As filed with the Securities and Exchange Commission on December 31, 2024

Registration No. 333-282351

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM F-4

REGISTRATION STATEMENT

Under

The Securities Act of 1933

SciSparc Ltd.

(Exact name of Registrant as specified in its charter)

| State of Israel | | 2834 | | Not Applicable |

(State or Other Jurisdiction of

Incorporation or Organization) | | (Primary Standard Industrial

Classification Code Number) | | (I.R.S. Employer

Identification Number) |

20 Raul Wallenberg Street, Tower A,

Tel Aviv 6971916 Israel

Tel: (+972) (3) 717-5777

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Puglisi & Associates

850 Library Ave., Suite 204

Newark, DE 19711

Tel: (302) 738-6680

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Please send copies of all communications to:

Shachar Hadar, Adv.

Matthew Rudolph, Adv.

Meitar | Law Offices

16 Abba Hillel Silver Rd.

Ramat Gan 52506, Israel

Tel: (+972) (3) 610-3100 | | Oded Har-Even, Esq.

Howard Berkenblit, Esq.

Sullivan & Worcester LLP

1251 Avenue of the Americas

New York, NY 10020

Tel: (212) 660-3000 | | David Huberman, Esq.

Greenberg Traurig, P.A.

One Azrieli Center

Round Tower, 30th floor

132 Menachem Begin Rd

Tel Aviv 6701101

Telephone: 312.364.1633 | | Gregory Irgo, Adv.

Ido Zaborof, Adv.

Lipa Meir & Co.,

Advocates

2 Weizmann St.,

Tel Aviv 6423902, Israel

Tel: (+972) (3) 607 0603 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effectiveness of this registration statement and the satisfaction or waiver of all other conditions under the Merger Agreement described herein.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this proxy statement/prospectus is not complete and may be changed. SciSparc may not sell its securities pursuant to the proposed transactions until the Registration Statement filed with the Securities and Exchange Commission is effective. This proxy statement/prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state or other jurisdiction where the offer or sale is not permitted.

Preliminary Proxy/Statement - Subject to completion, dated [●], 2024

PROPOSED MERGER

YOUR VOTE IS VERY IMPORTANT

To the Shareholders of SciSparc Ltd.:

You are cordially invited to attend a special meeting of the shareholders of SciSparc Ltd., or SciSparc, an Israeli limited company, which we refer to as “we,” “SciSparc,” or the “Company,” which will be held at , local time, on , 2025, at , unless postponed or adjourned to a later date. This is an important meeting that affects your investment in SciSparc.

On April 10, 2024, SciSparc and AutoMax Motors Ltd., an Israeli limited company, or AutoMax, entered into an Agreement and Plan of Merger as amended on August 14, 2024, or the Merger Agreement, pursuant to which SciSparc Merger Sub Ltd., an Israeli limited company and wholly-owned subsidiary of SciSparc, or Merger Sub, will merge with and into AutoMax, with AutoMax surviving as a wholly-owned subsidiary of SciSparc. Ordinary Shares, as well as pre-funded warrants exercisable into ordinary shares, of SciSparc will be issued to AutoMax’s shareholders at the effective time of such merger, or the Merger. The final exchange ratio, or the Exchange Ratio, has been determined pursuant to a formula described in more detail in the Merger Agreement and later in this proxy statement/prospectus. Under the Exchange Ratio formula described in the Merger Agreement, immediately following the Merger, AutoMax’s shareholders, and M.R.M Merhavit Holding & Management Ltd, or the Advisor, in connection with the Merger, are expected to own approximately 49.99% of SciSparc’s share capital, on a fully-diluted basis, subject to certain exceptions, and as further defined in the Merger Agreement, and SciSparc’s shareholders are expected to own approximately 50.01% of SciSparc’s share capital, on a fully-diluted basis, subject to certain exceptions. The Merger has been unanimously approved by the boards of directors of both companies and will be presented for approval by the shareholders of AutoMax. On August 14, 2024, the parties entered into an addendum to the Merger Agreement, or the Merger Agreement Addendum, pursuant to which the right to terminate the Merger Agreement if the Merger was not consummated by August 30, 2024, was deferred to November 30, 2024. On November 26, 2024, the parties entered into a second addendum to the Merger Agreement, or the Merger Agreement Second Addendum, pursuant to which the right to terminate the Merger Agreement, if the Merger was not consummated by November 30, 2024, was deferred to March 31, 2025. The Merger is expected to close in the first quarter of 2025, subject to the approval of SciSparc’s shareholders, approval of the AutoMax shareholders, including a separate approval by AutoMax shareholders who are not controlling shareholders of AutoMax or SciSparc, and court approval (as further detailed under “Regulatory Approvals”), as well as other customary conditions.

Upon the effective time of the Merger, the officers of SciSparc will include Mr. Oz Adler, Chief Executive Officer and Chief Financial Officer and Dr. Adi Zuloff-Shani, Chief Technology Officer. In addition, each of Mr. Alon Dayan, Mr. Lior Vider and Mr. Itschak Shrem will resign from SciSparc’s board of directors upon the effective time of the Merger. In accordance with the Merger Agreement and subject to the approval by the SciSparc shareholders of Proposal No. 1 at the Special Meeting and immediately upon the resignation of Mr. Dayan and Mr. Vider from SciSparc’s board of directors in accordance with the terms of the Merger Agreement, AutoMax’s designees to SciSparc’s board of directors will be assigned to two separate classes, whereby one such designee will be assigned to Class I with a term of office expiring at the annual general meeting of SciSparc to be held in 2027 and the other such designee will be assigned to Class III with a term of office expiring at the annual general meeting of SciSparc to be held in 2026.

SciSparc’s ordinary shares are currently listed on the Nasdaq Capital Market under the symbol “SPRC.” Prior to consummation of the Merger, SciSparc intends to file an additional listing application with Nasdaq, as required by Nasdaq to effect the additional listing of SciSparc’s ordinary shares issuable in connection with the Merger. After completion of the Merger, SciSparc will continue to trade on the Nasdaq Capital Market under SciSparc’s existing name, SciSparc Ltd., and existing trading symbol, “SPRC”. The closing price of SciSparc’s ordinary shares on Nasdaq as of December 30, 2024, the latest practicable date before the date of this prospectus, was $0.466.

SciSparc is holding a special meeting of shareholders, or the Special Meeting, for the following purposes, as more fully described in the accompanying proxy statement:

1. To approve the consummation of the Merger and the other transactions contemplated by the Merger Agreement, including the issuance of SciSparc ordinary shares and the pre-funded warrants at the effective time of the Merger to the shareholders of AutoMax;

2. To approve the form of indemnification agreement for directors and officers of SciSparc, attached as Annex C to this proxy statement/prospectus, or the Indemnification Agreement, effective upon the effective time of the Merger, and to authorize the execution and delivery of such Indemnification Agreement with all office holders of SciSparc to be in office immediately following the effective time of the Merger or thereafter elected or appointed to the board of directors of SciSparc; and

3. To approve a one-time cash bonus to SciSparc’s Chief Executive Officer, chairman of the board of directors, or Chairman, and President, contingent upon the approval and the closing of the Merger.

4. Subject to and contingent upon the approval of Proposal No. 1, to elect each of Tomer Levy and Yaarah Alfi to serve on the SciSparc board of directors upon the effective time of the Merger and to ratify the class structure of the SciSparc board of directors.

We know of no other matters to be submitted at the Special Meeting other than as specified herein. If any other business is properly brought before the Special Meeting, the persons named as proxies may vote in respect thereof in accordance with their best judgment.

After careful consideration, SciSparc’s board of directors has determined that the Merger is fair to and in the best interests of SciSparc and its shareholders, has approved the Merger Agreement, the Merger, the issuance of ordinary shares and the pre-funded warrants of SciSparc to AutoMax’s shareholders pursuant to the terms of the Merger Agreement, the approval of form of Indemnification Agreement, the approval of a one-time cash bonus to SciSparc’s Chief Executive Officer, Chairman and President, contingent upon the approval and the closing of the Merger, the appointment of each of Tomer Levy and Yaarah Alfi to serve on the SciSparc board of directors upon of the effective time of the Merger, the ratification of the class structure of the SciSparc board of directors, and the other actions contemplated by the Merger Agreement, and has determined to recommend that the SciSparc shareholders vote to approve each of the proposals set forth in this proxy statement/prospectus. Accordingly, SciSparc’s board of directors unanimously recommends that the SciSparc shareholders vote FOR each of the Proposals Nos. 1 through 4 described above.

