UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

| Filed by the Registrant ☒ | Filed by a Party other than the Registrant ☐ | |

Check the appropriate box: | ||

| ☐ | Preliminary Proxy Statement | |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ☐ | Definitive Proxy Statement | |

| ☒ | Definitive Additional Materials | |

| ☐ | Soliciting Material Pursuant to §240.14a-12 | |

Nuveen Global High Income Fund (JGH)

(Exact Name of Registrant as Specified in its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

| Payment of Filing Fee (Check the appropriate box): | ||||||

| ☒ | No fee required. | |||||

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||||

| (1) | Title of each class of securities to which transaction applies:

| |||||

| (2) | Aggregate number of securities to which transaction applies:

| |||||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||||

| (4) | Proposed maximum aggregate value of transaction:

| |||||

| (5) | Total fee paid:

| |||||

| Fee paid previously with preliminary materials: | ||||||

| Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | ||||||

| (1) | Amount Previously Paid:

| |||||

| (2) | Form, Schedule or Registration No.:

| |||||

| (3) | Filing Party:

| |||||

| (4) | Date Filed:

| |||||

Nuveen Global High Income Fund (JGH)

|

|

| ||

| March 11, 2021 | Nuveen Fund Advisors, LLC | Proxy Advisory Firm Presentation | ||

3. | ||

5. | ||

10. | ||

11. | ||

13. | ||

14. | ||

15. | ||

16. | ||

| 2 |

Executive Summary – JGH (“The Fund”)

| ∎ | Under the Board’s active stewardship, JGH provides shareholders with attractive returns by investing in a diversified, prudently levered portfolio of global high-yield bonds, plus preferred and convertible securities |

| ∎ | The Fund has delivered on its stated investment objective: providing high current income by paying a meaningfully higher distribution yield than its benchmark’s (the Bloomberg Barclays Global High Yield Hedged Index) income return while also delivering attractive total returns |

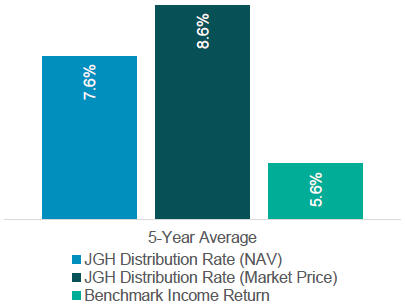

| — | As of 2/28/2021, the Fund’s trailing 5-year average NAV distribution rate was 7.60% which is over 200 basis points higher than its benchmark’s income return of 5.56% |

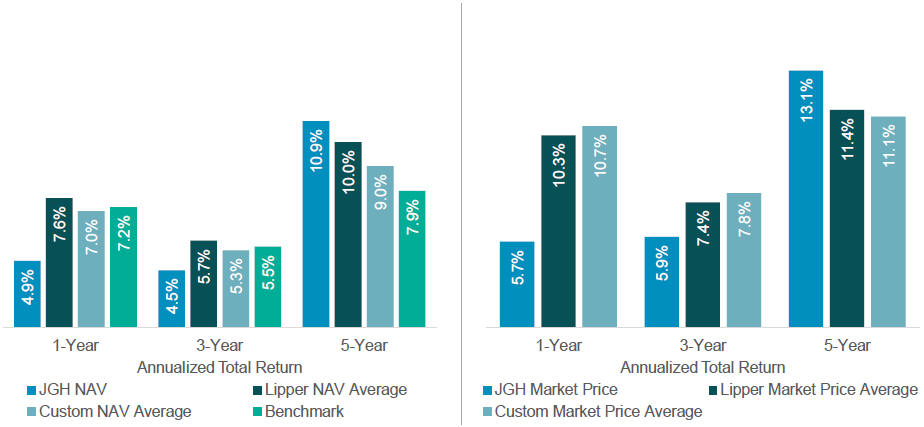

| — | The Fund has also provided compelling long-term returns, with a 5-year annualized return of 10.92% on net asset value and 13.11% on market price as of 2/28/2021, outperforming its Lipper and custom peers1 |

| — | Based on the Fund’s strong long-term track record to date, Nuveen believes that over the course of 2021 the Fund will continue to provide investors with high current income and attractive returns |

| ∎ | JGH’s Board is composed entirely of highly qualified, wholly independent Trustees who have broad and diverse qualifications |

| — | The Fund’s Trustees have exhibited strong, independent governance by drawing upon their deep experience across product types, asset classes, investment strategies and market cycles, which stands in stark contrast to the Saba hedge fund’s proposed nominees that lack any relevant CEF experience |

| — | Long-standing, proactive focus on regular secondary market reviews and taking action to address discounts, including multi-year complex-wide share repurchase and fund rationalization programs |

| — | Implementation of dividend management programs designed to help support secondary market trading for funds, including recent adoption of level distribution policy for JGH with a 32% distribution increase |

1See Appendix D for a list of Lipper and custom peers

| 3 |

Executive Summary (Continued)

| — | Created innovative complex-wide breakpoint pricing methodology that lowers fees for all shareholders with current annualized shareholder savings of $26.7MM / year |

| — | Effectively managed leverage redemptions during the COVID-19 sell-off in March 2020 and continue to develop innovative financing solutions - led industry efforts in developing financing solutions during the ARPs crisis on behalf of common and preferred shareholders |

| ∎ | Saba is an aggressive hedge fund activist out to make a quick profit at the expense of the long-term interests of all JGH’s shareholders |

| — | Saba has a track record of pushing for actions that, if successful, would leave JGH smaller with higher per share expenses and diminished income and return prospects |

| — | Saba’s two hand-picked nominees’ only closed-end fund experience relates to their activities in service of Saba’s interests, and if elected, these nominees will likely seek to take actions that would only advance Saba’s near-term self-serving interests and negatively impact the Fund’s scale and portfolio holdings |

| — | Saba historically has withdrawn its nominees and exited its position whenever a fund acquiesces to its demands, demonstrating its short-sighted focus |

| ∎ | Following the SEC’s decision to rescind the Boulder Letter in response to market developments and a thorough deliberative process by the Board, the Fund adopted a Control Share By-Law to protect the long-term interests of all of its investors |

| — | This action empowers shareholders to protect their long-term interests from a large holder who has no duties to the Fund and may pursue a short-term agenda in opposition to the long-term interests of all shareholders, endangering the very existence of the Fund and its business strategy |

