As filed with the U.S. Securities and Exchange Commission on March 24, 2016

Registration No. 333- 209619

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

| | Pre-Effective Amendment No. 1 | x |

| | | |

| | Post-Effective Amendment No. __ | o |

| | (Check appropriate box or boxes) | |

ANGEL OAK FUNDS TRUST

(Exact Name of Registrant as Specified in Charter)

One Buckhead Plaza

3060 Peachtree Road NW, Suite 500

Atlanta, Georgia 30305

(Address of Principal Executive Offices)

Registrant’s Telephone Number, including Area Code: (404) 953-4900

Dory S. Black, Esq.

c/o Angel Oak Capital Advisors, LLC

3060 Peachtree Road NW, Suite 500

Atlanta, Georgia 30305

(Name and Address of Agent for Service)

WITH A COPY TO:

| Douglas P. Dick |

| Stephen T. Cohen |

| Dechert LLP |

| 1900 K Street NW |

| Washington, DC 20006 |

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective under the Securities Act of 1933, as amended (the “Securities Act”).

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

No filing fee is required because of reliance on Section 24(f) of the Investment Company Act of 1940, as amended.

| Title of Securities Being Registered: | Institutional Class and Class A shares of beneficial interest, without par value, of the Angel Oak High Yield Opportunities Fund |

RAINIER INVESTMENT MANAGEMENT MUTUAL FUNDS Rainier High Yield Fund |

601 Union Street, Suite 2801

March 31, 2016

Dear Shareholder,

You are receiving this letter and the accompanying notice and Proxy Statement/Prospectus because of your investment in the Rainier High Yield Fund (the “Fund” or the “Rainier Fund”), a series of Rainier Investment Management Mutual Funds (the “Rainier Trust”). The Fund’s investment adviser is Rainier Investment Management, LLC (“Rainier”), and the Fund’s portfolio is managed by Matthew R. Kennedy, CFA, Director of Fixed Income Management for Rainier, and James H. Hentges, CFA, Portfolio Manager for Rainier (together, the “Portfolio Managers”), who have managed the Fund since its inception in 2009.

The Portfolio Managers have informed Rainier of their intention to resign from Rainier and to become employees of Angel Oak Capital Advisors, LLC (“Angel Oak”), an Atlanta, Georgia based investment adviser specializing in fixed income investments. Angel Oak currently manages two fixed income mutual funds with approximately $5.5 billion in assets and provides investment advisory services to other pooled investment vehicles (e.g., private funds), high net worth individuals, and banking institutions.

In connection with the anticipated resignation of the Portfolio Managers from Rainier, the Board of Trustees of the Rainier Trust (the “Rainier Board”) has approved the reorganization (the “Reorganization”) of the Fund into the Angel Oak High Yield Opportunities Fund (the “Acquiring Fund”), a newly formed series of Angel Oak Funds Trust (the “Angel Oak Trust”), subject to the approval of the shareholders of the Rainier Fund. Importantly, the Acquiring Fund is expected to be managed in a manner that is substantially similar to the manner in which the Rainier Fund is managed. In addition, the Acquiring Fund has an investment objective and investment strategies that are substantially similar to those of the Rainier Fund.

If approved by shareholders, upon completion of the Reorganization, your Institutional Shares and Original Shares of the Fund would be exchanged for Institutional Class and Class A shares of the Acquiring Fund, respectively, of the same number and value, without (i) the imposition of any sales load or other charge or (ii) the recognition, generally, of gain or loss by the Rainier Fund or its shareholders for federal income tax purposes. The Acquiring Fund is advised by Angel Oak. Concurrent with the Reorganization, the Portfolio Managers would become employees of Angel Oak and would manage the Acquiring Fund on behalf of Angel Oak with support from certain additional Angel Oak portfolio managers.

You are being asked to approve the Reorganization, which would result in your becoming a shareholder of the Acquiring Fund. Angel Oak and Angel Oak Trust have committed that, for a period of at least two years following the Reorganization, the management fee rate paid by the Acquiring Fund would be the same as the management fee rate currently paid by the Fund and any increase to the rate thereafter would be subject to prior shareholder approval. Angel Oak and Angel Oak Trust have also committed that the net annual operating expense ratio paid by the Acquiring Fund through May 31, 2018 would be the same as or lower than the net annual operating expense ratio currently paid by the Fund. The Reorganization has been approved by the Rainier Board and the Acquiring Fund’s Board of Trustees, subject to shareholder approval.

For the reasons discussed in this letter and in the enclosed Proxy Statement/Prospectus and based on the recommendations of Rainier, a special meeting of shareholders of the Fund (the “Special Meeting”) will be held on April 15, 2016, at the offices of Rainier at Two Union Square, 601 Union Street, Suite 2801, Seattle, Washington 98101 at 10:00 a.m. Pacific time so that Fund shareholders may consider the proposed Reorganization.

If shareholders of the Fund approve the Reorganization and all other closing conditions are met, the Reorganization will take effect on or about April 15, 2016, or such other date as the parties may agree. Upon the completion of the Reorganization, each shareholder of the Fund would receive a number of full and fractional Institutional Class and/or Class A shares of the Acquiring Fund equal in aggregate net asset value at the time of the exchange to the aggregate net asset value of such shareholder’s shares of the Fund, as follows:

| PROPOSED REORGANIZATION |

| Rainier Fund: | à | Acquiring Fund: |

| | | |

| Rainier Investment Management Mutual Funds | | Angel Oak Funds Trust |

| Rainier High Yield Fund, Original Shares | à | Angel Oak High Yield Opportunities Fund, Class A |

| Rainier High Yield Fund, Institutional Shares | à | Angel Oak High Yield Opportunities Fund, Institutional Class |

The Rainier Fund would be terminated after the closing of the Reorganization.

More information about the Reorganization is contained in the enclosed Proxy Statement/Prospectus. You should review the Proxy Statement/Prospectus carefully and retain it for future reference.

Shareholders of record of the Rainier Fund as of the close of business on February 19, 2016, the record date (“Record Date”), are entitled to vote on the proposed Reorganization at the Special Meeting and at any adjournment or postponement thereof.

While you are, of course, welcome to join us at the Special Meeting, we urge you to vote by phone, on the internet or by mail today so that the maximum number of shares may be voted. You may revoke your proxy before it is exercised at the Special Meeting, as described in the Proxy Statement/Prospectus.

Whether or not you are planning to attend the Special Meeting, we need your vote. Your vote is important no matter how many shares you own. In the event that insufficient votes are received from shareholders, the Special Meeting may be adjourned to permit further solicitation of proxies. Please vote by phone, on the internet or by mail today. Instructions on how to vote are included on the enclosed proxy card.

Thank you for taking the time to consider this important proposal and for your continuing investment.

Sincerely,

| /s/ Melodie B. Zakaluk | |

| Melodie B. Zakaluk | |

| President, CEO and Trustee | |

| Rainier Investment Management Mutual Funds | |

RAINIER INVESTMENT MANAGEMENT MUTUAL FUNDS Rainier High Yield Fund |

601 Union Street, Suite 2801

Seattle, WA 98101

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD APRIL 15, 2016

NOTICE IS HEREBY GIVEN that a SPECIAL MEETING OF SHAREHOLDERS (the “Special Meeting”) of the Rainier High Yield Fund (the “Fund”), a series of Rainier Investment Management Mutual Funds (the “Trust”), will be held on April 15, 2016, at 10:00 a.m., Pacific time, at Two Union Square, 601 Union Street, Suite 2801, Seattle, Washington 98101 to consider and vote on the proposal (the “Proposal”) described below and to transact such other business as may properly come before the Special Meeting or any adjournments or postponements thereof:

| PROPOSAL: | To reorganize the Rainier High Yield Fund from a series of Rainier Investment Management Mutual Funds to a series of Angel Oak Funds Trust (the “Reorganization”). |

The Reorganization is not expected to result in any material change in the way the Fund is managed or in its investment objective and strategies. The Fund’s net fees and expenses are not expected to increase for at least two years as a result of the Reorganization.

The Trust has fixed the close of business on February 19, 2016 as the record date (the “Record Date”) for determining shareholders entitled to notice of and to vote at the Special Meeting.

