As filed with the Securities and Exchange Commission on November 18, 2016

Registration No. 333-194280

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Post-Effective Amendment No. 8

to

FORM S-11

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

_______________________

GRIFFIN CAPITAL ESSENTIAL ASSET REIT II, INC.

(Exact Name of Registrant as Specified in Its Governing Instruments)

Griffin Capital Plaza

1520 E. Grand Avenue

El Segundo, California 90245

(310) 469-6100

(Address, Including Zip Code and Telephone Number,

Including Area Code, of Registrant’s Principal Executive Offices)

Kevin A. Shields

Chief Executive Officer

Griffin Capital Essential Asset REIT II, Inc.

Griffin Capital Plaza

1520 E. Grand Avenue

El Segundo, California 90245

(310) 469-6100

(Name, Address, Including Zip Code and Telephone Number,

Including Area Code, of Agent for Service)

Copies to:

Michael K. Rafter, Esq.

Nelson Mullins Riley & Scarborough LLP

Atlantic Station

201 17th Street NW, Suite 1700

Atlanta, Georgia 30363

(404) 322-6000

_______________________

Approximate date of commencement of proposed sale to the public: As soon as practicable following effectiveness of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: x

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check One):

|

| |

Large accelerated filer o | Accelerated filer o |

Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company o |

_____________________________________________________________________

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant files a further amendment which specifically states that this Registration Statement will thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement becomes effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

This Post-Effective Amendment No. 8 consists of the following:

| |

| 1. | The Registrant's prospectus filed September 12, 2016, included herewith; |

| |

| 2. | Supplement No. 3 to the Registrant's prospectus dated November 18, 2016, included herewith, which amends and supersedes all prior supplements to the prospectus; |

| |

| 3. | Part II, included herewith; and |

| |

| 4. | Signatures, included herewith. |

|

| | | | |

| | | | PROSPECTUS SEPTEMBER 12, 2016 |

| GRIFFIN CAPITAL ESSENTIAL ASSET REIT II |

Maximum Offering of $2,200,000,000 in Shares of Common Stock

Griffin Capital Essential Asset REIT II, Inc. is a Maryland corporation that intends to qualify as a real estate investment trust, or "REIT," for federal income tax purposes for the taxable year ended December 31, 2015. We are offering up to a maximum of $2.0 billion in shares of common stock in our primary offering. We are currently offering up to approximately $1.56 billion in shares of Class T common stock at $10.00 per share and $0.2 billion in shares of Class I common stock at $9.30 per share. As of August 9, 2016, we have received gross offering proceeds in our primary offering of approximately $0.5 billion from the sale of 54,887,338 Class A shares, Class T shares, and Class I shares. As of August 9, 2016, we have approximately $1.5 billion in shares remaining in our primary offering. We are also offering up to $0.2 billion in shares of our common stock (approximately 21 million shares) pursuant to our distribution reinvestment plan ("DRP") at a purchase price during this offering of $9.50 per share for all share classes. No person may own (actually or constructively) more than 9.8% of our outstanding common stock unless our board of directors waives this restriction. We will offer these shares until July 31, 2017, which is three years after the effective date of this offering, unless extended by our board of directors as permitted under applicable law, or extended with respect to shares offered pursuant to our DRP. We reserve the right to reallocate the shares offered between the primary offering and the DRP, and to reallocate shares among classes of stock. We may terminate this offering in our sole discretion.

We expect to use a substantial amount of the net investment proceeds from this offering to primarily invest in single tenant net lease properties essential to the business operations of the tenant diversified by corporate credit, physical geography, product type and lease duration. The sponsor of this offering is Griffin Capital Corporation. We are externally managed by Griffin Capital Essential Asset Advisor II, LLC, our advisor, which is an affiliate of our sponsor.

We are an "emerging growth company" under the federal securities laws and are subject to reduced public company reporting requirements. Investing in our common stock involves a high degree of risk. You should purchase these securities only if you can afford a complete loss of your investment. See "Restrictions on Ownership and Transfer" beginning on page 172 to read about limitations on transferability. See "Risk Factors" beginning on page 21 for a discussion of certain factors that should be carefully considered by prospective investors before making an investment in the shares offered hereby. These risks include but are not limited to the following:

| |

| • | No public market currently exists for our shares and we may not list our shares on a national exchange immediately after completion of this offering, if at all. It will be difficult to sell your shares. If you sell your shares, it will likely be at a substantial discount. Our charter does not require us to pursue a liquidity transaction at any time. |

| |

| • | Until we generate operating cash flows sufficient to pay distributions to you, we may pay distributions from the net investment proceeds of this offering or from borrowings in anticipation of future cash flows. We may pay distributions from sources other than our cash flows from operations, including from the net investment proceeds from our public offerings, and as a result, we would have less cash available for investments and your overall return may be reduced. We are not prohibited from undertaking such activities by our charter, bylaws or investment policies, and we may use an unlimited amount from any source to pay our distributions, and we may use offering proceeds to fund a portion of our distributions. |

| |

| • | This is an initial public offering; we have a limited operating history, and the prior performance of real estate programs sponsored by affiliates of our sponsor may not be indicative of our future results. |

| |

| • | This is a "best efforts" offering. If we are unable to raise substantial funds in this offering, we may not be able to invest in a diverse portfolio of real estate and real estate-related investments, and the value of your investment may fluctuate more widely with the performance of specific investments. |

| |

| • | We have a limited operating history and, as of August 1, 2016, we owned 19 properties. We are a "blind pool" because we have not identified any additional investments we will make with the net investment proceeds from this offering. As a result, you will not be able to evaluate the economic merits of our future investments prior to their purchase. We may be unable to invest the net investment proceeds from this offering on acceptable terms to investors, or at all. |

| |

| • | There are substantial conflicts of interest among us and our sponsor, advisor, property manager and dealer manager. |

| |

| • | Our advisor will face conflicts of interest relating to the purchase of properties, including conflicts with Griffin Capital Essential Asset REIT, Inc. ("GCEAR"), and such conflicts may not be resolved in our favor, which could adversely affect our investment opportunities. |

| |

| • | We have no employees and must depend on our advisor to select investments and conduct our operations, and there is no guarantee that our advisor will devote adequate time or resources to us. |

| |

| • | We will pay substantial fees and expenses to our advisor, its affiliates and participating broker-dealers, which will reduce cash available for investment and distribution. |

| |

| • | We may incur substantial debt, which could hinder our ability to pay distributions to our stockholders or could decrease the value of your investment, and our board of directors may authorize us to exceed our charter limit on leverage of 300% of net assets. |

| |

| • | We may fail to qualify as a REIT, which could adversely affect our operations and our ability to make distributions. |

Neither the Securities and Exchange Commission, the Attorney General of the State of New York nor any other state securities regulator has approved or disapproved of our common stock, determined if this prospectus is truthful or complete or passed on or endorsed the merits of this offering. Any representation to the contrary is a criminal offense.

The use of projections or forecasts in this offering is prohibited. Any representation to the contrary and any predictions, written or oral, as to the amount or certainty of any present or future cash benefit or tax consequence which may flow from an investment in our shares of common stock is prohibited.

|

| | | | | | | | | | | | | | | | | | | |

| | | | Less | | Plus | | |

| | Price to Public | | Sales Commissions* | | Dealer Manager Fee* | | Advisor Funding of Dealer Manager Fee* | | Net Investment Proceeds (Before Expenses) |

| Primary Offering | | | | | | | | | |

| Per Class A Share** | $ | 10.00 |

| | $ | 0.70 |

| | $ | 0.30 |

| | $ | — |

| | $ | 9.00 |

|

| Per Class T Share | $ | 10.00 |

| | $ | 0.30 |

| | $ | 0.30 |

| | $ | 0.20 |

| | $ | 9.60 |

|

| Per Class I Share | $ | 9.30 |

| | $ | — |

| | $ | 0.28 |

| | $ | 0.19 |

| | $ | 9.21 |

|

| Total Maximum | $ | 2,000,000,000 |

| | $ | 63,600,000 |

| | $ | 60,000,000 |

| | $ | 35,200,000 |

| | $ | 1,911,600,000 |

|

| Distribution Reinvestment Plan | | | | | | | | | |

| Per Class A Share | $ | 9.50 |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | 9.50 |

|

| Per Class T Share | $ | 9.50 |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | 9.50 |

|

| Per Class I Share | $ | 9.50 |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | 9.50 |

|

| Total Maximum | $ | 200,000,000 |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | 200,000,000 |

|

*The maximum amount of selling commissions we will pay with respect to Class T shares is 3% of the gross offering proceeds in our primary offering. The maximum amount of dealer manager fees to be paid with respect to Class T shares and Class I shares is 3% of the gross offering proceeds in our primary offering. There will also be an ongoing stockholder servicing fee with respect to Class T shares. Our advisor will fund 2% of the dealer manager fee with respect to Class T shares and Class I shares (which may be recouped under certain circumstances to the extent we pay a Contingent Advisor Payment, as defined below), which will reduce the amount we pay for such fee, and we will fund the remaining 1%. Commencing November 2, 2015, our advisor began funding our organization and offering expenses, up to 1% of gross offering proceeds from our primary offering, which may be recouped by our advisor under certain circumstances to the extent we pay a Contingent Advisor Payment. See "Management Compensation." If our advisor did not fund 2% of the dealer manager fee and our organization and offering expenses of 1%, the net investment amount reflected on customer account statements would be 3% lower. The selling commissions and, in some cases, the dealer manager fee, will not be charged or may be reduced with regard to shares sold to or for the account of certain categories of purchasers. The reduction in these fees will be accompanied by a reduction in the per share purchase price, except that shares sold under the DRP will be sold at $9.50 per share. See "Plan of Distribution." The selling commissions, stockholder servicing fee, and dealer manager fee will not exceed the 10% limitation on underwriting compensation imposed by FINRA.

