UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant☐ Filed by a Party other than the Registrant☒

Check the appropriate box:

☐ Preliminary Proxy Statement

☐Confidential, for Use of the Commission Only (as permitted by Rule 14-a6(e)(2))

☐ Definitive Proxy Statement

☒ Definitive Additional Materials

☐ Soliciting Material Under §240.14a-12

TICC Capital Corp.

(Name of Registrant as Specified In Its Charter)

NexPoint Advisors, L.P.

Dr. Bob Froehlich

John Honis

Timothy K. Hui

Ethan Powell

William M. Swenson

Bryan A. Ward

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

☒ No fee required.

☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

(1) Title of each class of securities to which transaction applies:

____________________________________________________________________________________________________

(2) Aggregate number of securities to which transaction applies:

____________________________________________________________________________________________________

(3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

____________________________________________________________________________________________________

(4) Proposed maximum aggregate value of the transaction:

____________________________________________________________________________________________________

(5) Total fee paid:

____________________________________________________________________________________________________

☐ Fee paid previously with preliminary materials.

☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.

(1) Amount Previously Paid:

____________________________________________________________________________________________________

(2) Form, Schedule or Registration Statement No.:

____________________________________________________________________________________________________

(3) Filing Party:

____________________________________________________________________________________________________

(4) Date Filed:

____________________________________________________________________________________________________

NexPoint Advisors, L.P. (“NexPoint”) has filed a definitive proxy statement with the Securities and Exchange Commission (the “SEC”) and an accompanying BLUE proxy card to be used to solicit votes for the special meeting of stockholders of TICC Capital Corp. (the “Company”) scheduled to be held on October 27, 2015 (the “Special Meeting”): (i) AGAINST the Company’s proposal to approve a new investment advisory agreement between the Company and TICC Management, LLC, (ii) FOR a competing slate of six director nominees nominated by NexPoint and (iii) AGAINST the Company’s proposal to adjourn the Special Meeting in the event that a quorum is present and the Company’s proposals did not receive sufficient votes for approval.

On October 8, 2015, representatives of NexPoint gave a presentation to representatives of Institutional Shareholder Services Inc. regarding the Company (the “ISS Presentation”). Slides for the ISS Presentation are attached hereto.

Superior Proposal for TICC Capital Corp. Stockholders (NASDAQ: TICC) October 2015 1 Please refer to Important Disclosures and Disclaimers on Page 55

AGENDA Introduction and Executive Summary NexPoint’s Value Proposition for Stockholders Appendix I: Q&A Appendix II: NexPoint’s Capabilities Appendix III: NexPoint’s Board Nominees Important Information Contact Information 2

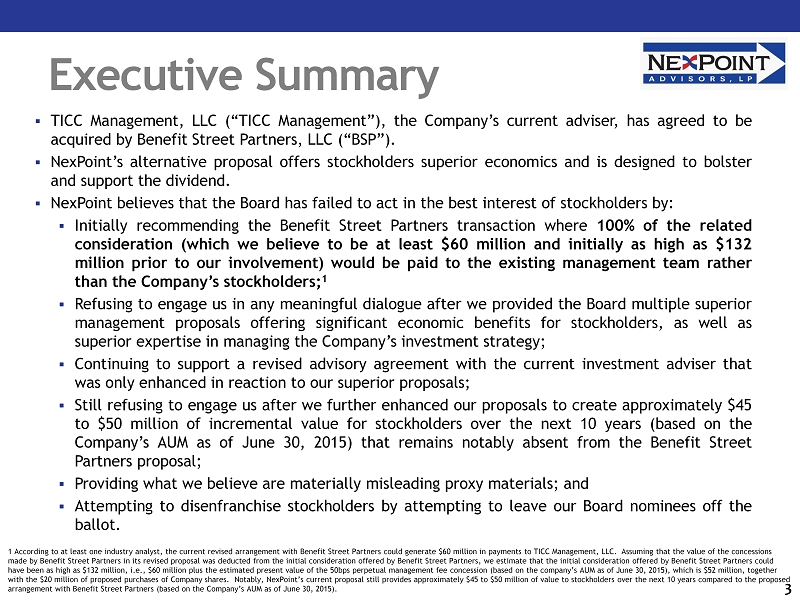

Executive Summary ▪ TICC Management, LLC (“TICC Management”), the Company’s current adviser, has agreed to be acquired by Benefit Street Partners, LLC (“BSP”) . ▪ NexPoint’s alternative proposal offers stockholders superior economics and is designed to bolster and support the dividend . ▪ NexPoint believes that the Board has failed to act in the best interest of stockholders by : ▪ Initially recommending the Benefit Street Partners transaction where 100 % of the related consideration (which we believe to be at least $ 60 million and initially as high as $ 132 million prior to our involvement) would be paid to the existing management team rather than the Company’s stockholders ; 1 ▪ Refusing to engage us in any meaningful dialogue after we provided the Board multiple superior management proposals offering significant economic benefits for stockholders, as well as superior expertise in managing the Company’s investment strategy ; ▪ Continuing to support a revised advisory agreement with the current investment adviser that was only enhanced in reaction to our superior proposals ; ▪ Still refusing to engage us after we further enhanced our proposals to create approximately $ 45 to $ 50 million of incremental value for stockholders over the next 10 years (based on the Company’s AUM as of June 30 , 2015 ) that remains notably absent from the Benefit Street Partners proposal ; ▪ Providing what we believe are materially misleading proxy materials ; and ▪ Attempting to disenfranchise stockholders by attempting to leave our Board nominees off the ballot . 3 1 According to at least one industry analyst, the current revised arrangement with Benefit Street Partners could generate $60 mi llion in payments to TICC Management, LLC. Assuming that the value of the concessions made by Benefit Street Partners in its revised proposal was deducted from the initial consideration offered by Benefit Street Pa rtners, we estimate that the initial consideration offered by Benefit Street Partners could have been as high as $132 million, i.e., $60 million plus the estimated present value of the 50bps perpetual management fee c onc ession (based on the company’s AUM as of June 30, 2015), which is $52 million, together with the $20 million of proposed purchases of Company shares. Notably, NexPoint’s current proposal still provides approximately $45 to $50 million of value to stockholders over the next 10 years compared to th e proposed arrangement with Benefit Street Partners (based on the Company’s AUM as of June 30, 2015).

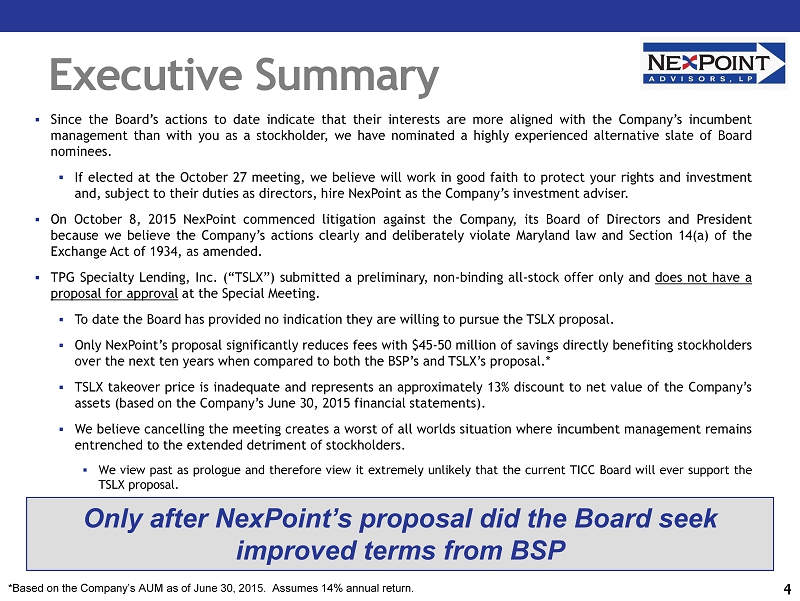

Executive Summary ▪ Since the Board’s actions to date indicate that their interests are more aligned with the Company’s incumbent management than with you as a stockholder, we have nominated a highly experienced alternative slate of Board nominees . ▪ If elected at the October 27 meeting, we believe will work in good faith to protect your rights and investment and, subject to their duties as directors, hire NexPoint as the Company’s investment adviser . ▪ On October 8 , 2015 NexPoint commenced litigation against the Company, its Board of Directors and President because we believe the Company’s actions clearly and deliberately violate Maryland law and Section 14 (a) of the Exchange Act of 1934 , as amended . ▪ TPG Specialty Lending, Inc . (“TSLX”) submitted a preliminary, non - binding all - stock offer only and does not have a proposal for approval at the Special Meeting . ▪ To date the Board has provided no indication they are willing to pursue the TSLX proposal . ▪ Only NexPoint’s proposal significantly reduces fees with $ 45 - 50 million of savings directly benefiting stockholders over the next ten years when compared to both the BSP’s and TSLX’s proposal . * ▪ TSLX takeover price is inadequate and represents an approximately 13 % discount to net value of the Company’s assets (based on the Company’s June 30 , 2015 financial statements) . ▪ We believe cancelling the meeting creates a worst of all worlds situation where incumbent management remains entrenched to the extended detriment of stockholders . ▪ We view past as prologue and therefore view it extremely unlikely that the current TICC Board will ever support the TSLX proposal . 4 Only after NexPoint’s proposal did the Board seek improved terms from BSP *Based on the Company’s AUM as of June 30, 2015. Assumes 14% annual return.

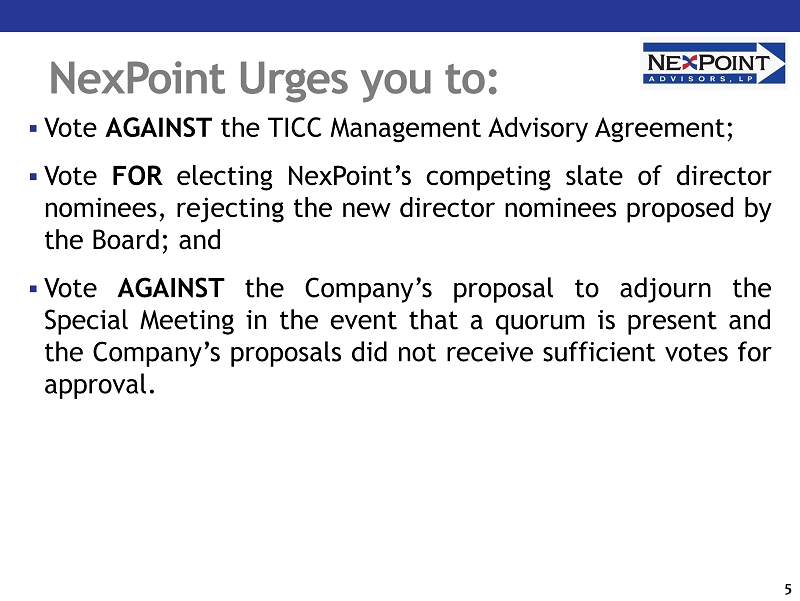

NexPoint Urges you to: ▪ Vote AGAINST the TICC Management Advisory Agreement ; ▪ Vote FOR electing NexPoint’s competing slate of director nominees, rejecting the new director nominees proposed by the Board ; and ▪ Vote AGAINST the Company’s proposal to adjourn the Special Meeting in the event that a quorum is present and the Company’s proposals did not receive sufficient votes for approval . 5

