UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

|

| |

| o | Registration statement pursuant to Section 12(b) or 12(g) of the Securities Exchange Act of 1934 |

or

|

| |

| x | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended December 31, 2015 |

or

|

| |

| o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

or

|

| |

| o | Shell company report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Commission file number: 001- 36563

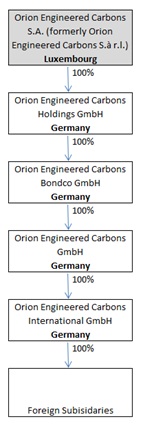

ORION ENGINEERED CARBONS S.A.

(Exact Name of Registrant as Specified in its Charter)

N/A

(Translation of Registrant’s Name into English)

Grand Duchy of Luxembourg

(Jurisdiction of Incorporation or Organization)

6, Route de Trèves

L-2633 Senningerberg (Municipality of Niederanven),

Grand Duchy of Luxembourg

(Address of Principal Executive Office)

christian.eggert@orioncarbons.com

(Name, Telephone, E-Mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of Each Class | | Name of Each Exchange On Which Registered |

| Common Shares, no par value | | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

59,635,126 common shares, no par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities

Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Note—checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one):

Large accelerated filer ¨ Accelerated Filer x Non-accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

| | | | |

U.S. GAAP o | | International Financial Reporting Standards as issued by the International Accounting Standards Board x | | Other o |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

TABLE OF CONTENTS

CERTAIN DEFINED TERMS

In this annual report, unless otherwise specified or if the context so requires:

| |

| • | References to the “Company” are exclusively to Orion Engineered Carbons S.A., a Luxembourg joint stock corporation (société anonyme); |

| |

| • | References in this report to “Orion,” “we,” “us” or “our” are to Orion Engineered Carbons S.A. and its consolidated subsidiaries; |

| |

| • | References in this report to “Kinove Holdings” are to Kinove Luxembourg Holdings 1 S.à r.l., a Luxembourg limited liability company (société à responsabilité limitée); |

| |

| • | References in this report to “Luxco Coinvest” are to Kinove Luxembourg Coinvestment S.C.A., an investment vehicle that is owned by members of the Company’s management; |

| |

| • | References to the “Rhône Investors” are to investment funds managed by affiliates of Rhône Capital L.L.C.; |

| |

| • | References to the “Triton Investors” are to investment funds managed directly or indirectly by Triton Managers III Limited and TFF III Limited; |

| |

| • | References to the “ADIA Investor” are to Luxinva S.A., a wholly-owned subsidiary of the Abu Dhabi Investment Authority, a public institution wholly-owned by the Government of the Emirate of Abu Dhabi; |

| |

| • | References to the “Principal Shareholders” are to the Rhône Investors and the Triton Investors; |

| |

| • | References to the “Acquisition” are to the acquisition of the carbon black business line from Evonik Industries AG, completed on July 29, 2011; and |

| |

| • | References to the “New Credit Agreement” are to the Credit Agreement, dated as of July 25, 2014, among the Company, Orion Engineered Carbons Holdings GmbH, Orion Engineered Carbons Bondco GmbH, Orion Engineered Carbons GmbH, OEC Finance US LLC, the revolving borrowers named therein, the guarantors named on the signature page thereto, the lenders named therein, and Goldman Sachs Bank USA as administrative agent. |

PRESENTATION OF CERTAIN FINANCIAL AND OTHER INFORMATION

The Company (also referred to in this report as the “Successor”) was incorporated on April 13, 2011 as Kinove Luxembourg 2 S.à r.l. On July 29, 2011, the Company completed the Acquisition from Evonik Industries AG (“Evonik”) of its carbon black business line (referred to in this report as “Evonik Carbon Black” or the “Predecessor”). On July 28, 2014 the Company changed its legal form into a joint stock corporation named Orion Engineered Carbons S.A.

In this report, references to “Euro” and “€” are to the single currency adopted by participating member states of the European Union (the “EU”) relating to Economic and Monetary Union, references to “$”, “US$” and “U.S. Dollars” are to the lawful currency of the United States of America and references to “Korean Won” are to the lawful currency of the Republic of Korea.

Non-IFRS Financial Measures

The financial statements included in this report were prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”).

In this report, we present certain financial measures that are not recognized by IFRS and that may not be permitted to appear on the face of IFRS-compliant financial statements or notes thereto.

The non-IFRS financial measures used in this report are Contribution Margin, Contribution Margin per Metric Ton (collectively, “Contribution Margins”), Adjusted EBITDA, Net Working Capital and Capital Expenditures. We define Contribution Margin as revenue less variable costs (such as raw materials, packaging, utilities and distribution costs). We define Contribution Margin per Metric Ton as Contribution Margin divided by volume measured in metric tons. We define Adjusted EBITDA as operating result (EBIT) before depreciation and amortization, adjusted for acquisition related expenses, restructuring expenses, consulting fees related to group strategy, share of profit or loss of joint venture and certain other items. Adjusted EBITDA is defined similarly in the New Credit Agreement. Adjusted EBITDA is used by our management to evaluate our operating performance and make decisions regarding allocation of capital because it excludes the effects of certain items that have less bearing on our underlying business performance. We define Net Working Capital as inventories plus current trade receivables minus trade payables. We define Capital Expenditures as cash paid for the acquisition of intangible assets and property, plant and equipment as shown in the consolidated financial statements.

We also use Segment Adjusted EBITDA Margin, which we define as Adjusted EBITDA for the relevant segment divided by the revenue for that segment. Adjusted EBITDA for our segments and Segment Adjusted EBITDA Margin are financial measures permitted under IFRS.

We use Adjusted EBITDA, Contribution Margins and Net Working Capital, as well as Adjusted EBITDA by segment and Segment Adjusted EBITDA Margin, as internal measures of performance to benchmark and compare performance among our own operations. We use these measures, together with other measures of performance under IFRS, to compare the relative performance of operations in planning, budgeting and reviewing the performance of our business. We believe these measures are useful measures of financial performance in addition to consolidated profit (or loss) for the period, operating result (EBIT) and other profitability measures under IFRS because they facilitate operating performance comparisons from period to period and company to company and, with respect to Contribution Margin, eliminate volatility in feedstock prices. By eliminating potential differences in results of operations between periods or companies caused by factors such as depreciation and amortization methods, historic cost and age of assets, financing and capital structures and taxation positions or regimes, we believe that Adjusted EBITDA can provide a useful additional basis for comparing the current performance of the underlying operations being evaluated. For these reasons, we believe EBITDA-based measures are often used by the investment community as a means of comparison of companies in our industry. By deducting variable costs (such as raw materials, packaging, utilities and distribution costs) from revenue, we believe that Contribution Margins can provide a useful basis for comparing the current performance of the underlying operations being evaluated by indicating the portion of revenue that is not consumed by variable costs (such as raw materials packaging, utilities and distribution costs) and therefore contributes to the coverage of all costs and profits.

