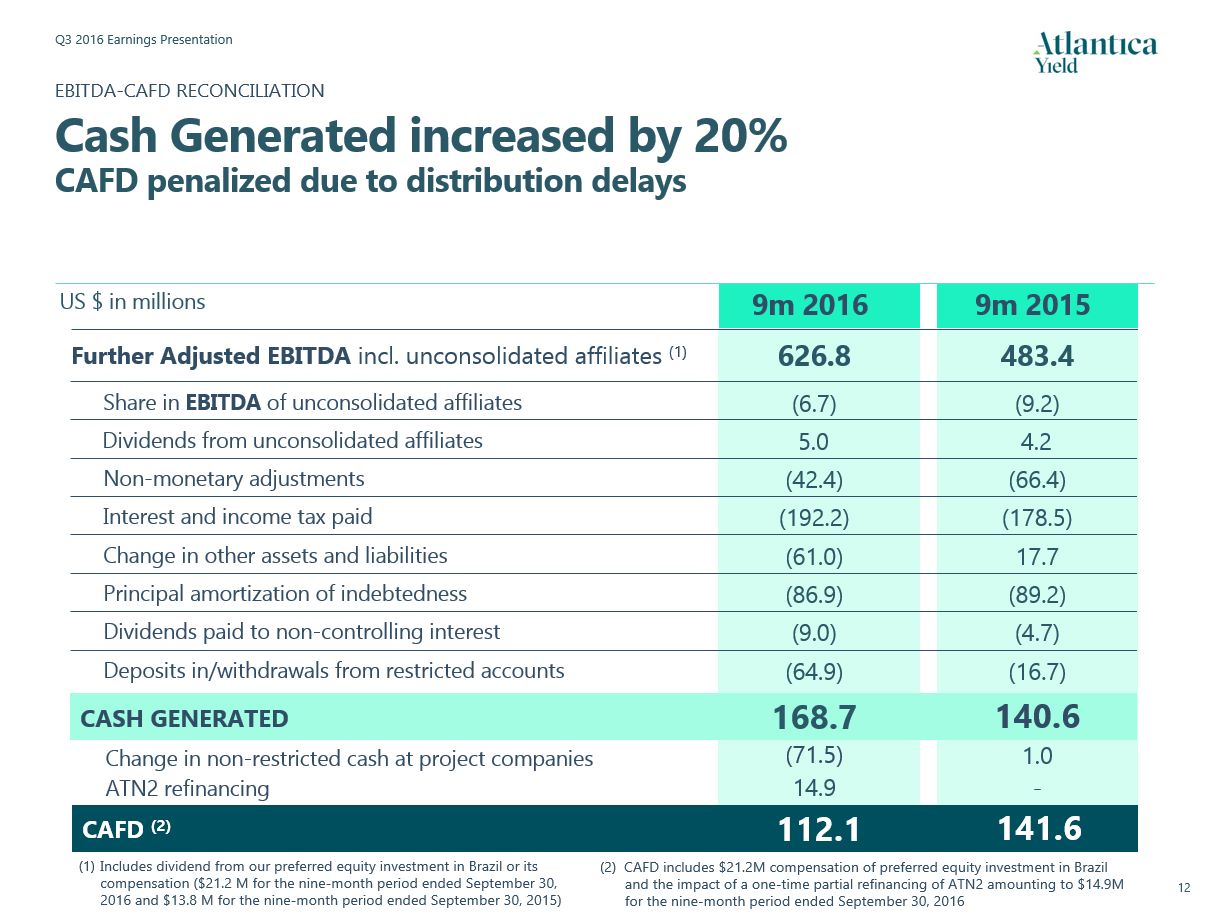

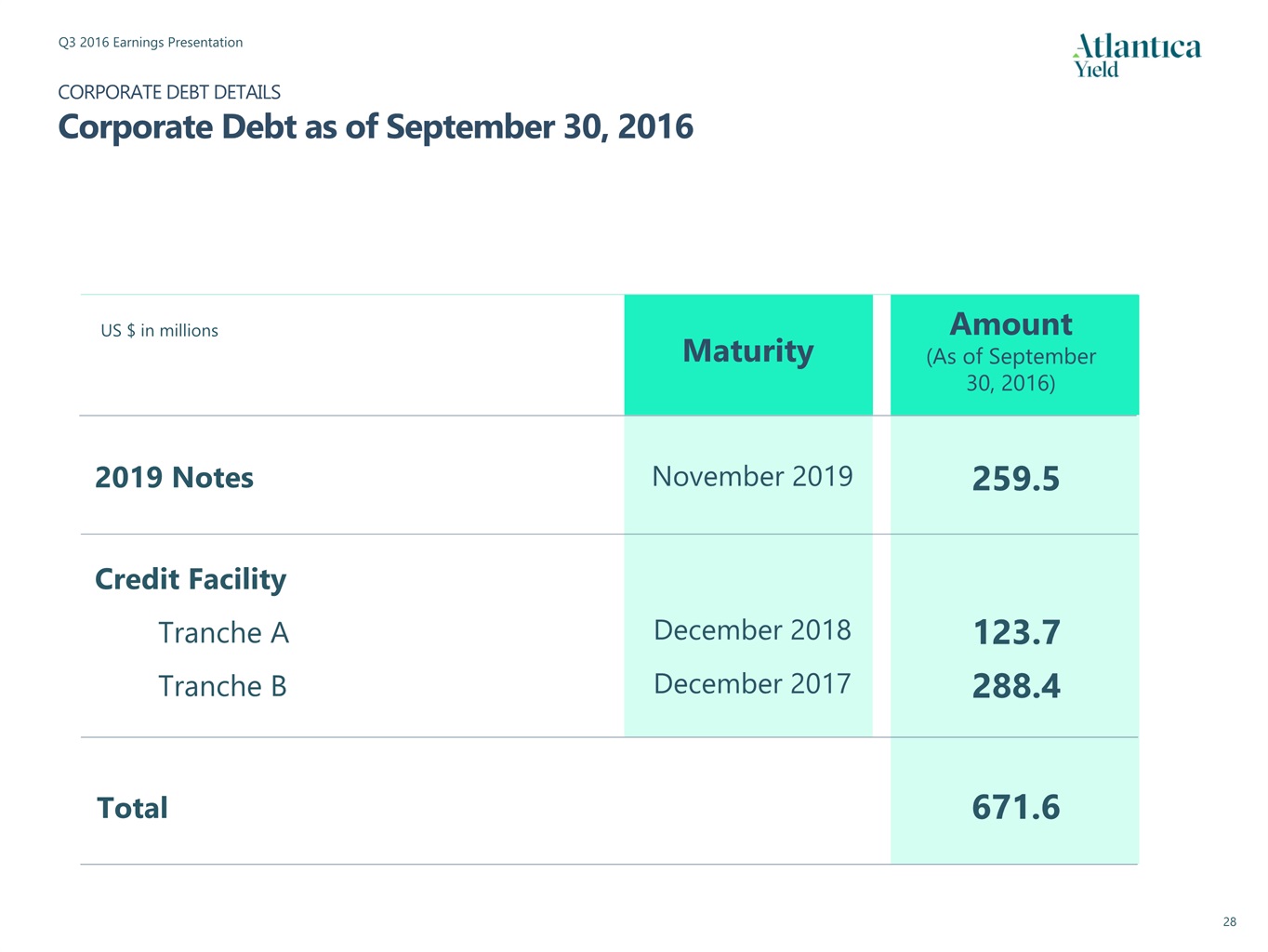

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 FY 2015 1Q16 2Q16 3Q16 Revenues 99,505 93,380 118,304 190,265 267,345 214,967 790,881 206,376 261,302 295,272 F.A. EBITDA margin (%) 89.7% 87.4% 88.9% 83.9% 81.8% 71.2% 80.5% 75.0% 79.5% 89.5% Further Adj. EBITDA incl. unconsolidated affiliates 89,253 81,598 105,186 159,600 218,650 153,074 636,510 154,879 207,645 264,262 ABY pro-rata share of EBITDA from unconsolidated affiliates - - (5,477) (1,622) (2,121) (3,071) (12,291) (2,332) (2,193) (2,157) Further Adjusted EBITDA 89,253 81,598 99,709 157,978 216,529 150,003 624,219 152,547 205,452 262,105 Dividends from unconsolidated affiliates - - - - 4,163 254 4,417 - 4,984 - Non-monetary items (8,631) (9,748) (21,229) (23,741) (21,447) (24,993) (91,410) (18,356) (12,563) (11,508) Interest and income tax paid (15,078) (67,886) (19,291) (113,023) (46,161) (131,759) (310,234) (27,613) (137,372) (27,183) Principal amortization of indebtedness net of new indebtedness at project level (10,058) (11,556) (8,790) (41,873) (38,573) (86,153) (175,389) (14,254) (53,851) (18,792) Deposits