Your vote is very important, regardless of the number of shares you own. Whether or not you expect to attend the Special Meeting in person, please complete, date, sign and promptly return the accompanying proxy card in the enclosed postage paid envelope to ensure that your shares will be represented and voted at the Special Meeting.

More information about SciSparc, AutoMax and the proposed transactions is contained in this proxy statement/prospectus. SciSparc urges you to read this proxy statement/prospectus carefully and in its entirety. IN PARTICULAR, YOU SHOULD CAREFULLY CONSIDER THE MATTERS DISCUSSED UNDER “RISK FACTORS” BEGINNING ON PAGE 11.

SciSparc is excited about the opportunities the Merger brings to its shareholders, and thanks you for your consideration and continued support.

| | Sincerely, |

| | |

| | |

| | Amitay Weiss |

| | Chairman of the Board |

None of the Securities and Exchange Commission, the Israel Securities Authority or any state securities commission has approved or disapproved the Merger described in this proxy statement/prospectus or the SciSparc ordinary shares and pre-funded warrants to be issued in connection with the Merger or passed upon the adequacy or accuracy of this proxy statement/prospectus. Any representation to the contrary is a criminal offense.

The accompanying proxy statement is dated , 2025, and is first being mailed to SciSparc shareholders on or about , 2025.

PRELIMINARY PROXY STATEMENT, SUBJECT TO COMPLETION

SCISPARC LTD.

20 RAUL WALLENBERG ST.

TOWER A, 2ND FLOOR

TEL AVIV 6971916 ISRAEL

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON , 2025

Dear Shareholders of SciSparc Ltd.:

You are cordially invited to attend the Special Meeting of the shareholders of SciSparc Ltd., or SciSparc, to be held at , local time, on , 2025, at , for the following purposes:

1. To approve the consummation of the Merger and the other transactions contemplated by the Merger Agreement, including the issuance of SciSparc ordinary shares and the pre-funded warrants at the effective time of the Merger to the shareholders of AutoMax;

2. To approve the form of Indemnification Agreement for directors and officers of SciSparc, attached as Annex C to this proxy statement/prospectus, upon the effective time of the Merger, and to authorize the execution and delivery of such Indemnification Agreement with all office holders of SciSparc to be in office immediately following the effective time of the Merger or thereafter elected or appointed to the board of directors of SciSparc; and

3. To approve a one-time cash bonus to SciSparc’s Chief Executive Officer, Chairman and President, contingent upon the approval and the closing of the Merger.

4. Subject to and contingent upon the approval of Proposal No. 1, to elect each of Tomer Levy and Yaarah Alfi to serve on the SciSparc board of directors upon the effective time of the Merger and to ratify the class structure of the SciSparc board of directors.

We know of no other matters to be submitted at the Special Meeting other than as specified herein. If any other business is properly brought before the Special Meeting, the persons named as proxies may vote in respect thereof in accordance with their best judgment.

Under Israeli law, one or more shareholders holding at least 1% of the voting rights at the Special Meeting of the shareholders may request that the board of directors include a matter in the agenda of a Special Meeting of the shareholders to be convened in the future, provided that it is appropriate to discuss such a matter at the Special Meeting. Notwithstanding the foregoing, as a company listed on an exchange outside of Israel, a matter relating to the appointment or removal of a director may only be requested by one or more shareholders holding at least 5% of the voting rights at the Special Meeting of the shareholders. SciSparc’s Amended and Restated Articles of Association contain procedural guidelines and disclosure items with respect to the submission of shareholder proposals for special meetings.

The board of directors of SciSparc has fixed , 2025 as the record date for the determination of shareholders entitled to notice of, and to vote at, the Special Meeting and any adjournment or postponement thereof. Only holders of record of ordinary shares of SciSparc at the close of business on the record date are entitled to notice of, and to vote at, the Special Meeting. At the close of business on the record date, SciSparc had ordinary shares outstanding and entitled to vote.

Your vote is important. The affirmative vote of a simple majority of shareholders present (in person or by proxy) and voting (not including abstentions) is required for approval of Proposals Nos. 1, and 4. The approval of each of Proposals Nos. 2, and 3, require the affirmative vote of a simple majority, plus either (i) a simple majority of shares voted at the Special Meeting, excluding the shares of controlling shareholders, if any, and of shareholders who have a personal interest in the approval of the resolution (each, an “Interested Shareholder”), or (ii) the total number of shares of non-controlling shareholders and of shareholders who do not have a personal interest in the resolution voting against approval of the resolution does not exceed two percent (2%) of the outstanding voting power in SciSparc. We encourage you to read this proxy statement/prospectus carefully. If you have any questions or need assistance voting your shares, please contact our Chief Executive Officer:

Oz Adler

20 Raul Wallenberg St., Tower A, 2nd Floor,

Tel Aviv Israel, 6971916

+972-3-7175777

Even if you plan to attend the Special Meeting in person, SciSparc requests that you sign and return the enclosed proxy card or grant your proxy by telephone or through the Internet to ensure that your shares will be represented at the Special Meeting if you are unable to attend.

| | By Order of the Board of Directors of |

| | SciSparc Ltd. |

| | |

| | |

| | Amitay Weiss |

| | Chairman of the Board |

| | Tel-Aviv, Israel |

| | , 2025 |

THE SCISPARC BOARD OF DIRECTORS HAS DETERMINED AND BELIEVES THAT EACH OF THE PROPOSALS OUTLINED ABOVE IS ADVISABLE TO, AND IN THE BEST INTERESTS OF, SCISPARC AND ITS SHAREHOLDERS AND HAS APPROVED EACH SUCH PROPOSAL. THE SCISPARC BOARD OF DIRECTORS RECOMMENDS THAT SCISPARC SHAREHOLDERS VOTE “FOR” EACH SUCH PROPOSAL.

REFERENCES TO ADDITIONAL INFORMATION

This proxy statement/prospectus incorporates important business and financial information about SciSparc that is not included in or delivered with this document. You may obtain this information without charge through the Securities and Exchange Commission, or the SEC, website (www.sec.gov) or upon your written or oral request by contacting the Chief Financial Officer of SciSparc Ltd., at 20 Raul Wallenberg St., Tower A, 2nd Floor, Tel Aviv Israel, 6971916, or by calling +972-3-7175777.

To facilitate timely delivery of these documents, any request should be made no later than , 2025 to receive them before the Special Meeting.

For additional details about where you can find information about SciSparc, please see the section entitled “Where You Can Find More Information” in this proxy statement/prospectus.

ABOUT THIS DOCUMENT

SciSparc Ltd., which we refer to herein as the “Company,” “SciSparc,” “we,” “our,” or “us,” is providing these proxy materials in connection with the solicitation by our board of directors of proxies to be voted at a Special Meeting of our shareholders to be held on , 2025, commencing at , local time, at , or at any adjournment or postponement thereof. This proxy statement/prospectus and the enclosed proxy card will be mailed to each shareholder entitled to notice of, and to vote at, the Special Meeting of shareholders commencing on or about , 2025.

You are cautioned not to rely on any information other than the information contained in or incorporated by reference into this proxy statement/prospectus. No one has been authorized to provide you with information that is different from that contained in or incorporated by reference into this proxy statement/prospectus. This proxy statement/prospectus is dated , 2025. You should not assume that the information contained in this proxy statement/prospectus is accurate as of any other date, nor should you assume that the information incorporated by reference into this proxy statement/prospectus is accurate as of any date other than the date of such incorporated document. The mailing of this proxy statement/prospectus to our shareholders will not create any implication to the contrary.

This proxy statement/prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any securities, or the solicitation of a proxy, in any jurisdiction in which or from any person to whom it is unlawful to make any such offer or solicitation in such jurisdiction.

TABLE OF CONTENTS

QUESTIONS AND ANSWERS ABOUT THE SPECIAL MEETING AND THE MERGER

The following section provides answers to frequently asked questions about the Merger and other matters relating to the Special Meeting. This section, however, provides only summary information. For a more complete response to these questions and for additional information, please refer to the cross-referenced sections. SciSparc urges its shareholders to read this document in its entirety prior to making any decision.

