UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

Date: October 25, 2022

UBS Group AG

Commission File Number: 1-36764

UBS AG

Commission File Number: 1-15060

(Registrants' Names)

Bahnhofstrasse 45, Zurich, Switzerland

Aeschenvorstadt 1, Basel, Switzerland

(Address of principal executive offices)

Indicate by check mark whether the registrants file or will file annual reports under cover of Form 20‑F or Form 40-F.

Form 20-F x Form 40-F o

This Form 6-K consists of the presentation materials related to the Third Quarter 2022 Results of UBS Group AG and UBS AG and the related speaker notes and Q&A session, which appear immediately following this page

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

25 October 2022

Speeches by Ralph Hamers, Group Chief Executive Officer, and Sarah Youngwood, Group Chief Financial Officer

Including analyst Q&A session

Transcript.

Numbers for slides refer to the third quarter 2022 results presentation. Materials and a webcast replay are available at www.ubs.com/investors

33

Ralph Hamers

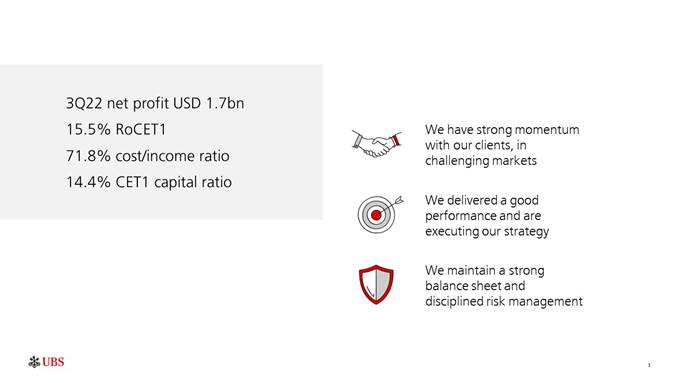

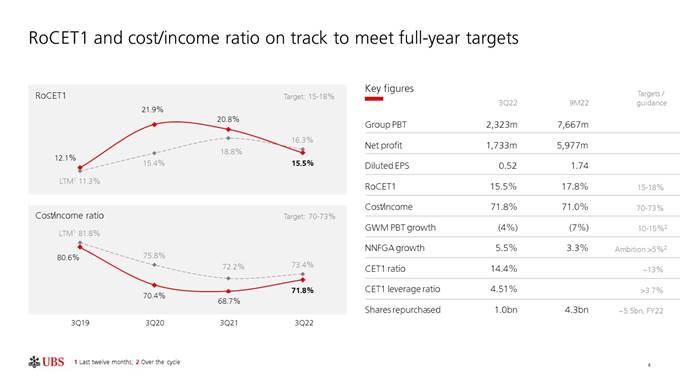

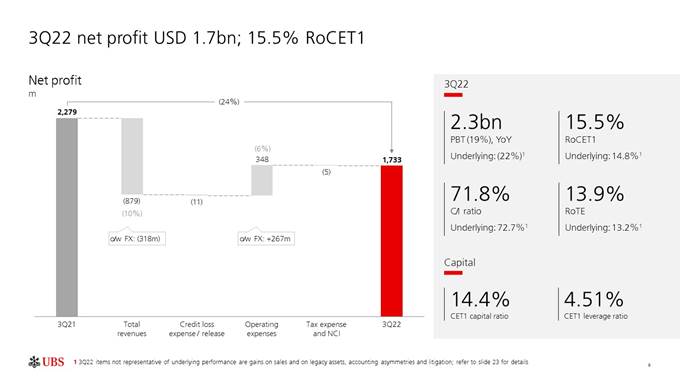

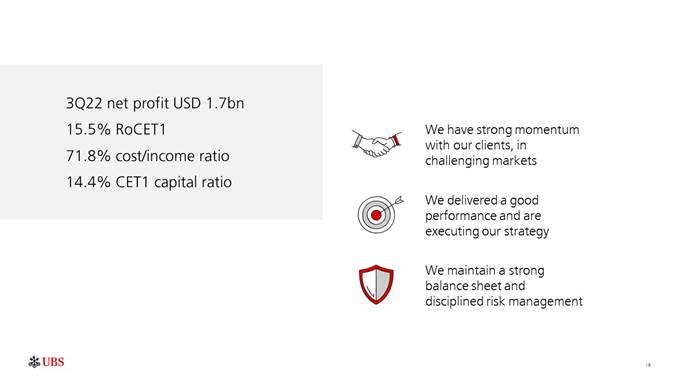

Slide 3 – 3Q22 net profit USD 1.7bn; 15.5% RoCET1, 71.8% cost/income ratio, and 14.4% CET1 capital ratio

Hey, thank you, Sarah. Good morning, everyone.

I'm pleased to share good results with you for this quarter. Amidst significant macroeconomic and geopolitical uncertainty, we executed with discipline. We delivered $1.7 billion in net profit and our return on CET1 capital was 15.5%. Our capital position remains strong with a CET1 ratio of 14.4%, as you can see, and we manage cost well, leading to a cost/income ratio of 71.8%. And our balance sheet for all seasons and strong risk management continued to be an asset for our clients and the investors.

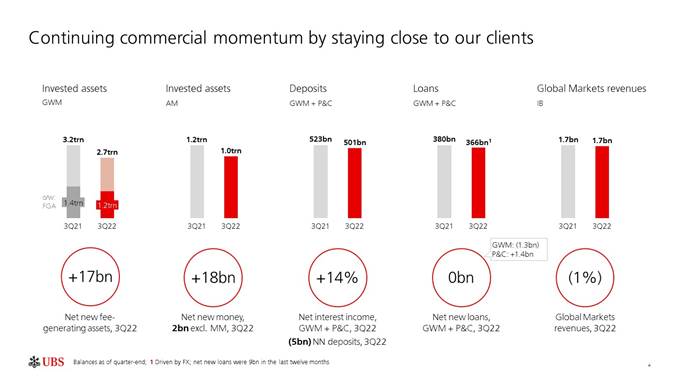

Slide 4 – Continuing commercial momentum by staying close to our clients

Turning to the next slide where you have the overall overview of the commercial momentum. This quarter, I spent a lot of time with clients across the globe and their feedback was really consistent. They're concerned about inflation, about the energy prices, the war in Ukraine, residual effects from the pandemic, economies are slowing down. Central banks are raising rates at record pace, and that's affecting asset levels. It's affecting market volatility and investor sentiment across the globe as well. And we expect this to continue at least through the end of the year.

Client activity has been differentiated across segments. Institutional clients remained very active on the back of high volatility of foreign exchange and rates. But private investors generally remained on the sidelines, waiting for signs of improvement.

In all cases, our teams have stayed close to our clients, providing them with advice and solutions. And you can see the snapshot here on this slide. We help private clients seeking opportunities to protect and grow their wealth. They diversified their portfolio through mandate solutions, and made additional commitments to private markets. And as a result, for the need for guidance, which we gave, we saw $17 billion in net new fee-generating assets coming in through the quarter.

Wealth management clients are seeking higher yielding products on the back of higher interest rates. We're capturing this demand through savings, through CDs, money market funds, and half of the $16 billion of net new money coming in through asset management in money markets – So, I have the $16 billion in money markets, so $8 billion is actually coming from GWM clients. We also continue to actively manage our deposit offering and optimize net interest income. And that's where we saw 14% growth year-on-year in our deposit taking businesses.

In lending, we've seen our clients deleveraging Lombard loans specifically in Asia Pacific, but we saw demand for mortgages in Switzerland and the US. The net impact is a loan book that was flat this quarter excluding foreign exchange. And as I mentioned, institutional clients continue to trade actively, and that resulted in another strong performance for Global Markets given our mix and geographic footprint. We benefited from foreign exchange and rates volatility, which resulted in the FRC revenues being up 64%, but we were impacted by equities being down. And I think this shows the – our ability and flexibility to deploy resources across the asset classes, and that shows the value of the way we are organized. It also kind of shows the – that our technology investments, specifically in electronic FX, are supporting a record quarter in e-FX as well. As you can see, consistent execution of our strategy is driving organic growth despite volatile market conditions.

34

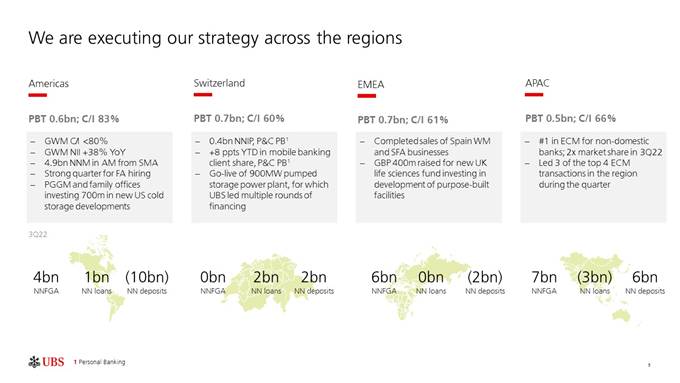

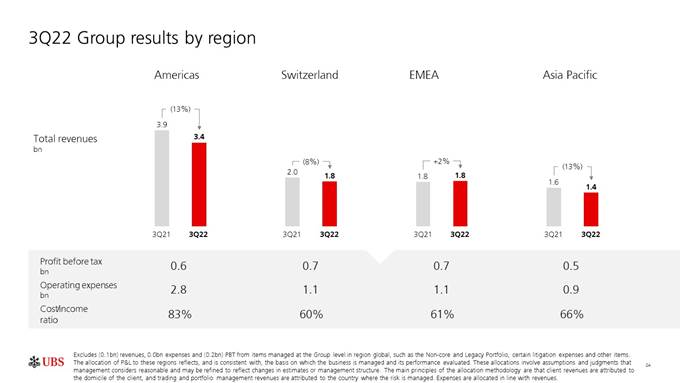

Slide 5 – We are executing our strategy across the regions

Now, moving to the more regional picture. That's basically where the execution of our strategy towards our clients really comes together. In the US, the economy is holding up relatively better than other regions, consumer balance sheet and economic, well, employment data are solid, but inflation remains high. As a result, we project Fed funds to peak at 5% to 5.25%, and such elevated rates increase the risk of recession. Interest rate hikes have reduced asset levels and muted client activity as well, but they have supported net interest income which is up 38% year-over-year. So, that's on the US and Wealth Management specifically there.

