We will likely need to conduct additional clinical trials in the future to support new product approvals, or for the approval of new indications for the use of Aorfix. Clinical testing is expensive, and typically takes many years, which carries an uncertain outcome. The data obtained from clinical trials may be inadequate to support approval or clearance of a submission. In addition, the occurrence of unexpected findings in connection with clinical trials may prevent or delay obtaining approval or clearance. The initiation and completion of any of our clinical trials may be prevented, delayed, or halted for numerous reasons, including, but not limited to, the following:

| | • | | the FDA, institutional review boards, or IRBs, or other regulatory authorities do not approve a clinical study protocol, force us to modify a previously approved protocol, or place a clinical study on hold; |

| | • | | subjects do not enroll in, or enroll at the expected rate, or complete a clinical study; |

| | • | | subjects or investigators do not comply with study protocols; |

| | • | | subjects do not return for post-treatment follow-up at the expected rate; |

| | • | | subjects experience serious or unexpected adverse side effects for a variety of reasons that may or may not be related to our products such as the advanced stage of co-morbidities that may exist at the time of treatment, causing a clinical study to be put on hold; |

| | • | | sites participating in an ongoing clinical study may withdraw, requiring us to engage new sites; |

| | • | | difficulties or delays associated with establishing additional clinical sites; |

| | • | | third-party clinical investigators decline to participate in our clinical studies, do not perform the clinical studies on the anticipated schedule, or are inconsistent with the investigator agreement, clinical study protocol, good clinical practices, and other FDA and IRB requirements; |

| | • | | third-party organizations do not perform data collection and analysis in a timely or accurate manner; |

| | • | | regulatory inspections of our clinical studies require us to undertake corrective action or suspend or terminate our clinical studies; |

| | • | | changes in federal, state, or foreign governmental statutes, regulations or policies; |

| | • | | interim results are inconclusive or unfavorable as to immediate and long-term safety or efficacy; |

| | • | | the study design is inadequate to demonstrate safety or efficacy; or |

| | • | | the clinical trials do not meet the study endpoints. |

Failure can occur at any stage of clinical testing. Our clinical trials may produce negative or inconclusive results, and we may decide, or regulators may require us, to conduct additional clinical and/or non-clinical testing in addition to those we have planned. Our failure to adequately demonstrate the efficacy and safety of any of our devices would prevent receipt of regulatory clearance or approval and, ultimately, the commercialization of that device or indication for use.

If we are unable to protect our intellectual property, our business may be negatively affected.

Our success depends in large part on our ability to secure effective intellectual property protection for our products and processes in the United States and internationally. We attempt to protect our intellectual property rights, both in the United States and in foreign countries, through a combination of patent, trade secret, trademark, and copyright laws, as well as licensing agreements and third-party confidentiality and invention assignment agreements. Because of the differences in foreign trademark, patent and other laws concerning proprietary rights, our intellectual property rights may not receive the same degree of protection in foreign countries as they would in the United States. Our failure to obtain or maintain adequate protection of our intellectual property rights for any reason could have a material adverse effect on our business, results of operations and financial condition.

8

We have filed and intend to continue to file patent applications for various aspects of our technology to cover our products and processes. While we generally apply for patents in those countries where we intend to make, have made, use, or sell patented products, we may not accurately predict all of the countries where patent protection will ultimately be desirable. If we fail to timely file a patent application in any such country, we may be precluded from doing so at a later date. Additionally, we may fail to secure necessary patents prior to or after obtaining regulatory clearances, thereby permitting competitors to market competing products. Moreover, we cannot assure you that any of our patent applications will be approved. We also cannot assure you that the patents issuing as a result of our foreign patent applications will have the same scope of coverage as our U.S. patents. Further, we cannot be certain that we will be the first creator of inventions covered by any patent application because some patent applications are maintained in secrecy for a period of time. Thus, we could adopt technology without knowledge of a pending patent application. In addition, the patents we already own could be challenged, re-examined, invalidated or circumvented by others and may not be of sufficient scope or strength to provide us with any meaningful protection or commercial advantage. Further, we cannot assure you that competitors will not infringe our patents, or that we will have adequate resources to enforce our patents.

