The Board of Directors of VinHMS Pte. Ltd. present this report together with audited financial statements for the period from 01 November 2023 (Incorporation date) to 31 December 2023.

Board of Directors

The directors in office at the date of this statement are:

Mr. Nguyen Van Hoang

Mr. Koh Hsien Loong, Mark Greory

SUBSEQUENT EVENTS

According to Board of Directors, in all material respects, there have been no other significant events occurring after the balance sheet date affecting the financial position and operation of the Company which would require adjustments to or disclosures to be made in the financial statements for the period from 01 November 2023 (Incorporation date) to 31 December 2023.

AUDITOR

The accompanying financial statements for the period from 01 November 2023 (Incorporation date) to 31 December 2023 have been audited by Parker Russell Vietnam Company Limited (Parker Russell Vietnam).

BOARD OF DIRECTORS’ STATEMENT OF RESPONSIBILITY

Board of Directors of the Company are responsible for preparing the financial statements of each year, which give a true and fair view of the financial position of the Company and of its results and cash flows for the period.

In preparing those financial statements, Board of Directors are required to:

·

Select suitable accounting policies and then apply them consistently;

·

Make judgments and estimates that are reasonable and prudent;

·

State whether applicable accounting principles have been complied with, material differences are disclosed and explained in the financial statements;

·

Design, execute and maintain an effective internal control related to the appropriate preparation and presentation of financial statements so as to obtain reasonable assurance that the financial statements are free of material misstatements caused by even frauds and errors; and

·

Prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company will continue in business.

BOARD OF DIRECTORS’ STATEMENT OF RESPONSIBILITY (CONTINUED)

Board of Directors confirm that the Company has complied with the above requirements in preparing these financial statements.

Board of Directors are responsible for ensuring that proper accounting records are kept, which disclose, with reasonable accuracy at any time, the financial position of the Company and to ensure that the financial statements comply with International Financial Reporting Standards. It is also responsible for safeguarding the assets of the Company and hence for taking reasonable steps for the prevention and detection of frauds and other irregularities.

We have audited the accompanying financial statements of VinHMS Pte. Ltd., prepared on 10 May 2024 as set out from page 5 to page 18, which comprise Statement of financial position as at 31 December 2023, Statement of profit and loss, Statement of changes in equity and Statement of cash flows for the period from 01 November 2023 (Incorporation date) to, and a summary of significant accounting policies and other explanatory information.

In our opinion, the accompanying financial statements give a true and fair view of, in all material respects, the financial position of the Company as at 31 December 2023 and the results of its operations and its cash flows for the period from 01 November 2023 (Incorporation date) to 31 December 2023, in accordance with International Financial Reporting Standards.

Basis for Opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company and have fulfilled our other responsibilities under those relevant ethical requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Going Concern

The Company’s financial statements have been prepared using the going concern basis of accounting. The use of this basis of accounting is appropriate unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so. As part of our audit of the financial statements, we have concluded that management’s use of the going concern basis of accounting in the preparation of the Company’s financial statements is appropriate. Management has not identified a material uncertainty that may cast significant doubt on the entity’s ability to continue as a going concern, and accordingly none is disclosed in the financial statements. Based on our audit of the financial statements, we also have not identified such a material uncertainty. However, neither management nor the auditor can guarantee the Company’s ability to continue as a going concern.

Responsibilities of Management for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with IFRSs and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Management are responsible for overseeing the Company’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

The objectives of our audit are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the planning and performance of the audit. We also:

·

Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

·

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control.

·

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

·

Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We are required to communicate with management regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit. We are also required to provide management with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

/s/ Nguyen Song Toan

Nguyen Song Toan

Partner

Audit Practising Registration Certificate

No. 1551-2023-238-1

For and on behalf of

Parker Russell Vietnam Company Limited (Parker Russell Vietnam)

For the period from 01 November 2023 (Incorporation date) to 31 December 2023

Owners'

contributed

capital

Retained

earnings

Total

SGD

SGD

SGD

Current year’s opening balance

-

-

-

Unpaid capital

13,676

-

13,676

Loss for the period

-

(2,897

)

(2,897

)

Current year’s closing balance

13,676

(2,897

)

10,779

Charter capital

According to the Company’s Enterprise Registration Certificate, the Company’s charter capital is USD 10,000. The charter capital has not been fully contributed by the shareholders as at 31 December 2023. In February 2024, the charter capital was contributed by the shareholders.

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

1. GENERAL INFORMATION

1.1. Structure of ownership

VinHMS Pte. Ltd. (“the Company”) is incorporated in Singapore, as a private company limited under the Enterprise Registration Certificate No. dated 01 November 2023. The charter capital of the Company is USD 10,000.

The Company’s office is located at 8 Burn Road, #05-02, Trivex, Singapore (369977).

1.2. Principal activities

The principal activity of the Company is publishing of software/applications (Non-games) (58202)

1.3. Financial year

The Company’s financial year begins on 01 January and ends on 31 December.

2. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs)

New and amended IFRSs that are effective for the current year

Amendments to IAS 1 Presentation of Financial Statements and IFRS Practice Statement 2 Making Materiality Judgements – Disclosure of Accounting Policies

The Company has adopted the amendments to IAS 1 for the first time in the current year. The amendments change the requirements in IAS 1 with regard to disclosure of accounting policies. The amendments replace all instances of the term ‘’significant accounting policies” with “material accounting policy information’’. Accounting policy information is material if, when considered together with other information included in an entity’s financial statements, it can reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements.

The supporting paragraphs in IAS 1 are also amended to clarify that accounting policy information that relates to immaterial transactions, other events or conditions is immaterial and need not be disclosed. Accounting policy information may be material because of the nature of the related transactions, other events or conditions, even if the amounts are immaterial. However, not all accounting policy information relating to material transactions, other events or conditions is itself material.

Amendments to IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors – Definition of Accounting Estimates

The Company has adopted the amendments to IAS 8 for the first time in the current year. The amendments replace the definition of accounting estimates. Under the new definition, accounting estimates are “monetary amounts in financial statements that are subject to measurement uncertainty”. The definition of a change in accounting estimates was deleted.

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

2. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs) (CONTINUED)

New and revised IFRSs in issue but not yet effective

Amendments to IAS 1 Classification of Liabilities as Current or Non-Current

The amendments to IAS 1 affect only the presentation of liabilities as current or non-current in the statement of financial position and not the amount or timing of recognition of any asset, liability, income or expenses, or the information disclosed about those items.

The amendments clarify that the classification of liabilities as current or non-current is based on rights that are in existence at the end of the reporting period, specify that classification is unaffected by expectations about whether an entity will exercise its right to defer settlement of a liability, explain that rights are in existence if covenants are complied with at the end of the reporting period, and introduce a definition of

‘settlement’ to make clear that settlement refers to the transfer to the counterparty of cash, equity instruments, other assets or services.

