Exhibit 99.1

Safe Harbor

With the exception of historical information, certain matters disclosed in this presentation are forward-looking statements. Forward-looking statements involve known and unknown risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements. Potential risks and uncertainties are described in the filings of SunEdison, Inc. (“SunEdison”) and TerraForm Power, Inc. (“TerraForm” and, together with SunEdison, the “Companies”) with the Securities and Exchange Commission (SEC), including SunEdison Inc.’s most recent report on Form 10-K, TerraForm Power, Inc.’s registration statement for its initial public offering, and each Company’s reports on Forms 10-Q and 8-K, in addition to the risks and uncertainties described on page 3 of this presentation. These forward-looking statements represent the Companies’ judgment as of the date of this presentation and the Companies disclaim any intent or obligation to update these forward-looking statements, except as otherwise required by law.

This presentation also includes non-GAAP financial measures. You can find a reconciliation of the non-GAAP financial measures to the most directly comparable GAAP financial measures in the appendix to this presentation.

TerraForm POWER

a SunEdison company

2

Forward-Looking Statements

This report contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements are subject to certain risks, uncertainties and assumptions, including the timing of the completion of the First Wind acquisition, and typically can be identified by the use of words such as “expect,” “estimate,” “anticipate,” “forecast,” “intend,” “project,” “target,” “plan,” “believe” and similar terms and expressions. Certain matters discussed in this presentation and conference call are forward-looking statements. The forward-looking statements contained in this presentation represent the SunEdison and TerraForm’s judgment as of the date of this presentation and are based on current expectations and assumptions. Although SunEdison and TerraForm believe that their expectations and assumptions are reasonable, they can give no assurance that these expectations and assumptions will prove to have been correct, and actual results may vary materially. Factors that could cause actual results to differ materially from those set forth in the forward-looking statements include, among others: the failure of counterparties to fulfill their obligations under off-take agreements; price fluctuations, termination provisions and buyout provisions in offtake agreements; TeraForm’s ability to enter into contracts to sell power on acceptable terms as offtake agreements expire; delays or unexpected costs during the completion of projects under construction; TerraForm’s ability to successfully identify, evaluate and consummate acquisitions from SunEdison, Inc. or third parties, including the acquisition of the First Wind wind generating projects from Sellers and to integrate such assets; government regulation; operating and financial restrictions under agreements governing indebtedness; SunEdison and TerraForm’s ability to borrow additional funds and access capital markets; SunEdison and TerraForm’s ability to compete against traditional and renewable energy companies; hazards customary to the power production industry and power generation operations, such as unusual weather conditions and outages, and TerraForm’s ability to operate its business efficiently and enter into new business segments or new geographies. Furthermore, any dividends are subject to available capital, market conditions and compliance with associated laws and regulations and other matters that our board of directors deem relevant. SunEdison and TerraForm undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as otherwise required by law. The foregoing review of factors that could cause SunEdison and TerraForm’s actual results to differ materially from those contemplated in the forward-looking statements included in this report should be considered in connection with information regarding risks and uncertainties that may affect SunEdison and TerraForm’s future results included in SunEdison and TerraForm’s filings with the Securities and Exchange Commission available at www.sec.gov.

TerraForm POWER

a SunEdison company

3

USA: Mt. Signal 266 MW

Section 1: Executive Summary

TerraForm POWER

a SunEdison company

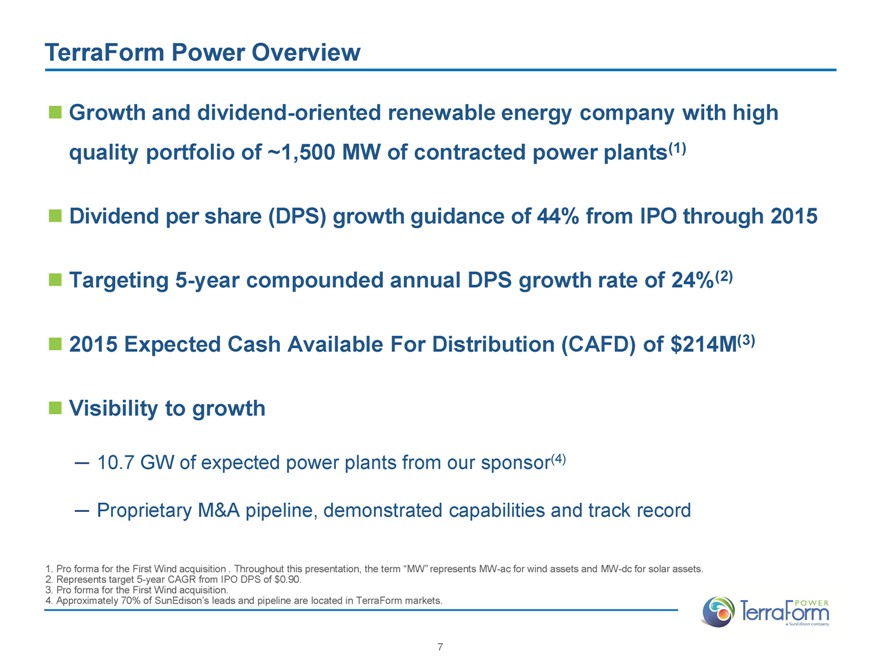

TerraForm Power Overview

Growth and dividend-oriented renewable energy company with high quality portfolio of ~1,500 MW of contracted power plants(1)

Dividend per share (DPS) growth guidance of 44% from IPO through 2015

Targeting 5-year compounded annual DPS growth rate of 24%(2)

2015 Expected Cash Available For Distribution (CAFD) of $214M(3)

Visibility to growth

10.7 GW of expected power plants from our sponsor(4)

Proprietary M&A pipeline, demonstrated capabilities and track record

1. Pro forma for the First Wind acquisition . Throughout this presentation, the term “MW” represents MW-ac for wind assets and MW-dc for solar assets.

2. Represents target 5-year CAGR from IPO DPS of $0.90.

3. Pro forma for the First Wind acquisition.

4. Approximately 70% of SunEdison’s leads and pipeline are located in TerraForm markets.

TerraForm POWER

a SunEdison company

7

TerraForm Increased Scale Since IPO

Acquisitions and drop downs since IPO have significantly increased TERP’s scale

TerraForm POWER a SunEdison company TerraForm POWER a SunEdison company % Increase

@ IPO July 2014 HUDSON ENERGY SOLAR CapitalDynamics SunEdison Drop Downs firstwind

Total MW 808 MW 1,507 MW 86%

Call Right Pipeline(1) 1.1 GW 3.3 GW 202%

2015 EBITDA Guidance $193M $360M 87%

2015 CAFD Guidance $107M $214M 100%

Dividend Guidance $0.90 $1.30 44%

Long-Term 15% 24% 60%

Dividend Growth Target

1. TerraForm also has a 6-year right of first offer on other projects that SunEdison develops in the U.S., Canada, the U.K. and Chile.

TerraForm POWER

a SunEdison company

8

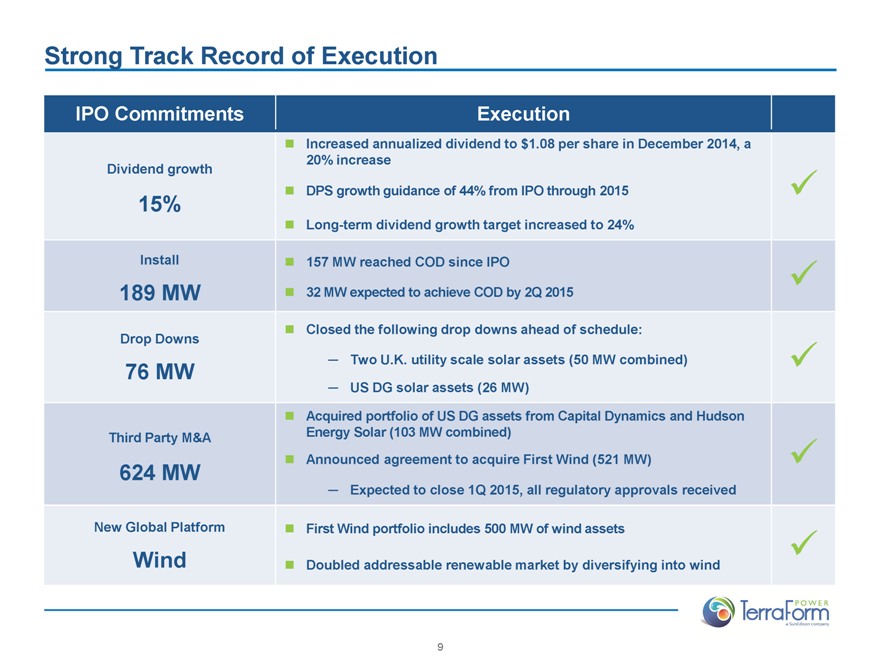

Strong Track Record of Execution

IPO Commitments Execution

Increased annualized dividend to $1.08 per share in December 2014, a 20% increase

Dividend growth

DPS growth guidance of 44% from IPO through 2015

15%

Long-term dividend growth target increased to 24%

Install 157 MW reached COD since IPO

189 MW 32 MW expected to achieve COD by 2Q 2015

Closed the following drop downs ahead of schedule:

Drop Downs

Two U.K. utility scale solar assets (50 MW combined)

76 MW

US DG solar assets (26 MW)

Third Party M&A Acquired portfolio of US DG assets from Capital Dynamics and Hudson Energy Solar (103 MW combined)

Announced agreement to acquire First Wind (521 MW)