We believe you should support the Board’s recommendation “FOR” the Board-approved nominees on the WHITE proxy card

| 4 |

Snapshot: Nuveen Global High Income Fund (JGH)

∎ $549 MM managed assets with $392 MM common net assets

∎ Formed in November 2014 through the merger of JGG and JGT and was designed to provide shareholders a more scaled, straightforward global high income fund

∎ JGH’s investment objective is to deliver high current income

∎ Managed assets include at least 65% high yield securities, at least 40% non-U.S. securities, and up to 25% in emerging markets debt with up to 15% invested in unhedged non-U.S. dollar bonds

∎ Fund’s Portfolio Team includes both Nuveen’s CIO of Global Fixed Income and Head of High Yield

∎ JGH is in the Lipper High Yield Funds (Leverage) category

∎ Lipper peer category has an emphasis on domestic high yield investing, so Nuveen felt it was appropriate to develop a custom peer group that more closely matches JGH’s global high yield mandate

∎ Custom peer group includes CEFs that (i) employ leverage, (ii) allocate > 30% to non-US fixed income, and (iii) invest greater than 50% in securities rated below investment grade (see Appendix D for peer lists)

|

JGH has delivered on its investment objective by paying a meaningfully higher level of distributions as compared to its benchmark’s income return over time

|

As of 28 February 2021

Source: Nuveen, Bloomberg

Benchmark: Bloomberg Barclays Global High Yield Hedged Index, an unmanaged index considered representative of fixed-rate, non-investment grade debt of companies in the U.S, developed markets and emerging markets.

| 5 |

Snapshot: Nuveen Global High Income Fund (JGH)

JGH was designed for investors seeking high current income from a global high yield

investment and the fund has delivered on its investment objective over time

As of 28 February 2021

Source: Nuveen, Lipper, Bloomberg

Benchmark: Bloomberg Barclays Global High Yield Hedged Index, an unmanaged index considered representative of fixed-rate, non-investment grade debt of companies in the U.S, developed markets and emerging markets.

| 6 |

Snapshot: Nuveen Global High Income Fund (JGH)

JGH’s Board has a proactive focus on maximizing long-term value for all shareholders

JGH has delivered competitive peer- and benchmark-relative NAV

and market price total returns over time

As of 28 February 2021

Source: Nuveen, Lipper, Bloomberg

Benchmark: Bloomberg Barclays Global High Yield Hedged Index, an unmanaged index considered representative of fixed-rate, non-investment grade debt of companies in the U.S, developed markets and emerging markets.

| 7 |

Snapshot: Nuveen Global High Income Fund (JGH)

JGH has attractive peer-relative performance over time

| ∎ | JGH has generally out-performed in positive markets and under-performed in negative markets |

| ∎ | Over the 5-year trailing period, JGH out-performed its benchmark as well as Lipper and custom peers |

| ∎ | Two quarters over the last 3 years have had a meaningful impact on the Fund’s peer relative 1- and 3-year trailing returns |

| ∎ | JGH under-performed in market sell-offs in 2018 Q4 and 2020 Q1 |

| ∎ | After the initial Covid-19 sell-off and related drawdown, JGH has meaningfully outperformed the average Lipper and custom peers |

JGH Quarterly NAV Total Returns & Percentile Rankings

| 2018 | 2019 | 2020 | ||||||||||||||||||||||||||||||||||||||||||||||

| Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | |||||||||||||||||||||||||||||||||||||

JGH NAV | -0.8 | % | 0.2 | % | 2.8 | % | -8.6 | % | 10.6 | % | 3.6 | % | 1.1 | % | 4.9 | % | -26.1 | % | 17.5 | % | 5.8 | % | 9.3 | % | ||||||||||||||||||||||||

JGH Market Price | -2.6 | % | -2.1 | % | 3.1 | % | -10.4 | % | 13.4 | % | 4.1 | % | 2.6 | % | 7.3 | % | -30.3 | % | 21.2 | % | 4.0 | % | 17.0 | % | ||||||||||||||||||||||||

Lipper NAV % Rank | 62 | % | 73 | % | 21 | % | 91 | % | 9 | % | 21 | % | 53 | % | 3 | % | 88 | % | 15 | % | 50 | % | 23 | % | ||||||||||||||||||||||||

Custom NAV % Rank | 67 | % | 25 | % | 8 | % | 92 | % | 8 | % | 67 | % | 58 | % | 8 | % | 83 | % | 33 | % | 33 | % | 50 | % | ||||||||||||||||||||||||

Green text indicates top quartile performance and red text indicates bottom quartile performance.

As of 31 December 2020

Source: Nuveen, Lipper, Bloomberg

Benchmark: Bloomberg Barclays Global High Yield Hedged Index, an unmanaged index considered representative of fixed-rate, non-investment grade debt of companies in the U.S. developed markets and emerging markets.

| 8 |

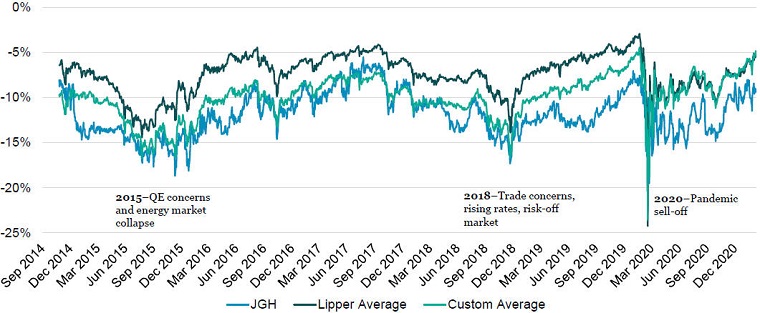

Snapshot: Nuveen Global High Income Fund (JGH)

| Ø | The relationship between market price and net asset value can vary significantly over time |

| ∎ | Fluctuating market sentiment on underlying asset class/investment strategy is often the primary driver of large discounts |

| ∎ | Yield and total return versus peers is often a secondary driver |

| ∎ | Since JGH’s inception in 2014, global high yield funds have experienced three distinct markets |