Demand for separately managed accounts and alternatives continue to drive inflows that fueled over $4 billion of net new fee-generating assets, mostly from our existing financial adviser base.

We also had a strong quarter in advisor recruiting and our hiring pipeline remains strong as well for the fourth quarter and that should – should support our flows also through the fourth quarter and beyond. These hires in the line are a commitment to drive scale and improve the GWM, America's cost income ratio, which was below 80% this quarter. So, you see the scale coming through there. We remain firmly committed to our US growth strategy, which is focused on personally-advised clients. We will also continue to develop digital solutions with remote advice within our existing technology budget.

Now moving to Switzerland, our economists expect it to narrowly avoid a recession due to relatively lower inflation and limited dependence on Russian gas. That said, many of our Swiss retail and small business clients will also be impacted by disruptions across the rest of Europe and we are focusing on supporting them through the energy crisis. The stability of our business in Switzerland, is by the way, demonstrated by a continued solid growth, $2 billion in net new loans, $2 billion in net new deposits, and $400 million in net new investment products, a real solid performance in Switzerland.

Now moving to EMEA, that's where the macroeconomic and geopolitical environment is having the most significant impact, as you can imagine. Clients turn to us, as indicated earlier, for advice in these uncertain and unprecedented times and the net fee generating assets on the back of that increased by more than $6 billion in EMEA. We also completed the sale of our Spanish business and also the SFA Wealth Management business in Switzerland, and that further optimized our footprint. And as you know, we are looking at further improvement of efficiency and profitable growth in EMEA as part of our strategy and we're delivering it this quarter again.

Lastly, Asia Pacific, we continue to believe that there is attractive, structural long-term growth prospects in the region. But the short term, it is clear that our clients are dealing with COVID-related restrictions still, as delaying recovery also in the property sector. We think there is a path back to 5% economic growth in China and Asia Pacific as a whole at some point next year, but the question is really about timing.

We expect these dynamics will restrict our clients willingness to take on leverage, and also it will limit their willingness to transact at least through the end of this year. And that said, they continue to look for us for diversification and investment expertise. And as a result, we saw another strong quarter in net new fee-generating assets also in this region with $7 billion of inflows.

Our analyzed net new fee generating assets growth rates in Asia Pacific is actually 12% year-to-date. In Asia Pacific's primary markets, we outperformed fee pools and took market share. We claimed the number one position in equity capital markets for non-domestic banks, and that's three of the top four equity raises in Asia Pacific, including Hong Kong's largest IPO in over a year.

So in summary, all of the regions are faced with complex macro and geopolitical environments, but we're clearly showing to be very focused on supporting our clients and be very flexible in the way we allocate our resources across the Investment Bank as well and using our global footprint and diverse capabilities to continue to add value for our clients.

35

Slide 6 – RoCET1 and cost/income ratio on track to meet full-year targets

Turning to slide 6 here for you, that demonstrates how the consistent execution of our strategy has delivered a good financial quarter. Net profit at $1.7 billion. Return on CET1 capital at 15.5%. Cost/income ratio as earlier mentioned at 71.8%. Of course, we are – we will continue to be focused on efficiency and expenses, and our cost discipline will further intensify as we fight inflationary pressures and we prepare for tougher times to come.

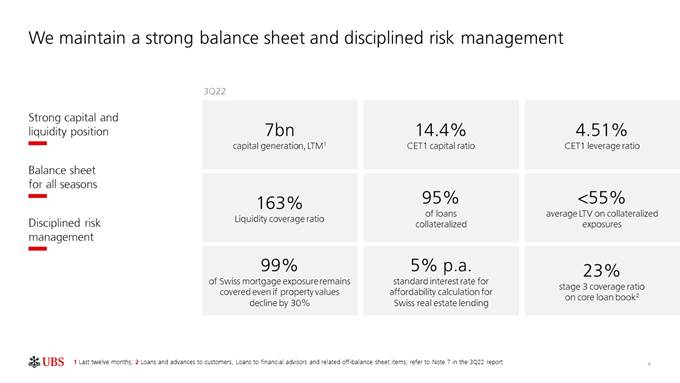

Slide 7 – We maintained a strong balance sheet and disciplined risk management

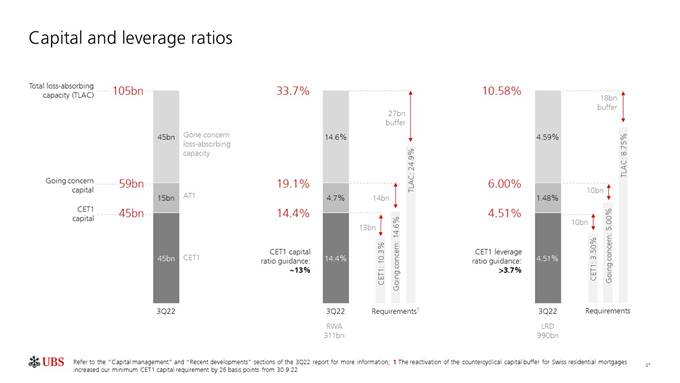

Turning to slide 7, given the environment that we're in, we felt it was important to give you a peek into the position of strength that we have facing some of these uncertainties. Our capital ratios remain well above our target levels at 14.4% in CET1 capital. We continue to operate with a significant amount of liquidity to support our clients and meet regulatory requirements as well. Our balance sheet for all seasons is supported by a high-quality loan book, 95% of our loans are collateralized and the average loan to value is less than 55%. We have a model that uses limited credit risk and has a high capital generative character. And with that, we remain confident in our ability to deliver attractive and sustainable capital returns to shareholders.

So, to summarize, we delivered a good performance in the quarter. Our capital-light model, our global diversification, the balance sheet for all seasons continue to be real competitive advantage.

In the first nine months of the year, we consistently executed with discipline, performed in line with our targets every quarter, and that gives us also confidence in our ability to meet our return on CET1 and cost/income ratio targets for the full year on a reported and also underlying basis.

With that, Sarah, over to you.

36

Sarah Youngwood

Slide 9 – 3Q22 net profit USD 1.7bn; 15.5% RoCET1, 71.8% cost/income ratio

Thank you, Ralph. Good morning, everyone.

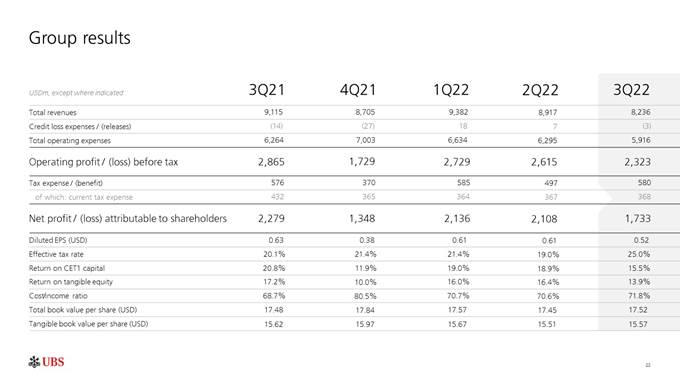

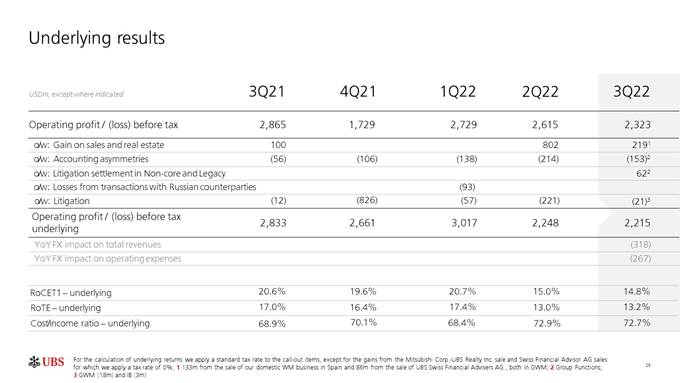

We delivered a good set of results while maintaining a balance sheet for all seasons and against a complex market backdrop. Net profit in the quarter was $1.7 billion. Ralph just walked you through the reported profitability with return on CET1 of 15.5% and a cost/income ratio of 71.8%. Our underlying profitability was not very different. Slide 23 in appendix walks through the items, which are the same in nature as last quarter.

