Capital contributions represent capital contributed by the owner of each subsidiary in excess of par value to fund working capital and shipyard installments and capital contributed through contributed services.

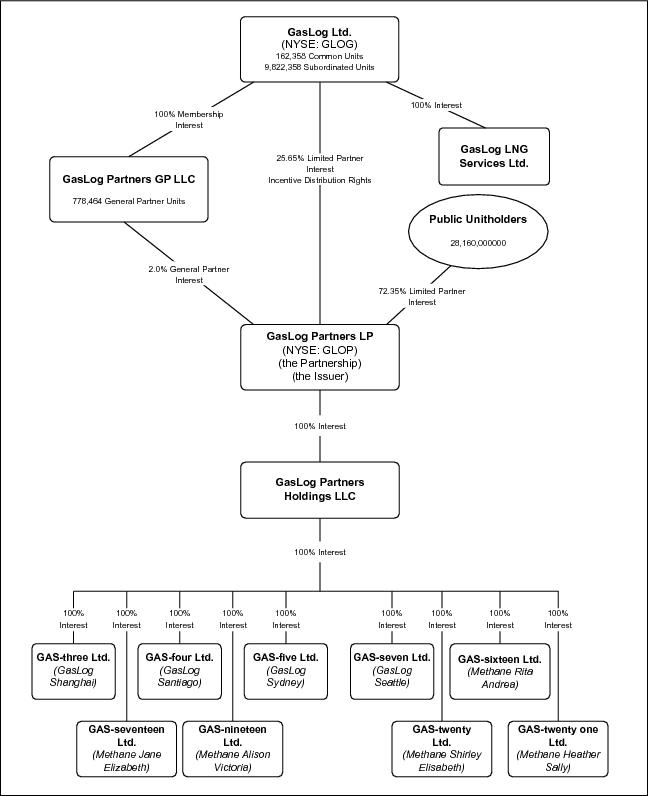

As described in Note 1, on May 12, 2014, the Partnership completed its IPO and issued (1) 162,358 common units, 9,822,358 subordinated units and all of the IDRs to GasLog, (2) 400,913 general partner units to the general partner and (3) 9,660,000 common units (including 1,260,000 units in relation to the overallotment option exercised in full by the underwriters) at a price of $21.00 per unit. The net proceeds from the IPO amounted to $186,030,150 after deducting underwriting discount and underwriters’ expenses of $13,729,850 and the equity offering expenses of $3,100,000.

On September 29, 2014, GasLog Partners completed an equity offering of 4,500,000 common units at a public offering price of $31.00 per unit. The net proceeds from this offering after deducting underwriting discounts and other offering expenses, were approximately $133,005,596. In connection with the offering, the Partnership issued 91,837 general partner units to its general partner in order for GasLog to retain its 2.0%. The net proceeds from the issuance of the general partner units were $2,846,947.

On June 26, 2015, GasLog Partners completed an equity offering of 7,500,000 common units at a public offering price of $23.90 per unit. The net proceeds from this offering after deducting underwriting discounts and other offering expenses, were $171,831,076. In connection with the

offering, the Partnership issued 153,061 general partner units to its general partner in order for GasLog to retain its 2.0% general partner interest. The net proceeds from the issuance of the general partner units were $3,658,158.

On August 5, 2016, GasLog Partners completed an equity offering of 2,750,000 common units at a public offering price of $19.50 per unit. The net proceeds from this offering after deducting underwriting discounts and other offering expenses, were $52,298,687. In connection with the offering, the Partnership issued 56,122 general partner units to its general partner in order for GasLog to retain its 2.0% general partner interest. The net proceeds from the issuance of the general partner units were $1,094,379.

As of December 31, 2016, the Partnership’s capital consisted of 24,572,358 outstanding common units, 9,822,358 outstanding subordinated units and 701,933 outstanding general partner units.

Cash distribution

On July 30, 2014, the board of directors declared a prorated quarterly cash distribution with respect to the quarter ended June 30, 2014 of $0.20604 per unit. The distribution was prorated for the period beginning on May 12, 2014, which was the closing date of the IPO, and ending on June 30, 2014, and corresponds to a quarterly distribution of $0.375 per outstanding unit, or $1.50 per outstanding unit on an annualized basis. The prorated cash distribution was paid on August 14, 2014 to all unitholders of record as of August 11, 2014.

On October 29, 2014, the board of directors declared a quarterly cash distribution with respect to the quarter ended September 30, 2014 of $0.375 per unit. The quarter ended September 30, 2014 was the Partnership’s first full quarter since the IPO. The cash distribution was paid on November 14, 2014 to all unitholders of record as of November 10, 2014.

On January 28, 2015, the board of directors declared a quarterly cash distribution, with respect to the quarter ended December 31, 2014, of $0.4345 per unit. The cash distribution was paid on February 12, 2015, to all unitholders of record as of February 9, 2015.

On April 29, 2015, the board of directors declared a quarterly cash distribution, with respect to the quarter ended March 31, 2015, of $0.4345 per unit. The cash distribution was paid on May 14, 2015 to all unitholders of record as of May 11, 2015.

On July 29, 2015, the board of directors declared a quarterly cash distribution, with respect to the quarter ended June 30, 2015, of $0.4345 per unit. The cash distribution was paid on August 13, 2015 to all unitholders of record as of August 10, 2015.

On October 28, 2015, the board of directors declared a quarterly cash distribution, with respect to the quarter ended September 30, 2015, of $0.478 per unit. The cash distribution was paid on November 12, 2015 to all unitholders of record as of November 9, 2015.

On January 27, 2016, the board of directors declared a quarterly cash distribution, with respect to the quarter ended December 31, 2015, of $0.478 per unit. The cash distribution was paid on February 12, 2016, to all unitholders of record as of February 8, 2016.

On April 27, 2016, the board of directors declared a quarterly cash distribution, with respect to the quarter ended March 31, 2016, of $0.478 per unit. The cash distribution was paid on May 13, 2016, to all unitholders of record as of May 9, 2016.

On July 27, 2016, the board of directors declared a quarterly cash distribution, with respect to the quarter ended June 30, 2016 of $0.478 per unit. The cash distribution was paid on August 12, 2016, to all unitholders of record as of August 8, 2016.

On October 26, 2016, the board of directors declared a quarterly cash distribution, with respect to the quarter ended September 30, 2016 of $0.478 per unit. The cash distribution was paid on November 11, 2016, to all unitholders of record as of November 7, 2016.

F-22

Voting Rights

The following is a summary of the unitholder vote required for the approval of the matters specified below. Matters that require the approval of a “unit majority” require:

|

| | • | | during the subordination period, the approval of a majority of the outstanding common units, excluding those common units held by the general partner and its affiliates, voting as a single class and a majority of the subordinated units voting as a single class; and |

|

| | • | | after the subordination period, the approval of a majority of the outstanding common units voting as a single class. |

In voting their common units and subordinated units the general partner and its affiliates will have no fiduciary duty or obligation whatsoever to the Partnership or the limited partners, including any duty to act in good faith or in the best interests of the Partnership or the limited partners.

Each outstanding common unit is entitled to one vote on matters subject to a vote of common unitholders. However, to preserve the Partnership’s ability to claim an exemption from U.S. federal income tax under Section 883 of the Code, if at any time any person or group owns beneficially more than 4.9% of any class of units then outstanding, any units beneficially owned by that person or group in excess of 4.9% may not be voted on any matter and will not be considered to be outstanding when sending notices of a meeting of unitholders, calculating required votes (except for purposes of nominating a person for election to the board of directors), determining the presence of a quorum or for other similar purposes under the Partnership Agreement, unless otherwise required by law. Effectively, this means that the voting rights of any such unitholders in excess of 4.9% will be redistributed pro rata among the other common unitholders holding less than 4.9% of the voting power of all classes of units entitled to vote. The general partner, its affiliates and persons who acquired common units with the prior approval of the board of directors will not be subject to this 4.9% limitation except with respect to voting their common units in the election of the elected directors.

The Partnership holds a meeting of the limited partners every year to elect one or more members of the board of directors and to vote on any other matters that are properly brought before the meeting. The general partner retains the right to appoint four of the directors.

General Partner Interest

The Partnership Agreement provides that the general partner initially will be entitled to 2.0% of all distributions that the Partnership makes prior to its liquidation. The general partner has the right, but not the obligation, to contribute a proportionate amount of capital to the Partnership to maintain its 2.0% general partner interest if the Partnership issues additional units. The general partner’s 2.0% interest, and the percentage of the Partnership’s cash distributions to which it is entitled, will be proportionately reduced if the Partnership issues additional units in the future and the general partner does not contribute a proportionate amount of capital to the Partnership in order to maintain its 2.0% general partner interest. The general partner will be entitled to make a capital contribution in order to maintain its 2.0% general partner interest in the form of the contribution to the Partnership of common units based on the current market value of the contributed common units.