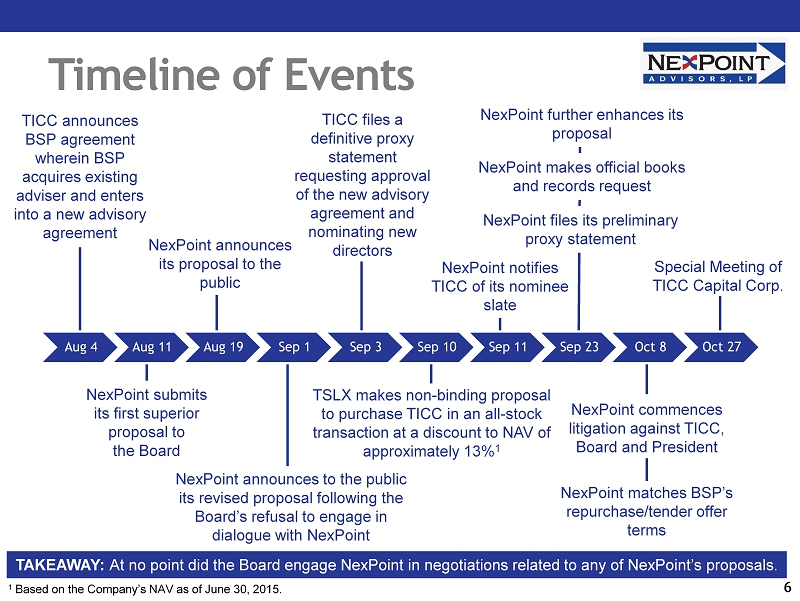

Timeline of Events 6 TICC announces BSP agreement wherein BSP acquires existing adviser and enters into a new advisory agreement NexPoint announces its proposal to the public Special Meeting of TICC Capital Corp. NexPoint submits its first superior proposal to the Board NexPoint announces to the public its revised proposal following the Board’s refusal to engage in dialogue with NexPoint TSLX makes non - binding proposal to purchase TICC in an all - stock transaction at a discount to NAV of approximately 13% 1 NexPoint makes official books and records request NexPoint files its preliminary proxy statement TICC files a definitive proxy statement requesting approval of the new advisory agreement and nominating new directors TAKEAWAY: At no point did the Board engage NexPoint in negotiations related to any of NexPoint’s proposals. NexPoint further enhances its proposal NexPoint notifies TICC of its nominee slate 1 Based on the Company’s NAV as of June 30, 2015. NexPoint commences litigation against TICC, Board and President NexPoint matches BSP’s repurchase/tender offer terms Aug 4 Aug 11 Aug 19 Sep 1 Sep 3 Sep 10 Sep 11 Sep 23 Oct 8 Oct 27

AGENDA Introduction and Executive Summary NexPoint’s Value Proposition for Stockholders Appendix I: Q&A Appendix II: NexPoint’s Capabilities Appendix III: NexPoint’s Board Nominees Important Information Contact Information 7

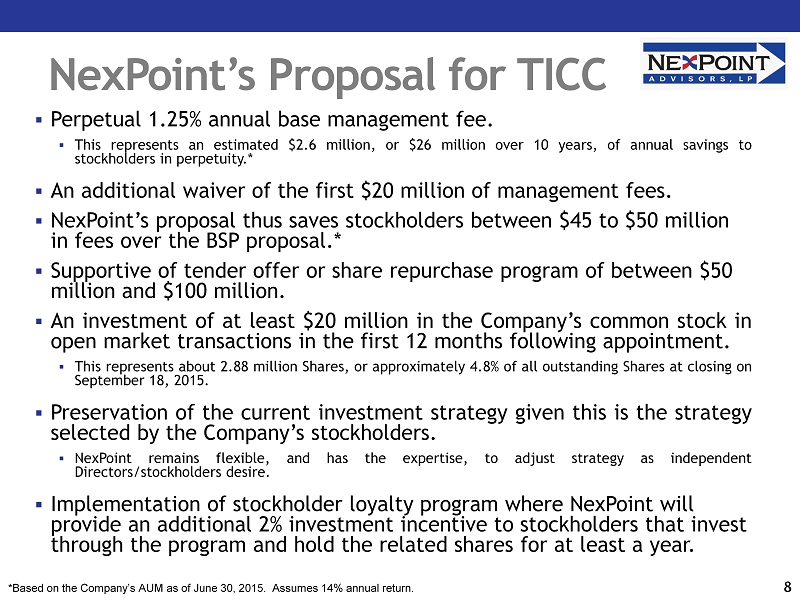

NexPoint’s Proposal for TICC ▪ P erpetual 1 . 25 % annual base management fee . ▪ This represents an estimated $ 2 . 6 million, or $ 26 million over 10 years, of annual savings to stockholders in perpetuity . * ▪ An additional waiver of the first $ 20 million of management fees . ▪ NexPoint’s proposal thus saves stockholders between $45 to $50 million in fees over the BSP proposal.* ▪ Supportive of tender offer or share repurchase program of between $50 million and $100 million. ▪ An investment of at least $ 20 million in the Company’s common stock in open market transactions in the first 12 months following appointment . ▪ This represents about 2 . 88 million Shares, or approximately 4 . 8 % of all outstanding Shares at closing on September 18 , 2015 . ▪ Preservation of the current investment strategy given this is the strategy selected by the Company’s stockholders . ▪ NexPoint remains flexible, and has the expertise, to adjust strategy as independent D irectors/stockholders desire . ▪ Implementation of stockholder loyalty program where NexPoint will provide an additional 2% investment incentive to stockholders that invest through the program and hold the related shares for at least a year . 8 *Based on the Company’s AUM as of June 30, 2015. Assumes 14% annual return.

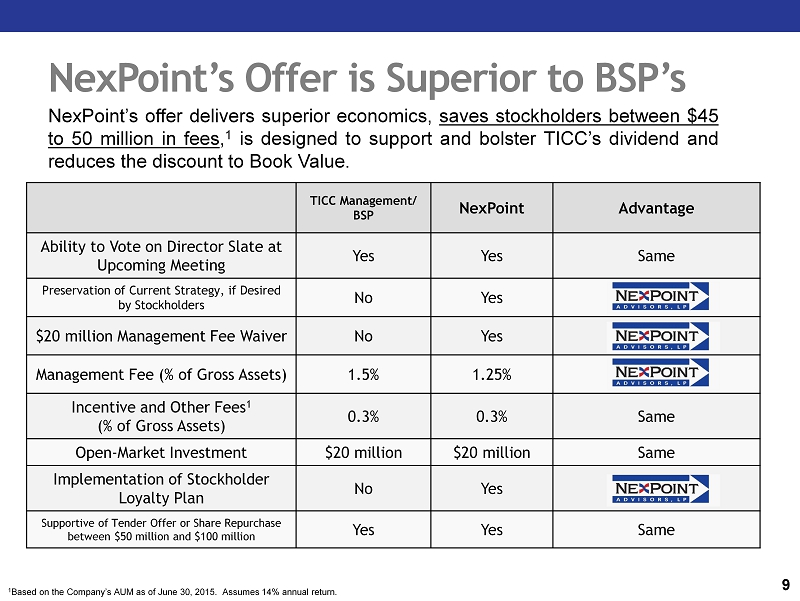

NexPoint’s Offer is Superior to BSP’s TICC Management/ BSP NexPoint Advantage Ability to Vote on Director Slate at Upcoming Meeting Yes Yes Same Preservation of Current Strategy, if Desired by Stockholders No Yes NexPoint $20 million Management Fee Waiver No Yes NexPoint Management Fee (% of Gross Assets) 1.5% 1.25% NexPoint Incentive and Other Fees 1 (% of Gross Assets) 0.3% 0.3% Same Open - Market Investment $20 million $20 million Same Implementation of Stockholder Loyalty Plan No Yes NexPoint Supportive of Tender Offer or Share Repurchase between $50 million and $100 million Yes Yes Same NexPoint’s offer delivers superior economics, saves stockholders between $ 45 to 50 million in fees , 1 is designed to support and bolster TICC’s dividend and reduces the discount to Book Value . 1 Based on the Company’s AUM as of June 30, 2015. Assumes 14% annual return. 9

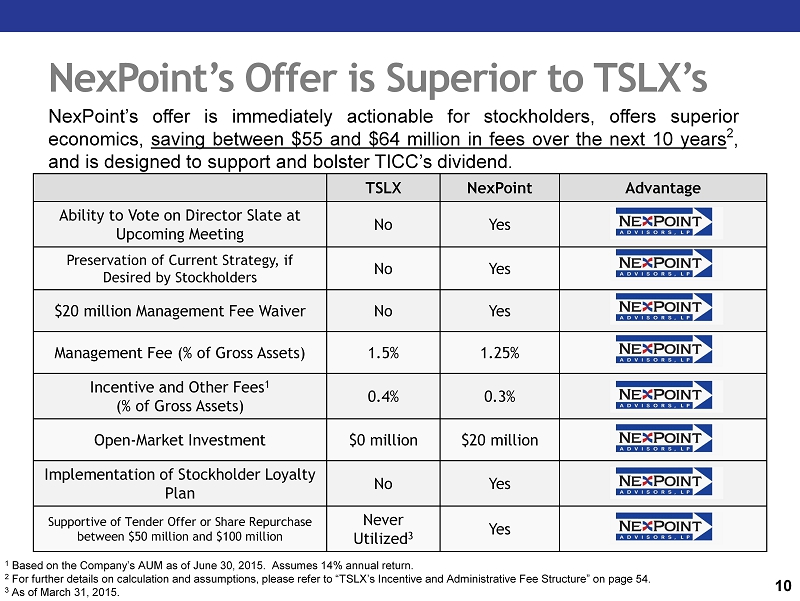

NexPoint’s Offer is Superior to TSLX’s 10 NexPoint’s offer is immediately actionable for stockholders, offers superior economics, saving between $ 55 and $ 64 million in fees over the next 10 years 2 , and is designed to support and bolster TICC’s dividend . TSLX NexPoint Advantage Ability to Vote on Director Slate at Upcoming Meeting No Yes NexPoint Preservation of Current Strategy, if Desired by Stockholders No Yes NexPoint $20 million Management Fee Waiver No Yes NexPoint Management Fee (% of Gross Assets) 1.5% 1.25% NexPoint Incentive and Other Fees 1 (% of Gross Assets) 0.4% 0.3% NexPoint Open - Market Investment $0 million $20 million NexPoint Implementation of Stockholder Loyalty Plan No Yes NexPoint Supportive of Tender Offer or Share Repurchase between $50 million and $100 million Never Utilized 3 Yes Same 1 Based on the Company’s AUM as of June 30, 2015. Assumes 14% annual return. 2 For further details on calculation and assumptions, please refer to “TSLX’s Incentive and Administrative Fee Structure” on pa ge 54. 3 As of March 31, 2015.

NexPoint Offers Superior Economics ▪ Don’t be misled by either BSP or TSLX . ▪ Applicable fees under both BSP and TSLX proposals are materially higher than those proposed by NexPoint . ▪ NexPoint was the first to commit to open market purchases of the Company’s shares to help reduce TICC’s discount to NAV . ▪ The stockholder loyalty program will further help reduce the discount as shares are purchased in the open market when they are trading at a discount . ▪ I nclude the same support as that announced by BSP for a tender offer or share repurchase program of between $ 50 million and $ 100 million . ▪ What it boils down to is that under BSP’s management proposal, initially as much as $ 132 million and now at least $ 60 million (which was solely reduced as a result of our superior bid in favor of stockholders) is being paid to current management of the Company, rather than to the proper beneficiaries : the Company’s stockholders . ▪ In contrast, our proposal offers stockholders $ 45 - 50 million in savings over the BSP proposal and $ 55 - 64 million in savings over the TSLX proposal . 1 11 1 Based on the Company’s AUM as of June 30, 2015. Assumes 14% annual return. For further details on calculation and assumption s, please refer to “TSLX’s Incentive and Administrative Fee Structure” on page 55.

