Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant ¨ Filed by a party other than the Registrant x

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| x | Definitive Additional Materials | |

| ¨ | Soliciting Material Under Rule 14a-12 | |

ASHFORD HOSPITALITY PRIME, INC.

(Name of the Registrant as Specified In Its Charter)

SESSA CAPITAL (MASTER), L.P.

SESSA CAPITAL GP, LLC

SESSA CAPITAL IM, L.P.

SESSA CAPITAL IM GP, LLC

JOHN E. PETRY

LAWRENCE A. CUNNINGHAM

PHILIP B. LIVINGSTON

DANIEL B. SILVERS

CHRIS D. WHEELER

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount previously paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing party:

| |||

| (4) | Date Filed:

| |||

On February 26, 2016, Sessa Capital (Master), L.P. posted the following materials to http://FixAshfordPrime.com:

Table of Contents

TO VOTE

On February 26, 2016, Sessa Capital (Master), LP. (“Sessa Capital”) and the other Participants (as defined below) filed with the Securities and Exchange Commission (the “SEC”) a proxy statement and an accompanying WHITE proxy card to be used to solicit proxies for, among other matters, the election of its slate of director nominees at the 2016 annual shareholders meeting of Ashford Hospitality Prime, Inc. (“AHP”). The participants in the proxy solicitation include Sessa Capital, Sessa Capital GP, LLC, Sessa Capital IM, L.P., Sessa Capital IM GP, LLC, John E. Petry, Lawrence A. Cunningham, Philip B. Livingston, Daniel B. Silvers, and Chris D. Wheeler (collectively, the “Participants”).

This website includes news and information, commentary, and other content relating to AHP by the Participants, and may include such content by persons not affiliated with the Participants (“Third Party Content”), through links to third party websites including the SEC, or as published on the site. In addition, any financial projections and statements included on this site may be derived from SEC filings and other reports by third parties not affiliated with the Participants. Neither the Participants nor their affiliates shall be responsible or have any liability for any misinformation contained in any third party filing or report or any Third Party Content. Although Sessa Capital believes that the statements included on this site are substantially accurate in all material respects, Sessa Capital makes no representation or warranty, express or implied, as to the accuracy or completeness of such statements, and expressly disclaims any liability relating to such statements. Sessa Capital disclaims any obligation to update the information, commentary and other content contained on this website.

Caution Regarding Forward-Looking Statements

This website may contain “forward-looking statements.” All statements contained herein that are not clearly historical in nature or that necessarily depend on future events are forward-looking; the words “may,” “will,” “could,” “expect” “anticipate,” “believe,” “estimate,” “plan,” “intend” and similar expressions generally identify forward-looking statements. These forward-looking statements are based on current views with respect to future events and financial performance. Actual results could differ materially from those projected in such forward-looking statements. These forward-looking statements arc subject to risks, uncertainties and assumptions, including, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of Sessa Capital.

You should not put undue reliance on any forward-looking statements. You should understand that many important factors, including those discussed or referred to on the site, could cause results to differ materially from those expressed or suggested in any forward- looking statement. In light of the significant uncertainties inherent in the projected results and forward-looking statements included herein, the inclusion of such information should not be regarded as a representation as to future results or that the objectives and strategic initiatives expressed or implied by such projected results and forward-looking statements will be achieved. Except as required by law, neither the Participants nor any of their affiliates undertakes any obligation to disclose the results of any revisions that may be made to these forward-looking statements to reflect new information or events or circumstances that occur after the date of such projected results or statements or to reflect the occurrence of unanticipated events or otherwise.

Additional Information

Sessa Capital strongly advises all stockholders of AHP to read Sessa Capitals proxy statement and any other proxy materials relating to the Participants’ solicitation because they contain important information including information about the Participants. Such proxy materials are available at no charge on the SEC’s web site at http://www.sec.gov. In addition, the Participants in this proxy solicitation will provide copies of the proxy statement without charge upon request. Requests for copies should be directed to the Participants’ proxy solicitor, Innisfree M&A Incorporated at (888) 750-5834.

I confirm that I have read the above information.

Agree »

©2016

Table of Contents

Sessa Capital PRESS RELEASES PRESENTATIONS SEC FILINGS OTHER IMPORTANT DOCUMENTS NOMINEES HOW TO VOTE

WELCOME TO FiXASHFORDPRIME.COM

Thank you for visiting FixAshfordPrime.com. As one of the largest shareholders of Ashford Hospitality Prime, Inc. (NYSE:

AHP) (“Ashford Prime” or the “Company”), we are deeply concerned by the Company’s poor financial performance, the alarming pattern of conflict-of-interest transactions approved by the incumbent Board – and specifically Ashford Prime’s Chairman and Chief Executive Monty J. Bennett – and seemingly stalled strategic review process. As a result, we believe change Is needed immediately at the Board level.

In our view, reconstituting Ashford Prime’s Board with our five highly-qualified independent directors is the only way for shareholders to protect the value of their investment and the only chance for a successful, fair and transparent strategic alternatives process.

Your vote at Ashford Prime’s 2016 Annual Meeting is important! It will determine the future of the Company and directly impact the value of your investment. We ask for your support – by voting the WHITE proxy card – so that we can address the significant corporate governance deficiencies at the Company and get the strategic review process on track.

This website contains important information about Ashford Prime’s upcoming Annual Meeting, including how to vote your shares, press releases, letters to shareholders, biographies of our nominees and our proxy statement, so you can make an informed decision about the future of your investment.

We urge you to view the materials contained on this site carefully and to check back often for frequent updates.

We thank you for your support.

© 2016 Sessa Capital, LLC | Contact Us

Table of Contents

Sessa Capital PRESS RELEASES PRESENTATIONS SEC FILINGS OTHER IMPORTANT DOCUMENTS NOMINEES HOW TO VOTE

PRESS RELEASES

February 26, 2016 - Sessa Capital Files Definitive Proxy Materials Related To Ashford Prime

February 17, 2016 - Sessa Capital Believes Ashford Hospitality Prime’s Dilutive Penny Preferred Share Issuance Will Violate NYSE Regulations

February 3, 2016 - Sessa Capital Files Lawsuit Against Ashford Hospitality Prime Over Change in Control Provision

February 2, 2016 - Sessa Capital Comments on Ashford Hospitality Prime’s Sale of 13.3% Voting Rights for $43,750

January 15, 2016 - Sessa Capital Nominates Control Slate of Five Highly Qualified Director Candidates

© 2016 Sessa Capital, LLC | Contact Us

Table of Contents

Sessa Capital PRESS RELEASES PRESENTATIONS SEC FILINGS OTHER IMPORTANT DOCUMENTS NOMINEES HOW TO VOTE

PRESENTATIONS

Please check back later for future updates.

© 2016 Sessa Capital, LLC | Contact Us

Table of Contents

Sessa Capital PRESS RELEASES PRESENTATIONS SEC FILINGS OTHER IMPORTANT DOCUMENTS NOMINEES HOW TO VOTE

SEC FILINGS

February 26, 2016 - DEFC14A

February 17, 2016 - SC 13D/A

February 17, 2016 - DFAN14A

February 12, 2016 - PREC14A

February 4, 2016 - SC 13D/A

February 4, 2016 - DFAN14A

February 2, 2016 - DFAN14A

January 15, 2016 - C 13D/A

January 15, 2016 - DFAN14A

January 8, 2016 - SC 13D/A

December 11, 2015 - SC 13D/A

September 2, 2015 - SC 13D

© 2016 Sessa Capital, LLC | Contact Us

Table of Contents

Sessa Capital PRESS RELEASES PRESENTATIONS SEC FILINGS OTHER IMPORTANT DOCUMENTS NOMINEES HOW TO VOTE

OTHER IMPORTANT DOCUMENTS

February 17, 2016 - Memorandum of Law in Support of Motion for Preliminary Injunction

February 10, 2016 - Letter Sent to NYSE Regarding Potential Violations of NYSE Rules by Ashford Prime

February 3, 2016 - Complaint Filed in the Circuit Court for Baltimore City, Maryland Regarding Invalid Proxy Penalty

January 7, 2016 - Letter from John Petry to Ashford Prime Lead Director Curtis B. McWilliams and Director W. Michael Murphy

December 10, 2015 - Letter from John Petry to the Board of Directors of Ashford Prime

September 1, 2015 - Letter from John Petry to the Board of Directors of Ashford Prime

© 2016 Sessa Capital, LLC | Contact Us

Table of Contents

Sessa Capital PRESS RELEASES PRESENTATIONS SEC FILINGS OTHER IMPORTANT DOCUMENTS NOMINEES HOW TO VOTE

DIRECTOR NOMINEES

Lawrence A. Cunningham

Lawrence A. Cunningham is an expert on corporate governance and related matters, having published over forty related research articles, as well as dozens of other works on matters of corporate governance in such periodicals as Directors & Boards. The New York Times, and The Wall Street Journal. He is the Henry St. George Tucker III Research Professor at The George Washington University Law School in Washington D.C. and Executive Board Member of the University’s Center for Law, Economics and Finance (C-LEAF), and the Director of C-LEAF in New York. Previously, Mr. Cunningham served as Associate Dean of Boston College Law School and Director of the Samuel and Ronnie Heyman Center on Corporate Governance at Cardozo School of Law in New York City. Consulting assignments have included corporate governance matters for companies such as Bacardi, Charter Communications, and the Securities Investor Protection Corporation. Prior to his twenty years of writing and teaching, Mr. Cunningham served as of counsel for Roberts, Sheridan & Kotel for seven years and practiced corporate law with Cravath, Swaine & Moore for six years, engaging in the areas of governance, securities, and mergers and acquisitions in both roles. Mr. Cunningham has also authored a number of books, including The Essays of Warren Buffett: Lessons for Corporate America, in collaboration with Warren Buffett. He is a Member of the Dean’s Council of Lemer College of Business of the University of Delaware and a recent nominee to the Editorial Board of the Museum of Financial History in New York. Mr. Cunningham received a Bachelor’s degree in economics from the University of Delaware and a J.D. from Cardozo School of Law in New York City.

