Table of Contents

Submitted on a confidential basis on August 22, 2014

CONFIDENTIAL TREATMENT REQUESTED

This draft registration statement has not been filed publicly with the Securities and Exchange Commission

and all information contained herein remains confidential.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Euronav NV

(Exact name of Registrant as specified in its Charter)

| Belgium | 4412 | N/A | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

Euronav NV De Gerlachekaai 20 2000 Antwerpen Belgium Tel: 011-32-3-247-4411 | Seward & Kissel LLP Attention: Gary J. Wolfe One Battery Park Plaza New York, New York 10004 Tel: (212) 574-1200 | |

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices) | (Name, address and telephone number of agent for service) |

Copies to:

Gary J. Wolfe, Esq. Robert E. Lustrin, Esq. Seward & Kissel LLP One Battery Park Plaza New York, New York 10004 Tel: (212) 574-1223 (telephone number) Fax: (212) 480-8421 (facsimile number) | Stephen P. Farrell, Esq. Finnbarr D. Murphy, Esq. Morgan, Lewis & Bockius LLP 101 Park Avenue New York, New York 10178 Tel: (212) 309-6000 (telephone number) Fax: (212) 309-6001 (facsimile number) |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

Table of Contents

If any of the securities being registered on this Form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ��

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

| ||||

Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee(3) | ||

Ordinary Shares, no par value | $ | $ | ||

| ||||

| ||||

| (1) | Includes ordinary shares that may be sold pursuant to exercise of the underwriters’ option to purchase additional shares. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (3) | Calculated in accordance with Rule 457(o) under the Securities Act of 1933. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the U.S. Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this Preliminary Prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This Prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED AUGUST 22, 2014

PRELIMINARY PROSPECTUS

Ordinary Shares

Euronav NV

We are offering of our ordinary shares, and the selling shareholders are selling of our ordinary shares. We will not receive any proceeds from the sale of ordinary shares by the selling shareholders.

This is our initial public offering in the United States and currently our ordinary shares are not listed on any United States securities exchange. We intend to apply to list our ordinary shares on the New York Stock Exchange under the symbol “EURN.” Our ordinary shares currently trade on the NYSE Euronext Brussels, under the symbol “EURN.” On August 19, 2014, the closing price of our ordinary shares trading on the NYSE Euronext Brussels was €9.15 per share, which was equivalent to approximately $12.18 per share based on the Bloomberg Composite Rate of €0.7508 per $1.00 in effect on that date.

We qualify as an “emerging growth company” as defined in the Securities Act of 1933, as amended, and, as such, we are eligible for reduced reporting requirements. See “Summary—Implications of Being an Emerging Growth Company.”

Investing in our ordinary shares involves risks. See “Risk Factors” beginning on page 19.

We have granted the underwriters an option to purchase up to an additional of our ordinary shares to cover over-allotments and the selling shareholders have granted the underwriters an option to purchase up to an additional of our ordinary shares to cover over-allotments.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

PRICE $ PER SHARE

| Initial Public Offering Price | Underwriting Discounts and Commissions (1) | Proceeds (Before Expenses) to Euronav NV | Proceeds to Selling Shareholders | |||||||||||||

Per Share | $ | $ | $ | $ | ||||||||||||

Total | $ | $ | $ | $ | ||||||||||||

| (1) | See “Underwriting” for additional information regarding the total underwriter compensation. |

The underwriters expect to deliver the ordinary shares to purchasers on or about , 2014.

| Deutsche Bank Securities | J.P. Morgan |

Table of Contents

Flandre,one of our VLCCs

CAP Lara, one of our Suezmax vessels

FSO Asia, one of our FSOs

Table of Contents

| 1 | ||||

| 11 | ||||

| 13 | ||||

| 17 | ||||

| 19 | ||||

| 43 | ||||

| 44 | ||||

| 46 | ||||

| 47 | ||||

| 48 | ||||

| 49 | ||||

| 50 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 54 | |||

| 81 | ||||

| 99 | ||||

| 108 | ||||

| 125 | ||||

| 130 | ||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS, MANAGEMENT AND SELLING SHAREHOLDERS | 133 | |||

| 134 | ||||

| 137 | ||||

| 141 | ||||

| 142 | ||||

| 153 | ||||

| 157 | ||||

| 157 | ||||

| 157 | ||||

| 158 | ||||

| 158 | ||||

| F-1 | ||||

| A-1 |

You should rely only on the information contained in this prospectus or in any free writing prospectus we may authorize to be delivered to you. We have not, the selling shareholders have not and the underwriters have not, authorized any other person to provide you with additional, different or inconsistent information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We may not and the selling shareholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission (the “SEC”) is effective. We are not and the selling shareholders are not and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information appearing in this prospectus is accurate as of any date other than the date on the front cover of this prospectus unless otherwise specified herein. Our business, financial condition, results of operations and prospects may have changed since that date. Information contained on our website does not constitute part of this prospectus.

Until , 2014 (the 25th day after the date of this prospectus), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Table of Contents

This summary highlights information that appears later in this prospectus. This summary may not contain all of the information that may be important to you. As an investor or prospective investor, you should carefully review the entire prospectus, including the section of this prospectus entitled “Risk Factors” and the more detailed information that appears later in this prospectus before you consider making an investment in our ordinary shares. The information presented in this prospectus assumes, unless otherwise indicated, that the underwriters’ over-allotment option to purchase additional ordinary shares is not exercised.

Unless otherwise indicated, references to “Euronav,” the “Company,” “we,” “our,” “us” or similar terms refer to, Euronav NV, and its subsidiaries. All references in this prospectus to “Chevron,” “Total,” “Valero,” “Rosneft,” and “Maersk Oil” refer to Chevron Corporation, Total S.A., Valero Energy Corporation, TSC Rosnefteflot” and Maersk Oil Qatar AS, respectively, and certain of each of their subsidiaries that are our customers. References to our “ordinary shares” refer to the shares offered hereby and references to our “existing ordinary shares” refer to the shares issued and listed on the NYSE Euronext in Belgium prior to the closing of this offering. Unless otherwise indicated, all references to “U.S. dollars,” “USD,” “dollars,” “US$” and “$” in this prospectus are to the lawful currency of the United States of America and references to “Euro,” “EUR,” and “€” are to the lawful currency of Belgium. We refer you to a glossary of shipping terms in Appendix A for the definition of certain industry terms used in this prospectus.

OUR BUSINESS

We are a fully-integrated provider of international maritime shipping and offshore services engaged primarily in the transportation and storage of crude oil. We were incorporated under the laws of Belgium on June 26, 2003, and we grew out of the combination of certain tanker businesses carried out by three companies that had a strong presence in the shipping industry: Compagnie Maritime Belge NV, or CMB, formed in 1895, Compagnie Nationale de Navigation SA, or CNN, formed in 1938, and Ceres Hellenic Shipping Enterprises Ltd., or Ceres Hellenic, formed in 1950. Our predecessor started doing business under the name “Euronav” in 1989.

Our principal shareholders are TankLog Holdings Ltd. (controlled by the Livanos family), or TankLog, and Saverco NV (controlled by Marc Saverys), or Saverco. Both the Livanos and the Saverys families have had a continuous presence in the shipping industry since the early nineteenth century: the Livanos family has owned and operated Ceres Hellenic since its formation in 1950, and the Saverys family owned a shipyard which was founded in 1829, owned and operated various shipowning companies since the 1960s, and acquired CMB in 1991. TankLog, which currently owns 16.4% of our outstanding ordinary shares, is represented on our Board of Directors by Peter Livanos, who serves as the Chairman of our Board of Directors through his appointment as permanent representative of TankLog. The Vice Chairman of our Board of Directors, Marc Saverys, is also the Chief Executive Officer of CMB and controls Saverco, a company that is currently CMB’s majority shareholder and owns 12.4% of our outstanding ordinary shares. Upon completion of this offering, Tanklog and Saverco will own approximately % and %, respectively, of our outstanding ordinary shares.

As of August 18, 2014, we owned and operated a modern fleet of 53 vessels (including five chartered-in vessels) with an aggregate carrying capacity of approximately 13.3 million deadweight tons, or dwt, consisting of 27 very large crude carriers, or VLCCs, one ultra large crude carrier, or ULCC, 23 Suezmax vessels, and two floating, storage and offloading vessels, or FSOs. In addition, we currently commercially manage two Suezmax vessels owned by third-parties.