Different companies and analysts may calculate measures based on EBITDA, contribution margins and working capital differently, so making comparisons among companies on this basis should be done carefully. Adjusted EBITDA, Contribution Margins and Net Working Capital are not measures of performance under IFRS and should not be considered in isolation or construed as substitutes for revenue, consolidated profit (loss) for the period, operating result (EBIT), gross profit and other IFRS measures as an indicator of our operations in accordance with IFRS.

Reconciliation of Non-IFRS Financial Measures

The non-IFRS financial measures contained in this report are unaudited (except for Adjusted EBITDA, being the total of our Adjusted EBITDA by segment) and have not been prepared in accordance with IFRS or the accounting standards of any other jurisdiction and may not be comparable to other similarly titled measures of other companies. For a reconciliation of these non-IFRS financial measures to the most directly comparable IFRS measures, see “Item 5. Operating and Financial Review and Prospects—Reconciliation of Non-IFRS Financial Measures.”

INDUSTRY, RANKING AND OTHER DATA

Information included in this report relating to industries, industry size, share of industry sales, industry position, industry capacities, industry demand, growth rates, penetration rates, average prices and other industry data pertaining to our business consists of estimates based on data reports compiled by professional third-party organizations and analysts, on data from external sources, on our best knowledge of our sales and industries in which we operate and on our own calculations based on such information. In many cases we are required to rely on internally developed estimates because there is no readily available external information (whether from trade associations, government bodies or other organizations) to validate industry-related analyses and estimates. While we have compiled, extracted and reproduced industry data from external sources, including third-party, industry or general publications, we have not independently verified the data and cannot guarantee its accuracy or completeness. Similarly, while we believe our internal estimates to be reasonable, they have not been verified by any independent sources, and we cannot guarantee their accuracy. Forecasts and other forward-looking information with respect to industry and ranking are subject to the same qualifications and additional uncertainties regarding the other forward-looking statements in this report.

TRADEMARKS AND TRADE NAMES

We own or have rights to certain trademarks and trade names that we use in conjunction with the operations of our business. Each trademark, trade name or service mark of any other company appearing in this report belongs to its holder. Solely for convenience, trademarks and trade names referred to in this report may appear without the “®” or “™” symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent possible under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, such other companies.

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains and refers to certain forward-looking statements with respect to our financial condition, results of operations and business. These statements constitute forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Forward-looking statements include, among others, statements concerning the potential exposure to market risks, statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions and statements that are not limited to statements of historical or present facts or conditions.

Forward-looking statements are typically identified by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “objectives,” “outlook,” “probably,” “project,” “will,” “seek,” “target” and other words of similar meaning. These forward-looking statements include, without limitation, statements about the following matters:

| |

| • | our strategies for (i) strengthening our position in specialty carbon blacks and rubber carbon blacks, (ii) increasing our rubber carbon black margins and (iii) strengthening the competitiveness of our operations; |

| |

| • | the outcome of any pending or possible litigation or regulatory proceedings, including the U.S. Environmental Protection Agency (the “EPA”) enforcement action described herein; and |

| |

| • | our expectation that the markets we serve will continue to grow. |

All these forward-looking statements are based on estimates and assumptions that, although believed to be reasonable, are inherently uncertain. Therefore, undue reliance should not be placed upon any forward-looking statements. There are important factors that could cause actual results to differ materially from those contemplated by such forward-looking statements. These factors include, among others:

| |

| • | negative or uncertain worldwide economic conditions; |

| |

| • | volatility and cyclicality in the industries in which we operate; |

| |

| • | operational risks inherent in chemicals manufacturing, including disruptions as a result of severe weather conditions and natural disasters; |

| |

| • | our dependence on major customers; |

| |

| • | our ability to compete in the industries and markets in which we operate; |

| |

| • | our ability to develop new products and technologies successfully and the availability of substitutes for our products; |

| |

| • | our ability to implement our business strategies; |

| |

| • | volatility in the costs and availability of raw materials and energy; |

| |

| • | our ability to realize benefits from investments, joint ventures, acquisitions or alliances; |

| |

| • | our ability to realize benefits from planned plant capacity expansions and site development projects and the potential delays to such expansions and projects; |

| |

| • | information technology systems failures, network disruptions and breaches of data security; |

| |

| • | our relationships with our workforce, including negotiations with labor unions, strikes and work stoppages; |

| |

| • | our ability to recruit or retain key management and personnel; |

| |

| • | our exposure to political or country risks inherent in doing business in some countries; |

| |

| • | environmental, health and safety regulations, including nanomaterial and greenhouse gas emissions regulations, and the related costs of maintaining compliance and addressing liabilities; |

| |

| • | current and potentially future investigations and enforcement actions by the EPA or other governmental or supranational agencies; |

| |

| • | our operations as a company in the chemical sector, including the related risks of leaks, fires and toxic releases; |

| |

| • | market and regulatory changes that may affect our ability to sell or otherwise benefit from co-generated energy; |

| |

| • | tax audits, litigation or legal proceedings, including product liability and environmental claims; |

| |

| • | our ability to protect our intellectual property rights; |

| |

| • | our ability to generate the funds required to service our debt and finance our operations; |

| |

| • | fluctuations in foreign currency exchange and interest rates; |

| |

| • | the availability and efficiency of hedging; |

| |

| • | changes in international and local economic conditions, including with regard to the Euro and the Eurozone debt crisis, dislocations in credit and capital markets and inflation or deflation; |

| |

| • | potential impairments or write-offs of certain assets; |

| |

| • | required increases in our pension fund contributions; |

| |

| • | the adequacy of our insurance coverage; |

| |

| • | changes in our jurisdictional earnings mix or in the tax laws of those jurisdictions; |

| |

| • | our indemnities to and from Evonik (as defined below); |

| |

| • | challenges to our decisions and assumptions in assessing and complying with our tax obligations; |

| |

| • | potential conflicts of interests with our principal shareholders; |

| |

| • | effect of exchange rate fluctuations on U.S. Dollar amounts received in dividends; |

| |

| • | our status as a foreign private issuer; and |

| |

| • | potential difficulty in obtaining or enforcing judgments or bringing actions against us in the United States. |

In light of these risks, our results could differ materially from the forward-looking statements contained in this report. For further information regarding factors that could affect our business and financial results and the related forward-looking statements, see “Item 3. Key Information—D. Risk Factors.”

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

| |

| A. | Selected Financial Data |

The following table sets forth selected historical financial information for fiscal years 2015, 2014, 2013, 2012 and 2011 and as of December 31, 2015, 2014, 2013, 2012 and 2011. The financial information for fiscal years 2015, 2014 and 2013 and balance sheet information as of December 31, 2015 and 2014 has been derived from our audited consolidated financial statements included elsewhere in this report. The financial information for fiscal years 2012 and 2011 and balance sheet information as of December 31, 2013, 2012 and 2011 has been derived from our audited consolidated or combined financial statements, which are not included in this report. This information should be read in conjunction with the consolidated financial statements included elsewhere in this report, the related notes and other financial information included herein, as well as in conjunction with quarterly financial information previously furnished to the Securities and Exchange Commission (the “SEC”).

