Goodwin Procter LLP Counselors at Law Exchange Place Boston, MA 02109 T: 617.570.1000 F: 617.523.1231 |

July 15, 2014

VIA EDGAR AND FEDERAL EXPRESS

Pamela Long

Securities and Exchange Commission

Division of Corporation Finance

Mail Stop 4561

100 F Street, NE

Washington, D.C. 20549

| Re: | Vascular Biogenics Ltd. |

| Amendment No. 1 to Registration Statement on Form F-1 |

| Filed June 25, 2014 |

| File No. (333-196584) |

Dear Ms. Long:

This letter is submitted on behalf of Vascular Biogenics Ltd. (the “Company”) in response to the comments of the staff of the Division of Corporation Finance (the “Staff”) of the Securities and Exchange Commission (the “Commission”) with respect to the Company’s filing of its Registration Statement on Form F-1 on June 6, 2014, as amended by Amendment No. 1 filed on June 25, 2014 (the “Registration Statement”), as set forth in the Staff’s letter dated July 1, 2014 (the “Comment Letter”). The Company is concurrently filing Amendment No. 2 to the Registration Statement on Form F-1 (“Amendment No. 2”), which includes changes on pages 77, F-21, F-22 and F-35 thereof to reflect responses to the Staff’s comments.

For reference purposes, the text of the Comment Letter has been reproduced and italicized herein with responses below each numbered comment. Unless otherwise indicated, page references in the descriptions of the Staff’s comments refer to the Registration Statement. All capitalized terms used and not otherwise defined herein shall have the meanings set forth in the Registration Statement.

The responses provided herein are based upon information provided to Goodwin Procter LLP by the Company. In addition to confidentially submitting this letter via EDGAR, we are sending via Federal Express four (4) copies of this letter.

United States Securities and Exchange Commission

July 15, 2014

Page 2

Financial Statements, page F-1

Note 8—Convertible Loan, Page F-21

| 1. | We have considered your response to prior comment two. It continues to be unclear why you have accounted for the difference between the fair value of the convertible loan and the principal amount as a deemed distribution. We note that you also believe that this represents a transaction with shareholders and as you state in your June 6, 2014 response in comment 2 “the Company viewed this transaction as being carried out [by its shareholders] in their capacity as shareholders.” Please address each of the following in your response: |

| • | We note that you attempted to obtain funding in 2013 from third parties. Please tell us the nature and the terms of the funding that you attempted to secure. To the extent that the funding represented a liability, compare the terms of that funding with the convertible loan agreement. |

RESPONSE: The Company respectfully advises the Staff that it had discussions in 2013 with potential investors (mainly venture capitalists) in order to raise additional funds. The Company’s focus was only on an investment in preferred shares of the Company. There was no liability funding from third parties that was contemplated during this time.

| • | We note that the loan has an annual interest rate of 10%. Please compare this annual interest rate to the interest rate implicit in other arrangements which include a financing element, such as but not limited to operating leases. |

RESPONSE: The Company respectfully advises the Staff that it did not receive any loans in the past and, therefore, the Company cannot make the requested comparisons. Because the Company is in the research and development stage and has not yet generated revenues, the Company does not have financing arrangements other than equity. Please note that the probability of repayment of the convertible loan was remote because it would occur only upon an exit event. This was clear from a number of vantage points given the Company’s cash position as well as the Company’s development status and the short time frame for completion of such a transaction. Therefore, while the coupon rate is 10%, it is, in the Company’s view, irrelevant for the overall analysis of the transaction.

| • | Please explain why you did not allocate any portion of the difference between the fair value of the convertible loan and the principal amount as an interest or other finance cost of the loan. Please also explain how the cost of capital of the convertible loan compares with your historic cost of capital. |

United States Securities and Exchange Commission

July 15, 2014

Page 3

RESPONSE: The Company respectfully advises the Staff that it does not have historical comparatives since the Company did not receive financing in the past and therefore it did not allocate any portion of the differences in fair value to interest or other finance cost of the loan. There is no historical cost of capital in the Company to refer to as a comparative or representative figure.

| • | In your response to prior comment two you address paragraph AG76(a) of IAS 39. Please explain why the difference between the fair value of the loan and the transaction was not deferred at initial recognition with changes in market participant factors reported as a gain or loss. We note that subsequent to the initial recognition you have reported changes in the fair value of the convertible loan. Specifically address AG76(b) of IAS 39 in your response. |

RESPONSE: The Company respectfully advises the Staff that, as detailed in its previous letters, the Company analyzed the substance of the transaction, concluding that the transaction price did not represent the fair value of the liability because the funding was provided by our controlling shareholders and determined, in accordance with publications referred to in our previous letters, to treat the fair value difference as deemed distributions to shareholders. The conclusion was that the difference was a capital distribution. Please find enclosed relevant guidance.

