Exhibit 99.2

|

2015 Third Quarter | Earnings Presentation

November 11, 2015

|

Disclaimer

Concerning Forward-Looking Statements and Non-GAAP Information

This document includes forward-looking statements, beliefs or opinions, including statements with respect to Avolon’s business, financial condition, results of operations and plans. These forward-looking statements involve known and unknown risks and uncertainties, many of which are beyond our control and all of which are based on our management’s current beliefs and expectations about future events. Forward-looking statements are sometimes identified by the use of forward-looking terminology such as “believe,” “expects,” “may,” “will,” “could,” “should,” “shall,” “risk,” “intends,” “estimates,” “aims,” “plans,” “predicts,” “continues,” “assumes,” “positioned” or “anticipates” or the negative thereof, other variations thereon or comparable terminology or by discussions of strategy, plans, objectives, goals, future events or intentions. These forward-looking statements include all matters that are not historical facts. Forward-looking statements may and often do differ materially from actual results. No assurance can be given that such future results will be achieved.

These risks, uncertainties and assumptions include, but are not limited to, the following: risks and uncertainties relating to the closing of the merger transaction with Bohai; general economic and financial conditions; the financial condition of our lessees; our ability to obtain additional capital to finance our growth and operations on attractive terms; decline in the value of our aircraft and market rates for leases; the loss of key personnel; lessee defaults and attempts to repossess aircraft; our ability to regularly sell aircraft; our ability to successfully re-lease our existing aircraft and lease new aircraft; our ability to negotiate and enter into profitable leases; periods of aircraft oversupply during which lease rates and aircraft values decline; changes in the appraised value of our aircraft; changes in interest rates; competition from other aircraft lessors; and the limited number of aircraft and engine manufacturers. These and other important factors, including those discussed under “Item 3. Key Information—Risk Factors” included in our Annual Report on Form 20-F filed with the U.S. Securities and Exchange Commission on March 3, 2015, may cause our actual events or results to differ materially from any future results, performances or achievements expressed or implied by the forward-looking statements contained in this document. Such forward-looking statements contained in this document speak only as of the date of this document. We expressly disclaim any obligation or undertaking to update these forward-looking statements contained in this document to reflect any change in our expectations or any change in events, conditions, or circumstances on which such statements are based unless required to do so by applicable law.

The financial information included herein includes financial information that is not presented in accordance with generally accepted accounting principles in the United States (“GAAP”), including adjusted net income, adjusted return on equity (“adjusted ROE”) and adjusted earnings per share. The Appendix to this presentation includes a reconciliation of adjusted net income, adjusted ROE and adjusted earnings per share with the most directly comparable financial measures calculated in accordance with GAAP. See slides 14 to 16.

Avolon | Slide 2

|

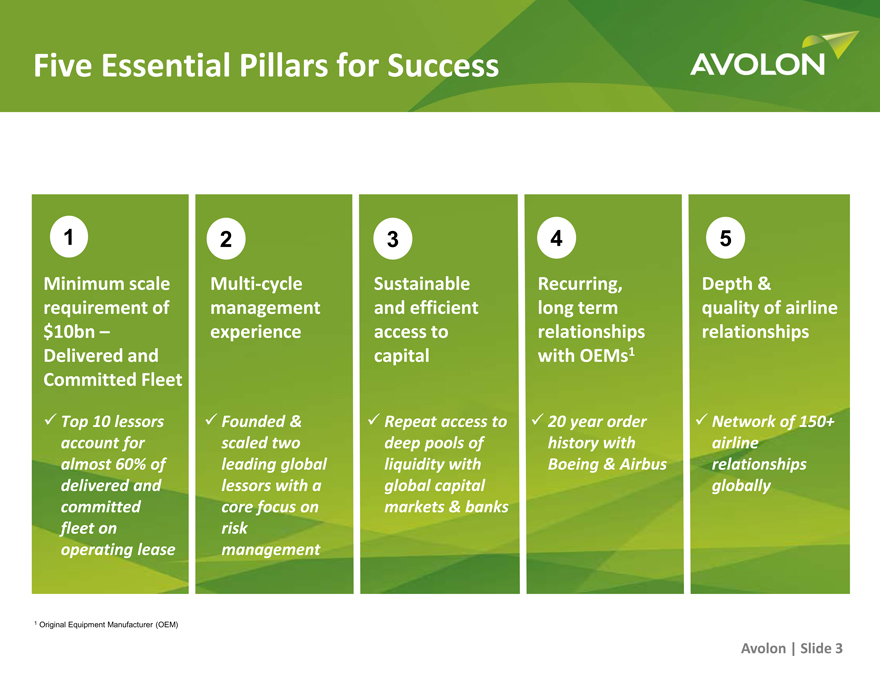

Five Essential Pillars for Success

1 |

| 2 3 4 5 |

Minimum scale Multi-cycle Sustainable Recurring, Depth & requirement of management and efficient long term quality of airline $10bn – experience access to relationships relationships Delivered and capital with OEMs1 Committed Fleet