**As of October 30, 2015, we ceased offering shares of Class A common stock in our primary offering.

________________________

The dealer manager of this offering, Griffin Capital Securities, LLC, a member firm of the Financial Industry Regulatory Authority, is an affiliate of our sponsor and will offer the shares on a best efforts basis. The minimum permitted purchase is generally $2,500.

September 12, 2016

SUITABILITY STANDARDS

An investment in our shares of common stock involves significant risks and is only suitable for persons who have adequate financial means, desire a relatively long-term investment and will not need liquidity from their investment. Initially, there will be no public market for our shares and we cannot assure you that one will develop, which means that it may be difficult for you to sell your shares. This investment is not suitable for persons who seek liquidity or guaranteed income, or who seek a short-term investment.

In consideration of these factors, we have established suitability standards for an initial purchaser or subsequent transferee of our shares. These suitability standards require that a purchaser of shares have, excluding the value of a purchaser's home, furnishings and automobiles, either:

| |

| • | a net worth of at least $250,000; or |

| |

| • | a gross annual income of at least $70,000 and a net worth of at least $70,000. |

Several states have established suitability requirements that are more stringent than our standards described above. Shares will be sold only to investors in these states who meet our suitability standards set forth above along with the special suitability standards set forth below:

| |

| • | For Alabama Residents - Shares will only be sold to residents of the State of Alabama representing that they have a liquid net worth of at least 10 times their investment in us and our affiliates. |

| |

| • | For Iowa Residents - Shares will only be sold to residents of the State of Iowa representing that they have either (a) a net worth of $300,000 or (b) a minimum annual income of $70,000 and a net worth of $100,000. In addition, an Iowa investor must limit his or her investment in us to 10% of such investor's liquid net worth. |

| |

| • | For Kansas Residents - It is recommended by the Office of the Kansas Securities Commissioner that Kansas investors not invest, in the aggregate, more than 10% of their liquid net worth in this and other non-traded real estate investment trusts. |

| |

| • | For Kentucky Residents - Investments by residents of the State of Kentucky must not exceed 10% of such investor's liquid net worth in our shares or the shares of our affiliates' non-publicly traded real estate investment trusts. |

| |

| • | For Maine Residents - The Maine Office of Securities recommends that an investor's aggregate investment in this offering and similar direct participation investments not exceed 10% of the investor's liquid net worth. |

| |

| • | For Massachusetts Residents - Shares will only be sold to residents of Massachusetts representing that they have a liquid net worth of at least 10 times their investment in us and other illiquid direct participation programs. |

| |

| • | For Nebraska Residents - In addition to our suitability requirements, Nebraska investors must limit their investment in this offering and in the securities of other direct participation programs to 10% of such investor's net worth. An investment by a Nebraska investor that is an accredited investor within the meaning of the Federal securities laws is not subject to the foregoing limitations. |

| |

| • | For New Jersey Residents - New Jersey investors must have either (a) a minimum liquid net worth of at least $100,000 and a minimum annual gross income of not less than $85,000, or (b) a minimum liquid net worth of $350,000. In addition, a New Jersey investor's investment in us, our affiliates, and other non-publicly traded direct investment programs (including real estate investment trusts, business development programs, oil and gas programs, equipment leasing programs and commodity pools, but excluding unregistered, federally and state exempt private offerings) may not exceed ten percent (10%) of his or her liquid net worth. |

| |

| • | For New Mexico Residents - A New Mexico resident may not invest more than 10% of his or her liquid net worth in us and other direct participation investments. |

| |

| • | For North Dakota Residents - North Dakota residents must represent that, in addition to the stated net income and net worth standards, they have a net worth of at least 10 times their investment in us. |

| |

| • | For Ohio Residents - It shall be unsuitable for an Ohio investor's aggregate investment in shares of us, our affiliates, and in other non-traded real estate investment trusts to exceed ten percent (10%) of his or her liquid net worth. |

| |

| • | For Oregon Residents - Shares will only be sold to residents of the State of Oregon representing that they have a net worth of at least 10 times their investment in us and that they meet one of our suitability standards. |

| |

| • | For Pennsylvania Residents - Shares will only be sold to residents of the State of Pennsylvania representing that they have a net worth of at least 10 times their investment in our securities and that they meet one of our suitability standards. |

| |

| • | For Tennessee Residents - A Tennessee resident's investment in us must not exceed 10% of his or her liquid net worth. |

For purposes of determining investor suitability, "liquid net worth" shall be defined as that portion of net worth consisting of cash, cash equivalents, and readily marketable securities.

The minimum initial investment is at least $2,500 in shares, except for purchases by (1) our existing stockholders, including purchases made pursuant to the DRP, and (2) existing investors in other programs sponsored by our sponsor, which may be in lesser amounts; provided however, that the minimum initial investment for purchases made by an IRA is at least $1,500. In addition, you may not transfer, fractionalize or subdivide your investment so as to retain an amount less than the applicable minimum initial investment. In order for retirement plans to satisfy the minimum initial investment requirements, unless otherwise prohibited by state law, a husband and wife may contribute funds from their separate IRAs, provided that each such contribution is at least $100. You should note that an investment in shares of our common stock will not, in itself, create a retirement plan and that in order to create a retirement plan, you must comply with all applicable provisions of the Internal Revenue Code (Code).

After you have purchased the minimum investment, any additional purchases must be in increments of at least $100, except for purchases of shares pursuant to our DRP, which may be in a lesser amount.

Our sponsor and each participating broker-dealer, authorized representative or any other person selling shares on our behalf are required to make every reasonable effort to determine that the purchase of

shares is a suitable and appropriate investment for each investor based on information provided by the investor regarding the investor's financial situation and investment objectives. Our sponsor or the participating broker-dealer, authorized representative or any other person selling shares on our behalf will make this determination based on information provided by such investor to our sponsor or the participating broker-dealer, authorized representative or any other person selling shares on our behalf, including such investor's age, investment objectives, investment experience, income, net worth, financial situation and other investments held by such investor, as well as any other pertinent factors.

Our sponsor or the participating broker-dealer, authorized representative or any other person selling shares on our behalf will maintain records for at least six years of the information used to determine that an investment in the shares is suitable and appropriate for each investor.

In making this determination, our sponsor or the participating broker-dealer, authorized representative or other person selling shares on our behalf will, based on a review of the information provided by you, consider whether you:

| |

| • | meet the minimum income and net worth standards established in your state; |

| |

| • | can reasonably benefit from an investment in our common stock based on your overall investment objectives and portfolio structure; |

| |

| • | are able to bear the economic risk of the investment based on your overall financial situation; and |

| |

| • | have an apparent understanding of: |

| |

| • | the fundamental risks of an investment in our common stock; |

| |

| • | the risk that you may lose your entire investment; |

| |

| • | the lack of liquidity of our common stock; |

| |

| • | the restrictions on transferability of our common stock; |

| |

| • | the background and qualifications of our advisor and its affiliates; and |

| |

| • | the tax consequences of an investment in our common stock. |

In the case of sales to fiduciary accounts, the suitability standards must be met by the fiduciary account, by the person who directly or indirectly supplied the funds for the purchase of the shares or by the beneficiary of the account. Given the long-term nature of an investment in our shares, our investment objectives and the relative illiquidity of our shares, our suitability standards are intended to help ensure that shares of our common stock are an appropriate investment for those of you who become investors.

TABLE OF CONTENTS

QUESTIONS AND ANSWERS ABOUT THIS OFFERING

Below we have provided some of the more frequently asked questions and answers relating to an offering of this type. Please see "Prospectus Summary" and the remainder of this prospectus for more detailed information about this offering.

| |

| Q: | What is a real estate investment trust? |

| |

| A: | In general, a real estate investment trust, or REIT, is a company that: |

| |

| • | combines the capital of many investors to acquire or provide financing for commercial real estate; |

| |

| • | allows individual investors the opportunity to invest in a diversified portfolio of real estate under professional management; |

| |

| • | pays distributions to investors of at least 90% of its taxable income; and |

| |

| • | avoids the "double taxation" treatment of income that generally results from investments in a corporation because a REIT generally is not subject to federal corporate income taxes on its net income, provided certain income tax requirements are satisfied. |

In order to qualify as a REIT, an otherwise taxable domestic corporation must:

| |

| • | be managed by an independent board of directors or trustees; |

| |

| • | be jointly owned by 100 or more stockholders without five or fewer investors owning in total more than 50% of the REIT; |

| |

| • | have 95% of its income derived from dividends, interest and property income; |

| |

| • | invest at least 75% of its assets in real estate; and |

| |

| • | derive at least 75% of its gross income from rents or mortgage interest. |

There are three basic types of REITs, which are as follows:

| |

| • | equity REITs that invest in or own real estate and earn income through collecting rent; |

| |

| • | mortgage REITs that lend money to owners and developers or invest in financial instruments; and |

| |

| • | hybrid REITs that are a combination of equity and mortgage REITs. |

We intend to operate primarily as an equity REIT, although our charter does not prohibit us from investing in mortgages as well.

