UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

for the fiscal year ended: December 31, 2014

Commission file number: 001-36671

Atento S.A.

(Exact name of Registrant as specified in its charter)

Atento S.A.

(Exact name of Registrant’s name into English)

Grand Duchy of Luxembourg

(Jurisdiction of incorporation or organization)

4 rue Lou Hemmer, L - 1748 Luxembourg Findel

Grand Duchy of Luxembourg

(Address of principal executive offices)

Mauricio Teles Montilha, Chief Financial Officer

Address: Avenida das Nações Unidas, 14.171, 2º andar, Rochaverá, Ebony Tower, 04794-000, São Paulo, Brasil

Telephone No.: +55 (11) 3779-0881

e-mail: investor.relations@atento.com

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

| Ordinary Shares, no par value | | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital stock or common stock as of the close of the period covered by the annual report.

73,619,511 ordinary shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | | | |

US GAAP ¨ | | International Financial Reporting Standards as issued by the International Accounting Standards Board x | | Other ¨ |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow.

¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

¨ Yes x No

Atento S.A.

TABLE OF CONTENTS

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Basis of Presentation and Other Information

Except where the context otherwise requires or where otherwise indicated, the terms “Atento”, “we”, “us”, “our”, “the Company”, and “our business” refer to Atento S.A., a public limited liability company (société anonyme) incorporated under the laws of Luxembourg on March 5, 2014, together with its consolidated subsidiaries.

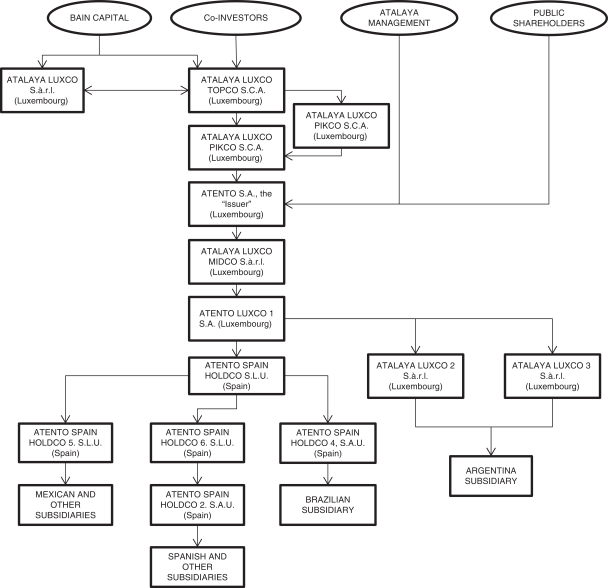

“AIT Group” refers to Atento Inversiones Teleservicios S.A.U. and its subsidiaries (including Atento Venezuela, S.A. and Teleatención de Venezuela, C.A.) as held by Telefónica, S.A. (together with its consolidated subsidiaries, “Telefónica” or the “Telefónica Group”) prior to the Acquisition. “Atento Group” refers to the direct and indirect subsidiaries and assets of Atento Inversiones y Teleservicios, S.A.U. (excluding Atento Venezuela, S.A. and Teleatención de Venezuela, C.A.) that were acquired indirectly by funds associated with Bain Capital Partners, LLC (together with affiliates of such funds, “Bain Capital”) on December 12, 2012 (the “Acquisition”) through Atalaya Luxco Midco S.à.r.l. (the “Successor”) and certain of its affiliates. Use of the term “Predecessor” refers to the Atento Group prior to the Acquisition, and use of the term “Atento” refers to the Atento Group subsequent to the Acquisition.

Atento S.A. was formed as a direct subsidiary of Atalaya Luxco Topco S.C.A. (“Topco”). In April 2014, Topco also incorporated Atalaya Luxco PIKCo S.C.A. (“PikCo”) and on May 15, 2014 Topco contributed to PikCo: (i) all of its equity interests in its then direct subsidiary, Atalaya Luxco Midco S.à.r.l. (“Midco”), the consideration for which was an allocation to PikCo’s account “capital contributions not remunerated by shares” (the “Reserve Account”) equal to €2 million, resulting in Midco becoming a direct subsidiary of PikCo; and (ii) all of its debt interests in Midco (comprising three series of preferred equity certificates (the “Original Luxco PECs”)), the consideration for which was the issuance by PikCo to Topco of preferred equity certificates having an equivalent value. On May 30, 2014, Midco authorized the issuance of, and PikCo subscribed for, a fourth series of preferred equity certificates (together with the Original Luxco PECs, the “Luxco PECs”).

In connection with the completion of Atento’s initial public offering (the “IPO”), Topco transferred its entire interest in Midco (being €31,000 of share capital) to PikCo, the consideration for which was an allocation to PikCo’s Reserve Account equal to €31,000. PikCo then contributed (the “Contribution”) all of the Luxco PECs to Midco, the consideration for which was an allocation to Midco’s Reserve Account equal to the value of the Luxco PECs immediately prior to the Contribution. Upon completion of the Contribution, the Luxco PECs were capitalized by Midco. PikCo then transferred the remainder of its interest in Midco (being €12,500 of share capital) to the Company, in consideration for which the Company issued two new shares of its capital stock to PikCo. The difference between the nominal value of these shares and the value of Midco’s net equity was allocated to the Company’s share premium account. As a result of this transfer, Midco became a direct subsidiary of Atento S.A. The Company completed a share split (the “Share Split”) whereby Atento issued approximately 2,219.212 ordinary shares for each ordinary share outstanding as of September 3, 2014. The foregoing is collectively referred as the “Reorganization Transaction”.

On October 7, 2014, upon the closing of our initial public offering, Atento issued 4,819,511 ordinary shares without nominal value at a price of $15.00 per share. As a result of the completion of the IPO, including the Share Split and the Reorganization Transaction, Atento has 73,619,511 ordinary shares outstanding and owns 100% of the issued and outstanding share capital of Midco.

As mentioned above, pursuant to the implementation of the Reorganization Transaction Midco became a wholly-owned subsidiary of Atento, which was a newly-formed company incorporated under the laws of Luxembourg with nominal assets and liabilities for the purpose of facilitating the IPO, and did not conduct any operations prior to the completion of the IPO. Following the Reorganization Transaction and the IPO, Atento’s financial statements presented the consolidated results of Midco’s operations. The consolidated financial statements of Midco are substantially the same as the consolidated financial statements of Atento after to the IPO, as adjusted for the Reorganization Transaction. Upon consummation, the Reorganization Transaction was retroactively reflected in Atento’s calculations for earnings per share.

In this Annual Report, all references to “U.S. dollar” and “$” are to the lawful currency of the United States and all references to “euro” or “€” are to the single currency of the participating member states of the European and Monetary Union of the Treaty Establishing the European Community, as amended from time to time. In addition, all references to Brazilian Reais (BRL), Mexican Peso (MXN), Chilean Peso (CLP), Argentinean Peso (ARS), Colombian Peso (COP) and Peruvian Nuevos Soles (PEN) are to the lawful currencies of Brazil, Mexico, Chile, Argentina, Colombia and Peru, respectively.

3

The following table shows the exchange rates of the U.S. dollar to these currencies for the years and dates indicated as reported by the relevant central banks of the European Union and each country, as applicable.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2012 | | | 2013 | | | 2014 | |

| | | Average | | | December 31 | | | Average | | | December 31 | | | Average | | | December 31 | |

Euro (EUR) | | | 0.78 | | | | 0.76 | | | | 0.75 | | | | 0.73 | | | | 0.75 | | | | 0.82 | |

Brazil (BRL) | | | 1.95 | | | | 2.04 | | | | 2.16 | | | | 2.34 | | | | 2.35 | | | | 2.66 | |

Mexico (MXN) | | | 13.16 | | | | 12.97 | | | | 12.77 | | | | 13.08 | | | | 13.33 | | | | 14.74 | |

Colombia (COP) | | | 1,797.34 | | | | 1,768.23 | | | | 1,869.31 | | | | 1,926.83 | | | | 2,000.23 | | | | 2,390.44 | |

Chile (CLP) | | | 486.37 | | | | 479.96 | | | | 495.40 | | | | 524.61 | | | | 570.51 | | | | 606.75 | |

Peru (PEN) | | | 2.64 | | | | 2.55 | | | | 2.70 | | | | 2.80 | | | | 2.84 | | | | 2.98 | |

Argentina (ARS) | | | 4.55 | | | | 4.92 | | | | 5.48 | | | | 6.52 | | | | 8.12 | | | | 8.55 | |

PRESENTATION OF FINANCIAL INFORMATION

We present our historic financial information under International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (the “IASB”).

