As publicly filed with the Securities and Exchange Commission on April 7, 2016

Registration No. 333-203044

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT 7 TO

FORM F-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

ECOLOMONDO CORPORATION INC.

(Exact name of registrant as specified in its charter)

| Canada | 3559 | Not applicable |

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer Identification No.) |

| incorporation or organization) | Classification Code Number) |

Ecolomondo Corporation Inc.

3435 Pitfield Blvd.

St. Laurent, Quebec

Canada H4S 1H7

450-587-5999

(Address, including zip code, and telephone number, including area code,

of registrant’s principal executive offices)

Mr. Elio Sorella

President & Chief Executive Officer

Ecolomondo Corporation Inc.

3435 Pitfield Blvd.

St. Laurent, Quebec

Canada H4S 1H7

450-587-5999

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| Michael Stolzar, Esq. | Mitchell S. Nussbaum |

| Karlen & Stolzar LLP | David C. Fischer |

| 445 Hamilton Avenue, Suite 1102 | Tahra T. Wright |

| White Plains, NY 10601 | Loeb & Loeb LLP |

| 914-949-4600 | 345 Park Avenue |

| New York, NY 10154 | |

| 212-407-4000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: . [ ]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: [ ]

| CALCULATION OF REGISTRATION FEE | ||

| TITLE OF EACH CLASS OF SECURITIES TO BE | PROPOSED MAXIMUM AGGREGATE | |

| REGISTERED | OFFERING PRICE(1)(2) | AMOUNT OF REGISTRATION FEE(3) |

| Class A Common Shares, no par value | $16,100,000 | $2,074 |

| (1) | Includes 300,000 Class A Common Shares that may be sold pursuant to exercise of the underwriters’ option to purchase additional shares. | |

| (2) | Estimated solely for the purpose of determining the amount of registration fee in accordance with Rule 457(o) under the Securities Act of 1933. | |

| (3) | Previously paid. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

PRELIMINARY PROSPECTUS

ECOLOMONDO CORPORATION INC. This is the initial public offering of our Class A Common Shares. We are offering 2,000,000 of our Class A Common Shares. The public offering is being underwritten on a firm commitment basis. We currently expect the initial public offering price to be between $ 6.50 and $ 7.50 per Class A Common Share. We have granted the underwriters an option for a period of 45 days after the closing of this offering to purchase up to 15% of the total number of our Class A Common Shares to be offered by us pursuant to this offering (excluding shares subject to this option), solely for the purpose of covering over-allotments, at the initial public offering price less the underwriting discount. See “Underwriting” section of this prospectus. A portion or all of the 2,000,000 Class A Common Shares might be sold in Canada as part of this offering. Leede Jones Gable Inc. will act as agent in connection with the offering of shares in Canada, which will be qualified in Canada under a prospectus to be filed with the securities regulatory authority in each of the provinces and territories of Canada where we plan to offer our shares. We have applied to have our Class A Common Shares listed on The NASDAQ Capital Market under the symbol “EECO.” We are an “emerging growth company” as defined by the Jumpstart Our Business Startup Act of 2012 and, as such, we have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings. See “Prospectus Summary-Implications of Being an Emerging Growth Company.” Investing in our Class A Common Shares involves a high degree of risk. See “Risk Factors”. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense. | ||||||||

| Per Share | Total(1) | |||||||

| Public Offering Price | $ | 7.00 | $ | 16,100,000 | ||||

| Underwriting Discount (8.75%)(2) | $ | 0.6125 | $ | 1,408,750 | ||||

| Proceeds to Ecolomondo Corporation Inc.(before expenses) | $ | 6.3875 | $ | 14,691,250 | ||||

| (1) | Assuming the underwriters exercise in full their option to purchase up to an additional 15% of the total number of our Class A Common Shares to be offered by us pursuant to this offering, to cover over-allotments. | |||||||

| (2) | Does not include reimbursement of out-of-pocket expenses in an amount not to exceed $150,000, payable to Chardan Capital Markets, LLC, the sole book running manager and as a practical matter, the underwriters, for this offering. For further information, see “Underwriting” section. | |||||||

The underwriters expect to deliver the shares to purchasers on or about _____, 2016. Sole Book-Running Manager | ||||||||

We are responsible for the information contained in this prospectus and in any free-writing prospectus we prepare or authorize. We have not authorized anyone to provide you with different information, and we take no responsibility for any other information others may give you. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than its date.

TABLE OF CONTENTS

1

SPECIAL CAUTIONARY NOTE

You should rely only on the information contained in this prospectus or any free-writing prospectus we may authorize to be delivered or made available to you. We and the underwriters have not authorized anyone to provide you with additional or different information. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, our Class A Common shares only in jurisdictions where offers and sales are permitted. The information in this prospectus or any free-writing prospectus is accurate only as of the date of such prospectus, regardless of the time of delivery of such prospectus or any sale of our Class A Common shares.

Until ______, 2016, (25 days after the date of this prospectus) all dealers that buy, sell or trade our Class A Common shares, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

No action is being taken in any jurisdiction outside the United States, except for Canada, to permit a public offering of our Class A Common shares or possession or distribution of this prospectus in any such jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States and Canada are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus applicable to those jurisdictions. A portion or all of the 2,000,000 Class A Common Shares might be sold in Canada as part of this offering. Leede Jones Gable Inc. will act as agent in connection with the offering of shares in Canada, which will be qualified in Canada under a prospectus to be filed with the securities regulatory authority in each of the provinces and territories of Canada where we plan to offer our shares.

2

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus. You should read the following summary together with the more detailed information appearing in this prospectus, including “Risk Factors”, “Use of Proceeds”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, “Business” and our financial statements and related notes before deciding whether to purchase our Class A Common Shares. Some of the statements in this summary constitute forward-looking statements, with respect to which you should review the section of this prospectus entitled “Special Note Regarding Forward-Looking Statements.” Unless the context otherwise requires, the terms “Ecolomondo,” “our company,” “we,” “us,” “our” and “our business” in this prospectus refer to Ecolomondo Corporation Inc.together with its subsidiaries, if any.

All references in dollars are expressed in U.S. dollars unless otherwise indicated. All financial information with respect to us has been prepared in accordance with the accounting principles generally accepted in the United States of America (US GAAP).

Ecolomondo Corporation Inc.

Company Overview

We are a development stage clean tech company that has designed, engineered and developed a thermo-reaction process using a pyrolysis platform that converts hydrocarbon waste into marketable commodity end-products, namely carbon black substitute, oil, gas and steel. We plan to manufacture turnkey facilities based on this technology platform and sell them to clients, and collect royalties from their operation, or operate them through wholly or jointly-owned subsidiaries. Based on our research, we expect these turnkey facilities to be attractive to clients because of what we believe to be low forecasted capital cost per ton of capacity, an ability to generate profits from their operations, and because of a global environmental need to better manage and to effectively treat hydrocarbon waste.

Our process is a Canadian developed green technology, called Thermal Decomposition Process, which we refer to as “TDP”. TDP is a comprehensive, effective and green solution that we believe could achieve commercial acceptance while reducing the need to landfill. The TDP platform operates under positive pressure, in the absence of oxygen and with very low emissions. We consider the automated process to be safe, robust and environmentally friendly. It has been studied by Canada’s renowned technical institute, Polytechnique Montreal (Chemical Engineering Department), affiliated with the University of Montreal, and by Western University (Institute for Chemicals and Fuels From Alternative Resources).

