UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20‑F

☐REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

OR

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 001‑36744

Cnova N.V.

(Exact name of Registrant as specified in its charter)

THE NETHERLANDS

(Jurisdiction of incorporation or organization)

Cdiscount S.A., 120-126,

Quai de Bacalan CS 11584, 33067

Bordeaux Cedex, France,

+33 5 55 71 45 00

CNova Comércio Eletrônico S.A.

Rua Gomes de Carvalho 1609, Vila Olimpia 04547-006

São Paulo SP, Brazil

+55 11 4949 8000

(Address of principal executive offices)

Cnova N.V.

WTC Schiphol Airport

Tower D, 7th Floor

Schiphol Boulevard 273

1118 BH Schiphol

The Netherlands

Tel: +31 20 795 0671

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Ordinary shares, par value € 0.05 per share |

| The NASDAQ Stock Market LLC |

|

| Euronext Paris |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None.

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: As of December 31, 2015, the registrant had outstanding 441,297,846 ordinary shares, par value € 0.05 per share and 412,114,952 special voting shares, par value € 0.05 per share.

Indicate by check mark if the registrant is a well‑known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S‑T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☐ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated file, or a non‑accelerated filer. See the definitions of “accelerated filer” and “large accelerated filer” in Rule 12b‑2 of the Exchange Act (Check one):

Large accelerated filer ☐ | Accelerated filer ☒ | Non‑accelerated filer ☐ |

Indicate by check mark which basis for accounting the registrant has used to prepare the financing statements included in this filing:

U.S. GAAP ☐ | International Financial Reporting Standards as issued | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Exchange Act).

☐ Yes ☒ No

FORM 20‑F

ANNUAL REPORT FOR THE FISCAL YEAR ENDED DECEMBER 31, 2015

TABLE OF CONTENTS

|

|

|

i | ||

ii | ||

iv | ||

| 1 | ||

| 1 | ||

| 1 | ||

| 49 | ||

| 79 | ||

| 80 | ||

| 107 | ||

| 118 | ||

| 133 | ||

| 135 | ||

| 137 | ||

| 167 | ||

| 168 | ||

| 169 | ||

Material Modifications to the Rights of Security Holders and Use of Proceeds | 169 | |

| 169 | ||

| 174 | ||

| 174 | ||

| 174 | ||

| 174 | ||

| 175 | ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 175 | |

| 175 | ||

| 175 | ||

| 176 | ||

| 176 | ||

| 176 | ||

| 176 | ||

| 177 | ||

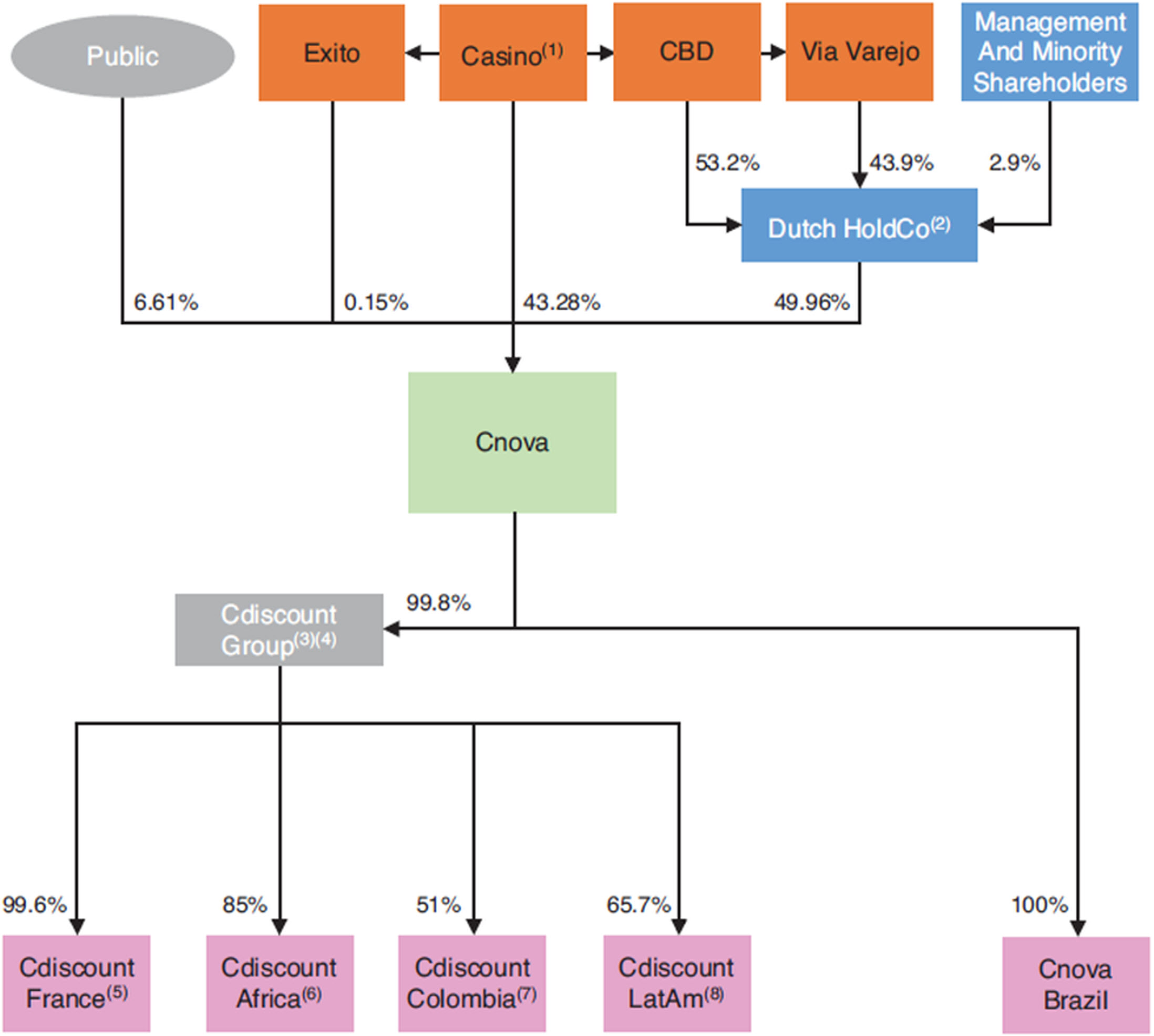

In this annual report, the terms “Cnova,” “we,” “us,” “our” and “the Company” refer to Cnova N.V. and, where appropriate, its subsidiaries. Any reference to “our brands” or “our domain names” in this annual report includes the brands “Cdiscount,” “Extra,” “Casas Bahia,” and “Ponto Frio” and related domain names, which are either registered in the names of our Parent Companies or in the name of Cdiscount, Via Varejo or our Parent Companies as more fully described herein. Additionally, unless the context indicates otherwise, the following definitions apply throughout this annual report:

|

|

|

Name |

| Definition |

Big C Supercenter |

| Big C Supercenter plc and its subsidiaries |

Casino |

| Casino, Guichard‑Perrachon S.A. |

Casino Group |

| Casino, Guichard‑Perrachon S.A. and its subsidiaries and, where appropriate, the controlling holding companies of Casino, including Rallye S.A. and Euris S.A.S. which are ultimately controlled by Mr. Jean‑Charles Naouri |

CBD |

| Companhia Brasileira de Distribuição and, where appropriate, its subsidiaries (together, commonly known as Grupo Pão de Açúcar, or GPA) |

Cdiscount |

| Cdiscount S.A. and, where appropriate, its subsidiaries |

Cdiscount Group |

| Cdiscount Group S.A.S. (formerly Casino Entreprise S.A.S.) and, where appropriate, its subsidiaries |

Cnova Brazil or Nova OpCo |

| CNova Comércio Eletrônico S.A., a wholly owned subsidiary of Cnova owning the Brazilian non‑food eCommerce businesses of CBD and Via Varejo following the completion of the 2014 Reorganization |

