| | | | |

OMB APPROVAL |

| OMB Number: | | 3235-0570 |

| Expires: | | January 31, 2017 |

| Estimated average burden |

| hours per response: | | 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22957

Invesco Management Trust

(Exact name of registrant as specified in charter)

| | |

| 11 Greenway Plaza, Suite 1000 Houston, Texas | | 77046 |

| (Address of principal executive offices) | | (Zip code) |

Sheri Morris 11 Greenway Plaza, Suite 1000 Houston, Texas 77046

(Name and address of agent for service)

Registrant’s telephone number, including area code: (713) 626-1919

Date of fiscal year end: 8/31

Date of reporting period: 8/31/16

Item 1. Report to Stockholders.

Letters to Shareholders

| | | | |

Philip Taylor | | | | Dear Shareholders: This annual report includes information about your Fund, including performance data and a complete list of its investments as of the close of the reporting period. Inside is a discussion of how your Fund was managed and the factors that affected its performance during the reporting period. In December 2015, the US Federal Reserve raised short-term interest rates for the first time since 2006, signaling its belief that the economy was likely to continue strengthening. Indeed, throughout the reporting period, US economic data were generally positive and the economy expanded at a moderate rate – but there were some bumps along the road. Job growth in May 2016 was very weak, but it was followed by strong increases in nonfarm payrolls in June and July. Increased concerns about global economic weakness caused US stock market indexes to sink at the start of calendar year 2016, but they eventually recovered; they sank again |

following the UK’s decision to leave the European Union, but then quickly recovered and reached record highs later in the summer. Strong demand for income-producing investments, particularly those perceived to be lower risk, benefited bonds as well as dividend-paying stocks, including utilities stocks. While economic news in the US was generally positive, news overseas was less upbeat. The European Central Bank, and central banks in China and Japan – as well as other countries – maintained extraordinarily accommodative monetary policies in response to economic weakness.

Short-term market volatility can prompt some investors to abandon their investment plans – and can cause others to settle for average results. The investment professionals at Invesco, in contrast, invest with high conviction and a long-term perspective. At Invesco, investing with high conviction means offering a wide range of strategies designed to go beyond market benchmarks. We trust our research-driven insights, have confidence in our investment processes and build portfolios that reflect our beliefs. Our goal is to look past market noise in an effort to find attractive opportunities at attractive prices – consistent with the investment strategies spelled out in each fund’s prospectus. Of course, investing with high conviction can’t guarantee a profit or ensure investment success; no investment strategy or risk analysis can. To learn more about how we invest with high conviction, visit invesco.com/HighConviction.

You, too, can invest with high conviction by maintaining a long-term investment perspective and by working with your financial adviser on a regular basis. During periods of short-term market volatility or uncertainty, your financial adviser can keep you focused on your long-term investment goals – a new home, a child’s college education, or a secure retirement. He or she also can share research about the economy, the markets and individual investment options.

Visit our website for more information on your investments

Our website, invesco.com/us, offers a wide range of market insights and investment perspectives. On the website, you’ll find detailed information about our funds, including performance, holdings and portfolio manager commentaries. You can access information about your account by completing a simple, secure online registration. Click on the “Need to register” link in the “Account Access” box on our homepage to get started.

In addition to the resources accessible on our website and through our mobile app, you can obtain timely updates to help you stay informed about the markets, the economy and investing by connecting with Invesco on Twitter, LinkedIn or Facebook. You can access our blog at blog.invesco.us.com. Our goal is to provide you the information you want, when and where you want it.

Finally, I’m pleased to share with you Invesco’s commitment to both the Principles for Responsible Investment and to considering environmental, social and governance issues in our robust investment process. I invite you to learn more at invesco.com/esg.

Have questions?

For questions about your account, contact an Invesco client services representative at 800 959 4246. For Invesco-related questions or comments, please email me directly at phil@invesco.com.

All of us at Invesco look forward to serving your investment management needs. Thank you for investing with us.

Sincerely,

Philip Taylor

Senior Managing Director, Invesco Ltd.

|

| 2 Invesco Conservative Income Fund |

| | | | |

Bruce Crockett | | | | Dear Fellow Shareholders: Among the many important lessons I’ve learned in more than 40 years in a variety of business endeavors is the value of a trusted advocate. As independent chair of the Invesco Funds Board, I can assure you that the members of the Board are strong advocates for the interests of investors in Invesco’s mutual funds. We work hard to represent your interests through oversight of the quality of the investment management services your funds receive and other matters important to your investment, including but not limited to: n Ensuring that Invesco offers a diverse lineup of mutual funds that your financial adviser can

use to strive to meet your financial needs as your investment goals change over time. n Monitoring how the portfolio management teams of the Invesco funds are performing in

light of changing economic and market conditions. |

| n | | Assessing each portfolio management team’s investment performance within the context of the investment strategy described in the fund’s prospectus. |

| n | | Monitoring for potential conflicts of interests that may impact the nature of the services that your funds receive. |

We believe one of the most important services we provide our fund shareholders is the annual review of the funds’ advisory and sub-advisory contracts with Invesco Advisers and its affiliates. This review is required by the Investment Company Act of 1940 and focuses on the nature and quality of the services Invesco provides as the adviser to the Invesco funds and the reasonableness of the fees that it charges for those services. Each year, we spend months carefully reviewing information received from Invesco and a variety of independent sources, such as performance and fee data prepared by Lipper Inc., an independent, third-party firm widely recognized as a leader in its field. We also meet with our independent legal counsel and other independent advisers to review and help us assess the information that we have received. Our goal is to assure that you receive quality investment management services for a reasonable fee.

I trust the measures outlined above provide assurance that you have a worthy advocate when it comes to choosing the Invesco Funds.

As always, please contact me at bruce@brucecrockett.com with any questions or concerns you may have. On behalf of the Board, we look forward to continuing to represent your interests and serving your needs.

Sincerely,

Bruce L. Crockett

Independent Chair

Invesco Funds Board of Trustees

|

| 3 �� Invesco Conservative Income Fund |

Management’s Discussion of Fund Performance

Performance summary

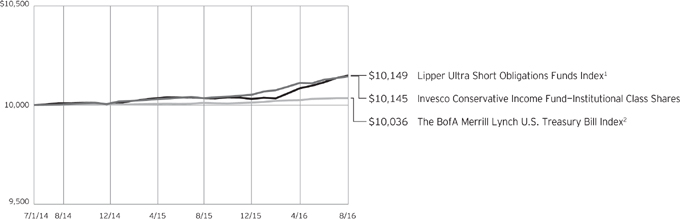

For the fiscal year ended August 31, 2016, Institutional Class shares of Invesco Conservative Income Fund (the Fund) outperformed The BofA Merrill Lynch U.S. Treasury Bill Index.

Your Fund’s long-term performance appears later in this report.

Fund vs. Indexes

Total returns, 8/31/15 to 8/31/16, at net asset value (NAV). Performance shown does not include applicable contingent deferred sales charges (CDSC) or front-end sales charges, which would have reduced performance.

| | | | | |

| Institutional Class Shares | | | | 1.08 | % |

The BofA Merrill Lynch U.S. Treasury Bill Index▼ (Broad Market/Style-Specific Index) | | | | 0.28 | |

| Lipper Ultra Short Obligations Funds Indexn (Peer Group Index) | | | | 1.14 | |

Source(s): ▼Bloomberg L.P.; nLipper Inc. | | | | | |

Market conditions and your Fund

Positive economic growth in the US continued, but at a slightly slower pace than the prior fiscal year. The US economy continued to add jobs, bringing the unemployment rate below 5% while inflation remained subdued.1 Against this backdrop, the Fed raised the federal funds target rate from a range of zero to 0.25% to a range of 0.25% to 0.50% in December 2015.2 The quarter-point increase was the first increase in almost a decade.2 Working against these positive developments, however, were global macroeconomic headwinds in the form of slow global growth and

the potential impact of Brexit – the decision by UK voters to leave the European Union. These risks, coupled with continued low US inflation, limited the Fed to just the one quarter-point hike over the reporting period.

Short-term yields increased primarily due to the Fed’s increase in the fed funds rate. For example, the 12-month US

Treasury bill yielded 0.59% on August 31, 2016, up 21 basis points from a year earlier.3 (A basis point is one one-hundredth of a percentage point.) The three-month US dollar Libor increased 51 basis points to 0.84% over the reporting period.3 However, much of that increase occurred late in the reporting period as money market investors shifted assets from prime money market funds to government money market funds; this resulted in declining demand for Libor-based assets such as certificates of deposit and commercial paper. Looking forward, expectations are that the Fed will raise the federal funds target rate, but at a slower and more methodical pace than the markets thought last year at this time.

During the fiscal year, the Fund’s outperformance versus the broad market/style-specific index was primarily generated by the Fund’s overweight allocation to corporate bonds. The Fund maintained an average allocation to the financials sector of 38% during the fiscal

year. Additional meaningful contributors to the Fund’s performance were our commercial paper holdings, corporate issues, and automobile-related and credit card asset-backed securities. Our positions in student loan asset-backed securities, non-US agencies and investment-grade industrials slightly detracted from relative Fund performance.

