Exhibit 99.3.1

May 23, 2014

Board of Trustees

Conahasset Bancshares, Inc.

Boards of Directors

Conahasset Bancshares, Inc.

Pilgrim Bancshares, Inc.

Pilgrim Bank

40 South Main Street

Cohasset, Massachusetts 02025

Members of the Boards of Trustees and Directors:

We have completed and hereby provide an updated appraisal of the estimated pro forma market value of the common stock which is to be issued in connection with the mutual-to-stock conversion described below.

This updated appraisal is furnished pursuant to the requirements in the Code of Federal Regulations and has been prepared in accordance with the “Guidelines for Appraisal Reports for the Valuation of Savings Institutions Converting from the Mutual to the Stock Form of Organization” (the “Valuation Guidelines”) of the Office of Thrift Supervision (“OTS”) and accepted by the Federal Reserve Board (“FRB”), the Office of the Comptroller of the Currency (“OCC”), the Federal Deposit Insurance Corporation (“FDIC”) and the Massachusetts Commissioner of Banks (the “Commissioner”), and applicable regulatory interpretations thereof. Our original appraisal report, dated February 14, 2014 (the “Original Appraisal”), is incorporated herein by reference. As in the preparation of our Original Appraisal, we believe the data and information used herein is reliable; however, we cannot guarantee the accuracy and completeness of such information.

On March 4, 2014, the Board of Trustees of Conahasset Bancshares, MHC, (the “MHC”), a mutual holding company that owns all of the outstanding shares of common stock of Conahasset Bancshares, Inc., a Maryland corporation (“Bancshares”), adopted the plan of conversion whereby the MHC will convert to stock form. As a result of the conversion, Bancshares, which currently owns all of the issued and outstanding common stock of Pilgrim Bank, Cohasset, Massachusetts (“Pilgrim Bank” or the “Bank”) will be succeeded by a Maryland corporation with the name of Pilgrim Bancshares, Inc. (“Pilgrim Bancshares” or the “Company”). Following the conversion, the MHC will no longer exist. For purposes of this document, the existing consolidated entity will hereinafter be referred to as Pilgrim Bancshares or the Company.

Pilgrim Bancshares will offer its common stock in a subscription offering to Eligible Account Holders, Supplemental Eligible Account Holders and Tax-Qualified Employee Stock Benefit Plans including Pilgrim Bank’s employee stock ownership plan (the “ESOP”), as such terms are defined in the Company’s prospectus for purposes of applicable federal regulatory guidelines governing mutual-to-stock conversions. To the extent shares remain available for purchase after satisfaction of all subscriptions received in the subscription offering, the shares may be offered for sale to members of the general public in a community offering and/or a syndicated community offering. A portion of the net proceeds received from the sale of the common stock will be used to purchase all of the then to be issued and outstanding capital stock of Pilgrim Bank and the balance of the net proceeds will be retained by the Company.

| Washington Headquarters | ||

| Three Ballston Plaza | Telephone: (703) 528-1700 | |

| 1100 North Glebe Road, Suite 600 | Fax No.: (703) 528-1788 | |

| Arlington, VA 22201 | Toll-Free No.: (866) 723-0594 | |

| www.rpfinancial.com | E-Mail: mail@rpfinancial.com |

Board of Trustees

Boards of Directors

May 23, 2014

Page 2

At this time, no other activities are contemplated for the Company other than the ownership of the Bank, a loan to the newly-formed ESOP and reinvestment of the proceeds that are retained by the Company. In the future, Pilgrim Bancshares may acquire or organize other operating subsidiaries, diversify into other banking-related activities, pay dividends or repurchase its stock, although there are no specific plans to undertake such activities at the present time.

The plan of conversion provides for the establishment of a new charitable foundation (the “Foundation”). The Foundation contribution will total $725,000 and will be funded with Pilgrim Bancshares common stock contributed by the Company in an amount equal to 3.0% of the shares of common stock sold in the offering and the remainder in cash. The purpose of the Foundation is to provide financial support to charitable organizations in the communities in which Pilgrim Bank operates and to enable those communities to share in the Bank’s long-term growth. The Foundation will be dedicated completely to community activities and the promotion of charitable causes.

The estimated pro forma market value is defined as the price at which the Company’s common stock, immediately upon completion of the Offering, would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts.

Our valuation is not intended, and must not be construed, as a recommendation of any kind as to the advisability of purchasing shares of the Company’s common stock. Moreover, because such valuation is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of common stock in the conversion will thereafter be able to buy or sell such shares at prices related to the foregoing valuation of the pro forma market value thereof. RP Financial is not a seller of securities within the meaning of any federal and state securities laws and any report prepared by RP Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities. RP Financial maintains a policy which prohibits RP Financial, its principals or employees from purchasing stock of its financial institution client institutions.

This updated appraisal reflects the following noteworthy items: (1) a review of recent developments in Pilgrim Bancshares’ financial condition, including financial data through March 31, 2014; (2) an updated comparison of Pilgrim Bancshares’ financial condition and operating results versus the Peer Group companies identified in the Original Appraisal; and, (3) a review of stock market conditions since the date of the Original Appraisal incorporating stock prices as of May 23, 2014.

Board of Trustees

Boards of Directors

May 23, 2014

Page 3

Discussion of Relevant Considerations

1.Financial Results

Table 1 presents summary balance sheet and income statement details for the twelve months ended December 31, 2013 and updated financial information through March 31, 2014. Pilgrim Bancshares’ assets decreased by $2.2 million or 1.27% from December 31, 2013 to March 31, 2014. Investment securities and certificates of deposit (“CDs”) held with other banks accounted for most of the decline in assets during the first quarter. The balance of net loans receivable also declined slightly during the first quarter. Overall, cash and investments (inclusive of FHLB stock and investment in The Co-operative Central Reserve Fund) decreased from $28.3 million or 16.50% of assets at December 31, 2013 to $26.2 million or 15.48% of assets at March 31, 2014. Loans receivable decreased from $132.9 million or 77.48% of assets at December 31, 2013 to $132.5 million or 78.20% of assets at March 31, 2014. The balance of bank-owned life insurance increased slightly during the first quarter of 2014.

Updated credit quality measures showed credit quality improved slightly during the first quarter of 2014. Pilgrim Bancshares’ non-performing assets decreased from $2.4 million or 1.37% of assets at December 31, 2013 to $1.7 million or 0.98% of assets at March 31, 2014. Non-accruing 1-4 family permanent mortgage loans comprised the entire balance of Pilgrim Bancshares’ non-performing assets at March 31, 2014.

The Company’s interest-bearing funding composition showed a decrease in deposits during the first quarter of 2014, which was funded by asset shrinkage and an increase in borrowings. Deposits decreased from $153.7 million or 89.61% of assets at December 31, 2013 to $149.4 million or 88.20% of assets at March 31, 2014. Deposit run-off during the first quarter consisted of transaction and savings account deposits, which was partially offset by an increase in CDs. The balance of borrowings increased from $5.0 million or 2.91% of assets at December 31, 2013 to $7.0 million or 4.13% of assets at March 31, 2014. FHLB advances continued to account for all of the Company’s borrowings. Pilgrim Bancshares’ equity increased from $12.5 million to $12.7 million during the first quarter, which was the result of retention of first quarter earnings and a reduction in the accumulated other comprehensive loss from December 31, 2013 to March 31, 2014. The slight increase in equity combined with asset shrinkage increased the Company’s equity-to-assets ratio from 7.29% at December 31, 2013 to 7.51% at March 31, 2014.

Pilgrim Bancshares’ operating results for the twelve months ended December 31. 2013 and March 31, 2014 are also set forth in Table 1. The Company’s updated reported earnings were slightly higher, increasing from $368,000 or 0.22% of average assets for the twelve months ended December 31, 2013 to $446,000 or 0.26% of average assets for the twelve months ended March 31, 2014. The increase in net income was primarily due to an increase in net interest income and, to a lesser extent, an increase in loan sales gains and a recovery of loan loss provisions. Partially offsetting the improvement in earnings were a decrease in non-interest operating income and an increase in operating expenses.

Pilgrim Bancshares’ net interest income was up slightly during the most recent twelve month period, as the Company’s interest rate spread increased from 2.75% during the

Board of Trustees

Boards of Directors

May 23, 2014

Page 4

Table 1

Pilgrim Bancshares, Inc.

Recent Financial Data

| At Dec. 31, 2013 | At March 31, 2014 | |||||||||||||||

| Amount | Assets | Amount | Assets | |||||||||||||

| ($000) | (%) | ($000) | (%) | |||||||||||||

Balance Sheet Data | ||||||||||||||||

Total assets | $ | 171,556 | 100.00 | % | $ | 169,371 | 100.00 | % | ||||||||

Cash, cash equivalents | 8,991 | 5.24 | 8,602 | 5.08 | ||||||||||||

Investment securities/CDs | 18,261 | 10.64 | 16,565 | 9.78 | ||||||||||||

Loans receivable, net | 132,923 | 77.48 | 132,455 | 78.20 | ||||||||||||

FHLB stock/Co-op Central Res. Fund | 1,051 | 0.61 | 1,059 | 0.63 | ||||||||||||

Bank-Owned Life Insurance | 2,181 | 1.27 | 2,193 | 1.29 | ||||||||||||

Deposits | 153,732 | 89.61 | 149,379 | 88.20 | ||||||||||||

Borrowings | 5,000 | 2.91 | 7,000 | 4.13 | ||||||||||||

Total equity | 12,504 | 7.29 | 12,726 | 7.51 | ||||||||||||

| 12 Months Ended | 12 Months Ended | |||||||||||||||

| Dec. 31, 2013 | March 31, 2014 | |||||||||||||||

| Amount | Avg. Assets | Amount | Avg. Assets | |||||||||||||

| ($000) | (%) | ($000) | (%) | |||||||||||||

Summary Income Statement | ||||||||||||||||

Interest income | $ | 5,963 | 3.49 | % | $ | 6,092 | 3.58 | % | ||||||||

Interest expense | (1,175 | ) | (0.69 | ) | (1,125 | ) | (0.66 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net interest income | 4,788 | 2.80 | 4,967 | 2.92 | ||||||||||||

Provisions for loan losses | — | 0.00 | 36 | 0.02 | ||||||||||||

Net interest income after prov. | 4,788 | 2.80 | 5,003 | 2.94 | ||||||||||||

Gain on sale of loans | — | 0.00 | 19 | 0.01 | ||||||||||||

Other non-interest operating income | 593 | 0.35 | 526 | 0.31 | ||||||||||||

Net gain on sales and calls of securities | 5 | 0.00 | 5 | 0.00 | ||||||||||||

Writedown of securities | (247 | ) | (0.14 | ) | (247 | ) | (0.14 | ) | ||||||||

Non-interest operating expense | (4,611 | ) | (2.70 | ) | (4,627 | ) | (2.72 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Income before income tax expense | 528 | 0.31 | 679 | 0.40 | ||||||||||||

Income taxes | (160 | ) | (0.09 | ) | (233 | ) | (0.14 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net income | $ | 368 | 0.22 | % | $ | 446 | 0.26 | % | ||||||||

Sources: Pilgrim Bancshares’ prospectus, audited and unaudited financial statements, and RP Financial calculations.

Board of Trustees

Boards of Directors

May 23, 2014

Page 5

three months ended March 31, 2013 to 3.30% during the three months ended March 31, 2014. The increase in the Company’s interest rate spread was mostly attributable to an increase in average yield earned on interest-earning assets, which was supported by an increase in the concentration of loans that comprised interest-earning assets. Slightly lower funding costs during the first quarter of 2014 compared to the year ago quarter also contributed to the increase in the Company’s interest rate spread. Overall, net interest income increased from $4.8 million or 2.80% of average assets during the twelve months ended December 31, 2013 to $5.0 million or 2.92% of average assets during the twelve months ended March 31, 2014.