Dutch HoldCo |

| Marneylectro B.V., a wholly owned subsidiary of Lux HoldCo, organized under Dutch law |

Euris |

| Euris S.A.S. |

Éxito |

| Almacenes Éxito S.A. and, where appropriate, its subsidiaries |

Founding Shareholders |

| Casino, CBD, Via Varejo, Éxito and certain former managers of Nova Pontocom. The interests of CBD, Via Varejo and former managers of Nova Pontocom in Cnova are held indirectly through Lux HoldCo and/or Dutch HoldCo |

Lux HoldCo |

| Marneylectro S.à r.l., a company organized under Luxembourg law and whose entire issued share capital is held by CBD, Via Varejo and former managers of Nova Pontocom |

Nova HoldCo |

| Nova Pontocom Comércio Eletrônico S.A., following the completion of the 2014 Reorganization, which was spun off to GPA, Via Varejo and minority holders in 2015 and subsequently liquidated (as detailed in “ITEM 3.D: Risk Factors - Risks Related to the 2014 Reorganization” and “ITEM 4.C: Organizational Structure - The 2014 Reorganization” and “ITEM 4.C: Organizational Structure – The Restructurings”) |

Nova Pontocom |

| Nova Pontocom Comércio Eletrônico S.A. and, where appropriate, its subsidiaries, prior to completion of the 2014 Reorganization |

Parent Companies |

| Casino, CBD and Éxito, each of which is an affiliate of Cnova |

Rallye |

| Rallye S.A. and, where appropriate, its subsidiaries |

Via Varejo |

| Via Varejo S.A. and, where appropriate, its subsidiaries |

Voting Depository |

| Stichting Cnova Special Voting Shares |

We also have a number of other registered trademarks, service marks and pending applications relating to our brands. Solely for convenience, trademarks and trade names referred to in this annual report may appear without the “®” or “™” symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent possible under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. Except for the trademarks and domain names licensed to us by our indirect shareholders CBD and Via Varejo, we do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. Each trademark, trade name or service mark of any other company appearing in this annual report is the property of its respective holder.

This annual report includes other statistical, market and industry data and forecasts which we obtained from publicly available information and independent industry publications and reports that we believe to be reliable sources. These publicly available industry publications and reports generally state that they obtain their information from sources that they believe to be reliable, but they do not guarantee the accuracy or completeness of the information. Although we believe that these sources are reliable, we have not independently verified the information contained in such publications. Certain estimates and forecasts involve uncertainties and risks and are subject to change based on various factors, including those discussed under the headings “Special Note Regarding Forward‑Looking Statements” and “ITEM 3.D: Risk Factors” in this annual report.

i

SPECIAL NOTE REGARDING FORWARD‑LOOKING STATEMENTS

This annual report contains forward‑looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) and the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995, that are based on our management’s beliefs and assumptions and on information currently available to our management. Forward‑ looking statements include information concerning our possible or assumed future results of operations, business strategies, financing plans, competitive position, industry environment, potential growth opportunities, potential market opportunities and the effects of competition. Forward‑looking statements include all statements that are not historical facts and can be identified by terms such as “anticipates,” “believes,” “could,” “seeks,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “will,” “would” or similar expressions that convey uncertainty of future events or outcomes and the negatives of those terms. These statements include, but are not limited to, statements regarding:

· | our ability to compete successfully in our highly competitive market; |

· | our ability to maintain and grow our existing customers base; |

· | the extent to which we are able to benefit from the relationships with our Parent Companies; |

· | our ability to achieve growth in the higher‑margin areas of our business, including our marketplaces and home furnishings products category; |

· | our ability to attract and retain talented personnel; |

· | our ability to monetize traffic from mobile activity; |

· | our ability to successfully optimize, operate and manage our fulfillment centers; |

· | our ability to keep good relations with our vendors and the ability of our vendors to maintain their commercial position; |

· | our ability to protect our sites, networks and systems against security breaches; |

· | the extent to which our sites are affected by significant interruptions or delays in service; |

· | our ability to continue the use of our domain names and prevent third parties from acquiring and using domain names that infringe on our domain names; |

· | our ability to maintain and enhance our brands, as well as our customer reputation; |

· | our ability to comply with European, French, Brazilian and other laws and regulations relating to privacy and data protection; |

· | our ability to comply with additional or unexpected laws and regulations applying to our business, including consumer protection laws and tax laws; |

· | our ability to successfully integrate our businesses and realize many of the anticipated benefits of the restructurings completed in 2015 and 2016; |

· | the outcome of our internal review of Cnova Brazil; |

· | the impact on our business of the restatement of our previously issued financial statements and our identification of material weaknesses in our internal control over financial reporting; |

· | the outcome of ongoing shareholder class action litigation; and |

· | the potential reorganization of Cnova Brazil within Via Varejo and Casino’s potential tender offer of all of our publicly held ordinary shares contingent upon the completion of such reorganization. |

The forward‑looking statements contained in this annual report reflect our views as of the date of this annual report about future events and are subject to risks, uncertainties, assumptions and changes in circumstances that may cause events or our actual activities or results to differ significantly from those expressed in any forward‑looking statement. In addition, Cnova operates in highly-volatile market environments such as Brazil or other countries, subject to rapid changes and difficult macro-environment. Although we believe that the expectations reflected in the forward‑looking statements are reasonable, we cannot guarantee future events, results, actions, levels of activity,

ii

performance or achievements. Readers are cautioned not to place undue reliance on these forward‑looking statements. A number of important factors could cause actual results to differ materially from those indicated by the forward‑looking statements, including, but not limited to, those factors described in “ITEM 3.D: Risk Factors,” “ITEM 4: Information on the Company” and “ITEM 5: Operating and Financial Review and Prospects.”

All of the forward‑looking statements included in this annual report are based on information available to us as of the date of this annual report. Unless we are required to do so under U.S. federal securities laws or other applicable laws, we undertake no obligation to publicly update or revise any forward‑looking statement, whether as a result of new information, future events or otherwise.

iii

Internal Review of Cnova Brazil

As disclosed in a press release dated December 18, 2015, the Board of Directors of Cnova N.V. engaged legal counsel to work with forensic accountants and perform an internal investigation of alleged employee misconduct related to inventory management at the Company’s Brazilian subsidiary’s distribution centers (DCs). Subsequently, the scope of the investigation at the Company’s Brazilian subsidiary (“Cnova Brazil”) was expanded to include: (i) an overstatement of Cnova Brazil net sales and accounts receivable (Customers’ Claims); (ii) inconsistencies linked to the amount and valuation of damaged and/or returned items in Cnova Brazil’s inventory (Reverse Logistics); (iii) incorrect entries recorded at Cnova Brazil concerning primarily accounts payable; (iv) altered account reconciliations that were intentionally prepared by Cnova Brazil accounting staff at the direction of former Cnova Brazil personnel and provided to mislead Cnova Brazil’s independent registered public accounting firm; (v) the unsupported capitalization of software development costs related to certain vendor expenses and employee payroll expenses into intangible asset accounts; and (vi) the improper deferral of certain operating expenses at Cnova Brazil (the “Investigation”). The Investigation also identified (i) a non-recurring Brazilian Imposto sobre Operações relativas à Circulaçãode Mercadorias e Prestação (“ICMS”) tax credit of 75 million Brazilian reais related to the sale of certain products by Cnova Brazil, which was recognized by the Company in December 2014, the impact of which on the Company’s results of operations for the three months ended December 31, 2014, was not previously disclosed; (ii) misconduct by Cnova Brazil IT personnel who intentionally altered records related to user access to certain of Cnova Brazil’s IT systems to mislead the independent registered public accounting firm.

On February 24, 2016, we disclosed that the audit committee of the Company’s board of directors, in consultation with management, determined that the Company’s financial statements contained in the previously filed annual report on Form 20-F for the year ended December 31, 2014, should no longer be relied upon and would need to be restated in connection with the issues discovered. Based on the results of the internal review, we have determined that certain adjustments should be made to prior period financial statements.