We wish to remind you that the Fund is subject to interest rate risk, meaning when interest rates rise, the value of fixed income securities tends to fall. This risk may be greater in the current market environment because interest rates are at or near historic lows. The degree to which the value of fixed income securities may decline due to rising interest rates may vary depending on the speed and magnitude of the increase in interest rates, as well as individual security characteristics such as price, maturity, duration, coupon and market forces such as supply and demand for similar securities. We are monitoring interest rates, and the market, economic and geopolitical factors that may impact the direction, speed and magnitude of changes to interest rates across the maturity spectrum, including the potential impact of monetary policy changes by the Fed and foreign central banks. If interest rates rise, markets may experience increased volatility, which may affect the value and/or liquidity of certain of the Fund’s investments.

Thank you for investing in Invesco Conservative Income Fund.

| 1 | Source: Bureau of Labor Statistics |

| 2 | Source: US Federal Reserve |

| | |

By security type | | % of total net assets |

| | | | | |

Commercial Paper | | | | 43.5 | % |

| U.S. Dollar Denominated | | | | | |

| Bonds and Notes | | | | 21.9 | |

| Asset-Backed Securities | | | | 19.8 | |

| Repurchase Agreements | | | | 6.7 | |

| U.S. Treasury Securities | | | | 2.9 | |

| Certificates of Deposit | | | | 2.2 | |

| Other Assets Less Liabilities | | | | 3.0 | |

| | |

| Top Five Debt Issuers |

| % of total net assets |

| | | | |

| |

| 1. U.S. Treasury | | | 2.9 | % |

| 2. Pentair Finance SA | | | 2.2 | |

| 3. Ford Motor Credit Co. LLC | | | 2.1 | |

4. Sunoco Logistics Partners

Operations LP | | | 2.1 | |

5. Ford Credit Floorplan Master Owner Trust | | | 2.1 | |

| | | | | |

Total Net Assets | | | $ | 104.7 million | |

| |

Total Number of Holdings | | | | 125 | |

The Fund’s holdings are subject to change, and there is no assurance that the Fund will continue to hold any particular security.

Data presented here are as of August 31, 2016.

|

| 4 Invesco Conservative Income Fund |

The views and opinions expressed in management’s discussion of Fund performance are those of Invesco Advisers, Inc. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Invesco Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

See important Fund and, if applicable, index disclosures later in this report.

| | |

| | Laurie Brignac Chartered Financial Analyst, Portfolio Manager, is manager of Invesco Conservative Income |

| Fund. She joined Invesco in 1992. Ms. Brignac earned a BS from Louisiana State University. |

| | |

| | Joseph Madrid Chartered Financial Analyst, Portfolio Manager, is manager of Invesco Conservative Income |

| Fund. He joined Invesco in 2009. Mr. Madrid earned a BA in accounting from Baldwin-Wallace College and an MBA from the University of New Mexico. |

| | |

| | Marques Mercier Portfolio Manager, is manager of Invesco Conservative Income Fund. He joined Invesco in 1994. |

| Mr. Mercier earned a BA in English and an MBA from the University of Houston. |

|

| 5 Invesco Conservative Income Fund |

Your Fund’s Long-Term Performance

Results of a $10,000 Investment – Oldest Share Class(es) since Inception

Fund and index data from 7/1/14

Past performance cannot guarantee comparable future results.

The data shown in the chart include reinvested distributions and Fund expenses including management fees.

Index results include reinvested dividends. Performance of the peer group, if applicable, reflects fund expenses and management fees; performance of a market index does not. Performance

shown in the chart and table(s) does not reflect deduction of taxes a shareholder would pay on Fund distributions or sale of Fund shares.

| | | | |

Average Annual Total Returns | |

As of 8/31/16 | |

| |

| Institutional Class Shares | | | | |

| Inception (7/1/14) | | | 0.66 | % |

| 1 Year | | | 1.08 | |

| | | | |

Average Annual Total Returns | |

| As of 6/30/16, the most recent calendar quarter end | |

| |

| Institutional Class Shares | | | | |

| Inception (7/1/14) | | | 0.64 | % |

| 1 Year | | | 0.91 | |

The performance data quoted represent past performance and cannot guarantee comparable future results; current performance may be lower or higher. Please visit invesco.com/performance for the most recent month-end performance. Performance figures reflect reinvested distributions and changes in net asset value unless otherwise stated. Investment return and principal value will fluctuate so that you may have a gain or loss when you sell shares.

The net annual Fund operating expense ratio set forth in the most recent Fund prospectus as of the date of

this report for Institutional Class shares was 0.28%.1 The total annual Fund operating expense ratio set forth in the most recent Fund prospectus as of the date of this report for Institutional Class shares was 1.02%. The expense ratios presented above may vary from the expense ratios presented in other sections of this report that are based on expenses incurred during the period covered by this report.

Institutional Class shares do not have a front-end sales charge or a CDSC; therefore, performance is at net asset value.

Fund performance reflects any applicable fee waivers and/or expense reimbursements. Had the adviser not waived fees and/or reimbursed expenses currently or in the past, returns would have been lower. See current prospectus for more information.

| 1 | Total annual Fund operating expenses after any contractual fee waivers and/or expense reimbursements by the adviser in effect through at least December 31, 2016. See current prospectus for more information. |

|

| 6 Invesco Conservative Income Fund |

Invesco Conservative Income Fund’s investment objective is to provide capital preservation and current income while maintaining liquidity.

| n | | Unless otherwise stated, information presented in this report is as of August 31, 2016, and is based on total net assets. |

| n | | Unless otherwise noted, all data provided by Invesco. |

| n | | To access your Fund’s reports/prospectus, visit invesco.com/fundreports. |

About share classes

| n | | Institutional Class shares are available to only certain investors. Please see the prospectus for more information. |

Principal risks of investing in the Fund

| n | | Changing fixed income market conditions risk. The current low interest rate environment was created in part by the Federal Reserve Board (FRB) and certain foreign central banks keeping the federal funds and equivalent foreign rates at or near zero. Increases in the federal funds and equivalent foreign rates may expose fixed income markets to heightened volatility and reduced liquidity for certain fixed income investments, particularly those with longer maturities. In addition, decreases in fixed income dealer market-making capacity may also potentially lead to heightened volatility and reduced liquidity in the fixed income markets. As a result, the value of the Fund’s investments and share price may decline. Changes in central bank policies could also result in higher than normal shareholder redemptions, which could potentially increase portfolio turnover and the Fund’s transaction costs. |

| n | | Collateralized loan obligations risk. CLOs are subject to the risks of substantial losses due to actual defaults by underlying borrowers, which will be greater during periods of economic or financial stress. CLOs may also lose value due to collateral defaults and disappearance of subordinate tranches, market anticipation of defaults, and investor aversion to CLO securities as a class. The risks of CLOs will be greater if the Fund invests in CLOs that hold loans of uncreditworthy borrowers or if the Fund holds subordinate tranches of the CLO that absorbs losses from the defaults before senior tranches. In addition, CLOs are subject to interest rate risk and credit risk. |

| n | | Debt securities risk. The prices of debt securities held by the Fund will be affected by changes in interest rates, the creditworthiness of the issuer and other factors. An increase in prevailing interest rates typically causes the value of existing debt securities to fall and often has a greater impact on longer-duration debt securities and higher quality debt securities. Falling interest rates will cause the Fund to reinvest the proceeds of debt securities that have been repaid by the issuer at lower interest rates. Falling interest rates may also reduce the Fund’s distributable income because interest payments on floating rate debt instruments held by the Fund will decline. The Fund could lose money on investments in debt securities if the issuer or borrower fails to meet its obligations to make interest payments and/or to repay principal in a timely manner. Changes in an issuer’s financial strength, the market’s perception of such strength or in the credit rating of the issuer or the security may affect the value of debt securities. The Adviser’s credit analysis may fail to anticipate such changes, which could result in buying a debt security at an inopportune time or failing to sell a debt security in advance of a price decline or other credit event. |

| n | | Derivatives risk. The value of a derivative instrument depends largely on (and is derived from) the value of an underlying security, currency, commodity, interest rate, index or other asset (each referred to as an underlying asset). In addition to risks relating to the underlying assets, the use of derivatives may include other, possibly greater, risks, including counterparty, leverage and liquidity risks. Counterparty risk is the risk that the counterparty to the derivative contract will default on its obligation to pay the Fund the amount owed or otherwise perform under the derivative contract. Derivatives create leverage risk because they do not require payment up |

|

This report must be accompanied or preceded by a currently effective Fund prospectus, which contains more complete information, including sales charges and expenses. Investors should read it carefully before investing. |

