UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

Date: March 5, 2021

UBS Group AG

Commission File Number: 1-36764

UBS AG

Commission File Number: 1-15060

(Registrants' Name)

Bahnhofstrasse 45, Zurich, Switzerland and

Aeschenvorstadt 1, Basel, Switzerland

(Address of principal executive offices)

Indicate by check mark whether the registrants file or will file annual reports under cover of Form 20‑F or Form 40-F.

Form 20-F x Form 40-F o

This Form 6-K consists of the 31 December 2020 Pillar 3 report of UBS Group and significant regulated subsidiaries and sub-groups, which appears immediately following this page.

31 December 2020 Pillar 3 report

UBS Group and significant regulated subsidiaries and sub-groups

Terms used in this report, unless the context requires otherwise

“UBS,” “UBS Group,” “UBS Group AG consolidated,” “Group,” “the Group,” “we,” “us” and “our” | UBS Group AG and its consolidated subsidiaries |

“UBS AG consolidated” | UBS AG and its consolidated subsidiaries |

“UBS Group AG” and “UBS Group AG standalone” | UBS Group AG on a standalone basis |

“UBS AG” and “UBS AG standalone” | UBS AG on a standalone basis |

“UBS Switzerland AG” and “UBS Switzerland AG standalone” | UBS Switzerland AG on a standalone basis |

“UBS Europe SE consolidated” | UBS Europe SE and its consolidated subsidiaries |

“UBS Americas Holding LLC” and “UBS Americas Holding LLC consolidated” | UBS Americas Holding LLC and its consolidated subsidiaries |

Table of contents | |||

| |||

UBS Group | |||

18 | Section 1 | ||

21 | Section 2 | ||

23 | Section 3 | Linkage between financial statements and regulatory exposures | |

26 | Section 4 | ||

58 | Section 5 | ||

69 | Section 6 | Comparison of A-IRB approach and standardized approach for credit risk | |

74 | Section 7 | ||

77 | Section 8 | ||

87 | Section 9 | ||

88 | Section 10 | ||

92 | Section 11 | ||

101 | Section 12 | ||

103 | Section 13 | ||

106 | Section 14 | ||

109 | Section 15 | ||

110 | Section 16 | Requirements for global systemically important banks and related indicators | |

|

|

| |

|

|

| |

Significant regulated subsidiaries and sub-groups | |||

112 | Section 1 | ||

112 | Section 2 | ||

117 | Section 3 | ||

124 | Section 4 | ||

125 | Section 5 | ||

|

|

| |

Switchboards

For all general inquiries.

ubs.com/contact

Zurich +41-44-234 1111

London +44-207-567 8000

New York +1-212-821 3000

Hong Kong +852-2971 8888

Singapore +65-6495 8000

Investor Relations

Institutional, professional and

retail investors are supported by UBS’s Investor Relations team.

UBS Group AG, Investor Relations

P.O. Box, CH-8098 Zurich, Switzerland

ubs.com/investors

Zurich +41-44-234 4100

New York +1-212-882 5734

Media Relations

Global media and journalists

are supported by UBS’s Media Relations team.

ubs.com/media

Zurich +41-44-234 8500

mediarelations@ubs.com

London +44-20-7567 4714

ubs-media-relations@ubs.com

New York +1-212-882 5858

mediarelations-ny@ubs.com

Hong Kong +852-2971 8200

sh-mediarelations-ap@ubs.com

Office of the Group Company Secretary

The Group Company Secretary receives inquiries regarding compensation and related issues addressed to members of the Board of Directors.

UBS Group AG, Office of the

Group Company Secretary

P.O. Box, CH-8098 Zurich, Switzerland

sh-company-secretary@ubs.com

Zurich +41-44-235 6652

Shareholder Services

UBS’s Shareholder Services team,

a unit of the Group Company Secretary Office, is responsible

for the registration of UBS Group AG registered shares.

UBS Group AG, Shareholder Services

P.O. Box, CH-8098 Zurich, Switzerland

sh-shareholder-services@ubs.com

Zurich +41-44-235 6652

US Transfer Agent

For global registered share-related

inquiries in the US.

Computershare Trust Company NA

P.O. Box 505000

Louisville, KY 40233-5000, USA

Shareholder online inquiries:

www-us.computershare.com/

investor/Contact

Shareholder website:

computershare.com/investor

Calls from the US

+1-866-305-9566

Calls from outside the US

+1-781-575-2623

TDD for hearing impaired

+1-800-231-5469

TDD for foreign shareholders

+1-201-680-6610

Imprint

Publisher: UBS Group AG, Zurich, Switzerland | ubs.com

Language: English

© UBS 2021. The key symbol and UBS are among the registered and unregistered trademarks of UBS. All rights reserved.

Scope of Basel III Pillar 3 disclosures

The Basel Committee on Banking Supervision (the BCBS) Basel III capital adequacy framework consists of three complementary pillars. Pillar 1 provides a framework for measuring minimum capital requirements for the credit, market, operational and non-counterparty-related risks faced by banks. Pillar 2 addresses the principles of the supervisory review process, emphasizing the need for a qualitative approach to supervising banks. Pillar 3 requires banks to publish a range of disclosures, mainly covering risk, capital, leverage, liquidity and remuneration.

This report provides Pillar 3 disclosures for the UBS Group and prudential key figures and regulatory information for UBS AG standalone, UBS Switzerland AG standalone, UBS Europe SE consolidated and UBS Americas Holding LLC consolidated in the respective sections under “Significant regulated subsidiaries and sub-groups.”

As UBS is considered a systemically relevant bank (an SRB) under Swiss banking law, UBS Group AG and UBS AG are required to comply with regulations based on the Basel III framework as applicable to Swiss SRBs on a consolidated basis. Capital and other regulatory information as of 31 December 2020 for UBS Group AG consolidated is provided in the “Capital, liquidity and funding, and balance sheet” section of our Annual Report 2020 and for UBS AG consolidated in the “Capital, liquidity and funding, and balance sheet” section of the combined UBS Group AG and UBS AG Annual Report 2020, available under “Annual reporting” at ubs.com/investors.

Local regulators may also require the publication of Pillar 3 information at a subsidiary or sub-group level. Where applicable, these local disclosures are provided under “Holding company and significant regulated subsidiaries and sub-groups” at ubs.com/investors.

COVID-19 regulatory measures

COVID-19 temporary regulatory measures in Switzerland

In March 2020, the Swiss Federal Council adopted provisional emergency legislation to support small and medium-sized Swiss companies suffering from substantial reductions in revenue due to the COVID-19 pandemic.

In December 2020, the Swiss Parliament approved the COVID-19 Joint and Several Guarantee Act, which became effective on 19 December 2020. This Act codified the measures adopted under emergency legislation into ordinary law and provides for regulation of the loan programs and guarantees over their life cycle. The new Act extends the standard amortization period of loans from five to eight years.

Under the aforementioned legislation, and until 31 July 2020, affected companies were able to apply through their banks for emergency loans, amounting to a maximum of 10% of their annual turnover, with a ceiling of CHF 20 million. As of that date, we had committed CHF 2.7 billion of loans up to CHF 0.5 million, which are 100% guaranteed by the Swiss government, and CHF 0.6 billion of loans between CHF 0.5 million and CHF 20 million, which are 85% government-guaranteed. As of 31 December 2020, the total committed loans amounted to CHF 3.0 billion (31 July 2020: CHF 3.3 billion), of which CHF 1.8 billion was drawn. We intend to donate any economic profits from this program to COVID-19 relief efforts, although no such profits were made in 2020.

Furthermore, the Swiss Federal Council deactivated the countercyclical buffer on residential real estate loans in March 2020 until further notice, at the request of the Swiss National Bank (the SNB), to support the lending capacity of banks. This led to a reduction of 29 basis points of UBS’s common equity tier 1 (CET1) capital requirement as of 31 December 2020, with no impact on UBS’s capital ratios.