Philip B. Livingston

Philip Livingston has significant public and private company board experience having served as a director for Broadsoft Corporation, Insurance Auto Auction, Cott Corporation, MSC Software and Seitel Inc. He is currently a director of SITO Mobile and Rand Worldwide Inc. and most recently served as Chief Executive Officer and a director of Ambassadors Group, a provider of People To People educational travel services from May 2014 to October 2015. Prior to joining Ambassadors Group, he was Chief Executive Officer of LexisNexis Web Based Marketing Solutions until October 2013. Previously, Mr. Livingston served as Chief Financial Officer for Celestial Seasonings, Inc., Catalina Marketing Corporation and World Wrestling Entertainment From 1999 to 2003 he served as President of Financial Executives International, the leading professional association of chief financial officers and controllers. In that role he led the organization’s support of regulatory and corporate governance reforms culminating in the Sarbanes-Oxley Act. Mr. Livingston earned a BA in Business Management and a BS in Government and Politics from the University of Maryland and a MBA in Finance and Accounting from the University of California, Berkeley.

John E. Petry

John Petry founded Sessa Capital in November 2012 and is the sole portfolio manager responsible for portfolio management, risk management, and overseeing research. Prior to launching Sessa Capital, Mr. Petry was a Principal at Columbus Hill Capital Management from November 2010 to February 2012, an opportunistic credit hedge fund that focused on distressed investing. Previously, he was a Partner at Gotham Capital from 1997 to October 2010, where he employed a value-based approach to investing. During that time, Mr. Petry managed hedge fund Sissa Capital. Prior to Gotham Capital, he was an Analyst at Opus Capital, a value-oriented hedge fund, from 1995 to 1997 and an Associate at Conning and Company from 1993 to 1995. Mr. Petry graduated from University of Pennsylvania, Wharton School, with a B.S in Economics in 1993.

Table of Contents

Daniel B. Silvers

Daniel B. Silvers brings significant operational and investing experience in the hospitality sector. He is the Founder and Managing Member of Matthews Lane Capital Partners LLC. He currently serves on the boards of directors of Forestar Group Inc. and India Hospitality Corp. He has previously served on the boards of directors of International Game Technology. Universal Health Services, Inc. and bwin.party digital entertainment plc, as well as serving as President of Western Liberty Bancorp. an acquisition-oriented company which bought and recapitalized Service1st Bank of Nevada, a community bank in Las Vegas, NV. In 2015, Mr. Silvers was featured in the National Association of Corporate Directors’ “A New Generation of Board Leadership: Directors Under Age 40” list of emerging corporate directors. Prior to founding Matthews Lane, Mr. Silvers was the President of SpringOwl Asset Management LLC, having joined a predecessor entity in 2009. Previously, Mr. Silvers was a Vice President at Fortress Investment Group, a leading global alternative asset manager, where he worked from 2005 to 2009. Prior to joining Fortress, he was a senior member of the real estate, gaming and lodging investment banking group at Bear, Stearns & Co. Inc., where he worked from 1999 to 2005. Mr. Silvers holds a B.S. in Economics and an M.B.A. in Finance from The Wharton School of the University of Pennsylvania. He has also received a Corporate Governance certification through the Director Education & Certification Program at the UCLA Anderson School of Management. Mr. Silvers is active in a number of not-for-profits, including Horace Mann School, University of Pennsylvania and UJA-Federation of New York.

Chris D. Wheeler

Chris D. Wheeler has over thirty-five years of experience in real estate M&A development, management and financing. He is the former Chairman and Chief Executive Officer of Gables Residential Trust, a publicly-traded multifamily REIT, which was sold to ING Clarion in 2005 for $2.8 billion. Most recently, Mr. Wheeler served as a senior real estate advisor to the CEO of a family office and to the senior executives of a Fortune 50 company. Previously, Mr. Wheeler worked at Trammell Crow in a number of roles, most recently as Group Managing Partner for Trammell Crow Residential where he oversaw its multifamily residential operations throughout the Southeast, Mid-Atlantic and Northeast regions. He formerly served as Director on the Executive Committee of the National Multi Housing Council (NMHC) and on the Board of Governors for the National Association of Real Estate Investment Trusts (NAREIT). Mr. Wheeler graduated with honors from California Institute of Technology with a degree in applied physics and received an MBA from Harvard Business School.

© 2016 Sessa Capital, LLC | Contact Us

Table of Contents

Sessa Capital PRESS RELEASES PRESENTATIONS SEC FILINGS OTHER IMPORTANT DOCUMENTS NOMINEES HOW TO VOTE

HOW TO VOTE

Please sign and date the WHITE proxy card supplied by Sessa Capital and return it in the enclosed postage-paid envelope whether or not you attend the meeting. The Proxy Statement is first being sent or given to stockholders on or about February 26, 2016.

If your shares are held in the name of a brokerage firm, bank or other custodian on the Record Date, only that firm can vote those shares and, with respect to the election of directors, only upon receipt of your specific instructions. Accordingly, we urge you to contact the person responsible for your account and instruct that person to sign and return on your behalf the WHITE proxy card as soon as possible.

YOUR VOTE IS IMPORTANT. If you agree with the reasons for Sessa Capital’s solicitation set forth in the Proxy Statement and believe that the election of our Nominees to the Board of Directors (the “Board”) of Ashford Prime can make a difference, please vote for the election of our Nominees, no matter how many or how few shares you own.

WE URGE YOU NOT TO SIGN ANY PROXY CARD SENT TO YOU BY THE COMPANY. IF YOU HAVE ALREADY DONE SO, YOU MAY REVOKE YOUR PREVIOUSLY SIGNED PROXY BY SIGNING AND RETURNING A LATER-DATED WHITE PROXY CARD IN THE ENCLOSED POSTAGE-PAID ENVELOPE, BY DELIVERING A WRITTEN NOTICE OF REVOCATION TO SESSA CAPITAL OR TO THE SECRETARY OF THE COMPANY, OR BY INSTRUCTING US BY TELEPHONE OR VIA THE INTERNET AS TO HOW YOU WOULD LIKE YOUR SHARES VOTED (INSTRUCTIONS ARE ON YOUR WHITE PROXY CARD).

Thank you for your support.

On behalf of Sessa Capital,

John E. Petry

IF YOU HAVE ANY QUESTIONS, REQUIRE ASSISTANCE IN VOTING THE WHITE PROXY CARD, OR NEED ADDITIONAL COPIES OF OUR PROXY MATERIALS, PLEASE CONTACT OUR PROXY SOLICITOR AT THE PHONE NUMBER LISTED BELOW:

Innisfree M&A Incorporated

501 Madison Avenue, 20th Floor

New York, NY 10022

Stockholders call toll-free: (888) 750-5834

Banks and brokers call collect: (212) 750-5833

© 2016 Sessa Capital, LLC | Contact Us

Table of Contents

Sessa Capital PRESS RELEASES PRESENTATIONS SEC FILINGS OTHER IMPORTANT DOCUMENTS NOMINEES HOW TO VOTE

CONTACT

IF YOU HAVE ANY QUESTIONS, REQUIRE ASSISTANCE IN VOTING THE WHITE PROXY CARD, OR NEED ADDITIONAL COPIES OF OUR PROXY MATERIALS, PLEASE CONTACT OUR PROXY SOLICITOR AT THE PHONE NUMBER LISTED BELOW:

Scott Winter/Jonathan Salzberger

Innisfree M&A Incorporated

501 Madison Avenue, 20th Floor

New York, NY 10022

(212) 750-5833

Stockholders call toll-free: (888) 750-5834

Media Contacts:

Sard Verbinnen & Co

Dan Gagnier / Mark Harnett

212.687.8080

Daniel Goldstein

310.201.2040

© 2016 Sessa Capital, LLC | Contact Us

Table of Contents

SESSA CAPITAL FILES DEFINITIVE PROXY MATERIALS RELATED

TO ASHFORD PRIME

Highlights Ashford Prime’s Corporate Governance Deficiencies, Track Record of

Poor Financial Performance, and Need for aReconstituted Board

Urges Shareholders to Support Sessa’s Five Highly-Qualified Director Nominees

at 2016 Annual Meeting

New York – February 26, 2016 – Sessa Capital (Master), L.P. (“Sessa”), the third largest shareholder of Ashford Hospitality Prime, Inc. (NYSE: AHP) (“Ashford Prime” or the “Company”), today announced that it filed definitive proxy materials with the Securities and Exchange Commission in connection with Sessa’s five nominees for election to Ashford Prime’s seven member Board of Directors at the Company’s upcoming 2016 Annual Meeting of Stockholders.