The Company was incorporated on April 13, 2011 and prior to the Acquisition had no operations. The Successor period for 2011 covers the period from incorporation through December 31, 2011. For the Predecessor period ended July 29, 2011, financial information set forth below has been derived from Evonik Carbon Black’s audited combined financial statements. We historically operated as a business line of Evonik and reported our results as part of Evonik’s business unit “Inorganic Materials.”

|

| | | | | | |

| | Successor | Predecessor |

| Income Statement Data | Year Ended December 31, | Period Ended December 31, | Period Ended July 29, |

| | 2015 | 2014 | 2013 | 2012 | 2011 | 2011 |

(in € million) | | | | | | |

| Revenue | 1,111.8 | 1,318.4 | 1,339.6 | 1,397.5 | 545.1 | 780.6 |

| Cost of sales | (791.5) | (1,017.3) | (1,070.8) | (1,116.0) | (455.1) | (611.5) |

| Gross profit | 320.3 | 301.1 | 268.8 | 281.6 | 89.9 | 169.1 |

| | | | | | | |

| Selling expenses | (108.1) | (99.6) | (92.1) | (96.2) | (42.1) | (61.2) |

| Research and development costs | (13.4) | (13.0) | (10.1) | (9.5) | (4.8) | (5.8) |

| General and administrative expenses | (62.1) | (54.6) | (52.5) | (54.3) | (14.1) | (19.3) |

| Other operating income | 7.5 | 4.4 | 8.3 | 18.5 | 12.1 | 145.0 |

| Other operating expenses | (21.8) | (34.0) | (38.7) | (52.5) | (57.0) | (31.7) |

| Operating result (EBIT) | 122.4 | 104.3 | 83.8 | 87.6 | (16.0) | 196.0 |

| Finance income | 17.3 | 39.3 | 17.1 | 5.2 | 7.6 | 0.3 |

| Finance costs | (73.4) | (182.7) | (112.7) | (103.1) | (76.0) | (12.0) |

| Share of profit or loss of joint ventures | 0.5 | 0.5 | 0.4 | 0.4 | 0.2 | 0.5 |

| Financial result | (55.7) | (142.8) | (95.2) | (97.5) | (68.3) | (11.3) |

| Profit or (loss) before income taxes | 66.7 | (38.5) | (11.4) | (9.8) | (84.3) | 184.7 |

| Income taxes | (23.8) | (17.4) | (7.5) | (8.9) | 9.8 | (62.1) |

| Profit or (loss) for the period | 42.9 | (55.9) | (19.0) | (18.7) | (74.5) | 122.7 |

| | | | | | | |

Earnings Per Share - basic (€ per share)(1) | 0.72 | (1.11) | (0.43) | (0.43) | (1.70) | 2.80 |

Earnings Per Share - diluted (€ per share)(1) | 0.72 | — | — | — | — | — |

| Dividends per share (€ per share) | 0.67 | 0.67 | — | — | — | — |

|

| | | | | | |

| | Successor | Predecessor |

| Statement of Cash Flows Data | Year Ended December 31, | Period Ended December 31, | Period Ended July 29, |

| | 2015 | 2014 | 2013 | 2012 | 2011 | 2011 |

(in € million) | | | | | | |

| Cash flows from (used in)operating activities | 214.4 | 172.4 | 190.9 | 177.1 | 16.8 | 5.6 |

| Cash flows from (used in) investing activities | (74.8) | (64.5) | (77.2) | (71.3) | (787.7) | (19.8) |

| Cash flows from (used in) financing activities | (143.5) | (110.0) | (114.7) | (131.1) | 861.0 | 27.1 |

|

| | | | | |

| Balance Sheet Data | As of December 31, |

| | 2015 | 2014 | 2013 | 2012 | 2011 |

(in € million) | | | | | |

| Cash and cash equivalents | 65.3 | 70.5 | 70.5 | 74.9 | 98.9 |

| Property, plant and equipment | 385.9 | 358.2 | 333.5 | 334.6 | 325.5 |

| Total assets | 970.5 | 1,022.2 | 1,007.0 | 1,092.7 | 1,141.7 |

| Total liabilities | 920.8 | 966.9 | 1,081.2 | 1,089.5 | 1,118.0 |

Total equity(1) | 49.7 | 55.3 | (74.3) | 3.2 | 23.7 |

| |

| (1) | Our share capital as of December 31, 2015 was €59,635,126, represented by 59,635,126 common shares with no par value. |

Our reporting currency is the Euro. Fluctuations in the exchange rate between the Euro and the U.S. Dollar will affect the U.S. Dollar amounts received by owners of our common shares on conversion of dividends, if any, declared in Euro on the common shares and will affect the U.S. Dollar price of our common shares on the New York Stock Exchange (the “NYSE”). The following tables set forth, for the periods and dates indicated, the period end, average, high and low exchange rates in U.S. Dollars per €1.00.

Exchange Rates for the Previous Six Months

|

| | | | |

| | Period End | Average Rate(1) | High | Low |

| September 2015 | 1.1162 | 1.1228 | 1.1358 | 1.1104 |

| October 2015 | 1.1042 | 1.1228 | 1.1437 | 1.0963 |

| November 2015 | 1.0562 | 1.0726 | 1.1026 | 1.0562 |

| December 2015 | 1.0859 | 1.0888 | 1.1025 | 1.0573 |

| January 2016 | 1.0832 | 1.0865 | 1.0964 | 1.0743 |

| February 2016 (through February 26, 2016) | 1.0932 | 1.1104 | 1.1362 | 1.0888 |

Exchange Rates for the Previous Five Years Ended December 31, 2015

|

| | | | |

| | Period End | Average Rate(2) | High | Low |

| 2011 | 1.2973 | 1.4002 | 1.4875 | 1.2926 |

| 2012 | 1.3186 | 1.2909 | 1.3463 | 1.2062 |

| 2013 | 1.3779 | 1.3303 | 1.3816 | 1.2774 |

| 2014 | 1.2101 | 1.3210 | 1.3927 | 1.2101 |

| 2015 | 1.0859 | 1.1032 | 1.2015 | 1.0524 |

| |

| (1) | The average of the daily exchange rates during the relevant period. |

| |

| (2) | The average of the month-end rates during the relevant period. |

Our inclusion of these exchange rates and other exchange rates specified elsewhere in this report should not be construed as representations that Euro amounts included in this report actually represent such U.S. Dollar amounts or could have been or could be converted into U.S. Dollars at any particular rate, if at all. The Euro foreign exchange reference rate used in this report is the noon buying rate in New York City for cable transfers in foreign currencies as certified for customs purposes by the Federal Reserve Bank of New York. On February 26, 2016, this rate was $1.0932 per €1.00. These exchange rates may differ from the exchange rate in effect on and as of the date of this report.

| |

| B. | Capitalization and Indebtedness |

Not applicable.

| |

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

The following risks may have material adverse effects on our business, financial condition and results of operations. Additional risks and uncertainties of which we are not presently aware or that we currently deem immaterial could also materially affect our business operations and financial condition.