The amendments are applied retrospectively for annual periods beginning on or after 1 January 2024, with early application permitted. The IASB has aligned the effective date with the 2022 amendments to IAS 1. If an entity applies the 2020 amendments for an earlier period, it is also required to apply the 2022 amendments early.

The Board of Directors anticipates that the adoption of those Standards listed above will have no material impact on the financial statements of the Company in future period.

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES

3.1 Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards.

3.2 Basis of preparation

The financial statements have been prepared on the historical cost basis except for certain properties and financial instruments that are measured at fair values at the end of each reporting period, as explained in the accounting policies below. Historical cost is generally based on the fair value of the consideration given in exchange for goods and services.

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date, regardless of whether that price is directly observable or estimated using another valuation technique. In estimating the fair value of an asset or a liability, the Company takes into account the characteristics of the asset or liability if market participants would take those characteristics into account when pricing the asset or liability at the measurement date. Fair value for measurement and/or disclosure purposes in these financial statements is determined on such a basis, except for share-based payment transactions that are within the scope of IFRS 2 Share-based Payment, leasing transactions that are within the scope of IFRS 16 Leases, and measurements that have some similarities to fair value but are not fair value, such as net realizable value in IAS 2 Inventories or value in use in IAS 36 Impairment of Assets.

3.3 Going concern

The Board of Directors has, at the time of approving the financial statements, a reasonable expectation that the Company has adequate resources to continue in operational existence for foreseeable future. Thus they continue to adopt the going concern basis of accounting n preparing the financial statements.

3.4 Foreign currencies

In preparing the financial statements of the individual entities, transactions in currencies other than the Company’s functional currency (SGD) are recorded at the rates of exchange prevailing at the dates of the transactions. At end of each reporting period, monetary items denominated in foreign currencies are retranslated at the rates prevailing at the end of the reporting period. Non- monetary items that are measured in terms of historical cost in a foreign currency are not retranslated.

3.5 Taxation

Income tax expense represents the sum of the tax currently payable and deferred tax.

Current tax

The tax currently payable is based on taxable profit for the year. Taxable profit differs from 'profit before tax' as reported in the statement of profit or loss because of items of income or expense that are taxable or deductible in other years and items that are never taxable or deductible. The Company's current tax is calculated using tax rates that have been enacted or substantively enacted by the end of the reporting period. Current tax are recognized in profit or loss.

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

Deferred tax

Deferred tax is recognized on temporary differences between the carrying amounts of assets and liabilities in the consolidated financial statements and the corresponding tax bases used in the computation of taxable profit. Deferred tax liabilities are generally recognized for all taxable temporary differences. Deferred tax assets are generally recognized for all deductible temporary differences to the extent that it is probable that taxable profits will be available against which those deductible temporary differences can be utilized. Such deferred tax assets and liabilities are not recognized if the temporary difference arises from the initial recognition (other than in a business combination) of assets and liabilities in a transaction that affects neither the taxable profit nor the accounting profit. In addition, deferred tax liabilities are not recognized if the temporary difference arises from the initial recognition of goodwill.

The carrying amount of deferred tax assets is reviewed at the end of each reporting period and reduced to the extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to be recovered.

Deferred tax liabilities and assets are measured at the tax rates that are expected to apply in the period in which the liability is settled or the asset realized, based on tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period.

The measurement of deferred tax liabilities and assets reflects the tax consequences that would follow from the manner in which the Company expects, at the end of the reporting period, to recover or settle the carrying amount of its assets and liabilities.

3.6 Provisions

Provisions are recognized when the Company has a present obligation (legal or constructive) as a result of a past event, it is probable that the Company will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation.

The amount recognized as a provision is the best estimate of the consideration required to settle the present obligation at the end of the reporting period, taking into account the risks and uncertainties surrounding the obligation. When a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows (when the effect of the time value of money is material).

When some or all of the economic benefits required to settle, a provision are expected to be recovered from a third party, a receivable is recognized as an asset if it is virtually certain that reimbursement will be received and the amount of the receivable can be measured reliably.

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.7 Financial instruments

Financial assets and financial liabilities are recognized when the Company becomes a party to the contractual provisions of the instruments. Financial assets and financial liabilities are initially measured at fair value. Transaction costs directly attributable to the acquisition of financial assets or financial liabilities at fair value through profit or loss are recognized immediately in profit or loss.

3.8 Financial assets

All regular way purchases or sales of financial assets are recognized and derecognized on a trade date basis. Regular way purchases or sales are purchases or sales of financial assets that require delivery of assets within the time frame established by regulation or convention in the marketplace.

All recognised financial assets are measured subsequently in their entirety at either amortised cost or fair value, depending on the classification of the financial assets.

Classification of financial assets

Debt instruments that meet the following conditions are measured subsequently at amortised cost:

·

The financial asset is held within a business model whose objective is to hold financial assets in order to collect contractual cash flows

·

The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

Debt instruments that meet the following conditions are measured subsequently at fair value through other comprehensive income (FVTOCI):

·

The financial asset is held within a business model whose objective is achieved by both collecting contractual cash flows and selling the financial assets.

·

The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

By default, all other financial assets are measured subsequently at fair value through profit or loss (FVTPL).

Effective interest method

The effective interest method is a method of calculating the amortized cost of a financial asset and of allocating interest income over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash receipts (including all fees and points paid or received that form an integral part of the effective interest rate, transaction costs and other premiums or discounts) through the expected life of the financial asset, or, where appropriate, a shorter period, to the net carrying amount on initial recognition.

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Loans and receivables (including trade and other receivables, bank balances and cash, and deposits) are measured at amortized cost using the effective interest method, less any impairment.

Interest income is recognized by applying the effective interest rate, except for short-term receivables when the effect of discounting is immaterial.

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.12 Financial assets (Continued)

Impairment of financial assets

The Company recognises a loss allowance for expected credit losses on investments in debt instruments that are measured at amortised cost or at FVTOCI, lease receivables, trade receivables and contract assets, as well as on financial guarantee contracts. The amount of expected credit losses is updated at each reporting date to reflect changes in credit risk since initial recognition of the respective financial instrument.

The Company always recognises lifetime expected credit losses (ECL) for trade receivables, contract assets and lease receivables. The expected credit losses on these financial assets are estimated using a provision matrix based on the Company’s historical credit loss experience, adjusted for factors that are specific to the debtors, general economic conditions and an assessment of both the current as well as the forecast direction of conditions at the reporting date, including time value of money where appropriate.