In December 2015, we, through our external legal counsel, self-reported the matter to the staff of the Division of Enforcement of the United States Securities and Exchange Commission (the “Staff”), and have updated the Staff on the progress of the internal review. Our cooperation with the Staff is ongoing. We also reported the matter to the French Autorité des Marchés Financiers (“AMF”) and the Netherlands Authority for the Financial Markets (“AFM”).

In June 2016, our legal advisors and external forensic accountants completed the internal review. Based on their findings, which have been shared with the United States Securities and Exchange Commission (the “SEC”), we have restated (i) our consolidated financial statements as of and for the fiscal years ended December 31, 2013 and 2014 and (ii) our selected financial information as of and for the fiscal year ended December 31, 2012.

Restatement of Previously Issued Consolidated Financial Statements

As a result of the internal review of Cnova Brazil, we determined that net sales, cost of goods sold, inventory, accounts receivable, accounts payable and operating profit/(loss) from ordinary activities had been misstated from 2012 to 2015 and intangible assets needed to be corrected from 2012 to 2015. The nature of errors resulting from these incorrect statements are listed below and led to a correction of the accounting records processed during 2015 and the first few months of 2016. No tax impact was considered as the company assessed that the related deferred tax assets may not be recovered. In addition, the portion of adjustments listed below which relate to periods prior to July 2, 2012, the date Cnova Brazil started to be fully consolidated are recorded against the goodwill at that date:

· | Inventories: |

As of December 31, 2015, a physical count of all seven of Cnova Brazil distribution centers was completed in Brazil with the support of external consultants. The results did not reveal any significant discrepancy.

Nevertheless, the work performed allowed to identify damaged/returned items that management decided to sell to discounters in April 2016. This change in estimate led to record an additional depreciation of a cumulated amount at December 31, 2015 of R$46.9 million (including a R$4.8 million impact for 2014) based on the net realizable value approach.

· | Net Sales & Accounts Receivable: |

Prior to the internal review, under the Cnova Brazil’s customer service practice in Brazil, a customer was sent a replacement of product when a report was lodged confirming that the first delivery was either not received

iv

or was received in damaged/unsuitable condition. In many cases, the replacement shipment was sent before the missing or damaged/unsuitable merchandise was returned to Cnova Brazil, and a second sale was recorded in the company’s books. The subsidiary maintains two sales in the books, being one receivable from customers and another from freight companies. A cut-off procedure allows to adjust the second sale but was incorrectly applied and did not cancel the accumulated sales amount. As a result, the corrections of errors identified have the following impacts:

‑ Decrease of 2013 and 2014 net sales by respectively R$16.2 million and R$ 40.1 million

‑ Decrease of 2013 and 2014 cost of sales and fulfillment costs by respectively R$0.6 million and R$ 1.7 million

‑ Decrease of the related accounts receivable with freight companies as of December 31, 2013 and 2014 by respectively R$15.4 million and R$38.4 million.

The cumulative impacts of errors at Cnova Brazil were:

‑ R$110.1 million on cumulative net sales over 2015, 2014, 2013 and prior years

‑ R$57.7 million on accounts receivable as of December 31, 2015.

In addition, management discovered a sales cut-off error on orders to be billed and consequently decided to decrease 2013 and 2014 net sales by respectively R$22.7 million and R$16.7 million and increase other current liabilities for the same amounts. At Cnova Brazil, the cumulated impact on cumulative net sales is R$19.8 million.

· | Accounts Payable and Other Accounts: |

Incorrect entries concerning accounts payable and other accounts were identified. They result from manipulated reports prepared by Cnova Brazil accounting staff at the direction of former Cnova Brazil employees. Consequently, management adjusted year-end accounts payable as of December 31, 2013 and 2014 by respectively an increase of R$7.6 million and a decrease of R$0.9 million and related cost of sales in the same amounts.

At Cnova Brazil, the cumulated impact on accounts payable as of December 31, 2015 is an increase of R$48.9 million.

· | Intangible assets: |

The internal review has uncovered that invoices and employees’ time were incorrectly capitalized as part of intangible assets. Consequently, management reduced year-end intangible assets as of December 31, 2013 and 2014 by respectively R$13.9 million and R$24.2 million. This has resulted in a corresponding increase of operating expenses in the same amounts for 2013 and 2014. At Cnova Brazil, the cumulated impact on intangible assets as of December 31, 2015 is a decrease of R$71.0 million.

· | Deferred costs related to freight and other expenses: |

The internal review has uncovered that invoices were incorrectly deferred to subsequent periods and that estimated accrual of invoices to be received were inaccurate. Consequently, management increased year-end accounts payable as of December 31, 2013 and 2014 by respectively R$4.0 million and R$19.5 million and related operating costs in the same amounts. At Cnova Brazil, the cumulated impact on accounts payable as of December 31, 2015 is an increase of R$21.7 million.

v

· | Additional adjustments: |

In addition, during and after the conclusion of the internal review, Cnova management performed a thorough review of Cnova Brazil’s accounts and recorded several adjustments, some with impacts on prior years. They relate primarily to i) suppliers rebates impacting the inventory valuation, ii) fixed asset count, iii) provision for losses on accounts receivable, and iv) marketplace liabilities. The following table identifies the various impacts on the restated consolidated income statement for each period:

|

|

|

|

|

|

|

|

Accounts impacted (in R$ million) |

| Adjustment as of January 1, 2013 |

| Adjustment as of December 31, 2013 |

| Adjustment as of December 31, 2014 |

|

Trade receivables, net(i) |

| 9.0 |

| 23.2 |

| (66.1) |

|

Inventories, net |

| 5.9 |

| (3.7) |

| (8.2) |

|

Other current assets |

| 0.4 |

| 1.5 |

| (2.7) |

|

Other non current assets |

| — |

| — |

| 4.3 |

|

Trade payables |

| (6.6) |

| — |

| — |

|

Other current liabilities |

| — |

| (2.1) |

| (2.9) |

|

|

|

|

|

|

|

|

|

Accounts impacted (in R$ million) |

| Adjustment as of January 1, 2013 |

| Adjustment as of December 31, 2013 |

| Adjustment as of December 31, 2014 |

|

Net sales(i) |

| 9.0 |

| 23.2 |

| (60.9) |

|

Cost of sales |

| (0.2) |

| (2.2) |

| (8.4) |

|

Fulfillment |

| — |

| (2.1) |

| (10.3) |

|

General and administrative |

| — |

| — |

| 2.1 |

|

Other revenue |

| — |

| — |

| 3.1 |

|

Financial Result |

| — |

| — |

| 1.7 |

|

Income tax |

| — |

| — |

| (3.1) |

|

Total in Real |

| 8.8 |

| 18.9 |

| (75.8) |

|

(i) | The main adjustment being on accounting reconciliation of credit card, rebates, and wholesales. |

The cumulative balance sheet overstatement impacted cost of sales for R$12.9 million, fulfillment costs for R$33.0 million and financial expense by R$3.4 million.

All the overstatements listed in this section sum up to a negative impact on net profit (loss) of R$83.5 million as of January 1, 2013, R$5.2 million for the year 2013 and R$ 186.8 million for the year 2014 (representing a cumulated amount of R$357.8 million at December 31, 2015).

In light of the findings of the internal review, we made the determination to restate previously reported (i) consolidated financial statements as of and for the fiscal years ended December 31, 2013 and 2014 and (ii) selected financial information as of and for the fiscal year ended December 31, 2012. In addition, the accompanying restated consolidated financial statements as of and for the fiscal years ended December 31, 2013 and 2014 have been revised to reflect in the proper periods the previously recorded out-of-period adjustments described above. See Note 3, “Restatement of previously financial statements” in our audited consolidated financial statements included elsewhere in this annual report.