NexPoint’s Superior Experience ▪ NexPoint will maintain the Company’s current investment strategy, which is what stockholders have elected ; ▪ Though remaining flexible, and with the expertise, to adjust the strategy should independent Board members or stockholders so choose . ▪ NexPoint has superior experience to both BSP and TSLX with respect to managing this strategy . ▪ BSP and TSLX are affiliates of traditional private equity sponsors that also specialize in middle market lending . ▪ Only NexPoint and its affiliates have been pioneers in leveraged loans and CLOs for over two decades . 12

Stockholder Focused Board ▪ NexPoint has nominated a highly qualified slate of directors who will be entirely focused on their fiduciary duties and delivering value for stockholders . ▪ Detailed biographies of our nominees are available in Appendix II of this presentation . ▪ If elected we expect to recommend engaging separate, premier legal counsel to advise the Board and TICC . ▪ All Board members will be expected to : ▪ Invest a portion of their board compensation in shares of TICC to further align interest of the board to stockholders . ▪ Comply with continuing education requirements . ▪ The current Board is more aligned with management than stockholders and is seeking to enrich them at stockholder’s expense through the BSP transaction . 13 Replacing the current Board is required to protect stockholder’s interests and investment in TICC, NexPoint’s nominees will protect stockholder value

AGENDA Introduction and Executive Summary NexPoint’s Value Proposition for Stockholders Appendix I: Q&A Appendix II: NexPoint’s Capabilities Appendix III: NexPoint’s Board Nominees Important Information Contact Information 14

Why is NexPoint sending me a proxy statement? ▪ NexPoint believes that the Board has failed to act in your best interests by continuing to support the BSP acquisition and recommending approval of the TICC Management Advisory Agreement while ignoring NexPoint’s repeated requests to meet with the Board, and refusing to engage NexPoint in any meaningful dialogue regarding the terms of NexPoint’s management proposals . ▪ NexPoint’s proposal offers stockholders material benefits that are notably absent from the transaction with BSP . ▪ Shockingly , in addition to the Board’s apparent dereliction of duty in refusing to negotiate with NexPoint, the Secretary of the Company apparently attempted to disenfranchise you and your fellow stockholders by refusing to accept NexPoint’s validly delivered nomination of competing directors . ▪ The Board and the Company continue to mislead and harm stockholders by continuing to leave our nominees off the ballot . ▪ We have commenced litigation to protect stockholder rights and freedom of choice . 15 Q: A :

I agree with NexPoint, what should I do? ▪ To protect your interest and preserve the value of your investment in the Company, NexPoint urges you to vote on the BLUE proxy card : ▪ Vote AGAINST the TICC Management Advisory Agreement ; ▪ Vote FOR electing NexPoint’s competing slate of director nominees ; and ▪ Vote AGAINST the Company’s proposal to adjourn the Special Meeting in the event that a quorum is present and the Company’s proposals did not receive sufficient votes for approval . 16 Q: A :

Can you tell me more about the Board’s conduct ? ▪ On August 11 , 2015 , NexPoint submitted a proposal to the Board that offered the Company and its stockholders significant economic savings compared to the BSP proposal . ▪ Despite NexPoint’s stated desire to discuss the terms of its proposal with the Board, the Board failed to have any discussions with NexPoint on the proposal terms . ▪ Without request from the Board, NexPoint unilaterally enhanced its proposal on September 1 , 2015 ; the Board still refused to engage meaningfully with NexPoint . ▪ Without even meeting with NexPoint in person or by telephone, or engaging in any dialogue with NexPoint regarding the terms of its proposal, the Board rejected NexPoint’s proposal on September 3 , 2015 . ▪ While the Board used NexPoint’s proposal to extract certain concessions from BSP, its failure to enter into any negotiations with NexPoint whatsoever indicates to NexPoint that the Board’s interests are inappropriately aligned with TICC Management and that the Board therefore approved the arrangement with TICC Management without fully considering the interest of the Company or its stockholders . ▪ The Board initially recommended the BSP transaction where 100 % of the related consideration (which we believe to be at least $ 60 million and initially as high as $ 132 million prior to our involvement) would be paid to the existing management team rather than the Company’s stockholders ; ▪ On September 11 , 2015 , the Secretary of the Company apparently attempted to disenfranchise you and your fellow stockholders by refusing to accept NexPoint’s validly delivered nomination of directors . ▪ October 5 , 2015 , the Company falsely informed stockholders that our director nominees were ineligible and that voting for our slate would be “wasting their votes” under what we believe is a meritless interpretation of Maryland law . 17 Q: A :

What is NexPoint’s proposal? ▪ Perpetual 1 . 25 % annual base management fee . ▪ An additional waiver of the first $ 20 million of management fees . ▪ An investment of at least $ 20 million in the Company’s common stock in open market transactions in the first 12 months following appointment . ▪ Supportive of tender offer or share repurchase program of between $ 50 million and $ 100 million . ▪ Preservation of the current investment strategy given this is the strategy selected by the Company’s stockholders . ▪ NexPoint remains flexible to adjust strategy as independent Directors/stockholders desire . ▪ Implementation of stockholder loyalty program where NexPoint will provide an additional 2% investment incentive to stockholders that invest through the program and hold the related shares for at least a year. 18 Q: A :

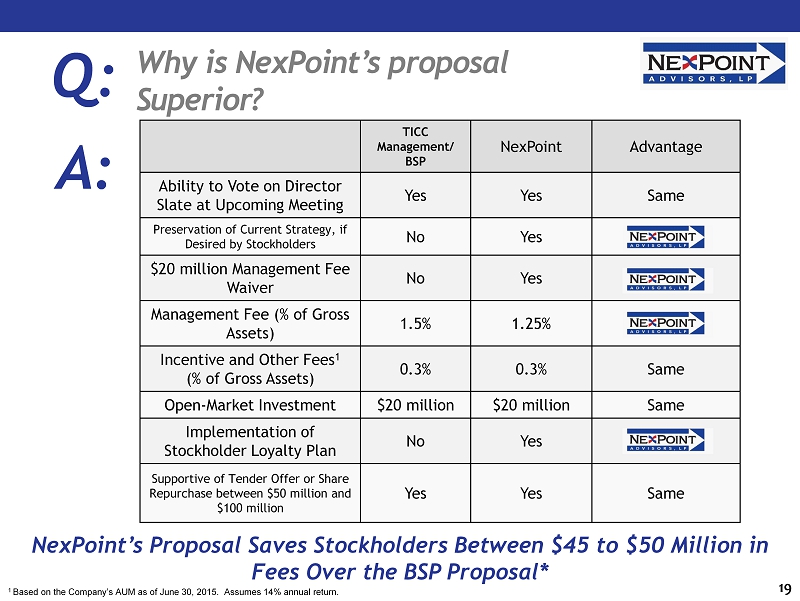

Why is NexPoint’s proposal Superior? 19 Q: A : 1 Based on the Company’s AUM as of June 30, 2015. Assumes 14% annual return. NexPoint’s Proposal Saves Stockholders Between $45 to $50 Million in Fees Over the BSP Proposal* TICC Management/ BSP NexPoint Advantage Ability to Vote on Director Slate at Upcoming Meeting Yes Yes Same Preservation of Current Strategy, if Desired by Stockholders No Yes NexPoint $20 million Management Fee Waiver No Yes NexPoint Management Fee (% of Gross Assets) 1.5% 1.25% NexPoint Incentive and Other Fees 1 (% of Gross Assets) 0.3% 0.3% Same Open - Market Investment $20 million $20 million Same Implementation of Stockholder Loyalty Plan No Yes NexPoint Supportive of Tender Offer or Share Repurchase between $50 million and $100 million Yes Yes Same

Why does NexPoint believe the BSP transaction is designed to enrich management? ▪ According to at least one industry analyst, this arrangement could generate estimated payments of $ 60 million to the Company’s current adviser, TICC Management (an amount we believe was initially as high as $ 132 million prior to our involvement) . 20 Q: A :

Can you tell me more about NexPoint and its qualifications? ▪ NexPoint, together with its affiliates, currently manages approximately $ 20 billion in net assets and believes that its core competencies are squarely within the Company's investment strategy . ▪ NexPoint is affiliated with Highland Capital Management, L . P . ("Highland "), which together with its affiliates, is one of the world's most experienced alternative credit managers , tested by numerous credit cycles, specializing in credit strategies, such as a broad range of leveraged loans, high yield bonds, direct lending, public and private equities and collateralized loan obligations (“CLOs”) . ▪ Highland also offers alternative investment - oriented strategies, including asset allocation, long/short equities, real estate and natural resources . ▪ Over the past two decades, Highland has been a pioneer in developing the loan and CLO markets . In 1996 , Highland launched its first CLO, the first non - bank issued asset backed security structure with syndicated bank loans as the underlying asset . ▪ Highland is now one of the largest U . S . CLO managers by assets under management and has structured and managed over $ 32 billion of CLO and other securitizations since 1996 . A pproximately 60 % of Highland’s $ 22 billion of assets under management are in CLO strategies . ▪ Today, Highland manages an extensive suite of over 18 registered 1940 Act funds comprising approximately $ 6 billion of aggregate assets under management . 21 Q: A :

Are there any alternative proposals on which I can vote? ▪ No, as discussed in the next Q&A . 22 Q: A :

What about the proposal from TPG Specialty Lending, Inc. (“TSLX ”)? ▪ TSLX submitted only a preliminary, highly conditional non - binding all - stock offer, which “ does not constitute or create any commitment, undertaking or other binding obligation” and is “based solely on publicly available information . *” ▪ TSLX presented no path forward on how it would implement its preliminary, non - binding offer (other than continued discussions with the Board) and has failed to present a proposal for approval at the Special Meeting . ▪ On the other hand, to allow the Company to start implementing NexPoint’s proposals and fee concessions, all stockholders need to do is elect NexPoint’s nominees . 23 Q: A : *TPG Specialty Lending press release issued on September 16, 2015.

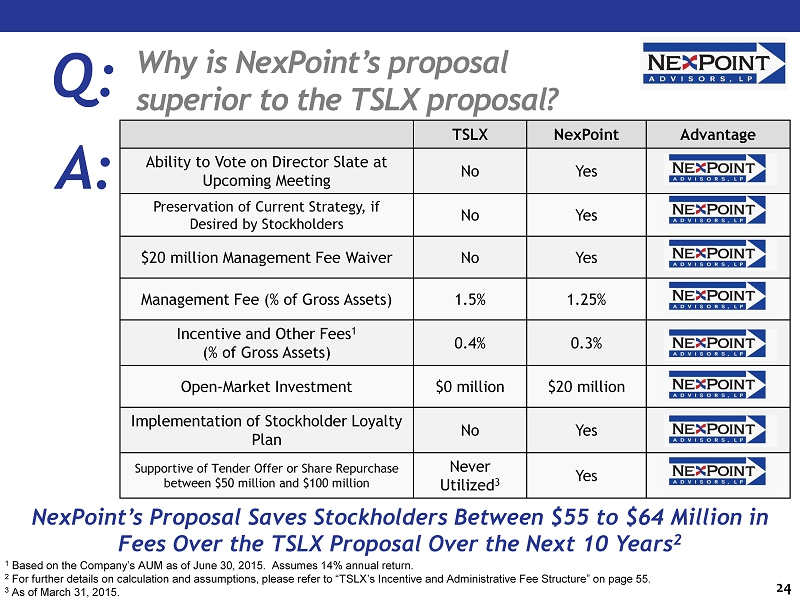

Why is NexPoint’s proposal superior to the TSLX proposal? 24 Q: A : NexPoint’s Proposal Saves Stockholders Between $55 to $64 Million in Fees Over the TSLX Proposal Over the Next 10 Years 2 TSLX NexPoint Advantage Ability to Vote on Director Slate at Upcoming Meeting No Yes NexPoint Preservation of Current Strategy, if Desired by Stockholders No Yes NexPoint $20 million Management Fee Waiver No Yes NexPoint Management Fee (% of Gross Assets) 1.5% 1.25% NexPoint Incentive and Other Fees 1 (% of Gross Assets) 0.4% 0.3% NexPoint Open - Market Investment $0 million $20 million NexPoint Implementation of Stockholder Loyalty Plan No Yes NexPoint Supportive of Tender Offer or Share Repurchase between $50 million and $100 million Never Utilized 3 Yes Same 1 Based on the Company’s AUM as of June 30, 2015. Assumes 14% annual return. 2 For further details on calculation and assumptions, please refer to “TSLX’s Incentive and Administrative Fee Structure” on pa ge 55. 3 As of March 31, 2015.