If you are a shareholder of record as of the close of business on the Record Date, you are entitled to vote at the Special Meeting and at any adjournment thereof. While you are welcome to join us at the Special Meeting, most shareholders will cast their votes by filling out and signing the enclosed proxy card. The Trust’s Board of Trustees has carefully reviewed the Proposal and recommends that you vote “FOR” the Proposal. If you have any questions regarding the issues to be voted on, please do not hesitate to call the Fund toll-free at 1-800-248-6314.

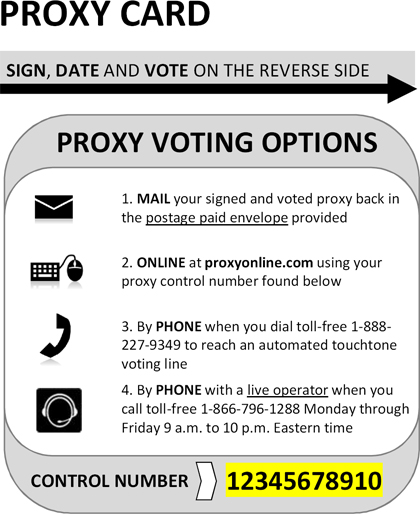

Whether or not you are planning to attend the Special Meeting, we need your vote prior to April 15, 2016. Voting is quick and easy. Everything you need is enclosed. To vote, you may use any of the following methods:

| INTERNET: | | Visit the web site shown on your proxy card. Enter the control number on your proxy card and follow the instructions. |

| PHONE: | | Please call the toll-free number on your proxy card. Enter the control number on your proxy card and follow the instructions. |

| MAIL: | | Please mark, sign, and date the enclosed proxy card and promptly return it in the enclosed, postage-paid envelope. BE SURE TO SIGN EACH CARD BEFORE MAILING IT. |

Voting by proxy will not prevent you from voting your shares in person at the Special Meeting. You may revoke your proxy before it is exercised at the Special Meeting, either by writing to the Secretary of the Trust at the Trust’s address noted in the Proxy Statement or in person at the time of the Special Meeting. A prior proxy can also be revoked by voting again through the web site or toll-free number listed on the enclosed proxy card.

Thank you for taking the time to consider this important proposal and for your continuing investment in the Fund.

Christopher E. Kashmerick

Secretary of the Trust

March 31, 2016

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR THE SHAREHOLDER MEETING TO BE HELD ON APRIL 15, 2016: This Notice and Proxy Statement are available on the internet at www.proxyonline.com/docs/rainierHY.pdf. The Fund’s most recent Annual Report to shareholders is available on the internet at www.rainierfunds.com.

QUESTIONS AND ANSWERS

The following is a summary of more complete information appearing later in the attached Proxy Statement/Prospectus (the “Proxy Statement”) or incorporated by reference herein. You should read carefully the entire Proxy Statement, including the Agreement and Plan of Reorganization, which is attached as Appendix A, because it contains details that are not in the Questions and Answers.

YOUR VOTE IS VERY IMPORTANT!

Question: What is this document and why did you send it to me?

Answer: The attached document is (i) a proxy statement for the Rainier High Yield Fund (the “Fund” or “Rainier Fund”), a series of Rainier Investment Management Mutual Funds, a Delaware statutory trust (the “Rainier Trust”), and (ii) a prospectus for the Institutional Class and Class A shares of the Angel Oak High Yield Opportunities Fund (the “Acquiring Fund”), a newly created series of Angel Oak Funds Trust (the “Angel Oak Trust”). The purpose of the Proxy Statement is to solicit votes from shareholders of the Fund to approve the proposed reorganization of the Rainier Fund into the Acquiring Fund (the “Reorganization”), as described in the Agreement and Plan of Reorganization between the Rainier Trust and the Angel Oak Trust (the “Plan”).

The Board of Trustees of the Rainier Trust and the Board of Trustees of the Angel Oak Trust have approved the Plan pursuant to which the Rainier Fund is expected to be reorganized into the Acquiring Fund. The Reorganization would result in shareholders of the Rainier Fund’s Institutional Shares and Original Shares becoming shareholders of the Acquiring Fund’s Institutional Class and Class A shares, respectively. The Reorganization is not expected to result in any material change in the way the Fund is managed or in its investment objective and strategies. The Fund’s net fees and expenses are not expected to increase for at least two years as a result of the Reorganization. The consummation of the Reorganization is contingent on shareholders of the Rainier Fund approving the Plan (the “Proposal”).

The Proxy Statement contains information that shareholders of the Rainier Fund should know before voting on the Proposal. The Proxy Statement should be reviewed and retained for future reference.

The Proposal requires the approval of Rainier Fund shareholders. Therefore, a Special Meeting of shareholders of the Rainier Fund (the “Special Meeting”) will be held on April 15, 2016 to consider the approval of the Proposal. We are sending this document to you for your use in deciding whether to approve the Proposal. This document includes a Notice of Special Meeting of Shareholders, the Proxy Statement and a proxy card.

Question: What is the purpose of the Reorganization?

Answer: As discussed in more detail in the Proxy Statement, the proposed Reorganization arises out of the anticipated resignation of the current portfolio managers (the “Portfolio Managers”) of the Rainier Fund from Rainier Investment Management, LLC, the Rainier Fund’s investment adviser (“Rainier”), and their joining Angel Oak. In light of this, the Board of Trustees of the Rainier Trust approved the Reorganization, subject to the approval of the shareholders of the Rainier Fund. Therefore, if shareholders approve the Reorganization, they should benefit from continuity of portfolio management; as further described in the Proxy Statement, the Portfolio Managers would manage the Acquiring Fund’s investments in substantially the same manner as they have the Rainier Fund, and the Acquiring Fund has an investment objective and principal investment strategies that are substantially similar to those of the Rainier Fund. Other potential benefits are discussed in more depth in the Proxy Statement.

Question: How will the Reorganizations work?

Answer: Pursuant to the Plan, the Rainier Fund will transfer all of its assets to the Acquiring Fund in return for Institutional Class and Class A shares of the Acquiring Fund and the Acquiring Fund’s assumption of all of the Rainier Fund’s liabilities as set forth in the Plan. The Rainier Fund will then distribute the Institutional Class and Class A shares it receives from the Acquiring Fund to holders of the Rainier Fund’s Institutional Shares and Original Shares, respectively.

Holders of Institutional Shares of the Rainier Fund will become Institutional Class shareholders of the Acquiring Fund and will receive Institutional Class shares of the Acquiring Fund in exchange for their Institutional Shares of the Rainier Fund. Holders of Original Shares of the Rainier Fund will become Class A shareholders of the Acquiring Fund and will receive Class A shares of the Acquiring Fund in exchange for their Original Shares of the Rainier Fund. Effective as of the closing date of the Reorganization (the “Closing Date”), each Rainier Fund shareholder will hold full and fractional Institutional Class and/or Class A shares of the Acquiring Fund equal in aggregate net asset value (“NAV”) to the aggregate NAV of such Rainier Fund shareholder’s Institutional Shares and Original Shares, respectively, of the Rainier Fund as of the Closing Date. Subsequently, the Rainier Fund will be liquidated and terminated as a series of the Rainier Trust.

PROPOSED REORGANIZATION |

| Rainier Fund: | à | Acquiring Fund: |

| | | |

| Rainier Investment Management Mutual Funds | | Angel Oak Funds Trust |

| Rainier High Yield Fund, Original Shares | à | Angel Oak High Yield Opportunities Fund, Class A |

| Rainier High Yield Fund, Institutional Shares | à | Angel Oak High Yield Opportunities Fund, Institutional Class |

Please refer to the Proxy Statement for a detailed explanation of the Proposal. If the Proposal is approved by shareholders of the Rainier Fund at the Special Meeting, the Reorganization presently is expected to take effect on or about April 15, 2016, or such other date as the parties may agree.

Question: How will the Reorganizations affect my investment?