Sessa believes change is needed at the Company’s Board of Directors given the poor performance of Ashford Prime’s stock and the Company’s pattern of conflict-of-interest transactions. In the filing, Sessa highlights the following:

| • | The serious conflicts of interest between Ashford Prime and Ashford Inc., its external manager, whose compensation is driven by asset growth and whose interests may not be aligned with Ashford Prime’s; |

| • | Ashford Prime’s attempt to place disproportionate control of the Company in the hands of its Chairman and CEO, Monty Bennett; |

| • | The Company’s potential payment of a large fee if directors not approved by the incumbent board are elected; |

| • | The potential grant to Chairman Bennett and other insiders of more voting power in the upcoming director election; |

| • | The Company’s seemingly stalled strategic review process, which Sessa believes has been impaired by the conflicts of interest; |

| • | The need for change at the board level and increased management oversight; and |

| • | The strength of Sessa’s proposed slate of nominees, which possesses the significant expertise, capital markets experience and operating acumen necessary to complete the strategic review and/or manage the Company’s operations. |

John Petry, Founder and Managing Partner of Sessa Capital stated, “As one of the largest shareholders in Ashford Prime, we are aligned with other shareholders and feel a duty to advocate for change at the Company. The market has judged Ashford Prime’s actions, under the control of Chairman & CEO Monty Bennett, as value destroying by punishing its stock price with a nearly 50% decline since the Company’s stock began trading just over two years ago. Among these actions were a number of conflict-of-interest transactions that we believe reflect poor corporate governance. Additionally, since the August 28, 2015 announcement of the strategic review process, the Company has demonstrated no meaningful progress.”

Table of Contents

Petry added: “In our view, reconstituting Ashford Prime’s Board with highly-qualified directors independent of Chairman Bennett is the only way for shareholders to protect the value of their investment and the only chance for a successful, fair and transparent strategic alternatives process. If elected, our slate would immediately pursue all options for renegotiating the Company’s onerous termination fee with its external advisor, addressing the potential conflicts of interest, pursuing the strategic review process and seeking to realize full value for Ashford Prime common shareholders.”

Sessa urges shareholders tovotethe WHITE proxy card for its five board nominees, whoare not beholdento Chairman Bennett and will represent the interests of all Ashford Prime shareholders.

Sessa’s nominees include:

| • | Lawrence A. Cunningham, Henry St. George Tucker III Research Professor at The George Washington University Law School in Washington D.C.; |

| • | Philip B. Livingston, who has extensive experience as a director, chief executive officer and chief financial officer of public companies; |

| • | John E. Petry, Founder and Managing Partner of Sessa Capital; |

| • | Daniel B. Silvers, Founder and Managing Member of Matthews Lane Capital Partners LLC, director of Forestar Group Inc. and India Hospitality Corp. and former senior member of the real estate, gaming and lodging investment banking group at Bear, Stearns & Co. Inc.; and |

| • | Chris D. Wheeler, partner at Triton Atlantic Partners, LLC, a real estate development and management company specializing in acquiring, developing and managing residential, resort, multi-family and commercial projects, and former chairman and chief executive officer of Gables Residential Trust. |

For additional details and materials, please visit FixAshfordPrime.com.

ADDITIONAL INFORMATION AND WHERE TO FIND IT

Sessa Capital (Master), L.P. (“Sessa Capital”) and the other Participants (as defined below) filed with the Securities and Exchange Commission (the “SEC”) a definitive proxy statement and an accompanying WHITE proxy card to be used to solicit proxies for, among other matters, the election of its slate of director nominees at the 2016 annual shareholders meeting of Ashford Hospitality Prime, Inc. (“AHP”). The participants in the proxy solicitation include Sessa Capital, Sessa Capital GP, LLC, Sessa Capital IM, L.P., Sessa Capital IM GP, LLC, John E. Petry, Lawrence A. Cunningham, Philip B. Livingston, Daniel B. Silvers, and Chris D. Wheeler (collectively, the “Participants”).

SESSA CAPITAL STRONGLY ADVISES ALL STOCKHOLDERS OF AHP TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS RELATING TO THE PARTICIPANTS’ SOLICITATION BECAUSE THEY CONTAIN IMPORTANT INFORMATION INCLUDING INFORMATION ABOUT THE PARTICIPANTS. SUCH PROXY MATERIALS ARE AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS’ PROXY SOLICITOR, INNISFREE M&A INCORPORATED AT (888) 750-5834.

Media Contacts:

Sard Verbinnen & Co

Dan Gagnier / Mark Harnett

212.687.8080

Daniel Goldstein

310.201.2040

Table of Contents

Investor Contacts:

Innisfree M&A Incorporated

Scott Winter / Jonathan Salzberger

212.750.5833

Table of Contents

SESSA CAPITAL BELIEVES ASHFORD HOSPITALITY PRIME’S DILUTIVE PENNY

PREFERRED SHARE ISSUANCE WILL VIOLATE NYSE REGULATIONS

Sends Letter to NYSE Claiming Intended AHP Actions Violate

NYSE Listing Obligations

Maryland Litigation Regarding AHP Termination Fee Structure Ongoing

New York – February 17, 2016 – Sessa Capital (Master), L.P. (“Sessa”), owner of 8.2% of the outstanding common shares of Ashford Hospitality Prime, Inc. (NYSE: AHP) (“Ashford Prime” or the “Company”) and Ashford Prime’s third largest shareholder, today disclosed that it sent a letter to the New York Stock Exchange (“NYSE”) protesting potential violations of the NYSE’s rules by Ashford Prime.

On February 1, 2016, Ashford Prime’s Board of Directors agreed to sell up to 13.3% of the Company’s voting interests, in the form of preferred stock sold for a penny a share, or a total of $43,750 (the “Penny Preferred”), to a group consisting primarily of Company management. Based on the most recent information Ashford Prime has made available, if the Penny Preferred is ultimately issued, more than half will be offered to Ashford Prime’s Chairman and CEO, Monty Bennett, and his father, the former Chairman of Ashford Hospitality Trust. Almost another 25% of the Penny Preferred will be offered to other members of Ashford Prime management.

In the letter to the NYSE, Sessa outlines its belief that the Penny Preferred violates sections 313.00(A), 312.02(b) and 303(A).08 of the NYSE rules, pertaining to the reduction of voting rights of common shareholders and requiring shareholder approval for certain stock issuances to insiders. These rules are meant to protect shareholders’ rights. Sessa seeks to protect Ashford Prime stockholders by heading off any action that could place Ashford Prime in non-compliance with NYSE rules and risk a delisting.

John Petry, Founder and Managing Partner of Sessa Capital stated, “We believe that Ashford Prime’s issuance of the Penny Preferred makes a mockery of NYSE rules designed to protect the rights of all shareholders, is directly contrary to existing shareholders’ interests, and is inconsistent with both NYSE rules and the fiduciary duties of the Company’s Board. If Ashford Prime issues the dilutive Penny Preferred, these protections to investors in NYSE-listed securities will be rendered almost meaningless and a dangerous precedent will be set for shareholders in all companies, not just those engaged in a contested board election. We have great respect for the NYSE’s hard work to ensure that its listed companies treat shareholders fairly; however, Chairman Bennett’s Penny Preferred threatens to undermine those efforts by tarnishing the reputation that has made the NYSE a leading global stock exchange.”

Petry concluded, “The Penny Preferred is the latest in a series of moves by Ashford Prime’s Board designed to disadvantage shareholders and to benefit insiders. We remain committed to defending our rights and the rights of all Ashford Prime shareholders and in furtherance of that goal will seek the election of our slate of five highly-qualified directors at the Company’s 2016 annual meeting of stockholders.”

1

Table of Contents

As previously disclosed, on February 3, 2015, Sessa filed a lawsuit in the Circuit Court for Baltimore City, Maryland, against Ashford Prime seeking a ruling that the Company’s directors breached their fiduciary duties by inserting a change-in-control provision pertaining to shareholder elections into the Company’s advisory agreement with its external adviser, Ashford Inc., an entity for which Chairman Bennett also serves as Chairman and CEO. The provision imposes an outsized termination fee on the Company if shareholders elect a majority of directors not approved by the incumbent directors and thereafter Ashford Inc. elects to collect the fee. The litigation is ongoing.

