Exhibit 99.2

Strategic Actions Frequently Asked Questions February 28, 2022

Forward - Looking Statements 2 This presentation contains forward - looking statements as that term is defined in the Private Securities Litigation Reform Act of 1995 . In some cases, such forward - looking statements may be identified by terms such as believe, expect, seek, may, will, intend, project, anticipate, plan, estimate, guidance or similar words . Forward - looking statements involve risks and uncertainties that could cause actual results to differ materially from those in the forward - looking statements . Although it is not possible to identify all of these risks and factors, they include, among others, the following : the inherent uncertainty of estimating reserves and the possibility that incurred losses may be greater than our loss and loss adjustment expense reserves ; inaccurate estimates and judgments in our risk management may expose us to greater risks than intended ; the downgrade in the financial strength rating of our regulated insurance subsidiaries announced May 7 , 2021 , or further downgrades, impacting our ability to attract and retain insurance and reinsurance business that our subsidiaries write, our competitive position, and our financial condition ; the potential loss of key members of our management team or key employees and our ability to attract and retain personnel ; adverse economic factors resulting in the sale of fewer policies than expected or an increase in the frequency or severity of claims, or both ; a persistent high inflationary environment could have a negative impact on our reserves, the value of our investments and investment returns, and our compensation expenses ; reliance on a select group of brokers and agents for a significant portion of our business and the impact of our potential failure to maintain such relationships ; reliance on a select group of customers for a significant portion of our business and the impact of our potential failure to maintain, or decision to terminate, such relationships ; our ability to obtain reinsurance coverage at prices and on terms that allow us to transfer risk and adequately protect our company against financial loss ; losses resulting from reinsurance counterparties failing to pay us on reinsurance claims, insurance companies with whom we have a fronting arrangement failing to pay us for claims, or a former customer with whom we have an indemnification arrangement that fails to perform their reimbursement obligations ; inadequacy of premiums we charge to compensate us for our losses incurred ; changes in laws or government regulation, including tax or insurance law and regulations ; the ongoing effect of Public Law No . 115 - 97 , informally titled the Tax Cuts and Jobs Act, which may have a significant effect on us including, among other things, by potentially increasing our tax rate, as well as on our shareholders ; in the event we do not qualify for the insurance company exception to the passive foreign investment company (“PFIC”) rules and are therefore considered a PFIC, there could be material adverse tax consequences to an investor that is subject to U . S . federal income taxation ; the Company or any of its foreign subsidiaries becoming subject to U . S . federal income taxation ; a failure of any of the loss limitations or exclusions we utilize to shield us from unanticipated financial losses or legal exposures, or other liabilities ; losses from catastrophic events, such as natural disasters and terrorist acts, which substantially exceed our expectations and/or exceed the amount of reinsurance we have purchased to protect us from such events ; the effects of the COVID - 19 pandemic and associated government actions on our operations and financial performance ; potential effects on our business of emerging claim and coverage issues ; exposure to credit risk, interest rate risk and other market risk in our investment portfolio ; the potential impact of internal or external fraud, operational errors, systems malfunctions or cyber security incidents ; our ability to manage our growth effectively ; failure to maintain effective internal controls in accordance with Sarbanes - Oxley Act of 2002 , as amended (“Sarbanes - Oxley”) ; and changes in our financial condition, regulations or other factors that may restrict our subsidiaries’ ability to pay us dividends . Additional information about these risks and uncertainties, as well as others that may cause actual results to differ materially from those in the forward - looking statements, is contained in our filings with the U . S . Securities and Exchange Commission ("SEC"), including our most recently filed Annual Report on Form 10 - K, Quarterly Report on Form 10 - Q, and our other documents on file with the SEC . These forward - looking statements speak only as of the date of this release and the Company does not undertake any obligation to update or revise any forward - looking information to reflect changes in assumptions, the occurrence of unanticipated events, or otherwise .