Daily Premium/Discount

As of 9 March 2021

Source: Nuveen, Lipper, Bloomberg

| 9 |

Proactively Addressing the Discount

JGH’s Board has a proactive focus on monitoring and mitigating discounts

| ∎ | Board authorized the merger of funds to create JGH, resulting in a more highly scaled, straightforward global high yield mandate that provides shareholders with approximately $138K in annual fee savings |

| ∎ | An innovative complex-wide breakpoint pricing methodology was created by the Board which provides roughly $216K in annual fee savings for JGH shareholders |

| ∎ | Board’s oversight of a complex-wide repurchase program resulted in JGH repurchasing shares in 2015, 2016 and 2018 for a combined amount of 900,000 shares (3.7% of O/S) at an average discount of 16.2%, generating approx. $2.5MM of accretion or $0.1040/ share. |

| ∎ | Board adopted a level distribution policy in February 2021 for 7 Nuveen funds designed to help support their prices in the secondary market - JGH increased its distribution by 32.2% which contributed to the narrowing of the discount by 250 bps since the announcement of the policy |

| ∎ | Board oversees a robust and dedicated Investor Relations program designed to increase awareness, engagement and advocacy for the Fund |

| ∎ | Board’s expense oversight has resulted in JGH’s fees and expenses are well below Lipper and custom peers |

| ∎ | Nuveen’s Finance & Treasury team runs a highly scaled $19.5 billion leverage platform which allows us to negotiate with multiple lenders generally resulting in more favorable terms and lower relative leverage costs over time |

| Total Operating Expenses | Leverage Costs | Total Operating Expenses Including Leverage Costs | ||||

| JGH | 1.288 | 0.586 | 1.874 | |||

| Lipper Peer Average | 1.316 | 0.845 | 2.160 | |||

| Custom Peer Average | 1.445 | 0.673 | 2.118 | |||

Note: Fees and expenses are from Lipper and are expressed as a percentage of common assets

As of 7 March 2021

Source: Nuveen, Lipper

| 10 |

Corporate Governance and Board Strengths

| Ø | Nuveen has taken considerable firm-wide steps to advance the interests of its CEF shareholders |

| ∎ | Closed-End Fund Committee closely monitors the structure, operation and performance of Nuveen closed-end funds and works with management to identify potential actions that are in the long-term interests of all fund shareholders |

| ∎ | The Committee meets no less than four times each year to discuss: |

| ✓ | Overall market conditions as they relate to closed-end funds, including trading volumes and liquidity |

| ✓ | Industry-wide closed-end fund distribution, total return and discount trends |

| ✓ | Nuveen closed-end fund distributions, total returns and discounts in the context of industry-wide results and relative to peers, with a particular focus on outliers |

| ✓ | Potential product actions, including modification of investment guidelines, share buybacks, repositioning and mergers |

| ✓ | Detailed quarterly report on leverage management, which includes a review of leverage costs, contribution to performance, counterparty concentration and risk |

| ✓ | Ensure a robust and liquid secondary market for closed-end funds through education and outreach |

| 11 |

Corporate Governance and Board Strengths

| ∎ | The Fund’s unitary board structure and members possess deep, relevant experience across the Nuveen market-leading family of closed-end funds, including global and high yield bond funds, providing unique viewpoints, insights, and qualifications across product types, asset classes, investment strategies and market cycles. |

| ∎ | The Board has a track record of taking thoughtful actions designed to enhance shareholder value, including engaging in frequent market trading reviews resulting in initiatives designed to address and mitigate discounts, including multi-year complex-wide share repurchases and numerous fund mergers. |

| ∎ | In order to continue fulfilling the Fund’s mission to deliver high current income to shareholders, governance provisions have been adopted to protect shareholders against short-term, self-interested hedge funds. |

| ∎ | The Fund’s board refreshment process is driven by continuous, thoughtful trustee selection and development, guided by annually renewed governance principles and relies on a search committee, an active candidate pool, and an extensive interview process. As a result: |

| ✓ | 50% of the Funds’ board is diverse in terms of gender and ethnicity, providing for a wide range of opinions, perspectives and experience. |

| ✓ | Matthew Thornton III was appointed as a trustee for the Fund in November 2020, AFTER the amended by-laws had been adopted by the Board in October of 2020. |

| ✓ | The refreshment process would NOT have identified either of Saba’s nominees as potential candidates |

| ∎ | Board service on any other closed-end or open-end fund complex is not permitted in order to avoid actual conflicts or the appearance of conflicts of interest, reinforcing duty of loyalty to Fund’s core shareholders. |

| 12 |

Control Share Provision: Background & Rationale

Following the SEC’s decision to rescind the Boulder letter and a thorough deliberative Board process, the Fund adopted a Control Share By-law to protect the long-term interests of fund shareholders.

This action:

| ∎ | Protects the Fund’s shareholders from a large shareholder who has NO DUTIES to the Fund and is likely to pursue its own short-term agenda, endangering the very existence of the Fund and its business strategy. |

| ∎ | Enfranchises shareholders who decide whether to reinstate control shareholders’ voting rights. |

| ∎ | Enables the Board to consider thoughtfully the large holder’s proposals so the Board is not at the mercy of an activist’s coercive tactics thereby enabling the Board to protect the interests of all shareholders. |

| ∎ | Is a relatively modest measure in the closed-end fund context because closed-end funds are limited in their ability to adopt defensive measures available to publicly traded corporations that have been proven to be effective against activist shareholders (e.g., rights plans, supervoting preferred stock). |

| ∎ | Does NOT prevent the Board from modifying the control share by-law including to exempt acquirers who are not activists seeking to engage in coercive activities advancing their own short-term interests at the expense of other investors in the Fund. |

| 13 |

The Shortcomings of Saba’s Proposal

Saba has not made the case that change is warranted or that its nominees are more likely to enhance fund governance and achieve improved fund outcomes compared to Board-approved nominees

| Ø | Unlike the current Trustees, Saba’s lack relevant experience |

| ∎ | Saba’s nominees in no way constitute a rounded slate that has the long-term interests of JGH’s core shareholders in mind |

| ∎ | These nominees may seek to advance Saba’s short-term goals rather than the long-term interests of all Fund shareholders |