Total revenue was down 10% against 6% lower expense. FX impacted both by $300 million for a net effect of around $50 million. The net credit loss release was $3 million compared to a $14 million release last year, reflecting great stability in our credit metrics and strong risk management.

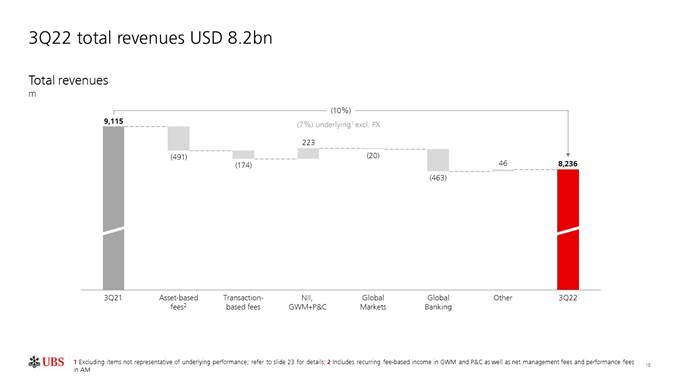

Slide 10 – Total revenues

On slide 10, the macroeconomic environment reflected depressed equity and fixed income markets, low levels of client activity, subdued M&A and capital markets and higher rates. Our revenue story mirrors the same themes with underlying revenue ex-FX down 7%. We had lower asset-based and transaction fees, lower global banking revenue, but higher combined NII in GWM and P&C. Global market revenue was broadly flat against a very strong prior year quarter.

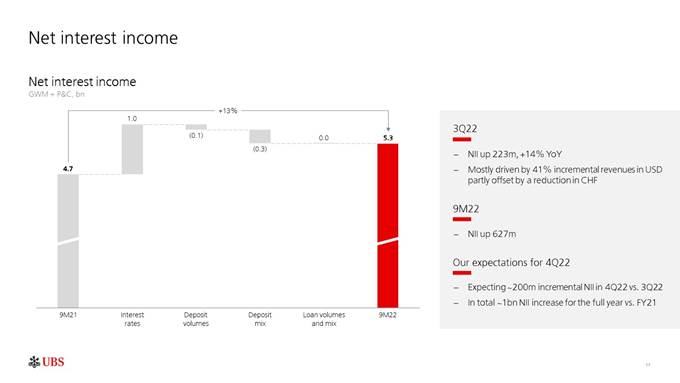

Slide 11 – Net interest income

Now moving to NII on page 11, the drivers of NII have been consistent over the course of this year with a strong benefit from rates, which you see in the first bar on the chart. Our actual deposit betas were better than we modeled. The rates impact was partially offset, as you see, by deposit volume and mix. On volume, next bar on the chart, the impact was driven by GWM, where deposits decreased by $23 billion last quarter and $13 billion this quarter, both in line with peers. FX accounted for almost half of the $13 billion decrease.

And regarding mix, we saw clients move from sweeps and current accounts into other UBS deposit products. In this quarter, on a net basis, we retained effectively all these assets within UBS, including over 60% in deposit products and another 25% in our own money market funds. So, overall, for this quarter, NII was up $223 million or 14% year-on-year. The US dollar increase in NII was 41%. But it was partially offset by a reduction in Swiss franc due to lower SNB benefit and deposit fees.

Looking ahead, based on the forwards, we expect approximately $200 million incremental NII in the fourth quarter versus the third quarter, of which two-thirds in GWM and one-third in P&C. This would lead to a total increase of $1 billion in 2022 versus last year. We expect 2023 NII to be higher than 4Q22 annualized given our exposure to Swiss franc and Euro, and no further SNB and deposit fee impacts. Our USD NII is expected to peak in 4Q22 or at the beginning of 2023.

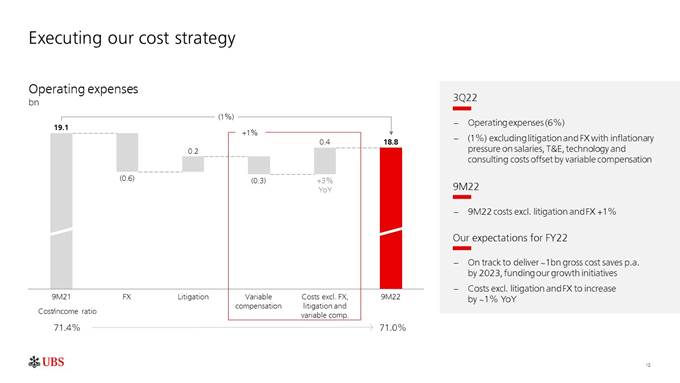

Slide 12 – Executing our cost strategy

Now turning to costs on page 12. This quarter's operating expense was down 6% year-on-year. Excluding litigation and FX, the number was down 1% with inflationary pressures on salaries, T&E, technology and consulting costs offset by variable compensation. Year-to-date, on the chart on the left, expense was down 1% or up 1% ex-litigation and FX. If you also exclude variable comp, expense was up 3%.

For the full year, we see expense ex-litigation and FX up 1% year-on-year. We are on track to deliver an incremental $400 million in 2022 as part of our program to deliver $1 billion cost saves by 2023 as announced last year. We are laser focused on costs and in the context of the current environment, we have put in place specific measures regarding non-critical hiring, T&E, consulting and tech prioritization.

37

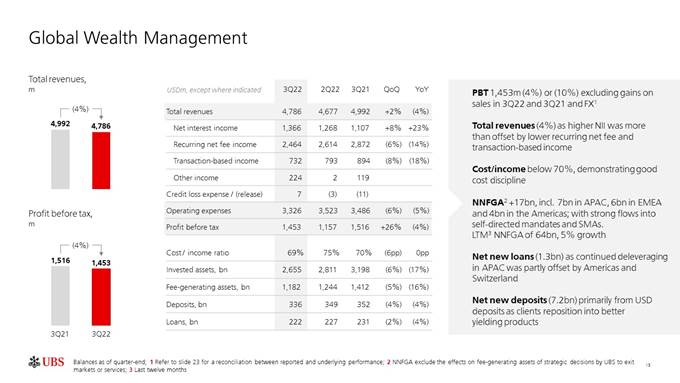

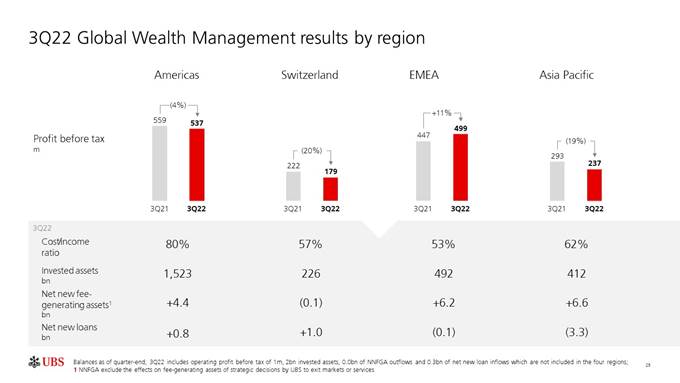

Slide 13 – Global Wealth Management

Let's move to our businesses on page 13, starting with GWM. GWM profit before tax in the quarter was $1.5 billion, down 4% against a record 3Q21. It was down 10% ex-FX and gains on sales in 3Q22 and 3Q21. Revenue was 4% lower than last year as market headwinds continued to challenge our asset-based and transaction revenue in all regions. These headwinds were partially offset by net interest income, which was up 23% year-on-year and up 8% sequentially as we continue to actively manage deposits across margins, volumes and mix.

The operating expense ex-litigation and FX was down 2% versus last year. This demonstrates our strong cost control that allowed us to deliver a cost/income ratio of less than 70% in GWM, and less than 80% in Americas. Net new fee generating assets were $17 billion in the quarter, a 5.5% annualized growth with positive flows into self-directed mandates, SMAs and alternatives. Ralph walked you through the strength we saw across the regions, and for the past 12 months, we attracted $64 billion of net new fee generating assets, which represents around a 5% growth rate.

Net new lending in 3Q was negative $1 billion, driven by deleveraging in APAC. However, we saw continued growth in Americas and Switzerland. Looking ahead, while client sentiment is likely to remain muted in the fourth quarter, our existing pipeline will be supportive of net new fee-generating assets.

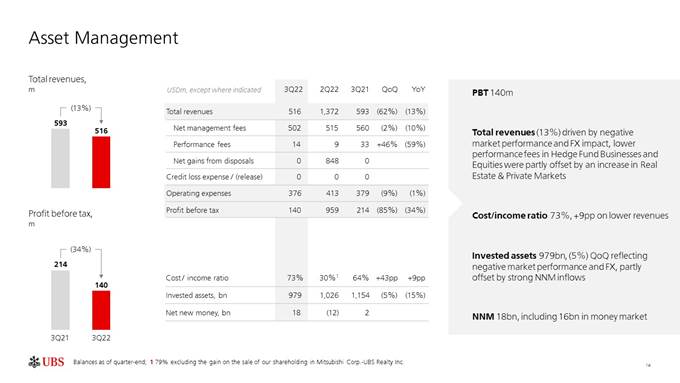

Slide 14 – Asset Management

Moving to Asset Management on page 14. With a profit before tax of $140 million, total revenue decreased by 13% or 8% ex-FX, with lower net management fees driven by market headwinds and lower performance fees. The cost/income ratio was 73%, up year-on-year, with lower revenue and expense broadly flat as we benefited from FX and continue to invest.

