Table of Contents

As filed with the Securities and Exchange Commission on November 13, 2014

Registration No. 333-197660

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 9 TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

VIRGIN AMERICA INC.

(Exact name of registrant as specified in its charter)

| Delaware | 4512 | 20-1585173 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

555 Airport Boulevard

Burlingame, California 94010

(650) 762-7000

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

C. David Cush

President and Chief Executive Officer

Virgin America Inc.

555 Airport Boulevard, Burlingame, California 94010

(650) 762-7000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies To:

Tad J. Freese Nathan C. Salha Latham & Watkins LLP 140 Scott Drive Menlo Park, California 94025 (650) 328-4600 | John J. Varley Senior Vice President and General Counsel Virgin America Inc. 555 Airport Boulevard Burlingame, California 94010 (650) 762-7000 | Alan F. Denenberg Davis Polk & Wardwell LLP 1600 El Camino Real Menlo Park, California 94025 (650) 752-2000 |

Approximate date of commencement of the proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer¨ | |||

| Non-accelerated filerx | (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

| ||||||||

Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price Per Share | Proposed Maximum Aggregate Offering Price (1)(2) | Amount of Registration Fee (3) | ||||

Common Stock, par value $0.01 per share | 15,338,225 | $24.00 | $368,117,400 | $44,224.24 | ||||

| ||||||||

| ||||||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended. |

| (2) | Includes the aggregate offering price of additional shares that the underwriters have the option to purchase to cover overallotments. |

| (3) | Previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated November 13, 2014.

PROSPECTUS

13,337,587 Shares

Common Stock

This is our initial public offering of shares of our common stock. We are offering 13,106,377 shares. In addition, VX Employee Holdings, LLC, a Virgin America employee stock ownership vehicle that we consolidate for financial reporting purposes, is offering 231,210 issued and outstanding shares as a selling stockholder. We will pay the underwriting discounts and expenses for this selling stockholder, but we will not receive any proceeds from the shares sold by this selling stockholder.

No public market currently exists for our shares of common stock.

Our common stock will be listed on the NASDAQ Global Select Market under the symbol “VA.” We anticipate that the initial public offering price per share will be between $21.00 and $24.00.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 25 of this prospectus.

| Per Share | Total | |||||||

Price to the Public | $ | $ | ||||||

Underwriting discounts and commissions (1) | $ | $ | ||||||

Proceeds to us (before expenses) | $ | $ | ||||||

Proceeds to selling stockholder (before expenses) | $ | $ | ||||||

| (1) | We refer you to “Underwriting” beginning on page 169 of this prospectus for additional information regarding underwriting compensation. |

Our principal stockholders, Cyrus Aviation Holdings, LLC (“Cyrus Holdings”), CM Finance Inc (which we refer to together with Cyrus Holdings as “Cyrus Capital”) and affiliates of Virgin Group Holdings Limited (which we refer to in this prospectus collectively as the “Virgin Group”), as option selling stockholders, have granted the underwriters an option to purchase up to 2,000,638 additional shares of common stock at the initial public offering price less the underwriting discount solely to cover overallotments. We will receive no proceeds from the sale of any shares sold by these option selling stockholders if the overallotment option is exercised.

PAR Investment Partners, L.P. (“PAR Capital”) has agreed to purchase approximately $52.1 million of common stock from the Virgin Group and Cyrus Holdings at a price per share equal to 96% of the initial public offering price, in a private placement to close concurrently with this offering. This private placement is subject to certain closing conditions, including requirements that there be no amendment that increases the top end of the price range set forth above and that total gross proceeds from the sale of shares by us in this offering will be at least $250 million. PAR Capital has entered into an agreement with the underwriters pursuant to which it has agreed not to dispose of its shares for a period of 180 days after the date of this prospectus. See “Summary—PAR Capital Private Placement” elsewhere in this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on or about , 2014.

| Barclays | Deutsche Bank Securities |

| BofA Merrill Lynch | Cowen and Company | Goldman, Sachs & Co. | ||

| Imperial Capital | LOYAL3 Securities | Raymond James | ||

, 2014.

Table of Contents

Table of Contents

| Page | ||||

| 1 | ||||

| 22 | ||||

| 25 | ||||

| 40 | ||||

| 41 | ||||

| 45 | ||||

| 47 | ||||

| 48 | ||||

| 52 | ||||

UNAUDITED PRO FORMA CONSOLIDATED BALANCE SHEET AND STATEMENTS OF OPERATIONS | 56 | |||

NOTES TO UNAUDITED PRO FORMA CONSOLIDATED BALANCE SHEET AND STATEMENTS OF OPERATIONS | 61 | |||

| 67 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 70 | |||

| 101 | ||||

| 103 | ||||

| 119 | ||||

| 127 | ||||

| 149 | ||||

| 153 | ||||

| 158 | ||||

| 163 | ||||

MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS | 165 | |||

| 169 | ||||

| 176 | ||||

| 176 | ||||

| 176 | ||||

| F-1 | ||||

We are responsible for the information contained in this prospectus or contained in any free writing prospectus prepared by or on behalf of us to which we have referred you. Neither we, the selling stockholders nor the underwriters, have authorized anyone to provide you with additional information or information different from that contained in this prospectus or in any free writing prospectus filed with the Securities and Exchange Commission, and we take no responsibility for any other information that others may give you. We and the selling stockholders are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock. Our business, results of operations or financial condition may have changed since such date.

Until , 2014 (25 days after the date of this prospectus), all dealers that buy, sell or trade shares of our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the dealer’s obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

For investors outside the United States: Neither we, the selling stockholders nor any of the underwriters have taken any action that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

i

Table of Contents

This summary highlights selected information about us and the common stock being offered by us and the selling stockholders. It may not contain all of the information that is important to you. Before investing in our common stock, you should read this entire prospectus carefully for a more complete understanding of our business and this offering, including our financial statements and the accompanying notes and the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Overview

Virgin America is a premium-branded, low-cost airline based in California that provides scheduled air travel in the continental United States and Mexico. We operate primarily from our focus cities of Los Angeles and San Francisco to other major business and leisure destinations in North America. We provide a distinctive offering for our passengers, whom we call guests, that is centered around our brand and our premium travel experience, while at the same time maintaining a low-cost structure through our point-to-point network and high utilization of our efficient, single fleet type. Our distinctive business model allows us to offer a product that is attractive to guests who historically favored legacy airlines but at a lower cost than that of legacy airlines. This business model enables us to compete effectively with other low-cost carriers, or LCCs, by generating a higher stage-length adjusted revenue per available seat mile. Conversely, while our lower density seating configuration and the cost of our premium services contribute to a higher stage-length adjusted cost per available seat mile than that of other LCCs, our underlying cost structure stemming principally from our single fleet type and point-to-point network is competitive within the industry. As of September 30, 2014, we provided service to 21 airports in the United States and Mexico with a fleet of 53 narrow-body aircraft.

Leveraging the reputation of the Virgin brand, a global brand founded by Sir Richard Branson, we target guests who value the experience associated with the Virgin brand and the high-quality product and service that we offer. Our employees, whom we call teammates, provide a personalized level of service to our guests that is a key component of our product. Other elements of our premium product available fleetwide include power outlets adjacent to every seat, inflight wireless internet access, distinctive on-board mood lighting, leather seats, high-quality food and beverage offerings and our Red® inflight entertainment system, which we believe is industry leading, featuring a nine-inch personal touch-screen interface with a variety of features available on-demand, including live television, movies, seat-to-seat text chat, games, interactive maps and music. We have won numerous awards for our product, including Best Domestic Airline inTravel + Leisure Magazine’s World’s Best Awards and Best Domestic Airline inCondéNast Traveler Magazine’s Readers’ Choice Awards for the past seven consecutive years as well as Best U.S. Business/First Class Airline in Condé Nast Traveler Magazine’s Business Travel Poll for the past six consecutive years.

