Table of Contents

Filed Pursuant to Rule 424(b)(2)

Registration No. 333-233213

CALCULATION OF REGISTRATION FEE

| ||||

Title of Each Class of Securities to be Registered | Maximum Aggregate Offering Price | Amount of Registration Fee(1) | ||

3.350% Notes due 2024 | $400,000,000 | $48,480 | ||

4.000% Notes due 2030 | $700,000,000 | $84,840 | ||

Guarantees(2) | ||||

Total | $1,100,000,000 | $133,320 | ||

| ||||

| ||||

| (1) | Calculated in accordance with Rules 457(o) and 457(r) under the Securities Act of 1933, as amended (the “Securities Act”). In accordance with Rules 456(b) and 457(r) under the Securities Act, the registrant initially deferred payment of all of the registration fee for the registrant’s Registration Statement on Form S-3 (File No. 333-233213) filed with the Securities and Exchange Commission on August 12, 2019. |

| (2) | In accordance with Rule 457(n), no separate fee is payable with respect to the Guarantees. |

Table of Contents

Filed Pursuant to Rule 424(b)(5)

Registration Statement No. 333-233213

Prospectus Supplement

(to the Prospectus dated August 12, 2019)

GLP Capital, L.P.

GLP Financing II, Inc.

$400,000,000 3.350% Senior Notes due 2024

$700,000,000 4.000% Senior Notes due 2030

GLP Capital, L.P. and GLP Financing II, Inc. (together, the “Issuers”) are offering $400.0 million aggregate principal amount of 3.350% senior notes due 2024 (the “2024 notes”) and $700.0 million aggregate principal amount of 4.000% senior notes due 2030 (the “2030 notes” and, together with the 2024 notes, the “notes”). We will pay interest on the 2024 notes semi-annually in arrears on March 1 and September 1 of each year, commencing on March 1, 2020. We will pay interest on the 2030 notes semi-annually in arrears on January 15 and July 15 of each year, commencing on January 15, 2020. Interest on the notes will accrue from August 29, 2019. The 2024 notes will mature on September 1, 2024 and the 2030 notes will mature on January 15, 2030.

We may redeem all or part of either series of notes at any time prior to the date that is, with respect to the 2024 notes 30 days, and with respect to the 2030 notes 90 days, prior to the maturity date of the applicable series of notes (the “Par Call Date”), at our option at a redemption price equal to 100% of the principal amount thereof, plus accrued and unpaid interest, if any, to, but not including, the redemption date, plus a “make-whole” premium. At any time on or following the applicable Par Call Date, we may redeem all or part of either series of notes at a redemption price equal to 100% of the principal amount thereof, plus accrued and unpaid interest, if any, to, but not including, the redemption date. See “Description of the Notes—Redemption—Optional Redemption.”

If we experience a change of control accompanied by a decline in the rating of either series of notes, we must give holders of such series of notes the opportunity to sell us their notes at 101% of their principal amount, plus accrued and unpaid interest, if any, to, but not including, the repurchase date. See “Description of the Notes—Repurchase at the Option of Holders—Change of Control and Rating Decline.”

In addition, the notes will be subject to redemption requirements imposed by gaming laws and regulations of gaming authorities in jurisdictions in which we conduct gaming operations. See “Description of the Notes—Redemption—Gaming Redemption.”

The notes will be guaranteed on a senior unsecured basis by Gaming and Leisure Properties, Inc. (“GLPI”), but will not initially be guaranteed by, or be obligations of, any subsidiary of the Issuers. GLPI does not have any material assets other than its investment in GLP Capital, L.P. GLP Financing II, Inc., a wholly-owned subsidiary of GLP Capital, L.P., is nominally capitalized and does not have any material assets or significant operations, other than with respect to acting asco-Issuer for the notes offered hereby, as well as for certain other debt obligations of GLP Capital, L.P.

The notes will rankpari passuin right of payment with all of our existing and future senior indebtedness, including our existing senior unsecured notes and borrowings under our senior unsecured credit facilities, and senior in right of payment to all of our future subordinated indebtedness, without giving effect to collateral arrangements. The notes will be effectively subordinated to all of our future secured indebtedness to the extent of the value of the assets securing such indebtedness. The notes will be structurally subordinated to all indebtedness and other liabilities of any of our subsidiaries, certain of which may in the future elect to guarantee our senior unsecured credit facilities.

The notes will be issued only in registered form in denominations of $2,000 and integral multiples of $1,000 thereafter.

Investing in the notes involves risks. See “Risk Factors”, beginning on pageS-20 of this prospectus supplement and on page 23 of GLPI’s Annual Report on Form10-K for the year ended December 31, 2018, and other reports filed with the Securities and Exchange Commission and incorporated by reference herein and therein.

| Price to Public(1) | Underwriting Discount | Proceeds to Us, Before Expenses | ||||||||||

Per 2024 note | 99.899 | % | 0.600 | % | 99.299 | % | ||||||

Total | $ | 399,596,000 | $ | 2,400,000 | $ | 397,196,000 | ||||||

Per 2030 note | 99.751 | % | 0.650 | % | 99.101 | % | ||||||

Total | $ | 698,257,000 | $ | 4,550,000 | $ | 693,707,000 | ||||||

| (1) | Plus accrued interest from August 29, 2019, if settlement occurs after that date. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

No gaming or regulatory agency has approved or disapproved of these securities, or passed upon the adequacy or accuracy of this prospectus supplement or the accompanying prospectus. Any representation to the contrary is a criminal offense.

We expect delivery of the notes will be made to investors in book-entry form through The Depository Trust Company on or about August 29, 2019.

Joint Book-Running Managers

| Wells Fargo Securities | BofA Merrill Lynch | Fifth Third Securities | J.P. Morgan |

| Barclays | Citizens Capital Markets | Credit Agricole CIB | M&T Securities |

SunTrust Robinson Humphrey

The date of this prospectus supplement is August 15, 2019.

Table of Contents

Prospectus Supplement

| Page | ||||

| S-ii | ||||

| S-iii | ||||

| S-iv | ||||

| S-v | ||||

| S-1 | ||||

| S-20 | ||||

| S-27 | ||||

| S-28 | ||||

| S-29 | ||||

| S-31 | ||||

| S-58 | ||||

| S-64 | ||||

| S-64 | ||||

| S-64 | ||||

| S-65 | ||||

Prospectus

| Page | ||||

| 1 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 13 | ||||

| 19 | ||||

| 22 | ||||

| 26 | ||||

| 52 | ||||

| 53 | ||||

| 58 | ||||

| 58 | ||||

S-i

Table of Contents

ABOUT THIS PROSPECTUS SUPPLEMENT

This document is in two parts. The first part is this prospectus supplement, which describes the specific terms of the offering and also adds to and updates information in the accompanying prospectus and the documents incorporated by reference therein. The second part, the accompanying prospectus, gives more general information, some of which may not apply to this offering. You should read this entire document, including this prospectus supplement, the accompanying prospectus and the documents incorporated by reference herein and therein. In the event that the description of this offering varies between this prospectus supplement and the accompanying prospectus or any document incorporated by reference herein or therein filed prior to the date of this prospectus supplement, you should rely on the information contained in this prospectus supplement; provided that if any statement in one of these documents is inconsistent with a statement in another document having a later date, the statement in the document having the later date modifies or supersedes the earlier statement. The accompanying prospectus is part of a registration statement that we filed with the U.S. Securities and Exchange Commission (the “SEC”) using a shelf registration statement. Under the shelf registration process, from time to time, we may offer and sell securities in one or more offerings.

You should rely only on the information contained in this prospectus supplement and the accompanying prospectus, including the documents incorporated by reference herein and therein, and any “free writing prospectus” we authorize to be delivered to you. We have not and the underwriters have not authorized anyone to provide you with any information other than information contained in this prospectus supplement and the accompanying prospectus, including the documents incorporated by reference herein and therein, and any “free writing prospectus” we have authorized for use in connection with this offering. If anyone provides you with different or additional information, you should not rely on it. This prospectus supplement and the accompanying prospectus, including the documents incorporated by reference herein and therein, and any authorized “free writing prospectus” are not an offer to sell or the solicitation of an offer to buy any securities other than the notes to which this prospectus supplement relates, nor is this prospectus supplement, the accompanying prospectus, including the documents incorporated by reference herein and therein, or any authorized “free writing prospectus” an offer to sell or the solicitation of an offer to buy securities in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction. You should assume that the information contained in this prospectus supplement and the accompanying prospectus, including the documents incorporated by reference herein and therein, and any authorized “free writing prospectus” is accurate only as of their respective dates regardless of the time of delivery of this prospectus supplement, the accompanying prospectus and any authorized “free writing prospectus”. Our business, financial condition, results of operations and prospects may have changed since those dates.