For all other financial instruments, the Group recognises lifetime ECL when there has been a significant increase in credit risk since initial recognition. However, if the credit risk on the financial instrument has not increased significantly since initial recognition, the Group measures the loss allowance for that financial instrument at an amount equal to 12-month ECL.

Lifetime ECL represents the expected credit losses that will result from all possible default events over the expected life of a financial instrument. In contrast, 12-month ECL represents the portion of lifetime ECL that is expected to result from default events on a financial instrument that are possible within 12 months after the reporting date.

There is no objective evidence of impairment for trade receivable, because trade receivable is only from related party. There is no past experience of bad collecting payments and no delayed payment.

Derecognition of financial assets

The Company derecognizes a financial asset when the contractual rights to the cash flows from the asset expire, or when it transfers the financial asset and substantially all the risks and rewards of ownership of the asset to another party. If the Company neither transfers nor retains substantially all the risks and rewards of ownership and continues to control the transferred asset, the Company recognizes its retained interest in the asset and an associated liability for amounts it may have to pay. If the Company retains substantially all the risks and rewards of ownership of a transferred financial asset, the Company continues to recognize the financial asset and also recognizes a collateralized borrowing for the proceeds received.

3.9 Financial liabilities and equity instruments

Classification as debt or equity

Debt and equity instruments issued by the Company are classified as either financial liabilities or as equity in accordance with the substance of the contractual arrangements and the definitions of a financial liability and an equity instrument.

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.13 Financial liabilities and equity instruments (continued)

Equity instruments

An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. Equity instruments issued by the Company are recognized at the proceeds received, net of direct issue costs.

Financial liabilities

Financial liabilities are classified 'other financial liabilities'.

Other financial liabilities

Other financial liabilities (including Trade and other payables) are initially measured at fair value, net of transaction costs, and are subsequently measured at amortized cost, using the effective interest method, with interest expense recognized on an effective yield basis.

The effective interest method is a method of calculating the amortized cost of a financial liability and of allocating interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments (including all fees and points paid or received that form an integral part of the effective interest rate, transaction costs and other premiums or discounts) through the expected life of the financial liability, or (where appropriate) a shorter period, to the net carrying amount on initial recognition.

Derecognition of financial liabilities

The Company derecognizes financial liabilities when, and only when, the Company's obligations are discharged, cancelled or they expire. The difference between the carrying amount of the financial liability derecognized and the consideration paid and payable is recognized in profit or loss.

4. CRITICAL ACCOUNTING JUDGMENTS

In the application of the Company’s accounting policies, which are described in note 3, management is required to make judgments, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the year in which the estimate is revised if the revision affects only that year, or in the year of the revision and future periods if the revision affects both current and future periods.

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

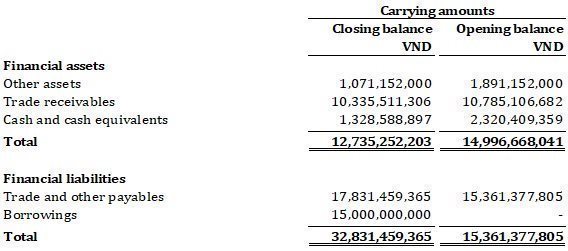

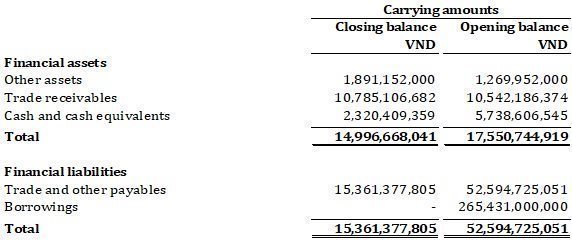

10. FINANCIAL INSTRUMENTS

Capital risk management

The Company manages its capital to ensure that the Company will be able to continue as a going concern while maximizing the return to stakeholders through the optimization of the debt and equity balance. The Company's overall strategy remains unchanged from prior year. The capital structure of the Company consists of net debt (borrowings offset by cash and cash equivalents)

and equity attributable to equity holders of the Company (comprising capital and retained earnings).

Categories of financial instruments

Carrying amounts

Closing balance

SGD

Financial assets

Unpaid share capital

13,676

Total

13,676

Financial liabilities

Trade and other payables

3,131

Total

3,131

Loans and receivables designated as at FVTPL

At the end of the reporting period, there are no significant concentrations of credit risk for loans and receivables designated at FVTPL. The carrying amount reflected above represents the Company's maximum exposure to credit risk for such loans and receivables.

Financial risk management objectives

These risks include market risk (including currency risk and interest rate risk), credit risk and liquidity risk.

The Company seeks to minimize the effects of these risks by using financial risk structures instructed by the Group. It should be governed by the Group's policies approved by the Board of General Directors, which provide principles on foreign exchange risk, interest rate risk, credit risk and liquidity risk. Compliance with policies and exposure limits is reviewed by the Group’s internal auditors on a continuous basis. The Company does not enter into or trade financial instruments, including derivative financial instruments, for speculative purposes.

Market risk

The Company’s activities expose it primarily to the financial risks of changes in foreign currency exchange rates and interest rates. The Company does not perform protection solution for market risk due to lack of purchasing market of the financial instrument.

Interest rate risk management

The Company has no interest rate risks because the Company has not arranged any loans and borrowings during the year.

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

24. FINANCIAL INSTRUMENTS (CONTINUED)

Credit risk

Credit risk refers to the risk that counterparty will default on its contractual obligations resulting in financial loss to the Company. The Company has a credit policy in place and the exposure to credit risk is monitored on an ongoing basis. At the balance sheet date there is no significant concentration of credit risk.