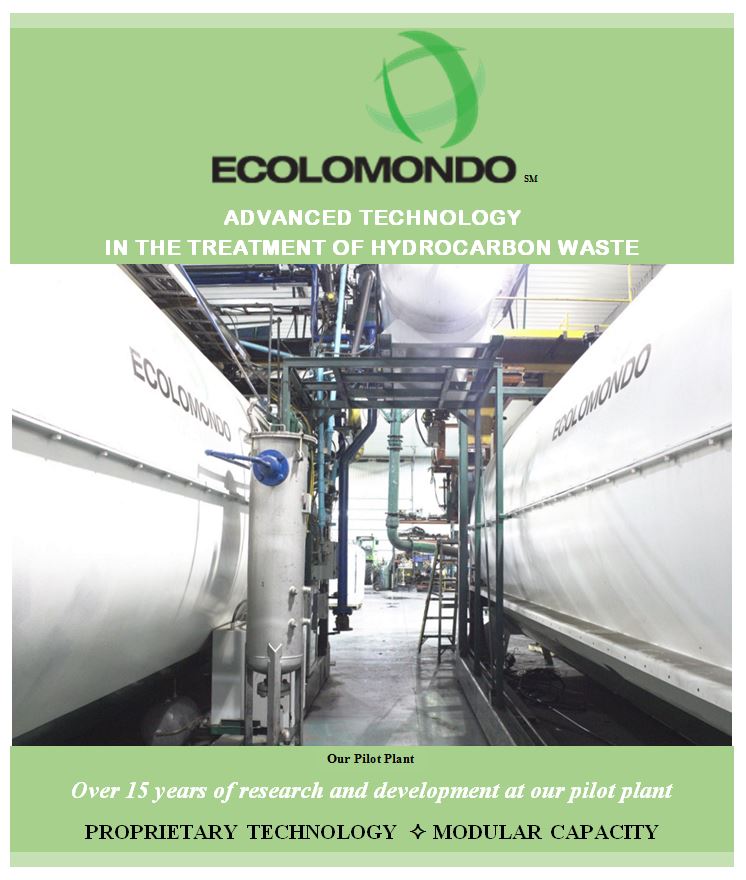

Since 1999, through ongoing research and development, we have developed and built an industrial-scale facility (which we call “Pilot”) consisting of two industrial size reactors, located in Contrecoeur, Quebec, Canada. Each reactor in the facility has the capacity to treat approximately 18 tons of tire waste per day. During the last 6 years, our Pilot facility tested and operated our latest generation TDP technology for over 1,600 hours, but not commercially on a continuous basis. During this period, even though Pilot concentrated mostly on tires, it performed testing to validate that TDP is capable to treat other types of hydrocarbon waste: disposable diapers, asphalt roof shingles, plastics and automobile shred residue (“car fluff”).

We believe our process extracts added value from these wastes, when compared to other technologies and other methods of treating hydrocarbon waste. We expect an abundant and continuous supply of waste feedstock to be available due to the growing consumption by an expanding population, and the emerging markets and changing environmental concerns and regulation, in particular, the need to reduce landfilling. We hope to become an industry leader in the treatment of these kinds of hydrocarbon waste.

Business Case for TDP Turnkey Facilities

Although we have not operated Pilot on a commercially continuous basis, Pilot has repeatedly processed industrial-scale batches of 6 tons. It also has demonstrated repeatedly that it produces consistent quality end-products of what we believe to be marketable quality.

Based on our experience at Pilot, we believe that TDP turnkey facilities can be profitable, because our end-products can easily replace, at cheaper cost, virgin commodity products for many applications. Furthermore, these TDP facilities would reduce the need to landfill, efficiently treat hydrocarbon waste, and contribute to a better environment.

3

Ecolomondo’s immediate and long term success is dependent on the commercial success of the TDP turnkey facilities. Based on our experience at Pilot, we believe that our TDP platform fulfills all of the key factors to achieve commercial acceptance. The main key factors are:

| • | High quality end-products: |

| o | Carbon black substitute: A quality carbon black substitute end-product is pivotal to the commercial success of any pyrolysis platform. We believe, based on our research and findings, that TDP’s carbon black substitute can replace utility carbon black in many rubber applications because of its quality, performance and characteristics. | |

| o | Oil: Oil resulting from a TDP reaction is considered more refined than conventional crude oil. After our post process refinement and fractioning, TDP oil is immediately ready for resale to refineries or as industrial fuel. | |

| o | Steel: Tires contain high-grade steel that is extracted at the shredding stage. It never enters the reactor and is a by-product of the shredding stage, considered as a high-quality product by steel foundries and recyclers. |

| • | Global markets for end-products: We believe that TDP facilities should find ready markets for their end-products because they can replace virgin commodity products that have high global demand, and this, at a lower price. | |

| • | High yield rate of carbon black substitute: Results at Pilot have consistently shown high production yields of carbon black substitute, thanks to our process optimization and automation. Since carbon black substitute is the end-product with the highest value, a high yield rate of carbon black substitute should improve revenues for TDP facilities. Even though carbon black substitute represents 41% of TDP’s output, it represents 77% of the forecasted revenue of a TDP turnkey facility. | |

| • | Low forecasted capital cost per ton of capacity:Based on our research and findings, we believe the capital cost per ton of capacity for TDP facilities to be lower than most other pyrolysis platforms. |

Industry

Waste-pyrolysis transforms hydrocarbon waste to recover commodity end-products for reuse. We believe the waste-pyrolysis industry is largely in a pre-commercial phase. Many companies have invested millions in its development over the last 50 years, but low commodity prices and lack of industry incentives such as tipping fees have prevented waste pyrolysis from operating profitably. We believe that waste-pyrolysis is becoming a commercially viable industry because of favorable commodity prices, a growing concern for the environment, and favorable government policies and regulations that restrict landfilling and encourage recycling. We expect current and future government programs, incentives and regulations to play an important role towards the development of the industry.

We believe, based on our findings, that few companies currently conduct significant activity in the hydrocarbon waste-pyrolysis industry and those that are active are not reaching the production yield levels of carbon black achieved by our TDP platform.

We also believe, based on our findings, that a few common factors explain why there has been little commercial success to date in the waste-pyrolysis industry. Our research indicates either the technology was not ready to commercialize, the capacity was too small or they were not scaled up, end-products were not consistent in quality or did not meet the market quality criteria, or the process was not sufficiently automated to achieve consistent yields.

Market Size

Total market size for the waste-pyrolysis industry, including TDP facilities, is determined by the volume of feedstock supply. In spite of any economic downturns and fluctuations, we expect an abundant and continuous supply of waste feedstock to be available due to the growing consumption by the expanding population, along with emerging markets and changing environmental concerns and regulation, in particular, the need to reduce landfilling and to promote recycling and reuse.

Unfortunately, there is no source available as firm data underlying our assumptions, however, we believe that out of a total estimated volume of hydrocarbon waste of 160 million tons per year, the estimated global feedstock supply available to the waste-pyrolysis industry could reach 40 million tons per year, including over 12 million tons per year in the United States. The average volume per year of scrap tires would be sufficient to supply feedstock to approximately 1,000 reactors worldwide, including approximately 250 located in the United States. These volumes help us approximate the market size for TDP facilities, however they are based upon our assumptions and estimates, and on information on hydrocarbon waste from industry and internet sources.

4

Our Strategy for Growth

Our overall strategy is to make profits from the sale, construction and commissioning of TDP turnkey facilities using our technology platform and to collect royalties from their operations. Initially, because tires generate end-products of higher value, we intend to focus on facilities that would convert scrap tires into commodity end-products: carbon black substitute, fuel oil, process gas and steel.