Slightly higher operating expenses translated into a slightly higher operating expense ratio for the Company’s updated earnings, as operating expenses increased from $4.611 million or 2.70% of average assets for the twelve months ended December 31, 2013 to $4.627 million or 2.72% of average assets for the twelve months ended March 31, 2014. Higher compensation costs accounted for most of the increase in operating expenses. Overall, Pilgrim Bancshares’ updated ratios for net interest income and operating expenses provided for a slightly higher expense coverage ratio (net interest income divided by operating expenses). Pilgrim Bancshares’ expense coverage ratio increased from 1.04x for the twelve months ended December 31, 2013 to 1.07x for the twelve months ended March 31, 2014.

Non-interest operating income, including gains on sale of loans, was down slightly during the most recent twelve month period, decreasing from $593,000 or 0.35% of average assets for the twelve months ended December 31, 2013 to $545,000 or 0.32% of average assets for the twelve months ended March 31, 2014. Overall, when factoring non-interest operating income into core earnings, the Company’s updated efficiency ratio of 83.95% (operating expenses, as a percent of net interest income and non-interest operating income) was slightly lower or more favorable compared to the 85.71% efficiency ratio recorded for the twelve months ended December 31, 2013.

The Company’s updated earnings showed no change in non-recurring gains and losses, with both twelve month periods showing net gains on sales and calls of securities of $5,000 or 0.00% of average assets and writedown of securities of $247,000 or 0.14% of average assets.

The Company recorded a reversal of loan loss provisions of $36,000 or 0.02% of average during the twelve months ended March 31, 2014, while no loan loss provisions were established during the twelve months ended December 31, 2013. As of March 31, 2014, the Company maintained an allowance for loan losses of $742,000, equal to 44.75% of non-accruing loans.

2.Peer Group Financial Comparisons

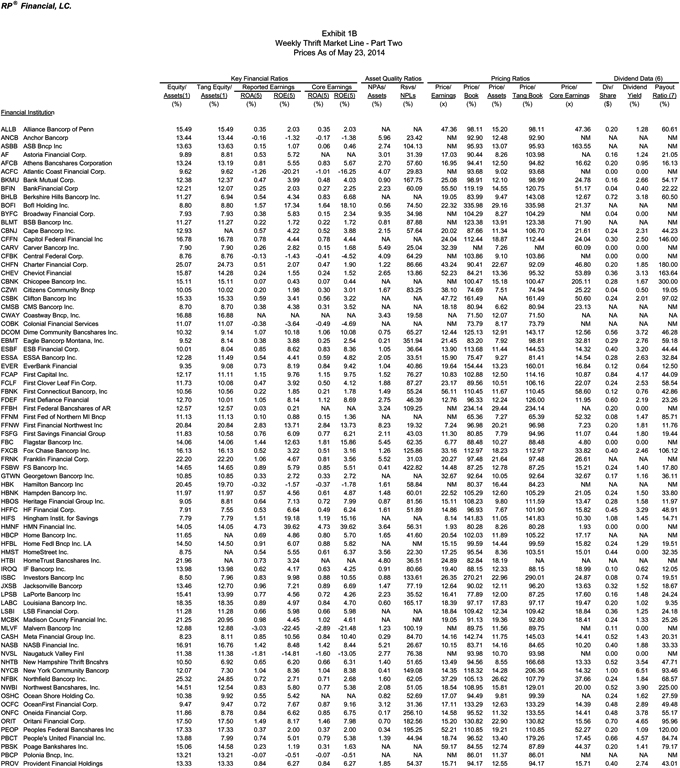

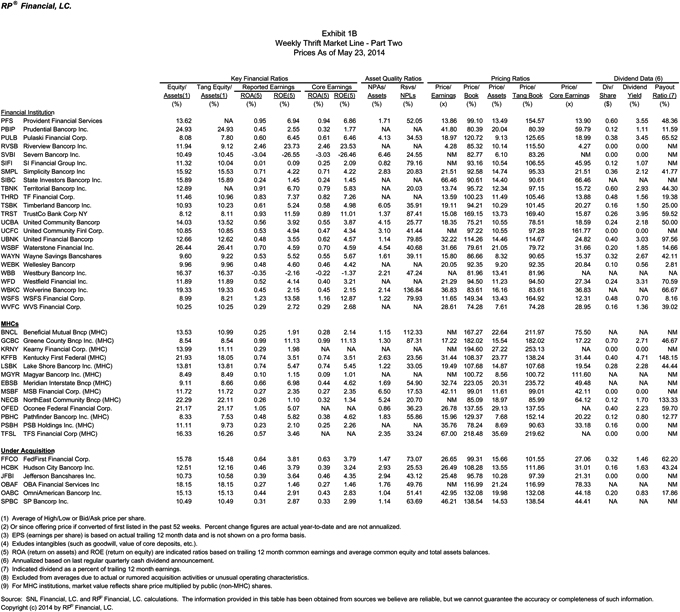

Tables 2 and 3 present the financial characteristics and operating results for Pilgrim Bancshares, the Peer Group and all publicly-traded thrifts. The Company’s and the Peer Group’s ratios are based on financial results through March 31, 2014, unless otherwise indicated for the Peer Group companies. FedFirst Financial Corporation of Pennsylvania and OBA Financial Services, Inc. of Maryland, which were two of the companies selected for the Peer Group in the Original Appraisal, are under pending acquisitions to sell control and, therefore, have been eliminated from the Peer Group.

Board of Trustees

Boards of Directors

May 23, 2014

Page 6

Table 2

Balance Sheet Composition and Growth Rates

Comparable Institution Analysis

As of March 31, 2014

| Balance Sheet as a Percent of Assets | Balance Sheet Annual Growth Rates | Regulatory Capital | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash & | MBS & | Net | Borrowed | Sub. | Total | Goodwill | Tangible | MBS, Cash & | Borrows. | Total | Tangible | Tangible | Tier 1 | Risk-Based | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Equivalents | Invest | BOLI | Loans | Deposits | Funds | Debt | Equity | & Intang | Equity | Assets | Investments | Loans | Deposits | & Subdebt | Equity | Equity | Capital (1) | Risk-Based | Capital | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Pilgrim Bancshares, Inc. | MA | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

March 31, 2014 | 5.08 | % | 10.41 | % | 1.29 | % | 78.20 | % | 88.20 | % | 4.13 | % | 0.00 | % | 7.51 | % | 0.00 | % | 7.51 | % | -1.47 | % | -40.53 | % | 13.72 | % | -3.74 | % | 77.37 | % | 2.27 | % | 2.27 | % | 7.61 | % | 12.91 | % | 13.67 | % | ||||||||||||||||||||||||||||||||||||||||||||

All Public Companies | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages | 5.72 | % | 20.23 | % | 1.90 | % | 67.48 | % | 74.23 | % | 10.79 | % | 0.39 | % | 13.28 | % | 0.68 | % | 12.66 | % | 4.88 | % | 0.00 | % | 8.20 | % | 3.90 | % | 18.90 | % | 5.34 | % | 0.05 | % | 12.32 | % | 19.86 | % | 20.82 | % | ||||||||||||||||||||||||||||||||||||||||||||

Medians | 3.98 | % | 17.07 | % | 1.94 | % | 69.41 | % | 75.54 | % | 10.42 | % | 0.00 | % | 12.25 | % | 0.03 | % | 11.38 | % | 2.82 | % | -0.03 | % | 6.41 | % | 1.11 | % | 3.92 | % | -0.20 | % | 0.00 | % | 11.60 | % | 17.60 | % | 18.88 | % | ||||||||||||||||||||||||||||||||||||||||||||

State of MA | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages | 4.51 | % | 14.58 | % | 1.94 | % | 76.27 | % | 72.33 | % | 14.94 | % | 0.15 | % | 11.65 | % | 0.51 | % | 11.14 | % | 14.94 | % | 0.19 | % | 16.98 | % | 13.23 | % | 53.29 | % | 0.43 | % | 0.00 | % | 13.59 | % | 16.83 | % | 17.87 | % | ||||||||||||||||||||||||||||||||||||||||||||

Medians | 4.68 | % | 9.09 | % | 1.55 | % | 80.38 | % | 70.50 | % | 16.12 | % | 0.00 | % | 11.27 | % | 0.00 | % | 11.06 | % | 15.52 | % | 0.00 | % | 15.58 | % | 10.27 | % | 25.93 | % | -0.10 | % | 0.00 | % | 13.59 | % | 17.45 | % | 18.45 | % | ||||||||||||||||||||||||||||||||||||||||||||

Comparable Recent Conversions(2) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

CWAY | Coastway Bancorp, Inc. | RI | 2.60 | % | 0.00 | % | 0.00 | % | 87.40 | % | 87.80 | % | 3.70 | % | 0.00 | % | 7.30 | % | 0.10 | % | 7.20 | % | 5.96 | % | 40.50 | % | 5.86 | % | 7.21 | % | -14.34 | % | 1.10 | % | 1.14 | % | 7.69 | % | 9.70 | % | 10.19 | % | ||||||||||||||||||||||||||||||||||||||||||

Comparable Group | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages | 5.23 | % | 24.14 | % | 2.15 | % | 65.57 | % | 72.45 | % | 13.76 | % | 0.00 | % | 12.85 | % | 0.42 | % | 12.43 | % | 10.69 | % | 0.04 | % | 10.94 | % | 8.28 | % | 32.21 | % | -2.44 | % | -0.02 | % | 11.45 | % | 18.45 | % | 19.39 | % | ||||||||||||||||||||||||||||||||||||||||||||

Medians | 4.68 | % | 11.03 | % | 2.35 | % | 75.78 | % | 73.97 | % | 9.43 | % | 0.00 | % | 11.91 | % | 0.00 | % | 11.41 | % | 8.29 | % | 0.00 | % | 9.04 | % | 3.28 | % | 25.93 | % | -0.91 | % | -0.01 | % | 10.60 | % | 17.45 | % | 18.45 | % | ||||||||||||||||||||||||||||||||||||||||||||

Comparable Group | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ALLB | Alliance Bancorp, Inc. of Pennsylvania | PA | 11.24 | % | 12.51 | % | 2.91 | % | 70.14 | % | 82.42 | % | 0.63 | % | 0.00 | % | 15.49 | % | 0.00 | % | 15.49 | % | -5.86 | % | -0.34 | % | 9.06 | % | -3.71 | % | -5.90 | % | -16.31 | % | -0.16 | % | 13.75 | % | 21.10 | % | 22.35 | % | ||||||||||||||||||||||||||||||||||||||||||

CBNK | Chicopee Bancorp, Inc. | MA | 6.07 | % | 7.58 | % | 2.38 | % | 81.45 | % | 76.13 | % | 8.70 | % | 0.00 | % | 15.11 | % | 0.00 | % | 15.11 | % | 2.32 | % | -0.15 | % | 6.47 | % | 1.24 | % | 19.33 | % | 0.01 | % | 0.00 | % | 13.70 | % | 18.30 | % | 19.20 | % | ||||||||||||||||||||||||||||||||||||||||||