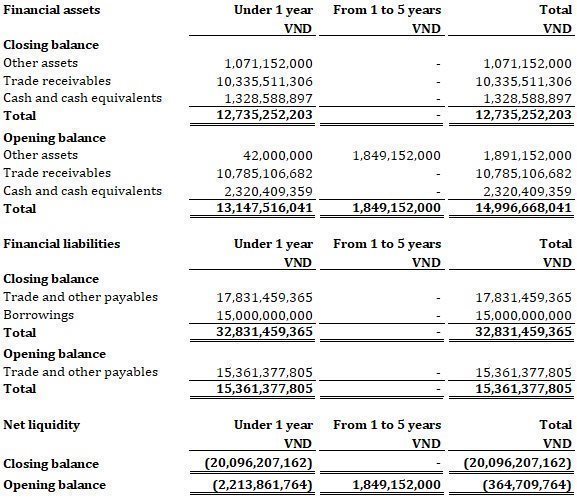

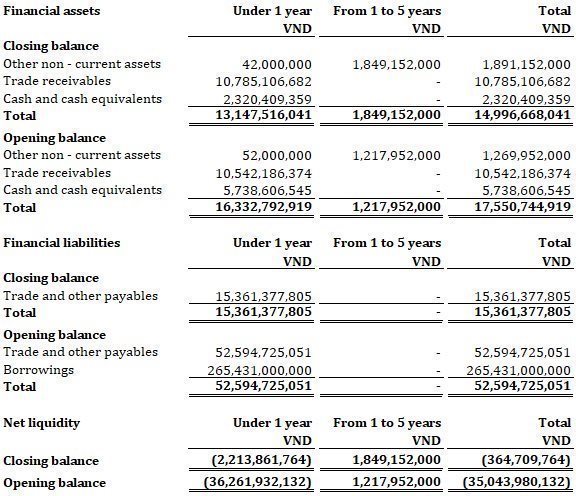

Liquidity risk management

The purpose of liquidity risk management is to ensure the availability of funds to meet present and future financial obligations. Liquidity is also managed by ensuring that the excess of maturing liabilities over maturing assets in any year is kept to manageable levels relative to the amount of funds that the Company believes can generate within that period. The Company policy is to regularly monitor current and expected liquidity requirements to ensure that the Company maintains sufficient reserves of cash, borrowings and adequate committed funding from its owner to meet its liquidity requirements in the short and longer term.

The below table illustrates current and future net liquidity risk management as follow:

Financial assets

Under 1 year

From 1 to 5 years

Total

SGD

SGD

SGD

Closing balance

Unpaid share capital

13,676

-

13,676

Total

13,676

-

13,676

Financial liabilities

Under 1 year

From 1 to 5 years

Total

SGD

SGD

SGD

Closing balance

Trade and other payables

3,131

-

3,131

Total

3,131

-

3,131

Net liquidity

Under 1 year

From 1 to 5

years

Total

SGD

SGD

SGD

Closing balance

10,545

-

10,545

The management assessed the liquidity risk concentration at low level. The Management believes that the Company will be able to generate sufficient funds to meet its financial obligations as and when they fall due.

11. APPROVAL OF FINANCIAL STATEMENTS

The Company’s financial statements were approved by Mr. Nguyen Van Hoang - Director and authorized for issue on 10 May 2024.

12. COMPARATIVE FIGURES

These financial statements cover the period from the inception of the Company on 01 November 2023 (incorporation date) to 31 December 2023, This is the first set of financial statements; hence, no comparative figures are presented.

Board of Management and General Director of VinHMS Software Production and Trading Joint Stock Company present this report together with audited financial statements for the year ended 31 December 2023.

Board of MANAGEMENT AND GENERAL DIRECTOR

Board of Management of the Company who held office during the year and at the date of this report are as follows:

Ms. Nguyen Mai Hoa

Chairwoman

Mr. Nguyen Van Hoang

Member

Ms. Doan Le Thanh Xuan

Member

General Director of the Company who held the office during the year and at the date of this report is as follows:

Mr. Nguyen Van Hoang

General Director

LEGAL REPRESENTATIVE

The legal representative of the Company who approved the financial statement for the year ended 31 Decmber 2023 and at the date of this report is Mr. Nguyen Van Hoang – General Director

SUBSEQUENT EVENTS

According to Board of Management and General Director, in all material respects, there have been no other significant events occurring after the balance sheet date affecting the financial position and operation of the Company which would require adjustments to or disclosures to be made in the financial statements for the year ended 31 December 2023.

AUDITOR

The accompanying financial statements for the year ended 31 December 2023 have been audited by Parker Russell Vietnam Company Limited (Parker Russell Vietnam).

BOARD OF MANAGEMENT AND GENERAL DIRECTOR’ STATEMENT OF RESPONSIBILITY

Board of Management and General Director of the Company are responsible for preparing the financial statements of each year, which give a true and fair view of the financial position of the Company and of its results and cash flows for the period.

In preparing those financial statements, Board of Management and General Director are required to:

·

Select suitable accounting policies and then apply them consistently;

·

Make judgments and estimates that are reasonable and prudent;

·

State whether applicable accounting principles have been complied with, material differences are disclosed and explained in the financial statements;

·

Design, execute and maintain an effective internal control related to the appropriate preparation and presentation of financial statements so as to obtain reasonable assurance that the financial statements are free of material misstatements caused by even frauds and errors; and

·

Prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company will continue in business.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

REPORT OF BOARD OF MANAGEMENT AND GENERAL DIRECTOR (CONTINUED)

BOARD OF MANAGEMENT AND GENERAL DIRECTOR’ STATEMENT OF RESPONSIBILITY (CONTINUED)

Board of Management and General Director confirm that the Company has complied with the above requirements in preparing these financial statements.

Board of Management and General Director are responsible for ensuring that proper accounting records are kept, which disclose, with reasonable accuracy at any time, the financial position of the Company and to ensure that the financial statements comply with International Financial Reporting Standards. It is also responsible for safeguarding the assets of the Company and hence for taking reasonable steps for the prevention and detection of frauds and other irregularities.

VinHMS Software Production and Trading Joint Stock Company

Opinion

We have audited the accompanying financial statements of VinHMS Software Production and Trading Joint Stock Company, prepared on 24 April 2024 as set out from page 5 to page 32, which comprise Statement of financial position as at 31 December 2023, Statement of profit and loss, Statement of changes in equity and Statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information.

In our opinion, the accompanying financial statements give a true and fair view of, in all material respects, the financial position of the Company as at 31 December 2023 and the results of its operations and its cash flows for the year ended 31 December 2023, in accordance with International Financial Reporting Standards.

Basis for Opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company and have fulfilled our other responsibilities under those relevant ethical requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Going Concern

The Company’s financial statements have been prepared using the going concern basis of accounting. The use of this basis of accounting is appropriate unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so. As part of our audit of the financial statements, we have concluded that management’s use of the going concern basis of accounting in the preparation of the Company’s financial statements is appropriate. Management has not identified a material uncertainty that may cast significant doubt on the entity’s ability to continue as a going concern, and accordingly none is disclosed in the financial statements. Based on our audit of the financial statements, we also have not identified such a material uncertainty. However, neither management nor the auditor can guarantee the Company’s ability to continue as a going concern.

Responsibilities of Management for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with IFRSs and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Management are responsible for overseeing the Company’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

The objectives of our audit are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the planning and performance of the audit. We also:

·

Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

·

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control.