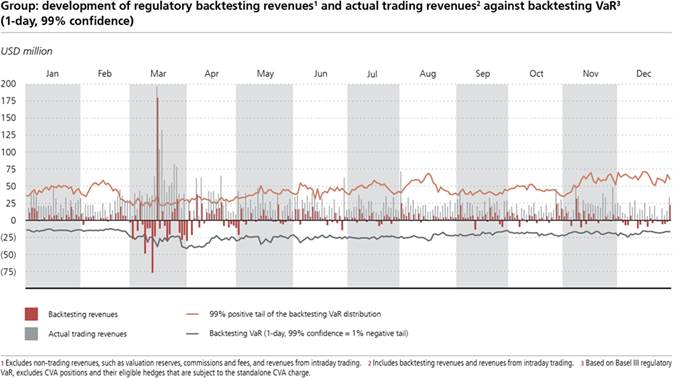

Banks that have model-based market risk RWA calculations, such as UBS, experienced an increased number of backtesting exceptions, driven by the higher volatility levels in the markets throughout 2020. These exceptions could ultimately result in higher bank-specific minimum capital requirements. To prevent procyclicality in capital requirements, the Swiss Financial Market Supervisory Authority (FINMA) introduced a temporary exemption, freezing the number of backtesting exceptions from 1 February 2020 until 1 July 2020, and subsequently introduced this exemption into supervisory practice: the exemption therefore continued to apply beyond 1 July 2020, subject to future withdrawal by the regulator. For UBS, the number of negative backtesting exceptions within a 250-business-day window increased from 0 to 3 by the end of 2020. The resulting FINMA VaR multiplier for market risk RWA remained unchanged at 3 as of 31 December 2020; UBS did not benefit from the exemption in 2020.

In addition, FINMA permitted banks to temporarily exclude central bank sight deposits from the leverage ratio denominator (the LRD) for the purpose of calculating going concern ratios. This exemption applied until 1 January 2021. Applicable dividends or similar distributions approved by shareholders after 25 March 2020 reduced the relief by the LRD equivalent of the capital distribution. As of 31 December 2020, these exclusions resulted in a temporary reduction of our LRD for going concern requirement purposes of USD 93 billion. Given our existing buffers to capital requirements and the temporary nature of this measure, this had no impact on our capacity to provide funding to our clients or the Swiss economy.

› Refer to the “Going and gone concern requirements and eligible capital” section of this report for more information about the effects of the temporary exemption granted by FINMA in connection with COVID-19

COVID-19 temporary regulatory measures outside Switzerland

Regulators in key jurisdictions outside of Switzerland have taken measures intended to encourage banks to take an accommodative stance when dealing with customers facing financial stress, and also to support liquidity in markets. These measures include temporary relaxation of capital buffer and Pillar 2 capital requirements, temporary modifications to the LRD and the establishment of special lending or financing facilities.

The BCBS has delayed the implementation deadline of Basel III rules by one year, to 1 January 2023. The accompanying transitional arrangement for the output floor has also been extended by one year, to 1 January 2028. Separately, the BCBS and the International Organization of Securities Commissions (IOSCO) have extended the final implementation phase of the framework for margin requirements for non-centrally cleared derivatives by one year, to 1 September 2022.

2

In May 2020, the Federal Reserve made a temporary change to permit the exclusion of US Treasury securities and deposits at Federal Reserve Banks from the calculation of the supplementary leverage ratio for bank holding companies (BHCs) and intermediate holding companies (IHCs), including UBS Americas Holding LLC. This temporary change will be in effect until 31 March 2021.

The EU and the European Central Bank (the ECB) have also communicated a series of regulatory measures to stabilize the economy in Europe. None of those measures had a significant impact on UBS Group during 2020.

Capital returns

The second tranche of the 2019 dividend (USD 0.365 per share) was paid on 27 November 2020 following shareholder approval at an extraordinary general meeting on 19 November 2020.

For 2020, the Board of Directors intends to propose an ordinary dividend per share of USD 0.37 for the 2020 financial year, to be approved at the general meeting of shareholders in April 2021.

In the first quarter of 2020, before the introduction of COVID-related share repurchase restrictions, we repurchased CHF 350 million (USD 364 million) of our shares. In the first quarter of 2021, we repurchased the remaining CHF 100 million of our 2018–2021 program, which is now complete and closed.

Furthermore, we have established a USD 2.0 billion capital reserve for potential share repurchases during the second half of 2020. On 11 February 2021, we launched a new three-year program of up to CHF 4 billion, of which up to USD 1 billion is in the process of being executed by the end of the first quarter of 2021.

International action regarding capital distributions

During 2020, regulators in several jurisdictions implemented measures restricting bank capital distributions and share repurchase programs. These measures were intended to maintain capital resilience and lending capacity following the outbreak of the COVID-19 pandemic. As at 31 December 2020, no such measures were in place in Switzerland.

In June 2020, the European Systemic Risk Board issued a recommendation to prevent EU financial institutions from making capital distributions and running share repurchase programs, which was extended in July 2020 until 1 January 2021. In December 2020, the ECB announced that EU banks under its supervision, including UBS Europe SE, should exercise extreme prudence with regard to dividends and share repurchases from 1 January until 30 September 2021.

In the US, the Federal Reserve Board (the FRB) has taken several actions, including a prohibition on increasing dividends and share repurchases, which started in the third quarter of 2020, keeping these restrictions largely unchanged throughout the fourth quarter. As a result, UBS Americas Holding LLC was restricted from distributing cash dividends on common equity in excess of the firm’s average net income over the four preceding quarters. In December, the FRB announced that it would continue capital distribution constraints for supervised firms for the first quarter of 2021 and would review the need to renew such constraints at a later date.

UBS continues to monitor policy developments regarding distributions.

Significant regulatory and disclosure requirements and changes effective in or from 2020

Significant BCBS and FINMA capital adequacy, liquidity and funding, and related disclosure requirements

This Pillar 3 report has been prepared in accordance with FINMA Pillar 3 disclosure requirements (FINMA Circular 2016/1 “Disclosure – banks”) as revised on 31 October 2019, the underlying BCBS guidance “Revised Pillar 3 disclosure requirements” issued in January 2015, the “Frequently asked questions on the revised Pillar 3 disclosure requirements” issued in August 2016, the “Pillar 3 disclosure requirements – consolidated and enhanced framework” issued in March 2017 and the subsequent “Technical Amendment – Pillar 3 disclosure requirements – regulatory treatment of accounting provisions” issued in August 2018.

Changes to Pillar 1 requirements

Revised FINMA circular on credit risk

Effective 1 January 2020, we have adopted the standardized approach for counterparty credit risk (SA-CCR). SA-CCR is a comprehensive, non-modeled approach for measuring counterparty credit risk associated with over-the-counter derivatives, exchange-traded derivatives and long settlement transactions that replaces the current exposure method (CEM).

The implementation impact from SA-CCR on risk-weighted assets was USD 1.8 billion, which was fully absorbed during the first quarter of 2020.

We also adopted the capital requirements for investments in funds in the banking book detailed in FINMA Circular 2017/7 “Credit risk – banks,” whereby investments in funds that are held in the banking book are consistently treated with one of the following three approaches, which vary in their degree of risk sensitivity and conservatism: the “look-through approach,” the “mandate-based approach” or the “fallback approach.” The implementation of these revised capital requirements for fund investments led to a USD 0.6 billion increase in RWA, which was fully absorbed during the first quarter of 2020.

In addition, we have implemented the FINMA revisions to the capital treatment concerning UBS’s exposures to central counterparties, which mainly include a single approach for calculating capital requirements for exposures arising from UBS’s contributions to the mutualized default fund resources of a qualifying central counterparty (a QCCP) which had no material impact on risk-weighted assets, and the specific guidance regarding multi-level client structures where UBS clears its trades through intermediaries linked to a central counterparty.

Swiss SRB going and gone concern requirements

As of 1 January 2020, we have fully phased in the going and gone concern requirements of the Swiss Capital Adequacy Ordinance (the CAO) that include the too-big-to-fail provisions applicable to Swiss SRBs.

As of 1 January 2020, instruments meeting gone concern requirements continue to remain eligible until one year before maturity; the previously applicable 50% haircut in the last year of eligibility has been removed. Instead, a maximum of 25% of the gone concern requirements can now be met with instruments that have a remaining maturity of between one and

3

two years (i.e., are in the last year of eligibility). Once at least 75% of the gone concern requirement has been met with instruments that have a remaining maturity of greater than two years, all instruments that have a remaining maturity of between one and two years remain eligible to be included in the total gone concern capital. Our gone concern instruments are reasonably evenly distributed across maturities, with no major cliffs; therefore, this 25% restriction has not affected us and we do not anticipate that it will affect us in the future.

Under the Swiss SRB framework, banks are eligible for a rebate on the gone concern requirement if they take actions that facilitate recovery and resolvability beyond the minimum requirements. The amount of the rebate for improved resolvability is assessed annually by FINMA. Based on actions we had completed by December 2019 to improve resolvability, FINMA granted a rebate on the gone concern requirement of 47.5% of the aforementioned maximum rebate in the third quarter of 2020, which resulted in a reduction of 2.54 percentage points for the RWA-based requirement and 0.89 percentage points for the LRD-based requirement.

