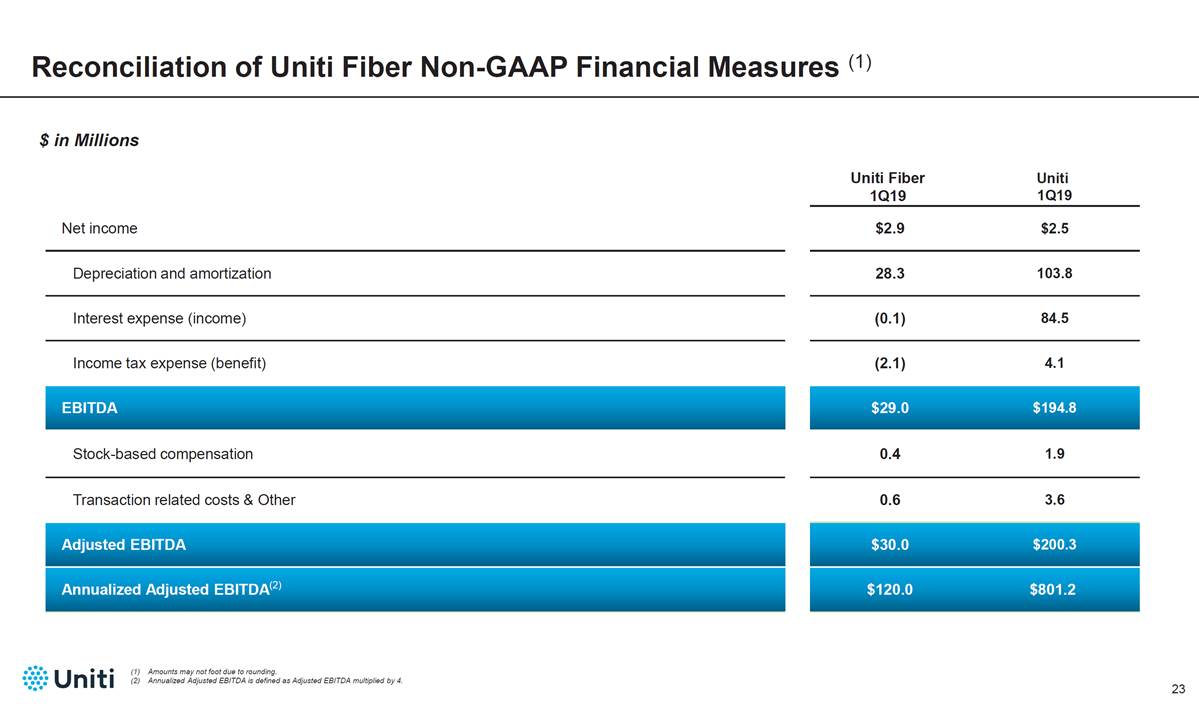

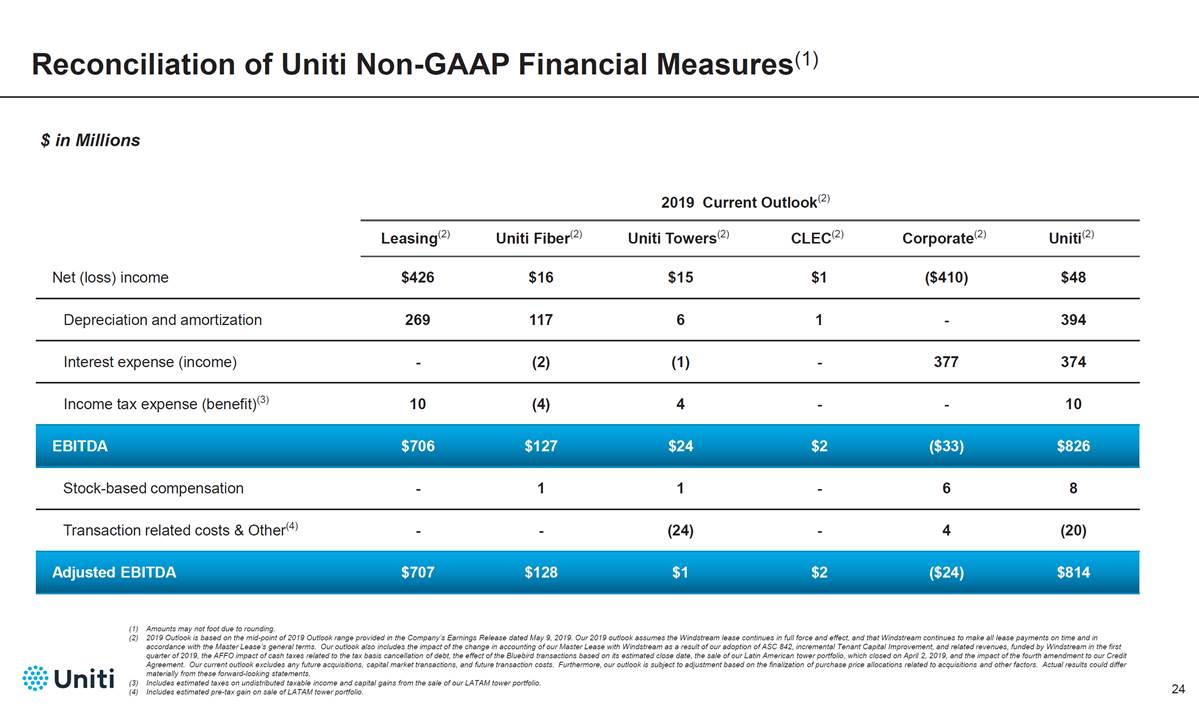

Non-GAAP Financial Measures We refer to EBITDA, Adjusted EBITDA, Funds From Operations (“FFO”) as defined by the National Association of Real Estate Investment Trusts (“NAREIT”) and Adjusted Funds From Operations (“AFFO”) in our analysis of our results of operations, which are not required by, or presented in accordance with, accounting principles generally accepted in the United States (“GAAP”). While we believe that net income, as defined by GAAP, is the most appropriate earnings measure, we also believe that EBITDA, Adjusted EBITDA, FFO and AFFO are important non-GAAP supplemental measures of operating performance for a REIT. We define “EBITDA” as net income, as defined by GAAP, before interest expense, provision for income taxes and depreciation and amortization. We define “Adjusted EBITDA” as EBITDA before stock-based compensation expense and the impact, which may be recurring in nature, of transaction and integration related costs, collectively “Transaction Related Costs”, the write off of unamortized deferred financing costs, costs incurred as a result of the early repayment of debt, gains or losses on dispositions, changes in the fair value of contingent consideration and financial instruments, and other similar items. We believe EBITDA and Adjusted EBITDA are important supplemental measures to net income because they provide additional information to evaluate our operating performance on an unleveraged basis. In addition, Adjusted EBITDA is calculated similar to defined terms in our material debt agreements used to determine compliance with specific financial covenants. Since EBITDA and Adjusted EBITDA are not measures calculated in accordance with GAAP, they should not be considered as alternatives to net income determined in accordance with GAAP. Because the historical cost accounting convention used for real estate assets requires the recognition of depreciation expense except on land, such accounting presentation implies that the value of real estate assets diminishes predictably over time. However, since real estate values have historically risen or fallen with market and other conditions, presentations of operating results for a REIT that use historical cost accounting for depreciation could be less informative. Thus, NAREIT created FFO as a supplemental measure of operating performance for REITs that excludes historical cost depreciation and amortization, among other items, from net income, as defined by GAAP. FFO is defined by NAREIT as net income attributable to common shareholders