Predecessor Financial Statements

We have historically conducted our business through the Atento Group, or the Predecessor up to the date of the Acquisition, and subsequent to the Acquisition, through Atento. Although the Acquisition was completed on December 12, 2012, for accounting purposes the Atento Group has been incorporated into the Atento’s operations since December 1, 2012.

The financial statements of the Predecessor included elsewhere in this Annual Report are the audited combined carve-out financial statements of the Atento Group as of and for the year ended December 31, 2011 and as of and for the eleven-month period ended November 30, 2012 (the “Predecessor financial statements”). The Predecessor financial statements are presented on a combined carve-out basis from the AIT Group’s historical consolidated financial statements, based on the historical results of operations, cash flows, assets and liabilities of the Predecessor acquired by the Successor and that are part of its consolidated group after the Acquisition. We believe that the assumptions and estimates used in preparation of the Predecessor financial statements are reasonable. However, the Predecessor financial statements do not necessarily reflect what the Predecessor’s financial position, results of operations or cash flows would have been if the Predecessor had operated as a separate entity during the periods presented. As a result, historical financial information is not necessarily indicative of the Predecessor’s future results of operations, financial position or cash flows.

Atento Financial Information

The consolidated financial information of Atento are the consolidated results of operations of Atento, which includes one-month period from December 1, 2012 to December 31, 2012, and the years ended December 31, 2013 and December 31, 2014.

Aggregated 2012 Financial Information

In addition, we also present in this Annual Report unaudited, non-IFRS aggregated financial information for the year ended December 31, 2012 (the “Aggregated 2012 Financial Information”). The Aggregated 2012 Financial Information is derived by adding together the corresponding data from the audited Predecessor financial statements for the period from January 1, 2012 to November 30, 2012 and the corresponding data from the audited Successor financial statements for the one-month period from December 1, 2012 to December 31, 2012, appearing elsewhere in this Annual Report, each prepared under IFRS as issued by the IASB. This presentation of the Aggregated 2012 Financial Information is for illustrative purposes only, is not presented in accordance with IFRS, and is not necessarily comparable to previous or subsequent periods, or indicative of results expected in any future period (including as a result of the effects of the Acquisition).

Rounding

Certain numerical figures set out in this Annual Report, including financial data presented in millions or thousands and percentages, have been subject to rounding adjustments, and, as a result, the totals of the data in

4

this Annual Report may vary slightly from the actual arithmetic totals of such information. Percentages and amounts reflecting changes over time periods relating to financial and other data set forth in “Selected Historical Financial Information” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” are calculated using the numerical data in the financial statements of the Predecessor or the Successor, or the tabular presentation of other data (subject to rounding) contained in this Annual Report, as applicable, and not using the numerical data in the narrative description thereof.

TRADEMARKS AND TRADE NAMES

This Annual Report includes our trademarks as “Atento,” which are protected under applicable intellectual property laws and are the property of the Company or our subsidiaries. This Annual Report also contains trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this Annual Report may appear without the® orTM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks and trade names.

CAUTIONARY STATEMENT WITH RESPECT TO FORWARD-LOOKING STATEMENTS

This Annual Report contains estimates and forward-looking statements, principally in “Item 3. Key Information—D. Risk Factors”, “Item 4. Information on the Company—B. Business Overview” and “Item 5. Operating and Financial Review and Prospects”. Some of the matters discussed concerning our business operations and financial performance include estimates and forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995.

Our estimates and forward-looking statements are based mainly on our current expectations and estimates on projections of future events and trends, which affect or may affect our businesses and results of operations. Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to certain risks and uncertainties and are made in light of information currently available to us. Our estimates and forward-looking statements may be influenced by the following factors, among others:

| | • | | the competitiveness of the customer relationship management and business process (“CRM BPO”) market; |

| | • | | the loss of one or more of our major clients, a small number of which account for a significant portion of our revenue, in particular Telefónica; |

| | • | | risks associated with operating in Latin America, where a significant proportion of our revenue is derived and where a large number of our employees are based; |

| | • | | our clients deciding to enter or further expand their own CRM BPO businesses in the future; |

| | • | | any deterioration in global markets and general economic conditions, in particular in Latin America and in the telecommunications and the financial services industries from which we derive most of our revenue; |

| | • | | increases in employee benefits expenses, changes to labor laws and labor relations; |

| | • | | failure to attract and retain enough sufficiently trained employees at our service delivery centers to support our operations; |

| | • | | inability to maintain our pricing and level of activity and control our costs; |

| | • | | consolidation of potential users of CRM BPO services; |

| | • | | the reversal of current trends towards CRM BPO solutions; |

| | • | | fluctuations of our operating results from one quarter to the next due to various factors including seasonality; |

| | • | | the significant leverage our clients have over our business relationships; |

| | • | | the departure of key personnel or challenges with respect to labor relations; |

| | • | | the long selling and implementation cycle for CRM BPO services; |

5

| | • | | difficulty controlling our growth and updating our internal operational and financial systems as a result of our increased size; |

| | • | | inability to fund our working capital requirements and new investments; |

| | • | | fluctuations in, or devaluation of, the local currencies in the countries in which we operate against our reporting currency, the U.S. dollars; |

| | • | | current political and economic volatility, particularly in Brazil, Mexico, Argentina and Europe; |

| | • | | our ability to acquire and integrate companies that complement our business; |

| | • | | technology’s quality and reliability provided by our technology and telecommunications providers, our reliance on a limited number of suppliers of such technology and the services and products of our clients; |

| | • | | our ability to invest in and implement new technologies; |

| | • | | disruptions or interruptions in our client relationships; |

| | • | | actions of the Brazilian, EU, Spanish, Argentinian, Mexican and other governments and their respective regulatory agencies, including adverse competition law rulings and the introduction of new regulations that could require us to make additional expenditures; |

| | • | | damage or disruptions to our key technology systems or the quality and reliability of the technology provided by technology telecommunications providers; |

| | • | | an increase in the cost of telecommunications services and other services on which we and our industry rely; |

| | • | | an actual or perceived failure to comply with data protection regulations, in particular any actual or perceived failure to ensure secure transmission of sensitive or confidential customer data through our networks; |

| | • | | the effect of labor disputes on our business; and |

| | • | | other risk factors listed in the section of this Annual Report entitled “Item 3. Key Information—D. Risk Factors”. |

The words “believe”, “may”, “will”, “estimate”, “continue”, “anticipate”, “intend”, “expect” and similar words are intended to identify estimates and forward-looking statements. Estimates and forward-looking statements are intended to be accurate only as of the date they were made, and we undertake no obligation to update or to review any estimate and/or forward-looking statement because of new information, future events or other factors. Estimates and forward-looking statements involve risks and uncertainties and are not guarantees of future performance. Our future results may differ materially from those expressed in these estimates and forward-looking statements. You should therefore not make any investment decision based on these estimates and forward-looking statements.

The forward-looking statements contained in this report speak only as of the date of this report. We do not undertake to update any forward-looking statement to reflect events or circumstances after that date or to reflect the occurrence of unanticipated events.

6

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

| A. | Directors and Senior Management |

Not applicable.

Not applicable.

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

| B. | Method and Expected Timetable |

Not applicable.

ITEM 3. KEY INFORMATION

| A. | Selected Financial Data |

The following selected financial information should be read in conjunction with the section “Item 5. Operating and Financial Review and Prospects” and our consolidated financial statements, included elsewhere in this Annual Report.

