Table of Contents

As confidentially submitted to the Securities and Exchange Commission on August 8, 2014. This draft registration statement has not been publicly filed with the Securities and Exchange Commission and all information contained herein remains strictly confidential.

RegistrationNo. -

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form F 1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Intercorp Financial Services Inc.

(Exact name of Registrant as specified in its charter)

| Republic of Panama | 6029 | Not applicable | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

Intercorp Financial Services Inc.

Torre Interbank, Av. Carlos Villarán 140

La Victoria

Lima 13, Peru

(51) (1) 615-9011

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Corporation Service Company

1180 Avenue of the Americas, Suite 210

New York, NY 10036

(212)299-5600

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

Antonia E. Stolper, Esq. Shearman & Sterling LLP 599 Lexington Avenue New York, New York 10022 (212)848-5009 | Juan Francisco Méndez, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017 (212)455-2579 |

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is apost-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is apost-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of this prospectus is expected to be made pursuant to Rule 434, check the following box. ¨

CALCULATION OF REGISTRATION FEE

| ||||

Title of each class of securities to be registered | Proposed maximum aggregate | Amount of registration fee | ||

Common shares(1) | US$ | US$ | ||

| ||||

| ||||

| (1) | Includes common shares that the underwriters have the option to purchase, if any, and common shares that are to be offered outside the United States but that may be resold from time to time in the United States in transactions requiring registration under the Securities Act. Offers and sales of common shares outside the United States are being made pursuant to Regulation S and are not covered by the Registration Statement. |

| (2) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted

SUBJECT TO COMPLETION, DATED , 2014

Preliminary Prospectus

Shares

Common Stock

This is a public offering of shares of Intercorp Financial Services, Inc. (“IFS”) by the selling shareholders identified in this prospectus. We will not receive any of the proceeds from the sale of the common shares by the selling shareholders.

Our common shares are listed on the Lima Stock Exchange (Bolsa de Valores de Lima) under the symbol “IFS”. On August 7, 2014, the last reported sales price of IFS common shares on the Lima Stock Exchange was US$ 32.31 per share. We will apply to have the common shares listed on the New York Stock Exchange under the symbol “IFSP”.

The selling shareholders have granted the underwriters an option for a period of 30 days to purchase from them up to an aggregate of additional common shares.

Investing in the common shares involves risks. See “Risks Factors” beginning on page 22.

| Price to Public | Underwriting Discount and Commissions | Proceeds to the Selling Shareholders | ||||||||||

Per Share | US$ | US$ | US$ | |||||||||

Total | US$ | US$ | US$ | |||||||||

Delivery of the common shares will be made on or about , 2014.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This offering has not and will not be registered in the Republic of Peru (“Peru”) and therefore is not and will not be subject to Peruvian laws applicable to public offerings in Peru. Neither this offering nor the common shares have been or will be registered in the Republic of Panama and therefore are not and will not be subject to the Panamanian laws applicable to public offerings in Panama. The information contained in this prospectus has not been and will not be approved or disapproved by the Peruvian Securities Commission (Superintendencia del Mercado de Valores, or “SMV”), the Lima Stock Exchange, or the Panamanian Superintendency of the Securities Market (Superintendencia del Mercado de Valores, or “Panamanian SMV”). The common shares may not be sold in Peru or Panama except in compliance with the securities laws of Peru and Panama, respectively.

Global Coordinators and Bookrunners

| BofA Merrill Lynch | Credit Suisse | |

The date of this prospectus is , 2014.

Table of Contents

We are responsible for the information contained in this prospectus. We have not authorized anyone to give you any other information and we take no responsibility for any other information that others may give you.

| Page | ||||

| ii | ||||

| 1 | ||||

| 16 | ||||

| 20 | ||||

| 22 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 45 | ||||

| 46 | ||||

Unaudited Pro Forma Condensed Combined Financial Information | 49 | |||

Management’s Discussion and Analysis of Results of Operations and Financial Condition | 53 | |||

| 88 | ||||

| Page | ||||

| 101 | ||||

| 120 | ||||

| 150 | ||||

| 165 | ||||

| 182 | ||||

| 194 | ||||

| 195 | ||||

| 201 | ||||

| 204 | ||||

| 207 | ||||

| 209 | ||||

| 217 | ||||

| 226 | ||||

| 227 | ||||

| 228 | ||||

| 229 | ||||

| 230 | ||||

| F-1 | ||||

Through and including , 2014 (the 25th day after the date of this prospectus), U.S. federal securities law requires all dealers that effect transactions in our common shares, whether or not participating in this offering, to deliver a prospectus. This requirement is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscription.

This prospectus has been prepared on the basis that all offers of common shares in any Member State of the European Economic Area which has implemented the Prospectus Directive (each, a “Relevant Member State”) will be made pursuant to an exemption under the Prospectus Directive from the requirement to produce a prospectus for offers of common shares. Accordingly, any person making or intending to make any offer of common shares within the European Economic Area that are the subject of the offering contemplated in this prospectus should only do so in circumstances in which no obligation arises for us or the underwriters to produce a prospectus for such offer. Neither we nor the underwriters have authorized, or hereby authorize, the making of any offer of common shares in circumstances in which an obligation arises for us or the underwriters to publish a prospectus for such offer. “Prospectus Directive” means Directive 2003/71/EC (and amendments thereto, including the 2010 PD Amending Directive, to the extent implemented in the Relevant Member State), and includes any relevant implementing measure in the Relevant Member State; and the expression “2010 PD Amending Directive” means Directive 2010/73/EU.

The distribution of this prospectus and the offering and sale of common shares in certain jurisdictions may be restricted by law. Persons who receive this prospectus must inform themselves about and observe any such restrictions. This prospectus does not constitute an offer of, or an invitation to purchase, any of the common shares in any jurisdiction in which such offer or invitation would be unlawful.

i

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Certain Definitions

All references to “we”, “us”, “our company” and “IFS” in this prospectus are to Intercorp Financial Services Inc., a corporation (sociedad anónima) organized under the laws of the Republic of Panama (“Panama”).

In this prospectus, we refer to our principal subsidiaries as follows: (i) in our banking segment: Banco Internacional del Perú, S.A.A. – Interbank, an open-stock corporation (sociedad anónima abierta) organized under the laws of Peru, as “Interbank”; (ii) in our insurance segment: Interseguro Compañía de Seguros, S.A., a corporation (sociedad anónima) organized under the laws of Peru, as “Interseguro”; and (iii) in our wealth management segment: Inteligo Group Corp., a corporation (sociedad anónima) organized under the laws of Panama, as “Inteligo”, Inteligo Bank Ltd., a corporation organized under the laws of The Bahamas, as “Inteligo Bank” and Inteligo SAB S.A., a corporation (sociedad anónima) organized under the laws of Peru, as “Inteligo SAB”.

In this prospectus, we also refer to our parent company, Intercorp Perú Ltd (“Intercorp Peru”), a holding company for a group of companies operating mainly in Peru under the name “Intercorp”. Intercorp Peru’s main subsidiaries include our company and Intercorp Retail Inc. (“Intercorp Retail”). Intercorp Retail acts as a holding company for the retail and real estate operations of Intercorp Peru in Peru. Through its subsidiary InRetail Peru Corp., whose shares are listed on the Lima Stock Exchange under the symbol “INRETAILC1”, Intercorp Retail has a controlling stake in (i) Supermercados Peruanos S.A. (“Supermercados Peruanos”), a supermarket chain, primarily operating under the Plaza Vea brand (“Plaza Vea”), (ii) Eckerd Peru S.A., a pharmacy chain operating under the Inkafarma brand (“Inkafarma”) controlled by Intercorp Peru since 2011, and (iii) InRetail Real Estate Corp., an owner, developer and operator of shopping malls. Intercorp Retail also controls directly (i) Tiendas Peruanas S.A. (“Tiendas Peruanas”), a department store chain operating under the Oechsle brand (“Oechsle”) that started operations in 2009, (ii) Financiera Uno S.A. (“Financiera Uno”), a consumer finance company that started operations in 2010, and (iii) Homecenters Peruanos S.A., a home improvement company operating under the Promart brand that started operations in 2010.

Financial Statements

Our audited combined financial statements as of and for the years ended December 31, 2013 and 2012 and as of January 1, 2012 included in this prospectus have been prepared innuevos soles and in accordance with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and audited by Medina, Zaldívar, Paredes & Asociados, a member firm of Ernst & Young Global, in accordance with the standards of the Public Company Accounting Oversight Board (“PCAOB”). The opening statement of financial position was prepared as of January 1, 2012, the date of transition to IFRS for the IFS financial statements, as required by IFRS 1—“First Time Adoption of International Financial Reporting Standards”.

We have historically prepared our financial statements in accordance with accounting principles prescribed by the Peruvian Superintendency of Banks, Insurance and Private Pension Fund Administrators (Superintendencia de Banca, Seguros y AFPs, or “SBS”), hereinafter “Peruvian SBS GAAP”. This is the first time we prepare our financial statements in accordance with IFRS as issued by the IASB. For more information about our transition to IFRS, see notes 3.1, 3.5 and 13.4 to our audited combined financial statements included in this prospectus.