| |

| Q: | What is Griffin Capital Essential Asset REIT II, Inc.? |

| |

| A: | Griffin Capital Essential Asset REIT II, Inc. is a Maryland corporation that intends to qualify as a REIT for federal income tax purposes for the taxable year ended December 31, 2015. We do not have any employees and are externally managed by our advisor, Griffin Capital Essential Asset Advisor II, LLC. |

| |

| Q: | What is your primary investment strategy? |

| |

| A: | We will seek to acquire a portfolio consisting primarily of single tenant business essential properties throughout the United States diversified by corporate credit, physical geography, product type and lease duration. We intend to acquire assets consistent with our acquisition philosophy by focusing primarily on properties: |

| |

| • | essential to the business operations of the tenant; |

| |

| • | located in primary, secondary and certain select tertiary markets; |

| |

| • | leased to tenants with stable and/or improving credit quality; and |

| |

| • | subject to long-term leases with defined rental rate increases or with short-term leases with high-probability of renewal and potential for increasing rent. |

See "Investment Objectives and Related Policies."

| |

| Q: | What is "Business Essential"? |

| |

| A: | We intend to primarily acquire assets essential to the business operations of each tenant. Real estate assets, including key distribution and/or manufacturing facilities or key office properties, are deemed "business essential" if the occupancy of those assets by the corporate tenant is important to its ongoing business operations such that its failure to continue to occupy the property would cause the corporate tenant substantial operational disruption. |

| |

| Q: | Why are you using the single tenant business essential investment strategy? |

| |

| A: | Our sponsor has been acquiring single tenant business essential properties for nearly two decades. Our sponsor's positive acquisition and ownership experience with single tenant business essential properties of the type we intend to acquire stems from the following: |

| |

| • | the credit quality of the lease payment is determinable and equivalent to the senior unsecured credit rating of the tenant; |

| |

| • | the essential nature of the asset to the tenant's business provides greater default protection relative to the tenant's balance sheet debt; and |

| |

| • | long-term leases provide a consistent and predictable income stream across market cycles and shorter-term leases offer income appreciation upon renewal and reset. |

See "Investment Objectives and Related Policies."

| |

| Q: | How will you own the properties? |

| |

| A: | Griffin Capital Essential Asset Operating Partnership II, L.P., our operating partnership, will own, directly or indirectly through one or more special purpose entities, all of the properties that we acquire. We are the sole general partner of our operating partnership, and therefore, we completely control the operating partnership. This structure is commonly known as an UPREIT. |

| |

| A: | UPREIT stands for "Umbrella Partnership Real Estate Investment Trust." An UPREIT is a REIT that holds all or substantially all of its properties through an operating partnership in which the REIT holds a controlling interest. Using an UPREIT structure may give us an advantage in acquiring properties from persons who might not otherwise sell their properties because of unfavorable tax results. Generally, a sale of property directly to a REIT, or a contribution in exchange for REIT shares, is a taxable transaction to the selling property owner. However, in an UPREIT structure, a seller of a property who |

desires to defer taxable gain on the sale of property may transfer the property to the operating partnership in exchange for limited partnership units in the operating partnership without recognizing gain for tax purposes.

| |

| Q: | What are the terms of your leases? |

| |

| A: | We will seek to secure leases with creditworthy tenants prior to or at the time of the acquisition of a property. Our leases will generally be economically "triple-net" leases, which means that the tenant is responsible for the cost of repairs, maintenance, property taxes, utilities, insurance and other operating costs. In certain of our leases, we may be responsible for replacement of specific structural components of a property such as the roof and structure of the building or the parking lot. Our leases will generally have terms of seven to 15 years, many of which will have tenant renewal options, most of which are for additional five-year terms. |

| |

| Q: | What properties do you currently own and who are your current tenants? |

| |

| A: | As of August 1, 2016, we owned 26 buildings located on 19 properties in 13 states, encompassing approximately 4.1 million rentable square feet. Our properties currently generate approximately $44.5 million in annual net rental revenues, on a cash basis. As of August 1, 2016, our portfolio was comprised as follows: |

|

| | | | | | | |

| Property | | Location | | Tenant | | Approx. Square Feet |

| Owens Corning | | Concord, North Carolina | | Owens Corning Sales, LLC | | 61,200 |

|

| Westgate II | | Houston, Texas | | Wood Group Mustang, Inc. | | 186,300 |

|

| Administrative Office of Pennsylvania Courts | | Mechanicsburg, Pennsylvania | | Administrative Office of Pennsylvania Courts | | 56,600 |

|

| American Express Center | | Phoenix, Arizona | | American Express Travel Related Services Company, Inc. | | 513,400 |

|

| MGM Corporate Center | | Las Vegas, Nevada | | MGM Resorts International | | 168,300 |

|

| American Showa | | Columbus, Ohio | | American Showa, Inc. | | 304,600 |

|

| Huntington Ingalls | | Hampton, Virginia | | Huntington Ingalls Incorporated | | 515,500 |

|

| Wyndham | | Parsippany, New Jersey | | Wyndham Worldwide Operations | | 203,500 |

|

| Exel | | Groveport, Ohio | | Exel, Inc. | | 312,000 |

|

| Morpho Detection | | Andover, Massachusetts | | Morpho Detection LLC | | 64,200 |

|

| FedEx Freight | | West Jefferson, Ohio | | FedEx Freight, Inc. | | 160,400 |

|

| Aetna | | Tucson, Arizona | | Aetna Life Insurance Company | | 100,300 |

|

| Bank of America I | | Simi Valley, California | | Bank of America, N.A. | | 206,900 |

|

| Bank of America II | | Simi Valley, California | | Bank of America, N.A. | | 273,200 |

|

| Atlas Copco | | Auburn Hills, Michigan | | Atlas Copco Assembly Systems LLC | | 120,000 |

|

| Toshiba TEC | | Durham, North Carolina | | Toshiba TEC Corporation | | 200,800 |

|

| NETGEAR | | San Jose, California | | NETGEAR, Inc. | | 142,700 |

|

| Nike | | Hillsboro, Oregon | | Nike, Inc. | | 266,800 |

|

| Zebra Technologies | | Lincolnshire, Illinois | | Zebra Technologies Corporation(1) | | 283,300 |

|

| Total | | | | | | 4,140,000 |

|

| |

(1) | Zebra Technologies Corporation ("Zebra Technologies") currently occupies the property pursuant to a sublease, which expires on February 28, 2017. On March 1, 2017, Zebra Technologies' direct lease will commence, with an expiration date of November 30, 2026. |

Many of our tenants or their parent companies are companies well-known throughout the United States, and a large portion of our properties are occupied by some of the most prestigious and established investment grade global corporations which were or currently are components of the Dow Jones Industrial Average and S&P 100. As of August 1, 2016, approximately 76.4% of our gross revenue is generated from leases with investment grade-rated tenants or tenants whose parent companies are investment grade-rated, or leases guaranteed by investment grade-rated companies, including American Express Travel Related Services Company, Inc., Atlas Copco AB, Bank of America, N.A., Nike, Inc., Wyndham Worldwide Operations, and Wood Group Mustang, Inc.

Please see "Real Estate Investments - Portfolio Summary" and " - Our Properties" for more detailed information about the properties in our portfolio and our current tenants.

| |

| Q: | What is a taxable REIT subsidiary? |

| |

| A: | A taxable REIT subsidiary is a fully taxable corporation and may be limited in its ability to deduct interest payments made to us. Our company is allowed to own up to 100% of the stock of taxable REIT subsidiaries that can perform activities unrelated to our leasing of space to tenants, such as third party management, development and other independent business activities. We will be subject to a 100% penalty tax on certain amounts if (i) the economic arrangements among our tenants, our taxable REIT subsidiary and us or (ii) payment terms for services provided by our taxable REIT subsidiary for us are not comparable to similar arrangements among unrelated parties. We, along with Griffin Capital Essential Asset TRS II, Inc., a wholly-owned subsidiary of our operating partnership, have made an election to treat Griffin Capital Essential Asset TRS II, Inc. as a taxable REIT subsidiary. Griffin Capital Essential Asset TRS II, Inc. will conduct certain activities that, if conducted by us, could cause us to receive non-qualifying income under the REIT gross income tests. |

| |

| Q: | If I buy shares, will I receive distributions, and how often? |

| |

| A: | Yes. We expect to pay distributions on a monthly basis to our stockholders. See "Description of Shares — Distribution Policy." |

| |

| Q: | Will the distributions I receive be taxable as ordinary income? |

| |

| A: | Yes and no. Generally, distributions that you receive, including distributions that are reinvested pursuant to our DRP, will be taxed as ordinary income to the extent they are from current or accumulated earnings and profits, as calculated for tax purposes. We expect that some portion of your distributions may not be subject to tax in the year received because depreciation expense reduces taxable income but does not reduce cash available for distribution. In addition, we may make distributions using offering proceeds, which would be considered return of capital and not subject to the ordinary tax rate. We are not prohibited from using offering proceeds to make distributions by our charter, bylaws, or investment policies, and we may use an unlimited amount from any source to pay our distributions, and we may use offering proceeds to fund a portion of our distributions. The portion of your distribution that is not subject to tax immediately is considered a return of capital for tax purposes and will reduce the tax basis of your investment. This, in effect, defers a portion of your tax until your investment is sold or we are liquidated, at which time you would be taxed at capital gains rates. However, because each investor's tax considerations are different, we suggest that you consult with your tax advisor. |