?Top 10 lessors ?Founded & ?Repeat access to ?20 year order ?Network of 150+ account for scaled two deep pools of history with airline almost 60% of leading global liquidity with Boeing & Airbus relationships delivered and lessors with a global capital globally committed core focus on markets & banks fleet on risk operating lease management

1 |

| Original Equipment Manufacturer (OEM) |

Avolon | Slide 3

|

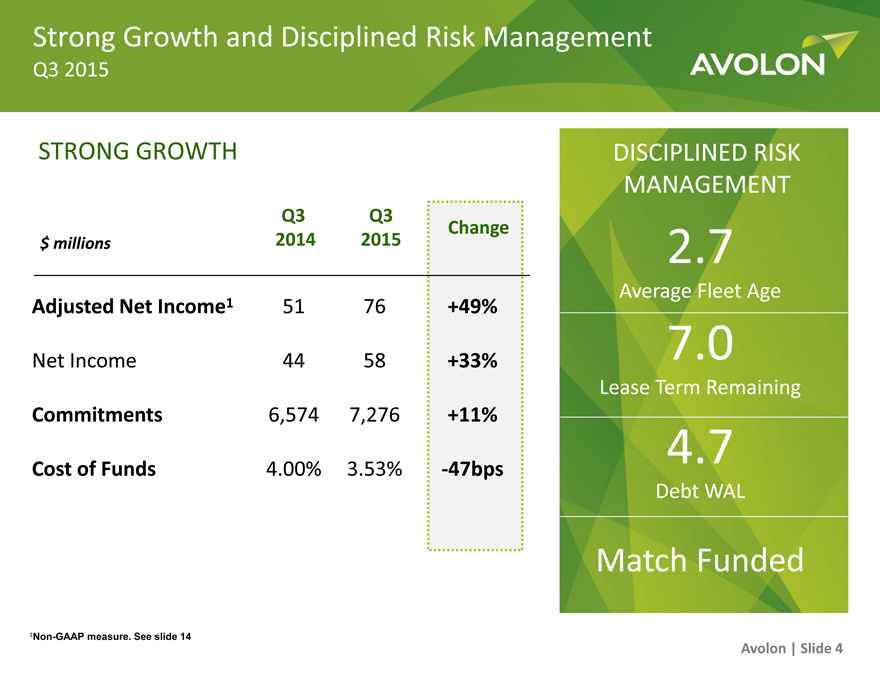

Strong Growth and Disciplined Risk Management

Q3 2015

STRONG GROWTH

Q3 Q3

Change

$ millions 2014 2015

Adjusted Net Income1 51 76 +49%

Net Income 44 58 +33%

Commitments 6,574 7,276 +11%

Cost of Funds 4.00% 3.53% -47bps

DISCIPLINED RISK MANAGEMENT

2.7

Average Fleet Age

7.0

Lease Term Remaining

4.7

Debt WAL

Match Funded

1Non-GAAP measure. See slide 14

Avolon | Slide 4

|

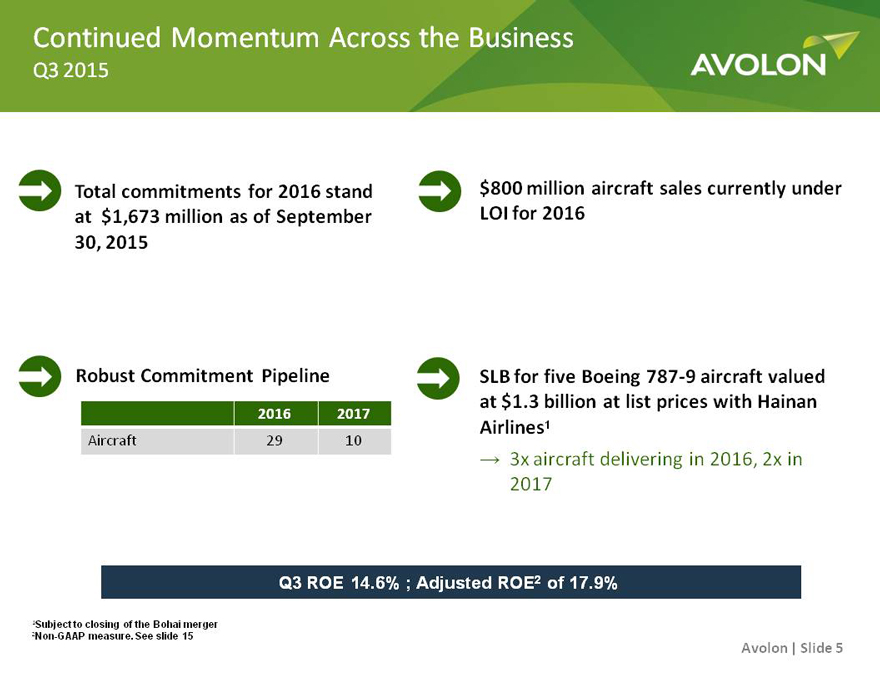

Continued Momentum Across the Business

Q3 2015