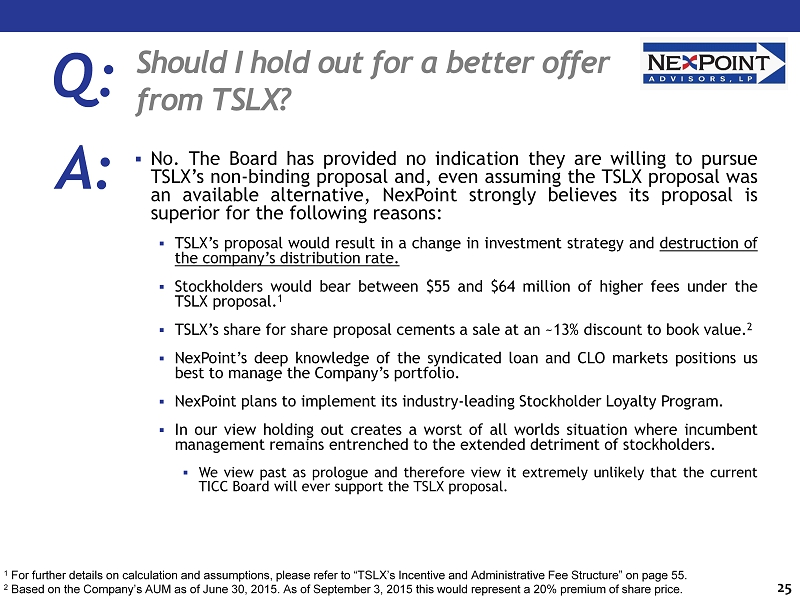

Should I hold out for a better offer from TSLX? 25 Q: A : ▪ No . The Board has provided no indication they are willing to pursue TSLX’s non - binding proposal and, even assuming the TSLX proposal was an available alternative, NexPoint strongly believes its proposal is superior for the following reasons : ▪ TSLX’s proposal would result in a change in investment strategy and destruction of the company’s distribution rate . ▪ Stockholders would bear between $ 55 and $ 64 million of higher fees under the TSLX proposal . 1 ▪ TSLX’s share for share proposal cements a sale at an ~ 13 % discount to book value . 2 ▪ NexPoint’s deep knowledge of the syndicated loan and CLO markets positions us best to manage the Company’s portfolio . ▪ NexPoint plans to implement its industry - leading Stockholder Loyalty Program . ▪ In our view holding out creates a worst of all worlds situation where incumbent management remains entrenched to the extended detriment of stockholders . ▪ We view past as prologue and therefore view it extremely unlikely that the current TICC Board will ever support the TSLX proposal . 1 For further details on calculation and assumptions, please refer to “TSLX’s Incentive and Administrative Fee Structure” on pa ge 55. 2 Based on the Company’s AUM as of June 30, 2015. As of September 3, 2015 this would represent a 20% premium of share price.

Can you tell me more about Nexpoint’s industry - leading loyalty program? ▪ Under this program, NexPoint plans to provide an effective 2 % gross - up of the contributions of stockholders that invest through the plan administrator and hold the related shares for at least one year . ▪ NexPoint believes that this program is effective in promoting long term stockholder loyalty and will help reduce the discount applicable to the Company’s current Share price . ▪ The plan administrator purchases the applicable shares in open market purchases when the Company’s shares are trading at a discount . 26 Q: A :

Why shouldn’t TICC to delay the meeting and seek alternatives such as engaging an investment banker to analyze strategic alternatives? ▪ The Board has already shown, in our view, that they put TICC Management’s interests ahead of stockholders . ▪ Delaying the vote leaves the current management and board in place and risks further value destruction . ▪ We view past as prologue and therefore view it extremely unlikely that the current TICC Board will ever act in the best interest of stockholders . ▪ NexPoint’s proposals create significant immediate and long term value for stockholders . 27 Q: A :

If elected, how will your nominees implement your management proposal? ▪ Both the Board and the Company’s stockholders are required to approve an investment advisory agreement between the Company and NexPoint . ▪ Stockholders are not being asked at the Special Meeting to approve an investment advisory agreement with NexPoint . ▪ If elected, NexPoint believes its director nominees will promptly work to maximize value for stockholders and, subject to their duties as directors, negotiate an investment advisory agreement with NexPoint so that NexPoint could become the Company’s investment adviser . 28 Q: A :

AGENDA Introduction and Executive Summary NexPoint’s Value Proposition for Stockholders Appendix I: Q&A Appendix II: NexPoint’s Capabilities Appendix III: NexPoint’s Board Nominees Important Information Contact Information 29

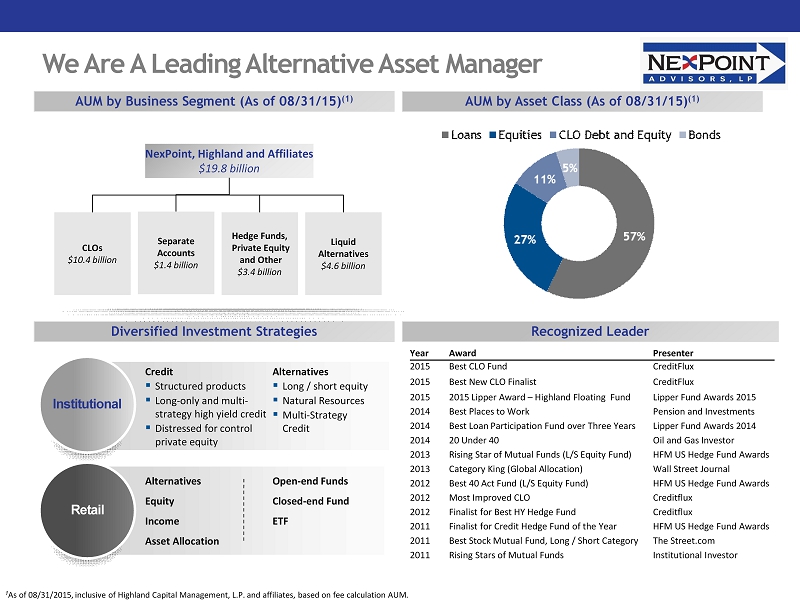

We Are A Leading Alternative Asset Manager CLOs $10.4 billion Liquid Alternatives $4.6 billion NexPoint , Highland and Affiliates $19.8 billion Hedge Funds, Private Equity and Other $3.4 billion Separate Accounts $1.4 billion Year Award Presenter 2015 Best CLO Fund CreditFlux 2015 Best New CLO Finalist CreditFlux 2015 2015 Lipper Award – Highland Floating Fund Lipper Fund Awards 2015 2014 Best Places to Work Pension and Investments 2014 Best Loan Participation Fund over Three Years Lipper Fund Awards 2014 2014 20 Under 40 Oil and Gas Investor 2013 Rising Star of Mutual Funds (L/S Equity Fund) HFM US Hedge Fund Awards 2013 Category King (Global Allocation) Wall Street Journal 2012 Best 40 Act Fund (L/S Equity Fund) HFM US Hedge Fund Awards 2012 Most Improved CLO Creditflux 2012 Finalist for Best HY Hedge Fund Creditflux 2011 Finalist for Credit Hedge Fund of the Year HFM US Hedge Fund Awards 2011 Best Stock Mutual Fund, Long / Short Category The Street.com 2011 Rising Stars of Mutual Funds Institutional Investor Institutional Retail Credit ▪ Structured products ▪ Long - only and multi - strategy high yield credit ▪ Distressed for control private equity Alternatives ▪ Long / short equity ▪ Natural Resources ▪ Multi - Strategy Credit Alternatives Equity Income Asset Allocation Open - end Funds Closed - end Fund ETF AUM by Business Segment (As of 08/31/15) (1) Diversified Investment Strategies Recognized Leader AUM by Asset Class (As of 08/31/15) (1) 1 As of 08/31/2015, inclusive of Highland Capital Management, L.P. and affiliates, based on fee calculation AUM .

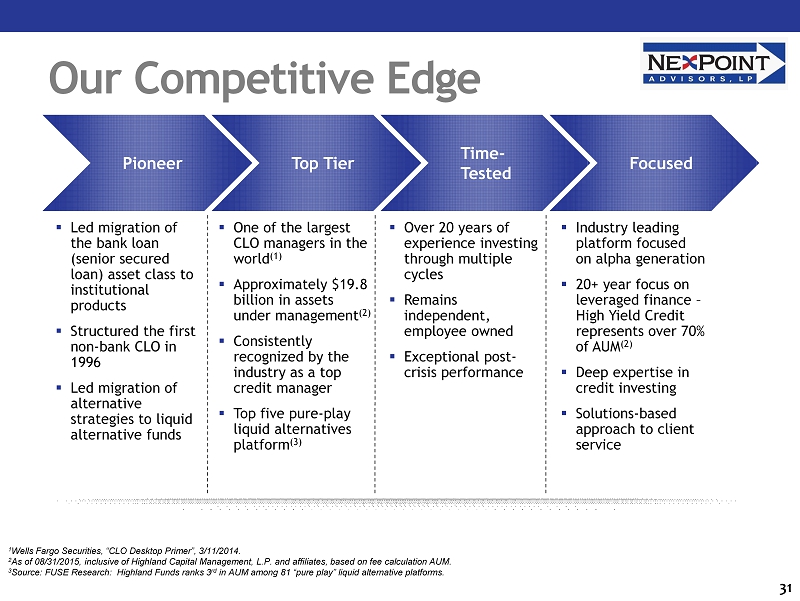

Our Competitive Edge 31 ▪ Led migration of the bank loan (senior secured loan) asset class to institutional products ▪ Structured the first non - bank CLO in 1996 ▪ Led migration of alternative strategies to liquid alternative funds ▪ One of the largest CLO managers in the world (1) ▪ Approximately $19.8 billion in assets under management (2) ▪ Consistently recognized by the industry as a top credit manager ▪ Top five pure - play liquid alternatives platform (3) ▪ Over 20 years of experience investing through multiple cycles ▪ Remains independent, employee owned ▪ Exceptional post - crisis performance ▪ Industry leading platform focused on alpha generation ▪ 20+ year focus on leveraged finance – High Yield Credit represents over 70% of AUM (2) ▪ Deep expertise in credit investing ▪ Solutions - based approach to client service Pioneer Top Tier Time - Tested Focused 1 Wells Fargo Securities, “CLO Desktop Primer”, 3 / 11 / 2014 . 2 As of 08 / 31 / 2015 , inclusive of Highland Capital Management, L . P . and affiliates, based on fee calculation AUM . 3 Source : FUSE Research : Highland Funds ranks 3 rd in AUM among 81 “pure play” liquid alternative platforms .

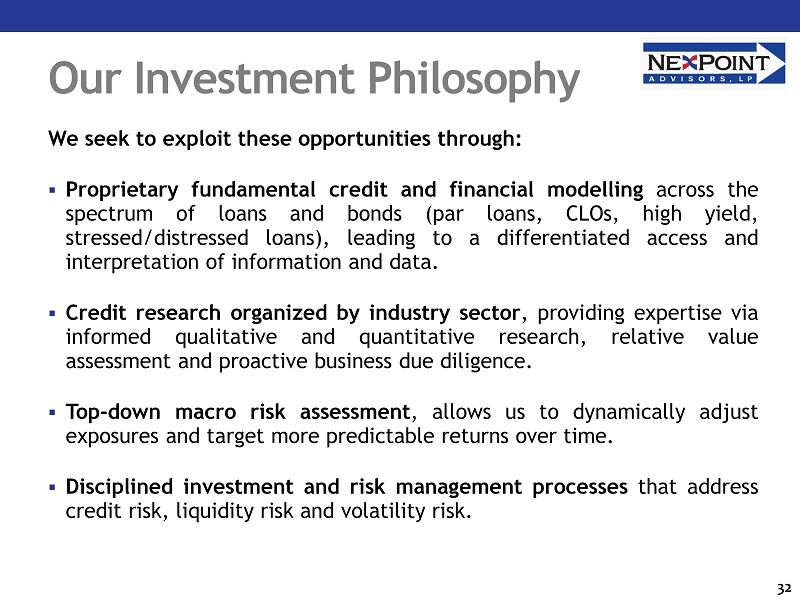

Our Investment Philosophy 32 We seek to exploit these opportunities through : ▪ Proprietary fundamental credit and financial modelling across the spectrum of loans and bonds (par loans, CLOs, high yield, stressed/distressed loans), leading to a differentiated access and interpretation of information and data . ▪ Credit research organized by industry sector , providing expertise via informed qualitative and quantitative research, relative value assessment and proactive business due diligence . ▪ Top - down macro risk assessment , allows us to dynamically adjust exposures and target more predictable returns over time . ▪ Disciplined investment and risk management processes that address credit risk, liquidity risk and volatility risk .