What is the Merger?

On April 10, 2024, SciSparc and AutoMax entered into the Merger Agreement, pursuant to which Merger Sub will merge with and into AutoMax, with AutoMax surviving as a wholly-owned subsidiary of SciSparc. Ordinary Shares of SciSparc will be issued to AutoMax’s shareholders at the effective time of such merger, or the Merger. The Exchange Ratio will be determined pursuant to a formula described in more detail in the Merger Agreement and later in this proxy statement/prospectus. Under the Exchange Ratio formula described in the Merger Agreement, immediately following the Merger, AutoMax’s shareholders, and the Advisor in connection with the Merger, are expected to own approximately 49.99% of SciSparc’s share capital, on a fully-diluted basis, subject to certain exceptions, and as further defined in the Merger Agreement, and SciSparc’s shareholders are expected to own approximately 50.01% of SciSparc’s share capital on a fully-diluted basis, subject to certain exceptions. The Merger has been unanimously approved by the boards of directors of both companies and will be presented for approval by the shareholders of AutoMax, including a separate approval by AutoMax’s shareholders who are not controlling shareholders of AutoMax or SciSparc. On August 14, 2024, the parties entered into the Merger Agreement Addendum, pursuant to which the rights to terminate the Merger Agreement if the Merger was not consummated by August 30, 2024, was deferred to November 30, 2024. On November 26, 2024, the parties entered into the Merger Agreement Second Addendum, pursuant to which the right to terminate the Merger Agreement if the Merger was not consummated by November 30, 2024, was deferred to March 31, 2025. The Merger is expected to close during the first quarter of 2025, subject to the approval of the shareholders of SciSparc, approval of AutoMax shareholders, and court approval, as detailed in section entitled “Regulatory Approvals” in this proxy statement/prospectus, as well as other customary conditions. Since the Merger is subject to a number of conditions, neither SciSparc nor AutoMax can anticipate either the timing of the closing of the Merger or whether it will occur at all.

At the effective time of the Merger, SciSparc anticipates that per each AutoMax ordinary share AutoMax shareholders will receive the number of SciSparc’s outstanding shares on fully-diluted basis, subject to certain exceptions, divided by 0.5001, multiplied by 0.4749, divided by (the number of AutoMax’s outstanding shares, minus SciSparc’s holdings in AutoMax), so, that in any event, AutoMax shareholders (other than SciSparc), together with the Advisor in connection with the Merger, shall own approximately 49.99% of SciSparc’s share capital, on a fully-diluted basis, subject to certain exceptions. Under the Exchange Ratio formula described in the Merger Agreement, immediately following the Merger, AutoMax’s shareholders, together with its Advisor in connection with the Merger, are expected to own approximately 49.99% of SciSparc’s share capital and SciSparc’s shareholders are expected to own approximately 50.01% of SciSparc’s share capital, on a fully-diluted basis, subject to certain exceptions.

For a more complete description of the Merger, please see the section entitled “The Merger Agreement” in this proxy statement/prospectus.

What will happen to SciSparc if, for any reason, the Merger does not close?

If, for any reason, the Merger does not close, the SciSparc board of directors may, following the termination of the Merger Agreement, elect to, among other things, attempt to complete another strategic transaction similar to the Merger, attempt to sell or otherwise dispose of certain assets of SciSparc or continue to operate the business of SciSparc.

Why are the two companies proposing to merge?

SciSparc and AutoMax believe that the Merger will result in a combined company that will maximize shareholder value.

SciSparc’s board of directors considered a number of factors that supported its decision to approve the Merger Agreement. In the course of its deliberations, SciSparc’s board of directors also considered a variety of risks and other countervailing factors related to entering into the Merger Agreement.

For a discussion of SciSparc’s reasons for the Merger, please see the section entitled “The Merger – Reasons for the Merger.”

What is the anticipated business of the combined company?

SciSparc anticipates to continue its current business activities as the parent company, while AutoMax’s current business activities will continue to be carried out by AutoMax as a wholly-owned subsidiary of SciSparc.

Why am I receiving these materials?

You are receiving these proxy materials because you have been identified as a shareholder of SciSparc as of the record date, and you are entitled to vote at the Special Meeting to approve the matters described in this proxy statement/prospectus. This proxy statement/prospectus contains important information about the proposed Merger and the Special Meeting and you should read it carefully and in its entirety. The enclosed voting materials allow you to authorize a proxy to vote your SciSparc ordinary shares without attending the Special Meeting. As promptly as practicable, please complete, sign, date and mail your proxy card in the pre-addressed postage-paid envelope provided or call the toll-free telephone number listed on your proxy card or access the Internet Web site described in the instructions on the enclosed proxy card.

What am I voting on?

There are four matters scheduled for a vote at the Special Meeting:

1. The approval of the consummation of the Merger and the other transactions contemplated by the Merger Agreement, including the issuance of SciSparc ordinary shares and the pre-funded warrants at the effective time of the Merger to the shareholders of AutoMax;

2. To approve the form of Indemnification Agreement for directors and officers of SciSparc, attached as Annex C to this proxy statement/prospectus, effective upon the effective time of the Merger, and to authorize the execution and delivery of such Indemnification Agreement with all office holders of SciSparc to be in office immediately following the effective time of the Merger or thereafter elected or appointed to the board of directors of SciSparc; and

3. To approve a one-time cash bonus to SciSparc’s Chief Executive Officer, Chairman and President, contingent upon the approval and closing of the Merger.

4. Subject to and contingent upon the approval of Proposal No. 1, to elect each of Tomer Levy and Yaarah Alfi to serve on the SciSparc board of directors upon the effective time of the Merger and to ratify the class structure of the SciSparc board of directors.

What is required to consummate the Merger?

To consummate the Merger, Proposals Nos. 1, 2, 3, and 4 must be approved at the Special Meeting, or at any permitted adjournment thereof, by the requisite holders of SciSparc ordinary shares on the record date for the Special Meeting. The Merger will not occur if Proposals Nos. 1, 2, 3, and 4 are not approved by SciSparc’s shareholders.

In addition to the requirement of obtaining such shareholder approvals, each of the other closing conditions set forth in the Merger Agreement must be satisfied or waived.

For a more complete description of the closing conditions under the Merger Agreement, we urge you to read the section entitled “The Merger Agreement – Conditions to the Completion of the Merger” in this proxy statement/prospectus.

Are there any federal or state regulatory requirements that must be complied with or federal or state regulatory approvals or clearances that must be obtained in connection with the Merger?

Neither SciSparc nor AutoMax is required to make any filings or obtain any approvals or clearances from any antitrust regulatory authorities in the United States or other countries to consummate the Merger. In the United States, SciSparc must comply with applicable federal and state securities laws and Nasdaq rules and regulations in connection with the issuance of the shares in connection with the Merger, including the filing with the SEC of this proxy statement/prospectus. In addition, in connection with the Merger, AutoMax has obtained a Withholding Tax Ruling and a 104H Tax Ruling from the tax authorities in Israel; both SciSparc and AutoMax are required to comply with the provisions thereunder.

What will AutoMax shareholders receive in the Merger?

As a result of the Merger, AutoMax shareholders will be entitled to receive SciSparc ordinary shares and pre-funded warrants exercisable into ordinary shares of SciSparc in exchange for AutoMax ordinary shares in an amount to be calculated by the application of an Exchange Ratio formula in the Merger Agreement.

At the effective time of the Merger, each outstanding share of AutoMax will be converted into the right to receive a number of SciSparc ordinary shares, in accordance with the Exchange Ratio.

The Merger Agreement does not provide for an adjustment to the total number of SciSparc ordinary shares that AutoMax shareholders will be entitled to receive to account for changes in the market price of SciSparc ordinary shares. Accordingly, the market value of the shares of SciSparc ordinary shares issued pursuant to the Merger will depend on the market value of the SciSparc ordinary shares at the time the Merger closes and could vary significantly from the market value of the SciSparc ordinary shares on the date of this prospectus.