Launch facility.We expect to partner in a joint venture with Ecological Recycling CG Inc. (“ERCG”) for the sale and operation of our first commercial TDP turnkey facility, which we call “Launch”. We and ERCG signed a binding LOI on May 12, 2014, with an addendum to specify some conditions on July 2, 2014, a second addendum signed on November 2, 2014, to extend the termination date to May 12, 2015, a third addendum signed on May 12, 2015, to extend the termination date to November 12, 2015, and a fourth addendum that extends the termination date for additional periods of 6 months after May 12, 2016 unless a written notice is sent by one party to the other party. Since no notice was received, the termination date is currently November 12, 2016. We expect Launch to be built in Hawkesbury, Ontario, Canada; we already have had meetings with local authorities to identify specific locations where we expect that permits can be issued for its construction and operation, however we cannot enter into definitive agreements prior to the successful completion of this offering because we require the proceeds from this offering for our portion of the investment in the Launch joint venture. If we are successful, we intend to use Launch as a showpiece to help us garner attention to our latest generation of our innovative technology. We expect the sale price of this 2-reactor facility to the joint venture to be $17,550,000 and be financed equally between us and ERCG. ERCG is expected to make capital contributions in the amount of $8,775,000 for a 50% interest in Launch and is also expected to contribute $475,000 in working capital. When in full operation, we expect Launch to have production yields of approximately 12,000 tons per year; we estimated that sufficient waste tire feedstock is available in the region and that Launch can sign off-take agreements at the projected prices described further in this document. We expect Launch to be completed and be in full production within one year from the successful completion of this offering. We are currently negotiating with several engineering firms to supervise construction and commissioning of the Launch facility; these firms have provided us with specific timetable for construction, delivery and commissioning of Launch. The timetable will not change, whether the joint venture agreement is completed or whether we have to finance Launch on our own. Our Launch partner has deposited C$1,000,000 (USD$722,500 as of December 31, 2015) in trust with the Company’s conveyance lawyer to secure his portion of the purchase price. The Company will endeavor to enter into definitive agreements with ERCG after the successful completion of this offering, for the construction of the Launch facility at a location to be determined in the Hawkesbury area (Ontario, Canada).

If the funds from the proceeds of this offering are not sufficient to finance our equity and working capital needs for the joint venture, we plan to secure the shortfall through debt financing. We hope to obtain the financing needed for this project from Export Development Canada (“EDC”), a government-owned export credit agency that supports Canadian companies in international business opportunities. We had several meetings with EDC but we are not in a position to enter into definitive agreements nor to have more updates prior to the successful completion of this offering, because EDC cannot commit to financing Launch until we have completed our financing with this offering, and because we need the proceeds from this offering to obtain financing from the EDC. EDC is an option, however we may consider other lending institutions if need be; however, at this time there are no current commitments for such financing.

New Jersey facility. On May 14, 2014, we concluded a binding Letter of Intent with the Matzel Group to sell an 8-reactor TDP turnkey facility. On October 10, 2015, we signed a binding LOI replacing the LOI signed on May 14, 2014, whereby the Matzel Group has opted to partner with Ecolomondo in a joint venture for a 4-reactor turnkey TDP facility to be located in New Jersey. The sale price for this 4-reactor facility is $37.5 million. The $100,000 non-refundable deposit given by the Matzel Group for the 8-reactor facility will be transferred to the new joint venture project, with the Matzel Group paying an additional $150,000 non-refundable deposit, which has been received. As indicated in the binding LOI, the Matzel Group and Ecolomondo will be equal partners in the joint venture, each partner contributing equity capital of $2,812,500 (including the non-refundable deposits), which is 7.5% of the purchase price of $37.5 million. We expect that the 85% balance of the purchase price will be financed through debt financing by the joint venture entity. The Matzel Group is a New Jersey and Pennsylvania-based real estate developer specializing in commercial, resort, recreational and residential development and construction, known for insightful planning and superior construction quality. We estimate that this 4-reactor facility would be able to treat 24,000 tons of tire waste per year. We expect that this facility could become a showcase for a 4-reactor facility. We expect that the density and size of the population in this area to result in a sufficient supply of scrap tire feedstock for this facility.

Abitibi facility. On March 25, 2016, we concluded a binding Letter of Intent with CVE Abitibi Inc. to create a joint venture for the acquisition of a 2-reactor TDP turnkey facility. The sale price by Ecolomondo to the joint venture is $19,750,000. CVE Abitibi Inc. paid a non-refundable commitment fee of $125,000, which has been received. This LOI terminates on September 30, 2016 and this date may be extended upon mutual written agreement of the parties. We expect this facility to be located near Malartic (Quebec), Canada, which is a large mining community in northern Quebec. CVE Abitibi Inc. is a group of 14 corporate and individual investors from the region. As indicated in the binding LOI, CVE Abitibi Inc. and Ecolomondo will be equal partners in the joint venture, each partner contributing equal capital of $1,481,250 (including the non-refundable deposit), which is 7.5% of the purchase price of $19,750,000. We expect that the 85% balance of the purchase price will be financed through debt financing by the joint venture entity.

5

We are in discussions with potential buyers and strategic partners throughout the world.

| • | We have signed a number of non-binding Memoranda of Understanding (MOU’s) for the sale of TDP facilities in: |

| Argentina | Belgium | Brazil | Cameroun | |

| Canada | Caribbean | Colombia | ||

| Nigeria | Romania | Turkey | United Arab Emirates | |

| United States. |

| • | We are negotiating LOIs for the sale of TDP facilities in: Belgium, Brazil, Canada, Malaysia, Nigeria and Saudi Arabia. | |

| • | We are in discussion to negotiate MOU’s for the sale of TDP facilities in: Bulgaria, France, India, Italy, Morocco and Vietnam. |

The status of reaching definitive agreements with counterparties varies with each case and is constantly evolving. Prior to entry into definitive agreements, the counterparties need to perform required due diligence on the ability to secure feedstock, location, offtake agreements, financing and security deposits. We are also in discussions with other interested parties in Algeria, Mexico and Spain. A significant factor impacting our execution of additional MOU’s and LOIs is the consummation of this offering, which should cause other parties to believe the Company can satisfy its obligations.

Our Competitive Advantages

We believe the technological advancements in our TDP platform and post process treatment of the end-products, along with production output of 6 tons per batch, as determined by testing at Pilot, should provide each TDP facility with a competitive advantage in the commodity markets of carbon black, oil and steel because of their lower costs. We believe our TDP technology provides competitive advantages over other pyrolysis platforms that treat hydrocarbon waste. Based on our findings, we believe TDP benefits from technological advancements, post process treatment of the end-products and automation developed with years of testing and experience at Pilot. We believe that a key advantage instrumental in the future success of the TDP platform is the added value of the resulting commodity end-products, carbon black, oil, steel and gas. In addition, our TDP platform requires no scale up because it is already at industrial scale, and is also modular, giving each facility flexibility in size and capacity. Over the last 6 years, and with over 1,600 hours of testing, our research and technical teams have achieved many milestones and gathered considerable expertise in waste-pyrolysis and our TDP platform, during which they made many technological improvements, not only to the equipment but also to the process. As a result, we expect our process to be able to produce marketable commodity end-products out of hydrocarbon waste with added value and at production yields that should be profitable.

Certain Risks Affecting Us

Our business may be subject to a number of risks and uncertainties that you should understand before making an investment decision. These risks are discussed more fully in the section entitled “Risk Factors” following this prospectus summary.