Answer: Your investment in the Acquiring Fund following the Reorganization will be substantially similar to your current investment in the Rainier Fund. Immediately following the Reorganization, you will continue to be a shareholder in a class of shares of the Acquiring Fund with similar characteristics to the class of Rainier Fund shares in which you invested; however, the Acquiring Fund will be advised by Angel Oak, rather than Rainier. Holders of Original Shares of the Rainier Fund will receive Class A shares of the Acquiring Fund without being subject to the sales charge normally applicable to the purchase of Class A shares of the Acquiring Fund. Additionally, Rainier Fund shareholders who receive Class A shares of the Acquiring Fund will be permitted to purchase additional Class A shares of the Acquiring Fund in the future without being subject to the sales charge, provided that they have continuously held Class A shares of the Acquiring Fund since the Reorganization.

Although the investment adviser will change from Rainier to Angel Oak, the Portfolio Managers will continue to be primarily responsible for the day-to-day management of the Acquiring Fund’s portfolio immediately after the Reorganization, supported by certain additional Angel Oak portfolio managers.

In addition, although the Acquiring Fund’s investment objective will be the same as that of the Rainier Fund and its principal investment strategies will be substantially similar to those of the Rainier Fund, the Acquiring Fund will have different fundamental and non-fundamental investment restrictions and will be subject to a “manager-of-managers” exemptive order that will allow the Acquiring Fund to replace sub-advisers that are not affiliated with Angel Oak or the Acquiring Fund and to modify any existing or future sub-advisory agreement with such unaffiliated sub-advisers at any time without shareholder approval, subject to the approval of the Angel Oak Trust Board (though the Acquiring Fund currently has no plans to retain a sub-adviser).

The value of your investment in the Rainier Fund prior to the Reorganization will be the same as the value of your investment in the Acquiring Fund immediately following such Reorganization, and your interest in the Rainier Fund will not be diluted. The Reorganization will generally not result in recognition of gain or loss by the Rainier Fund, the Acquiring Fund or their shareholders for federal income tax purposes.

Question: Will I be charged any sales load, commission or other similar fee in connection with the Reorganization?

Answer: No. You will not be charged any sales load (including any deferred sales load), commission or other similar fee in connection with the Reorganization. Additionally, the Class A sales load, including any deferred sales load, will be waived for future purchases and redemptions of Class A shares of the Acquiring Fund by Rainier Fund shareholders who receive Class A shares of the Acquiring Fund as part of the Reorganization and have continuously held Class A shares of the Acquiring Fund since the Reorganization.

Question: Will the Reorganizations result in any taxes for the Rainier Fund, the Acquiring Fund or their shareholders?

Answer: If the Plan is carried out, none of the Rainier Fund, the Acquiring Fund or their shareholders will recognize any gain or loss for federal income tax purposes solely as a result of the Reorganization, except for (A) gain or loss that may be recognized on the transfer of “section 1256 contracts” as defined in Section 1256(b) of the Internal Revenue Code of 1986, as amended (the “Code”), (B) gain that may be recognized on the transfer of stock in a “passive foreign investment company” as defined in Section 1297(a) of the Code, and (C) any other gain or loss that may be required to be recognized upon the transfer of an asset regardless of whether such transfer would otherwise be a nonrecognition transaction under the Code. As a condition to the closing of the Reorganization, the Rainier Fund and the Acquiring Fund will receive an opinion of counsel confirming this position. Certain tax attributes of the Rainier Fund will carry over to the Acquiring Fund. Rainier Fund shareholders should consult their tax advisor about possible state and local tax consequences of the Reorganization, if any, because the information about tax consequences in this Proxy Statement relates to the federal income tax consequences of the Reorganization only.

Question: Why do I need to vote?

Answer: Your vote is needed to ensure that a quorum is present and sufficient votes are obtained at the Special Meeting so that the Proposal can be acted upon. Your immediate response on the enclosed proxy card will help prevent the need for any further solicitations for a shareholder vote. Your vote is very important to us regardless of the number of shares you own.

Question: How does the Rainier Trust’s Board recommend that I vote?

Answer: After careful consideration and upon the recommendation of Rainier, the Rainier Trust Board recommends that shareholders vote “FOR” the Proposal.

Question: Who is paying for expenses related to the Special Meeting and the Reorganizations?

Answer: Angel Oak will pay all direct costs relating to the Reorganization, including the costs relating to the Special Meeting and the Proxy Statement, but excluding brokerage and other transaction costs, which are not expected to be significant. Neither the Rainier Fund nor Acquiring Fund will incur any expenses in connection with the Reorganization.

Question: How do I vote my shares?

Answer: Although you may attend the Special Meeting and vote in person, you do not have to do so. You can vote your shares by completing and signing the enclosed proxy card(s) and mailing it in the enclosed postage-paid envelope. You may also vote by touch-tone telephone by calling the toll-free number printed on your proxy card(s) and following the recorded instructions.

If you simply sign and date the proxy card, but do not indicate a specific vote for the Proposal, your shares will be voted “FOR” the Proposal and to grant discretionary authority to the persons named in the card as to any other matters that properly come before the Special Meeting. Abstentions will be treated as present for determining whether a quorum is present with respect to a particular matter, but will not be counted as voting on any matter at the Special Meeting when the voting requirement is based on achieving a percentage of the “voting securities present.”

Shareholders who execute proxies may revoke them at any time before they are voted by (1) filing with the Rainier Fund a written notice of revocation, (2) timely voting a proxy bearing a later date, or (3) attending the Special Meeting and voting in person.

Question: If I vote by mail, how do I sign the proxy card?

Answer: Individual Accounts: Shareholders should sign exactly as their names appear on the account registration shown on the proxy card.

Joint Accounts: Either owner may sign, but the name of the person signing should conform exactly to a name shown on the account registration shown on the proxy card.

All Other Accounts: The person signing must indicate his or her capacity. For example, a trustee for a trust or other entity should sign, “Ann B. Collins, Trustee.”

Question: Who do I call if I have questions?

Answer: If you have any questions about the proposal or the proxy card, please do not hesitate to call 1-866-796-1288.

Please complete, sign and return the enclosed proxy card in the enclosed envelope. You may proxy vote by internet or telephone in accordance with the instructions set forth on the enclosed proxy card. No postage is required if mailed in the United States.

PROXY STATEMENT/PROSPECTUS

March 31, 2016

for the Reorganization of the

RAINIER HIGH YIELD FUND

(a series of Rainier Investment Management Mutual Funds)

601 Union Street, Suite 2801

Seattle, WA 98101

1-800-248-6314

into the

ANGEL OAK HIGH YIELD OPPORTUNITIES FUND

(a series of Angel Oak Funds Trust)

One Buckhead Plaza

3060 Peachtree Road NW, Suite 500

Atlanta, Georgia 30305

(404) 953-4900

This Proxy Statement/Prospectus (the “Proxy Statement”) is being sent to you in connection with the approval by the Board of Trustees (the “Board”) of Rainier Investment Management Mutual Funds (the “Rainier Trust”), a Delaware statutory trust, of an Agreement and Plan of Reorganization (the “Plan”) with respect to the Rainier High Yield Fund (the “Rainier Fund”), a series of the Rainier Trust. Pursuant to the Plan, the Rainier Fund would be reorganized (the “Reorganization”) into the Angel Oak High Yield Opportunities Fund (the “Acquiring Fund”), a series of Angel Oak Funds Trust (the “Angel Oak Trust”) advised by Angel Oak Capital Advisors, LLC (“Angel Oak”). The Reorganization is contingent on shareholders of the Rainier Fund approving the Plan.

Consequently, this Proxy Statement is being sent to you in connection with the solicitation of proxies by the Board of Trustees of the Rainier Trust, for exercise at a Special Meeting of Shareholders (the “Special Meeting”) of the Rainier Fund to be held on April 15, 2016, at 10:00 a.m., Pacific time, at Two Union Square, 601 Union Street, Suite 2801, Seattle, Washington 98101 to consider and vote on the following proposal (the “Proposal”) and to transact such other business as may properly come before the Special Meeting or any adjournments or postponements thereof:

PROPOSAL: To reorganize the Rainier High Yield Fund from a series of Rainier Investment Management Mutual Funds to a series of Angel Oak Funds Trust.

The Reorganization is not expected to result in any material change in the way the Rainier Fund is managed or in its investment objective and strategies. The Rainier Fund’s net fees and expenses are not expected to increase for at least two years as a result of the Reorganization.