In January 2014, we agreed to acquire 15 modern VLCCs with an average age at the time of acquisition of approximately 4.1 years from Maersk Tankers Singapore Pte Ltd., or Maersk Tankers, which we refer to as the “Maersk Acquisition Vessels,” for a total purchase price of $980.0 million payable as the vessels are delivered to us charter-free. This acquisition has been fully financed through a combination of new equity and debt issuances and borrowings under our $500.0 Million Senior Secured Credit Facility. During the period from February 2014 through the date of this prospectus, we took delivery of 14 of the Maersk Acquisition Vessels,Nautilus,Nucleus,Navarin,Newton,Sara,Ilma, Nautic,Ingrid, Noble, Nectar, Simone, Neptun, Sonia,andIris,and we expect to take delivery of the remaining vessel between November 2014 and March 2015. In addition, in July 2014, we agreed to acquire four additional modern VLCCs from Maersk Tankers for an aggregate purchase price of $342.0 million, which we refer to as the “VLCC Acquisition Vessels.” The purchase price of the VLCC Acquisition Vessels will be financed using the net proceeds of $121.0 million that we received in an underwritten private offering of 10,556,808 of our ordinary shares in Belgium in July 2014 (see “Recent and Other Developments - Private Offering of Ordinary Shares in Belgium”), available cash on hand, and borrowings under new secured credit facilities, including a new $340.0 million credit facility for which we received a non-binding term sheet, which we refer to as the “Proposed $340.0 Million Credit Facility.” Three of these vessels are expected to be delivered to us during the third and fourth quarters of 2014 and the last vessel during the second quarter of 2015. After taking delivery of the four VLCC Acquisition Vessels (three of which we currently charter in) and the remaining Maersk Acquisition Vessel, we will own and operate 55 double-hulled tankers (including our two FSOs) with an aggregate carrying capacity of approximately 13.9 million dwt. The weighted average age of our fleet as of August 18, 2014, taking into account these vessel acquisitions, including those to be delivered to us after this date, was approximately 6.8 years, as compared to an industry average age of approximately 9.8 years, according to Drewry Shipping Consultants Ltd., or Drewry.

We currently charter our vessels, non-exclusively, to leading international energy companies, such as Chevron, Maersk Oil, Total and Valero, although there is no guarantee that these companies will continue their relationships with us. We pursue a chartering strategy that seeks an optimal mix of employment of our vessels depending on the fluctuations of freight

1

Table of Contents

rates in the market and our own judgment as to the direction of those rates in the future. Our vessels are therefore routinely employed on a combination of spot market voyages, fixed-rate contracts and long-term time charters, which typically include a profit sharing component. We principally employ our VLCCs, and expect to employ the four undelivered VLCC Acquisition Vessels and the remaining undelivered Maersk Acquisition Vessel, through the Tankers International Pool, or the TI Pool, a spot market-oriented pool in which we were a founding member in 2000. As of August 18, 2014, 19 of our vessels were employed directly in the spot market, 25 of our vessels were employed in the TI Pool, seven of our vessels were employed on long-term charters, including five with profit sharing components, of which the average remaining duration is 4.5 months, and our two FSOs were employed on long-term service contracts. While we believe that our chartering strategy allows us to capitalize on opportunities in an environment of increasing rates by maximizing our exposure to the spot market, our vessels operating in the spot market may be subject to market downturns to the extent spot market rates decline. At times when the freight market may become more challenging, we will try to timely shift our exposure to more time charter contracts and potentially dispose of some of our assets which should provide us with incremental stable cash flows and stronger utilization rates supporting our business during periods of market weakness. We believe that our chartering strategy and our fleet size management, combined with the leadership of our experienced management team should enable us to capture value during cyclical upswings and to withstand the challenging operating environment such as the one seen in the past several years.

We operate in a capital intensive industry and have historically financed our purchase of tankers and other capital expenditures through a combination of cash generated from operations, equity capital, borrowings from commercial banks and the issuance of convertible notes. Our ability to generate adequate cash flows on a short- and medium-term basis depends substantially on the trading performance of our vessels. Historically, market rates for charters of our vessels have been volatile. For example, during the year ended December 31, 2013, our voyage charter and pool revenues decreased by 3% compared to the same period in 2012, from $175.9 million to $171.2 million, and our time charter revenue decreased by 8%, from $144.9 million to $133.4 million. During the six months ended June 30, 2014, our voyage charter and pool revenues increased by 60% compared to the same period in 2013, from $81.3 million to $130.1 million, reflecting higher realized spot market charter rates, and our time charter revenue decreased by 2% compared to the same period in 2013, from $72.5 million to $71.1 million because we had slightly less days on time charter. Periodic adjustments to the supply of and demand for oil tankers cause the industry to be cyclical in nature. We expect continued volatility in market rates for our vessels in the foreseeable future with a consequent effect on our short- and medium-term revenue and liquidity.

For our fiscal year ended December 31, 2013, we had $304.6 million in revenue and incurred a net loss of $89.7 million, and for the six month period ended June 30, 2014, we had $201.2 million in revenue and incurred a net loss of $21.2 million. There is no guarantee that our past results will be indicative of our future performance.

Our Fleet

The following table sets forth summary information regarding our fleet as of August 18, 2014:

| Vessel Name | Type | Deadweight Tons (DWT) | Year Built | Shipyard(1) | Charterer | Employment | Charter Expiry Date(2) | |||||||||||

Owned Vessels | ||||||||||||||||||

TI Europe | ULCC | 441,561 | 2002 | Daewoo | Spot | N/A | ||||||||||||

Sara | VLCC | 323,183 | 2011 | STX | TI Pool | N/A | ||||||||||||

Alsace | VLCC | 320,350 | 2012 | Samsung | TI Pool | N/A | ||||||||||||

TI Hellas | VLCC | 319,254 | 2005 | Hyundai | TI Pool | N/A | ||||||||||||

Antarctica(3) | VLCC | 315,981 | 2009 | Hyundai | Total | Time Charter(4) | May 2015 | |||||||||||

Olympia(3) | VLCC | 315,981 | 2008 | Hyundai | Total | Time Charter(4) | April 2015 | |||||||||||

Ilma | VLCC | 314,000 | 2012 | Hyundai | TI Pool | N/A | ||||||||||||

Simone | VLCC | 314,000 | 2012 | STX | TI Pool | N/A | ||||||||||||

Sonia | VLCC | 314,000 | 2012 | STX | TI Pool | N/A | ||||||||||||

Ingrid | VLCC | 314,000 | 2012 | Hyundai | TI Pool | N/A | ||||||||||||

Iris | VLCC | 314,000 | 2012 | Hyundai | TI Pool | N/A | ||||||||||||

Nucleus | VLCC | 307,284 | 2007 | Dalian | TI Pool | N/A | ||||||||||||

Nautilus | VLCC | 307,284 | 2006 | Dalian | TI Pool | N/A | ||||||||||||

| Navarin | VLCC | 307,284 | 2007 | Dalian | TI Pool | N/A | ||||||||||||

Nautic | VLCC | 307,284 | 2008 | Dalian | TI Pool | N/A | ||||||||||||

Newton | VLCC | 307,284 | 2009 | Dalian | TI Pool | N/A | ||||||||||||

Nectar | VLCC | 307,284 | 2008 | Dalian | TI Pool | N/A | ||||||||||||

Neptun | VLCC | 307,284 | 2007 | Dalian | TI Pool | N/A | ||||||||||||

Noble | VLCC | 307,284 | 2008 | Dalian | TI Pool | N/A | ||||||||||||

Flandre | VLCC | 305,688 | 2004 | Daewoo | TI Pool | N/A | ||||||||||||

V.K. Eddie(5) | VLCC | 305,261 | 2005 | Daewoo | TI Pool | N/A | ||||||||||||

TI Topaz | VLCC | 319,430 | 2002 | Hyundai | TI Pool | N/A | ||||||||||||

Famenne | VLCC | 298,412 | 2001 | Hitachi | TI Pool | N/A | ||||||||||||

Artois | VLCC | 298,330 | 2001 | Hitachi | TI Pool | N/A | ||||||||||||

Cap Diamant | Suezmax | 160,044 | 2001 | Hyundai | Rosneft | Time Charter | October 2014 | |||||||||||

Cap Pierre | Suezmax | 159,083 | 2004 | Samsung | Spot | N/A | ||||||||||||

Cap Leon | Suezmax | 159,049 | 2003 | Samsung | Spot | N/A | ||||||||||||

Cap Philippe | Suezmax | 158,920 | 2006 | Samsung | Valero | Time Charter(4) | May 2015 | |||||||||||

Cap Guillaume | Suezmax | 158,889 | 2006 | Samsung | Valero | Time Charter(4) | February 2015 | |||||||||||

Cap Charles | Suezmax | 158,881 | 2006 | Samsung | Spot | N/A | ||||||||||||

Cap Victor | Suezmax | 158,853 | 2007 | Samsung | Spot | N/A | ||||||||||||

Cap Lara | Suezmax | 158,826 | 2007 | Samsung | Spot | N/A | ||||||||||||

2

Table of Contents

| Vessel Name | Type | Deadweight Tons (DWT) | Year Built | Shipyard(1) | Charterer | Employment | Charter Expiry Date(2) | |||||||||||