Total commitments for 2016 stand $800 million aircraft sales currently under at $1,673 million as of September LOI for 2016 30, 2015

Robust Commitment Pipeline SLB for five Boeing 787-9 aircraft valued at $1.3 billion at list prices with Hainan

2016 2017

Airlines1

Aircraft 29 10 ’

3x aircraft delivering in 2016, 2x in 2017

Q3 ROE 14.6% ; Adjusted ROE2 of 17.9%

1Subject to closing of the Bohai merger

2Non-GAAP measure. See slide 15

Avolon | Slide 5

|

FINANCIAL HIGHLIGHTS

|

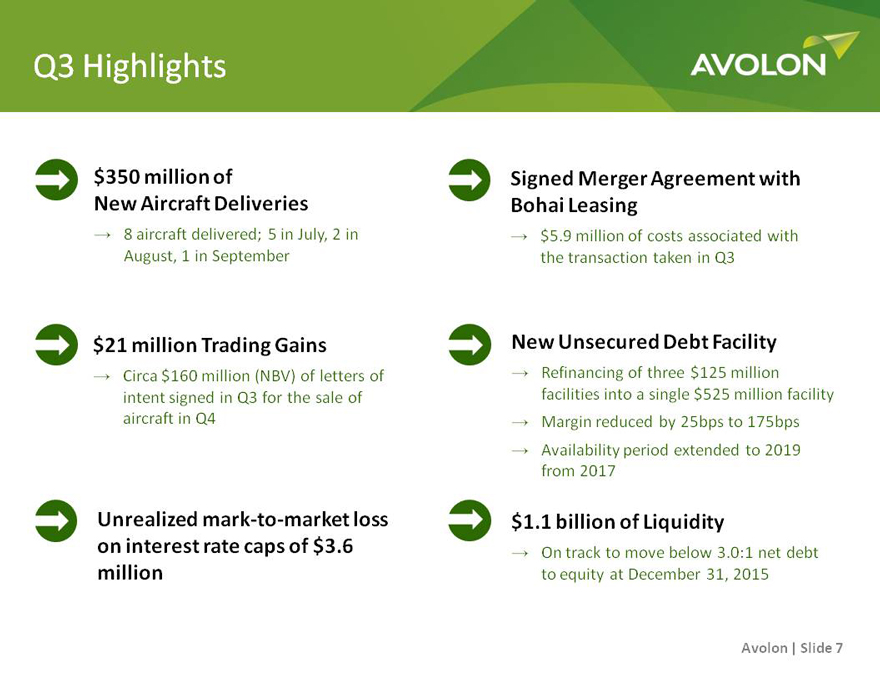

Q3 Highlights

$350 million of New Aircraft Deliveries

’ 8 aircraft delivered; 5 in July, 2 in August, 1 in September

$21 million Trading Gains

’ Circa $160 million (NBV) of letters of intent signed in Q3 for the sale of aircraft in Q4

Unrealized mark-to-market loss on interest rate caps of $3.6 million

Signed Merger Agreement with Bohai Leasing

’ $5.9 million of costs associated with the transaction taken in Q3

New Unsecured Debt Facility

’ Refinancing of three $125 million facilities into a single $525 million facility