|

|

| NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

| | | front equal to the economic exposure created by owning the derivative. As a result, an adverse change in the value of the underlying asset could result in the Fund sustaining a loss that is substantially greater than the amount invested in the derivative, which may make the Fund’s returns more volatile and increase the risk of loss. Derivative instruments may also be less liquid than more traditional investments and the Fund may be unable to sell or close out its derivative positions at a desirable time or price. This risk may be more acute under adverse market conditions, during which the Fund may be most in need of liquidating its derivative positions. Derivatives may also be harder to value, less tax efficient and subject to changing government regulation that could impact the Fund’s ability to use certain derivatives or their cost. Also, derivatives used for hedging or to gain or limit exposure to a particular market segment may not provide the expected benefits, particularly during adverse market conditions. |

| n | | Emerging markets securities risk. Emerging markets (also referred to as developing markets) are generally subject to greater market volatility, political, social and economic instability, uncertain trading markets and more governmental limitations on foreign investment than more developed markets. In addition, companies operating in emerging markets may be subject to lower trading volume and greater price fluctuations than companies in more developed markets. Securities law and the enforcement of systems of taxation in many emerging market countries may change quickly and unpredictably. In addition, investments in emerging markets securities may also be subject to additional transaction costs, delays in settlement procedures, and lack of timely information. |

| n | | Financial services sector risk. The Fund concentrates its investments in the financial services sector. The Fund may be susceptible to adverse economic or regulatory occurrences affecting the financial services sector. Financial services companies are subject to extensive government regulation and are disproportionately affected by unstable interest rates, each of which could adversely |

continued on page 8

|

| 7 Invesco Conservative Income Fund |

continued from page 7

affect the profitability of such companies. Financial services companies may also have concentrated portfolios, which makes them especially vulnerable to unstable economic conditions.

| n | | Foreign government debt risk. Investments in foreign government debt securities (sometimes referred to as sovereign debt securities) involve certain risks in addition to those relating to foreign securities or debt securities generally. The issuer of the debt or the governmental authorities that control the repayment of the debt may be unable or unwilling to repay principal or interest when due in accordance with the terms of such debt, and the Fund may have limited recourse in the event of a default against the defaulting government. Without the approval of debt holders, some governmental debtors have in the past been able to reschedule or restructure their debt payments or declare moratoria on payments. |

| n | | Foreign securities risk. The Fund’s foreign investments may be adversely affected by political and social instability, changes in economic or taxation policies, difficulty in enforcing obligations, decreased liquidity or increased volatility. Foreign investments also involve the risk of the possible seizure, nationalization or expropriation of the issuer or foreign deposits (in which the Fund could lose its entire investments in a certain market) and the possible adoption of foreign governmental restrictions such as exchange controls. Unless the Fund has hedged its foreign securities risk, foreign securities risk also involves the risk of negative foreign currency rate fluctuations, which may cause the value of securities denominated in such foreign currency (or other instruments through which the Fund has exposure to foreign currencies) to decline in value. Currency exchange rates may fluctuate significantly over short periods of time. Currency hedging strategies, if used, are not always successful. |

| n | | Liquidity risk. The Fund may be unable to sell illiquid investments at the time or price it desires and, as a result, could lose its entire investment in such investments. Liquid securities can become illiquid during periods of market stress. If a significant amount of the Fund’s securities become illiquid, the Fund may not be able to timely pay redemption proceeds and may need to sell securities at significantly reduced prices. |

| n | | Management risk. The Fund is actively managed and depends heavily on the Adviser’s judgment about markets, interest rates or the attractiveness, relative values, liquidity, or potential appreciation of particular investments made for the Fund’s portfolio. The Fund could experience losses if these judgments prove to be incorrect. Additionally, legislative, regulatory, or tax developments may adversely affect management of the Fund and, therefore, the ability of the Fund to achieve its investment objective. |

| n | | Market risk. The market values of the Fund’s investments, and therefore the value of the Fund’s shares, will go up and down, sometimes rapidly or unpredictably. Market risk may affect a single issuer, industry or section of the economy, or it may affect the market as a whole. Individual stock prices tend to go up and down more dramatically than those of certain other types of investments, such as bonds. During a general downturn in the financial markets, multiple asset classes may decline in value. When markets perform well, there can be no assurance that specific investments held by the Fund will rise in value. |

| n | | Money market fund risk. The Fund may lose money by investing in money market funds, which seek to preserve the value of an investment at $1.00 per share, because the share price of a money market fund can fall below the $1.00 share price. The Fund’s sponsor has no legal obligation to provide financial support to the Fund. The credit quality of a money market fund’s holdings can change rapidly in certain markets, and the default of a single holding could have an adverse impact on the money market fund’s share price. A money market fund’s share price can also be negatively affected during periods of high redemption pressures, illiquid markets and/or significant market volatility. Furthermore, amendments to money market fund regulations could impact a money market fund’s operations and possibly negatively impact its return. |

| n | | Mortgage- and asset-backed securities risk. Mortgage- and asset-backed securities, including collateralized debt obligations and collateralized mortgage obligations, are subject to prepayment or call risk, which is the risk that a borrower’s payments may be received earlier or later than expected due to changes in prepayment rates on |

| | | underlying loans. This could result in the Fund reinvesting these early payments at lower interest rates, thereby reducing the Fund’s income. Mortgage- and asset-backed securities also are subject to extension risk, which is the risk that an unexpected rise in interest rates could reduce the rate of prepayments, causing the price of the mortgage- and asset-backed securities and the Fund’s share price to fall. An unexpectedly high rate of defaults on the mortgages held by a mortgage pool may adversely affect the value of mortgage-backed securities and could result in losses to the Fund. The Fund may invest in mortgage pools that include subprime mortgages, which are loans made to borrowers with weakened credit histories or with lower capacity to make timely payments on their mortgages. |

| n | | Municipal securities risk. The risk of a municipal obligation generally depends on the financial and credit status of the issuer. Constitutional amendments, legislative enactments, executive orders, administrative regulations, voter initiatives, and the issuer’s regional economic conditions may affect the municipal security’s value, interest payments, repayment of principal and the Fund’s ability to sell the security. Failure of a municipal security issuer to comply with applicable tax requirements may make income paid thereon taxable, resulting in a decline in the security’s value. In addition, there could be changes in applicable tax laws or tax treatments that reduce or eliminate the current federal income tax exemption on municipal securities or otherwise adversely affect the current federal or state tax status of municipal securities. |

| n | | Repurchase agreement risk. The Fund is subject to the risk that the counter-party may default on its obligation to repurchase the underlying instruments collateralizing the repurchase agreement, which may cause the Fund to lose money. These risks are magnified to the extent that a repurchase agreement is secured by securities other than cash or US government securities. |

| n | | TBA transactions risk. TBA transactions involve the risk of loss if the securities received are less favorable than what was anticipated by the Fund when entering into the TBA transaction, or if the counterparty fails to deliver the securities. |

|

| 8 Invesco Conservative Income Fund |

| n | | US government obligations risk. Obligations of US government agencies and authorities receive varying levels of support and may not be backed by the full faith and credit of the US government, which could affect the Fund’s ability to recover should they default. No assurance can be given that the US government will provide financial support to its agencies and authorities if it is not obligated by law to do so. |

| n | | When-issued, delayed delivery and forward commitment risks. When-issued and delayed delivery transactions subject the Fund to market risk because the value or yield of a security at delivery may be more or less than the purchase price or yield generally available when delivery occurs, and counterparty risk because the Fund relies on the buyer or seller, as the case may be, to consummate the transaction. These transactions also have a leveraging effect on the Fund because the Fund commits to purchase securities that it does not have to pay for until a later date, which increases the Fund’s overall investment exposure and, as a result, its volatility. |

| n | | Yield risk. The Fund’s yield will vary as the short-term securities in its portfolio mature or are sold and the proceeds are reinvested in other securities. When interest rates are very low, the Fund’s expenses could absorb all or a portion of the Fund’s income and yield. Additionally, inflation may outpace and diminish investment returns over time. |

| n | | Zero coupon or pay-in-kind securities risk. The value, interest rates, and liquidity of non-cash paying instruments, such as zero coupon and pay-in-kind securities, are subject to greater fluctuation than other types of securities. The higher yields and interest rates on pay-in-kind securities reflect the payment deferral and increased credit risk associated with such instruments and that such investments may represent a higher credit risk than loans that periodically pay interest. |

About indexes used in this report

| n | | The BofA Merrill Lynch U.S. Treasury Bill Index measures total return on cash, including price and interest income, based on short term government Treasury bills. |

| n | | The Lipper Ultra Short Obligations Funds Index is an unmanaged index considered representative of ultra- short funds tracked by Lipper. |

| n | | The Fund is not managed to track the performance of any particular index, including the index(es) described here, and consequently, the performance of the Fund may deviate significantly from the performance of the index(es). |

| n | | A direct investment cannot be made in an index. Unless otherwise indicated, index results include reinvested dividends, and they do not reflect sales charges. Performance of the peer group, if applicable, reflects fund expenses; performance of a market index does not. |