624 MW

Expected to close 1Q 2015, all regulatory approvals received

New Global Platform First Wind portfolio includes 500 MW of wind assets

Wind Doubled addressable renewable market by diversifying into wind

TerraForm POWER

a SunEdison company

9

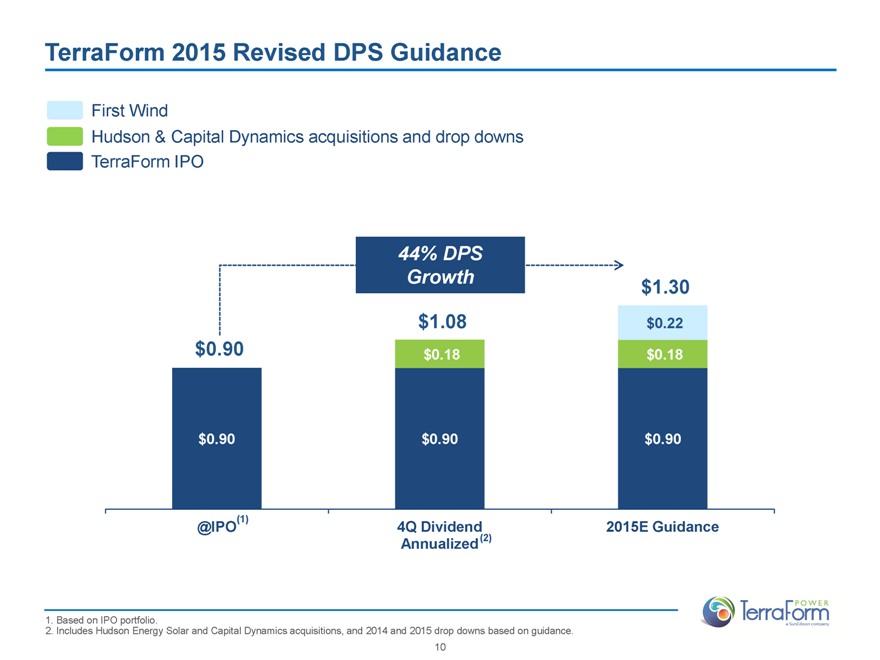

TerraForm 2015 Revised DPS Guidance

First Wind

Hudson & Capital Dynamics acquisitions and drop downs

TerraForm IPO

44% DPS Growth $1.30

$1.08 $0.22

$ 0.90 $0.18 $0.18

$0.90 $0.90 $0.90

@IPO(1) 4Q Dividend Annualized (2) 2015E Guidance

1. Based on IPO portfolio.

2. Includes Hudson Energy Solar and Capital Dynamics acquisitions, and 2014 and 2015 drop downs based on guidance.

TerraForm POWER

a SunEdison company

10

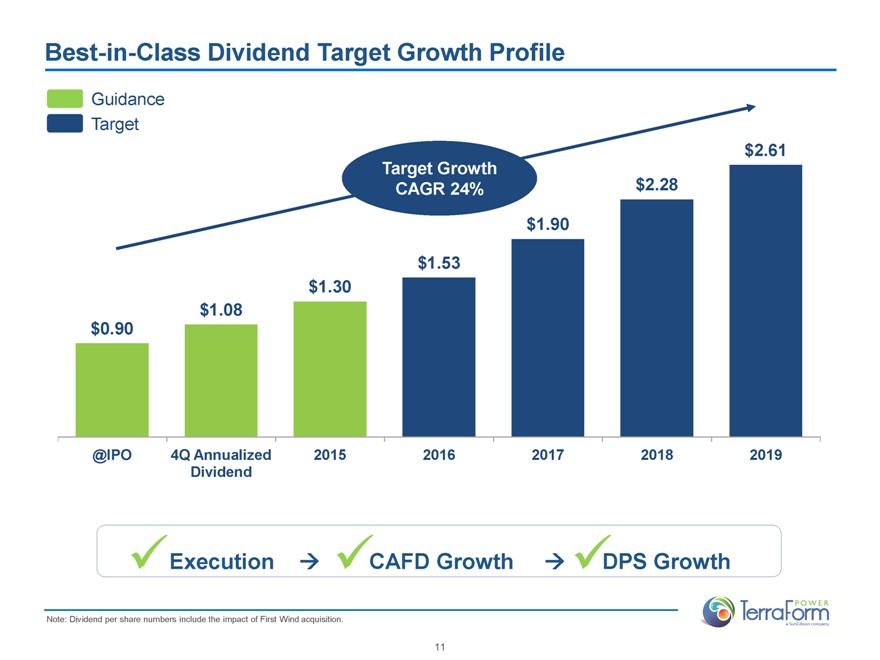

Best-in-Class Dividend Target Growth Profile

Guidance

Target

$2.61

Target Growth CAGR 24% $2.28

$1.90

$1.53

$1.30

$1.08

$0.90

@IPO 4Q Annualized Dividend 2015 2016 2017 2018 2019

Execution CAFD Growth DPS Growth

Note: Dividend per share numbers include the impact of First Wind acquisition.

TerraForm POWER

a SunEdison company

11

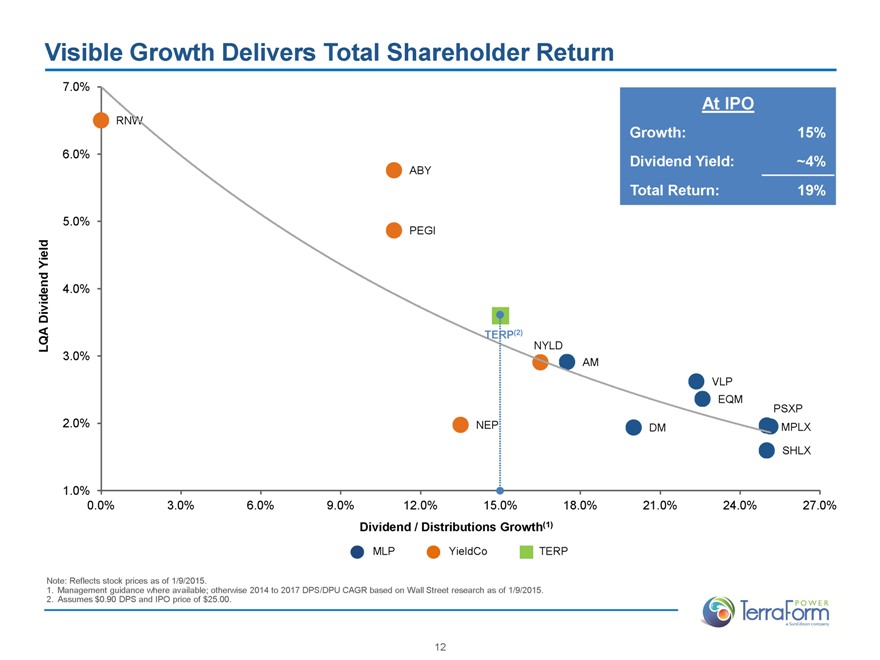

Visible Growth Delivers Total Shareholder Return

7.0%

At IPO

RNW

Growth: 15%

6.0% Dividend Yield: ~4%

ABY

Total Return: 19%

5.0%

PEGI

Yield

Dividend 4.0%

TERP(2)

LQA NYLD

3.0% AM

VLP

EQM

PSXP

2.0% NEP DM MPLX

SHLX

1.0%

0.0% 3.0% 6.0% 9.0% 12.0% 15.0% 18.0% 21.0% 24.0% 27.0%

Dividend / Distributions Growth(1)

MLP YieldCo TERP

Note: Reflects stock prices as of 1/9/2015.

1. Management guidance where available; otherwise 2014 to 2017 DPS/DPU CAGR based on Wall Street research as of 1/9/2015.

2. Assumes $0.90 DPS and IPO price of $25.00.

TerraForm POWER

a SunEdison company

12

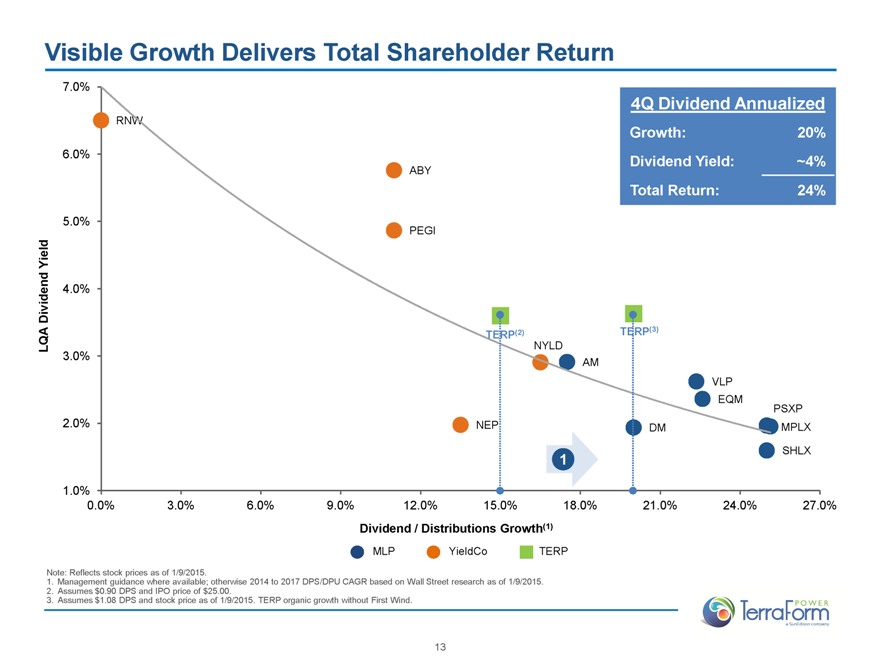

Visible Growth Delivers Total Shareholder Return

4Q Dividend Annualized

Growth: 20%

Dividend Yield: ~4%

Total Return: 24%

LQA Dividend Yield

7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0%

RNW

ABY

PEGI

TERP(2)

TERP(3)

NYLD

AM

VLP

EQM

PSXP

NEP

DM

MPLX

SHLX

1

0.0% 3.0% 6.0% 9.0% 12.0% 15.0% 18.0% 21.0% 24.0% 27.0%

Dividend / Distributions Growth(1)

MLP YieldCo TERP

Note: Reflects stock prices as of 1/9/2015.