into/withdrawals from debt service accounts (10,572) (884) (211) (6,352) (10,090) (183) (16,837) (34,155) 12,291 (43,027) Change in non-restricted cash at project companies (16,748) 29,139 16,255 47,092 (62,285) 71,155 72,217 (41,090) 59,969 (90,385) Dividends paid to non-controlling interests - - - - (4,665) (3,642) (8,307) - (5,479) (3,473) Changes in other assets and liabilities (38) 7,738 (27,944) 24,516 21,105 62,143 79,821 (13,237) (33,824) (13,957) Asset refinancing - - - - - - - 14,893 - - Cash Available For Distribution (CAFD) 28,127 28,401 38,500 44,595 58,576 36,825 178,496 18,736.. 39,607 53,780 . Dividends declared (1) 23,696 20,736 �� 34,074 40,087 43,093 - 117,254 - 29,063.. 16,335 # of shares at the end of the period 80,000,000 80,000,000 80,000,000 100,217,260 100,217,260 100,217,260 100,217,260 100,217,260 100,217,260 100,217,260 DPS (in $ per share) 0.2962 0.2592 0.3400 0.4000 0.4300 - 1.1700 - 0.2900.. 0.1630 Project debt 2,487.1 3,823.1 3,796.7 5,241.2 6,042.6 5,470.7 5,470.7 5,666.8 5,512.1 5,612.9 Project cash (178.9) (198.8) (182.5) (373.3) (618.9) (469.2) (469.2) (529.4) (469.7) (587.6) Net