Our gone concern requirements are further reduced when higher quality capital instruments (CET1 capital, low-trigger loss-absorbing AT1 or certain low-trigger tier 2 capital instruments) are used to meet gone concern requirements. As of 31 December 2020, UBS has used low-trigger tier 2 capital instruments to fulfill gone concern requirements, resulting in a reduction of 1.25 percentage points for the RWA-based requirement and 0.35 percentage points for the LRD-based requirement.

Until 31 December 2021, the gone concern requirement following the application of the rebate for resolvability measures and the reduction for the use of higher quality capital instruments is floored at 8.6% and 3% for the RWA- and LRD-based requirements, respectively. From 1 January 2022 onwards, this floor increases to 10% and 3.75% for the RWA- and LRD-based requirements, respectively.

› Refer to the “Capital, liquidity and funding, and balance sheet” section of our Annual Report 2020, available under ”Annual reporting” at ubs.com/investors, for information about the current capital requirements

Gone concern capital requirements for UBS AG standalone and UBS Switzerland AG

Effective 1 January 2020, UBS AG standalone is subject to the gone concern capital requirements for Switzerland-based intermediate parent banks of global systemically important banks (G-SIBs) on a standalone basis, as stipulated in the revised CAO issued in November 2019. We have provided the necessary disclosure since the first quarter of 2020.

UBS Switzerland AG is subject to a lower gone concern requirement effective 1 January 2020, corresponding to 62% of the Group’s gone concern requirement (before applicable reductions) as outlined in the revised CAO.

› Refer to the “UBS AG standalone” and the “UBS Switzerland AG standalone” sections of this report for more information about the revised gone concern capital requirements

Revision of the Swiss Banking Act

In June 2020, the Swiss Federal Council adopted a dispatch on the partial revision of the Banking Act. The proposed measures

would strengthen the Swiss depositor protection scheme by requiring banks to deposit half of their contribution obligations for the deposit protection scheme in securities or cash with a custodian. A related adjustment to the Intermediated Securities Act would require custodians of securities to separate their own portfolios from the portfolios of their clients. Furthermore, the revision would amend the section of the Swiss Banking Act on bank insolvency provisions, including the ranking of claims in case of a bail-in and the required subordination of bail-in bonds, except those issued by a holding company with pari passu liabilities of less than 5% of the total bail-in bond capital.

As the next step, both chambers of the Parliament will debate the bill; the revised Banking Act is not expected to come into force until the start of 2022. We expect moderate additional costs for all Switzerland-based Group entities in scope.

Results of the annual Comprehensive Capital Analysis and Review

In June 2020, the Federal Reserve released the results of its annual Dodd–Frank Act Stress Tests (DFAST) and Comprehensive Capital Analysis and Review (CCAR).

UBS’s intermediate holding company, UBS Americas Holding LLC, exceeded minimum capital requirements under the severely adverse scenario and the Federal Reserve did not object to its capital plan. As a result, UBS Americas Holding LLC will no longer be subject to the qualitative assessment component of CCAR.

Following the completion of the annual DFAST and CCAR, UBS Americas Holding LLC was assigned a stress capital buffer (an SCB) of 6.7% under the SCB rule (based on Dodd–Frank Act stress test results and planned future dividends), which results in the imposition of restrictions if the SCB is not maintained above specified regulatory minimum capital requirements.

The Federal Reserve also conducted sensitivity analyses to model the economic effects of the COVID-19 pandemic. As a result of these supplementary analyses, the Federal Reserve determined that firms should resubmit revised capital plans based on a new stress scenario. In December 2020, the Federal Reserve released the results of this second CCAR of 2020. UBS Americas Holding LLC’s projected stress capital ratios exceeded regulatory capital minima under the updated supervisory scenarios.

Restatement of compensation-related liabilities

During 2020, UBS restated its balance sheet and statement of changes in equity as of 1 January 2018 to correct a liability understatement in connection with a legacy Global Wealth Management deferred compensation plan in the Americas region, resulting in a decrease in equity attributable to shareholders of USD 32 million. The corresponding effects on regulatory capital and other disclosed metrics were reflected in the comparative period figures where applicable. The restatement had no effect on net profit / (loss) for the current period or for any comparative periods.

› Refer to “Note 1b Changes in accounting policies, comparability and other adjustments” in the “Consolidated financial statements” section of our Annual Report 2020 report for more information

4

Changes to Pillar 3 disclosure requirements

First publication of the Pillar 3 ”CCR8 – Exposures to central counterparties” table

Following the adoption of the FINMA revisions to the capital treatment concerning UBS’s exposures to central counterparties in January 2020, we disclose the semi-annual “CCR8 – Exposures to central counterparties” table.

Other changes to Pillar 3 disclosures

Simplification of Pillar 3 disclosures

Given the current immaterial business volumes and declining trend of total securitization exposures over the past years, we have condensed the following semi-annual Pillar 3 disclosures into one single tabular disclosure titled ”Securitization exposures in the banking and trading book and associated regulatory capital requirements”:

– ”SEC1 – Securitization exposures in the banking book”;

– ”SEC2 – Securitization exposures in the trading book”;

– ”SEC3 – Securitization exposures in the banking book and associated regulatory capital requirements – bank acting as originator or as sponsor”; and

– ”SEC4 – Securitization exposures in the banking book and associated regulatory capital requirements – bank acting as investor.”

The new table is presented in this report and in our 30 June 2020 Pillar 3 report.

Market risk RWA are mainly based on the internal models approach, with the exception of securitization exposures in the trading book, which are subject to the standardized approach. From the second quarter of 2020 onward, the MR1 table is therefore no longer separately presented and RWA from securitization exposures in the trading book continues to be disclosed in the “OV1 – Overview of RWA” and in the narrative of section 7 on securitization exposures in the trading book.

Significant model updates and accounting and methodology changes effective in or from 2020

Removal of market risk RWA multiplier

When our value-at-risk (VaR) model was structurally changed in the first quarter of 2016, FINMA introduced a temporary market risk RWA multiplier of 1.3 to be applied in the calculation of VaR and stressed VaR (SVaR) RWA. As of 30 June 2020, we have removed this specific multiplier, following the demonstration of model performance.

Operational risk RWA model recalibration

During the fourth quarter of 2020, FINMA approved the annual Group advanced measurement approach (AMA) recalibration, resulting in a reduction of operational risk RWA by USD 1.8 billion, to USD 75.8 billion.

Phase-in of RWA effects

Effective from the third quarter of 2020, we began to phase in RWA increases related to the fourth quarter of 2020 release of new probability of default (PD) and loss given default (LGD) parameters for the mortgage portfolios in the US. As agreed with FINMA, the RWA effects of such model updates will be phased in over six quarters, until the end of 2021, with an estimated quarterly RWA increase of USD 0.5 billion.

Changes to accounting treatment affecting Pillar 1 and Pillar 3 disclosures of UBS AG standalone

In June 2020, we aligned the accounting treatment of investments in associates in the UBS AG International Financial Reporting Standards (IFRS) standalone accounts with the ”equity method” accounting applied in the UBS Group IFRS financial statements. Previously, we had applied a ”cost less impairment” approach for these investments in the UBS AG standalone IFRS financial statements. Effective 30 June 2020, UBS AG standalone CET1 capital, LRD and RWA increased by approximately USD 0.9 billion, USD 0.9 billion and USD 2.4 billion, respectively.

› Refer to the “UBS AG standalone” section of our 30 June 2020 Pillar 3 report for more information about the restated comparatives

Significant regulatory and disclosure requirements to be adopted in 2021 or later

In September 2020, the Swiss Federal Council adopted an amendment to the Liquidity Ordinance for the implementation of the net stable funding ratio (the NSFR). The NSFR regulation was finalized in the fourth quarter of 2020 with the release of the revised FINMA liquidity circular, and will become effective on 1 July 2021. It applies to UBS Group AG at the consolidated level and to UBS AG, UBS Switzerland AG and UBS Swiss Financial Advisers AG at the standalone level. UBS is on schedule to operationalize the NSFR regulation; its overall effect on UBS is expected to be limited.

In October 2020, the US banking regulators finalized the NSFR rule for supervised firms to ensure a minimum level of stable funding. The rule becomes effective as of 1 July 2021 and will require semi-annual disclosure from 1 January 2023. As a Category III firm under the Federal Reserve’s Tailoring Rule (2019), UBS’s intermediate holding company, UBS Americas Holding LLC, and its subsidiary bank, UBS Bank USA, will be subject to an NSFR requirement of 85%.