Historically, as described in “Presentation of financial and other information” above, we conducted our business through the Atento Group (“Predecessor”) through November 30, 2012, and subsequent to the Acquisition, through Atalaya Luxco Midco S.à.r.l (“Midco” or the “Successor”), and therefore our historical financial statements present the results of operations of Predecessor and Successor, respectively. Prior to completion of the IPO we implemented the Reorganization Transaction pursuant to which the Successor became a wholly-owned subsidiary of Atento S.A., a newly-formed public limited liability holding company incorporated under the laws of Luxembourg with nominal assets and liabilities for the purpose of facilitating the IPO, and which not had conducted any operations prior to the completion of the IPO. Following the Reorganization Transaction and the IPO, our financial statements present the results of operations of Atento. The consolidated financial statements of Atento are substantially the same as the consolidated financial statements of Midco prior to the IPO, as adjusted for the Reorganization Transaction. Upon consummation, the Reorganization Transaction was reflected retroactively in the Company’s earnings per share calculations.

The following table sets forth selected historical financial data of the Atento Group and Atento. We prepare our financial statements in accordance with IFRS as issued by the IASB. As a result of the Acquisition, we applied acquisition accounting whereby the purchase price paid was allocated to the acquired assets and assumed liabilities at fair value. Our financial reporting periods presented in the table below are as follow:

| | • | | The financial statements of the Predecessor included elsewhere in this Annual Report are the audited combined carve-out financial statements of the Atento Group as of and for the year ended December 2011 and as of and for the eleven-month period ended November 30, 2012 (the “Predecessor financial statements”). The Predecessor financial statements are presented on a combined carve-out basis from the AIT Group’s historical consolidated financial statements, based on the historical results of operations, cash flows, assets and liabilities of the Predecessor acquired by the Successor and that are part of its consolidated group after the Acquisition. We believe that the assumptions and estimates used in preparation of the Predecessor financial statements are reasonable. However, the Predecessor financial statements do not necessarily reflect what the Predecessor’s financial position, results of operations or cash flows would have been if the Predecessor had operated as a separate entity during the periods presented. As a result, historical financial information is not necessarily indicative of the Predecessor’s future results of operations, financial position or cash flows. |

7

| | • | | The Company period reflects the consolidated results of operations of Atento; which includes theone-month period from December 1, 2012 to December 31, 2012, and the years ended December 31, 2013 and December 31, 2014. |

| | • | | The unaudited Aggregated 2012 Financial Information set forth below is derived by adding together the corresponding data from the audited Predecessor financial statements for the period from January 1, 2012 to November 30, 2012, to the corresponding data from the audited Atento’s financial information for the one-month period from December 1, 2012 to December 31, 2012, appearing elsewhere in this Annual Report, each prepared under IFRS as issued by the IASB. This presentation of the Aggregated 2012 Financial Information is for illustrative purposes only, is not presented in accordance with IFRS, and is not necessarily comparable to previous or subsequent periods, or indicative of results expected in any future period (including as a result of the effects of the Acquisition). |

Summary Consolidated Historical Financial Information

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Predecessor | | | | | | Non-IFRS

Aggregated | | | | | | | |

| | | As of and for the year

ended

December 31, | | | As of and

for the

period from

Jan 1 – Nov 30, | | | As of and

for the

period from

Dec 1 – Dec 31, | | | As of and

for the

year ended

December 31, | | | As of and for the year

ended

December 31, | |

($ in millions other than share and per share data) | | 2010 | | | 2011 | | | 2012 | | | 2012 | | | 2012 | | | 2013 | | | 2014 | |

| | | (unaudited) | | | | | | | | | | | | (unaudited) | | | | | | | |

Revenue | | | 2,128.8 | | | | 2,417.3 | | | | 2,125.9 | | | | 190.9 | | | | 2,316.8 | | | | 2,341.1 | | | | 2,298.3 | |

Operating profit / (loss) | | | 183.4 | | | | 155.6 | | | | 163.8 | | | | (42.4 | ) | | | 121.4 | | | | 105.0 | | | | 87.2 | |

Profit / (loss) for the period | | | 112.2 | | | | 90.3 | | | | 90.2 | | | | (56.6 | ) | | | 33.6 | | | | (4.0 | ) | | | (42.1 | ) |

Profit / (loss) for the period from continuing operations | | | 112.2 | | | | 89.6 | | | | 90.2 | | | | (56.6 | ) | | | 33.6 | | | | (4.0 | ) | | | (42.1 | ) |

Profit / (loss) attributable to equity holders | | | 111.1 | | | | 87.9 | | | | 89.7 | | | | (56.6 | ) | | | 33.1 | | | | (4.0 | ) | | | (42.1 | ) |

Earnings per share—basic and diluted | | | n/a | | | | n/a | | | | n/a | | | | (0.82 | ) | | | n/a | | | | (0.06 | ) | | | (0.61 | ) |

Weighted average number of shares outstanding—basic and diluted | | | n/a | | | | n/a | | | | n/a | | | | 68,800,000 | | | | n/a | | | | 68,800,000 | | | | 69,603,252 | |

| | | | | | | |

Balance sheet data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total assets | | | 1,152.6 | | | | 1,224.6 | | | | 1,263.8 | | | | 1,961.0 | | | | n/a | | | | 1,842.2 | | | | 1,657.9 | |

Total share capital | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | — | | | | 0.0 | |

Invested equity/equity | | | 658.2 | | | | 631.2 | | | | 670.1 | | | | (32.7 | ) | | | n/a | | | | (134.0 | ) | | | 464.9 | |

Selected Consolidated Other Financial Information

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Predecessor | | | | | | Non-IFRS

Aggregated | | | | | | | | | | | | | | | | | | | |

| ($ millions) | | As of and

for the

period from

Jan 1 –Nov 30,

2012 | | | As of and

for the

period from

Dec 1 – Dec 31,

2012 | | | For the year

ended

December 31,

2012 | | | For the year

ended

December 31,

2013 | | | Change

(%) | | | Change

excluding

FX (%) | | | For the year

ended

December 31,

2014 | | | Change

(%) | | | Change

excluding

FX (%) | |

| | | | | | | | | (unaudited) | | | | | | | | | | | | | |

Revenue | | | 2,125.9 | | | | 190.9 | | | | 2,316.8 | | | | 2,341.1 | | | | 1.0 | | | | 7.5 | | | | 2,298.3 | | | | (1.8 | ) | | | 7.7 | |

EBITDA(1) | | | 241.9 | | | | (34.9 | ) | | | 207.0 | | | | 234.0 | | | | 13.0 | | | | 22.9 | | | | 207.0 | | | | (11.5 | ) | | | (0.8 | ) |

Adjusted EBITDA(1) | | | 235.9 | | | | 32.2 | | | | 268.1 | | | | 295.1 | | | | 10.1 | | | | 16.9 | | | | 306.4 | | | | 3.8 | | | | 13.7 | |

Adjusted Earnings/(Loss)(2) | | | 86.2 | | | | (8.9 | ) | | | 77.3 | | | | 85.2 | | | | 10.2 | | | | 36.1 | | | | 82.7 | | | | (2.9 | ) | | | 7.5 | |

Adjusted Earnings per share (in U.S. dollars)(3) | | | 1.17 | | | | (0.12 | ) | | | 1.05 | | | | 1.16 | | | | 10.2 | | | | 36.1 | | | | 1.12 | | | | (2.9 | ) | | | 7.5 | |

Capital Expenditures(4) | | | (76.9 | ) | | | (28.4 | ) | | | (105.3 | ) | | | (103.0 | ) | | | (2.2 | ) | | | 4.0 | | | | (120.1 | ) | | | 16.6 | | | | 25.9 | |

Total debt with third parties | | | 88.4 | | | | 849.2 | | | | 849.2 | | | | 851.2 | | | | 0.2 | | | | 4.0 | | | | 653.3 | | | | (23.2 | ) | | | (12.8 | ) |

Cash and cash equivalents and short-term financial investments | | | 83.3 | | | | 229.0 | | | | 229.0 | | | | 213.5 | | | | (6.8 | ) | | | (3.1 | ) | | | 238.3 | | | | 11.6 | | | | 27.3 | |