| ∎ | Saba’s nominees do not have comparable experience with funds, nor do they have the extensive experience with investment company governance that the Fund’s current Trustees possess |

| Ø | Saba has not demonstrated a bona fide interest in fund governance or stewardship in service to a fund’s core, long-term shareholders |

| ∎ | Saba historically has withdrawn its nominees and sold out of its position whenever a fund acquiesces to its demands |

| ∎ | Saba has nominated a short slate of Directors, disenfranchising voters of their full voting right |

| ∎ | Saba often nominates the same individuals for multiple proxy contests; one of Saba’s JGH nominees has also been nominated by Saba for proxy contests at least nine times |

| Ø | Saba’s interests do not align with the long-term interests of all JGH shareholders |

| ∎ | We believe Saba’s hedge fund investors seek a short-term arbitrage opportunity, not high current income over the long-term that the Fund was designed to provide |

| ∎ | We believe Saba’s sole focus is on discount arbitrage, not on ways to enhance JGH’s ability to achieve its fundamental investment objective of high current income, which we believe is the primary long-term driver of JGH’s market price relative to net asset value |

| ∎ | If successful, we believe Saba would take actions that would actually impair rather than enhance JGH’s ability to achieve its fundamental investment objective |

We believe you should support the Board’s recommendation “FOR” the Board-approved nominees on the WHITE proxy card

| 14 |

| ◾ | Under this Board’s active stewardship, JGH has fulfilled its stated investment objective of providing high current income by paying a meaningfully higher distribution yield than its benchmark over all relevant time periods and has lowered Fund expenses relative to peers |

| ◾ | JGH’s discount reflects underlying market fundamentals, not Board inattention or ineffectiveness, as evidenced by our Board taking a proactive approach to monitoring and mitigating the discount |

| ◾ | The JGH Board has extensive track record of enhancing shareholder value with deep experience across product types, asset classes, investment strategies and market cycles |

| ◾ | JGH’s nominees—Jack B. Evans, Albin F. Moschner and Matthew Thornton III—each have superior qualifications when compared to Saba’s nominees and contribute to the Board’s focus on protecting the interests of all shareholders |

| ◾ | Saba has not made the case that change is needed or that its nominees would be better able than the Board nominees to oversee JGH |

| ◾ | Saba does not have a bona fide interest in fund governance, but instead would seek to coerce JGH into taking actions that would generate short-term trading profits for Saba’s hedge fund investors at the expense of the long-term interests of JGH’s core shareholders |

| ◾ | We strongly feel the Board-nominated trustees will provide the best protection for JGH shareholders against coercive action by short-term hedge fund investors like Saba, in-line with the investor protections afforded by the 1940 Act |

| 15 |

| 16 |

Board Nominees for Election at the Annual Meeting

JACK B. EVANS | Mr. Evans has served as Chairman since 2019 and President (1996-2019) of The Hall-Perrine Foundation, a private philanthropic corporation. Mr. Evans was formerly President and Chief Operating Officer (1972-1995) of the SCI Financial Group, Inc., a regional financial services firm headquartered in Cedar Rapids, Iowa. Formerly, he was a member of the Board of the Federal Reserve Bank of Chicago from 1998 to 2003 as well as a Director of Alliant Energy from 2000 to 2004 and President Pro Tem of the Board of Regents for the State of Iowa University System from 2007-2013. Mr. Evans is Chairman of the Board (since 2009) of United Fire Group, a Life Trustee of Coe College and formerly served as a Director and Public Member of the American Board of Orthopaedic Surgery from 2015 to 2020 and served on the Board of The Gazette Company from 1994-2015. He has a Bachelor of Arts from Coe College and an M.B.A. from the University of Iowa. Mr. Evans joined the Board in 1999.

| |

ALBIN F. MOSCHNER | Mr. Moschner is a consultant in the wireless industry and, in July 2012, founded Northcroft Partners, LLC, a management consulting firm that provides operational, management and governance solutions. Prior to founding Northcroft Partners, LLC, Mr. Moschner held various positions at Leap Wireless International, Inc., a provider of wireless services, where he was a consultant from February 2011 to July 2012, Chief Operating Officer from July 2008 to February 2011, and Chief Marketing Officer from August 2004 to June 2008. Before he joined Leap Wireless International, Inc., Mr. Moschner was President of the Verizon Card Services division of Verizon Communications, Inc. from 2000 to 2003, and President of One Point Services at One Point Communications from 1999 to 2000. Mr. Moschner also served at Zenith Electronics Corporation as Director, President and Chief Executive Officer from 1995 to 1996, and as Director, President and Chief Operating Officer from 1994 to 1995. Mr. Moschner was formerly Chairman (2019) and a member of the Board of Directors (2012-2019) of USA Technologies, Inc. and, from 1996 until 2016, he was a member of the Board of Directors of Wintrust Financial Corporation. In addition, he is emeritus (since 2018) of the Advisory Boards of the Kellogg School of Management (1995-2018) and the Archdiocese of Chicago Financial Council (2012-2018). Mr. Moschner received a Bachelor of Engineering degree in Electrical Engineering from The City College of New York in 1974 and a Master of Science degree in Electrical Engineering from Syracuse University in 1979. Mr. Moschner joined the Board in 2016.

| |

MATTHEW THORNTON III | Mr. Thornton has over 40 years of broad leadership and operating experience from his career with FedEx Corporation (“FedEx”), which, through its portfolio of companies, provides transportation, e-commerce and business services. In November 2019, Mr. Thornton retired as Executive Vice President and Chief Operating Officer of FedEx Freight Corporation (FedEx Freight), a subsidiary of FedEx, where, from May 2018 until his retirement, he had been responsible for day-to-day operations, strategic guidance, modernization of freight operations and delivering innovative customer solutions. From September 2006 to May 2018, Mr. Thornton served as Senior Vice President, U.S. Operations at Federal Express Corporation (FedExExpress), a subsidiary of FedEx. Prior to September 2006, Mr. Thornton held a range of positions of increasing responsibility with FedEx, including various management positions. In addition, Mr. Thornton currently (since 2014) serves on the Board of Directors of The Sherwin-Williams Company, where he is a member of the Audit Committee and the Nominating and Corporate Governance Committee, and the Board of Directors of Crown Castle International (since 2020), where he is a member of the Strategy Committee and the Compensation Committee. Formerly (2012-2018), he was a member of the Board of Directors of Safe Kids Worldwide®, a non-profit organization dedicated to the prevention of childhood injuries. Mr. Thornton is a member (since 2014) of the Executive Leadership Council (ELC), the nation’s premier organization of global black senior executives. He is also a member of the National Association of Corporate Directors (NACD). Mr. Thornton has been recognized by Black Enterprise on its 2017 list of the Most Powerful Executives in Corporate America and by Ebony on its 2016 Power 100 list of the world’s most influential and inspiring African Americans. Mr. Thornton received a B.B.A. degree from the University of Memphis in 1980 and an M.B.A. from the University of Tennessee in 2001. Mr. Thornton joined the Board in 2020. | |