GTWN | Georgetown Bancorp, Inc. | MA | 3.01 | % | 8.20 | % | 1.09 | % | 85.26 | % | 67.62 | % | 20.16 | % | 0.00 | % | 10.85 | % | 0.00 | % | 10.85 | % | 26.97 | % | 0.67 | % | 24.26 | % | 23.75 | % | 73.95 | % | -4.47 | % | -0.04 | % | 9.62 | % | 13.23 | % | 14.35 | % | ||||||||||||||||||||||||||||||||||||||||||

HBNK | Hampden Bancorp, Inc. | MA | 4.66 | % | 21.27 | % | 2.42 | % | 69.54 | % | 70.16 | % | 16.92 | % | 0.00 | % | 11.97 | % | 0.00 | % | 11.97 | % | 7.49 | % | -0.05 | % | 13.50 | % | 5.32 | % | 27.21 | % | -1.01 | % | -0.01 | % | 11.29 | % | 16.60 | % | 17.70 | % | ||||||||||||||||||||||||||||||||||||||||||

ONFC | Oneida Financial Corp. | NY | 7.93 | % | 37.94 | % | 2.33 | % | 43.18 | % | 86.48 | % | 0.13 | % | 0.00 | % | 11.86 | % | 3.38 | % | 8.49 | % | 9.09 | % | 0.13 | % | 6.71 | % | 11.67 | % | 0.00 | % | -0.81 | % | -0.01 | % | 9.22 | % | 15.43 | % | 16.17 | % | ||||||||||||||||||||||||||||||||||||||||||

PEOP | Peoples Federal Bancshares, Inc. | MA | 4.70 | % | 8.62 | % | 3.38 | % | 81.41 | % | 71.80 | % | 9.31 | % | 0.00 | % | 17.33 | % | 0.00 | % | 17.33 | % | 3.97 | % | -0.18 | % | 9.01 | % | 0.68 | % | 69.70 | % | -3.75 | % | -0.04 | % | 15.04 | % | 23.43 | % | 24.48 | % | ||||||||||||||||||||||||||||||||||||||||||

WVFC | WVS Financial Corp. | PA | 0.65 | % | 87.49 | % | 1.29 | % | 9.78 | % | 44.81 | % | 44.65 | % | 0.00 | % | 10.25 | % | 0.00 | % | 10.25 | % | 18.08 | % | 0.21 | % | -8.94 | % | 1.11 | % | 48.73 | % | 2.31 | % | 0.02 | % | 9.91 | % | 27.30 | % | 27.50 | % | ||||||||||||||||||||||||||||||||||||||||||

WEBK | Wellesley Bancorp, Inc. | MA | 3.55 | % | 9.56 | % | 1.40 | % | 83.78 | % | 80.17 | % | 9.56 | % | 0.00 | % | 9.96 | % | 0.00 | % | 9.96 | % | 23.44 | % | 0.05 | % | 27.44 | % | 26.16 | % | 24.66 | % | 4.52 | % | 0.05 | % | 9.06 | % | 12.17 | % | 13.39 | % | ||||||||||||||||||||||||||||||||||||||||||

| (1) | The tangible capital ratio as defined under the latest OTS guidelines at period-end. For holding companies this represents the value for the company’s largest subsidiary. |

| (2) | Ratios are based on the date of the most recent financial statements disclosed in the offering prospectus. |

| Source: | SNL Financial, LC. and RP® Financial, LC. calculations. The information provided in this table has been obtained from sources we believe are reliable, but we cannot guarantee the accuracy or completeness of such information. |

Copyright (c) 2014 by RP® Financial, LC.

Board of Trustees

Boards of Directors

May 23, 2014

Page 7

Table 3

Income as Percent of Average Assets and Yields, Costs, Spreads

Comparable Institution Analysis

For the 12 Months Ended March 31, 2014

| Net Interest Income | Non-Interest Income | Non-Op. Items | Yields, Costs, and Spreads | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Loss | NII | Gain | Other | Total | Provision | MEMO: | MEMO: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net | Provis. | After | on Sale of | Non-Int | Non-Int | Net Gains/ | Extrao. | for | Yield | Cost | Yld-Cost | Assets/ | Effective | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Income | Income | Expense | NII | on IEA | Provis. | Loans | Income | Expense | Losses (1) | Items | Taxes | On IEA | Of IBL | Spread | FTE Emp. | Tax Rate | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Pilgrim Bancshares, Inc. | MA | �� | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

March 31, 2014 | 0.26 | % | 3.58 | % | 0.66 | % | 2.92 | % | -0.02 | % | 2.94 | % | 0.01 | % | 0.31 | % | 2.72 | % | -0.14 | % | 0.00 | % | 0.14 | % | 3.90 | % | 0.77 | % | 3.13 | % | $ | 5,293 | 35.00 | % | ||||||||||||||||||||||||||||||||||||||

All Public Companies | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages | 0.56 | % | 3.67 | % | 0.68 | % | 2.99 | % | 0.14 | % | 2.85 | % | 0.30 | % | 0.58 | % | 3.01 | % | 0.01 | % | 0.00 | % | 0.18 | % | 3.94 | % | 0.87 | % | 3.09 | % | $ | 5,749 | 27.15 | % | ||||||||||||||||||||||||||||||||||||||

Medians | 0.57 | % | 3.63 | % | 0.64 | % | 3.03 | % | 0.09 | % | 2.91 | % | 0.06 | % | 0.45 | % | 2.85 | % | 0.00 | % | 0.00 | % | 0.23 | % | 3.92 | % | 0.84 | % | 3.14 | % | $ | 5,003 | 31.95 | % | ||||||||||||||||||||||||||||||||||||||

State of MA | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages | 0.53 | % | 3.70 | % | 0.66 | % | 3.05 | % | 0.16 | % | 2.89 | % | 0.03 | % | 0.32 | % | 2.57 | % | 0.06 | % | 0.00 | % | 0.26 | % | 3.93 | % | 0.86 | % | 3.07 | % | $ | 7,164 | 34.44 | % | ||||||||||||||||||||||||||||||||||||||

Medians | 0.50 | % | 3.75 | % | 0.69 | % | 3.05 | % | 0.15 | % | 2.84 | % | 0.02 | % | 0.29 | % | 2.61 | % | 0.00 | % | 0.00 | % | 0.24 | % | 4.03 | % | 0.90 | % | 3.07 | % | $ | 6,694 | 35.19 | % | ||||||||||||||||||||||||||||||||||||||

Comparable Recent Conversions(2) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

CWAY | Coastway Bancorp, Inc. | RI | 0.35 | % | 4.88 | % | 0.96 | % | 3.91 | % | 0.27 | % | 3.65 | % | 1.53 | % | 1.03 | % | 5.60 | % | 0.00 | % | 0.00 | % | 0.26 | % | 4.33 | % | 0.82 | % | 3.51 | % | $ | 2,619 | 41.98 | % | ||||||||||||||||||||||||||||||||||||

Comparable Group | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages | 0.41 | % | 3.50 | % | 0.56 | % | 2.94 | % | 0.15 | % | 2.79 | % | 0.02 | % | 0.84 | % | 3.01 | % | 0.00 | % | 0.00 | % | 0.23 | % | 3.72 | % | 0.74 | % | 2.98 | % | $ | 5,821 | 36.82 | % | ||||||||||||||||||||||||||||||||||||||

Medians | 0.36 | % | 3.75 | % | 0.52 | % | 3.04 | % | 0.12 | % | 2.87 | % | 0.02 | % | 0.39 | % | 2.70 | % | 0.00 | % | 0.00 | % | 0.23 | % | 3.96 | % | 0.68 | % | 3.15 | % | $ | 5,652 | 36.07 | % | ||||||||||||||||||||||||||||||||||||||

Comparable Group | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ALLB | Alliance Bancorp, Inc. of Pennsylvania | PA | 0.35 | % | 3.82 | % | 0.53 | % | 3.28 | % | 0.21 | % | 3.08 | % | 0.00 | % | 0.18 | % | 2.71 | % | 0.00 | % | 0.00 | % | 0.20 | % | 4.01 | % | 0.69 | % | 3.32 | % | $ | 5,124 | 36.02 | % | ||||||||||||||||||||||||||||||||||||

CBNK | Chicopee Bancorp, Inc. | MA | 0.07 | % | 3.86 | % | 0.70 | % | 3.16 | % | 0.46 | % | 2.70 | % | 0.02 | % | 0.49 | % | 3.09 | % | 0.00 | % | 0.00 | % | 0.05 | % | 4.18 | % | 1.00 | % | 3.18 | % | $ | 4,686 | 41.96 | % | ||||||||||||||||||||||||||||||||||||

GTWN | Georgetown Bancorp, Inc. | MA | 0.33 | % | 4.20 | % | 0.50 | % | 3.70 | % | 0.25 | % | 3.45 | % | 0.03 | % | 0.52 | % | 3.48 | % | 0.00 | % | 0.00 | % | 0.19 | % | 4.38 | % | 0.66 | % | 3.72 | % | $ | 4,878 | 36.10 | % | ||||||||||||||||||||||||||||||||||||

HBNK | Hampden Bancorp, Inc. | MA | 0.57 | % | 3.68 | % | 0.76 | % | 2.92 | % | 0.11 | % | 2.81 | % | 0.06 | % | 0.50 | % | 2.42 | % | -0.06 | % | 0.00 | % | 0.32 | % | 3.91 | % | 1.05 | % | 2.86 | % | $ | 6,180 | 36.03 | % | ||||||||||||||||||||||||||||||||||||

ONFC | Oneida Financial Corp. | NY | 0.84 | % | 3.07 | % | 0.36 | % | 2.71 | % | 0.07 | % | 2.64 | % | 0.03 | % | 4.39 | % | 5.92 | % | 0.04 | % | 0.00 | % | 0.35 | % | 3.55 | % | 0.44 | % | 3.11 | % | $ | 2,232 | 29.38 | % | ||||||||||||||||||||||||||||||||||||

PEOP | Peoples Federal Bancshares, Inc. | MA | 0.37 | % | 3.36 | % | 0.43 | % | 2.93 | % | 0.00 | % | 2.93 | % | 0.01 | % | 0.29 | % | 2.59 | % | 0.00 | % | 0.00 | % | 0.26 | % | 3.58 | % | 0.62 | % | 2.96 | % | $ | 7,423 | 41.85 | % | ||||||||||||||||||||||||||||||||||||

WVFC | WVS Financial Corp. | PA | 0.29 | % | 1.91 | % | 0.47 | % | 1.45 | % | -0.03 | % | 1.47 | % | 0.00 | % | 0.17 | % | 1.21 | % | 0.01 | % | 0.00 | % | 0.15 | % | 1.95 | % | 0.56 | % | 1.39 | % | $ | 8,131 | 34.49 | % | ||||||||||||||||||||||||||||||||||||

WEBK | Wellesley Bancorp, Inc. | MA | 0.48 | % | 4.07 | % | 0.69 | % | 3.38 | % | 0.14 | % | 3.24 | % | 0.02 | % | 0.18 | % | 2.70 | % | 0.03 | % | 0.00 | % | 0.30 | % | 4.17 | % | 0.88 | % | 3.29 | % | $ | 7,916 | 38.74 | % | ||||||||||||||||||||||||||||||||||||

| (1) | Net gains/losses includes gain/loss on sale of securities and nonrecurring income and expense. |

| (2) | Ratios are based on the date of the most recent financial statements disclosed in the offering prospectus. |

| Source: | SNL Financial, LC. and RP® Financial, LC. calculations. The information provided in this table has been obtained from sources we believe are reliable, but we cannot guarantee the accuracy or completeness of such information. |

Copyright (c) 2014 by RP® Financial, LC.