Incentive Distribution Rights

Incentive distribution rights represent the right to receive an increasing percentage of quarterly distributions of available cash from operating surplus after the minimum quarterly distribution and the target distribution levels have been achieved. GasLog holds the incentive distribution rights following completion of the IPO. The incentive distribution rights may be transferred separately from any other interests, subject to restrictions in the Partnership Agreement. Except for transfers of incentive distribution rights to an affiliate or another entity as part of a merger or consolidation with or into, or sale of substantially all of the assets to, such entity, the approval of a majority of the Partnership’s common units (excluding common units held by the general partner and its affiliates), voting separately as a class, generally is required for a transfer of the incentive distribution rights to

F-23

a third party prior to March 31, 2019. Any transfer by GasLog of the incentive distribution rights would not change the percentage allocations of quarterly distributions with respect to such right.

The following table illustrates the percentage allocation of the additional available cash from operating surplus in respect to such rights:

| | | | | | | | | | | | |

| | Marginal Percentage Interest in Distributions |

| | Total Quarterly

Distribution

Target Amount | | Unitholders | | General

Partner | | Holders of

IDRs |

Minimum Quarterly Distribution | | | | | | | | $0.375 | | | | | 98.0 | % | | | | | 2.0 | % | | | | | 0 | % | |

First Target Distribution | | | | $0.375 | | | | | up to | | | | | $0.43125 | | | | | 98.0 | % | | | | | 2.0 | % | | | | | 0 | % | |

Second Target Distribution | | | | $0.43125 | | | | | up to | | | | | $0.46875 | | | | | 85.0 | % | | | | | 2.0 | % | | | | | 13.0 | % | |

Third Target Distribution | | | | $0.46875 | | | | | up to | | | | | $0.5625 | | | | | 75.0 | % | | | | | 2.0 | % | | | | | 23.0 | % | |

Thereafter | | Above | | | | | | $0.5625 | | | | | 50.0 | % | | | | | 2.0 | % | | | | | 48.0 | % | |

Subordinated Units

GasLog holds all of the Partnership’s subordinated units. The principal difference between the common units and subordinated units is that in any quarter during the subordination period the subordinated units are entitled to receive the minimum quarterly distribution of $0.375 per unit only after the common units have received the minimum quarterly distribution and arrearages in the payment of the minimum quarterly distribution from prior quarters. Subordinated units will not accrue arrearages. The subordination period generally will end if the Partnership has earned and paid at least $0.375 on each outstanding common and subordinated unit and the corresponding distribution on the general partner’s 2.0% interest for any three consecutive four-quarter periods ending on or after March 31, 2017. After the subordination period ends all subordinated units will convert into common units on a one-for-one basis and the common units will no longer be entitled to arrearages.

7. Borrowings

Borrowings as of December 31, 2015 and 2016 consisted of the following:

| | | | |

| | As of December 31, |

| | 2015 | | 2016 |

Amounts due within one year | | | | 336,000,000 | | | | | 48,081,252 | |

Less: unamortized deferred loan issuance costs | | | | (2,852,551 | ) | | | | | (2,958,763 | ) | |

| | | | |

Borrowings—current portion | | | | 333,147,449 | | | | | 45,122,489 | |

| | | | |

Amounts due after one year | | | | 540,000,000 | | | | | 776,914,972 | |

Less: unamortized deferred loan issuance costs | | | | (6,445,249 | ) | | | | | (8,285,320 | ) | |

| | | | |

Borrowings—non-current portion | | | | 533,554,751 | | | | | 768,629,652 | |

| | | | |

Total | | | | 866,702,200 | | | | | 813,752,141 | |

| | | | |

Terminated Facilities:

(a) DnB Bank ASA and Export-Import Bank of Korea:

On March 14, 2012, GAS-three Ltd. and GAS-four Ltd. entered into a loan agreement of up to $272,500,000 with DnB Bank ASA and the Export-Import Bank of Korea, in order to partially finance the acquisition of two LNG vessels. On January 18, 2013 and March 19, 2013, GAS-three Ltd. and GAS-four Ltd. drew down $272,500,000 in total from the loan facility for the financing of theGasLog Shanghai and theGasLog Santiago. Each tranche was repayable in 45 equal quarterly installments, as well as a balloon payment of $40,000,000 due together with the final installment in the first quarter of 2025. In connection with the Partnership’s IPO on May 12, 2014, the credit facility was amended to, among other things, permit GasLog to contribute GAS-three Ltd. and GAS-four Ltd. to the Partnership and add GasLog Partners Holdings LLC, as a guarantor. On

F-24

November 19, 2014, the outstanding amount of $246,432,264, for both tranches under the credit facility, was fully repaid.

(b) Nordea Bank Finland PLC, ABN Amro Bank N.V. and Citibank International PLC syndicated loan:

On October 3, 2011, GAS-five Ltd. and GasLog’s subsidiary GAS-six Ltd. entered into a loan agreement of up to $277,000,000 with Nordea Bank Finland PLC, ABN Amro Bank N.V. and Citibank International PLC in order to partially finance the acquisition of two LNG vessels. The loan agreement provided for two equal tranches that were drawn on May 24, 2013 and July 19, 2013 for the financing of theGasLog Sydney and theGasLog Skagen. Each tranche was repayable in 23 quarterly installments, together with a final balloon payment of $89,617,647 payable concurrently with the last installments in 2019. In connection with the Partnership’s IPO on May 12, 2014, the credit facility entered was amended to among other things, (1) divide the facility into two separate facilities on substantially the same terms as the initial facility, with one of the facilities executed by GAS-five Ltd. for the portion allocated to theGasLog Sydney, (2) permit GasLog’s contribution of GAS-five Ltd. to the Partnership and (3) add GasLog Partners Holdings LLC as a guarantor and remove GasLog Carriers Ltd., a wholly owned subsidiary of GasLog, as guarantor in connection with the GAS-five Ltd. facility. In connection with these amendments, the Partnership prepaid $82,633,649 of the new GAS-five Ltd. facility with proceeds of the IPO. On November 19, 2014, the outstanding amount of $48,225,101 under the GAS-five Ltd. credit facility was fully repaid.

(c) Citibank N.A. London Branch facility:

On April 1, 2014, in connection with the acquisition of the three LNG carriers from BG Group (Note 3), GasLog signed a loan agreement of $325,500,000 with Citibank, N.A. London Branch acting as security agent and trustee for and on behalf of the other finance parties. The loan had a two year maturity without intermediate payments bearing interest at LIBOR plus a margin and was drawn on April 9, 2014, to partially finance the deliveries of theMethane Rita Andrea, theMethane Jane Elizabeth and theMethane Lydon Volney. In connection with the closing of the Partnership’s acquisition of the two entities that own theMethane Rita Andrea and theMethane Jane Elizabeth on September 29, 2014, the Partnership and GasLog Partners Holdings LLC executed a supplemental deed that, among other things, permitted the Partnership to acquire GAS-sixteen Ltd. and GAS-seventeen Ltd. from GasLog and added the Partnership and GasLog Partners Holdings LLC as guarantors. The debt of $217,000,000 was assumed by the Partnership for the acquisition of GAS-sixteen Ltd. and GAS-seventeen Ltd. On October 9, 2014, the Partnership prepaid $25,000,000 from a portion of the proceeds of the follow-on equity offering (Note 6). The assumed balance of $192,000,000 was fully repaid on November 19, 2014.

(d) Citibank N.A. London Branch facility:

Following the acquisition of GAS-nineteen Ltd., GAS-twenty Ltd. and GAS-twenty one Ltd., the Partnership assumed $325,500,000 of outstanding indebtedness of the acquired entities. The loan agreement was signed by GAS-nineteen Ltd., GAS-twenty Ltd. and GAS-twenty one Ltd., on May 12, 2014 with Citibank N.A. London Branch, acting as security agent and trustee for and on behalf of the other finance parties. The loan has a two-year maturity bearing interest at LIBOR plus a margin and $108,500,000 was drawn on each of June 3, 2014, on June 10, 2014 and on June 24, 2014 to partially finance the deliveries of theMethane Alison Victoria, theMethane Shirley Elisabeth and theMethane Heather Sally, respectively. Using the proceeds of the equity offering completed in June 2015, GasLog Partners prepaid $10,000,000 of the GAS-nineteen Ltd. tranche on September 4, 2015, $5,000,000 of the GAS-twenty Ltd. tranche on December 10, 2015 and $5,000,000 of the GAS-twenty one Ltd. tranche on December 29, 2015. On April 5, 2016, the outstanding amount of $305,500,000 under the facility was fully repaid.

F-25

(e) Credit Suisse AG facility:

On January 18, 2012, GAS-seven Ltd. entered into a loan agreement of up to $144,000,000 with Credit Suisse AG, for the purpose of financing one of the newbuilding vessels. The agreement provided for a single tranche that was drawn on December 4, 2013 for the financing of theGasLog Seattle. On July 25, 2016, the outstanding amount of $124,000,000 under the facility was fully repaid.