You also should review the section of this prospectus entitled "Federal Income Tax Considerations."

| |

| Q: | What kind of offering is this and how many shares are issued and outstanding? |

| |

| A: | Through our dealer manager, we are offering a maximum of $2.0 billion in shares of our common stock in our primary offering. Through October 30, 2015, we offered shares of Class A common stock at a price of $10.00 per share and sold approximately $0.24 billion in shares of such Class A common stock in our primary offering. We are currently offering up to approximately $1.56 billion in shares of Class T common stock at $10.00 per share and $0.2 billion in shares of Class I common stock at $9.30 per share in our primary offering. These shares are being offered on a "best efforts" basis. As of August 9, 2016, we have 56,157,447 shares of Class A common stock, Class T common stock, and Class I common stock issued and outstanding. Through August 9, 2016, we have received aggregate gross offering proceeds of approximately $0.5 billion from the sale of shares in our primary offering. We are also offering $0.2 billion in shares of our common stock at $9.50 per share pursuant to our DRP to those stockholders who elect to participate in such plan as described in this prospectus. We reserve the right to reallocate the shares of common stock we are offering between our primary offering and our DRP, and to reallocate shares among classes of stock. |

| |

| Q: | What are some of the more significant risks involved in an investment in your shares? |

| |

| A: | An investment in our shares is subject to significant risks. You should carefully consider the information set forth under "Risk Factors" beginning on page 21 for a discussion of the material risk factors relevant to an investment in our shares. Some of the more significant risks include the following: |

| |

| • | This is an initial public offering; we have a limited operating history, and you should not rely upon the past performance of other real estate investment programs sponsored by affiliates of our sponsor to predict our future results. |

| |

| • | There is currently no public trading market for our shares and there may never be one; therefore, it will be difficult for you to sell your shares. Our charter does not require us to pursue a liquidity transaction at any time. |

| |

| • | We established the offering price on an arbitrary basis; as a result, the actual value of your investment may be substantially less than what you pay. |

| |

| • | We have paid, and may continue to pay distributions from sources other than cash flow from operations, including out of net investment proceeds from this offering; therefore, we will have fewer funds available for the acquisition of properties, and our stockholders' overall return may be reduced. |

| |

| • | This is a "best efforts" offering. If we are unable to raise substantial funds, we will be limited in the number and type of investments we may make, and the value of your investment will fluctuate with the performance of the specific properties we acquire. |

| |

| • | Because this is a "blind pool" offering, you will not have the opportunity to evaluate the investments we will make with the proceeds of this offering before you purchase our shares. |

| |

| • | Our ability to operate profitably will depend upon the ability of our advisor to efficiently manage our day-to-day operations. |

| |

| • | Because our dealer manager is one of our affiliates, you will not have the benefit of an independent review of the prospectus or us as is customarily performed in underwritten offerings. |

| |

| • | Our sponsor, advisor, property manager and their officers and certain of their key personnel will face competing demands relating to their time, which may cause our operating results to suffer. |

| |

| • | Our advisor will face conflicts of interest relating to the purchase of properties, including conflicts with Griffin Capital Essential Asset REIT, Inc., and such conflicts may not be resolved in our favor, which could adversely affect our investment opportunities. |

| |

| • | Our advisor will face conflicts of interest relating to the incentive fee structure under our operating partnership agreement, which could result in actions that are not necessarily in the long-term best interests of our stockholders. |

| |

| • | Payment of substantial fees and expenses to our advisor and its affiliates will reduce cash available for investment and distribution. |

| |

| • | You are bound by the majority vote on matters on which our stockholders are entitled to vote and, therefore, your vote on a particular matter may be superseded by the vote of other stockholders. |

| |

| • | Many of our properties will depend upon a single tenant for all or a majority of their rental income, and our financial condition and ability to make distributions may be adversely affected by the bankruptcy or insolvency, a downturn in the business, or a lease termination of a single tenant. |

| |

| • | Three of our 19 current tenants each represent in excess of 10% of our annualized net rental income; therefore we currently rely on these three tenants and adverse effects to their business could affect our performance. |

| |

| • | We may not be able to sell our properties at a price equal to, or greater than, the price for which we purchased such properties, which may lead to a decrease in the value of our assets. |

| |

| • | Adverse economic conditions may negatively affect our property values, returns and profitability. |

| |

| • | Increases in interest rates could increase the amount of our debt payments and adversely affect our ability to make distributions to you. |

| |

| • | Disruptions in the credit markets could have a material adverse effect on our results of operations, financial condition and ability to pay distributions to you. |

| |

| • | Failure to qualify as a REIT would adversely affect our operations and our ability to make distributions as we will incur additional tax liabilities. |

| |

| • | You may have tax liability on distributions you elect to reinvest in our common stock. |

| |

| • | There are special considerations that apply to employee benefit plans, IRAs or other tax-favored benefit accounts investing in our shares which could cause an investment in our shares to be a prohibited transaction which could result in additional tax consequences. |

| |

| Q: | Why did you cease to offer Class A shares and begin to offer Class T shares and Class I shares, and what are the similarities and differences between the classes? |

| |

| A: | We ceased offering Class A shares and began to offer Class T shares and Class I shares due to recent regulatory developments and trends related to non-traded alternative investment products such as the investment opportunity being offered by this prospectus. Concerns over the amount of selling commissions paid from offering proceeds and disclosure of the same on customer account statements have resulted in many sponsors of alternative investment products electing to utilize share class structures that involve a lower up-front selling commission paid from offering proceeds. After extensive consideration and discussions with various constituencies, we ceased offering our Class A shares, which featured a 7% up-front selling commission, and commenced offering our Class T shares, which feature a 3% up-front selling commission, and Class I shares, which feature no up-front selling commission, as discussed in further detail elsewhere in this prospectus. |

Some differences among Class A shares, Class T shares, and Class I shares relate to the amount of selling commissions and stockholder servicing fees payable with respect to each class of shares, and the amount of funding of certain costs by our advisor. Class A shares were subject to a 7% selling commission and 3% dealer manager fee, both of which were paid out of offering proceeds at the time of sale of the share. Class T shares, in contrast, are subject to a 3% selling commission which is paid out of offering proceeds at the time of sale of the share. Class I shares are not subject to a selling commission. Class T shares and Class I shares are also subject to an aggregate dealer manager fee of 3%, 2% of which will be funded by our advisor, and 1% of which will be funded by us. Class T shares also feature a stockholder servicing fee, which accrues daily at a rate of 1/365th of 1% of the purchase price per share of Class T

shares sold in our primary offering up to a maximum of 4% in the aggregate and is payable quarterly. Our dealer manager will generally re-allow 100% of the stockholder servicing fee to participating broker-dealers. We will cease paying the stockholder servicing fee with respect to the Class T shares sold in this offering at the earlier of (i) the date at which the aggregate underwriting compensation from all sources equals 10% of the gross proceeds from the sale of shares in our primary offering (i.e., excluding proceeds from sales pursuant to our DRP); (ii) the fourth anniversary of the last day of the fiscal quarter in which our initial public offering (excluding our DRP offering) terminates; (iii) the date that such Class T share is redeemed or is no longer outstanding; and (iv) the occurrence of a merger, listing on a national securities exchange, or an extraordinary transaction. We cannot predict if or when this will occur. We currently estimate that we will pay stockholder servicing fees up to six years, but in no event will our underwriting expenses exceed 10% of our gross offering proceeds. We cannot predict the length of time over which we will pay this fee due to, among many factors, the varying dates of purchase and the timing of a liquidity event. The aggregate amount of stockholder servicing fees we expect to pay (based on the assumption of $1.56 billion in gross offering proceeds pursuant to the sale of Class T shares) is approximately $62.4 million. Class I shares are not subject to a stockholder servicing fee. We will not pay selling commissions, the dealer manager fee, or the stockholder servicing fee with respect to shares of any class sold pursuant to our DRP. See "Plan of Distribution" for further detail regarding the selling commissions and stockholder servicing fees payable with respect to Class T shares, and the dealer manager fees payable with respect to Class T shares and Class I shares.

Class I shares will also differ from Class A shares and Class T shares in regards to the annualized distribution rate attributable to such shares. While we expect that our board of directors will declare the same daily distribution amount with respect to Class I shares as compared to Class A shares and Class T shares, the lower purchase price of Class I shares will result in a higher annualized distribution percentage rate (when compared to the purchase price) for such shares as compared to Class A shares and Class T shares.