We also own trade secrets and confidential information that we try to protect by entering into confidentiality agreements with consultants, key employees and other relevant parties. However, the confidentiality agreements may not be honored or, if breached, we may not have sufficient remedies to protect our confidential information. Further, our competitors may independently learn our trade secrets or develop similar or superior technologies. To the extent that our consultants, key employees or others apply technological information to our projects that they develop independently or others develop, disputes may arise regarding the ownership of proprietary rights to such information, and such disputes may not be resolved in our favor. If we are unable to protect our intellectual property adequately, our business and commercial prospects will likely suffer.

We rely on our trademarks, trade names, and brand names to distinguish our products from the products of our competitors, and have registered or applied to register many of these trademarks. We cannot assure you that our trademark applications will be approved. Third parties may also oppose our trademark applications, or otherwise challenge our use of the trademarks. In the event that our trademarks are successfully challenged, we could be forced to rebrand our products, which could result in loss of brand recognition, and could require us to devote resources advertising and marketing new brands. Further, we cannot assure you that competitors will not infringe our trademarks, or that we will have adequate resources to enforce our trademarks.

We may need to engage in expensive and prolonged litigation to assert or defend any of our intellectual property rights or to determine the scope and validity of rights claimed by other parties.

If our products or processes infringe upon the intellectual property of third parties, the sale of our products may be challenged and we may have to defend costly and time-consuming infringement claims.

The market for medical devices is subject to frequent litigation regarding patent and other intellectual property rights. We face the risk of claims that we have infringed third parties’ intellectual property rights. Any claim of intellectual property infringement, even those without merit, could be expensive and time consuming to defend and with no certainty as to the outcome, litigation could be too expensive for us to pursue. Our failure to prevail in such litigation or our failure to pursue litigation could result in the loss of our rights that could substantially hurt our business. Our competitors in both the United States and foreign countries, many of which have substantially greater resources and have made substantial investments in competing technologies, may have applied for or obtained, or may in the future apply for and obtain, patents that will prevent, limit or otherwise interfere with our ability to make and sell our products. We have not conducted an independent review of patents issued to third parties. The large number of patents, the rapid rate of new patent issuances, the complexities of the technology involved and uncertainty of litigation increase the risk of business assets and management’s attention being diverted to patent litigation. In addition, because of our developmental stage, claims that our products infringe on the patent rights of others are more likely to be asserted after commencement of commercial sales of new products incorporating our technology.

Our failure to obtain rights to intellectual property of third parties, or the potential for intellectual property litigation, could divert management’s attention and force us to do one or more of the following things:

| | • | | stop selling, making, or using products that use the disputed intellectual property; |

| | • | | obtain a license from the intellectual property owner to continue selling, making, licensing, or using products, which license may not be available on reasonable terms, or at all; |

| | • | | redesign our products, processes or services; or |

| | • | | pay significant damages. |

9

Any of these outcomes could have a negative impact on our operating profits and harm our future prospects. If any of the foregoing occurs, we may be unable to manufacture and sell our products and may suffer severe financial harm. Whether or not an intellectual property claim is valid, the cost of responding to it, in terms of legal fees and expenses and the diversion of management resources, could harm our business.

We may face product liability claims that could result in costly litigation and significant liabilities.

Manufacturing and marketing Aorfix, and clinical testing of our products and product candidates, may expose us to product liability claims. Although we have, and intend to maintain, product liability insurance, the coverage limits of our insurance policies may not be adequate and one or more successful claims brought against us may have a material adverse effect on our business and results of operations. Additionally, adverse product liability actions could negatively affect our reputation, continued product sales, and our ability to obtain and maintain regulatory approval for our products.

Our ability to maintain our competitive position depends on our ability to attract and retain highly qualified personnel.

We believe that our continued success depends to a significant extent upon the efforts and abilities of our executive officers, particularly Simon Hubbert, our Chief Executive Officer, William J. Kullback, our Chief Financial Officer, Peter Phillips, our Chief Technology Officer and Michael Gioffredi, our President, North America. The loss of any of the foregoing individuals would harm our business. Our ability to retain our executive officers and other key employees, and our success in attracting and hiring additional skilled employees, will be critical to our future success.

Our U.S. operations are currently based at a location that may be at risk from earthquakes.

Our U.S. operations are currently at a single location in Irvine, California, near known earthquake fault zones. Any future earthquake could cause substantial delays in our operations, damage or destroy our equipment, and cause us to incur additional expenses. An earthquake could seriously harm our business and results of operations. The insurance coverage we maintain may not be adequate to cover our losses in any particular case.