For regulatory purposes, includingBanco Central de Reserva del Perú (the “Central Reserve Bank of Peru”) regulations and the reporting requirements of the SMV, we and our Peruvian subsidiaries prepare and will continue to prepare and make available to shareholders statutory financial statements as prescribed by the SBS and the SMV, which currently is and in the near future is expected to be prepared in accordance with Peruvian SBS GAAP.

ii

Table of Contents

Intercorp Peru approved a shareholders structure reorganization on July 18, 2014, with effective date August 1, 2014, through which we became the direct owner of 100% of the capital stock of Inteligo. As a result, Inteligo became our subsidiary. Given that the reorganization will not lead to a change in Intercorp Peru’s control of the subsidiaries under IFS, the reorganization is considered a transaction among entities under common control. As a result, the reorganization is accounted for using the pooling-of-interest method. Through the effective date of the reorganization, the financial statements are presented as audited combined financial statements.

Inteligo Bank, which contributes over 99% of Inteligo’s net profit for the year ended December 31, 2013, had previously adopted IFRS as issued by the IASB, and therefore Inteligo prepared its financial statements for all years presented in this prospectus in accordance with IFRS as issued by the IASB. Inteligo SAB, however, has more recently adopted IFRS, and has prepared its individual financial statements in accordance with IFRS since January 1, 2012.

We have included in this prospectus certain information reported by the SBS and the SMV for the Peruvian banking and insurance sector as a whole as well as for individual financial institutions in Peru, including Interbank and Interseguro, which report to the SBS and the SMV in Peruvian SBS GAAP. All statements in this prospectus regarding our relative market position and financial performancevis-a-vis the financial services and insurance sectors in Peru, are based, out of necessity, on information obtained from SBS and SMV statistics. Statements in this prospectus regarding our relative market position and financial performance however, do not include information relating to Inteligo as Inteligo is not regulated by and does not report to the SBS or the SMV. In addition, for certain financial information related to our compound annual growth rate (“CAGR”) we have included such information pursuant to Peruvian SBS GAAP in order to be able to show prospective investors our growth over a longer period than two years. IFRS differs in certain respects from Peruvian SBS GAAP. Consequently, information presented in this prospectus in accordance with Peruvian SBS GAAP or based on information from the SBS or SMV may not be comparable with our financial information prepared in accordance with IFRS. Unless otherwise indicated, all financial information provided in this prospectus has been prepared in accordance with IFRS.

We manage our business in three segments: Banking, Insurance and Wealth Management. For information on our results of operations per our business segments, see note 27 to our audited combined financial statements included in this prospectus.

Currency Translation

We have translated some of thenuevos soles amounts contained in this prospectus into U.S. dollars for convenience purposes only. Unless otherwise indicated or the context otherwise requires, the rate used to translatenuevos soles amounts to U.S. dollars was S/. 2.795 to US$1.00, which was the exchange rate reported for December 31, 2013 by the SBS. The Federal Reserve Bank of New York does not report a noon buying rate fornuevos soles. The U.S. dollar equivalent information presented in this prospectus is provided solely for convenience of investors and should not be construed as implying that thenuevos soles or other currency amounts represent, or could have been or could be converted into, U.S. dollars at such rates or at any other rate. See “Exchange Rates” for information regarding historical exchange rates ofnuevos soles to U.S. dollars.

Effect of Rounding

Certain figures included in this prospectus and in our audited combined financial statements have been rounded for ease of presentation. Percentage figures included in this prospectus have not in all cases been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this prospectus may vary from those obtained by performing the same calculations using the figures in our audited combined financial statements. Certain other amounts that appear in this prospectus may not sum due to rounding.

iii

Table of Contents

Market and Industry Data

Unless otherwise indicated, statistical information relating to our Peruvian subsidiaries, Interbank and Interseguro, regarding market share, ranking, and other measures, as well as information on other Peruvian financial institutions and the Peruvian financial system generally, has been derived from reports and information published by the SBS, the SMV, the Central Reserve Bank of Peru, theFederación Latinoamericana de Bancos(Federation of Latin American Banks, or “FELABAN”), theAsociación de Bancos del Perú(Association of Peruvian Banks, or “ASBANC”), Swiss Re Sigma’s report, “World Insurance in 2013: Steering Towards Recovery” (“Swiss Re Sigma 2013 Report”), or from other publicly available sources and industry publications. Industry publications generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Similarly, any internal surveys, estimates and market research used in this prospectus, while believed to be reliable, have not been independently verified, and we do not make any representation as to the accuracy of such information.

In this prospectus, unless otherwise indicated, all macroeconomic data relating to Peru is based on information published by the SBS, the Central Reserve Bank of Peru, the PeruvianMinisterio de Economía y Finanzas (Ministry of the Economy and Finance), and the PeruvianInstituto Nacional de Estadística e Informática(National Institute of Statistics and Information Processing, or “INEI”).

References in this prospectus to GDP refer to real gross domestic product, except for GDP per capita and penetration ratios of loan products.

References in this prospectus to the group of peer countries in Latin America refer to Brazil, Chile, Colombia and Mexico.

References in this prospectus to the four largest banks in Peru or the four largest Peruvian banks refer to Banco de Crédito del Peru, BBVA, Interbank and Scotiabank.

Socioeconomic levels are determined based on the data collected by INEI in their national annual surveyEncuesta Nacional de Hogares(ENAHO). INEI assigns a score to each household based on their ranking on the following four factors: (i) characteristics of the household living space, (ii) level of living space overcrowding, (iii) level of education of household head and (iv) ownership of durable goods/properties; and then groups them in five socioeconomic classes (A, B, C, D, E).

Loan Portfolio Data

Unless otherwise indicated, references in this prospectus to performing loans refer to loans in compliance with their original contractual obligations. References to past-due loans refer to overdue loans defined as follows. Commercial loans are considered past-due once amortization payments are 15 days overdue. Loans tomicro-businesses are considered past-due once amortization payments are 30 days overdue. In the case of consumer, mortgage and leasing loans, the amortization portion of a coupon is considered past-due once 30 days overdue and the total amount of the loan is considered past-due once an amortization payment is 90 days overdue. Past-due loans do not include refinanced and restructured loans. References to total gross loans include total loans outstanding, including past-due loans and refinanced loans, and references to total loans, net are to gross loansplus accrued interestless allowances for loan losses and deferred interest.

Certain Financial Definitions and Conventions

We present return on assets, or ROA, and return on equity, or ROE, in this prospectus. We define our ROA as net profit for the year divided by average total assets and our ROE as net profit for the year divided by average shareholders’ equity. We present average balances and nominal average interest rates in this prospectus. Except as otherwise indicated, average balances are based on quarterly balances. Nominal average interest rates have been calculated by dividing interest earned on assets or paid on liabilities by the corresponding average balances on such assets or liabilities.

iv

Table of Contents

This summary highlights selected information described in greater detail elsewhere in this prospectus. You should carefully read this prospectus in its entirety before investing in our common shares, including “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited combined financial statements and related notes. Unless otherwise indicated, all financial information provided in this section has been prepared in accordance with IFRS.

Overview

IFS is a leading provider of financial services in the fast-growing, underpenetrated and profitable Peruvian financial system. Through one of the largest distribution networks in Peru (as measured by the number of financial stores, ATMs, correspondent agents and sales force), IFS provides a wide range of products spanning banking, insurance and wealth management services to individual and commercial clients.

Our main subsidiaries are Interbank, a universal bank, Interseguro, an insurance company, and Inteligo, a wealth management services provider. We operate our subsidiaries through a coordinated strategy, focusing on specific businesses which we believe offer high growth opportunities. We are the second largest provider of consumer loans (retail loans other than mortgages) in Peru in terms of total loans outstanding, the leading provider of annuities in terms of premiums, and operate a fast-growing wealth management business.

Inteligo was acquired by IFS effective on August 1, 2014. We believe that Inteligo strengthens our position as a leading provider of diversified financial services in Peru, since it complements our banking and insurance segments with a rapidly growing and highly profitable wealth management business. Inteligo benefits from a recurring source of fee income from financial advisory services catering to the increasing number of high net worth individuals in Peru.

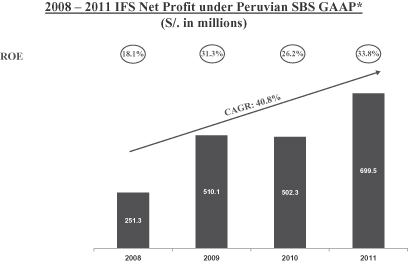

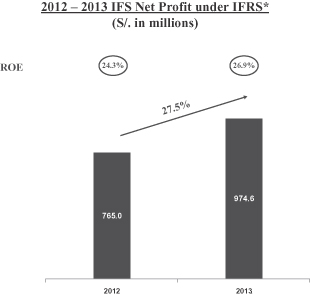

Since our initial public offering in Peru in 2007, we have generated high levels of growth and profitability. Through December 31, 2011, under Peruvian SBS GAAP and prior to the acquisition of Inteligo, our net profit grew at a three-year CAGR of 40.8% for the period ended December 31, 2011, with an average ROA and average ROE of 2.6% and 27.3%, respectively. For the two years ended December 31, 2013, our average ROA and average ROE was 2.8% and 25.5%, respectively, and for 2013 our net profit grew 27.5%, in each case under IFRS and including the effect of the recent acquisition of Inteligo for these periods.

1

Table of Contents

The following charts show the evolution of our net profit and ROE from 2008 through 2011 in accordance with Peruvian SBS GAAP, and for 2012 and 2013 in accordance with IFRS.

| * | Excludes Inteligo. |

| * | Includes Inteligo. |

As of December 31, 2013, we had total assets of S/. 36.2 billion (approximately US$12.9 billion), total gross loans of S/. 20.9 billion (approximately US$7.5 billion), total deposits of S/. 22.1 billion (approximately US$7.9 billion) and shareholders’ equity of S/. 3.7 billion (approximately US$1.3 billion). For the year ended December 31, 2013, our net profit was S/. 974.6 million (approximately US$348.7 million).