·

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

·

Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We are required to communicate with management regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit. We are also required to provide management with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

/s/ Nguyen Song Toan

Nguyen Song Toan

Partner

Audit Practising Registration Certificate

No. 1551-2023-238-1

For and on behalf of

Parker Russell Vietnam Company Limited (Parker Russell Vietnam)

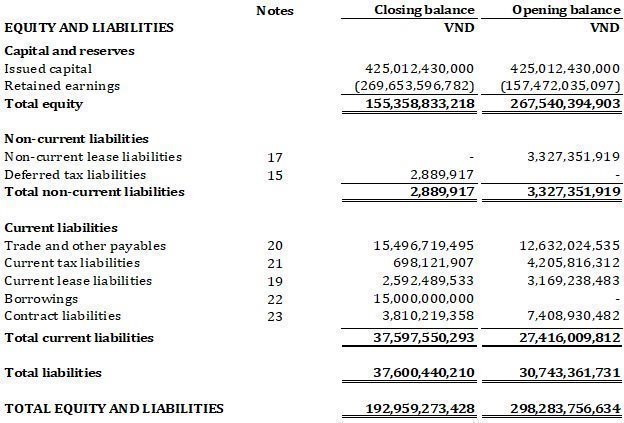

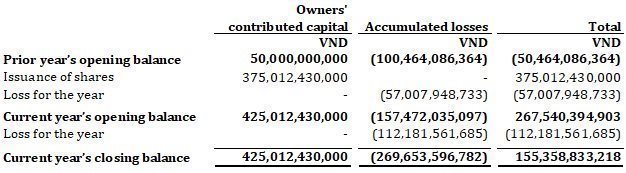

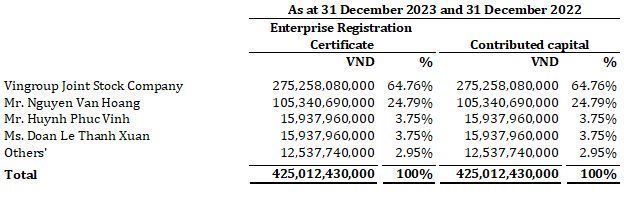

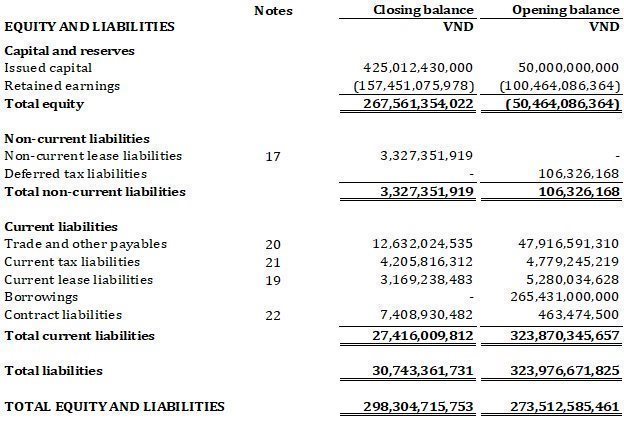

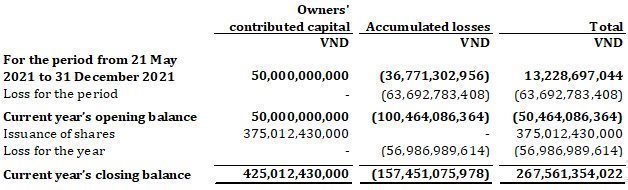

According to the Company’s Enterprise Registration Certificate and the amendment, the Company’s charter capital is VND 425,012,430,000. The charter capital has been fully contributed by the shareholders as at 31 December 2023.

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

1. GENERAL INFORMATION

1.1. Structure of ownership

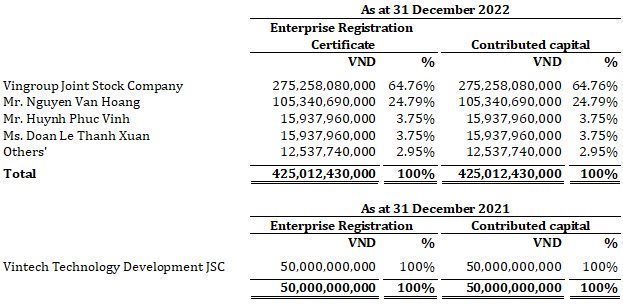

VinHMS Software Production and Trading Joint Stock Company (“the Company”) is incorporated in Vietnam, as a joint stock company under the Enterprise Registration Certificate No. 0315396330 issued by Department of Planning and Investment of Ha Noi City dated 21 November 2018, and the latest amendment dated 18 December 2023. The charter capital of the Company is VND 425,012,430,000.

The Company’s office is located at No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area City, Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam.

Number of employees as at 31 December 2023 was 73 (As at 31 December 2022: 79).

1.2. Principal activities

The principal activities of the Company are software production and rendering of software solutions.

1.3. Financial year

The Company’s financial year begins on 01 January and ends on 31 December.

2. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs)

New and amended IFRSs that are effective for the current year

Amendments to IAS 1 Presentation of Financial Statements and IFRS Practice Statement 2 Making Materiality Judgements – Disclosure of Accounting Policies

The Company has adopted the amendments to IAS 1 for the first time in the current year. The amendments change the requirements in IAS 1 with regard to disclosure of accounting policies. The admendments replace all instances of the term ‘’significant accounting policies” with “material accounting policy information’’. Accounting policy information is material if, when considered together with other information included in an entity’s financial statements, it can reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements.

The supporting paragraphs in IAS 1 are also amended to clarify that accounting policy information that relates to immaterial transactions, other events or conditions is immaterial and need not be disclosed. Accounting policy information may be material because of the nature of the related transactions, other events or conditions, even if the amounts are immaterial. However, not all accounting policy information relating to material transactions, other events or conditions is itself material.

Amendments to IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors – Definition of Accounting Estimates

The Company has adopted the amendments to IAS 8 for the first time in the current year. The amendments replace the definition of accounting estimates. Under the new definition, accounting estimates are “monetary amounts in financial statements that are subject to measurement uncertainty”. The definition of a change in accounting estimates was deleted.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

2. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRSs) (CONTINUED)

New and revised IFRSs in issue but not yet effective

Amendments to IAS 1 Classification of Liabilities as Current or Non-Current

The amendments to IAS 1 affect only the presentation of liabilities as current or non-current in the statement of financial position and not the amount or timing of recognition of any asset, liability, income or expenses, or the information disclosed about those items.

The amendments clarify that the classification of liabilities as current or non-current is based on rights that are in existence at the end of the reporting period, specify that classification is unaffected by expectations about whether an entity will exercise its right to defer settlement of a liability, explain that rights are in existence if covenants are complied with at the end of the reporting period, and introduce a definition of ‘settlement’ to make clear that settlement refers to the transfer to the counterparty of cash, equity instruments, other assets or services.