Shareholders who authorize proxies may revoke them at any time before they are voted by writing to the Rainier Trust, by attending the Special Meeting in person, by authorizing a proxy at a later date through the toll-free number or through the Internet address listed in the enclosed voting instructions, or by submitting a later dated proxy card.

This Proxy Statement sets forth the information you should know before voting on the Proposal. You should read it and keep it for future reference. Additional information is set forth in the Statement of Additional Information (the “SAI”) dated March 31, 2016 relating to this Proxy Statement, which is also incorporated by reference into this Proxy Statement.

The Rainier Fund’s Summary Prospectus, Annual Report to Shareholders for the fiscal year ended March 31, 2015, containing audited financial statements, and Semi-Annual Report to Shareholders for the fiscal period ended September 30, 2015, containing unaudited financial statements, have been previously delivered to shareholders.

Copies of the Proxy Statement, SAI, Summary Prospectus or Prospectus, Annual Report to Shareholders for the most recent fiscal year, and Semi-Annual Report to Shareholders for the most recent fiscal period for the Rainier Fund and other information about the Rainier Fund, and the Rainier Trust are available upon request and without charge by calling 1-800-248-6314, by writing to the Rainier Fund, c/o U.S. Bancorp Fund Services, LLC, P.O. Box 701, Milwaukee, Wisconsin 53201-0701 or by visiting www.rainierfunds.com.

This Proxy Statement will be mailed on or about March 31, 2016 to shareholders of record of the Rainier Fund as of the close of business on February 19, 2016 (the “Record Date”).

The Rainier Fund and the Acquiring Fund are each subject to the informational requirements of the Securities Exchange Act of 1934 and in accordance therewith file reports and other information including proxy materials, reports and charter documents with the SEC. These reports and other information can be inspected and copied at the public reference facilities maintained by the SEC at 100 F Street, NE, Washington, DC 20549. Reports and other information about the Rainier Fund and Acquiring Fund are available on the EDGAR database on the SEC’s website at www.sec.gov. Copies of such material can also be obtained from the Public Reference Branch, Office of Consumer Affairs and Information Services, SEC, 100 F Street, NE, Washington, DC 20549 at prescribed rates.

The SEC has not approved or disapproved the Acquiring Fund’s shares to be issued in the Reorganizations, nor has it passed on the accuracy or adequacy of this Proxy Statement. Any representation to the contrary is a criminal offense.

No person has been authorized to give any information or to make any representations other than those contained in this Proxy Statement and in the materials expressly incorporated by reference herein and, if given or made, such other information or representations must not be relied upon as having been authorized by the Rainier Fund or Acquiring Fund.

| | | |

| | 2 |

| | | |

| | 19 |

| | | |

| | 21 |

| | | |

| | 21 |

| | | |

| | A-1 |

| | | |

| | B-1 |

| | | |

| | C-1 |

| | | |

| | D-1 |

| | | |

| | E-1 |

| | | |

| | F-1 |

| TO REORGANIZE THE RAINIER HIGH YIELD FUND FROM A SERIES OF RAINIER INVESTMENT MANAGEMENT MUTUAL FUNDS TO A SERIES OF ANGEL OAK FUNDS TRUST. |

You are receiving this Proxy Statement/Prospectus because of your investment in the Rainier Fund, which is advised by Rainier Investment Management, LLC (“Rainier”). As discussed in more detail below, the proposed Reorganization arises out of the anticipated resignation of Matthew R. Kennedy, CFA, Director of Fixed Income Management for Rainier, and James H. Hentges, CFA, Portfolio Manager for Rainier (together, the “Portfolio Managers”), who have managed the Fund since its inception in 2009, and the subsequent agreement (the “Agreement”) between Rainier and Angel Oak that provides, among other things, for the parties to support a reorganization of the Rainier Fund with and into the Acquiring Fund.

At a meeting of the Board of Rainier Trust held on January 12, 2016 (the “Meeting”), Rainier recommended, and the Board approved, the proposed reorganization of the Rainier Fund, one of the series of the Rainier Trust, with and into the Acquiring Fund, a newly created series of the Angel Oak Trust, subject to the approval of the Rainier Fund’s shareholders. In connection with the approval of the proposed Reorganization, the Board approved an Agreement and Plan of Reorganization (the “Plan”), which provides for: (a) the transfer of all the assets and liabilities of the Rainier Fund as set forth in the Plan to the Acquiring Fund, in exchange for shares of the Acquiring Fund; and (b) the distribution of the shares of the Acquiring Fund pro rata by the Rainier Fund to its shareholders in complete liquidation of the Rainier Fund.

The Acquiring Fund would commence operations upon the completion of the Reorganization, and would be advised by Angel Oak. The current Portfolio Managers of the Rainier Fund would be primarily responsible for the day-to-day management of the Acquiring Fund following the Reorganization. For more information regarding Rainier and Angel Oak, please see the section titled “Comparison of Investment Advisers and Investment Advisory Fees.”

The expected benefits of the proposed Reorganization are discussed elsewhere in this Proxy Statement and include the following:

| ● | the continuity of the portfolio management team and investment objective and principal investment strategies through the retention of the Portfolio Managers as Portfolio Managers to the Acquiring Fund; |

| | ● | the net fees and expenses of the Acquiring Fund will be no higher than those of the Rainier Fund for at least 2 years; and |

| ● | the expected tax-free nature of the Reorganization for U.S. federal income tax purposes. |

For a detailed discussion of the Board’s considerations, see the section titled “Board Consideration of the Reorganization.”

How Will The Reorganization Work?

Subject to the terms and conditions of the Plan, the Reorganization will involve three steps:

| ● | the transfer of all the assets and liabilities of the Rainier Fund to the Acquiring Fund, as set forth in the Plan, in exchange for shares of the Acquiring Fund having equivalent value to the net assets transferred; |

| ● | the pro rata distribution of shares of the Acquiring Fund to the shareholders of record of the Rainier Fund as of the effective date of the Reorganization in full redemption of all shares of the Rainier Fund; and |

| ● | the complete liquidation and termination of the Rainier Fund. |

As a result of the Reorganization, shareholders of the Rainier Fund’s Institutional Shares and Original Shares will hold Institutional Class and Class A shares of the Acquiring Fund, respectively. The total value of the shares of the Acquiring Fund that a shareholder will receive in the Reorganization will be the same as the total value of the shares of the Rainier Fund held by the shareholder immediately before the Reorganization. If approved by shareholders, the Reorganization is expected to occur on or about April 15, 2016. The class structure of the Acquiring Fund is similar to that of the Rainier Fund, but there are important differences. Information about the class structure of the Rainier Fund and Acquiring Fund is below under “Comparison of Current Fees and Expenses.”

What Differences Are There in the Management Structure of the Rainier Fund and the Acquiring Fund?

Rainier serves as the investment adviser to the Rainier Fund, and the Portfolio Managers are primarily responsible for the day-to-day portfolio management of the Rainier Fund. Following the Reorganization, Angel Oak will serve as the investment adviser of the Acquiring Fund, and the Portfolio Managers will continue to be primarily responsible for the day-to-day portfolio management of the Acquiring Fund, supported by additional Angel Oak portfolio managers. Neither the Rainier Fund, nor the Acquiring Fund currently employs any sub-advisory firms.

Currently, the Rainier Trust Board may terminate any investment adviser or sub-adviser of the Rainier Fund without shareholder approval. The Rainier Trust Board may replace any investment adviser or sub-adviser of the Rainier Fund with another party only with the approval of shareholders.

Similarly, the Angel Oak Trust Board may terminate any investment adviser or sub-adviser of the Acquiring Fund without shareholder approval. However, pursuant to a “manager-of-managers” exemptive order granted to the Acquiring Fund and Angel Oak by the SEC, the Acquiring Fund may replace sub-advisers that are not affiliated with Angel Oak or the Acquiring Fund and may modify any existing or future sub-advisory agreement with such unaffiliated sub-advisers at any time without shareholder approval, subject to the approval of the Angel Oak Trust Board. The Angel Oak Trust Board may replace the Acquiring Fund’s investment adviser only with the approval of shareholders.