At the effective time of the Merger, AutoMax shareholders will receive SciSparc ordinary shares in exchange for AutoMax shares held by them in an amount equal to the number of AutoMax shares held by each AutoMax shareholder multiplied by the Exchange Ratio. Certain AutoMax shareholders will receive pre-funded warrants exercisable into SciSparc’s ordinary shares. No fractional SciSparc ordinary shares will be issued in connection with the Merger. Instead, each AutoMax shareholder who otherwise would be entitled to receive a fractional SciSparc ordinary share (after aggregating all fractional SciSparc ordinary shares issuable to such shareholder) will receive such amount rounded to the nearest whole number of SciSparc ordinary shares.

Under the Exchange Ratio formula described in the Merger Agreement, immediately following the Merger, AutoMax’s shareholders (other than SciSparc, which currently holds shares in AutoMax) and its Advisor are expected to own approximately 49.99% of SciSparc’s share capital and SciSparc’s shareholders are expected to own approximately 50.01% of SciSparc’s share capital on a fully-diluted basis (subject to certain exceptions).

The Exchange Ratio is the result of the following calculation (rounded to four decimal places): the number of the SciSparc outstanding shares on a fully-diluted basis (subject to certain exceptions) divided by 0.5001, multiplied by 0.4749, then divided by the number of the AutoMax outstanding shares less the number of the AutoMax ordinary shares held by SciSparc; so that, in any event, immediately following the effective time, holders of AutoMax outstanding shares (and its Advisor, but other than SciSparc), will hold together 49.99% of SciSparc’s share capital, on a fully-diluted basis (subject to certain exceptions), immediately following the effective time.

For example, if the Merger was consummated as of December 30, 2024, then based on 10,828,251 SciSparc outstanding shares and 118,310,565 AutoMax outstanding shares, each AutoMax shareholder would have been entitled to receive 1.097 SciSparc shares, equal to $0.51, based on the closing price of SciSparc ordinary shares on Nasdaq on December 30, 2024.

For a more complete description of what AutoMax shareholders will receive in the Merger, please see the sections entitled “Market Price and Dividend Information” and “The Merger Agreement – Merger Consideration” in this proxy statement/prospectus.

What is the AutoMax Shareholder Support Agreement?

In connection with the execution of the Merger Agreement, certain shareholders of AutoMax entered into a shareholder support agreement, or the AutoMax Shareholder Support Agreement, covering approximately 55.56% of the outstanding shares of AutoMax. The AutoMax Shareholder Support Agreement provides, among other things, that the shareholders who are party to the AutoMax Shareholder Support Agreement will vote all of the shares of AutoMax held by them in favor of the adoption of the Merger Agreement, the approval of the Merger and the other transactions contemplated by the Merger Agreement.

What is the closing financing?

As part of the Merger Agreement, SciSparc has agreed to transfer to AutoMax a total of $4.25 million at the closing, less any amount due by AutoMax to SciSparc under any loan agreement between the parties, or the Closing Financing Amount. As of the date of his prospectus, SciSparc has advanced to AutoMax the aggregate amount of the Closing Financing Amount, $4.25 million, as a loan, under the Bridge Loan (as defined below) and its amendments thereto, to enable AutoMax to have sufficient cashflow to further develop its operations. As a result of AutoMax receiving the entire Closing Financing Amount, SciSparc will have no obligations to transfer additional financing amounts to AutoMax at the closing of the Merger. On the closing date of the Merger, SciSparc will be due interest from the period starting December 1, 2024 and ending on the effective date of the Merger.

Did SciSparc’s board of directors obtain a third-party valuation or fairness opinion in determining whether or not to proceed with the Merger?

Yes. SciSparc’s board of directors obtained an independent third-party valuation report from E.D.B. Consulting and Investments Ltd., or E.D.B. SciSparc’s board of directors did not, however, obtain a fairness opinion. SciSparc’s board of directors ensured that the third-party valuation met all necessary regulatory and legal standards, as there was no legal requirement under Israeli law to obtain a fairness opinion in connection with the approval of the Merger. The board of directors of SciSparc also considered the cost implications, as fairness opinions can be expensive, and determined that the third-party valuation provided sufficient information at a lower cost. SciSparc’s board of directors believed that the valuation, conducted by a reputable independent firm with industry expertise, offered comprehensive and reliable data adequate for making an informed decision about the Merger. For more information see “Summary — Valuation Report of E.D.B. Consulting and Investments Ltd”.

What will happen to AutoMax’s outstanding options, warrants and Series B bonds in the Merger?

As a result of the Merger, each AutoMax warrant, option and certain convertible rights that had resulted from a prior AutoMax transaction (in each case, whether or not vested) that is outstanding and unexercised immediately prior to the effective time, shall be cancelled immediately prior to the effective time for no consideration.

According to the terms of AutoMax’s Series B Bonds and the Trust Deed, the Series B Bonds will be due for principal repayment in four (4) unequal annual installments, which will be paid annually as of February 28, 2023 until 2026, inclusive, such that the first payment that was made on February 28, 2023 constituted 10% of the aggregate principal amount of the Series B Bonds, the second payment, that was made on February 28, 2024, constituted 15% of the aggregate principal amount of the Series B Bonds, the third payment, due on February 28, 2025, will constitute 30% of the aggregate principal amount of the Series B Bonds, and the fourth and final payment, due on February 28, 2026, will constitute 45% of the aggregate principal amount of the Series B Bonds. Following the closing of the Merger the Series B Bonds will remain outstanding and subject to repayment in accordance with the terms of the Trust Deed. The Series B Bonds bear interest at a rate of 5.9% per annum. As of December 31, 2024, NIS 34,245 (approximately $9,460 thousand) in principal amount of Series B Bonds remains outstanding and will therefore become a liability of the combined company following the completion of the Merger.

Will holders of the SciSparc ordinary shares issued in the Merger be able to sell those shares without restriction?

The sale of the SciSparc ordinary shares and pre-funded warrants issued as consideration in the Merger are being registered under the Securities Act of 1933, as amended, or the Securities Act, pursuant to the registration statement of which this prospectus forms a part, and will be able to be sold without restriction following the consummation of the Merger for so long as such registration statement remains effective, other than shares held by affiliates that will be subject to resale restrictions as control securities under Rule 144.

Who will be the directors of SciSparc following the Merger?

At and immediately after the effective time of the Merger, the board of directors of SciSparc is expected to be composed of the individuals set forth in the table below. The directors shall serve until their respective successors are duly elected or appointed and qualified or their earlier death, resignation or removal.

| Designee | | Age | | Position(s) |

| AutoMax Designees | | | | |

| Yaarah Alfi | | 36 | | Chief Financial Officer of AutoMax, director nominee of SciSparc |

| Tomer Levy | | 29 | | VP Business Development and Headquarters, director of AutoMax, director nominee of SciSparc |

| SciSparc Designees | | | | |

| Amitay Weiss | | 62 | | Chairman of SciSparc’s board of directors |

| Amnon Ben Shay | | 61 | | Director |

| Moshe Revach | | 48 | | Director |

| Liat Sidi | | 49 | | Director |

Who will be the executive officers of SciSparc immediately following the Merger?

Immediately following the Merger, the executive management team of SciSparc is expected to be composed as set forth below:

| Name | | Position with SciSparc | | Current Position | | Age |

| Oz Adler | | Chief Executive Officer and Chief Financial Officer | | Chief Executive Officer and Chief Financial Officer | | 38 |

| | | | | | | |

| Dr. Adi Zuloff-Shani | | Chief Technology Officer | | Chief Technology Officer | | 55 |

What interests do the current officers and directors of SciSparc have in the merger?