Board of Trustees

Boards of Directors

May 23, 2014

Page 8

In general, the comparative balance sheet ratios for the Company and the Peer Group did not vary significantly from the ratios exhibited in the Original Appraisal. Consistent with the Original Appraisal, the Company’s updated interest-earning asset composition reflected a higher concentration of loans and a lower concentration of cash and investments relative to the comparable Peer Group ratios. Overall, the Company maintained a slightly lower level of interest-earning assets than the Peer Group, as updated interest-earning assets-to-assets ratios equaled 93.69% and 94.94% for the Company and the Peer Group, respectively.

The updated mix of deposits and borrowings maintained by Pilgrim Bancshares and the Peer Group also did not change significantly from the Original Appraisal. Pilgrim Bancshares’ funding composition continued to reflect a higher concentration of deposits and a lower concentration of borrowings, relative to the comparable Peer Group measures. Updated interest-bearing liabilities-to-assets ratios equaled 92.33% and 86.21% for the Company and the Peer Group, respectively. Pilgrim Bancshares’ updated tangible equity-to-assets ratio equaled 7.51%, which remained below the comparable Peer Group ratio of 10.69%. Overall, Pilgrim Bancshares’ updated interest-earning assets-to-interest-bearing liabilities (“IEA/IBL”) ratio equaled 101.47%, which remained below the comparable Peer Group ratio of 110.13%. As discussed in the Original Appraisal, the additional capital realized from stock proceeds should serve to increase Pilgrim Bancshares’ IEA/IBL ratio to a ratio that is more comparable to the Peer Group’s ratio, as the level of interest-bearing liabilities funding assets will be lower due to the increase in capital realized from the offering and the net proceeds realized from the offering will be primarily deployed into interest-earning assets.

Updated growth rates for Pilgrim Bancshares are based on annualized growth for the fifteen months ended March 31, 2014, while the Peer Group’s growth rates are based on annual growth for the twelve months ended March 31, 2014 or the most recent twelve month period available. Pilgrim Bancshares recorded a 1.47% decrease in assets, versus asset growth of 10.69% for the Peer Group. Asset shrinkage by the Company was due to a 40.53% decrease in cash investments, which funded a 13.72% increase in loans. Asset growth for the Peer Group was primarily realized through a 10.94% increase in loans, while the Peer Group’s cash and investments increased nominally.

Pilgrim Bancshares’ deposits declined by 3.74%, which was funded by asset shrinkage and a 77.37% increase in borrowings. The relatively high percentage increase in the Company’s borrowings was due to adding a limited amount of borrowings to a modest balance of borrowings maintained at yearend 2012. Comparatively, asset growth for the Peer Group was funded by deposit growth of 8.28% and a 32.21% increase in borrowings. Retention of earnings supported a 2.27% increase in the Company’s capital, while the Peer Group’s capital declined by 2.44% during the twelve month period. The reduction in the Peer Group’s capital reflects retention of earnings being more than offset by capital management strategies such as dividend payments and stock repurchases. The Company’s post-conversion capital growth rate will initially be constrained by maintenance of a higher pro forma capital position. Dividend payments and stock repurchases, pursuant to regulatory limitations and guidelines, could also potentially slow the Company’s capital growth rate in the longer term following the stock offering.

Table 3 displays comparative operating results for Pilgrim Bancshares and the Peer Group, based on the Company’s and the Peer Group’s earnings for the twelve months ended March 31, 2014, unless otherwise indicated for the Peer Group companies. Pilgrim Bancshares

Board of Trustees

Boards of Directors

May 23, 2014

Page 9

and the Peer Group reported updated net income to average assets ratios of 0.26% and 0.41%, respectively. The Peer Group’s higher return continued to be primarily realized through earnings advantages with respect to non-interest operating income and non-operating gains and losses, which were somewhat offset by the Company’s earnings advantages with respect to operating expenses and loan loss provisions.

In terms of core earnings strength, updated expense coverage ratios for Pilgrim Bancshares and the Peer Group equaled 1.07x and 0.98x, respectively. The Company’s higher expense coverage continued to be supported by a lower operating expense ratio, which was partially offset by the Peer Group’s slightly higher net interest income ratio.

Non-interest operating income remained a larger contributor to the Peer Group’s earnings, as such income amounted to 0.32% and 0.86% of the Company’s and the Peer Group’s average assets, respectively. Accordingly, taking non-interest operating income into account in assessing Pilgrim Bancshares’ core earnings strength relative to the Peer Group’s core earnings, the Company’s updated efficiency ratio of 83.95% remained higher or slightly less favorable than the Peer Group’s efficiency ratio of 79.21%.

Net gains and losses realized from the sale of assets and other non-operating items continued to have a more significant impact on the Company’s earnings, as the Company reported a non-operating loss equal to 0.14% of average assets. Comparatively, net non-operating gains and losses equaled 0.00% of average assets for the Peer Group. As set forth in the Original Appraisal, typically, such gains and losses are discounted in valuation analyses as they tend to have a relatively high degree of volatility, and, thus, are not considered part of core operations. Extraordinary items remained a non-factor in the Company’s and the Peer Group’s updated earnings.

Loan loss provisions remained a less significant factor in the Company’s updated earnings, as the Company recorded a reduction in loan loss provisions equal to 0.02% of average assets compared to loan loss provisions established by the Peer Group equal to 0.15% of average assets.

The Company’s effective tax rate of 35.00% remained slightly lower than the Peer Group’s effective tax rate of 36.82%. As set forth in the prospectus, the Company’s effective marginal tax rate is equal to 40.0%.

The Company’s updated credit quality measures continued to imply more significant credit risk exposure relative to the Peer Group’s credit quality measures. As shown in Table 4, the Company’s non-performing assets/assets and non-performing loans/loans ratios of 4.04% and 5.15%, respectively, were higher than the comparable Peer Group ratios of 1.03% and 1.35%. It should be noted that the measures for non-performing assets and non-performing loans include performing loans that are classified as troubled debt restructurings. The Company’s updated reserve coverage ratios continued to reflect a lower level of reserves as a percent of non-performing loans (10.83% versus 111.66% for the Peer Group) and a lower level of reserves as a percent of loans (0.56% versus 0.99% for the Peer Group). Net loan charge-offs remained a slightly larger factor for the Peer Group, as net loan charge-offs as a percent of loans equaled 0.00% for the Company and 0.15% for Peer Group.

Board of Trustees

Boards of Directors

May 23, 2014

Page 10

Table 4

Credit Risk Measures and Related Information

Comparable Institution Analysis

As of March 31, 2014

| REO/ Assets | NPAs & 90+Del/ Assets (1) | NPLs/ Loans (1) | Rsrves/ Loans HFI | Rsrves/ NPLs (1) | Rsrves/ NPAs & 90+Del (1) | Net Loan Chargeoffs (2) | NLCs/ Loans | |||||||||||||||||||||||||||||

| (%) | (%) | (%) | (%) | (%) | (%) | ($000) | (%) | |||||||||||||||||||||||||||||

Pilgrim Bancshares, Inc. | MA | |||||||||||||||||||||||||||||||||||

March 31, 2014 | 0.00 | % | 4.04 | % | 5.15 | % | 0.56 | % | 10.83 | % | 10.83 | % | $ | 3 | 0.00 | % | ||||||||||||||||||||

All Public Companies | ||||||||||||||||||||||||||||||||||||

Averages | 0.40 | % | 2.46 | % | 2.85 | % | 1.33 | % | 69.74 | % | 76.00 | % | $ | 4,880 | 0.32 | % | ||||||||||||||||||||

Medians | 0.17 | % | 1.69 | % | 2.14 | % | 1.17 | % | 54.99 | % | 42.30 | % | $ | 1,074 | 0.15 | % | ||||||||||||||||||||

State of | MA | |||||||||||||||||||||||||||||||||||

Averages | 0.04 | % | 1.09 | % | 1.39 | % | 0.96 | % | 90.18 | % | 85.22 | % | $ | 1,614 | 0.11 | % | ||||||||||||||||||||

Medians | 0.01 | % | 1.07 | % | 1.29 | % | 0.93 | % | 78.59 | % | 69.16 | % | $ | 135 | 0.04 | % | ||||||||||||||||||||

Comparable Recent Conversions(3) | ||||||||||||||||||||||||||||||||||||

CWAY | Coastway Bancorp, Inc. | RI | 0.44 | % | 3.06 | % | 1.56 | % | 0.42 | % | 13.93 | % | 11.92 | % | $ | 385 | 0.13 | % | ||||||||||||||||||

Comparable Group | ||||||||||||||||||||||||||||||||||||

Averages | 0.12 | % | 1.03 | % | 1.35 | % | 0.99 | % | 111.66 | % | 104.70 | % | $ | 564 | 0.15 | % | ||||||||||||||||||||

Medians | 0.01 | % | 0.93 | % | 1.68 | % | 0.94 | % | 69.30 | % | 61.15 | % | $ | 172 | 0.07 | % | ||||||||||||||||||||

Comparable Group | ||||||||||||||||||||||||||||||||||||

ALLB | Alliance Bancorp, Inc. of Pennsylvania | PA | 0.73 | % | 2.46 | % | 2.06 | % | 1.42 | % | 69.30 | % | 41.22 | % | $ | 1,074 | 0.37 | % | ||||||||||||||||||

CBNK | Chicopee Bancorp, Inc. | MA | 0.02 | % | 1.79 | % | 2.15 | % | 0.91 | % | 42.17 | % | 41.63 | % | $ | 2,559 | 0.54 | % | ||||||||||||||||||

GTWN | Georgetown Bancorp, Inc. | MA | 0.00 | % | 0.52 | % | 0.60 | % | 0.95 | % | 157.42 | % | 157.42 | % | $ | 174 | 0.08 | % | ||||||||||||||||||

HBNK | Hampden Bancorp, Inc. | MA | 0.17 | % | 1.48 | % | 1.85 | % | 1.11 | % | 60.02 | % | 53.00 | % | $ | 402 | 0.08 | % | ||||||||||||||||||

ONFC | Oneida Financial Corp. | NY | 0.01 | % | 0.17 | % | 0.36 | % | 0.93 | % | 259.43 | % | 239.38 | % | $ | 170 | 0.05 | % | ||||||||||||||||||

PEOP | Peoples Federal Bancshares, Inc. | MA | 0.00 | % | 0.34 | % | 0.42 | % | 0.82 | % | 195.35 | % | 195.35 | % | $ | 28 | 0.01 | % | ||||||||||||||||||

WVFC | WVS Financial Corp. | PA | 0.00 | % | 0.18 | % | 1.79 | % | 0.72 | % | 40.32 | % | 40.32 | % | $ | 10 | 0.03 | % | ||||||||||||||||||

WEBK | Wellesley Bancorp, Inc. | MA | 0.00 | % | 1.33 | % | 1.57 | % | 1.09 | % | 69.30 | % | 69.30 | % | $ | 95 | 0.03 | % | ||||||||||||||||||

| (1) | Includes TDRs for the Company and the Peer Group. |

| (2) | Net loan chargeoffs are shown on a last twelve month basis. |

| (3) | Ratios are based on the date of the most recent financial statements disclosed in the offering prospectus. |

| Source: | SNL Financial, LC and RP® Financial, LC. calculations. The information provided in this table has been obrained from sources we believe are reliable, but we cannot guarantee the accuracy or completeness of such information. |

Copyright (c) 2014 by RP® Financial, LC.