Net debt with third parties(5) | | | 5.1 | | | | 620.2 | | | | 620.2 | | | | 637.7 | | | | 2.8 | | | | 6.6 | | | | 415.0 | | | | (34.9 | ) | | | (26.2 | ) |

| (1) | In considering the financial performance of the business, our management analyzes the financial performance measures of EBITDA and adjusted EBITDA at a company and operating segment level, to facilitate decision-making. EBITDA is defined as profit/(loss) for the period from continuing operations before net finance costs, income taxes and depreciation and amortization. Adjusted EBITDA is defined as EBITDA adjusted to exclude Acquisition and integration related costs, restructuring costs, sponsor management fees, asset impairments, site-relocation costs, financing and IPO fees, and other items which are not related to our core results of operations. EBITDA and adjusted EBITDA are not measures defined by IFRS. The most directly comparable IFRS measure to EBITDA and adjusted EBITDA is profit/(loss) for the period from continuing operations. |

8

We believe EBITDA and adjusted EBITDA, as defined above, are useful metrics for investors to understand our results of continuing operations and profitability because they permit investors to evaluate our recurring profitability from underlying operating activities. We also use these measures internally to establish forecasts, budgets and operational goals to manage and monitor our business, as well as to evaluate our underlying historical performance. We believe EBITDA facilitates comparisons of operating performance between periods and among other companies in industries similar to ours because it removes the effect of variation in capital structures, taxation, and non-cash depreciation and amortization charges, which may differ between companies for reasons unrelated to operating performance. We believe adjusted EBITDA better reflects our underlying operating performance because it excludes the impact of items which are not related to our core results of continuing operations.

EBITDA and adjusted EBITDA measures are frequently used by securities analysts, investors and other interested parties in their evaluation of companies comparable to us, many of which present EBITDA-related performance measures when reporting their results.

EBITDA and adjusted EBITDA have limitations as analytical tools. These measures are not presentations made in accordance with IFRS, are not measures of financial condition or liquidity and should not be considered in isolation or as alternatives to profit or loss for the period from continuing operations or other measures determined in accordance with IFRS. EBITDA and adjusted EBITDA are not necessary comparable to similarly titled measures used by other companies.

See below under the heading “Reconciliation of EBITDA and Adjusted EBITDA to profit/(loss)” for a reconciliation of profit/(loss) for the period from continuing operations to EBITDA and adjusted EBITDA.

| (2) | In considering the Company’s financial performance, our management analyzes the performance measure of adjusted earnings/(loss). Adjusted earnings/(loss) is defined as profit/(loss) for the period from continuing operations adjusted for Acquisition and integration related costs, amortization of Acquisition-related intangible assets, restructuring costs, sponsor management fees, assets impairments, site relocation costs, financing and IPO fees, PECs interest expense, other and tax effects. Adjusted earnings/(loss) are not a measure defined by IFRS. The most directly comparable IFRS measure to adjusted earnings/(loss) is our profit/(loss) for the period from continuing operations. |

We believe adjusted earnings/(loss), as defined above, is useful to investors and is used by our management for measuring profitability because it represents a group measure of performance which excludes the impact of certain non-cash charges and other charges not associated with the underlying operating performance of the business, while including the effect of items that we believe affect shareholder value and in-year return, such as income-tax expense and net finance costs.

Management expects to use adjusted earnings/(loss) to (i) provide senior management a monthly report of our operating results that is prepared on an adjusted earnings basis; (ii) prepare strategic plans and annual budgets on the basis of adjusted earnings; and (iii) review senior management’s annual compensation, in part, using adjusted performance measures.

Adjusted earnings/(loss) is defined to exclude items that are not related to our core results of operations. Adjusted earnings/(loss) measures are frequently used by securities analysts, investors and other interested parties in their evaluation of companies comparable to us, many of which present an adjusted earnings related performance measure when reporting their results.

Adjusted earnings/(loss) have limitations as an analytical tool. Adjusted earnings/(loss) is neither a presentation made in accordance with IFRS nor a measure of financial condition or liquidity, and should not be considered in isolation or as an alternative to profit or loss for the period from continuing operations or other measures determined in accordance with IFRS. Adjusted earnings/(loss) is not necessarily comparable to similarly titled measures used by other companies.

See below for a reconciliation of our adjusted earnings/(loss) to our profit/(loss) for the period from continuing operations.

| (3) | Adjusted earnings per share calculated considering 73,619,511 Atento ordinary shares as of December 31, 2014. The weighted average number of ordinary shares for the year ended December 31, 2014 was not considered in this calculation. |

Adjusted earnings/(loss) per share is not a measure defined by IFRS. The most directly comparable IFRS measure to adjusted earnings/(loss) per share is our Basic result per share. We believe adjusted earnings/(loss) per share, as defined above and related to the item (2) Adjusted earnings/(loss) included in this section, is useful to investors, and is used by our management for measuring profitability.

9

| (4) | We defined “capital expenditure” as the sum of the additions to property, plant and equipment and the additions to intangible assets. |

| (5) | In considering our financial condition, our management analyzes net debt with third parties, which is defined as total debt less cash, cash equivalents (net of any outstanding bank overdrafts) and short-term financial investments and non-current payables to Atento Group companies (which represent the PECs). In 2013, the PECs were classified as our subordinated debt relating to our other present and future obligations, and in 2014 they were capitalized in connection with the IPO. Net debt with third parties is not a measure defined by IFRS. |

Net debt with third parties has limitations as an analytical tool. Net debt with third parties is neither a measure defined by or presented in accordance with IFRS nor a measure of financial performance, and should not be considered in isolation or as an alternative financial measure determined in accordance with IFRS. Net debt with third parties is not necessarily comparable to similarly titled measures used by other companies.

See below under the heading “Reconciliation of total debt with third parties” for a reconciliation of Total debt to net debt with third parties utilizing IFRS reported balances obtained from the financial information. Total debt is the most directly comparable financial measure under IFRS.

Cash flow selected data:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Predecessor | | | | | | Non-IFRS

Aggregated | | | | |

| | | For the

year ended

December 31, | | | January 1

to

November 30, | | | December 1

to

December 31, | | | For the

year ended

December 31, | | | For the year ended

December 31, | |

| ($ in millions) | | 2011 | | | 2012 | | | 2012 | | | 2012 | | | 2013 | | | 2014 | |

| | | | | | | | | | | | (unaudited) | | | | | | | |

Net cash flow from/(used in) operating activities | | | 116.6 | | | | 163.6 | | | | (68.3 | ) | | | 95.3 | | | | 99.6 | | | | 135.3 | |

Net cash flow from/(used in) investment activities | | | (134.6 | ) | | | (118.7 | ) | | | (846.1 | ) | | | (964.8 | ) | | | (123.4 | ) | | | (149.8 | ) |

Net cash flow from/(used in) financing activities | | | 27.0 | | | | (75.0 | ) | | | 1.109.6 | | | | 1.034.6 | | | | 31.2 | | | | 38.8 | |

Effect of changes in exchange rates | | | (0.1 | ) | | | (2.2 | ) | | | 5.1 | | | | 2.9 | | | | 5.8 | | | | (26.3 | ) |

Net increase/(decrease) in cash and cash equivalents | | | 8.8 | | | | (32.3 | ) | | | 200.3 | | | | 168.0 | | | | 13.2 | | | | (2.1 | ) |

Cash and cash equivalents at beginning of period | | | 73.1 | | | | 81.9 | | | | — | | | | 81.9 | | | | 200.3 | | | | 213.5 | |

Cash and cash equivalents at end of period | | | 81.9 | | | | 49.6 | | | | 200.3 | | | | 200.3 | | | | 213.5 | | | | 211.4 | |

Cash and cash equivalents and short-term financial investments at end of period | | | 103.6 | | | | 83.3 | | | | 229.0 | | | | 229.0 | | | | 213.5 | | | | 238.3 | |