’ Margin reduced by 25bps to 175bps

’ Availability period extended to 2019 from 2017

$1.1 billion of Liquidity

’ On track to move below 3.0:1 net debt to equity at December 31, 2015

Avolon | Slide 7

|

Q3 2015

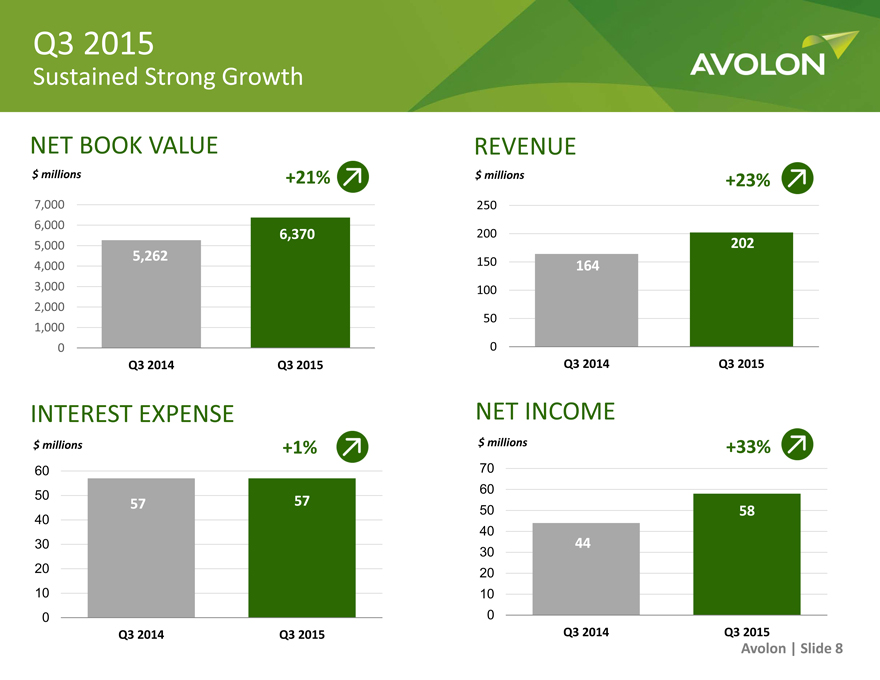

Sustained Strong Growth

NET BOOK VALUE

$ millions +21%

7,000 6,000

6,370

5,000

5,262

4,000 3,000 2,000 1,000 0

Q3 2014 Q3 2015

INTEREST EXPENSE

$ millions +1%

60

50 57 57

40 30 20 10 0

Q3 2014 Q3 2015

REVENUE

$ millions +23%

250 200

202

150 164 100 50 0

Q3 2014 Q3 2015

NET INCOME

$ millions +33%

70 60

50 58 40

44

30 20 10 0

Q3 2014 Q3 2015

Avolon | Slide 8

|

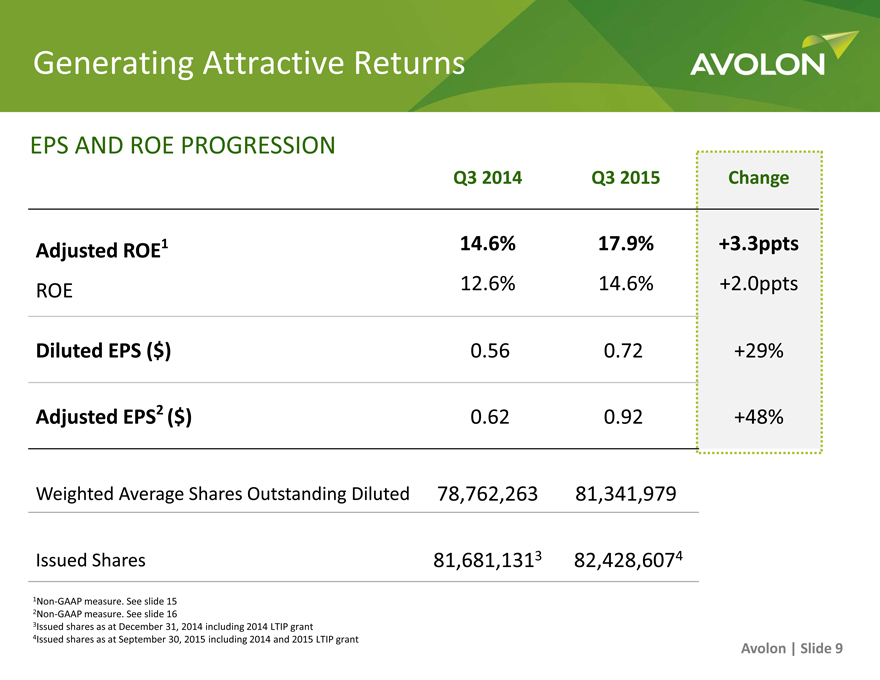

Generating Attractive Returns

EPS AND ROE PROGRESSION

Q3 2014 Q3 2015 Change

Adjusted ROE1 14.6% 17.9% +3.3ppts

ROE 12.6% 14.6% +2.0ppts

Diluted EPS ($) 0.56 0.72 +29%

Adjusted EPS2 ($) 0.62 0.92 +48%

Weighted Average Shares Outstanding Diluted 78,762,263 81,341,979