Other information

| n | | The returns shown in management’s discussion of Fund performance are based on net asset values (NAVs) calculated for shareholder transactions. Generally accepted accounting principles require adjustments to be made to the net assets of the Fund at period end for financial reporting purposes, and as such, the NAVs for shareholder transactions and the returns based on those NAVs may differ from the NAVs and returns reported in the Financial Highlights. |

|

| 9 Invesco Conservative Income Fund |

Schedule of Investments

August 31, 2016

| | | | | | | | | | | | | | | | |

| | | Interest

Rate | | | Maturity

Date | | | Principal

Amount

(000) | | | Value | |

Commercial Paper–43.55%(a) | | | | | | | | | | | | | | | | |

| Asset-Backed Securities — Consumer Receivables–1.90% | | | | | | | | | | | | | | | | |

Sheffield Receivables Co. LLC(b) | | | 0.00 | % | | | 02/15/2017 | | | $ | 1,000 | | | $ | 995,945 | |

Thunder Bay Funding LLC(b) | | | 0.00 | % | | | 02/21/2017 | | | | 1,000 | | | | 994,205 | |

| | | | | | | | | | | | | | | | 1,990,150 | |

| | | | |

| Asset-Backed Securities — Fully Supported Bank–6.56% | | | | | | | | | | | | | | | | |

Chesham Finance LLC (Multi-CEP’s)(b) | | | 0.00 | % | | | 04/03/2017 | | | | 1,000 | | | | 992,218 | |

Collateralized Commercial Paper II Co. LLC (CEP-JPMorgan Securities LLC)(b) | | | 0.00 | % | | | 01/05/2017 | | | | 1,000 | | | | 996,352 | |

Institutional Secured Funding Ltd. (Multi-CEP’s)(b) | | | 0.00 | % | | | 11/23/2016 | | | | 700 | | | | 698,587 | |

Halkin Finance LLC (Multi-CEP’s)(b) | | | 0.00 | % | | | 04/03/2017 | | | | 1,200 | | | | 1,190,662 | |

LMA Americas LLC (CEP-Credit Agricole Corporate & Investment Bank S.A.)(b) | | | 0.00 | % | | | 02/02/2017 | | | | 2,000 | | | | 1,990,381 | |

Mountcliff Funding LLC (Multi-CEP’s)(b) | | | 0.00 | % | | | 11/01/2016 | | | | 1,000 | | | | 998,764 | |

| | | | | | | | | | | | | | | | 6,866,964 | |

| | | | |

| Asset-Backed Securities — Multi-Purpose–1.43% | | | | | | | | | | | | | | | | |

CAFCO LLC(b) | | | 0.00 | % | | | 02/03/2017 | | | | 1,500 | | | | 1,493,181 | |

| | | | |

| Brewers–1.42% | | | | | | | | | | | | | | | | |

Anheuser-Busch InBev Worldwide Inc.(b) | | | 0.00 | % | | | 03/13/2017 | | | | 1,497 | | | | 1,489,852 | |

| | | | |

| Consumer Finance–2.13% | | | | | | | | | | | | | | | | |

Ford Motor Credit Co. LLC(b) | | | 0.00 | % | | | 01/03/2017 | | | | 1,000 | | | | 996,469 | |

Ford Motor Credit Co. LLC(b) | | | 0.00 | % | | | 05/04/2017 | | | | 1,250 | | | | 1,238,477 | |

| | | | | | | | | | | | | | | | 2,234,946 | |

| | | | |

| Diversified Banks–6.18% | | | | | | | | | | | | | | | | |

Bank of Nova Scotia (Canada)(b) | | | 0.00 | % | | | 11/01/2016 | | | | 1,000 | | | | 998,962 | |

Bank of Nova Scotia (Canada)(b) | | | 0.00 | % | | | 02/23/2017 | | | | 1,000 | | | | 993,948 | |

BPCE S.A. (France)(b) | | | 0.00 | % | | | 03/03/2017 | | | | 1,000 | | | | 994,086 | |

Credit Suisse AG | | | 0.00 | % | | | 03/01/2017 | | | | 1,000 | | | | 993,236 | |

ING US Funding LLC | | | 0.00 | % | | | 02/13/2017 | | | | 1,000 | | | | 994,647 | |

Natixis | | | 0.00 | % | | | 03/03/2017 | | | | 500 | | | | 496,910 | |

Sumitomo Mitsui Trust Bank Ltd.(b) | | | 0.00 | % | | | 01/13/2017 | | | | 1,000 | | | | 995,969 | |

| | | | | | | | | | | | | | | | 6,467,758 | |

| | | | |

| Electric Utilities–2.58% | | | | | | | | | | | | | | | | |

Electricite de France S.A. (France)(b) | | | 0.00 | % | | | 10/03/2016 | | | | 1,300 | | | | 1,299,095 | |

Electricite de France S.A. (France)(b) | | | 0.00 | % | | | 01/23/2017 | | | | 400 | | | | 398,118 | |

Entergy Corp.(b) | | | 0.00 | % | | | 09/12/2016 | | | | 1,000 | | | | 999,724 | |

| | | | | | | | | | | | | | | | 2,696,937 | |

| | | | |

| Industrial Machinery–2.24% | | | | | | | | | | | | | | | | |

Pentair Finance S.A.(b) | | | 0.00 | % | | | 09/07/2016 | | | | 2,350 | | | | 2,349,582 | |

| | | | |

| Integrated Oil & Gas–2.37% | | | | | | | | | | | | | | | | |

BP Capital Markets PLC (United Kingdom)(b) | | | 0.00 | % | | | 05/11/2017 | | | | 1,000 | | | | 991,771 | |

Chevron Corp.(b) | | | 0.00 | % | | | 06/02/2017 | | | | 1,500 | | | | 1,489,435 | |

| | | | | | | | | | | | | | | | 2,481,206 | |

| | | | |

| Life & Health Insurance–0.24% | | | | | | | | | | | | | | | | |

Prudential PLC (United Kingdom)(b) | | | 0.00 | % | | | 04/24/2017 | | | | 250 | | | | 248,394 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

10 Invesco Conservative Income Fund

| | | | | | | | | | | | | | | | |

| | | Interest

Rate | | | Maturity

Date | | | Principal

Amount

(000) | | | Value | |

| Life Sciences Tools & Services–1.43% | | | | | | | | | | | | | | | | |

Thermo Fisher Scientific Inc.(b) | | | 0.00 | % | | | 10/11/2016 | | | $ | 1,500 | | | $ | 1,498,042 | |

| | | | |

| Managed Health Care–0.33% | | | | | | | | | | | | | | | | |

Humana Inc.(b) | | | 0.00 | % | | | 09/16/2016 | | | | 350 | | | | 349,870 | |

| | | | |

| Movies & Entertainment–0.95% | | | | | | | | | | | | | | | | |

Viacom Inc.(b) | | | 0.00 | % | | | 09/14/2016 | | | | 1,000 | | | | 999,715 | |

| | | | |

| Multi-Utilities–1.19% | | | | | | | | | | | | | | | | |

Engie S.A. (France)(b) | | | 0.00 | % | | | 11/21/2016 | | | | 1,250 | | | | 1,248,480 | |

| | | | |

| Oil & Gas Equipment & Services–0.69% | | | | | | | | | | | | | | | | |

Schlumberger Holdings Corp.(b) | | | 0.00 | % | | | 09/01/2016 | | | | 720 | | | | 719,988 | |

| | | | |

| Oil & Gas Storage & Transportation–4.49% | | | | | | | | | | | | | | | | |

Enbridge Energy Partners L.P.(b) | | | 0.00 | % | | | 09/19/2016 | | | | 1,000 | | | | 999,556 | |

Plains All American Pipeline L.P.(b) | | | 0.00 | % | | | 09/07/2016 | | | | 1,500 | | | | 1,499,791 | |

Sunoco Logistics Partners Operations L.P.(b) | | | 0.00 | % | | | 09/06/2016 | | | | 2,200 | | | | 2,199,702 | |

| | | | | | | | | | | | | | | | 4,699,049 | |

| | | | |

| Other Diversified Financial Services–2.86% | | | | | | | | | | | | | | | | |

AXA Financial Inc.(b) | | | 0.00 | % | | | 01/03/2017 | | | | 1,000 | | | | 996,816 | |

Eni Finance USA Inc.(b) | | | 0.00 | % | | | 11/01/2016 | | | | 1,000 | | | | 998,453 | |

Eni Finance USA Inc.(b) | | | 0.00 | % | | | 01/03/2017 | | | | 1,000 | | | | 996,517 | |

| | | | | | | | | | | | | | | | 2,991,786 | |

| | | | |

| Packaged Foods & Meats–0.96% | | | | | | | | | | | | | | | | |

Mondelez International Inc.(b) | | | 0.00 | % | | | 09/13/2016 | | | | 1,000 | | | | 999,736 | |

| | | | |

| Property & Casualty Insurance–0.95% | | | | | | | | | | | | | | | | |

Suncorp-Metway Ltd. (Australia)(b) | | | 0.00 | % | | | 01/17/2017 | | | | 1,000 | | | | 997,301 | |

| | | | |

| Publishing–1.55% | | | | | | | | | | | | | | | | |

Thomson Reuters Corp.(b) | | | 0.00 | % | | | 09/06/2016 | | | | 1,625 | | | | 1,624,834 | |

| | | | |

| Regional Banks–0.81% | | | | | | | | | | | | | | | | |

Bank of Tokyo-Mitsubishi UFJ, Ltd. (The) | | | 0.00 | % | | | 02/14/2017 | | | | 850 | | | | 845,574 | |

| | | | |

| Soft Drinks–0.29% | | | | | | | | | | | | | | | | |

Coca-Cola Co. (The)(b) | | | 0.00 | % | | | 01/05/2017 | | | | 300 | | | | 299,438 | |