2

Table of Contents

We operate the following three business segments:

| • | Banking: Interbank is the second largest provider of consumer loans (retail loans other than mortgages) in Peru in terms of total loans outstanding as of December 31, 2013, according to the SBS. Within the consumer loan segment in Peru, Interbank is the second largest provider of credit card financing and the largest private bank provider of payroll loans to public sector employees. Additionally, it is the fourth largest bank in Peru in terms of retail mortgages and commercial lending, as well as overall deposits and total assets. Interbank has built one of the most convenient and extensive retail banking distribution networks in Peru with a total of 268 financial stores, more than 2,400 ATMs and more than 3,200 correspondent agents. |

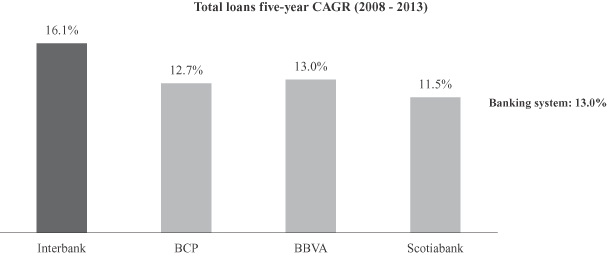

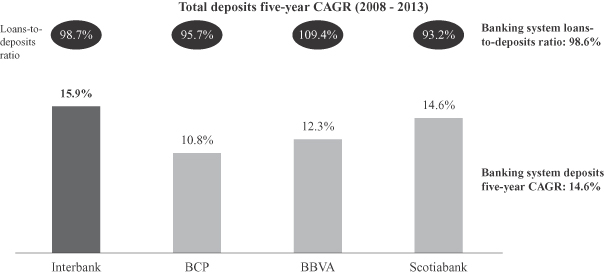

Interbank’s five-year CAGR in loans, deposits and net profit was 16.1%, 15.9%, and 19.1%, respectively, under Peruvian SBS GAAP, for the period ended December 31, 2013. For the year ended December 31, 2013, Interbank’s year-over-year growth in loans, deposits and net profit was 26.6%, 38.7%, and 8.2%, respectively, and its ROE was 23.7%, under IFRS.

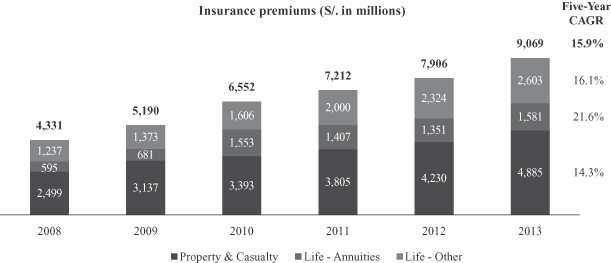

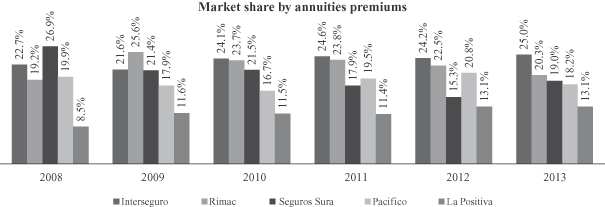

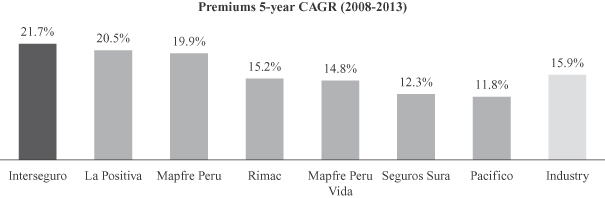

| • | Insurance: Interseguro is the leading provider of annuities in Peru, the fastest-growing insurance product in the Peruvian insurance industry over the last five years, with a 25.0% market share as measured by premiums for the year ended December 31, 2013, according to the SBS. In addition to its leading position in annuities, Interseguro also offers individual life and retail insurance products. |

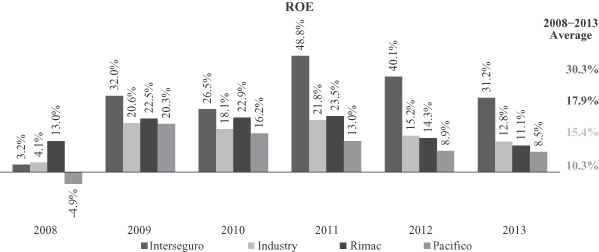

Interseguro’s five-year CAGR in premiums and net profit was 21.7% and 87.6%, respectively, under Peruvian SBS GAAP, for the period ended December 31, 2013. For the year ended December 31, 2013, Interseguro’s year-over-year growth in premiums and net profit was 26.3% and 87.7%, respectively, and its ROE was 48.2%, under IFRS.

| • | Wealth management: Inteligo is a fast-growing provider of wealth management services through Inteligo Bank and brokerage services through Inteligo SAB. Inteligo caters mainly to Peruvian high net worth individuals, particularly clients with investable assets between US$0.5 million and US$10 million who benefit from Peru’s rapid wealth creation. |

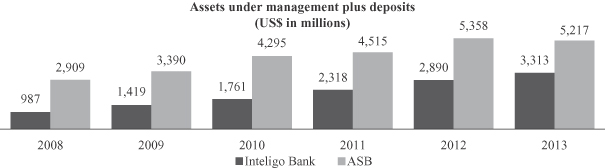

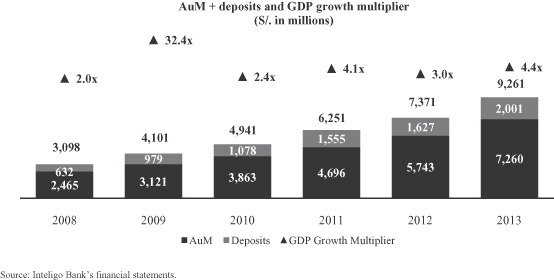

Inteligo Bank’s five-year CAGR in assets under management plus deposits was 24.5%, under IFRS, for the period ended December 31, 2013. For the year ended December 31, 2013, Inteligo Bank’s year-over-year growth in assets under management plus deposits was 25.6%, and Inteligo’s ROE was 26.5%, under IFRS.

The following table provides certain financial information about our three business segments.

| As of and for the year ended December 31, 2013 | ||||||||||||||||||||||||

| Total Assets | Total Equity | Net Profit | ||||||||||||||||||||||

| S/. in millions | % | S/. in millions | % | S/. in millions | % | |||||||||||||||||||

Banking | 29,873.0 | 82.6 | 2,804.9 | 75.6 | 615.0 | 63.1 | ||||||||||||||||||

Insurance | 3,870.1 | 10.7 | 541.1 | 14.6 | 281.6 | 28.9 | ||||||||||||||||||

Wealth management | 2,718.7 | 7.5 | 453.7 | 12.2 | 109.3 | 11.2 | ||||||||||||||||||

Corporate and eliminations(1) | (282.6 | ) | (0.8 | ) | (87.3 | ) | (2.4 | ) | (31.3 | ) | (3.2 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total | 36,179.2 | 100.0 | 3,712.4 | 100.0 | 974.6 | 100.0 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| (1) | Corporate and eliminations corresponds to expenses of IFS and elimination of intercompany transactions. See note 27 to our audited combined financial statements. |

3

Table of Contents

The following table provides certain financial information about our combined business.

| As of and for the years ended December 31, | ||||||||||||

| 2013 | 2013 | 2012 | ||||||||||

| (US$ in millions)(1)(2) | (S/. in millions)(1) | |||||||||||

Total assets | 12,944.2 | 36,179.2 | 29,473.5 | |||||||||

Total gross loans | 7,494.5 | 20,947.2 | 16,535.9 | |||||||||

Total deposits | 7,895.3 | 22,067.5 | 16,138.6 | |||||||||

Total equity | 1,328.2 | 3,712.4 | 3,619.3 | |||||||||

Net profit | 348.7 | 974.6 | 765.0 | |||||||||

Dividends declared(3) | — | 432.8 | 452.2 | |||||||||

Assets under management plus deposits(4) | 3,313.4 | 9,260.9 | 7,370.7 | |||||||||

Net interest margin | — | 5.9 | % | 6.3 | % | |||||||

ROA | — | 2.9 | % | 2.8 | % | |||||||

ROE | — | 26.9 | % | 24.3 | % | |||||||

Past-due-loan ratio | — | 1.7 | % | 1.8 | % | |||||||

Efficiency ratio(5) | — | 41.5 | % | 43.5 | % | |||||||

Financial stores | — | 268 | 261 | |||||||||

ATMs | — | 2,433 | 2,403 | |||||||||

Correspondent agents | — | 3,214 | 2,535 | |||||||||

| (1) | Except for percentages and ratios and number of financial stores, ATMs and correspondent agents. |

| (2) | Amounts stated in U.S. dollars as of and for the year ended December 31, 2013 have been translated fromnuevos soles at the exchange rate of S/. 2.795 = US $1.00. See “Exchange Rates”. |

| (3) | Dividends are declared and paid in U.S. dollars and were US$165.8 million and US$168.4 million for 2013 and 2012, respectively. |

| (4) | Refers to assets under management plus deposits of Inteligo Bank. |

| (5) | Efficiency ratio is calculated by dividing (x) salaries and employee benefits plus administrative expenses plus depreciation and amortization by (y) net interest and similar income plus other income plus net premiums earned. |

Market Opportunity

We believe that the current ongoing growth of the Peruvian economy, the increasing size of the middle class, the low penetration rates of financial services, the rapid growth of private wealth creation and the healthy, well-capitalized and profitable financial system offer significant opportunities for our continued profitable growth. These market opportunities are further described below.