Cap Theodora | Suezmax | 158,819 | 2008 | Samsung | Valero | Time Charter(4) | March 2015 | |||||||||||

Cap Felix | Suezmax | 158,765 | 2008 | Samsung | Spot | N/A | ||||||||||||

Fraternity | Suezmax | 157,714 | 2009 | Samsung | Spot | N/A | ||||||||||||

Eugenie(5) | Suezmax | 157,672 | 2010 | Samsung | Spot | N/A | ||||||||||||

Felicity | Suezmax | 157,667 | 2009 | Samsung | Spot | N/A | ||||||||||||

Capt. Michael(5) | Suezmax | 157,648 | 2012 | Samsung | Spot | N/A | ||||||||||||

Devon(5) | Suezmax | 157,642 | 2011 | Samsung | Spot | N/A | ||||||||||||

Maria(5) | Suezmax | 157,523 | 2012 | Samsung | Spot | N/A | ||||||||||||

Finesse | Suezmax | 149,994 | 2003 | Universal | Spot | N/A | ||||||||||||

Filikon | Suezmax | 149,989 | 2002 | Universal | Spot | N/A | ||||||||||||

Cap Georges | Suezmax | 146,652 | 1998 | Samsung | Spot | N/A | ||||||||||||

Cap Laurent | Suezmax | 146,645 | 1998 | Samsung | Spot | N/A | ||||||||||||

Cap Romuald | Suezmax | 146,640 | 1998 | Samsung | Spot | N/A | ||||||||||||

Cap Jean | Suezmax | 146,627 | 1998 | Samsung | Petrobras | Time Charter | November 2014 | |||||||||||

Total DWT – Owned Vessels | 11,014,245 | |||||||||||||||||

Maersk Acquisition Vessels To Be Delivered | ||||||||||||||||||

Sandra(6) | VLCC | 323,527 | 2011 | STX | TI Pool(7) | N/A | ||||||||||||

Total DWT – Maersk Acquisition Vessels | 323,527 | |||||||||||||||||

VLCC Acquisition Vessels To Be Delivered | ||||||||||||||||||

Maersk Hojo(8) (9) | VLCC | 302,965 | 2013 | Ariake | TI Pool(7) | N/A | ||||||||||||

Maersk Hakone(8) (9) | VLCC | 302,624 | 2010 | Ariake | TI Pool(7) | N/A | ||||||||||||

Maersk Hirado(8) (9) | VLCC | 302,550 | 2011 | Ariake | TI Pool(7) | N/A | ||||||||||||

Maersk Hakata(10) | VLCC | 302,550 | 2010 | Ariake | TI Pool(7) | N/A | ||||||||||||

Total DWT – VLCC Acquisition Vessels | 1,210,689 | |||||||||||||||||

| Chartered-In Expiry Date | ||||||||||||||||||

Chartered-In Vessels | ||||||||||||||||||

KHK Vision | VLCC | 305,749 | 2007 | Daewoo | TI Pool | October 2014 (+/- 30 days) | ||||||||||||

Cap Isabella(11) | Suezmax | 157,258 | 2013 | Samsung | Spot | March 2015 | ||||||||||||

Total DWT – Chartered-In Vessels | �� | 463,007 | ||||||||||||||||

| Management Contract Expiry Date | ||||||||||||||||||

Vessels Under Management | ||||||||||||||||||

Suez Rajan | Suezmax | 158,574 | 2011 | Hyundai | October 2014 | |||||||||||||

Suez Hans | Suezmax | 158,574 | 2011 | Hyundai | September 2014 | |||||||||||||

| Service Contract Expiry Date | ||||||||||||||||||

FSO Vessels | ||||||||||||||||||

FSO Africa(5) | FSO | 442,000 | 2002 | Daewoo | Maersk Oil | Service Contract | September 2017 (+2year option) | |||||||||||

FSO Asia(5) | FSO | 442,000 | 2002 | Daewoo | Maersk Oil | Service Contract | July 2017 (+2year option) | |||||||||||

3

Table of Contents

| (1) | As used in this prospectus, “Samsung” refers to Samsung Heavy Industries Co., Ltd, “Hyundai” refers to Hyundai Heavy Industries Co., Ltd., “Universal” refers to Universal Shipbuilding Corporation, “Hitachi refers to Hitachi Zosen Corporation, “Daewoo” refers to Daewoo Shipbuilding and Marine Engineering S.A., “Ariake” refers to Japan Marine United Corp., Ariake Shipyard, Japan, “Dalian” refers to Dalian Shipbuilding Industry Co. Ltd., and “STX” refers to STX Offshore and Shipbuilding Co. Ltd. |

| (2) | Assumes no exercise by the charterer of any option to extend (if applicable). |

| (3) | In April 2014, a purchase option to buy theOlympia and theAntarctica was exercised. We expect to deliver theOlympia in September 2014 and theAntarctica in January 2015. Both vessels will remain employed under their current time charter contract until their respective delivery dates. |

| (4) | Profit sharing component under time charter contracts. |

| (5) | Vessels in which we hold a 50% ownership interest. |

| (6) | Expected to be delivered to us between November 2014 and March 2015. |

| (7) | Expected to operate in the TI Pool upon its delivery to us. |

| (8) | Vessel is chartered-in by us until its delivery to us. |

| (9) | Vessel is expected to be delivered to us during the third or fourth quarter of 2014. |

| (10) | Vessel is expected to be delivered to us during the second quarter of 2015. |

| (11) | Vessel is chartered-in on bareboat charter. The bareboat charter will be terminated upon delivery of the vessel to its new owner during the third or fourth quarter of 2014. |

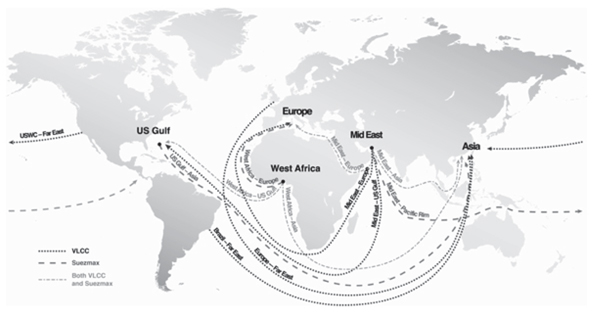

Employment of our Fleet

Our tanker fleet is employed worldwide through a combination of primarily spot market voyage fixtures, including through the TI Pool, fixed-rate contracts and time charters. We deploy our two FSOs as floating storage units under fixed-rate service contracts in the offshore services sector. For the year 2014, our fleet will have approximately 15,462 available days for hire, of which, as of August 18, 2014, 74% are expected to be available to be employed on the spot market, either directly or through the TI Pool, and 26% are expected to be on time charters, with or without a profit sharing element.

Spot Market

A spot market voyage charter is a contract to carry a specific cargo from a load port to a discharge port for an agreed freight per ton of cargo or a specified total amount. Under spot market voyage charters, we pay voyage expenses such as port, canal and bunker costs. Spot charter rates have historically been volatile and fluctuate due to seasonal changes, as well as general supply and demand dynamics in the crude oil marine transportation sector. Although the revenue we generate in the spot market is less predictable, we believe our exposure to this market provides us with the opportunity to capture better profit margins during periods when vessel demand exceeds supply, leading to improvements in tanker charter rates. As of August 18, 2014, we employed 19 of our vessels directly in the spot market.

A majority of our Suezmaxes operating in the spot market participate in an internal Revenue Sharing Agreement, or RSA, together with the four Suezmaxes that we jointly own with JM Maritime as well as Suezmaxes owned by third-parties. Under the RSA, each vessel owner is responsible for its own costs, including voyage-related expenses, but will share in the net revenues, after the deduction of voyage-related expenses, retroactively on a semi-annual basis. Calculation of allocations and contributions under the RSA are based on a pool points system and are paid after the deduction of the pool fee to Euronav, as pool manager, from the gross pool income. We believe this arrangement results in an increased market presence and allows us to benefit from additional market information which in turn is beneficial to our performance in the spot market.

Tankers International Pool

We principally employ and commercially manage our VLCCs through the TI Pool, a leading spot market-oriented VLCC pool in which other shipowners with vessels of similar size and quality participate along with us. We participated in the formation of the TI Pool in 2000 to allow us and other TI Pool participants, consisting of third-party owners and operators of similarly sized vessels, to gain economies of scale, obtain increased cargo flow of information, logistical efficiency and greater vessel utilization. As of August 18, 2014, the TI Pool was comprised of 36 vessels, including 25 of our VLCCs. We also expect to employ the remaining undelivered Maersk Acquisition Vessel and the four VLCC Acquisition Vessels in the TI Pool upon their delivery to us.