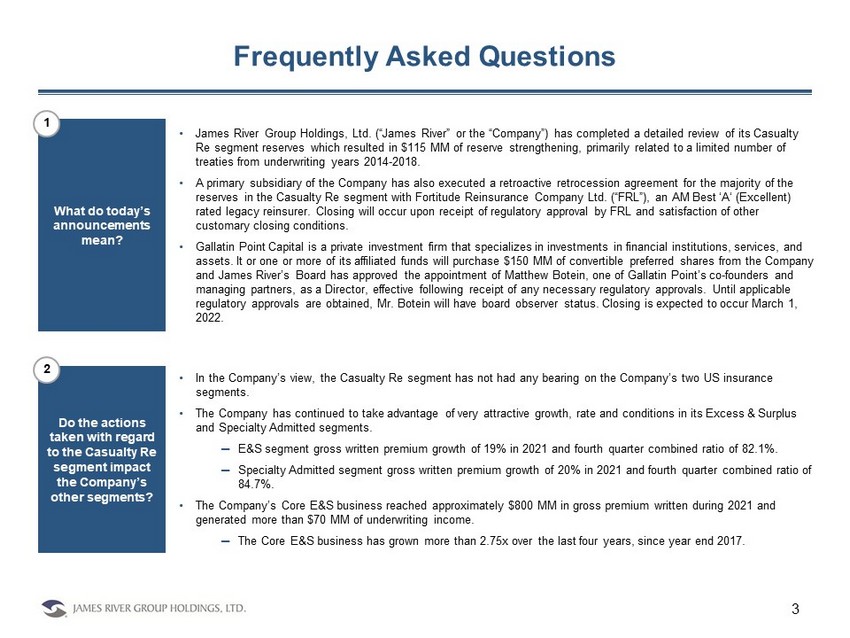

Frequently Asked Questions 3 • James River Group Holdings, Ltd. (“James River” or the “Company”) has completed a detailed review of its Casualty Re segment reserves which resulted in $115 MM of reserve strengthening, primarily related to a limited number of treaties from underwriting years 2014 - 2018. • A primary subsidiary of the Company has also executed a retroactive retrocession agreement for the majority of the reserves in the Casualty Re segment with Fortitude Reinsurance Company Ltd. (“FRL”), an AM Best ‘A‘ (Excellent) rated legacy reinsurer. Closing will occur upon receipt of regulatory approval by FRL and satisfaction of other customary closing conditions. • Gallatin Point Capital is a private investment firm that specializes in investments in financial institutions, services, and assets. It or one or more of its affiliated funds will purchase $150 MM of convertible preferred shares from the Company and James River’s Board has approved the appointment of Matthew Botein , one of Gallatin Point’s co - founders and managing partners, as a Director, effective following receipt of any necessary regulatory approvals. Until applicable regulatory approvals are obtained, Mr. Botein will have board observer status. Closing is expected to occur March 1, 2022. What do today’s announcements mean? Do the actions taken with regard to the Casualty Re segment impact the Company’s other segments? • In the Company’s view, the Casualty Re segment has not had any bearing on the Company’s two US insurance segments. • The Company has continued to take advantage of very attractive growth, rate and conditions in its Excess & Surplus and Specialty Admitted segments. ─ E&S segment gross written premium growth of 19% in 2021 and fourth quarter combined ratio of 82.1%. ─ Specialty Admitted segment gross written premium growth of 20% in 2021 and fourth quarter combined ratio of 84.7%. • The Company’s Core E&S business reached approximately $800 MM in gross premium written during 2021 and generated more than $70 MM of underwriting income. ─ The Core E&S business has grown more than 2.75x over the last four years, since year end 2017. 1 2