Risks Related to Our Business

Negative or uncertain worldwide economic conditions may result in business volatility and may adversely impact our business, financial condition, results of operations and cash flows.

Our operations and performance are materially affected by worldwide economic conditions. Because carbon black is used in a diverse group of end products, demand for carbon black has historically been related to real gross domestic product (“GDP”) and general global economic conditions. In particular, a large part of our sales has direct exposure to the cyclical automotive industry and, to a lesser extent, the construction industry. As a result, our business experiences a level of inherent cyclicality. The nature of our business and our large fixed asset base make it difficult to rapidly adjust our fixed costs downward when demand for our products declines, which could materially affect our profitability. A global or regional economic downturn may reduce demand for our products, which would decrease our revenue and could have a material adverse effect on our business, financial condition, results of operations and cash flows. For example, our results of operations dropped sharply in the wake of the global financial and economic crisis in the second half of 2008 and 2009. In periods with significant market turmoil and tightened credit availability, we expect to experience difficulty in collecting accounts receivable, pricing pressure and reduced global business activity.

Structural changes in the industries in which we operate may result in business volatility and may adversely affect our business, financial condition, results of operations and cash flows.

Our business is influenced by structural changes in the industries in which we operate, such as the entry of new suppliers, product substitution, changing technologies, industry consolidation and the migration of customers to lower-cost countries. Some of our customers have in the past shifted, and may continue to shift, manufacturing capacity from mature regions, such as North America and Europe, to emerging regions, such as Asia and South America. Although we have developed and implemented strategies to meet these changes in demand, we cannot be certain that we will be able to successfully expand capacity in emerging regions. Our ability to expand in these regions depends in part on their economic and political conditions and on our ability to establish and finance operations, construct additional manufacturing capacity or form strategic business alliances including acquisitions and joint ventures. Over the last few years, for instance, our competitors in China have aggressively added capacity at a far greater rate than demand has increased, which has resulted in pressured margins in the region. In addition, we may not be successful in reducing capacity in mature regions commensurate with industry demand. Similarly, demand for our customers’ products and our competitors’ reactions to market conditions could affect our results. Our business is also sensitive to changes in industry capacity utilization. Prices tend to decrease when capacity utilization decreases, which could adversely affect our business, financial condition, results of operations and cash flows.

Our business is subject to operational risks, which could adversely affect our business, financial condition, results of operations and cash flows.

Our operations are subject to hazards inherent in chemicals manufacturing and the related use, storage, transportation and disposal of feedstocks, products and wastes, including but not limited to, fires and explosions, accidents, severe weather and natural disasters (including hurricanes, tornados, ice storms, droughts, floods and earthquakes), mechanical failures, unscheduled downtime at our production facilities, transportation interruptions, pipeline leaks and ruptures, quality problems, technical difficulties, energy grid shutdowns, discharges or releases of toxic or hazardous substances or gases, other environmental risks, and sabotage, terrorist attacks or other acts of violence as well as potential boycotts, general strikes, sanctions or blockades.

Such events could disrupt our supply of raw materials or otherwise affect production, transportation and delivery of our products or affect demand for our products. We could incur significant expenditures in connection with such operational risks. These may be caused both by external factors, such as natural disasters, war, acts of terrorism, strikes, official orders, technical interruptions or material defects, or accidents or mistakes in internal procedures, such as fire, explosion or release of toxic or hazardous substances. In all of these cases, our property or third-party property or the environment may sustain damage, or there may be human exposure to hazardous substances, personal injuries or fatalities, resulting in material financial liabilities and civil or criminal law consequences, the temporary or permanent closure of the relevant production site or power plant and a negative impact on our financial condition, results of operations and cash flows.

We are dependent on major customers for a significant portion of our sales, and a significant adverse change in a customer relationship could adversely affect our business, financial condition, results of operations and cash flows.

Customer concentration is driven by the consolidated nature of the industries we serve. In 2015, our top ten customers accounted for approximately 57% of our volume in kmt. The top five customers in our Specialty Carbon Black segment and the top five customers in our Rubber Carbon Black segment represented approximately 28% and approximately 59% of our Specialty Carbon Black and Rubber Carbon Black segment volumes measured in kmt for 2015, respectively. Our success in strengthening relationships and growing business with our largest customers and retaining their business over extended time periods could affect our future results. The loss of any of our major customers, including due to industry consolidation, or a reduction in volumes sold to them, could adversely affect our results of operations. Any deterioration

in the financial condition of any of our customers or the industries they serve that impairs our customers’ ability to make payments to us could increase our uncollectible receivables and could adversely affect our business, financial condition, results of operations and cash flows.

We may not be able to compete successfully in the industries and markets in which we operate.

The industries in which we operate are highly competitive and this competition could harm our business, financial condition, results of operations and cash flows. Competition is based on price, product innovation, product quality, distribution capability, and industry and customer knowledge. We face competition from global and regional suppliers, both in developed and in emerging regions. More recently, a significant percentage of tire demand is met by imports from, and a shift in production to, low-cost emerging regions. This has adversely affected utilization rates of carbon black producers in developed regions and resulted in plant closures. While we aim to operate at low cost and are focused on reducing our fixed and variable cost base across our production chain, there may be improvements in the cost competitiveness of other manufacturers relative to us or in the performance properties of substitutable products and raw materials, which could result in advantages for our competitors and adversely affect our business. Furthermore, some of our competitors may have greater financial and other resources and larger capitalization than we do. If we are unable to respond successfully to changing competitive conditions, the demand for our products could be adversely affected.

The markets in which we operate are highly competitive and this competition, and the challenges we face to gain share in those markets and new markets, could harm our business, financial condition, results of operations and cash flows.

We may not successfully develop new products and technologies that address our customers’ changing requirements or competitive challenges, and our customers may substitute our products by using other products we do not offer.

The industries into which we sell our products are subject to periodic technological changes, ongoing product improvements, product substitution and changes in customer requirements. Increased competition from existing or newly developed products offered by our competitors or companies whose products offer a similar or better functionality to our products may negatively affect demand for our products. We work to identify, develop and market innovative products on a timely basis to meet our customers’ changing requirements and competitive challenges. Should we not be able to substantially maintain or further develop our product portfolio, customers may elect to source comparable products from competitors, which could adversely affect our business, financial condition, results of operations and cash flows.

Although carbon black continues to offer opportunities for product and process innovation, we cannot be certain that the investments we make in our Innovation Group will result in proportional increases in revenue or profits. In addition, the timely commercialization of products that we are developing may be disrupted or delayed by manufacturing or other technical difficulties, industry acceptance or insufficient industry size to support a new product, competitors’ new products, and difficulties in moving from the experimental stage to the production stage. These disruptions or delays could adversely affect our business, financial condition, results of operations and cash flows.