If any future acquisitions or business development efforts are unsuccessful, our business may be harmed.

As part of our business strategy to be an innovative leader in the treatment of aortic disorders, we may need to acquire other companies, technologies, and product lines in the future. Acquisitions involve numerous risks, including the following:

| | • | | the possibility that we will pay more than the value we derive from the acquisition, which could result in future non-cash impairment charges; |

| | • | | difficulties in integration of the operations, technologies, and products of the acquired companies, which may require significant attention of our management that otherwise would be available for the ongoing development of our business; |

| | • | | the assumption of certain known and unknown liabilities of the acquired companies; and |

| | • | | difficulties in retaining key relationships with employees, customers, partners, and suppliers of the acquired company. |

In addition, we may invest in new technologies that may not succeed in the marketplace. If they are not successful, we may be unable to recover our initial investment, which could include the cost of acquiring the license, funding development efforts, acquiring products, or purchasing inventory. Any of these would negatively impact our future growth and cash reserves.

We are increasingly dependent on sophisticated information technology and if we fail to properly maintain the integrity of our data or if our products do not operate as intended, our business could be materially affected.

We are increasingly dependent on sophisticated information technology for our products and infrastructure. Our information systems require an ongoing commitment of significant resources to maintain, protect, and enhance existing systems and develop new systems to keep pace with continuing changes in information processing technology, evolving systems and regulatory standards, the increasing need to protect patient and customer information, and changing customer patterns. In addition, third parties may attempt to illegally access our products or systems and may obtain data relating to patients with our products or our proprietary information. If we fail to maintain or protect our information systems and data integrity effectively, we could lose existing customers, have difficulty attracting new customers, have problems in determining product cost estimates and establishing appropriate pricing, have difficulty preventing, detecting, and controlling fraud, have disputes with customers, physicians, and other health care professionals, have regulatory sanctions or penalties imposed, have increases in operating expenses, incur expenses or lose revenues as a result of a data privacy breach, or suffer other adverse consequences. There can be no assurance that our process of consolidating the number of systems we operate, upgrading and expanding our information systems capabilities, protecting and enhancing our systems and developing new systems to keep pace with continuing changes in information processing technology will be successful or that additional systems issues will not arise in the future. Any significant breakdown, intrusion, interruption, corruption, or destruction of these systems, as well as any data breaches, could have a material adverse effect on our business.

10

Failure to comply with the U.S. Foreign Corrupt Practices Act, the UK Bribery Act or other anti-corruption laws could result in fines, criminal penalties, contract terminations and an adverse effect on our business.

We operate in the medical device industry in several countries throughout the world, many of which pose elevated risks of anti-corruption violations. We sell our products through our direct sales force and through distributors to our end customers, including state-or-government-owned hospitals. This puts us and our distributors in contact with persons who may be considered “foreign officials” or “foreign public officials” under the U.S. Foreign Corrupt Practices Act of 1977, or the FCPA, and the Bribery Act 2010 of the Parliament of the United Kingdom, or the UK Bribery Act, respectively. In March 2013, we adopted an Anti-Bribery Policy, and we are committed to doing business in accordance with all applicable anti-corruption laws. We are subject, however, to the risk that we, our affiliated entities, or our or their respective officers, directors, employees and agents may take actions determined to be in violation of such anti-corruption laws, including the FCPA and the UK Bribery Act. Any such violation could result in substantial fines, sanctions, civil and/or criminal penalties and curtailment of our operations in certain jurisdictions, and might adversely affect our business, results of operations or financial condition. In addition, actual or alleged violations, as well as any investigation thereof, could damage our reputation and have an adverse impact on our business.

Risks Related to the Regulation of Our Industry

If third party payors do not provide reimbursement for the use of Aorfix and our related products, our revenues may be negatively impacted.