1. Management guidance where available; otherwise 2014 to 2017 DPS/DPU CAGR based on Wall Street research as of 1/9/2015.

2. Assumes $0.90 DPS and IPO price of $25.00.

3. Assumes $1.08 DPS and stock price as of 1/9/2015. TERP organic growth without First Wind.

TerraForm POWER

a SunEdison company

13

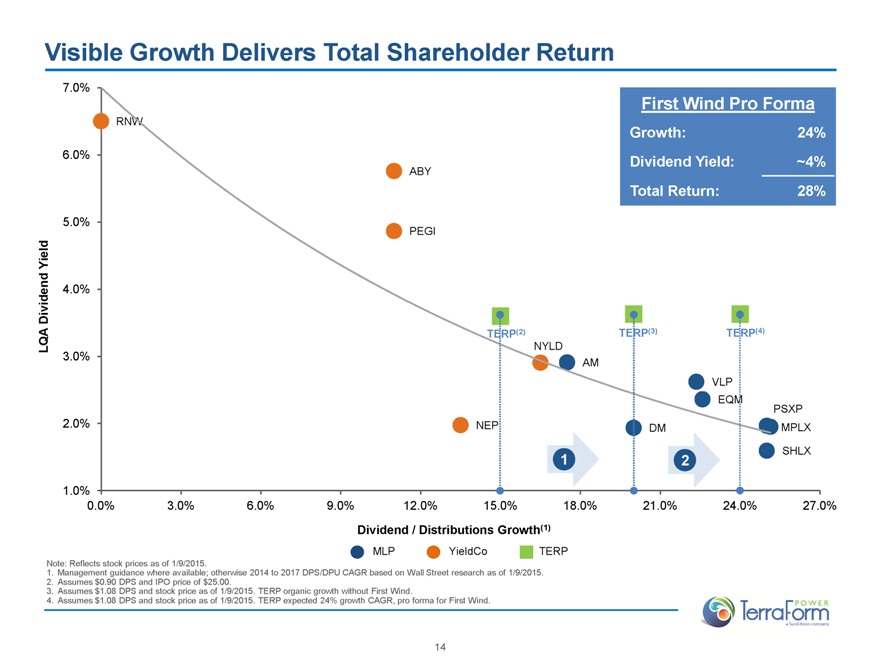

Visible Growth Delivers Total Shareholder Return

First Wind Pro Forma

Growth: 24%

Dividend Yield: ~4%

Total Return: 28%

LQA Dividend Yield

7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0%

RNW

ABY

PEGI

TERP(2)

TERP(3)

TERP(4)

NYLD

AM

VLP

EQM

PSXP

NEP

DM

MPLX

SHLX

1 2

0.0% 3.0% 6.0% 9.0% 12.0% 15.0% 18.0% 21.0% 24.0% 27.0%

Dividend / Distributions Growth(1)

MLP YieldCo TERP

Note: Reflects stock prices as of 1/9/2015.

1. Management guidance where available; otherwise 2014 to 2017 DPS/DPU CAGR based on Wall Street research as of 1/9/2015.

2. Assumes $0.90 DPS and IPO price of $25.00.

3. Assumes $1.08 DPS and stock price as of 1/9/2015. TERP organic growth without First Wind.

4. Assumes $1.08 DPS and stock price as of 1/9/2015. TERP expected 24% growth CAGR, pro forma for First Wind.

TerraForm POWER

a SunEdison company

14

Section 2: Our Portfolio

USA: Alamosa 8 MW

TerraForm POWER

a SunEdison company

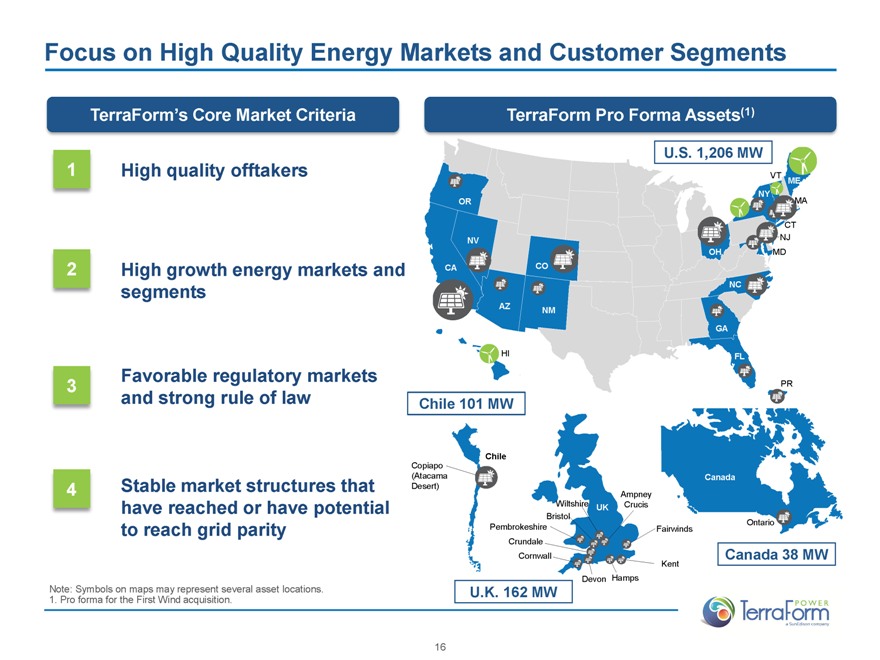

Focus on High Quality Energy Markets and Customer Segments

TerraForm’s Core Market Criteria

1 High quality offtakers

2 High growth energy markets and segments

3 Favorable regulatory markets and strong rule of law

4 Stable market structures that have reached or have potential to reach grid parity

Note: Symbols on maps may represent several asset locations.

1. Pro forma for the First Wind acquisition.

TerraForm Pro Forma Assets(1)

U.S. 1,206 MW

OR NV CA CO AZ NM HI

VT ME NY MA CT NJ MD OH NC GA FL PR

Chile 101 MW

Chile

Copiapo (Atacama Desert)

Wiltshire

UK

Ampney Crucis

Bristol

Pembrokeshire

Crundale

Cornwall

Fairwinds

Kent

Hamps

Canada

Ontario

Canada 38 MW

Devon

U.K. 162 MW

TerraForm POWER

a SunEdison company

16

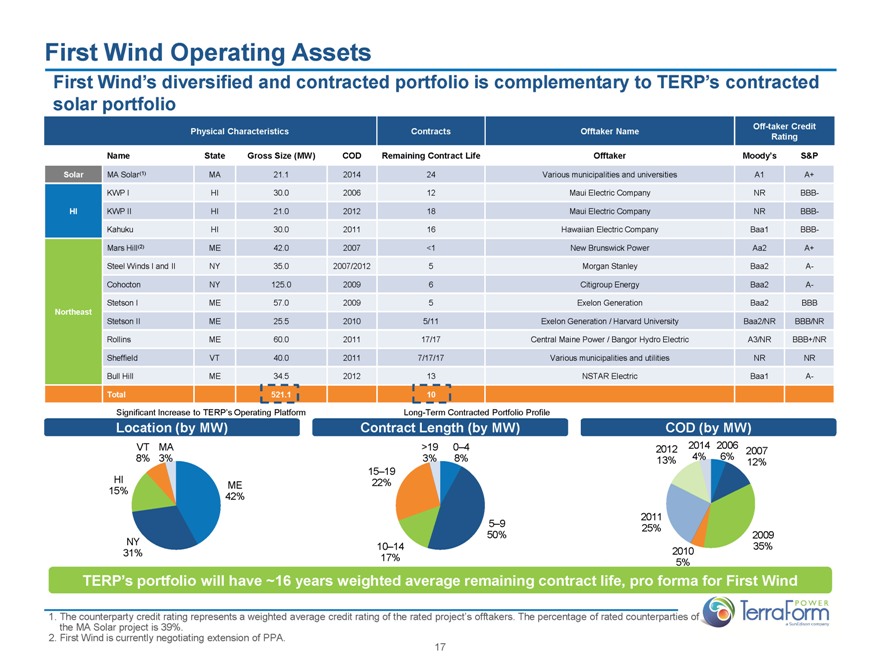

First Wind Operating Assets

First Wind’s diversified and contracted portfolio is complementary to TERP’s contracted solar portfolio

Physical Characteristics Contracts Offtaker Name Off-taker Credit Rating

Name State Gross Size (MW) COD Remaining Contract Life Offtaker Moody’s S&P

Solar MA Solar(1) MA 21.1 2014 24 Various municipalities and universities A1 A+

KWP I HI 30.0 2006 12 Maui Electric Company NR BBB-

HI KWP II HI 21.0 2012 18 Maui Electric Company NR BBB-

Kahuku HI 30.0 2011 16 Hawaiian Electric Company Baa1 BBB-

Mars Hill(2) ME 42.0 2007 <1 New Brunswick Power Aa2 A+

Steel Winds I and II NY 35.0 2007/2012 5 Morgan Stanley Baa2 A-

Cohocton NY 125.0 2009 6 Citigroup Energy Baa2 A-

Stetson I ME 57.0 2009 5 Exelon Generation Baa2 BBB Northeast

Stetson II ME 25.5 2010 5/11 Exelon Generation / Harvard University Baa2/NR BBB/NR

Rollins ME 60.0 2011 17/17 Central Maine Power / Bangor Hydro Electric A3/NR BBB+/NR

Sheffield VT 40.0 2011 7/17/17 Various municipalities and utilities NR NR

Bull Hill ME 34.5 2012 13 NSTAR Electric Baa1 A-

Total 521.1 10

Significant Increase to TERP’s Operating Platform

Location (by MW)

VT 8%

MA 3%

HI 15%

ME 42%

NY 31%

Long-Term Contracted Portfolio Profile

Contract Length (by MW)

>19 3%

0–4 8%

15–19 22%

10–14 17%

5–9 50%

COD (by MW)

2012 13%

2014 4%

2006 6%

2007 12%

2011 25%

2009 35%

2010 5%

TERP’s portfolio will have ~16 years weighted average remaining contract life, pro forma for First Wind

1. The counterparty credit rating represents a weighted average credit rating of the rated project’s offtakers. The percentage of rated counterparties of the MA Solar project is 39%.