computed in accordance with GAAP, excluding gains or losses from real estate dispositions, plus real estate depreciation and amortization and impairment charges. We compute FFO in accordance with NAREIT’s definition. The Company defines AFFO, as FFO excluding (i) transaction and integration costs; (ii) certain non-cash revenues and expenses such as stock-based compensation expense, amortization of debt and equity discounts, amortization of deferred financing costs, depreciation and amortization of non-real estate assets, straight line revenues, non-cash income taxes, and the amortization of other non-cash revenues to the extent that cash has not been received, such as revenue associated with the amortization of tenant capital improvements; (iii) the impact, which may be recurring in nature, of the write-off of unamortized deferred financing fees, additional costs incurred as a result of early repayment of debt, gains or losses on dispositions, changes in the fair value of contingent consideration and financial instruments and similar items less maintenance capital expenditures. We believe that the use of FFO and AFFO, and their respective per share amounts, combined with the required GAAP presentations, improves the understanding of operating results of REITs among investors and analysts, and makes comparisons of operating results among such companies more meaningful. We consider FFO and AFFO to be useful measures for reviewing comparative operating performance. In particular, we believe AFFO, by excluding certain revenue and expense items, can help investors compare our operating performance between periods and to other REITs on a consistent basis without having to account for differences caused by unanticipated items and events, such as transaction and integration related costs. The Company uses FFO and AFFO, and their respective per share amounts, only as performance measures, and FFO and AFFO do not purport to be indicative of cash available to fund our future cash requirements. While FFO and AFFO are relevant and widely used measures of operating performance of REITs, they do not represent cash flows from operations or net income as defined by GAAP and should not be considered an alternative to those measures in evaluating our liquidity or operating performance. Further, our computations of EBITDA, Adjusted EBITDA, FFO and AFFO may not be comparable to that reported by other REITs or companies that do not define FFO in accordance with the current NAREIT definition or that interpret the current NAREIT definition or define EBITDA, Adjusted EBITDA and AFFO differently than we do. 25