| 17 |

Trustees Not Up for Election in 2021

WILLIAM C. HUNTER | Dr. Hunter became Dean Emeritus of the Henry B. Tippie College of Business at the University of Iowa in 2012, after having served as Dean of the College since July 2006. He had been Dean and Distinguished Professor of Finance at the University of Connecticut School of Business from 2003 to 2006. From 1995 to 2003, he was the Senior Vice President and Director of Research at the Federal Reserve Bank of Chicago. He has held faculty positions at Emory University, Atlanta University, the University of Georgia and Northwestern University. He has consulted with numerous foreign central banks and official agencies in Europe, Asia, Central America and South America. He has been a Director of Wellmark, Inc. since 2009. He is a past Director (2005-2015) and a past President (2010-2014) of Beta Gamma Sigma, Inc., The International Business Honor Society and a past Director (2004-2018) of the Xerox Corporation. Dr. Hunter received his PhD (1978) and MBA (1970) from Northwestern University and his BS from Hampton University (1970). Dr. Hunter joined the Board in 2004. | |

JOHN K. NELSON

| Mr. Nelson is currently on the Board of Directors of Core12, LLC. (since 2008), a private firm which develops branding, marketing, and communications strategies for clients. Mr. Nelson has extensive experience in global banking and markets, having served in several senior executive positions with ABN AMRO Holdings N.V. and its affiliated entities and predecessors, including LaSalle Bank Corporation from 1996 to 2008, ultimately serving as Chief Executive Officer of ABN AMRO N.V. North America. During his tenure at the bank, he also served as Global Head of its Financial Markets Division, which encompassed the bank’s Currency, Commodity, Fixed Income, Emerging Markets, and Derivatives businesses. He was a member of the Foreign Exchange Committee of the Federal Reserve Bank of the United States and during his tenure with ABN AMRO served as the bank’s representative on various committees of The Bank of Canada, European Central Bank, and The Bank of England. Mr. Nelson previously served as a senior, external advisor to the financial services practice of Deloitte Consulting LLP (2012-2014). At Fordham University, he served as a director of The President’s Council (2010- 2019) and previously served as a director of The Curran Center for Catholic American Studies (2009-2018). He served as a trustee and Chairman of The Board of Trustees of Marian University (2011-2013). Mr. Nelson is a graduate of Fordham University and holds a BA in Economics (1984) and an MBA in Finance (1991). Mr. Nelson joined the Board in 2013.

| |

JUDITH M. STOCKDALE | Ms. Stockdale retired at the end of 2012 as Executive Director of the Gaylord and Dorothy Donnelley Foundation, a private foundation working in land conservation and artistic vitality in the Chicago region and the Low Country of South Carolina. She is currently a board member of the Land Trust Alliance (since 2013). Her previous positions include Executive Director of the Great Lakes Protection Fund, Executive Director of Openlands, and Senior Staff Associate at the Chicago Community Trust. She has served on the Advisory Council of the National Zoological Park, the Governor’s Science Advisory Council (Illinois) and the Nancy Ryerson Ranney Leadership Grants Program. She has served on the Boards of Brushwood Center, Forefront f/k/a Donors Forum and the U.S. Endowment for Forestry and Communities. Ms. Stockdale, a native of the United Kingdom, has a Bachelor of Science degree in geography from the University of Durham (UK) and a Master of Forest Science degree from Yale University. Ms. Stockdale joined the Board in 1997. | |

| 18 |

Trustees Not Up for Election in 2021

CAROLE E. STONE |

Ms. Stone recently retired from the Board of Directors of the Cboe Global Markets, Inc. (formerly, CBOE Holdings, Inc.) having served from 2010-2020. She previously served on the Boards of the Chicago Board Options Exchange and C2 Options Exchange, Incorporated. Ms. Stone retired from the New York State Division of the Budget in 2004, having served as its Director for nearly five years and as Deputy Director from 1995 through 1999. She has also served as the Chair of the New York Racing Association Oversight Board, as a Commissioner on the New York State Commission on Public Authority Reform and as a member of the boards of directors of several New York State public authorities. Ms. Stone has a Bachelor of Arts in Business Administration from Skidmore College. Ms. Stone joined the Board in 2007. | |

TERENCE J. TOTH | Mr. Toth, the Board’s independent Chair, was a Co-Founding Partner of Promus Capital (2008 to 2017). From 2010 to 2019, he was a Director of Fulcrum IT Services, LLC and from 2008 to 2013, he served as a Director of Legal & General Investment Management America, Inc. From 2004 to 2007, he was Chief Executive Officer and President of Northern Trust Global Investments, and Executive Vice President of Quantitative Management & Securities Lending from 2000 to 2004. He also formerly served on the Board of the Northern Trust Mutual Funds. He joined Northern Trust in 1994 after serving as Managing Director and Head of Global Securities Lending at Bankers Trust (1986 to 1994) and Head of Government Trading and Cash Collateral Investment at Northern Trust from 1982 to 1986. He currently serves on the Boards of Quality Control Corporation (since 2012) and Catalyst Schools of Chicago (since 2008). He is on the Mather Foundation Board (since 2012) and is Chair of its Investment Committee. Mr. Toth graduated with a Bachelor of Science degree from the University of Illinois, and received his MBA from New York University. In 2005, he graduated from the CEO Perspectives Program at Northwestern University. Mr. Toth joined the Board in 2008. | |