ADDITIONAL INFORMATION AND WHERE TO FIND IT

Sessa Capital (Master), L.P. (“Sessa Capital”) and the other Participants (as defined below) have made a preliminary filing with the Securities and Exchange Commission (the “SEC”) of a proxy statement and accompanying WHITE proxy card to be used to solicit proxies for, among other matters, the election of its slate of director nominees at the 2016 annual shareholders meeting of Ashford Hospitality Prime, Inc. (“AHP”). The participants in the proxy solicitation are anticipated to be Sessa Capital, Sessa Capital GP, LLC, Sessa Capital IM, L.P., Sessa Capital IM GP, LLC, John E. Petry, Lawrence A. Cunningham, Philip B. Livingston, Daniel B. Silvers, and Chris D. Wheeler (collectively, the “Participants”).

SESSA CAPITAL STRONGLY ADVISES ALL STOCKHOLDERS OF AHP TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE, WHEN AVAILABLE, UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO THE PARTICIPANTS’ PROXY SOLICITOR.

As of the date of this release, Sessa Capital owned directly 2,330,726 shares of common stock, $0.01 par value (the “Common Stock”), of AHP and Philip B. Livingston owned 4,000 shares of Common Stock.

Sessa Capital GP, LLC, as a result of being the sole general partner of Sessa Capital, Sessa Capital IM, L.P., as a result of being the investment adviser for Sessa Capital, Sessa Capital IM GP, LLC, as a result of being the sole general partner of Sessa Capital IM, L.P., and John Petry, as a result of being the manager of Sessa Capital GP, LLC and Sessa Capital IM GP, LLC, may be deemed to be the beneficial owner of Common Stock owned directly by Sessa Capital.

Media Contacts:

Sard Verbinnen & Co

Dan Gagnier / Mark Harnett

212.687.8080

Daniel Goldstein

310.201.2040

Investor Contacts:

Innisfree M&A Incorporated

Scott Winter / Jonathan Salzberger

212.750.5833

2

Table of Contents

SESSA CAPITAL FILES LAWSUIT AGAINST ASHFORD HOSPITALITY PRIME OVER

CHANGE IN CONTROL PROVISION

Claims “Proxy Penalty” Breaches Fiduciary Duty and Threatens to Penalize Shareholders

for Electing Non-Incumbent Directors

Highlights Growing Number of Corporate Governance Issues at Ashford Prime

Remains Committed to Nominating Control Slate of Five Highly Qualified Directors

at 2016 Annual Meeting

New York – February 3, 2016 – Sessa Capital (Master), L.P. (“Sessa”), owner of 8.2% of the outstanding common shares of Ashford Hospitality Prime, Inc. (NYSE: AHP) (“Ashford Prime” or the “Company”) and Ashford Prime’s third largest shareholder, today announced it has filed a lawsuit in the Circuit Court for Baltimore City, Maryland, against the Company. The suit seeks a ruling that the directors of Ashford Prime breached their fiduciary duties by inserting a change-in-control provision pertaining to shareholder elections (the “Proxy Penalty”) into the Company’s advisory agreement with the Company’s external adviser, Ashford Inc., an entity for which Monty Bennett, the Chairman and CEO of the Company, also serves as Chairman and CEO.

The Proxy Penalty imposes an outsized termination fee on the Company if shareholders elect a majority of directors not approved by the incumbent directors and thereafter Ashford Inc. elects to collect the fee. Sessa believes the Proxy Penalty is unjust and excessive, and is invalid and unenforceable under Maryland law. In the lawsuit, Sessa seeks an injunction prohibiting the Company from paying a termination fee triggered by shareholders choosing to elect new directors constituting a majority of the board.

John Petry, Sessa’s Founder and Managing Partner, stated, “We are disappointed that we had to resort to litigation to remove the Proxy Penalty. It should never have existed in the first place. We brought the litigation only after Ashford Prime failed to eliminate the Proxy Penalty in the coming election. Ashford Prime threatens to apply this massive termination fee to shareholder elections in a manner that undermines corporate democracy. From a corporate governance perspective, we feel that the Proxy Penalty is worse than a poison pill, because Ashford Prime’s directors and Ashford Inc. deliberately went around shareholders to create a contractual provision that financially coerces shareholders into supporting incumbents over ‘unapproved’ directors in an election.”

Petry continued, “Director elections are the primary safeguard that shareholders have against unresponsive directors, and the Proxy Penalty deters Ashford Prime shareholders from exercising their fundamental right to a fair election. Ashford Prime’s Board of Directors, by amending the advisory agreement with Ashford Inc. such that the losing directors can choose whether to approve their replacements or trigger a massive fee, has created an unfair election. Unfortunately, we are left with no

1

Table of Contents

choice but to seek legal action to stop this self-serving conduct. We urge the Board to allow shareholders to vote for the directors of their choosing in a fair and open election.”

Petry added, “The number of corporate governance shortcomings at Ashford Prime continues to grow. Just yesterday, the Company enabled holders of its operating partnership units to purchase preferred voting shares of the Company for one penny per share. The recipients of this penny stock include Chairman Bennett, who stands to receive at least 1.27 million shares (for only $12,716), his father and other partners. In total, these new shares will represent approximately 13.3% of the Company’s voting interests, sold for $43,750.”

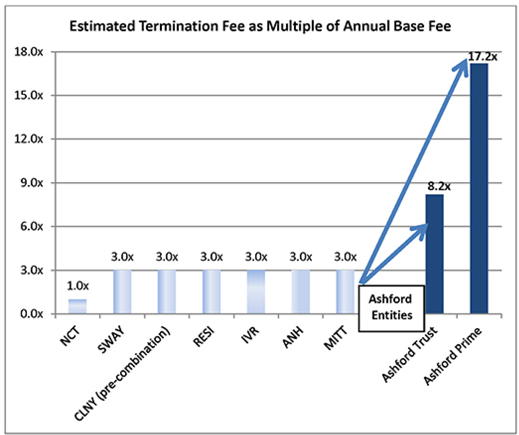

Petry concluded, “In October, Chairman Bennett said that the termination fee could be $4 to $5 per Company share. At the midpoint of this estimate, the fee would be almost $150 million, or nearly 50% of the Company’s market capitalization as of February 2, 2016. This estimated fee is approximately 17 times the $8.7 million base advisory fee paid to Ashford Inc., as reported in its most recent 10-K, and Sessa believes the termination fee is excessive and not customary for the industry. If Chairman Bennett’s numbers are correct, the Company would likely pay more to terminate the advisory agreement than it would pay in base fees for the remainder of the agreement’s entire 10-year term, based on the Company’s current market capitalization.”

As previously announced on January 15, 2016, Sessa has nominated a slate of five highly-qualified directors for election at the Company’s 2016 Annual Meeting of Stockholders. After the Company announced a strategic review process on August 28, 2015, Sessa communicated to the Company that a sale process on a level playing field for all potential bidders was the best way to maximize shareholder value. Yet nearly half a year later, the Company has provided neither meaningful action nor an update. Sessa continues to believe that the incumbent Ashford Prime Board has failed in its duties to Ashford Prime shareholders, and Sessa will defend its rights and the rights of all Ashford Prime shareholders.

Media Contacts:

Sard Verbinnen & Co

Dan Gagnier / Mark Harnett

212.687.8080

Daniel Goldstein 310.201.2040

Investor Contacts:

Innisfree M&A Incorporated

Scott Winter / Jonathan Salzberger

212.750.5833

# # #

2

Table of Contents

SESSA CAPITAL COMMENTS ON ASHFORD HOSPITALITY PRIME’S SALE OF 13.3% VOTING RIGHTS TO CHAIRMAN, CHAIRMAN’S FATHER AND OTHER PARTNERS FOR $43,750

New York – February 2, 2016 – Sessa Capital (Master), L.P. (“Sessa”), owner of 8.2% of the outstanding common shares of Ashford Hospitality Prime, Inc. (NYSE: AHP) (“Ashford Prime” or the “Company”) and Ashford Prime’s third largest shareholder, today commented on the Company’s announcement that it has amended its operating partnership agreement to enable holders of its Operating Partnership units to purchase preferred voting shares of the Company for $.01 per share. These new shares will represent approximately 13.3% of Ashford Prime’s voting interests on a diluted basis.

John Petry, Sessa’s Founder and Managing Partner, stated: “We are deeply troubled by the actions of Ashford Prime’s Board of Directors, in the midst of a contested election, to bestow a significant block of voting shares on company-friendly hands. OP unitholders are not shareholders, but by giving them the right to vote alongside common shareholders who paid much more than $.01 per share for their stock, the incumbent directors created voting rights where none previously existed. The timing of this action makes it apparent the action was designed to help the incumbent directors hold their positions, including Ashford Prime’s Chairman Monty Bennett. Simply put, when faced with a proxy fight, Ashford Prime’s incumbent directors sold nearly 13.3% of the Company’s voting stock to a group of predominantly insiders for $43,750.”

Petry added, “To add insult to injury, not only has the Ashford Prime Board infringed on the rights of the Company’s common shareholders by diluting their voting power through the sale of voting shares to insiders for $.01 per share, the Company claims this extraordinary grant was somehow governance- enhancing. The need for new, highly-qualified directors, who will uphold their fiduciary duty and act in the interest of all shareholders, not just Mr. Bennett, has never been greater. Ultimately, we have confidence that Ashford Prime shareholders will judge these self-serving actions for themselves at the 2016 Annual Meeting.”