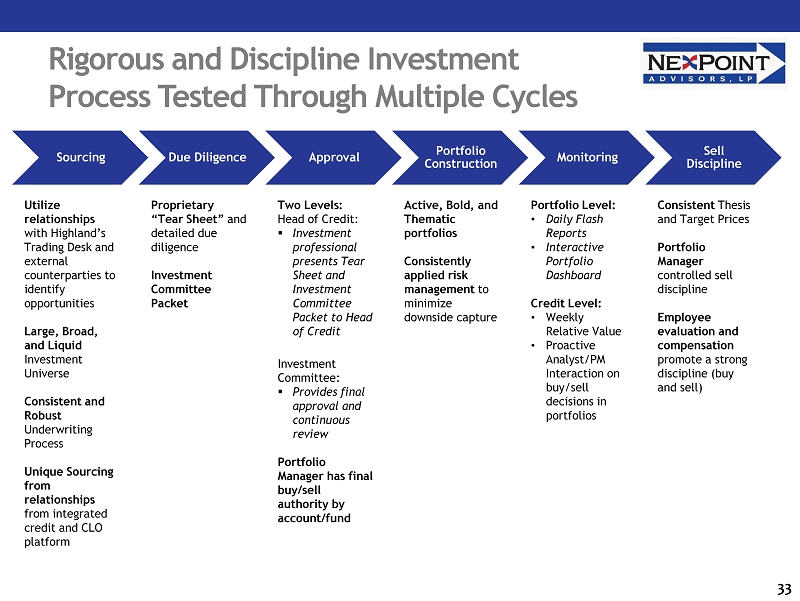

Rigorous and Discipline Investment Process Tested Through Multiple Cycles 33 Sourcing Due Diligence Approval Portfolio Construction Monitoring Sell Discipline Utilize relationships with Highland’s Trading Desk and external counterparties to identify opportunities Large, Broad, and Liquid Investment Universe Consistent and Robust Underwriting Process Unique Sourcing from relationships from integrated credit and CLO platform Proprietary “Tear Sheet” and detailed due diligence Investment Committee Packet Two Levels: Head of Credit: ▪ Investment professional presents Tear Sheet and Investment Committee Packet to Head of Credit Investment Committee: ▪ Provides final approval and continuous review Portfolio Manager has final buy/sell authority by account/fund Active, Bold, and Thematic portfolios Consistently applied risk management to minimize downside capture Portfolio Level: • Daily Flash Reports • Interactive Portfolio Dashboard Credit Level: • Weekly Relative Value • Proactive Analyst/PM Interaction on buy/sell decisions in portfolios Consistent Thesis and Target Prices Portfolio Manager controlled sell discipline Employee evaluation and compensation promote a strong discipline (buy and sell)

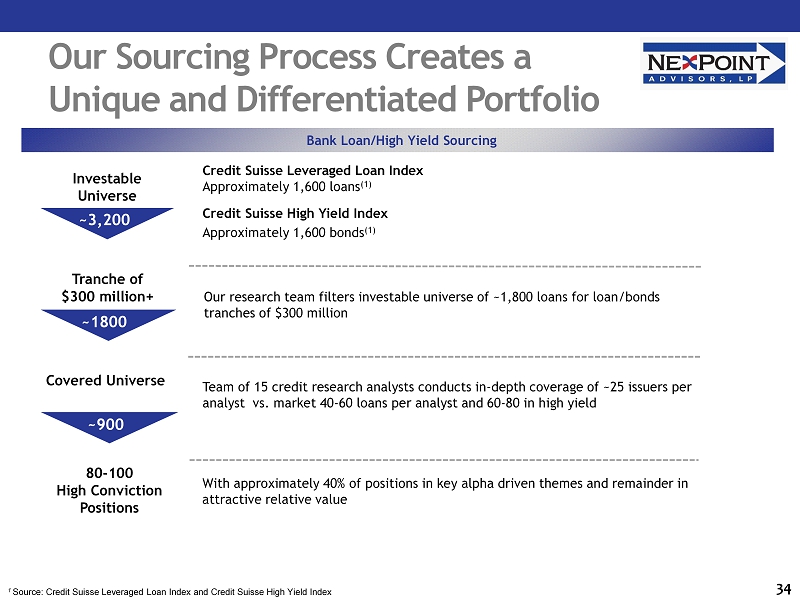

Our Sourcing Process Creates a Unique and Differentiated Portfolio 34 Credit Suisse Leveraged Loan Index Approximately 1,600 loans (1) Credit Suisse High Yield Index Approximately 1,600 bonds (1 ) Investable Universe Tranche of $300 million+ Covered Universe Team of 15 credit research analysts conducts in - depth coverage of ~25 issuers per analyst vs. market 40 - 60 loans per analyst and 60 - 80 in high yield Our research team filters investable universe of ~1,800 loans for loan/bonds tranches of $300 million ~3,200 ~1800 ~900 80 - 100 High Conviction Positions Bank Loan/High Yield Sourcing With approximately 40% of positions in key alpha driven themes and remainder in attractive relative value 1 Source: Credit Suisse Leveraged Loan Index and Credit Suisse High Yield Index

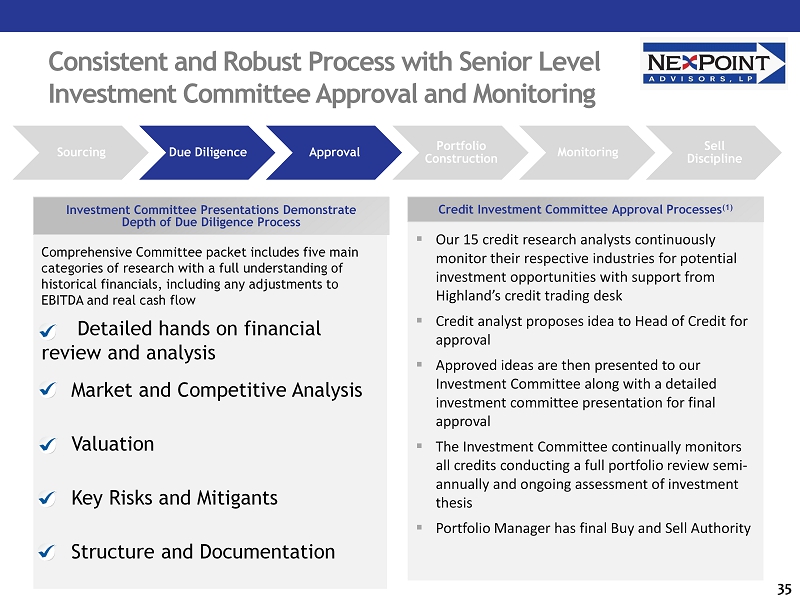

Comprehensive Committee packet includes five main categories of research with a full understanding of historical financials, including any adjustments to EBITDA and real cash flow Detailed hands on financial review and analysis Market and Competitive Analysis Valuation Key Risks and Mitigants Structure and Documentation Consistent and Robust Process with Senior Level Investment Committee Approval and Monitoring 35 ▪ Our 15 credit research analysts continuously monitor their respective industries for potential investment opportunities with support from Highland’s credit trading desk ▪ Credit analyst proposes idea to Head of Credit for approval ▪ Approved ideas are then presented to our Investment Committee along with a detailed investment committee presentation for final approval ▪ The Investment Committee continually monitors all credits conducting a full portfolio review semi - annually and ongoing assessment of investment thesis ▪ Portfolio Manager has final Buy and Sell Authority Sourcing Due Diligence Approval Portfolio Construction Monitoring Sell Discipline Credit Investment Committee Approval Processes (1) Investment Committee Presentations Demonstrate Depth of Due Diligence Process

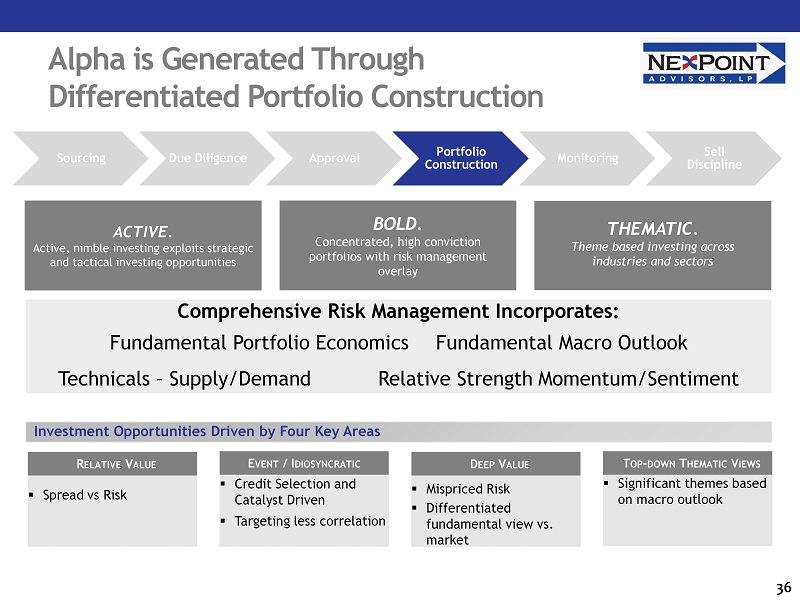

Alpha is Generated Through Differentiated Portfolio Construction 36 Sourcing Due Diligence Approval Portfolio Construction Monitoring Sell Discipline THEMATIC. Theme based investing across industries and sectors Comprehensive Risk Management Incorporates: Fundamental Portfolio Economics Fundamental Macro Outlook Technicals – Supply/Demand Relative Strength Momentum/Sentiment ACTIVE . Active , nimble investing exploits strategic and tactical investing opportunities BOLD. Concentrated, high conviction portfolios with risk management overlay R ELATIVE V ALUE E VENT / I DIOSYNCRATIC D EEP V ALUE T OP - DOWN T HEMATIC V IEWS Investment Opportunities Driven by Four Key Areas ▪ Spread vs Risk ▪ Credit Selection and Catalyst Driven ▪ Targeting less correlation ▪ Mispriced Risk ▪ Differentiated fundamental view vs. market ▪ Significant themes based on macro outlook

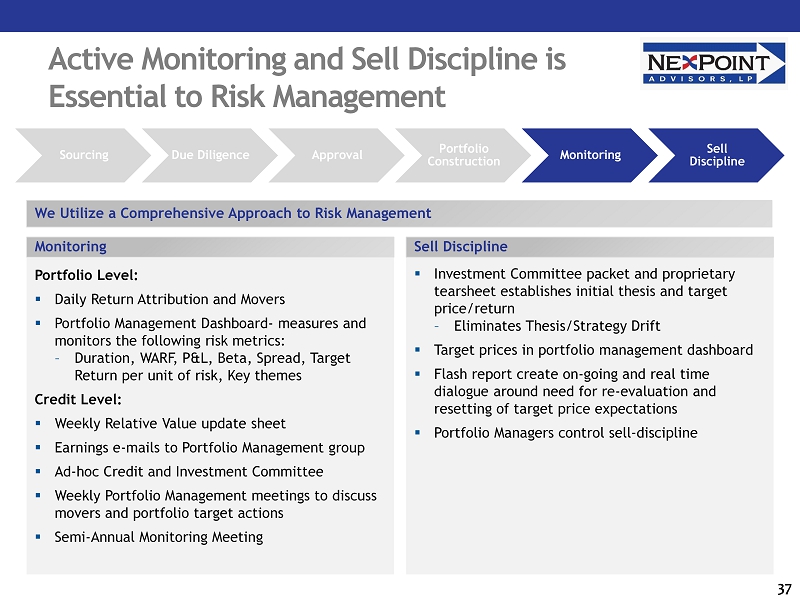

Active Monitoring and Sell Discipline is Essential to Risk Management 37 Sourcing Due Diligence Approval Portfolio Construction Monitoring Sell Discipline Portfolio Level: ▪ Daily Return Attribution and Movers ▪ Portfolio Management Dashboard - measures and monitors the following risk metrics: – Duration, WARF, P&L, Beta, Spread, Target Return per unit of risk, Key themes Credit Level: ▪ Weekly Relative Value update sheet ▪ Earnings e - mails to Portfolio Management group ▪ Ad - hoc Credit and Investment Committee ▪ Weekly Portfolio Management meetings to discuss movers and portfolio target actions ▪ Semi - Annual Monitoring Meeting ▪ Investment Committee packet and proprietary tearsheet establishes initial thesis and target price/return – Eliminates Thesis/Strategy Drift ▪ Target prices in portfolio management dashboard ▪ Flash report create on - going and real time dialogue around need for re - evaluation and resetting of target price expectations ▪ Portfolio Managers control sell - discipline We Utilize a Comprehensive Approach to Risk Management Monitoring Sell Discipline