2. First Wind is currently negotiating extension of PPA.

TerraForm POWER

a SunEdison company

17

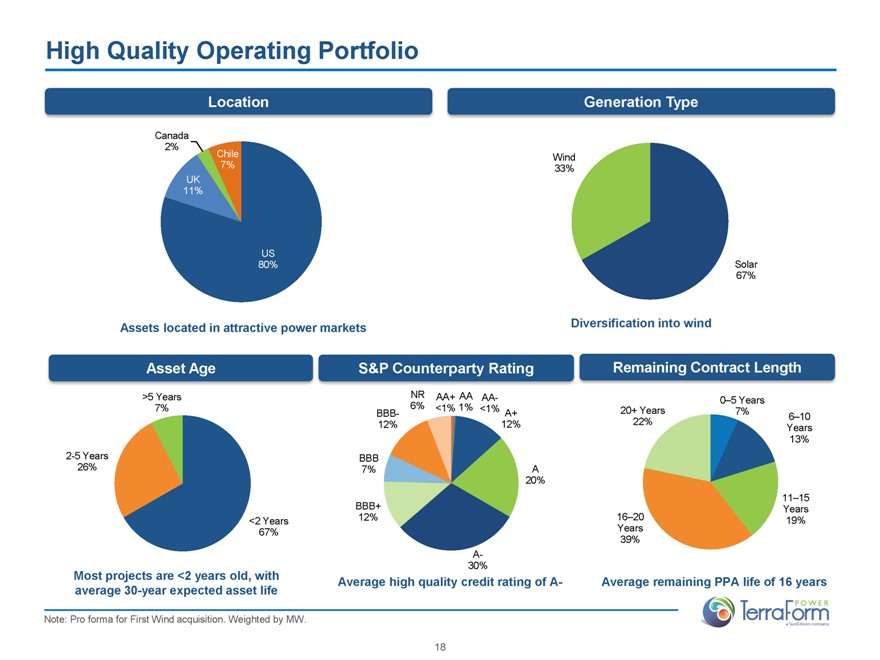

High Quality Operating Portfolio

Location

Canada 2%

Chile 7%

UK 11%

US 80%

Assets located in attractive power markets

Generation Type

Wind 33%

Solar 67%

Diversification into wind

Asset Age

>5 Years 7%

2-5 Years 26%

<2 Years 67%

Most projects are <2 years old, with

average 30-year expected asset life

S&P Counterparty Rating

NR 6%

AA+ <1%

AA 1%

AA- <1%

A+ 12%

A 20%

A- 30%

BBB+ 12%

BBB 7%

BBB- 12%

Average high quality credit rating of A-

Remaining Contract Length

0–5 Years 7%

20+ Years 22%

6–10 Years 13%

11–15 Years 19%

16–20 Years 39%

Average remaining PPA life of 16 years

Note: Pro forma for First Wind acquisition. Weighted by MW.

TerraForm POWER

a SunEdison company

18

USA: KWP I 30 MW

Section 3: Key Growth Drivers

TerraForm POWER

a SunEdison company

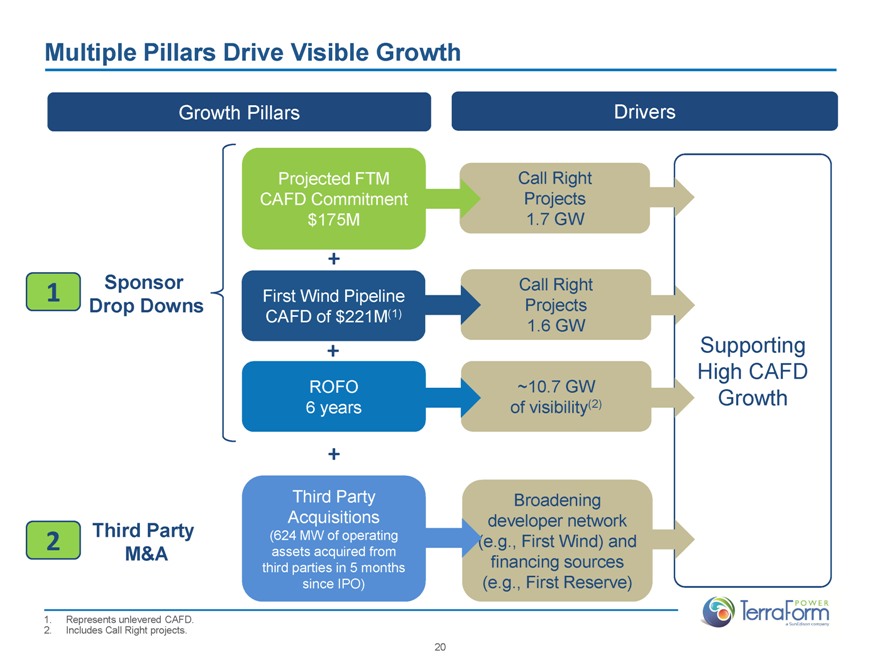

Multiple Pillars Drive Visible Growth

| | | | | | | | |

| | | Growth Pillars | | Drivers | | |

| | | | | Projected FTM CAFD Commitment $175M | | Call Right Projects 1.7 GW | | |

| | | | | + | | | | |

1 | | Sponsor Drop Downs | | First Wind Pipeline CAFD of $221M(1) | | Call Right Projects 1.6 GW | | |

| | | | | + | | | | Supporting High CAFD Growth |

| | | | | ROFO 6 years | | ~10.7 GW of visibility(2) | | |

| | | | | + | | | | |

2 | | Third Party M&A | | Third Party Acquisitions (624 MW of operating assets acquired from third parties in 5 months since IPO) | | Broadening developer network (e.g., First Wind) and financing sources (e.g., First Reserve) | | |

1. Represents unlevered CAFD.

2. Includes Call Right projects.

TerraForm POWER

a SunEdison company

20

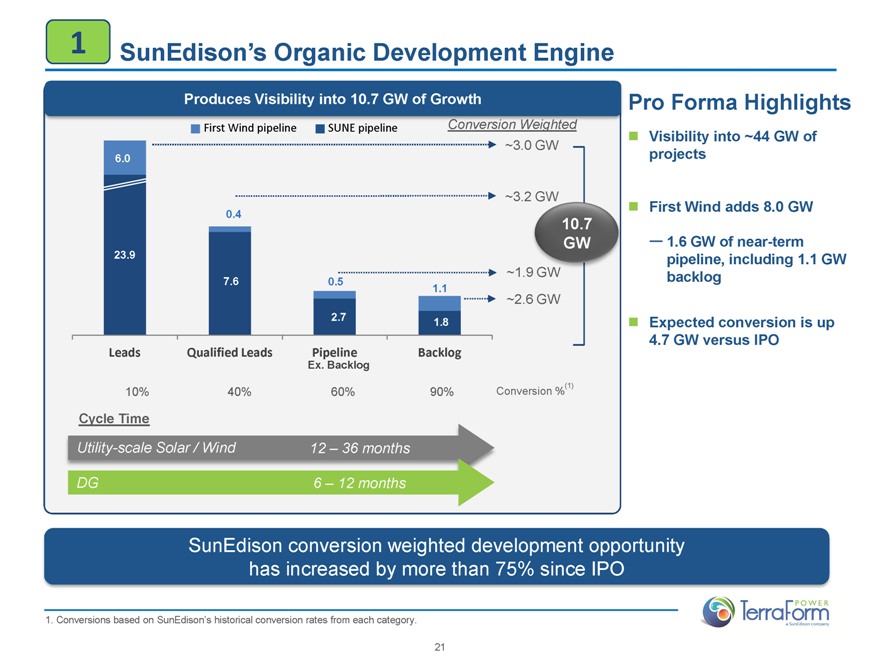

1 SunEdison’s Organic Development Engine

Produces Visibility into 10.7 GW of Growth

First Wind pipeline SUNE pipeline Conversion Weighted

6.0 ~3.0 GW

~3.2 GW

0.4 10.7 GW

23.9 ~1.9 GW

7.6 0.5 1.1 ~2.6 GW

2.7 1.8

Leads 10%

Qualified Leads 40%

Pipeline Ex. Backlog 60%

Backlog 90%

Conversion %(1)

Cycle Time

Utility-scale Solar / Wind

12 – 36 months

DG

6 – 12 months

Pro Forma Highlights

Visibility into ~44 GW of projects

First Wind adds 8.0 GW

1.6 GW of near-term pipeline, including 1.1 GW backlog

Expected conversion is up 4.7 GW versus IPO

SunEdison conversion weighted development opportunity has increased by more than 75% since IPO