MARGARET L. WOLFF |

Ms. Wolff retired from Skadden, Arps, Slate, Meagher & Flom LLP in 2014 after more than 30 years of providing client service in the Mergers & Acquisitions Group. During her legal career, Ms. Wolff devoted significant time to advising boards and senior management on U.S. and international corporate, securities, regulatory and strategic matters, including governance, shareholder, fiduciary, operational and management issues. From 2013 to November 2017, she was a board member of Travelers Insurance Company of Canada and The Dominion of Canada General Insurance Company (each of which is a part of Travelers Canada, the Canadian operation of The Travelers Companies, Inc.). Ms. Wolff has been a trustee of New York-Presbyterian Hospital since 2005 and, since 2004, she has served as a trustee of The John A. Hartford Foundation (a philanthropy dedicated to improving the care of older adults) where she currently is the Chair. From 2005 to 2015, she was a trustee of Mt. Holyoke College and served as Vice Chair of the Board from 2011 to 2015. Ms. Wolff received her Bachelor of Arts from Mt. Holyoke College and her Juris Doctor from Case Western Reserve University School of Law. Ms. Wolff joined the Board in 2016. | |

| 19 |

Trustees Not Up for Election in 2021

ROBERT L. YOUNG | Mr. Young has more than 30 years of experience in the investment management industry. From 1997 to 2017, he held various positions with J.P. Morgan Investment Management Inc. (“J.P. Morgan Investment”) and its affiliates (collectively, “J.P. Morgan”). Most recently, he served as Chief Operating Officer and Director of J.P. Morgan Investment (from 2010 to 2016) and as President and Principal Executive Officer of the J.P. Morgan Funds (from 2013 to 2016). As Chief Operating Officer of J.P. Morgan Investment, Mr. Young led service, administration and business platform support activities for J.P. Morgan’s domestic retail mutual fund and institutional commingled and separate account businesses, and co-led these activities for J.P. Morgan’s global retail and institutional investment management businesses. As President of the J.P. Morgan Funds, Mr. Young interacted with various service providers to these funds, facilitated the relationship between such funds and their boards, and was directly involved in establishing board agendas, addressing regulatory matters, and establishing policies and procedures. Before joining J.P. Morgan, Mr. Young, a former Certified Public Accountant (CPA), was a Senior Manager (Audit) with Deloitte & Touche LLP (formerly, Touche Ross LLP), where he was employed from 1985 to 1996. During his tenure there, he actively participated in creating, and ultimately led, the firm’s midwestern mutual fund practice. Mr. Young holds a Bachelor of Business Administration degree in Accounting from the University of Dayton and, from 2008 to 2011, he served on the Investment Committee of its Board of Trustees. Mr. Young joined the Board in 2017. | |

| 20 |

Appendix B

Overview of Nuveen

| 21 |

Overview of Nuveen’s Approach to CEFs

| ∎ | Widely-recognized as a CEF leader, including secondary market support |

| – | 33 closed-end fund mergers since 2012 involving 107 funds, $85MM cumulative shareholder fee and expense savings |

| – | Long-standing complex-wide share repurchase program, including JGH which has experienced $2.5MM in accretion |

| – | Sponsor of CEFConnect.com, leading industry website for independent CEF information |

| – | Award-winning educational and promotion campaigns |

| – | Nuveen has a unitary Board structure with significant experience across asset classes and product types |

| 22 |

Nuveen global fixed income overview

We manage $300 billion of global fixed income strategies1

Our advantage

| • | Significant scale across all major sectors of the fixed income market |

| • | Deep sector expertise with 117 fixed income investment professionals |

| • | Heritage of risk management and focus on client outcomes |

Investment professionals

| Number

| Average Years Experience | ||||||

Portfolio managers | 36 | 20 | ||||||

Research analysts2 | 64 | 12 | ||||||

Traders | 17 | 16 | ||||||

Total/average | 117 | 15 | ||||||

AUM by strategy ($ billions)

Data is as of 31 Dec 2020.

1 Includes dedicated fixed income accounts and underlying assets within target date, target risk and other multi-asset products.

2 Includes the chief investment officer, head of global fixed income; head of fixed income strategy; and fixed income risk and operations professionals

| 23 |

Leveraged finance leadership team

Leveraged finance management committee guides the platform and sets the strategic vision and priorities in partnership with Nuveen

Management committee

| Scott Grace Head of leveraged finance |  | Anders Persson Chief investment officer, head of Nuveen global fixed income |  | Kevin Lorenz Head of high yield |  | Scott Caraher Head of senior loans | |||||||

| Himani Trivedi Head of structured credit |  | James Kim Head of leveraged finance research and co-head of distressed |  | Chris Williams Head of leveraged finance trading | |||||||||

Investment team and specialists

| PORTFOLIO MANAGEMENT | RESEARCH | TRADING | PRODUCT SPECIALISTS / CPMs | |||

• 12 portfolio managers

• Loans, CLOs, high yield, distressed, converts, hedged credit

• Average experience of 22 years | • 27 research analysts and asset class specialists

• Integrated fundamental research platform covering 26 subsectors and leveraged by all strategies

• Average experience of 13 years | • 6 traders

• Dedicated trading team covers all asset classes for leveraged finance

• Average experience of 15 years | • 9 product specialists and CPMs

• Leveraged finance focused specialists provide market and strategy perspectives to clients

• Average experience of 15 years | |||

| Infrastructure support from a $1T diversified asset management firm |

| Legal | Compliance | Technology | Operations | Risk | Finance | Fund administration | Distribution | Marketing | Client service |