Other than the foregoing, there are no differences between Class A shares, Class T shares, and Class I shares. Each share of our common stock, regardless of class, will be entitled to one vote per share on matters presented to the common stockholders for approval, and the net asset value, or NAV, per share will be the same across share classes.

| |

Q: | What services do you expect to be provided to Class T stockholders in connection with the payment of the stockholder servicing fee? |

| |

| A: | With respect to our Class T shares, we will pay our dealer manager a quarterly stockholder servicing fee in arrears, all or a portion of which may be reallowed to participating broker-dealers, in connection with ongoing services provided to our Class T stockholders. Participating broker-dealers are expected to provide ongoing or regular account or portfolio maintenance for the stockholder, which may include one or more of the following: assisting with recordkeeping, assisting and processing distribution payments, assisting with share repurchase requests, offering to contact the stockholder periodically to provide information about the stockholder's investment in us or to answer questions about the account statement or valuations, and/or providing other similar services as the stockholder may reasonably require in connection with their investment. We expect that a Class I stockholder receives similar services pursuant to such stockholder's arrangement and/or other compensation with the registered investment adviser or other person through whom such stockholder purchased their shares, and therefore we do not pay a stockholder servicing fee with respect to Class I shares.

|

| |

| Q: | How does a "best efforts" offering work? |

| |

| A: | When shares are offered on a "best efforts" basis, the dealer manager and the participating broker-dealers are only required to use their best efforts to sell the shares and have no firm commitment or obligation to purchase any of the shares. Therefore, we may not sell all or any of the shares that we are offering. |

| |

| Q: | How long will this offering last? |

| |

| A: | The offering will not last beyond July 31, 2017 (three years after the effective date of this offering), unless extended by our board of directors as permitted under applicable law, or extended with respect to shares offered pursuant to our DRP. We may need to renew the registration of this offering annually with certain states in which we expect to offer and sell shares. We reserve the right to reallocate the shares offered between our primary offering and our DRP, and to reallocate shares among classes of common stock. We also reserve the right to terminate this offering earlier at any time. |

| |

| Q: | What will you do with the money raised in this offering? |

| |

| A: | We will use the net offering proceeds from your investment to primarily invest in single tenant business essential properties in accordance with our investment objectives. The diversification of our portfolio is dependent upon the amount of proceeds we receive in this offering. We will also incur acquisition fees and acquisition expenses in connection with our acquisition of real estate investments. We may also use net offering proceeds to pay down debt or make distributions if our cash flows from operations are insufficient. See "Estimated Use of Proceeds" for a detailed discussion on the use of proceeds in connection with this offering. |

| |

| A: | Generally, you may buy shares pursuant to this prospectus provided that you have either (1) a net worth of at least $70,000 and a gross annual income of at least $70,000, or (2) a net worth of at least $250,000. For this purpose, net worth does not include your home, furnishings and automobiles. Some states have higher suitability requirements. You should carefully read the more detailed description under "Suitability Standards" immediately following the cover page of this prospectus. |

| |

| Q: | For whom is an investment in your shares recommended? |

| |

| A: | An investment in our shares may be appropriate if you (1) meet the suitability standards as set forth herein, (2) seek to diversify your personal portfolio with a finite-life, real estate-based investment, (3) seek to receive current income, (4) seek to preserve capital, (5) wish to obtain the benefits of potential long-term capital appreciation, and (6) are able to hold your investment for a long period of time. On the other hand, we caution persons who require liquidity or guaranteed income, or who seek a short-term investment. |

| |

| Q: | May I make an investment through my IRA, SEP or other tax-favored account? |

| |

| A: | Yes. You may make an investment through your IRA, a simplified employee pension (SEP) plan or other tax-favored account. In making these investment decisions, you should consider, at a minimum, (1) whether the investment is in accordance with the documents and instruments governing your IRA, plan or other account, (2) whether the investment satisfies the fiduciary requirements associated with your IRA, plan or other account, (3) whether the investment will generate unrelated business taxable income (UBTI) to your IRA, plan or other account, (4) whether there is sufficient liquidity for such investment under your IRA, plan or other account, (5) the need to value the assets of your IRA, plan or other account annually or more frequently, and (6) whether the investment would constitute a prohibited transaction under applicable law. |

| |

| Q: | Is there any minimum investment required? |

| |

| A: | Yes. Generally, you must invest at least $2,500. Investors who already own our shares and existing investors in other programs sponsored by our sponsor can make additional purchases for less than the |

minimum investment. You should carefully read the more detailed description of the minimum investment requirements appearing under "Suitability Standards" immediately following the cover page of this prospectus.