It is important for you to read and consider all information contained in this prospectus supplement and the accompanying prospectus, including the documents incorporated by reference herein and therein, and any authorized “free writing prospectus,” in making your investment decision. See “Where You Can Find More Information” in this prospectus supplement and the accompanying prospectus and “Information Incorporated by Reference” in this prospectus supplement and in the accompanying prospectus.

This prospectus supplement and the accompanying prospectus contain, or incorporate by reference, forward-looking statements. Such forward-looking statements should be considered together with the cautionary statements and important factors included or referred to in this prospectus supplement, the accompanying prospectus and the documents incorporated by reference herein or therein. See “Cautionary Statement Regarding Forward-Looking Statements” in this prospectus supplement and in the accompanying prospectus.

S-ii

Table of Contents

Except as otherwise indicated or required by the context, references in this prospectus supplement to:

| • | “2020 Notes” refers to the Issuers’ 4.875% senior unsecured notes in the aggregate principal amount of $1.0 billion that mature on November 1, 2020; |

| • | “Capital Corp.” refers to GLP Financing II, Inc., a Delaware corporation and wholly-owned subsidiary of the Operating Partnership; |

| • | “Credit Facility” refers to the Company’s senior unsecured credit facility consisting of a $1,175.0 million revolving credit facility and a $525.0 million Term Loan A-1 facility. The revolving credit facility matures on May 21, 2023 and the Term Loan A-1 facility matures on April 28, 2021. See “Description of Certain Other Indebtedness—Credit Facility”; |

| • | “GLPI” refers to Gaming and Leisure Properties, Inc., a Pennsylvania corporation and the guarantor of the notes offered hereby, and, unless the context otherwise requires, none of its subsidiaries; |

| • | “Issuers” refer to the Operating Partnership and Capital Corp. and none of their consolidated subsidiaries; |

| • | “Operating Partnership” refers to GLP Capital, L.P., a Pennsylvania limited partnership and wholly-owned subsidiary of GLPI through which GLPI owns substantially all of its real estate assets; |

| • | “Revolver” refers to the $1,175.0 million revolving credit facility under the Credit Facility; |

| • | “Term Loan A-1” refers to the $525.0 million unsecured Term Loan A-1 under the Credit Facility; |

| • | “Tender Offer” refers to the cash tender offer to purchase up to $500.0 million of the outstanding 2020 Notes for up to $512.0 million in cash, subject to the relevant terms and conditions set forth in the Offer to Purchase, dated August 15, 2019 (the “Offer to Purchase”) related to the Tender Offer, which we launched on August 15, 2019 and which will expire at 11:59 p.m., New York City time on September 12, 2019 (neither this prospectus supplement nor the accompanying prospectus constitute an offer to purchase any of our outstanding 2020 Notes and any such offer will be effected solely through the Offer to Purchase); |

| • | “Transactions” refers collectively to (i) the issuance of the notes offered hereby, (ii) the use of approximately $340.0 million of the net proceeds from this offering to repay outstanding borrowings under the Revolver, excluding any accrued and unpaid interest thereon, (iii) the use of approximately $236.0 million of the net proceeds from this offering to repay outstanding borrowings under the Term Loan A-1 facility, excluding any accrued and unpaid interest thereon, and (iv) the use of approximately $512.0 million of the net proceeds from this offering to finance the Tender Offer, assuming $500.0 million of the 2020 Notes are tendered in the Tender Offer; and |

| • | “We”, “our”, “us” and “the Company” refer to GLPI and its consolidated subsidiaries; provided that with respect to the discussion of the terms of the notes on the cover page of this prospectus supplement, in the section entitled “Prospectus Supplement Summary—The Offering,” and in the section entitled “Description of the Notes,” references to “we”, “our” and “us” refer only to the Issuers and none of their subsidiaries. |

S-iii

Table of Contents

PRESENTATION OF NON-GAAP FINANCIAL INFORMATION

Funds From Operations (“FFO”), Adjusted Funds From Operations (“AFFO”) and Adjusted Earnings Before Interest, Tax, Depreciation and Amortization (“Adjusted EBITDA”), which are presented in this prospectus supplement, are not required by, or presented in accordance with, generally accepted accounting principles in the United States (“GAAP”). We use these non-GAAP financial measures as performance measures for benchmarking against our peers and as internal measures of business operating performance, which is used as a bonus metric. We believe FFO, AFFO and Adjusted EBITDA provide a meaningful perspective of the underlying operating performance of our current business. This is especially true since these measures exclude real estate depreciation and we believe that real estate values fluctuate based on market conditions rather than depreciating in value ratably on a straight-line basis over time. In addition, in order for GLPI to qualify as a REIT, it must distribute 90% of its REIT taxable income annually. We adjust AFFO accordingly to provide our investors an estimate of the taxable income available for this distribution requirement.

FFO, AFFO and Adjusted EBITDA are non-GAAP financial measures that are considered supplemental measures for the real estate industry and a supplement to GAAP measures. The National Association of Real Estate Investment Trusts defines FFO as net income (computed in accordance with GAAP), excluding (gains) or losses from sales of property and real estate depreciation. We define AFFO as FFO excluding stock based compensation expense, the amortization of debt issuance costs, bond premiums and original issuance discounts, other depreciation, the amortization of land rights, straight-line rent adjustments, direct financing lease adjustments, losses on debt extinguishment, retirement costs and goodwill and loan impairment charges, reduced by maintenance capital expenditures. Finally, we define Adjusted EBITDA as net income excluding interest, taxes on income, depreciation, (gains) or losses from sales of property, stock based compensation expense, straight-line rent adjustments, direct financing lease adjustments, the amortization of land rights, losses on debt extinguishment, retirement costs and goodwill and loan impairment charges.

FFO, AFFO and Adjusted EBITDA are not recognized terms under GAAP. These non-GAAP financial measures: (i) do not represent cash flow from operations as defined by GAAP; (ii) should not be considered as an alternative to net income as a measure of operating performance or to cash flows from operating, investing and financing activities; and (iii) are not alternatives to cash flow as a measure of liquidity. In addition, these measures should not be viewed as an indication of our ability to fund all of our cash needs, including to make cash distributions to our shareholders, to fund capital improvements, or to make interest payments on our indebtedness. FFO, AFFO and Adjusted EBITDA, as presented, may not be comparable to similarly titled measures reported by other real estate companies, including REITs due to the fact that not all real estate companies use the same definitions. Our presentation of these measures does not replace the presentation of our financial results in accordance with GAAP.

For reconciliations of our net income to FFO, AFFO and Adjusted EBITDA, see the section entitled “Prospectus Supplement Summary—Summary Historical Consolidated Financial Information”.

S-iv

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this prospectus supplement and the accompanying prospectus, including the documents incorporated by reference herein and therein, and in any “free writing prospectus” that we have authorized for use in connection with this offering, may constitute “forward-looking statements” within the meaning of the safe harbor from civil liability provided for such statements by the Private Securities Litigation Reform Act of 1995 (set forth in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Forward-looking statements include information concerning our business strategy, plans, goals and objectives.