As of 31 Dec 2020

| ||

| 24 |

Dedicated leveraged finance investment team

Well-resourced team covering the broad spectrum of leveraged finance investments

| HIGH YIELD | SENIOR LOANS | CLOs | CONVERTIBLES | DISTRESSED | ||||||

PORTFOLIO MANAGEMENT | Kevin Lorenz, CFA1 (NY) | Scott Caraher1 (NY) | Himani Trivedi1 (SF) | Ron Yee1 (SF) | James Kim1 (SF) | |||||

| Jean Lin, CFA1 (NY) | Anders Persson, CFA1 (CLT) | Aashh Parekh, CFA (CLT) | Ji Min Shin1 (NY) | |||||||

| Kristal Seales, CFA1 (NY) | Brent Engel1 (SF) | |||||||||

| Jake Fitzpatrick, CFA1 (MINN) | ||||||||||

RESEARCH | James Kim1 (SF) | |||||||||||||

| Research analysts | |||||||||||||

CONSUMER/RETAIL | ENERGY/COMMODITY | HEALTHCARE | INDUSTRIALS | TECHNOLOGY, MEDIA | FINANCIALS | |||||||||

| Mark Churchill, CFA (MINN) | Dasol Park (SF) | Derrick Beveridge, CFA3 (CLT) | David Bode (CLT) | AND TELECOM | Jill Hamilton, CFA2,3 (CLT) | |||||||||

| Peter Fauler, CFA2 (CLT) | Andy Pham, CFA3 (SF) | Jill Hamilton, CFA2 (CLT) | Marc Dallon (MINN) | Sina Almasian (SF) | Sharon Walton (MINN) | |||||||||

| Carlos Gonzalez3 (SF) | Andrew Watson2 (SF) | Ventsi Stoichev (SF) | Peter Fauler, CFA2,3 (CLT) | Phil Graf, CFA3 (SF) | ||||||||||

| Adam Willinger, CFA2 (SF) | Martin Kemnec, CFA (SF) | Coale Mechlin (SF) | RESEARCH GENERALIST | |||||||||||

| Adam Willinger, CFA2 (SF) | Andrew Watson2 (SF) | Connor Sparta (CLT) | ||||||||||||

| Zane Willing (SF) | ||||||||||||||

Specialists | ||||||||||||||

MACRO SPECIALIST | CLO SPECIALISTS | DISTRESSED SPECIALISTS | ||||||||||||

| Quinn Brody (NY) | Josh Grumer (NY) | Pei Jie Gao (NY) | ||||||||||||

| Yang Hong (SF) | Sean Monaghan (SF) | |||||||||||||

| Petros Karasakalidis (SF) | Trent Porter, CFA (NY) | |||||||||||||

| Buo Zhang (SF) | ||||||||||||||

TRADING | Christopher Williams1 (CLT) | |||||||||

| Nicholas Maddern, CFA (NY) | Ron Polye, CFA (CLT) | Buo Zhang (SF) | Chris Lai (SF) | Aaron Deering, CFA1 (SF) | ||||||

| Stephen Virgilio (NY) | ||||||||||

CLIENT PORTFOLIO MANAGERS |

David Wilson, CFA (CHIC) Ravi Chintapalli, CFA (CHIC) |

Jim Fink (CLT) Lindsay Gruhl (SF) | Larry Holzenthaler (SF) Shannon Jin, CFA (SF) |

Greg Kuhn (LA) Saheedat Onifade (NY) | Loren Sageser (LA) Laura Stolfi (NY) | |||||

As of 28 Feb 2021 Locations: CLT (Charlotte); NY (New York); MINN (Minneapolis); CHIC (Chicago); SF (San Francisco); LA (Los Angeles) Note: Organizational chart is meant to show functional groupings but does not illustrate actual reporting lines 1 Leverage finance investment committee member 2 Analyst covers more than one industry 3 Industry pod coordinator |  | |||||||||

| 25 |

Nuveen Asset Management

JGH Manager Biographies

Kevin Lorenz, CFA

Head of High Yield

Kevin is head of high yield and responsible for retail and institutional high yield bond focused portfolio management. Kevin has served in a variety of roles since joining the firm in 1987. He has been investing in high yield over his entire career and has focused exclusively on high yield since 1995. Kevin is also a member of the global fixed income investment committee, which discusses and debates investment policy for all global fixed income products.

He began his career at the firm as a generalist focusing on the private placement market. Kevin has been quoted in The New York Times, Barron’s, The Wall Street Journal, Reuters and other financial press as well as appearances on CNBC for his seasoned views on the high yield asset class.

Kevin graduated with a B.S. in Accounting from Rider University and an M.B.A. in Finance from Indiana University. He holds the CFA designation and is a member of the New York Society of Security Analysts.

Anders S. Persson, CFA

CIO of Global Fixed Income

Anders is chief investment officer and is responsible for overseeing all portfolio management, research, trading and investment risk management activities. He is also member of the Nuveen Global Investment Committee.

Prior to his current role, he was head of global fixed income portfolio management and head of research. Before joining the firm, he was a founding member of the team that established SG Cowen’s European high yield effort in London, and later worked to establish the high-yield research effort within Schroders Investment Management. He has also worked as a sell-side high-yield research analyst at Wells Fargo (formerly First Union).

Anders graduated with a B.S. from Lander College and an M.B.A. from Winthrop University. He is a member of the CFA Institute and the North Carolina Society of Security Analysts.

Jacob J. Fitzpatrick, CFA

Associate Portfolio manager

Jake is an associate portfolio manager for Nuveen’s global fixed income team and a member of the leveraged finance sector team.

Jake began working in the investment industry in 2006 and joined the firm in 2015. Previously, he worked as a co-manager of structured product portfolios at Allianz Investment Management. In that role, he was responsible for the investment strategy and allocation of insurance product premiums within the core capital markets. He began his career at U.S. Bancorp Asset Management, where he was a corporate and municipal bond trader for the firm’s mutual funds and wealth management group.

Jake graduated with a B.S. in Finance from the University of Minnesota’s Carlson School of Management and holds the CFA designation.

Firm tenure for Nuveen Asset Management investment professionals may include years of service at predecessor advisory operations.

| 26 |

Appendix C

Misleading Statements Made by Saba

| 27 |

Saba Misleads JGH Shareholders

| Saba’s Misleading Statements | The Truth | |

Control Share provision disenfranchises shareholders | Saba is a self-interested, short-term focused hedge fund that puts long-term shareholder interests and the opportunity for future returns at risk. Control Share provisions are in place to protect the long-term interests of all Fund shareholders. | |

Trustee voting by-law amendments deprive shareholders the right to elect/replace trustees | A vote is scheduled for the upcoming shareholder meeting on 4/6 that will offer shareholders the opportunity to affirm current board members or elect new board members. The current majority shares outstanding standard ensures a representative board that aligns with the objectives of a broad base of shareholders, rather than an election dominated by the interests of select shareholders. | |

The fund trades at a significant discount to NAV and has poor investment performance | JGH has compelling long-term returns, with a 5-year annualized return of 10.92% on NAV and 13.11% on market price as of 2/28/21. JGH outperforms its benchmark of the Bloomberg Barclays Global High Yield Hedged Index over 3-year, 5-year and since inception periods.