| |

| Q: | How do I subscribe for shares? |

| |

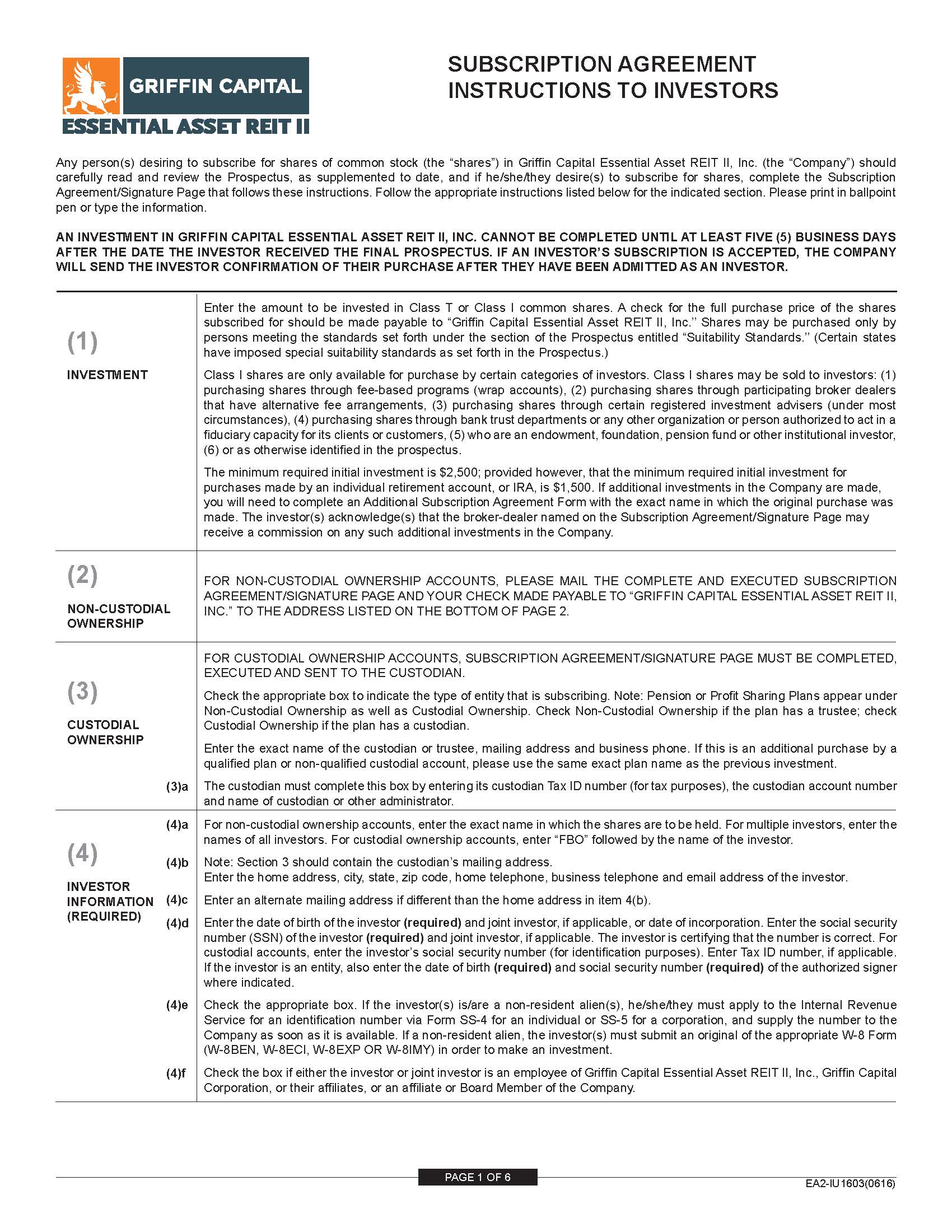

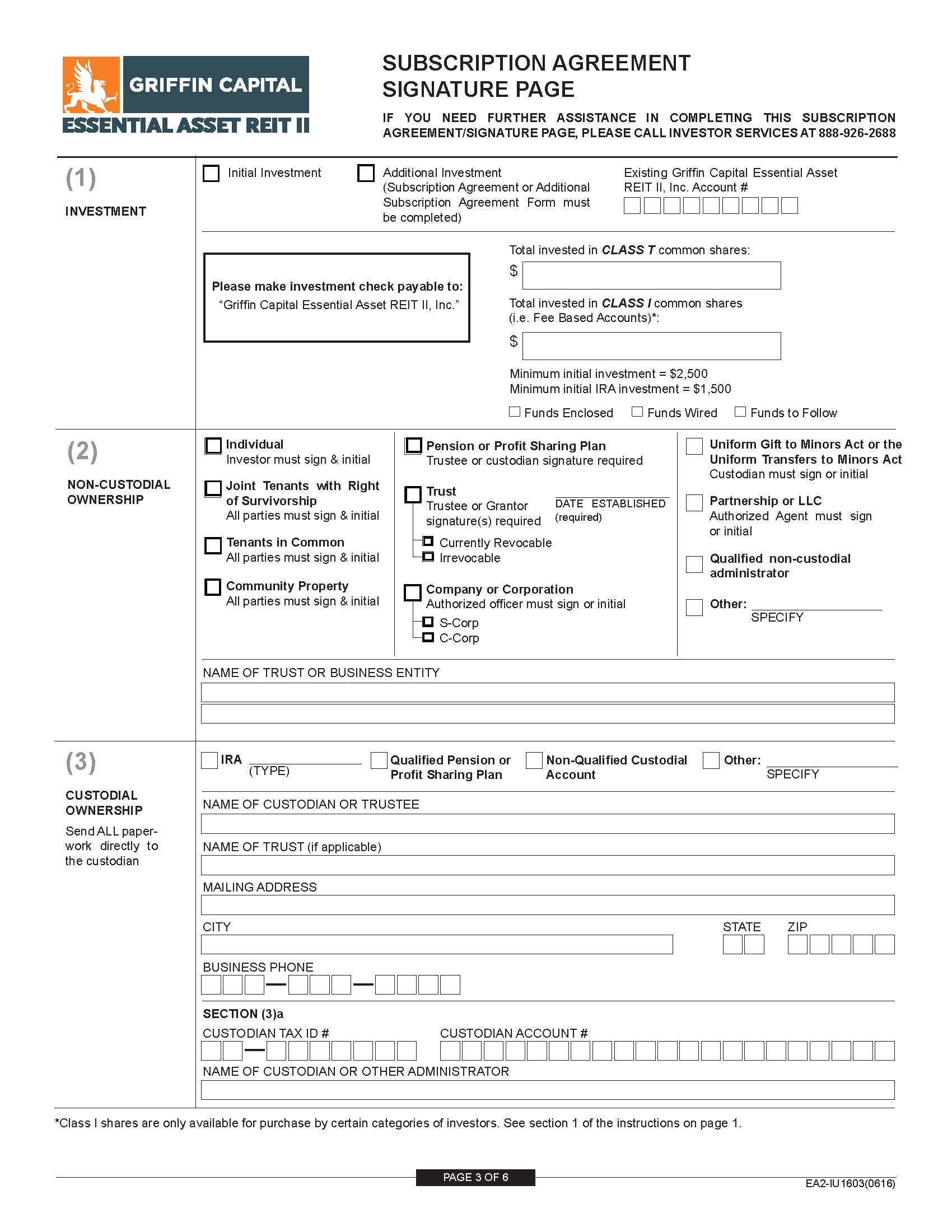

| A: | If you meet the suitability standards described herein and choose to purchase shares in this offering, you must complete a subscription agreement, like the one contained in this prospectus as Appendix B, for a specific number of shares and pay for the shares at the time you subscribe. |

| |

| Q: | May I reinvest my distributions? |

| |

| A: | Yes. Under our DRP, you may reinvest the distributions you receive. Distributions on shares will be reinvested into additional shares of the same class. The purchase price per share under our DRP will be $9.50 per share during this offering. No selling commissions, dealer manager fees, or stockholder servicing fees will be paid on shares sold under the DRP. Please see "Description of Shares — DRP" for more information regarding our DRP. |

| |

| Q: | If I buy shares in this offering, how may I later sell them? |

| |

| A: | At the time you purchase the shares, they will not be listed for trading on any national securities exchange. As a result, if you wish to sell your shares, you may not be able to do so promptly or at all, or you may only be able to sell them at a substantial discount from the price you paid. Subject to applicable law, however, you may sell your shares to any buyer that meets the applicable suitability standards and is willing to make representations similar to the ones contained in our subscription agreement, unless such sale would cause the buyer to own more than 9.8% of the value of our then-outstanding capital stock (which includes common stock and any preferred stock we may issue) or more than 9.8% of the value or number of shares, whichever is more restrictive, of our then-outstanding common stock. See "Suitability Standards" and "Description of Shares — Restrictions on Ownership and Transfer." We are offering a share redemption program, as discussed under "Description of Shares — Share Redemption Program," which may provide limited liquidity for some of our stockholders; however, our share redemption program contains significant restrictions and limitations and we may suspend or terminate our share redemption program if our board of directors determines that such program is not in the best interests of our stockholders. |

| |

| Q: | What is the impact of being an "emerging growth company"? |

A: We do not believe that being an "emerging growth company," as defined by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, will have a significant impact on our business or this offering. As an "emerging growth company," we are eligible to take advantage of certain exemptions from, or reduced disclosure obligations relating to, various reporting requirements that are normally applicable to public companies. Such exemptions include, among other things, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations relating to executive compensation in proxy statements and periodic reports, and exemptions from the requirement to hold a non-binding advisory vote on executive compensation and obtain shareholder approval of any golden parachute payments not previously approved. If we take advantage of any of these exemptions, some investors may find our common stock a less attractive investment as a result.

Additionally, under Section 107 of the JOBS Act, an "emerging growth company" may take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. This means an "emerging growth company" can delay adopting certain accounting standards until such standards are otherwise applicable to private companies. However, we are electing to "opt out" of such extended transition period, and will therefore comply with new or revised accounting standards on the applicable dates on which the adoption of such standards is

required for non-emerging growth companies. Section 107 of the JOBS Act provides that our decision to opt out of such extended transition period for compliance with new or revised accounting standards is irrevocable.

We could remain an "emerging growth company" for up to five years, or until the earliest of (i) the last day of the first fiscal year in which we have total annual gross revenue of $1 billion or more, (ii) the date that we become a "large accelerated filer" as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, or the Exchange Act (which would occur if the market value of our common stock held by non-affiliates exceeds $700 million, measured as of the last business day of our most recently completed second fiscal quarter), or (iii) the date on which we have, during the preceding three year period, issued more than $1 billion in non-convertible debt.

Q: Will I be notified of how my investment is doing?

| |

| A: | Yes. You will be provided with periodic updates on the performance of your investment with us, including: |

| |

| • | an investor update letter, distributed quarterly; |

| |

| • | a quarterly account statement from the transfer agent; |

| |

| • | an annual IRS Form 1099. |

We will provide this information to you via U.S. mail or other courier, facsimile, electronic delivery, in a filing with the Securities and Exchange Commission or annual report, or posting on our website at www.griffincapital.com. Additional information can also be found on our website or on the SEC's website, www.sec.gov.

| |

| Q: | When will I get my detailed tax information? |

| |

| A: | Your IRS Form 1099 will be placed in the mail by January 31 of each year. |

| |

| Q: | Who can help answer my questions? |

| |

| A: | If you have more questions about the offering or if you would like additional copies of this prospectus, you should contact your registered representative or contact: |

Griffin Capital Securities, LLC

18191 Von Karman Avenue

Suite 300

Irvine, CA 92612

Telephone: (949) 270-9300

Email: chuang@griffincapital.com

Attention: Charles Huang

PROSPECTUS SUMMARY

This prospectus summary highlights material information contained elsewhere in this prospectus. Because it is a summary, it may not contain all of the information that is important to you. To understand this offering fully, you should read the entire prospectus carefully, including the "Questions and Answers About this Offering" and "Risk Factors" sections and the financial statements (including the financial statements incorporated by reference in this prospectus), before making a decision to invest in our shares.

Griffin Capital Essential Asset REIT II, Inc.

Griffin Capital Essential Asset REIT II, Inc. is a Maryland corporation incorporated in 2013 that intends to qualify as a REIT for federal income tax purposes for the taxable year ended December 31, 2015. We expect to use a substantial amount of the net investment proceeds from this offering primarily to acquire single tenant business essential properties. Although, as of August 1, 2016, we owned 26 buildings located on 19 properties in 13 states, this offering is considered a "blind pool" because we have not identified any additional investments we will make with proceeds from this offering.

As of August 9, 2016, we had received gross offering proceeds of approximately $0.6 billion from the sale of 56,138,360 Class A shares, Class T shares, and Class I shares in connection with our offering, including proceeds raised and shares issued under our DRP.

Our office is located at Griffin Capital Plaza, 1520 East Grand Avenue, El Segundo, California 90245. Our telephone number is (310) 469-6100 and our fax number is (310) 606-5910. Additional information about us may be obtained at www.griffincapital.com, but the contents of that site are not incorporated by reference in or otherwise a part of this prospectus.

Our Advisor

Griffin Capital Essential Asset Advisor II, LLC is our advisor and is responsible for managing our affairs on a day-to-day basis and identifying and making acquisitions on our behalf, subject to oversight by our board of directors. Our advisor was formed in Delaware in November 2013 and is owned by our sponsor, through a series of holding companies. See the "Management — Our Advisor" section of this prospectus.

Our Sponsor

Our advisor is managed by our sponsor, Griffin Capital Corporation. Our sponsor, formed as a California corporation in 1995, is a privately-owned real estate investment company specializing in the acquisition, financing and management of institutional-quality property in the U.S. Led by senior executives, averaging more than two decades of real estate experience collectively encompassing over $22 billion of transaction value, our sponsor and its affiliates have acquired or constructed approximately 55.5 million square feet of space since 1995. As a principal, our sponsor has engaged in a full spectrum of transaction risk and complexity, ranging from ground-up development, opportunistic acquisitions requiring significant re-tenanting or asset re-positioning to structured single tenant acquisitions. Our sponsor currently serves as sponsor for Griffin Capital Essential Asset REIT, Inc. ("GCEAR"), as a co-sponsor for Griffin-American Healthcare REIT III, Inc. ("GAHR III"), and as co-sponsor for Griffin-American Healthcare REIT IV, Inc. ("GAHR IV"), each of which are publicly-registered, non-traded REITs. Our sponsor is also the sponsor of Griffin-Benefit Street Partners BDC Corp. ("GB-BDC"), a non-diversified, closed-end management investment company that has elected to be regulated as a business development company under the Investment Company Act of 1940 (the "1940 Act"), and Griffin Institutional Access Real Estate Fund ("GIREX"), a non-diversified, closed-end management investment company that is operated as an interval fund under the 1940 Act. As of August 1, 2016, our sponsor and its affiliates own, manage, sponsor and/or co-sponsor a portfolio consisting of approximately 38 million square feet of space, located in 30 states, and 0.1 million square feet located in the United Kingdom, representing approximately $6.8 billion in asset value. Based on total asset value, our sponsor's portfolio of properties consists of approximately 50% office, 40% medical, 6% industrial, and 4% other. Approximately 53% of our sponsor's portfolio consisted of single tenant assets, based on total asset value. See the "Management — Affiliated Companies" section of this prospectus.