In the European Union, the European Commission adopted the updated Capital Requirements Regulation in June 2019, which will become effective from 28 June 2021. The regulation requires UBS Europe SE to provide a detailed annual NSFR disclosure and a semi-annual NSFR key metrics disclosure.

› Refer to the “Capital, liquidity and funding, and balance sheet” section of our Annual Report 2020, available under ”Annual reporting” at ubs.com/investors, for more information about the NSFR

Basel III finalization and adjustments to market risk framework

The BCBS announced the finalization of the Basel III framework in December 2017, and published the final rules on the minimum capital requirements for market risk (the Fundamental Review of the Trading Book) in January 2019. In response to COVID-19, the Group of Central Bank Governors and Heads of Supervision, which acts as the Basel Committee’s oversight body, endorsed the deferral of the implementation date by one year, to 1 January 2023. The accompanying transitional arrangements for the output floor have also been extended by one year, to 1 January 2028. The most significant changes include:

– placing floors on certain model inputs under the IRB approach to calculate credit risk RWA;

5

– requiring the use of standardized approaches for calculation of the credit valuation adjustment and for operational risk RWA;

– placing an aggregate output floor on the group RWA equal to 72.5% of the RWA calculated using a revised standardized approach; and

– revising the LRD calculation and introducing a leverage ratio surcharge for G-SIBs.

The revisions to the minimum capital requirements on market risk include adjustments to the risk sensitivity of the standardized approach, the calibration of certain elements of the framework and adjustments of the internal models approach. The revised BCBS standards will take effect from 1 January 2023.

We do not expect the Swiss regulations to become mandatory until after the BCBS target effective date of 1 January 2023.

Leverage ratio treatment

In June 2019, the BCBS aligned the leverage ratio measurement of client-cleared derivatives with SA-CCR. This treatment permits both cash and non-cash forms of segregated initial margin, as well as cash and non-cash variation margin, received from a client to offset the replacement cost and potential future exposure for client-cleared derivatives only. This will help to mitigate any potential effect on the LRD from the finalization of the Basel III framework. The modified standardized approach for counterparty credit risk for leverage ratio purposes will become effective 1 January 2023. We expect the effective date in Switzerland to be aligned with the adoption of the Basel III finalization.

Pillar 3 disclosure requirements

The BCBS has updated the Pillar 3 disclosure requirements to reflect the revisions to the operational risk, market risk, credit risk, credit value adjustments and leverage ratio under the finalized Basel III framework. In addition, there will be new disclosure requirements on asset encumbrance and, if required by national supervisors at the jurisdictional level, on capital distribution constraints. Further, banks are asked to disclose their leverage ratios based on quarter-end and daily average values of securities financing transactions. These requirements will become effective 1 January 2023. We expect the effective date in Switzerland to be aligned with the adoption of the Basel III finalization.

Revisions to the CVA risk framework

In July 2020, the BCBS replaced the Credit Valuation Adjustment (CVA) risk framework published in December 2017 with an updated standard. This final standard incorporates changes proposed in the consultation published in November 2019, and includes recalibrated risk weights, different treatment of certain client cleared derivatives and an overall recalibration of the standardized and basic approach including a reduced value of the aggregate multiplier for banks using the SA-CVA. These revisions come into effect on 1 January 2023. We expect the effective date in Switzerland to be aligned with the adoption of the Basel III finalization.

Capital treatment of securitizations of non-performing loans

The BCBS issued a technical amendment in November 2020 that sets out capital requirements for non-performing loan securitizations, with an expected implementation date no later than 1 January 2023. The technical amendment establishes a 100% risk weight for certain tranches of non-performing loan securitizations. The risk weights applicable to the other positions are determined by the existing hierarchy of approaches, in conjunction with a 100% risk weight floor and a ban on the use of certain inputs for capital requirements. This amendment does not change the applicable capital requirements to securitizations of performing assets. We expect the effective date in Switzerland to be aligned with the adoption of the Basel III finalization.

Significant BCBS and FINMA consultation papers

Minimum haircut floors for securities financing transactions

On 26 January 2021, the BCBS issued a consultation to seek public feedback on two technical amendments to the standard on minimum haircut floors for securities financing transactions (SFTs). The amendments seek to address an interpretative issue relating to collateral upgrade transactions and correct for a misstatement of the formula used to calculate haircut floors for netting sets of SFTs. Comments on this consultative paper are due by 31 March 2021.

Frequency and comparability of Pillar 3 disclosures

The table on the next page summarizes the reporting frequency for each disclosure as per the current FINMA requirements applicable to UBS.

We provide quantitative comparative information as of 30 September 2020 for disclosures required on a quarterly basis and as of 30 June 2020 for disclosures required on a semi-annual basis. Where specifically required by FINMA and / or the BCBS, we disclose comparative information for additional reporting dates.

Where required, movement commentary is aligned with the corresponding disclosure frequency required by FINMA and always refers to the latest comparative period. Throughout this report, signposts are displayed at the beginning of a section, table or chart – Annual | Semi-annual | Quarterly | – indicating whether the disclosure is provided annually, semi-annually or quarterly. A triangle symbol – p p p – indicates the end of the signpost.

› Refer to our 31 March 2020, 30 June 2020 and 30 September 2020 Pillar 3 reports, available under “Pillar 3 disclosures” at ubs.com/investors, for more information about previously published quarterly movement commentary

› Refer to our 30 June 2020 Pillar 3 report, available under “Pillar 3 disclosures” at ubs.com/investors, for more information about previously published semi-annual movement commentary

6

The following table outlines the annual, semi-annual and quarterly disclosure requirements that are satisfied in this report for UBS Group and significant regulated subsidiaries and sub-groups as applicable. For specific disclosures, this report may refer to our Annual Report 2020.

FINMA reference1 | Disclosure title in this report | Section of this report | Page number in this report |

Annual disclosure requirements | |||

OVA | Bank risk management approach | Introduction and basis for preparation | 11–12

|

LI1 | Differences between accounting and regulatory scopes of consolidation and mapping of financial statements with regulatory risk categories | Section 3 Linkage between financial statements and regulatory exposures | 23 |

LI2 | Main sources of differences between regulatory exposure amounts and carrying values in financial statements (under the regulatory scope of consolidation) | Section 3 Linkage between financial statements and regulatory exposures | 25 |

LIA | Explanations of differences between accounting and regulatory exposure amounts | Section 3 Linkage between financial statements and regulatory exposures | 24 |

PV1 | Prudent valuation adjustments (PVA) | Section 11 Going and gone concern requirements and eligible capital | 99 |

Disclosure of G-SIB indicators | Section 16 Requirements for global systemically important banks and related indicators | 109 | |

LIQA | Liquidity risk management | Section 14 Liquidity coverage ratio | 107 |

CRA | Credit risk management | Section 4 Credit risk | 27 |

CRB | Additional disclosure related to the credit quality of assets: – Breakdown of exposures by industry – Breakdown of exposures by geographical area – Breakdown of exposures by residual maturity – Credit-impaired exposures by industry – Credit-impaired exposures by geographical area – Past due exposures – Breakdown of restructured exposures between credit-impaired and non-credit-impaired | Section 4 Credit risk |

28 28 29 30 30 32 32 |

CRC | Credit risk mitigation | Section 4 Credit risk | 33 |

CRD | Qualitative disclosures on banks’ use of external credit ratings under the standardized approach for credit risk | Section 4 Credit risk | 37 |

CRE | Internal ratings-based models | Section 4 Credit risk | 39 |

CR9 | IRB – backtesting of probability of default (PD) per portfolio | Section 4 Credit risk | 50–56 |

CCRA | Counterparty credit risk management | Section 5 Counterparty credit risk | 58 |

SECA | – Introduction – Objectives, roles and involvement

| Section 7 Securitization | 74 74–75 |

MRA | Market risk | Section 8 Market risk | 77 |

MRB | Internal models approach | Section 8 Market risk | 80 |

Interest rate risk in the banking book | Section 10 Interest rate risk in the banking book | 88 | |

IRRBB1 | Quantitative information about IRRBB | Section 10 Interest rate risk in the banking book | 89 |

IRRBBA1 | Quantitative disclosures relating to the position structure and interest rate reset of IRRBB risk | Section 10 Interest rate risk in the banking book | 90–91 |