As Ralph mentioned, net new money was strong in the quarter at $18 billion, of which $16 billion in money market funds with significant wins in the US and EMEA. Excluding money markets, net new money was $2 billion driven by fixed income.

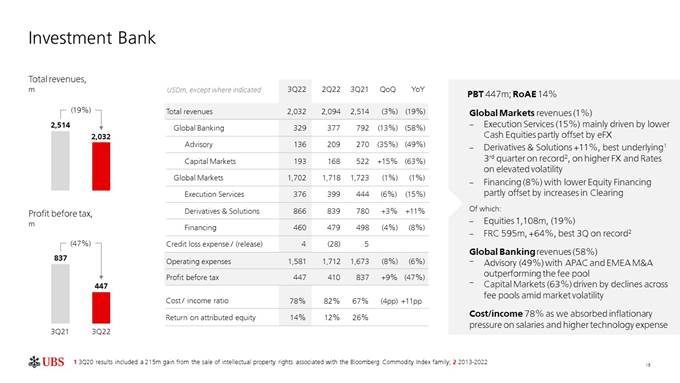

Slide 15 – Investment Bank

Now, on to slide 15. The IB delivered $447 million in profit before tax and a 14% return on attributed equity. These are solid results considering our revenue mix and geographic footprint. Thanks to our capital-light business model, we can operate with a RWA density of 30% compared to our estimates of around 50% for US peers.

Revenue in Global Markets of $1.7 billion was down 1%, or up 2% ex-FX, against a very strong prior-year quarter. If you think about the environment, it was one where volatility in equities was lower than in FX and rates. And in that context, we had a record third quarter performance in e-FX, FX, rates, and prime brokerage offset by reductions in equity derivatives and cash. Global Banking revenue was down 58% to $329 million, in line with very low levels of industry activity across Advisory and Capital Markets.

The operating expense was up 3% ex litigation and FX, largely driven by inflationary pressures and salaries and higher technology expense.

38

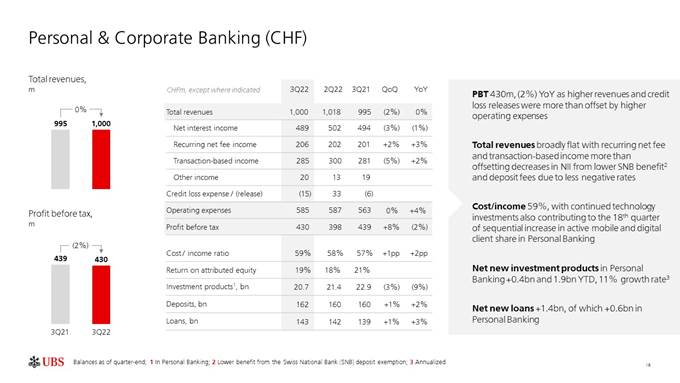

Slide 16 – Personal & Corporate Banking (CHF)

On page 16, moving to P&C, which had strong momentum and an 8 percentage point year-to-date increase in share of Personal Banking clients that are active mobile users.

Profit before tax in the third quarter was CHF 430 million. Total revenue was broadly flat year-on-year, as increases in recurring and transaction-based income were offset by lower NII. Transaction-based income increased 2% on higher revenue from FX and credit card transactions, reflecting higher spending both on travel and domestic. Recurring net fee income was up 3% on the back of more than 2 billion of net new investment products over the past 12 months.

For the quarter in Personal Banking, net new investment product had an annualized growth rate of 8%. The credit loss release was 15 million compared with 6 million a year ago. Costs ex-litigation were up 4% as we continue to make investments in technology to execute our digital strategy.

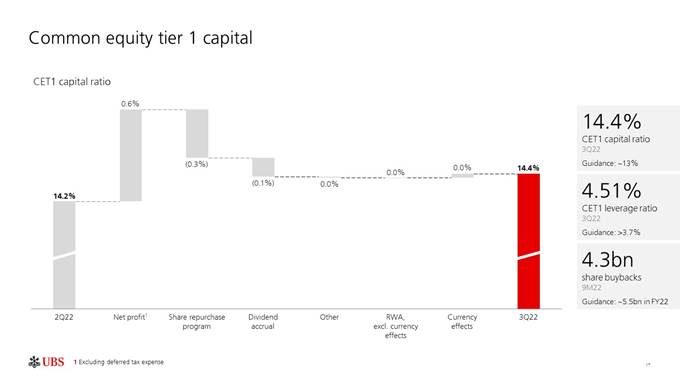

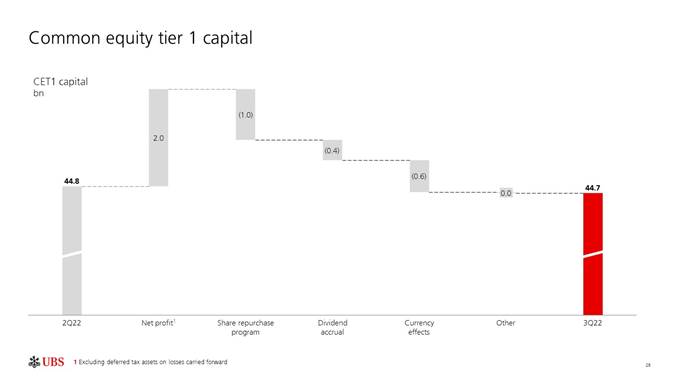

Slide 17 – Common equity tier 1 capital

Finally, on page 17, we maintained a strong capital position this quarter, well above our guidance while continuing to distribute capital according to our plans. As of the end of September, our CET1 capital ratio was 14.4% and our CET1 leverage ratio was 4.51%.

Turning to the CET1 capital ratio walk starting at 14.2% at the end of last quarter. Net profit contributed 60 basis points, partially offset by capital returns to our shareholders of around 40 basis points. The net currency effect was nil quarter-on-quarter as the FX impact on CET1 and RWA offset each other.

Our capital return story remains strong. We increased our dividend accrual from 51 to 55 cents, a 10% year-on-year increase, and we are on track to buyback approximately $5.5 billion of shares for the full year. In the first nine months of the year, we have repurchased $4.3 billion, and as of last Friday, the number was $4.6 billion. This translates into a payout ratio of 94% year-to-date including dividend accruals and buybacks.

Slide 18 – 3Q22 net profit USD 1.7bn; 15.5% RoCET1, 71.8% cost/income ratio, and 14.4% CET1 capital ratio

To conclude, while no one is immune to the macro environment, UBS is well-positioned to face short-term challenges. We have strong capital, capital returns, diversification and limited credit risk. This is in addition to NII tailwinds across currencies and expense flexibility. We are executing our strategy and focused on delivering consistent and attractive returns to shareholders.

With that, let's open up for questions.

39

Analyst Q&A (CEO and CFO)

Stefan Stalmann, Autonomous

Yes. Good morning. Thank you very much for the presentation and for taking my questions. I wanted to ask, please, on your cost guidance. You had previously said that cost might be up by 2% for the year on an FX adjusted basis. Now, you're saying it could be plus 1%. Could you maybe talk about what has changed? Have you reassessed variable compensation? Have you showed, slowed your investment spending plans or anything else to consider?

And the second question goes back to what you said about NII in 2023, Sarah. I missed what you said exactly. You talked about an annualization and that NII next year would be higher than an annualized number, but I missed the basis. Could you maybe repeat that for me? Thank you very much.

Ralph Hamers

Sure, Stefan. Sarah, on cost?

Sarah Youngwood

Yeah. So, on cost, we get the guidance that we would be up 1% ex-FX and litigation. And that is in line with where we are for year-to- date this year versus a year ago. In terms of the 2% guidance that you're referring to, this was done ex-variable comp. And on that basis, we are approximately at 3% and we will expect to continue to work on being below 3%, so with a 2, but still rounding to 3%.

And what's happening here is that you're seeing very strong cost discipline with the reported and ex-FX and ex-litigation story. And you're seeing that we're managing the entire cost base, but we are, of course, seeing some inflationary pressures that were higher than those that we were predicting at the time when we gave the guidance.

Yeah. And on the NII, it's – so literally it's as follows. So, we see uptick on NII. Dollar rates coming through, but euro and Swiss francs and pound rates coming through also in the fourth quarter, and with that increasing our NII guidance there by another $200 million. And then, how to look at that from a ‘23 perspective is that we are indicating that that will continue, the uplift there will continue in the different currencies more so than in the US dollar because we expect that to peak in the fourth quarter, maybe beginning of 2023. And therefore for 2023, you should start thinking about the annualized number for the fourth quarter, so four times fourth quarter, with upside. That's the way we guided.

Stefan Stalmann, Autonomous

Great. Thank you very much. Very clear. Thank you.

Amit Goel, Barclays

Hi. Thank you. I have one question on the NII I guidance, again, just to check. When we talked about the $200 million and talked about $1 billion next year, what kind of mix effect and/or deposit flow assumptions are in that?