Once the difference between the fair value of the liability and the cash received was charged to equity based on AG 64, the Company does not believe it falls under the scope of AG76.

Please note that even if the Company had implemented AG76(b) and deferred the Day 1 loss, there would have been no amortization of this loss since there were no changes in market participant factors. For that reason, applying AG76(b) would result in a reduction of the Company’s liability with a parallel increase in equity and no financial expenses at all in the Company’s statement of comprehensive loss.

Please also note that we did record a Day 2 P&L charge related to this loan.

In addition, the Company’s accounting treatment may be also seen as compliant with AG76(a) and (b). In this case, the deferral of the loss that these paragraphs require was recorded in equity as a reflection of the substance of the transaction. Since there was no change in market participant factors over the terms of the instrument, that deferral was not recognized in the P&L.

| • | Please explain why you did not consider amortizing the difference as a financing or other expense. Specifically address BC222(v)(ii) in your response. |

United States Securities and Exchange Commission

July 15, 2014

Page 4

RESPONSE: The Company respectfully advises the Staff that under its accounting treatment, this question is not relevant. As mentioned, even if the Company would have implemented AG 76(b), there would have been no amortization of this loss.

If you should have any questions concerning the enclosed matters, please contact the undersigned at (617) 570-1035.

| Sincerely, |

| /s/ Lawrence S. Wittenberg |

| Lawrence S. Wittenberg |

Enclosures

cc:

Amos Ron,Vascular Biogenics Ltd.

Dror Harats,Vascular Biogenics Ltd.

Mitchell S. Bloom,Goodwin Procter LLP

Brent B. Siler,Cooley LLP

Darren K. DeStefano,Cooley LLP

Vascular Biogenics Ltd.

Deloitte. iGAAP 2014 Volume B Financial Instruments – IFRS 9 and related Standards LexisNexis®

1

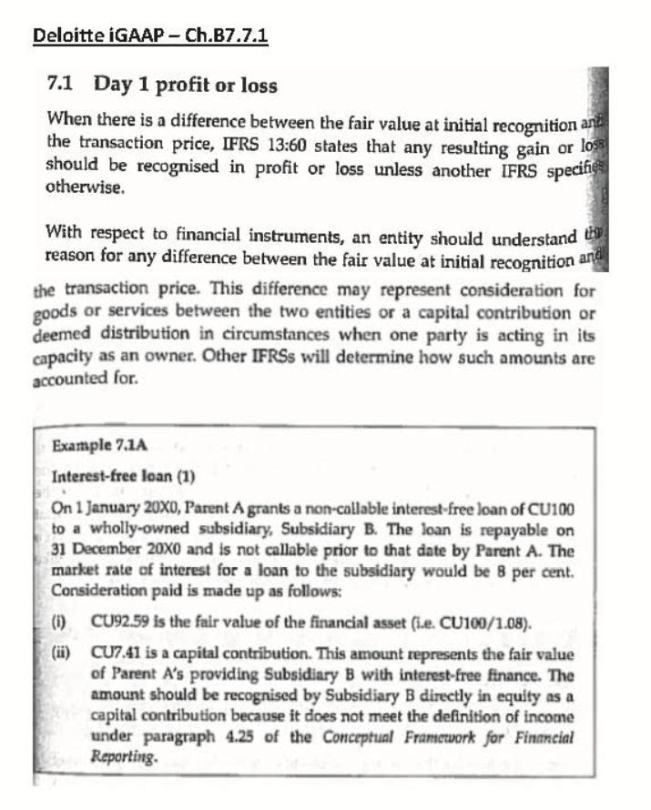

Deloitte iGAAP – Ch.B7.7.1 7.1 Day 1 profit or loss When there is a difference between the fair value at initial recognition and the transaction price, IFRS 13:60 states that any resulting gain or loss should be recognised in profit or loss unless another IFRS specifies otherwise. With respect to financial instruments, an entity should understand the reason for any difference between the fair value at initial recognition and the transaction price. This difference may represent consideration for goods or services between the two entities or a capital contribution or deemed distribution in circumstances when one party is acting in its capacity as an owner. Other IFRSs will determine how such amounts are accounted for. Example 7.1A Interest-free loan (1) On 1 January 20X0, Parent A grants a non-callable interest-free loan of CU100 to a wholly-owned subsidiary, Subsidiary B. The loan is repayable on 31 December 20X0 and is not callable prior to that date by Parent A. The market rate of interest for a loan to the subsidiary would be 8 per cent. Consideration paid is made up as follows: (i) CU92.59 is the fair value of the financial asset (i.e. CU100/1.08). (ii) CU7.41 is a capital contribution. This amount represents the fair value of Parent A’s providing Subsidiary B with interest-free finance. The amount should be recognised by Subsidiary B directly in equity as a capital contribution because it does not meet the definition of income under paragraph 4.25 of the Conceptual Framework for Financial Reporting.