LCCs in the United States generally operate point-to-point networks with a single fleet type, a single class of service with a relatively high density seating configuration, high degree of outsourced operational services and high aircraft utilization. While we have many of these characteristics, we differentiate ourselves from other LCCs in the United States with additional attributes that business and high-end leisure travelers value. In contrast to most LCCs, we have three classes of service onboard our aircraft. In addition to our Main Cabin economy product, we offer our guests a First Class product and a premium economy class product called Main Cabin Select. We also provide a number of other amenities that are important to frequent travelers, including our Elevate® loyalty program with tiered benefits for our most loyal guests, lounge access in certain airports, including our own Virgin America Loft at Los Angeles International Airport (LAX), interline and codeshare partnerships with other airlines and a wide range of distribution channels and contractual travel discounts for over 250 major corporate customers and travel agents. While these amenities result in a higher cost per available seat mile, or CASM, than we could otherwise achieve with a more traditional LCC model, we believe that these amenities, along with our premium on-board features, enabled us to realize the highest average passenger revenue per available seat mile, or PRASM, in 2013 among U.S. LCCs within most of our markets.

1

Table of Contents

Our disciplined cost control is also core to our strategy, and we maintain the cost simplicity of other LCCs. We operate one of the youngest fleets among U.S. airlines, comprised entirely of fuel-efficient Airbus A320-family aircraft. Our single fleet type allows us to avoid the operational complexities and cost disadvantages of carriers with multiple and older fleet types. In addition, our long-haul, point-to-point network results in high aircraft utilization and efficient scheduling of our aircraft and crews. We believe that our teammates are productive and attentive to our guests, contributing to our cost advantage while maintaining our high-quality travel experience. We also outsource many non-core functions, such as certain ground handling activities, major airframe and engine maintenance and call center functions, leading to efficient, cost-competitive services and flexibility in these areas.

Executing our strategy of providing a premium travel experience within a disciplined, competitive cost structure has led to improved financial results. For 2013, we recorded operating revenues of $1.4 billion, operating income of $80.9 million and net income of $10.1 million. We increased our revenue per available seat mile, or RASM, in 2013 by 9.3% compared to 2012, the largest increase of any major U.S. airline. Furthermore, our CASM of 10.98 cents increased by only 0.7% from 2012. On a stage-length adjusted basis, our 2013 CASM was competitive within the industry and below that of legacy airlines. We completed a recapitalization of a majority of our operating lease and debt obligations in May 2013, contributing to a $34.7 million decline in aircraft rent expense and a $44.8 million decline in interest expense for 2013 compared to 2012. As a result of our RASM increase and the reduction in rent and interest expense, our financial performance improved from a net loss of $145.4 million in 2012 to net income of $10.1 million in 2013. In the first nine months of 2014, we had net income of $56.2 million, compared to a net loss of $4.0 million in the first nine months of 2013. Our RASM in the first nine months of 2014 increased by 4.8% from the prior year period, while our CASM in the first nine months of 2014 increased by only 2.4% from the prior year period.

Our business model relies on attracting guests who value the premium product that we provide. Because we provide a high level of amenities to our guests, it generally requires a longer period of time for us to reach profitability in each new market that we enter than it might require for a traditional LCC that does not provide this higher level of service. However, we believe that in the long term, our business model enables us to have financially successful routes as evidenced by our PRASM premium over other LCCs in our markets and in part by our recent history of operating profitability in 2013 after two years of rapid growth into new markets in 2011 and 2012.

Our Competitive Strengths

We believe the following strengths allow us to compete successfully in the U.S. airline industry:

Premium Travel Experience. We believe our premium guest experience, attractive amenities, customer-focused teammates and wide array of inflight entertainment options differentiate us from other airlines in the United States. A key component of our product strength is the consistency across our entire fleet. In contrast to airlines with multiple aircraft types, our product offering is identical on every Airbus 320-family aircraft, allowing for the same enhanced travel experience on every flight. We also differentiate ourselves from other LCCs by providing both First Class and Main Cabin Select products in addition to our Main Cabin economy product. With just eight seats on every aircraft—fewer than most first class cabins offered on competing airlines, our First Class cabin has an exclusive feel with a dedicated attendant providing a personal level of service. Unlike many other airlines, we do not provide complimentary upgrades to First Class, enhancing the exclusivity of this product. In addition to more leg room, which is a standard feature of most premium economy products, we offer additional features within Main Cabin Select, such as complimentary on-demand current-run movies, premium television programs, premium beverages and Main Cabin meals and snacks. We have differentiated our product in all three classes of service as compared to other domestic airlines, leading to a travel experience that can only be found on Virgin America.

World-Class Virgin Brand. We believe that the Virgin brand is widely recognized in the United States and is known for being innovative, stylish, entrepreneurial and hip. We believe that the brand is recognized

2

Table of Contents

worldwide from the Virgin Group’s offerings in music, air travel, wireless service and a wide variety of other products. We capitalize on the strength of the Virgin brand to target guests who value an enhanced travel experience and association with the Virgin brand. We believe that the Virgin brand has helped us to establish ourselves as a premium airline in the domestic market in a short period of time. When we enter a new market, awareness of the Virgin brand generates interest from new guests. The power of the Virgin brand provides an opportunity for low-cost public relations events that generate extensive media coverage in new markets and has led to other cooperative marketing relationships for us with major companies. In addition to capitalizing on the Virgin brand strength, we are rapidly establishing Virgin America as a distinct and premium brand for air travel in the United States in its own right. We believe our guests associate the Virgin and Virgin America brands with a distinctive high-quality and high-value travel experience.

Low-Cost, Disciplined Operating Structure. A core component of our business model is our disciplined cost structure. Key components of this low cost structure include our modern, fuel-efficient single-aircraft fleet, our high aircraft utilization, our point-to-point operations, our productive and engaged workforce, our outsourcing of non-core activities and our lean, scalable overhead structure. We are committed to maintaining this disciplined cost structure and believe we will continue to improve our competitive cost position as we grow and further leverage our existing infrastructure. In 2013, the average stage-length adjusted domestic CASM of legacy airlines was 31% higher, and the average stage-length adjusted domestic CASM of LCCs was only 17% lower, than our stage-length adjusted CASM. Our lower seating density and three-class cabin configuration, which is a similar configuration to that of many legacy airlines, is the primary reason that our stage-length adjusted CASM was higher than that of other LCCs in 2013. However, our seating configuration with three classes of service was also a primary contributor to our higher stage-length adjusted PRASM in 2013 when compared to other LCCs. For example, Spirit Airlines configures an Airbus A320 aircraft with 178 seats in a single class of service compared to our seating density of 146 seats for the same aircraft. We believe that Spirit Airlines’s 22% higher seating density per aircraft contributed to its lower stage-length adjusted PRASM and lower stage-length adjusted CASM in 2013, when compared to ours.