And then secondly, I'm just kind of curious if you don't mind just going into a bit more color in terms of the costs, which are the areas where maybe you've kind of homed in some of the spending, what impact that has, and also how you're thinking about investment into Asia, as well at present? Thank you.

40

Ralph Hamers

Sarah can give you some more insights on the NII. We kind of – go ahead.

Sarah Youngwood

So, on the NII, and we already gave you a lot of information with guidance in the fourth quarter as well as additional directional guidance for 2023, and so that's okay. We'll pick up with even more than that next quarter when we report earnings. But we feel that the exposure that we have with half of our balance sheet being in US dollars, but the rest are not being in US dollars gives us upside in those other currencies that is worth mentioning to you at this point.

Ralph Hamers

And the cost and also in Asia specifically, but also on the cost, and what Sarah was indicating is that we are really focused on the cost side. We have been the whole year. Clearly, we had inflationary pressures that basically nobody had foreseen, but nevertheless, we manage a tight ship here. And also in the fourth quarter, as she was indicating that where we really want to be very clear, making sure that we don't impact the strategic investments nor that we don't impact the good cost, but that we are very strict on non-critical hires. So, we continue hiring, but only for the critical hires because we want to hold back on some that we have to be more careful around T&E and consultancy costs as well.

So, it will not be kind of impacting the strategic projects at this moment in time, and looking at further participation in the technology projects. So those are the four areas we're very much focused on.

Then into your question around Asia. Asia we know always go through bigger downturns and upturns than anywhere, but the underlying current is always positive. And specifically, if you look at it from a wealth pool perspective and a wealth pool development perspective, and that's the underlying basis for our strategy in Asia Pacific. We expect this to grow over time anywhere between 5% to 9%. So, it is an area where we want to continue to grow where we see $7 billion of net new fee generating assets just for the quarter. We expect some of that flows to continue as well. So, it's an important region for us to continue to invest in the wealth business as well.

Amit Goel, Barclays

Thank you. Sorry. Can I just follow-up just on that point then? So, there are some volume and mix assumptions within the $200 million. It's not a static balance sheet assumption. Okay.

Sarah Youngwood

That's right. This is not a static balance sheet. This is guidance.

Amit Goel, Barclays

Thank you.

41

Anke Reigen, Royal Bank of Canada

Yeah. Thank you very much for taking my question. It's basically just around the costs. Thank you for giving the nine-month trend on the costs ex-FX effects and litigation. I was wondering if you can give us the revenue equivalent on an FX adjusted basis for the nine months.

And I hear you on strategic investments, but do you see any need to potentially at what point or jaws would you thinking consider further actions on costs?

And then I think you mentioned in terms of the US offering all the costs will be included in your current budget. Can you just confirm that and how you going on about your bidding out the US offering without the Wealthfront acquisition. Thank you very much.

Ralph Hamers

Sure. You go ahead.

Sarah Youngwood

So, on the revenue ex-FX and the gains were down 7% and we actually put that on one of the slides the revenue slides. Yes. That's a revenues slide…

Anke Reigen, Royal Bank of Canada

Is that by month?

Sarah Youngwood

That's the year on... 3Q 2021 versus 2022. For the nine months, I can pull it for you. There was even more FX on the revenue in this quarter than last quarter, although last quarter there was some, too. So, we can come back to you with the exact math on what the FX was on for the nine months.

Ralph Hamers

Ok. Hey and Anke, on your costs or investments in strategy and also to the US very specifically. So, clearly jaws are important and we will not continue to invest in areas where we don't foresee growth to come through. Right? So, but we are committed to the strategy as we laid it out and that foresees a continuation of technology investments as well. But we have not really increased our technology investments even this year, but we have been able to generate quite some room in terms of the efficiency of the technology investments through agile. So, that's where we create the room to continue technology investments that are in aligned quite some of our strategic initiatives, both in the investment bank as well as on the wealth side and P&C.

Now, more to your question. In US, clearly a change of tactic is not a change of strategy. The US is a very important region for us. It's the largest wealth pool in the world. We expect this to continue to grow over time by around 5%. That's why it is a focus of our strategy. That's why we will continue to invest there and the investments that we are making in the US are first and for all to support our financial advisors basically in what we call the personally advice segment where we need further digital enhancement in terms of supporting them in the work they do, the workstations, the processes behind fulfilling the needs of our clients.

42

It is about developing more banking products and also to deliver those digitally. And you've seen this quarter that we've been quite successful in developing additional banking products more on the savings on the deposit side. That's very important there as well, so the banking products who supports that part of our strategy in the US.

Then looking at the higher wealth segment, the family offices, to do more bespoke business there by a very good combination of what we can do from the investment bank perspective and the coverage on the wealth side, so that's also there. And then on the digital first and remote advice, it's a business that we do already. We have quite some remote advice and wealth management advice centers activities already. That's for the lower wealth band, so to say. That's where we will continue to invest as well to support that business that we have there, which has always been the idea, and that will all continue within the plans and the tech purchase that we have.

Anke Reigen, Royal Bank of Canada

Okay. Thank you very much.

Adam Terelak, Mediobanca

Good morning. Thank you very much for the questions. I had one on understanding the flows picture and then one on capital.

So, clearly, net new fee-generating assets have been very strong. I just want to understand how, kind of, the flows into money markets fits into that. You mentioned how much is being captured in asset management, but is that included within the fee-generating asset flow print in GWM? I just wanted to understand that and kind of some of the deposit moves against some of your mandated business within GWM would be great.

And then, secondly, on capital, clearly the demand for your balance sheet from your wealth clients is much lower than you may have anticipated when you put out plans early in the year. I just wanted to hear kind of an update on your thinking on balance sheet deployment against kind of the excess capital and buybacks and how that might change, given clearly there's a much lower demand for your balance sheet in the more uncertain times. Thank you.

Ralph Hamers

Well, thank you. So, on the flow side, net new fee-generating assets that is truly so that $17 billion of which more than that is actually into the mandates. So that's not the money market business of asset management. It is including the SMA business in the US. So, for example, in the US, you see actually the number is $4.4 billion of net new fee-generating assets coming through in the US, $4.9 billion of that is in SMA business. The money market business is outside of these numbers.

Adam Terelak, Mediobanca

And any color on what the flows are built into – given the uncertainty?

Ralph Hamers

Yeah. So, for the fourth quarter, you can expect some continuation, for example, in Asia Pacific but certainly also in the US on the back of a strong quarter in terms of hiring financial advisors both in the third quarter and this continuing also in the fourth quarter. You can continue – you can assume that that will support flows also in the fourth quarter.

43

Sarah Youngwood

So going to your capital questions, maybe if I lay out our capital priorities, that might be helpful. So it's – as it was maintaining a balance sheet for all seasons, including, of course, our regulatory requirements, investing in growth opportunities, offering a progressive dividend and then distributing excess capital to our shareholders. And so the – you have seen us deploy exactly like that in this year where on – you have – we have supported our clients but also you see for example this quarter, a reduction in our risk RWA and in the IB RWA, which is what we believe is the right decision to make on a risk-adjusted basis.

You have seen us, for example, reducing by 46% our LTM book and we have done that. But on the flip side, you have seen us increasing some of the lending because it was appropriate to do so and done in a cautious but absolutely open for business way in GWM or in P&C. And so those are things that we have done. And of course, all the deleveraging in Asia is affecting also the reductions in the lending.

So, we are open for business. We want to maintain this balance sheet, but that can also support supporting our clients. And in fact, our clients are seeing us as a source of strength and we have done 94% of capital return, if you take the guidance I have given you plus on the dividend for this year, and we continue to expect to have material share repurchase and a progressive dividend for next year.

Adam Terelak, Mediobanca

All right. Thank you very much.

Flora Bocahut, Jefferies

Yes. Good morning. I have two questions on the NII gain please. The first question is just to follow-up on the guidance that you provided for ‘23, where you said that we basically can consider four times the Q4 NII with upside. Is that guidance based on the group and NII or is it based on the sum of GWM plus P&C? And actually talking about these, what's driving the difference whereby, you know, the group NII is lower than the NII in GWM plus P&C? Is that because of the accounting asymmetries in the group's content? And if so, how do you expect this to evolve in the coming quarters?

And then the second question is on the loan growth outlook for 2023, specifically in the wealth management business. Because if I look at the trend, obviously, you know, there's been a slowdown in the growth, especially outside the Americas. But even in Americas, whether I look QoQ or year-on-year, it's now hardly growing anymore. So, what do you expect in terms of loan growth in Wealth Management from here, given the environment of higher rates? Thank you.

Ralph Hamers

Thank you. So, on the loan growth, clearly, as Sarah was indicating, we are open for business, and specifically the loan growth in the Wealth Management businesses is not a very high risk, prospect. It doesn't have a high risk normally. But for the moment, with markets going down, we see Lombards going down as well because they're a reflection of the underlying collateral. And therefore, you know, if markets continue to be like this or go up, you could expect some pickup, but it – I don't expect markets to really go up very fast next year. So, from that perspective, from the Lombard, I wouldn't expect too much coming through.

One could maybe see some loan growths coming through in what we call the Global Family and Institutional Wealth business. We're setting that business up, as you know, across the globe. That is a little bit more chunky. That business is larger loans as well. So this will may not be kind of a perfect trend quarter-on-quarter, but some deals may come through there, that would add to the loan portfolio in wealth.