2

BDO NEED TO KNOW IFRS 13 Fair Value Measurement

3

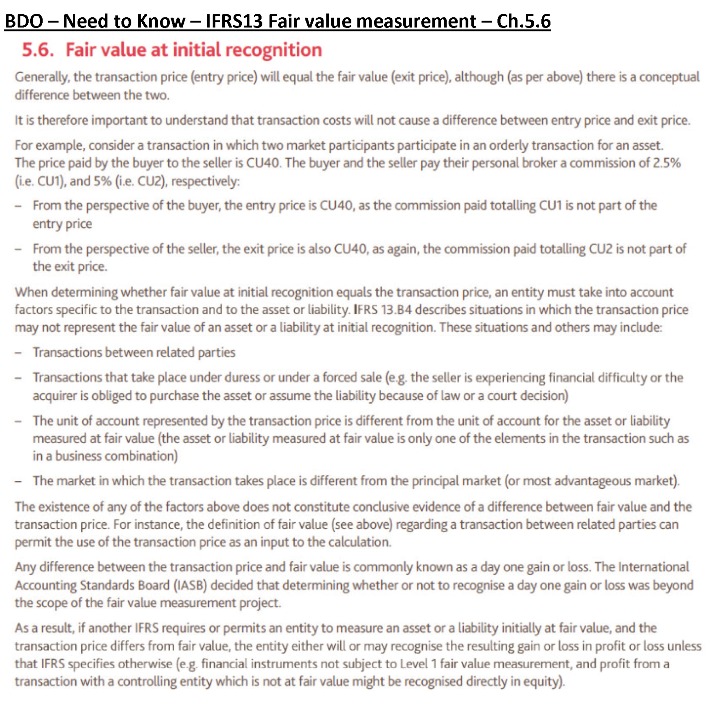

BDO – Need to Know – IFRS13 Fair value measurement – Ch.5.6 5.6. Fair value at initial recognition Generally, the transaction price (entry price) will equal the fair value (exit price), although (as per above) there is a conceptual difference between the two. It is therefore important to understand that transaction costs will not cause a difference between entry price and exit price. For example, consider a transaction in which two market participants participate in an orderly transaction for an asset. The price paid by the buyer to the seller is CU40. The buyer and the seller pay their personal broker a commission of 2.5% (i.e. CU1), and 5% (i.e. CU2), respectively: - From the perspective of the buyer, the entry price is CU40, as the commission paid totalling CU1 is not part of the entry price - From the perspective of the seller, the exit price is also CU40, as again, the commission paid totalling CU2 is not part of the exit price. When determining whether fair value at initial recognition equals the transaction price, an entity must take into account factors specific to the transaction and to the asset or liability. IFRS 13.B4 describes situations in which the transaction price may not represent the fair value of an asset or a liability at initial recognition. These situations and others may include: - Transactions between related parties - Transactions that take place under duress or under a forced sale (e.g. the seller is experiencing financial difficulty or the acquirer is obliged to purchase the asset or assume the liability because of law or a court decision) - The unit of account represented by the transaction price is different from the unit of account for the asset or liability measured at fair value (the asset or liability measured at fair value is only one of the elements in the transaction such as in a business combination) - The market in which the transaction takes place is different from the principal market (or most advantageous market). The existence of any of the factors above does not constitute conclusive evidence of a difference between fair value and the transaction price. For instance, the definition of fair value (see above) regarding a transaction between related parties can permit the use of the transaction price as an input to the calculation. Any difference between the transaction price and fair value is commonly known as a day one gain or loss. The International Accounting Standards Board (IASB) decided that determining whether or not to recognise a day one gain or loss was beyond the scope of the fair value measurement project. As a result, if another IFRS requires or permits an entity to measure an asset or a liability initially at fair value, and the transaction price differs from fair value, the entity either will or may recognise the resulting gain or loss in profit or loss unless that IFRS specifies otherwise (e.g. financial instruments not subject to Level 1 fair value measurement, and profit from a transaction with a controlling entity which is not at fair value might be recognised directly in equity).

4