Existing Facilities:

(a) Citibank N.A., London Branch, Nordea Bank Finland PLC London Branch, DVB Bank America N.V., ABN Amro Bank N.V., Skandinaviska Enskilda Banken AB and BNP Paribas:

On November 12, 2014, GAS-three Ltd., GAS-four Ltd., GAS-five Ltd., GAS-sixteen Ltd., GAS-seventeen Ltd, GasLog Partners LP and GasLog Partners Holdings LLC entered in a loan agreement with Citibank N.A., London Branch, acting as security agent and trustee for and on behalf of the other finance parties mentioned above, for a credit facility for up to $450,000,000 (the “Partnership Facility”) for the purpose of refinancing in full the existing debt facilities. The agreement provides for a single tranche that was drawn on November 18, 2014. The credit facility bears interest at LIBOR plus a margin. The balance outstanding as of December 31, 2016 was $405,000,000 and is repayable in 12 quarterly installments of $5,625,000 and a final balloon payment of $337,500,000 together with the last quarterly installment in 2019.

On May 8, 2015, the GasLog Partners entered into a supplemental deed relating to the aforementioned loan facility, via which the Partnership’s lenders unanimously approved changes to the facility agreement to reflect the amendments to the three time charters agreed with BG Group on April 21, 2015. As the aforementioned deed did not result in substantially different terms to the original loan agreement, the amendments were considered a modification of the existing terms. Consequently, the additional fees of $515,441 incurred during the year ended December 31, 2015 have been accounted for as deferred financing fees and will be amortized over the remaining term of the loan facility using the effective interest method.

Securities covenants and guarantees

The Partnership Facility is secured as follows: (i) first priority mortgages over the vessels owned by the borrowers, (ii) guarantees from the Partnership and its subsidiary GasLog Partners Holdings LLC, (iii) a pledge or a negative pledge of the share capital of the borrowers and (iv) a first priority assignment of all earnings and insurances related to the vessels owned by the borrowers.

The Partnership Facility contains customary events of default, including nonpayment of principal or interest, breach of covenants or material inaccuracy of representations, default under other material indebtedness and bankruptcy. In addition, the Partnership Facility contains covenants requiring that the aggregate fair market value of the vessels securing the facility remains above 120% of the aggregate amount outstanding under the facility. In the event that the value of the vessels falls below the threshold, the Partnership could be required to provide the lender with additional security or prepay a portion of the outstanding loan balance, which could negatively impact the Partnership’s liquidity.

The Partnership, as corporate guarantor for the Partnership Facility is also subject to specified financial covenants on a consolidated basis. These financial covenants include the following as defined in the agreements:

|

| | (i) | | the aggregate amount of all unencumbered cash and cash equivalents must be not less than the higher of 3.0% of total indebtedness or $15,000,000; |

|

| | (ii) | | total indebtedness divided by total capitalization must be less than 60.0%; |

|

| | (iii) | | the ratio of EBITDA over debt service obligations as defined in the Partnership’s guarantees (including interest and debt repayments) on a trailing 12 months basis must be not less than 110.0%; and |

F-26

|

| | (iv) | | the Partnership is permitted to declare or pay any dividends or distributions, subject to no event of default having occurred or occurring as a consequence of the payment of such dividends or distributions. |

The Partnership Facility also imposes certain restrictions relating to the Partnership, including restrictions that limit its ability to make any substantial change in the nature of its business or to the corporate structure without approval from the lenders.

Compliance with the financial covenants is required on a semi-annual basis.

GasLog Partners was in compliance with the Partnership Facility covenants as of December 31, 2016.

(b) Five Vessel Refinancing

On February 18, 2016, subsidiaries of the Partnership and GasLog entered into credit agreements (the “Five Vessel Refinancing”) to refinance the debt maturities that were scheduled to become due in 2016 and 2017. The Five Vessel Refinancing is comprised of a five-year senior tranche facility of up to $396,500,000 and a two-year bullet junior tranche of up to $180,000,000. The vessels covered by the Five Vessel Refinancing are the Partnership-ownedMethane Alison Victoria,Methane Shirley Elisabeth andMethane Heather Sallyand the GasLog-ownedMethane Lydon Volney andMethane Becki Anne. ABN AMRO Bank N.V. and DNB (UK) Ltd. were mandated lead arrangers to the transaction. The other banks in the syndicate are: DVB Bank America N.V., Commonwealth Bank of Australia, ING Bank N.V., London Branch, Credit Agricole Corporate and Investment Bank and National Australia Bank Limited.

On April 5, 2016, $216,864,780 and $89,875,000 under the senior and junior tranche, respectively, of the Five Vessel Refinancing were drawn by the Partnership to refinance $305,500,000 of the outstanding debt of GAS-nineteen Ltd., GAS-twenty Ltd. and GAS-twenty one Ltd. The balance outstanding as of December 31, 2016 was $207,828,747 under the senior tranche that is repayable in 18 quarterly installments and $89,874,999 under the junior tranche that shall be repaid in full 24 months after the drawdown date.

Securities covenants and guarantees

The Five Vessel Refinancing is secured as follows: (i) first and second priority mortgages over the ships owned by the respective borrowers, (ii) guarantee from GasLog, guarantees up to the value of the commitments relating to theMethane Alison Victoria, Methane Shirley Elisabeth andMethane Heather Sally from the Partnership and GasLog Partners Holdings LLC and a guarantee from GasLog Carriers Ltd. for up to the value of the commitments on the remaining vessels, (iii) a share charge over the share capital of the respective borrower and (iv) first and second priority assignment of all earnings and insurance related to the ship owned by the respective borrower.

The Five Vessel Refinancing impose certain operating and financial restrictions on the Partnership and GasLog. These restrictions generally limit the Partnership’s and GasLog’s collective subsidiaries’ ability to, among other things: (a) incur additional indebtedness, create liens or provide guarantees, (b) provide any form of credit or financial assistance to, or enter into any non-arms’ length transactions with, the Partnership or any of its affiliates, (c) sell or otherwise dispose of assets, including ships, (d) engage in merger transactions, (e) enter into, terminate or amend any charter, (f) amend shipbuilding contracts, (g) change the manager of ships, or (h) acquire assets, make investments or enter into any joint venture arrangements outside of the ordinary course of business.

The GasLog and the Partnership’s guarantees to the Five Vessel Refinancing impose specified financial covenants that apply to the Partnership and GasLog and its subsidiaries on a consolidated basis.

The financial covenants that apply to the Partnership include the following:

|

| | (v) | | the aggregate amount of all unencumbered cash and cash equivalents must be not less than the higher of 3.0% of total indebtedness or $15,000,000; |

F-27

|

| | (vi) | | total indebtedness divided by total assets must be less than 60.0%; |

|

| | (vii) | | the ratio of EBITDA over debt service obligations as defined in the Partnership’s guarantees (including interest and debt repayments) on a trailing 12 months basis must be not less than 110.0%; and |

|

| | (viii) | | the Partnership is permitted to declare or pay any dividends or distributions, subject to no event of default having occurred or occurring as a consequence of the payment of such dividends or distributions. |

The financial covenants that apply to GasLog and its subsidiaries on a consolidated basis include the following:

|

| | (i) | | net working capital (excluding the current portion of long-term debt) must be not less than $0; |

|

| | (ii) | | total indebtedness divided by total assets must not exceed 75.0%; |

|

| | (iii) | | the ratio of EBITDA over debt service obligations as defined in the GasLog guarantees (including interest and debt repayments) on a trailing 12 months basis must be not less than 110.0%; |

|

| | (iv) | | the aggregate amount of all unencumbered cash and cash equivalents must be not less than the higher of 3.0% of total indebtedness and $50,000,000 after the first drawdown; |

|

| | (v) | | GasLog is permitted to pay dividends, provided that it holds unencumbered cash and cash equivalents equal to at least 4.0% of total indebtedness, subject to no event of default having occurred or occurring as a consequence of the payment of such dividends; and |

|

| | (vi) | | GasLog’s market value adjusted net worth must at all times be not less than $350,000,000. |

The Five Vessel Refinancing also imposes certain restrictions relating to the Partnership and GasLog, and their other subsidiaries, including restrictions that limit the Partnership’s and GasLog’s ability to make any substantial change in the nature of the Partnership’s or GasLog’s business or to engage in transactions that would constitute a change of control, as defined in the Five Vessel Refinancing, without repaying all of the Partnership’s and GasLog’s indebtedness under the Five Vessel Refinancing in full.

The Five Vessel Refinancing contain customary events of default, including nonpayment of principal or interest, breach of covenants or material inaccuracy of representations, default under other material indebtedness and bankruptcy. In addition, they contain covenants requiring the Partnership, GasLog and certain of their subsidiaries to maintain the aggregate of (i) the market value, on a charter exclusive basis, of the mortgaged vessel or vessels and (ii) the market value of any additional security provided to the lenders, at not less than 115.0% until the maturity of the junior tranche, and 120.0% at any time thereafter, of the then outstanding amount under the applicable facility and any related swap exposure. If the Partnership and GasLog fail to comply with these covenants and are not able to obtain covenant waivers or modifications, the lenders could require prepayments or additional collateral sufficient for the compliance with such covenants, otherwise indebtedness could be accelerated.