Forward-looking statements included or incorporated by reference in this prospectus supplement and the accompanying prospectus include, but are not limited to, statements regarding our ability to grow our portfolio of gaming facilities and to secure additional avenues of growth beyond the gaming industry and our intended use of proceeds from this offering. In addition, statements preceded by, followed by or that otherwise include the words “believes”, “expects”, “anticipates”, “intends”, “projects”, “estimates”, “plans”, “may increase”, “may fluctuate” and similar expressions or future or conditional verbs such as “will”, “should”, “would”, “may” and “could” are generally forward-looking in nature and not historical facts. You should understand that the following important factors could affect future results and could cause actual results to differ materially from those expressed in such forward-looking statements:

| • | the availability of and the ability to identify suitable and attractive acquisition and development opportunities and the ability to acquire and lease properties on favorable terms; |

| • | the degree and nature of our competition; |

| • | the ability to receive, or delays in obtaining, the regulatory approvals required to own and/or operate our properties, or other delays or impediments to completing our planned acquisitions or projects; |

| • | our ability to maintain our status as a REIT, given the highly technical and complex Internal Revenue Code (the “Code”) provisions for which only limited judicial and administrative authorities exist, where even a technical or inadvertent violation could jeopardize REIT qualification and where requirements may depend in part on the actions of third parties over which we have no control or only limited influence; |

| • | the satisfaction of certain asset, income, organizational, distribution, shareholder ownership and other requirements on a continuing basis in order for GLPI to maintain its REIT status; |

| • | the ability and willingness of our tenants, operators and other third parties to meet and/or perform their obligations under their respective contractual arrangements with us, including lease and note requirements and in some cases, their obligations to indemnify, defend and hold us harmless from and against various claims, litigation and liabilities; |

| • | the ability of our tenants and operators to maintain the financial strength and liquidity necessary to satisfy their respective obligations and liabilities to third parties, including without limitation to satisfy obligations under their existing credit facilities and other indebtedness; |

| • | the ability of our tenants and operators to comply with laws, rules and regulations in the operation of our properties, to deliver high quality services, to attract and retain qualified personnel and to attract customers; |

| • | the satisfaction of the mortgage loan made to Eldorado Resorts, Inc. (“Eldorado”) by way of substitution of one or more additional Eldorado properties acceptable to Eldorado and us, which will be transferred to us; |

S-v

Table of Contents

| • | the ability to generate sufficient cash flows to service our outstanding indebtedness; |

| • | the access to debt and equity capital markets, including for acquisitions or refinancings due to maturities; |

| • | adverse changes in our credit rating; |

| • | fluctuating interest rates; |

| • | the impact of global or regional economic conditions; |

| • | the availability of qualified personnel and our ability to retain our key management personnel; |

| • | our obligation to indemnify Penn National Gaming, Inc. (“Penn”) and its subsidiaries under certain circumstances if the Penn Spin-Off (as defined in the section entitled “Prospectus Supplement Summary—About Our Company” and as further described in GLPI’s Annual Report on Form 10-K for the year ended December 31, 2018 (“2018 10-K”)) fails to be tax-free; |

| • | changes in the U.S. tax law and other state, federal or local laws, whether or not specific to real estate, real estate investment trusts or to the gaming, lodging or hospitality industries; |

| • | changes in accounting standards; |

| • | the impact of weather events or conditions, natural disasters, acts of terrorism and other international hostilities, war or political instability; |

| • | other risks inherent in the real estate business, including potential liability relating to environmental matters and illiquidity of real estate investments; and |

| • | additional factors as discussed in the 2018 10-K, in GLPI’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2019 (“2019 Q1 10-Q”) and June 30, 2019 (“2019 Q2 10-Q”), and in GLPI’s Current Reports on Form 8-K filed with the SEC. |

Other unknown or unpredictable factors may also cause actual results to differ materially from those projected by the forward-looking statements. Most of these factors are difficult to anticipate and are generally beyond our control. Given these uncertainties, you should not place undue reliance on these forward-looking statements. You should consider the areas of risk described above in connection with considering any forward-looking statements that may be made by us generally and any forward-looking statements that are included or incorporated by reference herein or in the accompany prospectus supplement specifically. We do not undertake any obligation to release publicly any revisions to any forward-looking statements, to report events or to report the occurrence of unanticipated events unless required to do so by law.

S-vi

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus supplement, in the accompanying prospectus and in the documents incorporated by reference herein and therein and does not contain all of the information that may be important to you. You should carefully read this entire prospectus supplement, the accompanying prospectus and the documents incorporated herein and therein by reference, including the section entitled “Risk Factors” beginning on pageS-19 of this prospectus supplement and in GLPI’s 201810-K, 2019 Q110-Q and 2019 Q210-Q, before making an investment decision regarding the notes.

About our company

GLPI is a self-administered and self-managed Pennsylvania REIT, which was incorporated in February 2013 as a wholly-owned subsidiary of Penn National Gaming, Inc. (“Penn”). GLPI’s primary business consists of acquiring, financing, and owning real estate property to be leased to gaming operators intriple-net lease arrangements. On November 1, 2013, Penn contributed to GLPI, through a series of internal corporate restructurings, substantially all of the assets and liabilities associated with Penn’s real property interests and real estate development business, as well as the assets and liabilities of Hollywood Casino Baton Rouge and Hollywood Casino Perryville (the “TRS Properties”) and thenspun-off GLPI to holders of Penn’s common and preferred stock in atax-free distribution (the “PennSpin-Off”). GLPI elected on its U.S. federal income tax return for the taxable year beginning on January 1, 2014 to be treated as a REIT and, together with its indirect wholly-owned subsidiary, GLP Holdings, Inc., jointly elected to treat each of GLP Holdings, Inc., Louisiana Casino Cruises, Inc. (d/b/a Hollywood Casino Baton Rouge) and Penn Cecil Maryland, Inc. (d/b/a Hollywood Casino Perryville) as a “taxable REIT subsidiary” (“TRS”) effective on the first day of the first taxable year of GLPI as a REIT. As a result of the PennSpin-Off, GLPI owns substantially all of Penn’s former real property assets (as of the PennSpin-Off) and leases back most of those assets to Penn for use by its subsidiaries, under a unitary master lease, atriple-net operating lease with an initial term of 15 years (expiring October 31, 2028) with no purchase option, followed by four5-year renewal options (exercisable by Penn) on the same terms and conditions (the “Penn Master Lease”). GLPI also owns and operates the TRS Properties through an indirect wholly-owned subsidiary, GLP Holdings, Inc.

In April 2016, the Company acquired substantially all of the real estate assets of Pinnacle Entertainment, Inc. (“Pinnacle”) for approximately $4.8 billion. GLPI originally leased these assets back to Pinnacle under a unitarytriple-net lease with an initial term of 10 years (expiring April 30, 2026) with no purchase option, followed by five5-year renewal options (exercisable by Pinnacle) on the same terms and conditions (the “Pinnacle Master Lease”). On October 15, 2018, the Company completed its previously announced transactions with Penn, Pinnacle and Boyd Gaming Corporation (“Boyd”) to accommodate Penn’s acquisition of the majority of Pinnacle’s operations, pursuant to a definitive agreement and plan of merger between Penn and Pinnacle, dated December 17, 2017 (the “Penn-Pinnacle Merger”). Concurrent with the Penn-Pinnacle merger, the Company amended the Pinnacle Master Lease to allow for the sale of the operating assets of Ameristar Casino Hotel Kansas City, Ameristar Casino Resort Spa St. Charles and Belterra Casino Resort from Pinnacle to Boyd (the “Amended Pinnacle Master Lease”) and entered into a new unitarytriple-net master lease agreement with Boyd (the “Boyd Master Lease”) for these properties on terms similar to the Company’s Amended Pinnacle Master Lease. The Boyd Master Lease has an initial term of 10 years (from the original April 2016 commencement date of the Pinnacle Master Lease and expiring April 30, 2026), with no purchase option, followed by five5-year renewal options (exercisable by Boyd) on the same terms and conditions. The Company also purchased the real estate assets of Plainridge Park Casino (“Plainridge Park”) from Penn for $250.0 million, exclusive of transaction fees and taxes and added this property to the Amended Pinnacle Master Lease. The Amended Pinnacle Master Lease was assumed by Penn at the consummation of the Penn-Pinnacle Merger. The Company also entered into a mortgage loan agreement with Boyd in connection with Boyd’s acquisition of Belterra Park Gaming & Entertainment Center (“Belterra Park”), whereby the Company loaned Boyd $57.7 million.