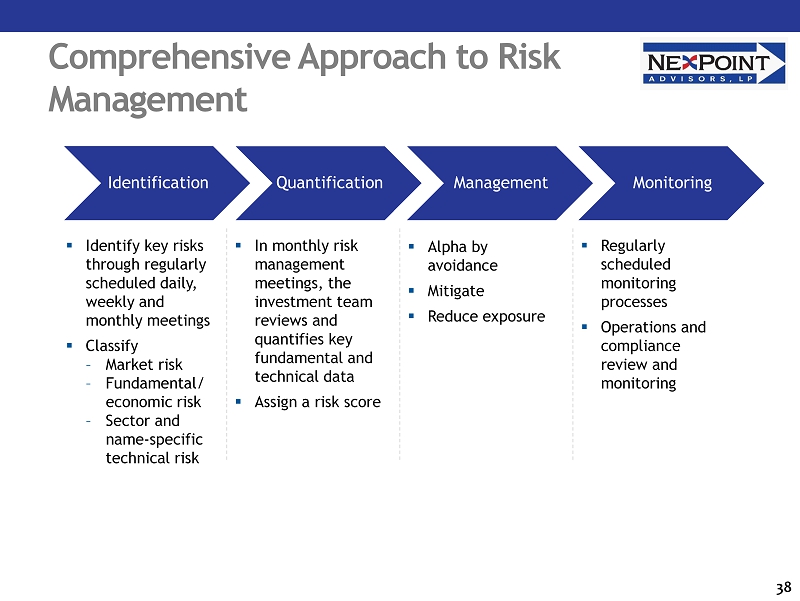

Comprehensive Approach to Risk Management 38 ▪ Identify key risks through regularly scheduled daily, weekly and monthly meetings ▪ Classify – Market risk – Fundamental/ e conomic risk – Sector and name - specific technical risk ▪ In monthly risk management meetings, the investment team reviews and quantifies key fundamental and technical data ▪ Assign a risk score ▪ Alpha by avoidance ▪ Mitigate ▪ Reduce exposure ▪ Regularly scheduled monitoring processes ▪ Operations and compliance review and monitoring Identification Quantification Management Monitoring

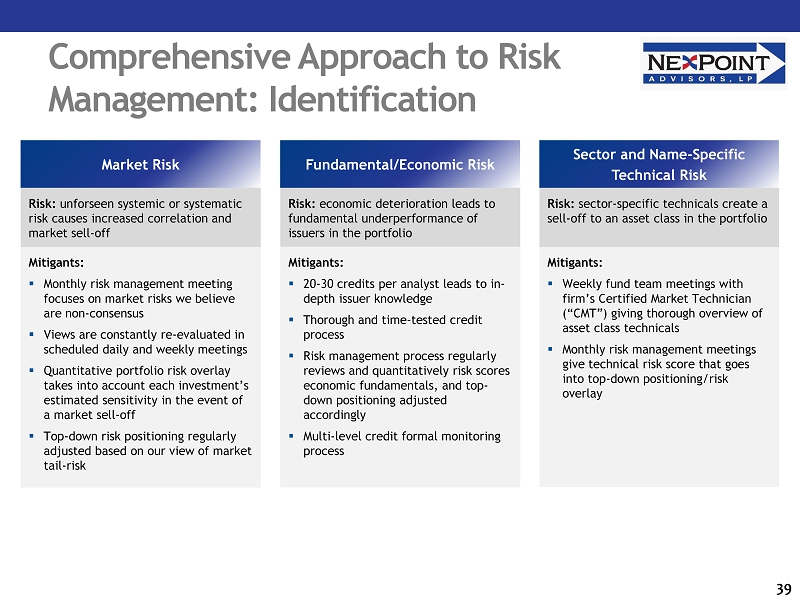

Comprehensive Approach to Risk Management: Identification 39 Market Risk Mitigants : ▪ Monthly risk management meeting focuses on market risks we believe are non - consensus ▪ Views are constantly re - evaluated in scheduled daily and weekly meetings ▪ Quantitative portfolio risk overlay takes into account each investment’s estimated sensitivity in the event of a market sell - off ▪ Top - down risk positioning regularly adjusted based on our view of market tail - risk Risk: unforseen systemic or systematic risk causes increased correlation and market sell - off Fundamental/Economic Risk Risk: economic deterioration leads to fundamental underperformance of issuers in the portfolio Mitigants : ▪ 20 - 30 credits per analyst leads to in - depth issuer knowledge ▪ Thorough and time - tested credit process ▪ Risk management process regularly reviews and quantitatively risk scores economic fundamentals, and top - down positioning adjusted accordingly ▪ Multi - level credit formal monitoring process Sector and Name - Specific Technical Risk Mitigants : ▪ Weekly fund team meetings with firm’s Certified Market Technician (“CMT”) giving thorough overview of asset class technicals ▪ Monthly risk management meetings give technical risk score that goes into top - down positioning/risk overlay Risk: sector - specific technicals create a sell - off to an asset class in the portfolio

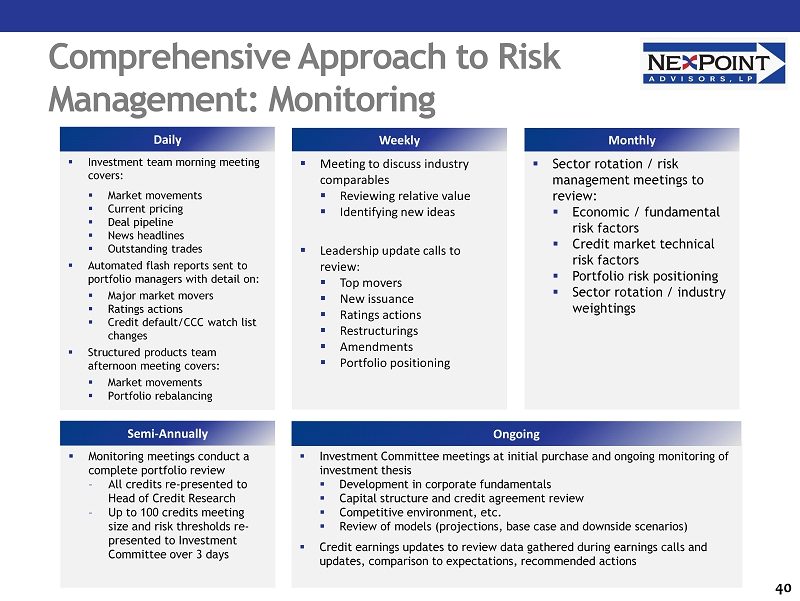

▪ Investment Committee meetings at initial purchase and ongoing monitoring of investment thesis ▪ Development in corporate fundamentals ▪ Capital structure and credit agreement review ▪ Competitive environment, etc . ▪ Review of models (projections, base case and downside scenarios) ▪ Credit earnings updates to review data gathered during earnings calls and updates, comparison to expectations, recommended actions ▪ Monitoring meetings conduct a complete portfolio review – All credits re - presented to Head of Credit Research – Up to 100 credits meeting size and risk thresholds re - presented to Investment Committee over 3 days ▪ Investment team morning meeting covers: ▪ Market movements ▪ Current pricing ▪ D eal pipeline ▪ N ews headlines ▪ O utstanding trades ▪ Automated flash reports sent to portfolio managers with detail on: ▪ M ajor market movers ▪ Ratings actions ▪ Credit default/CCC watch list changes ▪ Structured products team afternoon meeting covers: ▪ Market movements ▪ Portfolio rebalancing ▪ Meeting to discuss industry comparables ▪ Reviewing relative value ▪ Identifying new ideas ▪ Leadership update calls to review: ▪ Top movers ▪ New issuance ▪ Ratings actions ▪ Restructurings ▪ Amendments ▪ Portfolio positioning ▪ Sector rotation / risk management meetings to review: ▪ Economic / fundamental risk factors ▪ Credit market technical risk factors ▪ Portfolio risk positioning ▪ Sector rotation / industry weightings Comprehensive Approach to Risk Management: Monitoring 40 Daily Weekly Monthly Semi - Annually Ongoing

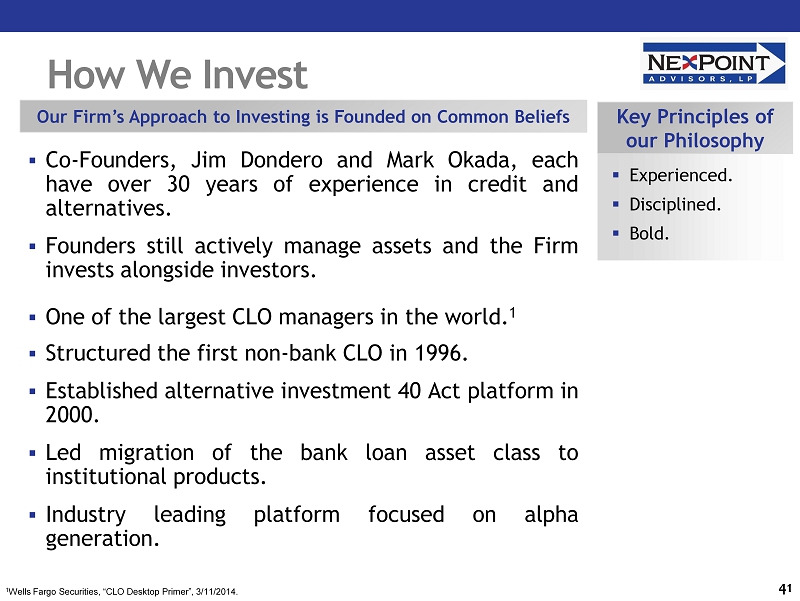

Our Firm’s Approach to Investing is Founded on Common Beliefs ▪ Experienced. ▪ Disciplined. ▪ Bold. Key Principles of our Philosophy 1 Wells Fargo Securities, “CLO Desktop Primer”, 3/11/2014. How We Invest ▪ Co - Founders, Jim Dondero and Mark Okada, each have over 30 years of experience in credit and alternatives . ▪ Founders still actively manage assets and the Firm invests alongside investors . ▪ One of the largest CLO managers in the world . 1 ▪ Structured the first non - bank CLO in 1996 . ▪ Established alternative investment 40 Act platform in 2000 . ▪ Led migration of the bank loan asset class to institutional products . ▪ Industry leading platform focused on alpha generation . 41

AGENDA Introduction and Executive Summary NexPoint’s Value Proposition for Stockholders Appendix I: Q&A Appendix II: NexPoint’s Capabilities Appendix III: NexPoint’s Board Nominees Important Information Contact Information 42

Meet the Nominees ▪ Dr . Bob Froehlich ▪ John Honis ▪ Timothy K . Hui ▪ William M . Swenson ▪ Ethan Powell ▪ Bryan A . Ward Additionally, If elected we expect to recommend engaging separate, premier legal counsel to advise the Board and TICC . 43