The amendments are applied retrospectively for annual periods beginning on or after 1 January 2024, with early application permitted. The IASB has aligned the effective date with the 2022 amendments to IAS 1. If an entity applies the 2020 amendments for an earlier period, it is also required to apply the 2022 amendments early.

The Board of General Directors anticipates that the adoption of those Standards listed above will have no material impact on the financial statements of the Company in future period.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES

3.1 Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards.

3.2 Basis of preparation

The financial statements have been prepared on the historical cost basis except for certain properties and financial instruments that are measured at fair values at the end of each reporting period, as explained in the accounting policies below. Historical cost is generally based on the fair value of the consideration given in exchange for goods and services.

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date, regardless of whether that price is directly observable or estimated using another valuation technique. In estimating the fair value of an asset or a liability, the Company takes into account the characteristics of the asset or liability if market participants would take those characteristics into account when pricing the asset or liability at the measurement date. Fair value for measurement and/or disclosure purposes in these financial statements is determined on such a basis, except for share-based payment transactions that are within the scope of IFRS 2 Share-based Payment, leasing transactions that are within the scope of IFRS 16 Leases, and measurements that have some similarities to fair value but are not fair value, such as net realizable value in IAS 2 Inventories or value in use in IAS 36 Impairment of Assets.

3.3 Going concern

The General Director has, at the time of approving the financial statements, a reasonable expectation that the Company has adequate resources to continue in operational existence for foreseable future. Thus they continue to adopt the going concern basis of accounting n preparing the financial statements.

3.4 Revenue

Revenue is measured based on the consideration to which the Company expects to be entitled in a contract with a customer and excludes amounts collected on behalf of third parties. The Company recognises revenue when it transfers control of a product or service to a customer.

Revenue recognition

The Company recognises revenue from the following major sources:

·

Sale from production of software

·

Sale from renderring of software solutions

Production of software

The Company produces software based on the customers’requests. The software will be produces for specialised business operations of the customers. Such services are recognised as a performance obligation satisfied either over the time or point in time. For over the time, revenue is recognised for the services based on the stage of completion of the contract. For point in time, revenue is recognised when control of the software has transferred to customers.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.4 Revenue (continued)

Renderring of software solutions

The Company renderred of software solutions by providing license of the software. Such services are recognised as a performance obligation satisfied over the time. Revenue is recognised for the services when the license is transferred to the customers and customers can use the software.

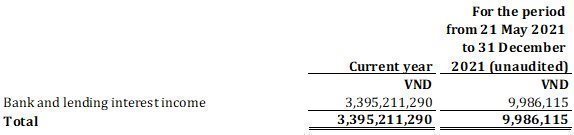

Interest income

Interest income from a financial asset is recognized when it is probable that the economic benefits will flow to the Company and the amount of income can be measured reliably. Interest income is accrued on a time basis, by reference to the principal outstanding and at the effective interest rate applicable, which is the rate that exactly discounts estimated future cash receipts through the expected life of the financial asset to that asset's net carrying amount on initial recognition.

3.5 Leasing

The Company assesses whether a contract is or contains a lease, at inception of the contract. The Company recognises a right-of-use asset and a corresponding lease liability with respect to all lease arrangements in which it is the lessee, except for short-term leases (defined as leases with a lease term of 12 months or less) and leases of low value assets (such as tablets and personal computers, small items of office furniture and telephones). For these leases, the Company recognises the lease payments as an operating expense on a straight-line basis over the term of the lease unless another systematic basis is more representative of the time pattern in which economic benefits from the leased assets are consumed.

The lease liability is initially measured at the present value of the lease payments that are not paid at the commencement date, discounted by using the rate implicit in the lease. If this rate cannot be readily determined, the Company uses average incremental borrowing rate in market.

Lease payments included in the measurement of the lease liability comprise:

·

Fixed lease payments (including in-substance fixed payments), less any lease incentives receivable;

·

Variable lease payments that depend on an index or rate, initially measured using the index or rate at the commencement date;

·

The amount expected to be payable by the lessee under residual value guarantees;

·

The exercise price of purchase options, if the lessee is reasonably certain to exercise the options; and

·

Payments of penalties for terminating the lease, if the lease term reflects the exercise of an option to terminate the lease.

The lease liability is presented as a separate line in the statement of financial position.

The lease liability is subsequently measured by increasing the carrying amount to reflect interest on the lease liability (using the effective interest method) and by reducing the carrying amount to reflect the lease payments made.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.4 Leasing (continued)

The Company remeasures the lease liability (and makes a corresponding adjustment to the related right-of-use asset) whenever:

·

The lease term has changed or there is a significant event or change in circumstances resulting in a change in the assessment of exercise of a purchase option, in which case the lease liability is remeasured by discounting the revised lease payments using a revised discount rate.

·

The lease payments change due to changes in an index or rate or a change in expected payment under a guaranteed residual value, in which cases the lease liability is remeasured by discounting the revised lease payments using an unchanged discount rate (unless the lease payments change is due to a change in a floating interest rate, in which case a revised discount rate is used).

·

A lease contract is modified and the lease modification is not accounted for as a separate lease, in which case the lease liability is remeasured based on the lease term of the modified lease by discounting the revised lease payments using a revised discount rate at the effective date of the modification.

The Company did not make any such adjustments during the periods presented.

The right-of-use assets comprise the initial measurement of the corresponding lease liability, lease payments made at or before the commencement day, less any lease incentives received and any initial direct costs. They are subsequently measured at cost less accumulated depreciation and impairment losses.

Right-of-use assets are depreciated over the shorter period of lease term and useful life of the underlying asset. If a lease transfers ownership of the underlying asset or the cost of the right-of-use asset reflects that the Company expects to exercise a purchase option, the related right-of-use asset is depreciated over the useful life of the underlying asset. The depreciation starts at the commencement date of the lease.

The right-of-use assets are presented as a separate line in the statement of financial position.

The Company applies IAS 36 to determine whether a right-of-use asset is impaired and accounts for any identified impairment loss.

3.6 Foreign currencies

In preparing the financial statements of the individual entities, transactions in currencies other than the Company’s functional currency (VND) are recorded at the rates of exchange prevailing at the dates of the transactions. At end of each reporting period, monetary items denominated in foreign currencies are retranslated at the rates prevailing at the end of the reporting period. Non-monetary items that are measured in terms of historical cost in a foreign currency are not retranslated.

3.7 Taxation

Income tax expense represents the sum of the tax currently payable and deferred tax.