Established Presence in Los Angeles and San Francisco. We have built our network around the Los Angeles and San Francisco metropolitan areas, the second- and third-largest domestic air travel markets in the United States in 2013. We believe that these two markets, with a combined population of approximately 27 million people and strong economic bases in the technology, media and entertainment industries, serve as an excellent platform for long-term growth. Los Angeles and San Francisco both have large populations of technologically savvy, entrepreneurial and innovative individuals who we believe value our brand and premium guest experience. We have made significant investments in these key markets since 2010, and as of September 30, 2014 we provide service to 18 destinations from Los Angeles and 20 destinations from San Francisco. These destinations include eight of the top ten domestic destinations served from LAX and nine of the top ten domestic destinations served from San Francisco International Airport (SFO), based on passenger volume. This investment provides greater network coverage across North America for travelers from these two focus markets, and we expect that this investment will allow us to continue to grow by leveraging the loyal guest base that we have established in each market.

Our Team and Entrepreneurial Culture. Our teammates and culture are essential elements of our success because they contribute significantly to our premium travel experience. We start by hiring the right teammates through a rigorous process that includes numerous interviews, as well as pre-employment testing for our frontline teammates and our pilots. Key characteristics of Virgin America teammates include a friendly, personable nature, a willingness to think differently, a passionate approach to his or her work and intense pride in Virgin America and our product. We empower our teammates with a high level of authority to resolve guest issues throughout the travel experience, from making flight reservations to interactions at the airport and in flight. We strive to create an environment for our teammates where open communication is both encouraged and expected and where we celebrate our successes together. We believe our positive work environment has contributed to our having one of the highest customer satisfaction rankings in the airline industry.

3

Table of Contents

Our Growth Strategy

Our goal is to generate above-average RASM in each market we serve by providing the leading domestic air travel product through our brand and our premium guest experience, while at the same time maintaining our competitive cost structure through the efficient operations we have established. Key elements of our growth strategy include:

Leverage Our Recent Expansion.We have significantly expanded our fleet size and route network since 2010. We increased our operating fleet from 28 aircraft as of June 30, 2010 to 53 aircraft as of April 30, 2013, and we introduced service to 11 new airports during that period, doubling the number of destinations served. Airline routes tend to become more profitable as they mature because of increased demand as travelers become aware of the service and through repeat business. Our RASM in markets that we entered in 2011 and 2012 increased from 2012 to 2013 by 20.5% as compared to our overall RASM increase of 9.3%. In addition, as we continue to expand our network by increasing the number of markets served from Los Angeles and San Francisco, we expect our network to become more attractive to frequent travelers who prefer to concentrate their travel with one airline, increasing demand for service on our existing routes. We intend to leverage our recent expansion to drive higher RASM.

Expand Our Route Network.We currently serve only 15 of the 50 largest metropolitan areas in the United States and three leisure destinations in Mexico. We believe there are significant opportunities to expand our service from our focus cities of Los Angeles and San Francisco to other large markets throughout the United States, Canada and Mexico. We have firm commitments to take delivery of ten Airbus A320-family aircraft from July 2015 through June 2016, and we expect to continue to grow at a measured, disciplined pace beyond 2016. While we expect most of our expansion in the next several years will focus on the opportunities we have at Los Angeles and San Francisco, we are also growing our presence in Dallas, Texas. Through the use of recently acquired slots at New York LaGuardia Airport (LGA) and Ronald Reagan Washington National Airport (DCA), we added service at Dallas Love Field (DAL) to these markets in October 2014. We also moved our service between Dallas and LAX and Dallas and SFO from Dallas/Fort Worth International Airport (DFW) to DAL. DAL is located in a growing, affluent section of the Dallas/Fort Worth metropolitan area and is the closest airport to downtown Dallas. In addition, the airline facilities at DAL are limited by federal law to only 20 gates, providing a structural barrier to entry. We believe our new service at DAL will further diversify our route network and allow us to provide service to LGA and DCA. In addition, we intend to expand our codeshare and interline relationships with other airlines that are complementary to our network, expanding travel destination options for our guests while adding new sources of revenue and more guests.

Maintain Competitive Unit Operating Costs.We are highly focused on maintaining competitive unit operating costs. We expect to realize economies of scale as we continue to grow by leveraging our distribution, marketing and technology costs across our platform and by better utilizing our facilities and ground assets across a larger network. Our fleet is 100% financed by operating leases, of which 26 leases will expire between 2015 and 2022. As our leases expire, we expect to have the opportunity to lower our costs by renewing at lower lease rates or by opportunistically replacing these aircraft with new Airbus A320-family aircraft with lower operating costs sourced in the open market. In addition, we expect our cost structure will continue to benefit from our highly productive and flexible workforce as we grow our fleet and network.

Continue to Grow Our Base of Frequent Travelers.We intend to continue to grow our share of business travelers, a focus that is uncommon among U.S. LCCs, because we believe this population of airline travelers allows us to achieve increased RASM. We target the business community by providing a premium travel service between our focus cities and many of the most important business destinations in North America, as well as key leisure destinations that we believe are important to business travelers when flying for leisure travel. We have already attracted a significant base of frequent business and premium leisure travelers who regularly fly with us and who we believe prefer our premium product attributes. We believe that these types of guests also value a

4

Table of Contents

larger route network and frequent flights within markets. As we grow our network from California and expand our interline and codeshare partnerships, we believe we will be well positioned to attract additional business and high-end leisure travelers. We consider guests who book within 14 days of departure as business travelers. Using this as a measure, we believe that approximately 30% of our guests in 2013 were business travelers, representing approximately 40% of our revenue in 2013.

Continue to Enhance Our Product and Guest Experience.We believe our guest experience is unique in the industry and revolves around our teammates’ focus on guest service, extensive entertainment options, compelling passenger comfort features and an association with our brand that would be difficult to replicate. We nevertheless are continually developing new enhancements to our product. For example, in early 2014, we further expanded our First Class food service on select flights to include enhanced gourmet food offerings and linen service. In the second quarter of 2014, we launched a redesigned version of the Virgin America website, enhancing the ease of use and functionality as well as providing a more customized experience for our guests. In 2015, we plan to upgrade the monitors within our inflight entertainment system to include a “swipe” touch capability, similar to that found on many modern personal electronic devices. This upgrade will include a redesign of the software behind our Red inflight entertainment system, allowing for future software features to what we believe is already an industry-leading system. Additionally, we continually analyze new technologies for longer-term enhancements to our fleet, inflight product and airport experience.