44

And then on the mortgage side, that really depends on, yeah, on how the economies develop really. So we'll see. So, yeah, I think the summary is, overall, a subdued demand for loans. That's what you could expect next year with some more – maybe a more spiky profile in terms of the quarter development on the back of the successes in Global Family and Institutional Wealth business.

Sarah Youngwood

So in terms of your question on NII, so the – and all of the numbers we have covered were for GWM and P&C. If you look at the total group on the difference is not accounting estimates, which is in instruments at fair value, which is not in NII and but IB . And so, it's really an accounting. We reported to you when we give you Global Markets and when we give you banking, there's a component of NII and there's a component of the other fee pieces. But for you to think about it, it is much easier to think about the spread businesses in terms of NII, that's GWM and P&C. And then, the markets businesses in terms of the volatility and what we're seeing in the macroeconomic environment as well as banking based on the wallet that we are seeing. So, that's the nature of the guidance that we have given you.

Ralph Hamers

And you can track it because we report as such.

Flora Bocahut, Jefferies

Thank you.

Jeremy Sigee, BNP Paribas Exane

Thank you. I just wanted to follow up about Asia Wealth Management, please, and thank you for the comments earlier on. You talked about caution from clients in terms of their appetite for leverage and transacting. And I just wondered if you could put in context the strong net new money flows relative to that. So you know if clients are not interested in leverage or transacting, what's the nature of these flows? What's the source of strength? And is it flight to safety or capital out of China? What – sort of how would you characterize those strong net new money flows against the backdrop of caution?

And then, sort of following on from that, you talked about caution remaining at least through to the end of the year. I just wondered if you're seeing any signs of stabilization or improvement or really, we're just sitting and waiting for the time being?

Ralph Hamers

And the last question on what?

Jeremy Sigee, BNP Paribas Exane

The broader mood.

Ralph Hamers

Oh, the broader mood. Okay, thank you. So in – in the Asia flow, see the $6.6 billion, so almost $7 billion of net new fee generating assets there. It's – I mean, the real underlying trend there is that clients are seeking more guidance and therefore they are more open to do mandate business with us, moving away from their own transactional behavior. You know, the transactional business is not necessary caught by the fee generating assets. And therefore, you see the – you see clients moving to get more advice and do more mandate business with us.

45

It's – so, it's not necessarily flight to safety. It is a flight to advice and guidance in a period in which it's more about trends rather than the occasional opportunity. And that is a bit of a change of behavior that we see in our client base and we're very happy to be able to cater that as well. Over time, and certainly if things kind of bottom out or at least are more predictable in 2023, we would expect some of the transactional business on the back of the change behavior to come back in Asia as well.

Now, the overall mood, Jeremy, yeah, that's a very interesting one. I think…

Jeremy Sigee, BNP Paribas Exane

And particularly in Asia, sorry, I was meaning particularly in Asia, so whether the mood abroad to sort of confidence amongst the Asian clients because you said, you know, don't expect much improvement until the end of the year. And I just wondered sort of, are there any signs of improvement yet or is it still just too early?

Ralph Hamers

No, that's too early. Maybe to kick off has been the confirmation of Xi as the President for another five years, which at least at least gives us predictability around how policies will develop in China. We do expect, the COVID measures to be lifted over time, not very quickly because until the New Year, that may still be kind of a moment of caution because people like travelling and see families. But thereafter, we would expect some lift of measures there as well further continuation of further support of the property sector should help as well. If we're through that, we would expect some more positive signals to come through and support for the Asian economic development. And therefore we do think it will go back to 5% Asia and then specifically driven by China, as you as you know. But the timing of that is really the question.

Jeremy Sigee, BNP Paribas Exane

Okay. Thank you.

Magdalena Stoklosa, Morgan Stanley

Thank you very much. I still have question about this kind of the sources of flows, net new money flows this quarter because, of course, you know, the numbers have been very, very strong. So, can I just kind of tackle it from slightly different perspective? When you look at those flows in the third quarter, is it existing or is it new clients? Are – is there a certain level of concentration in those kind of flows across geographies? Or is it kind of much more broader based, I suppose, you know, particularly in APAC, but maybe also the underlying EMEA trends because that number was also quite strong?

And my second question is on your kind of some IB expectations because, of course, you know, fixed income trading, particularly on the macro side for the industry, for yourself have been kind of very strong over the last kind of nine months in particular. And I'm just curious, you know, how do you think that's kind of higher for a longer interest rate environment will look like for that fixed income trading into 2023 as the kind of – as the higher rates kind of settle in and the volatility potentially comes down a little bit?

And also, you know, I've heard you this morning kind of talking about Advisory unlikely to return in the fourth quarter, but how do you think about your Advisory business into next year because, of course, mix-wise, it's very important for you? Thanks very much.

46

Ralph Hamers

Magdalena, there's a whole slate of questions right there. Okay. I'll try to make a beginning here. So on the flows, it's literally a combination of existing clients being more interested in and doing many business with us. Specifically in Asia, that's where we see that change. And EMEA and in the US, the US particularly driven through the success of our as SMA business as well. And EMEA is also new clients are coming on. And Asia, by the way, is also new clients coming on. So, it's a bit of a mix bag. This is about net new fee-generating assets, by the way, margin, not net new money. Right?

So, we do separate those two concepts. And because net new money may not be net new fee-generating assets or the other way around. So, I want to kind of caution that we really stick to our definition of net new fee-generating assets, which basically means it is about assets that we manage on behalf of our clients where there is inflow coming through, new money coming into a mandate or dividends being paid within the mandate and staying within the mandate. That's the way these assets grow, and that's important.

Then on the fixed income business, specifically more on the FX business, that's basically where we really profit. Clearly, we – in the second quarter, we already indicated the shift from the market and specifically for our franchise, an important shift from what we would call micro which is more the equities business that we are really, really leading in globally as well as you know, to more the macro, which is the fixed income in a rates business that we have a very high exposure, we have a very strong position in the foreign exchange business. And that's where we have profited from our institutional clients being very active on the back end of the volatility there.

Now, these rates will continue. They will have their effect on FX as well. So, the combination of that and with that, the resources that we have moved from the equities business and the some of the leverage we use for that business, depending on how the market develops, we will continue to profit from it. And where the market is going, honestly, I don't know. I really don't know Magda on that one.

And then, on the banking business, more on the capital markets business. Yes. What I said this morning was more that, given where the market currently is, the volatility in the market, the fact that there is a bit of a risk of behavior on the investor side that with six or seven weeks to go in this year because basically you should – I mean, we have – we probably have the first week of December, but thereafter, markets are normally closed anyway. So we have six more weeks. I don't think that business will perform well. The markets are just not there. And in the next year, I think it will take quite some time for the confidence to come back in the market. That's one.

And then, there will be investor appetite. But then, you still need also the ones who need the capital or want to sell their business from that perspective to be able to accept the fact that it will go at lower valuations because the high valuations are still fresh in their mind. And so, it may take some time as well before they have turned the corner around accepting lower valuations for the Capital Markets business. So, and once there, yeah, you will probably see the supply and demand coming back and getting a better market situation. But, yeah, so I would be surprised that going into the first quarter, that the first quarter would be good there, I don't think so.

Magdalena Stoklosa, Morgan Stanley

Thank you very much.

47

Kian Abouhossein, JPMorgan

Thanks for taking my question. Two questions. One is on cost just coming back to the numbers. I'm just thinking 2023, I recall under Kirt, the guidance was that the cost growth of 2% plus, minus variable in 2023 should not be too different. And I was wondering, can you reconfirm that clearly things have changed in terms of inflation, outlook, et cetera? Does that kind of indication still hold, first of all?

And then the second question is on cost income target of 70% to 73% that you're clearly making this here. Can you run me through your kind of stress scenario since you have a lot of mark-to-market revenues? How you think about the offsets that you can take in order to bring yourself back towards that level or even close to that level so we can understand how the dynamic would work on your controlling the cost?

Ralph Hamers

Sarah?

Sarah Youngwood

So first of all, in terms of how we think about expense our primary lens is cost income ratio.And we are currently in our planning phase for 2023 and you can be assured that we are intently focused on being within our targets and we are looking at that in different scenarios.

And to your point, we actually are looking at actions that we would take if the environment deteriorated significantly from where it is today. So, we mentioned, for example, that we're executing this billion-dollar growth expense save that we are on track for the $400 million that we had planned for this year. We've executed the $200 million of last year. There is $400 million that is planned for next year. Those saves can be reinvested and that's what we have done so far but we don't have to. That's one on of the levers, for example, Ralph and I both talked about on the levers that we are already taking, the non-critical hires, the T&E, consulting, making sure that our prioritization is very intentional for the tech investments that we're doing already. And then, if we need to do more, as we said, we will. But if we do it too early, there is an optionality cost to that.

Kian Abouhossein, JPMorgan

And just on – should we think about the times of absolute cost guidance is not relevant anymore? We should think from now on, going into 2023 around cost income targets?

A: The primary lens is definitely cost income target. Once we give you the guidance, if we think that there is anything complementary that would be useful. We will. And you see, for example, that this quarter we are giving you a guidance to make sure that you can be helped as you prepare the fourth quarter.

Kian Abouhossein, JPMorgan

All right. Thank you.