Issued Shares 81,681,1313 82,428,6074

1Non-GAAP measure. See slide 15 2Non-GAAP measure. See slide 16

3Issued shares as at December 31, 2014 including 2014 LTIP grant

4 |

|

Issued shares as at September 30, 2015 including 2014 and 2015 LTIP grant

Avolon | Slide 9

|

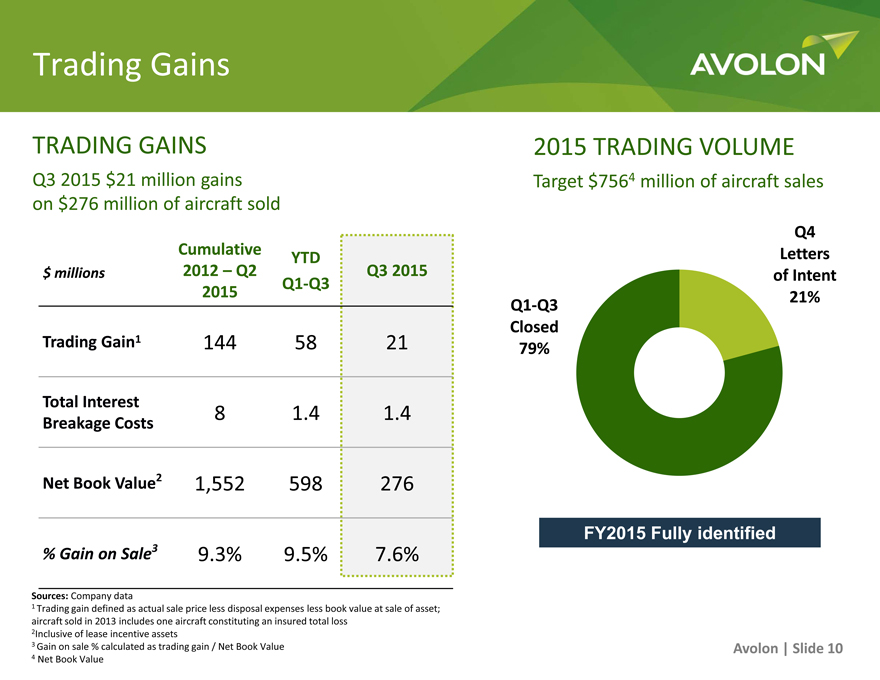

Trading Gains

TRADING GAINS 2015 TRADING VOLUME

Q3 2015 $21 million gains Target $7564 million of aircraft sales on $276 million of aircraft sold

Cumulative YTD

$ millions 2012 – Q2 Q3 2015

2015 Q1-Q3

Trading Gain1 144 58 21

Total Interest 8 1.4 1.4

Breakage Costs

Net Book Value2 1,552 598 276

% Gain on Sale3 9.3% 9.5% 7.6%

Q4 Letters of Intent Q1-Q3 21% Closed 79%

FY2015 Fully identified

Sources: Company data

1 Trading gain defined as actual sale price less disposal expenses less book value at sale of asset; aircraft sold in 2013 includes one aircraft constituting an insured total loss