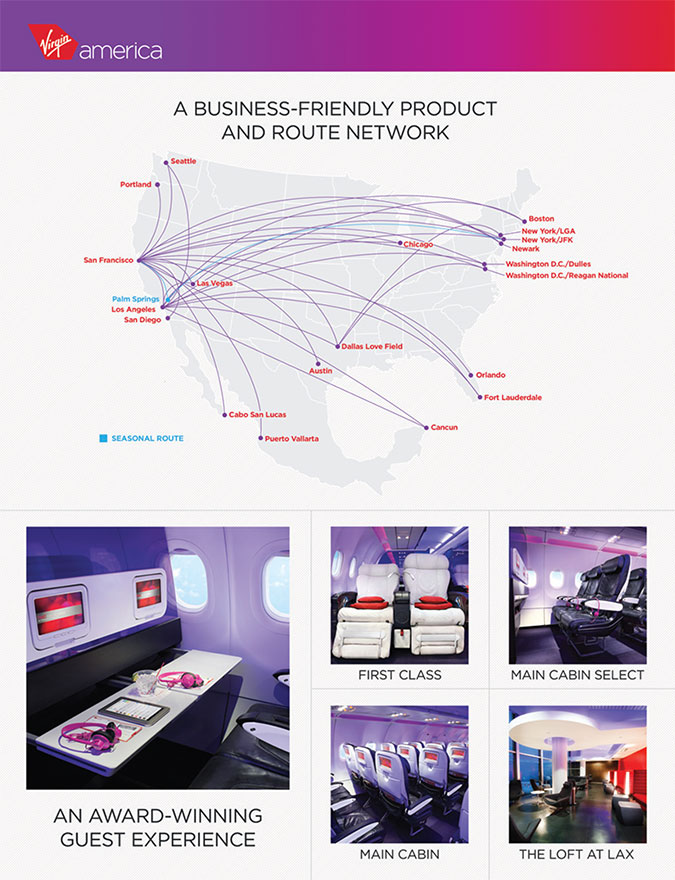

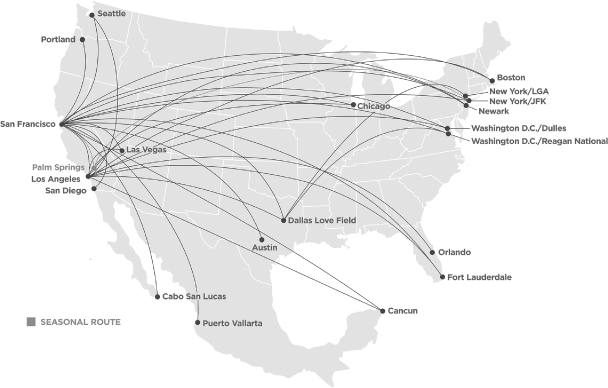

Route Network

We served 21 airports throughout North America as of September 30, 2014. The majority of our routes operate to and from our focus cities of Los Angeles and San Francisco. Our current network is a mix of long-haul, transcontinental service combined with short-haul West coast service and select Mexico leisure destinations. Below is a route map of our network.

5

Table of Contents

We use publicly available data related to existing traffic, fares and capacity in domestic markets to identify growth opportunities. To monitor the profitability of each route, we analyze monthly profitability reports as well as near-term forecasting. We routinely make adjustments to capacity and frequency of flights within our network based on the financial performance of our markets, and we discontinue service in markets where we determine that long-term profitability is not likely to meet our expectations.

Our future network plans include growing from our focus cities of Los Angeles and San Francisco to other major markets in North America. By continuing to add destinations in select markets from Los Angeles and San Francisco, we can leverage our existing base of loyal guests and grow our share of revenue within these focus cities while also expanding our customer base as we gain new guests in new markets. We have also recently added service from DAL to LGA and DCA. We believe this DAL opportunity will further diversify our route network and provide growth into strategic airports that are limited by regulation.

Fleet

We fly only Airbus A320-family aircraft and operate only CFM engines, which provide us significant operational and cost advantages compared to airlines that operate multiple fleet and engine types. Flight crews are entirely interchangeable across all of our aircraft, and maintenance, spare parts inventories and other operational support are highly simplified relative to more complex fleets. Due to this commonality among Airbus single-aisle aircraft, we retain the benefits of a fleet consisting of a single family of aircraft while still having flexibility to match the capacity and range of the aircraft to the demands of many routes.

We have a fleet of 53 Airbus single-aisle aircraft, consisting of ten Airbus A319s and 43 Airbus A320s. The average age of the fleet was 5.6 years at September 30, 2014. Our Airbus A319 aircraft accommodate 119 guests, and our Airbus A320 aircraft accommodate 146-149 guests. All of the existing aircraft are financed under operating leases.

We plan to grow our fleet with additional Airbus A320-family aircraft, and we currently have an order with Airbus for ten Airbus A320 aircraft to be delivered between July 2015 and June 2016 and 30 Airbus A320 new engine option, or A320neo, aircraft to be delivered between 2020 and 2022. We have an option to cancel our Airbus A320neo positions up to two years in advance of delivery in groups of five aircraft, but we could incur a loss of deposits and credits as a cancellation fee. We may elect to supplement these deliveries by additional acquisitions from Airbus or in the open market if demand conditions merit. Twenty-six of our existing operating leases will expire between 2015 and 2022, and we believe there will be an opportunity to extend these leases at a reduced lease rate or to replace them with new or used Airbus A320-family aircraft. Although we expect to grow our fleet as we increase our flights on our existing route network and expand our route network to new markets, we are only committed to grow to 63 aircraft. As a result, our fleet plan provides significant flexibility.

Our Airbus A320 aircraft deliveries in 2015 and 2016 will be equipped with sharklets, a new wingtip device that we believe will create up to 3.0% additional fuel efficiency in our network. In addition to lowering our average fuel cost per flight, the sharklets provide increased range. This will reduce technical stops on our transcontinental flights that occasionally occur during specific weather patterns as well as allow for the possibility of operations to the state of Hawaii. Operating to Hawaii will require additional Federal Aviation Authority, or FAA, certification for extended twin-engine over-water operations, and we are currently evaluating these markets and the additional operational requirements.

6

Table of Contents

Risk Factors

Our business is subject to numerous risks and uncertainties, including those highlighted in the section entitled “Risk Factors” immediately following this prospectus summary, that represent potential challenges we face in connection with the successful implementation of our strategy and the growth of our business. We expect a number of factors to cause our results of operations to fluctuate on a quarterly and annual basis, which may make it difficult to predict our future performance. Such factors include:

| • | the price and availability of aircraft fuel; |

| • | our ability to compete in an extremely competitive industry; |

| • | the successful execution and implementation of our strategy; |

| • | security concerns resulting from any threatened or actual terrorist attacks or other hostilities; |

| • | our reliance upon technology and automated systems to operate our business; |

| • | our reputation and business being adversely affected in the event of an emergency, accident or similar incident; |

| • | changes in economic conditions; |

| • | our limited profitable operating history; |

| • | changes in governmental regulation; and |

| • | our ability to obtain financing or access capital markets. |

Corporate Information

We were incorporated in the state of Delaware in 2004 as Best Air Holdings, Inc. We changed our name to Virgin America Inc. in November 2005. Our principal executive offices are located at 555 Airport Boulevard, Burlingame, California 94010. Our general telephone number is (650) 762-7000, and our website address is www.virginamerica.com. We have not incorporated by reference into this prospectus any of the information on, or accessible through, our website, and you should not consider our website to be a part of this document. Our website address is included in this document for reference only.

Virgin America®, the Virgin America logo and the Virgin signature are trademarks of Virgin America Inc. in the United States and other countries by license from certain entities affiliated with the Virgin Group. This prospectus also contains trademarks and trade names of other companies.

2014 Recapitalization

As of September 30, 2014, we had a total of $678.8 million of contractual obligations for principal and accrued interest outstanding under certain secured related-party notes, which we refer to in this prospectus as the “Related-Party Notes.” As of September 30, 2014, the Virgin Group held approximately $417.1 million aggregate principal amount and accrued interest of the Related-Party Notes, and Cyrus Capital held approximately $261.7 million aggregate principal amount and accrued interest of the Related-Party Notes. The Virgin Group and Cyrus Capital also hold the majority of our outstanding warrants to purchase shares of our common stock, which we refer to in this prospectus as the “Related-Party Warrants.”