In considering the recommendation of SciSparc’s board of directors to vote in favor of the Merger, shareholders should be aware that, aside from their interests as shareholders, certain of SciSparc’s directors and officers have interests in the Merger that differ from, or extend beyond, those of SciSparc’s shareholders generally. SciSparc’s directors were aware of and considered these interests, among other matters, in evaluating the Merger and in recommending to shareholders that they approve the Merger. Shareholders should take these interests into account in deciding whether to approve the Merger. These interests include, among other things, the fact that:

| ● | Each of Amnon Ben Shay, Moshe Revach and Liat Sidi will continue to be a director of the combined company after the effective time of the Merger, and, following the closing of the Merger, will be eligible to be compensated as a non-employee director of the combined company pursuant to the compensation policy of SciSparc; |

| ● | Subject to the approval of SciSparc shareholders by the requisite majority, as described further in this prospectus, SciSparc’s Chief Executive Officer, Chairman and President will each be entitled to receive a one-time cash bonus, subject to and upon the closing of the Merger; |

| ● | Pursuant to the Merger Agreement and form of Indemnification Agreement, SciSparc’s directors and executive officers are entitled to continued indemnification, expense advancement and insurance coverage; and |

| ● | Mr. Amitay Weiss, the Chairman of SciSparc’s board of directors, serves as the chairman of AutoMax’s board of directors. Pursuant to the terms of the Merger Agreement, Mr. Amitay Weiss will continue to be a director of the combined company after the closing of the Merger and will receive compensation as a director and be entitled to continued indemnification. In addition, if approved by SciSparc shareholders, Mr. Amitay Weiss will be entitled to receive a one-time cash bonus of $50,000 as the Chairman of SciSparc upon the closing of the Merger. These interests may present him with actual or potential conflicts of interest. Mr. Amitay Weiss recused himself from the decision of approving the Merger and did not participate in the discussion or voting on the matter due to his personal interest. |

What is the one-time bonus to be granted to SciSparc’s Chief Executive Officer, Chairman and President?

SciSparc is proposing that in connection with, and subject to, the closing of the Merger, Mr. Oz Adler, SciSparc’s Chief Executive Officer, shall receive a cash bonus in the amount of $315,000. In addition, SciSparc is proposing that each of Mr. Amitay Weiss, SciSparc’s Chairman of the board of directors, and Mr. Itschak Shrem, SciSparc’s President, shall receive a cash bonus in the amount of $50,000 each.

SciSparc’s reasons for granting the above mentioned bonuses include providing an appropriate award for advancing SciSparc’s Restructuring Plan (as defined below), including the recipients’ individual contributions to the execution of the Merger Agreement and incentivizing individual excellence and corporate performance. For more information see the section titled “Proposal No. 3 – Approval of a one-time cash bonus to the SciSparc Chief Executive Officer, Chairman and President.”

What are the material Israeli income tax consequences of the Merger to me?

You are urged to consult with your own tax advisor for a full understanding of the tax consequences of the Merger to you, including the consequences under any applicable, state, local, foreign or other tax laws.

For a more detailed description of the material Israeli tax consequences of the Merger, see the section entitled “The Merger – Certain Material Israeli Income Tax Consequences of the Merger.”

As a SciSparc shareholder, how does the SciSparc board of directors recommend that I vote?

After careful consideration, the SciSparc board of directors recommends that SciSparc shareholders vote:

| ● | “FOR” Proposal No. 1 to approve the consummation of the Merger and the other transactions contemplated by the Merger Agreement, including the issuance of SciSparc ordinary shares and the pre-funded warrants at the effective time of the Merger to the shareholders of AutoMax; |

| ● | “FOR” Proposal No. 2 to approve the form of Indemnification Agreement for directors and officers of SciSparc; and |

| ● | “FOR” Proposal No. 3 to approve a one-time cash bonus to SciSparc’s Chief Executive Officer, Chairman and President, contingent upon the approval and closing of the Merger. |

| ● | “FOR” Proposal No. 4, subject to and contingent upon the approval of Proposal No. 1, to elect each of Tomer Levy and Yaarah Alfi to serve on the SciSparc board of directors upon the effective time of the Merger and to ratify the class structure of the SciSparc board of directors. |

What risks should I consider in deciding whether to vote in favor of the matters set forth above?

You should carefully review the section of this proxy statement/prospectus entitled “Risk Factors,” which sets forth certain risks and uncertainties related to the Merger, risks and uncertainties to which SciSparc’s business will be subject, risks and uncertainties to which SciSparc, as an independent company, is subject and risks and uncertainties to which AutoMax, as an independent company, is subject.

When do you expect the Merger to be consummated?

SciSparc anticipates that the Merger will occur as promptly as practicable after the Special Meeting to be held , 2025 and following satisfaction or waiver of all closing conditions, but cannot predict the exact timing. For a more complete description of the closing conditions under the Merger Agreement, please see the section entitled “The Merger Agreement –Conditions to the Completion of the Merger” in this proxy statement/prospectus.

What do I need to do now?

SciSparc urges you to read this proxy statement/prospectus carefully, including its annexes, and to consider how the Merger affects you.

If you are a shareholder of record of SciSparc, you may provide your proxy instructions in one of two different ways. First, you can mail your signed proxy card in the enclosed return envelope. Second, you may also provide your proxy instructions via telephone or the Internet by following the instructions on your proxy card or instruction form. Please provide your proxy instructions only once, unless you are revoking a previously delivered proxy instruction, and as soon as possible so that your shares can be voted at the Special Meeting. The laws of Israel, under which SciSparc is incorporated, permit electronically transmitted proxies, provided that each such proxy contains or is submitted with information from which it can determine that the proxy was authorized by the shareholder.

The telephone and Internet voting procedures below are designed to authenticate shareholders’ identities, to allow shareholders to grant a proxy to vote their shares and to confirm that shareholders’ instructions have been recorded properly. Shareholders granting a proxy to vote via the Internet should understand there may be costs associated with electronic access, such as usage charges from Internet access providers and telephone companies, that must be borne by the shareholder.

Whether you hold your shares directly as the shareholder of record or beneficially in “street name,” you may vote your shares by proxy without attending the Special Meeting. Depending on how you hold your shares, you may vote your shares in one of the following ways:

Shareholders of Record: For Shares Registered in Your Name

| ● | By telephone or over the Internet. You may vote your shares by telephone or via the Internet by following the instructions provided on your proxy card. If you vote by telephone or via the Internet, you do not need to return a proxy card by mail. If you have Internet access, we encourage you to record your vote on the Internet. It is convenient, reduces the use of natural resources and saves significant postage and processing costs. In addition, when you vote via the Internet or by phone prior to the Special Meeting’s date, your vote is recorded immediately and there is no risk that postal delays will cause your vote to arrive late and therefore not be counted. |

| ● | By Mail. If you received printed proxy materials, you may submit your vote by completing, signing and dating each proxy card received and returning it in the prepaid envelope. Sign your name exactly as it appears on the proxy card. |

| ● | In person at the Special Meeting. You may vote your shares in person at the Special Meeting. Even if you plan to attend the Special Meeting in person, we recommend that you also submit your proxy card or voting instructions or vote by telephone or via the Internet by the applicable deadline so that your vote will be counted if you later decide not to attend the Special Meeting. |

Beneficial Shareholders: For Shares Registered in the Name of a Broker or Bank

Most beneficial owners whose ordinary shares are held in “street name” receive instructions for granting proxies from their banks, brokers or other agents, rather than using SciSparc’s proxy card. If you are a beneficial owner of your shares, you should have received a Voting Instruction Form from the broker or other nominee holding your shares. You should follow the voting instructions provided by your broker or nominee in order to instruct your broker or other nominee on how to vote your shares. The availability of telephone and Internet voting will depend on the voting process of the broker or nominee. Shares held beneficially may be voted in person at the Special Meeting only if you contact the broker or nominee giving you the right to vote the shares and obtain a legal proxy from such broker or nominee.

General Information for All Shares Voted Via the Internet or By Telephone

Votes submitted by telephone or via the Internet must be received by 11:59 p.m., Eastern Time on , 2025. Submitting your proxy by telephone or via the Internet will not affect your right to vote in person should you decide to attend the Special Meeting.

Who can vote at the Special Meeting?

If, on the record date, your SciSparc ordinary shares are registered directly in your name with the SciSparc transfer agent, you are considered to be the shareholder of record with respect to those shares, and the proxy materials and proxy card are being sent directly to you by SciSparc. If you are an SciSparc shareholder of record, you may attend the Special Meeting of SciSparc shareholders and vote your shares in person. Even if you plan to attend the Special Meeting in person, SciSparc requests that you sign and return the enclosed proxy to ensure that your shares will be represented at the Special Meeting if you are unable to attend.