Current tax

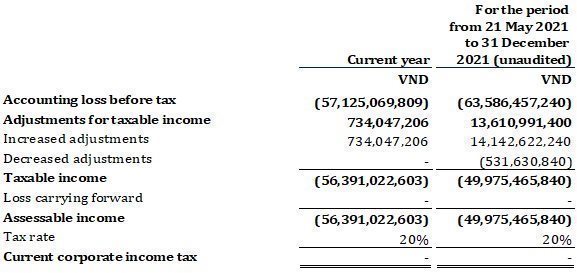

The tax currently payable is based on taxable profit for the year. Taxable profit differs from 'profit before tax' as reported in the statement of profit or loss because of items of income or expense that are taxable or deductible in other years and items that are never taxable or deductible. The Company's current tax is calculated using tax rates that have been enacted or substantively enacted by the end of the reporting period. Current tax are recognized in profit or loss.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

Deferred tax

Deferred tax is recognized on temporary differences between the carrying amounts of assets and liabilities in the consolidated financial statements and the corresponding tax bases used in the computation of taxable profit. Deferred tax liabilities are generally recognized for all taxable temporary differences. Deferred tax assets are generally recognized for all deductible temporary differences to the extent that it is probable that taxable profits will be available against which those deductible temporary differences can be utilized. Such deferred tax assets and liabilities are not recognized if the temporary difference arises from the initial recognition (other than in a business combination) of assets and liabilities in a transaction that affects neither the taxable profit nor the accounting profit. In addition, deferred tax liabilities are not recognized if the temporary difference arises from the initial recognition of goodwill.

The carrying amount of deferred tax assets is reviewed at the end of each reporting period and reduced to the extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to be recovered.

Deferred tax liabilities and assets are measured at the tax rates that are expected to apply in the period in which the liability is settled or the asset realized, based on tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period.

The measurement of deferred tax liabilities and assets reflects the tax consequences that would follow from the manner in which the Company expects, at the end of the reporting period, to recover or settle the carrying amount of its assets and liabilities.

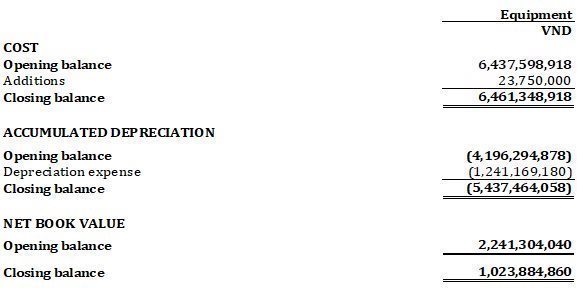

3.8 Property, plant and equipment

Fixtures and equipment are stated at cost less accumulated depreciation and accumulated impairment losses.

Depreciation is recognized so as to write off the cost or valuation of assets (other than freehold land and properties under construction) less their residual values over their useful lives, using the straight--line method. The estimated useful lives and depreciation method are reviewed at the end of each reporting period, with the effect of any changes in estimate accounted for on a prospective basis.

An item of property, plant and equipment is derecognized upon disposal or when no future economic benefits are expected to arise from the continued use of the asset. Any gain or loss arising on the disposal or retirement of an item of property, plant and equipment is determined as the difference between the sales proceeds and the carrying amount of the asset and is recognized in profit or loss.

3.9 Intangible assets

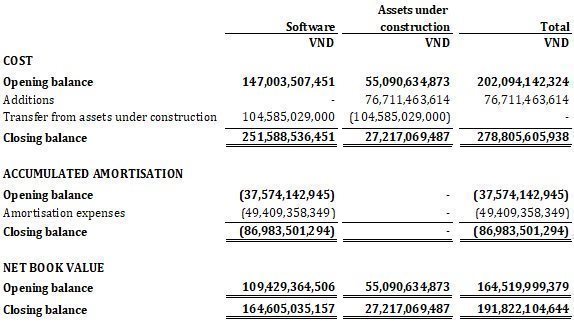

Acquired computer software licenses

Acquired computer software licenses are initially capitalized at cost, which includes the purchase price (net of any discounts and rebates) and other directly attributable cost of preparing the asset for its intended use. Direct expenditure including employee costs, which enhances or extends the performance of computer software beyond its specifications and which can be reliably measured, is added to the original cost of the software. Costs associated with maintaining the computer software are recognized as an expense when incurred.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.9 Intangible assets (continued)

Computer software licenses are subsequently carried at cost less accumulated amortization and accumulated impairment losses. These costs are amortized to profit or loss using the straight-line method over their estimated useful lives of three years.

Internally-generated intangible assets – research and development expenditure

Expenditure on research activities is recognised as an expense in the period in which it incurred.

An internally-generated intagible asset arising from development (or from the development phase of an internal project) is recognised if, and only if, all of the following conditions have been demonstrated:

·

The technical feasibility of completing the intangible asset so that it will be available for use or sale

·

The intention to complete the intangible asset and use or sell it

·

The ability to use or sell the intangible asset

·

How the intangible asset will generate probable future economic benefits

·

The availability of adequate technical, financial and other resoures to complete the development and to use or sell the intangible asset

·

The ability to measure reliably the expenditure attributable to the intangible asset during its development

The amount initially recognised for internally-generated intangible assets is the sum of expenditure incurred from the date when the intangible asset first meets the recognition criteria listed above. Where no internally-generated intangible asset can be recognised, development expenditure is recognised in profit or loss in the period in which it incurred.

Subsequent to initial recognition, internally-generated intnagible assets are reported at cost less accumulated amortisation and accumulated impairment losses, on the same basis as intangible assets that are acquired seperately.

Derecognition of intangible assets

An intangible asset is derecognized on disposal, or when no future economic benefits are expected from use or disposal. Gains or losses arising from derecognition of an intangible asset, measured as the difference between the net disposal proceeds and the carrying amount of the asset, are recognized in profit or loss when the asset is derecognized.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.8 Intangible assets (Continued)

Impairment of tangible and intangible assets

At the end of each reporting period, the Company reviews the carrying amounts of its tangible and intangible assets to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). When it is not possible to estimate the recoverable amount of an individual asset, the Group estimates the recoverable amount of the cash -generating unit to which the asset belongs. When a reasonable and consistent basis of allocation can be identified, corporate assets are also allocated to individual cash-generating units, or otherwise they are allocated to the smallest group of cash-generating units for which a reasonable and consistent allocation basis can be identified.

Recoverable amount is the higher of fair value less costs of disposal and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (or cash-generating unit) is reduced to its recoverable amount. An impairment loss is recognized immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease.

When an impairment loss subsequently reverses, the carrying amount of the asset (or a cash- generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognized for the asset (or cash-generating unit) in prior years. A reversal of an impairment loss is recognized immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase.

3.10 Provisions

Provisions are recognized when the Company has a present obligation (legal or constructive) as a result of a past event, it is probable that the Company will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation.