Reconciliation of EBITDA and Adjusted EBITDA to profit/(loss):

| | | | | | | | | | | | | | | | | | | | |

| | | Predecessor | | | | | | Non-IFRS

Aggregated | | | | |

| | | Period from

Jan 1 – Nov 30, | | | Period from

Dec 1 – Dec 31, | | | Year ended

December 31, | | | Year ended

December 31, | |

| ($ in millions) | | 2012 | | | 2012 | | | 2012 | | | 2013 | | | 2014 | |

| | | | | | | | | (unaudited) | | | | | | | |

Profit/(loss) for the period from continuing operations | | | 90.2 | | | | (56.6 | ) | | | 33.6 | | | | (4.0 | ) | | | (42.1 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net finance expense | | | 12.9 | | | | 6.0 | | | | 19.0 | | | | 100.7 | | | | 110.8 | |

Income tax expense | | | 60.7 | | | | 8.1 | | | | 68.8 | | | | 8.3 | | | | 18.5 | |

Depreciation and amortization | | | 78.1 | | | | 7.5 | | | | 85.6 | | | | 129.0 | | | | 119.8 | |

| | | | | | | | | | | | | | | | | | | | |

EBITDA (non-GAAP) (unaudited) | | | 241.9 | | | | (34.9 | ) | | | 207.0 | | | | 234.0 | | | | 207.0 | |

| | | | | | | | | | | | | | | | | | | | |

Acquisition and integration related costs(a) | | | 0.2 | | | | 62.4 | | | | 62.6 | | | | 29.3 | | | | 9.9 | |

Restructuring costs(b) | | | 3.9 | | | | 4.7 | | | | 8.6 | | | | 12.8 | | | | 26.7 | |

Sponsor management fees(c) | | | — | | | | — | | | | — | | | | 9.1 | | | | 7.3 | |

Site relocation costs(d) | | | 1.7 | | | | 0.7 | | | | 2.4 | | | | 1.8 | | | | 1.7 | |

Financing and IPO fees(e) | | | — | | | | — | | | | — | | | | 6.1 | | | | 51.9 | |

Asset impairments and Other(f) | | | (11.8 | ) | | | (0.6 | ) | | | (12.4 | ) | | | 2.0 | | | | 1.9 | |

| | | | | | | | | | | | | | | | | | | | |

Adjusted EBITDA (non-GAAP) (unaudited) | | | 235.9 | | | | 32.2 | | | | 268.1 | | | | 295.1 | | | | 306.4 | |

| | | | | | | | | | | | | | | | | | | | |

10

| (a) | Acquisition and integration costs incurred in 2012, 2013, and 2014 are costs associated with the Acquisition and post-Acquisition process targeting primarily financial and operational improvements. Nearly all of the $62.6 million in expenses for the year ended December 31, 2012, are directly related to Acquisition and integration related costs (banking, advisory, legal fees, etc.). For the year ended December 31, 2013, of the $29.3 million, $27.9 million are related to professional fees incurred to establish Atento as a standalone company not affiliated to Telefónica. These projects are mainly related to full strategy review including growth implementation plan and operational set-up with a leading consulting firm ($14.7 million), improvement of financial and cash flow reporting ($5.9 million), improving the efficiency in procurement ($4.8 million) and headhunting fees related primarily to strengthening the senior management team post-Acquisition ($1.4 million). Acquisition and integration related cost incurred for the year ended December 31, 2014 primarily resulted from consulting fees incurred in connection with the full strategy review including our growth implementation plan and operational set-up with a leading consulting firm ($4.0 million), improving the efficiency in procurement ($2.3 million), and IT transformation projects ($2.5 million). These projects have substantially been completed by the end of 2014. |

| (b) | Restructuring costs incurred in 2012, 2013 and 2014 primarily included a number of restructuring activities and other personnel costs that were not related to our core result of operations. In 2012, restructuring costs primarily represented costs incurred in Chile related to the implementation of a new service delivery model with Telefónica, which affected the profile of certain operations personnel, and other restructuring costs for certain changes to the executive team in EMEA and Americas region. For the year ended December 31, 2013, $8.6 million of our restructuring costs were related to the relocation of corporate headquarters and severance payments directly related to the Acquisition. In addition in 2013, we incurred in restructuring costs in Spain of $1.5 million (relating to restructuring expenses incurred as a consequence of significant reduction in activity levels as a result of adverse market conditions in Spain), and in Chile of $1.4 million (relating to restructuring expenses incurred in connection with the implementation of a new service delivery model with Telefónica). Restructuring costs incurred for the year ended December 31, 2014, are primarily related to headcount restructuring activities in Spain. In addition, we incurred restructuring costs not related to our core results of operations in Argentina and Peru of $4.8 million related to the restructuring of specific operations, Chile of $2.5 million related to restructuring expenses incurred in connection with the implementation of a new service delivery model with Telefónica, and in connection with certain changes to the executive team, and an additional $0.7 million related to the relocation of corporate headquarters. |

| (c) | Sponsor management fees represent the annual advisory fee paid to Bain Capital Partners, LLC that are expensed during the period presented. These fees have ceased following the offering. |

| (d) | Site relocation costs incurred for the year ended December 31, 2012, 2013 and 2014 include costs associated with our current strategic initiative of relocating call centers from tier 1 cities to tier 2 cities in Brazil in order to get efficiencies through rental cost reduction and attrition and absenteeism improvement. |

| (e) | Financing and IPO fees for the year ended December 31, 2013 primarily relate to professional fees incurred in 2013 in connection with the issuance of the Senior Secured Notes and to pay financial advisory fees. Financing fees and IPO fees for the year ended December 31, 2014 primarily relate to fees incurred in connection with the IPO process including advisory, auditing and legal expenses among others. These fees have ceased in 2014. |

| (f) | Asset impairments and other costs incurred for the year ended 31, 2012 related to a release of an employee benefit accrual of $11.3 million following the better-than-expected outcome of the collective bargain agreement negotiation in Spain. Asset impairment and other costs for the year ended December 31, 2013 relates to charges associated to projects for inventory control in Brazil which are not related to our core results of operations. Asset impairment and other cost incurred for the year ended December 31, 2014, mainly relate to the goodwill and other intangible asset impairment relating to our operation in Czech Republic of $3.7 million and Spain of $28.8 million and other non-recurrent costs of $4.6 million during the year ended December 31, 2014, primarily related to a Revenue adjustment in Spain ($2.4 million) related to prior fiscal years and a one off tax penalty in Colombia ($1.3 million), offset by the amendment of the MSA with Telefónica by which the minimum revenue commitment for Spain was reduced against a $34.5 million penalty fee compensated by Telefónica. |

11

Reconciliation of Adjusted earnings/(loss) to profit/(loss):

The following table reconciles our adjusted earnings/(loss) to our profit/(loss) for the period from continuing operations:

| | | | | | | | | | | | | | | | | | | | |

| | | Predecessor | | | | | | Non-IFRS

Aggregated | | | | | | | |

| ($ in millions) | | Period from

Jan 1 – Nov 30,

2012 | | | Period from

Dec 1 – Dec 31,

2012 | | | Year ended

December 31,

2012 | | | Year ended

2013 | | | December 31,

2014 | |

| | | | | | | | | (unaudited) | | | | | | | |

Profit/(loss) attributable to equity holders of the parent | | | 90.2 | | | | (56.6 | ) | | | 33.6 | | | | (4.0 | ) | | | (42.1 | ) |

| | | | | | | | | | | | | | | | | | | | |

Acquisition and integration related costs(a) | | | 0.2 | | | | 62.4 | | | | 62.6 | | | | 29.3 | | | | 9.9 | |

Amortization of Acquisition related Intangible assets(b) | | | — | | | | — | | | | — | | | | 40.7 | | | | 36.6 | |

Restructuring costs(c) | | | 3.9 | | | | 4.7 | | | | 8.6 | | | | 12.8 | | | | 26.7 | |

Sponsor management fees(d) | | | — | | | | — | | | | — | | | | 9.1 | | | | 7.3 | |