We intend to enter into a recapitalization agreement with the Virgin Group, Cyrus Capital and certain of our other security holders, which we refer to in this prospectus as the “2014 Recapitalization Agreement.” The 2014 Recapitalization Agreement would provide that we would retain net proceeds in connection with this offering of $219.6 million, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus) (after we pay underwriting discounts on the shares sold in this offering) and

7

Table of Contents

that remaining net proceeds, which we estimate to be $51.5 million (based on an assumed initial public offering price of $22.50 per share, the midpoint of the price range set forth on the cover of this prospectus), would be used to repay a portion of the Related-Party Notes. Remaining principal and accrued interest under the Related-Party Notes would either be (1) exchanged for a new $50.0 million note bearing interest at a rate of 5.0% per annum, compounded annually, which we refer to as the “Post-IPO Note”; (2) repaid in connection with the release to us of cash collateral held by our credit card processors in exchange for a letter of credit facility arranged by the Virgin Group, which we refer to as the “Letter of Credit Facility”; or (3) exchanged for shares of our common stock, as described more fully in “2014 Recapitalization” elsewhere in this prospectus. In addition, Related-Party Warrants either would be exchanged without receipt of cash consideration for shares of our common stock in amounts agreed to in the 2014 Recapitalization Agreement or be cancelled in their entirety, as described more fully in “2014 Recapitalization” elsewhere in this prospectus.

We anticipate that, after consummation of the transactions contemplated by the 2014 Recapitalization Agreement, which we refer to in this prospectus as the “2014 Recapitalization,” and upon the closing of this offering, only the Post-IPO Note, and none of the Related-Party Notes or the Related-Party Warrants, would remain outstanding. We also anticipate that each issued and outstanding share of our Class A, Class A-1, Class B, Class C and Class G common stock and each issued and outstanding share of our convertible preferred stock would be converted into one share of common stock in accordance with our certificate of incorporation. Based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus), we do not anticipate that any warrants to purchase common stock will be outstanding upon the closing of this offering.

For more information, see “2014 Recapitalization” elsewhere in this prospectus. The transactions contemplated by the 2014 Recapitalization Agreement, which we refer to in this prospectus as the “2014 Recapitalization,” would be contingent upon the consummation of this offering.

Immediately after this offering of 13,337,587 shares of our common stock at an assumed initial public offering price of $22.50 per share, the midpoint of the price range set forth on the cover of this prospectus, after deducting underwriting discounts and estimated offering expenses payable by us and the application of such net proceeds as described under “Use of Proceeds” elsewhere in this prospectus and after the PAR Capital Private Placement described below, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus), our principal stockholders, the Virgin Group and Cyrus Holdings, will own approximately 19.0% (which does not include the Virgin Group’s non-voting common stock) and 32.8% of our outstanding common stock.

Following this offering, the Virgin Group will have the right to designate a member of our board of directors pursuant to amended and restated license agreements related to our use of the Virgin name and brand that we intend to enter into with the Virgin Group. Mr. Evan Lovell, a member of our board of directors since April 2013 and a partner of the Virgin Group, plans to remain on our board of directors following this offering as the Virgin Group’s designee.

PAR Capital Private Placement

PAR Capital has agreed to purchase approximately $52.1 million of common stock from the Virgin Group and Cyrus Holdings in a private placement at a price per share equal to 96% of the initial public offering price. We estimate the number of shares to be sold by the Virgin Group and Cyrus Holdings to be 2,314,814 shares, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus). This private placement will close concurrently with this offering. If there is an increase in the top end of the price range for this offering from that stated on the cover of this prospectus, PAR Capital has the option not to proceed with the private placement. The sale of these shares will not be registered under the Securities Act. This private placement, which we refer to as the “PAR Capital Private Placement,” is subject to customary closing conditions, including a requirement that total gross proceeds from the sale of shares

8

Table of Contents

by us in this offering will be at least $250 million. In connection with the PAR Capital Private Placement, we have agreed to pay to the Virgin Group and Cyrus Holdings an aggregate amount equal to the aggregate discount to the initial public offering price of the shares purchased by PAR Capital from the Virgin Group and Cyrus Holdings. We estimate the aggregate amount of this payment to be approximately $2.1 million, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus). We have also agreed to pay a private placement commission to Barclays Capital Inc. and Deutsche Bank Securities Inc. in connection with the PAR Capital Private Placement, which we expect to be between $0.65 million and $1.17 million, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus). This offering is not conditioned upon the closing of the PAR Capital Private Placement. If the PAR Capital Private Placement does not close, the Virgin Group and Cyrus Holdings will continue to hold the shares they would have otherwise sold to PAR Capital.

9

Table of Contents

THE OFFERING

Common stock offered by us | 13,106,377 shares |

Common stock offered by the selling stockholder | 231,210 shares |

Common stock to be sold by the Virgin Group and Cyrus Holdings to PAR Capital in the PAR Capital Private Placement | 2,314,814 shares(1) |

Shares outstanding after the offering | 43,213,844 shares(2) |

Underwriters’ overallotment option to purchase additional shares | Our principal stockholders, Cyrus Holdings, CM Finance Inc and the Virgin Group, as option selling stockholders, have granted the underwriters an option to purchase up to 2,000,638 additional shares of common stock solely to cover overallotments. |

Use of proceeds | We estimate that we will receive net proceeds from this offering of approximately $271.1 million, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus) and after deducting underwriting discounts and expenses of this offering payable by us. |

| VX Employee Holdings, LLC, a Virgin America employee ownership vehicle that we consolidate for financial reporting purposes will sell 231,210 issued and outstanding shares as a selling stockholder, and we will distribute the gross proceeds, which we estimate to be $5.2 million, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus), to eligible teammates, which do not include our officers. We will pay the underwriting discounts and expenses of VX Employee Holdings, LLC in this offering. We will not receive any proceeds from the sale of shares by the selling stockholder in this offering. |

From the 13,106,377 shares of common stock we are selling in this offering, we will retain net proceeds of $219.6 million, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus), $214.5 million of which will be used for general corporate purposes, including working capital, sales and marketing activities, general and administrative matters and capital expenditures, including future flight equipment acquisitions, and $5.1 million of which, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus), will be used for certain required disbursement items as described in “Use of Proceeds” elsewhere in this prospectus.

In connection with the 2014 Recapitalization, we intend to use the remaining net proceeds received by us from this offering, which we |

10

Table of Contents

estimate will be $51.5 million, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus), to repay principal and accrued interest on certain Related-Party Notes held by Cyrus Capital and the Virgin Group. For more information, see “2014 Recapitalization” and “Use of Proceeds” elsewhere in this prospectus. |

| If the overallotment option is exercised, Cyrus Holdings, CM Finance Inc and the Virgin Group, as option selling stockholders, will sell the shares of our common stock deliverable upon such exercise, and we will not receive any proceeds from the sale of such shares. See “Principal and Selling Stockholders” elsewhere in this prospectus. |

Risk factors | See “Risk Factors” and the other information included elsewhere in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