REMA | Remuneration policy | Section 15 Remuneration | 108 |

ORA | Operational risk | Section 9 Operational risk | 87 |

- | Calculation of VaR- and SVaR-based RWA as of 31 December 2020 | Section 8 Market risk | 82

|

- | Calculation of RniV-based RWA as of 31 December 2020 | Section 8 Market risk | 84

|

- | Calculation of IRC-based RWA as of 31 December 2020 | Section 8 Market risk | 85

|

- | Comprehensive risk measure | Section 8 Market risk | 86 |

7

FINMA reference1 | Disclosure title in this report | Section in this report | Page number in this report |

Semi-annual disclosure requirements | |||

CR1 | Credit quality of assets | Section 4 Credit risk | 31 |

CR2 | Changes in stock of defaulted loans, debt securities and off-balance sheet exposures | Section 4 Credit risk | 32 |

CR3 | Credit risk mitigation techniques – overview | Section 4 Credit risk | 34 |

CR4 | Standardized approach – credit risk exposure and credit risk mitigation (CRM) effects | Section 4 Credit risk | 35 |

CR5 | Standardized approach – exposures by asset classes and risk weights | Section 4 Credit risk | 38 |

CR6 | IRB – credit risk exposures by portfolio and PD range | Section 4 Credit risk | 40–47 |

CR7 | IRB – effect on RWA of credit derivatives used as CRM techniques | Section 4 Credit risk | 36 |

CR10 | IRB (equities under the simple risk-weight method) | Section 4 Credit risk | 57 |

CCR1 | Analysis of counterparty credit risk (CCR) exposure by approach | Section 5 Counterparty credit risk | 59 |

CCR2 | Credit valuation adjustment (CVA) capital charge | Section 5 Counterparty credit risk | 59 |

CCR3 | Standardized approach – CCR exposures by regulatory portfolio and risk weights | Section 5 Counterparty credit risk | 60 |

CCR4 | IRB – CCR exposures by portfolio and PD scale | Section 5 Counterparty credit risk | 61–65 |

CCR5 | Composition of collateral for CCR exposure | Section 5 Counterparty credit risk | 66 |

CCR6 | Credit derivatives exposures | Section 5 Counterparty credit risk | 66 |

CCR8 | Exposures to central counterparties | Section 5 Counterparty credit risk | 68 |

SEC1, SEC2, SEC3, SEC4 | Tailored table “Securitization exposures in the banking and trading book and associated regulatory capital requirements“ | Section 7 Securitizations | 76 |

MR1 | The data is reflected in the “Securitization exposures in the banking and trading book and associated regulatory capital requirements” table | Section 7 Securitizations | 76 |

MR3 | IMA values for trading portfolios | Section 8 Market risk | 81 |

MR4 | Comparison of VaR estimates with gains / losses | Section 8 Market risk | 83 |

CC1 | Composition of regulatory capital | Section 11 Going and gone concern requirements and eligible capital | 96–98 |

CC2 | Reconciliation of accounting balance sheet to balance sheet under the regulatory scope of consolidation | Section 11 Going and gone concern requirements and eligible capital | 94–95 |

CCA | Main features of regulatory capital instruments and other TLAC-eligible instruments | n/a – The CCA table is published on our website. Refer to the document titled “Capital and total loss-absorbing capacity instruments of UBS Group AG consolidated and UBS AG consolidated and standalone – key features” under “Bondholder information” at ubs.com/investors, for more information. | n/a |

CCyB1 | Geographical distribution of credit exposures used in the countercyclical capital buffer | Section 11 Going and gone concern requirements and eligible capital | 93 |

TLAC1 | TLAC composition for G-SIBs (at resolution group level) | Section 12 Total loss-absorbing capacity | 100 |

TLAC2 | Material sub-group entity – creditor ranking at legal entity level | Significant regulated subsidiaries and sub-groups: Section 5 UBS Americas Holding LLC consolidated | 125 |

TLAC3 | Creditor ranking at legal entity level for the resolution entity, UBS Group AG | Section 12 Total loss-absorbing capacity | 101 |

- | Main legal entities consolidated under IFRS but not included in the regulatory scope of consolidation | Section 3 Linkage between financial statements and regulatory exposures | 24

|

8

FINMA reference1 | Disclosure title in this report | Section in this report | Page number in this report |

|

Quarterly disclosure requirements | ||||

KM1 | Key metrics | UBS Group: Section 1 Key metrics

Significant regulated subsidiaries and sub-groups: Section 2 UBS AG standalone Section 3 UBS Switzerland AG standalone Section 4 UBS Europe SE consolidated Section 5 UBS Americas Holding LLC consolidated |

18–19

111 116 123 124

|

|

KM2 | Key metrics – TLAC requirements (at resolution group level) | Section 1 Key metrics | 18, 20 |

|

OV1 | Overview of RWA | Section 2 Overview of risk-weighted assets | 21–22 |

|

CR8 | RWA flow statements of credit risk exposures under IRB | Section 4 Credit risk | 49 |

|

CCR7 | RWA flow statements of CCR exposures under internal model method (IMM) and value-at-risk (VaR) | Section 5 Counterparty credit risk | 67 |

|

MR2 | RWA flow statements of market risk exposures under an internal models approach | Section 8 Market risk | 79 |

|

LR1 | BCBS Basel III leverage ratio summary comparison | Section 13 Leverage ratio | 104 |

|

LR2 | BCBS Basel III leverage ratio common disclosure | Section 13 Leverage ratio | 103 |

|

LIQ1 | Liquidity coverage ratio | Section 14 Liquidity coverage ratio | 106 |

|

- | High-quality liquid assets | Section 14 Liquidity coverage ratio | 105 |

|

- | Swiss SRB going and gone concern requirements and information | UBS Group: Section 11 Going and gone concern requirements and eligible capital

Significant regulated subsidiaries and sub-groups: Section 2 UBS AG standalone Section 3 UBS Switzerland AG standalone |

92

113 117 |

|

-

| Swiss SRB going concern requirements and information including temporary FINMA exemption | UBS Group: Section 11 Going and gone concern requirements and eligible capital

Significant regulated subsidiaries and sub-groups: Section 2 UBS AG standalone Section 3 UBS Switzerland AG standalone |

93

112 118 |

|

-

| Swiss SRB going and gone concern information | Significant regulated subsidiaries and sub-groups: Section 2 UBS AG standalone Section 3 UBS Switzerland AG standalone |

114 119 |

|

-

| Reconciliation of IFRS total assets to BCBS Basel III total on-balance sheet exposures excluding derivatives and securities financing transactions | Section 13 Leverage ratio | 102 |

|

-

| Swiss SRB leverage ratio denominator | Significant regulated subsidiaries and sub-groups: Section 2 UBS AG standalone Section 3 UBS Switzerland AG standalone |

115 120 |

|

1 Disclosure requirement per FINMA Circular 2016/1 “Disclosure – banks.”

9

Format of Pillar 3 disclosures

As defined by FINMA, certain Pillar 3 disclosures follow a fixed format, whereas other disclosures are flexible and may be modified to a certain degree to present the most relevant information. Pillar 3 requirements are presented under the relevant FINMA table / template reference (e.g., OVA, OV1, LI1, etc.). Pillar 3 disclosures may also include row labeling (1, 2, 3, etc.) as prescribed by FINMA. Naming conventions used in our Pillar 3 disclosures are based on the FINMA guidance and may not reflect UBS naming conventions.

The FINMA-defined asset classes used within this Pillar 3 report are as follows:

– Central governments and central banks, consisting of exposures relating to governments at the level of the nation state and their central banks. The European Union is also treated as a central government.

– Banks and securities dealers, consisting of exposures to legal entities holding banking licenses and securities firms subject to adequate supervisory and regulatory arrangements, including risk-based capital requirements. Securities firms can only be assigned to this asset class if they are subject to a supervision equivalent to that of banks.

– Public-sector entities and multi-lateral development banks, consisting of exposures to institutions established on the basis of public law in different forms, such as administrative entities or public companies and regional governments, the Bank for International Settlements, the International Monetary Fund, and eligible multi-lateral development banks recognized by FINMA.

– Corporates: specialized lending, consisting of exposures relating to income-producing real estate and high-volatility commercial real estate, commodities finance, project finance and object finance.

– Corporates: other lending, consisting of all exposures to corporates that are not specialized lending. This asset class includes private commercial entities, such as corporations, partnerships or proprietorships, insurance companies and funds (including managed funds).