Piers Brown, HSBC

Yeah. Good morning, everybody. I've just got two questions. First off, on the US Wealth strategy, so you said you're still investing in tech platforms and new client segments. And given that Wwealthfront is not proceeding but we've seen a very significant pullback across tech valuations, how are you thinking currently about opportunities to expand via M&A going forward?

48

And the second question is just on a topic which came up on the 2Q call and I see you've highlighted again in the outlook statement of 3Q report but the change to Swiss liquidity requirements, which I think became effective in July. Have you got any better clarity in terms of how that may impact the P&L as you move into next year? Thank you.

Ralph Hamers

Yeah. Thank you. So, Piers, so on the Wealth business in the US, it – so, we were never really looking at getting into new segments per se. Right? So, we have a lot of clients in what we would call lower wealth bands, $250,000 to $1 million and $2 million. That's one. We have 2 million clients in Workplace Wealth. Those are segments that we already cater for, for which we feel that we have to be more efficient in terms of how we deliver our services but also that we need to have a service to keep those invested assets with us.

Clearly, over time, if you have an appealing digital offer in view of the generational transfer of wealth from even wealthier customers to their – to the next generation, you should also be able to keep that in-house. So, it's not necessary that we're looking for new wealth segments. This is about the segments that we're already in and making sure that we have the right offer for those segments as well.

Now, even on the personally advised, which is the core of our business there, we need quite a lot of technology investments in order to support them in the way they advise their clients, their workstations, the back office, the banking business that we're developing is a lot of technology investments as well. So across the different segments that we cater for, we will continue to have high technology investments in the US in order to get better productivity and a better user experience.

Sarah Youngwood

On the liquidity ordinance, so as you know, it became effective in July 2022 and there is a transition period of 18 months. And the way I think about it is if you look at our current level of liquidity, they are very high. And so, when you think about the change in the minimum liquidity requirements, that will be from – not from the levels of cushions that we have today. So, we have this level of excess liquidity. And therefore, when you think about the balance of the two, we don't think that it should have a material impact on our profitability. And we're certainly in discussions to continue to make sure that we get the full clarity on the second phase of the implementation.

Piers Brown, HSBC

Great. Thank you very much.

Nicolas Payen, Kepler Cheuvreux

Yes. Good morning. I have two questions please. The first one is on RWA. I wanted to know if we should expect any regulatory inflation for Q4 this year and maybe also into next year?

And the second one is coming back on your staff increase client advisor in Americas and I would like to know whether or not this the trend will continue in Americas especially in other region? And if you have already witnessed some flows coming from this advisory in America? Thank you very much.

49

Sarah Youngwood

So, on the regulatory cost inflation, we have all of that embedded in the numbers that we are giving to you. And so, there is always additional things to do. And we are reflecting that in our cost base, but we are not pointing to specific growth in that regard. Of course, all the critical hires that are necessary for that, we always prioritize.

In terms of the growth in the FAs, we did have a strong recruiting quarter, which Ralph pointed out. And we also have a pipeline which Ralph also talked about and we are not being more specific about what level it might be going forward, but this was a very good recruiting quarter.

Nicolas Payen, Kepler Cheuvreux

Thank you.

Andrew Coombs, Citi

Good morning. Two questions please. Firstly on the NII sensitivity in your prepared remarks, you talked about the deposit beta being better than expected but at the same time you've seen quite a significant offset from a mix shift in a deposit base. So perhaps, you could elaborate on your expectations on the impact to deposit mix shift going forward into 2023, and how much of an offset that might provide?

And then my second question, which is on the net new fee generating assets. The demand you're seeing both in asset management and wealth management. You talked about an increase in demand for CDs and money market products following the move up in rates and the additional yield that's providing. Are you seeing a mix shift within the existing client base, as well, into the lower margin products and as you can say on the average fee margin on those assets, the broader asset base would be helpful as well? Thank you.

Sarah Youngwood

So if you look at on the charts that we gave, you see the proportions for this year and that was related to US dollars. And in US dollar, we have gone very fast, very high and therefore, you have seen across the industry a fair bit of both volume and mix impact. So that's a normal phenomenon. To the extent that the rate curves in Europe are less fast, then you would be at a different point there. And then, we also have our very strong P&C business, which is a different type of business in terms of having all of the cash flow accounts of our clients.

In terms of retention, I talked about all of the assets we are staying on our platform and also – so this is sweeps and the accounts that are going into other products. And it's exactly what you said in terms of going into deposit products that are priced attractively. And for that, we got 60% retention, and then, another 25% in our own money market funds. And then, on the rest is going to be things like, for example, Treasury, which has also been interesting in the US.

Ralph Hamers

I think the core message here is that it's been a particularly strong quarter as to how we have dealt with this sensitivity of clients around rates and how they're looking at it. We have been really able to manage this, keep the money within the UBS business lines, so to say. Between what we would do within the bank in terms of deposits or as invested assets in Treasuries or money markets, and then the money market specifically on the asset management side.

So, I think, the team did a fabulous job keeping it in, in the house with a – approach to ensure to maximize profitability around that as well. So – and given the fact that we have all of these options and that we are so close to our clients, that's why we can do this. So, a job really well done.

50

Andrew Coombs, Citi

And I think it's your retention, but what does it imply in terms of margin mix shift?

Sarah Youngwood

We're not sharing that type of information at this point.

Andrew Coombs, Citi

Okay. Thank you.

Andrew Lim, Société Générale

Hi. Morning. Thanks for taking my questions. So the first one just point of clarification on the NII for 2023. So you gave that prior guidance of 4Q annualized with a bit of upside. Is that on a static balance sheet basis or is that actual guidance, which takes in account deposit outflows and mix shifts and so forth?

And then secondly, on your buybacks, you've guided $5.5 billion for the full year. So that marks a bit of a slowdown on the quarterly run rate for buybacks despite your CET1 ratio inching higher this quarter. I'm just wondering why maybe you you are slowing that down a bit. And then looking towards 2023, you're still sitting on a lot of excess capital. I'm wondering whether you would consider having a payout ratio of above 100% to try and bring that down a bit. Thank you.

Sarah Youngwood

And so on the guidance that we have, given all of the guidance that we have given, both the fourth quarter guidance as well as the indication, directional, for 2023, all of that was guidance. It was not on a static balance sheet.

In terms of the buybacks, it's simply what happens at that time of the year in terms of the liquidity in the market and also, obviously, it's based on the level of our stock price. So our stock price went up, there might be more, but the guidance we have given is based on our current stock price and the liquidity expected. Remember that December is going to have lower liquidity than another month. In terms of 2023, we expect to have material share repurchase, but we are not being more specific about the levels.

Andrew Lim, Société Générale

That's great. Thank you.

Benjamin Goy, Deutsche Bank

Hi. Good morning. Two questions, please. The first one also on interest rate sensitivity, given the Swiss franc or Swiss rates are the now the major driver. I was wondering about the deposit beta you're assuming the CHF 700 million that is stated in the sensitivity guidance, in particular, thinking about that deposit beta was better in the US and Europe's Swiss deposits are still growing.

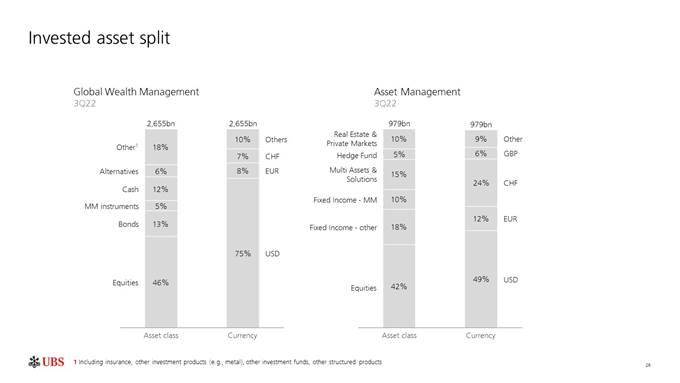

And then secondly, thank you for slide 26 on 12% of your clients cash is invested in – of client asset invested in cash and another 5% in money market product. So, I'm just wondering how this looks like, let's say early in the year and what put you to change it or are there any major change is expected from here? Thank you.

51

Sarah Youngwood

So on the interest rate sensitivity and the beta that you can expect in Europe. The first thing to say is that, betas typically become higher as you go up the curve. And so, in the US, we are towards higher point in a curve and we went there extraordinarily quickly. What is expected in Switzerland and in the rest of Europe is something that is much more measured and therefore we are at a lower point in that curve. And so, that should be combined also with the fact that it is always a weighted average of our products. And we do have in Swiss franc also the retail bank that has lower beta products.

And then in terms of the composition, we thought it would be helpful. So thanks for appreciating it. As you try to think about the impacts of the different markets on our invested assets, both in GWM and in AM and I think that those are things that don't evolve particularly quickly.

So, I think it's a good place for you to start.

Benjamin Goy, Deutsche Bank

Understood. Thank you.

Jon Peace, Credit Suisse

Yeah. Thank you. I'm sorry to have one more on rate sensitivity, but just looking for a – still, a little bit of help in sizing the 2023 benefits. You do offer the guidance at 100 basis point higher rates will add $0.7 billion on the franc curve and $0.2 billion on the euro curve. But do you think those could be substantially offset by deposit beta or mix effects? Because I see consensus has basically about a $200 million uplift on the Q4 run rate, and we might come to a higher number if we use that that sensitivity.