As a reinforcing agent in rubber, carbon black competes primarily with precipitated silica in combination with silane, which is not part of our product portfolio. Historically, silica has offered some performance benefits over carbon black in the area of rolling resistance. To date, silica-based tire applications have gained position in passenger car tire treads. Although substitution has not been significant due to carbon black’s cost advantage, technological advances and changing customer requirements may lead to increased demand for silica-based tires, especially in developed regions. For example, Evonik announced in 2010 plans to significantly increase its capacity for precipitated silica to satisfy increasing demand. Increased substitution and competition from precipitated silica producers, including Evonik, could adversely affect our business, financial condition, results of operations and cash flows. If we should decide to include precipitated silica in combination with silane in our product portfolio in the future, we may be restricted in our ability to do so under our intellectual property sharing arrangements with Evonik.

Alternative materials, procedures or technologies may be developed, or existing ones may be improved, and may replace those currently offered in the carbon black industry. If such newly developed or improved products are being offered at lower prices, have preferable features or other advantages, in particular from a regulatory perspective, and we are not able to offer similar new or improved products, we may lose substantial business, which could have an adverse effect on our business, financial condition, results of operations and cash flows.

We may be unable to implement our business strategies in an effective manner.

Our future financial performance and success largely depend on our ability to maintain our current position and to implement our business strategies for growth successfully. We have undertaken, and will continue to undertake, various initiatives to realign our product portfolio away from standard specialty carbon black and rubber carbon black products to higher margin applications, and we continue to focus on cost reduction initiatives to optimize our asset base, improve operating efficiencies and generate cost savings. We cannot guarantee that we will successfully implement our business strategies or that implementing these strategies will sustain or improve and not harm our results of operations. In particular, we may not be able to increase or sustain our manufacturing efficiency or asset utilization, enhance our current portfolio of products or achieve other fixed or variable cost savings. In addition, the costs involved in implementing our strategies may be significantly higher than we currently anticipate. For example, our ability to complete capacity expansions as planned may be delayed or interrupted by the need to obtain environmental and other regulatory approvals, the availability of labor and materials, unforeseen hazards, such as weather conditions, adverse political or market developments, and other risks customarily associated with construction projects. Moreover, the cost of expanding capacity could have a negative impact on our financial results until capacity utilization is sufficient to absorb the incremental costs associated with the expansion. Further, labor or governmental restrictions could impede or delay our ability to reduce headcount.

Our business strategies are based on our assumptions about future demand for our products and the new products and applications we are developing and on our continuing ability to produce our products profitably. Each of these factors depends, among other things, on our ability to realign our product portfolio, divest businesses or discontinue product lines on favorable terms and with minimal disruptions, finance our operations and product development activities, maintain high-quality and efficient manufacturing operations, relocate and close certain manufacturing facilities with minimal disruption to our operations, respond to competitive and regulatory changes, access quality raw materials in a cost-effective and timely manner, and retain and attract highly skilled technical, managerial, marketing and finance personnel. Any failure to develop, revise or implement our business strategies in a timely and effective manner may adversely affect our business, financial condition, results of operations and cash flows.

We are subject to volatility in the costs and availability of raw materials and energy, which could decrease our margins and adversely affect our business, financial condition, results of operations and cash flows.

Our manufacturing processes consume significant amounts of raw materials and energy, the costs of which are subject to fluctuations in worldwide supply and demand as well as other factors beyond our control. In 2015, raw materials accounted for 72% of our cost of sales. Approximately 76% of the cost of raw material used in the production of carbon black is related to petroleum-based or coal-based feedstock known as carbon black oil, with some limited use of other raw materials, such as nitrogen tetroxide, hydrogen and natural gas. We obtain a considerable portion of our raw materials and energy from selected key suppliers. Although we maintain raw material reserves, if any of these suppliers is unable to meet its obligations under supply agreements with us on a timely basis or at all, we may be forced to incur higher costs to obtain the necessary raw materials and energy elsewhere or, in certain limited cases, may not be able to obtain carbon black oil or raw materials at all. Additionally, raw material sourcing and related infrastructure in certain jurisdictions where we operate may be subject to local regulations that may reduce, delay or halt the physical supply of raw materials. Our inability to source quality raw materials or energy in a timely fashion and pass through cost increases to our customers could have an adverse impact on our business, financial condition, results of operations and cash flows.

Most of our carbon black supply contracts contain provisions that adjust prices to account for changes in a relevant feedstock price index. While we have re-negotiated many of our customer contracts to reduce the time-lag after which we are able to pass through changes in carbon black oil prices to our customers, we are still exposed to oil price fluctuations and there can be no assurance that we will be able to shift price risks to our customers. Success in offsetting increased raw material and energy costs with price increases is also influenced by competitive and economic conditions, as well as the speed and severity of such changes, and could vary significantly, depending on the segment served. Such increases may not be accepted by our customers, may not be fully reflected in the indices used in our pricing formulas, may not be sufficient to compensate for increased raw material and energy costs or may decrease demand for our products and our volume of sales. Rapid and significant oil or energy price fluctuations have had and are likely to continue to have significant and varying effects on our earnings and results of operations, partly because oil price changes affect our sales prices and our cost of raw materials and energy at different times and amounts, and partly due to other factors, such as differentials affecting the ultimate carbon black oil price paid by us (versus a particular reference price index), carbon black oil usage amounts and ongoing efficiency initiatives. Failure to fully offset the effects of fluctuating raw material or energy costs could have a material adverse effect on our business, financial condition, results of operations and cash flows. Further, volatility in costs and pricing could result in commercial disputes with suppliers and customers regarding the interpretations of complex contractual pricing arrangements, which could adversely affect our business.

Significant movements in the market price for crude oil tend to create volatility in our carbon black feedstock costs, which can affect both our Net Working Capital and operating results. Changes in raw material and energy prices have a direct impact on our Net Working Capital levels. In general, increases in the cost of raw materials lead to an increase in our Net Working Capital requirements, as our inventories and current trade receivables increase as a result of higher carbon black oil and other feedstock prices and related sales price levels, partially offset by an increase in trade payables. Due to the quantity of carbon black oil and finished goods that we typically keep in stock together with the levels of receivables and payables maintained, increases occur gradually over a two to three-month period but can vary depending on inventory levels and working capital levels generally. Conversely, decreases in the cost of raw materials lead to a decrease in our Net Working Capital requirements within a two to three-month period following the decrease in costs. Net Working Capital swings are particularly significant in an environment of high price volatility such as those seen in the fourth quarter of 2014.

Any failure to realize benefits from investments, joint ventures, acquisitions or alliances could adversely affect our business, financial condition, results of operations and cash flows.

We have made, and may continue to make, investments and acquisitions and enter into joint ventures. The success of acquisitions of new technologies, companies and products, or arrangements with third parties is not always predictable and we may not achieve our anticipated objectives. Our investments may require high initial expenditures, and as in the case of Deutsche Gasrußwerke GmbH & Co. KG (the “German JV”), our joint venture with, among others, the tire manufacturers Continental, Pirelli and Goodyear, ongoing expenditures for modernization and expansion. The German JV finances itself independently. However, any potential future lack of external financing sources may jeopardize such joint venture and may result in negative impacts on our own supply chain and business. Our investments can only be operated profitably if their utilization is warranted by corresponding demands. Should we build up overcapacities that remain unused due to erroneous assessments of market development, this could have a material adverse effect on our business, financial condition, results of operations and cash flows.