S-1

Table of Contents

In addition to the acquisition of Plainridge Park described above, on October 1, 2018, the Company closed its previously announced transaction to acquire certain real property assets from Tropicana Entertainment Inc. (“Tropicana”) and certain of its affiliates pursuant to a Purchase and Sale Agreement (the “Real Estate Purchase Agreement”) dated April 15, 2018 between Tropicana and GLP Capital L.P., which was subsequently amended on October 1, 2018 (as amended, the “Amended Real Estate Purchase Agreement”). Pursuant to the terms of the Amended Real Estate Purchase Agreement, the Company acquired the real estate assets of Tropicana Atlantic City, Tropicana Evansville, Tropicana Laughlin, Trop Casino Greenville and the Belle of Baton Rouge (the “GLP Assets”) from Tropicana for an aggregate cash purchase price of $964.0 million, exclusive of transaction fees and taxes (the “Tropicana Acquisition”). Concurrent with the Tropicana Acquisition, Eldorado acquired the operating assets of these properties from Tropicana pursuant to an Agreement and Plan of Merger dated April 15, 2018 by and among Tropicana, GLP Capital, Eldorado and a wholly-owned subsidiary of Eldorado, and leased the GLP Assets from the Company pursuant to the terms of a new unitarytriple-net master lease with an initial term of 15 years, with no purchase option followed by four successive5-year renewal periods (exercisable by Eldorado) on the same terms and conditions (the “Eldorado Master Lease”). Additionally, on October 1, 2018 the Company made a mortgage loan to Eldorado in the amount of $246.0 million in connection with Eldorado’s acquisition of Lumiere Place Casino and Hotel (“Lumiére Place”).

As of June 30, 2019, GLPI’s portfolio consisted of interests in 46 gaming and related facilities, including the TRS Properties, the real property associated with 33 gaming and related facilities operated by Penn, the real property associated with 6 gaming and related facilities operated by Eldorado (including one mortgaged facility), the real property associated with 4 gaming and related facilities operated by Boyd (including one mortgaged facility) and the real property associated with the Casino Queen in East St. Louis, Illinois. These facilities are geographically diversified across 16 states and were 100% occupied at June 30, 2019. GLPI expects to continue growing our portfolio by pursuing opportunities to acquire additional gaming facilities to lease to gaming operators under prudent terms.

As of June 30, 2019, the majority of our earnings are the result of the rental revenues we receive from ourtriple-net master leases with Penn, Boyd and Eldorado. Additionally, we have rental revenue from the Casino Queen property which is leased back to a third-party operator on atriple-net basis and the Meadows property which is leased to Penn under a single propertytriple-net lease (the “Penn Meadows Lease”). In addition to rent, the tenants are required to pay the following executory costs: (1) all facility maintenance, (2) all insurance required in connection with the leased properties and the business conducted on the leased properties, including coverage of the landlord’s interests, (3) taxes levied on or with respect to the leased properties (other than taxes on the income of the lessor) and (4) all utilities and other services necessary or appropriate for the leased properties and the business conducted on the leased properties.

Additionally, in accordance with ASC 842, we record revenue for the ground lease rent paid by our tenants with an offsetting expense in land rights and ground lease expense within the condensed consolidated statement of income as we have concluded that as the lessee we are the primary obligor under the ground leases. We sublease these ground leases back to our tenants, who are responsible for payment directly to the landlord. Gaming revenue for our TRS Properties is derived primarily from gaming on slot machines and to a lesser extent, table game and poker revenue, which is highly dependent upon the volume and spending levels of customers at our TRS Properties. Other revenues at our TRS Properties are derived from our dining, retail and certain other ancillary activities.

We may periodically loan funds to casino owner-operators pursuant to secured mortgage loans for the purchase of gaming related properties. Interest income related to mortgage loans receivable is recorded as revenue from mortgaged real estate within our condensed consolidated statements of income in the period earned. At June 30, 2019, we had financial interests in two casino properties, Belterra Park and Lumière Place, pursuant to the secured mortgage loans made by us to the respective casino owner-operators, Boyd and Eldorado.

S-2

Table of Contents

Our Adjusted EBITDA and AFFO for the six months ended June 30, 2019 were $519.3 million and $368.0 million, respectively. For definitions of Adjusted EBITDA and AFFO and reconciliations to our net income, see “Presentation ofNon-GAAP Financial Information” and “Prospectus Supplement Summary—Summary Historical Consolidated Combined Financial Information”.

The Operating Partnership is a wholly-owned subsidiary of GLPI through which GLPI owns substantially all of its assets and was formed under Pennsylvania law in March 2013.

Our history

Our competitive strengths

High quality geographically diverse portfolio

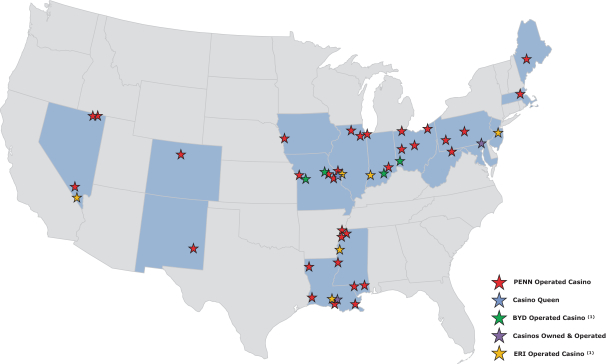

As of June 30, 2019, our portfolio consisted of interests in 46 gaming and related facilities, including the TRS Properties, the real property associated with 33 gaming and related facilities operated by Penn, the real property associated with 6 gaming and related facilities operated by Eldorado (including one mortgaged facility), the real property associated with 4 gaming and related facilities operated by Boyd (including one mortgaged facility) and the real property associated with the Casino Queen in East St. Louis, Illinois. These facilities are geographically diversified across 16 states and were 100% occupied at June 30, 2019.

We believe that these properties represent some of the top revenue-producing casinos in leading U.S. regional gaming markets.

S-3

Table of Contents

Map of Our Properties

| (1) | Includes two properties for which GLPI has provided mortgage loans (one operated by BYD and one by ERI) |

Strong operating company tenants

As of June 30, 2019, approximately 80% of our collective rental income, excluding deferrals and land leasegross-ups, was derived from tenant leases with Penn, and approximately 20% was derived from tenant leases with Casino Queen, Eldorado and Boyd. Each of Penn, Eldorado and Boyd are leading, diversified, multi-jurisdictional owners and managers of gaming and pari-mutuel properties and established gaming providers with strong financial performance records. These three tenants have each operated casinos as public companies, with each of Penn and Boyd having done so for several decades. As derived from their respective Quarterly Reports on Form10-Q filed with the SEC for the quarter ended June 30, 2019, Penn, Boyd and Eldorado generated approximately $1.3 billion, $846.1 million and $637.1 million of total revenues, respectively, for the three months ended June 30, 2019. The Company has not independently verified this information and is providing this data for informational purposes and Penn’s, Boyd’s and Eldorado’s respective quarterly reports on Form10-Q for the quarter ended June 30, 2019 are not incorporated by reference into, and do not constitute a part of, this prospectus supplement or the accompanying prospectus. Each of these three tenants has historically exhibited sufficient liquidity and ability to satisfy their rent obligations. Additionally, the regional markets where they have historically operated casinos have generally proven more profitable and stable during economic cycles than the Las Vegas gaming market.

S-4

Table of Contents

Tenant Rent Diversification

Three Months Ended June 30, 2019 | PENN Master Lease | Amended Pinnacle Master Lease | ERI Master Lease and Mortgage | BYD Master Lease and Mortgage | PENN Meadows Lease | Casino Queen Lease | Total | |||||||||||||||||||||

Building base rent | $ | 68,482 | $ | 56,297 | $ | 15,229 | $ | 18,702 | $ | 3,284 | $ | 2,276 | $ | 164,270 | ||||||||||||||

Land base rent | 23,492 | 17,778 | 3,340 | 2,933 | — | — | 47,543 | |||||||||||||||||||||

Percentage rent | 21,873 | 7,905 | 3,340 | 2,796 | 2,792 | 1,356 | 40,062 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total cash rental income | $ | 113,847 | $ | 81,980 | $ | 21,909 | $ | 24,431 | $ | 6,076 | $ | 3,632 | $ | 251,875 | ||||||||||||||

Straight-line rent adjustments | 2,232 | (6,319 | ) | (2,894 | ) | (2,235 | ) | 573 | — | (8,643 | ) | |||||||||||||||||

Ground rent in revenue | 926 | 1,729 | 2,115 | 418 | — | — | 5,188 | |||||||||||||||||||||

Other rental revenue | — | — | — | — | 143 | — | 143 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total rental income | $ | 117,005 | $ | 77,390 | $ | 21,130 | $ | 22,614 | $ | 6,792 | $ | 3,632 | $ | 248,563 | ||||||||||||||