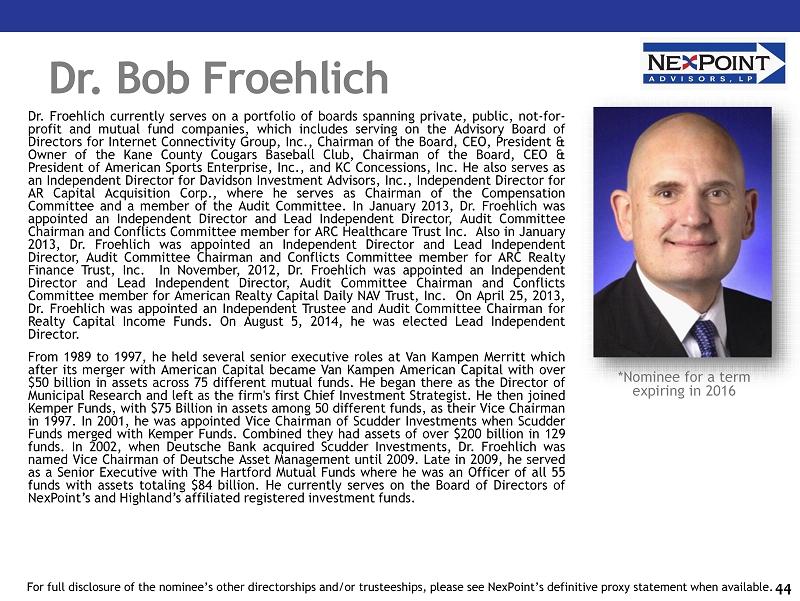

Dr . Bob Froehlich Dr . Froehlich currently serves on a portfolio of boards spanning private, public, not - for - profit and mutual fund companies, which includes serving on the Advisory Board of Directors for Internet Connectivity Group, Inc . , Chairman of the Board, CEO, President & Owner of the Kane County Cougars Baseball Club, Chairman of the Board, CEO & President of American Sports Enterprise, Inc . , and KC Concessions, Inc . He also serves as an Independent Director for Davidson Investment Advisors, Inc . , Independent Director for AR Capital Acquisition Corp . , where he serves as Chairman of the Compensation Committee and a member of the Audit Committee . In January 2013 , Dr . Froehlich was appointed an Independent Director and Lead Independent Director, Audit Committee Chairman and Conflicts Committee member for ARC Healthcare Trust Inc . Also in January 2013 , Dr . Froehlich was appointed an Independent Director and Lead Independent Director, Audit Committee Chairman and Conflicts Committee member for ARC Realty Finance Trust, Inc . In November, 2012 , Dr . Froehlich was appointed an Independent Director and Lead Independent Director, Audit Committee Chairman and Conflicts Committee member for American Realty Capital Daily NAV Trust, Inc . On April 25 , 2013 , Dr . Froehlich was appointed an Independent Trustee and Audit Committee Chairman for Realty Capital Income Funds . On August 5 , 2014 , he was elected Lead Independent Director . From 1989 to 1997 , he held several senior executive roles at Van Kampen Merritt which after its merger with American Capital became Van Kampen American Capital with over $ 50 billion in assets across 75 different mutual funds . He began there as the Director of Municipal Research and left as the firm's first Chief Investment Strategist . He then joined Kemper Funds, with $ 75 Billion in assets among 50 different funds, as their Vice Chairman in 1997 . In 2001 , he was appointed Vice Chairman of Scudder Investments when Scudder Funds merged with Kemper Funds . Combined they had assets of over $ 200 billion in 129 funds . In 2002 , when Deutsche Bank acquired Scudder Investments, Dr . Froehlich was named Vice Chairman of Deutsche Asset Management until 2009 . Late in 2009 , he served as a Senior Executive with The Hartford Mutual Funds where he was an Officer of all 55 funds with assets totaling $ 84 billion . He currently serves on the Board of Directors of NexPoint’s and Highland’s affiliated registered investment funds . 44 *Nominee for a term expiring in 2016 For full disclosure of the nominee’s other directorships and/or trusteeships, please see NexPoint’s definitive proxy statemen t w hen available.

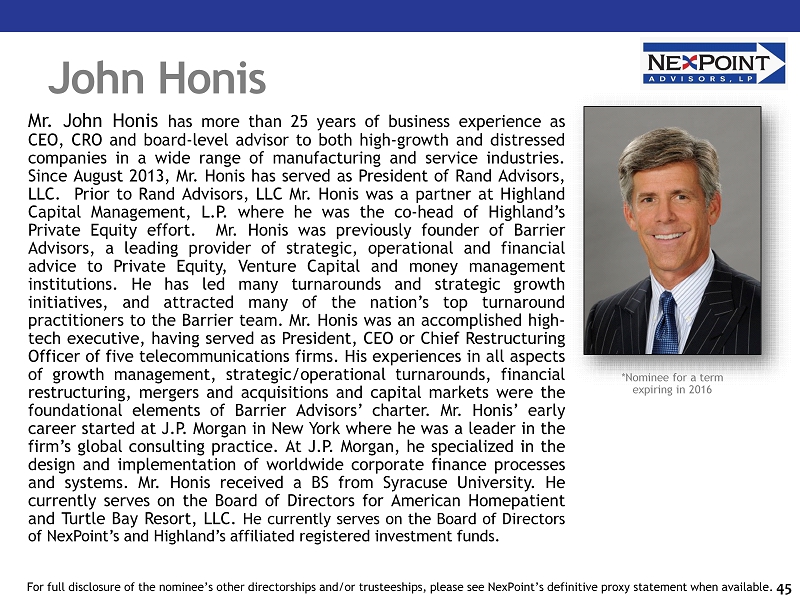

John Honis Mr . John Honis has more than 25 years of business experience as CEO, CRO and board - level advisor to both high - growth and distressed companies in a wide range of manufacturing and service industries . Since August 2013 , Mr . Honis has served as President of Rand Advisors, LLC . Prior to Rand Advisors, LLC Mr . Honis was a partner at Highland Capital Management, L . P . where he was the co - head of Highland’s Private Equity effort . Mr . Honis was previously founder of Barrier Advisors, a leading provider of strategic, operational and financial advice to Private Equity, Venture Capital and money management institutions . He has led many turnarounds and strategic growth initiatives, and attracted many of the nation’s top turnaround practitioners to the Barrier team . Mr . Honis was an accomplished high - tech executive, having served as President, CEO or Chief Restructuring Officer of five telecommunications firms . His experiences in all aspects of growth management, strategic/operational turnarounds, financial restructuring, mergers and acquisitions and capital markets were the foundational elements of Barrier Advisors’ charter . Mr . Honis’ early career started at J . P . Morgan in New York where he was a leader in the firm’s global consulting practice . At J . P . Morgan, he specialized in the design and implementation of worldwide corporate finance processes and systems . Mr . Honis received a BS from Syracuse University . He currently serves on the Board of Directors for American Homepatient and Turtle Bay Resort, LLC . He currently serves on the Board of Directors of NexPoint’s and Highland’s affiliated registered investment funds . 45 *Nominee for a term expiring in 2016 For full disclosure of the nominee’s other directorships and/or trusteeships, please see NexPoint’s definitive proxy statemen t w hen available.

Timothy K . Hui Mr . Timothy K . Hui has served as Dean of Educational Resources at at Cairn University (formerly, Philadelphia Biblical University) since July 2012 and also from July 2006 to January 2008 . Mr . Hui served as Vice President at Cairn University from February 2008 to June 2012 . He served as Associate Provost for Graduate Education at Cairn University from July 2004 to June 2006 . He served as Assistant Provost for Educational Resources of Cairn University from July 2001 to June 2004 . Mr . Hui served as the Managing Partner of the law firm of Hui & Malik L . L . P . He was in private practice as an attorney . He has been a Director of Learning Resources of the Cairn University since September 1998 . He has been an Independent Trustee of NexPoint Credit Strategies Fund since May 19 , 2006 . He served as a Director of Prospect Street Income Shares Inc . , since 2005 . He served as a Director of Prospect Street High Income Portfolio Inc . since January 2000 . Mr . Hui received a Bachelor of Science degree in Christian Education from Cairn University and received a Masters degree in Theology and a Doctorate degree in Theology from the Dallas Theological Seminary . He also received a Masters in Library Sciences from the University of North Texas and his Juris Doctor degree from Southern Methodist University . He currently serves on the Board of Directors of NexPoint’s and Highland’s affiliated registered investment funds . 46 *Nominee for a term expiring in 2017 For full disclosure of the nominee’s other directorships and/or trusteeships, please see NexPoint’s definitive proxy statemen t w hen available.

William M . Swenson Mr . Swenson has extensive experience raising debt and equity capital globally for middle market companies in various industries . Mr . Swenson’s experience spans Direct Lending, Debt Capital Markets (Loans, Bonds, Mezzanine and Private Debt), Origination, Portfolio and Credit Risk Management, Leveraged Finance and Structuring, Loan Syndications and Sales/Trading, Institutional Investor Relations and Venture Capital . Mr . Swenson currently serves as an advisor to an alternative energy producer and assists with project capital raises . Prior to this role, he served as a Managing Director at Canaccord Genuity from March 2014 to May 2015 . Mr . Swenson’s previous roles served included serving as Managing Director at North Sea Partners, LLC from February 2012 to March 2014 , Managing Director at Guggenheim Securities from January 2010 to January 2012 , Senior Managing Director – Head of Capital Markets and President of Broker Dealer at CIT from January 2004 to August 2007 , Managing Director - Global Head of Loan Sales and Trading at CIBC from August 1995 to August 2003 and Vice President of Leveraged Finance and Debt Capital Market at CitiBank from 1983 to 1992 . 47 *Nominee for a term expiring in 2017 For full disclosure of the nominee’s other directorships and/or trusteeships, please see NexPoint’s definitive proxy statemen t w hen available.

Ethan Powell Mr . Powell is Chief Product Strategist at NexPoint and Highland Capital Management Fund Advisors, L . P . In this role he is responsible for evaluating and optimizing the registered product lineup offered by Highland . Additionally, Mr . Powell works with portfolio managers and wholesalers on appropriate positioning of strategies in the market place . Prior to his current role, Mr . Powell was a senior fund analyst responsible for working with portfolio management teams and service providers in the operation and marketing of the funds . Prior to joining Highland in April 2007 , Mr . Powell spent most of his career with Ernst and Young providing audit and merger and acquisition services within the firm’s Transaction Advisory Services Group in Houston, Texas . Mr . Powell’s primary focus was acquisitions in the Energy industry . Mr . Powell received an MS in Management Information Systems and a BS in Accounting from Texas A&M University . Mr . Powell is a holder of the right to use the Chartered Financial Analyst designation and is a licensed Certified Public Accountant . He currently serves on the Board of Directors of NexPoint’s and Highland’s affiliated registered investment funds . 48 *Nominee for a term expiring in 2018 *Interested Person For full disclosure of the nominee’s other directorships and/or trusteeships, please see NexPoint’s definitive proxy statemen t w hen available.

Bryan A . Ward Mr . Ward currently focuses on private investments in the oil and gas, real estate and power generation sector . Prior to this from 2001 - 2014 he held various senior roles including Special Projects Advisor, Senior Manager and Information Technology consultant at Accenture primarily focused on the business development and delivery of innovative strategy, technology and business process solutions for clients across multiple industry segments . He interacted with C - Suite level clients at domestic and international Fortune Global 1000 enterprises as well as smaller independent and privately owned organizations . Before this role he served as a Senior Vice President and later Interim CEO of Anderson Consulting start - up entity, Quaris Inc . , from 1998 - 2000 . From 1991 - 1997 he was a Senior Manager at Anderson Consulting . He was a founding managing team member of Affiliated Computer Services (ACS) and served in this capacity from 1991 to 1998 . Mr . Ward previously worked in business development at MTech Corp and formerly at Petroleum Landman for ARCO Oil and Gas . He currently serves as a Board Member for EquityMetrix , LLC and is on the Advisory Board for the University of Texas Dallas Center for Brain Health . He currently serves on the Board of Directors of NexPoint’s and Highland’s affiliated registered investment funds . 49 *Nominee for a term expiring in 2018 For full disclosure of the nominee’s other directorships and/or trusteeships, please see NexPoint’s definitive proxy statemen t w hen available.