Total Commercial Paper (Cost $45,579,037) | | | | | | | | | | | | | | | 45,592,783 | |

| | | | |

Bonds & Notes–21.88%(c) | | | | | | | | | | | | | | | | |

| Automobile Manufacturers–1.64% | | | | | | | | | | | | | | | | |

Daimler Finance North America LLC, Sr. Unsec. Gtd. Notes(b) | | | 1.50 | % | | | 07/05/2019 | | | | 1,000 | | | | 995,396 | |

Hyundai Capital America, Sr. Unsec. Gtd. Notes(b) | | | 4.00 | % | | | 06/08/2017 | | | | 235 | | | | 239,738 | |

Toyota Motor Credit Corp., Sr. Unsec. Medium-Term Global Notes | | | 1.25 | % | | | 10/05/2017 | | | | 179 | | | | 179,253 | |

Volkswagen Group of America Finance LLC, Sr. Unsec. Gtd. Floating Rate Notes(b)(d) | | | 1.09 | % | | | 11/22/2016 | | | | 300 | | | | 299,720 | |

| | | | | | | | | | | | | | | | 1,714,107 | |

| | | | |

| Biotechnology–0.16% | | | | | | | | | | | | | | | | |

AbbVie Inc., Sr. Unsec. Global Notes | | | 1.80 | % | | | 05/14/2018 | | | | 164 | | | | 164,870 | |

| | | | |

| Brewers–0.19% | | | | | | | | | | | | | | | | |

Molson Coors Brewing Co., Sr. Unsec. Gtd. Global Notes | | | 1.45 | % | | | 07/15/2019 | | | | 201 | | | | 200,848 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

11 Invesco Conservative Income Fund

| | | | | | | | | | | | | | | | |

| | | Interest

Rate | | | Maturity

Date | | | Principal

Amount

(000) | | | Value | |

| Consumer Finance–1.15% | | | | | | | | | | | | | | | | |

American Express Credit Corp., Series 0000, Sr. Unsec. Medium-Term Floating Rate Notes(d) | | | 0.95 | % | | | 09/22/2017 | | | $ | 200 | | | $ | 199,825 | |

Capital One Bank (USA), N.A., Sr. Unsec. Notes | | | 1.20 | % | | | 02/13/2017 | | | | 1,000 | | | | 1,000,052 | |

| | | | | | | | | | | | | | | | 1,199,877 | |

| | | | |

| Diversified Banks–8.80% | | | | | | | | | | | | | | | | |

ABN AMRO Bank N.V. (Netherlands), Sr. Unsec. Floating Rate Notes(b)(d) | | | 1.54 | % | | | 10/28/2016 | | | | 300 | | | | 300,384 | |

Australia & New Zealand Banking Group Ltd. (Australia), | | | | | | | | | | | | | | | | |

Sr. Unsec. Medium-Term Global Notes | | | 1.45 | % | | | 05/15/2018 | | | | 1,000 | | | | 1,000,239 | |

Sr. Unsec. Medium-Term Global Notes | | | 1.50 | % | | | 01/16/2018 | | | | 350 | | | | 351,245 | |

Bank of Montreal (Canada), Sr. Unsec. Floating Rate Global Notes(d) | | | 1.02 | % | | | 04/10/2018 | | | | 250 | | | | 249,200 | |

Bank of Tokyo-Mitsubishi UFJ, Ltd. (The), Sr. Unsec. Notes(b) | | | 1.70 | % | | | 03/05/2018 | | | | 650 | | | | 651,051 | |

Barclays Bank PLC (United Kingdom), Series 1, Sr. Unsec. Medium-Term Global Notes | | | 5.00 | % | | | 09/22/2016 | | | | 1,000 | | | | 1,001,931 | |

Mizuho Bank Ltd. (Japan), Sr. Unsec. Gtd. Floating Rate Notes(b)(d) | | | 1.09 | % | | | 09/25/2017 | | | | 250 | | | | 249,747 | |

Mizuho Securities USA Inc., Sr. Unsec Medium-Term Floating Rate Notes(b)(d) | | | 1.03 | % | | | 12/21/2016 | | | | 1,000 | | | | 999,985 | |

National Australia Bank Ltd. (Australia), Sr. Unsec. Medium-Term Global Notes | | | 2.00 | % | | | 01/14/2019 | | | | 300 | | | | 303,095 | |

Royal Bank of Canada (Canada), | | | | | | | | | | | | | | | | |

Sr. Unsec. Global Notes | | | 1.50 | % | | | 07/29/2019 | | | | 1,000 | | | | 999,093 | |

Sr. Unsec. Medium-Term Floating Rate Global Notes(d) | | | 1.12 | % | | | 09/09/2016 | | | | 300 | | | | 300,015 | |

Swedbank AB (Sweden), Sr. Unsec. Notes(b) | | | 2.13 | % | | | 09/29/2017 | | | | 500 | | | | 503,891 | |

Toronto-Dominion Bank (The) (Canada), Sr. Unsec. Medium-Term Notes | | | 1.40 | % | | | 04/30/2018 | | | | 1,000 | | | | 1,002,514 | |

U.S. Bank, N.A., Sr. Unsec. Global Notes | | | 1.40 | % | | | 04/26/2019 | | | | 1,000 | | | | 1,002,272 | |

Wells Fargo Bank, N.A., Sr. Unsec. Medium-Term Notes | | | 1.65 | % | | | 01/22/2018 | | | | 300 | | | | 301,868 | |

| | | | | | | | | | | | | | | | 9,216,530 | |

| | | | |

| Electric Utilities–0.96% | | | | | | | | | | | | | | | | |

Southern Power Co., Sr. Unsec. Global Notes | | | 1.85 | % | | | 12/01/2017 | | | | 1,000 | | | | 1,007,080 | |

| | | | |

| Health Care Equipment–0.46% | | | | | | | | | | | | | | | | |

Stryker Corp., Sr. Unsec. Global Notes | | | 2.00 | % | | | 03/08/2019 | | | | 476 | | | | 482,337 | |

| | | | |

| Integrated Oil & Gas–0.66% | | | | | | | | | | | | | | | | |

Exxon Mobil Corp., Sr. Unsec. Global Notes | | | 1.44 | % | | | 03/01/2018 | | | | 438 | | | | 440,682 | |

Shell International Finance B.V. (Netherlands), Sr. Unsec. Gtd. Floating Rate Global Notes(d) | | | 1.13 | % | | | 05/10/2017 | | | | 250 | | | | 250,342 | |

| | | | | | | | | | | | | | | | 691,024 | |

| | | | |

| Integrated Telecommunication Services–0.96% | | | | | | | | | | | | | | | | |

Verizon Communications Inc., Sr. Unsec. Global Notes | | | 1.35 | % | | | 06/09/2017 | | | | 1,000 | | | | 1,002,027 | |

| | | | |

| IT Consulting & Other Services–0.29% | | | | | | | | | | | | | | | | |

International Business Machines Corp., Sr. Unsec. Floating Rate Global Notes(d) | | | 1.25 | % | | | 08/18/2017 | | | | 300 | | | | 301,152 | |

| | | | |

| Life & Health Insurance–0.24% | | | | | | | | | | | | | | | | |

Pricoa Global Funding I, Sec. Notes(b) | | | 1.15 | % | | | 11/25/2016 | | | | 250 | | | | 250,177 | |

| | | | |

| Managed Health Care–1.24% | | | | | | | | | | | | | | | | |

Aetna Inc., Sr. Unsec. Global Notes | | | 1.75 | % | | | 05/15/2017 | | | | 1,000 | | | | 1,003,063 | |

UnitedHealth Group Inc., Sr. Unsec. Floating Rate Global Notes(d) | | | 1.13 | % | | | 01/17/2017 | | | | 300 | | | | 300,359 | |

| | | | | | | | | | | | | | | | 1,303,422 | |

| | | | |

| Motorcycle Manufacturers–0.29% | | | | | | | | | | | | | | | | |

Harley-Davidson Financial Services, Inc., Sr. Unsec. Gtd. Notes(b) | | | 2.25 | % | | | 01/15/2019 | | | | 300 | | | | 305,844 | |

| | | | |

| Multi-Utilities–0.96% | | | | | | | | | | | | | | | | |

Dominion Resources, Inc., Series B, Sr. Unsec. Global Notes | | | 1.60 | % | | | 08/15/2019 | | | | 1,000 | | | | 1,000,942 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

12 Invesco Conservative Income Fund

| | | | | | | | | | | | | | | | |

| | | Interest

Rate | | | Maturity

Date | | | Principal

Amount

(000) | | | Value | |

| Pharmaceuticals–1.19% | | | | | | | | | | | | | | | | |

Actavis Funding SCS, Sr. Unsec. Gtd. Global Notes | | | 1.85 | % | | | 03/01/2017 | | | $ | 250 | | | $ | 250,652 | |