Board of Trustees

Boards of Directors

May 23, 2014

Page 11

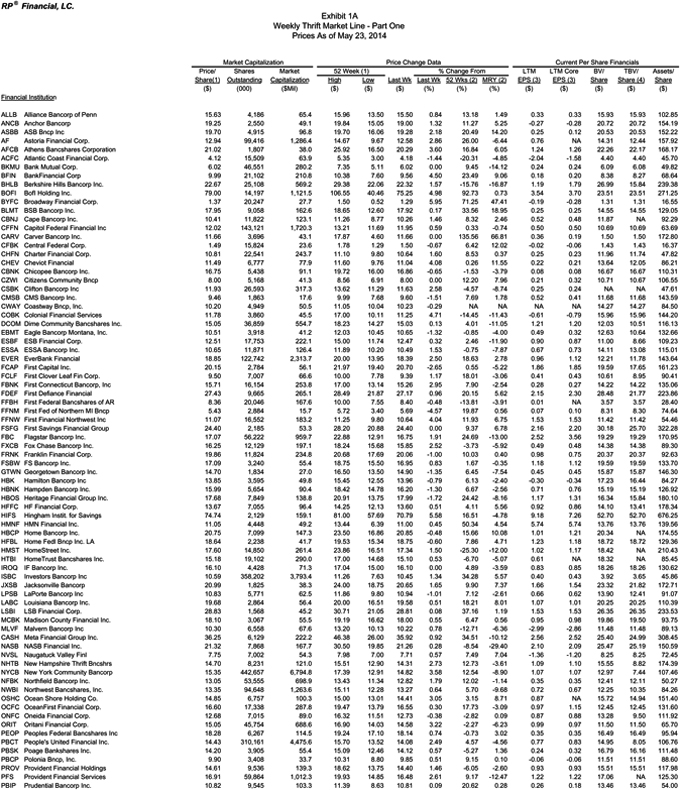

3.Stock Market Conditions

Since the date of the Original Appraisal, the performance of the broader stock market has been mixed. The release of minutes from the Federal Reserve’s previous meeting, which indicated that some Federal Reserve officials were considering raising interest rates sooner than expected, pressured stocks lower heading into the second half of February 2014. Despite data showing a softening economy, stocks traded higher to close out February. Stocks declined sharply on the first day of trading in March as the Ukraine crisis sparked a global selloff which was followed by a rebound in the stock market to close out the first week of March as the threat of the Ukraine crisis escalating diminished and the February employment report showed better-than-expected job growth. Data showing that China’s economy weakened sharply during the first two months of 2014 and rising tensions in Ukraine contributed to stocks trading lower into mid-March. The broader stock market traded unevenly in the second half of March, as investors reacted to mixed reports on the economy and comments from the Federal Reserve Chairwoman signaling that the Federal Reserve could begin raising interest rates earlier than expected. New assurances from the Federal Reserve Chairwoman on the Federal Reserve’s plan to keep rates low until the job market returned to normal health and remarks from China’s premier that the Chinese government was ready to take steps to support China’s economy helped to lift stocks at the close of March.

Stocks edged higher at the start of the second quarter of 2014, which was followed by a downturn as investors reacted to March employment data in which the unemployment rate was unchanged from February and job growth was slightly below expectations. Led by advances in technology shares, the broader stock market traded higher for the first time in four sessions at the start of the first quarter earnings season. Stocks retreated heading into mid-April, with once high-flying biotechnology and Internet companies leading the decline. A strong retail sales report for March helped stocks to rebound in mid-April, with technology stocks leading the market higher. Investor confidence was also bolstered by reassurances from the Federal Reserve Chairwoman on maintaining her stance for keeping interest rates low. A rebound in technology stocks and a series of deals in the healthcare sector helped to extend gains in the broader stock market heading into late-April. The Dow Jones Industrial Average (“DJIA”) closed at a record high at the end of April, as a number of positive first quarter earnings reports helped to offset investors’ worries about tensions in Ukraine and slowing growth in China. Stocks traded unevenly during the first three weeks of May, as investors reacted to mixed data on the economy and gravitated towards lower risk investments. The release of minutes from the Federal Reserve’s April policy meeting, which suggested that Federal Reserve officials were in no hurry to raise interest rates, and better-than-expected new home sales for April contributed to gains in the broader stock market heading into the last week of May. On May 23, 2014, the DJIA closed at 16606.27 or 2.80% higher since the date of the Original Appraisal and the NASDAQ closed at 4185.81 or 1.37% lower since the date of the Original Appraisal.

Thrift stocks generally experienced an uneven performance as well since the date of the Original Appraisal. Similar to the broader stock market, thrift issues rallied at the end of February 2014 and then sold off at the start of March. Lessening concerns about Ukraine, financial sector merger activity and rising home prices boosted thrift shares following the March 1 selloff. The mid-March global selloff sparked by news of a slowdown in China’s economy impacted thrift shares as well, which was followed by a rebound supported by some favorable economic data including a pick-up in industrial production. Mixed signals from the Federal

Board of Trustees

Boards of Directors

May 23, 2014

Page 12

Reserve regarding the end of its quantitative easing program and a decline in February pending home sales were factors that pressured thrift stocks lower in late-March. Thrift stocks traded up at the end of the first quarter, as comments by the Federal Reserve Chairwoman that the Federal Reserve would continue to support the economic recovery were well received in the broader stock market.

Consistent with the broader stock market, thrift stocks traded lower in early-April 2014 with the release of the March employment report. A disappointing first quarter earnings report posted by J.P. Morgan, along with a selloff in the broader stock market, pressured financial shares lower heading into mid-April. Led by Citigroup’s better-than-expected first quarter earnings report, financial shares participated in the broader stock market rally going in the second half of April. News that Bank of America would suspend its stock buyback program and a planned increase in its quarterly dividend pressured financial shares lower in late-April. Thrift shares traded in a narrow range during early-May and then bounced higher, as the Federal Reserve Chairwoman reiterated the Federal Reserve’s stance to keep short-term interest rates near zero for the foreseeable future. Fresh concerns over the pace of economic growth and weakness in the housing sector pressured financial shares lower in mid-May. Indications that the Federal Reserve was planning to stay the course on keeping interest rates low and a favorable report on new home sales for April boosted thrift shares ahead of the last week of May. On May 23, 2014, the SNL Index for all publicly-traded thrifts closed at 697.7, an increase of 1.84% since February 14, 2014.

Since the date of the Original Appraisal, the updated pricing measures for the Peer Group and all publicly-traded thrifts generally reflected declines that were consistent with decline in the SNL Index for all publicly-traded thrifts. The increase in the average market capitalization for all publicly-traded thrifts was viewed to be largely related to Investors Bancorp of New Jersey becoming a fully-converted institution since the date of the Original Appraisal. Investors Bancorp completed its second-step conversion offering in May 2014 and as of May 23, 2014, Investors Bancorp’s market capitalization was $3.8 billion. Since the date of the Original Appraisal, the stock prices of the remaining eight Peer Group companies were equally divided between closing at a lower or higher price as of May 23, 2014.

Average Pricing Characteristics

| At Feb. 14, 2014 | At May 23, 2014 | % Change | ||||||||||

Peer Group(1) | ||||||||||||

Price/Earnings (x) | 24.68 | x | 23.68 | x | (4.05 | )% | ||||||

Price/Core Earnings (x) | 22.76 | 23.58 | 3.60 | |||||||||

Price/Book (%) | 97.35 | % | 96.19 | % | (1.19 | ) | ||||||

Price/Tangible Book(%) | 102.31 | 100.94 | (1.34 | ) | ||||||||

Price/Assets (%) | 13.08 | 12.55 | (4.05 | ) | ||||||||

Avg. Mkt. Capitalization ($Mil) | $ | 69.07 | $ | 68.17 | (1.30 | ) | ||||||

Board of Trustees

Boards of Directors

May 23, 2014

Page 13

Average Pricing Characteristics (continued)

| At Feb. 14, 2014 | At May 23, 2014 | % Change | ||||||||||

All Publicly-Traded Thrifts(1) | ||||||||||||

Price/Earnings (x) | 17.42 | x | 17.78 | x | 2.07 | % | ||||||

Price/Core Earnings (x) | 18.14 | 17.71 | (2.37 | ) | ||||||||

Price/Book (%) | 104.92 | % | 104.01 | % | (0.87 | ) | ||||||

Price/Tangible Book(%) | 113.87 | 112.22 | (1.45 | ) | ||||||||

Price/Assets (%) | 13.36 | 13.05 | (2.32 | ) | ||||||||

Avg. Mkt. Capitalization ($Mil) | $ | 344.10 | $ | 387.37 | 12.57 | |||||||

| (1) | FedFirst Financial Corporation of Pennsylvania and OBA Financial Services of Maryland have been excluded from the Peer Group averages for both dates shown, as the result of becoming targets of announced acquisitions since the date of the Original Appraisal. |

As set forth in the Original Appraisal, the “new issue” market is separate and distinct from the market for seasoned issues like the Peer Group companies in that the pricing ratios for converting issues are computed on a pro forma basis, specifically: (1) the numerator and denominator are both impacted by the conversion offering amount, unlike existing stock issues in which price change affects only the numerator; and (2) the pro forma pricing ratio incorporates assumptions regarding source and use of proceeds, effective tax rates, stock plan purchases, etc. which impact pro forma financials, whereas pricing for existing issues are based on reported financials. The distinction between the pricing of converting and existing issues is perhaps most evident in the case of the price/book (“P/B”) ratio in that the P/B ratio of a converting thrift will typically result in a discount to book value, whereas in the current market for existing thrifts the P/B ratio may reflect a premium to book value. Therefore, it is appropriate to also consider the market for new issues, both at the time of the conversion and in the aftermarket.

As shown in Table 5, one standard conversion and three second-step conversions have been completed during the past three months. The standard conversion offering, which was completed by Home Bancorp of Wisconsin on April 24, 2014, is considered to be more relevant for Pilgrim Bancshares’ pro forma pricing. Home Bancorp’s offering was completed at slightly above the midpoint of its offering range, raising gross proceeds of $9.0 million. Home Bancorp’s pro forma price/tangible book ratio at the closing value equaled 65.80%. Home Bancorp’s stock price closed 7.40% below its offering price after one week of trading and was down 17.50% from its offering price through May 23, 2014. Home Bancorp’s stock is quoted on the OTC Bulletin Board.

Shown in Table 6 are the current pricing ratios for the two fully-converted offerings completed during the past three months that trade on NASDAQ, both of which were second-step offerings. The current P/TB ratio of the fully-converted recent conversions equaled 102.90%, based on closing stock prices as of May 23, 2014.