Controls and Procedures

Based on the results of the internal review of Cnova Brazil, our management identified: (i) control deficiencies in our internal control over financial reporting associated with: (a) entity-level controls at Cnova Brazil; (b) entity-level controls at Cnova NV; (c) replacement shipments and reverse logistics processes at Cnova Brazil distribution centers; (d) accounts reconciliations and cut-off procedures of Cnova Brazil; (e) capitalization of certain expenses at Cnova Brazil; (f) IT general controls at Cnova Brazil; and (g) deferred taxes; and (ii) the need to restate prior period consolidated financial statements. A material weakness is a deficiency, or combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the company’s annual or interim financial statements will not be prevented or detected and corrected on a timely basis. Furthermore, our Chief Executive Officer (“CEO”) and Chief Financial Officer (“CFO”), evaluated the effectiveness of the Company’s disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act), as of

vi

December 31, 2015 and concluded that, due to material weaknesses in our internal control over financial reporting, our disclosure controls and procedures were not effective as of December 31, 2015.

For a discussion of management’s consideration of our controls and procedures and material weaknesses identified, see Part II, Item“ITEM 15 - Controls and Procedures” included in this annual report.

vii

Item 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

Item 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

A. Selected Financial Data

The following tables set forth our selected consolidated financial data. The consolidated income statement data for the years ended December 31, 2013, 2014 and 2015 as well as the consolidated balance sheet data as of December 31, 2014 and 2015 are derived from our audited consolidated financial statements included in "ITEM 18: Financial Statements" and have been adjusted for the effects of the restatement more fully described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued financial statements”) to our audited consolidated financial statements.

The consolidated income statement data for the year ended December 31, 2011 as well as the consolidated balance sheet data as of December 31, 2011 and 2012 have been derived from our audited consolidated financial statements, which are not included in this annual report. The consolidated income statement data for the year ended December 31, 2012 has been derived from 2012 restated unaudited financial statements. They all have been adjusted, when applicable, from previously reported amounts for the effects of the restatement more fully described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued financial statements”) to our audited consolidated financial statements included elsewhere in this annual report. We also prepared unaudited pro forma consolidated financial information by applying certain pro forma adjustments to the historical audited consolidated financial statements of Cnova and unaudited pro forma income statement data for the year ended 2012. See “ITEM 3.A: Selected Financial Data - Unaudited Pro Forma Income Statement Data for the Years Ended December 31, 2012” for further discussion of pro forma adjustments.

The selected consolidated historical financial information should be read in conjunction with “ITEM 5: Operating and Financial Review and Prospects,” our financial statements and the accompanying notes included elsewhere in this annual report. Our financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and have been audited by Ernst & Young Audit, an independent registered public accounting firm. Following deficiencies identified during the internal review performed at Cnova Brazil, the consolidated historical financial information was restated as described in “Explanatory Note” on page iv of this annual report.

The consolidated financial statements prior to 2014 were prepared based on the operations of Cdiscount Group and Nova Pontocom, as the combined operations of these two entities are deemed to have been the predecessor of Cnova (Nova Pontocom included from July 2, 2012 - the date control of Nova Pontocom was obtained by Casino - and has been accounted for as a reorganization of entities under common control of Casino). We did not operate as a standalone entity before November 2014, and, accordingly, the following discussion is not necessarily indicative of our future performance and does not reflect what our financial performance would have been had we operated as a standalone

1

company prior to November 2014. Furthermore, our results of operations in any period may not necessarily be indicative of the results that may be expected in future periods. See “ITEM 3.D: Risk Factors” of this annual report.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Year ended December 31, |

| ||||||||||||||||

|

| 2011 |

| 2012 unaudited |

| 2013 |

| 2014 |

| 2015 |

| 2015 |

| ||||||

|

|

|

|

|

| As restated(1) |

|

| As restated(2) |

|

| As restated(2) |

|

|

|

|

|

|

|

|

| (in thousands, except per share amounts) |

| ||||||||||||||||

Consolidated Income Statement |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Sales |

| € | 1,109,707 |

| € | 1,992,342 |

| € | 2,897,047 |

| € | 3,416,368 |

| € | 3,448,511 |

| € | 3,744,738 |

|

Cost of sales |

|

| (958,314) |

|

| (1,686,353) |

|

| (2,473,902) |

|

| (2,989,946) |

|

| (3,036,834) |

|

| (3,297,698) |

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fulfillment |

|

| (69,770) |

|

| (134,679) |

|

| (202,688) |

|

| (248,218) |

|

| (275,737) |

|

| (299,422) |

|

Marketing |

|

| (33,294) |

|

| (54,020) |

|

| (78,474) |

|

| (70,009) |

|

| (77,882) |

|

| (84,572) |

|

Technology and content |

|

| (30,674) |

|

| (52,215) |

|

| (79,204) |

|

| (85,691) |

|

| (98,700) |

|

| (107,178) |

|

General and administrative |

|

| (20,362) |

|

| (29,352) |

|

| (45,250) |

|

| (49,037) |

|

| (76,739) |

|

| (83,331) |

|

Operating profit/(loss) before Restructuring, Litigation, Initial public offering expenses, Gain/(loss) from disposal of non-current assets and impairment of assets |

|

| (2,710) |

|

| 35,724 |

|

| 17,529 |

|

| (26,533) |

|

| (117,381) |

|

| (127,464) |

|

Restructuring |

|

| (2,412) |

|

| (2,897) |

|

| (2,790) |

|

| (8,413) |

|

| (17,133) |

|

| (18,604) |

|

Litigation |

|

| 751 |

|

| (124) |

|

| (3,145) |

|

| (3,135) |

|

| (3,124) |

|

| (3,392) |

|

Initial public offering expenses |

|

| — |

|

| — |

|

| — |

|

| (15,985) |

|

| (3,702) |

|

| (4,020) |

|

Gain/(loss) from disposal of non-current assets |

|

| (271) |

|

| (644) |

|

| 835 |

|

| 14 |

|

| (6,108) |

|

| (6,633) |

|

Impairment of assets |

|

| (158) |

|

| (2,845) |

|

| (1,139) |

|

| (2,588) |

|

| (14,614) |

|

| (15,869) |

|

Operating profit/(loss) |

|

| (4,800) |

|

| 29,213 |

|

| 11,290 |

|

| (56,640) |

|

| (162,062) |

|

| (175,983) |

|

Financial income |

|

| 1,718 |

|

| 3,119 |

|

| 5,297 |

|

| 8,091 |

|

| 34,602 |

|

| 37,574 |

|

Financial expense |

|

| (4,960) |

|

| (27,065) |

|

| (60,900) |

|

| (75,487) |

|

| (94,615) |

|

| (102,743) |

|

Profit/(loss) before tax |

|

| (8,042) |

|

| 5,268 |

|

| (44,312) |

|

| (124,035) |

|

| (222,075) |

|

| (241,151) |

|

Income tax gain/(expense) |

|

| (1,666) |

|

| (6,177) |

|

| 15,704 |

|

| 13,113 |

|

| (20,308) |

|

| (22,052) |

|

Share of profits/(losses) of associates |

|

| — |

|

| — |

|

| — |

|

| (2,369) |

|

| — |

|

| — |

|

Net profit(loss) from continuing activities |

|

| (9,707) |

|

| (909) |

|

| (28,608) |

|

| (113,291) |

|

| (242,383) |

|

| (263,203) |

|

Net profit/(loss) from discontinuing activities |

|

| — |

|

| (229) |

|

| 180 |

|

| (1,864) |

|

| (16,665) |

|

| (18,097) |

|

Net profit/(loss) for the year |

|

| (9,707) |

|

| (1,138) |

|

| (28,428) |

|

| (115,155) |

|

| (259,048) |

|

| (281,300) |

|

Attributable to Cnova equity owners |

|

| (9,643) |

|

| (1,432) |

|

| (27,696) |

|

| (112,495) |

|

| (244,223) |

|

| (265,202) |

|

Attributable to non-controlling interests |

|

| (64) |

|

| 293 |

|

| (733) |

|

| (2,660) |

|

| (14,825) |

|

| (16,098) |

|

Earnings (loss) per share (in € and $ respectively) |

|

| (0.05) |

|

| (0.02) |

|

| (0.07) |

|

| (0.27) |

|

| (0.55) |

|

| (0.60) |

|

Diluted earnings per share (in € and $ respectively) |

|

| (0.05) |

|

| (0.02) |

|

| (0.07) |

|

| (0.27) |

|

| (0.55) |

|

| (0.60) |

|

2

(1) | The information for the year ended December 31, 2012 has been adjusted and includes the 2012 related corrections uncovered by the internal investigation in Brazil as well as the other adjustments related to 2012 both mentioned in the “Explanatory Note” on page iv of this annual report. |