Teva Pharmaceutical Finance Netherlands III B.V., Sr. Unsec. Gtd. Global Notes | | | 1.40 | % | | | 07/20/2018 | | | | 1,000 | | | | 998,474 | |

| | | | | | | | | | | | | | | | 1,249,126 | |

| | | | |

| Regional Banks–2.14% | | | | | | | | | | | | | | | | |

Branch Banking & Trust Co., Unsec. Sub. Global Notes | | | 5.63 | % | | | 09/15/2016 | | | | 673 | | | | 673,802 | |

Macquarie Bank Ltd. (Australia), | | | | | | | | | | | | | | | | |

Sr. Unsec. Floating Rate Notes(b)(d) | | | 1.36 | % | | | 10/27/2017 | | | | 250 | | | | 249,747 | |

Sr. Unsec. Notes(b) | | | 2.35 | % | | | 01/15/2019 | | | | 300 | | | | 303,117 | |

PNC Bank, N.A., Sr. Unsec. Notes | | | 1.95 | % | | | 03/04/2019 | | | | 1,000 | | | | 1,013,634 | |

| | | | | | | | | | | | | | | | 2,240,300 | |

| | | | |

| Specialized Finance–0.21% | | | | | | | | | | | | | | | | |

International Lease Finance Corp., Sr. Sec. Gtd. Notes(b) | | | 6.75 | % | | | 09/01/2016 | | | | 225 | | | | 225,309 | |

| | | | |

| Technology Hardware, Storage & Peripherals–0.34% | | | | | | | | | | | | | | | | |

Apple Inc., Sr. Unsec. Global Notes | | | 1.30 | % | | | 02/23/2018 | | | | 350 | | | | 351,851 | |

Total Bonds & Notes (Cost $22,834,096) | | | | | | | | | | | | | | | 22,906,823 | |

| | | | |

Asset-Backed Securities–19.81% | | | | | | | | | | | | | | | | |

| Auto Loans/Leases–8.26% | | | | | | | | | | | | | | | | |

Ally Auto Receivables Trust, Series 2015-1, Class A3, Pass Through Ctfs. | | | 1.39 | % | | | 09/16/2019 | | | | 1,000 | | | | 1,002,258 | |

BMW Vehicle Lease Trust, Series 2014-1, Class A4, Pass Through Ctfs. | | | 0.99 | % | | | 08/21/2017 | | | | 166 | | | | 165,633 | |

CarMax Auto Owner Trust, Series 2014-4, Class A3, Pass Through Ctfs. | | | 1.25 | % | | | 11/15/2019 | | | | 868 | | | | 868,985 | |

Enterprise Fleet Financing LLC, Series 2014-2, Class A2 , Pass Through Ctfs.(b) | | | 1.05 | % | | | 03/20/2020 | | | | 1,220 | | | | 1,217,325 | |

Ford Credit Auto Owner Trust, Series 2016-A, Class A3, Pass Through Ctfs. | | | 1.39 | % | | | 07/15/2020 | | | | 450 | | | | 451,346 | |

Ford Credit Floorplan Master Owner Trust, Series 2012-2, Class A, Pass Through Ctfs. | | | 1.92 | % | | | 01/15/2019 | | | | 2,173 | | | | 2,179,591 | |

Huntington Auto Trust, Series 2015-1, Class A3, Pass Through Ctfs. | | | 1.24 | % | | | 09/16/2019 | | | | 750 | | | | 750,479 | |

Mercedes-Benz Auto Lease Trust, Series 2016-A, Class A2A, Pass Through Ctfs. | | | 1.34 | % | | | 07/16/2018 | | | | 1,000 | | | | 1,001,054 | |

NextGear Floorplan Master Owner Trust, | | | | | | | | | | | | | | | | |

Series 2015-1A, Class A, Pass Through Ctfs.(b) | | | 1.80 | % | | | 07/15/2019 | | | | 250 | | | | 249,323 | |

Series 2015-2A, Class A, Pass Through Ctfs.(b) | | | 2.38 | % | | | 10/15/2020 | | | | 250 | | | | 249,329 | |

Nissan Auto Receivables Owner Trust, Series 2016-A, Class A2A, Pass Through Ctfs. | | | 1.06 | % | | | 02/15/2019 | | | | 300 | | | | 300,111 | |

Nissan Master Owner Trust Receivables, Series 2015-A, Class A1, Floating Rate Pass Through Ctfs.(d) | | | 0.91 | % | | | 01/15/2020 | | | | 210 | | | | 210,195 | |

| | | | | | | | | | | | | | | | 8,645,629 | |

| | | | |

| Credit Cards–6.32% | | | | | | | | | | | | | | | | |

Cabela’s Credit Card Master Note Trust, Series 2011-4A, Class A2, Floating Rate Pass Through Ctfs.(b)(d) | | | 1.06 | % | | | 10/15/2019 | | | | 400 | | | | 400,167 | |

Chase Issuance Trust, | | | | | | | | | | | | | | | | |

Series 2013-A1, Class A1, Pass Through Ctfs. | | | 1.30 | % | | | 02/18/2020 | | | | 300 | | | | 300,774 | |

Series 2014-A7, Class A7, Pass Through Ctfs. | | | 1.38 | % | | | 11/15/2019 | | | | 1,382 | | | | 1,386,223 | |

Discover Card Execution Note Trust, Series 2013-A5, Class A5, Pass Through Ctfs. | | | 1.04 | % | | | 04/15/2019 | | | | 200 | | | | 200,013 | |

First National Master Note Trust, Series 2015-1, Class A, Floating Rate Pass Through Ctfs.(d) | | | 1.28 | % | | | 09/15/2020 | | | | 250 | | | | 250,953 | |

Golden Credit Card Trust (Canada), | | | | | | | | | | | | | | | | |

Series 2012-2A, Class A1, Pass Through Ctfs.(b) | | | 1.77 | % | | | 01/15/2019 | | | | 1,100 | | | | 1,102,360 | |

Series 2013-2A, Class A, Floating Rate Pass Through Ctfs.(b)(d) | | | 0.94 | % | | | 09/15/2018 | | | | 100 | | | | 100,005 | |

Synchrony Credit Card Master Note Trust, Series 2014-1, Class A, Pass Through Ctfs. | | | 1.61 | % | | | 11/15/2020 | | | | 1,000 | | | | 1,004,416 | |

World Financial Network Credit Card Master Trust, | | | | | | | | | | | | | | | | |

Series 2012-B, Class A, Pass Through Ctfs. | | | 1.76 | % | | | 05/17/2021 | | | | 875 | | | | 879,721 | |

Series 2015-C, Class A, Pass Through Ctfs. | | | 1.26 | % | | | 03/15/2021 | | | | 990 | | | | 991,127 | |

| | | | | | | | | | | | | | | | 6,615,759 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

13 Invesco Conservative Income Fund

| | | | | | | | | | | | | | | | |

| | | Interest

Rate | | | Maturity

Date | | | Principal

Amount

(000) | | | Value | |

| Equipment Leasing–2.47% | | | | | | | | | | | | | | | | |

Kubota Credit Owner Trust, Series 2016-1A, Class A2, Pass Through Ctfs.(b) | | | 1.25 | % | | | 04/15/2019 | | | $ | 1,000 | | | $ | 1,000,107 | |

MMAF Equipment Finance LLC, | | | | | | | | | | | | | | | | |

Series 2015-AA, Class A2, Pass Through Ctfs.(b) | | | 0.96 | % | | | 09/18/2017 | | | | 96 | | | | 95,958 | |

Series 2016-AA, Class A2, Pass Through Ctfs.(b) | | | 1.39 | % | | | 12/17/2018 | | | | 1,500 | | | | 1,498,453 | |

| | | | | | | | | | | | | | | | 2,594,518 | |

| | | | |

| Loans–2.29% | | | | | | | | | | | | | | | | |

Ally Master Owner Trust, Series 2014-5, Class A2, Pass Through Ctfs. | | | 1.60 | % | | | 10/15/2019 | | | | 570 | | | | 571,512 | |

CNH Equipment Trust, Series 2016-B, Class A2A, Pass Through Ctfs. | | | 1.31 | % | | | 10/15/2019 | | | | 1,000 | | | | 1,000,653 | |

John Deere Owner Trust, Series 2015-A, Class A3, Pass Through Ctfs. | | | 1.32 | % | | | 06/17/2019 | | | | 825 | | | | 827,096 | |

| | | | | | | | | | | | | | | | 2,399,261 | |

| | | | |

| Student Loans–0.25% | | | | | | | | | | | | | | | | |

SLM Student Loan Trust, | | | | | | | | | | | | | | | | |

Series 2003-14, Class A5, Floating Rate Pass Through Ctfs.(d) | | | 0.94 | % | | | 01/25/2023 | | | | 190 | | | | 189,063 | |