(c) Citigroup Global Market Limited, Credit Suisse AG, Nordea Bank AB, Skandinaviska Enskilda Banken AB (publ), HSBC Bank Plc, ING Bank N.V., London Branch, Danmarks Skibskredit A/S, Korea Development Bank and DVB Bank America N.V.:

On July 19, 2016, GasLog entered into a credit agreement to refinance the existing indebtedness on eight of its on-the-water vessels of up to $1,050,000,000 (the “Legacy Facility Refinancing”) with a number of international banks, extending the maturities of six existing credit facilities to 2021. The vessels covered by the Legacy Facility Refinancing are theGasLog Savannah, theGasLog Singapore, theGasLog Skagen, theGasLog Seattle, theSolaris, theGasLog Saratoga, theGasLog Salem and theGasLog Chelsea. Citigroup Global Market Limited, Credit Suisse AG and Nordea Bank AB were mandated lead arrangers to the transaction. The other banks in the syndicate are: Skandinaviska Enskilda Banken AB (publ), HSBC Bank Plc, ING Bank N.V., London Branch, Danmarks Skibskredit A/S, Korea Development Bank and DVB Bank America N.V. Nordea Bank

F-28

AB, London Branch is the agent and security agent for the transaction. The Legacy Facility Refinancing is comprised of a five-year term loan facility of up to $950,000,000 and a revolving credit facility of up to $100,000,000.

Following the acquisition of GAS-seven Ltd., the Partnership assumed $122,292,478 which was drawn on July 25, 2016 under the term loan facility to refinance the existing indebtedness of $124,000,000 of GAS-seven Ltd. The aforementioned refinancing was considered an extinguishment of the existing debt facility. Consequently, the unamortized loan fees of $2,434,486 were written off to profit or loss for the year ended December 31, 2016. The balance outstanding as of December 31, 2016 was $122,292,478 under the term loan that is repayable in ten semi-annual installments of $3,754,594 each and a balloon payment of $84,746,538 due together with the last installment in July 2021, while the revolving credit facility available amount of $12,872,892 can be drawn at any time until December 31, 2020. Amounts drawn bear interest at LIBOR plus a margin.

Securities covenants and guarantees

The credit agreement is secured as follows: (i) first priority mortgages over the ships owned by the respective borrowers, (ii) guarantee from GasLog, guarantees up to the value of the commitments relating to theGasLog Seattle from the Partnership and GasLog Partners Holdings LLC and a guarantee from GasLog Carriers Ltd. for up to the value of the commitments on the remaining vessels, (iii) a share security over the share capital of each of the respective borrowers and (iv) a first priority assignment of all earnings, excluding the vessels participating in the spot market, and insurance related to the ships owned by the respective borrowers.

The Legacy Facility Refinancing imposes certain operating and financial restrictions on GasLog. These restrictions generally limit GasLog’s ability to, among other things: (a) incur additional indebtedness, create liens or provide guarantees, (b) provide any form of credit or financial assistance to, or enter into any non-arms’ length transactions with any of GasLog’s affiliates, (c) sell or otherwise dispose of assets, including ships, (d) engage in merger transactions, (e) enter into, terminate or amend any charter, (f) amend shipbuilding contracts, (g) change the manager of ships, or (h) acquire assets, make investments or enter into any joint venture arrangements outside of the ordinary course of business.

The Legacy Facility Refinancing also imposes specified financial covenants that apply to GasLog and its subsidiaries on a consolidated basis.

|

| | (i) | | net working capital (excluding the current portion of long-term debt) must be not less than $0; |

|

| | (ii) | | total indebtedness divided by total assets must not exceed 75.0%; |

|

| | (iii) | | the ratio of EBITDA over debt service obligations as defined in the GasLog guarantees (including interest and debt repayments) on a trailing 12 months basis must be not less than 110.0%; |

|

| | (iv) | | the aggregate amount of all unencumbered cash and cash equivalents must be not less than the higher of 3.0% of total indebtedness and $50,000,000 after the first drawdown; |

|

| | (v) | | GasLog is permitted to pay dividends, provided that it holds unencumbered cash and cash equivalents equal to at least 4.0% of total indebtedness, subject to no event of default having occurred or occurring as a consequence of the payment of such dividends; and |

|

| | (vi) | | GasLog’s market value adjusted net worth must at all times be not less than $350,000,000. |

The Legacy Facility Refinancing also imposes certain customary restrictions relating to GasLog and its subsidiaries, including restrictions that limit GasLog’s ability to make any substantial change in the nature of its business or to engage in transactions that would constitute a change of control, as defined in the Legacy Facility Refinancing, without repaying all of GasLog’s indebtedness under the Legacy Facility Refinancing in full.

The Legacy Facility Refinancing contains customary events of default, including non-payment of principal or interest, breach of covenants or material inaccuracy of representations, default under other material indebtedness and bankruptcy. In addition, it contains covenants requiring GasLog to

F-29

maintain the aggregate of (i) the market value, on a charter exclusive basis, of the mortgaged vessels and (ii) the market value of any additional security provided to the lenders at any time at not less than 120.0% of the then outstanding amount plus any undrawn amounts under the applicable facilities. If GasLog fails to comply with these covenants and are not able to obtain covenant waivers or modifications, the lenders could require prepayments or additional collateral sufficient for the compliance with such covenants, otherwise indebtedness could be accelerated.

(d) Loan from related parties

Following the IPO on May 12, 2014, the Partnership entered into a $30,000,000 revolving credit facility with GasLog to be used for general partnership purposes. The credit facility is unsecured and provides for an availability period of 36 months and bears interest at a rate of 5.0% per annum, with no commitment fee for the first year. After the first year, the interest increased to a rate of 6.0% per annum, with an annual 2.4% commitment fee on the undrawn balance. Each advance drawn will be repayable within a period of 6 months after the respective drawdown date but is subject to unconditional right of immediate renewal if no repayment is made. As of December 31, 2015, the outstanding balance of the revolving credit facility was $15,000,000. Amounts of $10,000,000 and $5,000,000 were repaid into the revolving facility on March 31, 2016 and August 17, 2016, respectively, leaving a balance of zero. On November 18, 2016, the Partnership drew $10,000,000 which was repaid on December 30, 2016. As of December 31, 2016, the outstanding balance of the revolving credit facility was nil.

Borrowings Repayment Schedule

The maturity table below reflects the principal repayments of the borrowings outstanding as of December 31, 2016 based on their repayment schedules:

| | | |

| | As of December 31,

2016 |

Not later than one year | | | | 48,081,252 | |

Later than one year and not later than three years | | | | 523,537,505 | |

Later than three years and not later than five years | | | | 253,377,467 | |

| | |

Total | | | | 824,996,224 | |

| | |

The weighted average total interest rate, for the above mentioned credit facilities, as of December 31, 2016 was 3.56% (December 31, 2015: 3.03%).

As the bank facilities bear interest at variable interest rates, the aggregate fair value of the aforementioned facilities as of December 31, 2016 is equal to the amount outstanding of $824,996,224. The fair value of the revolving credit facility as of December 31, 2016 was nil.

8. Other Payables and Accruals

An analysis of other payables and accruals is as follows:

| | | | |

| | As of December 31, |

| | 2015 | | 2016 |

Unearned revenue | | | | 17,365,081 | | | | | 17,418,644 | |

Accrued legal and professional fees | | | | 194,979 | | | | | 171,492 | |

Accrued crew costs | | | | 2,401,536 | | | | | 2,400,086 | |

Accrued off-hire | | | | 156,841 | | | | | 140,815 | |

Accrued purchases | | | | 1,047,089 | | | | | 1,090,957 | |

Accrued interest | | | | 3,355,589 | | | | | 6,856,835 | |

Accrued board of directors fees | | | | 218,750 | | | | | 187,500 | |

Other payables and accruals | | | | 849,751 | | | | | 1,056,065 | |

| | | | |

Total | | | | 25,589,616 | | | | | 29,322,394 | |

| | | | |

F-30

The unearned revenue of $17,418,644 represents monthly charter hires received in advance as of December 31, 2016 relating to January 2017 (December 31, 2015: $17,365,081).