Proposed NASDAQ Global Select Market symbol | “VA” |

| (1) | The number of shares of common stock to be sold by the Virgin Group and Cyrus Holdings to PAR Capital in the PAR Capital Private Placement is based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus). |

| (2) | The number of shares outstanding after the offering is based on 1,950,671 shares of our common stock (including non-voting common stock) outstanding (on an as converted to common stock basis) as of September 30, 2014, and excludes: |

| • | an aggregate of 411,710 shares of common stock reserved for issuance under our 2005 Stock Incentive Plan; |

| • | 1,052,491 shares of common stock issuable upon the exercise of stock options outstanding as of September 30, 2014 at a weighted-average exercise price of $15.97 per share, of which 115,411 are vested and exercisable; |

| • | 297,269 shares of common stock issuable upon the vesting of restricted stock units, or RSUs, as of September 30, 2014 under our 2005 Stock Incentive Plan that vest once the price of our stock equals or exceeds $30.20 per share on a daily moving-average basis over a 90-day period after the expiration of the lockup agreements described in this prospectus; |

| • | 655,904 shares of common stock issuable upon the vesting of additional RSUs outstanding as of September 30, 2014, of which 604,384 shares vest once the price of our stock meets certain price thresholds, which range from $18.87 to $37.74 per share, on a daily moving-average basis over a six-month period after completion of this offering, (provided that 298,054 of such shares are also subject to additional service conditions which range from 12 to 36 months) and 51,520 of which have no stock price thresholds and vest over service terms ending between January 2015 and January 2017; |

| • | 343,722 shares of common stock issuable upon the vesting of RSUs approved by our board of directors to be granted to certain executive officers, members of our board of directors and other management contingent upon completion of this offering and which vest over a three-year service term; |

| • | rights to purchase 109,703 shares of common stock at an exercise price of $27.25 per share outstanding as of September 30, 2014; |

11

Table of Contents

| • | an aggregate of 600,000 shares of common stock reserved for issuance under our 2014 Equity Incentive Award Plan; and |

| • | an aggregate of 160,000 shares of common stock reserved for issuance under our 2014 Employee Stock Purchase Plan. |

Except as otherwise indicated, information in this prospectus (including the number of shares outstanding after this offering) reflects or assumes that the following will have taken place, which we refer to in this prospectus as the “Transactions”:

| • | that we have effected a 1-for-7.5489352 reverse stock split of our common stock prior to the consummation of this offering; |

| • | that our amended and restated certificate of incorporation, which we will file in connection with the completion of this offering, is in effect; |

| • | that the Virgin Group and Cyrus Holdings have sold an aggregate of 2,314,814 shares of common stock, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus), to PAR Capital in the PAR Capital Private Placement; |

| • | that 218,550 shares of common stock approved by our board of directors have been issued to certain executive officers and management upon completion of this offering; |

| • | that 39,582 shares of common stock have been issued upon the exercise of rights to purchase such shares at an exercise price of $27.25 per share; |

| • | that the 2014 Recapitalization has been completed, including that we have issued 27,898,664 shares of common stock in connection therewith, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus); |

| • | that each issued and outstanding share of our convertible preferred stock and our Class A, Class A-1, Class B, Class C and Class G common stock has converted into one share of common stock in connection with the 2014 Recapitalization, which we refer to in this prospectus as “on an as converted to common stock basis”; and |

| • | that there has been no exercise of the underwriters’ overallotment option to purchase up to 2,000,638 additional shares of our common stock from the option selling stockholders. |

The number of shares outstanding after the offering will depend primarily on the price per share at which our common stock is sold in this offering and the total size of this offering. In connection with this offering and pursuant to the 2014 Recapitalization:

| • | the principal and accrued interest outstanding pursuant to our Related-Party Notes either (i) would be repaid with a portion of the net proceeds from this offering and amounts equal to the release of credit card holdbacks in connection with the establishment of the Letter of Credit Facility, (ii) would be exchanged for the Post-IPO Note or (iii) would be exchanged for shares of our common stock based on the initial public offering price of this offering; |

| • | our currently outstanding warrants to purchase shares of our common stock, including our Related-Party Warrants, either (i) would be exchanged without receipt of cash consideration for shares of our common stock in amounts agreed to in the 2014 Recapitalization Agreement, which depend in part on the initial public offering price of this offering or (ii) would otherwise be cancelled; and |

| • | each issued and outstanding share of our convertible preferred stock and our Class A, Class A-1, Class B, Class C and Class G common stock would be converted into one share of common stock. |

12

Table of Contents

In this prospectus, in calculating the number of shares of common stock to be issued pursuant to the 2014 Recapitalization, we have assumed the application of the net proceeds to us as set forth in “Use of Proceeds” elsewhere in this prospectus an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus) and an assumed initial public offering date of September 30, 2014 for purposes of calculating accrued interest on the Related-Party Notes. For more information, see “Use of Proceeds” and “2014 Recapitalization” elsewhere in this prospectus.

A change in the offering price and, accordingly, the amount of net proceeds received by us, would result in changes to the application of the net proceeds as set forth in “Use of Proceeds” elsewhere in this prospectus and in the following variables: (1) the amount of principal and accrued interest outstanding pursuant to our Related-Party Notes that are not repaid with net proceeds from this offering; (2) the number of shares of common stock that would be issued upon exchange of such Related-Party Notes; and (3) the number of shares of common stock that would be issued upon exchange of our Related-Party Warrants. The following table shows (in thousands, except per share data) the effects of various initial public offering prices on these variables based on the assumptions described above. The initial public offering prices shown below are hypothetical and illustrative only.

Assumed Initial | Repayment of Related- Party Notes (1) | Shares of Common Stock Issued Upon Exchange for Related-Party Notes (2) | Shares of Common Stock Issued Upon Exchange for Related- Party Warrants (3) | Pro Forma Shares of Common Stock Outstanding (4) | Pro Forma as Adjusted Shares of Common Stock Outstanding (5) | |||||||||||||||

$21.00 | $ | 133,373,809 | 25,197,260 | 3,806,839 | 32,876,960 | 44,319,279 | ||||||||||||||

21.50 | 139,417,086 | 24,282,412 | 4,324,529 | 32,725,497 | 43,922,121 | |||||||||||||||

22.00 | 145,460,364 | 23,419,639 | 4,818,688 | 32,591,411 | 43,553,507 | |||||||||||||||

22.50 | 151,503,642 | 22,607,785 | 5,290,879 | 32,475,852 | 43,213,844 | |||||||||||||||

23.00 | 157,546,920 | 21,831,220 | 5,742,543 | 32,365,311 | 42,888,943 | |||||||||||||||

23.50 | 163,590,198 | 21,087,710 | 6,174,992 | 32,259,489 | 42,577,882 | |||||||||||||||

24.00 | 169,633,476 | 20,375,175 | 6,589,418 | 32,158,066 | 42,279,773 | |||||||||||||||

| (1) | Reflects the sum of $100.0 million of cash collateral to be released to us in connection with the Letter of Credit Facility by certain companies that process substantially all of our credit card transactions, which will be used to repay principal and accrued interest on certain Related-Party Notes, and that portion of the net proceeds from the shares sold by us in this offering that we intend to use to repay principal and accrued interest on certain Related-Party Notes after deducting from the net proceeds the amount that we will retain for general corporate purposes. See “Use of Proceeds” elsewhere in this prospectus. The net proceeds that we will retain for purposes other than repayment of Related-Party Notes include $214.5 million (including the $1.8 million reimbursement to us for offering expenses paid by us prior to September 30, 2014), plus the following amounts that vary based on the initial public offering price: (i) amounts we have agreed to pay to certain of our aircraft lessors in settlement of accelerated lease obligations triggered by the repayment of Related-Party Notes as part of the 2014 Recapitalization; (ii) the amount we have agreed to pay to the Virgin Group and Cyrus Holdings in connection with the PAR Capital Private Placement, which will be equal to the number of shares purchased by PAR Capital multiplied by 4% of the initial public offering price per share; (iii) the commission that we have agreed to pay to Barclays Capital Inc. and Deutsche Bank Securities Inc. in connection with the PAR Capital Private Placement, which we expect to be between $0.65 million and $1.17 million, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus); and (iv) amounts that we intend to use to pay withholding taxes on the 218,550 shares of common stock to be issued to certain executive officers and management upon completion of this offering. |

| (2) | Reflects the exchange of the remaining Related-Party Notes (i.e., after the repayments listed in footnote (1) to this table are allocated between the notes as described under “2014 Recapitalization” elsewhere in this prospectus) for shares of our common stock calculated by dividing principal and accrued interest due under such notes by the initial public offering price per share, or in the case of certain FNPA Notes or FNPA II Notes, by dividing 117.0% of the principal and accrued interest due under such notes by the initial public offering price per share. |

| (3) | Reflects the exchange of certain Related-Party Warrants without receipt of cash consideration for a number of shares of our common stock equal to the aggregate value of such warrants divided by the initial public offering price per share, where the aggregate value of a warrant is calculated by multiplying (i) the number of shares issuable upon exercise of |