(2) | The effects of the restatement on the Company’s consolidated income statement for the year ended December 31, 2013 and 2014 are described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued financial statements”) to our audited consolidated financial statements. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| As of December 31, |

| ||||||||||

|

| 2011 |

| 2012 unaudited |

| 2013 |

| 2014 |

| 2015 |

| 2015 |

|

|

|

|

| As restated(1) |

| As restated(2) |

| As restated(2) |

|

|

|

|

|

|

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| ($ thousands) |

|

Consolidated Balance Sheet data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

| 31,578 |

| 176,601 |

| 263,550 |

| 573,321 |

| 400,793 |

| 435,221 |

|

Trade receivables, net |

| 119,020 |

| 118,723 |

| 120,745 |

| 117,656 |

| 129,651 |

| 140,788 |

|

Inventories, net |

| 119,574 |

| 274,775 |

| 360,674 |

| 400,111 |

| 414,956 |

| 450,601 |

|

Total assets |

| 478,304 |

| 1,537,391 |

| 1,716,191 |

| 2,140,043 |

| 1,718,651 |

| 1,866,283 |

|

Trade payables |

| 358,583 |

| 742,616 |

| 920,450 |

| 1,311,234 |

| 1,216,022 |

| 1,320,479 |

|

Financial debt |

| 21,495 |

| 78,005 |

| 163,317 |

| 104,603 |

| 146,968 |

| 159,592 |

|

Total equity |

| 52,016 |

| 585,258 |

| 469,436 |

| 521,542 |

| 98,071 |

| 106,495 |

|

(1) | The information for the year ended December 31, 2012 has been adjusted and includes the 2012 related corrections uncovered by the internal investigation in Brazil as well as the other adjustments related to 2012 both mentioned in the “Explanatory Note” on page iv of this annual report. |

(2) | The effects of the restatement on the Company’s consolidated balance sheets as of December 31, 2013 and 2014 are described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued financial statements”) to our audited consolidated financial statements. |

The share capital of Cnova is composed of 441,297,846 ordinary shares as of December 31, 2015.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| For the Year ended December 31, |

| |||||||||||||||||||

|

| 2011 |

| 2012 unaudited |

| 2013 |

| 2014 |

| 2015 |

| |||||||||||

|

|

|

|

| Actual |

| Pro Forma |

|

|

|

|

|

|

|

|

|

|

|

|

| ||

€ thousands |

|

|

|

|

| As restated (1) |

| As restated(2) |

| As restated(2) |

|

|

|

|

| |||||||

Other Financial Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross profit (thousands)(3) |

| € | 151,393 |

| € | 305,990 |

| € | 369,496 |

| € | 423,145 |

| € | 426,422 |

| € | 411,677 |

| $ | 447,040 |

|

Adjusted EBITDA (thousands)(4) |

| € | 7,542 |

| € | 53,042 |

| € | 24,213 |

| € | 43,986 |

| € | 4,228 |

| € | (79,902) |

| $ | (86,766) |

|

Free cash flow - continuing activities (thousands)(5) |

| € | (6,325) |

| € | 155,587 |

| € | 105,300 |

| € | 122,589 |

| € | 210,975 |

| € | (64,154) |

| $ | (69,665) |

|

Net cash/(Net financial debt) (thousands)(6) |

| € | 54,471 |

| € | 151,725 |

| € | 190,733 |

| € | 164,060 |

| € | 533,878 |

| € | 253,838 |

| $ | 275,643 |

|

(1) | The information for the year ended December 31, 2012 has been adjusted and includes the 2012 related corrections uncovered by the internal investigation in Brazil as well as the other adjustments related to 2012 both mentioned in the “Explanatory Note” on page iv of this annual report. |

(2) | The effects of the restatement on the Company’s consolidated balance sheets as of December 31, 2013 and 2014 are described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued Financial Statements”) to our audited consolidated financial statements. |

(3) | Gross profit is a non-GAAP financial measure that we calculate as net sales minus cost of sales. Please see "Non-GAAP Financial Measures -Gross Profit and Gross Margin" for more information and for the computation of gross profit. |

(4) | Adjusted EBITDA is a non-GAAP financial measure that we calculate as operating profit/(loss) before restructuring, litigation, initial public offering expenses, gain/(loss) from disposal of non-current assets and impairment of assets and before depreciation and amortization expense and share-based payments. Please see "Non-GAAP Financial Measures - Adjusted EBITDA" for more information and for a reconciliation of adjusted EBITDA to operating profit/(loss) before restructuring, litigation, initial public offering expenses, gain/(loss) from disposal of non-current assets and impairment of assets, the most directly comparable financial measure calculated and presented in accordance with GAAP. |

3

(5) | Free cash flow is a non-GAAP financial measure that we calculate as net cash from/(used in) operating activities as presented in our cash flow statement less capital expenditures (purchase of property and equipment and intangible assets). Please see "Non-GAAP Financial Measures - Free Cash Flow and Free Cash Flow Less the Financial Expense Paid in Relation to Factoring Activities" for more information and for a reconciliation of free cash flow to net cash from/(used in) operating activities, the most directly comparable financial measure calculated and presented in accordance with GAAP. |

(6) | Net cash/(net financial debt) is a non-GAAP financial measure that we calculate as the sum of cash and cash equivalents and cash pool balances held in arrangements with Casino Group and presented in other current assets, less current and non-current financial debt. Please see "Non-GAAP Financial Measures – Net cash/(net financial debt)" for more information and for a reconciliation of net cash/(net financial debt) to non-current financial debt, the most directly comparable financial measure calculated and presented in accordance with GAAP. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| For the Year ended December 31, | |||||||||||||||||||

|

| 2011 |

| 2012 unaudited |

| 2013 |

| 2014 |

| 2015 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

€ thousands (except Adjusted EPS) |

|

|

| Actual |

| Pro Forma |

| As restated(2) |

| As restated(2) |

|

|

|

| |||||||

New Other Financial Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted net profit/(loss) attributable to equity holders of Cnova (thousands)(3) |

| € | (7,737) |

| € | 3,332 |

| € | (43,594) |

| € | (29,197) |

| € | (87,170) |

| € | (189,533) |

| $ | (205,814) |

Adjusted EPS(4) |

| € | (0.04) |

| € | 0.01 |

| € | (0.11) |

| € | (0.07) |

| € | (0.22) |

| € | (0.45) |

| $ | (0.49) |

(1) | The information for the year ended December 31, 2012 has been adjusted and includes the 2012 related corrections uncovered by the internal investigation in Brazil as well as the other adjustments related to 2012 both mentioned in the “Explanatory Note” on page iv of this annual report. |

(2) | The effects of the restatement on the Company’s consolidated income statement for the year ended December 31, 2013 and 2014 are described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued financial statements”) to our audited consolidated financial statements. |

(3) | Adjusted net profit/(loss) attributable to equity holders of Cnova is a non-GAAP financial measure that we calculate as net profit/(loss) attributable to equity holders of Cnova before restructuring, litigation, initial public offering expenses, gain/(loss) from disposal of non-current assets and impairment of assets and the related tax impacts. Please see "-Non-GAAP Financial Measures-Adjusted Net Profit/(loss) attributable to equity holders of Cnova / Adjusted EPS" for more information and for a reconciliation of adjusted net profit/(loss) attributable to equity holders of Cnova to net profit/(loss) attributable to equity holders of Cnova, the most directly comparable financial measure calculated and presented in accordance with GAAP. |