As previously announced on January 15, 2016, Sessa plans to nominate a slate of five highly-qualified directors for election at the Company’s 2016 Annual Meeting of Shareholders. Sessa’s nominees are Larry Cunningham, Phil Livingston, John Petry, Daniel Silvers and Chris Wheeler.

Media Contacts:

Sard Verbinnen & Co

Dan Gagnier / Mark Harnett

212.687.8080

Daniel Goldstein

310.201.2040

Investor Contacts:

Innisfree M&A Incorporated

Scott Winter / Jonathan Salzberger

212.750.5833

# # # #

1

Table of Contents

SESSA CAPITAL, ONE OF ASHFORD HOSPITALITY PRIME’S LARGEST SHAREHOLDERS, NOMINATES CONTROL SLATE OF FIVE HIGHLY QUALIFIED DIRECTOR CANDIDATES FOR ELECTION TO BOARD AT 2016 ANNUAL MEETING

Believes Overhaul of Board is Needed to Revive Stalled Strategic Review Process and

to Remedy Poor Corporate Governance and Conflicts of Interest

New York, NY, – January 15, 2016 – Sessa Capital (Master), L.P. (“Sessa”), owner of 8.2% of the outstanding common shares of Ashford Hospitality Prime, Inc. (NYSE: AHP) (“Ashford Prime” or the “Company”) and Ashford Prime’s third largest shareholder, today announced it will nominate a slate of five highly-qualified, independent directors for election at the Company’s 2016 Annual Meeting of Stockholders.

Sessa’s nominees will be Larry Cunningham, Phil Livingston, John Petry, Daniel Silvers and Chris Wheeler.

Sessa believes corporate governance failures have been an unshakable burden on Ashford Prime since it started trading as a public company in November 2013 and have only worsened over time. Therefore, Sessa has concluded that a sale process on a level playing field for all potential bidders is the best way to maximize value for all shareholders.

Despite a brief period of outperformance following the Company’s announcement of its decision to pursue strategic alternatives, the stock has since resumed the downward slide it has exhibited since it started trading.

Additionally, since Sessa’s initial investment, the Company has engaged in a number ofconflict-of-interest transactions, reflecting poor corporate governance, and remained virtually silent on the status of the strategic review process announced by the Company on August 28, 2015. The Company’s actions appear to benefit Monty Bennett, the Chairman and CEO of the Company and Chairman and CEO of its external manager Ashford Inc., at the expense of all shareholders.

Despite Sessa’s repeated calls for the Company to address its corporate governance deficiencies and reverse the series of shareholder-unfriendly actions that have exacerbated the conflicts of interest inherent in Ashford Prime’s organizational structure, the Company has only made matters worse.

Since June 2015, Ashford Prime has:

| • | Amended its advisory agreement with Ashford Inc., an entity dominated by Mr. Bennett, in an attempt to impose a large termination fee if shareholders elect directors not acceptable to Ashford Inc.; |

1

Table of Contents

| • | Completed a share issuance dilutive to the Chairman’s own subsequent estimate of NAV1 in order to purchase an asset at a cap rate much richer than its own properties are valued by the market; and |

| • | Purchased $16.6 million of stock in Ashford Inc. at a 59% premium at the time and an 88% premium to yesterday’s close. |

The termination fee payable to Ashford Inc. undercuts the integrity of the strategic review process. Management has estimated the termination fee to be up to $5 per share, or nearly 50% of the Company’s $11.21 closing share price as of January 14, 2016. Quite simply, this fee makes a fair strategic process virtually impossible. The estimated fee is about 17 times the Company’s annualized base advisory fee paid to Ashford Inc. Sessa believes a customary fee in the industry would be less than 1/5 that amount. If management’s numbers are correct, the Company would likely pay more to terminate the advisory agreement than it would pay in base fees for the remainder of the agreement’s entire 10-year term based on the Company’s current market capitalization.

Rather than use the three separate renegotiations of the advisory agreement in the past two years to fix the problems relating to the fee, the Company’s Board appears to have conceded to amendments which, as a whole, have significantly broadened and worsened the fee – to the Company’s detriment and to Ashford Inc.’s benefit. In fact, the Bennett family’s potential ownership of more than half of Ashford Inc. leaves them the primary beneficiaries of this termination fee, with the Bennetts’ proportional interest in the termination fee approaching $100 million.

John Petry, Sessa’s Founder and Managing Partner, commented: “Having witnessed Ashford Prime’s Board and management disenfranchise shareholders and take one self-serving action after another, the time for change and accountability at the Board-level has come. In our view, the only chance for a successful, fair and transparent strategic alternatives process requires independent, highly-qualified directors to oversee its execution. Our slate is comprised of such individuals that are not beholden to Monty Bennett, who has presided over a loss of approximately 45% of the Company’s share value since trading began. Our slate, if elected, would immediately pursue all options for renegotiating the termination fee, addressing the potential conflicts of interest, accelerating the strategic review process and seeking to eliminate the Company’s persistent discount to its net asset value.”

Nominee Bios

| Lawrence A. Cunningham | Lawrence A. Cunningham is an expert on corporate governance and | |

| related matters, having published over forty related research articles, as well as dozens of other works on matters of corporate governance in such periodicals as Directors & Boards, The New York Times, and The Wall Street Journal. He is the Henry St. George Tucker III Research |

| 1 | As discussed on the Company’s second quarter 2015 earnings conference call |

2

Table of Contents

| Professor at The George Washington University Law School in Washington D.C. and Executive Board Member of the University’s Center for Law, Economics and Finance (C-LEAF), and the Director of C-LEAF in New York. Previously, Mr. Cunningham served as Associate Dean of Boston College Law School and Director of the Samuel and Ronnie Heyman Center on Corporate Governance at Cardozo School of Law in New York City. Consulting assignments have included corporate governance matters for companies such as Bacardi, Charter Communications, and the Securities Investor Protection Corporation. Prior to his twenty years of writing and teaching, Mr. Cunningham served as of counsel for Roberts, Sheridan & Kotel for seven years and practiced corporate law with Cravath, Swaine & Moore for six years, engaging in the areas of governance, securities, and mergers and acquisitions in both roles. Mr. Cunningham has also authored a number of books, includingThe Essays of Warren Buffett: Lessons for Corporate America, in collaboration with Warren Buffett. He is a Member of the Dean’s Council of Lerner College of Business of the University of Delaware and a recent nominee to the Editorial Board of the Museum of Financial History in New York. Mr. Cunningham received a Bachelor’s degree in economics from the University of Delaware and a J.D. from Cardozo School of Law in New York City. | ||

| Philip Livingston | Philip Livingston has significant public and private company board experience having served as a director for Broadsoft Corporation, Insurance Auto Auction, Cott Corporation, MSC Software and Seitel Inc. He is currently a director of SITO Mobile and Rand Worldwide Inc. and most recently served as Chief Executive Officer and a director of Ambassadors Group, a provider of People To People educational travel services from May 2014 to October 2015. Prior to joining Ambassadors Group, he was Chief Executive Officer of LexisNexis Web Based Marketing Solutions until October 2013. Previously, Mr. Livingston served as Chief Financial Officer for Celestial Seasonings, Inc., Catalina Marketing Corporation and World Wrestling Entertainment. From 1999 to 2003 he served as President of Financial Executives International, the leading professional association of chief financial officers and controllers. In that role he led the organization’s support of regulatory and corporate governance reforms culminating in the Sarbanes-Oxley Act. Mr. Livingston earned a BA in Business Management and a BS in Government and Politics from the University of Maryland and a MBA in Finance and Accounting from the University of California, Berkeley. | |

| John Petry | John Petry founded Sessa Capital in November 2012 and is the sole portfolio manager responsible for portfolio management, risk management, and overseeing research. Prior to launching Sessa Capital, Mr. Petry was a Principal at Columbus Hill Capital Management from November 2010 to February 2012, an opportunistic credit hedge fund that focused on distressed investing. Previously, he was a Partner at | |

3

Table of Contents

| Gotham Capital from 1997 to October 2010, where he employed a value-based approach to investing. During that time, Mr. Petry managed hedge fund Sissa Capital. Prior to Gotham Capital, he was an Analyst at Opus Capital, a value-oriented hedge fund, from 1995 to 1997 and an Associate at Conning and Company from 1993 to 1995. Mr. Petry graduated from University of Pennsylvania, Wharton School, with a B.S in Economics in 1993. | ||