– Retail: residential mortgages, consisting of residential mortgages, regardless of exposure size, if the owner occupies or rents out the mortgaged property.

– Retail: qualifying revolving retail exposures, consisting of unsecured and revolving credits to individuals that exhibit appropriate loss characteristics relating to credit card relationships at UBS.

– Retail: other, consisting primarily of Lombard lending that represents loans made against the pledge of eligible marketable securities or cash, as well as exposures to small businesses, private clients and other retail customers without mortgage financing.

– Equity, consisting of instruments that have no stated or predetermined maturity and represent a residual interest in the net assets of an entity.

– Other assets, consisting of the remainder of exposures which UBS is exposed to, mainly non-counterparty-related assets.

Governance over Pillar 3 disclosures

The Board of Directors (the BoD) and senior management are responsible for establishing and maintaining an effective internal control structure over the disclosure of financial information, including Pillar 3 disclosures. In line with BCBS and FINMA requirements, we have a BoD-approved Pillar 3 disclosure governance policy in place, which includes information about the key internal controls and procedures designed to govern the preparation, review and sign-off of Pillar 3 disclosures. This Pillar 3 report has been verified and approved in line with that policy.

10

Risk management framework

Our Group-wide risk management framework is applied across all risk types. The table below presents an overview of risk management disclosures that are provided separately in our Annual Report 2020, available under “Annual reporting” at ubs.com/investors.

Annual |

OVA – Bank risk management approach | ||||||||

Pillar 3 disclosure requirement |

| Annual Report 2020 section |

| Disclosure |

| Annual Report 2020 page number | ||

|

|

|

|

|

|

|

| |

Business model and risk profile |

| Our strategy, business model and environment |

| – | Risk factors |

| 56–66 | |

|

|

| – | Current market climate and industry trends |

| 31–33 | ||

|

| Risk, capital, liquidity and funding, and balance sheet |

| –

–

–

–

–

–

–

–

–

–

–

– | Overview of risks arising from our business activities

Risk categories

Top and emerging risks

Risk appetite framework

Risk measurement

Credit risk – Key developments, Main sources of credit risk, Overview of measurement, monitoring and management techniques, Credit risk profile of the Group

Market risk – Key developments, Main sources of market risk, Overview of measurement, monitoring and management techniques

Interest rate risk in the banking book

Other market risk exposures

Country risk framework, Country risk exposure

Operational risk framework

Risk management and control principles |

| 91–92

93

94

97–100

103–105

106–107

124

128–131

131–132

133–136

140

98 | |

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

Risk governance |

| Risk, capital, liquidity and funding, and balance sheet |

| –

–

–

–

– | Risk categories

Risk governance

Interest rate risk in the banking book – Risk management and governance

Liquidity and funding management – Strategy, objectives and governance

Capital management – Capital management objectives, Capital planning and activities |

| 93 95–96 129

158

144 | |

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

Communication and enforcement of risk culture within the bank |

| Risk, capital, liquidity and funding, and balance sheet |

| – – – – | Risk governance Risk appetite framework Internal risk reporting Operational risk framework |

| 95–96 97–100 101 140 | |

Scope and main features of risk measurement systems |

| Risk, capital, liquidity and funding, and balance sheet |

| – –

–

– – | Risk measurement Credit risk – Overview of measurement, monitoring and management techniques Market risk – Overview of measurement, monitoring and management techniques Country risk exposure measure Advanced measurement approach model |

| 103–105 107

124

133 141 | |

| ||||||||

| ||||||||

Risk information reporting |

| Risk, capital, liquidity and funding, and balance sheet |

| – – – | Risk governance Internal risk reporting Risk management and control principles |

| 95–96 101 98 | |

|

| |||||||

11

OVA – Bank risk management approach (continued) | |||||||

Pillar 3 disclosure requirement |

| Annual Report 2020 section |

| Disclosure |

| Annual Report 2020 page number | |

|

|

|

|

|

|

| |

Stress testing |

| Risk, capital, liquidity and funding, and balance sheet |

| – | Risk appetite framework |

| 97–100 |

|

| – | Stress testing |

| 103–104 | ||

|

| – | Credit risk models – Stress loss |

| 119 | ||

|

| – | Market risk stress loss |

| 125 | ||

|

| – | Interest rate risk in the banking book |

| 128–131 | ||

|

| – | Other market risk exposures |

| 131–132 | ||

|

| – | Liquidity management – Stress testing |

| 158 | ||

Strategies and processes applied to manage, hedge and mitigate risks |

| Risk, capital, liquidity and funding, and balance sheet |

| – | Credit risk – Overview of measurement, monitoring and management techniques |

| 107 |

|

|

| – | Credit risk mitigation |

| 114–115 | |

|

|

| – | Market risk – Overview of measurement, monitoring and management techniques |

| 124 | |

|

|

| – | Value-at-risk |

| 125–128 | |

|

|

| – | Interest rate risk in the banking book |

| 128–131 | |

|

|

| – | Other market risk exposures |

| 131–132 | |

|

|

| – | Country risk exposure |

| 133–136 | |

|

|

| – | Operational risk framework |

| 140 | |

|

|

| – | Liquidity and funding management |

| 158–161 | |

|

|

| – | Currency management |

| 171 | |

|

|

| – | Risk management and control principles |

| 98 | |

| Consolidated financial statements |

| – | Note 10 Derivative instruments |

| 320–321 | |

|

|

| – | Note 20d Maximum exposure to credit risk |

| 343 | |

|

|

| – | Note 21i Maximum exposure to credit risk for financial instruments measured at fair value |

| 362 | |

|

|

| – | Note 22 Offsetting financial assets and financial liabilities |

| 364–365 | |

p

12

Our approach to measuring risk exposure and risk-weighted assets

Depending on the intended purpose, the measurement of risk exposure that we apply may differ. Exposures may be measured for financial accounting purposes under IFRS for deriving our regulatory capital requirement or for internal risk management and control purposes. Our Pillar 3 disclosures are generally based on measures of risk exposure used to derive the regulatory capital required under Pillar 1. Our RWA are calculated according to the BCBS Basel III framework, as implemented by the Swiss Capital Adequacy Ordinance issued by the Swiss Federal Council and by the associated circulars issued by FINMA.

The table below provides a summary of the approaches we use for the main risk categories to determine the regulatory risk exposure and RWA.

Category | Definition of risk | Regulatory risk exposure | Risk-weighted assets (RWA) |

I. Credit risk | |||

Credit risk | Credit risk is the risk of a loss resulting from the failure of a counterparty to meet its contractual obligations toward UBS arising from transactions such as loans, debt securities held in our banking book and undrawn credit facilities.

Refer to section 4, Credit risk. | Exposure at default (EAD) is the amount we expect a counterparty to owe us at the time of a possible default. For banking products, the EAD generally equals the IFRS carrying amount as of the reporting date. The EAD is expected to remain constant over the 12-month period. For loan commitments, a credit conversion factor is applied to model expected future drawdowns over the 12-month period. | We apply two approaches to measure credit risk RWA: – Advanced internal ratings-based (A-IRB) approach, applied for the majority of our businesses. Counterparty risk weights are determined by reference to internal probability of default and loss given default estimates. – Standardized approach (SA), generally based on external ratings for a sub-set of our credit portfolio where internal measures are not available. |

Non-counterparty-related risk | Non-counterparty-related risk (NCPA) denotes the risk of a loss arising from changes in value or from liquidation of assets not linked to any counterparty, for example, premises, equipment and software, and deferred tax assets on temporary differences.

Refer to section 2, Overview of risk-weighted assets. | The IFRS carrying amount is the basis for measuring NCPA exposure. | We measure non-counterparty-related risk RWA by applying prescribed regulatory risk weights to the NCPA exposure. |

Equity positions in the banking book | Risk from equity positions in the banking book refers to the investment risk arising from equity positions and other relevant investments or instruments held in our banking book.

Refer to section 4, Credit risk. | The IFRS carrying amount is the basis for measuring risk exposure for equity securities held in our banking book, but reflecting a net position. | We measure the RWA from equity positions in the banking book by applying prescribed regulatory risk weights to our listed and unlisted equity exposures. |

13

Category | Definition of risk | Regulatory risk exposure | Risk-weighted assets (RWA) |

II. Counterparty credit risk | |||

Counterparty credit risk | Counterparty credit risk is the risk that a counterparty for over-the-counter (OTC) derivatives, exchange-traded derivatives (ETDs) or securities financing transactions (SFTs) will default before the final settlement of a transaction and cause a loss to the firm if the transaction has a positive economic value at the time of default.