1. Conversions based on SunEdison’s historical conversion rates from each category.

TerraForm POWER

a SunEdison company

21

1

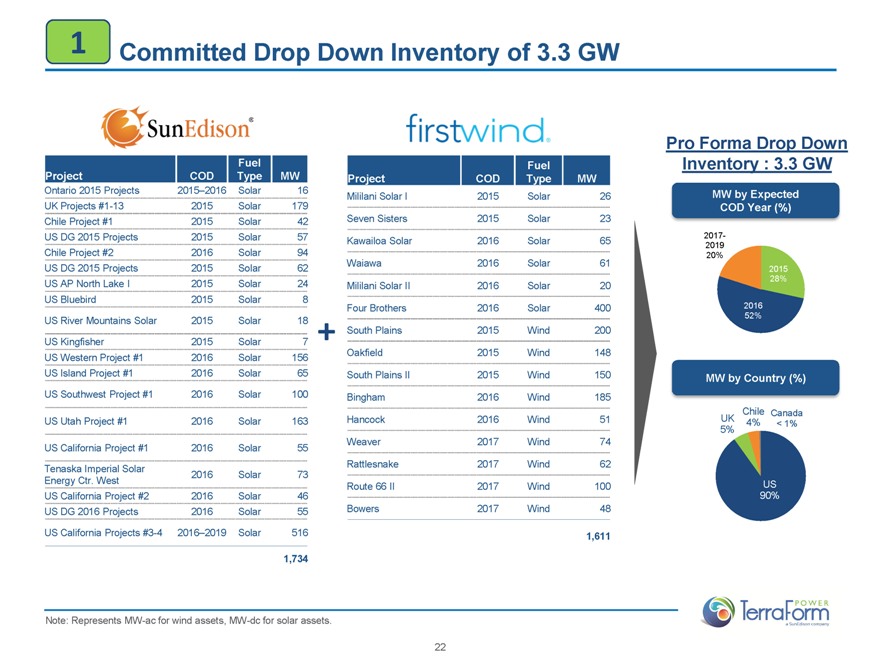

Committed Drop Down Inventory of 3.3 GW

SunEdisonR

Project COD Fuel Type MW

Ontario 2015 Projects 2015–2016 Solar 16

UK Projects #1-13 2015 Solar 179

Chile Project #1 2015 Solar 42

US DG 2015 Projects 2015 Solar 57

Chile Project #2 2016 Solar 94

US DG 2015 Projects 2015 Solar 62

US AP North Lake I 2015 Solar 24

US Bluebird 2015 Solar 8

US River Mountains Solar 2015 Solar 18

US Kingfisher 2015 Solar 7

US Western Project #1 2016 Solar 156

US Island Project #1 2016 Solar 65

US Southwest Project #1 2016 Solar 100

US Utah Project #1 2016 Solar 163

US California Project #1 2016 Solar 55

Tenaska Imperial Solar 2016 Solar 73

Energy Ctr. West

US California Project #2 2016 Solar 46

US DG 2016 Projects 2016 Solar 55

US California Projects #3-4 2016–2019 Solar 516

1,734

+

firstwindR

Project COD Fuel Type MW

Mililani Solar I 2015 Solar 26

Seven Sisters 2015 Solar 23

Kawailoa Solar 2016 Solar 65

Waiawa 2016 Solar 61

Mililani Solar II 2016 Solar 20

Four Brothers 2016 Solar 400

South Plains 2015 Wind 200

Oakfield 2015 Wind 148

South Plains II 2015 Wind 150

Bingham 2016 Wind 185

Hancock 2016 Wind 51

Weaver 2017 Wind 74

Rattlesnake 2017 Wind 62

Route 66 II 2017 Wind 100

Bowers 2017 Wind 48

1,611

Pro Forma Drop Down

Inventory : 3.3 GW

MW by Expected

COD Year (%)

2017-

2019

20%

2015

28%

2016

52%

MW by Country (%)

Chile Canada

UK 4% < 1%

5%

US

90%

Note: Represents MW-ac for wind assets, MW-dc for solar assets.

POWER

TerraForm

a SunEdison company

22

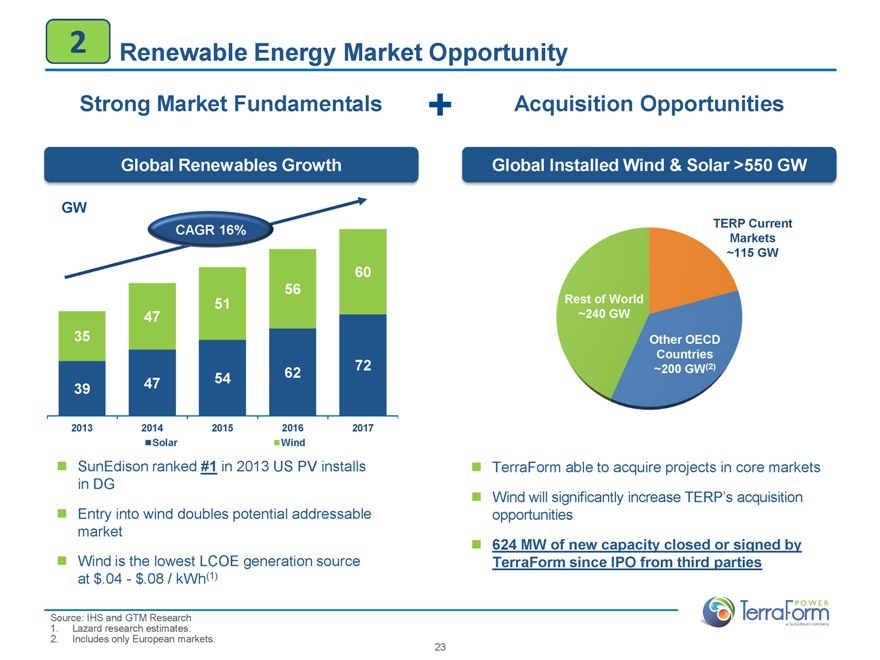

2

Renewable Energy Market Opportunity

Strong Market Fundamentals

+

Acquisition Opportunities

Global Renewables Growth

GW

CAGR 16%

60

56

51

47

35

72

47 54 62

39

2013 2014 2015 2016 2017

Solar Wind

SunEdison ranked #1 in 2013 US PV installs in DG

Entry into wind doubles potential addressable market

Wind is the lowest LCOE generation source at $.04 - $.08 / kWh(1)

Global Installed Wind & Solar >550 GW

TERP Current

Markets

~115 GW

Rest of World

~240 GW

Other OECD

Countries

~200 GW(2)

TerraForm able to acquire projects in core markets

Wind will significantly increase TERP’s acquisition opportunities

624 MW of new capacity closed or signed by TerraForm since IPO from third parties

Source: IHS and GTM Research

1. Lazard research estimates.

2. Includes only European markets.

POWER

TerraForm

a SunEdison company

23

2

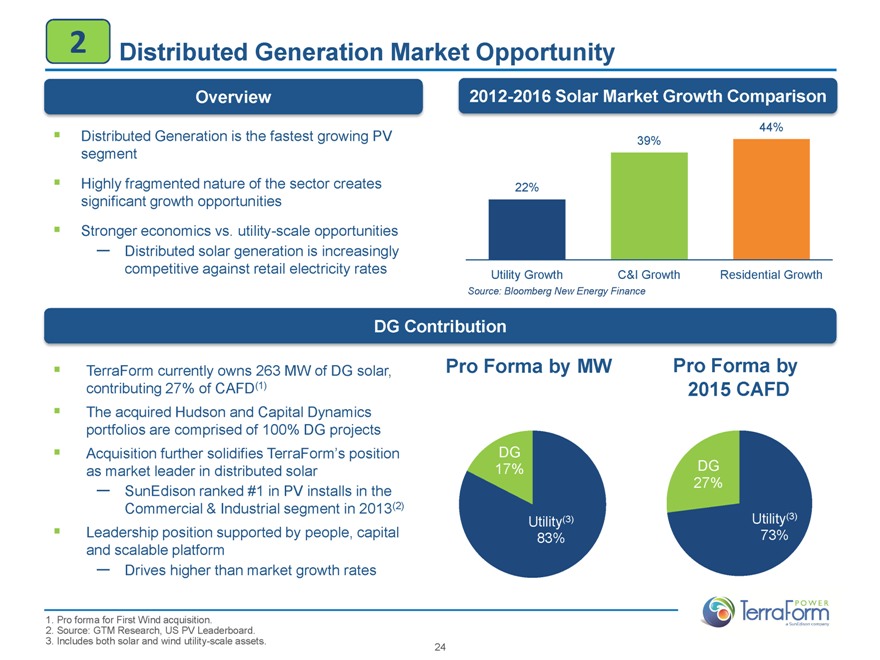

Distributed Generation Market Opportunity

Overview

Distributed Generation is the fastest growing PV segment

Highly fragmented nature of the sector creates significant growth opportunities

Stronger economics vs. utility-scale opportunities

— Distributed solar generation is increasingly competitive against retail electricity rates

2012-2016 Solar Market Growth Comparison

22%

39%

44%

Utility Growth C&I Growth Residential Growth

Source: Bloomberg New Energy Finance

DG Contribution

TerraForm currently owns 263 MW of DG solar, contributing 27% of CAFD(1)

The acquired Hudson and Capital Dynamics portfolios are comprised of 100% DG projects

Acquisition further solidifies TerraForm’s position as market leader in distributed solar

— SunEdison ranked #1 in PV installs in the Commercial & Industrial segment in 2013(2)

Leadership position supported by people, capital and scalable platform

— Drives higher than market growth rates

Pro Forma by MW

DG

17%

Utility(3)

83%

Pro Forma by

2015 CAFD

DG

27%

Utility(3)