The amount recognized as a provision is the best estimate of the consideration required to settle the present obligation at the end of the reporting period, taking into account the risks and uncertainties surrounding the obligation. When a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows (when the effect of the time value of money is material).

When some or all of the economic benefits required to settle, a provision are expected to be recovered from a third party, a receivable is recognized as an asset if it is virtually certain that reimbursement will be received and the amount of the receivable can be measured reliably.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.11 Financial instruments

Financial assets and financial liabilities are recognized when the Company becomes a party to the contractual provisions of the instruments. Financial assets and financial liabilities are initially measured at fair value. Transaction costs directly attributable to the acquisition of financial assets or financial liabilities at fair value through profit or loss are recognized immediately in profit or loss.

3.12 Financial assets

All regular way purchases or sales of financial assets are recognized and derecognized on a trade date basis. Regular way purchases or sales are purchases or sales of financial assets that require delivery of assets within the time frame established by regulation or convention in the marketplace.

All recognised financial assets are measured subsequently in their entirety at either amortised cost or fair value, depending on the classifiation of the financial assets.

Classification of financial assets

Debt instruments that meet the following conditions are measured subsequently at amortised cost:

·

The financial asset is held within a business model whose objective is to hold fiancial assets in order to collect contractual cash flows

·

The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

Debt instruments that meet the following conditions are measured subsequently at fair value through other comprehensive income (FVTOCI):

·

The financial asset is held within a business model whose objective is achieved by both collecting contractual cash flows and selling the financial assets.

·

The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

By default, all other financial assets are measured subsequently at fair value through profit or loss (FVTPL).

Effective interest method

The effective interest method is a method of calculating the amortized cost of a financial asset and of allocating interest income over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash receipts (including all fees and points paid or received that form an integral part of the effective interest rate, transaction costs and other premiums or discounts) through the expected life of the financial asset, or, where appropriate, a shorter period, to the net carrying amount on initial recognition.

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Loans and receivables (including trade and other receivables, bank balances and cash, and deposits) are measured at amortized cost using the effective interest method, less any impairment.

Interest income is recognized by applying the effective interest rate, except for short-term receivables when the effect of discounting is immaterial.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.12 Financial assets (Continued)

Impairment of financial assets

The Company recognises a loss allowance for expected credit losses on investments in debt instruments that are measured at amortised cost or at FVTOCI, lease receivables, trade receivables and contract assets, as well as on financial guarantee contracts. The amount of expected credit losses is updated at each reporting date to reflect changes in credit risk since initial recognition of the respective financial instrument.

The Company always recognises lifetime expected credit losses (ECL) for trade receivables, contract assets and lease receivables. The expected credit losses on these financial assets are estimated using a provision matrix based on the Company’s historical credit loss experience, adjusted for factors that are specific to the debtors, general economic conditions and an assessment of both the current as well as the forecast direction of conditions at the reporting date, including time value of money where appropriate.

For all other financial instruments, the Group recognises lifetime ECL when there has been a significant increase in credit risk since initial recognition. However, if the credit risk on the financial instrument has not increased significantly since initial recognition, the Group measures the loss allowance for that financial instrument at an amount equal to 12-month ECL.

Lifetime ECL represents the expected credit losses that will result from all possible default events over the expected life of a financial instrument. In contrast, 12-month ECL represents the portion of lifetime ECL that is expected to result from default events on a financial instrument that are possible within 12 months after the reporting date.

There is no objective evidence of impairment for trade receivable, because trade receivable is only from related party. There is no past experience of bad collecting payments and no delayed payment.

Derecognition of financial assets

The Company derecognizes a financial asset when the contractual rights to the cash flows from the asset expire, or when it transfers the financial asset and substantially all the risks and rewards of ownership of the asset to another party. If the Company neither transfers nor retains substantially all the risks and rewards of ownership and continues to control the transferred asset, the Company recognizes its retained interest in the asset and an associated liability for amounts it may have to pay. If the Company retains substantially all the risks and rewards of ownership of a transferred financial asset, the Company continues to recognize the financial asset and also recognizes a collateralized borrowing for the proceeds received.

3.13 Financial liabilities and equity instruments

Classification as debt or equity

Debt and equity instruments issued by the Company are classified as either financial liabilities or as equity in accordance with the substance of the contractual arrangements and the definitions of a financial liability and an equity instrument.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

3. MATERIAL ACCOUNTING POLICIES (CONTINUED)

3.13 Financial liabilities and equity instruments (continued)

Equity instruments

An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. Equity instruments issued by the Company are recognized at the proceeds received, net of direct issue costs.

Financial liabilities

Financial liabilities are classified 'other financial liabilities'.

Other financial liabilities

Other financial liabilities (including Trade and other payables) are initially measured at fair value, net of transaction costs, and are subsequently measured at amortized cost, using the effective interest method, with interest expense recognized on an effective yield basis.

The effective interest method is a method of calculating the amortized cost of a financial liability and of allocating interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments (including all fees and points paid or received that form an integral part of the effective interest rate, transaction costs and other premiums or discounts) through the expected life of the financial liability, or (where appropriate) a shorter period, to the net carrying amount on initial recognition.

Derecognition of financial liabilities

The Company derecognizes financial liabilities when, and only when, the Company's obligations are discharged, cancelled or they expire. The difference between the carrying amount of the financial liability derecognized and the consideration paid and payable is recognized in profit or loss.

4. CRITICAL ACCOUNTING JUDGMENTS

In the application of the Company’s accounting policies, which are described in note 3, management is required to make judgments, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the year in which the estimate is revised if the revision affects only that year, or in the year of the revision and future periods if the revision affects both current and future periods.

VINHMS SOFTWARE PRODUCTION AND TRADING JOINT STOCK COMPANY

No. 7, Bang Lang 1 Street, Vinhomes Riverside Urban Area,

Viet Hung Ward, Long Bien District, Ha Noi City, Vietnam

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED)

These accompanying notes are an integral part of and should be read in conjunction with the financial statements

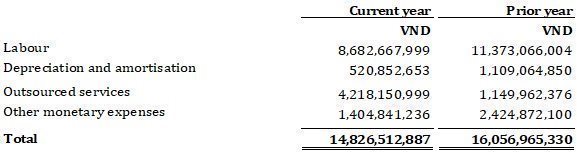

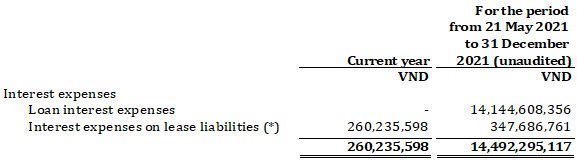

10. FINANCE COST