High growth economy with strong macroeconomic fundamentals

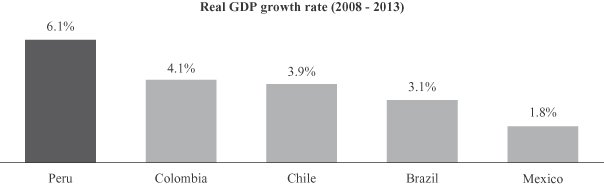

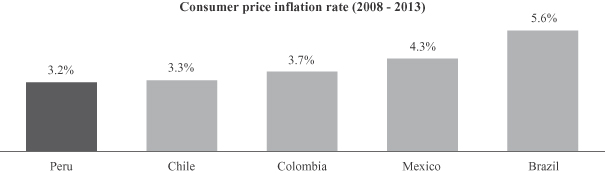

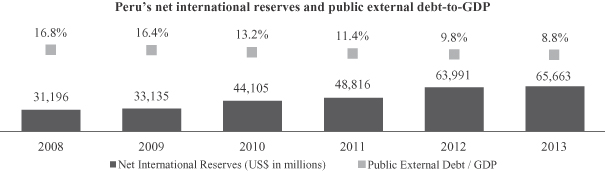

Peru’s average GDP growth rate was 6.1% between 2008 and 2013, while its average inflation rate was 3.2% during the same period. The Peruvian government’s conservative fiscal policy, coupled with the Central Reserve Bank of Peru’s responsible management of inflation and international reserves, has helped Peru to improve and maintain investment grade ratings of A3 by Moody’s Investor Service (“Moody’s”), BBB+ by Standard & Poor’s Rating Services (“S&P”) and BBB+ by Fitch Ratings Ltd. (“Fitch”). In its most recent forecast as of July 2014, the Central Reserve Bank of Peru has estimated real GDP growth for Peru of 4.4%, 6.0% and 6.3% in 2014, 2015 and 2016, respectively.

Expansion of purchasing power of middle and upper socioeconomic classes

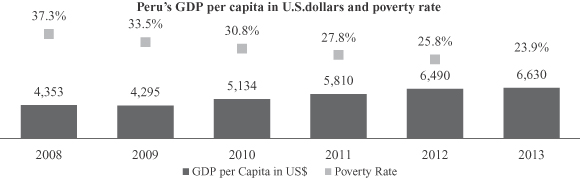

According to INEI, the poverty rate in Peru has declined to 23.9% in 2013, from 37.3% in 2008, and GDP per capita in U.S. dollars has grown 1.6x during the same period. According to INEI, Peru’s middle and upper

4

Table of Contents

socio-economic segments (segments A, B and C) have significantly expanded and, as of 2012, represented 45% of the population compared to 28% in 2004. The increase in the number of people belonging to the middle and upper classes creates the need for financial services, particularly for increasingly sophisticated banking, insurance and wealth management products.

Low financial services penetration

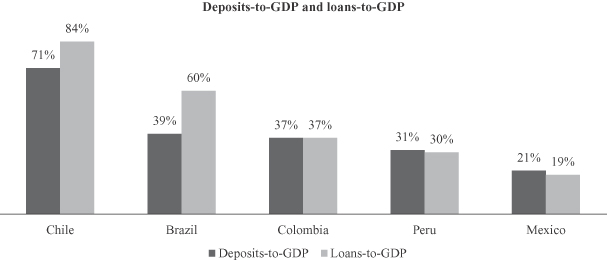

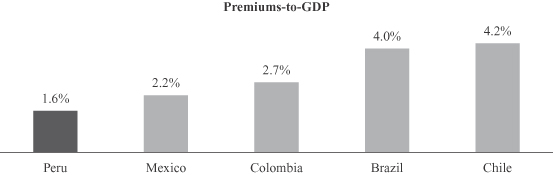

Despite the recent growth, we believe that growth potential in Peru’s financial services sector continues to be significant. Banking penetration in Peru as of December 31, 2013, measured as the ratio of loans-to-GDP was 30.4%, below the average ratio of 49.9% for the group of peer countries in Latin America and less than half than the ratio of 84.1% for Chile, according to the IMF and local regulators. We believe that penetration potential is even more significant in retail banking. In terms of retail loan penetration, including credit cards and branches per inhabitant, Peru is well below its peer countries in Latin America. As of December 31, 2013, the estimated total number of credit cards per inhabitant in Peru was only 0.26 as compared to 1.25 cards per inhabitant for Chile. The ratio of consumer loans-to-GDP and the ratio of mortgage loans-to-GDP in Peru were only 5.4% and 5.3%, respectively, while the averages for the group of peer countries in Latin America were 8.6% and 8.8%, respectively, as of December 31, 2013. Furthermore, as of December 31, 2013, there were only approximately 186,400 mortgages outstanding in Peru for a population of 30.5 million, compared to approximately 1.3 million mortgages outstanding in Chile for a population of 17.2 million. Similarly, insurance penetration in Peru, measured as the ratio of premiums-to-GDP as of December 31, 2013, is estimated to be 1.6%, which is lower than the average ratio of 3.3% for the group of peer countries in Latin America, and less than half the ratio of 4.2% for Chile, according to the Swiss Re Sigma 2013 Report.

Growth of private wealth in Peru

We believe the continuing growth in private wealth in Peru will further increase the market for wealth management services for Peruvian clients. According to INEI, the number of households in Peru with annual disposable income in excess of US$75,000, increased from 1.2% of the total population in 2008 to 2.1% in 2013. We expect the number of high net worth individuals in Peru and the size of their investible assets to continue to grow.

Healthy, well-capitalized and profitable financial system

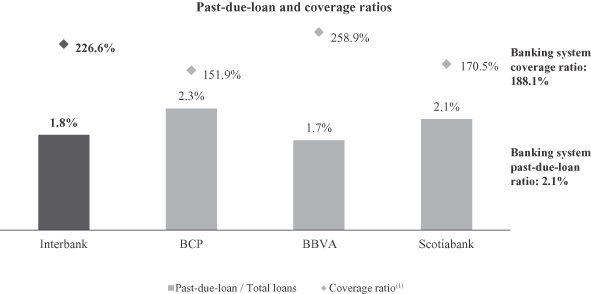

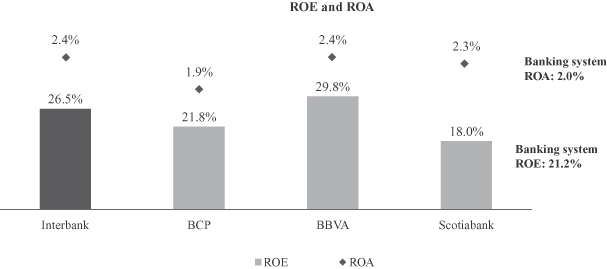

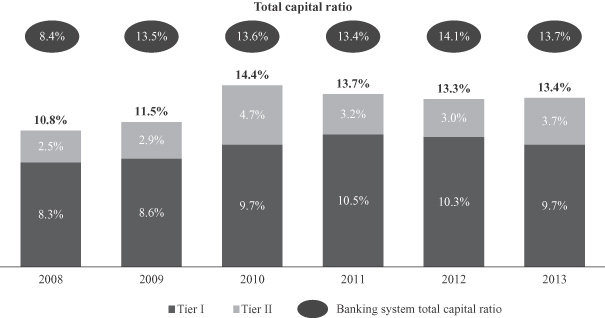

As a result of sound regulation, the Peruvian financial system is healthy, well-capitalized and profitable. Gross loans have grown at a five-year CAGR of 13.0% for the period ended December 31, 2013, while the banking system’s asset quality has remained strong with a ratio of past-due loans as a percentage of total gross loans of 2.1% and a ratio of allowance for loan losses as a percentage of past-due loans of 188.1% as of December 31, 2013, according to the SBS. Capitalization has consistently been well above regulatory requirements with a total capital ratio of the banking system of 13.7% as of December 31, 2013, according to the SBS. Insurance companies in Peru are also well-capitalized with an industry regulatory solvency ratio of 28.4% as of December 31, 2013. Furthermore, profitability remains high, with a 21.2% ROE for the banking system, and a 12.8% ROE for the insurance industry for the year ended December 31, 2013, according to the SBS.