73%

1. Pro forma for First Wind acquisition.

2. Source: GTM Research, US PV Leaderboard.

3. Includes both solar and wind utility-scale assets.

POWER

TerraForm

a SunEdison company

24

2

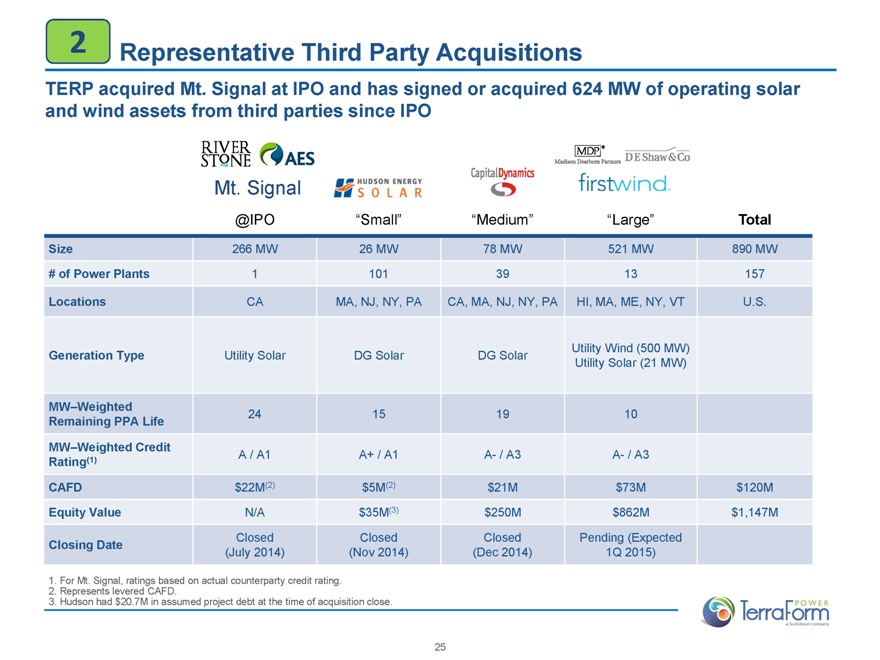

Representative Third Party Acquisitions

TERP acquired Mt. Signal at IPO and has signed or acquired 624 MW of operating solar and wind assets from third parties since IPO

RIVER

STONE AES

Mt. Signal

HUDSON ENERGY

SOLAR

CapitalDynamics

MDPR

Madison Dearborn Partners

FirstwindR

DEShaw&Co

@IPO “Small” “Medium” “Large” Total

Size 266 MW 26 MW 78 MW 521 MW 890 MW

# of Power Plants 1 101 39 13 157

Locations CA MA, NJ, NY, PA CA, MA, NJ, NY, PA HI, MA, ME, NY, VT U.S.

Generation Type Utility Solar DG Solar DG Solar Utility Wind (500 MW)

Utility Solar (21 MW)

MW–Weighted 24 15 19 10

Remaining PPA Life

MW–Weighted Credit

Rating(1) A / A1 A+ / A1 A- / A3 A- / A3

CAFD $22M(2) $5M(2) $21M $73M $120M

Equity Value N/A $35M(3) $250M $862M $1,147M

Closed Closed Closed Pending (Expected

Closing Date (July 2014) (Nov 2014) (Dec 2014) 1Q 2015)

1. For Mt. Signal, ratings based on actual counterparty credit rating.

2. Represents levered CAFD.

3. Hudson had $20.7M in assumed project debt at the time of acquisition close.

25

POWER

TerraForm

a SunEdison company

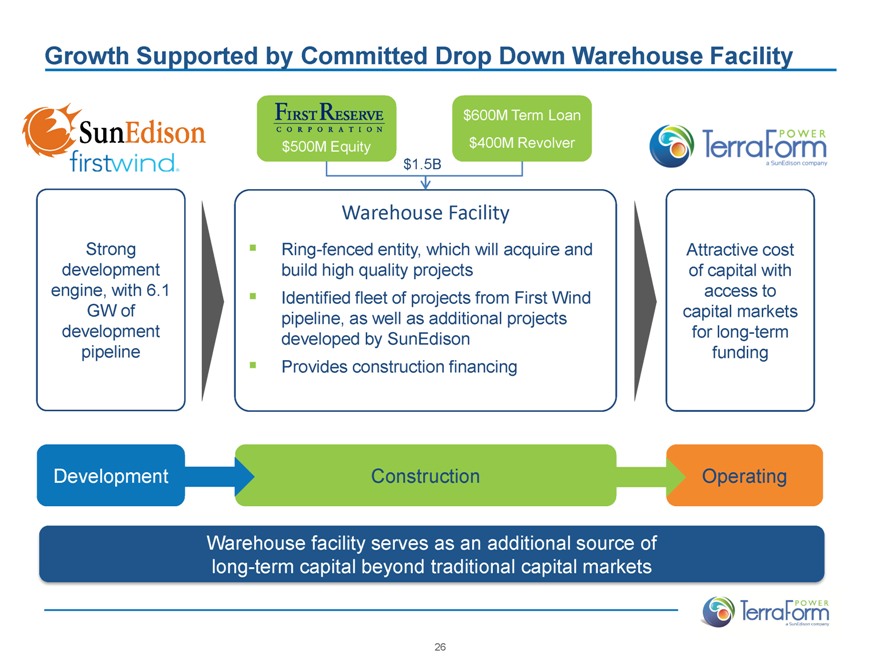

Growth Supported by Committed Drop Down Warehouse Facility

SunEdison

firstwind

Strong development engine, with 6.1 GW of development pipeline

First Reserve

CORPORATION

$500M Equity

$1.5B

$600M Term Loan

$400M Revolver

Warehouse Facility

Ring-fenced entity, which will acquire and build high quality projects

Identified fleet of projects from First Wind pipeline, as well as additional projects developed by SunEdison

Provides construction financing

POWER

TerraForm

a SunEdison company

Attractive cost of capital with access to capital markets for long-term funding

Development

Construction

Operating

Warehouse facility serves as an additional source of long-term capital beyond traditional capital markets

POWER

TerraForm

a SunEdison company

26

USA: DG 2009-2013 Portfolio of 15.2 MW

Section 4: Financials

POWER

TerraForm

a SunEdison company

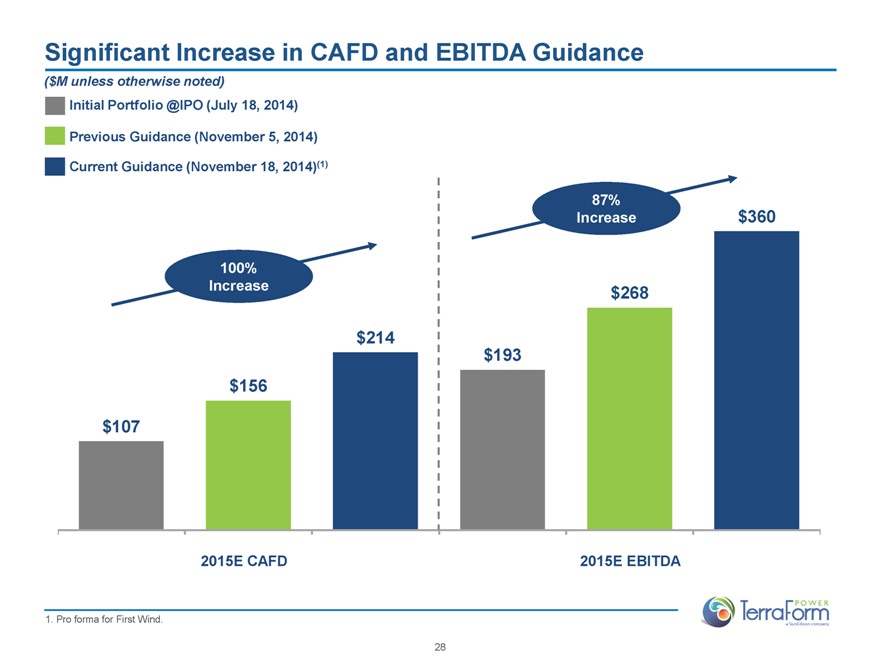

Significant Increase in CAFD and EBITDA Guidance

($M unless otherwise noted)

Initial Portfolio @IPO (July 18, 2014)

Previous Guidance (November 5, 2014)

Current Guidance (November 18, 2014)(1)

100%

Increase

$107

$156

$214

87%

Increase

$193

$268

$360

2015E CAFD

2015E EBITDA

1. Pro forma for First Wind.

POWER

TerraForm

a SunEdison company

28

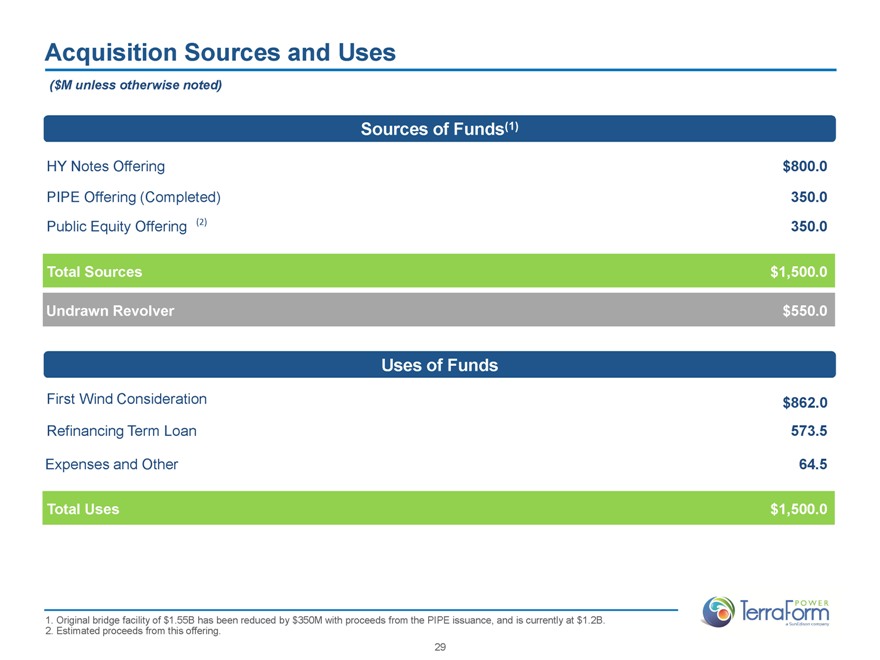

Acquisition Sources and Uses

($M unless otherwise noted)

Sources of Funds(1)

HY Notes Offering

$800.0

PIPE Offering (Completed)

350.0

Public Equity Offering (2)

350.0

Total Sources

$1,500.0

Undrawn Revolver

$550.0

Uses of Funds

First Wind Consideration

$862.0

Refinancing Term Loan

573.5

Expenses and Other

64.5

Total Uses

$1,500.0

1. Original bridge facility of $1.55B has been reduced by $350M with proceeds from the PIPE issuance, and is currently at $1.2B.