9. General and Administrative Expenses

An analysis of general and administrative expenses is as follows:

| | | | | | |

| | For the year ended December 31, |

| | 2014 | | 2015 | | 2016 |

Board of directors’ fees | | | | 673,370 | | | | | 1,093,424 | | | | | 993,354 | |

Share-based compensation (Note 19) | | | | — | | | | | 205,196 | | | | | 479,856 | |

Legal and professional fees | | | | 1,123,447 | | | | | 2,060,426 | | | | | 1,124,376 | |

Commercial management fees (Note 12) | | | | 2,927,500 | | | | | 3,420,000 | | | | | 3,390,000 | |

Administrative fees (Note 12) | | | | 1,417,732 | | | | | 3,822,000 | | | | | 4,802,000 | |

Directors and officers’ liability insurance | | | | 334,234 | | | | | 426,259 | | | | | 67,651 | |

Other expenses | | | | 454,332 | | | | | 496,068 | | | | | 853,461 | |

| | | | | | |

Total | | | | 6,930,615 | | | | | 11,523,373 | | | | | 11,710,698 | |

| | | | | | |

10. Vessel Operating Costs

An analysis of vessel operating costs is as follows:

| | | | | | |

| | For the year ended December 31, |

| | 2014 | | 2015 | | 2016 |

Management fees and other vessel management expenses (Note 12) | | | | 4,018,065 | | | | | 4,920,000 | | | | | 4,968,000 | |

Crew wages | | | | 20,630,242 | | | | | 23,779,553 | | | | | 23,358,239 | |

Technical maintenance expenses | | | | 3,679,661 | | | | | 9,162,543 | | | | | 11,166,142 | |

Provisions and stores | | | | 1,661,028 | | | | | 2,380,648 | | | | | 2,237,528 | |

Insurance expenses | | | | 2,747,045 | | | | | 3,735,793 | | | | | 3,329,172 | |

Other operating expenses | | | | 2,995,321 | | | | | 3,761,355 | | | | | 2,950,980 | |

| | | | | | |

Total | | | | 35,731,362 | | | | | 47,739,892 | | | | | 48,010,061 | |

| | | | | | |

11. Net Financial Income and Costs

An analysis of financial income and financial costs is as follows:

| | | | | | |

| | For the year ended December 31, |

| | 2014 | | 2015 | | 2016 |

Financial income | | | | | | |

Financial income | | | | 48,545 | | | | | 28,535 | | | | | 180,455 | |

| | | | | | |

Total financial income | | | | 48,545 | | | | | 28,535 | | | | | 180,455 | |

| | | | | | |

Financial costs | | | | | | |

Amortization of deferred loan issuance costs | | | | 12,767,545 | | | | | 3,642,748 | | | | | 6,713,906 | |

Interest expense on loans | | | | 22,441,806 | | | | | 27,330,951 | | | | | 28,552,938 | |

Realized loss on cash flow hedges | | | | 996,326 | | | | | — | | | | | — | |

Commitment fees | | | | — | | | | | 14,000 | | | | | 619,767 | |

Other financial costs | | | | 1,518,988 | | | | | 223,840 | | | | | 315,829 | |

| | | | | | |

Total financial costs | | | | 37,724,665 | | | | | 31,211,539 | | | | | 36,202,440 | |

| | | | | | |

During the year ended December 31, 2016, an amount of $2,434,486 representing the write-off of the unamortized deferred loan issuance costs in connection with the repayment of the loan agreement of GAS-seven Ltd. with Credit Suisse AG on July 25, 2016 is included in Amortization of deferred loan issuance costs.

F-31

During the year ended December 31, 2014, (i) an amount of $9,018,650 representing the write-off of the unamortized deferred loan issuance costs in connection with the repayment of the then existing debt facilities (Note 7) is included in Amortization of deferred loan issuance costs and (ii) an amount of $1,232,161 related to termination fees for the aforementioned debt is included in Other financial costs.

12. Related Party Transactions

The Partnership has the following balances with related parties which are included in the consolidated statements of financial position:

Amounts due from related parties

| | | | |

| | As of December 31, |

| | 2015 | | 2016 |

Due from GasLog LNG Services(a) | | | | 779,509 | | | | | 4,353,376 | |

| | | | |

Total | | | | 779,509 | | | | | 4,353,376 | |

| | | | |

Amounts due to related parties

| | | | |

| | As of December 31, |

| | 2015 | | 2016 |

Due to GasLog(b) | | | | 999,767 | | | | | 255,016 | |

Due to GasLog Carriers Ltd. (“GasLog Carriers”)(c) | | | | 27,100,600 | | | | | — | |

| | | | |

Total | | | | 28,100,367 | | | | | 255,016 | |

| | | | |

|

| | (a) | | The balances represent mainly net amounts advanced to the Manager to cover future operating expenses of the Partnership. |

|

| | (b) | | The balances of $999,767 and $255,016 as of December 31, 2015 and December 31, 2016, respectively, represent payments made by GasLog on behalf of the Partnership. |

|

| | (c) | | As of December 31, 2015, the balance due to GasLog Carriers, the parent company of GAS-seven Ltd. prior to its acquisition by the Partnership, represented mainly amounts paid directly by GasLog Carriers on behalf of GAS-seven Ltd. covering expenses during the construction period. As of December 31, 2016, $26,904,206 of the outstanding balance was contributed to the share capital of GAS-seven Ltd. by GasLog Carriers (Note 17) and the balance was fully settled. |

Loans due to related parties

| | | | |

| | As of December 31, |

| | 2015 | | 2016 |

Revolving credit facility with GasLog | | | | 15,000,000 | | | | | — | |

| | | | |

Total | | | | 15,000,000 | | | | | — | |

| | | | |

The details of the revolving credit facility with GasLog are disclosed in Note 7.

F-32

The Partnership had the following transactions with related parties for the years ended December 31, 2014, 2015 and 2016:

| | | | | | | | | | |

Company | | Details | | Account | | 2014 | | 2015 | | 2016 |

GasLog | | Commercial management fee(i) | | General and administrative expenses | | | | 2,927,500 | | | | | 3,420,000 | | | | | 3,390,000 | |

GasLog | | Administrative services fee(ii) | | General and administrative expenses | | | | 1,417,732 | | | | | 3,822,000 | | | | | 4,802,000 | |

GasLog LNG Services | | Management fees and other vessel management expenses(iii) | | Vessel operating costs | | | | 4,018,065 | | | | | 4,920,000 | | | | | 4,968,000 | |

GasLog LNG Services | | Other vessel operating costs | | Vessel operating costs | | | | 177,534 | | | | | 175,450 | | | | | 50,000 | |

GasLog | | Professional and advisory fees(iv) | | General and administrative expenses | | | | — | | | | | 734,936 | | | | | — | |

GasLog | | Interest on revolving credit facility (Note 7) | | Interest expense | | | | 200,694 | | | | | 1,680,000 | | | | | 413,333 | |

GasLog | | Commitment fee on revolving credit facility (Note 7) | | Other financial costs | | | | — | | | | | 14,000 | | | | | 566,667 | |

GasLog | | Interest on interest rate swaps (Note 16) | | Loss on interest rate swaps | | | | — | | | | | — | | | | | 548,808 | |

|

| | (i) | | Commercial Management Agreements |

|

| | | | On July 19, 2013, GAS-five Ltd., and on August 28, 2013, GAS-three Ltd. and GAS-four Ltd., entered into commercial management agreements with GasLog (the “Pre-IPO Commercial Management Agreements”) that were amended upon completion of the IPO. Pursuant to the Pre-IPO Commercial Management Agreements, GasLog provided commercial management services relating to the operation of the vessels, including and not limited to negotiation of the vessels’ possible employment, assessing market conditions on specific issues, keeping proper accounting records and handling and advising on claims or disputes. The annual commercial management fee was $540,000 for each vessel payable quarterly in advance in lump sum amounts. |

|

| | | | Upon completion of the IPO on May 12, 2014, the vessel-owning subsidiaries of the Initial Fleet entered into amended commercial management agreements with GasLog (the “Amended Commercial Management Agreements”), pursuant to which GasLog provides certain commercial management services, including chartering services, consultancy services on market issues and invoicing and collection of hire payables, to the Partnership. The annual commercial management fee under the amended agreements is $360,000 for each vessel payable quarterly in advance in lump sum amounts. In December 2013, GAS-seven Ltd. entered into a commercial management agreement with GasLog for an annual commercial management fee of $540,000 that was amended to $360,000 when the vessel was acquired by the Partnership on November 1, 2016. |

|

| | | | The same provisions are included in the commercial management agreements that GAS-sixteen Ltd., GAS-seventeen Ltd., GAS-nineteen Ltd., GAS-twenty Ltd. and GAS-twenty one Ltd., entered into with GasLog upon the deliveries of theMethane Rita Andrea, theMethane Jane Elizabeth, the Methane Alison Victoria, theMethane Shirley Elisabeth and theMethane Heather Sally, respectively, into GasLog’s fleet in April 2014 and June 2014 (together with the Amended Commercial Management Agreements and the commercial management agreement between GAS-seven Ltd. and GasLog, the “Commercial Management Agreements”). |

|

| | (ii) | | Administrative Services Agreement |

|

| | | | Upon completion of the IPO on May 12, 2014, the Partnership entered into an administrative services agreement (the “Administrative Services Agreement”) with GasLog, pursuant to which GasLog will provide certain management and administrative services. The services provided under the Administrative Services Agreement are provided as the Partnership may direct, and include bookkeeping, audit, legal, insurance, administrative, clerical, banking, financial, advisory, client and investor relations services. The Administrative Services Agreement will continue indefinitely until terminated by the Partnership upon 90 days’ notice for any reason in the sole discretion of the Partnership’s board of directors. GasLog receives a service fee of $588,000 per vessel per year in connection with providing services under this agreement. On November 16, 2016, the Board of Directors approved an increase in the service fee payable to GasLog under the terms of the Administrative Services Agreement. With effect from January 1, 2017, fees of $630,000 per vessel per year will be payable. |

|

| | (iii) | | Ship Management Agreements |

|

| | | | On August 16, 2010, GAS-three Ltd. and GAS-four Ltd., and on March 31, 2011, GAS-five Ltd., entered into ship management agreements (“Pre-IPO Ship Management Agreements”) with GasLog LNG Services that were amended upon completion of the IPO. The Pre-IPO Ship Management Agreements provided for the following: |

|

| | • | | Management Fees—A fixed monthly charge of $30,000 per vessel was payable by the Partnership to the Manager for the provision of management services such as crew, operational and technical management, procurement, accounting, budgeting and reporting, health, safety, security and environmental protection, insurance arrangements, sale or purchase of vessels, general administration and quality assurance. |