If, on the record date, your ordinary shares are held in a brokerage account or by another nominee, you are considered the beneficial owner of ordinary shares held in “street name,” and the proxy materials are being forwarded to you by your broker or other nominee together with a voting instruction card. As the beneficial owner, you are also invited to attend the Special Meeting of SciSparc shareholders. Because a beneficial owner is not the shareholder of record, you may not vote these shares in person at the Special Meeting unless you obtain a proxy from the broker, trustee or nominee that holds your shares, giving you the right to vote the shares at the Special Meeting.

How are votes counted?

Votes will be counted in the Special Meeting, including votes “For” and “Against,” abstentions and, if applicable, broker non-votes. Abstentions will have no effect and will not be counted towards the vote total with respect to Proposals Nos. 1 through 4. Broker non-votes will not be counted towards the vote total for any proposal.

What are “broker non-votes”?

If you hold SciSparc ordinary shares beneficially in street name and do not provide your broker or other agent with voting instructions, your SciSparc ordinary shares may constitute “broker non-votes.” Broker non-votes occur on a matter when banks, brokers and other nominees are not permitted to vote on certain non-discretionary matters without instructions from the beneficial owner and instructions are not given. These matters are referred to as “non-discretionary” matters. Proposals Nos. 1 through 4 are non-discretionary matters. As a result, banks, brokers and other nominees will not have discretion to vote on Proposals Nos. 1 through 4.

Broker non-votes will not be considered as votes cast by the holders of SciSparc ordinary shares present in person or represented by proxy at the Special Meeting, and will therefore not have any effect with respect to Proposals Nos. 1 through 4.

How many votes are needed to approve each proposal?

The following table summarizes the minimum vote needed to approve each proposal and the effect of abstentions and broker non-votes.

| Proposal Number | | Proposal Description | | Vote Required for Approval |

| 1. | | To approve the consummation of the Merger and the other transactions contemplated by the Merger Agreement, including the issuance of SciSparc ordinary shares and the pre-funded warrants at the effective time of the Merger to the shareholders of AutoMax. | | A simple majority of shareholders present (in person or by proxy) and voting on the matter (excluding abstentions) |

| | | | | |

| 2. | | To approve the form of Indemnification Agreement for directors and officers of SciSparc, attached as Annex C to this proxy statement/prospectus, effective upon the effective time of the Merger, and to authorize the execution and delivery of such Indemnification Agreement with all office holders of SciSparc to be in office immediately following the effective time of the Merger or thereafter elected or appointed to the board of directors of SciSparc. | | A simple majority of all votes properly cast in person or by proxy at the Special Meeting (excluding abstentions), and the fulfillment of one of the following additional voting requirements: (i) the majority of the Shares that are voted at the Special Meeting in favor of the Proposal, excluding abstentions, includes a majority of the votes of shareholders who are not controlling shareholders or do not have a personal interest in the approval of the Proposal (each, an “Interested Shareholder”); or (ii) the total number of Shares of the shareholders mentioned in clause (i) above that are voted against the Proposal does not exceed two percent (2%) of the total voting rights in the Company. |

| | | | | |

| 3. | | To approve a one-time cash bonus to SciSparc’s Chief Executive Officer, Chairman and President, contingent upon the approval and closing of the Merger. | | A simple majority of all votes properly cast in person or by proxy at the Special Meeting (excluding abstentions), and the fulfillment of one of the following additional voting requirements: (i) the majority of the Shares that are voted at the Special Meeting in favor of the Proposal, excluding abstentions, includes a majority of the votes of shareholders who are not controlling shareholders or do not have a personal interest in the approval of the Proposal (each, an “Interested Shareholder”); or (ii) the total number of Shares of the shareholders mentioned in clause (i) above that are voted against the Proposal does not exceed two percent (2%) of the total voting rights in the Company. |

| | | | | |

| 4. | | Subject to and contingent upon the approval of Proposal No. 1, to elect each of Tomer Levy and Yaarah Alfi to serve on the SciSparc board of directors upon the effective time of the Merger and to ratify the class structure of the SciSparc board of directors. | | A simple majority of all votes properly cast in person or by proxy at the Special Meeting. |

| (1) | The term “controlling shareholder” means a shareholder having the ability to direct the activities of a company, other than by virtue of being an office holder. A shareholder is presumed to be a controlling shareholder if the shareholder holds 50% or more of the voting rights in a company or has the right to appoint the majority of the directors of the company or its general manager. To the knowledge of SciSparc, there is no shareholder who is a controlling shareholder. For the purpose of Proposals Nos. 2 and 3, the term controlling shareholder shall also include a person who holds 25% or more of the voting rights in the general meeting of the company if there is no other person who holds more than 50% of the voting rights in the company; for the purpose of a holding, two or more persons holding voting rights in the company each of which has a personal interest in the approval of the transaction being brought for approval of the company will be considered to be joint holders. |

| (2) | Under the Israeli Companies Law, 5759-1999, or the Companies Law, a “personal interest” of a shareholder in an action or transaction of a company includes a personal interest of any of the shareholder’s relatives (i.e. spouse, brother or sister, parent, grandparent, child as well as child, brother, sister or parent of such shareholder’s spouse or the spouse of any of the above) or an interest of a company with respect to which the shareholder or the shareholder’s relative (as defined above) holds 5% or more of such company’s issued shares or voting rights, in which any such person has the right to appoint a director or the chief executive officer or in which any such person serves as director or the chief executive officer, including the personal interest of a person voting pursuant to a proxy which the proxy grantor has a personal interest, whether or not the person voting pursuant to such proxy has discretion with regards to the vote; and excludes an interest arising solely from the ownership of ordinary shares of a company. |

Under Israeli law, every voting shareholder is required to notify the Company whether such shareholder is an Interested Shareholder. To avoid confusion, every shareholder voting by means of the enclosed proxy card or voting instruction form, or via telephone or internet voting, will be deemed to confirm that such shareholder is NOT an Interested Shareholder. If you are an Interested Shareholder (in which case your vote will only count for or against the ordinary majority, and not for or against the special tally under Proposals Nos. 2 and 3), please notify Mr. Oz Adler, Chief Financial Officer, at c/o SciSparc Ltd., 20 Raul Wallenberg Street, Tower A, Tel Aviv 6971916, Israel, telephone: +972-3-717-5777 or by email (oz@scisparc.com). If your shares are held in “street name” by your broker, bank or other nominee and you are an Interested Shareholder, you should notify your broker, bank or other nominee of that status, and they in turn should notify the Company as described in the preceding sentence.

When and where will the Special Meeting of SciSparc shareholders be held?

The Special Meeting of SciSparc shareholders will be held at , local time, on , 2025, at . Subject to space availability, all SciSparc shareholders as of the record date, or their duly appointed proxies, may attend the meeting. Since seating is limited, admission to the meeting will be on a first-come, first-served basis. Registration and seating will begin at , local time. Any such change will be announced in a Report of Foreign Private Issuer on Form 6-K furnished to the SEC.

What happens if I do not return a proxy card or otherwise provide proxy instructions, as applicable?

Shareholder of Record: Shares Registered in Your Name

If you are a shareholder of record and do not vote by telephone, through the Internet, by completing the enclosed proxy card or in person at the Special Meeting, your shares will not be voted.

Beneficial Owner: Shares Registered in the Name of a Broker or Bank

Proposals Nos. 1, 2, 3, and 4 are non-discretionary matters. As a result, banks, brokers and other nominees will not have discretion to vote on Proposals Nos. 1, 2, 3 and 4.

What if I return a proxy card or otherwise vote but do not make specific choices?

If you return a signed and dated proxy card or otherwise vote without marking voting selections, your shares will be voted, as applicable, “For” the approval of the consummation of the Merger and the other transactions contemplated by the Merger Agreement, including the issuance of SciSparc ordinary shares and pre-funded warrants at the effective time of the Merger to the shareholders of AutoMax, as contemplated by the Merger Agreement (Proposal No. 1); “For” the approval of the form of Indemnification Agreement between SciSparc and its directors (Proposal No.2); “For” the approval of a one-time cash bonus to SciSparc’s Chief Executive Officer, Chairman and President (Proposal No. 3); and “For” the approval of the election of each of Tomer Levy and Yaarah Alfi and ratification of classes, subject to approval of Proposal No. 1. (Proposal No. 4)

May I change my vote after I have submitted a proxy or provided proxy instructions?