Our Property Manager

Griffin Capital Essential Asset Property Management II, LLC, formed in 2013, is our property manager and manages and leases our properties. Griffin Capital Property Management, LLC is the sole member of our property manager and is also the sole member of Griffin Capital Essential Asset Property Management, LLC, the property manager for GCEAR. Our sponsor, Griffin Capital Corporation, through a series of holding companies, is the indirect owner of Griffin Capital Property Management, LLC. See "Management — Affiliated Companies — Our Property Manager" and "Conflicts of Interest." Our property manager was organized to manage the properties that we acquire. Our property manager derives substantially all of its income from the property management services it performs for us. See "Management — Affiliated Companies — Property Management Agreements" below and "Management Compensation."

As of August 1, 2016, our property manager and its affiliates had 94 properties under management, with approximately 23.1 million rentable square feet located in 23 states. The property management function is frequently contracted out to third party providers. As of August 1, 2016, our property manager and its affiliates had 57 contracts with third party providers.

Our Dealer Manager

Griffin Capital Securities, LLC, a Delaware limited liability company and an affiliate of our advisor and our sponsor, serves as our dealer manager. Griffin Capital Securities, LLC was formed in 2015 through a series of transactions in connection with our sponsor's recent corporate reorganization. Griffin Capital Securities, LLC's predecessor, Griffin Capital Securities, Inc., became approved as a member of the Financial Industry Regulatory Authority (FINRA) in 1995. See the "Management - Affiliated Companies - Our Dealer Manager" and the "Conflicts of Interest - Affiliated Dealer Manager" sections of this prospectus.

Our Management

We operate under the direction of our board of directors, the members of which are accountable to us and our stockholders as fiduciaries. Currently, we have five directors – Kevin A. Shields, our Chief Executive Officer, Michael J. Escalante, our President, and three independent directors, Samuel Tang, Kathleen S. Briscoe, and J. Grayson Sanders. All of our executive officers and two of our directors are affiliated with our advisor. Our charter, which requires that a majority of our directors be independent of our advisor, provides that our independent directors are responsible for reviewing the performance of our advisor and must approve other matters set forth in our charter. See the "Conflicts of Interest — Certain Conflict Resolution Procedures" section of this prospectus. Our directors are elected annually by our stockholders.

Conflicts of Interest

Our advisor will experience conflicts of interest in connection with the management of our business affairs, including the following:

| |

| • | The management personnel of our advisor and its affiliates, each of whom also makes investment and operational decisions for three other non-traded REITs and five other entities which own properties, must determine which investment opportunities to recommend to us or an affiliated program or joint venture and must determine how to allocate resources among us and the other affiliated programs; |

| |

| • | Our advisor may receive higher fees by providing an investment opportunity to an entity other than us; |

| |

| • | Our advisor receives fees commensurate with the acquisition price we pay to purchase properties, and if we use leverage to purchase such properties, we will acquire a greater number of properties and our advisor will receive a greater amount of fees. Further, our advisor may recommend that we acquire assets at higher acquisition prices that may not otherwise be in your best interest; |

| |

| • | We may engage in transactions with other programs sponsored by affiliates of our advisor which may entitle such affiliates to fees in connection with its services, as well as entitle our advisor and its affiliates to fees on both sides of the transaction; |

| |

| • | We may structure the terms of joint ventures between us and other programs sponsored by our advisor and its affiliates; |

| |

| • | Our advisor and its affiliates, including Griffin Capital Essential Asset Property Management II, LLC, our property manager, will have to allocate their time between us and other real estate programs and activities in which they are involved, including GCEAR; |

| |

| • | Our advisor and its affiliates will receive substantial fees in connection with transactions involving the purchase, management and sale of our properties regardless of the quality of the property acquired or the services provided to us; and |

| |

| • | Our advisor may receive substantial compensation in connection with a potential listing or other liquidity event. |

These conflicts of interest could result in decisions that are not in our best interests. See the "Conflicts of Interest" and the "Risk Factors — Risks Related to Conflicts of Interest" sections of this prospectus for a detailed discussion of the various conflicts of interest relating to your investment, as well as the procedures that we have established to mitigate a number of these potential conflicts.