F-33

|

| | • | | Superintendent Fees—A fee of $1,000 per day was payable to the Manager for each day in excess of 25 days per calendar year for which a superintendent performed visits to the vessels. |

|

| | • | | Share of General Expenses—A monthly lump sum amounting to 11.25% of the Management Fee was payable to the Manager during the term of this agreement. |

|

| | • | | Annual Incentive Bonus—Annual Incentive Bonus might be payable to the Manager, at the Partnership’s discretion, for remittance to the crew of an amount of up to $72,000 based on Key Performance Indicators predetermined annually. |

|

| | | | The same provisions are included in the ship management agreement that GAS-seven Ltd. entered into with the Manager upon its delivery from the shipyard in 2013 that was amended in May 2015 (see below). |

|

| | | | Upon completion of the IPO on May 12, 2014, each of the vessel owning subsidiaries of the Initial Fleet entered into an amended ship management agreement (collectively, the “Amended Ship Management Agreements”) under which the vessel owning subsidiaries pay a management fee of $46,000 per month to the Manager and reimburse the Manager for all expenses incurred on their behalf. The Amended Ship Management Agreements also provide for superintendent fees of $1,000 per day payable to the Manager for each day in excess of 25 days per calendar year for which a superintendent performed visits to the vessels, an annual incentive bonus of up to $72,000 based on key performance indicators predetermined annually and contain clauses for decreased management fees in case of a vessel’s lay-up. The management fees are subject to an annual adjustment, agreed between the parties in good faith, on the basis of general inflation and proof of increases in actual costs incurred by the Manager. Each Amended Ship Management Agreement continues indefinitely until terminated by either party. The same provisions are included in the ship management agreements that GAS-sixteen Ltd., GAS-seventeen Ltd., GAS-nineteen Ltd., GAS-twenty Ltd. and GAS-twenty one Ltd. entered into with the Manager upon the deliveries of theMethane Rita Andrea, theMethane Jane Elizabeth, theMethane Alison Victoria, theMethane Shirley Elisabeth and theMethane Heather Sally, respectively, into GasLog’s fleet in April 2014 and June 2014 (together with the Amended Ship Management Agreements and the ship management agreement between GAS-seven Ltd. and the Manager, the “Ship Management Agreements”). In May 2015, the Ship Management Agreements were further amended to delete the annual incentive bonus and superintendent fees clauses and in the case of GAS-seven Ltd. to also increase the fixed monthly charge to $46,000 with effect from April 1, 2015. In April 2016, the Ship Management Agreements were amended to consolidate all ship management related fees into a single fee structure. |

|

| | (iv) | | Professional and advisory fees paid to third parties by GasLog on behalf of the Partnership. |

|

| | | | Omnibus Agreement |

|

| | | | Upon completion of the IPO on May 12, 2014, the Partnership entered into an omnibus agreement with GasLog, our general partner and certain of our other subsidiaries. The omnibus agreement governs among other things (i) when and the extent to which the Partnership and GasLog may compete against each other, (ii) the time and the value at which the Partnership may exercise the right to purchase certain offered vessels by GasLog (iii) certain rights of first offer granted to GasLog to purchase any of its vessels on charter for less than five full years from the Partnership and vice versa and (iv) GasLog’s provisions of certain indemnities to the Partnership. On September 29, 2014, June 26, 2015 and October 27, 2016 the Partnership exercised the option to acquire (i) theMethane Rita Andrea and theMethane Jane Elizabeth, (ii) theMethane Alison Victoria, theMethane Shirley Elisabeth and theMethane Heather Sally and (iii) theGasLog Seattle, respectively. |

13. Commitments and Contingencies

Future gross minimum revenues receivable upon collection of hire under non-cancellable time charter agreements as of December 31, 2016, are as follows (30 off-hire days are assumed when each vessel will undergo scheduled dry-docking; in addition early delivery of the vessels by the charterers or any exercise of the charterers’ options to extend the terms of the charters are not accounted for):

| | | |

| | As of December 31, 2016 |

Not later than one year | | | | 229,769,704 | |

Later than one year and not later than three years | | | | 329,363,583 | |

Later than three years and not later than five years | | | | 62,770,000 | |

| | |

Total | | | | 621,903,287 | |

| | |

Following the acquisition of (i) theMethane Rita Andrea and theMethane Jane Elizabethand (ii)the Methane Alison Victoria,the Methane Shirley Elisabethand the Methane Heather Sally, the Partnership, through its subsidiaries (i) GAS-sixteen Ltd. and GAS-seventeen Ltd. and (ii) GAS-nineteen Ltd., GAS-twenty Ltd. and GAS-twenty one Ltd., respectively, is counter guarantor for the acquisition from BG Group of 83.33% of depot spares with an aggregate value of $6,000,000, of which $660,000 have been purchased and paid as of December 31, 2016 by GasLog. These spares should be acquired before the end of the initial term of the charter party agreements.

F-34

Various claims, suits and complaints, including those involving government regulations, arise in the ordinary course of the shipping business. In addition, losses may arise from disputes with charterers, environmental claims, agents and insurers and from claims with suppliers relating to the operations of the Partnership’s vessels. Currently, management is not aware of any such claims or contingent liabilities requiring disclosure in the consolidated financial statements.

14. Financial Risk Management

The Partnership’s activities expose it to a variety of financial risks, including market risk, liquidity risk and credit risk. The Partnership’s overall risk management program focuses on the unpredictability of financial markets and seeks to minimize potential adverse effects on the Partnership’s financial performance. The Partnership makes use of derivative financial instruments such as interest rate swaps to mitigate certain risk exposures.

Market risk

Interest Rate Risk:The Partnership is subject to market risks relating to changes in interest rates because it has floating rate debt outstanding. Significant increases in interest rates could adversely affect the Partnership’s operating margins, results of operations and its ability to service its debt. The Partnership uses interest rate swaps to reduce its exposure to market risk from changes in interest rates. The principal objective of these contracts is to minimize economic risks and costs associated with its floating rate debt and not for speculative or trading purposes. As of December 31, 2016, the Partnership had economically hedged 47.27% of its floating interest rate exposure on its outstanding borrowings by swapping the variable rate for a fixed rate (December 31, 2015: 14.61% and December 31, 2014: 14.45%).

The aggregate principal amount of the Partnership’s outstanding floating rate debt which was not economically hedged as of December 31, 2016 was $434,996,225 (December 31, 2015: $748,000,000). As an indication of the extent of the Partnership’s sensitivity to interest rate changes, an increase or decrease in LIBOR by 10 basis points would have decreased or increased, respectively, the profit during the year ended December 31, 2016 by $730,246, based upon its debt level during the period (December 31, 2015: $905,278 and December 31, 2014: $583,628).

Interest Rate Swaps:The fair value of the swaps as of December 31, 2016 was estimated as a net asset of $4,171,800 (December 31, 2015: net liability of $2,405,448). For the years ended December 31, 2016 and December 31, 2015, the interest rate swaps were not designated as cash flow hedging instruments (Note 16). For the year ended December 31, 2014, the interest rate swaps were designated as cash flow hedging instruments and a loss of $367,580 was recognised directly in the consolidated statement of changes in owners’/partners’ equity.

As of December 31, 2016, if interest rates had increased or decreased by 10 basis points with all other variables held constant, the positive/(negative) impact, respectively, on the fair value of the interest rate swaps would have amounted to approximately $1,766,052 (December 31, 2015: $501,126 and December 31, 2014: $628,280) affecting loss on swaps in the respective periods.

Currency Risk: Currency risk is the risk that the value of financial instruments will fluctuate due to changes in foreign exchange rates. Currency risk arises when future commercial transactions and recognized assets and liabilities are denominated in a currency that is not the Partnership’s functional currency. The Partnership is exposed to foreign exchange risk arising from various currency exposures primarily with respect to general and crew costs denominated in Euros. Specifically, for the year ended December 31, 2016, approximately $25,599,786, of the operating and administrative expenses were denominated in euros (December 31, 2015: $24,579,264 and December 31, 2014: $18,350,197). As of December 31, 2016, approximately $2,811,462 of the Partnership’s outstanding trade payables and accruals were denominated in euros (December 31, 2015: $4,963,344).