And then, second question on the buyback for next year, appreciate that you probably won't give us a number until the full year. But just could you help us understand the process you go through in Q4 in sizing that buyback? Is it a backward looking look at how far your CET1 is above your management targets and you pay that out or is it a desire to maintain a higher buffer and then it's based on a forward look on earnings with payout of perhaps 100%? Thanks.

Ralph Hamers

Yeah. Yeah, thank you, Jon. So on NII let's not go into further details. The guidance is the guidance, right? And that's why we give it and that's where we want to keep it as well.

Then, on your questions around the 2023 buyback, we go through this every year. And looking at what is the starting capital position going into the year? What are our expectations as to making sure that we have a balance sheet to get through more challenging times? What kind of growth do we expect in the business? And on the back of that, how can we then manage our capital? And in the end, we manage our capital to around the 13% CET1. So that's the way you can think about it. And whether we can kind of generate – if we generate more capital and use less for our growth, clearly that will lead to a higher payout or buyback. So, those are the components that we would look at.

The point is we have a highly capital-generative model. We have a low capital intensive model to generate our income, and we have a buffer to the 13% that we want to manage to.

Jon Peace, Credit Suisse

Thank you.

52

Sarah Youngwood

And maybe before we close, I can just answer a question that came earlier, which was the nine months year-on-year revenue ex-FX, the number is plus 2%.

Ralph Hamers

Okay. Thank you. In the absence of any further questions, I'd like to thank you all for being here at this early morning. As indicated, given the market backdrop, I think we delivered a good quarter – a good quarter both in terms of staying close to our clients and the flows that are coming through, both in the wealth manager as well as the asset manager with $18 billion of net new money coming through on the asset manager. You see that both on the institutional side as well as the wealth side.

We do provide for the right products and services and advisory to our clients. And these, while challenging circumstances reclined, do need guidance. And on the other side, it shows the flexibility of our investment bank in terms of the allocation of resources to move quickly from a market that is more micro related to market, is more macro driven and being able to profit from that as well with an increase in our FRC revenues to 64% and P&C doing well over time, a very stable business growing both on the lending side as well as on the deposit side. So, also there very much client-focused and client-driven business on the back of that, delivering $1.7 billion of net profit.

Thank you very much and see you next quarter.

53

Cautionary Statement Regarding Forward-Looking Statements | This document contains statements that constitute “forward-looking statements,” including but not limited to management’s outlook for UBS’s financial performance, statements relating to the anticipated effect of transactions and strategic initiatives on UBS’s business and future development and goals or intentions to achieve climate, sustainability and other social objectives. While these forward-looking statements represent UBS’s judgments, expectations and objectives concerning the matters described, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from UBS’s expectations. Russia’s invasion of Ukraine has led to heightened volatility across global markets, to the coordinated implementation of sanctions on Russia and Belarus, Russian and Belarusian entities and nationals, and to heightened political tensions across the globe. In addition, the war has caused significant population displacement, and if the conflict continues, the scale of disruption will increase and may come to include wide-scale shortages of vital commodities, including causing energy shortages and food insecurity. The speed of implementation and extent of sanctions, as well as the uncertainty as to how the situation will develop, may have significant adverse effects on the market and macroeconomic conditions, including in ways that cannot be anticipated. This creates significantly greater uncertainty about forward-looking statements. Other factors that may affect our performance and ability to achieve our plans, outlook and other objectives also include, but are not limited to: (i) the degree to which UBS is successful in the ongoing execution of its strategic plans, including its cost reduction and efficiency initiatives and its ability to manage its levels of risk-weighted assets (RWA) and leverage ratio denominator (LRD), liquidity coverage ratio and other financial resources, including changes in RWA assets and liabilities arising from higher market volatility; (ii) the degree to which UBS is successful in implementing changes to its businesses to meet changing market, regulatory and other conditions; (iii) increased interest rate volatility in major markets; (iv) developments in the macroeconomic climate and in the markets in which UBS operates or to which it is exposed, including movements in securities prices or liquidity, credit spreads, and currency exchange rates, the effects of economic conditions, including increasing inflationary pressures, market developments, and increasing geopolitical tensions, and changes to national trade policies on the financial position or creditworthiness of UBS’s clients and counterparties, as well as on client sentiment and levels of activity, including the COVID-19 pandemic and the measures taken to manage it, which have had and may also continue to have a significant adverse effect on global and regional economic activity, including disruptions to global supply chains and labor market displacements; (v) changes in the availability of capital and funding, including any changes in UBS’s credit spreads and ratings, as well as availability and cost of funding to meet requirements for debt eligible for total loss-absorbing capacity (TLAC); (vi) changes in central bank policies or the implementation of financial legislation and regulation in Switzerland, the US, the UK, the European Union and other financial centers that have imposed, or resulted in, or may do so in the future, more stringent or entity-specific capital, TLAC, leverage ratio, net stable funding ratio, liquidity and funding requirements, heightened operational resilience requirements, incremental tax requirements, additional levies, limitations on permitted activities, constraints on remuneration, constraints on transfers of capital and liquidity and sharing of operational costs across the Group or other measures, and the effect these will or would have on UBS’s business activities; (vii) UBS’s ability to successfully implement resolvability and related regulatory requirements and the potential need to make further changes to the legal structure or booking model of UBS Group in response to legal and regulatory requirements, or other external developments; (viii) UBS’s ability to maintain and improve its systems and controls for complying with sanctions in a timely manner and for the detection and prevention of money laundering to meet evolving regulatory requirements and expectations, in particular in current geopolitical turmoil; (ix) the uncertainty arising from domestic stresses in certain major economies; (x) changes in UBS’s competitive position, including whether differences in regulatory capital and other requirements among the major financial centers adversely affect UBS’s ability to compete in certain lines of business; (xi) changes in the standards of conduct applicable to our businesses that may result from new regulations or new enforcement of existing standards, including measures to impose new and enhanced duties when interacting with customers and in the execution and handling of customer transactions; (xii) the liability to which UBS may be exposed, or possible constraints or sanctions that regulatory authorities might impose on UBS, due to litigation, contractual claims and regulatory investigations, including the potential for disqualification from certain businesses, potentially large fines or monetary penalties, or the loss of licenses or privileges as a result of regulatory or other governmental sanctions, as well as the effect that litigation, regulatory and similar matters have on the operational risk component of our RWA, as well as the amount of capital available for return to shareholders; (xiii) the effects on UBS’s business, in particular cross-border banking, of sanctions, tax or regulatory developments and of possible changes in UBS’s policies and practices; (xiv) UBS’s ability to retain and attract the employees necessary to generate revenues and to manage, support and control its businesses, which may be affected by competitive factors; (xv) changes in accounting or tax standards or policies, and determinations or interpretations affecting the recognition of gain or loss, the valuation of goodwill, the recognition of deferred tax assets and other matters; (xvi) UBS’s ability to implement new technologies and business methods, including digital services and technologies, and ability to successfully compete with both existing and new financial service providers, some of which may not be regulated to the same extent; (xvii) limitations on the effectiveness of UBS’s internal processes for risk management, risk control, measurement and modeling, and of financial models generally; (xviii) the occurrence of operational failures, such as fraud, misconduct, unauthorized trading, financial crime, cyberattacks, data leakage and systems failures, the risk of which is increased with cyberattack threats from nation states; (xix) restrictions on the ability of UBS Group AG to make payments or distributions, including due to restrictions on the ability of its subsidiaries to make loans or distributions, directly or indirectly, or, in the case of financial difficulties, due to the exercise by FINMA or the regulators of UBS’s operations in other countries of their broad statutory powers in relation to protective measures, restructuring and liquidation proceedings; (xx) the degree to which changes in regulation, capital or legal structure, financial results or other factors may affect UBS’s ability to maintain its stated capital return objective; (xxi) uncertainty over the scope of actions that may be required by UBS, governments and others to achieve goals relating to climate, environmental and social matters, as well as the evolving nature of underlying science and industry and the possibility of conflict between different governmental standards and regulatory regimes; and (xxii) the effect that these or other factors or unanticipated events may have on our reputation and the additional consequences that this may have on our business and performance. The sequence in which the factors above are presented is not indicative of their likelihood of occurrence or the potential magnitude of their consequences. Our business and financial performance could be affected by other factors identified in our past and future filings and reports, including those filed with the US Securities and Exchange Commission (the SEC). More detailed information about those factors is set forth in documents furnished by UBS and filings made by UBS with the SEC, including UBS’s Annual Report on Form 20-F for the year ended 31 December 2021. UBS is not under any obligation to (and expressly disclaims any obligation to) update or alter its forward-looking statements, whether as a result of new information, future events, or otherwise.

54

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrants have duly caused this report to be signed on their behalf by the undersigned, thereunto duly authorized.

UBS Group AG

By: _/s/ David Kelly_______________

Name: David Kelly

Title: Managing Director

By: _/s/ Ella Campi________________

Name: Ella Campi

Title: Executive Director

UBS AG

By: _/s/ David Kelly_______________

Name: David Kelly

Title: Managing Director

By: _/s/ Ella Campi________________

Name: Ella Campi

Title: Executive Director

Date: October 25, 2022