Daniel B. Silvers | Daniel B. Silvers brings significant operational and investing experience in the hospitality sector. He is the Founder and Managing Member of Matthews Lane Capital Partners LLC. He currently serves on the boards of directors of Forestar Group Inc. and India Hospitality Corp. He has previously served on the boards of directors of International Game Technology, Universal Health Services, Inc. and bwin.party digital entertainment plc, as well as serving as President of Western Liberty Bancorp, an acquisition-oriented company which bought and recapitalized Service1st Bank of Nevada, a community bank in Las Vegas, NV. In 2015, Mr. Silvers was featured in the National Association of Corporate Directors’ “A New Generation of Board Leadership: Directors Under Age 40” list of emerging corporate directors. Prior to founding Matthews Lane, Mr. Silvers was the President of SpringOwl Asset Management LLC, having joined a predecessor entity in 2009. Previously, Mr. Silvers was a Vice President at Fortress Investment Group, a leading global alternative asset manager, where he worked from 2005 to 2009. Prior to joining Fortress, he was a senior member of the real estate, gaming and lodging investment banking group at Bear, Stearns & Co. Inc., where he worked from 1999 to 2005. Mr. Silvers holds a B.S. in Economics and an M.B.A. in Finance from The Wharton School of the University of Pennsylvania. He has also received a Corporate Governance certification through the Director Education & Certification Program at the UCLA Anderson School of Management. Mr. Silvers is active in a number of not-for-profits, including Horace Mann School, University of Pennsylvania and UJA-Federation of New York. | |

| Chris D. Wheeler | Chris D. Wheeler has over thirty-five years of experience in real estate M&A, development, management and financing. He is the former Chairman and Chief Executive Officer of Gables Residential Trust, a publicly-traded multifamily REIT, which was sold to ING Clarion in 2005 for $2.8 billion. Most recently, Mr. Wheeler served as a senior real estate advisor to the CEO of a family office and to the senior executives of a Fortune 50 company. Previously, Mr. Wheeler worked at Trammell Crow in a number of roles, most recently as Group Managing Partner for Trammell Crow Residential where he oversaw its multifamily residential operations throughout the Southeast, Mid-Atlantic and Northeast regions. He formerly served as Director on the Executive Committee of the National Multi Housing Council (NMHC) and on the Board of | |

4

Table of Contents

| Governors for the National Association of Real Estate Investment Trusts (NAREIT). Mr. Wheeler graduated with honors from California Institute of Technology with a degree in applied physics and received an MBA from Harvard Business School. |

Media Contacts:

Sard Verbinnen & Co

Dan Gagnier / Mark Harnett

212.687.8080

Daniel Goldstein

310.201.2040

Investor Contacts:

Innisfree M&A Incorporated

Scott Winter / Jonathan Salzberger

212.750.5833

# # # #

5

Table of Contents

| SESSA CAPITAL (Master), L.P., | * | IN THE | ||||||

Plaintiff, | * | CIRCUIT COURT | ||||||

| v. | * | FOR | ||||||

| MONTY J. BENNETT,et al., | * | BALTIMORE CITY | ||||||

Defendants. | * | CASE NO.: 24-C-16-000557 OG | ||||||

* * * * * * * * * * * * *

PLAINTIFF’S MEMORANDUM OF LAW IN SUPPORT OF

MOTION FOR PRELIMINARY INJUNCTION

Table of Contents

- i-

Table of Contents

Table of Authorities

Cases | ||||

Aprahamian v. HBO & Company, 531 A.2d 1204 (Del. Ch. 1987) | 17, 19 | |||

BAA, PLC v. Acacia Mut. Life Ins. Co., 400 Md. 136, 158 (2007) | 18 | |||

Blasius Indus., Inc. v. Atlas Corp., 564 A.2d 651 (Del. Ch. 1988) | passim | |||

Brown v. McLanahan, 148 F.2d 703, 708-709 (4th Cir. 1945) | 27 | |||

Coffman v. Maryland Publ’g Co., 167 Md. 275, 289 (1934) | 16 | |||

Daniels v. New Germany Fund, Inc., No. MJG-05-1890, 2006 U.S. Dist. LEXIS 96145, *10 (D. Md. Mar. 26, 2006) | 19 | |||

DMF Leasing, Inc. v. Budget Rent-A-Car of Maryland, Inc., 161 Md. App. 640, 649 (2005) | 15 | |||

Fogle v. H&G Restaurant, Inc., 337 Md. 441, 455-56 (1995) | 14 | |||

Hamot v. Telos Corp., No. 24-C-07-005603 (Cir. Ct. 8th JC, June 27, 2008) | 32 | |||

In re MONY Group Inc., S’holder Litig., 852 A.2d 9, 32 (Del. Ch. 2004) | 31 | |||

Kallick v. SandRidge Energy, Inc., 68 A.3d 242 (Del. Ch. 2013) | passim | |||

Kann v. Kann, 344 Md. 689, 713 (1997) | 16 | |||

Kenney v. Morgan, 22 Md. App. 698, 713-14 (1974) | 18 | |||

Kramer v. Liberty Prop. Trust, 408 Md. 1, 24 (2008) | 20 | |||

In re Laureate Educ., Inc., No. 24-C-07-000664, 2007 Md. Cir. Ct. LEXIS 11 (June 26, 2007) | 16 | |||

Lerner v. Lerner, 306 Md. 771, 776-77 (1986) | 14 | |||

Luther v. C. J. Luther Co., 94 N.W. 69, 73 (Wisc. 1903) | 27 | |||

Malone v. Brincat, 722 A.2d 5, 14 (Del. 1998) | 28 | |||

Maryland Trust Co. v. Tulip Realty Co., 220 Md. 399, 412-13 (1959) | 15 | |||

Maryland-National Capital Park & Planning Comm’n v. Washington Nat’l Arena, 282 Md. 588, 616 (1977) | 30 | |||

MM Cos. v. Liquid Audio, Inc., 813 A.2d 1118, 1127 (Del. 2003) | 18, 19 | |||

- ii-

Table of Contents

Mottu v. Primrose, 23 Md. 482, 499-500 (1865) | 17 | |||

Pontiac Gen. Emps. Ret. Sys. v. Healthways, Inc., No. 9789-VCL, at *72-73 (Del. Ch. Nov. 3, 2014) | 31 | |||

San Antonio Fire & Police Pension Fund v. Amylin Pharmaceuticals, Inc., 983 A.2d 304 (Del. Ch. 2009) | 20 | |||

Shaker, et al. v. Foxby Corp., et al., No. 24-C-04-007613, 2005 Md. Cir. Ct. LEXIS 16, *15 (Mar. 15, 2005) | passim | |||

Shenker v. Laureate Educ., Inc., 411 Md. 317, 337-39 (2009) | 3, 16, 17, 18 | |||

State Comm’n On Human Relations v. Talbot Cnty. Det. Ctr., 370 Md. 115, 140 (2002) | 30 | |||

Storetrax.com, Inc. v. Gurland, 397 Md. 37, 53-54 (2007) | 16, 17 | |||

Sutton Holding Corp. v. DeSoto, Inc.,C. A. No. 12051, 1991 Del. Ch. LEXIS 85 (Del. Ch. May 14, 1991) | 24, 33 | |||

Statutes | ||||

Md. Code Ann., Corps & Ass’n § 2-405.1(a) | 16, 18 | |||

Md. Code Ann., Corps. & Ass’ns § 2-404(b) | 17 | |||

- iii-

Table of Contents

| SESSA CAPITAL (Master), L.P., | * | IN THE | ||||||

Plaintiff, | * | CIRCUIT COURT | ||||||

| v. | * | FOR | ||||||

| MONTY J. BENNETT,et al., | * | BALTIMORE CITY | ||||||

Defendants. | * | CASE NO.: 24-C-16-000557 OG | ||||||

* * * * * * * * * * * * *

PLAINTIFF’S MEMORANDUM OF LAW IN SUPPORT OF

MOTION FOR PRELIMINARY INJUNCTION

Plaintiff, Sessa Capital (Master), L.P. (“Sessa” or the “Plaintiff”), by its attorneys, respectfully submits this Memorandum of Law (the “Memorandum”) in support of its Motion for Preliminary Injunction, pursuant to Maryland Rules 15-501,et seq., (the “Motion”) for an order that the board of directors (the “Board”) of Ashford Hospitality Prime, Inc. (“Ashford Prime” or the “Company”) and the individual directors that compose the Board (the “Director Defendants”) stop violating their fiduciary duties and approve Sessa’s nominees for the Board.

Sessa is a shareholder of Ashford Prime and has announced its intention to nominate five new directors (the “Sessa Candidates”) to the seven member Board of Ashford Prime and seeks to let Ashford Prime shareholders exercise their right to vote freely for the directors of their own choice. The Director Defendants1 have a different plan and are obstructing the voting rights of the shareholders.

Facing increased scrutiny from shareholders, and concerned about the possible results of free shareholder voting, the Director Defendants and the Company’s outside advisor, Defendant

| 1 | The Director Defendants are Monty J. Bennett, Douglas A. Kessler, Stefani D. Carter, Curtis B. McWilliams, W. Michael Murphy, Matthew D. Rinaldi, and Andrew Strong. |

- 1-

Table of Contents

Ashford Inc., inserted an expanded definition of the term “Company Change of Control” in the “Termination Fee” provision of the Company’s advisory agreement with Ashford Inc., creating what hereinafter will be referred to as the “Proxy Penalty.”2 The Proxy Penalty provides that, if Ashford Prime shareholders vote to replace a majority of the incumbent Board, Defendant Ashford Inc. can terminate the advisory agreement, and impose a penalty, in the form of a Termination Fee on Ashford Prime. The Termination Fee was estimated by Defendant Bennett to be $4.00 to $5.00 per fully diluted Ashford Prime share; at $4.50 per share the amount would be almost $150 million but could be more, approximately half of the Company’s current equity value. However, under the terms of the Proxy Penalty, if the incumbent Board “approves” the Sessa Candidates for the limited purposes of the agreement, then the Proxy Penalty is neutralized, and no Termination Fee may be imposed. In short, the Board itself controls whether the $150 million penalty will or will not be imposed in the context of the Sessa Candidates’ running for the Board.