The Partnership does not hedge movements in exchange rates but management monitors the exchange rate fluctuations on a continuous basis. As an indication of the extent of the Partnership’s sensitivity to changes in exchange rate, a 10% increase in the average euro/dollar exchange rate

F-35

would have decreased its profit and cash flows during the year ended December 31, 2016 by $2,559,979, based upon its expenses during the year (December 31, 2015: $2,457,926 and December 31, 2014: $1,835,020).

Liquidity risk

Liquidity risk is the risk that arises when the maturity of assets and liabilities does not match. An unmatched position potentially enhances profitability, but can also increase the risk of losses.

The Partnership manages its liquidity risk by having secured credit lines and by receiving capital contributions to fund its commitments and by maintaining cash and cash equivalents.

The following tables detail the Partnership’s expected cash flows for its financial liabilities. The tables have been drawn up based on the undiscounted cash flows of financial liabilities based on the earliest date on which the Partnership can be required to pay. The table includes both interest and principal cash flows. Variable future interest payments were determined based on an average LIBOR plus the margins applicable to the Partnership’s loans at the end of each year presented.

| | | | | | | | | | | | | | |

| | Weighted-

average

effective

interest

rate | | Less

than 1

month | | 1-3 months | | 3-12 months | | 1-5 years | | 5+ years | | Total |

December 31, 2016 | | | | | | | | | | | | | | |

Trade accounts payable | | | | | | 1,271,606 | | | | | 82,404 | | | | | 66,951 | | | | | — | | | | | — | | | | | 1,420,961 | |

Due to related parties | | | | | | — | | | | | 255,016 | | | | | — | | | | | — | | | | | — | | | | | 255,016 | |

Other payables and accruals* | | | | | | 7,086,508 | | | | | 4,107,072 | | | | | 710,170 | | | | | — | | | | | — | | | | | 11,903,750 | |

Other non-current liabilities | | | | | | — | | | | | — | | | | | — | | | | | 182,284 | | | | | — | | | | | 182,284 | |

Variable interest loans | | | | 3.56 | % | | | | | 8,461,873 | | | | | 7,358,520 | | | | | 55,079,988 | | | | | 835,818,500 | | | | | — | | | | | 906,718,881 | |

Fixed interest loans** | | | | | | — | | | | | — | | | | | 317,101 | | | | | 528,432 | | | | | — | | | | | 845,533 | |

| | | | | | | | | | | | | | |

Total | | | | | | 16,819,987 | | | | | 11,803,012 | | | | | 56,174,210 | | | | | 836,529,216 | | | | | — | | | | | 921,326,425 | |

| | | | | | | | | | | | | | |

December 31, 2015 | | | | | | | | | | | | | | |

Trade accounts payable | | | | | | 2,466,299 | | | | | 169,397 | | | | | 107,594 | | | | | — | | | | | — | | | | | 2,743,290 | |

Due to related parties | | | | | | — | | | | | 137,267 | | | | | 27,963,100 | | | | | — | | | | | — | | | | | 28,100,367 | |

Other payables and accruals* | | | | | | 2,620,286 | | | | | 5,390,640 | | | | | 213,609 | | | | | — | | | | | — | | | | | 8,224,535 | |

Other non-current liabilities | | | | | | — | | | | | — | | | | | — | | | | | 182,200 | | | | | — | | | | | 182,200 | |

Variable interest loans | | | | 2.90 | % | | | | | — | | | | | 10,519,557 | | | | | 344,866,578 | | | | | 579,965,690 | | | | | — | | | | | 935,351,825 | |

Fixed interest loans*** | | | | | | — | | | | | 318,500 | | | | | 962,500 | | | | | 15,462,000 | | | | | — | | | | | 16,743,000 | |

| | | | | | | | | | | | | | |

Total | | | | | | 5,086,585 | | | | | 16,535,361 | | | | | 374,113,381 | | | | | 595,609,890 | | | | | — | | | | | 991,345,217 | |

| | | | | | | | | | | | | | |

|

| | * | | Unearned revenue is excluded since it is not a financial liability. |

|

| | ** | | A commitment fee of 2.4% and 0.9% is charged on the available amount of the revolving credit facility with GasLog and the available amount of the revolving credit facility of GAS-seven Ltd., respectively. |

|

| | *** | | Interest is charged at 6.0% on the outstanding amount, while the commitment fee is charged at 2.4% on the available amount of the revolving credit facility with GasLog. |

The amounts included above for variable interest rate instruments is subject to change if changes in variable interest rates differ from those estimates of interest rates determined at the end of the reporting period.

The following tables detail the Partnership’s expected cash flows for its derivative financial liabilities. The table has been drawn up based on the undiscounted contractual net cash inflows and outflows on derivative instruments that are settled on a net basis. When the amount payable or receivable is not fixed, the amount disclosed has been determined by reference to the projected interest rates as illustrated by the yield curves existing at the end of the reporting period. The

F-36

undiscounted contractual cash flows are based on the contractual maturities of the interest rate swaps.

| | | | | | | | | | | | |

| | Less

than 1

month | | 1-3 months | | 3-12 months | | 1-5 years | | 5+ years | | Total |

December 31, 2016 | | | | | | | | | | | | |

Interest rate swaps | | | | (31,065 | ) | | | | | — | | | | | (1,581,228 | ) | | | | | 5,359,222 | | | | | 819,359 | | | | | 4,566,288 | |

| | | | | | | | | | | | |

Total | | | | (31,065 | ) | | | | | — | | | | | (1,581,228 | ) | | | | | 5,359,222 | | | | | 819,359 | | | | | 4,566,288 | |

| | | | | | | | | | | | |

December 31, 2015 | | | | | | | | | | | | |

Interest rate swaps | | | | — | | | | | (364,171 | ) | | | | | (1,171,764 | ) | | | | | (901,456 | ) | | | | | — | | | | | (2,437,391 | ) | |

| | | | | | | | | | | | |

Total | | | | — | | | | | (364,171 | ) | | | | | (1,171,764 | ) | | | | | (901,456 | ) | | | | | — | | | | | (2,437,391 | ) | |

| | | | | | | | | | | | |

The Partnership expects to be able to meet its current obligations resulting from financing and operating its vessels using the liquidity existing at year-end) and the cash generated by operating activities. The Partnership expects to be able to meet its long-term obligations resulting from financing its vessels through cash generated from operations.

Credit risk

Credit risk is the risk that a counterparty will fail to discharge its obligations and cause a financial loss. The Partnership is exposed to credit risk in the event of non-performance by any of its counterparties. To limit this risk, the Partnership deals exclusively with financial institutions and customers with high credit ratings.

| | | | |

| | As of December 31, |

| | 2015 | | 2016 |

Cash and cash equivalents | | | | 62,676,654 | | | | | 50,457,609 | |

Short-term investments | | | | — | | | | | 1,500,000 | |

Trade and other receivables | | | | 5,619,945 | | | | | 3,158,171 | |

For the years ended December 31, 2014, December 31, 2015 and December 31, 2016, all of the Partnership’s revenue was earned from subsidiaries of Royal Dutch Shell plc (“Shell”) and accounts receivable were not collateralized; however, management believes that the credit risk is partially offset by the creditworthiness of the Partnership’s counterparty and the fact that the hire is being collected in advance. The Partnership did not experience credit losses on its accounts receivable portfolio during the years ended December 31, 2014, December 31, 2015 and December 31, 2016. The carrying amount of financial assets recorded in the consolidated financial statements represents the Partnership’s maximum exposure to credit risk. Management monitors exposure to credit risk, and they believe that there is no substantial credit risk arising from the Partnership’s counterparty.

The credit risk on liquid funds and derivative financial instruments is limited because the counterparties are banks with high credit ratings assigned by international credit rating agencies.

15. Capital Risk Management

The Partnership’s objectives when managing capital are to safeguard the Partnership’s ability to continue as a going concern and to pursue future growth opportunities. Among other metrics, the Partnership monitors capital using a total indebtedness to total assets ratio, which is total debt and

F-37

derivative financial instruments divided by total assets. The total indebtedness to total assets ratio is as follows:

| | | | |

| | As of December 31, |

| | 2015 | | 2016 |

Derivative financial instruments—non-current asset | | | | — | | | | | (6,008,285 | ) | |

Borrowings—current liability | | | | 333,147,449 | | | | | 45,122,489 | |

Derivative financial instruments—current liability | | | | 1,623,197 | | | | | 1,836,485 | |

Borrowings—non-current liability | | | | 533,554,751 | | | | | 768,629,652 | |

Derivative financial instruments—non-current liability | | | | 782,251 | | | | | — | |

| | | | |

Total indebtedness | | | | 869,107,648 | | | | | 809,580,341 | |

| | | | |

Total assets | | | | 1,538,214,881 | | | | | 1,489,138,934 | |

Total indebtedness/total assets | | | | 56.50 | % | | | | | 54.37 | % | |

16. Derivative Financial Instruments

The fair value of the derivative assets is as follows:

| | | | |

| | As of December 31, |

| | 2015 | | 2016 |

Derivative assets carried at fair value through profit or loss (FVTPL) | | | | |

Interest rate swaps | | | | — | | | | | 6,008,285 | |

| | | | |

Total | | | | — | | | | | 6,008,285 | |

| | | | |

Derivative financial instruments, non-current asset | | | | — | | | | | 6,008,285 | |

| | | | |

Total | | | | — | | | | | 6,008,285 | |

| | | | |

The fair value of the derivative liabilities is as follows:

| | | | |

| | As of December 31, |

| | 2015 | | 2016 |

Derivative liabilities carried at fair value through profit or loss (FVTPL) | | | | |