Board of Trustees

Boards of Directors

May 23, 2014

Page 14

Table 5

Pricing Characteristics and After-Market Trends

Conversions Completed in the Last Three Months

Institutional Information | Pre-Conversion Data | Offering Information | Contribution to | Insider Purchases | Pro Forma Data | Post-IPO Pricing Trends | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Financial Info. | Asset Quality | Char. Found. | % Off Incl. Fdn.+Merger Shares | Pricing Ratios(2)(5) | Financial Charac. | Closing Price: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Excluding Foundation | % of | Benefit Plans | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Institution | Conversion Date | Ticker | Assets | Equity/ Assets | NPAs/ Assets | Res. Cov. | Gross Proc. | % Offer | % of Mid. | Exp./ Proc. | Form | Public Off. Excl. Fdn. | ESOP | Recog Plans | Stk Option | Mgmt.& Dirs. | Initial Div. Yield | P/TB | Core P/E | P/A | Core ROA | TE/ A | Core ROE | IPO Price | First Trading Day | % Chge | After First Week(3) | % Chge | After First Month(4) | % Chge | Thru 5/23/14 | % Chge | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ($Mil) | (%) | (%) | (%) | ($Mil.) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%)(1) | (%) | (%) | (x) | (%) | (%) | (%) | (%) | ($) | ($) | (%) | ($) | (%) | ($) | (%) | ($) | (%) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Standard Conversions | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Home Bancorp Wisconsin, Inc. - WI | 4/24/14 | | HWIS- OTCBB | | $ | 115 | 6.14 | % | 1.53 | % | 158 | % | $ | 9.0 | 100 | % | 102 | % | 14.2 | % | N.A | N.A. | 8.0 | % | 4.0 | % | 10.0 | % | 5.1 | % | 0.00 | % | 65.8 | % | NM | 7.4 | % | -2.3 | % | 11.3 | % | -20.1 | % | $ | 10.00 | $ | 9.61 | -3.9 | % | $ | 9.26 | -7.4 | % | $ | 8.25 | -17.5 | % | $ | 8.25 | -17.5 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages - Standard Conversions: |

| $ | 115 | 6.14 | % | 1.53 | % | 158 | % | $ | 9.0 | 100 | % | 102 | % | 14.2 | % | N.A. | N.A. | 8.0 | % | 4.0 | % | 10.0 | % | 5.1 | % | 0.00 | % | 65.8 | % | NM | 7.4 | % | -2.3 | % | 11.3 | % | -20.1 | % | $ | 10.00 | $ | 9.61 | -3.9 | % | $ | 9.26 | -7.4 | % | $ | 8.25 | -17.5 | % | $ | 8.25 | -17.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Medians - Standard Conversions: |

| $ | 115 | 6.14 | % | 1.53 | % | 158 | % | $ | 9.0 | 100 | % | 102 | % | 14.2 | % | N.A. | N.A. | 8.0 | % | 4.0 | % | 10.0 | % | 5.1 | % | 0.00 | % | 65.8 | % | NM | 7.4 | % | -2.3 | % | 11.3 | % | -20.1 | % | $ | 10.00 | $ | 9.61 | -3.9 | % | $ | 9.26 | -7.4 | % | $ | 8.25 | -17.5 | % | $ | 8.25 | -17.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Second Step Conversions | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

New Investors Bancorp, Inc. - NJ* | 5/8/14 | | ISBC- NASDAQ | | $ | 16,437 | 8.56 | % | 0.95 | % | 124 | % | $ | 2,195.8 | 61 | % | 110 | % | 2.1 | % | C/S | $ | 10M/0.5 | % | 3.0 | % | 4.0 | % | 10.0 | % | 0.1 | % | 0.78 | % | 108.4 | % | 31 | 19.4 | % | 0.6 | % | 18.0 | % | 3.4 | % | $ | 10.00 | $ | 10.42 | 4.2 | % | $ | 10.40 | 4.0 | % | $ | 10.59 | 5.9 | % | $ | 10.59 | 5.9 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Sugar Creek Financial Corp. - IL* | 4/9/14 | | SUGR- OTCBB | | $ | 87 | 11.96 | % | 2.05 | % | 25 | % | $ | 3.7 | 56 | % | 100 | % | 24.7 | % | N.A. | N.A. | 8.0 | % | 4.0 | % | 10.0 | % | 4.8 | % | 0.00 | % | 52.1 | % | 20.15 | 7.4 | % | 0.4 | % | 14.3 | % | 2.6 | % | $ | 7.00 | $ | 9.20 | 31.4 | % | $ | 9.00 | 28.6 | % | $ | 9.20 | 36.4 | % | $ | 9.30 | 36.4 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Clifton Bancorp Inc. - NJ* | 4/2/14 | | CSBK- NASDAQ | | $ | 1,099 | 17.42 | % | 0.41 | % | 67 | % | $ | 170.6 | 64 | % | 87 | % | 1.7 | % | N.A. | N.A. | 6.0 | % | 4.0 | % | 10.0 | % | 0.6 | % | 0.00 | % | 76.4 | % | 47.03 | 21.2 | % | 0.5 | % | 27.7 | % | 1.6 | % | $ | 10.00 | $ | 11.61 | 16.1 | % | $ | 11.57 | 15.7 | % | $ | 11.55 | 15.5 | % | $ | 11.93 | 19.3 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages - Second Step Conversions: |

| $ | 5,874 | 12.65 | % | 1.14 | % | 72 | % | $ | 790.0 | 61 | % | 99 | % | 9.5 | % | N.A. | N.A. | 5.7 | % | 4.0 | % | 10.0 | % | 1.9 | % | 0.26 | % | 78.9 | % | 32.7x | 16.0 | % | 0.5 | % | 20.0 | % | 2.5 | % | $ | 9.00 | $ | 10.41 | 17.2 | % | $ | 10.32 | 16.1 | % | $ | 10.45 | 19.3 | % | $ | 10.61 | 20.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Medians - Second Step Conversions: |

| $ | 1,099 | 11.96 | % | 0.95 | % | 67 | % | $ | 170.6 | 61 | % | 100 | % | 2.1 | % | N.A. | N.A. | 6.0 | % | 4.0 | % | 10.0 | % | 0.6 | % | 0.00 | % | 76.4 | % | 31.0x | 19.4 | % | 0.5 | % | 18.0 | % | 2.6 | % | $ | 10.00 | $ | 10.42 | 16.1 | % | $ | 10.40 | 15.7 | % | $ | 10.59 | 15.5 | % | $ | 10.59 | 19.3 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages - All Conversions: |

| $ | 4,434 | 11.02 | % | 1.24 | % | 94 | % | $ | 594.8 | 70 | % | 100 | % | 10.7 | % | N.A. | N.A. | 6.3 | % | 4.0 | % | 10.0 | % | 2.7 | % | 0.20 | % | 75.6 | % | 32.7x | 13.9 | % | -0.2 | % | 17.8 | % | -3.1 | % | $ | 9.25 | $ | 10.21 | 12.0 | % | $ | 10.06 | 10.2 | % | $ | 9.90 | 10.1 | % | $ | 10.02 | 11.0 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Medians - All Conversions: |

| $ | 607 | 10.26 | % | 1.24 | % | 96 | % | $ | 89.8 | 63 | % | 101 | % | 8.1 | % | N.A. | N.A. | 7.0 | % | 4.0 | % | 10.0 | % | 2.7 | % | 0.00 | % | 71.1 | % | 31.0x | 13.4 | % | 0.4 | % | 16.2 | % | 2.1 | % | $ | 10.00 | $ | 10.02 | 10.2 | % | $ | 9.83 | 9.9 | % | $ | 9.90 | 10.7 | % | $ | 9.95 | 12.6 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Note: * - Appraisal performed by RP Financial; BOLD = RP Fin. Did the business plan, “NT” - Not Traded; “NA” - Not Applicable, Not Available; C/S-Cash/Stock.

| (1) | As a percent of MHC offering for MHC transactions. |

| (2) | Does not take into account the adoption of SOP 93-6. |

| (3) | Latest price if offering is less than one week old. |

| (4) | Latest price if offering is more than one week but less than one month old. |

| (5) | Mutual holding company pro forma data on full conversion basis. |

| (6) | Simultaneously completed acquisition of another financial institution. |

| (7) | Simultaneously converted to a commercial bank charter. |

| (8) | Former credit union. |

May 23, 2014

Board of Trustees

Boards of Directors

May 23, 2014

Page 15

Table 6

Market Pricing Comparatives

Prices As of May 23, 2014

| Market | Per Share Data | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capitalization | Core | Book | Dividends(3) | Financial Characteristics(5) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Price/ | Market | 12 Month | Value/ | Pricing Ratios(2) | Amount/ | Payout | Total | Equity/ | Tang Eq/ | NPAs/ | Reported | Core | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Financial Institution | Share | Value | EPS(1) | Share | P/E | P/B | P/A | P/TB | P/Core | Share | Yield | Ratio(4) | Assets | Assets | Assets | Assets | ROA | ROE | ROA | ROE | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ($) | ($Mil) | ($) | ($) | (x) | (%) | (%) | (%) | (x) | ($) | (%) | (%) | ($Mil) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

All Non-MHC Public Companies | $ | 16.06 | $ | 387.37 | $ | 0.84 | $ | 15.46 | 17.78x | 104.01 | % | 13.05 | % | 112.22 | % | 17.71x | $ | 0.29 | 1.81 | % | 53.76 | % | $ | 2,715 | 13.20 | % | 12.60 | % | 2.42 | % | 0.56 | % | 4.47 | % | 0.57 | % | 4.52% | |||||||||||||||||||||||||||||||||||||||||||

Converted Last 3 Months (no MHC) | $ | 11.26 | $ | 2,055.31 | $ | 0.27 | $ | 11.30 | 31.15x | 101.33 | % | 22.92 | % | 102.90 | % | 33.09x | $ | 0.23 | 1.46 | % | 62.50 | % | $ | 9,843 | 23.10 | % | 22.88 | % | 0.60 | % | 0.57 | % | 2.64 | % | 0.54 | % | 2.51% | |||||||||||||||||||||||||||||||||||||||||||

Converted Last 3 Months (no MHC) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

CSBK | Clifton Bancorp, Inc. of NJ | $ | 11.93 | $ | 317.26 | $ | 0.21 | $ | 13.10 | NM | 91.07 | % | 25.26 | % | 91.07 | % | NM | $ | 0.25 | 2.16 | % | NM | $ | 1,256 | 27.73 | % | 27.73 | % | 0.41 | % | 0.48 | % | 1.72 | % | 0.45 | % | 1.62% | |||||||||||||||||||||||||||||||||||||||||||

ISBC | Investors Bancorp Inc of NJ | $ | 10.59 | $ | 3,793.36 | $ | 0.32 | $ | 9.49 | 31.15x | 111.59 | % | 20.58 | % | 114.73 | % | 33.09x | $ | 0.20 | 0.75 | % | 62.50 | % | $ | 18,430 | 18.46 | % | 18.03 | % | 0.78 | % | 0.66 | % | 3.55 | % | 0.63 | % | 3.40% | ||||||||||||||||||||||||||||||||||||||||||

| (1) | Core income, on a diluted per-share basis. Core income is net income after taxes and before extraordinary items, less net income attributable to noncontrolling interest, gain on the sale of securities, amortization of intangibles, goodwill and nonrecurring items. Assumed tax rate is 35%. |

| (2) | P/E = Price to earnings; P/B = Price to book; P/A = Price to assets; P/TB = Price to tangible book value; and P/Core = Price to core earnings. P/E and P/Core =NM if the ratio is negative or above 35x. |

| (3) | Indicated 12 month dividend, based on last quarterly dividend declared. |

| (4) | Indicated 12 month dividend as a percent of trailing 12 month earnings. |

| (5) | ROAA (return on average assets) and ROAE (return on average equity) are indicated ratios based on trailing 12 month earnings and average equity and assets balances. |

| (6) | Excludes from averages and medians those companies the subject of actual or rumored acquisition activities or unusual operating characteristics. |

| Source: | SNL Financial, LC. and RP® Financial, LC. calculations. The information provided in this report has been obtained from sources we believe are reliable, but we cannot guarantee the accuracy or completeness of such information. |

Copyright (c) 2014 by RP® Financial, LC.