Site relocation costs(e) | | | 1.7 | | | | 0.7 | | | | 2.4 | | | | 1.8 | | | | 1.7 | |

Financing and IPO fees(f) | | | — | | | | — | | | | — | | | | 6.1 | | | | 51.9 | |

PECs interest expense(g) | | | — | | | | 1.9 | | | | 1.9 | | | | 25.7 | | | | 25.4 | |

Asset impairments and Other(h) | | | (11.8 | ) | | | (0.6 | ) | | | (12.4 | ) | | | 2.0 | | | | 1.9 | |

DTA adjustment in Spain(i) | | | — | | | | — | | | | — | | | | — | | | | 9.8 | |

Tax effect(j) | | | 2.0 | | | | (21.4 | ) | | | (19.4 | ) | | | (38.3 | ) | | | (46.4 | ) |

| | | | | | | | | | | | | | | | | | | | |

Adjusted earnings /(loss) (non-GAAP) (unaudited) | | | 86.2 | | | | (8.9 | ) | | | 77.3 | | | | 85.2 | | | | 82.7 | |

| | | | | | | | | | | | | | | | | | | | |

Adjusted earnings/(loss) per share—Basic

(in U.S. dollars)(k) | | | 1.17 | | | | (0.12 | ) | | | 1.05 | | | | 1.16 | | | | 1.12 | |

Adjusted earnings/(loss) per share—Diluted

(in U.S. dollars)(k) | | | 1.17 | | | | (0.12 | ) | | | 1.05 | | | | 1.16 | | | | 1.12 | |

| (a) | Acquisition and integration costs incurred in 2012, 2013, and 2014 are costs associated with the Acquisition and post financial and operational improvements. Nearly all of the $62.6 million in expenses for the year ended December 31, 2012, are directly related to Acquisition and integration related costs (banking, advisory, legal fees, etc.). For the year ended December 31, 2013, of the $29.3 million, $27.9 million are related to professional fees incurred to establish Atento as a standalone company not affiliated to Telefónica. These projects are mainly related to full strategy review including growth implementation plan and operational set-up with a leading consulting firm ($14.7 million), improvement of financial and cash flow reporting ($5.9 million), improving the efficiency in procurement ($4.8 million) and headhunting fees related primarily to strengthening the senior management team post-Acquisition ($1.4 million). Acquisition and integration related cost incurred for the year ended December 31, 2014 primarily resulted from consulting fees incurred in connection with the full strategy review including our growth implementation plan an operational set-up with a leading consulting firm ($4.0 million), improving the efficiency in procurement ($2.3 million), and IT transformation projects ($2.5 million). These projects have substantially been completed by the end of 2014. |

| (b) | Amortization of Acquisition related intangible assets represents the amortization expense of intangible assets resulting from the Acquisition and has been adjusted to eliminate the impact of the amortization arising from the Acquisition which is not in the ordinary course of our daily operations and distorts comparison with peers and results for prior periods. Such intangible assets primarily include contractual relationships with customers, for which the useful life has been estimated at primarily nine years. |

| (c) | Restructuring costs incurred in 2012, 2013 and 2014 primarily included a number of restructuring activities and other personnel costs that were not related to our core result of operations. In 2012, restructuring costs primarily represented costs incurred in Chile related to the implementation of a new service delivery model with Telefónica, which affected the profile of certain operations personnel, and other restructuring costs for certain changes to the executive team in EMEA and Americas region. For the year ended December 31, 2013, $8.6 million of our restructuring costs were related to the relocation of corporate headquarters and severance payments directly related to the Acquisition. In addition in 2013, we incurred in restructuring costs in Spain of $1.5 million (relating to restructuring expenses incurred as a consequence of significant reduction in activity levels as a result of adverse market conditions in Spain), and in Chile of $1.4 million (relating to restructuring expenses incurred in connection with the implementation of a new service delivery model with Telefónica). Restructuring costs incurred for the year ended December 31, 2014, are primarily |

12

| | related to headcount restructuring activities in Spain. In addition, we incurred restructuring costs not related to our core results of operations in Argentina and Peru of $4.8 million related to the restructuring of specific operations, Chile of $2.5 million related to restructuring expenses incurred in connection with the implementation of a new service delivery model with Telefónica, and in connection with certain changes to the executive team, and an additional $0.7 million related to the relocation of corporate headquarters. |

| (d) | Sponsor management fees represent the annual advisory fee paid to Bain Capital Partners, LLC that are expensed during the period presented. These fees have ceased in following the offering. |

| (e) | Site relocation costs incurred for the year ended December 31, 2012, 2013 and 2014 include costs associated with our current strategic initiative of relocating call centers from tier 1 cities to tier 2 cities in Brazil in order to get efficiencies through rental cost reduction and attrition and absenteeism improvement. |

| (f) | Financing and IPO fees for the year ended December 31, 2013 primarily relate to professional fees incurred in 2013 in connection with the issuance of the Senior Secured Notes and to pay financial advisory fees. Financing fees and IPO fees for the year ended December 31, 2014 primarily relate to fees incurred in connection with the IPO process including advisory, auditing and legal expenses among others. These fees have ceased in 2014. |

| (g) | PECs Interest expense represents accrued interest on the preferred equity certificates that were capitalized in connection with the IPO. |

| (h) | Asset impairments and other costs incurred for the year ended 31, 2012 related to a release of an employee benefit accrual of $11.3 million following the better-than-expected outcome of the collective bargain agreement negotiation in Spain. Asset impairment and other costs for the year ended December 31, 2013 relates to charges associated to projects for inventory control in Brazil which are not related to our core results of operations. Asset impairment and other cost incurred for the year ended December 31, 2014, mainly relate to the goodwill and other intangible asset impairment relating to our operation in Czech Republic of $3.7 million and Spain of $28.8 million and other non-recurrent costs of $4.6 million during the year ended December 31, 2014, primarily related to a revenue adjustment in Spain ($2.4 million) related to prior fiscal years and a one off tax penalty in Colombia ($1.3 million), offset by the amendment of the MSA with Telefónica by which the minimum revenue commitment for Spain was reduced against a $34.5 million penalty fee compensated by Telefónica. |

| (i) | Deferred tax asset adjustment as a consequence of the tax rate reduction in Spain from 30% to 28% in 2015 and to 25% in 2016. |

| (j) | The tax effect represents the tax impact of the total adjustments based on a tax rate of 33.0% for the period from January 1, 2012 to November 30, 2012, 31.0% for the one-month period from December 1, 2012 to December 31, 2012, 30.0% for 2013 and 39.5% for the year ended December 31, 2014. The adjustments for the year ended December 31, 2014 include $43.8 million of IPO fees that are not deductible and $9.8 million of DTA adjustments that are both excluded from the adjustments base for tax effect calculation. |

| (k) | The adjusted earnings/(loss) per share, for the period presented in the table above, were calculated considering the number of ordinary shares of 73,619,511 as of December 31, 2014. |