Prior to the Reorganization, the sole initial shareholder of the Acquiring Fund will have approved the Acquiring Fund’s participation in this manager-of-managers arrangement, and shareholders of the Rainier Fund, including in their ultimate capacities as shareholders of the Acquiring Fund, will not be asked to vote on this matter.

Additional information regarding the manager-of-managers exemptive order is included in the attached Appendix F.

Please note that the investment objective of the Acquiring Fund will be the same as that of the Rainier Fund. Additionally, the principal investment strategies of the Acquiring Fund will be substantially similar to those of the Rainier Fund, and the differences between them are described below under “Comparison of Investment Objectives, Principal Investment Strategies and Policies.”

However, the Acquiring Fund will have different fundamental and non-fundamental investment restrictions (to modernize those restrictions and make them more consistent with other series of the Angel Oak Trust) and will be subject to a “manager-of-managers” exemptive order that will allow the Acquiring Fund to replace sub-advisers that are not affiliated with Angel Oak or the Acquiring Fund and to modify any existing or future sub-advisory agreement with such unaffiliated sub-advisers at any time without shareholder approval, subject to the approval of the Angel Oak Trust Board (though the Acquiring Fund currently has no plans to retain a sub-adviser).

What is the Effect of My Voting “FOR” the Proposal?

By voting “FOR” the Proposal, you will be agreeing to become a shareholder of the Acquiring Fund. As a result, you are agreeing to all of the features of the Acquiring Fund.

In the event that shareholders of the Rainier Fund do not approve the Proposal, the Board in consultation with Rainier, will consider the options available to the Rainier Fund, including its possible liquidation or retention of another investment adviser.

Shareholder Approval

Approval of the Proposal requires the affirmative vote of the holders of a majority of the outstanding shares of the Rainier Fund, as defined in the Investment Company Act of 1940, as amended (the “1940 Act”). Please see the section entitled “Information on Voting” for more details.

Comparison of Current Fees and Expenses

The following tables describe the fees and expenses associated with holding shares of the Rainier Fund and Acquiring Fund. In particular, the tables compare the fee and expense information for the shares of the Rainier Fund and the pro forma estimated fees and expenses of shares of the Acquiring Fund following the Reorganization. The information shown in these tables is as of February 29, 2016. Pro forma expense ratios of the Acquiring Fund shown should not be considered an actual representation of future expenses or performance. Such pro forma expense ratios of the Acquiring Fund project anticipated expense levels, but actual ratios may be greater or less than those shown. Although the Total Annual Fund Operating Expenses for the Acquiring Fund are expected to initially be substantially higher than those of the Rainier Fund, the Total Annual Fund Operating Expenses After Fee Waiver/Expense Reimbursement paid by the Acquiring Fund through May 31, 2018 will be the same as or lower than the net annual operating expense ratio currently paid by the Fund. Additionally, to the extent Angel Oak is successful at using its distribution capabilities to help the Acquiring Fund to experience asset growth, Angel Oak expects that such growth will lead to lower Total Annual Fund Operating Expenses over time.

Expense Summary of the Rainier Fund and the Acquiring Fund

| Shareholder fees (fees paid directly from your investment) | | Rainier Fund Institutional Shares | | (pro forma) Acquiring Fund Institutional Class | | Rainier Fund Original Shares | | (pro forma) Acquiring Fund Class A |

| Maximum Sales Charge (Load) Imposed on Purchases (as a % of the offering price) | | None | | None | | None | | 2.25%1 |

| Maximum Deferred Sales Charge (Load) (as a % of amount redeemed) | | None | | None | | None | | None1 |

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

| Management Fees | | 0.55% | | 0.55% | | 0.55% | | 0.55% |

| Distribution and Service (12b-1) Fees | | 0.00% | | 0.00% | | 0.25% | | 0.25% |

| Other Expenses | | 0.19% | | 0.49%2 | | 0.31% | | 0.49%2 |

| Total Annual Fund Operating Expenses | | 0.74% | | 1.04% | | 1.11% | | 1.29% |

Less Fee Waiver/Expense Reimbursement | | -0.09%3 | | -0.39%4 | | -0.21%3 | | -0.39%4 |

Total Annual Fund Operating Expenses After Fee Waiver/Expense Reimbursement | | 0.65% | | 0.65% | | 0.90% | | 0.90% |

| 1 | Class A shares purchased without an initial sales charge and redeemed within 18 months of the date of purchase may be subject to a contingent deferred sales charge of 1.00%. The Class A sales charge (load), including any deferred sales load, will be waived for future purchases and redemptions of Class A shares of the Acquiring Fund by Rainier Fund shareholders who receive Class A shares of the Acquiring Fund as part of the Reorganization and have continuously held Class A shares of the Acquiring Fund since the Reorganization. |

| 2 | “Other Expenses” for the Acquiring Fund have been restated to reflect changes in the contractual fees paid by the Fund to its service providers. |

| 3 | Rainier has contractually agreed to reduce its fees and/or pay Fund expenses in order to limit Total Annual Fund Operating Expenses After Fee Waiver/Expense Reimbursement for shares of the Rainier Fund to 0.65% and 0.90% of the Rainier Fund’s average net assets of its Institutional and Original Shares, respectively (the “Expense Caps”). This obligation excludes acquired fund fees and expenses, loads, taxes, interest, brokerage commissions, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation, and other expenses not incurred in the ordinary course of the Rainier Fund’s business. The Expense Caps will remain in effect until at least July 31, 2016. Rainier may request recoupment of previously waived fees and paid expenses from the Rainier Fund for three years from the date they were waived or paid, subject to the Expense Caps. The Expense Caps may not be changed by Rainier during that period without prior approval of the Board. The obligation may be terminated at any time by the Board upon written notice to Rainier, and will terminate if the management agreement is terminated. |

| 4 | Angel Oak has contractually agreed to waive its fees and/or reimburse certain expenses (exclusive of any front-end sales loads, taxes, interest on borrowings, dividends on securities sold short, brokerage commissions, 12b-1 fees, acquired fund fees and expenses, expenses incurred in connection with any merger or reorganization and extraordinary expenses) to limit the Total Annual Fund Operating Expenses After Fee Waiver/Expense Reimbursement to 0.65% of the Acquiring Fund’s average daily net assets (the “Expense Limit”) through May 31, 2018. The contractual arrangement may only be changed or eliminated by the Board of Trustees of the Angel Oak Trust upon 60 days’ written notice to Angel Oak. Angel Oak may recoup from the Acquiring Fund any waived amount or reimbursed expenses pursuant to this agreement if such recoupment does not cause the Acquiring Fund to exceed the lesser of (i) the Expense Limit in effect at the time of the waiver or reimbursement and (ii) the Expense Limit in effect at the time of recoupment and the recoupment is made within three years after the fiscal year in which Angel Oak incurred the expense. |

Holders of the Rainier Fund’s Original Shares will not be charged any sales load in connection with their receipt of Class A shares of the Acquiring Fund as a result of the Reorganization. Additionally, the Class A sales charge (load), including any deferred sales load, will be waived for future purchases and redemptions of Class A shares of the Acquiring Fund by Rainier Fund shareholders who receive Class A shares of the Acquiring Fund as part of the Reorganization and have continuously held Class A shares of the Acquiring Fund since the Reorganization.

You would pay the following expenses on a $10,000 investment assuming that the Rainier Fund and Acquiring Fund have a 5% annual return, that fund operating expenses remain the same, and that you redeem your shares at the end of each period. The pro forma Class A expenses below do not reflect the sales charge (load) on Class A shares because such sales charge (load) will be waived for future purchases of Class A shares of the Acquiring Fund by Rainier Fund shareholders who receive Class A shares of the Acquiring Fund as part of the Reorganization and have continuously held Class A shares of the Acquiring Fund since the Reorganization. Your actual costs may be higher or lower than those shown. The expenses below reflect the Expense Caps and Expense Limit for the first two years only.

| | | One Year | | Three Years | | Five Years | | Ten Years |

| Rainier Fund Institutional Shares | | $66 | | $218 | | $393 | | $901 |

Acquiring Fund Institutional Class shares (pro forma) | | $66 | | $251 | | $496 | | $1,198 |

| | | | | | | | | |

| Rainier Fund Original Shares | | $92 | | $310 | | $570 | | $1,313 |

Acquiring Fund Class A shares (pro forma) | | $92 | | $330 | | $631 | | $1,486 |

The Acquiring Fund also offers Class C shares subject to a maximum 1.00% contingent deferred sales charge on shares redeemed within one year of purchase and a 1.00% distribution and service (12b-1) fee; however, Class C shares of the Acquiring Fund are not being offered or issued as part of the Reorganization and are not currently available for purchase.