Our success in marketing our Aorfix and our related products depends in large part on whether U.S., Japan, EEA and other government health administrative authorities, private health insurers and other organizations will reimburse customers for the cost of our products. Reimbursement for EVAR has been in place for a considerable period of time. Reimbursement codes for EVAR are in place in the United States, Japan, United Kingdom, Italy, Germany, Spain and other countries with developed healthcare systems. Our Company does not obtain specific or special reimbursement codes other than those codes which cover products in the EVAR market. Reimbursement systems in international markets vary significantly by country and by region within some countries, and reimbursement approvals must be obtained on a country-by-country basis. Further, many international markets have government managed healthcare systems that control reimbursement for new devices and procedures. In most markets there are private insurance systems as well as government-managed systems. If sufficient reimbursement is not available for our current or future products, in either the United States, Japan, the EEA or elsewhere, the demand for our products will be adversely affected. See “Business—Reimbursement”

We may be subject to or otherwise affected by federal and state healthcare laws, including anti-kickback, fraud and abuse and health information privacy and security laws, and could face substantial penalties if we are unable to fully comply with such laws and such penalties could adversely impact our reputation and business operations.

Our business operations and activities may be directly, or indirectly, subject to various federal, state and local fraud and abuse laws, including, without limitation, the federal Anti-Kickback Statute and the federal False Claims Act. In addition, we may be subject to patient privacy regulation by the federal government, state governments and foreign jurisdictions in which we conduct our business.

Healthcare fraud and abuse and health information privacy and security laws potentially applicable to our operations include:

| | • | | the federal Anti-Kickback Statute, which applies to our marketing practices, educational programs, pricing policies and relationships with healthcare providers, by prohibiting, among other things, soliciting, offering, receiving, or providing compensation, directly or indirectly, intended to induce the purchase or recommendation of an item or service reimbursable under a federal healthcare program, such as the Medicare or Medicaid programs; |

| | • | | federal false claims laws that prohibit, among other things, knowingly presenting, or causing to be presented, claims for payment from Medicare, Medicaid or other governmental healthcare programs that are false or fraudulent; |

| | • | | the federal “Stark Law,” which prohibits a physician from referring Medicare or Medicaid patients to an entity providing “designated health services,” in which the physician has an ownership or investment interest or with which the physician has entered into a financial arrangement; |

| | • | | the federal Health Insurance Portability and Accountability Act of 1996, or HIPAA, and its implementing regulations (all as amended by the Health Information Technology for Economic and Clinical Health Act), which created federal criminal laws that prohibit executing a scheme to defraud any healthcare benefit program or making false statements relating to healthcare matters and also imposes certain regulatory and contractual requirements regarding the privacy, security and transmission of individually identifiable health information; |

| | • | | federal “sunshine” requirements imposed by the ACA on device and pharmaceutical manufacturers regarding any payment or “transfer of value” made or distributed to physicians and teaching hospitals. Failure to submit required information may result in civil monetary penalties of up to an aggregate of $150,000 per year (or up to an aggregate of $1 million per year for |

11

| | “knowing failures”, for all payments, transfers of value or ownership or investment interests) that are not timely, accurately, and completely reported in an annual submission. Manufacturers were required to begin collecting data on August 1, 2013 and were required to submit reports to the CMS by March 31, 2014 (and the 90th day of each subsequent calendar year); and |

| | • | | state law equivalents of each of the above federal laws, such as anti-kickback and false claims laws that may apply to items or services reimbursed by any third-party payor, including commercial insurers, state transparency requirements and state laws governing the privacy and security of certain health information, many of which differ from each other in significant ways and often are not preempted by HIPAA, thus complicating compliance efforts. |

In addition, certain states mandate implementation of corporate compliance programs (and/or the maintenance of databases to ensure compliance with these laws) and/or impose additional restrictions on our financial relationships with physicians and other healthcare providers.

Another development affecting fraud and abuse risks is the increased use of the whistleblower or qui tam provisions of the False Claims Act. The False Claims Act imposes liability on any person or entity who, among other things, knowingly presents, or causes to be presented, a false or fraudulent claim for payment by a federal healthcare program. The qui tam provisions of the False Claims Act allow a private individual to bring civil actions on behalf of the federal government alleging that the defendant has submitted a false claim to the federal government, and to share in any monetary recovery. In recent years, the number of suits brought by private individuals has increased dramatically. In addition, various states have enacted false claim laws analogous to the False Claims Act. Many of these state laws apply where a claim is submitted to any third-party payor and not merely a federal healthcare program.