13

Table of Contents

| such warrant by (ii) the excess, if any, of the initial public offering price per share over, in most instances, the exercise price per share provided for in such warrant, provided that, in the case of certain outstanding warrants to purchase shares of common stock with an exercise price of $26.42 per share, an exercise price of $18.87 was used instead as provided for in the 2014 Recapitalization Agreement. |

| (4) | Reflects: (i) the issuance of the shares of common stock listed in footnote (2) to this table upon exchange for Related-Party Notes; (ii) the issuance of the shares of common stock listed in footnote (3) to this table upon exchange for Related-Party Warrants; (iii) the conversion of each share of our convertible preferred stock and our Class A, Class A-1, Class B, Class C and Class G common stock into one share of our common stock; (iv) the issuance of 218,550 shares of common stock approved by our board of directors to certain executive officers and management upon completion of this offering; (iv) the issuance of 39,582 shares of common stock upon the exercise of rights to purchase such shares; and (v) the issuance of that number of additional shares of our common stock required to raise, at a price per share equal to the initial public offering price per share, (a) the amount set forth in footnote (1) to this table for repayment of Related-Party Notes (other than the $100.0 million of cash collateral to be released to us in connection with the Letter of Credit Facility) and (b) the amount we have agreed to pay to certain of our aircraft lessors in settlement of accelerated lease obligations triggered by the repayment of Related-Party Notes as part of the 2014 Recapitalization. |

| (5) | Reflects the issuance of the shares of common stock in connection with the 2014 Recapitalization as listed in footnote (4) to this table and the issuance by us of additional shares of our common stock not already assumed to have been sold on a pro forma basis in clause (v) of footnote (4) above. |

In each case, the total number of shares of common stock outstanding after this offering above is based on 1,950,671 shares of our common stock outstanding (on an as converted to common basis) as of September 30, 2014, subject to the same exclusions described above.

Because the share amounts set forth above are based on the accrued interest outstanding pursuant to our Related-Party Notes as of September 30, 2014, such amounts do not take into account shares of common stock to be issued in the 2014 Recapitalization in exchange for unpaid interest on the Related-Party Notes accrued from September 30, 2014 through the closing date of this offering. Such interest contractually accrues at a rate of approximately $3.9 million per month in the aggregate.

For more information, see “2014 Recapitalization” elsewhere in this prospectus.

14

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL AND OPERATING DATA

The following tables summarize the consolidated financial and operating data for our business for the periods presented. You should read this summary consolidated financial and operating data in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes, included elsewhere in this prospectus.

We derived the summary consolidated statements of operations data for the years ended December 31, 2011, 2012 and 2013 from our audited consolidated financial statements included in this prospectus. We derived the summary consolidated statement of operations data for the nine months ended September 30, 2013 and 2014 and the consolidated balance sheet data as of September 30, 2014 from our unaudited consolidated financial statements included in this prospectus. The unaudited interim financial statements have been prepared on the same basis as the audited financial statements and include all adjustments, which consist of only normal recurring adjustments, necessary for the fair presentation of the financial information set forth in those statements. Our historical results are not necessarily indicative of the results to be expected in the future, and results for the nine months ended September 30, 2014 are not indicative of the results expected for the full year.

| Year Ended December 31, | Nine Months Ended September 30, | |||||||||||||||||||

| 2011 | 2012 | 2013 | 2013 | 2014 | ||||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||

Consolidated Statements of Operations Data: | ||||||||||||||||||||

Operating revenues | $ | 1,037,108 | $ | 1,332,837 | $ | 1,424,678 | $ | 1,064,750 | $ | 1,117,769 | ||||||||||

Operating expenses | 1,064,504 | 1,364,570 | 1,343,797 | 1,007,458 | 1,031,449 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operating income (loss) | (27,396 | ) | (31,733 | ) | 80,881 | 57,292 | 86,320 | |||||||||||||

Other expense | (72,993 | ) | (113,640 | ) | (70,420 | ) | (61,328 | ) | (29,055 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) before income tax | (100,389 | ) | (145,373 | ) | 10,461 | (4,036 | ) | 57,265 | ||||||||||||

Income tax expense | 14 | 15 | 317 | — | 1,028 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) | $ | (100,403 | ) | $ | (145,388 | ) | $ | 10,144 | $ | (4,036 | ) | $ | 56,237 | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) per share: | ||||||||||||||||||||

Basic (1) | $ | (143.09 | ) | $ | (207.20 | ) | $ | 5.60 | $ | (5.75 | ) | $ | 31.04 | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Diluted (1) | $ | (143.09 | ) | $ | (207.20 | ) | $ | 3.68 | $ | (5.75 | ) | $ | 18.13 | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Shares used in per share calculation: | ||||||||||||||||||||

Basic (1) | 701,671 | 701,671 | 701,671 | 701,671 | 701,671 | |||||||||||||||

Diluted (1) | 701,671 | 701,671 | 1,646,821 | 701,671 | 1,992,446 | |||||||||||||||

Pro forma net income per share(2) | ||||||||||||||||||||

(unaudited) | ||||||||||||||||||||

Basic | — | — | $ | 2.08 | — | $ | 2.34 | |||||||||||||

Diluted | — | — | 2.03 | — | 2.27 | |||||||||||||||

Pro forma shares used in per share calculation(2) | ||||||||||||||||||||

(unaudited) | ||||||||||||||||||||

Basic | — | — | 32,446,072 | — | 32,563,041 | |||||||||||||||

Diluted | — | — | 33,196,528 | — | 33,643,782 | |||||||||||||||

Non-GAAP Financial Data (unaudited): | ||||||||||||||||||||

EBITDA (3) | $ | (17,241 | ) | $ | (20,473 | ) | $ | 94,844 | $ | 67,059 | $ | 96,737 | ||||||||

EBITDAR (3) | 170,635 | 216,327 | 296,915 | 223,117 | 234,177 | |||||||||||||||

15

Table of Contents

| (1) | See Note 15 to our consolidated financial statements included elsewhere in this prospectus for an explanation of the method used to calculate the basic and diluted earnings per share. |

| (2) | The unaudited pro forma basic and diluted net income per share for the year ended December 31, 2013 and the nine months ended September 30, 2014 were computed to give effect to the issuance of our common stock, as well as the conversion of our convertible preferred stock, Class A common stock and non-Class A common stock into common stock as a result of the 2014 Recapitalization, including the application of certain proceeds from the offering that have been assumed to pay down a portion of related-party debt and additional required disbursement items. The computation is computed using the if converted method as though the conversion had occurred as of the beginning of the period or the original date of issuance, if later. See Note 15 to our consolidated financial statements included elsewhere in this prospectus for an explanation of the pro forma adjustments used to calculate basic and diluted earnings per share and shares used for computation of basic and diluted earnings per share. |