13

Reconciliation of total debt to net debt with third parties

| | | | | | | | | | | | |

| | | As of December 31, | |

| ($ in millions) | | 2012 | | | 2013 | | | 2014 | |

Debt: | | | | | | | | | | | | |

7.375% Senior Secured Notes due 2020 | | | — | | | | 297.7 | | | | 300.3 | |

Brazilian Debentures | | | 443.0 | | | | 345.9 | | | | 245.9 | |

Vendor Loan Note(1) | | | 145.1 | | | | 151.7 | | | | — | |

Contingent Value Instrument | | | 52.3 | | | | 43.4 | | | | 36.4 | |

Preferred Equity Certificates | | | 471.6 | | | | 519.6 | | | | — | |

Finance lease payables | | | 8.7 | | | | 11.9 | | | | 9.0 | |

Other borrowings | | | 200.1 | | | | 0.6 | | | | 61.7 | |

| | | | | | | | | | | | |

Total Debt | | | 1,320.8 | | | | 1,370.8 | | | | 653.3 | |

| | | | | | | | | | | | |

Preferred Equity Certificates | | | (471.6 | ) | | | (519.6 | ) | | | — | |

| | | | | | | | | | | | |

Total Debt excluding PECs | | | 849.2 | | | | 851.2 | | | | 653.3 | |

| | | | | | | | | | | | |

Cash and cash equivalents | | | (200.3 | ) | | | (213.5 | ) | | | (211.4 | ) |

Short term financial investments | | | (28.7 | ) | | | — | | | | (26.9 | ) |

| | | | | | | | | | | | |

Net Debt with third parties (non-GAAP) (unaudited)(2) | | | 620.2 | | | | 637.7 | | | | 415.0 | |

| | | | | | | | | | | | |

Adjusted EBITDA (non-GAAP) for the period (unaudited) | | | 268.1 | | | | 295.1 | | | | 306.4 | |

| | | | | | | | | | | | |

Net Debt with third parties/Adjusted EBITDA (non-GAAP) (unaudited) | | | 2.3 | x | | | 2.2 | x | | | 1.4 | x |

| | | | | | | | | | | | |

| (1) | Reflects the prepayment to Telefónica of the entire indebtedness under the Vendor Loan Note. |

| (2) | In considering our financial condition, our management analyzes net debt with third parties, which is defined as total debt less cash, cash equivalents, and short-term financial investments. Net debt is not a measure defined by IFRS and it has limitations as an analytical tool. Net debt is neither a measure defined by or presented in accordance with IFRS nor a measure of financial performance, and should not be considered in isolation or as an alternative financial measure determined in accordance with IFRS. Net debt is not necessarily comparable to similarly titled measures used by other companies. |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

Risks Related to Our Business

The CRM BPO market is very competitive.

Our industry is very competitive, and we expect competition to remain intense from a number of sources in the future. In 2014, the top three CRM BPO companies, including us, represented approximately 12.5% of the global CRM BPO solutions market, based on company filings, IDC and our estimates. We believe that the principal competitive factors in the markets in which we operate are service quality, price, the ability to add value to a client’s business and industry expertise. We face competition primarily from CRM BPO companies and IT services companies. In addition, the trend toward off-shore outsourcing, international expansion by foreign and domestic competitors and continuing technological changes may result in new and different competitors entering our markets. These competitors may include entrants from the communications, software and data networking industries or entrants in geographical locations with lower costs than those in which we operate.

Some of these existing and future competitors may have greater financial, human and other resources, longer operating histories, greater technological expertise and more established relationships in the industries that we currently serve or may serve in the future. In addition, some of our competitors may enter into strategic or commercial relationships among themselves or with larger, more established companies in order to increase their ability to address customer needs and reduce operating costs, or enter into similar arrangements with potential

14

clients. Further, trends of consolidation in our industry and among CRM BPO competitors may result in new competitors with greater scale, a broader footprint, better technologies and price efficiencies attractive to our clients. Increased competition, our inability to compete successfully, pricing pressures or loss of market share could result in reduced operating profit margins which could have a material adverse effect on our business, financial condition, results of operations and prospects.

Telefónica, certain of its affiliates and a few other major clients account for a significant portion of our revenue and any loss of a large portion of business from these clients could have a material adverse effect on our business, financial condition, results of operations and prospects.

We have derived and believe that we will continue to derive a significant portion of our revenue from companies within the Telefónica Group and a few other major client groups. For the years ended December 31, 2012, 2013 and 2014, we generated 50.0%, 48.5% and 46.5%, respectively, of our revenue from the services provided to the Telefónica Group. Our contracts with Telefónica Group companies in Brazil and Spain comprised approximately 66.3% and 65.3%, respectively, of our revenue from the Telefónica Group for the years ended December 31, 2013 and 2014. Our 15 largest client groups (including the Telefónica Group) on a consolidated basis accounted for a total of 82.1% of the year ended December 31, 2014.

We are party to a master services agreement (the “MSA”) with Telefónica for the provision of certain CRM BPO services to Telefónica Group companies which governs the services agreements entered with the Telefónica Group companies. As of December 31, 2014, 38 companies within the Telefónica Group were a party to 160 arm’s-length contracts with us. While our service contracts with the Telefónica Group companies have traditionally been renewed, there can be no assurance that such contracts will be renewed upon their expiration. The MSA expires on December 31, 2021, and although the MSA is an umbrella agreement which governs our services agreements with the Telefónica Group companies, the termination of the MSA on December 31, 2021 does not automatically result in a termination of any of the local services agreements in force after that date. The MSA contemplates a right of termination prior to December 31, 2021 if a change of control of the Company occurs as a result of a sale to a Telefónica competitor. In addition, there can be no assurance that the MSA will be renewed upon its expiration. Furthermore, the MSA or any other agreement with any of the Telefónica Group companies may be amended in a manner adverse to us or terminated early.

In addition, there can be no assurance that the volume of work to be performed by us for the various Telefónica Group companies will not vary significantly from year to year in the aggregate, particularly since we are not the exclusive outsourcing provider for the Telefónica Group. As a consequence, our revenue or margins from the Telefónica Group may decrease in the future. A number of factors other than the price and quality of our work and the services we provide could result in the loss or reduction of business from Telefónica Group companies, and we cannot predict the timing or occurrence of any such event. For example, a Telefónica Group company may demand price reductions, increased quality standards, change its CRM BPO strategy, or under certain circumstances transfer some or all of the work and services we currently provide to Telefónica in-house.

The loss of a significant part of our revenue derived from these clients, in particular the Telefónica Group, as a result of the occurrence of one or more of the above events would have a material adverse effect on our business, financial condition, results of operations and prospects.

A substantial portion of our revenue, operations and investments are located in Latin America and we are therefore exposed to risks inherent in operating and investing in the region.

For the year ended December 31, 2014, we derived 33.9% of our revenue from Americas and 51.6% from Brazil. We intend to continue to develop and expand our facilities in the Americas and Brazil. Our operations and investments in the Americas and Brazil are subject to various risks related to the economic, political and social conditions of the countries in which we operate, including risks related to the following:

| | • | | inconsistent regulations, licensing and legal requirements may increase our cost of operations as we endeavor to comply with myriad of laws that differ from one country to another in an unpredictable and adverse manner; |

| | • | | currencies may be devalued or may depreciate or currency restrictions or other restraints on transfer of funds may be imposed; |

| | • | | the effects of inflation and currency depreciation and fluctuation may require certain of our subsidiaries to undertake a mandatory recapitalization; |

| | • | | governments may expropriate or nationalize assets or increase their participation in companies; |

15

| | • | | governments may impose burdensome regulations, taxes or tariffs; |

| | • | | political changes may lead to changes in the business environments in which we operate; and |

| | • | | economic downturns, political instability and civil disturbances may negatively affect our operations. |

Any deterioration in global market and economic conditions, especially in Latin America, and, in particular in the telecommunications and financial services industries from which we generate most of our revenue, may adversely affect our business, financial condition, results of operations and prospects.

Global market and economic conditions, including in Latin America, in the past several years have presented volatility and increasing risk perception, with tighter credit conditions and recession or slow growth in most major economies continuing into 2015. Our results of operations are affected directly by the level of business activity of our clients, which in turn is affected by the level of economic activity in the industries and markets that they serve. Many of our clients’ industries are especially vulnerable to any crisis in the financial and credit markets or economic downturn. A substantial portion of our clients are concentrated in the telecommunications and financial services industries which were especially vulnerable to the global financial crisis and economic downturn that began in 2008. For the year ended December 31, 2014, 49.1% of our revenue was derived from clients in the telecommunications industry. During the same period, clients in the financial services industry (including insurance) contributed 35.2% to our revenue. Our business and future growth largely depend on continued demand for our services from clients in these industries.

As our business has grown, we have become increasingly exposed to adverse changes in general global economic conditions, which may result in reductions in spending by our clients and their customers. Global economic concerns such as the varying pace of global economic recovery continue to create uncertainty and unpredictability and may have an adverse effect on the cost and availability of credit, leading to decreased spending by businesses. Any deterioration of general economic conditions, or weak economic performance in the economies of the countries in which we operate, in particular in Brazil and Americas where, for the years ended December 31, 2012, 2013 and 2014, 83.7%, 84.5% and 85.5% of our revenue (in each case, before holding company level revenue and consolidation adjustments), respectively, was generated and in our key markets such as the telecommunications and financial services industries where, for the year ended December 31, 2014, 84.3% of our revenue was generated, may have a material adverse effect on our business, financial condition, results of operations and prospects.