By pooling our VLCCs with those of other shipowners, we are able to derive synergies, including (i) the potential for increased vessel utilization by securing backhaul voyages for our vessels, and (ii) the performance of the Contracts of Affreightment, or COAs. Backhaul voyages involve the transportation of cargo on part of the return leg of a voyage. COAs, which can involve backhauls, may generate higher effective time charter equivalent, or TCE, revenues than otherwise might be obtainable directly in the spot market. Additionally, by operating a large number of vessels as an integrated transportation system, the TI Pool offers customers greater flexibility and an additional level of service while achieving scheduling efficiencies. The TI Pool is an owner-focused pool that does not charge commissions to its members, a practice that differs from that of other commercial pools; rather, the TI Pool aggregates gross charter revenues it receives and deducts voyage expenses and administrative costs before distributing net revenues to the pool members in accordance with their allocated pool points, which are based on each vessel’s speed, fuel consumption and cargo-carrying capacity. We believe this results in lower TI Pool membership costs, compared to other similarly sized pools. For example, in 2013, TI Pool membership costs were approximately $650 per vessel per day (with each vessel receiving its proportional share of pool membership expenses), while other similarly sized pools charged up to $1,300 per vessel per day (based on 1.25% of gross rates plus $300 per day).

4

Table of Contents

Tankers International LLC, or Tankers International, of which we own 40% of the outstanding interests, is the manager of the pool and is also responsible for the commercial management of the pool participants, including negotiating and entering into vessel employment agreements on behalf of the pool participants. Technical management of the pooled vessels is performed by each shipowner, who bears the operating costs for its vessels.

Time Charters

Time charters provide us with a fixed and stable cash flow for a known period of time. Time charters may help us mitigate, in part, our exposure to the spot market, which tends to be volatile in nature, being seasonal and generally weaker in the second and third quarters of the year due to refinery shutdowns and related maintenance during the warmer summer months. In the future, we may opportunistically employ more of our vessels under time charter contracts. We may also enter into time charter contracts with profit sharing arrangements, which we believe will enable us to benefit if the spot market increases above a base charter rate as calculated either by sharing sub charter profits of the charterer or by reference to a market index and in accordance with a formula provided in the applicable charter contract. As of August 18, 2014, we employed seven of our vessels on fixed-rate time charters, including five with profit sharing components.

FSOs and Offshore Service Contracts

We currently deploy our two FSOs as floating storage units under service contracts with Maersk Oil in the offshore services sector. As our tanker vessels age, we may seek to extend their useful lives by employing such vessels on long-term offshore projects at rates higher than may otherwise be achieved in the time charter market, or sell such vessels to third-party owners in the offshore conversion market at a premium.

Management of our Business

Technical and Commercial Management

Our vessels are technically managed in-house through our wholly-owned subsidiaries, Euronav Ship Management SAS, Euronav SAS and Euronav Ship Management (Hellas) Ltd. Our in-house technical management services include providing technical expertise necessary for all vessel operations, supervising the maintenance, upkeep and general efficiency of vessels, arranging and supervising newbuilding construction, drydocking, repairs and alterations, and developing, implementing, certifying and maintaining a safety management system.

Our VLCCs are commercially managed by Tankers International while operating in the TI Pool. All of the participants in the TI Pool collectively pay a pool management fee equivalent to the costs of running the pool business, after deducting voyage expenses, interest adjustments and administration costs, including legal, banking and other professional fees. The net charge is the pool administration cost, which is apportioned to each vessel by calendar days. During the year ended December 31, 2013, we paid an aggregate of $1.8 million for the commercial management of our vessels operating in the TI Pool.

Our Suezmax vessels trading in the spot market are commercially managed by Euronav (UK) Agencies Ltd., our London commercial department. Commercial management services include securing employment for our vessels.

Our time chartered vessels, both VLCCs and Suezmax vessels, are managed by our operations department based in Antwerp.

POSITIVE INDUSTRY FUNDAMENTALS

We believe that the following demand and supply factors create an attractive environment for us to successfully execute our business plan and to grow our business:

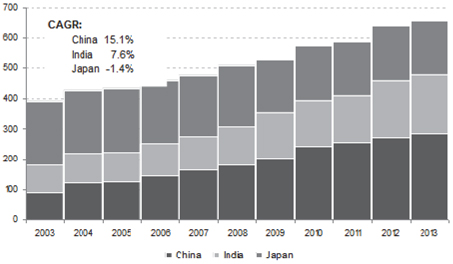

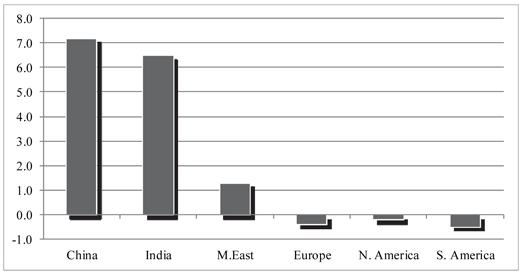

Increased global oil consumption is resulting in increased tanker ton mile demand. The demand for seaborne transportation of oil has historically been affected by worldwide economic growth, and, in turn, global oil demand. Increases in oil consumption, which in 2013 accounted for approximately one-third of global energy consumption, as well as a shift in global refinery capacity to the emerging markets, has resulted in growing oil trade distances and increasing tanker ton mile demand. In particular, seaborne crude oil imports have increased significantly in China and India to meet rising demand, with Chinese and Indian crude oil imports increasing by 212.1 million tons and 117.8 million tons, respectively, during the period from 2000 to 2013, according to Drewry. While there is no guarantee that past growth rates will continue, we believe this global demand for oil and attendant increase in ton miles over longer trade distances will support continued demand for tanker capacity.

5

Table of Contents

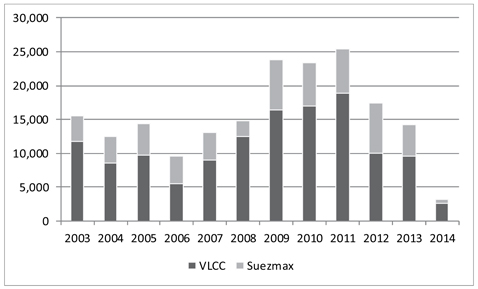

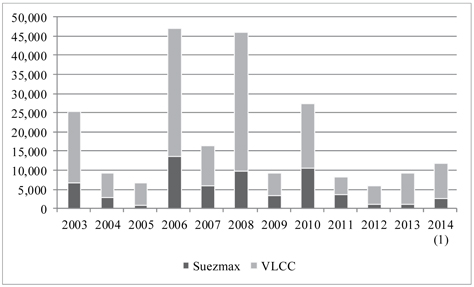

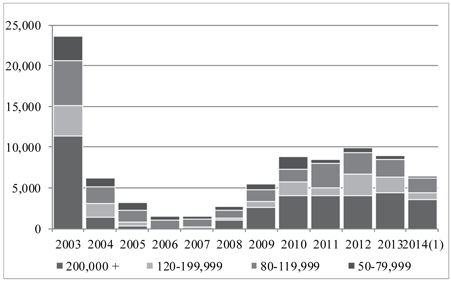

A limited orderbook should restrict the supply of new tankers. In general, the supply of tankers is influenced by the current orderbook for newbuilding vessels and the rate of removal of vessels from the worldwide fleet for scrapping or conversion as vessels age. Following a period of rapid expansion from 2007 through 2012, the worldwide tanker fleet grew by only 1.4% in 2013, according to Drewry, of which VLCCs and Suezmaxes grew by 2.0% and 1.4%, respectively, representing the lowest annual increase since 2007. Very few vessel orders were placed in both sectors during 2011, 2012 and 2013, although the pace of new ordering in the VLCC sector increased in the closing months of 2013 and the first half of 2014.

Favorable newbuilding and secondhand tanker prices encourage growth. In general, the demand and supply for tanker capacity influences charterhire rates and vessel values. In late 2013, rates generally started an upward trend in the crude tanker sector, primarily due to lower levels of fleet growth, coupled with increasing ton mile demand, which has led to an improving balance between vessel supply and demand. According to Drewry, the tanker sector remains one of the most fragmented in shipping with the worldwide VLCC fleet of 629 vessels being held by 132 different owners and the world Suezmax fleet of 494 vessels being held by 115 different owners. This is not only inefficient in terms of management and administration cost, but may offer numerous opportunities for further consolidation and may result in enhanced returns for the whole market.