Implications of Being an Emerging Growth Company

We are an “emerging growth company”, as defined in Section 2(a) of the Securities Act of 1933, as amended, or the Securities Act, as modified by the Jumpstart Our Business Startups Act, or “JOBS Act.” As such, we are eligible to take advantage of exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies”, including, but not limited to:

| • | Not being required to comply with the auditor’s attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act; | |

| • | Being permitted to present only two years of audited financial statements and only two years of related management’s discussion and analysis of financial condition and results of operations; | |

| • | Reduced disclosure obligations regarding executive compensation; |

6

| • | Not being required to comply with any new requirements that may be adopted by the Public Company Accounting Oversight Board, or the PCAOB regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements; and | |

| • | Exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. |

We have taken advantage of some of the reduced reporting burdens in this prospectus and may take advantage of additional exemptions in the future. Accordingly, the information contained herein may be different than the information provided by other public companies. We do not know if some investors will find our shares less attractive as a result of our utilization of these or other exemptions. The result may be a less active trading market for our shares and our share price may be more volatile.

In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have irrevocably elected not to avail ourselves of this exemption from new or revised accounting standards, and, therefore, we will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

We will remain an “emerging growth company” until the earliest of (a) the last day of the first fiscal year in which our annual gross revenues exceed $1.0 billion, (b) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which would occur if the market value of our shares that are held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, (c) the date on which we have issued more than $1.0 billion in non-convertible debt the preceding three-year period, or (d) the last day of our fiscal year containing the fifth anniversary of the date on which our Class A Common Shares become publicly traded in the United States.

Corporate Information

We were incorporated in Canada under The Canada Business Corporations Act on January 9, 2007 under the legal name of 4403100 Canada Inc., doing business under the name of Ecolomondo Corp. On May 23, 2014, we changed our legal name from 4403100 Canada Inc. to Ecolomondo Corporation Inc.4403100 Canada Inc. acquired 9083-5018 Quebec Inc. on March 25, 2009 as a wholly-owned subsidiary. 9083-5018 Quebec Inc. is the company that owns our intellectual property and our Pilot plant in Contrecoeur, Quebec, Canada.

Our principal executive offices are located at 3435 Pitfield Boul., St. Laurent, Quebec, Canada H4S 1H7, and our telephone number at that location is (450) 587-5999. Our corporate website address is http://www.ecolomondocorp.com. The information contained in or accessible from our corporate website is not part of this prospectus. Rights to the “Ecolomondo”name and related images and symbols were acquired in the acquisition of March 25, 2009. We will review the trademarks of our Company’s name and logo soon after the consummation of this offering. All other trade names, trademarks and service marks appearing in this prospectus are the property of their respective owners.

7

The Offering

This public offering is being underwritten on a firm commitment basis. See “Underwriting” section of this prospectus.

| Class A Common Shares offered by us | 2,000,000 (A portion or all of the 2,000,000 Class A Common Shares might be sold in Canada as part of this offering. Leede Jones Gable Inc. will act as agent in connection with the offering of shares in Canada, which will be qualified in Canada under a prospectus to be filed with the securities regulatory authority in each of the provinces and territories of Canada where we plan to offer our shares.) |

| Class A Common Shares outstanding prior to this offering | 20,080,000 (after giving effect to a25 to 1Reverse Stock Split, which became effective on October 9, 2014) |

| Class A Common Shares to be outstanding immediately after this offering | 22,080,000 shares |

| Over-allotment option | We have granted the underwriters a 45-day option to purchase up to 15% of the total number of Class A Common Shares to be offered by us pursuant to this offering (excluding shares subject to this option) |

| Use of proceeds | We anticipate that the net proceeds received from this offering, after deducting estimated underwriting discounts and other estimated offering expenses payable by us, should be approximately $12,375,000, and approximately $14,291,250, if the underwriters exercise their over-allotment option in full. |

| |

Almost all of the net proceeds from this offering are to be used to finance Ecolomondo’s expansion and future working capital requirements. The Company is free of long-term debt and does not have to use these funds to reimburse any loans or debt. The net proceeds from this offering will not be used to redeem the Class J Preferred Shares that are issued and outstanding, nor to reimburse advances from companies under common control. | |

| |

We intend to use approximately $6,000,000 of the net proceeds from this offering to finance our portion of equity and working capital needs for Launch. If the funds to be allocated to finance our equity and working capital needs for the joint venture are not sufficient, we plan to secure the shortfall through debt financing which we will endeavor to obtain at that time. Please read “Financial Details of our Launch Project” for additional details, in the Business section. | |

| |

We intend to use a further $2,812,500 of the net proceeds from this offering to finance our equity portion for our joint venture with the Matzel Group to be located in New Jersey. We expect that the 85% balance of the purchase price will be financed through debt financing by the joint venture entity. We intend to use a further $1,481,250 of the net proceeds from this offering to finance our equity portion for our joint venture with CVE Abitibi Inc. to be located near Malartic, in northern Quebec. We expect that the 85% balance of the purchase price will be financed through debt financing by the joint venture entity. | |

| |

We are planning the construction and commissioning of Launch to be performed by third parties. After the completion of Launch’s construction, and if there is a minimum of $5,000,000 in working capital available from the proceeds of this offering, we may consider using $2,500,000 of these proceeds to construct an assembly plant where we can build and assemble equipment and apparatus for TDP turnkey plants that we hope to sell in the future. This amount includes $1,500,000 in capital investments and start-up costs, and $1,000,000 in working capital. Should the working capital not achieve the $5,000,000 threshold, or if we require more working capital for our operations and expansion, or if we are obliged to finance Launch on our own, we will postpone our plans to construct the assembly plant to a later date. If we proceed with the assembly plant, it may require hiring up to 30 employees, including but not limited to administrative, engineers, chemists, welders, mechanics and general labor. | |

| |

Currently, we have no specific plan for the use of the remainder of the net proceeds and intend to use such proceeds for general corporate purposes, including public company compliance costs, working capital needs, operating expenses and costs associated with research and development and future developments. See “Use of Proceeds.” | |

| Risk factors | You should carefully read and consider the information set forth under the heading “Risk Factors” and all other information set forth in this prospectus before investing in our Class A Common Shares. |

| NASDAQ Capital Market symbol | We have applied to the NASDAQ Capital Market to have the following symbol: EECO. |

8

Summary Historical Financial Data

The Table “Summary Financial Data”, at next page, presents a summary of our historical financial data as of the dates and for the periods indicated. The summary statement of operations data has been derived from our our audited consolidated financial statements as of December 31, 2015 and 2014 that are included elsewhere in this prospectus. The summary historical financial data presented below should be read in conjunction with the sections entitled “Risk Factors,” “Selected Historical Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes thereto and other financial data included elsewhere in this prospectus.