Strengths

Leading financial services provider focused on highly attractive businesses

We are focused on some of the fastest growing and most profitable businesses in the Peruvian financial system. Within our banking segment, Interbank focuses on retail banking, with 49.1% of its loan portfolio constituting retail loans, compared to 34.3% for the Peruvian banking system, as of December 31, 2013,

5

Table of Contents

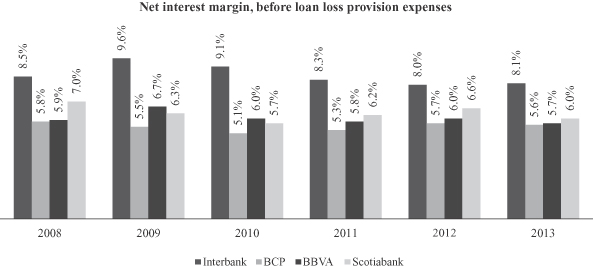

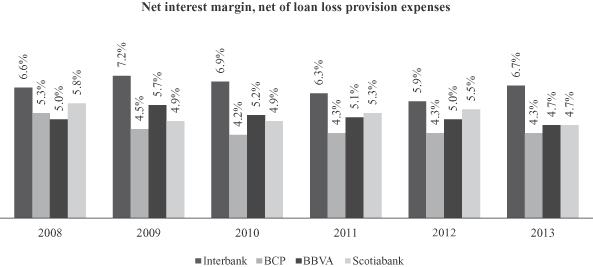

according to the SBS. Interbank is the second largest provider of consumer loans (other than mortgage loans) among banks in Peru, with a 20.1% market share as measured by gross consumer loans as of December 31, 2013. Interbank is also the second largest provider of credit card financing among banks in Peru, with a 22.6% market share by gross credit card loans, and the largest private bank provider of payroll loans to public sector employees, with a 24.6% market share by gross payroll loans, in each case as of December 31, 2013. Interbank has one of the highest net interest margins of the Peruvian banking system, due to its stronger focus on retail banking when compared to its peers. During 2013, Interbank’s net interest margin was 174 basis points higher than the average for the four largest Peruvian banks, according to the SBS. Under IFRS, Interbank’s net interest margin for the year ended December 31, 2013 was 6.2%.

In our insurance segment, Interseguro is the leading provider of annuities in Peru, with a market share of 25.0% as measured by premiums for the year ended December 31, 2013, according to the SBS. Furthermore, Interseguro has maintained the leading position in the Peruvian annuities market since 2010. Annuities represented the fastest-growing insurance product in the Peruvian insurance industry with a five-year CAGR in premiums of 21.6% for the period ended December 31, 2013, driven by the growing number of Peruvians retiring under the Peruvian private pension system. Growth of annuities is expected to further accelerate as the number of Peruvian private pension system’s retirees and their respective average pension balances increase. Over the ten years ended December 31, 2013, 67 thousand people have retired under the Peruvian private pension system compared to a total of 375 thousand and nearly three million expected retirees over the next ten and 30 years, respectively, according to the SBS, to whom Interseguro will offer annuities.

Within our wealth management segment, Inteligo is well-positioned to capture an increasing share of the growing number of wealthy individuals, resulting from strong economic growth and wealth creation in Peru. Inteligo’s five-year CAGR for assets under management plus deposits for the period ended December 31, 2013 was 24.5% under IFRS. We believe Inteligo’s position as a provider of wealth management services to this group of customers will help increase its share of wallet among high net worth individuals, while delivering high levels of growth and profitability.

Outstanding track record of profitable growth, resulting in consistent market share gains

Our strong track record of profitable growth is supported by our increased market share and high profitability across our business segments. In retail banking, Interbank’s total retail loans, including consumer and mortgage loans, achieved a five-year CAGR of 16.6%, compared to 15.7% for the Peruvian banking system, for the period ended December 31, 2013, according to the SBS. In addition, Interbank has increased its market share across retail products over the five-year period ended December 31, 2013. With respect to credit card loans, Interbank’s market share increased from 20.5% to 22.6%, and in mortgage loans, Interbank’s market share increased from 10.1% to 13.1%, in each case from 2008 to 2013.

Interbank has also increased its commercial lending and outpaced the Peruvian banking system, achieving a five-year CAGR of 15.6% in commercial loans outstanding compared to the system’s 11.8%, for the period ended December 31, 2013. Interbank’s market share in commercial loans has increased from 7.7% to 9.0% from 2008 to 2013.

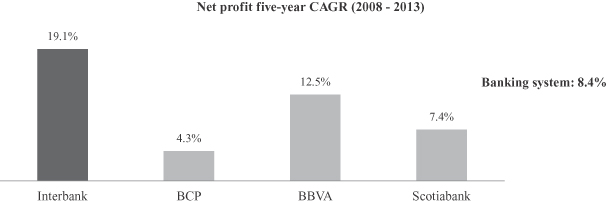

Interbank’s increasing market shares have been accompanied by high profitability, with net profit growing at a five-year CAGR of 19.1% compared to 8.4% for the Peruvian banking system for the period ended December 31, 2013.

Interseguro is one of the fastest growing insurance companies in Peru, achieving a five-year CAGR of 21.7% in premiums, compared to the industry’s 15.9%, for the period ended December 31, 2013, according to the SBS. In addition, Interseguro’s market share by annuities premiums has increased from 22.7% to 25.0% from 2008 to 2013. During this period, Interseguro’s net profit grew at a five-year CAGR of 87.6% compared to 50.2% for the Peruvian insurance industry.

6

Table of Contents

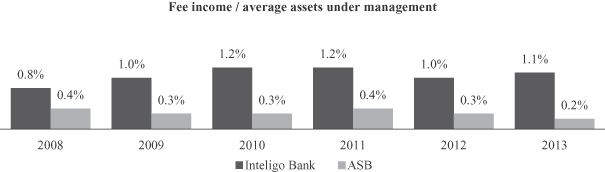

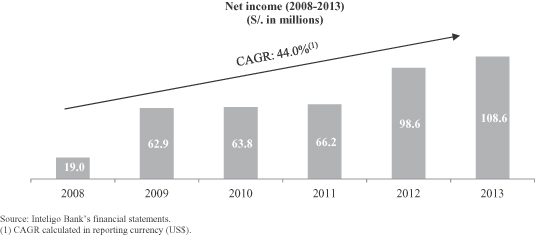

Inteligo Bank’s assets under management plus deposits grew at a five-year CAGR of 24.5% for the period ended December 31, 2013. Similarly, net profit grew at a five-year CAGR of 44.0% for the period ended December 31, 2013, supported by strong fees on assets under management, which stood at 1.08% in 2013 (calculated by dividing (x) fee income from financial services, net by (y) average assets under management).

Convenient, extensive and innovative distribution network with a customer-oriented approach

We believe that our convenient, extensive and innovative retail distribution network, together with our product-specific sales force, has made our products more accessible to our customers and has differentiated us from our competitors.

Interbank has built an omni-channel distribution network in Peru, serving over 1.9 million customers. As of December 31, 2013, Interbank had 268 financial stores and operated the second-largest ATM network in Peru with more than 2,400 ATMs, which includes the largest out-of-branch ATM network (under ourGlobal Net brand). Interbank has the largest number of financial stores inside supermarkets in Peru, which are open on weekends and Monday through Sunday from 9:00 a.m. to 9:00 p.m. Moreover, with the intention of providing underserved customers with more convenient services, Interbank operates a network of correspondent agents, called Interbank Agentes. The correspondent agents’ concept consists of providing commercial establishments with low-cost electronic terminals which allow customers to perform basic transactions. As of December 31, 2013, Interbank had over 3,200 correspondent agents.

Interseguro markets its annuities and individual life insurance products through its own dedicated sales force to ensure the delivery of high quality service and advice to clients. Interseguro’s specialized sales force is trained to provide a differentiated service for various customer types. As of December 31, 2013, Interseguro employed 128 agents exclusively dedicated to sell annuities and 240 agents to sell other insurance products. In addition to its own sales force, Interseguro leverages the retail distribution capacity of other IFS and Intercorp Peru subsidiaries, including Interbank’s distribution network and our affiliate Intercorp Retail’s sales points (Plaza Vea and Oechsle) to offer simple low-cost premium insurance products.

Inteligo has developed a proprietary financial advisory model that has been a key pillar in sustaining its growth. The model takes into account the financial objectives of its clients and emphasizes risk analysis and constant monitoring with portfolio rebalancing. Along with this, Inteligo has been able to successfully segment its target client base in order to deliver tailored products and advice.

Our commitment to innovation as part of our customer-oriented approach is demonstrated by continuous improvement of our banking products and distribution channels. For example, in May 2013, Interbank introduced “Imagine” financial stores, a concept jointly developed with IDEO, a design and innovation consulting firm. “Imagine” fosters a more pleasant and inviting environment to Interbank’s customers, and is designed to educate customers on the use of electronic and Internet banking tools in order to migrate low value transactions to electronic channels, while continuing to capture new customers and exploitcross-selling opportunities. Furthermore, Interbank has a full-time financial store functioning as an innovation lab (Explora), allowing it to constantly test new ideas and concepts. These types of initiatives, among others, have allowed Interbank to receive eight awards for creativity and innovation since 1998 fromCreatividad Empresarial, a consortium comprising local journalists and scholars, which is more than any other bank in Peru.

Sound risk management resulting in strong asset quality and high investment returns

Our experienced risk management teams focus on monitoring and managing risks across all business areas, including credit, market, liquidity, operational risks, among others. We believe our risk management expertise has allowed us to achieve strong asset quality and high investment returns.

7

Table of Contents

Interbank’s underwriting procedures are based on strong analytics and proprietary models, developed in partnership with internationally recognized risk management experts. These models, along with the risk management skills of its experienced risk management team, provide Interbank with competitive advantages. Despite its fast growth and high concentration in retail loans, which tend to have higher levels of delinquency, Interbank’s past-due loans as a percentage of total gross loans ratio as of December 2013 was 1.8%, the second lowest among the four largest banks in Peru and lower than the industry average of 2.1%.