Interest income from mortgaged real estate | — | — | 5,590 | 1,611 | — | — | 7,201 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total income from real estate | $ | 117,005 | $ | 77,390 | $ | 26,720 | $ | 24,225 | $ | 6,792 | $ | 3,632 | $ | 255,764 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Six Months Ended June 30, 2019 | PENN Master Lease | Amended Pinnacle Master Lease | ERI Master Lease and Mortgage | BYD Master Lease and Mortgage | PENN Meadows Lease | Casino Queen Lease | Total | |||||||||||||||||||||

Building base rent | $ | 136,964 | $ | 112,078 | $ | 30,459 | $ | 36,988 | $ | 6,567 | $ | 4,551 | $ | 327,607 | ||||||||||||||

Land base rent | 46,984 | 35,481 | 6,680 | 5,839 | — | — | 94,984 | |||||||||||||||||||||

Percentage rent | 43,558 | 15,738 | 6,680 | 5,566 | 5,584 | 2,712 | 79,838 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total cash rental income | $ | 227,506 | $ | 163,297 | $ | 43,819 | $ | 48,393 | $ | 12,151 | $ | 7,263 | $ | 502,429 | ||||||||||||||

Straight-line rent adjustments | 4,463 | (12,637 | ) | (5,789 | ) | (4,469 | ) | 1,145 | — | (17,287 | ) | |||||||||||||||||

Ground rent in revenue | 1,888 | 3,510 | 4,501 | 852 | — | — | 10,751 | |||||||||||||||||||||

Other rental revenue | — | — | — | — | 348 | — | 348 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total rental income | $ | 233,857 | $ | 154,170 | $ | 42,531 | $ | 44,776 | $ | 13,644 | $ | 7,263 | $ | 496,241 | ||||||||||||||

Interest income from mortgaged real estate | — | — | 11,181 | 3,213 | — | — | 14,394 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total income from real estate | $ | 233,857 | $ | 154,170 | $ | 53,712 | $ | 47,989 | $ | 13,644 | $ | 7,263 | $ | 510,635 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Stable cash flows

Our real estate properties are leased under long-termtriple-net leases guaranteed by our tenants, pursuant to which the tenant is responsible for all facility maintenance, insurance required in connection with the leased properties and the business conducted on the leased properties, taxes levied on or with respect to the leased properties and all utilities and other services necessary or appropriate for the leased properties and the business conducted on the leased properties.

Penn, Boyd and Eldorado are subject to such long-term cross-collateralized master lease agreements. The Penn Master Lease has an initial15-year term (with four5-year extensions), the Amended Pinnacle Master Lease has an initial10-year term (with five5-year extensions), the Boyd Master Lease has an initial10-year term (with five5-year extensions) and the Eldorado Master Lease has an initial15-year term (with four5-year extensions). There are approximately 9, 6.5, 6.5 and 14 years left under the initial terms of the Penn Master Lease, the Amended Pinnacle Master Lease, the Boyd Master Lease and the Eldorado Master Lease, respectively, and each includes a fixed building rent component with a set annual rent escalator (subject to minimum rent coverage).

S-5

Table of Contents

The Master Leases provide steadyin-place organic rent growth. As of June 30, 2019, on a stand-alone basis, approximately 84% of our rental income from rental properties was fixed, excluding deferrals and land leasegross-ups. This provides protection from fluctuations in the economy or regional gaming markets. See “—Master lease summaries” for a description of the lease agreements.

Balance sheet positioned for future growth

We believe there is a market opportunity to acquire additional casino and other leisure properties and that our balance sheet is well-positioned to support such growth. Our moderate leverage, which is in line with ourtriple-net peers, provides us with the ability to pursue either internal or external growth opportunities. Furthermore, our well-laddered debt maturity profile and capital structure provides further flexibility that we believe will enable us to better take advantage of potential opportunities as they arise.

Proven and experienced management team

Our management team boasts leading industry experience, while maintaining a prudent management approach. Peter M. Carlino, our chief executive officer, has more than 30 years of experience in the acquisition and development of gaming facilities and other real estate projects. Steven T. Snyder, our chief financial officer, is a finance professional with more than 20 years of experience in the gaming industry. Through years of public company experience, our management team also has extensive experience accessing both debt and equity capital markets to fund growth and maintain a flexible capital structure. We believe that our management team will be able to leverage their strong long-term gaming industry, real estate, investment banking, and lending relationships to source and finance future acquisitions.

Our business and growth strategies

Master leases have escalators and percentage rent components

Our leases have a substantial fixed rent component, representing 84% of our rental income excluding deferrals and land lease gross ups for the six months ended June 30, 2019. Approximately 77% of the fixed rent for the six months ended June 30, 2019 is subject to annual rent escalators based on certain rent coverage metrics. The leases generate steady growth in revenues from rental properties and provide a benchmark with which we can implement similar rent growth measures for properties that might be acquired in the future. The Penn Master Lease and the Amended Pinnacle Master Lease contain an escalation provision for up to 2% of the base rent. The Penn Meadows Lease also contains an annual escalator provision for up to 5% of the base rent. The escalator remains at 5% for ten years or until total rent is $31 million, at which point the escalator will be reduced to 2% annually thereafter. The Eldorado Master Lease contains an escalator provision for up to 2% of the base rent, which is guaranteed for the first five anniversaries of the lease so long as the escalator increase does not create an event of default. The Boyd Master Lease also contains an escalator provision for up to 2% of the base rent.

Attractive financing alternative for private or public single or multi-site operators

We have the flexibility to operate through an umbrella partnership, commonly referred to as an UPREIT structure, in which substantially all of our properties and assets are held by the Operating Partnership or by subsidiaries of the Operating Partnership. Conducting business through the Operating Partnership allows us flexibility in the manner in which we structure and acquire properties. In particular, an UPREIT structure enables us to acquire additional properties from sellers in exchange for limited partnership units, which provides property owners the opportunity to defer the tax consequences that would otherwise arise from a sale of their real properties and other assets to us. As a result, this structure potentially may facilitate our acquisition of assets in a more efficient manner and may allow us to acquire assets that the owner would otherwise be unwilling to sell

S-6

Table of Contents

because of tax considerations. We believe that this flexibility will provide us with an advantage in seeking future acquisitions. Further, we could purchase a property outright and roll the acquired asset into an existing master lease agreement with one of our current operators. Additionally, we may be able to partner with other third-party operators to diversify our tenant base.

Sale-leaseback and acquisitions in the gaming space

As the first publicly tradedtriple-net lease REIT focused on gaming, we believe we are well positioned to partner with gaming operators looking to monetize their real estate assets. To capitalize on this, we intend to explore future potential sale-leaseback opportunities with various regional gaming operators looking to shed real estate assets in an effort to focus on gaming operations. Sale-leasebacks continue to be highly attractive to gaming operators who have a need or a desire to receive immediate cash flow, while maintaining the use of the gaming facilities through long-term leases. We believe that the use of sale-leasebacks will help us grow our portfolio and, in turn, will provide shareholders with more stable and diversified revenue streams and reliable cash flows in the future.

Potential to expand outside of gaming

We believe that our focus ontriple-net lease structures will provide us with flexibility to diversify our tenant base in the future. Thetriple-net lease tenant universe spans virtually every real estate sector, including gaming, leisure, retail, and many others. The diverse array oftriple-net opportunities may provide potential tenant and industry diversification avenues for us over time. Further, we have a proven business model that supports scale across various markets and industries, and, we believe, will allow us to quickly expand by acquiring large portfolios.

Our portfolio

GLPI properties

As of June 30, 2019, our diversified high-quality real estate portfolio consisted of 46 gaming and related facilities, comprised of approximately 23.5 million of square footage and over 5,600 acres of owned and leased land and was broadly diversified by location across 16 states. As of June 30, 2019, our portfolio was 100% occupied.