Portfolio Turnover

Each of the Rainier Fund and Acquiring Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual operating expenses or in the example above, affect the funds’ performance. During the most recent fiscal year ended March 31, 2015, the portfolio turnover rate for the Rainier Fund was 33.69% of the average value of its portfolio. Because the Acquiring Fund will not have commenced operations prior to the Reorganization, no portfolio turnover information is available for the Acquiring Fund.

Comparison of Investment Objectives, Principal Investment Strategies, and Policies

The investment objective of the Rainier Fund is to earn a high level of current income with a secondary objective of capital appreciation. The investment objective and the Portfolio Managers with primary responsibility for the day-to-day portfolio management of the Acquiring Fund will be the same as those of the Rainier Fund.

The principal investment strategies of the Acquiring Fund will be the same as those of the Rainier Fund, except for the following additional principal investment strategies of the Acquiring Fund:

| | ● | The Acquiring Fund’s allocation of its assets into various asset classes will depend on the views of Angel Oak as to the best value relative to what is currently presented in the market place. Investment decisions are made based on fundamental research and analysis to identify issuers with the ability to improve their credit profile over time with attractive valuations, resulting in both income and potential capital appreciation. The Acquiring Fund’s portfolio managers lead a team of sector specialists responsible for researching opportunities within their sector and making recommendations to the Acquiring Fund’s portfolio managers. In selecting investments, Angel Oak may consider maturity, yield and ratings information and opportunities for price appreciation among other criteria. Angel Oak seeks to limit risk of principal by targeting assets that it considers undervalued. |

| | ● | The Fund may invest up to 15% of its net assets in illiquid private placements, Rule 144A securities, and securities of issuers that are bankrupt or in default that may be deemed to be illiquid. |

| | ● | The Acquiring Fund may invest in other investment companies, including closed-end investment companies and open-end investment companies, which may operate as traditional mutual funds or as ETFs. The other investment companies in which the Acquiring Fund invests may be affiliates of the Acquiring Fund. The Fund’s investments in other investment companies that primarily invest in below investment grade bonds of corporate issuers are counted towards the Fund’s 80% policy. For purposes of the Fund’s investment policies, the Fund’s investments in other investment companies are deemed to be investments in the type securities in which such other investment companies principally invest (e.g., the Fund’s investments in other investment companies that primarily invest in below investment grade bonds of corporate issuers are counted towards the Fund’s 80% policy). |

| | ● | In pursuing its investment objectives or for hedging purposes, the Acquiring Fund may utilize borrowing. Additionally, the Acquiring Fund may invest in credit default swaps, interest rate swaps, currency swaps, total return swaps, futures and forward contracts, and options. Such derivatives may trade over-the-counter or on an exchange and may principally be used for one or more of the following purposes: speculation, currency hedging, duration management, or to pursue the Acquiring Fund’s investment objective. The Acquiring Fund may borrow to the maximum extent permitted by applicable law, which generally means that the Acquiring Fund may borrow up to one-third of its total assets. The Acquiring Fund may also invest in repurchase agreements and reverse repurchase agreements. |

The Acquiring Fund’s use of borrowing, derivatives, and reverse repurchase agreements may be deemed to create leverage, which can increase the Acquiring Fund’s volatility and the effect, positive or negative, of the Acquiring Fund’s investments and its net asset value (“NAV”). The 1940 Act generally limits the extent to which the Acquiring Fund may utilize borrowings and “uncovered” transactions that may give rise to a form of leverage, including reverse repurchase agreements, dollar rolls, swaps, futures and forward contracts, options and other derivative transactions, to one-third of the Acquiring Fund’s total assets at the time utilized.

Derivatives, which are instruments that have a value based on another instrument, exchange rate or index, may be used as substitutes for securities in which the Acquiring Fund can invest. The Acquiring Fund uses derivatives to gain or adjust exposure to markets, sectors, securities and currencies and to manage exposure to risks relating to creditworthiness, interest rate spreads, volatility and changes in yield curves. In certain market environments, the Acquiring Fund may use interest rate swaps and futures contracts to help protect its portfolio from interest rate risk. The Acquiring Fund may also utilize foreign currency transactions, including currency options and forward currency contracts, to hedge non-U.S. Dollar investments or to establish or adjust exposure to particular foreign securities, markets or currencies.

| ● | The Acquiring Fund may invest in bank subordinated debt. |

| ● | The Acquiring Fund and Angel Oak have received exemptive relief from the SEC permitting Angel Oak (subject to certain conditions and the Angel Oak Trust Board’s approval) to select or change sub-advisers without obtaining shareholder approval. The relief also permits Angel Oak to materially amend the terms of agreements with a sub-adviser (including an increase in its fee) or to continue the employment of a sub-adviser after an event that would otherwise cause the automatic termination of services with Board approval, but without shareholder approval. Shareholders will be notified of any sub-adviser changes. The Acquiring Fund currently has no plans to retain a sub-adviser. |

The Acquiring Fund’s ability to use borrowing and various types of derivative instruments as part of its principal investment strategies is intended to provide the Fund’s portfolio management team with greater flexibility in managing the risks and exposures of the Acquiring Fund as compared to the Rainier Fund.

The Acquiring Fund will also have different fundamental and non-fundamental investment restrictions. Although there are differences in the fundamental investment restrictions of the Rainier Fund and the Acquiring Fund, because the Rainier Fund and Acquiring Fund have substantially similar investment strategies and policies, Angel Oak expects that the differences in investment restrictions will have little or no substantive effect. For more information regarding the investment restrictions of the Rainier Fund and the Acquiring Fund, please see the section titled “Comparison of Investment Restrictions.”

Summary of Principal Investment Strategies

The following describes the principal investment strategies of the Acquiring Fund. Additional information on the principal investment strategies of the Acquiring Fund is included in the attached Appendix B.

The Acquiring Fund’s allocation of its assets into various asset classes will depend on the views of the Adviser as to the best value relative to what is currently presented in the market place. Investment decisions are made based on fundamental research and analysis to identify issuers with the ability to improve their credit profile over time with attractive valuations, resulting in both income and potential capital appreciation. The Acquiring Fund’s portfolio managers lead a team of sector specialists responsible for researching opportunities within their sector and making recommendations to the Acquiring Fund’s portfolio managers. In selecting investments, the Adviser may consider maturity, yield and ratings information and opportunities for price appreciation among other criteria. The Adviser seeks to limit risk of principal by targeting assets that it considers undervalued.

The Acquiring Fund may sell a security if the Adviser no longer believes it is undervalued or if the Adviser believes that a different security will better help the Fund achieve its investment objective. if it achieves the valuation target or the underlying fundamentals deteriorate compared to the Adviser’s expectations, or when swapped for a more attractive security.

In pursuing its objective, the Acquiring Fund normally invests at least 80% of its net assets, plus any borrowings for investment purposes, in below investment grade bonds of corporate issuers. These “high-yield” securities (also known as “junk bonds”) will generally be rated BB or lower by Standard & Poor’s Rating Group (“S&P”) or will be of equivalent quality rating from another Nationally Recognized Statistical Ratings Organization. If a bond is unrated, Angel Oak Capital Advisors, LLC (the “Adviser”), the investment adviser to the Acquiring Fund, may determine whether it is of comparable quality and therefore eligible for the Acquiring Fund’s investment.