(4) | Adjusted EPS is a non-GAAP financial measure that we calculate as adjusted net profit/(loss) attributable to equity holders of Cnova divided by the weighted average number of outstanding ordinary shares of Cnova during the applicable period. Please see "-Non-GAAP Financial Measures-Adjusted Net Profit/(Loss) Attributable to Equity Holders of Cnova and Adjusted EPS" for more information and for a reconciliation of adjusted net profit/(loss) attributable to equity holders of Cnova to net profit/(loss) attributable to equity holders of Cnova, the most directly comparable financial measure calculated and presented in accordance with GAAP, and the related adjusted EPS. |

The following table sets forth selected operating data that Cnova uses as measures of its operating performance.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| For the Year ended December 31, |

|

|

| |||||||||||||

|

| 2011 |

| 2012 unaudited |

| 2013 |

| 2014 |

| 2015 |

| 2015 |

| |||||

Operating Data:(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

GMV (millions)(2) |

| € | 2,828.0 |

| € | 3,114.8 |

| € | 3,569.5 |

| € | 4,443.4 |

| € | 4,868.0 | $ | 5,286.1 |

|

GMV Cdiscount (millions)(2) |

| € | 1,335.1 |

| € | 1,624.1 |

| € | 1,900.1 |

| € | 2,288.2 |

| € | 2,741.5 | $ | 2,977.0 |

|

GMV Cdiscount France (millions)(2) |

| € | 1,335.1 |

| € | 1,624.1 |

| € | 1,900.1 |

| € | 2,277.9 |

| € | 2,709.3 | $ | 2,942.0 |

|

GMV Cdiscount International (millions)(2) |

| € | — |

| € | — |

| € | — |

| € | 10.3 |

| € | 32.2 | $ | 34.9 |

|

GMV Cnova Brazil (millions)(2) |

| € | 1,492.9 |

| € | 1,490.7 |

| € | 1,669.4 |

| € | 2,155.2 |

| € | 2,126.5 | $ | 2,309.2 |

|

Marketplace share(3) |

|

| 0% |

|

| 3% |

|

| 7% |

|

| 12% |

|

| 20% |

| 20% |

|

Marketplace share Cdiscount France(3) |

|

| 1% |

|

| 6% |

|

| 12% |

|

| 19% |

|

| 27% |

| 27% |

|

Marketplace share Cnova Brazil(3) |

|

| — |

|

| — |

|

| 1% |

|

| 4% |

|

| 11% |

| 11% |

|

Active customers (millions)(4) |

|

| 7.5 |

|

| 8.9 |

|

| 11.0 |

|

| 13.5 |

|

| 14.9 |

| 14.9 |

|

Orders (millions)(5) |

|

| 15.6 |

|

| 18.8 |

|

| 23.6 |

|

| 31.5 |

|

| 38.3 |

| 38.3 |

|

Number of items in placed orders |

|

| 32.4 |

|

| 36.9 |

|

| 43.9 |

|

| 55.5 |

|

| 66.9 |

| 66.9 |

|

Traffic (visits in millions)(6) |

|

| 716.1 |

|

| 895.2 |

|

| 1,099.1 |

|

| 1,326.6 |

|

| 1,710.6 |

| 1,710.6 |

|

4

(1) | Operating data, other than GMV Cdiscount France, GMV Cdiscount International, GMV Cnova Brazil, Marketplace share Cdiscount France and Marketplace share Cnova Brazil, are given for Cnova on a consolidated basis. Operating data, other than GMV, GMV Cdiscount, GMV Cdiscount France, GMV Cdiscount International and GMV Cnova Brazil, do not include our business-to-business ("B2B") sales. |

(2) | Gross Merchandise Volume (GMV) is defined as the sum of product sales, other revenues, marketplace business volumes (calculated based on approved and sent orders) and taxes. 2012 to 2015 GMV were also adjusted to reflect the effects of the restatement of the Company. |

(3) | Marketplace share of GMV includes marketplace share of www.cdiscount.com in France as well as extra.com.br, pontofrio.com, casasbahia.com.br and cdiscount.com.br in Brazil |

(4) | Active customers are customers having purchased at least once through our sites during each of the years indicated in the table above, calculated on a website-by-website basis because we operate multiple sites, each with unique systems of identifying users, which could result in an individual being counted more than once. |

(5) | Total number of placed orders before cancellation due to fraud detection and/or customer non-payment. |

(6) | Number of visits to our websites in millions. |

Exchange Rates

All references in this annual report to “U.S. dollars” or “$” are to the legal currency of the United States, all references to “€” or “euro” are to the currency introduced at the start of the third stage of the European economic and monetary union pursuant to the treaty establishing the European Community, as amended, and all references to the “real” or “R$” are to Brazilian reais, the official currency of the Federative Republic of Brazil (“Brazil”). This annual report contains translations of euro amounts into U.S. dollars at specific rates. Unless otherwise noted, all translations from euros to U.S. dollars and from U.S. dollars to euros in this annual report were made at a rate of $1.0859 per euro, the exchange rate set forth in the H.10 statistical release of the U.S. Federal Reserve Board on December 31, 2015.

The tables below show the high, low, average and period end exchange rates of U.S. dollars per euro for the periods shown. Average rates are computed by using the noon buying rate of the Federal Reserve Bank of New York for the euro on each business day during the relevant year indicated or each business day during the relevant month indicated.

|

|

|

|

|

|

|

|

|

|

Year ended December 31, |

| High |

| Low |

| Average |

| Year-End |

|

2011 |

| 1.4875 |

| 1.2926 |

| 1.3931 |

| 1.2973 |

|

2012 |

| 1.3463 |

| 1.2062 |

| 1.2859 |

| 1.3186 |

|

2013 |

| 1.3816 |

| 1.2774 |

| 1.3281 |

| 1.3779 |

|

2014 |

| 1.3927 |

| 1.2101 |

| 1.3297 |

| 1.2101 |

|

2015 |

| 1.2015 |

| 1.0524 |

| 1.1096 |

| 1.0859 |

|

|

|

|

|

|

|

|

|

|

|

Month Ended |

| High |

| Low |

| Average |

| Month-End |

|

January 31, 2016 |

| 1.0964 |

| 1.0743 |

| 1.0855 |

| 1.0832 |

|

February 29, 2016 |

| 1.1362 |

| 1.0868 |

| 1.1092 |

| 1.0868 |

|

March 31, 2016 |

| 1.1390 |

| 1.0845 |

| 1.1134 |

| 1.1390 |

|

April 30, 2016 |

| 1.1441 |

| 1.1239 |

| 1.1346 |

| 1.1441 |

|

May 31, 2016 |

| 1.1516 |

| 1.1135 |

| 1.1312 |

| 1.1135 |

|

June 30, 2016 |

| 1.1400 |

| 1.1024 |

| 1.1232 |

| 1.1032 |

|

The noon buying rate of the Federal Reserve Bank of New York for the euro on June 30, 2016 was €1.00 = $ 1.1032.