In addition, in the event that our recently completed acquisition of Qingdao Evonik Chemicals Co. Ltd. (“QECC”), now operating as Orion Engineered Carbons Qingdao Ltd. (“OECQ”), will not contribute to our performance as expected, we may be unable to compete effectively with other producers in that market, which could have an adverse effect on our business, financial condition, results of operations and cash flows.

Plant capacity expansions and site development projects may be delayed or may not achieve the expected benefits.

Our ability to complete as planned capacity expansions, including capacity conversions from rubber carbon black to specialty carbon black, and other site development projects, including those associated with yield efficiency improvements, may be delayed, interrupted, or otherwise limited by the need to obtain environmental and other regulatory approvals, unexpected cost increases, availability of labor and materials, unforeseen hazards such as weather conditions, and other risks customarily associated with construction projects. In addition, lower oil prices may result in lower yield efficiency improvements. Moreover, the costs of these activities could have a negative impact on our results of operations, and in the case of capacity expansion projects, until capacity utilization at the particular facility is sufficient to absorb the incremental costs associated with the expansion. In addition, our ability to expand capacity in emerging countries depends in part on economic and political conditions in these regions and, in some cases, on our ability to establish operations, construct additional manufacturing capacity or form strategic business alliances.

We may be subject to information technology systems failures, network disruptions and breaches of data security.

Our information technology systems are an important element for effectively operating our business. In 2013 we implemented new software (SAP) throughout Orion. The global implementation process of SAP is associated with certain risks for our business, such as failures, breakdowns and malfunctioning. This could adversely affect our business operations and materially impact the relationships we have with our customers and suppliers, our reputation and our operating costs and margins.

Information technology systems failures, in particular failures in connection with running SAP, including risks associated with upgrading our systems, network disruptions and breaches of data security could disrupt our operations by impeding our processing of transactions, our ability to protect customer or company information and our financial reporting leading to increased costs. It is possible that future technological developments could adversely affect the functionality of our computer systems and require further action and substantial funds to prevent or repair computer malfunctions. Our computer systems, including our back-up systems, could be damaged or interrupted by power outages, computer and telecommunications failures, computer viruses, cybercrimes, internal or external security breaches, events such as fires, earthquakes, floods, tornadoes and hurricanes, or errors by our employees or third party providers. Although we have taken steps to address these concerns by implementing sophisticated network security, back-up systems and internal control measures, there can be no assurance that a system failure or data security breach will not have a material adverse effect on our business, financial condition, results of operations and cash flows.

In addition to supporting our operations, we use our systems to collect and store confidential and sensitive data, including information about our business, our customers and our employees. As our technology continues to evolve, we anticipate that we will collect and store even more data in the future, and that our systems will increasingly use remote communication features that are sensitive to both willful and unintentional security breaches. Much of our value is derived from our confidential business information, including customer data, proprietary technology and trade secrets, and to the extent the confidentiality of such information is compromised, we may lose our competitive advantage and our business, financial condition, results of operations and cash flows may suffer. We also collect, retain and use personal information, including data we gather from customers for product development and marketing purposes, and data we obtain from employees. In the event of a breach in security that allows third parties access to this personal information, we are subject to a variety of laws on a global basis that require us to provide notification to the data owners, and that subject us to lawsuits, fines and other means of regulatory enforcement. Our reputation could suffer in the event of such a data breach, which could cause customers to purchase from our competitors. Ultimately, any compromise of our data security could have a material adverse effect on our business, financial condition, results of operations and cash flows.

If we are unable to successfully negotiate with the representatives of our employees, including labor unions and works councils, we may experience strikes and work stoppages.

We are party to collective bargaining agreements and social plans with our employees’ labor unions. We also are required to consult with our employee representatives, such as works councils, on certain matters such as restructuring, acquisitions and divestitures. Although we believe that our relations with our employees are good, there can be no assurance that new agreements will be reached or consultations will be completed without union or works council actions or on terms satisfactory to us. Current and future negotiations and consultations with employee representatives could have a material adverse effect on our business. In addition, a material work stoppage or union dispute could adversely affect our business, financial condition, results of operations and cash flows.

We may not be able to recruit or retain key management and personnel.

Our success is dependent on the management and leadership skills of our key management and personnel. The loss of any member of our key management team and personnel or an inability to attract, retain, develop and maintain additional personnel could prevent us from implementing our business strategy. In addition, our future growth and success also depend on our ability to attract, train, retain and motivate skilled managerial, sales, administration, research and development (“R&D”), operating and technical personnel. The loss of one or more member of our key management or operating personnel, or the failure to attract, retain and develop additional key personnel, could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We are exposed to political or country risk inherent in doing business in some countries.

We operate a global network of production plants, located in Europe, North America, South Korea, China, South Africa and Brazil. Accordingly, our business is subject to risks related to the differing legal, political, social and regulatory requirements and economic conditions of many jurisdictions. Risks inherent in international operations include the following: changes in the rate of economic growth, unsettled political or economic conditions, expropriation or other governmental actions; social unrest, war, terrorist activities or other armed conflict; national and regional labor strikes, confiscatory taxation or other adverse tax policies, deprivation of contract rights, trade regulations affecting production, pricing and marketing of products; reduced protection of intellectual property rights; restrictions on the repatriation of income or capital, exchange controls, inflation, deflation, currency fluctuations and devaluation, the effect of global environmental, health and safety issues on economic conditions, market opportunities and operating restrictions, changes in foreign laws and tax rates, changes in trade sanctions that result in losing access to customers and suppliers in those countries, costs associated with compliance with anti-bribery and anti-corruption laws, nationalization of private enterprises by foreign governments, and changes in financial policy and availability of credit or financing sources. These factors could adversely affect our business, financial condition, results of operations and cash flows.

Legal and Regulatory Risks

Our operations are subject to environmental, health and safety regulations. We have been and may in the future be subject to investigations by regulatory authorities (including currently by the EPA as described herein) in respect of alleged violations and may incur significant costs to maintain compliance with, and to address liabilities under, these laws and regulations.

We are subject to extensive domestic, foreign, federal, state and local laws and regulations governing environmental protection and occupational health and safety, all of which may be subject to change in the future. The production and processing of carbon black and other chemicals we produce involve the handling, transportation, manufacture, use and disposal of substances or components that may pose environmental risks or be considered toxic, hazardous or carcinogenic under these laws. We are also required to obtain permits or other approvals from various regulatory authorities for our operations, which may be required for matters including air emissions; wastewater and storm water discharges; storage, handling and disposal of hazardous substances; and operation, maintenance and closure of landfills. If we violate or otherwise fail to comply with these laws, regulations or permits or other approvals, we may incur fines or other sanctions, be required to undertake significant capital expenditures to achieve compliance, or be subject to other obligations by one or more regulatory authorities.