COMPETITIVE STRENGTHS

We believe that our future opportunities in our industry are enhanced by the following competitive strengths of our business:

Large fleet of modern, well-maintained tankers. Following our purchase of the Maersk Acquisition Vessels and the VLCC Acquisition Vessels, we will be one of the largest independent owners and operators of modern crude oil tankers in the world, with a fleet of 55 tankers, comprised of 29 VLCCs, 23 Suezmax tankers, one ULCC and two FSOs, with a total capacity of 13.9 million dwt. Pro forma for these acquisitions, our fleet has a weighted average age of 6.8 years, making it one of the younger fleets worldwide as compared to the industry average of 9.8 years, according to Drewry. We believe that operating a large fleet of modern vessels, enhanced by the size of the TI Pool with 36 vessels under management as of August 18, 2014, provides us with competitive advantages relative to smaller competitors, including greater access to information and insight into market pricing, which, in turn, enables us to deploy our vessels to maximize our revenue and cash flow. We also believe that operating a fleet of modern well-maintained tankers reduces off-hire time for maintenance and operating and drydocking costs. The scale and quality of our fleet provides us with both operational synergies and negotiating leverage, giving us the flexibility to capitalize on opportunities throughout the cycles by changing the optimal mix of employment of our vessels as well as adjusting our fleet size.

A fully-integrated owner, operator and manager with a strong reputation within the chartering community. We provide all of our technical operations in-house, including the supervision of newbuilding construction and the maintenance of our vessels through a safety management system, which allows us to monitor more closely our operations. We believe this enables us to maximize revenues, reduce our costs and offer our customers a more stable quality of performance, reliability and service efficiency than if we contracted for these services with third-parties. In addition, by leveraging the expertise of our experienced staff, crew and captains, who have an average of 16 years of service with us, we have developed a reputation for safe, reliable and effective shipping and offshore storage of crude oil in the maritime sector, and we have outperformed industry benchmarks set by Intertanko, the organization of independent tanker owners, and the Oil Companies International Marine Forum (OCIMF) in its Tanker Management and Self Assessment guide (TMSA) for operating days, lack of lost time incidents and operating expenses. We believe that our reputation for quality, reliability and safety enables us to compete effectively for charters, particularly with international energy companies that have high standards. In recognition of our reputation in the shipping industry, we have been invited to join, and are an active member of important organizations, including, ITOPF (International Tanker Owners Pollution Federation), Intertanko, in particular in its Marine and Environmental Protection Committee, and the P&I Club system.

Strong and strategic relationships with well-known international energy companies. We have and are continuing to develop non-exclusive chartering relationships with well-known international energy companies, such as Chevron, Maersk Oil, Total and Valero. Many of these companies have repeatedly been served by our predecessor for more than 20 years, although there is no guarantee that these companies will continue their relationships with us. In past years, Valero has chartered up to ten of our vessels at one point in time, primarily in connection with its refinery along the St. Lawrence River in Quebec, which is located in an environmentally sensitive area with significant operational and navigational challenges. In addition, we have the ability to provide our customers in French jurisdictions with marine transportation of crude oil, which requires French-flagged vessels, local offices, and the employment of French seafarers, all of which can present barriers to entry to new entrants in the French market. As of August 18, 2014, we had four ships flying French flags under charter arrangements with Total and Petroineos. We expect to continue to capitalize on and potentially grow our long-term relationships with international energy companies and other customers, and believe that our reputation and proven track record for safe, reliable and efficient operations position us favorably to capture additional opportunities to meet our customers’ future chartering needs.

6

Table of Contents

Experienced management team. Our senior executive officers, Paddy Rodgers, our Chief Executive Officer, Hugo De Stoop, our Chief Financial Officer, Captain Alex Staring, our Chief Operating Officer, and Egied Verbeeck, our General Counsel, each have a high degree of professional education and considerable experience in the shipping industry. With over 75 years of combined shipping experience, our senior executive officers have led our development from 10 vessels with an aggregate carrying capacity of approximately 3.0 million dwt in 2000 to an independent fleet of crude oil tankers with 55 vessels (including two FSOs) with an aggregate carrying capacity of 13.9 million dwt, pro forma for the addition of the Maersk Acquisition Vessels and the VLCC Acquisition Vessels. Our senior management team has demonstrated its ability to optimize our fleet’s size through the recent cyclical downturn and successfully complete opportunistic vessel acquisitions on a timely basis and at favorable prices.

Demonstrated access to financing. We believe that we have developed relationships with leading international commercial banks and other financial institutions. Throughout our history, and particularly during recent global financial crises, we demonstrated our ability to access traditional bank financing as well as equity and debt capital markets to finance our business and complete vessel acquisitions. Since 2008, we have raised $3.4 billion, consisting of $2.3 billion in traditional bank financing, $510.0 million in bond issuances and $625.0 million in equity issuances. Our ability to access financing has allowed us to act swiftly and decisively in completing acquisitions, including our purchase of four Hellespont ULCCs in 2004 through a 50% joint venture with Overseas Shipholding Group, Inc., or OSG, for $448.0 million, the Metrostar fleet of four VLCCs in 2005 for $477.5 million, the Ceres Hellenic fleet of 16 vessels in 2005 for $1.1 billion, the 15 Maersk Acquisition Vessels in 2014 for $980.0 million and the four VLCC Acquisition Vessels in 2014 for $342.0 million. While there is no guarantee that we will be able to access similar financing in the future, we believe that our success in financing and implementing our strategy provides us with a solid base for the future.

Principal shareholders’ and directors’ longstanding relationships in the shipping industry. Both the Livanos and the Saverys families have been a continuous presence in the shipping industry since the early nineteenth century as owners of Ceres Hellenic, and of CMB and CNN, respectively. Peter Livanos is the Chairman of our Board of Directors through his appointment as permanent representative of TankLog. The Vice Chairman of our Board of Directors, Marc Saverys, is the Chief Executive Officer of CMB and controls Saverco, a company that is currently CMB’s majority shareholder. TankLog and Saverco currently own approximately 16.4% and 12.4%, respectively, of our existing outstanding ordinary shares. Upon completion of this offering, TankLog and Saverco will own approximately % and %, respectively, of our outstanding ordinary shares.

OUR BUSINESS STRATEGIES

Our primary objectives are to manage the size of our fleet according to market circumstances and to maximize shareholder value. The key elements of our strategy are:

Selectively buy and sell vessels in our fleet in order to maintain high quality vessels at attractive prices. We believe that our recent purchase of the Maersk Acquisition Vessels and the VLCC Acquisition Vessels represented an attractive investment opportunity to grow our revenue and earnings at a favorable price. With respect to the 15 modern Maersk Acquisition Vessels, we paid $65.3 million on average per VLCC, and with respect to the four modern VLCC Acquisition Vessels, we paid $85.5 million on average per VLCC, as compared to the current price of newbuilding VLCCs of approximately $99.0 million per VLCC, according to Drewry. In addition, we believe that the Maersk Acquisition Vessels will enable us to capitalize on potential near-term improvements in tanker market charter rates, instead of having to wait several years to receive newbuilding vessels from shipyards. We also recently sold three VLCCs (Luxembourg, Antarctica and Olympia) for offshore conversion projects at what we believe are attractive prices compared to the sale prices of other similar vessels. When evaluating future transactions, we will consider and analyze, among other things, our charter rate expectations for the tanker sector, current vessel prices achieved in the sale and purchase market for vessels, the expected cash flow for vessels relative to the proposed price, vessel specifications, including modern, environmentally safe features, and any related charter employment. While there is no guarantee that we will be able to acquire and dispose of vessels according to this strategy in the future, we believe that our disciplined acquisition approach, combined with our management’s knowledge of the tanker sector, will provide us with opportunities to manage the size of our fleet and generate returns for our shareholders.

Optimize our exposure to the spot market to maximize revenues. We actively manage the employment of our operating fleet between spot market voyages and time charters. Our strategy is to maximize our exposure to the spot market, which has historically been volatile, but which we believe has delivered the highest returns on average, while securing stable cash flow in anticipation of decreasing markets by chartering some of our vessels on fixed-rate time charters or, in the case of our two FSOs, in the offshore storage sector on fixed-rate service contracts. As part of our focus on the spot market, we seek to leverage our participation in the TI Pool to benefit from the economies of scale and greater vessel utilization that the TI Pool can generate. We believe that the revenues that our vessels achieve in the TI Pool will exceed the rate we would otherwise achieve by operating these vessels outside of the TI Pool.

7

Table of Contents

Leverage our people and utilize our high quality assets to continue to capitalize on floating crude oil storage opportunities. We believe that we can increase shareholder value by opportunistically employing some of our vessels as crude oil storage units. We may look to deploy some of our vessels in the offshore market on long-term contracts for floating storage projects at rates higher than may otherwise be achieved in the tanker time charter market. We may also sell our vessels for conversion to third-party owners active in the offshore market at prices exceeding levels that could be realized in the conventional ship sale and purchase market. We currently operate two FSOs in which we own a 50% interest on long-term service contracts with Maersk Oil. Over the last several years, we have sold five of our ships into the offshore conversion market at a premium above prices achievable in the broader ship sale and purchase market. We believe that our presence in the offshore market, coupled with the growing trend toward offshore exploration and development projects globally, will lead to additional growth opportunities in the future.