2Inclusive of lease incentive assets

3 |

| Gain on sale % calculated as trading gain / Net Book Value Avolon | Slide 10 |

4 |

| Net Book Value |

Avolon | Slide 10

|

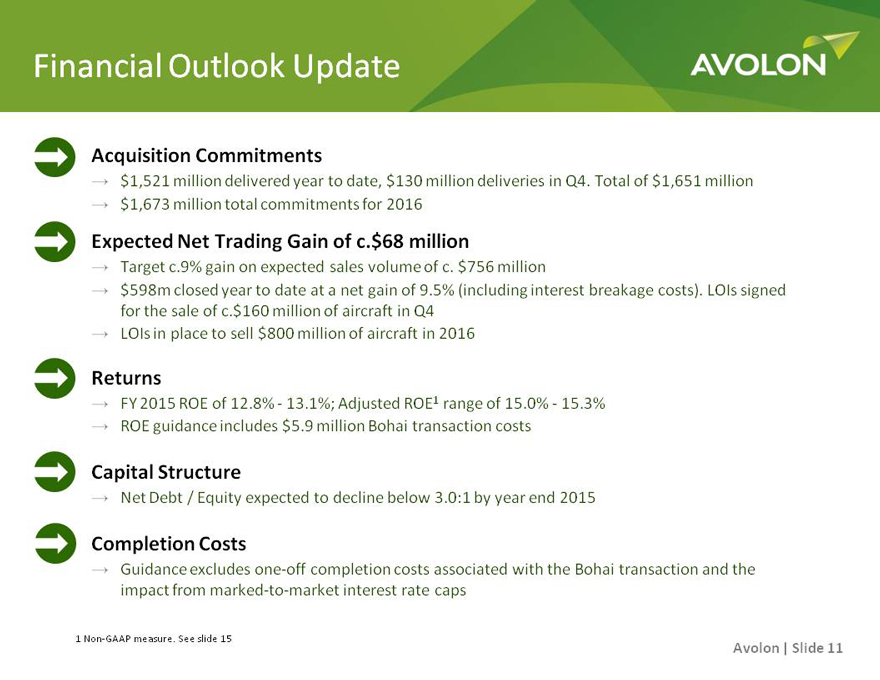

Financial Outlook Update

Acquisition Commitments

’ $1,521 million delivered year to date, $130 million deliveries in Q4. Total of $1,651 million

’ $1,673 million total commitments for 2016

Expected Net Trading Gain of c.$68 million

’ Target c.9% gain on expected sales volume of c. $756 million

’ $598m closed year to date at a net gain of 9.5% (including interest breakage costs). LOIs signed for the sale of c.$160 million of aircraft in Q4

’ LOIs in place to sell $800 million of aircraft in 2016

Returns

’ FY 2015 ROE of 12.8%—13.1%; Adjusted ROE1 range of 15.0%—15.3%

’ ROE guidance includes $5.9 million Bohai transaction costs

Capital Structure

’ Net Debt / Equity expected to decline below 3.0:1 by year end 2015

Completion Costs

’ Guidance excludes one-off completion costs associated with the Bohai transaction and the impact from marked-to-market interest rate caps