If environmental harm to soil, groundwater, surface water or natural resources is found to have occurred as a result of our current or historical operations, we may be required to incur significant remediation costs at our current or former production facilities or at third-party sites. Many of our facilities have a long history of operation, which may contribute to our environmental compliance and remediation costs due to past spills, past chemical storage, wastewater treatment and waste disposal practices and other activities. For instance, many of our facilities have onsite landfills that have been in use for a number of years, and we may incur significant costs when these landfills reach capacity in order to close them in accordance with applicable laws and regulations and to address contamination of soil and groundwater at, under or migrating from the facilities, including costs to address impacts to natural resources. Under certain laws and regulations, the obligations to investigate and remediate contamination at a facility or site may be imposed on current and former owners or operators, or on persons who may have sent waste to that facility or site for disposal. Liability under such laws and regulations may be without regard to fault or to the legality of the activities giving rise to the contamination. As a result, we may incur liabilities for wastes, including hazardous wastes, generated by our operations and disposed of onsite or at offsite locations, even if we were not responsible for the disposal. Further, we may also incur additional closure and cleanup costs in connection with the closure of plants, including costs relating to decommissioning of equipment, asbestos removal and closure of features such as storage tanks, wastewater treatment systems, ponds and landfills.

Environmental and safety regulations are subject to frequent change, as are the priorities of those who enforce them, and we could incur substantial costs to comply with future laws and regulations. The trend in environmental regulation is imposing increasingly stringent restrictions on activities that may affect the environment. Any new or amended environmental laws and regulations may result in costly measures for matters subject to regulation, including but not limited to more stringent limits or control requirements for our air emissions; new or increased compliance obligations relating to greenhouse gas (“GHG”) emissions; stricter requirements for noise, waste handling, storage, transport, disposal; and more stringent cleanup and remediation standards, which, in each case, could have a material adverse effect on our operations and financial condition.

Certain national and international health organizations have classified carbon black as a possible or suspect human carcinogen. To the extent that, in the future, (i) these organizations re-classify carbon black as a known or confirmed carcinogen, (ii) other organizations or government authorities in other jurisdictions classify carbon black or any of our other finished products, raw materials or intermediates as suspected or known carcinogens or (iii) there is discovery of adverse health effects attributable to production or use of carbon black or any of our other finished products, raw materials or intermediates, we could be required to incur significantly higher costs to comply with environmental, health and safety laws, or to comply with restrictions on sales of our products, and our reputation and business could be adversely affected. In addition, chemicals that are currently classified as harmless may be classified as dangerous in the future, and our products may have characteristics that are not recognized today but may be found in the future to impair human health or to be carcinogenic. See “Item 4. Information on the Company —B. Business Overview —Environmental, Health and Safety Matters.”

We are currently involved in an enforcement case with the EPA.

During 2008 and 2009, the EPA contacted all U.S. carbon black producers as part of an industry-wide EPA initiative, requesting extensive and comprehensive information under Section 114 of the U.S. Clean Air Act (the “Clean Air Act”), to determine, for each facility, that either: (i) the facility has been in compliance with the Clean Air Act; (ii) violations have occurred and enforcement litigation may be undertaken; or (iii) violations have occurred and a settlement of an enforcement case is appropriate. In response to information requests received by our U.S. facilities, we have furnished information to the EPA on each of our U.S. facilities. Our Belpre (Ohio) facility was an initial subject of these investigations and received notices under Section 113(a) of the Clean Air Act from the EPA in 2010 alleging violations of Prevention of Significant Deterioration (“PSD”) and Title V permitting requirements under the Clean Air Act. In October 2012, we received a corresponding notice and finding of violation (an “NOV”) alleging the failure to obtain PSD permits at several units of our Ivanhoe (Louisiana) facility and to include Best Available Control Technology (“BACT”) in the Title V permit. In January 2013 we also received an NOV issued by the EPA for our facility in Borger (Texas) alleging the failure to obtain PSD and Title V permits reflecting BACT during the years 1996 to 2008, and a similar NOV by the EPA was issued for our U.S. facility in Orange (Texas) in February 2013.

In November 2013, we began discussions with the EPA and the United States Department of Justice (the “DOJ”) about a potential settlement to resolve the NOVs. These discussions are currently ongoing and to date have focused on target emission levels, changes in raw materials and the possible air pollution control technology and other measures that might have to be installed and operated at one or more of our U.S. facilities to settle the EPA action (though any settlement would also likely may involve the imposition of civil penalties and environmental mitigation projects). We received a draft term sheet from the EPA in November 2013 specifying certain target emission reduction levels, pollution controls and other terms the EPA demanded in a settlement. The EPA revised such proposed specifications and terms in November 2014 in response to a counter-proposal presented by us. The discussions continue, with the last exchange of a proposal by us in February 2016 as an answer to a revised term sheet from the EPA received in January 2016. We currently expect that, if we continue to consider a possible settlement, likely at least one further proposal will be exchanged with the EPA and further meetings with the EPA on these matters will occur.

The EPA action could result in significant capital expenditures for pollution controls to reduce air emissions at our U.S. facilities on an ongoing basis. If we and the EPA/DOJ fail to reach a settlement agreement, the EPA/DOJ could bring a lawsuit against us. We would expect to assert various defenses to EPA/DOJ’s allegations. We are currently examining the technological solutions necessary and available to reach certain emission reduction levels in our various U.S. facilities on a going-forward basis. The costs of these solutions (and consequently, the costs of various proposed approaches outlined in the EPA’s and our proposals and counter-proposals) to date are uncertain and will remain uncertain until a mutually acceptable approach to settlement (if one were to be reached), including emission reduction levels, technologies and implementation periods (as well as a number of other important variables, such as local regulatory impact), comes into clearer focus. We also note that the installation of pollution control technologies at our U.S. plants in response to the EPA action would increase the ongoing operating costs of those plants. We may not be able to pass the cost increases on to our customers.

While we are currently unable to determine the amount of capital expenditures, civil penalties or mitigation costs resulting from a settlement with or an enforcement of claims by the EPA, we note that, based on their public announcements, two competitors, Cabot Corporation (“Cabot”) and Continental Carbon Corporation (“Continental”), have entered into settlement agreements with EPA/DOJ. In November 2013, Cabot agreed to pay a $975,000 civil penalty to the EPA and fund $450,000 in environmental mitigation projects. Cabot is also required to install certain technology controls as part of the settlement that it estimates will require investments of approximately $85 million. In March 2015, Continental agreed to pay a $650,000 civil penalty and fund $550,000 in environmental mitigation projects. Continental is also required to install certain technology controls as part of the settlement estimated to require investments of approximately $98 million. As of February 2016, none of our other domestic competitors have announced settlements with the government.