The following table presents selected statistical and other information concerning our properties as of June 30, 2019.

| Location | Tenant/ Operator | Approx. Property Square Footage(1) | Owned Acreage | Leased Acreage(2) | Hotel Rooms | |||||||||||||||||||

Tenant Occupied Properties | ||||||||||||||||||||||||

Hollywood Casino Lawrenceburg | Lawrenceburg, IN | Penn | 634,000 | 73.1 | 32.1 | 295 | ||||||||||||||||||

Hollywood Casino Aurora | Aurora, IL | Penn | 222,189 | 0.4 | 1.7 | — | ||||||||||||||||||

Hollywood Casino Joliet | Joliet, IL | Penn | 322,446 | 275.6 | — | 100 | ||||||||||||||||||

Argosy Casino Alton | Alton, IL | Penn | 124,569 | 0.2 | 3.6 | — | ||||||||||||||||||

Hollywood Casino Toledo | Toledo, OH | Penn | 285,335 | 42.3 | — | — | ||||||||||||||||||

Hollywood Casino Columbus | Columbus, OH | Penn | 354,075 | 116.2 | — | — | ||||||||||||||||||

Hollywood Casino at Charles Town Races | Charles Town, WV | Penn | 511,249 | 298.6 | — | 150 | ||||||||||||||||||

Hollywood Casino at Penn National Race Course | Grantville, PA | Penn | 451,758 | 573.7 | — | — | ||||||||||||||||||

S-7

Table of Contents

| Location | Tenant/ Operator | Approx. Property Square Footage(1) | Owned Acreage | Leased Acreage(2) | Hotel Rooms | |||||||||||||||

M Resort | Henderson, NV | Penn | 910,173 | 83.5 | — | 390 | ||||||||||||||

Hollywood Casino Bangor | Bangor, ME | Penn | 257,085 | 6.4 | 37.9 | 152 | ||||||||||||||

Zia Park Casino(3) | Hobbs, NM | Penn | 109,067 | 317.4 | — | — | ||||||||||||||

Hollywood Casino Gulf Coast | Bay St. Louis, MS | Penn | 425,920 | 578.7 | — | 291 | ||||||||||||||

Argosy Casino Riverside | Riverside, MO | Penn | 450,397 | 37.9 | — | 248 | ||||||||||||||

Hollywood Casino Tunica | Tunica, MS | Penn | 315,831 | — | 67.7 | 494 | ||||||||||||||

Boomtown Biloxi | Biloxi, MS | Penn | 134,800 | 1.5 | 1 | — | ||||||||||||||

Hollywood Casino St. Louis | Maryland Heights, MO | Penn | 645,270 | 220.8 | — | 502 | ||||||||||||||

Hollywood Gaming at Dayton Raceway | Dayton, OH | Penn | 191,037 | 119.7 | — | — | ||||||||||||||

Hollywood Gaming at Mahoning Valley Race Course | Youngstown, OH | Penn | 177,448 | 193.4 | — | — | ||||||||||||||

Resorts Casino Tunica(4) | Tunica, MS | Penn | 319,823 | — | 86.6 | 201 | ||||||||||||||

1st Jackpot Casino | Tunica, MS | Penn | 78,941 | 52.9 | 93.8 | — | ||||||||||||||

Ameristar Black Hawk | Black Hawk, CO | Penn | 775,744 | 104.1 | — | 535 | ||||||||||||||

Ameristar East Chicago | East Chicago, IN | Penn | 509,867 | — | 21.6 | 288 | ||||||||||||||

Ameristar Council Bluffs(3) | Council Bluffs, IA | Penn | 312,047 | 36.2 | 22.6 | 160 | ||||||||||||||

L’Auberge Baton Rouge | Baton Rouge, LA | Penn | 436,461 | 99.1 | — | 205 | ||||||||||||||

Boomtown Bossier City | Bossier City, LA | Penn | 281,747 | 21.8 | — | 187 | ||||||||||||||

L’Auberge Lake Charles | Lake Charles, LA | Penn | 1,014,497 | — | 234.5 | 995 | ||||||||||||||

Boomtown New Orleans | New Orleans, LA | Penn | 278,227 | 53.6 | — | 150 | ||||||||||||||

Ameristar Vicksburg | Vicksburg, MS | Penn | 298,006 | 74.1 | — | 148 | ||||||||||||||

River City Casino and Hotel | St. Louis, MO | Penn | 431,226 | — | 83.4 | 200 | ||||||||||||||

Jackpot Properties(5) | Jackpot, NV | Penn | 419,800 | 79.5 | — | 416 | ||||||||||||||

Plainridge Park Casino | Plainville, MA | Penn | 196,473 | 87.9 | — | — | ||||||||||||||

The Meadows Racetrack and | Washington, PA | Penn | 417,921 | 155.5 | — | — | ||||||||||||||

Casino Queen | East St. Louis, IL | Casino Queen | 330,502 | 67.2 | — | 157 | ||||||||||||||

Belterra Casino Resort | Florence, IN | Boyd | 782,393 | 167.1 | 148.5 | 662 | ||||||||||||||

Ameristar Kansas City | Kansas City, MO | Boyd | 763,939 | 224.5 | 31.4 | 184 | ||||||||||||||

Ameristar St. Charles | St. Charles, MO | Boyd | 1,272,938 | 241.2 | — | 397 | ||||||||||||||

Tropicana Atlantic City | Atlantic City, NJ | Eldorado | 4,232,018 | 18.3 | — | 2,366 | ||||||||||||||

Tropicana Evansville | Evansville, IN | Eldorado | 754,833 | 18.4 | 10.2 | 338 | ||||||||||||||

Tropicana Laughlin | Laughlin, NV | Eldorado | 936,453 | 93.6 | — | 1,487 | ||||||||||||||

Trop Casino Greenville | Greenville, MS | Eldorado | 94,017 | — | 7.4 | 40 | ||||||||||||||

Belle of Baton Rouge | Baton Rouge, LA | Eldorado | 386,398 | 13.1 | 0.8 | 288 | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

| 21,846,920 | 4,547.5 | 884.8 | 12,026 | |||||||||||||||||

Mortgaged Properties | ||||||||||||||||||||

Belterra Park Gaming & Entertainment Center(6) | Cincinnati, OH | Boyd | 372,650 | 160 | — | — | ||||||||||||||

Lumiére Place(6) | St. Louis, MO | Eldorado | 1,020,782 | 18.5 | — | 494 | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

| 1,393,432 | 178.5 | — | 494 | |||||||||||||||||

S-8

Table of Contents

| Location | Tenant/ Operator | Approx. Property Square Footage(1) | Owned Acreage | Leased Acreage(2) | Hotel Rooms | |||||||||||||||

Other Properties | ||||||||||||||||||||

Other owned buildings and land(7) | various | N/A | 23,400 | 3.9 | — | — | ||||||||||||||

TRS Properties | ||||||||||||||||||||

Hollywood Casino Baton Rouge | Baton Rouge, LA | GLPI | 95,318 | 25.1 | — | — | ||||||||||||||

Hollywood Casino Perryville | Perryville, MD | GLPI | 97,961 | 36.4 | — | — | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

| 193,279 | 61.5 | — | — | |||||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

Total | 23,457,031 | 4,791.4 | 884.8 | 12,520 | ||||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

| (1) | Square footage includesair-conditioned space and excludes parking garages and barns. |

| (2) | Leased acreage reflects land subject to leases with third-parties and includes land on which certain of the current facilities and ancillary supporting structures are located as well as parking lots and access rights. |

| (3) | These properties include hotels not owned by us. Square footage and rooms associated with properties not owned by us are excluded from the table above. |

| (4) | Property ceased gaming operations on June 30, 2019. |

| (5) | Encompasses two gaming properties in Jackpot, Nevada, Cactus Petes and The Horseshu. |

| (6) | We financed the purchase of these properties by their respective owner-operators through mortgage loans to the owner-operators. Square footage, acreage and rooms associated with these properties that we do not own are included in this table for informational purposes only. |

| (7) | This includes our corporate headquarters building and undeveloped land that we own at locations other than our tenant occupied properties. |

Master lease summaries

Penn Tenant; Penn Master Lease; Amended Pinnacle Master Lease; Penn Meadows Lease

Penn Tenant

Penn is a leading, diversified, multi-jurisdictional owner and manager of gaming and pari-mutuel properties, and an established gaming provider with strong financial performance. Penn is a publicly traded company that is subject to the informational filing requirements of the Exchange Act, and is required to file periodic reports on Form10-K and Form10-Q with the SEC. These reports are not incorporated by reference into, and do not constitute a part of, this prospectus supplement or the accompanying prospectus.

Penn Master Lease

The Penn Master Lease provides for the lease of land, buildings, structures and other improvements on the land, easements and similar appurtenances to the land and improvements relating to the operation of the leased properties. The obligations under the Penn Master Lease are guaranteed by Penn and by all Penn subsidiaries that occupy and operate the facilities leased under the Penn Master Lease, or that own a gaming license, other license or other material asset necessary to operate any portion of the facilities. A default by Penn or its subsidiaries with regard to any facility will cause a default with regard to the entire Penn portfolio.