Series 2004-7, Class A5, Floating Rate Pass Through Ctfs.(d) | | | 0.88 | % | | | 01/27/2020 | | | | 73 | | | | 72,635 | |

| | | | | | | | | | | | | | | | 261,698 | |

| | | | |

| Time Shares–0.22% | | | | | | | | | | | | | | | | |

Sierra Timeshare Receivables Funding LLC, | | | | | | | | | | | | | | | | |

Series 2012-3A, Class A, Pass Through Ctfs.(b) | | | 1.87 | % | | | 08/20/2029 | | | | 100 | | | | 99,037 | |

Series 2013-3A, Class A, Pass Through Ctfs.(b) | | | 0.00 | % | | | 10/20/2030 | | | | 127 | | | | 127,266 | |

| | | | | | | | | | | | | | | | 226,303 | |

Total Asset-Backed Securities (Cost $20,719,234) | | | | | | | | | | | | | | | 20,743,168 | |

| | | | |

U.S. Treasury Bills–2.86%(a) | | | | | | | | | | | | | | | | |

U.S. Treasury Bills | | | 0.38 | % | | | 01/12/2017 | | | | 1,000 | | | | 998,701 | |

U.S. Treasury Bills | | | 0.58 | % | | | 04/27/2017 | | | | 1,000 | | | | 997,039 | |

U.S. Treasury Bills | | | 0.41 | % | | | 06/22/2017 | | | | 1,000 | | | | 996,207 | |

Total U.S. Treasury Bills (Cost $2,991,456) | | | | | | | | | | | | | | | 2,991,947 | |

| | | | |

Certificates of Deposit–2.25% | | | | | | | | | | | | | | | | |

| Diversified Banks–1.29% | | | | | | | | | | | | | | | | |

Canadian Imperial Bank of Commerce | | | 1.24 | % | | | 03/03/2017 | | | | 1,000 | | | | 1,000,314 | |

Credit Suisse AG(d) | | | 1.02 | % | | | 09/21/2016 | | | | 350 | | | | 350,116 | |

| | | | | | | | | | | | | | | | 1,350,430 | |

| | | | |

| Diversified Capital Markets–0.96% | | | | | | | | | | | | | | | | |

UBS AG | | | 1.15 | % | | | 02/01/2017 | | | | 1,000 | | | | 1,000,405 | |

Total Certificates of Deposit (Cost $2,350,000) | | | | | | | | | | | | | | | 2,350,835 | |

TOTAL INVESTMENTS (excluding Repurchase Agreements)–90.35% (Cost $94,473,823) | | | | | | | | | | | | | | | 94,585,556 | |

| | | | |

| | | | | | | | | Repurchase

Amount | | | | |

Repurchase Agreements–6.68%(e) | | | | | | | | | | | | | | | | |

Citigroup Global Markets Inc., term agreement dated 12/03/2015, maturing value of $1,000,000 (collateralized by a foreign corporate obligation valued at $1,020,000; 7.50%, 04/22/2026)(d) | | | 0.90 | % | | | 12/02/2016 | | | | 1,000,000 | | | | 1,000,000 | |

J.P. Morgan Securities Inc., open agreement dated 07/20/2016, (collateralized by domestic non-agency mortgage-backed securities valued at $2,200,262; 1.50%-2.28%, 08/25/2035-09/25/2046)(f) | | | 1.20 | % | | | — | | | | — | | | | 2,000,000 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

14 Invesco Conservative Income Fund

| | | | | | | | | | | | | | | | |

| | | Interest

Rate | | | Maturity

Date | | | Repurchase

Amount | | | Value | |

Merrill Lynch, Pierce, Fenner & Smith, Inc., term agreement dated 08/31/2016, maturing value of $4,003,694 (collateralized by a domestic non-agency mortgage-backed security valued at $4,400,001; 0%, 08/10/2045) | | | 0.95 | % | | | 10/05/2016 | | | $ | 4,003,694 | | | $ | 4,000,000 | |

Total Repurchase Agreements (Cost $7,000,000) | | | | | | | | | | | | | | | 7,000,000 | |

TOTAL INVESTMENTS–97.03% (Cost $101,473,823) | | | | | | | | | | | | | | | 101,585,556 | |

OTHER ASSETS LESS LIABILITIES–2.97% | | | | | | | | | | | | | | | 3,106,717 | |

NET ASSETS–100.00% | | | | | | | | | | | | | | $ | 104,692,273 | |

Investment Abbreviations:

| | |

| CEP | | – Credit Enhancement Provider |

| Ctfs. | | – Certificates |

| Gtd. | | – Guaranteed |

| Sec. | | – Secured |

| Sr. | | – Senior |

| Sub. | | – Subordinated |

| Unsec. | | – Unsecured |

Notes to Schedule of Investments:

| (a) | Securities may be traded on a discount basis. The interest rate shown represents the discount rate at the time of purchase by the Fund. |

| (b) | Security purchased or received in a transaction exempt from registration under the Securities Act of 1933, as amended (the “1933 Act”). The security may be resold pursuant to an exemption from registration under the 1933 Act, typically to qualified institutional buyers. The aggregate value of these securities at August 31, 2016 was $53,975,852, which represented 51.56% of the Fund’s Net Assets. |

| (c) | Industry and/or sector classifications used in this report are generally according to the Global Industry Classification Standard, which was developed by and is the exclusive property and a service mark of MSCI Inc. and Standard & Poor’s. |

| (d) | Interest or dividend rate is redetermined periodically. Rate shown is the rate in effect on August 31, 2016. |

| (e) | Principal amount equals value at period end. See Note 1H. |

| (f) | Either party may terminate the agreement upon demand. Interest rates, principal amount and collateral are redetermined daily. |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

15 Invesco Conservative Income Fund

Statement of Assets and Liabilities

August 31, 2016

| | | | |

Assets: | | | | |

Investments, at value (Cost $94,473,823) | | $ | 94,585,556 | |

Repurchase agreements, at value and cost | | | 7,000,000 | |

Total investments, at value (Cost $101,473,823) | | | 101,585,556 | |

Cash | | | 91,042 | |

Receivable for: | | | | |

Fund shares sold | | | 3,000,000 | |

Interest | | | 140,005 | |

Fund expenses absorbed | | | 2,756 | |

Other assets | | | 10,900 | |

Total assets | | | 104,830,259 | |

| |

Liabilities: | | | | |

Payable for: | | | | |

Fund shares reacquired | | | 30 | |

Dividends | | | 82,729 | |

Accrued fees to affiliates | | | 794 | |

Accrued trustees’ and officers’ fees and benefits | | | 3,077 | |

Accrued other operating expenses | | | 51,356 | |

Total liabilities | | | 137,986 | |

Net assets applicable to shares outstanding | | $ | 104,692,273 | |

| | | | |

Net assets consist of: | | | | |

Shares of beneficial interest | | $ | 104,561,809 | |

Undistributed net investment income | | | 959 | |

Undistributed net realized gain | | | 17,772 | |

Net unrealized appreciation | | | 111,733 | |

| | | $ | 104,692,273 | |

|

Shares outstanding, $0.01 par value per share,

with an unlimited number of shares authorized: | |

Institutional Class | | | 10,450,452 | |

Institutional Class: | | | | |

Net asset value and offering price per share | | $ | 10.02 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

16 Invesco Conservative Income Fund

Statement of Operations

For the year ended August 31, 2016

| | | | |

Investment income: | |

Interest | | $ | 648,686 | |

| |

Expenses: | | | | |

Advisory fees | | | 140,955 | |

Administrative services fees | | | 50,000 | |

Custodian fees | | | 7,896 | |

Transfer agent fees | | | 5,074 | |

Trustees’ and officers’ fees and benefits | | | 17,271 | |

Registration and filing fees | | | 33,929 | |

Reports to shareholders | | | 9,816 | |

Professional services fees | | | 57,755 | |

Other | | | 11,490 | |

Total expenses | | | 334,186 | |

Less: Fees waived and expenses reimbursed | | | (176,317 | ) |

Net expenses | | | 157,869 | |

Net investment income | | | 490,817 | |

| |

Realized and unrealized gain from: | | | | |

Net realized gain from investment securities | | | 17,772 | |

Change in net unrealized appreciation of investment securities | | | 125,926 | |

Net realized and unrealized gain | | | 143,698 | |

Net increase in net assets resulting from operations | | $ | 634,515 | |

See accompanying Notes to Financial Statements which are an integral part of the financial statements.