Increases in employee benefits expenses as well as changes to labor laws could reduce our profit margin.

Employee benefits expenses accounted for $1,609.5 million in 2012, $1,643.5 million in 2013 and $1,636.4 million in 2014, representing 69.5%, 70.2% and 71.2%, respectively, of our revenue in those periods.

Employee salaries and benefits expenses in many of the countries in which we operate, principally in Latin America, have increased during the periods presented in this Annual Report as a result of economic growth, increased demand for CRM BPO services and increased competition for trained employees such as employees at our service delivery centers in Latin America. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Total operating expenses.”

We will attempt to control costs associated with salaries and benefits as we continue to add capacity in locations where we consider wage levels of skilled personnel to be satisfactory, but we may not be successful in doing so. We may need to increase salaries more significantly and rapidly than in previous periods in an effort to remain competitive, which may have a material adverse effect on our cash flows, business, financial condition, results of operations, profit margins and prospects. In addition, we may need to increase employee compensation more than in previous periods to remain competitive in attracting the quantity and quality of employees that our business requires. Wage increases or other expenses related to the termination of our employees may reduce our profit margins and have a material adverse effect on our cash flows, business, financial condition, results of operations and prospects. If we expand our operations into new jurisdictions, we may be subject to increased operating costs, including higher employee benefits expenses in these new jurisdictions relative to our current operating costs, which could have a negative effect on our profit margin.

Furthermore, most of the countries in which we operate have labor protection laws, including statutorily mandated minimum annual wage increases, legislation that imposes financial obligations on employers and laws governing the employment of workers. These labor laws in one or more of the key jurisdictions in which we operate, particularly Brazil, may be modified in the future in a way that is detrimental to our business. If these

16

labor laws become more stringent, or if there are continued increases in statutory minimum wages or higher labor costs in these jurisdictions, it may become more difficult for us to discharge employees, or cost-effectively downsize our operations as our level of activity fluctuates, both of which would likely reduce our profit margins and have a material adverse effect on our business, financial condition, results of operations and prospects.

We may fail to attract and retain key sufficiently trained employees at our service delivery centers to support our operations, which could have a material adverse effect on our business, financial condition, results of operations and prospects.

The CRM BPO industry relies on large numbers of trained employees at service centers, and our success depends to a significant extent on our ability to attract, hire, train and retain employees. The CRM BPO industry, including us, experiences high employee turnover. On average in the year ended December 31, 2014, we experienced monthly turnover rates of 7.1% of our overall operations personnel (we include both permanent and temporary employees, counting each from his or her first day of employment with us) requiring us to continuously hire and train new employees, particularly in Latin America, where there is significant competition for trained employees with the skills necessary to perform the services we offer to our clients. In addition, we compete for employees, not only with other companies in our industry, but also with companies in other industries and in many locations where we operate there are a limited number of properly trained employees. Increased competition for these employees, in the CRM BPO industry or otherwise, could have an adverse effect on our business. Additionally, a significant increase in the turnover rate among trained employees could increase our costs and decrease our operating profit margins.

In addition, our ability to maintain and renew existing engagements, obtain new business and increase our margins will depend, in large part, on our ability to attract, train and retain employees with skills that enable us to keep pace with growing demands for outsourcing, evolving industry standards, new technology applications and changing client preferences. Our failure to attract, train and retain personnel with the experience and skills necessary to fulfill the needs of our existing and future clients or to assimilate new employees successfully into our operations could have a material adverse effect on our business, financial condition, results of operations and prospects.

Our profitability will suffer if we are not able to maintain our pricing or control or adjust costs to the level of our activity.

Our profit margin, and therefore our profitability, is largely a function of our level of activity and the rates we are able to recover for our services. If we are unable to maintain the pricing for our services or an appropriate seat utilization rate, without corresponding cost reductions, our profitability will suffer. The pricing and levels of activity we are able to achieve are affected by a number of factors, including our clients’ perceptions of our ability to add value through our services, the length of time it takes for volume of new clients to ramp up, competition, introduction of new services or products by us or our competitors, our ability to accurately estimate, attain and sustain revenue from client contracts, margins and cash flows over increasingly longer contract periods and general economic and political conditions.

Our profitability is also a function of our ability to control our costs and improve our efficiency. As we increase the number of our employees and execute our strategies for growth, we may not be able to manage the significantly larger and more geographically diverse workforce that may result, which could adversely affect our ability to control our costs or improve our efficiency. Further, because there is no certainty that our business will grow at the rate that we anticipate, we may incur expenses for the increased capacity for a significant period of time without a corresponding growth in our revenues.

If our clients decide to enter or further expand their own CRM BPO businesses in the future or current trends towards providing CRM BPO services and/or outsourcing activities are reversed, it may materially adversely affect our business, results of operations, financial condition and prospects.

None of our current agreements with our clients prevents them from competing with us in our CRM BPO business and none of our clients have entered into any non-compete agreements with us. Our current clients may seek to provide CRM BPO services similar to those we provide. Some clients conduct CRM BPO services for other parts of their own businesses and for third parties. Any decision by our key clients to enter into or further expand their CRM BPO business activities in the future could cause us to lose valuable clients and suppliers and may materially adversely affect our business, financial condition, results of operations and prospects.

17

Moreover, we have based our strategy of future growth on certain assumptions regarding our industry, legal framework, services and future demand in the market for such services. However, the trend to outsource business processes may not continue and could be reversed by factors beyond our control, including negative perceptions attached to outsourcing activities or government regulations against outsourcing activities. Current or prospective clients may elect to perform such services in-house to avoid negative perceptions that may be associated with using an off-shore provider. Political opposition to CRM BPO or outsourcing activities may also arise in certain countries if there is a perception that CRM BPO or outsourcing activities have a negative effect on employment opportunities.

In addition, our business may be adversely affected by potential new laws and regulations prohibiting or limiting outsourcing of certain core business activities of our clients in key jurisdictions in which we conduct our business, such as in Brazil. The introduction of such laws and regulations or the change in interpretation of existing laws and regulations could adversely affect our business, financial condition, results of operations and prospects.

The consolidation of the potential users of CRM BPO services may adversely affect our business, financial condition, results of operations and prospects.

Consolidation of the potential users of CRM BPO services may decrease the number of clients who contract our services. Any significant reduction in or elimination of the use of the services we provide as a result of consolidation would result in reduced net revenue to us and could harm our business. Such consolidation may encourage clients to apply increasing pressure on us to lower the prices we charge for our services, which could have a material adverse effect on our business, financial condition, results of operations and prospects.

Our operating results may fluctuate from one quarter to the next due to various factors including seasonality.

Our operating results may differ significantly from quarter to quarter and our business may be affected by factors such as: client losses, the timing of new contracts and of new product or service offerings, termination of existing contracts, variations in the volume of business from clients resulting from changes in our clients’ operations or the onset of certain parts of the year, such as the summer vacation period in our geographically diverse markets and the year-end holiday season in Latin America, the business decisions of our clients regarding the use of our services, start-up costs, delays or difficulties in expanding our operational facilities and infrastructure, changes to our revenue mix or to our pricing structure or that of our competitors, inaccurate estimates of resources and time required to complete ongoing projects, currency fluctuation and seasonal changes in the operations of our clients.

We typically generate less revenue in the first quarter of the year than in the second quarter as our clients generally spend less after the year-end holiday season. We have also found that our revenue increases in the last quarter of the year, particularly in November and December when our business benefits from the increased activity of our clients and their customers, who generally spend more money and are otherwise more active during the year-end holiday season. These seasonal effects also cause differences in revenue and income among the various quarters of any financial year, which means that the individual quarters of a year should not be directly compared with each other or used to predict annual financial results.