The tables below show the high, low, average and period-end exchange rates of euros per real for the periods shown. Average rates are computed by using the foreign exchange reference rate as published by the European Central

5

Bank on its website for the real on each business day during the relevant year indicated or each business day during the relevant month indicated.

|

|

|

|

|

|

|

|

|

|

Year ended December 31, |

| High |

| Low |

| Average |

| Year-End |

|

2011 |

| 0.4585 |

| 0.3896 |

| 0.4303 |

| 0.4139 |

|

2012 |

| 0.4449 |

| 0.3613 |

| 0.3999 |

| 0.3699 |

|

2013 |

| 0.3955 |

| 0.3070 |

| 0.3507 |

| 0.3070 |

|

2014 |

| 0.3443 |

| 0.2924 |

| 0.3208 |

| 0.3105 |

|

2015 |

| 0.3442 |

| 0.2114 |

| 0.2743 |

| 0.2319 |

|

|

|

|

|

|

|

|

|

|

|

Month Ended |

| High |

| Low |

| Average |

| Month-End |

|

January 31, 2016 |

| 0.2324 |

| 0.2211 |

| 0.2272 |

| 0.2258 |

|

February 29, 2016 |

| 0.2312 |

| 0.2218 |

| 0.2276 |

| 0.2304 |

|

March 31, 2016 |

| 0.2518 |

| 0.2298 |

| 0.2428 |

| 0.2429 |

|

April 30, 2016 |

| 0.2539 |

| 0.2381 |

| 0.2478 |

| 0.2516 |

|

May 31, 2016 |

| 0.2537 |

| 0.2434 |

| 0.2501 |

| 0.2509 |

|

June 30, 2016 |

| 0.2786 |

| 0.2485 |

| 0.2595 |

| 0.2786 |

|

The reference rate of the European Central Bank for the real on June 30, 2016 was R$1.00 = € 0.2786.

We make no representation that any euro, U.S. dollar or Brazilian real amounts could have been, or could be, converted into U.S. dollars or euro, as the case may be, at any particular rate, at the rates stated above, or at all. The rates set forth above are provided solely for the reader’s convenience and may differ from the actual rates used in the preparation of the consolidated financial statements included in this annual report and other financial data appearing in this annual report.

Non‑GAAP Financial Measures

Gross Profit and Gross Margin

We define gross profit as net sales less cost of sales and gross margin as gross profit as a percentage of net sales. Gross profit and gross margin are included as a supplemental disclosure because they are performance measures used by our management and board of directors (the “board” or “board of directors”) to determine the commercial performance of our business.

The following table presents a computation of gross profit and gross margin for each of the periods indicated:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Year ended December 31, |

| ||||||||||||

|

| 2011 |

| 2012 unaudited |

| 2013 |

| 2014 |

| 2015 | 2015 |

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Actual |

| Pro Forma |

| As restated(2) |

| As restated(2) |

|

|

|

|

|

|

| (€ thousands, |

| (€ thousands, |

| (€ thousands, |

| (€ thousands, |

| (€ thousands, |

| ($ thousands, |

| ||

|

| except Gross margin) |

| except Gross margin) |

| except Gross margin) |

| except Gross margin) |

| except Gross margin) |

| except Gross margin) |

| ||

Net sales |

| 1,109,707 |

| 1,992,342 |

| 2,640,296 |

| 2,897,047 |

| 3,416,368 |

| 3,448,511 |

| 3,744,738 |

|

Less: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cost of sales |

| (958,314) |

| (1,686,353) |

| (2,270,800) |

| (2,473,902) |

| (2,989,946) |

| (3,036,834) |

| (3,297,698) |

|

Gross Profit |

| 151,393 |

| 305,990 |

| 369,496 |

| 423,145 |

| 426,422 |

| 411,677 |

| 447,040 |

|

Gross margin |

| 13.6% |

| 15.4% |

| 14.0% |

| 14.6% |

| 12.5% |

| 11.9% |

| 11.9% |

|

(1) | The information for the year ended December 31, 2012 has been adjusted and includes the 2012 related corrections uncovered by the internal investigation in Brazil as well as the other adjustments related to 2012 both mentioned in the “Explanatory Note” on page iv of this annual report. |

6

(2) | The effects of the restatement on the Company’s consolidated income statement for the year ended December 31, 2013 and 2014 are described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued financial statements”) to our audited consolidated financial statements. |

Adjusted EBITDA

To provide investors with additional information regarding our financial results, we have disclosed in the table below and elsewhere in this annual report adjusted EBITDA, a non-GAAP financial measure that we calculate as operating profit/(loss) before restructuring, litigation, initial public offering expenses, gain/(loss) from disposal of non-current assets and impairment of assets and before depreciation and amortization expense and share-based payment. We have provided a reconciliation below of adjusted EBITDA to operating profit/(loss) before restructuring, litigation, initial public offering expenses, gain/(loss) from disposal of non-current assets and impairment of assets, the most directly comparable GAAP financial measure.

We have included adjusted EBITDA in this annual report because it is a key measure used by our management and board of directors to evaluate our operating performance, generate future operating plans and make strategic decisions regarding the allocation of capital. In particular, the exclusion of certain expenses in calculating adjusted EBITDA facilitates operating performance comparisons on a period-to-period basis and, in the case of exclusion of the impact of stock-based compensation, excludes an item that we do not consider to be indicative of our core operating performance. Accordingly, we believe that adjusted EBITDA provides useful information to investors and others in understanding and evaluating our operating results in the same manner as our management and board of directors.

Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are:

· | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future, and adjusted EBITDA does not reflect cash capital expenditure requirements for such replacements or for new capital expenditure requirements; |

· | adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

· | adjusted EBITDA does not consider the potentially dilutive impact of equity-based compensation; |

· | adjusted EBITDA does not reflect tax payments that may represent a reduction in cash available to us; and |

· | other companies, including companies in our industry, may calculate adjusted EBITDA differently, which has an impact on its usefulness as a comparative measure. |

Because of these limitations, you should consider adjusted EBITDA in conjunction with other financial performance measures, including various cash flow metrics, operating profit/(loss) and our other GAAP results.

7

The following table reflects the reconciliation of operating profit/(loss) before restructuring, litigation, initial public offering expenses, gain/(loss) from disposal of non-currents assets and impairment of assets to adjusted EBITDA for each of the periods indicated:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Year ended December 31, |

| ||||||||||||

€ millions |

| 2011 |

| 2012 unaudited |

| 2013 |

| 2014 |

| 2015 |

| 2015 |

| ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Actual |

| Pro Forma |

| As restated(2) |

| As restated(2) |

|

|

|

|

|

|

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| ($ thousands) |

| ||

Operating profit/(loss) before restructuring, initial public offering expenses, litigation, gain/(loss) from disposal of non-current assets and impairment of assets |

| (2,710) |

| 35,724 |

| 2,751 |

| 17,529 |

| (26,533) |

| (117,381) |

| (127,464) |

|

Excluding: Share based payment expenses |

| 59 |

| 505 |

| 736 |

| 393 |

| 50 |

| 689 |

| 748 |

|

Excluding: Depreciation and amortization |

| 10,193 |

| 16,813 |

| 20,726 |

| 26,064 |

| 30,711 |

| 36,790 |

| 39,950 |

|

Adjusted EBITDA |

| 7,542 |

| 53,042 |

| 24,213 |

| 43,986 |

| 4,228 |

| (79,902) |

| (86,766) |

|

(1) | The information for the year ended December 31, 2012 has been adjusted and includes the 2012 related corrections uncovered by the internal investigation in Brazil as well as the other adjustments related to 2012 both mentioned in the “Explanatory Note” on page iv of this annual report. |

(2) | The effects of the restatement on the Company’s consolidated income statement for the year ended December 31, 2013 and 2014 are described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued financial statements”) to our audited consolidated financial statements. |

Adjusted Net Profit/(Loss) Attributable to Equity Holders of Cnova and Adjusted EPS

Adjusted net profit/(loss) attributable to equity holders of Cnova is calculated as net profit/(loss) attributable to equity holders of Cnova before restructuring, litigation, initial public offering expenses, gain/(loss) from disposal of non-current assets and impairment of assets and the related tax impacts. Adjusted EPS is calculated as adjusted net profit/(loss) attributable to equity holders of Cnova divided by the weighted average number of outstanding ordinary shares of Cnova during the applicable period. We have provided a reconciliation below of adjusted net profit/(loss) attributable to equity holders of Cnova to net profit/(loss) attributable to equity holders of Cnova, the most directly comparable GAAP financial measure.

Adjusted net profit/(loss) attributable to equity holders of Cnova is a financial measure used by Cnova's management and board of directors to evaluate the overall financial performance of the business. In particular, the

8

exclusion of certain expenses in calculating adjusted net profit/(loss) attributable to equity holders of Cnova facilitates the comparison of income on a period-to-period basis.