Our functional and reporting currency is the Canadian dollar because a significant portion of our business is conducted in Canada and our ancillary revenues and most expenses are denominated in Canadian dollars. This prospectus contains the translation of Canadian dollar amounts into U.S. dollars at a specific rate solely for the convenience of the reader. The conversion of Canadian dollars into U.S. dollars, in the prospectus, is based on the rates published by the Bank of Canada. We make no representation that any Canadian or U.S. dollar amounts could have been, or could be, converted into U.S. dollars at any particular rate, the rates stated below, or at all. The following Table sets forth information concerning exchange rates between the Canadian dollar and the U.S. dollar for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we used in this prospectus or will use in the preparation or our periodic reports or any other information to be provided to you. Because of the recent volatility of the Canadian dollar, except if specified otherwise, management has opted to make translations from Canadian dollars to U.S. dollars in this prospectus for pro forma data using a rate of C$1.00 to US$0.7225 (or US$1.00 to C$1.3840), which is the noon exchange rate of the most recent Company’s year end date of December 31, 2015.

| Canadian-U.S. Exchange Rates For 1.00 USD * | ||||||||||||||||||

| Year ended December 31 | ||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||||

| Period end | 1.3840 | 1.1601 | 1.0636 | 0.9949 | 1.0170 | 0.9946 | ||||||||||||

| Average | 1.2787 | 1.1045 | 1.0299 | 0.9996 | 0.9891 | 1.0299 | ||||||||||||

| High | 1.1728 | 1.0614 | 0.9839 | 0.9710 | 0.9449 | 0.9946 | ||||||||||||

| Low | 1.3990 | 1.1643 | 1.0697 | 1.0418 | 1.0604 | 1.0788 | ||||||||||||

The high and low exchange rates for recent months are as follows:

High and Low Canadian-U.S. Exchange Rates For 1.00 USD *

| Month | High | Low |

| September 2015 | 1.3147 | 1.3413 |

| October 2015 | 1.2904 | 1.3242 |

| November 2015 | 1.3095 | 1.3360 |

| December 2015 | 1.3360 | 1.3990 |

| January 2016 | 1.3969 | 1.4589 |

| February 2016 | 1.3523 | 1.4040 |

* Source: Bank of Canada, Daily Noon Exchange Rates: 10-Year Lookup, U.S. dollar.

As mentioned above, management has opted to translate from Canadian dollars to U.S. dollars throughout this document, except if specified otherwise, using the rate of the most recent Company’s year end date of December 31, 2015, which is 1.3840.

9

In Canadian dollars:

| Summary Financial Data | ||||||

| Year ended | ||||||

| December 31, 2015 | December 31, 2014 | ||||

(currency) | C$ | C$ | ||||

| ||||||

Ancillary revenues | 23,368 | 11,237 | ||||

| ||||||

Expenses | ||||||

General and administrative expenses | 229,567 | 263,088 | ||||

Research and development | 793,646 | 641,401 | ||||

Rent to companies under common control | 120,252 | 120,252 | ||||

Depreciation of equipment | 618,494 | 715,559 | ||||

Amortization of intangible assets | 280,753 | 280,753 | ||||

Financial expenses | 410 | 625 | ||||

Investment tax credits | (490,000 | ) | (332,752 | ) | ||

Total expenses | 1,553,122 | 1,688,926 | ||||

| ||||||

Loss before income taxes | (1,529,754 | ) | (1,677,689 | ) | ||

Income taxes | ||||||

Current | – | – | ||||

Deferred | (229,196 | ) | (253,076 | ) | ||

| (229,196 | ) | (253,076 | ) | ||

Net loss | (1,300,558 | ) | (1,424,613 | ) | ||

| ||||||

Net loss per share | ||||||

Basic and diluted | (0.06 | ) | (0.07 | ) | ||

| ||||||

Weighted average number of Class A Common Shares outstanding, basic and diluted | 20,080,000 | 20,080,000 | ||||

10

In United States dollars, converted with the exchange rates applicable on the last day of the period:

| Summary Financial Data | ||||||

| Year ended | ||||||

| December 31, 2015 | December 31, 2014 | |||||

| (currency)(1) | US$(2) | US$(3) | ||||

| Ancillary revenues | 16,883 | 9,686 | ||||

| Expenses | ||||||

| General and administrative expenses | 165,862 | 226,782 | ||||

| Research and development | 573,409 | 552,888 | ||||

| Rent to companies under common control | 86,882 | 103,657 | ||||

| Depreciation of equipment | 446,862 | 616,812 | ||||

| Amortization of intangible assets | 202,844 | 242,009 | ||||

| Financial expenses | 296 | 539 | ||||

| Investment tax credits | (354,025 | ) | (286,832 | ) | ||

| Total expenses | 1,122,131 | 1,455,854 | ||||

| Loss before income taxes | (1,105,247 | ) | (1,446,168 | ) | ||

| Income taxes | ||||||

| Current | – | – | ||||

| Deferred | (165,594 | ) | (218,152 | ) | ||

| (165,594 | ) | (218,152 | ) | |||

| Net loss | (939,653 | ) | (1,228,016 | ) | ||

| Net loss per share | ||||||

| Basic and diluted | (0.05 | ) | (0.06 | ) | ||

| Weighted average number of Class A Common Shares outstanding, basic and diluted | 20,080,000 | 20,080,000 | ||||

Note: Differences may be due to rounding.

Note 1: Canadian currency is converted into US$ using the period end rate of each period.

Note 2: C$1.00 is converted to US$0.7225 for the year ended December 31, 2015.

Note 3: C$1.00 is converted to US$0.8620 for the year ended December 31, 2014.

11

| Summary Balance Sheet Data | |||||||||||||||

| As of June 30, 2015 | |||||||||||||||

| Maximum(2) | |||||||||||||||

| Offering(1) | (including underwriters' over- | ||||||||||||||

| allotment option of 15%) | |||||||||||||||

| PRO-FORMA | PRO-FORMA | PRO-FORMA | PRO-FORMA | ||||||||||||

| ACTUAL | AS ADJUSTED | AS ADJUSTED | AS ADJUSTED | AS ADJUSTED | |||||||||||

| (currency) | C$ | C$ | US$ | C$ | US$ | ||||||||||

| Cash | 192,302 | 17,320,330 | 12,513,938 | 19,972,579 | 14,430,188 | ||||||||||

| Cash held in trust | 1,021,281 | 1,021,281 | 737,876 | 1,021,281 | 737,876 | ||||||||||

| Working capital(3) | (642,533 | ) | 16,485,495 | 11,910,770 | 19,137,744 | 13,827,020 | |||||||||

| Equipment, net | 5,198,375 | 5,198,375 | 3,755,826 | 5,198,375 | 3,755,826 | ||||||||||

| Total assets | 8,097,056 | 25,225,084 | 18,225,123 | 28,877,333 | 20,863,873 | ||||||||||

| Long-term debt | - | - | - | - | - | ||||||||||

| Preferred Shares | 3,988,879 | 3,988,879 | 2,881,965 | 3,988,879 | 2,881,965 | ||||||||||

| Total stockholders' equity (including Preferred Shares) | 4,094,469 | 21,222,497 | 15,333,254 | 23,874,746 | 17,249,504 | ||||||||||

Note: C$1.00 is converted to US$0.7225. Differences may be due to rounding. | |||||||||||||||

| Summary Balance Sheet Data | ||||||

| As of | As of | |||||

| June 30, 2015 | December 31, 2014 | |||||

| ACTUAL | ACTUAL | |||||

| (currency) | C$ | C$ | ||||

| Cash | $ | 192,302 | $ | 11,023 | ||

| Cash held in trust | 1,021,281 | 1,000,000 | ||||

| Working capital(3) | (642,533 | ) | 13,356 | |||

| Equipment, net | 5,198,375 | 5,816,869 | ||||

| Total assets | 8,097,056 | 8,780,708 | ||||

| Long-term debt | - | - | ||||

| Preferred Shares | 3,988,879 | 3,988,879 | ||||

| Total stockholders' equity (including Preferred Shares) | 4,094,469 | 5,395,027 | ||||

(1) Gives effect to (i) the 25 to 1 Reverse Stock Split and IPO Share Adjustments, and (ii) our issuance and sale of 2,000,000 Class A Common Shares in this offering at an assumed initial public offering price of $7.00 (C$9.69) per share, which is the midpoint of the price range listed on the cover page of this prospectus, after deducting underwriting discounts and commissions of $1,225,000 (C$1,695,502) and offering expenses payable by us of approximately $400,000 (C$553,633).