AGENDA Introduction and Executive Summary NexPoint’s Value Proposition for Stockholders Appendix I: Q&A Appendix II: NexPoint’s Capabilities Appendix III: NexPoint’s Board Nominees Important Information Contact Information 50

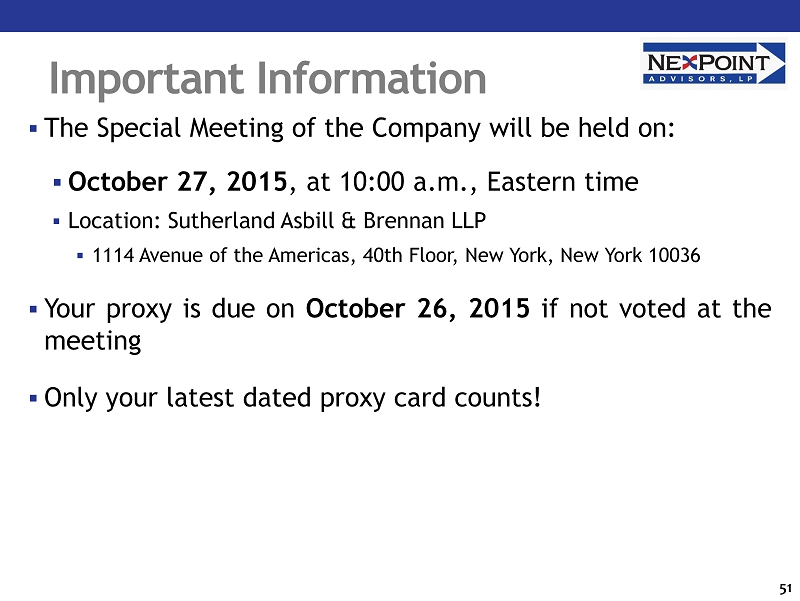

Important Information 51 ▪ The Special Meeting of the Company will be held on : ▪ October 27 , 2015 , at 10 : 00 a . m . , Eastern time ▪ Location : Sutherland Asbill & Brennan LLP ▪ 1114 Avenue of the Americas, 40 th Floor, New York, New York 10036 ▪ Your proxy is due on October 26 , 2015 if not voted at the meeting ▪ Only your latest dated proxy card counts!

AGENDA Introduction and Executive Summary NexPoint’s Value Proposition for Stockholders Appendix I: Q&A Appendix II: NexPoint’s Capabilities Appendix III: NexPoint’s Board Nominees Important Information Contact Information 52

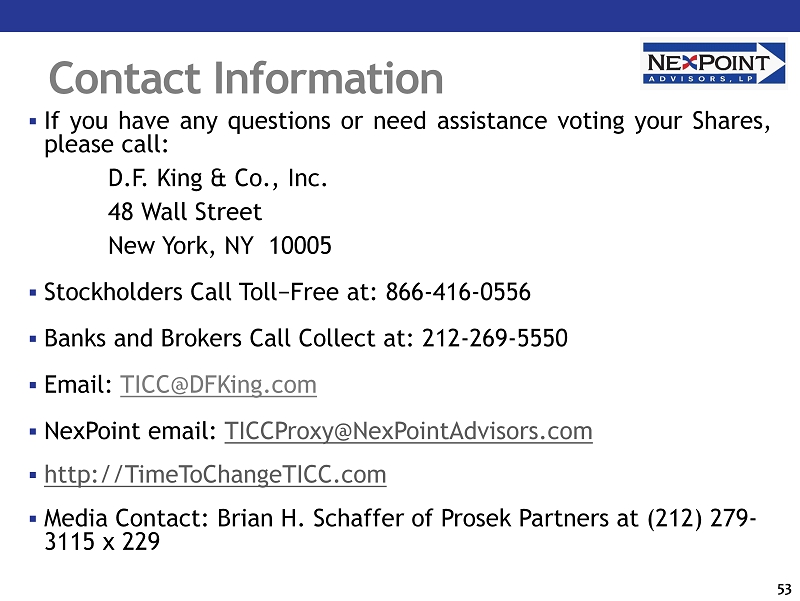

Contact Information ▪ If you have any questions or need assistance voting your Shares, please call : D.F . King & Co., Inc. 48 Wall Street New York, NY 10005 ▪ Stockholders Call Toll−Free at: 866 - 416 - 0556 ▪ Banks and Brokers Call Collect at: 212 - 269 - 5550 ▪ Email: TICC@DFKing.com ▪ NexPoint email: TICCProxy@NexPointAdvisors.com ▪ http://TimeToChangeTICC.com ▪ Media Contact: Brian H. Schaffer of Prosek Partners at (212 ) 279 - 3115 x 229 53

Thank you for your support NexPoint Advisors, L . P . 54

Disclosures and Disclaimers TSLX’s Incentive and Administrative Fee Structure . In addition to higher management fees, under TSLX’s incentive fee and administrative fee structure, stockholders would bear an additional approximately $ 10 - 14 million of incentive and administrative fees over the next 10 years beyond those under NexPoint’s proposal (estimated based on a 9 % - 20 % annual return and existing annual administrative expense reimbursements as a percentage of assets under management) . If the Company’s annual return were 8 % , 9 % , 14 % or 20 % , these estimated savings would be approximately $ 6 . 2 million, $ 10 million, $ 12 . 2 million or $ 13 . 7 million, respectively, each over 10 years . The estimated additional annual cost of administrative expense reimbursements under TSLX’s structure was calculated by determining the ratio of TSLX’s administrative expense reimbursements over the past 12 months to TSLX’s AUM as of June 30 , 2015 and applying that percentage to the Company’s AUM as of June 30 , 2015 . The Company’s actual administrative expense reimbursements over the past 12 months was then deducted from that amount to arrive at an estimate of the additional annual administrative expense reimbursements that would apply under the TSLX structure . That annual amount was then used to estimate such additional administrative expense reimbursements over the next 10 years . If the Company’s annual return over this period were less than 8 % - 20 % , these estimated savings would be lower . 55

Disclaimer About NexPoint Advisors, L.P. NexPoint , together with its affiliates, currently manages approximately $ 22 billion in net assets and believes that its core competences are squarely within the Company's investment strategy . NexPoint is indirectly wholly owned by a trust that is beneficially owned and controlled by James Dondero . Highland Capital Management, L . P . (" Highland ") is ultimately controlled by James Dondero and is therefore an affiliate of, and under common control with, NexPoint , which shares personnel and other resources with Highland . Highland (together with its affiliates) is one of the world's most experienced alternative credit managers, tested by numerous credit cycles, specializing in credit strategies, such as a broad range of leveraged loans, high yield bonds, direct lending, public and private equities and CLOs . Highland also offers alternative investment - oriented strategies, including asset allocation, long/short equities, real estate and natural resources . If NexPoint is retained by the Company as its investment adviser, the Company will have access to all of Highland's capabilities and expertise . Important Additional Information and Where to Find It NexPoint has filed a preliminary proxy statement with the U . S . Securities and Exchange Commission (the “ SEC ”) in connection with the solicitation of proxies from the stockholders of the Company in connection with the matters to be considered at the Company’s Special Meeting of Stockholders to be held on October 27 , 2015 , including the election of NexPoint’s nominees for director : Dr . Bob Froehlich, John Honis , Timothy K . Hui, Ethan Powell, William M . Swenson and Bryan A . Ward (collectively, the “ Nominees ”) . STOCKHOLDERS OF THE COMPANY ARE STRONGLY ENCOURAGED TO READ THE PROXY STATEMENT AND THE ACCOMPANYING PROXY CARD AND OTHER DOCUMENTS FILED BY NEXPOINT WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE AS THEY WILL CONTAIN IMPORTANT INFORMATION . When finalized, the proxy statement and proxy card will be mailed to all stockholders . The proxy statement and other relevant materials (when they become available), and any other documents filed by NexPoint with the SEC, may also be obtained free of charge at the SEC’s website at www . sec . gov . This is not the Company’s or TSLX’s proxy statement . If you have any questions, need free copies of the proxy statement or other relevant materials (when they become available, o r n eed assistance voting your Shares, please call: 56 D.F. King & Co., Inc. Stockholders 866 - 416 - 0556 Bank and Brokers 212 - 269 - 5550 TICC@dfking.com Media Contact Brian H. Schaffer Prosek Partners 212 - 279 - 3115 229 bschaffer@prosek.com

Disclaimer (cont’d) Participants in the Solicitation NexPoint and the Nominees are deemed to be participants in NexPoint’s solicitation of proxies from the Company’s stockholders in connection with the matters to be considered at the Company’s Special Meeting of Stockholders to be held on October 27 , 2015 . NexPoint is the beneficial owner of 100 shares of common stock of the Company and also proposes to become the Company’s investment adviser, for which it would receive advisory fees . Information regarding NexPoint and the Nominees, and their direct or indirect interests in the Company, by security holdings or otherwise, will be set forth in the proxy statement filed with the SEC by NexPoint . Third Party Information These materials may contain or refer to news, commentary and other information sourced from persons or companies that are not affiliated with NexPoint . The author and source of any third party information and the date of its publication are clearly and prominently identified . NexPoint has neither sought nor obtained permission to use or quote such third party information . NexPoint cannot guarantee the accuracy, timeliness, completeness or availability of such third party information, and does not explicitly or implicitly endorse or approve such third party information . NexPoint, the Nominees and their affiliates shall not be responsible or have any liability for any misinformation or inaccuracy in such third party information . NexPoint reserves the right to change any of its opinions expressed herein at any time as it deems appropriate and disclaims any obligation to notify the market or any other party of any such changes . NexPoint disclaims any obligation to update the information or opinions contained herein . These materials are provided for information purposes only, and are not intended to be, nor should they be construed as, an offer to sell or the solicitation of an offer to buy any security . These materials do not recommend the purchase or sale of any security . 57

Disclaimer (cont’d) NexPoint and its respective affiliates do not assume responsibility for investment decisions . This presentation does not recommend the purchase or sale of any security . Under no circumstances is this presentation to be used or considered as an offer to sell or a solicitation of an offer to buy any security . This document includes certain forward - looking statements, estimates and projections prepared with respect to, among other things, general economic and market conditions, changes in management, changes in the composition of the Company’s board, actions of the Company and its subsidiaries or competitors and the ability to implement business strategies and plans and pursue business opportunities . Such forward - looking statements, estimates and projections reflect various assumptions concerning anticipated results that are inherently subject to significant uncertainties and contingencies and have been included solely for illustrative purposes, including those risks and uncertainties detailed in the continuous disclosure and other filings of the Company, copies of which are available on the SEC’s website at www . sec . gov . No representations, express or implied, are made as to the accuracy of completeness of such forward - looking statements, estimates or projections or with respect to any other materials herein . NexPoint reserves the right to change any of the opinions expressed herein at any time as they deem appropriate . NexPoint and its respective affiliates may buy, sell, cover or otherwise change the form of their investment in the Company for any reason at any time, without notice . NexPoint disclaims any duty to provide any updates or changes to the analyses contained in this document, except as may be required by law . NexPoint disclaims any obligation to update the information contained herein . NexPoint has not sought or obtained consent from any third party to use any statements or information indicated in this presentation as having been obtained or derived from statements made or published by third parties . Any such statements or information should not be viewed as indicating the support of such third party for the views expressed herein . 58

Disclaimer (cont’d) NexPoint may have relied upon certain quantitative and qualitative assumptions when preparing the analysis which may not be articulated as part of the analysis . The realization of the assumptions on which the analysis was based are subject to significant uncertainties, variables, and contingencies and may change materially in response to small changes in the elements that comprise the assumptions, including the interaction of such elements . Furthermore, the assumptions on which the analysis was based may be necessarily arbitrary, may be made as of the date of the analysis, do not necessarily reflect historical experience with respect to securities similar to those that may be contained in the analysis, and do not constitute a precise prediction as to future events . Because of the uncertainties and subjective judgments inherent in selecting the assumptions on which the analysis was based and because future events and circumstances cannot be predicted, the actual results realized may differ materially from those projected in the analysis . The information that is contained in the analysis should not be construed as financial, legal, investment, tax, or other advice . You ultimately must rely upon your own examination and that of your professional advisors, including legal counsel and accountants as to the legal, economic, tax, regulatory, or accounting treatment, suitability, and other aspects of the analysis . NexPoint asks that you refrain from sending this document to any other party under any circumstances . 59