Our agreement with Evonik in connection with the Acquisition provides for a partial indemnity from Evonik against various exposures, including, but not limited to, capital investments, fines and costs arising in connection with Clean Air Act violations that occurred prior to July 29, 2011. All of the allegations made by the EPA as discussed above relate to alleged violations before that date. The indemnity provides for a recovery from Evonik of a share of the costs (including fines), expenses (including reasonable attorney’s fees, but excluding costs for maintenance and control in the ordinary course of business and any internal cost of monitoring the remedy), liabilities, damages and losses suffered and is subject to various contractual provisions including provisions set forth in the Share Purchase Agreement with Evonik, such as a de minimis clause, a basket, overall caps (which apply to all covered exposures and all covered environmental exposures, in the aggregate), damage mitigation and cooperating requirements, as well as a statute of limitations provision. Due to the cost-sharing and cap provisions in Evonik’s indemnity, we expect that substantial costs we would incur in this EPA enforcement initiative could exceed the scope of the indemnity, perhaps in the tens of millions of Euro. In addition, Evonik has signaled that it may likely defend itself against claims under the indemnity. While we intend to enforce our rights vigorously, there is no assurance that we will be able to recover costs incurred under the indemnity as we expect or at all. See “—Risks Related to Indebtedness, Currency Exposure and Other Financial Matters—Our agreements with Evonik in connection with the Acquisition require us to indemnify Evonik with respect to certain aspects of our business and require Evonik to indemnify us for certain retained liabilities. We cannot offer assurance that we will be able to enforce claims under these indemnities as we expect.”

We are in continuing discussions with the EPA about this enforcement action and, while the outcome of these discussions remains uncertain, we believe that any potential settlement with the EPA, if reached, would likely involve costs similar in nature to those announced by Cabot and Continental as noted above, except that the amounts could be significantly larger due to the greater number of U.S. facilities operated by us. Such costs will also be affected by the locations and characteristics of such facilities as well as the other factors affecting potential emission

reduction solutions referenced above. Were we to install, at all of our U.S. facilities, pollution controls using technology of the kind Cabot and Continental have indicated they are installing under their settlements, we believe that the capital costs for us could theoretically be 30% to 70% higher than those announced by Cabot and referenced above. We caution, however, that the actual capital costs we might need to incur, were we to settle the EPA matter, remain uncertain, as we have yet to reach an understanding with the EPA as to overall approaches to be taken toward settlements at our plants. In particular, technology solutions we might choose to implement may differ in scope and operation from those used by our competitors and other important factors, such as timing, locations, target levels and local regulations, could also affect capital costs differently. Given that specific penalties or costs for mitigation projects have not been discussed with the EPA to date, we also caution that the foregoing does not include any civil penalties or the costs of such mitigation projects that may be a part of any settlement with the EPA, were one to be reached. The capital costs necessary to settle the EPA matter, were we to do so, will remain uncertain until a mutually acceptable approach to settlement comes into clearer focus through further analysis and discussions and, accordingly, may differ significantly from the amounts indicated above. It remains uncertain as to whether acceptable settlement terms can be reached, whether we or the EPA will elect to pursue litigation instead and, in either case, the extent of any indemnification we will be able to obtain from Evonik. As a result, the financial impact of this enforcement action on us remains unclear.

This enforcement action could have a material adverse effect on our operating results and cash flows for the particular period in which we incur the related costs or liabilities. While capital expenditures made in response to the EPA action would be capitalized and amortized over time, civil penalties and the funding costs associated with environmental mitigation projects would reduce our results of operations in the reporting periods in which the costs are incurred or provided for.

Developing regulation of carbon black as a nano-scale material could require us to comply with costly new requirements.

Carbon black consists of particles that are nano-scale. The EPA and other governmental agencies are currently developing a regulatory approach under which they will collect further data on nano-scale materials, including carbon black, under the Toxic Substances Control Act. The EPA has proposed rules that would require manufacturers of nano-scale materials to submit additional manufacturing information, exposure and release information and available health and safety data. The EPA and other nations’ environmental regulatory authorities, including the European Commission, are also conducting extensive environmental health and safety testing of nano-scale materials. If carbon black is found to be harmful to humans or to the environment, it could be subject to more stringent regulatory control, which could require us to incur significantly higher costs to comply with new environmental, health and safety laws and could adversely affect our reputation and business. See “Item 4. Information on the Company —B. Business Overview—Environmental, Health and Safety Matters.”

In connection with such regulation, the European Commission is in the process of defining “nanomaterial.” According to its recommendation of October 18, 2011 (2011/696/EU) carbon black is defined as a nano-material. In a similar approach, the International Organization for Standardization (“ISO”) developed the ISO TC 229 “Nanotechnologies,” which considers carbon black a “nano-structured material.” The industry is not yet generally affected by these definitions. However, certain regulations regarding cosmetics applications or articles which are intended for food contact have already been implemented, and other regulations are being discussed which may affect the use of carbon black in the future. This development may significantly affect our business in a manner we cannot predict, including by increasing the costs of doing business.

Regulations requiring a reduction of greenhouse gas emissions could adversely affect our business, financial condition, results of operations and cash flows.

Significant volumes of carbon dioxide (“CO2”), a GHG, are emitted in carbon black manufacturing processes. Over the past few decades, concerns about the relationship between GHGs and global climate change have resulted in increased levels of scrutiny from regulators and the public alike, and have led to proposed and enacted regulations on both national and supranational levels, to monitor, regulate and control emissions of CO2 and other GHGs.

In December 2005, the European Commission published a directive that includes carbon black manufacturing in the combustion sector and in Phase II of the Emissions Trading Scheme for GHGs for the period from 2008 to 2012. The European Commission has developed allowable emission credits for Phase III of the Emissions Trading Scheme (the “ETS”), which will apply for the period 2013 to 2020. The ETS is anticipated to become progressively more stringent over time, which could have an impact on our costs of compliance under the ETS. The European Union member states (“EU Member States”) have included carbon black facilities in their national allocation plans, and we have taken actions to comply with applicable CO2 emission requirements. Certain industry sectors in the European Union, including the carbon black industry, currently receive a certain share of their emission allowances for free. This list of industry sectors is reviewed by the European Commission every five years, with the latest review in October 2014. Although the carbon black industry retained its placement in the 2014 review, we cannot predict the outcome of a future review by the European Commission. Additionally, there can be no assurance that we will be able to purchase emissions credits if our carbon black operations generate more CO2 than our allocations permit or that the cost of such credits will not be excessive.

In addition, effective January 2015, South Korea commenced a GHG emissions trading scheme (“South Korean ETS”), with the goal of achieving a 30% reduction in GHG emissions relative to the projected business-as-usual case by 2020, which is reported as approximating 4% reduction against the 2005 level. Participation is mandatory for South Korean legal entities that emit over 125,000 tons of CO2 equivalent (“tCO2e”) annually and for workplaces that discharge over 25,000 tCO2e annually. The design concept of the South Korean ETS is similar to the ETS. The South Korean ETS covers industries (including the petrochemical sector), electric power producers, the transportation sector and commercial properties, among others, including our South Korean operating entity. The emissions allowance allocated to our South Korean

operating entity in 2015 was set at 88% of the projected emissions when operating at full capacity. We have filed an appeal with South Korea’s Environment Ministry under Article 38 of the GHG Emissions Allowance and Trading Act to effectively seek an increase in the allowance. It is difficult to assess at this time our chances of success. The South Korean Environment Ministry will hold a hearing on our case expected to take place at the end of the first quarter of 2016. If our appeal fails to lead to a higher allowance we could have a carbon deficit, which would require us to purchase carbon credits.