1 |

| Non-GAAP measure. See slide 15 |

Avolon | Slide 11

|

APPENDIX

|

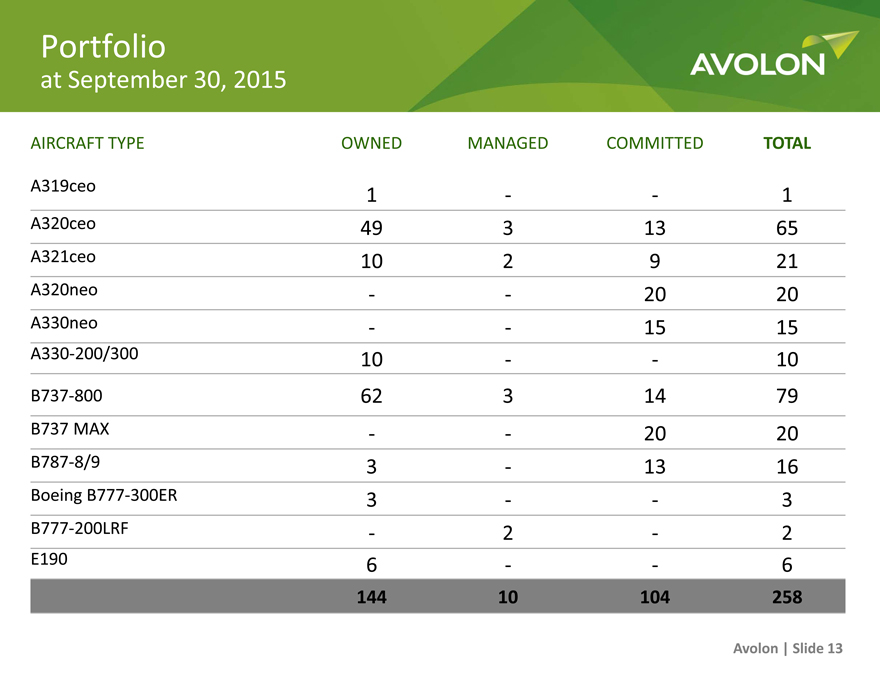

Portfolio

at September 30, 2015

AIRCRAFT TYPE OWNED MANAGED COMMITTED TOTAL

A319ceo 1 — 1

A320ceo 49 3 13 65

A321ceo 10 2 9 21

A320neo — 20 20

A330neo — 15 15

A330-200/300 10 — 10

B737-800 62 3 14 79

B737 MAX — 20 20

B787-8/9 3—13 16

Boeing B777-300ER 3 — 3

B777-200LRF—2—2

E190 6 — 6

144 10 104 258

Avolon | Slide 13

|

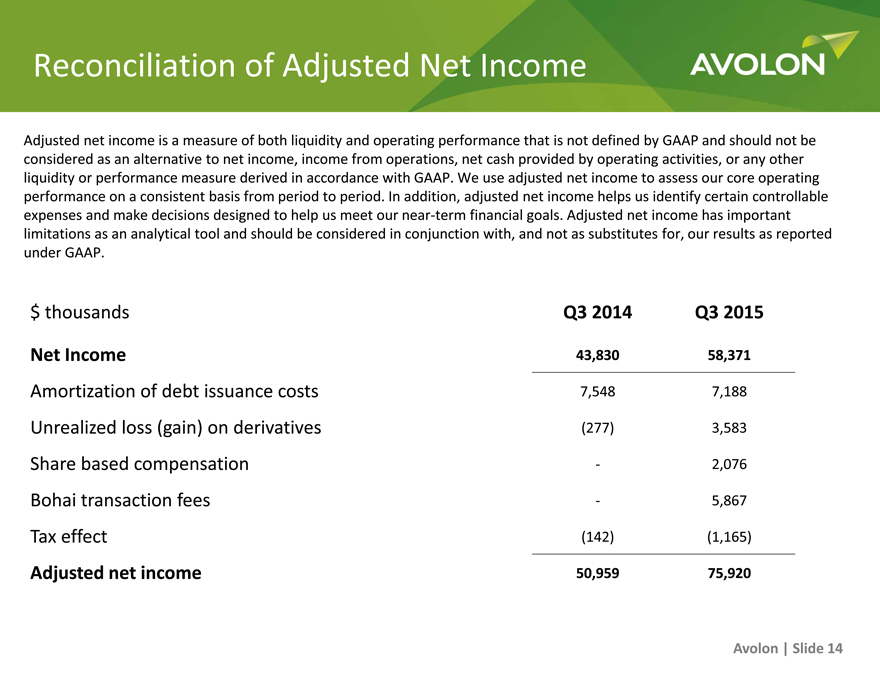

Reconciliation of Adjusted Net Income

Adjusted net income is a measure of both liquidity and operating performance that is not defined by GAAP and should not be considered as an alternative to net income, income from operations, net cash provided by operating activities, or any other liquidity or performance measure derived in accordance with GAAP. We use adjusted net income to assess our core operating performance on a consistent basis from period to period. In addition, adjusted net income helps us identify certain controllable expenses and make decisions designed to help us meet our near-term financial goals. Adjusted net income has important limitations as an analytical tool and should be considered in conjunction with, and not as substitutes for, our results as reported under GAAP.

$ thousands Q3 2014 Q3 2015

Net Income 43,830 58,371

Amortization of debt issuance costs 7,548 7,188

Unrealized loss (gain) on derivatives (277) 3,583

Share based compensation—2,076

Bohai transaction fees—5,867

Tax effect (142) (1,165)