Maintain a strong balance sheet with access to capital. We seek to optimize and constantly monitor our leverage while adapting it to changing market conditions. We plan to finance our business and future vessel acquisitions with a mix of debt and equity from commercial banks and from the capital markets. We believe that maintaining a strong balance sheet will enable us to access more favorable chartering opportunities as end users have increasingly favored well-capitalized owners, as well as give us a competitive advantage in pursuing vessel acquisitions.

Maintain cost efficient in-house vessel operations and corporate expenses. Through our in-house vessel operations, we believe that we are better able to monitor our operations, enabling us to maximize revenues and reduce our costs while offering our customers the quality of performances, services and reliability they demand, compared to other vessel owners and operators who outsource these functions. We have a track record of safe operations and outperform the industry benchmarks set by Intertanko, the organization of independent tanker vessels, and the OCIMF in its TMSA for operating days, lack of lost time incidents, and operating expenses, all of which ensures that maximum value can be delivered while minimizing human and environmental risks.

RECENT AND OTHER DEVELOPMENTS

Vessel Acquisitions and Dispositions

During the period from February 2014 through the date of this prospectus, we took delivery of 14 of the Maersk Acquisition Vessels,Nautilus,Nucleus,Navarin,Newton,Sara,Ilma, Nautic,Ingrid, Noble, Nectar, Simone, Neptun, Sonia,andIris,and we expect to take delivery of the remaining Maersk Acquisition Vessel between November 2014 and March 2015.

In April 2014, our counterparty exercised a purchase option to buy theOlympia and theAntarctica from us for an aggregate purchase price of $178.0 million, less a $20.0 million option fee that we received in January 2011. We expect to deliver theOlympia in September 2014 and theAntarctica in January 2015. Both vessels will remain employed under their current time charter contracts until their respective delivery dates. The sales resulted in a combined loss of $7.4 million which was recorded in the second quarter of 2014.

On July 7, 2014, we agreed to acquire an additional four modern VLCCs (three of which we currently charter in), charter-free, from Maersk Tankers for an aggregate purchase price of $342.0 million. Three of the vessels are expected to be delivered to us during the third and fourth quarter of 2014, with the remaining vessel expected to be delivered to us in the second quarter of 2015. The purchase price of the VLCC Acquisition Vessels will be financed using the net proceeds of $121.0 million that we received in an underwritten private offering of 10,556,808 of our ordinary shares in Belgium in July 2014 (see below), available cash on hand, and borrowings under new secured credit facilities, including $205.2 million that we expect to draw down under our Proposed $340.0 Million Credit Facility for which we received a non-binding term sheet on August 13, 2014. Please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations-Liquidity and Capital Resources” for a description of the expected terms of our Proposed $340.0 Million Credit Facility.

On July 31, 2014, theCap Isabella, a vessel that is on bareboat charter to us, was sold by its owner, Belle Shipholdings Ltd., or Belle Shipholdings to a third-party. The stock of Belle Shipholdings is held for the benefit of immediate family members of Peter Livanos, who serves as the Chairman of our Board of Directors through his appointment as permanent representative of TankLog. In the beginning of 2013, we sold theCap Isabella to Belle Shipholdings through a sale and lease back agreement, pursuant to which we are entitled to receive a share of the profit resulting from the sale of the vessel by Belle. As a result, we expect to receive approximately $4.3 million that will be recorded in the third or fourth quarter of 2014. The bareboat charter will be terminated upon delivery of the vessel to its new owner during the third or fourth quarter of 2014. Please see “Certain Relationships and Related Party Transactions.”

Private Offering of Ordinary Shares in Belgium

On July 14, 2014, we received gross proceeds of $125.0 million upon the issuance of 10,556,808 of our ordinary shares in an underwritten private offering in Belgium mainly to a group of qualified investors at €8.70 per share (or $11.84 per share based on the USD/EUR exchange rate of EUR 1.00 per $1.3610). The proceeds of the offering are expected to be used to partially finance the purchase price of the four VLCC Acquisition Vessels.

Appointment of New Chairman

At a meeting of our Board of Directors held on July 22, 2014, our Board of Directors resolved to appoint TankLog, with Peter Livanos serving as permanent representative on its behalf, as the Chairman of our Board, and Marc Saverys, our former Chairman of the Board, as Vice Chairman, each with immediate effect.

Exchange Offer

Concurrently with the pricing of this offering, we will offer to exchange all of the outstanding unregistered ordinary shares in Belgium (other than ordinary shares owned by our affiliates) for ordinary shares that have been registered under the Securities Act, which we refer to as the Exchange Offer. The Exchange Offer will be made only by means of a prospectus contained in our registration statement on Form F-4 that we will file in connection with that Exchange Offer and a related letter of transmittal. This offering is not contingent on the successful completion of the Exchange Offer. See “Business – Exchange Offer.”

RISK FACTORS

You should carefully consider the risks described in “Risk Factors” and the other information in this prospectus before deciding whether to invest in our ordinary shares.

8

Table of Contents

IMPLICATIONS OF BEING AN EMERGING GROWTH COMPANY

While we were incorporated in 2003, we had less than $1.0 billion in revenue during our last fiscal year, which means that we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act, or JOBS Act. An emerging growth company may take advantage of specified reduced reporting requirements that are otherwise applicable generally to public companies. These provisions include:

| • | the ability to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in the registration statement for our initial public offering; and |

| • | exemption from the auditor attestation requirement of management’s assessment of the effectiveness of the emerging growth company’s internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002, or Sarbanes-Oxley. |

We may take advantage of these provisions until the end of the fiscal year following the fifth anniversary of our initial public offering or such earlier time that we are no longer an emerging growth company. We will cease to be an emerging growth company if we have more than $1.0 billion in “total annual gross revenues” during our most recently completed fiscal year, if we become a “large accelerated filer” with market capitalization of more than $700 million, or as of any date on which we have issued more than $1.0 billion in non-convertible debt over the three year period prior to such date. We may choose to take advantage of some, but not all, of these reduced reporting requirements. For as long as we take advantage of the reduced reporting obligations, the information that we provide shareholders may be different from information provided by other public companies.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We currently prepare our consolidated financial statements in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, which do not have separate provisions for publicly traded and private companies. However, in the event we convert to U.S. GAAP while we are still an emerging growth company, we may be able to take advantage of the benefits of this extended transition period and, as a result, during such time that we delay the adoption of any new or revised accounting standards, our consolidated financial statements may not be comparable to other companies that comply with all public company accounting standards.

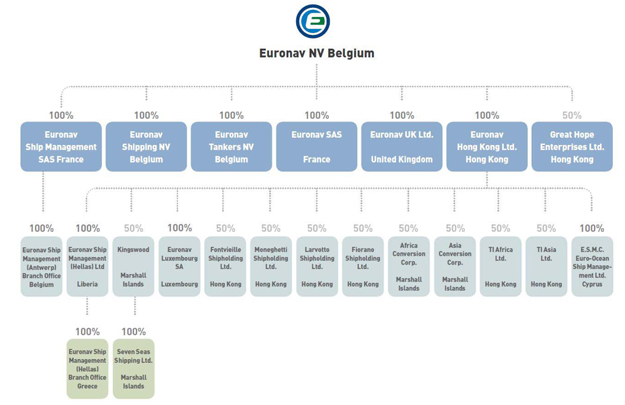

CORPORATE STRUCTURE

We were incorporated under the laws of Belgium on June 26, 2003, and we grew out of the combination of certain tanker activities carried out by three companies that had a strong presence in the shipping industry: CMB, formed in 1895, CNN, formed in 1938, and Ceres Hellenic, formed in 1950. Our predecessor started doing business under the name “Euronav” in 1989.

Our principal shareholders are TankLog (controlled by the Livanos family) and Saverco (controlled by Marc Saverys). Both the Livanos and the Saverys families have been a continuous presence in the shipping industry since the early nineteenth century as owners of Ceres Hellenic, and of CMB and CNN, respectively. Peter Livanos serves as the Chairman of our Board of Directors through his appointment as permanent representative of TankLog. The Vice Chairman of our Board of Directors, Marc Saverys, is the Chief Executive Officer of CMB and controls Saverco, a company that is currently CMB’s majority shareholder. TankLog and Saverco currently own approximately 16.4% and 12.4%, respectively, of our existing outstanding ordinary shares. Upon completion of this offering, TankLog and Saverco will own approximately % and %, respectively, of our outstanding ordinary shares.

We own our vessels either directly at the parent level, indirectly through our wholly-owned vessel owning subsidiaries, or jointly through our 50%-owned subsidiaries. We conduct our vessel operations through our wholly-owned subsidiaries Euronav Ship Management SAS, Euronav SAS and Euronav Ship Management (Hellas) Ltd., and also through the TI Pool. Our subsidiaries are incorporated under the laws of Belgium, France, United Kingdom, Liberia, Luxembourg, Cyprus, Hong Kong and the Marshall Islands. Our vessels are flagged in Belgium, the Marshall Islands, France, Panama and Greece.