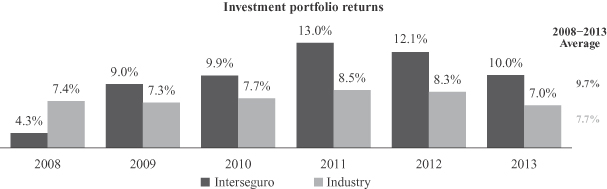

Interseguro’s investment team and its investment management approach have resulted in high investment returns. We believe that Interseguro was the first insurance company in Peru to invest in real estate as part of its investment strategy, taking advantage of high returns in the real estate sector in Peru, to diversify its investment portfolio and to extend its investment portfolio’s duration to better match its liabilities. Interseguro’s returns on its investment portfolio has outperformed the Peruvian insurance industry, achieving an average return of 9.7% from 2008 to 2013, compared to the Peruvian insurance industry’s average of 7.7%, according to data published by the SMV.

Affiliation with the Intercorp Peru group

Our ultimate parent company, Intercorp Peru, is one of Peru’s largest business groups, with activities spanning financial services, retail and real estate, among others. We believe that being part of this group gives us a competitive edge, because of the group’s deep knowledge of the Peruvian consumer, extensive focus and know-how in the Peruvian retail market, highly visible in-country presence and rapid decision-making capabilities.

Experienced management team with proven ability to foster a merit-based culture and a highly-motivated work force

We benefit from an experienced, diverse and talented management team. Most of the members of our senior management have held management positions with other major financial institutions in the United States, Latin America and Europe.

We are focused on attracting, developing and maintaining highly qualified personnel and believe that a merit-based culture that emphasizes teamwork enables them to maintain a motivated workforce that delivers high quality service. Interbank is the only Peruvian company that has been chosen by the Peruvian Great Place to Work Institute as one of the 20 best places to work in Peru for the past 12 consecutive years and one of the top 20 places to work in Latin America for the past two years. Similarly, Interseguro is the only Peruvian insurance company that has been chosen as one of the top five best places to work in Peru (medium-size category) by the Peruvian Great Place to Work Institute for the past four consecutive years, including first place in 2012 and second place in 2013 for Peru and fifth place for Latin America. Additionally, Inteligo SAB has been ranked among the top ten companies in its category (companies with 30 to 250 employees) since it started participating in the Great Place to Work institution survey in 2011, and currently it is the only Peruvian brokerage house included in the ranking.

Strategy

We aim to maintain our leadership position as one of the fastest growing and most profitable providers of financial services in Peru. We aim to provide the best customer experience to our customers based on convenient, agile and friendly service, which we believe leads to new customers and to increased satisfaction, cross-selling and retention of our existing customers.

Leverage our leading market positions in our key businesses to benefit from the significant growth potential of the financial sector

Interbank is a leader in retail banking, particularly in the issuance of credit cards, mortgage origination and payroll lending to public employees, which we believe continue to have significant growth potential in Peru. We believe that Peru’s low credit penetration combined with its strong economic growth will lead to robust growth in consumer and mortgage lending, that Interbank is well positioned to capture.

8

Table of Contents

As of December 31, 2013, the estimated total number of credit cards per inhabitant in Peru was only 0.26 as compared to 1.25 cards per inhabitant for Chile. The ratio of consumer loans-to-GDP and the ratio of mortgage loans-to-GDP in Peru were only 5.4% and 5.3%, respectively, while the averages for the group of peer countries in Latin America were 8.6% and 8.8%, respectively, as of December 31, 2013.

Interbank plans to continue to balance its growth between retail and commercial banking, as it believes that commercial lending will continue to exhibit strong growth in the coming years. We believe there are significant opportunities for Interbank in commercial banking, primarily focusing on Peruvian corporates and medium-size companies, where Interbank has a lower market share (9.0% in terms of gross loans as of December 31, 2013 according to the SBS) when compared to its retail business. Interbank focuses on high margin and fee generating products such as leasing, structured finance, cash management, trade finance and factoring in its commercial lending business.

Interseguro will continue to focus on its annuities business, which we expect to continue to benefit from the growth stemming from the increased number of retirees from the Peruvian private pension system, as well as an increase in total funds managed. Additionally, Interseguro plans to further develop its life and other insurance products targeted to individuals. We intend to capitalize on Interbank’s growing distribution network by continuing sales of insurance products in combination with banking products, and on Intercorp Peru’s extensive distribution network to continue our cross-selling efforts of low-cost premium policies.

We believe that Inteligo’s portfolio of clients and the size of its assets under management plus deposits will continue to grow along with increased wealth generation in Peru. We expect that growth of assets under management plus deposits will outpace Peru’s real economic growth driven by the accelerating demand for sophisticated wealth management services. From 2008 to 2013, Peru’s GDP grew at an average annual real rate of 6.1%, while Inteligo Bank’s assets under management plus deposits grew at a five-year CAGR of 24.5%.

Provide the most convenient, agile and friendly customer service experience through continuous innovation

We are committed to continuing to focus on innovation and providing the best possible and differentiated customer experience for our banking, insurance and wealth management clients. We intend to continue to improve the productivity of our banking distribution model, as well as our systems. We are focused on continuously improving user experience and are increasingly using our alternative channels to sell banking products, such as pre-approved loans.

Interbank aims to provide the most convenient, friendly and agile experience for its customers through a wide variety of distribution channels. To strengthen Interbank’s omni-channel offering, it will continue to invest in its digital channels. Interbank plans to continue to develop a best-in-class experience across multiple devices, including ATMs, desktop PCs, tablets and mobile phones. Interbank will continue to integrate our customer relationship management (“CRM”) and digital marketing capabilities to foster online sales of traditional and innovative products.

Even with Interbank’s extensive distribution network, we believe there is an opportunity to continue to grow physical channels in Peru because the country has one of the lowest branch and ATM penetrations as compared to the peer countries in Latin America. Interbank plans to pursue selective growth of its financial stores and use its ATM and correspondent agent networks to provide additional and more accessible points of contact to customers. In addition, Interbank will continue to improve its in-store customer experience by constantly testing new ideas and concepts through “Explora”, a full-time innovation financial store.

Interseguro markets its annuities and individual life insurance products through its own highly productive sales force to ensure its customers receive high quality financial advice and the best customer service. Interseguro’s sales agents are trained as financial advisors and are segmented according to customer needs.

9

Table of Contents

Interseguro’s CRM platform further facilitates agents maintaining a close relationship with their customers. Additionally, Interseguro offers retirees additional benefits, such as complimentary health screenings and discounts on a range of products and services.

Further develop our customer-centric vision with advanced CRM and analytics

In 2012, Interbank implemented a change from its product-based strategy in order to shift to a customer-centric vision. Having reached a substantial scale in terms of number of clients, loans and deposits, Interbank decided to increase its focus on specific profitable client segments with a customer-centric approach to improve cross-selling and retention without impacting its success in acquiring new clients. We believe that Interbank has a significant opportunity to increase its cross-selling as its number of products per customer remained low at 1.7 in 2013. As a consequence of this strategic shift, Interbank enhanced its CRM and analytics capabilities and is transforming these capabilities into a competitive advantage in the Peruvian market.

Interseguro expects to continue offering personalized and sophisticated assistance to its annuities and individual life insurance customers. The success of its customer-centric strategy is demonstrated by the fact that Interseguro is the largest annuities provider in Peru even though it does not have an affiliated pension fund administrator (“AFP”), unlike some of its competitors. Interseguro also aims to continue to develop simple and convenient retail insurance products that better serve the needs of the growing Peruvian middle class.

Inteligo will continue to focus on its target customers, providing them with advisory services, supported by a local investment team that possesses extensive knowledge of its Peruvian clients’ preferences for financial products. Inteligo’s position will further benefit from having a leading brokerage operation in Peru, Inteligo SAB, and being part of one of Peru’s leading financial groups.

Leverage existing operating capacity to generate additional revenue with low additional marginal cost

We aim to achieve high levels of profitability by leveraging our existing operating capacity. Despite the growth of our platform and portfolios, our efficiency ratio, as measured under IFRS, improved from 43.5% in the year ended December 31, 2012 to 41.5% in the year ended December 31, 2013. Interbank’s focus on cost-control strategies has led to a five-year CAGR of 9.0% in its total expenses, compared to the banking system’s 11.1%, for the period ended December 31, 2013 according to the SBS. We believe that cost control will be increasingly important in our efforts to maintain high profitability in an increasingly competitive environment. To accomplish these goals, we have invested in information technology and the development of simpler, more manageable, secure and modern business processes and platforms.

We have made substantial investments in recent years in expanding the number of our financial stores and developing our mobile platforms. Consequently, we believe we are well-positioned to significantly expand our client base without a substantial increase in expenses. Our budget for capital expenditures for the next three years is approximately S/. 460 million, primarily at Interbank, 70% of which is related to information technology expenditures and 30% is associated with expanding the number of financial stores. Among the budgeted expenditures for information technology, a substantial portion corresponds to new and ongoing IT projects intended to improve the quality and responsiveness of internal operating processes and to continue to improve our digital capabilities, CRM, cash management platform, information systems, among others, as well as product improvements.

Actively pursue cross-selling opportunities to leverage our customer base across IFS and Intercorp Peru

We are currently pursuing cross-selling opportunities, including, primarily, the sale of insurance products to our banking clients. We intend to leverage more of our and Intercorp Peru’s retail presence to cross-sell products

10

Table of Contents

across Interbank, Interseguro and Inteligo. We believe that Interbank’s current 1.9 million retail customers represent a significant opportunity to sell additional banking products and services, as well as Interseguro’s insurance products and Inteligo’s brokerage services. Additionally, we plan to capitalize on the future growth of Intercorp Peru’s retail business through its shopping malls, supermarkets, pharmacies and home improvement stores, to capture the cross-selling opportunities that those channels represent for IFS.