Board of Trustees

Boards of Directors

May 23, 2014

Page 16

Summary of Adjustments

In the Original Appraisal, we made the following adjustments to Pilgrim Bancshares’ pro forma value based upon our comparative analysis to the Peer Group:

Key Valuation Parameters: | Previous Valuation Adjustment | |

| Financial Condition | Slight Downward | |

| Profitability, Growth and Viability of Earnings | Slight Downward | |

| Asset Growth | No Adjustment | |

| Primary Market Area | Slight Upward | |

| Dividends | No Adjustment | |

| Liquidity of the Shares | Slight Downward | |

| Marketing of the Issue | No Adjustment | |

| Management | No Adjustment | |

| Effect of Govt. Regulations and Regulatory Reform | No Adjustment |

The factors concerning the valuation parameters of primary market area, dividends, liquidity of the shares, management and effect of government regulations and regulatory reform did not change since the Original Appraisal. Accordingly, those parameters were not discussed further in this update.

A slight downward adjustment remained appropriate for financial condition, based largely on the downward adjustment applied for the Company’s less favorable credit quality. Likewise, a slight downward adjustment remained appropriate for earnings, based on the Company’s lower core earnings measures, higher credit risk exposure and lower pro forma core ROE. No adjustment remained appropriate for the Company’s asset growth, as the Company’s lower historical asset growth rate was related to maintenance of a more leveraged capital position that has constrained asset growth so as to maintain compliance with the regulatory capital requirements. At the same time, the Company’s loan growth exceeded the Peer Group’s loan growth and the Company’s asset shrinkage was the result of a decrease in cash and investments. On pro forma basis, the additional capital realized from the net proceeds of the stock offering will provide the Company with a similar or higher tangible equity-to-assets ratio compared to the Peer Group and, thus, address current limitations on the Company’s ability to grow assets.

The general market for thrift stocks was up slightly since the date of the Original Appraisal, with the SNL Index for all publicly-traded thrifts increasing 1.84% since the date of the Original Appraisal compared to an increase of 2.80% in the DJIA. Comparatively, the updated pricing measures for the Peer Group and all publicly-traded thrifts were generally slightly lower since the date of the Original Appraisal. Home Bancorp of Wisconsin was the only standard conversion offering that has been completed during the past three months, which was a relatively small offering that closed at slightly above midpoint of its offering range. As of May 23, 2014, Home Bancorp’s closing stock price was below its IPO price.

Board of Trustees

Boards of Directors

May 23, 2014

Page 17

Overall, taking into account the foregoing factors, we believe that the Company’s estimated pro market value as set forth in the Original Appraisal remains appropriate.

Valuation Approaches

In applying the accepted valuation methodology promulgated by the FRB and the Commissioner, i.e., the pro forma market value approach, we considered the three key pricing ratios in valuing Pilgrim Bancshares’ to-be-issued stock — price/earnings (“P/E”), price/book (“P/B”), and price/assets (“P/A”) approaches — all performed on a pro forma basis including the effects of the conversion proceeds.

In computing the pro forma impact of the offering and the related pricing ratios, the valuation parameters utilized in the Original Appraisal were updated with financial data as of March 31, 2014.

Consistent with the Original Appraisal, this updated appraisal continues to be based primarily on fundamental analysis techniques applied to the Peer Group, including the P/E approach, the P/B approach and the P/A approach. Also consistent with the Original Appraisal, this updated appraisal incorporates a “technical” analysis of recently completed offerings, including principally the P/B approach which (as discussed in the Original Appraisal) is the most meaningful pricing ratio as the pro forma P/E ratios reflect an assumed reinvestment rate and do not yet reflect the actual use of proceeds.

The Company will adopt “Employers’ Accounting for Employee Stock Ownership Plans” (“ASC 718-40”), which will cause earnings per share computations to be based on shares issued and outstanding excluding unreleased ESOP shares. For purposes of preparing the pro forma pricing analyses, we have reflected all shares issued in the offering, including all ESOP shares, to capture the full dilutive impact, particularly since the ESOP shares are economically dilutive, receive dividends and can be voted. However, we did consider the impact of the adoption of ASC 718-40 in the valuation.

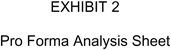

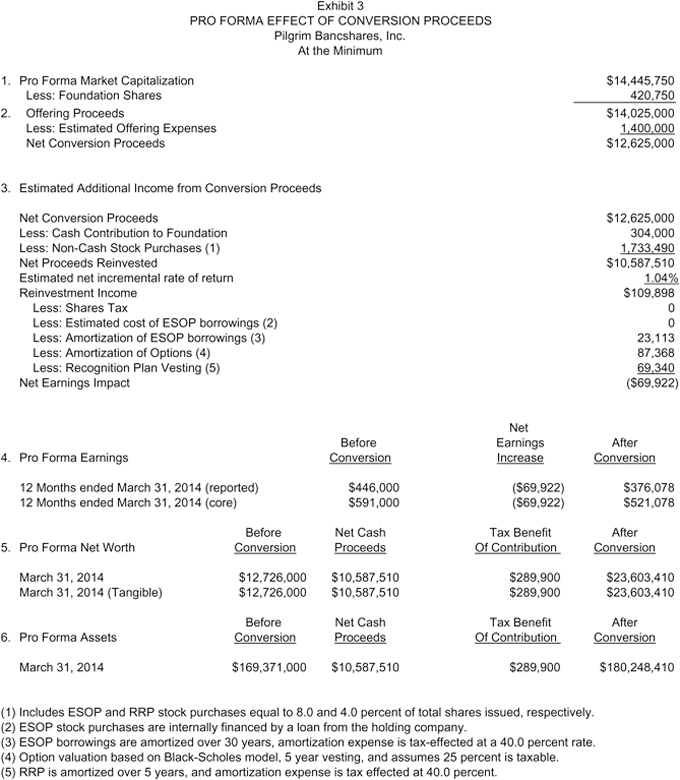

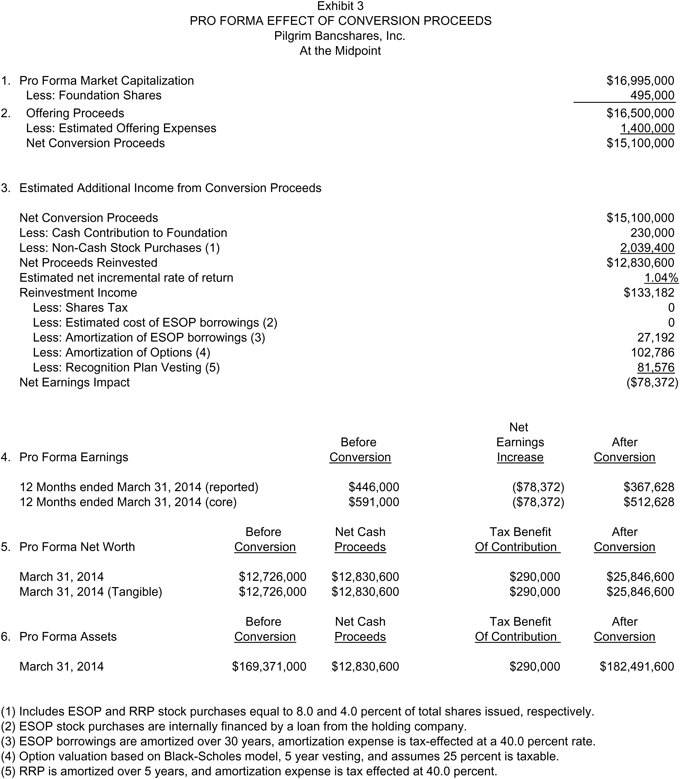

Based on the application of the three valuation approaches, taking into consideration the valuation adjustments discussed above and the dilutive impact of the stock contribution to the Foundation, RP Financial concluded that, as of May 23, 2014, the pro forma market value of Pilgrim Bancshares’ conversion stock was $16,995,000 at the midpoint, equal to 1,699,500 shares at $10.00 per share.

1.P/E Approach. In applying the P/E approach, RP Financial’s valuation conclusions considered both reported earnings and a recurring or “core” earnings base, that is, earnings adjusted to exclude any one time non-operating and extraordinary items, plus the estimated after tax-earnings benefit from reinvestment of net stock proceeds. The Company’s reported earnings equaled $446,000 for the twelve months ended March 31, 2014. In deriving Pilgrim Bancshares’ core earnings, the adjustments made to reported earnings were to eliminate gains on sale of securities equal to $5,000 and writedown of securities equal to $247,000. As shown below, on a tax-effected basis, assuming application of an effective marginal tax rate of 40.0%, the Company’s core earnings were determined to equal $591,000 for the twelve months ended March 31, 2014.