The Penn Master Lease provides for an initial term of 15 years with no purchase option. There are approximately 9 years left under the initial term of the Penn Master Lease. At Penn’s option, the Penn Master Lease may be extended for up to four5-year renewal terms beyond the initial term, on the same terms and conditions. If Penn

S-9

Table of Contents

elects to renew the term of the Penn Master Lease, the renewal will be effective as to all, but not less than all, of the leased property then subject to the Penn Master Lease, provided that each renewal option shall only be exercisable with respect to any of the barge-based facilities following an independent third party expert’s review of the total useful life of the applicable barged-based facility measured from the beginning of the initial term. If the exercise of any renewal term would cause the aggregate term to exceed 80% of the estimated useful life of any facility, such facility shall be included in such5-year renewal only for the period of time that is within 80% of the estimated useful life of such facility. In the event that a barge-based facility is not included in all or any portion of the final5-year renewal term, such property shall cease to be subject to the Penn Master Lease at the end of such partial period and will no longer be occupied by Penn absent the entry by GLPI and Penn into a new lease.

Penn does not have the ability to terminate its obligations under the Penn Master Lease prior to its expiration without the lessor’s consent. If the Penn Master Lease is terminated prior to its expiration other than with lessor’s consent, Penn may be liable for damages and incur charges such as continued payment of rent through the end of the lease term and maintenance costs for the property.

The Penn Master Lease is commonly known as atriple-net lease. Accordingly, in addition to rent, Penn is required to pay the following: (1) all facility maintenance, (2) all insurance required in connection with the leased properties, and the business conducted on the leased properties, including coverage of the landlord’s interests, (3) taxes levied on or with respect to the leased properties (other than taxes on the income of the lessor) and (4) all utilities and other services necessary or appropriate for the leased properties and the business conducted on the leased properties. Penn makes the rent payment in monthly installments.

Amended Pinnacle Master Lease

A subsidiary of Penn (“Pinnacle Tenant”), leases certain real property assets from the Company under the Amended Pinnacle Master Lease. The obligations of Pinnacle Tenant under the Amended Pinnacle Master Lease are guaranteed by Pinnacle and all subsidiaries of Pinnacle Tenant that operate the facilities leased under the Amended Pinnacle Master Lease, or that own a gaming license, other license or other material asset or permit necessary to operate any portion of the facilities. A default by Pinnacle Tenant with regard to any facility will cause a default with regard to the entire portfolio.

The Amended Pinnacle Master Lease provides for an initial term of 10 years with no purchase option. There are approximately 6.5 years left under the initial term of the Amended Pinnacle Master Lease. At Pinnacle Tenant’s option, the Amended Pinnacle Master Lease may be extended for up to five5-year renewal terms beyond the initial10-year term, on the same terms and conditions. If Pinnacle Tenant elects to renew the term of the Amended Pinnacle Master Lease, the renewal will be effective as to all, but not less than all, of the leased property then subject to the Amended Pinnacle Master Lease.

The Amended Pinnacle Master Lease is commonly known as atriple-net lease. Accordingly, in addition to rent, Pinnacle Tenant is required to pay the following: (1) all facility maintenance, (2) all insurance required in connection with the leased properties, and the business conducted on the leased properties, including coverage of the landlord’s interests, (3) taxes levied on or with respect to the leased properties (other than taxes on the income of the landlord) and (4) all utilities and other services necessary or appropriate for the leased properties and the business conducted on the leased properties.

Penn Meadows Lease

A subsidiary of Penn (“Penn Meadows Tenant”), leases certain real property assets from the Company under the Penn Meadows Lease. The Penn Meadows Lease provides for an initial term of 10 years with no purchase

S-10

Table of Contents

option. There are approximately 7 years left under the initial term of the Penn Meadows Lease. At Penn Meadows Tenant’s option, the Penn Meadows Lease may be extended for up to three5-year renewal terms and one4- year renewal term beyond the initial10-year term, on the same terms and conditions.

The Penn Meadows Lease is commonly known as atriple-net lease. Accordingly, in addition to rent, Penn Meadows Tenant is required to pay the following: (1) all facility maintenance, (2) all insurance required in connection with the leased properties, and the business conducted on the leased properties, including coverage of the landlord’s interests, (3) taxes levied on or with respect to the leased properties (other than taxes on the income of the landlord) and (4) all utilities and other services necessary or appropriate for the leased properties and the business conducted on the leased properties.

Boyd Tenant; Boyd Master Lease

Boyd

Boyd is a leading geographically diversified operator of gaming entertainment properties and an established gaming provider with strong financial performance. Boyd is a publicly traded company that is subject to the informational filing requirements of the Exchange Act, and is required to file periodic reports on Form10-K and Form10-Q with the SEC. These reports are not incorporated by reference into, and do not constitute a part of, this prospectus supplement or the accompanying prospectus.

Boyd Tenant; Boyd Master Lease

BOYD TCIV, LLC, one of Boyd’s wholly owned subsidiaries (“Boyd Tenant”), leases the real property assets from us. The obligations of Boyd Tenant under the Boyd Master Lease are guaranteed by the subsidiaries of Boyd Tenant that operate the facilities leased under the Boyd Master Lease, or that own a gaming license, other license or other material asset or permit necessary to operate any portion of the facilities. A default by Boyd Tenant with regard to any facility will cause a default with regard to the entire portfolio.

The Boyd Master Lease provides for an initial term of approximately 10 years. There are approximately 6.5 years left under the initial term of the Boyd Master Lease. Boyd Tenant does not have a purchase option under the Boyd Master Lease. However, Boyd Tenant has the right to purchase the fee interest in any portion of the leased premises that is subject to a ground lease in the event the Company does not exercise its option to purchase the fee that may be granted to us under such ground lease. At Boyd Tenant’s option, the Boyd Master Lease may be extended for up to five5-year renewal terms beyond the initial term, on the same terms and conditions. If Boyd Tenant elects to renew the term of the Boyd Master Lease, the renewal will be effective as to all, but not less than all, of the leased property then subject to the Boyd Master Lease.

The Boyd Master Lease is commonly known as atriple-net lease. Accordingly, in addition to rent, Boyd Tenant is required to pay the following: (1) all facility maintenance, (2) all insurance required in connection with the leased properties, and the business conducted on the leased properties, including coverage of the landlord’s interests, (3) taxes levied on or with respect to the leased properties (other than taxes on the income of the Landlord) and (4) all utilities and other services necessary or appropriate for the leased properties and the business conducted on the leased properties.

Eldorado Tenant; Eldorado Master Lease

Eldorado

Eldorado is a leading casino entertainment company that owns and operates properties across several states. Eldorado is a publicly traded company that is subject to the informational filing requirements of the Exchange

S-11

Table of Contents

Act, and is required to file periodic reports on Form10-K and Form10-Q with the SEC. These reports are not incorporated by reference into, and do not constitute a part of, this prospectus supplement or the accompanying prospectus.

Eldorado Tenant; Eldorado Master Lease

Tropicana Entertainment Inc. (the “Eldorado Tenant”), a wholly owned subsidiary of Eldorado, leases the real property assets from us. The obligations of Eldorado Tenant under the Eldorado Master Lease are guaranteed by Eldorado and the subsidiaries of the Eldorado Tenant that operate the facilities leased under the Eldorado Master Lease, or that own a gaming license, other license or other material asset or permit necessary to operate any portion of the facilities. A default by Eldorado Tenant with regard to any facility will cause a default with regard to the entire portfolio.

The Eldorado Master Lease provides for an initial term of 15 years and there is no purchase option except following a final unstayed decision of the New Jersey Casino Control Commission or the New Jersey Division of Gaming Enforcement requiring us to divest our interest in any portion of the leased premises located in New Jersey. There are approximately 14 years left under the initial term of the Eldorado Master Lease. Eldorado Tenant’s option, the Eldorado Master Lease may be extended for up to four5-year renewal terms beyond the initial term, on the same terms and conditions. If Eldorado Tenant elects to renew the term of the Eldorado Master Lease, the renewal will be effective as to all, but not less than all, of the leased property then subject to the Eldorado Master Lease.

The Eldorado Master Lease is commonly known as atriple-net lease. Accordingly, in addition to rent, Eldorado Tenant is required to pay the following: (1) all facility maintenance, (2) all insurance required in connection with the leased properties, and the business conducted on the leased properties, including coverage of the landlord’s interests, (3) taxes levied on or with respect to the leased properties (other than taxes on the income of the Landlord) and (4) all utilities and other services necessary or appropriate for the leased properties and the business conducted on the leased properties.