Continue focusing on maintaining a highly motivated team with a strong culture aligned to our strategy

We believe that a motivated workforce leads to high quality customer service, which in turn leads to satisfied customers and better results. Our commitment to fostering a motivated workforce and merit-based culture is demonstrated by being ranked among the top Peruvian and Latin American companies in all of our segments by the Great Place to Work Institute.

Interbank, Interseguro and Inteligo will continue their efforts to attract, develop and retain highly qualified personnel and to maintain a merit-based culture that emphasizes teamwork to keep a motivated workforce that delivers high quality service.

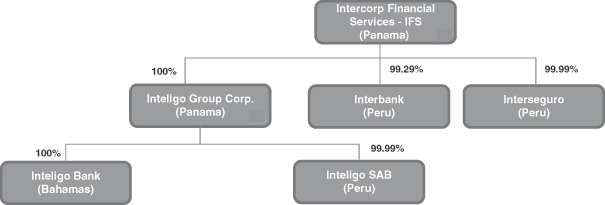

Corporate Structure

The following chart presents our corporate structure, indicating our principal subsidiaries and respective ownership interests.

History

IFS is a corporation (sociedad anónima) organized under the laws of Panama in 2006. We are the majority owner and controlling shareholder of our subsidiaries, Interbank, Interseguro and Inteligo, which comprise our banking, insurance and wealth management segments, respectively. We are responsible for coordinating, supervising and establishing their strategy and management policies. In 2007, we conducted an initial public offering of our common shares publicly in Peru and privately outside of Peru.

Interbank is an open-stock corporation (sociedad anónima abierta). Interbank was incorporated in Lima, Peru in 1897 and formerly conducted business under the names “Banco Internacional del Perú S.A.” and “Interbanc”. In August 1994, as part of the government’s privatization efforts, 91% of Interbank’s share capital

11

Table of Contents

was acquired by Corporación Interbank, which subsequently transferred its holdings in Interbank to the Rodríguez-Pastor family through Intercorp Peru, a limited liability company organized under the laws of the Commonwealth of The Bahamas that is listed on the Lima Stock Exchange. After Interbank’s acquisition by Intercorp Peru in 1994, Interbank began conducting business under the name “Interbank” as part of a rebranding and modernization effort, and has become a leading universal bank in Peru.

Interseguro is a corporation (sociedad anónima) that was incorporated in 1998 by Intercorp Peru, pursuant to an agreement between Intercorp Peru and The Bankers Trust Company (“Bankers Trust”) (at the time the controlling shareholder of Consorcio Nacional de Seguros S.A.A., the largest insurer in Chile) to benefit from the expansion of the insurance business in Peru. In connection with the sale of Bankers Trust to Deutsche Bank AG in 1999, Bankers Trust’s interest in Interseguro was sold to a group of Chilean investors, and in 2000 Intercorp Peru acquired the portion of Interseguro that it did not own.

Inteligo was incorporated under the laws of the Republic of Panama in 2006. Inteligo Bank is a corporation that was incorporated in 1995 in The Bahamas and formerly conducted business under the names of Interbank Overseas Ltd. and Blubank Ltd. It is licensed by the Central Bank of The Bahamas to conduct various types of banking, trust, financing, investment and financial advisory services activities. Inteligo SAB is a corporation (sociedad anónima)that started operations in 1993. It is organized under the laws of Peru, and is licensed by the SMV to operate in Peru and conduct brokerage, custody, portfolio management and advisory services.

On July 18, 2014, the board of directors of IFS approved the acquisition of Inteligo, effective on August 1, 2014. This reorganization entailed the acquisition of 100% of Intercorp Peru’s shares in Inteligo by IFS in exchange for 19.5 million IFS common shares.

Banking Segment

Interbank provides retail and commercial banking services to over 1.9 million total customers as of December 31, 2013. It is the fourth largest bank in Peru in terms of total assets, total loans and total deposits, with market shares of 11.4%, 11.7% and 11.7%, respectively, as of December 31, 2013 and in accordance with SBS. Interbank is focused on fast-growing and highly profitable retail banking businesses, such as credit card financing, payroll loans to public employees and mortgages, as well as Peruvian corporates and medium-size companies within commercial banking.

Given this focus, 49.1% of Interbank’s gross loans as of December 31, 2013 correspond to retail banking, compared to 34.3% for the Peruvian banking system, in accordance with the SBS. Interbank is the second largest provider of consumer financing (retail loans other than mortgages), the leading player among private banks in payroll loans to public sector employees, the second largest provider of credit card financing and the third largest bank in retail deposits in Peru. As part of its strategy to serve retail banking customers, Interbank has one of the most convenient and extensive retail banking distribution networks in Peru and is currently present in 23 of Peru’s 25 regions. Interbank serves its customers through 268 financial stores, more than 2,400 ATMs throughout Peru, which is the second largest ATM network nationwide and the largest out of branch ATM network, and more than 3,200 correspondent agents.

In the commercial banking line of business, which represents 50.9% of Interbank’s gross loans as of December 31, 2013 according to Peruvian GAAP, Interbank focuses on high margin and fee generating products such as leasing, structured finance, cash management, trade finance and factoring in its commercial lending business. These products and services are attractive not only for the financial margins they offer, but also for the fee income they generate. In addition, these products and services enhance customer loyalty and provide significant cross-selling opportunities.

For the years ended December 31, 2013 and 2012, Interbank’s net profit was S/. 615.0 million (US$220.0 million) and S/. 568.4 million, respectively. As of December 31, 2013 and 2012, Interbank had

12

Table of Contents

shareholders’ equity of S/. 2.8 billion (US$1.0 billion) and S/. 2.5 billion, respectively. Interbank’s ROE for the year ended December 31, 2013 and 2012 was 23.7% and 25.1%, respectively, and its ROA for the years ended December 31, 2013 and 2012 was 2.3% and 2.5%, respectively.

Insurance Segment

Interseguro is an insurance company that caters to Peru’s growing middle class. Interseguro is focused on annuities, the fastest growing insurance market segment in Peru, which is driven by the sale of annuities to individuals reaching retirement age in the Peruvian private pension system. Interseguro was the leader in the Peruvian annuities segment for the last four years, with a 25.0% market share by premiums for the year ended December 31, 2013.

The growth of annuities is expected to further accelerate as the number of Peruvian private pension system retirees and their respective average pension balances increase. Over the ten years ended December 31, 2013, 67 thousand people have retired under the Peruvian private pension system compared to a total of 375 thousand and nearly three million expected retirees over the next ten and 30 years, respectively, according to the SBS. In Peru, employees may choose to accumulate their retirement contribution in the public or the private pension system. Under the private pension system, a retiree has the option of converting the capital accumulated in a personal account maintained with an AFP into an annuity offered by a life insurance company, such as Interseguro. In addition to retirement annuities, Interseguro also offers disability annuities to members of the Peruvian private pension system who have been declared permanently or partially disabled, and survivorship annuities for beneficiaries of deceased members of the system. Once an annuity client chooses an insurance company, the decision is irrevocable.

Interseguro also offers traditional life insurance products, as well as low-cost premium retail insurance products, including credit life, mandatory traffic accident insurance (“SOAT”), card protection insurance, among others, mainly sold through IFS and Intercorp Peru’s complementary channels, such as Interbank financial stores and Intercorp Retail’s points of sale (Plaza Vea and Oechsle), and Interseguro’s own network of 368 specialized agents located throughout Peru. Interseguro’s life and retail insurance business lines have grown significantly over the last five years. Interseguro was the fifth largest insurance company and the fifth largest life insurance company in Peru in terms of premiums for the year ended December 31, 2013. In addition, in terms of assets Interseguro was the fourth largest insurance company and the fourth largest life insurance company in Peru as of December 31, 2013.

For the years ended December 31, 2013 and 2012, Interseguro’s net profit was S/. 281.6 million (US$100.7 million) and S/. 150.0 million, respectively. As of December 31, 2013 and 2012, Interseguro had shareholders’ equity of S/. 541.1 million (US$193.6 million) and S/. 704.9 million, respectively. Interseguro’s ROE for the years ended December 31, 2013 and 2012 was 48.2% and 27.1%, respectively. According to the SMV, for the years ended in December 31, 2013, Interseguro was the most profitable insurance company by net profit and achieved the second highest ROE, when compared to the six largest insurance companies in Peru.

Wealth Management

Inteligo is a fast-growing provider of wealth management services through Inteligo Bank and brokerage services through Inteligo SAB. Inteligo caters mainly to Peruvian high net worth individuals, particularly clients with investable assets between US$0.5 million and US$10 million who are benefitting from Peru’s rapid wealth creation. As of December 31, 2013, Inteligo Bank had assets under management plus deposits of S/. 9,260.9 million (US$3,313.4 million), having grown at a five-year CAGR of 24.5% for the period ended December 31, 2013. Increased wealth generation in Peru is expected to continue to create a market for wealth management

13

Table of Contents

services for Peruvian clients. Inteligo conducts various types of banking, trust, financing, brokerage and investing activities for high net worth individuals.

Inteligo SAB provides sales and trading operations for individual and institutional customers primarily in the Peruvian capital markets. As of December 31, 2013, Inteligo SAB was the fourth largest broker by market share in equities trading, according to the SMV.