The Acquiring Fund may purchase securities of companies in any capitalization range – small, medium or large. The Acquiring Fund’s principal investments include domestic corporate debt securities, collateralized loan obligations (“CLOs”), asset-backed fixed income securities, mortgage-backed securities, foreign debt securities (including corporate fixed income securities registered and sold in the United States by foreign issuers (“Yankee” bonds)), fixed and floating rate bonds, as well as zero coupon bonds. The Acquiring Fund intends to focus primarily on securities with credit ratings (or equivalent quality) between the range of BB and B of the high-yield market. However, the Acquiring Fund may invest in or continue to hold securities that have credit ratings lower than B, no longer make payments of interest or principal, or are in payment default. The Acquiring Fund may also invest in bank subordinated debt.

The Acquiring Fund may also invest in private placements and “Rule 144A” securities, which are subject to resale restrictions. The Acquiring Fund is permitted to invest up to 15% of its net assets in equity securities such as common stock, preferred stock, warrants, rights and exchange-traded funds (“ETFs”). The Acquiring Fund may also invest up to 20% of its assets in investment grade securities, including U.S. Treasury and U.S. government agency securities. The Acquiring Fund may invest up to 25% of its assets in foreign debt securities (including Yankee bonds), including those denominated in U.S. dollars. The Acquiring Fund may invest up to 15% of its net assets in illiquid private placements, Rule 144A securities, and securities of issuers that are bankrupt or in default that may be deemed to be illiquid. The Acquiring Fund may also invest in the securities of other investment companies that invest primarily in high-yield securities.

The Acquiring Fund may purchase bonds of any maturity, but the Acquiring Fund will normally have a dollar-weighted average maturity between two and fifteen years. The average maturity may be less than two years if the Adviser believes a temporary defensive posture is appropriate. In addition, duration may be one of the characteristics considered in security selection, but the Acquiring Fund does not focus on bonds with any particular duration. Duration is a measure of interest rate risk using the expected life of a debt security. Duration incorporates a bond’s yield, coupon interest payments, final maturity, call and put features and prepayment exposure into one measure, with a higher duration indicating greater sensitivity to interest rates.

In pursuing its investment objectives or for hedging purposes, the Acquiring Fund may utilize borrowing. Additionally, the Acquiring Fund may invest in credit default swaps, interest rate swaps, currency swaps, total return swaps, futures and forward contracts, and options. Such derivatives may trade over-the-counter or on an exchange and may principally be used for one or more of the following purposes: speculation, currency hedging, duration management, or to pursue the Acquiring Fund’s investment objective. The Acquiring Fund may borrow to the maximum extent permitted by applicable law, which generally means that the Acquiring Fund may borrow up to one-third of its total assets. The Acquiring Fund may also invest in repurchase agreements and reverse repurchase agreements.

Comparison and Summary of Principal Investment Risks

The principal investment risks of the Acquiring Fund will be the same as those of the Rainier Fund, except for certain additional principal investment risks of the Acquiring Fund. The following is a summary of the principal investment risks of the Acquiring Fund. Risks marked with an “*” reflect risks that have been identified as “Principal Investment Risks” of the Acquiring Fund that are not currently identified as “Principal Investment Risks” of the Rainier Fund. Additional information on the principal investment risks of the Acquiring Fund is included in the attached Appendix B.

| ● | Bank Subordinated Debt Risks.* Banks may issue subordinated debt securities, which have a lower priority to full payment behind other more senior debt securities. In addition to the risks generally associated with fixed income instruments (e.g., interest rate risk, credit risk, etc.), bank subordinated debt is also subject to risks inherent to banks. Because banks are highly regulated and operate in a highly competitive environment, it may be difficult for a bank to meet its debt obligations. Banks also may be affected by changes in legislation and regulations applicable to the financial markets. Bank subordinated debt is often issued by smaller community banks that may be overly concentrated in a specific geographic region, lack the capacity to comply with new regulatory requirements or lack adequate capital. |

| | ● | Borrowing Risks and Leverage Risks.* Borrowing for investment purposes creates leverage (i.e., exposure to potential gain or loss that exceeds the exposure created by investing the amount of the Fund’s net assets), which will exaggerate the effect of any change in the value of securities in the Fund’s portfolio on the Fund’s NAV and, therefore, may increase the volatility of the Fund. |

| | ● | CLO and Collateralized Debt Obligations (“CDOs”) Risks.* CLOs and other CDOs are subject to the typical risks associated with fixed-income securities and asset-backed securities. Additionally, the risks of an investment in a CLO or other CDO depend largely on the type of the collateral securities and the class of the CLO or other CDO in which the Fund invests. Such collateral may be insufficient to meet payment obligations and the class of the CLO or other CDO may be subordinate to other classes. CLOs and other CDOs are typically privately offered and sold, and thus, are not registered under the securities laws. As a result, investments in certain CLOs and other CDOs may be characterized by the Acquiring Fund as illiquid securities. |

| | ● | Derivatives Risks.* The Acquiring Fund’s derivative investments have risks, including the imperfect correlation between the value of such instruments and the underlying assets, rate or index; the loss of principal, including the potential loss of amounts greater than the initial amount invested in the derivative instrument; the possible default of the other party to the transaction; and illiquidity of the derivative investments. If a counterparty becomes bankrupt or otherwise fails to perform its obligations under a derivative contract due to financial difficulties, the Acquiring Fund may experience significant delays in obtaining any recovery under the derivative contract in a bankruptcy or other reorganization proceeding. Certain derivatives may give rise to a form of leverage. Leverage magnifies the potential for gain and the risk of loss. Certain of the Acquiring Fund’s transactions in derivatives could also affect the amount, timing and character of distributions to shareholders, which may result in the Acquiring Fund realizing more short-term capital gain and ordinary income subject to tax at ordinary income tax rates than it would if it did not engage in such transactions, which may adversely impact the Acquiring Fund’s after-tax returns. |

| | The derivative instruments and techniques that the Acquiring Fund may principally use include: |

| | ○ | Futures. A futures contract is a standardized agreement to buy or sell a specific quantity of an underlying instrument at a specific price at a specific future time. A decision as to whether, when and how to use futures involves the exercise of skill and judgment and even a well-conceived futures transaction may be unsuccessful because of market behavior or unexpected events. In addition to the derivatives risks discussed above, the prices of futures can be highly volatile, using futures can lower total return, and the potential loss from futures can exceed the Acquiring Fund’s initial investment in such contracts. |

| | ○ | Options. If the Acquiring Fund buys an option, it buys a legal contract giving it the right to buy or sell a specific amount of the underlying instrument or futures contract on the underlying instrument at an agreed-upon price typically in exchange for a premium paid by the Acquiring Fund. If the Acquiring Fund sells an option, it sells to another person the right to buy from or sell to the Acquiring Fund a specific amount of the underlying instrument or futures contract on the underlying instrument at an agreed-upon price typically in exchange for a premium received by the Acquiring Fund. A decision as to whether, when and how to use options involves the exercise of skill and judgment and even a well-conceived option transaction may be unsuccessful because of market behavior or unexpected events. The prices of options can be highly volatile and the use of options can lower total returns. |

| | ○ | Swaps. A swap contract is an agreement between two parties pursuant to which the parties exchange payments at specified dates on the basis of a specified notional amount, with the payments calculated by reference to specified securities, indexes, reference rates, currencies or other instruments. Swap agreements are particularly subject to counterparty credit, liquidity, valuation, correlation and leverage risk. Swaps could result in losses if interest rate or foreign currency exchange rates or credit quality changes are not correctly anticipated by the Acquiring Fund or if the reference index, security or investments do not perform as expected. The use of credit default swaps can result in losses if the Acquiring Fund’s assumptions regarding the creditworthiness of the underlying obligation prove to be incorrect. |

| ● | Equity and General Market Risk. Equity securities are susceptible to general stock market fluctuations and to volatile increases and decreases in value. The equity market may experience declines and companies whose equity securities are in the Fund’s portfolio may not increase their earnings at the rate anticipated. The Fund’s net asset value and investment return will fluctuate based upon changes in the value of its portfolio securities. |

| ● | Extension Risk.* When interest rates rise, certain obligations may be paid off by the obligor more slowly than anticipated, causing the value of these securities to fall. |