If the Director Defendants simply “approve” the Sessa Candidates for the limited purposes of the agreement, then Company shareholders will be able to fairly consider the competing candidates without fear of imposition of a penalty as a result of how they choose to vote. “Approval” does not constitute a recommendation of the Sessa Candidates to Ashford Prime’s shareholders, but instead is an action only relevant for purposes of the agreement between Ashford Prime and Ashford Inc. Approval will permit shareholders to evaluate the Sessa Candidates on an equal footing without the fear that their election could potentially result

| 2 | The Proxy Penalty is similar to a “proxy put” or “poison put,” which is a contractual provision in a financing instrument that allows the lender to accelerate the debt owed by the company if the majority of the company’s incumbent board is ousted as the result of a proxy contest. Some proxy puts include a provision that allows the incumbent board to “approve” the dissident slate and disable the proxy put. The recently adopted Proxy Penalty in this case operates in the same fashion. The Proxy Penalty in this instance is far more egregious than a traditional proxy put because the Proxy Penalty was inserted into an agreement with a related company – so much so that the same individual, David A. Brooks (“Brooks”), signed the agreement forall parties. Ashford Prime did not ask shareholders to approve the Proxy Penalty. |

- 2-

Table of Contents

in a drastic financial penalty on the Company. But the incumbent Director Defendants apparently do not want a fair election. Instead, in a breach of their duty of loyalty, the Director Defendants approved the Proxy Penalty and have failed to “approve” the Sessa Candidates.

“Directors of Maryland corporations stand in a fiduciary relationship to the corporations that they manage and the shareholders of those corporations, a relationship that imposes on directors duties of care, loyalty, and good faith.”Shenker v. Laureate Educ., Inc., 411 Md. 317, 337-39 (2009). And this Court has held when a shareholder demonstrates that acts of the board of directors violate shareholder voting rights or confer an advantage to any slate of candidates, absent a compelling justification, such actions represent a breach of fiduciary duty that Maryland courts must exercise their equity jurisdiction to invalidate.Shaker, et al. v. Foxby Corp., et al., No. 24-C-04-007613, 2005 Md. Cir. Ct. LEXIS 16, *15 (Mar. 15, 2005).

Plaintiff brings this motion to seek a narrow preliminary order to require the Board to “approve” the Sessa Candidates for limited purposes and allow the upcoming board of directors election to take place on a level playing field. Plaintiff seeks relief now because the contest for shareholder votes has begun and the annual meeting at which the director election will occur has historically been held in May for Ashford Prime and its former parent (the Company has not yet announced the actual date of the meeting). This relief must be provided early enough for a fair election to be had at the meeting which must include time to allow the shareholders to receive information about all the candidates, to fairly consider each, and to allow the Sessa Candidates to seek proxy votes on a level playing field. With Sessa’s filing of its preliminary proxy statement with the SEC on February 12, 2016, the election campaign for directors has begun. An election’s fairness is determined not only by what occurs on the date of the vote; it also depends on the candidates’ ability to campaign, inform, and refute misinformation which could otherwise

- 3-

Table of Contents

determine the election’s result. Even if the Company contrives a reason to move its traditional May annual meeting date to a later date in 2016, the election campaign is now underway and shareholders deserve clarity during the current campaign period as to whether they can support a dissident slate without a massive economic penalty. Thus, immediate relief is necessary. Absent a preliminary injunction, Ashford Prime’s shareholders will be permanently deprived of the opportunity to evaluate the Sessa Candidates on the merits, and vote on a fully informed basis.

Below, Plaintiff presents facts in support of this Motion, and demonstrates the Director Defendants’ breach of their fiduciary duties. As a result of that breach, the Court should issue a preliminary injunction pursuant to Maryland Rule 15-501, et seq. Plaintiff has also propounded discovery to the Defendants – and has moved to shorten the time to respond to that discovery – and will appropriately supplement the record at or before the hearing on this Motion.

| A. | The Parties and their Interests |

Ashford Hospitality Trust, Inc. (“Ashford Trust”) is a Maryland corporation, formed in 2003, and is qualified as a real estate investment trust.SeeExhibit 1, Ashford Trust Form 10-K for the fiscal year ended December 31, 2014, at pgs. 2-3. In November 2013, Ashford Trust spun-off Ashford Prime, which resulted in Ashford Prime becoming a publicly traded company.SeeExhibit 2, Ashford Prime Form 10-K for the fiscal year ended December 31, 2014, at pg. 4. In November 2014, Ashford Trust completed a spin-off of its asset management business, which resulted in Ashford Inc. becoming a publicly traded company.SeeExhibit 1 at pg. 3. Ashford Inc. provides advisory services to Ashford Trust and Ashford Prime through Ashford Hospitality Advisors LLC (“Ashford Advisors”), a Delaware limited liability company.SeeExhibit 3, Ashford Inc. Form 10-K for the fiscal year ended December 31, 2014, at pg. 3. Ashford Advisors is a subsidiary of and the operating company of Ashford Inc.Id.

- 4-

Table of Contents

Ashford Trust, Ashford Prime, and Ashford Inc. have a common chairman of their respective boards of directors (Defendant Bennett), and the officers and senior management for all three entities are the same (Defendant Bennett is Chief Executive Officer of each entity, Defendant Kessler is President of each entity and a director of Ashford Prime, Brooks is Chief Operating Officer of each entity, and Deric Eubanks is Chief Financial Officer of each entity). See Information listed on Ashford Trust, Ashford Prime, and Ashford Inc. websites, attached collectively asExhibit 4.

As of March 10, 2015, Bennett was the beneficial owner of 1,308,207 shares (5.23%) of the outstanding shares of Ashford Prime’s common stock, and the beneficial owner of 6,587,246 shares (6.2%) of the outstanding shares of Ashford Trust’s common stock. SeeExhibit 5, Ashford Prime, Schedule 14A, filed on April 17, 2015, at 26;Exhibit 6, Notice of Annual Meeting of Stockholders of Ashford Trust, at pg. 52. As of January 22, 2016, Bennett was the beneficial owner of 221,172 shares (11%) of the outstanding shares of Ashford Inc.’s common stock, and stood to receive another 195,570 shares (8.9%) under a deferred compensation plan.SeeExhibit 7, Ashford Inc. Schedule 14A, filed on January 27, 2016, at pg. 104. In addition, as of January 22, 2016, Bennett’s father owned 4.2% of Ashford Inc.’s common stock.Id. Under a merger agreement announced in September 2015 that is pending shareholder approval, Bennett and his father’s ownership of Ashford Inc. could increase substantially.SeeExhibit 8, Ashford Inc., Schedule 14A, filed on January 27, 2016. Kessler is the President and a Director of Ashford Prime.SeeExhibit 4. He is also the President of both Ashford Trust and Ashford Inc.Id. As of January 22, 2016, Kessler was the beneficial owner of 32,411 shares (1.6%) of the outstanding shares of Ashford Inc.’s common stock. SeeExhibit 7 at pg. 104.

- 5-

Table of Contents

Sessa has been a shareholder of the Company since March 9, 2015, beneficially owns approximately 8.2% of the Company’s common stock, and is one of the Company’s largest stockholders. Sessa has made Schedule 13D filings with the SEC since acquiring more than 5% of the Company’s common stock on August 25, 2016, and on January 15, 2016, Sessa notified the Company that Sessa intended to nominate five candidates for election to the Company’s seven member Board. On February 12, 2016, Sessa filed its preliminary proxy statement with the SEC in connection with Sessa’s solicitation of proxies for the Company’s 2016 annual meeting of stockholders.

| B. | The Board Entrenches Itself By Adopting The Proxy Penalty |

On November 19, 2013, Ashford Prime, Ashford Hospitality Prime Limited Partnership (“Ashford Hospitality”) and Ashford Advisors entered into an Advisory Agreement.SeeExhibit 9, Advisory Agreement (Ex. 10.2), Ashford Prime Form 8-K, dated November 19, 2013. Ashford Hospitality is a Delaware limited partnership and is Ashford Prime’s operating partnership. Pursuant to the Advisory Agreement, Ashford Advisors provided certain advisory services to Ashford Prime and Ashford Hospitality.Id. The Advisory Agreement was executed on behalf of Ashford Prime by Brooks, Chief Operating Officer.Id. Brooks also executed the Advisory Agreement on behalf of Ashford Hospitality Prime OP General Partner, LLC, the general partner of Ashford Hospitality, and on behalf of Ashford Advisors. Id.