JGH’s Board has a proactive focus on monitoring and mitigating discounts, including through multi-year complex-wide share repurchase and fund rationalization programs. | |

Poor fund performance is attributable to lack of effective management of the board of trustees | Jack B. Evans, Albin F. Moschner and Matthew Thornton III are all highly qualified nominees seeing to serve the long-term interests of shareholders. JGH’s trustees currently oversee 67 funds and have designed and implemented an innovative complex-wide breakpoint fee schedule that lowers fees for shareholders by approximately $26.7M per year.

On the other hand, Saba’s nominees lack any relevant closed-end fund experience and are beholden to the short-term interests of Saba. | |

| 28 |

Saba Misleads JGH Shareholders (Continued)

| Saba’s Misleading Statements | The Truth | |

Nuveen is engaged in CEF ESG violations through abuse of corporate governance principles | Nuveen and JGH are transparent about the applicability of ESG policies and proxy voting guidelines. We distinguish between operating companies and CEFs and frequently reinforce the adverse effects of activists in the CEF space that aren’t present in other public companies. JGH operates with the long-term interests of shareholders in mind. | |

JGH manipulates governance principals to trap investors in a high fee, poorly performing fund | JGH collects fees for investment stewardship, in turn paying a meaningfully higher distribution yield than its benchmark over the 3-year, 5-year and since inception periods. In order to continue fulfilling the Fund’s mission to deliver high current income to shareholders, governance provisions have been adopted to protect shareholders against short-term self-interested arbitragers.

None of these governance provisions “trap” shareholders in the Fund.

Since the adoption of JGH’s new bylaws, the discount of the Fund has narrowed significantly. | |

Shareholders were not given an opportunity to vote on bylaw and charter amendments implemented 10/5/20 | The Fund’s Board took carefully considered actions to protect the long-term interests all shareholders against self-interested activist hedge funds like Saba. Saba and other hedge funds have become increasingly aggressive in their efforts to undermine the long-term interests of shareholders. Mechanisms remain in place that allow all shareholders to express opinion and enact change on a majoritarian basis. | |

| 29 |

Appendix D

| 30 |

Peer groups

| • | Due to JGH’s mandate of global high yield investing compared to the Lipper peer group’s emphasis on domestic high yield investing, Nuveen felt it was appropriate to develop a custom peer group of funds focused on the global fixed income market. |

| • | The custom peer group as developed by primarily selecting CEFs that (i) employ leverage, (ii) allocate > 30% to non-US fixed income investments, and (iii) invest greater than 50% in securities rated below investment grade. |

Lipper | ||

Ticker Name | ||

JGH | Nuveen Global High Income Fund | |

ACP | Aberdeen Income Credit Strategies Fund | |

AWF | AllianceBernstein Global High Income Fund, Inc. | |

DYFN | Angel Oak Dynamic Financial Strategies Income Term Trust | |

FINS | Angel Oak Financial Strategies Income Term Trust | |

BGH | Barings Global Short Duration High Yield Fund | |

HYT | BlackRock Corporate High Yield Fund Inc | |

BLW | BlackRock Limited Duration Income Trust | |

DHF | BNY Mellon High Yield Strategies Fund | |

RA | Brookfield Real Assets Income Fund Inc. | |

CIK | Credit Suisse Asset Management Income Fund, Inc. | |

DHY | Credit Suisse High Yield Bond Fund | |

DHG | Deutsche High Income Opportunities Fund Inc | |

KHI | Deutsche High Income Trust | |

DSL | Doubleline Income Solutions Fund | |

DLY | Doubleline Yield Opportunities Fund | |

EHT | Eaton Vance 2021 Target Term Trust | |

FSD | First Trust High Income Long/Short Fund | |

FTHY | First Trust High Yield Opportunities 2027 Term Fund | |

FT | Franklin Universal Trust | |

GOF | Guggenheim Strategic Opportunities Fund | |

VLT | Invesco High Income Trust II | |

IVH | Ivy High Income Opportunities Fund | |

HYF | Managed High Yield Plus Fund Inc. | |

CIF | MFS Intermediate High Income Fund | |

NHS | Neuberger Berman High Yield Strategies Fund Inc. | |

NHF | NexPoint Strategic Opportunities Fund | |

JHAA | Nuveen Corporate Income 2023 Target Term Fund | |

JHB | Nuveen Corporate Income November 2021 Target Term Fund | |

JCO | Nuveen Credit Opportunities 2022 Target Term Fund | |

JHY | Nuveen High Income 2020 Target Term Fund | |

JHA | Nuveen High Income December 2018 Target Term Fund | |

JHD | Nuveen High Income December 2019 Target Term Fund | |

PHF | Pacholder High Yield Fund, Inc. | |

GHY | PGIM Global High Yield fund | |

ISD | PGIM High Yield Bond Fund | |

SDHY | PGIM Short Duration High Yield Opportunities Fund | |

HNW | Pioneer Diversified High Income Trust | |

PHT | Pioneer High Income Trust | |

HYB | The New America High Income Fund, Inc. | |

EAD | Wells Fargo Income Opportunities Fund | |

EHI | Western Asset Global High Income Fund Inc. | |

HIX | Western Asset High Income Fund II Inc. | |

Custom | ||

Ticker Name | ||

JGH | Nuveen Global High Income Fund | |

ACP | Aberdeen Income Credit Strategies Fund | |

AWF | AllianceBernstein Global High Income Fund, Inc. | |

BWG | BrandywineGLOBAL Global Income Opportunities Fund Inc | |

DSL | Doubleline Income Solutions Fund | |

FAM | First Trust/Aberdeen Global Opportunity Income Fund | |

MCR | MFS Charter Income Trust | |

MMT | MFS Multimarket Income Trust | |

GHY | PGIM Global High Yield fund | |

HNW | Pioneer Diversified High Income Trust | |

ERC | Wells Fargo Multi-Sector Income Fund | |

EHI | Western Asset Global High Income Fund Inc. | |

| 31 |