Refer to section 5, Counterparty credit risk. | We primarily use internal models to measure counterparty credit risk exposures to third parties. All internal models are approved by FINMA. – For OTC derivatives and ETDs, we apply the effective expected positive exposure (EEPE) and stressed expected positive exposure (stressed EPE) as defined in the Basel III framework. – For SFTs, we apply the close-out period approach.

In certain instances where risk models are not available: – Exposure on OTC derivatives and ETDs is calculated considering the net positive replacement values and potential future exposure. – Exposure for SFTs is based on the IFRS carrying amount, net of collateral mitigation. | We apply two approaches to measure counterparty credit risk RWA: – Advanced internal ratings-based (A-IRB) approach, applied for the majority of our businesses. Counterparty risk weights are determined by reference to internal counterparty ratings and loss given default estimates. – Standardized approach (SA), generally based on external ratings for a sub-set of our credit portfolio, where internal measures are not available.

We apply an additional credit valuation adjustment (CVA) capital charge to hold capital against the risk of mark-to-market losses associated with the deterioration of counterparty credit quality. |

Settlement risk | Settlement risk is the risk of loss resulting from transactions that involve exchange of value (e.g., security versus cash) where we must deliver without first being able to determine with certainty that we will receive the countervalue.

Refer to section 2, Overview of risk-weighted assets. | The IFRS carrying amount is the basis for measuring settlement risk exposure. | We measure settlement risk RWA through the application of prescribed regulatory risk weights to the settlement risk exposure. |

III. Securitization exposures in the banking book | |||

Securitization exposures in the banking book | Exposures arising from traditional and synthetic securitizations held in our banking book.

Refer to section 7, Securitizations. | The IFRS carrying amount after eligible regulatory credit risk mitigation and credit conversion factor is the basis for measuring securitization exposure. | Consistent with the BCBS, we apply the FINMA-defined hierarchy of approaches for banking book securitizations to measure RWA: – Internal ratings-based approach (SEC-IRBA), considering the advanced IRB risk weights, if the securitized pool largely consists of IRB positions and internal ratings are available. – External ratings-based approach (SEC-ERBA), if the IRB approach cannot be applied, risk weights are applied based on external ratings, provided that we are able to demonstrate our expertise in critically reviewing and challenging the external ratings. – Standardized approach (SEC-SA) or 1,250% risk weight factor, if none of the aforementioned approaches can be applied, we would apply the standardized approach where the delinquency status of a significant portion of the underlying exposure can be determined or a risk weight of 1,250%.

For re-securitization exposures we apply either the standardized approach or a risk weight factor of 1,250%. |

14

Category | Definition of risk | Regulatory risk exposure | Risk-weighted assets (RWA) |

IV. Market risk | |||

Value-at-risk (VaR) | VaR is a statistical measure of market risk, representing the market risk losses that could potentially be realized over a set time horizon (holding period) at an established level of confidence. For regulatory VaR, the holding period is 10 days and the confidence level is 99%. For our risk management measure Management VaR we apply a holding period of 1 day and a confidence level of 95%. For further differences between the regulatory and Management VaR, refer to the “Risk management and control” section of our Annual Report 2020.

Refer to section 8, Market risk. |

| The VaR component of market risk RWA is calculated by taking the maximum of the period-end VaR and the product of the average VaR for the 60 trading days immediately preceding the period end and a VaR multiplier. The quantity is then multiplied by a risk weight factor of 1,250% to determine RWA. The VaR multiplier is dependent on the number of VaR backtesting exceptions within the most recent 250-business-day window. |

Stressed VaR (SVaR) | SVaR is a 10-day 99% VaR measure that is estimated with model parameters that are calibrated to historical data covering a one-year period of significant financial stress relevant to the firm’s current portfolio.

Refer to section 8, Market risk. |

| The derivation of SVaR RWA is similar to the one explained above for VaR. Unlike VaR, SVaR is computed weekly, and as a result the average SVaR is computed over the most recent 12 observations. |

Add-on for risks not in VaR (RniV) | Potential risks that are not fully captured by our VaR model are referred to as RniV. We have a framework to identify and quantify these potential risks and underpin them with capital.

Refer to section 8, Market risk. |

| Our RniV framework is used to derive the RniV-based component of the market risk RWA, which is approved by FINMA. Starting in the second quarter of 2018, RniV and RWA resulting from RniV are recalibrated on a monthly basis.

As the RWA from RniV are add-ons, they do not reflect any diversification benefits across risks capitalized through VaR and SVaR. |

Incremental risk charge (IRC) | The IRC represents an estimate of the default and rating migration risk of all trading book positions with issuer risk, except for equity products and securitization exposures, measured over a one-year time horizon at a 99.9% confidence level.

Refer to section 8, Market risk. |

| The IRC is calculated weekly, and the results are used to derive the IRC-based component of the market risk RWA. The derivation is similar to that for VaR- and SVaR-based RWA, but without a VaR multiplier. |

Comprehensive risk measure (CRM) | The CRM is an estimate of the default and complex price risk, including the convexity and cross-convexity of the CRM portfolio across credit spread, correlation and recovery, measured over a one-year time horizon at a 99.9% confidence level.

Refer to section 8, Market risk. |

| Since the second quarter of 2019, we have not held eligible correlation trading positions. Prior to then, the CRM had been calculated weekly and used to derive the CRM-based component of the market risk RWA, with the calculation subject to a floor equal to 8% of the equivalent capital charge under the specific risk measure (SRM) for the correlation trading portfolio. |

Securitization / re-securitization in the trading book | Risk arising from traditional and synthetic securitizations held in our trading book.

Refer to section 7, Securitizations and | The exposure is equal to the fair value of the net long or short securitization position. | We measure trading book securitization RWA using the Ratings-based approach, i.e., applying risk weights based on external ratings. |

V. Operational risk | |||

Operational risk | Operational risk is the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events, including cyber risk. Operational risk includes, among others, legal risk, conduct risk and compliance risk.

Refer to section 9, Operational risk. |

| We use the advanced measurement approach to measure operational risk RWA in accordance with FINMA requirements. |

15

UBS Group AG consolidated

Key metrics of the fourth quarter of 2020

Quarterly | The KM1 and KM2 tables on the following pages are based on the Basel Committee on Banking Supervision (the BCBS) Basel III rules; however, they do not reflect the effects of the temporary exemption granted by the Swiss Financial Market Supervisory Authority (FINMA) in connection with COVID-19 that permits banks to exclude central bank sight deposits from the leverage ratio calculation. The KM2 table includes a reference to the total loss-absorbing capacity (TLAC) term sheet, published by the Financial Stability Board (the FSB). The FSB provides this term sheet at fsb.org/2015/11/total-loss-absorbing-capacity-tlac-principles-and-term-sheet.

During the fourth quarter of 2020, our common equity tier 1 (CET1) capital increased by USD 1.7 billion to USD 39.9 billion, mainly due to operating profit before tax, foreign currency effects and deferred tax assets on temporary differences, partially offset by a higher capital reserve for potential share repurchases, current tax expenses and accruals for dividends. Our tier 1 capital increased by USD 1.8 billion to USD 56.2 billion, primarily reflecting the aforementioned increase in our CET1 capital and foreign currency translation effects on our additional tier 1 (AT1) instruments.

The TLAC available as of 31 December 2020 included CET1 capital, AT1 and tier 2 capital instruments eligible under the TLAC framework, and non-regulatory capital elements of TLAC. Under the Swiss systemically relevant bank (SRB) framework, including transitional arrangements, TLAC excludes 45% of the gross unrealized gains on debt instruments measured at fair value through other comprehensive income for accounting purposes, which for regulatory capital purposes is measured at the lower of cost or market value. This amount was negligible as of 31 December 2020, but is included as available TLAC in the KM2 table in this section. Our available TLAC increased by USD 4.1 billion to USD 101.8 billion in the fourth quarter of 2020, reflecting the aforementioned USD 1.8 billion increase in our tier 1 capital and a USD 2.2 billion increase in non-regulatory capital instruments, which resulted mainly from the issuance of new instruments and foreign currency effects.

Risk-weighted assets (RWA) increased by USD 6 billion to USD 289.1 billion, including currency effects of USD 4.7 billion, mainly due to an increase of USD 5.1 billion in credit risk RWA, an increase of USD 1.2 billion in market risk RWA and an increase of USD 0.8 billion in amounts below the threshold for deduction, primarily related to deferred tax assets. This was partly offset by a reduction of USD 1.8 billion in operational risk RWA.