(2) Gives effect to (i) the 25 to 1 Reverse Stock Split and IPO Share Adjustments, and (ii) our issuance and sale of 2,300,000 Class A Common Shares in this offering, assuming the underwriters exercise their over-allotment option in full, at an assumed initial public offering price of $7.00 (C$9.69) per share, which is the midpoint of the price range listed on the cover page of this prospectus, after deducting underwriting discounts and commissions of $1,408,750 (C$1,949,827) and offering expenses payable by us of approximately $400,000 (C$553,633).

(3) Working capital is the amount by which current assets exceed current liabilities.

12

RISK FACTORS

Our business, as well as our Class A Common Shares, are highly speculative in nature and involve a high degree of risk. You should consider carefully the risks described below before making an investment decision. The risks described below are those which we consider material and of which we are currently aware. Our business, prospects, financial condition or operating results could be harmed by any of these risks. Furthermore, these factors represent risks and uncertainties that could cause actual results to differ materially from those implied by forward-looking statements. We refer you to our cautionary note regarding “Forward-Looking Statements,” which identifies the forward-looking statements in this prospectus. The trading price of our Class A Common Shares could decline due to any of these risks, and, as a result, you may lose all or part of your investment. Before deciding whether to invest in our Class A Common Shares, you should also refer to the other information contained in this prospectus, including our consolidated financial statements and the related notes.

Risks Related to Our Business and Industry

We are a development stage company that has generated limited revenue, with a limited operating history and a history of net losses.

We have generated limited revenues and have incurred substantial net losses since our inception, and have an accumulated deficit of C$8,666,524 as of December 31, 2015. As we attempt to grow our business in the future, we may continue to incur net losses and experience negative cash flow from operating activities. We may not be able to obtain additional capital in a timely manner or on acceptable terms, or at all. We may not be able to achieve or sustain profitability or positive cash flow from operating activities, and, even if we achieve positive operating cash flow, it may not be sufficient to satisfy our anticipated capital expenditures and other cash needs. Furthermore, we may not be able to fund our operating expenses and expenditures and may be unable to fulfill our financial obligations as they become due. We are subject to the substantial risk of failure facing businesses seeking to develop new products, and may result in voluntary or involuntary dissolution or liquidation proceedings and a total loss of your investment.

Our independent auditors have expressed substantial doubt about our ability to continue as a going concern, which may hinder our ability to obtain future financing.

The audit opinion for our consolidated financial statements for the years ended December 31, 2015 and 2014 includes an explanatory paragraph expressing substantial doubt about our ability to continue as a going concern. We have also included such explanatory information in the notes to the consolidated financial statements as of December 31, 2014 and June 30, 2015. We are a development stage company and have incurred losses since our inception. We have had minimal revenues and have incurred an accumulated deficit of C$8,666,524 through to December 31, 2015. Our ability to continue as a going concern is dependent upon numerous factors, including the ability to fund operations and future production. In addition, the current capital markets and general economic conditions in the United States and Canada provide no assurance that our funding initiatives can be successful. These factors raise doubt about our ability to continue as a going concern.

We might fail to establish the joint venture that we expect will purchase the first commercial TDP facility that we intend to build.

We have signed a Letter of Intent with Ecological Recycling CG Inc. (“ERCG”) to form a joint venture to purchase the first commercial TDP facility that we intend to build. ERCG still has to obtain the necessary financing for its share of the capital investment required for the joint venture. ERCG may be unable to obtain the necessary financing to complete its share of the capital investment required for Launch. Please read “Financial Details of our Launch Project” for additional details.

Definitive terms of the agreement with the joint venture partner are not yet concluded. We may be unable to agree on terms or we may be required to accept unfavorable terms to reach an agreement. If we cannot arrive to a satisfactory agreement with our joint venture partner, we may be forced to finance the construction and the commissioning of Launch on our own, which would require us to secure debt financing and to use more funds from the net proceeds of the offering, thereby reducing the amount of available working capital.

We expect the joint venture subsidiary to be governed by a five-person Board, with two-members selected by each of the joint venture partners and one member chosen jointly.

13

We have no experience in building and operating an industrial-scale TDP facility.

We have not yet begun construction of an industrial-scale TDP facility. The actual cost of constructing, operating and maintaining our TDP facilities may be higher than we planned. We cannot assure you that the Launch TDP facility can be completed on the schedule or within the budget that we intend, or at all. We have built the Pilot TDP facility ourselves but construction was spread over many years with numerous improvements and adjustments. Management lacks experience overseeing construction under industrial conditions and must rely on third parties, including an engineering firm, contractors and consultants, to oversee work and to construct and commission the Launch TDP facility. As a result, we will have less control over the work than would be the case if management oversaw the work directly.

Our first industrial-scale TDP facility, Launch, is to be owned and operated by a joint venture, in which we will be a 50% partner. The joint venture will need to hire and integrate experienced administrative personnel, technicians, engineers and mechanics. Costs from operations, maintenance, and feedstock may be higher than anticipated, feedstock may not be available in quantities sufficient for profitable operations, or revenues from end-products may be lower than we expect. The operation of Launch will require close ongoing oversight of maintenance, acquisition of feedstock and marketing of end-products in which we lack extensive experience. Also, construction and commissioning of Launch requires operating permits from various government authorities, however we expect these permits to be granted since a TDP facility complies with regulations applicable to the location in which we plan to build it. If we fail to secure them on time, the Launch project may have to be delayed.

Our industry is largely pre-commercial and has not yet proven to be commercially viable.

The waste-pyrolysis industry is largely in a pre-commercial stage and has not yet proven results on a large scale. A number of projects have used millions of dollars in investment from public, private and government funding, to develop waste-to-energy and waste-to-products pyrolysis facilities. Only a handful of projects may develop to industrial scale but we understand none seem to be operating on a continuous commercial basis yet. Waste-pyrolysis is becoming a serious option because of the growing concern about landfills and its effects on our ecosystem and because of higher commodity prices that encourages recycling. In addition, even if the technology can be commercially viable, other factors can slow or delay the commercialization of the waste-pyrolysis industry, including but not limited to: downward fluctuations in commodity prices, the cost of alternative means of disposing of waste and competition from other processors for the waste. The industry may develop only if it provides greater added value than present commercial uses or disposal methods of hydrocarbon waste. This may not happen because acceptance, development and commercialization of the pyrolysis industry may not happen. This may have a negative impact on the success of our TDP platform and consequently our results of operations.

Even though we have operated our Pilot facility at industrial-scale, with batch yields of 6 tons, for over1,600 hours, we have not decomposed tire waste on a continuous basis or for extended periods.

While we tested the performance and capacity of our TDP technology at Pilot, we cannot assure you that process efficiencies from the operation on an industrial-scale can produce similar yields and quality end-products. The operation of Pilot is in a controlled environment, with minimal variation in process conditions, under close supervision of an expert team. Operations on a commercial basis may be subject to a less controlled environment and less skilled labor. These factors and other unknown factors may negatively impact the performance of TDP facilities and consequently negatively impact our results.