SciSparc’s shareholders of record, may change their vote at any time before their proxy is voted at the Special Meeting in one of three ways. First, a shareholder of record of SciSparc can send a written notice to the Chief Executive Officer of SciSparc stating that it would like to revoke its proxy. Second, a shareholder of record of SciSparc can submit new proxy instructions either on a new proxy card or via telephone or the Internet. Third, a shareholder of record of SciSparc can attend the Special Meeting and vote in person. Attendance alone will not revoke a proxy. If an SciSparc shareholder of record or a shareholder who owns SciSparc shares in “street name” has instructed a broker to vote its SciSparc ordinary shares, the shareholder must follow directions received from its broker to change those instructions.

Your most current proxy card or telephone or Internet proxy is the one that is counted.

Should AutoMax’s and SciSparc’s shareholders send in their share certificates now?

No. To the extent AutoMax’s and SciSparc’s shareholders have certificated shares, such shareholders should keep their existing share certificates at this time. Similarly, holders of shares that are held in book-entry form should refrain from attempting to surrender their shares currently. Shareholders should await further instructions in relation to their share certificates, if any.

Am I entitled to dissenters’ rights?

No, SciSparc’s shareholders are not entitled to dissenters’ rights in connection with the Merger.

Have AutoMax’s shareholders agreed to adopt the Merger Agreement?

[Yes]. On [ ], 2025, AutoMax’s shareholders adopted the Merger Agreement and approved the Merger and related transactions.

Who is paying for this proxy solicitation?

SciSparc will bear the cost of soliciting proxies. In addition to these proxy materials, SciSparc’s directors and employees may also solicit proxies in person, by telephone, or by other means of communication. Directors and employees will not be paid any additional compensation for soliciting proxies. SciSparc and AutoMax may also reimburse brokerage firms, banks and other agents for the cost of forwarding proxy materials to beneficial owners.

What is the quorum requirement?

A quorum of shareholders is necessary to hold a valid meeting. The presence (in person or by proxy) of any two or more shareholders holding, in the aggregate, at least 15% of the voting power of SciSparc’s ordinary shares constitutes a quorum for purposes of the Special Meeting. On the record date, there were SciSparc ordinary shares outstanding and entitled to vote. Thus, the holders of at least [__] shares must be present in person or represented by proxy at the Special Meeting to have a quorum.

Your shares will be counted towards the quorum only if you submit a valid proxy (or one is submitted on your behalf by your broker, bank or other nominee) or if you vote in person at the Special Meeting. Abstentions and broker non-votes will be counted towards the quorum requirement. If half an hour has elapsed from the time set for the Special Meeting and a quorum is not present, the Special Meeting will be adjourned to the following day, at the same time and place, or to a different date, as shall be determined by the board of directors in a notice to the shareholders. If a quorum is not present at the adjourned Special Meeting, as stated above, a minimum of one shareholder, whether present in person or by proxy, shall be deemed as constituting a quorum.

What happens if a quorum is not present?

If half an hour has elapsed from the time set for the Special Meeting and a quorum is not present, the Special Meeting will be adjourned to the same day the following week, at the same time and place.

Who can help answer my questions?

If you are a SciSparc shareholder and would like additional copies, without charge, of this proxy statement/prospectus or if you have questions about the Merger and related transactions, including the procedures for voting your shares, you should contact the Chief Executive Officer of SciSparc, at the following address and phone number: 20 Raul Wallenberg St., Tower A, 2nd Floor, Tel Aviv Israel, 6971916, or by calling +972-3-7175777.

SUMMARY

This summary highlights selected information from this proxy statement/prospectus and may not contain all of the information that is important to you. To better understand the Merger, and the proposals being considered at the Special Meeting, you should read this entire proxy statement/prospectus carefully, including the Merger Agreement attached as Annex A, the form of the AutoMax Shareholder Support Agreement and form of Indemnification Agreement attached as Annexes B and C and the other annexes to which you are referred herein. You may obtain the information incorporated by reference into this proxy statement/prospectus without charge by following the instructions in the section entitled “Where You Can Find More Information” beginning on page 237.

The Companies

SciSparc Ltd.

20 Raul Wallenberg Street

Tower A

Tel Aviv

6971916 Israel

+972-3-7175777

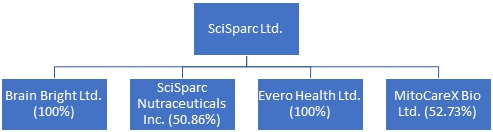

SciSparc is a specialty clinical-stage pharmaceutical company. SciSparc’s focus is creating and enhancing a portfolio of technologies and assets based on cannabinoid therapies. With this focus, SciSparc is currently engaged in the following development programs based on Δ9-tetrahydrocannabinol, or THC, and/or non-psychoactive cannabidiol, or CBD, and/or other cannabinoid receptors, or CBR, agonists: SCI-110 for the treatment of Tourette syndrome, or TS, for the treatment of obstructive sleep apnea, or OSA, and for the treatment of Alzheimer’s disease and agitation; SCI-160 for the treatment of pain; and SCI-210 for the treatment of Autism Spectrum Disorder, or ASD, and Status Epilepticus, or SE. SciSparc also has a majority-owned subsidiary whose business focuses on the sale of hemp seeds oil-based products and others on Amazon Marketplace.

SCI-110 is a proprietary drug candidate based on two components: (1) THC, which is the major cannabinoid molecule in the cannabis plant, and (2) CannAmide™, a proprietary Palmitoylethanolamide, or PEA, formulation. PEA is an endogenous fatty acid amide that belongs to the class of nuclear factor agonists, which are molecules that regulate the expression of genes. SciSparc believes that the combination of THC and PEA may induce a reaction known as the “sparing effect,” which has strong potential to treat various diseases such as TS, OSA and Alzheimer’s disease and agitation.

SCI-210 is a proprietary drug candidate based on two components: (1) CBD, and (2) CannAmide™. SciSparc believes that the combination of CBD and PEA may also induce a sparing effect reaction, which has strong potential to treat various diseases such as ASD and SE.

SCI-160 is a novel pharmaceutical preparation containing a cannabinoid receptor type 2, or CB2 receptor, agonist for the treatment of pain. This innovative CB2 receptor agonist was synthesized by Raphael Mechoulam, Ph.D., Professor of Medicinal Chemistry at the Hebrew University, a member of the SciSparc Scientific Advisory Board. SciSparc believes that modulating CB2 receptor activity by selective CB2 receptor agonists holds unique therapeutic potential for addressing pain conditions.

SciSparc believes that modulating CB2 receptor activity by selective CB2 receptor agonists holds unique therapeutic potential for addressing pain conditions.

Pursuant to the positive results obtained in a phase IIa TS study conducted at Yale School of Medicine, SciSparc is developing a regulatory dossier to be submitted to the U.S. Food and Drug Administration, or FDA, The German Federal Institute for Drugs and Medical Devices, or BfArM, and the Israeli Ministry of Health, or MoH, for its SCI-110 program for TS.

SciSparc was incorporated under the laws of the State of Israel on August 23, 2004. SciSparc’s ordinary shares are listed on the Nasdaq Capital Market under the symbol “SPRC”.

If the Merger is completed, the business of AutoMax will become the business of SciSparc as described beginning on page 175 of this proxy statement/prospectus under the caption “AutoMax Business.”

AutoMax Motors Ltd.