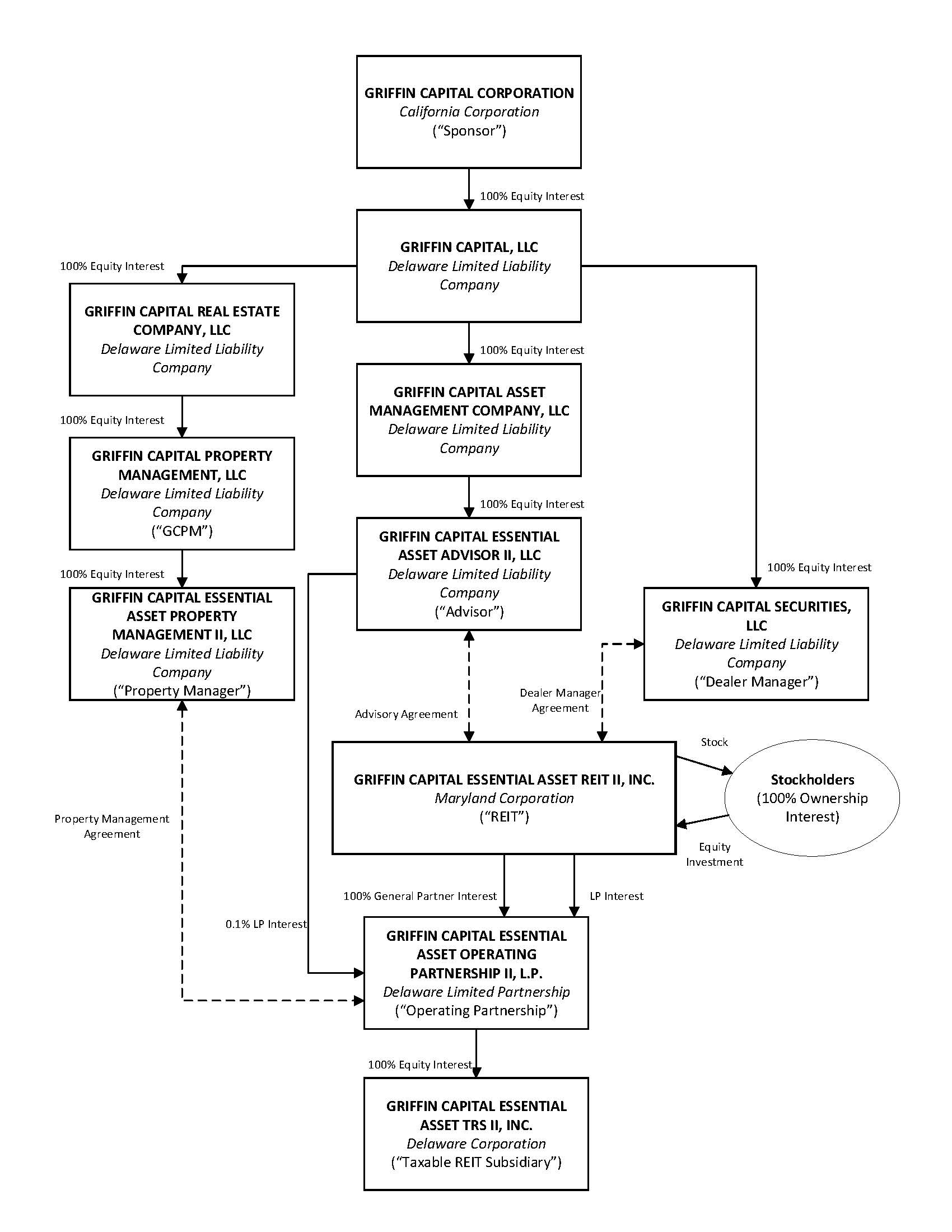

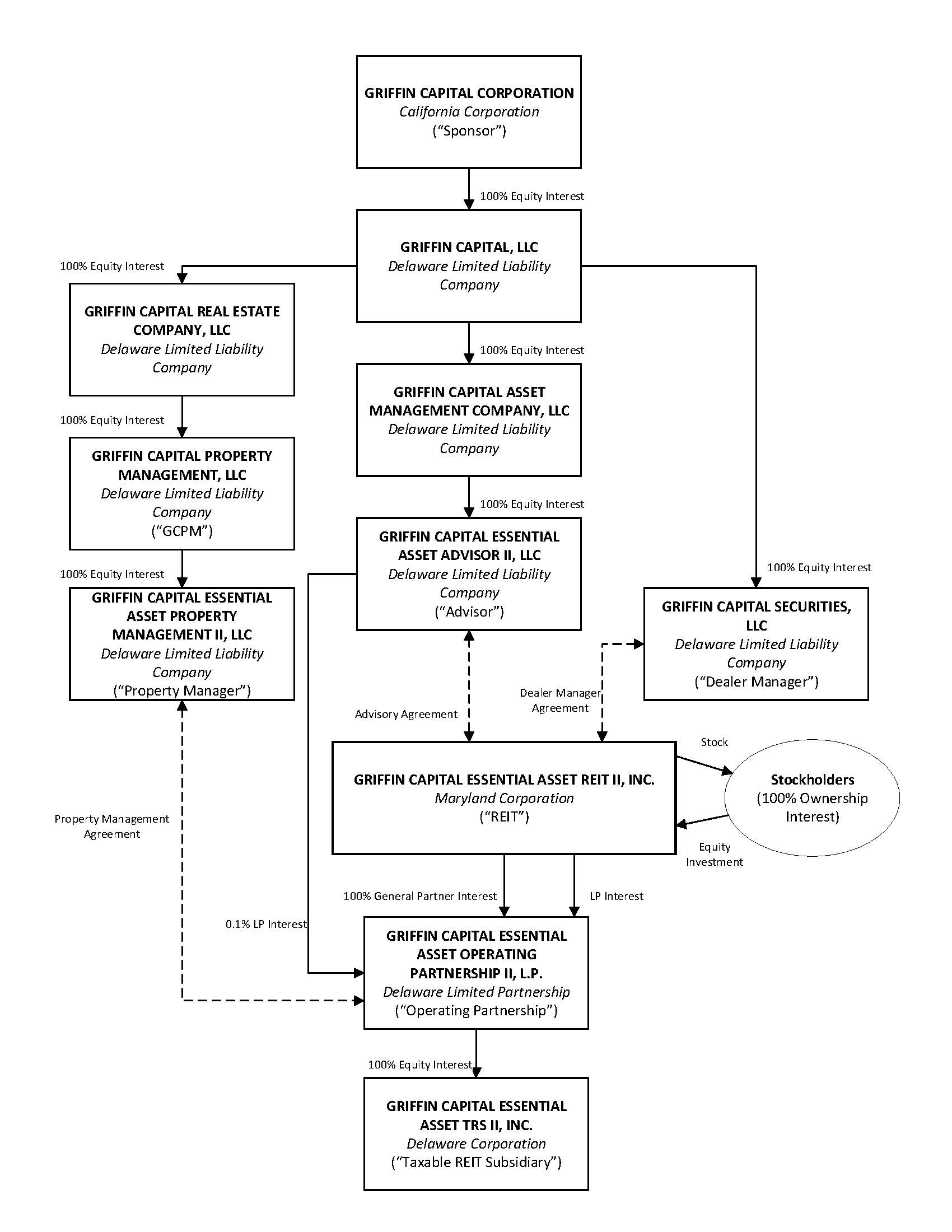

Our Structure

Below is a chart showing our ownership structure and certain entities that are affiliated with our advisor and sponsor as of June 30, 2016.

* The address of all of these entities is Griffin Capital Plaza, 1520 E. Grand Avenue, El Segundo, California 90245, except for Griffin Capital Securities, LLC, which is located at 18191 Von Karman Avenue, Suite 300, Irvine, CA 92612.

** Griffin Capital Corporation is controlled by Kevin A. Shields, our Chairman and Chief Executive Officer.

Compensation to Our Advisor and its Affiliates

Our advisor and its affiliates will receive compensation and reimbursements for services relating to this offering and the investment and management of our assets. The most significant items of compensation are summarized in the table below. Please see the "Management Compensation" section for a complete discussion of the compensation payable to our advisor and its affiliates. The selling commissions and dealer manager fees may vary for different categories of purchasers, as described in the "Plan of Distribution" section of this prospectus. The table below reflects actual amounts incurred for the sale of approximately $0.24 billion in Class A shares in our primary offering, the assumed sale of an additional approximately $1.56 billion in Class T shares in our primary offering, and the assumed sale of an additional approximately $0.2 billion in Class I shares in our primary offering, assumes that such shares will be sold through distribution channels associated with the highest possible selling commissions and dealer manager fees, and also accounts for the fact that shares will be sold through our DRP at $9.50 per share, with no selling commissions and no dealer manager fees.

|

| | | | |

Type of Compensation (Recipient) | | Determination of Amount | | Estimated Amount for Maximum Offering ($2.0 billion in shares) |

Offering Stage

|

Selling Commissions (Participating Dealers) | | 7% of gross proceeds from previously sold Class A shares in our primary offering and 3% of gross proceeds from the sale of Class T shares in our primary offering; we will not pay any selling commissions on sales of shares under our DRP; the dealer manager will re-allow all selling commissions to participating broker-dealers. As of October 30, 2015, we ceased offering shares of Class A common stock in our primary offering. | | $63,600,000 |

Dealer Manager Fee (Dealer Manager) | | 3% of gross proceeds from the sale of shares in our primary offering, of which 1.0% of the gross offering proceeds will be funded by us and the remaining 2.0% of the gross offering proceeds will be funded by our advisor. The amount funded by our advisor may be recouped by our advisor under certain circumstances to the extent we pay a Contingent Advisor Payment (as defined below under Acquisition Fees) upon closing of acquisitions, as described below. We will not pay a dealer manager fee on sales of shares under our DRP. See "Management Compensation." | | $60,000,000 |

| Other Organization and Offering Expenses (Advisor) | | Estimated to be 1% of gross offering proceeds from our primary offering in the event we raise the maximum offering. Effective November 2, 2015, our advisor began paying organization and offering expenses up to 1% of gross offering proceeds from the sale of Class T and Class I shares in our primary offering. Such expenses may be recouped by our advisor under certain circumstances to the extent we pay a Contingent Advisor Payment upon closing of acquisitions, as described below. We will reimburse our advisor for any amounts in excess of 1% of such amount. See "Management Compensation." | | Not determinable at this time. |

Operational Stage

|

| Stockholder Servicing Fee (Participating Dealers) | | A quarterly fee with respect to Class T shares that will accrue daily in an amount equal to 1/365th of 1% of the purchase price per share of Class T shares sold in our primary offering up to a maximum of 4% in the aggregate; the dealer manager will generally re-allow 100% of the stockholder servicing fee to participating broker-dealers. | | $62,400,000 |

|

| | | | |

Type of Compensation (Recipient) | | Determination of Amount | | Estimated Amount for Maximum Offering ($2.0 billion in shares) |

Acquisition Fees (Advisor) | | Effective as of November 2, 2015, our advisor is entitled to fees of up to 3.85% of the contract purchase price of each property or other real estate investments we acquire. The 3.85% of fees consist of the previous 2.0% base acquisition fee and up to an additional 1.85% contingent advisor payment (the "Contingent Advisor Payment"); provided, however, that the first $5.0 million of amounts paid by the advisor for dealer manager fees and organizational and offering expenses (the "Contingent Advisor Payment Holdback") will be retained by us until the later of (a) the termination of this offering, including any follow-on offerings, or (b) July 31, 2017, at which time such amount shall be paid to the advisor. In connection with a follow-on offering, the Contingent Advisor Payment Holdback may increase, based upon the maximum offering amount in such follow-on offering and the amount sold in prior offerings. The amount of the Contingent Advisor Payment paid upon the closing of an acquisition will be reviewed on an acquisition by acquisition basis and such payment shall not exceed the then outstanding amounts paid by the advisor for dealer manager fees and organizational and offering expenses at the time of such closing after taking into account the amount of the Contingent Advisor Payment Holdback described above. For these purposes, the amounts paid by the advisor and considered as "outstanding" will be reduced by the amount of the Contingent Advisor Payment previously paid. Our advisor may waive or defer all or a portion of the acquisition fee or the Contingent Advisor Payment at any time and from time to time, in our advisor's sole discretion. | | $66,408,517 (estimate without leverage)

$140,490,044 (estimate assuming 50% leverage)

$280,980,088 (estimate assuming 75% leverage)

|

Acquisition Expenses (Advisor) | | Actual expenses incurred by our advisor and unaffiliated third parties in connection with an acquisition, which we estimate to be approximately 1% of the contract purchase price of each property. In no event will the total of all acquisition fees and acquisition expenses payable with respect to a particular investment exceed 6% of the contract purchase price.

| | $18,245,460 (estimate without leverage)

$36,490,920 (estimate assuming 50% leverage)

$72,981,841 (estimate assuming 75% leverage) |

Asset Management Fees (Advisor) | | A monthly fee up to 0.0833%, which is one-twelfth of 1%, of our average invested assets.

| | Not determinable at this time. |

Property Management Fees (Property Manager) | | We expect that we will contract directly with non-affiliated third party property managers with respect to our individual properties. In such event, we will pay our property manager an oversight fee equal to 1% of the gross revenues of the property managed, plus reimbursable costs as applicable. Reimbursable costs and expenses include wages and salaries and other expenses of employees engaged in operating, managing and maintaining our properties, as well as certain allocations of office, administrative, and supply costs. In the event that we contract directly with our property manager with respect to a particular property, we will pay our property manager aggregate property management fees of up to 3%, or greater if the lease so allows, of gross revenues received for management of our properties, plus reimbursable costs as applicable. These property management fees may be paid or re-allowed to third party property managers. | | Not determinable at this time. |