Because of the breadth of these laws and the narrowness of the statutory exceptions and regulatory safe harbors available under the federal Anti-Kickback Statute, it is possible that some of our business activities, including our relationships with physicians or customers, could be subject to challenge under one or more of such laws. If our past or present operations are found to be in violation of any of such laws or any other governmental regulations that may apply to us, we may be subject to penalties, including civil and criminal penalties, damages, fines, exclusion from government healthcare programs and the curtailment or restructuring of our operations. Similarly, if the healthcare providers or entities with whom we do business are found to be non-compliant with applicable laws, they may be subject to sanctions, which could also have an adverse impact on us. Any penalties, damages, fines, curtailment or restructuring of our agreements with physicians as well as of our operations could adversely affect our ability to operate our business and our financial results. The risk of our being found in violation of these laws is increased by the fact that many of them have not been fully interpreted by the regulatory authorities or the courts, and their provisions are open to a variety of interpretations. Any action against us for violation of these laws, even if we successfully defend against them, could cause us to incur significant legal expenses and divert our management’s attention from the operation of our business. Moreover, we expect there will continue to be federal and state laws and regulations, proposed and implemented, that could impact our operations and business. The extent to which future legislation or regulations, if any, relating to healthcare fraud and abuse laws or enforcement, may be enacted or what effect such legislation or regulation would have on our business remains uncertain.

Our business is indirectly subject to health care industry cost-containment measures that could result in reduced sales of Aorfix.

Most of our customers, and the health care providers to whom our customers supply Aorfix, rely on third-party payors, including governmental healthcare programs and private health insurance plans, to reimburse some or all of the cost of the procedures in which Aorfix and our related products are used. The continuing efforts of governmental authorities, insurance companies, and other third-party payors of healthcare costs to contain or reduce these costs could lead to patients or customers being unable to obtain coverage and reimbursement from these third-party payors. If coverage and reimbursement cannot be obtained by patients or customers, sales of Aorfix may decline significantly and our customers may reduce or eliminate purchases of Aorfix. The cost-containment measures that health care providers are instituting, in the United States, Japan, the EEA and elsewhere, could harm the results of our operations and prospects. For example, managed care organizations have successfully negotiated volume discounts for pharmaceuticals. While this type of discount pricing has not been commonly used for medical devices, if managed care or other organizations were able to affect discount pricing for devices, it could result in lower prices to our customers from their customers and, in turn, reduce the amounts we can charge our customers for our medical devices.

Healthcare policy changes, including recent federal legislation to reform the U.S. healthcare system, may have a material adverse effect on us.

In response to perceived increases in health care costs in recent years, there have been and continue to be proposals by the federal government, state governments, regulators and third-party payors to control these costs and, more generally, to reform the U.S. healthcare system. Certain of these proposals could limit the prices we are able to charge for our products or the amounts of reimbursement available for our products and could limit the acceptance and availability of our products. Moreover, as discussed below, the ACA imposes significant new taxes on medical device makers such as us. The tax on medical devices and the adoption of proposals to control costs could have a material adverse effect on our financial position and results of operations.

12

The ACA includes, among other things, a deductible 2.3% excise tax on any entity that manufactures or imports medical devices offered for sale in the United States. This excise tax, which became effective on January 1, 2013, will result in a significant increase in the tax burden on our industry, and if any efforts we undertake to offset the excise tax are unsuccessful, the increased tax burden could have an adverse effect on our results of operations and cash flows. The total cost imposed on the medical device industry by the ACA may be up to approximately $20 billion over ten years. Other elements of the ACA, including (1) a new Patient-Centered Outcomes Research Institute to oversee, identify research priorities and conduct comparative clinical effectiveness research, (2) an independent payment advisory board that will submit recommendations to Congress to reduce Medicare spending if projected Medicare spending exceeds a specified growth rate, (3) payment system reforms including a national pilot program on payment bundling to encourage hospitals, physicians and other providers to improve the coordination, quality and efficiency of certain healthcare services through bundled payment models and other provisions may significantly affect the payment for, and the availability of, healthcare services and result in fundamental changes to federal healthcare reimbursement programs, any of which may materially affect numerous aspects of our business.

Regulatory policy changes, including recent proposals in the EEA to reform the legislation governing medical devices, may have a material adverse effect on us.

In September 2012, the European Commission published proposals for the revision of the EU regulatory framework for medical devices. The proposal would replace the Medical Devices Directive and two related directives concerning active implantable medical devices and in vitro diagnostic medical devices respectively with a new regulation concerning medical devices and another concerning in vitro diagnostic medical devices. Unlike Directives that must be implemented into national laws, the Regulations would be directly applicable in all EEA Member States and so are intended to eliminate current national differences in regulation of medical devices.