Board of Trustees

Boards of Directors

May 23, 2014

Page 18

| Amount | ||||

| ($000) | ||||

Net income | $ | 446 | ||

Deduct: Gain on sale of securities(1) | (3 | ) | ||

Add: Writedown of securities(1) | 148 | |||

|

| |||

Core earnings estimate | $ | 591 | ||

| (1) | Tax effected at 40.0%. |

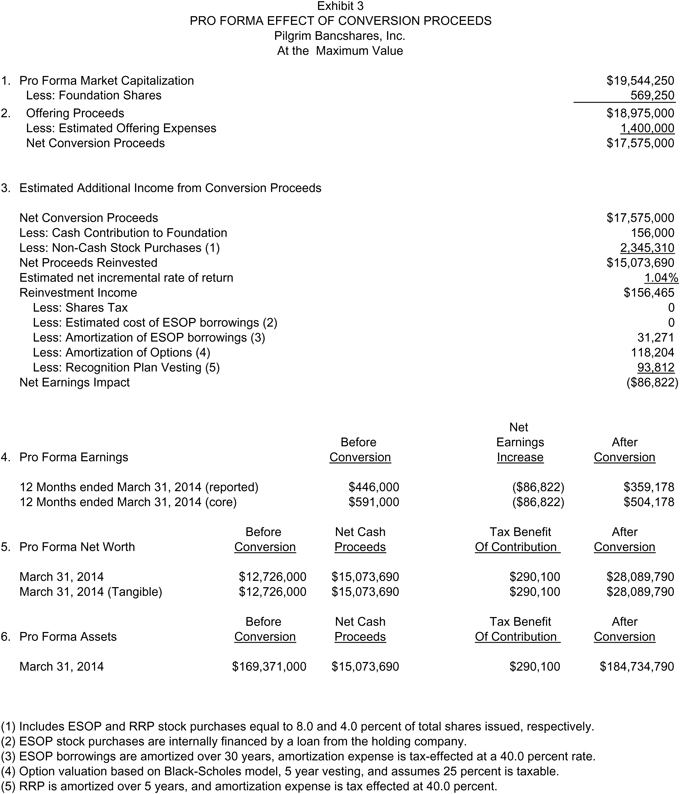

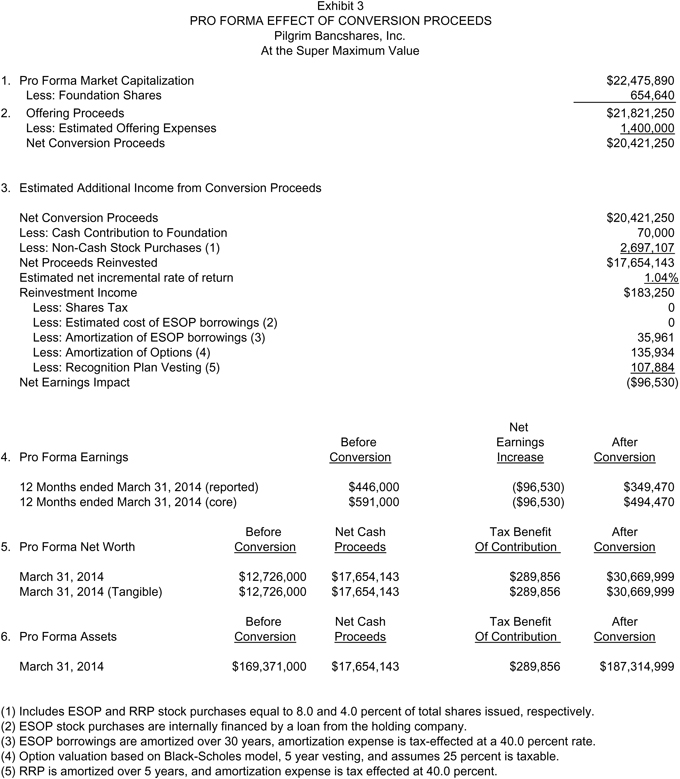

Based on Pilgrim Bancshares’ reported and estimated core earnings, and incorporating the impact of the pro forma assumptions discussed previously, the Company’s reported and core P/E multiples at the $17.0 million midpoint value equaled 46.23 times and 33.15 times, respectively. The Company’s updated reported and core P/E multiples provided for premiums of 95.23% and 40.59% relative to the Peer Group’s average reported and core P/E multiples of 23.68 times and 23.58 times, respectively (versus premiums of 139.19% and 70.88% relative to the Peer Group’s average reported and core P/E multiples as indicated in the Original Appraisal). The Company’s updated reported and core P/E multiples indicated premiums of 105.28% and 57.48% relative to the Peer Group’s median reported and core P/E multiples, which equaled 22.52 times and 21.05 times, respectively (versus premiums of 152.86% and 72.63% relative to the Peer Group’s median reported and core P/E multiples as indicated in the Original Appraisal). The Company’s pro forma P/E ratios based on reported earnings at the minimum and the super maximum equaled 38.41 times and 64.31 times, respectively, and based on core earnings at the minimum and the super maximum equaled 27.72 times and 45.45 times, respectively. The Company’s implied conversion pricing ratios relative to the Peer Group’s pricing ratios are indicated in Table 7, and the pro forma calculations are detailed in Exhibits 2 and 3.

2.P/B Approach. P/B ratios have generally served as a useful benchmark in the valuation of thrift stocks, with the greater determinant of long term value being earnings. In applying the P/B approach, we considered both reported book value and tangible book value. Based on the $17.0 million midpoint value, the Company’s P/B and P/TB ratios both equaled 65.75%. In comparison to the average P/B and P/TB ratios indicated for the Peer Group of 96.19% and 100.94%, respectively, Pilgrim Bancshares’ updated ratios reflected a discount of 31.65% on a P/B basis and a discount of 34.86% on a P/TB basis (versus discounts of 32.38% and 35.14% from the average Peer Group’s P/B and P/TB ratios as indicated in the Original Appraisal). In comparison to the median P/B and P/TB ratios indicated for the Peer Group of 96.81% and 99.29%, respectively, Pilgrim Bancshares’ updated ratios reflected discounts of 32.08% and 33.78% at the $17.0 million midpoint value (versus discounts of 31.86% and 33.76% from the Peer Group’s median P/B and P/TB ratios as indicated in the Original Appraisal). At the super maximum of the range, the Company’s P/B and P/TB ratios both equaled 73.26%. In comparison to the Peer Group’s average P/B and P/TB ratios, the Company’s P/B and P/TB ratios at the super maximum of the range reflected discounts of 23.84% and 27.42%, respectively. In comparison to the Peer Group’s median P/B and P/TB ratios, the Company’s P/B and P/TB ratios at the super maximum of the range reflected discounts of 24.33% and 26.22%, respectively. RP Financial considered the discounts under the P/TB approach to be reasonable, given the nature of the calculation of the P/B ratio which mathematically results in a ratio discounted to book value. The discounts reflected under the P/B approach were also supported by the premiums reflected in the Company’s P/E multiples.

Board of Trustees

Boards of Directors

May 23, 2014

Page 19

Table 7

Public Market Pricing Versus Peer Group

Pilgrim Bancshares, Inc. and the Comparables

As of May 23, 2014

| Market | Per Share Data | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capitalization | Core | Book | Dividends(3) | Financial Characteristics(5) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Price/ | Market | 12 Month | Value/ | Pricing Ratios(2) | Amount/ | Payout | Total | Equity/ | Tang. Eq./ | NPAs/ | Reported | Core | Offering | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Share | Value | EPS(1) | Share | P/E | P/B | P/A | P/TB | P/Core | Share | Yield | Ratio(4) | Assets | Assets | T. Assets | Assets | ROAA | ROAE | ROAA | ROAE | Range | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ($) | ($Mil) | ($) | ($) | (x) | (%) | (%) | (%) | (x) | ($) | (%) | (%) | ($Mil) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | ($Mil) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Pilgrim Bancshares, Inc. | MA | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Super Maximum | $ | 10.00 | $ | 22.48 | $ | 0.22 | $ | 13.65 | 64.31x | 73.26 | % | 12.00 | % | 73.26 | % | 45.45x | $ | 0.00 | 0.00 | % | 0.00 | % | $ | 187 | 16.37 | % | 16.37 | % | 3.66 | % | 0.19 | % | 1.14 | % | 0.26 | % | 1.61 | % | $ | 21.82 | ||||||||||||||||||||||||||||||||||||||||||||||||

Maximum | $ | 10.00 | $ | 19.54 | $ | 0.26 | $ | 14.37 | 54.41x | 69.59 | % | 10.58 | % | 69.59 | % | 38.76x | $ | 0.00 | 0.00 | % | 0.00 | % | $ | 185 | 15.21 | % | 15.21 | % | 3.71 | % | 0.19 | % | 1.28 | % | 0.27 | % | 1.79 | % | $ | 18.98 | ||||||||||||||||||||||||||||||||||||||||||||||||

Midpoint | $ | 10.00 | $ | 17.00 | $ | 0.30 | $ | 15.21 | 46.23x | 65.75 | % | 9.31 | % | 65.75 | % | 33.15x | $ | 0.00 | 0.00 | % | 0.00 | % | $ | 182 | 14.16 | % | 14.16 | % | 3.75 | % | 0.20 | % | 1.42 | % | 0.28 | % | 1.98 | % | $ | 16.50 | ||||||||||||||||||||||||||||||||||||||||||||||||

Minimum | $ | 10.00 | $ | 14.45 | $ | 0.36 | $ | 16.34 | 38.41x | 61.20 | % | 8.01 | % | 61.20 | % | 27.72x | $ | 0.00 | 0.00 | % | 0.00 | % | $ | 180 | 13.09 | % | 13.09 | % | 3.80 | % | 0.21 | % | 1.59 | % | 0.29 | % | 2.21 | % | $ | 14.03 | ||||||||||||||||||||||||||||||||||||||||||||||||

All Non-MHC Public Companies(6) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages | $ | 16.06 | $ | 387.37 | $ | 0.84 | $ | 15.46 | 17.78x | 104.01 | % | 13.05 | % | 112.22 | % | 17.71x | $ | 0.29 | 1.81 | % | 53.76 | % | $ | 2,715 | 13.20 | % | 12.60 | % | 2.42 | % | 0.56 | % | 4.47 | % | 0.57 | % | 4.52 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

Median | $ | 14.28 | $ | 103.27 | $ | 0.60 | $ | 14.35 | 17.11x | 94.53 | % | 12.28 | % | 99.39 | % | 16.25x | $ | 0.24 | 1.54 | % | 42.93 | % | $ | 846 | 12.21 | % | 11.38 | % | 1.78 | % | 0.57 | % | 4.56 | % | 0.61 | % | 4.51 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

All Non-MHC State of MA(6) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Averages | $ | 22.91 | $ | 155.45 | $ | 1.34 | $ | 20.60 | 20.62x | 105.03 | % | 12.43 | % | 111.60 | % | 20.81x | $ | 0.34 | 1.55 | % | 79.82 | % | $ | 1,395 | 11.94 | % | 11.46 | % | 1.00 | % | 0.51 | % | 4.85 | % | 0.50 | % | 4.58 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

Medians | $ | 17.84 | $ | 114.53 | $ | 0.45 | $ | 16.49 | 20.67x | 100.47 | % | 11.23 | % | 105.29 | % | 20.95x | $ | 0.24 | 1.45 | % | 48.31 | % | $ | 718 | 11.27 | % | 11.27 | % | 0.81 | % | 0.48 | % | 4.14 | % | 0.40 | % | 3.21 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

State of MA (7) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

BHLB | Berkshire Hills Bancorp Inc. | MA | $ | 22.67 | $ | 569.21 | $ | 1.79 | $ | 26.99 | 19.05x | 83.99 | % | 9.47 | % | 143.08 | % | 12.67x | $ | 0.72 | 3.18 | % | 60.50 | % | $ | 6,010 | 11.27 | % | 6.94 | % | 0.66 | % | 0.54 | % | 4.34 | % | 0.83 | % | 6.68 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

BLMT | BSB Bancorp Inc. | MA | $ | 17.95 | $ | 162.60 | $ | 0.25 | $ | 14.55 | NM | 123.38 | % | 13.91 | % | 123.38 | % | NM | $ | 0.00 | 0.00 | % | NM | $ | 1,169 | 11.27 | % | 11.27 | % | 0.81 | % | 0.22 | % | 1.72 | % | 0.22 | % | 1.72 | % | |||||||||||||||||||||||||||||||||||||||||||||||||

CBNK | Chicopee Bancorp Inc. | MA | $ | 16.75 | $ | 91.09 | $ | 0.08 | $ | 16.67 | NM | 100.47 | % | 15.18 | % | 100.47 | % | NM | $ | 0.28 | 1.67 | % | 300.00 | % | $ | 600 | 15.11 | % | 15.11 | % | 1.79 | % | 0.07 | % | 0.43 | % | 0.07 | % | 0.44 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

GTWN | Georgetown Bancorp Inc. | MA | $ | 14.70 | $ | 26.96 | $ | 0.45 | $ | 15.87 | 32.67x | 92.64 | % | 10.05 | % | 92.64 | % | 32.67x | $ | 0.17 | 1.16 | % | 36.11 | % | $ | 268 | 10.85 | % | 10.85 | % | 0.52 | % | 0.33 | % | 2.72 | % | 0.33 | % | 2.72 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

HBNK | Hampden Bancorp Inc. | MA | $ | 15.99 | $ | 90.41 | $ | 0.76 | $ | 15.19 | 22.52x | 105.29 | % | 12.60 | % | 105.29 | % | 21.05x | $ | 0.24 | 1.50 | % | 33.80 | % | $ | 718 | 11.97 | % | 11.97 | % | 1.48 | % | 0.57 | % | 4.56 | % | 0.61 | % | 4.87 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

HIFS | Hingham Instit. for Savings | MA | $ | 74.74 | $ | 159.10 | $ | 7.26 | $ | 52.70 | 8.14x | 141.83 | % | 11.05 | % | 141.83 | % | 10.30x | $ | 1.08 | 1.45 | % | 14.71 | % | $ | 1,440 | 7.79 | % | 7.79 | % | 0.74 | % | 1.51 | % | 19.18 | % | 1.19 | % | 15.16 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

PEOP | Peoples Federal Bancshares Inc | MA | $ | 18.28 | $ | 114.53 | $ | 0.35 | $ | 16.49 | NM | 110.85 | % | 19.21 | % | 110.85 | % | NM | $ | 0.20 | 1.09 | % | 120.00 | % | $ | 601 | 17.33 | % | 17.33 | % | 0.34 | % | 0.37 | % | 2.00 | % | 0.37 | % | 2.00 | % | ||||||||||||||||||||||||||||||||||||||||||||||||