If and when the Launch TDP facility or any other future TDP facility is constructed, operating and maintenance costs may be significantly higher than we anticipate. In addition, it may not operate as efficiently as we expect and may experience unplanned downtime, which may be significant. We have validated our process at Pilot with over 1,600 hours of run time, but not continuously for extended periods that will be expected under industrial conditions. As a result, the Launch TDP facility or any of our other future commercial TDP facilities may be unable to achieve the expected production yields which could adversely affect sales of TDP turnkey facilities, our business and results of operations.

14

We have no experience in building and operating a commercial TDP facility assembly plant.

Following Launch, we plan to build an assembly plant for construction of future TDP turnkey facilities. Management lacks experience overseeing such construction and must rely on third parties, including an engineering firm, contractors and consultants, to oversee work and to construct the new assembly plant. Also we need to establish operating policies, procedures and quality controls, hire a large number of specialized employees, control expenses, meet delivery schedules and be on budget, activities with which we have little experience. We cannot assure you that building TDP facilities on tight schedules, controlled budgets and with quality requirements will be feasible on an industrial-scale, or even if feasible, our management will be capable of doing so profitably.

Adequate demand for our TDP facilities may not develop if our clients are unable to procure sufficient volumes of feedstock.

The successful commercialization of our technology requires our clients operating TDP facilities to continuously acquire and process large volumes of feedstock, such as scrap tires. Our clients may experience difficulties in obtaining access to feedstock and/or transporting such feedstock to their TDP facilities. Such access to feedstock may be adversely affected by government regulations, transportation costs, actions by landfillers, sellers or competing processors of feedstock. Our clients may be unable to secure access to feedstock in volumes needed or to secure the transportation of feedstock to their facility on terms acceptable to them or at all. If they are unable to secure cost-effective and a steady flow of feedstock, their ability to operate the TDP facility on a commercial basis could be adversely affected, and our revenues from royalty streams could be diminished.

Adequate demand for our TDP facilities may not develop if there is inadequate demand for recycled end-products.

Recycled oil and carbon black. There has been a substantial increase in the demand for carbon black and hydrocarbon oil in recent years, but the demand for the recycled carbon black and fuel oil produced using our technology could be limited because of market resistance to pyrolysis-derived products.

Obtaining market acceptance in the carbon black industry is complicated by the fact that many potential carbon black industry customers have invested substantial amounts of time and money in developing established production channels. These potential customers generally have well-developed manufacturing processes and arrangements with suppliers of carbon black components and may display substantial resistance to changing these processes. In addition, the virgin carbon black market is dominated by a few large producers that may try to restrict new carbon black production. Pre-existing contractual commitments, unwillingness to invest in new infrastructure or technology, distrust of new production methods and long-standing relationships with current suppliers may slow market acceptance of our TDP carbon black substitute. To be successful, we must also demonstrate the ability of a TDP facility to produce carbon black substitute reliably on a commercial basis and be able to sell it at a competitive price. Failure to do so may cause TDP facilities to have lower revenues or even operate at a loss. This may have material adverse effect on our business, financial condition and results of operations.

We believe that some of the present and projected prices for virgin carbon black and fuel oil are a direct result of the significant increases in the cost of petroleum since the 1990s. If the prices of virgin products decline, the carbon black substitute, oil and steel produced by TDP facilities may also decline or may not be a cost-effective alternative to virgin products. Declining oil prices, or the perception of a future decline in oil prices, could adversely affect the prices that can be obtained by our clients or prevent our clients from entering into longer term agreements with their own customers. Therefore, unstable economic conditions along with other factors may impact the price of these end-products. This could have serious adverse effect on the profitability of our clients and consequently ours and revenues from royalty streams.

Recycled steel. Steel is a worldwide commodity affected by numerous factors. Steel is more recycled than all other materials and recycled steel is also a worldwide commodity. Demand for steel and recycled steel, and their price, depend on general economic conditions. Recycled steel producers, such as a TDP facility, do not have many options for selling their product as the industry is largely concentrated. If the world economic conditions deteriorate or if a TDP facility’s local economic conditions change, it may not be able to sell recycled steel at the projected price or to sell at all. Such conditions would negatively affect our clients’ results of operations and consequently negatively impact ours as well.

15

Processing of some feedstock may not be commercially profitable in the absence of government regulation.

Processing certain hydrocarbon waste can be trying, because presently there is no system for its collection and the products derived from it may not provide enough commercial value for a profitable operation of a TDP facility. For example, disposable diapers need a specific collection and storage system, and asphalt roof shingles, plastics and car fluff generate end-products of lesser quality which may not generate profits without tipping fees. For such feedstock, governments would need to intervene to impose a selective collection system, a special collection fee or tax to subsidize their recycling at their end-of-life cycle, or restrict landfilling of these products. Consequently, we cannot ensure that these policies may be adopted. Should government intervention not happen or should it stop, it could negatively affect our clients’ results of operations and consequently negatively impact ours as well.

Government regulations could adversely affect the sale or operation of our TDP facilities or handling and sale of their recycled end-products and we may incur significant costs complying with these regulations.

The construction and operation of TDP facilities may be subject to the receipt of approvals and operating permits from various regulatory agencies. The construction of any facility normally requires a construction permit by an authority or county or planning board, that confirms the conformity of the planned construction of building and land settlement with urban planning regulation. In addition, the operation of any facility normally requires a certificate of occupancy or a similar permit requirement, by the local authority, to confirm that the planned operations satisfy local regulations. Finally, a typical permit requirement is from the State or Provincial environment authority that requires the operations to conform with all environmental regulations (federal, State/provincial, local), including air, water and other biological resources, including the temporary storage of waste. In the United States, this environmental permit usually refers to UPA permits (“Uniform Procedures Act”) and is administered by the State department of environment, whereas in Canada it is administered by the provinces and in some instances is referred to as a “Certificate of Authorization”.

The regulatory agencies may not approve the projects in a timely manner or may impose restrictions or conditions on a facility that could potentially prevent construction from proceeding, lengthen its expected completion schedule and/or increase its anticipated cost. We may also face local or public opposition to a TDP facility being located in their vicinity which may obstruct the issuance of the necessary permits.

TDP facility operations also may be subject to governmental regulations and industry standards regarding the quality and specifications of the products that TDP facility operators are expected to produce, store and sell. For example, the demand for the fuel oil produced by our TDP facilities could be impacted by new regulations concerning the sulfur content in fuel oil.

Based on our consultant’s report prepared in 2013,1 we believe the specifications used for our TDP turnkey facilities conform to the governmental regulations in Canada and the United States, that are amongst the most restrictive regulations on air emissions, water and disposal of waste, however we have not reviewed applicable standards in every jurisdiction worldwide, so we cannot assure you that we will not incur additional costs to comply to regulations in other jurisdictions or that the regulation now in effect will not change at the time that the TDP turnkey facilities are constructed and operational. In addition, changes in government regulations and industry standards may occur at any time, reducing the capacity of a TDP facility and our customers’ sales volume, which would impact our royalty stream. Such regulations could also require us to make capital expenditures for equipment modifications, which we cannot evaluate at this point. These modifications may force increases in the capital cost of TDP facilities to be sold and this may impact negatively our sales of TDP turnkey facilities.

Our clients may use, produce and transport hazardous substances and materials such as propane in the operation of a TDP facility. Such operations are subject to a variety of federal, provincial/state and local laws and regulations governing the use, generation, manufacture, transportation, storage, handling and disposal of these substances, chemicals and materials. Our safety procedures for handling, storing, transporting and disposing of these substances, chemicals, materials and waste products may be incapable of eliminating all the risk of accidental injury or contamination from these activities. In the event of contamination or injury, we could be held liable for any resulting damages, including toxic tort claims. There can be no assurance that violations of the environmental, health and safety laws could not occur in the future as a result of, but not limited to, human error, accident, equipment failure, simple changes to environmental regulation and standards.