9

Table of Contents

The diagram below depicts our organizational structure, including the ownership of our direct and indirect management entities and vessel-owning subsidiaries, as of August 18, 2014. The diagram does not reflect ownership of the Company by our principal or other shareholders.

PRINCIPAL EXECUTIVE OFFICES

Our principal executive headquarters are located at De Gerlachekaai 20, 2000 Antwerpen, Belgium. Our telephone number at that address is 011-32-3-247-4411. We also have offices located in the United Kingdom, France, Greece and Hong Kong. Our website is www.euronav.com. The information contained on our website is not a part of this prospectus.

OTHER INFORMATION

Because we are incorporated under the laws of Belgium and substantially all of our assets are located outside of the United States, you may encounter difficulty protecting your interests as shareholders, and your ability to protect your rights through the U.S. federal court system may be limited. Please refer to the sections entitled “Risk Factors” and “Enforcement of Civil Liabilities” for more information.

10

Table of Contents

Issuer | Euronav NV, a company incorporated under the laws of Belgium. | |

Ordinary Shares offered to the public by us | ordinary shares ( ordinary shares, if the underwriters exercise their over-allotment option to purchase additional shares in full). | |

Ordinary Shares offered to the public by the selling shareholders | ordinary shares ( ordinary shares, if the underwriters exercise their over-allotment option to purchase additional shares in full). | |

Ordinary Shares outstanding immediately after the offering1 | ordinary shares ( ordinary shares, if the underwriters exercise their over-allotment option to purchase additional shares in full). | |

Use of proceeds | We estimate that we will receive net proceeds of approximately $ million from this offering ($ million if the underwriters’ option to purchase additional shares is exercised in full), after deducting underwriting discounts and commissions and estimated expenses payable by us. These estimates are based on an assumed initial public offering price of $ per share (the closing price of our existing ordinary shares on the NYSE Euronext Brussels on , 2014, based on the Bloomberg Composite Rate of € per $1.00 in effect on that date.

We intend to use the net proceeds of this offering for general corporate purposes and working capital, which may include the acquisition of additional new or secondhand vessels or the repayment of indebtedness.

In addition, the selling shareholders will receive $ million in net proceeds from the sale of ordinary shares offered by this prospectus to the public ($ million if the underwriters’ over-allotment option to purchase additional shares is exercised in full) (in each case, based on the assumed initial public offering price of $ per share). We will not receive any of the proceeds from the sale of these ordinary shares.

Please read “Use of Proceeds.” | |

Dividend policy | Our Board of Directors may, subject to the approval of our shareholders, as the case may be, from time to time, declare and pay cash dividends in accordance with our Articles of Association and applicable Belgian law. Our Board of Directors has not declared or paid a dividend since 2010, but will continue to assess the declaration and payment of dividends upon consideration of our financial results and earnings, restrictions in our debt agreements, market prospects, current capital expenditures, commitments, investment opportunities and the provisions of Belgian law affecting the payment of dividends to shareholders and other factors. During the 120 day period commencing on the date immediately following the pricing of the offering, or the “Transition Period,” the ordinary shares offered hereby and the existing ordinary shares issued in Belgium which are currently trading on the NYSE Euronext Brussels will have different dividend rights. If a dividend is declared during the Transition Period, holders of ordinary shares offered hereby would be entitled to receive dividends based only upon the earnings from our operations from and after the date of | |

11

Table of Contents

| issuance, while holders of existing ordinary shares would be entitled to receive dividends based upon our earnings for all prior periods. Upon the completion of the Transition Period, (i) the ordinary shares offered hereby will immediately have the same dividend rights as the existing ordinary shares and (ii) the ordinary shares and the existing shares will have the same rights and privileges in all respects. We cannot assure you that we will pay any dividends. Please see “Dividend Policy” and “Description of Share Capital.” | ||

U.S. Exchange listing | We intend to apply to have our ordinary shares listed for trading on the NYSE under the symbol “EURN.” | |

Transfer agent | Computershare Trust Company, N.A. | |

Tax Considerations | See “Tax Considerations” for a full discussion of the tax treatment of the Company and holders of our ordinary shares. | |

Risk factors | Investment in our ordinary shares involves a high degree of risk. You should carefully read and consider all of the information set forth under the heading “Risk Factors” and all other information set forth in this prospectus before investing in our ordinary shares. | |

| (1) | Includes 12,297,071 ordinary shares (consisting of 9,459,286 ordinary shares relating to the contribution of the principal amount and, at our option, up to 2,837,785 ordinary shares relating to the payment of interest in shares over five years) that we will issue at the closing of this offering if we exercise our option to force a conversion of our outstanding perpetual convertible preferred equity securities and excludes 1,147,621 ordinary shares issuable upon conversion of our outstanding convertible bonds due 2015. |

12

Table of Contents

SUMMARY FINANCIAL AND OPERATING DATA

The following table presents, in each case for the periods and as of the dates indicated, historical summary consolidated financial and other data. The summary consolidated statement of profit or loss data and summary cash flow data for the years ended December 31, 2013, 2012 and 2011 and the summary consolidated statement of financial position data for the years ended December 31, 2013 and 2012 have been derived from the audited consolidated financial statements, and the notes thereto, included in this prospectus. The summary consolidated statement of profit or loss data and summary cash flow data for the six months ended June 30, 2014 and 2013 and the summary consolidated statement of financial position data as of June 30, 2014 have been derived from the unaudited condensed consolidated interim financial statements, and the notes thereto, included in this prospectus. The financial statements included herein have been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB), and are in U.S. dollars. The following financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the consolidated financial statements and related notes, and other financial information appearing elsewhere in this prospectus.

Consolidated Statement of Profit or Loss Data

(US$ in thousands, except per share data)

| Six Months Ended June 30, | Year Ended December 31, | |||||||||||||||||||

| 2014 | 2013 | 2013 | 2012 | 2011 | ||||||||||||||||

Revenue | 201,157 | 153,818 | 304,622 | 320,836 | 326,315 | |||||||||||||||

Gains on disposal of vessels/other tangible assets | 6,390 | 0 | 8 | 10,067 | 22,153 | |||||||||||||||

Other operating income | 3,534 | 2,702 | 11,520 | 10,478 | 5,773 | |||||||||||||||

Expenses for shipping activities | (117,851 | ) | (99,228 | ) | (206,528 | ) | (210,558 | ) | (212,459 | ) | ||||||||||

Losses on disposal of vessels | (1 | ) | (215 | ) | (215 | ) | (32,080 | ) | (25,501 | ) | ||||||||||

Impairment on non-current assets held for sale | (7,415 | ) | — | — | — | — | ||||||||||||||

Depreciation tangible assets | (67,674 | ) | (67,880 | ) | (136,882 | ) | (146,881 | ) | (142,358 | ) | ||||||||||

Depreciation intangible assets | (10 | ) | (63 | ) | (75 | ) | (181 | ) | (213 | ) | ||||||||||

Employee benefits | (9,653 | ) | (6,505 | ) | (13,881 | ) | (15,733 | ) | (15,581 | ) | ||||||||||

Other operating expenses | (7,569 | ) | (5,832 | ) | (13,283 | ) | (15,065 | ) | (13,074 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Result from operating activities | (908 | ) | (23,203 | ) | (54,714 | ) | (79,117 | ) | (54,945 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Finance income | 623 | 720 | 1,993 | 5,349 | 5,663 | |||||||||||||||

Finance expenses | (37,138 | ) | (26,302 | ) | (54,637 | ) | (55,507 | ) | (52,484 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net finance expense | (36,515 | ) | (25,582 | ) | (52,644 | ) | (50,158 | ) | (46,821 | ) | ||||||||||

Share of profit (loss) of equity accounted investees (net of income tax) | 14,393 | 9,584 | 17,853 | 9,953 | 5,897 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Profit (loss) before income tax | (21,214 | ) | (39,201 | ) | (89,505 | ) | (119,322 | ) | (95,869 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Income tax expense | (38 | ) | (72 | ) | (178 | ) | 726 | (118 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Profit (loss) for the period | (21,252 | ) | (39,273 | ) | (89,683 | ) | (118,596 | ) | (95,987 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Attributable to: | ||||||||||||||||||||

Owners of the Company | (21,252 | ) | (39,273 | ) | (89,683 | ) | (118,596 | ) | (95,987 | ) | ||||||||||

Non-controlling interest | — | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Basic earnings per share | (0.20 | ) | (0.79 | ) | (1.79 | ) | (2.37 | ) | (1.92 | ) | ||||||||||

Diluted earnings per share | (0.20 | ) | (0.79 | ) | (1.79 | ) | (2.37 | ) | (1.92 | ) | ||||||||||