Adjusted net income 50,959 75,920

Avolon | Slide 14

|

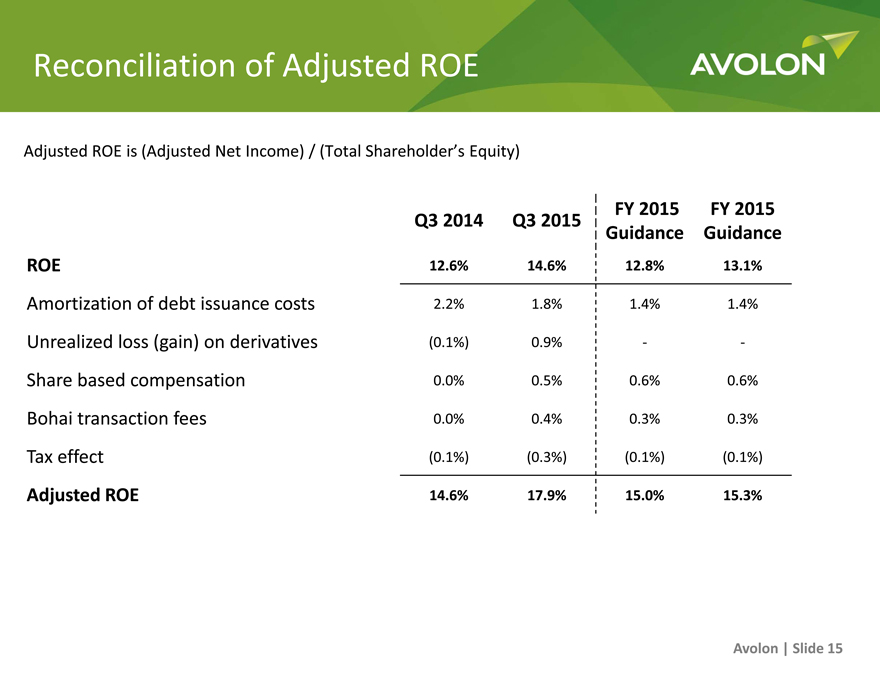

Reconciliation of Adjusted ROE

Adjusted ROE is (Adjusted Net Income) / (Total Shareholder’s Equity)

Q3 2014 Q3 2015 FY 2015 FY 2015

Guidance Guidance

ROE 12.6% 14.6% 12.8% 13.1%

Amortization of debt issuance costs 2.2% 1.8% 1.4% 1.4%

Unrealized loss (gain) on derivatives (0.1%) 0.9% —

Share based compensation 0.0% 0.5% 0.6% 0.6%

Bohai transaction fees 0.0% 0.4% 0.3% 0.3%

Tax effect (0.1%) (0.3%) (0.1%) (0.1%)

Adjusted ROE 14.6% 17.9% 15.0% 15.3%

Avolon | Slide 15

|

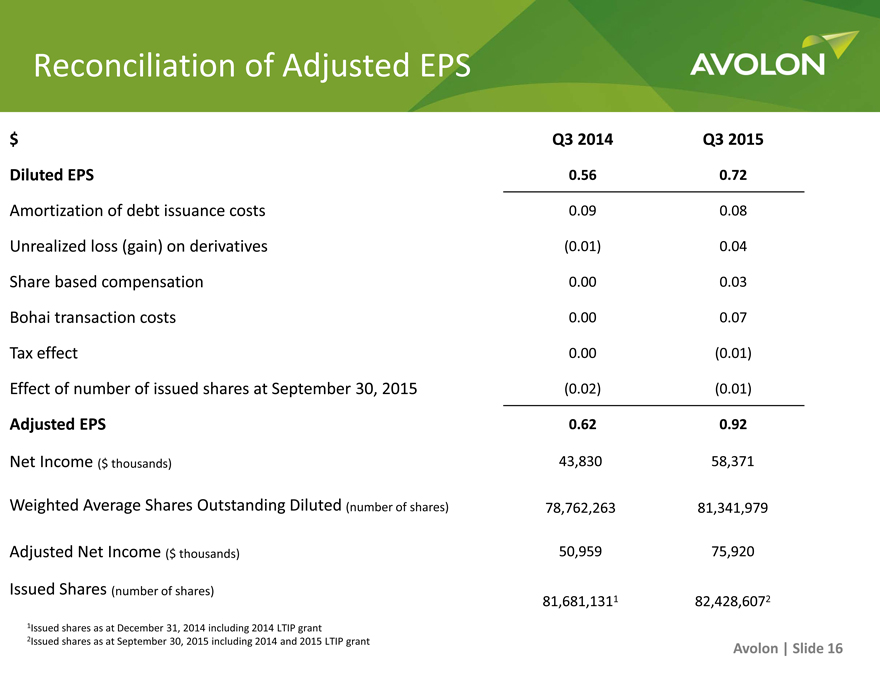

Reconciliation of Adjusted EPS

$ Q3 2014 Q3 2015

Diluted EPS 0.56 0.72

Amortization of debt issuance costs 0.09 0.08

Unrealized loss (gain) on derivatives (0.01) 0.04

Share based compensation 0.00 0.03

Bohai transaction costs 0.00 0.07

Tax effect 0.00 (0.01)

Effect of number of issued shares at September 30, 2015 (0.02) (0.01)

Adjusted EPS 0.62 0.92

Net Income ($ thousands) 43,830 58,371

Weighted Average Shares Outstanding Diluted (number of shares) 78,762,263 81,341,979

Adjusted Net Income ($ thousands) 50,959 75,920

Issued Shares (number of shares) 81,681,1311 82,428,6072

1Issued shares as at December 31, 2014 including 2014 LTIP grant

2Issued shares as at September 30, 2015 including 2014 and 2015 LTIP grant

Avolon | Slide 16

|

THANK YOU