2. Estimated proceeds from this offering.

POWER

TerraForm

a SunEdison company

29

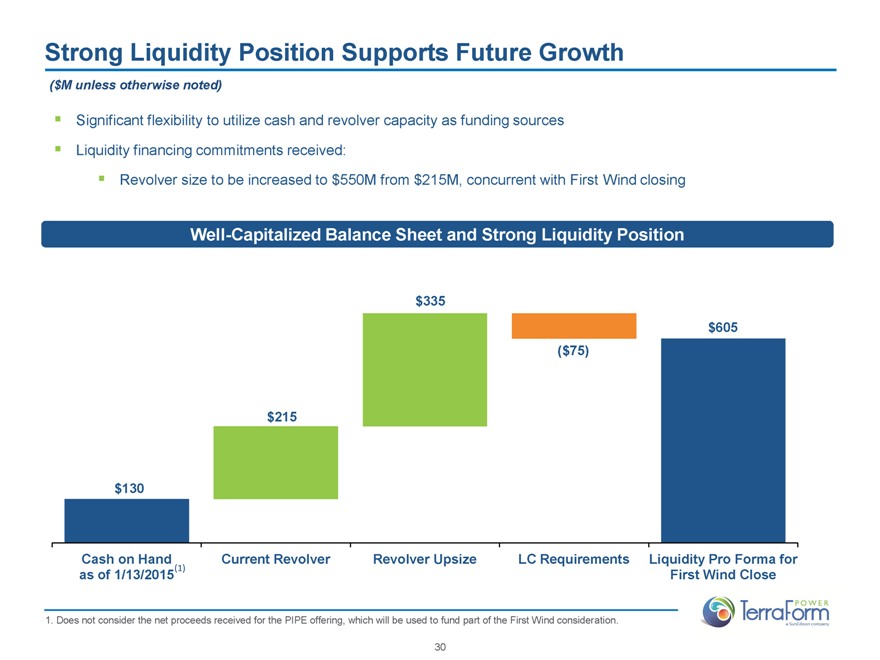

Strong Liquidity Position Supports Future Growth

($M unless otherwise noted)

Significant flexibility to utilize cash and revolver capacity as funding sources Liquidity financing commitments received:

Revolver size to be increased to $550M from $215M, concurrent with First Wind closing

Well-Capitalized Balance Sheet and Strong Liquidity Position

$335

$605

($75)

$215

$130

Cash on Hand

as of 1/13/2015(1)

Current Revolver

Revolver Upsize

LC Requirements

Liquidity Pro Forma for

First Wind Close

1. Does not consider the net proceeds received for the PIPE offering, which will be used to fund part of the First Wind consideration.

POWER

TerraForm

A SunEdison Company

30

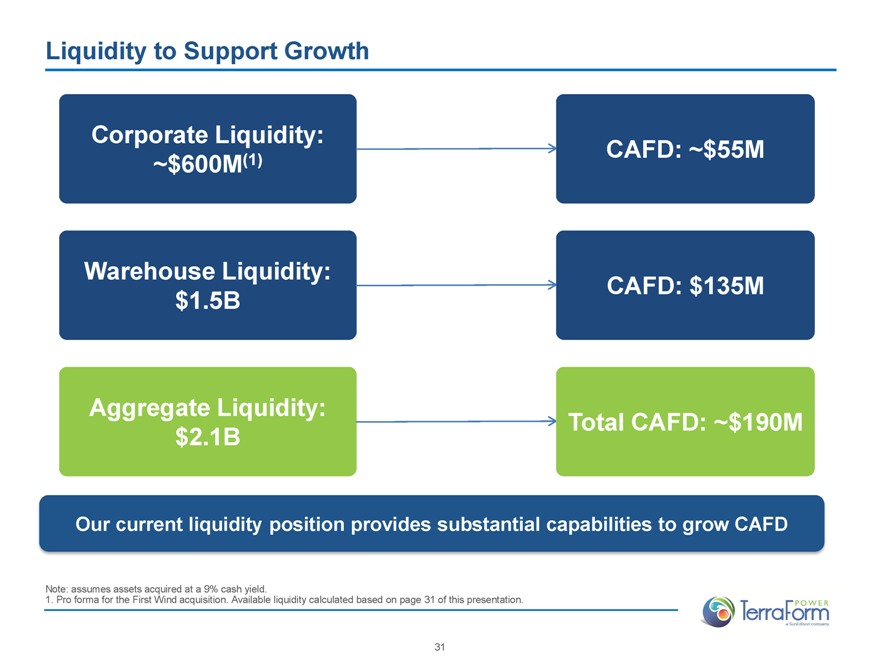

Liquidity to Support Growth

Corporate Liquidity:

~$600M(1) CAFD: ~$55M

Warehouse Liquidity: CAFD: $135M

$1.5B

Aggregate Liquidity: Total CAFD: ~$190M

$2.1B

Our current liquidity position provides substantial capabilities to grow CAFD

Note: assumes assets acquired at a 9% cash yield.

1. Pro forma for the First Wind acquisition. Available liquidity calculated based on page 31 of this presentation.

POWER

TerraForm

A SunEdison Company

31

Section 5: Summary

USA: Stetson Wind I 57 MW

POWER

TerraForm

A SunEdison Company

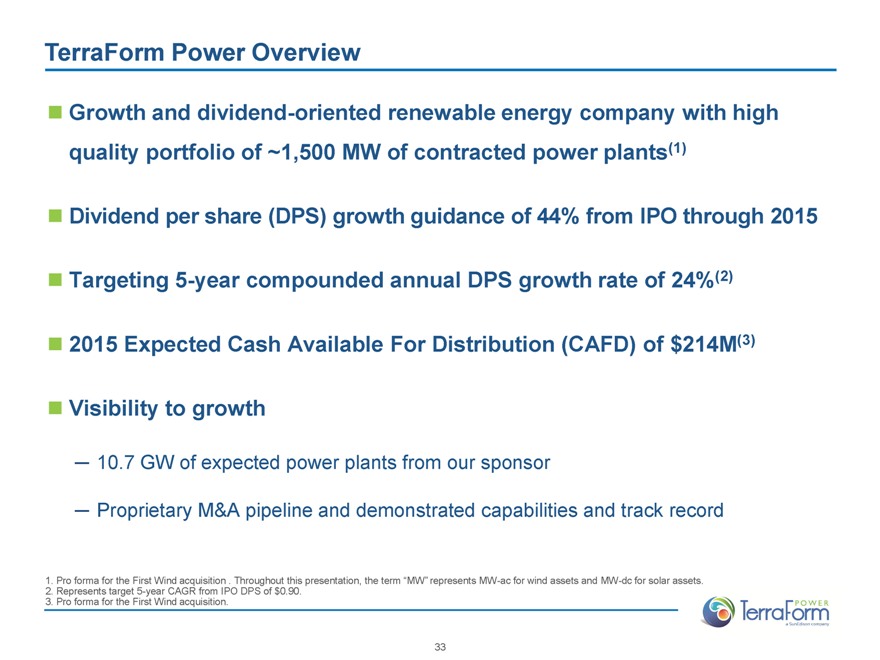

TerraForm Power Overview

Growth and dividend-oriented renewable energy company with high quality portfolio of ~1,500 MW of contracted power plants(1)

Dividend per share (DPS) growth guidance of 44% from IPO through 2015 Targeting 5-year compounded annual DPS growth rate of 24%(2) 2015 Expected Cash Available For Distribution (CAFD) of $214M(3)

Visibility to growth

10.7 GW of expected power plants from our sponsor

Proprietary M&A pipeline and demonstrated capabilities and track record

1. Pro forma for the First Wind acquisition . Throughout this presentation, the term “MW” represents MW-ac for wind assets and MW-dc for solar assets.