13

Table of Contents

Consolidated Statement of Financial Position Data (at period end)

(US$ in thousands, except for per share and fleet data)

| Six Months Ended June 30, | Year Ended December 31, | |||||||||||||||||||

| 2014 | 2013 | 2013 | 2012 | 2011 | ||||||||||||||||

Cash and cash equivalents | 274,487 | 74,309 | 113,051 | 163,108 | ||||||||||||||||

Vessels | 1,683,472 | 1,434,800 | 1,592,837 | 1,616,178 | ||||||||||||||||

Vessels under construction | — | — | — | 89,619 | ||||||||||||||||

Current and non-current bank loans | 874,337 | 847,763 | 911,474 | 938,992 | ||||||||||||||||

Equity attributable to Owners of the Company | 1,374,321 | 800,990 | 866,970 | 980,988 | ||||||||||||||||

Cash flow data | ||||||||||||||||||||

Net cash inflow/(outflow) | ||||||||||||||||||||

Operating activities | 1,378 | (31,736 | ) | (8,917 | ) | 69,812 | 28,060 | |||||||||||||

Investing activities | (512,476 | ) | 46,485 | 28,114 | (86,986 | ) | 39,852 | |||||||||||||

Financing activities | 711,578 | (25,311 | ) | (57,384 | ) | (33,117 | ) | (48,606 | ) | |||||||||||

Fleet Data (Unaudited) | ||||||||||||||||||||

VLCCs | ||||||||||||||||||||

Average number of vessels(1) | 14 | 11 | 11 | 13 | 14 | |||||||||||||||

Calendar days(2) | 2,540 | 2,027 | 4,085 | 4,940 | 5,264 | |||||||||||||||

Vessel operating days(3) | 2,477 | 1,996 | 4,036 | 4,891 | 5,119 | |||||||||||||||

Available days(4) | 2,489 | 1,999 | 4,044 | 4,910 | 5,198 | |||||||||||||||

Fleet utilization(5) | 100 | % | 100 | % | 100 | % | 99.6 | % | 98.5 | % | ||||||||||

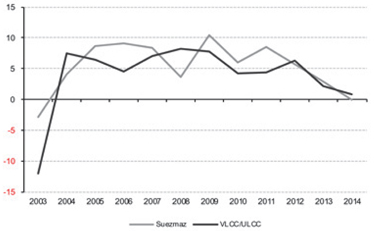

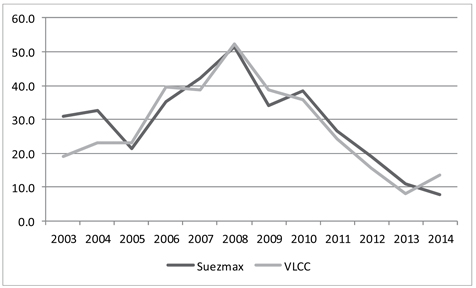

Daily TCE charter rates(6) | $ | 26,868 | 24,189 | $ | 25,788 | $ | 23,510 | $ | 24,455 | |||||||||||

Daily vessel operating expenses(7) | $ | 8,726 | 7,778 | $ | 8,178 | $ | 7,761 | $ | 7,440 | |||||||||||

Suezmaxes | ||||||||||||||||||||

Average number of vessels(1) | 19 | 19 | 19 | 18 | 18 | |||||||||||||||

Calendar days(2) | 3,439 | 3,353 | 6,848 | 6,588 | 6,570 | |||||||||||||||

Vessel operating days(3) | 3,422 | 3,273 | 6,661 | 6,436 | 6,448 | |||||||||||||||

Available days(4) | 3,430 | 3,275 | 6,664 | 6,489 | 6,456 | |||||||||||||||

Fleet utilization(5) | 100 | % | 100 | % | 100 | % | 99.2 | % | 99.9 | % | ||||||||||

Daily TCE charter rates(6) | $ | 24,305 | 19,147 | $ | 19,283 | $ | 21,052 | $ | 24,235 | |||||||||||

Daily vessel operating expenses(7) | $ | 8,241 | 7,579 | $ | 7,753 | $ | 7,868 | $ | 8,442 | |||||||||||

Average daily general and administrative expenses per vessel – owned tanker segment only(8) | 2,880 | 2,293 | $ | 2,485 | $ | 2,672 | $ | 2,420 | ||||||||||||

Other data | ||||||||||||||||||||

EBITDA (unaudited) (9) | 82,985 | 54,324 | $ | 100,096 | $ | 77,898 | $ | 93,523 | ||||||||||||

Adjusted EBITDA (unaudited) (9) | 101,459 | 73,145 | $ | 138,853 | $ | 120,719 | $ | 128,367 | ||||||||||||

Time charter equivalents revenues | 149,728 | 110,955 | $ | 232,519 | $ | 250,476 | $ | 281,476 | ||||||||||||

Basic weighted average shares outstanding | 104,324,074 | 50,000,000 | 50,230,438 | 50,000,000 | 50,000,000 | |||||||||||||||

Diluted weighted average shares outstanding | 104,324,074 | 50,000,000 | 50,230,438 | 50,000,000 | 50,000,000 | |||||||||||||||

| (1) | Average number of vessels is the number of vessels that constituted our fleet for the relevant period, as measured by the sum of the number of days each vessel was part of our fleet during the period divided by the number of calendar days in that period. |

| (2) | Calendar days are the total days the vessels were in our possession for the relevant period, including off-hire days associated with major repairs, drydockings or special or intermediate surveys. |

| (3) | Vessel operating days are the total days our vessels were in our possession for the relevant period net of all off-hire days (scheduled and unscheduled), including off-hire days, associated with major repairs, drydockings or special or intermediate surveys. |

| (4) | Available days are the total days our vessels were in our possession for the relevant period net of scheduled off-hire days associated with major repairs, drydockings or special or intermediate surveys. |

| (5) | Fleet utilization is the percentage of time that our vessels were available for revenue generating voyage days and is determined by dividing Vessel operating days by available days for the relevant period. The shipping industry uses fleet utilization to measure a company’s efficiency in finding suitable employment for its vessels and minimizing the number of days that its vessels are off-hire for reasons other than scheduled repairs or repairs under guarantee, vessel upgrades, special surveys or intermediate or vessel positioning. |

| (6) | Time Charter Equivalent, or TCE, is a measure of the average daily revenue performance of a vessel on a per voyage basis. Our method of calculating the TCE rate is consistent with industry standards and is determined by dividing total voyage revenues less voyage expenses by vessel operating days for the relevant time period. The period over which voyage revenues are recognized commences at the time the vessel leaves the port at which she discharged her cargo related to her previous |

14

Table of Contents

| voyage (or as the case may be when a vessel is leaving a yard at which she went to drydock or in the case of a newbuilding or a newly acquired vessel as from the moment the vessel is available to take a cargo. The period ends at the time that discharge of cargo is completed. Net voyage revenues are voyage revenues minus voyage expenses. Voyage expenses primarily consist of port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid by the charterer under a time charter contract. We may incur voyage related expenses when positioning or repositioning vessels before or after the period of a time charter, during periods of commercial waiting time or while off-hire during dry-docking or due to other unforeseen circumstances. |

The TCE rate is not a measure of financial performance under IFRS (non-IFRS measure), and should not be considered as an alternative to voyage revenues, the most directly comparable IFRS measure, or any other measure of financial performance presented in accordance with IFRS. However, TCE rate is standard shipping industry performance measure used primarily to compare period-to-period changes in a company’s performance and assists our management in making decisions regarding the deployment and use of our vessels and in evaluating their financial performance. Our calculation of TCE rates may not be comparable to that reported by other companies. The following table reflects the calculation of our TCE rates for the six months ended June 30, 2014 and 2013 and the years ended December 31, 2013, 2012 and 2011:

| Six Months Ended June 30, | Year Ended December 31, | |||||||||||||||||||

| 2014 | 2013 | 2013 | 2012 | 2011 | ||||||||||||||||

VLCC | ||||||||||||||||||||

Net VLCC revenues for all employment types | $ | 66,560,116 | $ | 48,287,795 | $ | 104,068,875 | $ | 114,987,548 | $ | 125,195,000 | ||||||||||

Total VLCC operating days | 2,477 | 1,996 | 4,036 | 4,891 | 5,119 | |||||||||||||||

Daily VLCC TCE Rate | $ | 26,868 | $ | 24,189 | $ | 25,788 | $ | 23,510 | $ | 24,557 | ||||||||||

SUEZMAX | ||||||||||||||||||||

Net Suezmax revenues for all employment types | $ | 83,167,458 | $ | 62,666,847 | $ | 128,449,941 | $ | 135,488,742 | $ | 156,280,502 | ||||||||||

Total Suezmax operating days | 3,422 | 3,273 | 6,661 | 6,436 | 6,448 | |||||||||||||||