The following table reflects the reconciliation of net profit/(loss) attributable to equity holders of Cnova to adjusted net profit/(loss) attributable to equity holders of Cnova and presents the computation of Adjusted EPS for each of the periods indicated.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 2011 |

| 2012 unaudited |

| 2013 |

| 2014 |

| 2015 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Actual |

| Pro Forma |

| As restated(2) |

| As restated(2) |

|

|

|

|

|

|

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| ($ thousands) |

| ||

Net profit/(loss) for the year attributable to equity holders of Cnova |

| (9,643) |

| (3,241) |

| (49,668) |

| (27,665) |

| (110,697) |

| (232,189) |

| (252,134) |

|

Excluding: restructuring expenses |

| 2,412 |

| 2,897 |

| 2,897 |

| 2,790 |

| 8,413 |

| 17,133 |

| 18,605 |

|

Excluding: litigation expenses |

| (751) |

| 124 |

| 124 |

| 3,145 |

| 3,135 |

| 3,124 |

| 3,392 |

|

Excluding: initial public offering expenses |

|

|

| — |

| — |

| — |

| 15,985 |

| 3,702 |

| 4,020 |

|

Excluding gain / (loss) from disposal of non-current assets |

| 271 |

| 644 |

| 644 |

| (835) |

| (14) |

| 6,108 |

| 6,633 |

|

Excluding: impairment of assets charges |

| 158 |

| 2,845 |

| 2,240 |

| 1,139 |

| 2,588 |

| 14,614 |

| 15,869 |

|

Excluding: income tax effect on above adjustments |

| (171) |

| (218) |

| (21) |

| (478) |

| (6,482) |

| (1,432) |

| (1,555) |

|

Excluding: recognition of previously unrecognized tax losses |

|

|

| 349 |

| 238 |

| (7,300) |

| — |

| — |

| — |

|

Excluding: minority interest effect on above adjustments |

| (13) |

| (68) |

| (48) |

| 7 |

| (98) |

| (593) |

| (644) |

|

Adjusted net profit/(loss) for the year attributable to equity holders of Cnova |

| (7,737) |

| 3,332 |

| (43,594) |

| (29,197) |

| (87,170) |

| (189,533) |

| (205,814) |

|

Weighted average number of ordinary shares |

| 190,974,069 |

| 301,214,819 |

| 411,455,569 |

| 411,455,569 |

| 414,961,806 |

| 441,297,846 |

| 441,297,846 |

|

Adjusted EPS on continued activities (€) |

| (0.04) |

| 0.01 |

| (0.11) |

| (0.07) |

| (0.21) |

| (0.43) |

| (0.47) |

|

Adjusted EPS on discontinued activities (€) |

|

|

| — |

| — |

| 0.00 |

| (0.01) |

| (0.02) |

| (0.03) |

|

Adjusted EPS (€) |

| (0.04) |

| 0.01 |

| (0.11) |

| (0.07) |

| (0.22) |

| (0.45) |

| (0.49) |

|

(1) | The information for the year ended December 31, 2012 has been adjusted and includes the 2012 related corrections uncovered by the internal investigation in Brazil as well as the other adjustments related to 2012 both mentioned in the “Explanatory Note” on page iv of this annual report. |

(2) | The effects of the restatement on the Company’s consolidated income statement for the year ended December 31, 2013 and 2014 are described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued financial statements”) to our audited consolidated financial statements |

Free Cash Flow and Free Cash Flow less the Financial Expense Paid in Relation to Factoring Activities

To provide investors with additional information regarding our financial results, we have also disclosed in the table below and elsewhere in this annual report free cash flow and free cash flow less the financial expense paid in relation to factoring activities, non-GAAP financial measures that we calculate as follows:

· | free cash flow is calculated as net cash from/(used in) operating activities as presented in our cash flow statement less capital expenditures (purchases of intangible assets, property and equipment), and |

· | free cash flow less the financial expense paid in relation to factoring activities is calculated as net cash from/(used in) operating activities as presented in our cash flow statement less capital expenditures (purchases of intangible assets, property and equipment) less the financial expense paid in relation to factoring activities. |

We have provided below a reconciliation of free cash flow and free cash flow less the financial expense paid in relation to factoring activities to net cash from/(used in) operating activities, the most directly comparable GAAP financial measure.

We have included free cash flow and free cash flow less the financial expense paid in relation to factoring activities in this annual report because they are measures that provide useful information to management and investors about the amount of cash generated by our business. Accordingly, we believe that free cash flow and free cash flow less the financial expense paid in relation to factoring activities provide useful information to management to run our

9

business and allocate resources. Free cash flow and free cash flow less the financial expense paid in relation to factoring activities also reflect changes in working capital.

Free cash flow and free cash flow less the financial expense paid in relation to factoring activities do not represent the increase or decrease in our cash balance, and you should not consider them in isolation or as substitutes for analysis of our results or cash flows as reported under GAAP. There are limitations to using free cash flow and free cash flow less the financial expense paid in relation to factoring activities as analytical tools, including that other companies, among them companies in our industry, may calculate free cash flow and free cash flow less the financial expense paid in relation to factoring activities differently or not at all. Because of these limitations, you should consider free cash flow and free cash flow less the financial expense paid in relation to factoring activities alongside other financial performance measures, including net cash from/(used in) operating activities, capital expenditures and our other GAAP results.

The following table presents a reconciliation of net cash from/(used in) operating activities to free cash flow and free cash flow less the financial expense paid in relation to factoring activities for each of the periods indicated:

10

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Year ended December 31, | ||||||||||||

|

| 2011 |

| 2012 unaudited |

| 2013 |

| 2014 |

| 2015 |

| 2015 | ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Actual |

| Pro Forma |

| As restated(2) |

| As restated(2) |

|

|

|

|

|

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| (€ thousands) |

| ($ thousands) |

Net cash from/(used in) continuing operating activities(3) |

| 17,630 |

| 192,639 |

| 150,934 |

| 171,108 |

| 282,144 |

| 2,322 |

| 2,521 |

Net cash from/(used in) discontinued operating activities |

| — |

| — |

| — |

| (932) |

| (2,037) |

| (7,337) |

| (7,967) |

Less purchase of property and equipment and intangible assets - continuing activities |

| (23,955) |

| (37,052) |

| (45,633) |

| (48,519) |

| (71,169) |

| (66,476) |

| (72,186) |

Less purchase of property and equipment and intangible assets - discontinued activities |

| — |

| — |

| — |

| — |

| 4,891 |

| (1,557) |

| (1,691) |

Free cash flow - continuing activities |

| (6,325) |

| 155,587 |

| 105,300 |

| 122,589 |

| 210,975 |

| (64,154) |

| (69,665) |

Free cash flow - discontinued activities |

| — |

| — |

| — |

| (932) |

| 2,854 |

| (8,894) |

| (9,658) |

Less financial expense paid in relation to factoring activities |

| — |

| (18,744) |

| (18,744) |

| (45,352) |

| (60,084) |

| (78,321) |

| (85,049) |

Free cash flow less financial expenses paid in relation to factoring activities - continuing activities |

| (6,325) |

| 136,843 |

| 86,556 |

| 77,237 |

| 150,891 |

| (142,475) |

| (154,714) |

Free cash flow less financial expenses paid in relation to factoring activities - discontinued activities |

| — |

| — |

| — |

| (932) |

| 2,854 |

| (8,894) |

| (9,658) |

(1) | The information for the year ended December 31, 2012 has been adjusted and includes the 2012 related corrections uncovered by the internal investigation in Brazil as well as the other adjustments related to 2012 both mentioned in the “Explanatory Note” on page iv of this annual report. |

(2) | The effects of the restatement on the Company’s consolidated income statement for the year ended December 31, 2013 and 2014 are described in the “Explanatory Note” on page iv of this annual report and in Note 3 (“Restatement of previously issued financial statements”) to our audited consolidated financial statements. |

11

Net cash/(net financial debt)