17 Invesco Conservative Income Fund

Statement of Changes in Net Assets

For the years ended August 31, 2016 and 2015

| | | | | | | | |

| | | 2016 | | | 2015 | |

Operations: | |

Net investment income | | $ | 490,817 | | | $ | 105,583 | |

Net realized gain | | | 17,772 | | | | 1,415 | |

Change in net unrealized appreciation (depreciation) | | | 125,926 | | | | (21,235 | ) |

Net increase in net assets resulting from operations | | | 634,515 | | | | 85,763 | |

Distributions to shareholders from net investment income | | | (490,935 | ) | | | (105,585 | ) |

|

Share transactions–net: | |

Net increase in net assets resulting from share transactions | | | 79,561,809 | | | | — | |

Net increase (decrease) in net assets | | | 79,705,389 | | | | (19,822 | ) |

|

Net assets: | |

Beginning of year | | | 24,986,884 | | | | 25,006,706 | |

End of year (includes undistributed net investment income of $959 and $118, respectively) | | $ | 104,692,273 | | | $ | 24,986,884 | |

Notes to Financial Statements

August 31, 2016

NOTE 1—Significant Accounting Policies

Invesco Conservative Income Fund (the “Fund”) is a series portfolio of Invesco Management Trust (the “Trust”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end series management investment company consisting of one portfolio authorized to issue an unlimited number of shares of beneficial interest. The assets, liabilities and operations of the portfolio are accounted for separately. Matters affecting the portfolio or class will be voted on exclusively by the shareholders of the portfolio or class.

The Fund’s investment objective is to provide capital preservation and current income while maintaining liquidity.

The Fund currently consists of one class of shares, Institutional Class. Institutional Class shares are sold at net asset value.

The following is a summary of the significant accounting policies followed by the Fund in the preparation of its financial statements.

| A. | Security Valuations — Securities, including restricted securities, are valued according to the following policy. |

Debt obligations (including convertible securities) and unlisted equities are fair valued using an evaluated quote provided by an independent pricing service. Evaluated quotes provided by the pricing service may be determined without exclusive reliance on quoted prices, and may reflect appropriate factors such as institution-size trading in similar groups of securities, developments related to specific securities, dividend rate (for unlisted equities), yield (for debt obligations), quality, type of issue, coupon rate (for debt obligations), maturity (for debt obligations), individual trading characteristics and other market data. Debt obligations are subject to interest rate and credit risks. In addition, all debt obligations involve some risk of default with respect to interest and/or principal payments.

A security listed or traded on an exchange (except convertible securities) is valued at its last sales price or official closing price as of the close of the customary trading session on the exchange where the security is principally traded, or lacking any sales or official closing price on a particular day, the security may be valued at the closing bid price on that day. Securities traded in the over-the-counter market are valued based on prices furnished by independent pricing services or market makers. When such securities are valued by an independent pricing service they may be considered fair valued. Futures contracts are valued at the final settlement price set by an exchange on which they are principally traded. Listed options are valued at the mean between the last bid and asked prices from the exchange on which they are principally traded. Options not listed on an exchange are valued by an independent source at the mean between the last bid and asked prices. For purposes of determining net asset value (“NAV”) per share, futures and option contracts generally are valued 15 minutes after the close of the customary trading session of the New York Stock Exchange (“NYSE”).

Investments in open-end and closed-end registered investment companies that do not trade on an exchange are valued at the end-of-day net asset value per share. Investments in open-end and closed-end registered investment companies that trade on an exchange are valued at the last sales price or official closing price as of the close of the customary trading session on the exchange where the security is principally traded.

Foreign securities’ (including foreign exchange contracts) prices are converted into U.S. dollar amounts using the applicable exchange rates as of the close of the NYSE. If market quotations are available and reliable for foreign exchange-traded equity securities, the securities will be valued at the market quotations. Because trading hours for certain foreign securities end before the close of the NYSE, closing market quotations may become unreliable. If between the time trading ends on a particular security and the close of the customary trading session on the NYSE, events occur that the Adviser determines are significant and make the closing price unreliable, the Fund may fair value the security. If the event is likely to have affected the closing price of the security, the security will be valued at fair value in good faith using procedures approved by the Board of Trustees. Adjustments to closing prices to reflect fair value may also be based on a screening process of an independent pricing service to indicate the degree of certainty, based on historical data, that the closing price in the principal market where a foreign security trades is not the current value as of the close of the NYSE. Foreign securities’ prices meeting the approved degree of certainty that the price is not reflective of current value will be priced at the indication of fair value from the independent pricing service. Multiple factors may be considered by the independent pricing service in determining adjustments to reflect fair value and may include information relating to sector indices, American

18 Invesco Conservative Income Fund

Depositary Receipts and domestic and foreign index futures. Foreign securities may have additional risks including exchange rate changes, potential for sharply devalued currencies and high inflation, political and economic upheaval, the relative lack of issuer information, relatively low market liquidity and the potential lack of strict financial and accounting controls and standards.

Securities for which market prices are not provided by any of the above methods may be valued based upon quotes furnished by independent sources. The last bid price may be used to value equity securities. The mean between the last bid and asked prices is used to value debt obligations, including corporate loans.

Securities for which market quotations are not readily available or became unreliable are valued at fair value as determined in good faith by or under the supervision of the Trust’s officers following procedures approved by the Board of Trustees. Issuer specific events, market trends, bid/asked quotes of brokers and information providers and other market data may be reviewed in the course of making a good faith determination of a security’s fair value.

The Fund may invest in securities that are subject to interest rate risk, meaning the risk that the prices will generally fall as interest rates rise and, conversely, the prices will generally rise as interest rates fall. Specific securities differ in their sensitivity to changes in interest rates depending on their individual characteristics. Changes in interest rates may result in increased market volatility, which may affect the value and/or liquidity of certain Fund investments.

Valuations change in response to many factors including the historical and prospective earnings of the issuer, the value of the issuer’s assets, general economic conditions, interest rates, investor perceptions and market liquidity. Because of the inherent uncertainties of valuation, the values reflected in the financial statements may materially differ from the value received upon actual sale of those investments.

| B. | Securities Transactions and Investment Income — Securities transactions are accounted for on a trade date basis. Realized gains or losses on sales are computed on the basis of specific identification of the securities sold. Interest income (net of withholding tax, if any) is recorded on the accrual basis from settlement date. Dividend income (net of withholding tax, if any) is recorded on the ex-dividend date. Bond premiums and discounts are amortized and/or accreted for financial reporting purposes. |

The Fund may periodically participate in litigation related to Fund investments. As such, the Fund may receive proceeds from litigation settlements. Any proceeds received are included in the Statement of Operations as realized gain (loss) for investments no longer held and as unrealized gain (loss) for investments still held.

Brokerage commissions and mark ups are considered transaction costs and are recorded as an increase to the cost basis of securities purchased and/or a reduction of proceeds on a sale of securities. Such transaction costs are included in the determination of net realized and unrealized gain (loss) from investment securities reported in the Statement of Operations and the Statement of Changes in Net Assets and the net realized and unrealized gains (losses) on securities per share in the Financial Highlights. Transaction costs are included in the calculation of the Fund’s net asset value and, accordingly, they reduce the Fund’s total returns. These transaction costs are not considered operating expenses and are not reflected in net investment income reported in the Statement of Operations and the Statement of Changes in Net Assets, or the net investment income per share and the ratios of expenses and net investment income reported in the Financial Highlights, nor are they limited by any expense limitation arrangements between the Fund and the investment adviser.

| C. | Country Determination — For the purposes of making investment selection decisions and presentation in the Schedule of Investments, the investment adviser may determine the country in which an issuer is located and/or credit risk exposure based on various factors. These factors include the laws of the country under which the issuer is organized, where the issuer maintains a principal office, the country in which the issuer derives 50% or more of its total revenues and the country that has the primary market for the issuer’s securities, as well as other criteria. Among the other criteria that may be evaluated for making this determination are the country in which the issuer maintains 50% or more of its assets, the type of security, financial guarantees and enhancements, the nature of the collateral and the sponsor organization. Country of issuer and/or credit risk exposure has been determined to be the United States of America, unless otherwise noted. |

| D. | Distributions — Distributions from net investment income, if any, are declared daily and paid monthly. Distributions from net realized capital gain, if any, are generally declared and paid annually and recorded on the ex-dividend date. The Fund may elect to treat a portion of the proceeds from redemptions as distributions for federal income tax purposes. |

| E. | Federal Income Taxes — The Fund intends to comply with the requirements of Subchapter M of the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), necessary to qualify as a regulated investment company and to distribute substantially all of the Fund’s taxable earnings to shareholders. As such, the Fund will not be subject to federal income taxes on otherwise taxable income (including net realized capital gain) that is distributed to shareholders. Therefore, no provision for federal income taxes is recorded in the financial statements. |

The Fund recognizes the tax benefits of uncertain tax positions only when the position is more likely than not to be sustained. Management has analyzed the Fund’s uncertain tax positions and concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions. Management is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next 12 months.

The Fund files tax returns in the U.S. Federal jurisdiction and certain other jurisdictions. Generally, the Fund is subject to examinations by such taxing authorities for up to three years after the filing of the return for the tax period.

| F. | Accounting Estimates — The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period including estimates and assumptions related to taxation. Actual results could differ from those estimates by a significant amount. In addition, the Fund monitors for material events or transactions that may occur or become known after the period-end date and before the date the financial statements are released to print. |

| G. | Indemnifications — Under the Trust’s organizational documents, each Trustee, officer, employee or other agent of the Trust is indemnified against certain liabilities that may arise out of the performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts, including the Fund’s servicing agreements, that contain a variety of indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. The risk of material loss as a result of such indemnification claims is considered remote. |

19 Invesco Conservative Income Fund