project debt 2,308.2 3,624.3 3,614.1 4,867.9 5,423.7 5,001.5 5,001.5 5,137.4 5,042.4 5,025.3 Corporate debt - 378.5 376.1 377.1 668.7 664.5 664.5 669.9 666.3 671.6 Corporate cash (86.2) (155.4) (84.9) (154.8) (43.6) (45.5) (45.5) (45.4) (84.9) (85.8) Net corporate debt (86.2) 223.1 291.2 222.3 625.1 619.0 619.0 624.5 581.4 585.8 Total net debt 2,222.0 3,847.4 3,905.3 3,090.2 6,048.8 5,620.5 5,620.5 5,761.9 5,623.8 5,611.2 Net Corporate Debt/CAFD pre corporate interests(2) na 2.2x 1.8x 1.3x 2.2x 2.9x 2.9x 2.9x 2.7x 2.7x Dividends are paid to shareholders in the quarter after they are declared;Ratios presented are the ratios shown on each quarter’s earnings presentations;Includes the impact of a one-time partial refinancing of ATN2. Debt details Key Financials US $ in thousands HISTORICAL FINANCIAL REVIEWKey Financials by Quarter US $ in millions (3) Dividend declared on August 3 2016 is the sum of $0.145 per share corresponding to the first quarter of 2016 and $0.145 per share corresponding to the second quarter of 2016.Includes $21.2M compensation of preferred equity investment in Brazil. (4) (4) (5)