Inteligo’s net profit for the years ended December 31, 2013 and 2012, was S/. 109.3 million (US$39.1 million) and S/. 99.3 million, respectively. As of December 31, 2013 and 2012, Inteligo had shareholders’ equity of S/. 453.7 million (US$162.3 million) and S/. 370.7 million, respectively. ROE for the years ended December 31, 2013 and 2012 was 26.5% and 28.3%, respectively, and its ROA for the years ended December 31, 2013 and 2012 was 4.2% and 4.7%, respectively. Inteligo Bank represents the principal source of net profit for Inteligo, contributing over 99% of its net profit for the year ended December 31, 2013.

Risks and Challenges

Our ability to leverage our strengths and successfully pursue the strategies described above is subject to a high degree of risk. See “Risk Factors” and the other information included in this prospectus for a discussion of factors you should consider before deciding to invest in our common shares. Such risks include, but are not limited to, the following:

| • | We are a holding company, and all of our operations are conducted by our subsidiaries. Our ability to pay dividends to you will depend on the ability of our subsidiaries to pay dividends to us. |

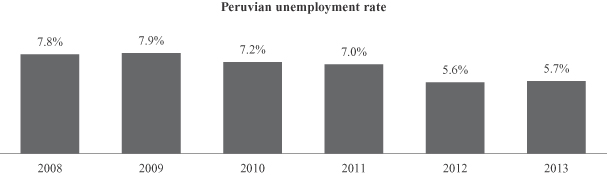

| • | Economic, social and political developments in Peru, including political instability, inflation and unemployment, could have a material adverse effect on our results of operations and financial condition. |

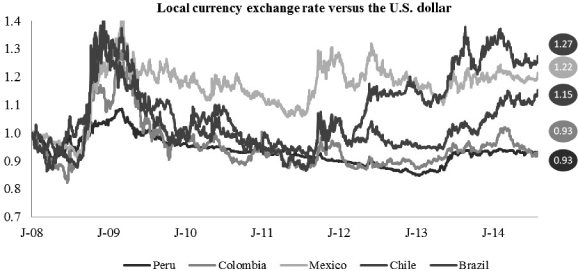

| • | A devaluation of the nuevo sol could have a material adverse effect on our financial condition and results of operations. |

| • | Interest rate changes could have a material adverse effect on our financial condition and results of operations. |

| • | The investment activities of our subsidiaries are subject to factors beyond their control and losses from their exposures could result in a material adverse effect on our financial condition and results of operations. |

| • | We could sustain losses if our asset quality declines. |

| • | Actual mortality and morbidity rates and other factors may differ from those assumed in the calculation of technical reserves and may have a material adverse effect on Interseguro’s financial condition and results of operations. |

| • | Our subsidiaries are subject to extensive supervision and regulation. Changes in existing regulations or the implementation of future regulations may adversely affect our business and results of operations. |

| • | The operations of our subsidiaries require the maintenance of banking, insurance and other licenses and any noncompliance with applicable license and operating obligations could have an adverse effect on our financial condition and results of operation. |

| • | Our subsidiaries face intense competition from other banking, insurance and financial institutions, and, if they are unable to compete successfully, our business and results of operations could be materially and adversely affected. |

14

Table of Contents

Corporate Information

Our principal executive offices are located at Av. Carlos Villarán 140, Urbanización Santa Catalina, La Victoria, Lima 13, Peru. Our telephone number is +(511) 615-9011. Our website address (the contents of which are not part of, and are not incorporated into, this prospectus) iswww.ifs.com.pe.

15

Table of Contents

SUMMARY COMBINED FINANCIAL AND OPERATING INFORMATION

The following table sets forth our summary combined financial information. The combined income statements data for the years ended December 31, 2013 and 2012 and the combined statements of financial position data as of December 31, 2013 and 2012 and January 1, 2012 (our IFRS transition date) are derived from our audited combined financial statements and related notes included elsewhere in this prospectus, which have been prepared in accordance with IFRS as issued by the IASB.

The results included below and elsewhere in this prospectus are not necessarily indicative of our future performance. The summary combined financial information presented below should be read in conjunction with “Presentation of Financial and Other Information,” “Management’s Discussion and Analysis of Results of Operations and Financial Condition” and our audited combined financial statements and related notes included elsewhere in this prospectus.

| For the years ended December 31, | ||||||||||||

| 2013 | 2013 | 2012 | ||||||||||

| (US$ in millions)(1)(2) | (S/. in millions)(1) | |||||||||||

COMBINED INCOME STATEMENTS | ||||||||||||

Net interest and similar income | 625.3 | 1,747.7 | 1,562.0 | |||||||||

Provision for loan losses, net of recoveries | (135.0 | ) | (377.2 | ) | (400.8 | ) | ||||||

|

|

|

|

|

| |||||||

Net interest and similar income after provision for loan losses | 490.3 | 1,370.5 | 1,161.3 | |||||||||

Fee income from financial services, net | 222.5 | 622.0 | 671.5 | |||||||||

Net gain on foreign exchange transactions | 65.6 | 183.4 | 193.9 | |||||||||

Net gain on sale of securities | 86.6 | 241.9 | 138.6 | |||||||||

Other revenues(3) | 77.3 | 216.1 | 185.5 | |||||||||

Total other income | 452.1 | 1,263.5 | 1,189.4 | |||||||||

Total premiums earned less claims and benefits | 32.2 | 89.9 | (60.5 | ) | ||||||||

Total other expenses | (526.3 | ) | (1,471.1 | ) | (1,318.3 | ) | ||||||

|

|

|

|

|

| |||||||

Income before translation result and income tax | 448.2 | 1,252.8 | 971.8 | |||||||||

Translation result | (4.5 | ) | (12.5 | ) | 6.5 | |||||||

Income tax | (95.1 | ) | (265.8 | ) | (213.4 | ) | ||||||

|

|

|

|

|

| |||||||

Profit for the year | 348.7 | 974.6 | 765.0 | |||||||||

|

|

|

|

|

| |||||||

Attributable to: | ||||||||||||

Equity holders of IFS | 347.1 | 970.2 | 760.9 | |||||||||

Non-controlling interest | 1.6 | 4.4 | 4.1 | |||||||||

Pro forma earnings per share(4) | 3.09 | 8.65 | 6.83 | |||||||||

Weighted average pro forma number of shares outstanding (4) | — | 109,895,694 | 110,006,980 | |||||||||

16

Table of Contents

| As of December 31, | As of January 1, | |||||||||||||||

| 2013 | 2013 | 2012 | 2012 | |||||||||||||

| (US$ in millions)(1)(2) | (S/. in millions)(1) | |||||||||||||||

COMBINED STATEMENTS OF FINANCIAL POSITION | ||||||||||||||||

Assets | ||||||||||||||||

Cash, due from banks and inter-bank funds | 2,721.3 | 7,606.0 | 5,781.3 | 2,545.0 | ||||||||||||

Trading securities and investments available-for-sale | 2,031.3 | 5,677.7 | 5,372.2 | 5,898.2 | ||||||||||||

Loans, net of unearned income | 7,571.2 | 21,161.5 | 16,711.0 | 15,002.2 | ||||||||||||

Allowance for loan losses | (248.4 | ) | (694.4 | ) | (588.6 | ) | (500.4 | ) | ||||||||

Investment property | 283.5 | 792.4 | 680.0 | 721.4 | ||||||||||||

Property, furniture and equipment, net | 205.4 | 574.2 | 562.8 | 545.8 | ||||||||||||

Other assets(5) | 379.9 | 1,061.7 | 954.9 | 795.1 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total assets | 12,944.2 | 36,179.2 | 29,473.5 | 25,007.4 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Liabilities and equity | ||||||||||||||||

Deposits and obligations | 7,895.3 | 22,067.5 | 16,138.6 | 14,599.3 | ||||||||||||

Due to banks and correspondents and inter-bank funds | 1,024.0 | 2,862.1 | 2,888.7 | 1,711.9 | ||||||||||||

Bonds, notes and other obligations | 1,225.4 | 3,425.0 | 3,177.1 | 2,639.6 | ||||||||||||

Insurance contract liabilities | 1,122.4 | 3,137.2 | 2,694.5 | 2,426.8 | ||||||||||||

Other liabilities(6) | 348.8 | 975.0 | 955.3 | 695.3 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total liabilities | 11,616.0 | 32,466.7 | 25,854.2 | 22,072.9 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Equity | ||||||||||||||||

Equity holders of IFS | 1,321.0 | 3,692.2 | 3,601.0 | 2,919.4 | ||||||||||||

Non-controlling interest | 7.2 | 20.2 | 18.3 | 15.1 | ||||||||||||

Total equity | 1,328.2 | 3,712.4 | 3,619.3 | 2,934.5 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total liabilities and equity | 12,944.2 | 36,179.2 | 29,473.5 | 25,007.4 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

17

Table of Contents

| As of and for the years ended December 31, | ||||||||||||

| 2013 | 2013 | 2012 | ||||||||||

| (US$ in millions)(1)(2) | (S/. in millions)(1) | |||||||||||

SELECTED FINANCIAL RATIOS | ||||||||||||

Performance Ratios | ||||||||||||

Net interest margin(7) | — | 5.9 | % | 6.3 | % | |||||||

Efficiency ratio(8) | — | 41.5 | % | 43.5 | % | |||||||

ROA | — | 2.9 | % | 2.8 | % | |||||||

ROE | — | 26.9 | % | 24.3 | % | |||||||

Capital and Balance Sheet Structure | ||||||||||||

Average total equity as a percentage of average total assets | — | 10.9 | % | 11.4 | % | |||||||