| (3) | EBITDA is earnings before interest, income taxes, and depreciation and amortization. EBITDAR is earnings before interest, income taxes, depreciation and amortization and aircraft rent. EBITDA and EBITDAR are included as supplemental disclosure because we believe they are useful indicators of our operating performance. Derivations of EBITDA and EBITDAR are well recognized performance measurements in the airline industry that are frequently used by companies, investors, securities analysts and other interested parties in comparing the operating performance of companies in our industry. We also believe EBITDA is useful for evaluating performance of our senior management team. EBITDAR is useful in evaluating our operating performance compared to our competitors because its calculation isolates the effects of financing in general, the accounting effects of capital spending and acquisitions (primarily aircraft, which may be acquired directly, directly subject to acquisition debt, by capital lease or by operating lease, each of which is presented differently for accounting purposes) and income taxes, which may vary significantly between periods and for different companies for reasons unrelated to overall operating performance. However, because derivations of EBITDA and EBITDAR are not determined in accordance with GAAP, such measures are susceptible to varying calculations, and not all companies calculate the measures in the same manner. As a result, derivations of EBITDA and EBITDAR as presented may not be directly comparable to similarly titled measures presented by other companies. |

These non-GAAP financial measures have limitations as an analytical tool. Some of these limitations are: they do not reflect our cash expenditures or future requirements for capital expenditures or contractual commitments; they do not reflect changes in, or cash requirements for, our working capital needs; they do not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt; although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and these measures do not reflect any cash requirements for such replacements; and other companies in our industry may calculate EBITDA and EBITDAR differently than we do, limiting their usefulness as a comparative measure. Because of these limitations, EBITDA and EBITDAR should not be considered in isolation or as a substitute for performance measures calculated in accordance with GAAP.

The following table represents the reconciliation of net income (loss) to EBITDA and EBITDAR for the periods presented below:

| Year Ended December 31, | Nine Months Ended September 30, | |||||||||||||||||||

| 2011 | 2012 | 2013 | 2013 | 2014 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||

Reconciliation: | ||||||||||||||||||||

Net income (loss) | $ | (100,403 | ) | $ | (145,388 | ) | $ | 10,144 | $ | (4,036 | ) | $ | 56,237 | |||||||

Interest expense | 75,577 | 116,110 | 71,293 | 61,575 | 31,225 | |||||||||||||||

Capitalized interest | (2,320 | ) | (2,176 | ) | (534 | ) | — | (1,840 | ) | |||||||||||

Interest income | (264 | ) | (294 | ) | (339 | ) | (247 | ) | (330 | ) | ||||||||||

Income tax expense | 14 | 15 | 317 | — | 1,028 | |||||||||||||||

Depreciation and amortization | 10,155 | 11,260 | 13,963 | 9,767 | 10,417 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

EBITDA | (17,241 | ) | (20,473 | ) | 94,844 | 67,059 | 96,737 | |||||||||||||

Aircraft rent | 187,876 | 236,800 | 202,071 | 156,058 | 137,440 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

EBITDAR | $ | 170,635 | $ | 216,327 | $ | 296,915 | $ | 223,117 | $ | 234,177 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

16

Table of Contents

The following table presents our historical consolidated balance sheet data as of September 30, 2014, on a pro forma basis to give effect to the 2014 Recapitalization, including the application of proceeds from this offering to repay Related-Party Notes and the associated conversion of certain of the remaining Related-Party Notes into common stock, and on a pro forma as adjusted basis to give effect to the receipt by us of the estimated net proceeds from the sale by us of 13,106,377 shares at an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus) after deducting underwriting discounts and estimated expenses payable by us and the application of such net proceeds as described in “Use of Proceeds” elsewhere in this prospectus.

| As of September 30, 2014 | ||||||||

| Pro Forma (1) | Pro Forma as Adjusted (2) | |||||||

Consolidated Balance Sheet Data: | ||||||||

Cash and cash equivalents | $ | 184,454 | $ | 398,978 | ||||

Total assets | 778,229 | 989,351 | ||||||

Long-term debt, including current portion | 117,926 | 117,926 | ||||||

Convertible preferred stock | — | — | ||||||

Total stockholders’ equity (deficit) | 242,552 | 455,227 | ||||||

| (1) | The unaudited pro forma consolidated balance sheet has been adjusted to illustrate the effect of: (a) the repayment of $100.0 million of principal and accrued interest due under the Related-Party Notes in connection with the release of $100.0 million of cash collateral held by our credit card processors in exchange for the establishment of the Letter of Credit Facility arranged by the Virgin Group; (b) the issuance of the $50.0 million Post-IPO Note in exchange for cancellation of $50.0 million of certain Related-Party Notes held by the Virgin Group; (c) the repayment of $51.5 million of principal and accrued interest due under certain Related-Party Notes using $51.5 million of the assumed net proceeds from the sale of shares by us in this offering assuming an initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus) (d) the exchange of approximately $477.3 million of principal and accrued interest due under the Related-Party Notes for 22,607,785 shares of our common stock, assuming an initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus); (e) the issuance of 5,290,879 shares of common stock in exchange for Related-Party Warrants to purchase 26,067,475 shares of our common stock, assuming an initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus); (f) the conversion of each share of our convertible preferred stock and our Class A, Class A-1, Class B, Class C and Class G common stock into one share of our common stock; (g) the issuance of 218,550 shares of common stock approved by our board of directors to certain executive officers and management upon completion of this offering; (h) payments of approximately $1.8 million, assuming an initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus), to certain of our aircraft lessors in settlement of accelerated lease obligations triggered by the repayment of Related-Party Notes as part of the 2014 Recapitalization using net proceeds from the sale of shares by us in this offering; and (i) the presentation of the excess of the recorded amount of debt and preferred stock above the cash and other consideration to be received of $45.9 million as additional paid in capital. |

| (2) | The unaudited pro forma as adjusted consolidated balance sheet has been further adjusted to illustrate the receipt by us of net proceeds of $214.5 million, assuming an initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus), as an increase in cash and cash equivalents. This amount includes the $1.8 million reimbursement to us for offering expenses paid by us prior to September 30, 2014, resulting in a net change to total stockholders’ equity of $212.7 million. Further, both additional paid in capital and accumulated deficit have been increased as a result of the sale of 231,210 shares by VX Employee Holdings, LLC and the related compensation expense in connection with the distribution to employees of the proceeds from the sale of these shares, which we estimate to be approximately $4.9 million, based on an assumed initial public offering price of $22.50 per share (the midpoint of the price range set forth on the cover of this prospectus). |

17

Table of Contents

The number of shares outstanding after the offering will depend primarily on the price per share at which our common stock is sold in this offering and the total size of this offering. In connection with this offering and pursuant to the 2014 Recapitalization:

| • | principal and accrued interest outstanding pursuant to our Related-Party Notes would be either (i) repaid with a portion of the net proceeds from this offering and amounts equal to the release of credit card holdbacks in connection with the establishment of the Letter of Credit Facility, (ii) exchanged for the Post-IPO Note or (iii) exchanged for shares of our common stock based on the initial public offering price of this offering; |

| • | outstanding warrants to purchase shares of our common stock, including our Related-Party Warrants, either (i) would be exchanged without receipt of cash consideration for shares of our common stock in amounts agreed to in the 2014 Recapitalization Agreement, which depend in part on the initial public offering price of this offering or (ii) would expire or otherwise be cancelled; and |