On October 22, 2013, the European Parliament approved a package of reforms to the European Commission’s proposals. Under the revised proposals, only designated “special notified bodies” would be entitled to conduct conformity assessments of high-risk devices. These special notified bodies will need to notify the European Commission when they receive an application for a conformity assessment for a new high-risk device. The Commission will then forward the notification and the accompanying documents on the device to the Medical Devices Coordination Group (MDCG) for an opinion. These new procedures may result in the re-assessment of our existing medical devices, or a longer or more burdensome assessment of our new products.

Our future success depends on our ability to develop, receive regulatory clearance or approval for, and introduce new products or product enhancements that will be accepted by the market in a timely manner.

It is important to our business that we continue to build a more complete product offering for treatment of AAA and other aortic disorders. As such, our success will depend in part on our ability to develop and introduce new products. Before we can market or sell a new regulated product or a significant modification to an existing product in the United States, we must obtain either clearance from the FDA under Section 510(k) of the FDCA or approval of a PMA application from the FDA, unless an exemption from pre-market review applies. In the 510(k) clearance process, the FDA must determine that a proposed device is “substantially equivalent” to a device legally on the market, known as a “predicate” device, with respect to intended use, technology and safety and effectiveness, in order to clear the proposed device for marketing. Clinical data is sometimes required to support substantial equivalence. The PMA pathway requires an applicant to demonstrate the safety and effectiveness of the device based, in part, on extensive data, including, but not limited to, technical, preclinical, clinical trial, manufacturing and labelling data. The PMA process is typically required for devices that are deemed to pose the greatest risk, such as life-sustaining, life-supporting or implantable devices. Products that are approved through a PMA application generally need FDA approval before they can be modified. Both the 510(k) and PMA processes can be expensive and lengthy and require the payment of significant fees, unless an exemption applies. The process of obtaining a PMA is much more costly and uncertain than the 510(k) clearance process and generally takes from one to three years, or longer, from the time the application is submitted to the FDA until an approval is obtained. In the United States, our currently commercialized products have received PMA approval.

The FDA can delay, limit or deny clearance or approval of a device for many reasons, including:

| | • | | we may not be able to demonstrate to the FDA’s satisfaction that our products are safe and effective for their intended users; |

| | • | | the data from our pre-clinical studies and clinical trials may be insufficient to support clearance or approval, where required; and |

| | • | | the manufacturing process or facilities we use may not meet applicable requirements. |

In addition, the FDA may change its clearance and approval policies, adopt additional regulations or revise existing regulations, or take other actions which may prevent or delay approval or clearance of our products under development or impact our ability to modify our currently approved or cleared products on a timely basis. Any delay in, or failure to receive or maintain, clearance or approval for our products could prevent us from generating revenue from these products and adversely affect our business operations and financial results. Additionally, the FDA

13

and other regulatory authorities have broad enforcement powers. Regulatory enforcement or inquiries, or other increased scrutiny on us, could affect the perceived safety and efficacy of our products and dissuade our customers from using our products. We may not be able to successfully develop and obtain regulatory clearance or approval for product enhancements, or new products, or these products may not be accepted by physicians or the payors who financially support many of the procedures performed with our products.

The success of any new product offering or enhancement to an existing product will depend on several factors, including our ability to:

| | • | | properly identify and anticipate physician and patient needs; |

| | • | | develop and introduce new products or product enhancements in a timely manner; |

| | • | | avoid infringing upon the intellectual property rights of third parties; |

| | • | | demonstrate, if required, the safety and efficacy of new products with data from preclinical studies and clinical trials; |

| | • | | obtain the necessary regulatory clearances or approvals for new products or product enhancements; |

| | • | | be fully compliant with regulatory requirements for marketing of new devices or modified products; |

| | • | | provide adequate training to potential users of our products; |

| | • | | receive adequate coverage and reimbursement for procedures performed with our products; and |

| | • | | develop an effective and compliant, dedicated marketing and distribution network. |

If we do not develop new products or product enhancements in time to meet market demand or if there is insufficient demand for these products or enhancements, our results of operations will suffer.

Our business is subject to extensive governmental regulation that could make it more expensive and time consuming for us to introduce new or improved products.