Among other things, the Advisory Agreement set forth the compensation to be paid by Ashford Prime for services rendered.SeeExhibit 9, Advisory Agreement at Section 6. The Advisory Agreement also established a “Termination Fee” payable to the Ashford Advisors, in cash, if Ashford Advisors elected to terminate the agreement upon certain “Company Change of

- 6-

Table of Contents

Control” events.SeeExhibit 9, Advisory Agreement at Section 16(d). Notably to this action, neither the identity nor the election of directors was relevant to what constituted a Company Change of Control, and therefore a change of directors would not trigger the right to terminate and payment of a Termination Fee.SeeExhibit 9, Advisory Agreement at 16(a). Two amended Advisory Agreements followed in May and November of 2014.SeeExhibit 10, Amended and Restated Advisory Agreement (Ex. 10.1), Ashford Prime Form 8-K, dated May 13, 2014;Exhibit 11, Second Amended and Restated Advisory Agreement (Ex. 10.1), Ashford Prime Form 10-Q, dated November 7, 2014. Again, neither amendment included or dealt with the identity of the directors of the Company or included the election of new and unapproved directors within the definition of Company Change of Control.SeeExhibit 10 at Section 16;Exhibit 11 at Section 16.

The motivation that led to the Board’s eventual insertion of the Proxy Penalty can be traced to Ashford Prime’s 2014 annual meeting. At the annual meeting, shareholders supported a non-binding resolution (“Proposal 3”) to opt out of the Maryland Unsolicited Takeover Act (“MUTA”).SeeExhibit 12, Ashford Prime Form 8-K, dated May 13, 2014. Opting out of the MUTA eliminates certain barriers to a change in control. A year later, the Company opted out of the MUTA.SeeExhibit 13, Ashford Prime Form 8-K, dated May 12, 2015. In the meantime, in February 2015, the Board adopted a proposal to restrict shareholders from nominating directors. The proposal would have required that only shareholders holding 1% or more of the Company’s stock continuously for at least one year would be eligible to nominate directors.SeeExhibit 13 at Proposal 5. At the Company’s annual meeting in May 2015, this proposal was soundly rejected by the Company’s shareholders, with 80% of the voting shareholders opposing the proposal.Id.

- 7-

Table of Contents

Just weeks after the rejection of the Board’s proposal to limit director nominations and after Proposal 3 was finally adopted by the Board to eliminate certain barriers to a change of control, on June 10, 2015, Ashford Prime executed a Third Amended and Restated Advisory Agreement (the “Third Amended Advisory Agreement”).SeeExhibit 14, Third Amended and Restated Advisory Agreement (Ex. 10.1), Ashford Prime Form 8-K, dated June 10, 2015. Ashford Inc., and Ashford Advisors, as the operating company of Ashford Inc., were parties to the Third Amended Advisory Agreement and were defined collectively as the “Advisor.”3Id. Brooks executed the Third Amended Advisory Agreement on behalf of Ashford Prime (as Chief Operating Officer), Ashford Advisors (as Chief Operating Officer), and Ashford Inc. (as Chief Operating Officer).Id.

In a dramatic departure from the three previous advisory agreements, the Third Amended Advisory Agreement included an expanded definition of the term Company Change of Control that created the extraordinary and onerous “Proxy Penalty.” Section 12(f) of the Third Amended Advisory Agreement added, to the events that constitute a Company Change of Control, the following:

(iv)during any five-year period, the members of the Board of Directors of the Company change such that the members who constitute the Board of Directors on the Effective Date [June 10, 2015] (the “Company Incumbent Board”) no longer constitute at least a majority of the board of the Company; provided, however, that any individual becoming a director after the Effective Date whose election to the board isapproved or recommended to stockholders of the Company by a vote of at least a majority of the Company Incumbent Board shall be considered as though such individual were a member of the Company Incumbent Board.

(emphasis added).SeeExhibit 14, Third Amended Advisory Agreement at pg. 26.

Rather than seeking shareholder approval for the Proxy Penalty at the 2015 Annual Meeting, Defendants unilaterally imposed it on the Company.SeeExhibit 13.

| 3 | Ashford Inc. was not a party to the original Advisory Agreement or the first two amended agreements because it had not yet been spun off from Ashford Trust. Ashford Advisors is a subsidiary of Ashford Inc. |

- 8-

Table of Contents

Since adopting the Proxy Penalty, Defendants have been unable or unwilling to state clearly the potential cost of the Termination Fee under the Third Amended Advisory Agreement.4 Initially, on August 7, 2015, Defendant Bennett stated the Termination Fee was as low “as a buck and change” per share of Ashford Prime. SeeExhibit 15, Second Quarter Earnings Call, August 7, 2015, at pg. 6, http://seekingalpha.com/article/3416576-ashford-hospitality-trusts-aht-ceo-monty-bennett-on-q2-2015-results-earnings-call-transcript?part=single. At the same time, Defendant Bennett said “[w]hat it is at any specific time is something that we’d have to go through at that specific time and go through this whole analysis, which is something that we haven’t done.” Id.

Subsequently, during an investor presentation on October 20, 2015, Defendant Bennett stated that the “management team, without speaking on behalf of the Ashford Prime Board,” estimated that the amount of the Termination Fee was in the range of $4 to $5 per fully diluted share.SeeWebcast Replay of Ashford Investor & Analyst Day, October 20, 2015,available at http://www.snl.com/IRWebLinkX/corporateprofile.aspx?iid=4384791. A Termination Fee of $5 would be approximately 50% of the closing price, $9.83, of Ashford Prime’s shares on February 12, 2016. At $4.50 per fully diluted share, the midpoint of Defendant Bennett’s range, the estimated Termination Fee is almost $150 million. By comparison, Ashford Prime paid Ashford Inc. $8.7 million in base advisory fees during 2014 (2015 results have not been released).SeeExhibit 16, Ashford Prime 2014 Annual Report at pg. 79.

The purpose of the change was to make board changes economically ruinous (at the incumbent Board’s discretion) and thereby to entrench the Director Defendants at the expense of

| 4 | A board of directors can never sell its fiduciary duties, but particularly cannot sell the shareholders’ fundamental right to choose the directors of the corporation. Thus, any consideration Ashford Prime may claim to have received from Ashford Inc. in the Third Amended Advisory Agreement cannot be used to justify the Defendant Directors breaching their fiduciary duty by adopting the Proxy Penalty. |

- 9-

Table of Contents

the shareholder franchise. Under this change, if non-incumbent directors are elected to the Board and become a majority, a Company Change of Control event occurs that permits Ashford to terminate the Third Amended Advisory Agreement and trigger payment of a Termination Fee.SeeExhibit 14 at Sections 12(d) and 12(f). If Ashford decides it does not want to provide services to Ashford Prime, and therefore terminates the Third Amended Advisory Agreement, Ashford nevertheless would be rewarded for its nonservice by receiving a Termination Free – a $150 million windfall payment that requires it to provide no further services.Id.

But, Ashford Prime has an easy way to prevent the imposition of such a steep penalty. The Termination Fee is not triggered if a majority of the incumbent Board approves or recommends the Sessa Candidates.SeeExhibit 14, Section 12(f) at pg. 26. Because the provision is in the disjunctive, a recommendation by the incumbent Board is not required – the incumbent Board can simply approve the competing candidates for the limited purposes of the Third Amended Advisory Agreement, without recommending the Sessa Candidates to shareholders. The incumbent Board, despite approving the candidates, can campaign as intensely as it wishes against those candidates but, if the Sessa Candidates are elected, such approval means the Company is not faced with the risk of having to pay a Termination Fee.

More egregiously, the Proxy Penalty was not the result of the Board acquiescing to the demands of an unrelated party in an arms-length negotiation. Instead, the shared management of Ashford and Ashford Prime colluded to insert the Proxy Penalty, with the shared intent to entrench the incumbent directors, and in turn ensure that, if the directors were to be ousted, Ashford would receive the potential financial windfall of a $150 million Termination Fee, a windfall that would be shared among the Director Defendants that own substantial stock of Ashford Inc.5SeeExhibit 4 andExhibit 7.

| 5 | As noted above, Bennett owns a greater percentage of stock in Ashford Inc. stock than he does in Ashford Prime. He stands to significantly increase his ownership of Ashford Inc. stock if the pending transaction between Ashford Inc., Remington Holdings, LP and related entities is consummated. SeeExhibit 7 andExhibit 8. |

- 10-

Table of Contents

| C. | The Board Fails To Approve The Sessa Candidates And Neutralize The Proxy Penalty |

On January 15, 2016, Sessa delivered to the Company a Notice of Proposed Nominees for Election to the Board of Directors (the “Sessa Notice”). The Sessa Notice advised Ashford Prime that Sessa intended to nominate five qualified individuals to the seven member Board of Ashford Prime: John E. Petry, Lawrence A. Cunningham, Philip B. Livingston, Daniel B. Silvers, and Chris D. Wheeler.SeeExhibit 17, Sessa Notice.

| • | Mr. Petry holds a B.S. in Economics from the Wharton School at the University of Pennsylvania. In addition, he was a partner at Gotham Capital for 13 years before founding Sessa Capital in 2012. |