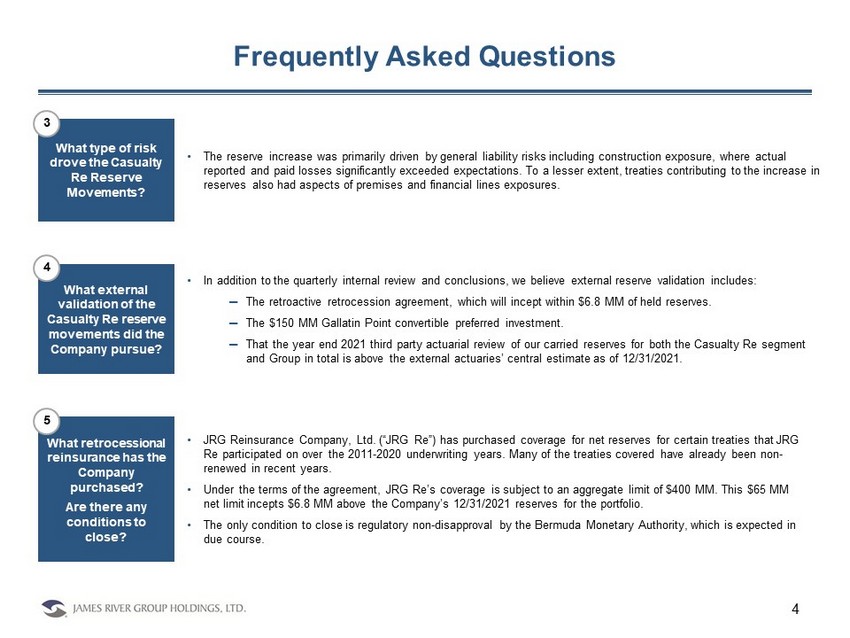

Frequently Asked Questions 4 • In addition to the quarterly internal review and conclusions, we believe external reserve validation includes: ─ The retroactive retrocession agreement, which will incept within $6.8 MM of held reserves. ─ The $150 MM Gallatin Point convertible preferred investment. ─ That the year end 2021 third party actuarial review of our carried reserves for both the Casualty Re segment and Group in total is above the external actuaries’ central estimate as of 12/31/2021. What external validation of the Casualty Re reserve movements did the Company pursue? What retrocessional reinsurance has the Company purchased? Are there any conditions to close? • JRG Reinsurance Company, Ltd. (“JRG Re”) has purchased coverage for net reserves for certain treaties that JRG Re participated on over the 2011 - 2020 underwriting years. Many of the treaties covered have already been non - renewed in recent years. • Under the terms of the agreement, JRG Re’s coverage is subject to an aggregate limit of $400 MM. This $65 MM net limit incepts $6.8 MM above the Company’s 12/31/2021 reserves for the portfolio. • The only condition to close is regulatory non - disapproval by the Bermuda Monetary Authority, which is expected in due course. 4 5 What type of risk drove the Casualty Re Reserve Movements? • The reserve increase was primarily driven by general liability risks including construction exposure, where actual reported and paid losses significantly exceeded expectations. To a lesser extent, treaties contributing to the increase in reserves also had aspects of premises and financial lines exposures. 3

Frequently Asked Questions 5 • James River will recognize an after - tax loss of $6.8 MM in connection with the transaction during the first quarter of 2022, which is expected to be reported as prior year reserve development within the Casualty Re segment. • As part of the transaction, James River will not recognize any earnings on the portfolio during the first quarter of 2022, which will result in an increase in current accident year losses of $5 MM in that quarter. • James River will pay FRL premium of $335 MM. ─ This includes $25 MM of cash paid to FRL at closing. The Company currently has this cash on hand. ─ The remaining $310 MM will be held by the Company on a funds withheld basis until balances decline to a certain level. • The total premium, initial funds withheld balance, and the aggregate limit will be adjusted for claims paid from October 1, 2021 to the closing date. • The Company will pay to FRL a crediting rate of 2% per annum, paid quarterly, on the funds withheld assets. This balance will decline as the liabilities run off. The expense of the interest credit will run through the Consolidated Income Statement. What is the cost of the retrocessional reinsurance transaction and financial impact on James River? 7 What Casualty Re liabilities are included in the transaction? Are further strategic actions expected with regard to this segment? • The retrocession transaction covers the majority of the historical reserves of the Casualty Re segment and a majority of the segment reserves related specifically to construction and construction defect risk. • The Casualty Re portfolio had been downsized and de - risked beginning in 2018 and has also gained significant improvement in both rate and terms and conditions, especially in the last two years. • The Company expects to meaningfully reduce gross written premium in the Casualty Re segment over the course of 2022. 6

Frequently Asked Questions 6 • The Company will maintain its quarterly internal reserve review process and its consistent third and fourth quarter third party reserve reviews. • James River hired a new Chief Actuary in August 2021 with 37 years of deep casualty reserve experience gained from his past history with AIG and Allied World Assurance AG. • He has completed a deep review of the full company reserves as of year end 2021, and led a process to continue to improve underwriting and actuarial data. • The Company has also benefitted from the experience of recent additions to the senior management team, including a Group Chief Underwriting Officer and Chief Claims Officer. Have the Company’s processes and timing for its internal and external reserve reviews changed? 9 What is the form and structure of the capital raise? • The Company is raising $150 MM through a private placement of convertible preferred shares. The capital will be treated as mezzanine equity under GAAP and will receive a high degree of equity credit under rating agency models. We expect to contribute the proceeds of the issuance to our insurance operating subsidiaries. • The security will pay a 7% preferred dividend for the first five years and will reset thereafter. • The convertible preferred shares will have the option to be converted into common shares at an initial 27.5% premium to the lower of the average of the volume weighted average prices (“VWAPs”) of James River’s common shares a) over the five trading days preceding our fourth quarter earnings announcement, or b) over the five trading days following our fourth quarter earnings announcement. The Initial Conversion Price will be subject to customary anti - dilution adjustments. • After two years, James River has the option to cause the convertible preferred shares to convert into common shares if the VWAP of the Company’s common shares exceeds 130% of the Conversion Price for at least 20 consecutive trading days. • The convertible preferred shares will vote with common shareholders on voting matters on an as converted basis; voting rights are capped at 9.9%. • The Company’s Board has approved Matthew Botein , one of Gallatin Point’s co - founders and managing partners, as a Class I Director with a term expiring at the 2024 annual meeting of the Company’s shareholders, effective following receipt of any necessary regulatory approvals. Until applicable regulatory approvals are obtained, Mr. Botein will have Board observer status. 8

Is the Company confident in its capital position? Frequently Asked Questions 7 10 • The Company is confident in its capital position. ─ Pro forma for the capital raise, operating leverage is 1.13x and financial leverage is 26% as of 12/31/2021. • As of December 31, 2021, reserves for incurred but not reported (“IBNR”) events represented 64.4% of net reserves which is up from 55.3% a year ago and is the highest level of IBNR since early 2018. • The Company believes it is well capitalized to support its continued ability to take advantage of the “once in a generation” market it is benefitting from in its Excess & Surplus and Specialty Admitted businesses. • James River has also reduced its quarterly Common Dividend to $0.05 per common share beginning with its next dividend payable on March 31, 2022. The Common Dividend reflects the Company’s current growth profile, which remains robust.