Interest rate swaps | | | | 2,405,448 | | | | | 1,836,485 | |

| | | | |

Total | | | | 2,405,448 | | | | | 1,836,485 | |

| | | | |

Derivative financial instruments, current liability | | | | 1,623,197 | | | | | 1,836,485 | |

Derivative financial instruments, non-current liability | | | | 782,251 | | | | | — | |

| | | | |

Total | | | | 2,405,448 | | | | | 1,836,485 | |

| | | | |

Interest rate swap agreements

The Partnership enters into interest rate swap agreements which convert the floating interest rate exposure into a fixed interest rate in order to hedge a portion of the Partnership’s exposure to fluctuations in prevailing market interest rates. Under the interest rate swaps, the counterparty effects quarterly floating-rate payments to the Partnership for the notional amount based on the three-month U.S. dollar LIBOR, and the Partnership effects quarterly payments to the counterparty on the notional amount at the respective fixed rates.

F-38

Interest rate swaps held for trading

The principal terms of the interest rate swaps held for trading were as follows:

| | | | | | | | | | | | | | |

Company | | Counterparty | | Trade

Date | | Effective

Date | | Termination

Date | | Fixed

Interest

Rate | | Notional Amount |

| | December 31,

2015 | | December 31,

2016 |

GAS-seven Ltd. | | Credit Suisse AG | | | | Mar 2012 | | | | | Nov 2013 | | | | | Nov 2020 | | | | | 2.23 | % | | | | | 96,000,000 | | | | | — | |

GAS-seven Ltd. | | Credit Suisse AG | | | | April 2014 | | | | | May 2014 | | | | | May 2019 | | | | | 1.77 | % | | | | | 32,000,000 | | | | | — | |

GasLog Partners | | GasLog | | | | Nov 2016 | | | | | Nov 2016 | | | | | July 2020 | | | | | 1.54 | % | | | | | — | | | | | 130,000,000 | |

GasLog Partners | | GasLog | | | | Nov 2016 | | | | | Nov 2016 | | | | | July 2021 | | | | | 1.63 | % | | | | | — | | | | | 130,000,000 | |

GasLog Partners | | GasLog | | | | Nov 2016 | | | | | Nov 2016 | | | | | July 2022 | | | | | 1.715 | % | | | | | — | | | | | 130,000,000 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | 128,000,000 | | | | | 390,000,000 | |

| | | | | | | | | | | | | | |

During 2014, the Partnership terminated the existing interest rate swap agreements of GAS-three Ltd., GAS-four Ltd. and GAS-five Ltd. (designated as cash flow hedging instruments and held for trading) by paying their fair values on the respective termination dates of $4,634,312 plus accrued interest of $616,235. The cumulative loss of $6,085,564 from the period that their hedging was effective was recycled to profit or loss during the year ended December 31, 2014.

In July 2016, the Partnership terminated the interest rate swap agreements of GAS-seven Ltd. associated with the Legacy Facility Refinancing (Note 7) paying their fair value on that date. The cumulative loss of $2,527,203 from the period that hedging was effective was recycled to profit or loss during the year ended December 31, 2016 (December 31, 2015: $593,225).

In November 2016, the Partnership entered into three interest rate swap agreements with GasLog at a notional aggregate value of $390,000,000, maturing between 2020 and 2022.

For the year ended December 31, 2014, the effective portion of changes in the fair value of derivatives designated as cash flow hedging instruments amounting to a loss of $367,580 has been recognized in other comprehensive income. The change in the fair value of the contracts not designated as cash flow instruments for the year ended December 31, 2016 amounted to a gain of $1,639,824 (December 31, 2015: $106,661 loss and December 31, 2014: $2,233,018 loss), which was recognized against earnings in the period incurred and is included in Loss on interest rate swaps.

An analysis of Loss on interest rate swaps is as follows:

| | | | | | |

| | For the year ended December 31, |

| | 2014 | | 2015 | | 2016 |

Realized loss on interest rate swaps held for trading | | | | (4,605,517 | ) | | | | | (2,444,536 | ) | | | | | (1,625,907 | ) | |

Unrealized (loss)/gain on interest rate swaps held for trading | | | | (2,233,018 | ) | | | | | (106,661 | ) | | | | | 1,639,824 | |

Recycled loss of cash flow hedges reclassified to profit or loss | | | | (6,085,564 | ) | | | | | (593,225 | ) | | | | | (2,527,203 | ) | |

Ineffective portion on cash flow hedges | | | | 20,874 | | | | | — | | | | | — | |

| | | | | | |

Total Loss on interest rate swaps | | | | (12,903,225 | ) | | | | | (3,144,422 | ) | | | | | (2,513,286 | ) | |

| | | | | | |

Fair value measurements

The fair value of the Partnership’s financial assets and liabilities approximate to their carrying amounts at the reporting date.

The fair value of interest rate swaps at the end of the reporting period is determined by discounting the future cash flows using the interest rate curves at the end of the reporting period and the estimation of the counterparty risk and the Partnership’s own risk inherent in the contract. The interest rate swaps met Level 2 classification, according to the fair value hierarchy as defined by IFRS 13Fair Value Measurement. There were no financial instruments in Levels 1 or 3 and no transfers between Levels 1, 2 or 3 during the periods presented. The definitions of the levels, provided by IFRS 13Fair Value Measurement, are based on the degree to which the fair value is observable:

F-39

|

| | • | | Level 1 fair value measurements are those derived from quoted prices in active markets for identical assets or liabilities; |

|

| | • | | Level 2 fair value measurements are those derived from inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly (i.e., as prices) or indirectly (i.e., derived from prices); and |

|

| | • | | Level 3 fair value measurements are those derived from valuation techniques that include inputs for the asset or liability that are not based on observable market data (unobservable inputs). |

17. Non-Cash Items on Statements of Cash Flows

As of December 31, 2016, there were capital expenditures before dropdown of $26,904,206 paid through capital contributions (December 31, 2015: $0, December 31, 2014: $0).

As of December 31, 2016, there were capital expenditures of $0 which had not been paid during the year ended December 31, 2016 and were included in current liabilities (December 31, 2015: $212,777, December 31, 2014: $179,092).

As of December 31, 2016, there were capital expenditures for vessels paid through related parties of $0 (December 31, 2015: $0, December 31, 2014: $158,204).

As of December 31, 2016, there were financing costs of $0 which had not been paid during the year ended December 31, 2016 and were included in liabilities (December 31, 2015: $30,248, December 31, 2014: $377,067).

As of December 31, 2016, there were financing costs of $1,378,785 paid through capital contributions (December 31, 2015: $0, December 31, 2014: $0).

As of December 31, 2016, there were financing costs paid by related parties of $0 (December 31, 2015: $44,193, December 31, 2014: $0).

As of December 31, 2016, there were offering costs of $5,035 which had not been paid during the year ended December 31, 2016 and were included in liabilities (December 31, 2015: $0, December 31, 2014: $86,766).

As of December 31, 2016, there were offering costs paid through related parties of $0 (December 31, 2015: $26,393, December 31, 2014: $0).

As of December 31, 2016, there were dividends declared of $0 which had not been paid during the year ended December 31, 2016 and were included in liabilities (December 31, 2015: $7,800,000, December 31, 2014: $8,810,000).

As of December 31, 2016, there were loan repayments of $1,707,522 made through capital contributions (December 31, 2015: $0, December 31, 2014: $0).

18. Earnings Per Unit

The Partnership calculates earnings per unit by allocating reported profit for each period to each class of units based on the distribution policy for available cash stated in the Partnership Agreement as generally described in Note 6 above.

Basic earnings per unit is determined by dividing profit for the year reported at the end of each period by the weighted average number of units outstanding during the period. Diluted earnings per unit is equal to basic earnings per unit since there are no potential ordinary units assumed to have been converted in common units.

On May 12, 2014, GasLog Partners completed its IPO and issued 9,822,358 common units, 9,822,358 subordinated units and 400,913 general partner units. On September 29, 2014, GasLog Partners completed an equity offering of 4,500,000 common units. In connection with this offering, the Partnership issued 91,837 general partner units to its general partner in order for GasLog to retain its 2.0%. On June 26, 2015, GasLog Partners completed an equity offering of 7,500,000 common units and issued 153,061 general partner units to its general partner in order for GasLog to

F-40

retain its 2.0%. On August 5, 2016, GasLog Partners completed an equity offering of 2,750,000 common units and issued 56,122 general partner units to its general partner in order for GasLog to retain its 2.0%. Earnings per unit is presented for the period in which the units were outstanding, with earnings calculated as follows:

| | | | | | |