Harehavim 15,

Jerusalem,

9346213, Israel

+972-2-622-5987

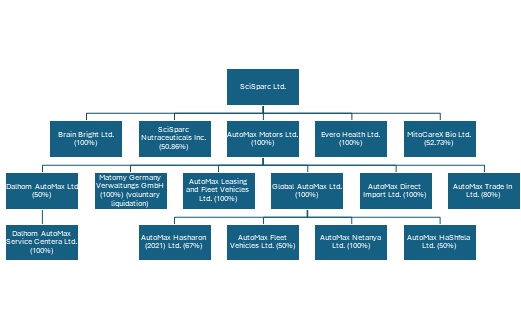

AutoMax imports and markets a variety of private vehicle models, from various categories such as small vehicles, crossovers, executive vehicles, premium vehicles, work vehicles, and buses manufactured by Temsa. AutoMax’s operations are conducted in Israel. AutoMax believes there are several primary factors that contribute to the success of vehicle importers in Israel, including: (i) innovative vehicle models and the manner in which these are branded among customers; (ii) trade conditions, especially the exchange rates of the foreign currencies in which the importer imports in comparison to the currency exchange rates of competitors; (iii) the existence of good relations with the manufacturer and/or the agent which is also reflected in import prices; (iv) the technological quality of the imported vehicles; (v) high marketing ability of the importer, which is also reflected in the adjustment of the vehicle and the prices to market demands; (vi) the level of provided service and the reputation of the importer; (vii) good geographical layout of purchasing agencies across the world (especially true for parallel importers, who purchase non-counterfeit product imported from different countries to be sold on the open market); and (viii) the geopolitical situation in the countries from which the vehicles are imported. AutoMax’s clients range from private customers to institutional customers, including companies that lease, rent, and operate vehicle fleets, and car dealerships.

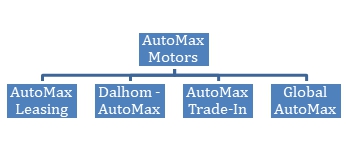

AutoMax operates through various subsidiaries, which include Dalhom AutoMax Ltd., of which it holds 50% of the voting rights, or Dalhom AutoMax; AutoMax Trade-In Ltd., of which it holds 80% of the voting rights, or AutoMax Trade-In; AutoMax Direct Import Ltd. (formerly known as AutoMax Leasing Ltd.), which it wholly owns, or AutoMax Direct Import; and Global AutoMax Ltd., which it wholly owns, or Global AutoMax.

Global AutoMax holds a number of subsidiaries: AutoMax HaShfela Ltd., in which it holds 50% of the voting rights; AutoMax Netanya Ltd., a wholly owned subsidiary; AutoMax Fleet Vehicles Ltd., in which Global AutoMax holds 50% of the voting rights; and AutoMax HaSharon Ltd., in which Global AutoMax holds 67% of the voting rights.

Industry Overview

The vehicle market in Israel differs from most vehicle markets in the world due to the absence of open land borders for free trade in vehicles and high import duties. The percentage of vehicle ownership in Israel is relatively low compared to various Western countries, due to, among other factors, the relatively high price of vehicles, mainly due to high taxation, inferior road infrastructure compared to other Western countries, and high population density. Furthermore, the vehicle market in Israel includes a relatively large number of vehicle importers, compared to other sectors in the economy, that import vehicles that are manufactured in different countries around the world. Most vehicle importers import several brands and products. The development of the automotive market in Israel is characterized by fluctuations resulting from changes in the macroeconomic environment of the economy, among other factors. The main characteristics of the automotive market that affect AutoMax’s activity and the competitors in this market are:

| | ● | High dependence on suppliers. The success of vehicle importers depends mainly on the relationship with manufacturers of the vehicles imported and the strategy of the manufacturers’ activity in relation to the launch of new products, brand positioning in the world, model policy, trade conditions, price policy and marketing support. It should be noted that the dependence on the vehicle manufacturers is mainly relevant to the direct importers who have, in practice, exclusive franchise agreements with manufacturers whose products they import to Israel. AutoMax believes that it has no significant reliance on the activity of a particular vehicle manufacturer. |

| | ● | Changes in consumer preferences. The vehicle preferences in Israel are subject to frequent changes, resulting from the preference of certain models by consumers, and due to a variety of factors, including but not limited to, engine type (diesel, oil, electric, hybrid or gasoline), the size of the vehicle, its design, technological advantages, environmental rating, fuel economy, safety standard, price and marketability on the resale market. |

| | | |

| | ● | Taxation of vehicles. The importing of most private vehicles in Israel is subject to purchase taxes, Value Added Tax and customs imposed at cumulative rates of approximately 30%-130% (or, oftentimes, more), of the cost of the vehicles. The aforementioned tax rates are among the highest in the world. Changes in tax rates, including reduction in tax rates given to vehicles of a certain type, have a direct impact on the preferences of customers in the area of activity. In addition, changes in taxation on vehicles provided to employees as part of their employment conditions may affect their preference in relation to receiving vehicles from the workplace versus purchasing. |

| | | |

| | ● | Fuel and electricity prices. Changes in fuel and electricity prices may have an impact on consumer preferences in the long term. Vehicle model preferences vary depending on the type of energy used (i.e., diesel, gas, gasoline, or electricity) and each such energy price. |

| | | |

| | ● | Regulation. The automotive industry in Israel is characterized by vast regulation and strict regulatory requirements, including the standardization requirements, which may affect the Company’s expenditure and the results of its operations. |

| | | |

| | ● | Infrastructure levels and density of the roads. According to research conducted by the Bank of Israel, the roads in Israel are characterized by high levels of density, especially in the areas with greater population concentration. This affects the scope of vehicle purchases and is expected to affect it in the future as well. |

| | | |

| | ● | Changes in currency and interest rates as well as the economic environment. |

Competition

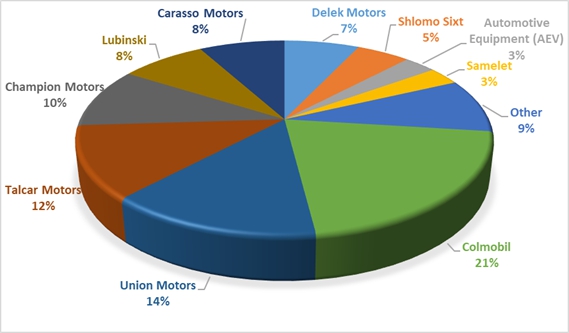

AutoMax operates in two highly competitive industries: the vehicle industry in Israel as an importer and seller and in the international vehicle industry as a purchaser of vehicles. The value chain in the automotive industry includes international vehicle manufacturers, vehicle importers, vehicle dealers (over 8,000 authorized vehicle dealers), financing entities and end users: households, corporate firms and public organizations. According to the Automotive Industry Review published by Dun & Bradstreet in February 2024, or the Automotive Industry Review, there are approximately 20 official import groups representing various manufacturers in Israel, which are responsible for approximately 97% of the automotive imports to Israel. Alongside these, there are several dozen parallel importers who are collectively responsible for approximately 3% of the imports. However, during the years 2019 to 2024, a small number of parallel importers were responsible for approximately 75% of the total parallel import to Israel. Additionally, there are vehicle leasing and rental companies, consisting of approximately five primary companies, alongside smaller companies.

According to the Automotive Industry Review, as of year-end-2023, there were approximately 4.1 million vehicles on the roads in Israel, of which, approximately 86% are private vehicles. According to the State of Israel Central Bureau of Statistics, despite a relatively low level of vehicle ownership in Israel, based on the number of vehicles per 1,000 residents, the traffic density remains among the highest in the world. Based on studies conducted in previous years, as detailed in Automotive Industry Review, the density is 3.5 times higher than the Organization for Economic Co-operation and Development, or the OECD, average. The main contributors are the concentration of population in central Israel, an underdeveloped public transportation system and the lack of correlation between the construction of roads and the increase in population.

SciSparc Merger Sub Ltd.

SciSparc Merger Sub Ltd. is a wholly-owned subsidiary of SciSparc, and was formed solely for the purposes of carrying out the Merger.

The Merger (see page 91 and page 110)

If the Merger is completed, Merger Sub will merge with and into AutoMax, with AutoMax surviving as a wholly-owned subsidiary of SciSparc.

At the effective time of the Merger, each AutoMax ordinary share outstanding immediately prior to the effective time (excluding certain AutoMax ordinary shares that may be cancelled pursuant to the Merger Agreement) will be automatically converted into the right to receive a number of SciSparc ordinary shares and pre-funded warrants. The Exchange Ratio has been determined pursuant to a formula described in more detail in the Merger Agreement and later in this proxy statement/prospectus. Under the Exchange Ratio formula described in the Merger Agreement, immediately following the Merger, AutoMax’s shareholders, and its Advisor in connection with the Merger, are expected to own approximately 49.99% of SciSparc’s share capital and SciSparc’s shareholders are expected to own approximately 50.01% of SciSparc’s share capital, on a fully-diluted basis, subject to certain exceptions.