______________________________

1 Ecolomondo TDP Compliance of Stack and Flare Emissions With 40 CFR Part 60 Standards of Performance and Environment Quebec, by Gilles Tremblay, January 3, 2013.

16

Even though we have not performed any analysis or assessment on the costs to comply with regulation and permitting, we believe that the risk that government regulation will create additional costs for TDP, considering the low emissions level compared to existing regulation standards in Quebec and in the United States, is minimal. Furthermore, any exposure to higher capital costs to comply should not significantly impact our profits because they would be absorbed by our clients that have TDP turnkey facilities in operation at that time, and for future TDP turnkey facilities, they will be reflected in the sales price.

If we fail to deliver equipment that comply with current or future regulations could result in the imposition of fines, revocation of permits, third-party property damage, product liability and personal injury claims, investigation and remediation costs, the suspension of production or a cessation of operations, and our liability may exceed our total assets. Environmental laws could become more stringent over time, imposing greater compliance costs and increasing risks and penalties associated with violations, which could impair our research, development or production efforts and harm our business. Consequently, considerable resources may be required to comply with environmental regulations. Federal, provincial or state, local and foreign environmental requirements may substantially increase our costs or delay or prevent the construction and operation of TDP facilities, which could have a material adverse effect on our business, financial condition and results of operations.

Like us, many companies have been developing technology in this area of business. Other parties may have or could obtain intellectual property rights which could limit our ability to operate freely. Also, competitors and potential competitors who have greater resources and experience than we do, may develop products and technologies that compete with ours and may gain market share at our expense.

Our ability to compete successfully could depend on our ability to develop and maintain proprietary technologies that produce carbon black substitute and fuel oil at commercial-scale and at costs below the prevailing market prices for virgin products.

Some of our competitors may have substantially greater production, financial, research and development, personnel and marketing resources than we do, and may also have larger and more developed patent portfolios. In addition, certain of our competitors may also benefit from local government programs and incentives that are not available to us. As a result, our competitors may be able to develop competing and/or superior technologies and processes and compete more aggressively and sustain competitive advantages over a longer period of time than we could. Our technologies and products may be rendered uneconomical or otherwise obsolete by technological advances or entirely different approaches developed by one or more of our competitors. As more companies develop new intellectual property in our markets, the possibility of a competitor acquiring patent or other rights that may limit our products or potential products increases, which could lead to litigation.

In addition, various governments have recently announced a number of funding programs focused on the development of clean technologies for the reduction of carbon emissions. Such programs could lead to increased funding for our competitors and the rapid increase in the number of participants within the pyrolysis industry.

Our limited resources relative to some of the resources of our competitors may cause us to fail to anticipate or respond adequately to new developments and other competitive pressures. This failure could reduce our competitiveness and market share, adversely affect our results of operations and financial position and prevent us from achieving or maintaining profitability.

Our commercialization strategy relies in part on our ability to negotiate and execute definitive agreements with third parties.

Our commercialization strategy involves definitive agreements with numerous third parties for the commercialization of our TDP platform. In particular, and not limited to, agreements for the supply and licensing of IT systems, engineering services, parts, financing, construction of facilities, sales and the purchase of our clients’ end-products. We must also negotiate and execute definitive contracts with third parties, such as joint venture partners and licensees, otherwise our failure to do so could adversely affect our results of operations, financial position, and prevent us from achieving our goals.

In addition, our clients may have to negotiate and enter into definitive agreements with third parties for financing, tipping fees, carbon credits, as well for feedstock supply. We may have to assist our clients in the negotiation of these types of agreements for which we have limited experience. Each of these agreements is important to our commercialization strategy and that of our clients. We cannot be certain that any of our clients or ourselves may be able to enter into definitive agreements with any or all of these third parties. If our clients are unable to secure and maintain their business relationships for any reason, our business could be adversely affected.

17

Our clients may also rely on third parties to assist in the sale or purchase of carbon black substitute, fuel oil and steel produced by their TDP facility. These third parties may not be effective at selling or willing to purchase these end-products. If they do not fulfill their obligations and default on their contractual duties or perform poorly, our business, results of operations and financial condition could be materially and adversely affected.

International operations could expose us to additional risks that we do not face in Canada or the United States, which could have an adverse effect on our operating results.

We expect to focus the initial commercialization of our TDP technology platform in Canada and in the United States, however international expansion in other continents is part of our growth strategy. As we expand internationally, our operations could be subject to a variety of risks that we do not face in Canada and in the United States.

Our overall success in international markets depends, in part, on our ability to succeed in differing legal, regulatory, economic, social and political conditions. We may not be successful in developing a business model that requires implementing policies and strategies, including joint ventures and licensing arrangements that may be required to effectively manage and control risks and expand our business, in each country where we plan to do business. Our failure to manage these risks successfully could harm our international operations, reduce our international sales and increase our costs, which could adversely affect our business, financial condition and results of operations.

Fluctuations in exchange rates could have a material adverse effect on our results of operations and the value of your investment.

Significant revaluation of the Canadian dollar may have a material adverse effect on your investment. Although we anticipate that the majority of our future revenues will be in U.S. dollars, our costs may be denominated in Canadian dollars and other currencies. Any significant revaluation of our currency may materially and adversely affect our revenues, earnings and financial position, and the value of, and any dividends payable on our Class A Common Shares in U.S. dollars. For example, to the extent that we need to convert U.S. dollars we receive from this initial public offering into Canadian dollars to pay our operating expenses, an appreciation of the Canadian dollar against the U.S. dollar would have an adverse effect on the amount of Canadian dollars we would receive from the conversion. Also, a significant appreciation of the Canadian dollar against the U.S. dollar may significantly reduce the U.S. dollar equivalent of our earnings, which in turn could adversely affect the price of our Class A Common Shares.

Hedging strategies are available in Canada to reduce our exposure to exchange rate fluctuations. To date, we have not entered into any hedging transactions for this purpose. While we may decide to enter into hedging transactions in the future, the availability and effectiveness of these hedges may be limited and we may not be able to adequately hedge our exposure or at all. As a result, fluctuations in exchange rates may have a material adverse effect on your investment.

Management has identified internal control deficiencies, which our management believes constitute material weaknesses.Our Chief Financial Officer does not have experience designing, developing and implementing appropriate internal controls and procedures in publicly-traded companies, which may hinder our ability to maintain effective internal controls over financial reporting. Any future material weaknesses or deficiencies in our internal control over financial reporting could harm stockholder and business confidence in our financial reporting, our ability to obtain financing and other aspects of our business.

In preparing our consolidated financial statements as of and for the year ended December 31, 2015, management identified deficiencies that constituted material weaknesses in our internal control over financial reporting, such as not having sufficient financial reporting and accounting staff with appropriate training in U.S. GAAP and SEC rules and regulations with respect to financial reporting and a lack of segregation of duties. Our Chief Financial Officer is an experienced CPA but does not have experience in designing, developing and implementing appropriate internal controls and reporting procedures. As a result, we cannot assure you that we will not identify or prevent future material weaknesses, or maintain our existing controls and procedures. If other deficiencies occur or we don’t maintain the effectiveness of the current controls, these weaknesses or deficiencies could result in misstatements of our results of operations, restatements of our financial statements, a decline in our stock price and investor confidence or other material effects on our business, reputation, results of operations, financial condition or liquidity, and may require us to incur substantial additional costs to improve our internal control system.