Leverage ratio exposure increased by USD 43 billion to USD 1,037 billion, including currency effects of USD 24 billion, driven by on-balance sheet exposures (other than securities financing transactions (SFTs) and derivatives), partly offset by decreases in SFTs and derivative exposures.

Average high-quality liquid assets (HQLA) increased by USD 3.1 billion, due to higher holdings of liquidity buffer securities. Average total net cash outflows increased by USD 3.5 billion due to higher customer deposit outflows. p

18

Quarterly |

KM1: Key metrics |

|

|

|

|

|

|

|

|

| |

USD million, except where indicated |

| |||||||||

|

|

| 31.12.20 |

| 30.9.20 |

| 30.6.201 |

| 31.3.201 | 31.12.191 |

Available capital (amounts) |

|

|

|

|

|

|

|

|

| |

1 | Common equity tier 1 (CET1) |

| 39,890 |

| 38,197 |

| 38,114 |

| 36,659 | 35,535 |

1a | Fully loaded ECL accounting model CET12 |

| 39,856 |

| 38,162 |

| 38,070 |

| 36,624 | 35,491 |

2 | Tier 1 |

| 56,178 |

| 54,396 |

| 53,505 |

| 51,884 | 51,842 |

2a | Fully loaded ECL accounting model Tier 12 |

| 56,144 |

| 54,360 |

| 53,460 |

| 51,850 | 51,797 |

3 | Total capital |

| 61,226 |

| 59,382 |

| 58,876 |

| 57,752 | 57,568 |

3a | Fully loaded ECL accounting model total capital2 |

| 61,193 |

| 59,347 |

| 58,831 |

| 57,718 | 57,524 |

Risk-weighted assets (amounts) |

|

|

|

|

|

|

|

|

| |

4 | Total risk-weighted assets (RWA) |

| 289,101 |

| 283,133 |

| 286,436 |

| 286,256 | 259,208 |

4a | Minimum capital requirement3 |

| 23,128 |

| 22,651 |

| 22,915 |

| 22,901 | 20,737 |

4b | Total risk-weighted assets (pre-floor) |

| 289,101 |

| 283,133 |

| 286,436 |

| 286,256 | 259,208 |

Risk-based capital ratios as a percentage of RWA |

|

|

|

|

|

|

|

|

| |

5 | Common equity tier 1 ratio (%) |

| 13.80 |

| 13.49 |

| 13.31 |

| 12.81 | 13.71 |

5a | Fully loaded ECL accounting model Common equity tier 1 ratio (%)2 |

| 13.79 |

| 13.48 |

| 13.29 |

| 12.79 | 13.69 |

6 | Tier 1 ratio (%) |

| 19.43 |

| 19.21 |

| 18.68 |

| 18.12 | 20.00 |

6a | Fully loaded ECL accounting model Tier 1 ratio (%)2 |

| 19.42 |

| 19.20 |

| 18.66 |

| 18.11 | 19.98 |

7 | Total capital ratio (%) |

| 21.18 |

| 20.97 |

| 20.55 |

| 20.17 | 22.21 |

7a | Fully loaded ECL accounting model total capital ratio (%)2 |

| 21.17 |

| 20.96 |

| 20.54 |

| 20.16 | 22.19 |

Additional CET1 buffer requirements as a percentage of RWA |

|

|

|

|

|

|

|

|

| |

8 | Capital conservation buffer requirement (2.5% from 2019) (%) |

| 2.50 |

| 2.50 |

| 2.50 |

| 2.50 | 2.50 |

9 | Countercyclical buffer requirement (%) |

| 0.02 |

| 0.02 |

| 0.02 |

| 0.02 | 0.08 |

9a | Additional countercyclical buffer for Swiss mortgage loans (%) |

|

|

|

|

|

|

|

| 0.23 |

10 | Bank G-SIB and / or D-SIB additional requirements (%) |

| 1.00 |

| 1.00 |

| 1.00 |

| 1.00 | 1.00 |

11 | Total of bank CET1-specific buffer requirements (%) |

| 3.52 |

| 3.52 |

| 3.52 |

| 3.52 | 3.58 |

12 | CET1 available after meeting the bank’s minimum capital requirements (%) |

| 9.30 |

| 8.99 |

| 8.81 |

| 8.31 | 9.21 |

Basel III leverage ratio4 |

|

|

|

|

|

|

|

|

| |

13 | Total Basel III leverage ratio exposure measure |

| 1,037,150 |

| 994,366 |

| 974,359 |

| 955,943 | 911,322 |

14 | Basel III leverage ratio (%) |

| 5.42 |

| 5.47 |

| 5.49 |

| 5.43 | 5.69 |

14a | Fully loaded ECL accounting model Basel III leverage ratio (%)2 |

| 5.41 |

| 5.47 |

| 5.49 |

| 5.42 | 5.68 |

Liquidity coverage ratio5 |

|

|

|

|

|

|

|

|

| |

15 | Total HQLA |

| 214,276 |

| 211,185 |

| 206,693 |

| 170,630 | 166,215 |

16 | Total net cash outflow |

| 140,891 |

| 137,345 |

| 133,786 |

| 122,383 | 124,112 |

17 | LCR (%) |

| 152 |

| 154 |

| 155 |

| 139 | 134 |

1 Refer to the “Introduction and basis for preparation” section of this report for information on the restatement of comparative information, as applicable. 2 The fully loaded ECL accounting model excludes the transitional relief of recognizing ECL allowances and provisions in CET1 capital in accordance with FINMA Circular 2013/1 “Eligible capital – banks.” 3 Calculated as 8% of total RWA, based on total capital minimum requirements, excluding CET1 buffer requirements. 4 Leverage ratio exposures and leverage ratios for the respective periods in 2020 do not reflect the effects of the temporary exemption that has been granted by FINMA in connection with COVID-19. Refer to the “Introduction and basis for preparation” section of this report and to “Application of the temporary COVID-19-related FINMA exemption of central bank sight deposits” in the “Going and gone concern requirements and eligible capital“ section of this report for more information. 5 Calculated based on quarterly average. Refer to the “Liquidity coverage ratio” section of this report for more information. | ||||||||||

p

19

UBS Group AG consolidated

Quarterly |

KM2: Key metrics – TLAC requirements (at resolution group level)1 | |||||||||||

USD million, except where indicated |

|

|

|

|

|

|

|

|

|

| |

|

| 31.12.20 |

| 30.9.20 |

| 30.6.202 |

| 31.3.202 |

| 31.12.192 | |

1 | Total loss-absorbing capacity (TLAC) available |

| 101,814 |

| 97,753 |

| 93,626 |

| 93,686 |

| 89,613 |

1a | Fully loaded ECL accounting model TLAC available3 |

| 101,780 |

| 97,717 |

| 93,581 |

| 93,652 |

| 89,569 |

2 | Total RWA at the level of the resolution group |

| 289,101 |

| 283,133 |

| 286,436 |

| 286,256 |

| 259,208 |

3 | TLAC as a percentage of RWA (%) |

| 35.22 |

| 34.53 |

| 32.69 |

| 32.73 |

| 34.57 |

3a | Fully loaded ECL accounting model TLAC as a percentage of fully loaded ECL accounting model RWA (%)3 |

| 35.21 |

| 34.51 |

| 32.67 |

| 32.72 |

| 34.56 |

4 | Leverage ratio exposure measure at the level of the resolution group4 |

| 1,037,150 |

| 994,366 |

| 974,359 |

| 955,943 |

| 911,322 |

5 | TLAC as a percentage of leverage ratio exposure measure (%)4 |

| 9.82 |

| 9.83 |

| 9.61 |

| 9.80 |

| 9.83 |

5a | Fully loaded ECL accounting model TLAC as a percentage of fully loaded ECL accounting model leverage exposure measure (%)3,4 |

| 9.81 |

| 9.83 |

| 9.60 |

| 9.80 |

| 9.83 |

6a | Does the subordination exemption in the antepenultimate paragraph of Section 11 of the FSB TLAC Term Sheet apply? |

| No | ||||||||

6b | Does the subordination exemption in the penultimate paragraph of Section 11 of the FSB TLAC Term Sheet apply? |

| No | ||||||||

6c | If the capped subordination exemption applies, the amount of funding issued that ranks pari passu with excluded liabilities and that is recognized as external TLAC, divided by funding issued that ranks pari passu with excluded liabilities and that would be recognized as external TLAC if no cap was applied (%) |

| N/A – Refer to our response to 6b. | ||||||||