2. Represents target 5-year CAGR from IPO DPS of $0.90.

3. Pro forma for the First Wind acquisition.

POWER

TerraForm

A SunEdison Company

33

Appendix

USA: Nellis Air Force Base 14 MW

POWER

TerraForm

A SunEdison company

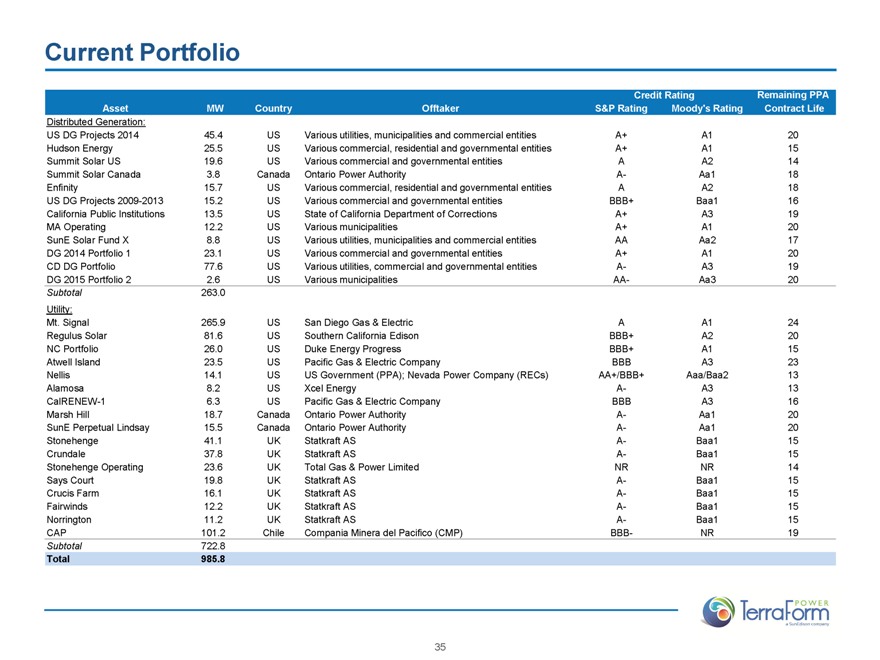

Current Portfolio

Credit Rating Remaining PPA

Asset MW Country Offtaker S&P Rating Moody’s Rating Contract Life

Distributed Generation:

US DG Projects 2014 45.4 US Various utilities, municipalities and commercial entities A+ A1 20

Hudson Energy 25.5 US Various commercial, residential and governmental entities A+ A1 15

Summit Solar US 19.6 US Various commercial and governmental entities A A2 14

Summit Solar Canada 3.8 Canada Ontario Power Authority A- Aa1 18

Enfinity 15.7 US Various commercial, residential and governmental entities A A2 18

US DG Projects 2009-2013 15.2 US Various commercial and governmental entities BBB+ Baa1 16

California Public Institutions 13.5 US State of California Department of Corrections A+ A3 19

MA Operating 12.2 US Various municipalities A+ A1 20

SunE Solar Fund X 8.8 US Various utilities, municipalities and commercial entities AA Aa2 17

DG 2014 Portfolio 1 23.1 US Various commercial and governmental entities A+ A1 20

CD DG Portfolio 77.6 US Various utilities, commercial and governmental entities A- A3 19

DG 2015 Portfolio 2 2.6 US Various municipalities AA- Aa3 20

Subtotal 263.0

Utility:

Mt. Signal 265.9 US San Diego Gas & Electric A A1 24

Regulus Solar 81.6 US Southern California Edison BBB+ A2 20

NC Portfolio 26.0 US Duke Energy Progress BBB+ A1 15

Atwell Island 23.5 US Pacific Gas & Electric Company BBB A3 23

Nellis 14.1 US US Government (PPA); Nevada Power Company (RECs) AA+/BBB+ Aaa/Baa2 13

Alamosa 8.2 US Xcel Energy A- A3 13

CalRENEW-1 6.3 US Pacific Gas & Electric Company BBB A3 16

Marsh Hill 18.7 Canada Ontario Power Authority A- Aa1 20

SunE Perpetual Lindsay 15.5 Canada Ontario Power Authority A- Aa1 20

Stonehenge 41.1 UK Statkraft AS A- Baa1 15

Crundale 37.8 UK Statkraft AS A- Baa1 15

Stonehenge Operating 23.6 UK Total Gas & Power Limited NR NR 14

Says Court 19.8 UK Statkraft AS A- Baa1 15

Crucis Farm 16.1 UK Statkraft AS A- Baa1 15

Fairwinds 12.2 UK Statkraft AS A- Baa1 15

Norrington 11.2 UK Statkraft AS A- Baa1 15

CAP 101.2 Chile Compania Minera del Pacifico (CMP) BBB- NR 19

Subtotal 722.8

Total 985.8

35

POWER

TerraForm

A SunEdison company

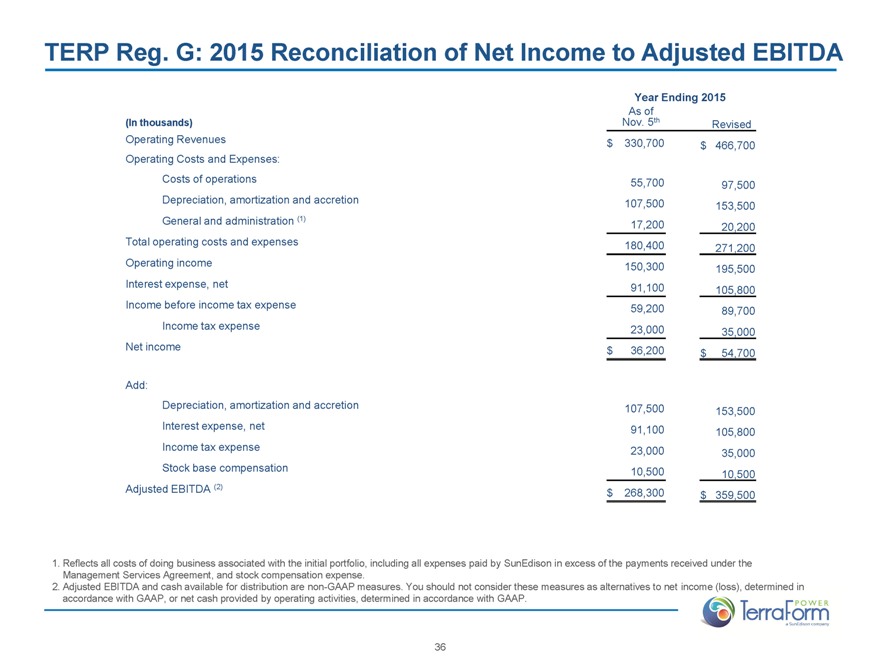

TERP Reg. G: 2015 Reconciliation of Net Income to Adjusted EBITDA

Year Ending 2015

As of

(In thousands)

Nov. 5th Revised

Operating Revenues

$ 330,700 $ 466,700

Operating Costs and Expenses:

Costs of operations

55,700 97,500

Depreciation, amortization and accretion

107,500 153,500

General and administration (1)

17,200 20,200

Total operating costs and expenses

180,400 271,200

Operating income

150,300 195,500

Interest expense, net

91,100 105,800

Income before income tax expense

59,200 89,700

Income tax expense

23,000 35,000

Net income

$ 36,200 $ 54,700

Add:

Depreciation, amortization and accretion

107,500 153,500

Interest expense, net

91,100 105,800

Income tax expense

23,000 35,000

Stock base compensation

10,500 10,500

Adjusted EBITDA (2)

$ 268,300 $ 359,500

1. Reflects all costs of doing business associated with the initial portfolio, including all expenses paid by SunEdison in excess of the payments received under the Management Services Agreement, and stock compensation expense.

2. Adjusted EBITDA and cash available for distribution are non-GAAP measures. You should not consider these measures as alternatives to net income (loss), determined in accordance with GAAP, or net cash provided by operating activities, determined in accordance with GAAP.

36

POWER

TerraForm

A SunEdison company

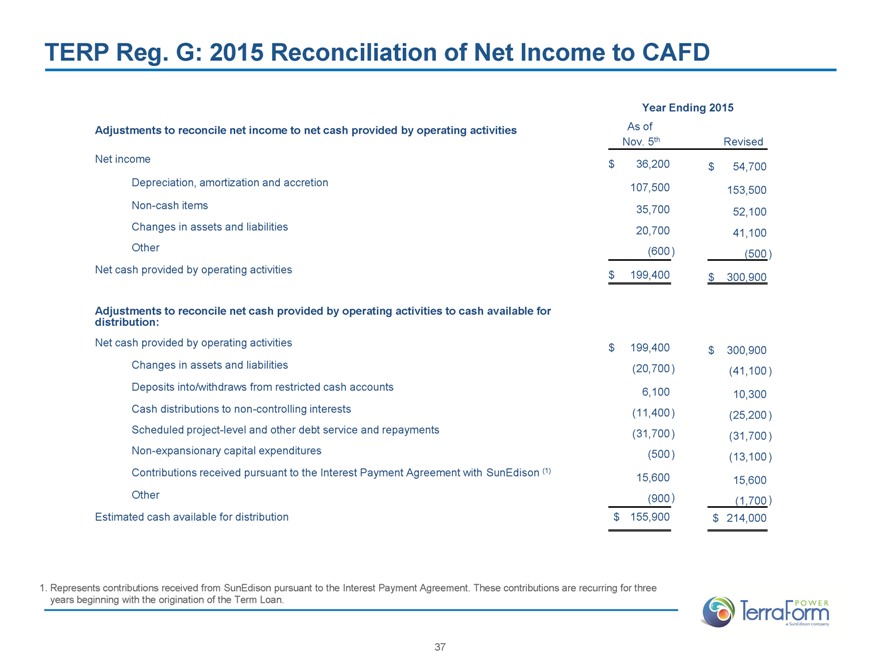

TERP Reg. G: 2015 Reconciliation of Net Income to CAFD

Year Ending 2015

Adjustments to reconcile net income to net cash provided by operating activities As of

Nov. 5th Revised

Net income $36,200 $54,700

Depreciation, amortization and accretion 107,500 153,500

Non-cash items 35,700 52,100

Changes in assets and liabilities 20,700 41,100

Other (600) (500)

Net cash provided by operating activities $199,400 $300,900

Adjustments to reconcile net cash provided by operating activities to cash available for distribution:

Net cash provided by operating activities $199,400 $300,900

Changes in assets and liabilities (20,700) (41,100)

Deposits into/withdraws from restricted cash accounts 6,100 10,300

Cash distributions to non-controlling interests (11,400) (25,200)

Scheduled project-level and other debt service and repayments (31,700) (31,700)

Non-expansionary capital expenditures (500) (13,100)

Contributions received pursuant to the Interest Payment Agreement with SunEdison (1) 15,600 15,600

Other (900) (1,700)

Estimated cash available for distribution $155,900 $214,000

1. Represents contributions received from SunEdison pursuant to the Interest Payment Agreement. These contributions are recurring for three years beginning with the origination of the Term Loan.

37

POWER

TerraForm

A SunEdison company