| ● | Fixed-Income Instruments Risks. The Fund will invest in fixed-income instruments and securities. Such investments may be secured, partially secured or unsecured and may be unrated, and whether or not rated, may have speculative characteristics. The market price of the Fund’s investments will change in response to changes in interest rates and other factors. Generally, when interest rates rise, the values of fixed-income instruments fall, and vice versa. In typical interest rate environments, the prices of longer-term fixed-income instruments generally fluctuate more than the prices of shorter-term fixed-income instruments as interest rates change. These risks may be greater in the current market environment because certain interest rates are near historically low levels. In addition, a fund with a longer average portfolio duration will be more sensitive to changes in interest rates than a fund with a shorter average portfolio duration. A fund with a negative average portfolio duration may decline in value as interest rates decrease. Most high yield investments pay a fixed rate of interest and are therefore vulnerable to inflation risk. The obligor of a fixed-income instrument may not be able or willing to pay interest or to repay principal when due in accordance with the terms of the associated agreement. |

| | ● | Floating or Variable Rate Securities Risk.* Floating or variable rate securities pay interest at rates that adjust in response to changes in a specified interest rate or reset at predetermined dates (such as the end of a calendar quarter). Securities with floating or variable interest rates are generally less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value if their interest rates do not rise as much, or as quickly, as comparable market interest rates. Although floating or variable rate securities are generally less sensitive to interest rate risk than fixed rate securities, they are subject to credit, liquidity and default risk and may be subject to legal or contractual restrictions on resale, which could impair their value. |

| ● | Foreign Securities Risks. Investments in securities or other instruments of non-U.S. issuers involve certain risks not involved in domestic investments and may experience more rapid and extreme changes in value than investments in securities of U.S. companies. Financial markets in foreign countries often are not as developed, efficient or liquid as financial markets in the United States, and therefore, the prices of non-U.S. securities and instruments can be more volatile. In addition, the Fund will be subject to risks associated with adverse political and economic developments in foreign countries, which may include the imposition of economic sanctions. Generally, there is less readily available and reliable information about non-U.S. issuers due to less rigorous disclosure or accounting standards and regulatory practices. |

| | ● | High-Yield Securities Risks. High-yield securities (also known as “junk bonds”) carry a greater degree of risk and are more volatile than investment grade securities and are considered speculative. High-yield securities may be issued by companies that are restructuring, are smaller and less creditworthy, or are more highly indebted than other companies. This means that they may have more difficulty making scheduled payments of principal and interest. Changes in the value of high-yield securities are influenced more by changes in the financial and business position of the issuing company than by changes in interest rates when compared to investment grade securities. The Fund’s investments in high-yield securities expose it to a substantial degree of credit risk. |

| ● | Illiquid Securities Risks.* The Fund may, at times, hold illiquid securities, by virtue of the absence of a readily available market for certain of its investments, or because of legal or contractual restrictions on sales. The Fund could lose money if it is unable to dispose of an investment at a time or price that is most beneficial to the Fund. |

| ● | Management Risk. The Fund may not meet its investment objective based on Angel Oak’s success or failure to implement investment strategies for the Fund. |

| ● | Mortgage-Backed and Asset-Backed Securities Risks.* Mortgage-backed and other asset-backed securities are subject to the risks of traditional fixed-income instruments. However, they are also subject to prepayment risk and extension risk, meaning that if interest rates fall, the underlying debt may be repaid ahead of schedule, reducing the value of the Fund’s investments and if interest rates rise, there may be fewer prepayments, which would cause the average bond maturity to rise, increasing the potential for the Fund to lose money. |

Certain mortgage-backed securities may be secured by pools of mortgages on single-family, multi-family properties, as well as commercial properties. Similarly, asset-backed securities may be secured by pools of loans, such as corporate loans, student loans, automobile loans and credit card receivables. The credit risk on such securities is affected by homeowners or borrowers defaulting on their loans. The values of assets underlying mortgage-backed and asset-backed securities, including CLOs, may decline and therefore may not be adequate to cover underlying investors. Some mortgage-backed and asset-backed securities have experienced extraordinary weakness and volatility in recent years. Possible legislation in the area of residential mortgages, credit cards, corporate loans and other loans that may collateralize the securities in which the Fund may invest could negatively impact the value of the Fund’s investments. To the extent the Fund focuses its investments in particular types of mortgage-backed or asset-backed securities, including CLOs, the Fund may be more susceptible to risk factors affecting such types of securities.

| | ● | Other Investment Companies Risks. The Fund will incur higher and duplicative expenses when it invests in mutual funds, ETFs, and other investment companies. There is also the risk that the Fund may suffer losses due to the investment practices of the underlying funds. When the Fund invests in other investment companies, the Fund will be subject to substantially the same risks as those associated with the direct ownership of securities held by such investment companies. ETFs may be less liquid than other investments, and thus their share values more volatile than the values of the investments they hold. Investments in ETFs are also subject to the following risks: (i) the market price of an ETF’s shares may trade above or below their net asset value; (ii) an active trading market for an ETF’s shares may not develop or be maintained; and (iii) trading of an ETF’s shares may be halted for a number of reasons. |

| | ● | Preferred Securities Risk.* Preferred securities may pay fixed or adjustable rates of return and are subject to many of the risks associated with debt securities (e.g., interest rate risk, call risk and extension risk). In addition, preferred securities are subject to issuer-specific and market risks applicable generally to equity securities. Because many preferred securities allow the issuer to convert their preferred stock into common stock, preferred securities are often sensitive to declining common stock values. A company’s preferred securities generally pay dividends only after the company makes required payments to holders of its bonds and other debt. For this reason, the value of preferred securities will usually react more strongly than bonds and other debt to actual or perceived changes in the company’s financial condition or prospects. Preferred securities of smaller companies may be more vulnerable to adverse developments than preferred stock of larger companies. |

| ● | Prepayment Risk.* When interest rates decline, fixed income securities with stated interest rates may have the principal paid earlier than expected, requiring the Acquiring Fund to invest the proceeds at generally lower interest rates. |

| ● | Rating Agencies Risks.* Ratings are not an absolute standard of quality, but rather general indicators that reflect only the view of the originating rating agencies from which an explanation of the significance of such ratings may be obtained. There is no assurance that a particular rating will continue for any given period of time or that any such rating will not be revised downward or withdrawn entirely. Such changes may negatively affect the liquidity or market price of the securities in which the Fund invests. The ratings of securitized assets may not adequately reflect the credit risk of those assets due to their structure. |

| ● | Repurchase Agreement Risks.* Repurchase agreements typically involve the acquisition by the Fund of fixed-income securities from a selling financial institution such as a bank or broker-dealer. The Fund may incur a loss if the other party to a repurchase agreement is unwilling or unable to fulfill its contractual obligations to repurchase the underlying security. |

| ● | Reverse Repurchase Agreement Risks.* A reverse repurchase agreement is the sale by the Fund of a debt obligation to a party for a specified price, with the simultaneous agreement by the Fund to repurchase that debt obligation from that party on a future date at a higher price. Similar to borrowing, reverse repurchase agreements provide the Fund with cash for investment purposes, which creates leverage and subjects the Fund to the risks of leverage. Reverse repurchase agreements also involve the risk that the other party may fail to return the securities in a timely manner or at all. The Fund could lose money if it is unable to recover the securities and/or if the value of collateral held by the Fund, including the value of the investments made with cash collateral, is less than the value of securities. |

| ● | RIC-Related Risks of Investments Generating Non-Cash Taxable Income.* Certain of the Fund’s investments will require the Fund to recognize taxable income in excess of the cash generated on those investments in that tax year, which could cause the Fund to have difficulty satisfying the annual distribution requirements applicable to regulated investment companies (“RICs”) and avoiding Fund-level U.S. federal income and/or excise taxes. |

| ● | Risks Relating to Fund’s RIC Status.* To qualify and remain eligible for the special tax treatment accorded to a RIC and its shareholders under the Internal Revenue Code of 1986, as amended, the Fund must meet certain source-of-income, asset diversification and annual distribution requirements. If the Fund fails to qualify as a RIC for any reason and becomes subject to corporate tax, the resulting corporate taxes could substantially reduce its net assets, the amount of income available for distribution and the amount of its distributions. |

| ● | Sector Risk.* To the extent the Acquiring Fund invests more heavily in particular sectors of the economy, its performance will be especially sensitive to developments that significantly affect those sectors. |