Our medical devices are subject to regulation by numerous government agencies, including the FDA, the Ministry of Health, Labour and Welfare in Japan, the EU Commission, EEA Competent Authorities, and comparable foreign agencies. The FDA and other U.S. agencies, Japan’s Ministry of Health, Labour and Welfare, the European Commission, EEA Competent Authorities, and foreign governmental agencies regulate, among other things, with respect to medical devices:

| | • | | design, development and manufacturing; |

| | • | | testing, labelling, content and language of instructions for use and storage; |

| | • | | marketing, sales and distribution; |

| | • | | pre-market clearance and approval; |

| | • | | record keeping procedures; |

| | • | | advertising and promotion; |

| | • | | recalls and field safety corrective actions; |

| | • | | post-market surveillance, including reporting of deaths or serious injuries and malfunctions that, if they were to recur, could lead to death or serious injury; |

| | • | | medical device tracking; |

| | • | | post-market approval studies; and |

| | • | | product import and export. |

14

We also are subject to numerous additional licensing and regulatory requirements relating to safe working conditions, manufacturing practices, environmental protection, fire hazard control, and disposal of hazardous or potentially hazardous substances. Some of the most important requirements we face include:

| | • | | FDA Regulations (Title 21 CFR 820); |

| | • | | Japanese Regulations including: Japan Pharmaceutical Affairs Law (e.g.Law No.145 Established as of August 10, 1960, Law No. 87 Revised as of July 26, 2005); Regulations for Buildings and Facilities (e.g.MHLW Ministerial Ordinance No.2, 1961); and, Manufacturing and Quality Control (MHLW Ministerial Ordinance No. 169, 2004); |

| | • | | European Union and EEA Member State legislation (e.g., the EU Medical Devices Directive 93/42/EEC) and CE mark requirements; |

| | • | | Medical Device Quality Management System Requirements (ISO 13485); |

| | • | | Occupational Safety and Health Administration requirements; and |

| | • | | California Department of Health Services requirements. |

Government regulation may impede our ability to conduct continuing clinical trials, to obtain necessary premarket approvals or clearance, to obtain export approvals, and to manufacture our existing and future products. Government regulation also could delay our marketing of new products for a considerable period of time and impose costly procedures on our activities. The FDA, Japan’s Ministry of Health, Labour and Welfare, EEA Notified Bodies, and other regulatory agencies may not approve or certify any of our future products on a timely basis, if at all. Any delay in obtaining, or failure to obtain, such approvals or certifications could negatively impact our marketing of any proposed products and reduce our product revenues. The regulations to which we are subject are complex and have become more stringent over time.

Even after we have obtained the proper regulatory clearance or approval to market a product, we have ongoing responsibilities under FDA regulations, Japan’s Ministry of Health, Labour and Welfare, the EEA Member State laws implementing the EU Medical Devices Directive, and other foreign laws and regulations. Our products remain subject to strict regulatory controls on manufacturing, marketing and use. We received FDA approval for Aorfix in February 2013 and continue to further develop our regulatory compliance program as we roll-out the product in the United States. We may be forced to modify or recall our product after release in response to regulatory action or unanticipated difficulties encountered in general use. Any such action could have a material effect on the reputation of our products and on our business and financial position.

Further, regulations may change, and any different or additional regulation could limit or restrict our ability to use any of our technologies, which could harm our business. We could also be subject to new international, federal, state or local regulations that could affect our research and development programs and harm our business in unforeseen ways. If this happens, we may have to incur significant costs to comply with such laws and regulations, which will harm our results of operations.

The failure to comply with applicable regulations could jeopardize our ability to sell our products and result in enforcement actions such as:

| | • | | termination of distribution; |

| | • | | recalls or seizures of products; |

| | • | | delays in the introduction of products into the market; |

| | • | | total or partial suspension of production; |

| | • | | refusal to grant future clearances, approvals or certificates; |

| | • | | withdrawals or suspensions of current clearances, approvals or certificates, resulting in prohibitions on sales of our products; and |

| | • | | in the most serious cases, criminal penalties. |

15

The medical device industry is the subject of numerous governmental investigations into marketing and other business practices. These investigations could result in the commencement of civil and/or criminal proceedings, substantial fines, penalties, and/or administrative remedies, divert the attention of our management, and have an adverse effect on our financial condition and results of operations.