Tax Status

We elected on our 2014 U.S. federal income tax return to be treated as a REIT and intend to continue to be organized and to operate in a manner that will permit us to qualify as a REIT. To qualify as a REIT, we must meet certain organizational and operational requirements, including a requirement to distribute at least 90% of our annual REIT taxable income to shareholders. As a REIT, we generally will not be subject to federal income tax on income that we distribute as dividends to our shareholders. If we fail or have failed to qualify as a REIT in any taxable year, we will be subject to U.S. federal income tax on our taxable income at regular corporate income tax rates, and dividends paid to our shareholders would not be deductible by us in computing taxable income. Any resulting corporate liability could be substantial and could materially and adversely affect our net income and net cash available for distribution to shareholders and holders of notes. Unless we were entitled to relief under certain Code provisions, we also would be disqualified fromre-electing to be taxed as a REIT for the four taxable years following the year in which we failed to qualify to be taxed as a REIT.

Our TRS Properties are able to engage in activities resulting in income that is not qualifying income for a REIT. As a result, certain activities of the Company which occur within our TRS Properties are subject to federal and state income taxes.

S-12

Table of Contents

Recent Developments

Tender Offer for Outstanding 2020 Notes

On August 15, 2019, we commenced the Tender Offer to purchase up to $500.0 million of the outstanding 2020 Notes for approximately $512.0 million in cash, subject to the relevant terms and conditions set forth in the Offer to Purchase related to the Tender Offer. The Tender Offer will expire at 11:59 p.m., New York City time, on September 12, 2019, unless the Tender Offer is extended or earlier terminated. As of August 14, 2019, there was $1.0 billion aggregate principal amount of 2020 Notes outstanding. If we complete the Tender Offer, a portion of the net proceeds of this offering will be used to fund the purchase of the 2020 Notes pursuant to the Tender Offer. See “Use of Proceeds.”

Our obligation to accept for payment, and to pay for, any 2020 Notes validly tendered pursuant to the Tender Offer is subject to, among other things, the satisfaction of the customary general conditions described in the Offer to Purchase related to the Tender Offer, including the consummation of this offering. The consummation of this offering is not conditioned on the completion of the Tender Offer. Neither this prospectus supplement nor the accompanying prospectus constitute an offer to purchase any of our outstanding 2020 Notes and any such offer will be effected solely through the Offer to Purchase.

Corporate Information

Our principal executive offices are located at 845 Berkshire Blvd., Suite 200, Wyomissing, Pennsylvania 19610, and our telephone number is (610)401-2900. Our website address is www.glpropinc.com. Information found on, or accessible through, our website is not a part of, and is not incorporated into, this prospectus supplement or the accompanying prospectus, and you should not consider it part of this prospectus supplement or the accompanying prospectus. For additional information, see “Where You Can Find More Information” in this prospectus supplement and the accompanying prospectus and “Information Incorporated by Reference” in this prospectus supplement and in the accompanying prospectus.

S-13

Table of Contents

The Offering

The following is a brief summary of some of the terms of this offering. For a more complete description of the terms of the notes, see the sections entitled “Description of the Notes” in this prospectus supplement and “Description of Debt Securities” in the accompanying prospectus. In this section, “we”, “our”, and “us” refer only to the Issuers and none of their subsidiaries.

Issuers | GLP Capital, L.P. and GLP Financing II, Inc. |

Securities | $400.0 million aggregate principal amount of 3.350% Senior Notes due 2024 and $700.0 million aggregate principal amount of 4.000% Senior Notes due 2030. |

Maturity | The 2024 notes will mature on September 1, 2024. The 2030 notes will mature on January 15, 2030. |

Interest Rate | Interest on the 2024 notes will be payable in cash and will accrue at a rate of 3.350% per annum. Interest on the 2030 notes will be payable in cash and will accrue at a rate of 4.000% per annum. |

Interest Payment Dates | We will pay interest on the 2024 notes on March 1 and September 1 of each year, commencing on March 1, 2020. We will pay interest on the 2030 notes on January 15 and July 15 of each year, commencing on January 15, 2020. Interest on the notes will accrue from August 29, 2019. |

Guarantees | The notes will be guaranteed on a senior unsecured basis by GLPI. The notes will not be guaranteed by any of our subsidiaries; provided that, in the event that $100.0 million principal amount or more of certain of our existing or future debt securities are guaranteed orco-issued by any of the Operating Partnership’s subsidiaries (other than Capital Corp.), such subsidiaries will be required to guarantee the notes. |

Ranking | The notes and GLPI’s guarantee of the notes will be our and GLPI’s general senior unsecured obligations and will: |

| • | rank equally in right of payment with all of our and GLPI’s existing and future senior unsecured indebtedness, including our existing senior unsecured notes and Credit Facility and GLPI’s guarantees thereof; |

| • | rank senior in right of payment to all of our and GLPI’s future subordinated indebtedness; |

| • | be effectively subordinated to all of our and GLPI’s future secured indebtedness to the extent of the value of the collateral securing such indebtedness; and |

| • | be structurally subordinated to all indebtedness and other liabilities of any of GLPI’s subsidiaries that is not an Issuer. |

S-14

Table of Contents

| Unless and until our subsidiaries become guarantors of the notes, creditors of our subsidiaries (including potentially lenders under the Credit Facility, as our subsidiaries may in the future elect to guarantee the Credit Facility without triggering a guarantee obligation with respect to the notes) and holders of any of our debt that is guaranteed by any of our subsidiaries will have a prior claim, ahead of the notes, on all of such subsidiaries’ assets. As of June 30, 2019, our subsidiaries had approximately $145.0 million of liabilities (excluding intercompany liabilities). |

| As of June 30, 2019, as adjusted to give effect to the Transactions, on a consolidated basis, we would have had approximately $5.8 billion of long-term indebtedness, net of unamortized issuance costs, bond premiums and original issuance discounts, including $1.1 billion representing the notes offered hereby, $4.475 billion of existing senior unsecured notes and approximately $289.0 million of indebtedness outstanding under the Credit Facility, and would have had approximately $1,174.6 million of availability under the Revolver (including $0.4 million of contingent obligations under letters of credit). To the extent less than $500.0 million of the 2020 Notes are tendered in the Tender Offer, there will be more existing senior unsecured notes outstanding than described above. |

Optional Redemption | The Issuers may redeem all or part of either series of notes at any time at their option at a redemption price equal to 100% of the principal amount thereof, plus accrued and unpaid interest, if any, to, but not including, the redemption date, plus a “make-whole” premium, as described under the section entitled “Description of the Notes—Redemption—Optional Redemption.” |

Redemption Based upon Gaming Laws | The notes will be subject to redemption requirements imposed by gaming laws and regulations of gaming authorities in jurisdictions in which we conduct gaming operations. See “Description of the Notes—Redemption—Gaming Redemption.” |

Change of Control Offer | If we experience a change of control accompanied by a decline in the rating of a series of notes, we must give holders of such series of notes the opportunity to sell us their notes at 101% of their principal amount, plus accrued and unpaid interest, if any, to, but not including, the repurchase date. See “Description of the Notes—Repurchase at the Option of Holders—Change of Control and Rating Decline.” |

Certain Indenture Provisions | The indenture governing the notes will contain covenants limiting, among other things: |

| • | the ability of the Issuers and their subsidiaries to incur additional indebtedness and use their assets to secure indebtedness; |

| • | the ability of the Issuers to amend or terminate the Penn Master Lease; and |

S-15

Table of Contents

| • | the ability of the Issuers to merge, consolidate or transfer all or substantially all of our and our subsidiaries’ assets, taken as a whole. |

| These covenants are subject to a number of important and significant limitations, qualifications and exceptions. See “Description of the Notes—Certain Covenants.” |

No Prior Market | The notes will be new securities for which there is currently no market. Although certain of the underwriters have informed us that they intend to make a market in the notes, they are not obligated to do so, and they may discontinue market making activities at any time without notice. Accordingly, we cannot assure you that a liquid market for the notes will develop or be maintained. |

Use of Proceeds | We estimate that the net proceeds from this offering, after the deduction of the underwriting discounts and commissions and our estimated expenses, will be approximately $1,087.9 million. |